International Workshop on New Generation Port Cities and Global Supply Chains The University of Hong Kong, 12-14 December 2005 New Port-Hinterland Relationships: Experiences from North America Jean-Paul Rodrigue, Hofstra University, New York Email: [email protected]Paper available at: http://people.hofstra.edu/faculty/Jean- paul_Rodrigue

Transcript

International Workshop on New Generation Port Cities and Global Supply ChainsThe University of Hong Kong, 12-14 December 2005

New Port-Hinterland Relationships: Experiences from North America

Jean-Paul Rodrigue, Hofstra University, New York

Email: [email protected] available at:http://people.hofstra.edu/faculty/Jean-paul_Rodrigue

Integration Forces Shaping Hinterlands

Geographical Integration Functional Integration

Spatial fragmentation of production and consumption. Exploitation of comparative advantages.

Logistics & SCM. Integration between maritime and inland transport systems.

SM

D

Origin / Destination Relationships

D S M

1 2 3

1 2 3

S M D

S M D

Supply / Demand Relationships

Information Flows

Physical Flows

Supplying Manufacturing Distribution

Global Production Networks

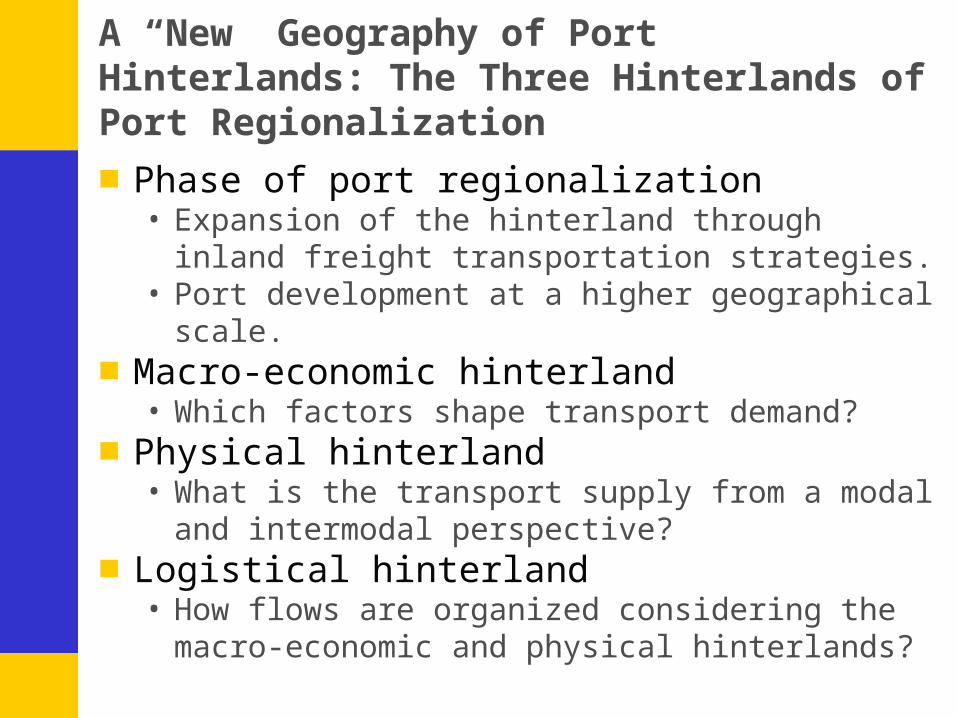

A “New” Geography of Port Hinterlands: The Three Hinterlands of Port Regionalization

■ Phase of port regionalization• Expansion of the hinterland through inland freight transportation

strategies.• Port development at a higher geographical scale.

■ Macro-economic hinterland• Which factors shape transport demand?

■ Physical hinterland• What is the transport supply from a modal and intermodal

perspective?■ Logistical hinterland

• How flows are organized considering the macro-economic and physical hinterlands?

Elements Logistical sites (production and consumption) as part of GPNs

Transport links and terminals

Mode, Timing, punctuality and frequency of services

Challenge International division of production and consumption

Additional capacity (modal and intermodal)

Supply chain management

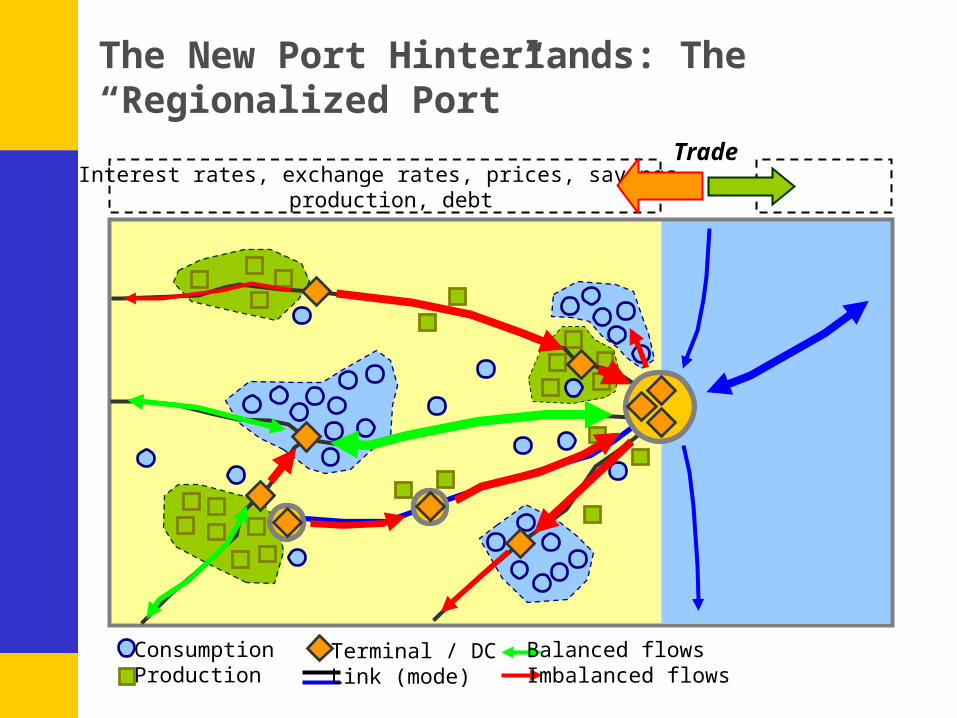

The New Port Hinterlands

■ Macro-economic port regionalization in North America• Tremendous growth in transport demand.• Shifting comparative advantages; less production but more

consumption.• De-industrialization, relocation and re-industrialization:

• The automotive industry is collapsing (GM, Ford, Delphi, etc).• Platform companies; emerging organizational/logistical structure.• Artificially induced demand; financial leverage; asset inflation and

debt.

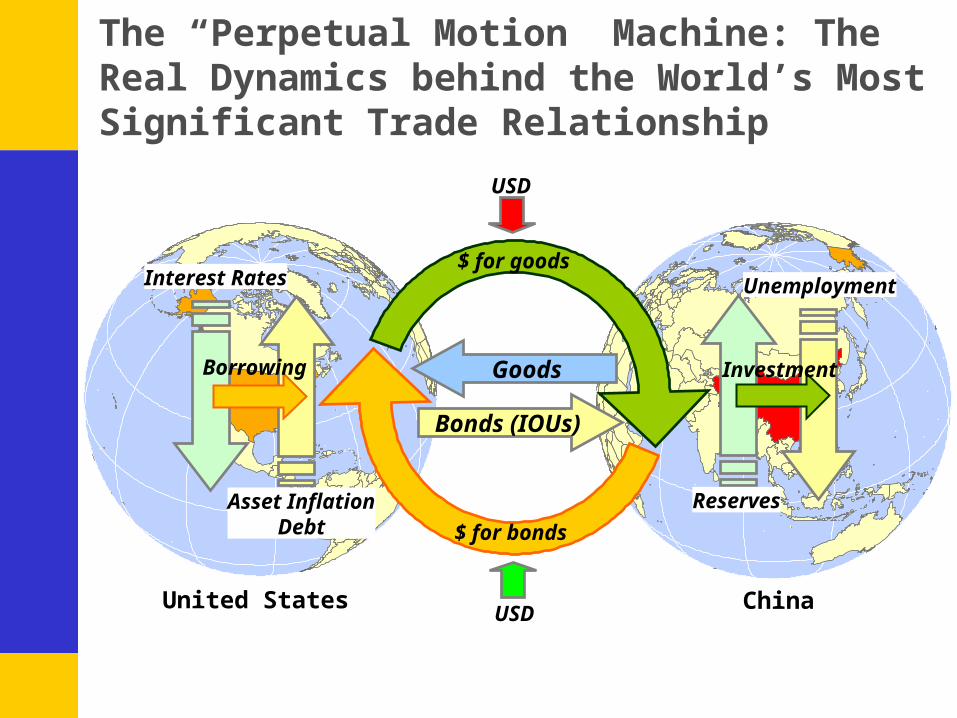

The “Perpetual Motion” Machine: The Real Dynamics behind the World’s Most Significant Trade Relationship

Goods

Bonds (IOUs)

Asset InflationDebt

Reserves

Interest Rates Unemployment$ for goods

$ for bonds

United States ChinaUSD

USD

Borrowing Investment

World’s 10 Largest Exporters and Importers, 2004

0 200 400 600 800 1000 1200 1400 1600

Germany

United States

China

Japan

France

Netherlands

Italy

United Kingdom

Canada

Belgium Imports

Exports

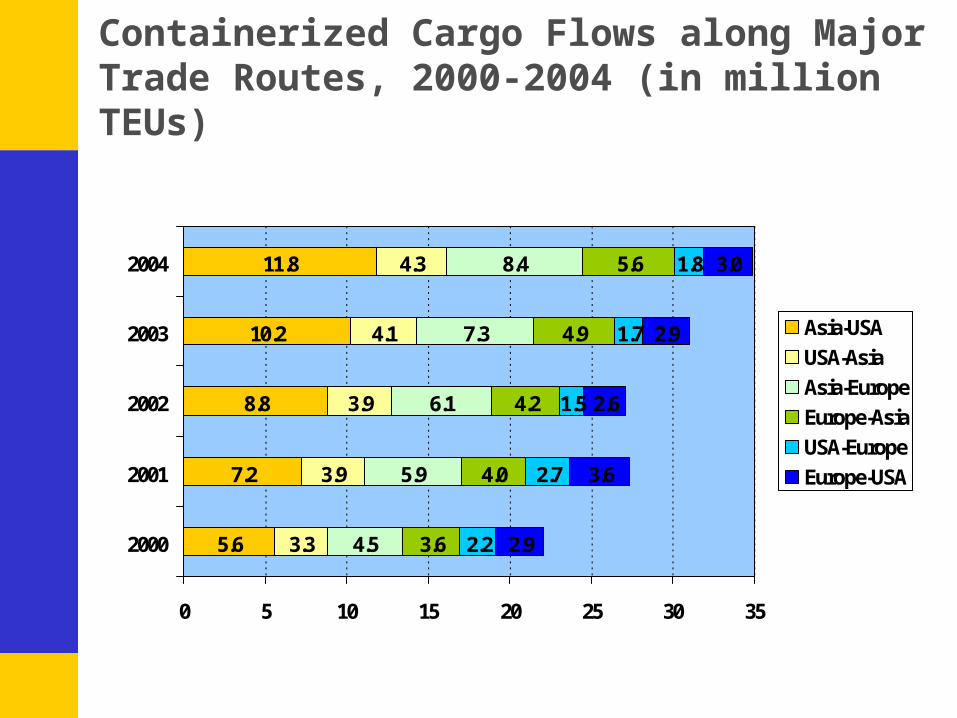

Containerized Cargo Flows along Major Trade Routes, 2000-2004 (in million TEUs)

5.6

7.2

8.8

10.2

11.8

3.3

3.9

3.9

4.1

4.3

4.5

5.9

6.1

7.3

8.4

3.6

4.0

4.2

4.9

5.6

2.2

2.7

1.5

1.7

1.8

2.9

3.6

2.6

2.9

3.0

0 5 10 15 20 25 30 35

2000

2001

2002

2003

2004

Asia-USA

USA-Asia

Asia-Europe

Europe-Asia

USA-Europe

Europe-USA

The Physical Hinterland

■ Physical port regionalization in North America• Capacity demands from long distance trade.• Port ranges; lateral corridors of port competition / cooperation.• Gateways; logistical platforms.• Inland freight corridors.

Traffic at the 50 Largest Container Ports, 2003

DubaiJeddah

Tacoma

Colombo

Salalah

Oakland

San Juan

Melbourne

Long Beach Charleston

Nhava Sheva

Los Angeles Hampton RoadsNew York/New Jersey

Kobe

Osaka

Tokyo

BusanNagoya

Dalian

Ningbo

Manila

Xiamen

Tianjin

Keelung

Quingdao

ShanghaiShenzhen

Kaohsiung

Hong Kong

Guangzhou

Singapore

Port Kalang

Laem Chabang

Tanjung Perak

Tanjung Priok

Tanjung Pelepas

Less than 2 million TEU

2 to 4 million TEU

4 to 7 million TEU

7 to 10 million TEU

More than 10 million TEU

Genoa

Piraeus

LeHavreAntwerp

Hamburg

Valencia

Barcelona

Algeciras

Rotterdam

Felixstowe

Gioia Tauro

Pacific Asia Europe

Traffic at Major North American Container Ports, 2003

El Paso

Chicago

Kansas CIty

Minneapolis

Salt Lake City

Tampa

Ponce

Miami

Tacoma

Mobile

Fraser

BostonAlbany

Tampico

Toronto

Seattle

Oakland

Manatee

Hueneme

Houston

HalifaxEverett

Mazatlan

Ensenada

Veracruz

ProgresoAltamira

Savannah

San Juan

Portland

Montreal

Gulfport

Freeport

Vancouver

San Diego

Canaveral

Baltimore

Manzanillo

Wilmington

St. John's

Saint John

Palm Beach

Long Beach

Fernandina

Charleston

Salina Cruz

New Orleans

Los Angeles

Richmond(VA)

Portland(ME)

Philadelphia

Lake Charles

Jacksonville

San Francisco

Hampton Roads

Puerto Morelos

Wilmington(NC)

Lazaro Cardenas

Port Everglades

New York/New Jersey

TEU (2003)

Less than 100,000

100,000 to 300,000

300,000 to 1 million

1 million to 2 million

More than 2 million

Cargo Handled by the Top 5 US Container Ports, 1984-2004 (in TEUs)

0

5

10

15

20

25

30

35

40

Mill

ions

42%

44%

46%

48%

50%

52%

54%

56%

58%

New York/New Jersey

Charleston

Oakland

Los Angeles

Long Beach

Total

Top 5 share

DeconcentrationRegionalization

Major Modal US Gateways, 2003

Newark

Chicago

Atlanta

Cleveland

New Orleans

Dallas-Fort Worth

Boston Logan AirportJFK International Airport

Seattle-Tacoma International

Miami International Airport,

Los Angeles International Airport

Philadelphia International AirportSan Francisco International Airpor

Port of Miami

Port of Tacoma

Port of Seattle

Port of Houston

Port of Oakland

Port of Beaumont

Port of Portland

Port of New York

Port of Savannah

Port of Baltimore

Port of CharlestonPort of Long Beach

Port of New Orleans

Port of Morgan City

Port of Los Angeles

Port of Philadelphia

Port of Jacksonville

Port of Norfolk Harbor

Port of Corpus ChristiPort of Port Everglades

Port of Huron

Port of Blaine

Port of Laredo

Port of Hidalgo

Port of El Paso

Port of Pembina

Port of Detroit

Port of Nogales

Port of Sweetgrass

Port of Calexico-East

Port of Alexandria Bay

Port of Otay Mesa Station

Port of Brownsville-Cameron

Port of Champlain-Rouses Pt.

Port of Buffalo-Niagara Falls

Land Gateways

$54 billion

Exports

Imports

Port Gateways

$69 billion

Exports

Imports

Air Gateways

$51 billion

Exports

Imports

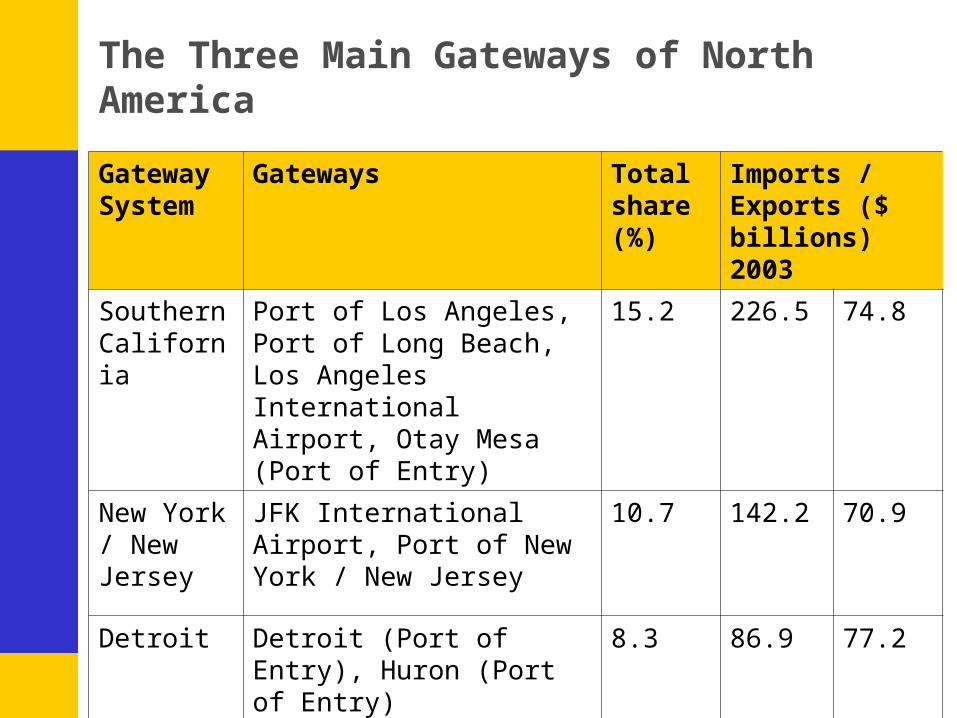

The Three Main Gateways of North America

Gateway System

Gateways Total share (%)

Imports / Exports ($ billions) 2003

Southern California

Port of Los Angeles, Port of Long Beach, Los Angeles International Airport, Otay Mesa (Port of Entry)

15.2 226.5 74.8

New York / New Jersey

JFK International Airport, Port of New York / New Jersey

10.7 142.2 70.9

Detroit Detroit (Port of Entry), Huron (Port of Entry)

8.3 86.9 77.2

Trucking Corridors and Major Metropolitan Freight Centers (more than 3,000 trucks per day)

Miami

Tampa

Boston

Dallas

Denver

Halifax

Atlanta

Detroit

Toronto

Chicago

Houston

Phoenix

Seattle

Calgary

Montreal

New York

Portland

Baltimore

Charlotte

Cleveland

St. Louis

San Diego

Vancouver

Pittsburgh

Cincinnati

New Orleans

Kansas City

Minneapolis

Los Angeles

Philadelphia

San Francisco

Major Road Traffic Bottlenecks

Number of North American Ports by Channel Depth (feet)

0 10 20 30 40 50 60

Above 76

71 - 75

66 - 75

61 - 65

56 - 60

51 - 55

46 - 50

41 - 45

36 - 40

31 - 35

26 - 30

LargeMediumSmall

The Logistical Hinterland

■ Logistical port regionalization in North America• Empty containers repositioning; coping with imbalances.• Modal shift; coping with congestion and costs.• Corridor flows; coping with the existing spatial structure along the

Boston – Washington corridor.

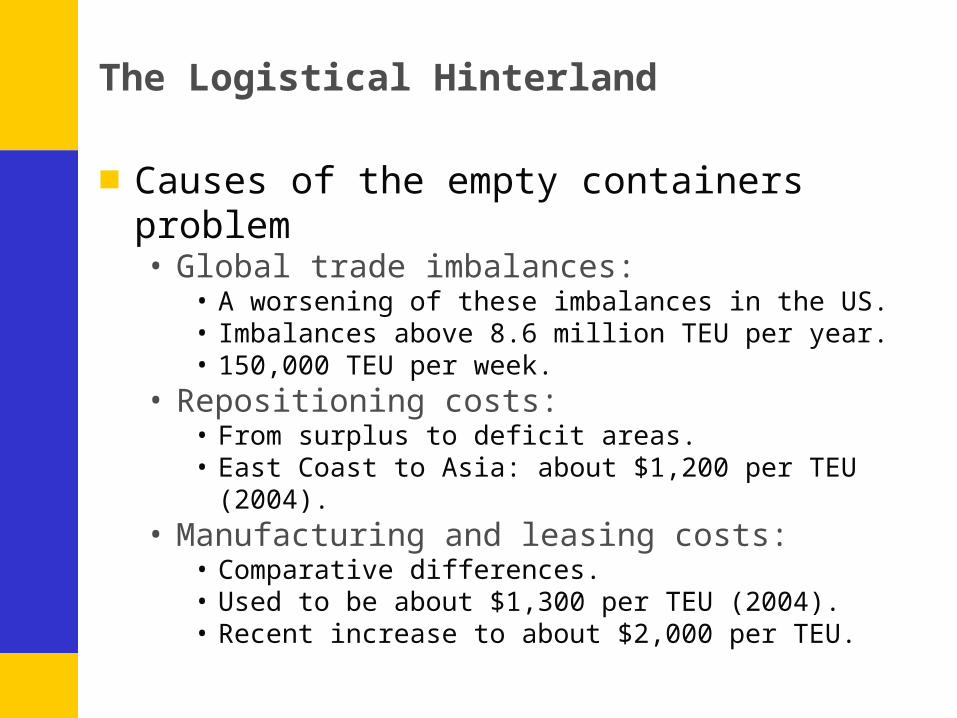

The Logistical Hinterland

■ Causes of the empty containers problem• Global trade imbalances:

• A worsening of these imbalances in the US.• Imbalances above 8.6 million TEU per year.• 150,000 TEU per week.

• Repositioning costs:• From surplus to deficit areas.• East Coast to Asia: about $1,200 per TEU (2004).

• Manufacturing and leasing costs:• Comparative differences.• Used to be about $1,300 per TEU (2004).• Recent increase to about $2,000 per TEU.

Container Repositioning Scales

Repositioning Distance (TEU – KM)

Repositioning Costs

LocalRegional

Internatio

nal

Container manufacturing cost

Reshuffling Storage depots

High imbalance

Low imbalance

Gateways as reverse logistics centers

Containers Handled by the Port of New York, 2001-2004

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

2001 2002 2003 2004

Empty TEUs

Loaded TEUs

The Logistical Hinterland

■ Inertia in modal shift• Does not occur as fast as expected.• Transport economics hint at a gradual process.• Reasons for inertia:

• Accumulated investments / stakes in modes and terminals.• Management preferences.• Proven reliability.

■ North American hinterlands and modal shift• Particularly takes place at the fringe.• A port competition through regional modal cooperation.

MaturityShiftInertia

Principles of Modal Shift

Modal Share (A

/B)

Time

Comparative AdvantagesReal Modal Share

Expected Modal Share

Underperformance

Over performance

Costs of Shipping a 40 foot Container to New York: Towards a $100 per Barrel Logistics?

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Barrel at $30 Barrel at $60 Barrel at $100

From Hong Kong

From Mexico

Some Short Sea Shipping Systems in North America

East Coast Port Inland Distribution Network (New York, Boston, Albany).

Columbia Coastal; Several East Coast ports linked, new Philadelphia – Baltimore container barge service.

Great Lakes Detroit-Windsor Truck Ferry. Rochester-Toronto Fast Ferry.

Gulf Coast Teco Ocean Shipping; bulk commodities.

Osprey Lines; container-on-barge services in Texas, Mississippi River service (Baton Rouge to New Orleans).

West Coast Totem Ocean Trailer Express (Ro/Ro), Horizon Lines and Lynden Transport (Alaska and Washington).

The Boston / Washington Port Hinterland

Virginia Inland Port

Camden

Albany

ReadingHanover

WorcesterFramingham

Springfield

East Hartford

Boston

Albany

Camden

Davisville

Wilmington BridgeportNew York / New Jersey

§

PIDN Barge Ports

Active

Study

PIDN Rail Hub

Active

Study

Rail Service Status

Active

Study

Barge Service Status

Active

Study

Rail / Road Terminal

Interstate0 60 120 180 24030

Kilometers

Conclusion

■ What’s next for North American hinterlands?• Anticipated growth of freight flows:

• Both in tons and tons-km.• Additional demands on the capacity of modes and terminals to handle

them.• Unlikely to take place.

• Imbalanced freight flows:• Disequilibrium in the division of labor, trade, production and consumption.• Short/medium term: additional pressures to manage the disequilibrium

(e.g. empties).• Long term: rebalancing the flows and the hinterlands.

• Regionalization of hinterlands:• Ports adapting to the freight flows reality.• Attempt at re-balancing by offering a wider hinterland range.