22

Intro to Financial Management Risk and Return

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | reynold-cannon |

| View: | 218 times |

| Download: | 2 times |

Intro to Financial Management

Risk and Return

Review

• Homework• What is “the time value of money?”• How do you calculate and what do these ratios mean?

– Current ratio– Acid-test– Inventory turnover– ROS, Return on sales– ROA, Return on assets– ROE, Return on equity– Debt ratio– Leverage ratio– P/E

Review

• How do you calculate and what do these ratios mean?– Current ratio– Acid-test– Accounts receivable turnover– Inventory turnover– Operating return on assets– Operating profit margin– Asset turnover– Accounts receivable turnover– Debt ratio– Leverage ratio– ROE– P/E

Returns

• Holding period– Return– Rate of return

• Expected cash flow– Weighted average of all possible cash flows– Deal or No Deal

• Expected rate of return– Weighted average of all possible returns– E.g. 90% probability of getting $1, 10% probability of $0– Use 6r

Risk

• Clearly important– What is it?– If it’s important, we need to measure it

• “What defines modern times is the mastery of risk”

• In finance, risk is the standard deviation of future returns– Other measures have been tried– Note that standard deviation includes upside risk– Most investors only care about downside risk (behavioral)

– σ = sqrt( Ʃ(ri - 6r )2 * P(ri) )

• Compare two different investments– T-bill at 4%– Stock with range of returns

Investors’ Risk and Return

Risk – By Asset Class

Worst Annual Return

Since 1925Average Annual Return

Since 1925

Stocks-43.4%

(-67.6% worst 12 mo.)9.6%

(162.9% best 12 mo.)

Bonds -7.8% 5.5%

Cash .1% 3.7%

Sources: personal.fidelity.com, Morgan Stanley, www.efficientfrontier.com, Federal Reserve – St. Louis

Investors’ Risk and Return

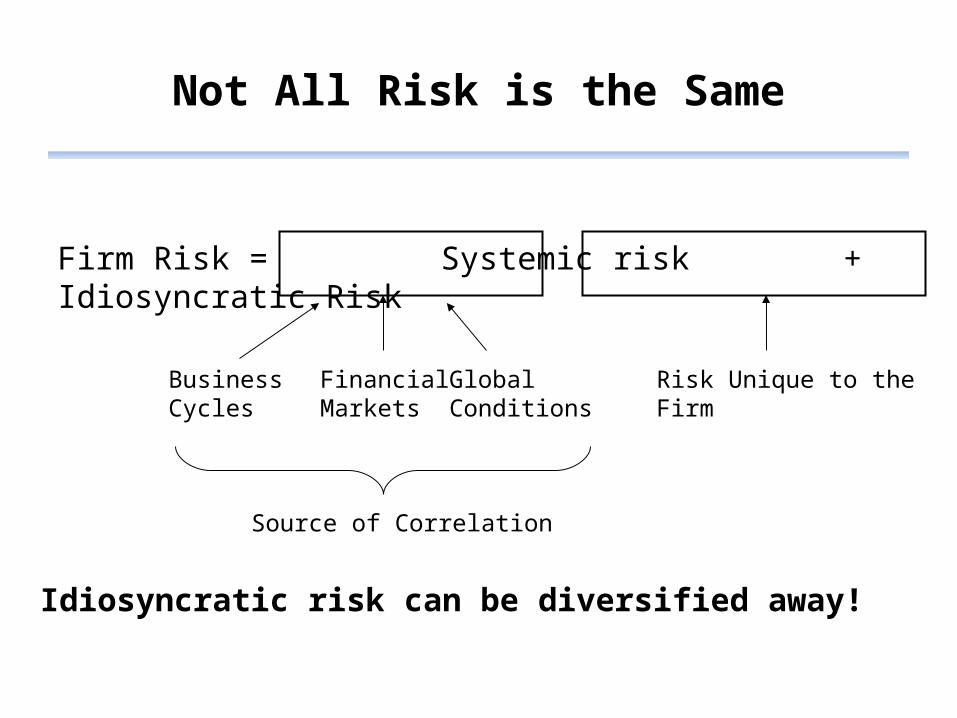

Not All Risk is the Same

Firm Risk = Systemic risk + Idiosyncratic Risk

BusinessCycles

FinancialMarkets

GlobalConditions

Risk Unique to theFirm

Source of Correlation

Idiosyncratic risk can be diversified away!

Diversification – Simple Example

IBM and AT&T

When IBM went down, AT&T went up.When AT&T went down, IBM went up.

If stocks are perfectly positively correlated, diversification has no effect on risk

If stocks are perfectly negatively correlated, portfolio is perfectly diversified.

What do you want as an investor?

Risk and Diversification

With large portfolio, 30 – 200 stocks, idiosyncratic moves cancel out!

Market Risk

• Have to decide what the “market” is.– DJIA?– S&P 500?

• Pick a benchmark

• Calculate holding period returns for the benchmark• Calculate holding period returns for investment• Compare them

Characteristic Line

Source: Wikipedia, characteristic line.

Note: the slope is the change in portfolio divided by the change in the market – beta β

Characteristic line is the best fit line for the points.

Beta

• Measures the relationship between an investment’s returns and the market’s returns

• Beta is the risk that is left after having diversified the portfolio

• Interpreting beta– < 1 less risk than the market. When the market goes up (down),

the investment goes up (down) to a smaller degree– = 1 same risk as the market– > 1 more risk than the market. When the market goes up

(down), the investment goes up more (less) to a greater degree

Understanding Beta

• Rank the beta of these companies

– Walmart– Ford– McDonalds– Bank of America– AT&T– JP Morgan– Apple– Microsoft

Understanding Beta

• Rank the beta of these companies

– Walmart .36– McDonalds .46– AT&T .60– Apple .82– Microsoft .99– JP Morgan 1.24– Bank of America 2.19– Ford 2.37

Source: finance/yahoo.com Jan. 16, 2012

Calculating Portfolio Beta

portfolio= Σ wj*j

Where

wj = % invested in stock

I = Beta of stock j

Asset Allocation

• How investor spreads portfolio across investments

• Single biggest determinate of investment results

Required Rate of Return

• Minimum rate of return necessary to attract an investor– Includes opportunity cost of next best investment

Require rate of return = risk-free rate of return + risk premium

• Use U.S. Treasury Bill rate as risk-free rate

• Risk premium is the return we require for taking risk

Capital Asset Pricing Model (CAPM)

•Beta is the determinate of required returns• rf is the rate of U.S. T-Bills (known)

• rm is the market return (known)

• r is then determined by β

CAPM Examples

• Risk-free rate = .02%• Market risk = 9%• What is required rate of return if beta = 0, 1, 2?

• What if the risk-free rate rises to 4%?

• What if the market risk = 12%?

Security Market Line

Graph of the CAPM