57

INTRODUCTION TO FHA | JUNE, 2016

INTRODUCTION TO FHA | JUNE, 2016

INTRODUCTION TO THE FHA LOAN PROGRAM

Introduction to FHA 2

The Federal Housing Administration (FHA) is a division of the U.S. Department of Housing and Urban Development (HUD). The goals of this division are to:

Insure FHA mortgage loans (also known as government mortgages) Expand homeownership opportunities Increase minority homeownership Make the home buying process less complicated and expensive Assist existing homeowners in avoiding foreclosure

FHA-insured mortgages can be used to purchase homes and to refinance existing mortgages. FHA loans are designed for low to moderate income borrowers who are unable to make a large down payment. The most popular FHA loan has a minimum cash investment requirement of 3.5 percent but permits 100 percent of the money needed at closing to be a gift from an acceptable source or an acceptable secondary financing source.

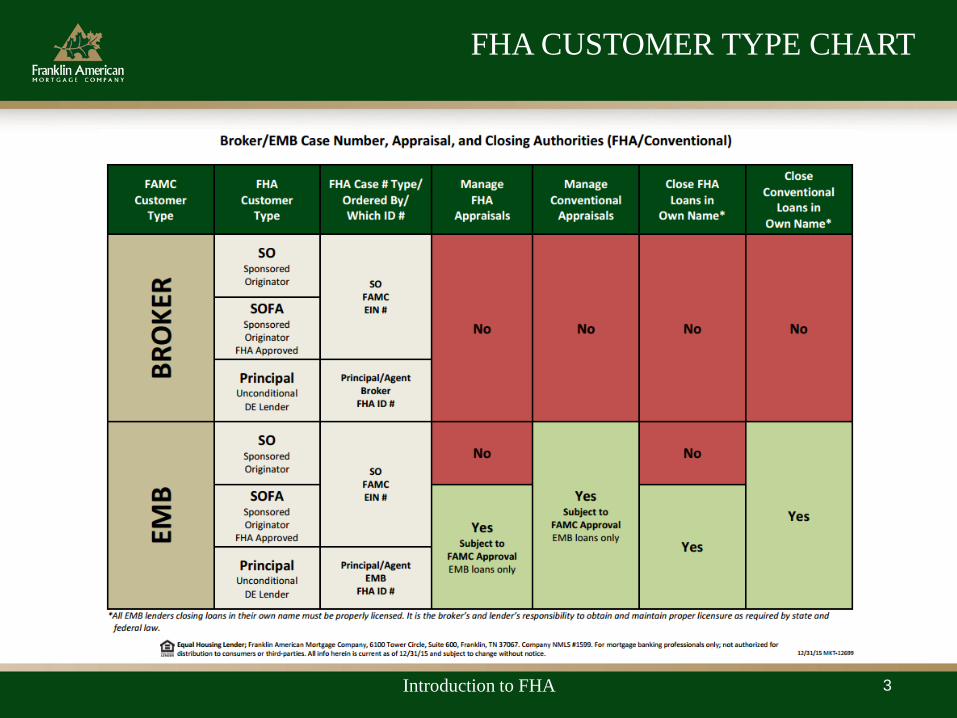

FHA CUSTOMER TYPE CHART

Introduction to FHA 3

FHA Features and Benefits

• Lower downpayment at competitive rates

• Total cash investment may be as low as 3.5%

• Loan(s) to 100% of total investment with gift from an eligible source

• Seller may pay pre-paids & closing costs up to 6% (or may be paid by broker through "premium pricing")

• Cash reserves as required by AUS (except for 3 and 4 units, then 3-month PITI needed or as required per Manual underwriting requirements)

• Minimum credit score of 620 (streamlines require 640)

• Higher and flexible qualifying ratios

• Non-occupying co-borrowers allowed on purchase and rate/term refinance loans

• Upfront MIP may be financed

• Borrower may request "Streamline Refinance" (to reduce rate and payment)

• FHA Loans are assumable (and require qualifying)

• No pre-payment penalties

FHA PROGRAM BENEFITS

Introduction to FHA 4

Required Disclosures

In addition to the required RESPA disclosures FHA requires the following additional disclosures: FAMC Submission Form

• Can be found on the FAMC Website

• www.franklinamerican.com>Forms>FHA

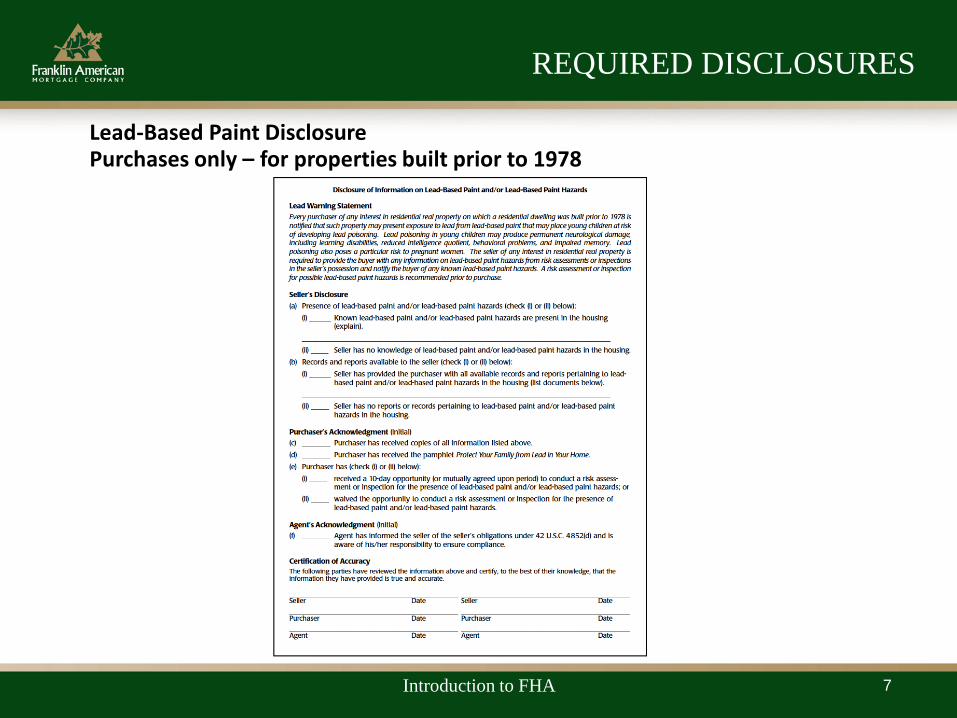

Lead Based Paint Disclosure

• Executed at application

• May be part of the purchase agreement

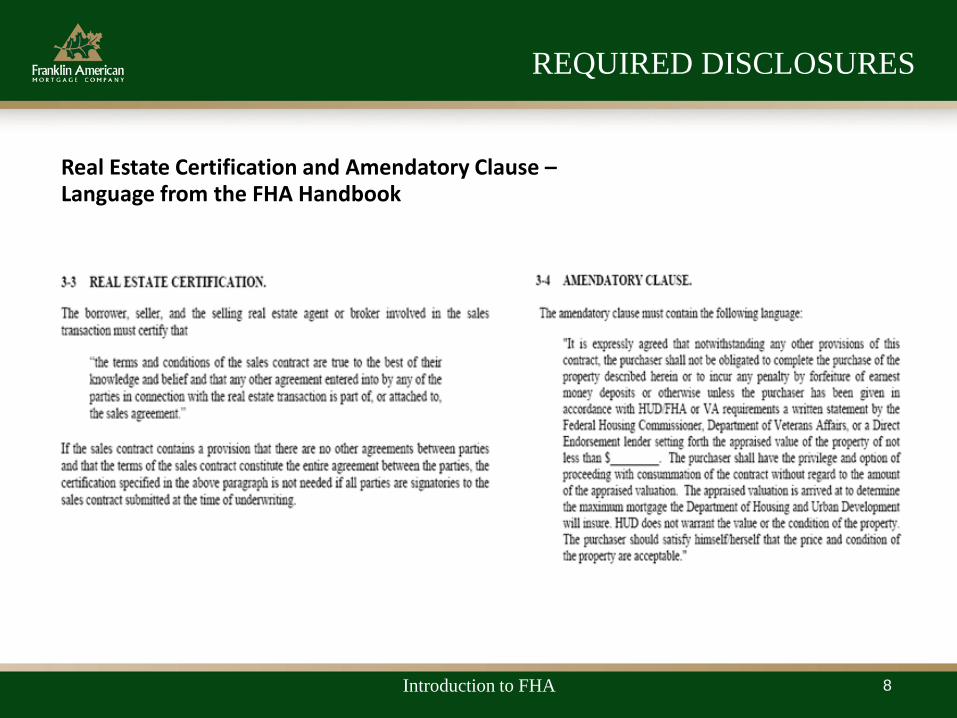

Real Estate Certification

• A separate certification is not needed if the sales contract contains a statement that there are no other

agreements between parties and the terms constitute the entire agreement between the parties, and all

parties are signatories to the sales contract submitted at the time of underwriting.

Amendatory Clause

• Must be signed and dated prior to final underwriting approval if the Conditional Commitment was not

provided to the borrower before executing the sales contract.

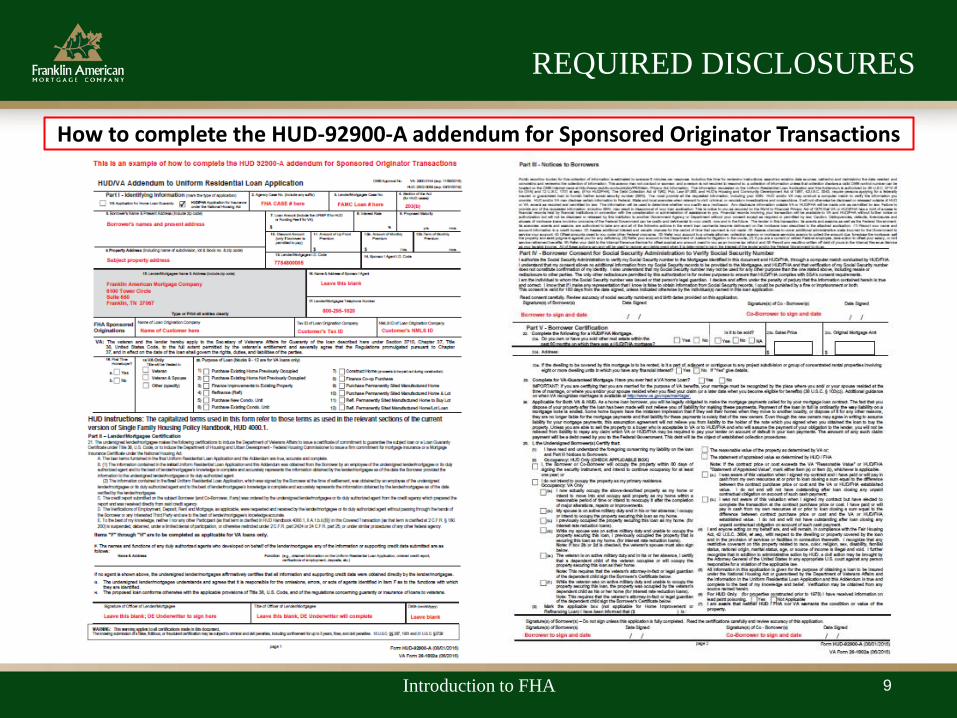

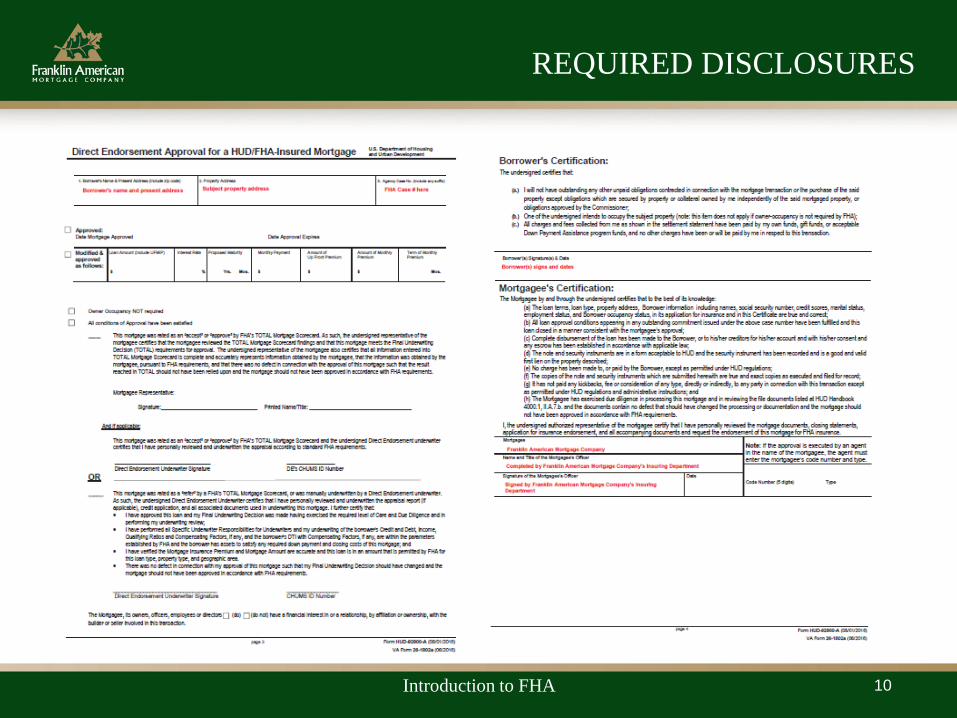

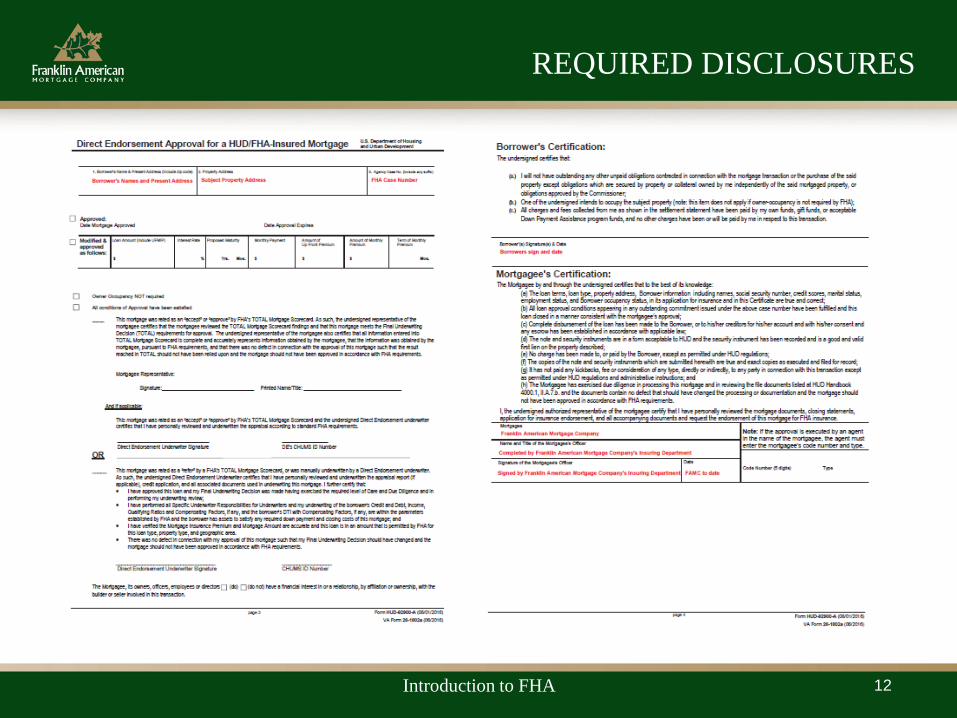

Initial HUD/VA Addendum to Uniform Residential Loan Application - HUD 92900-A

• Executed at application

• Pages 1 and 2 signed at initial application

• Pages 1 through 4 signed at closing

REQUIRED DISCLOSURES

Introduction to FHA 5

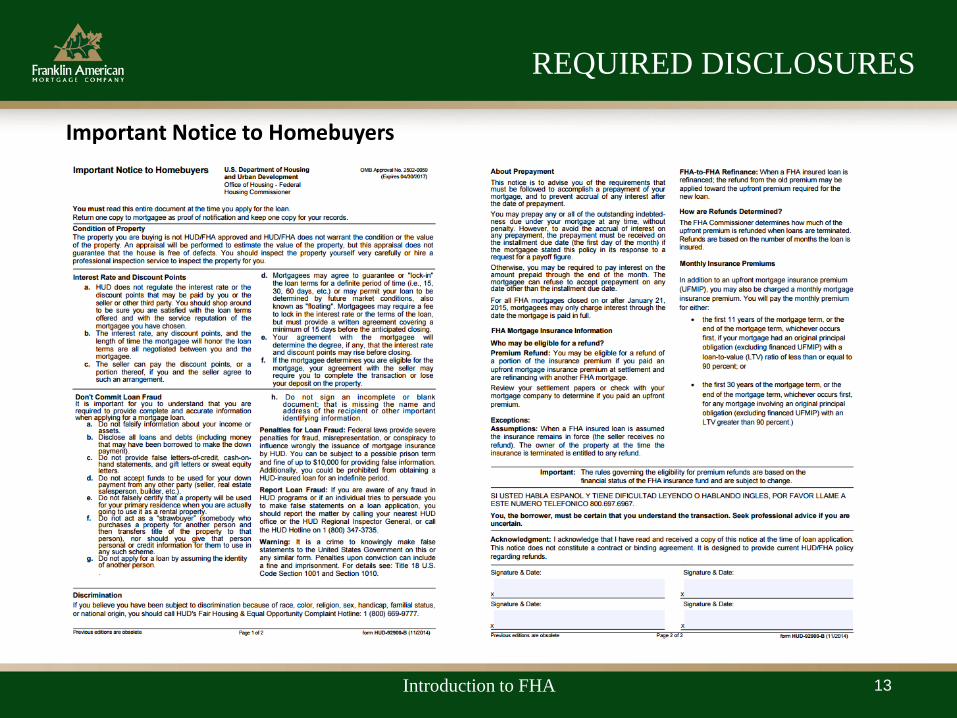

Required Disclosures, Continued Important Notice to Homebuyers – HUD 92900-B

• Executed at application

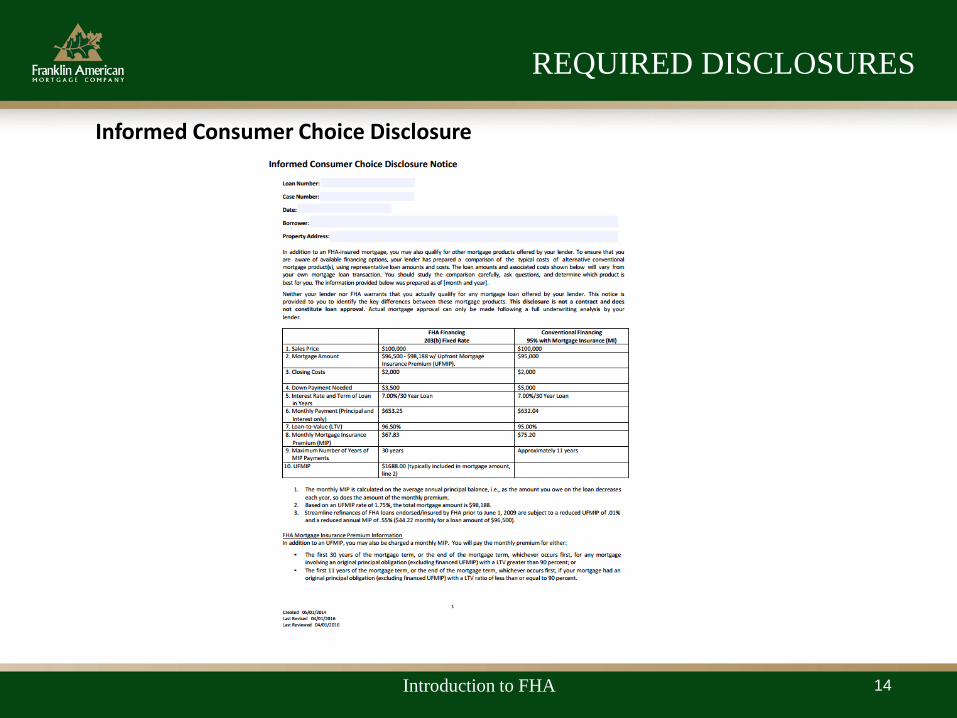

Informed Consumer Choice Disclosure Notice

• Executed at application

FHA ARM disclosure (if applicable)

• Provide to borrower within 3 days of application

• 5/1 ARM disclosures can be found on our website at: www.franklinamerican.com

FHA FORMS AVAILABLE AT:

http://portal.hud.gov/hudportal/HUD?src=/program_offices/administration/hudclips/forms

REQUIRED DISCLOSURES

Introduction to FHA 6

Lead-Based Paint Disclosure Purchases only – for properties built prior to 1978

REQUIRED DISCLOSURES

Introduction to FHA 7

Real Estate Certification and Amendatory Clause – Language from the FHA Handbook

REQUIRED DISCLOSURES

Introduction to FHA 8

REQUIRED DISCLOSURES

Introduction to FHA 9

How to complete the HUD-92900-A addendum for Sponsored Originator Transactions

REQUIRED DISCLOSURES

Introduction to FHA 10

REQUIRED DISCLOSURES

Introduction to FHA 11

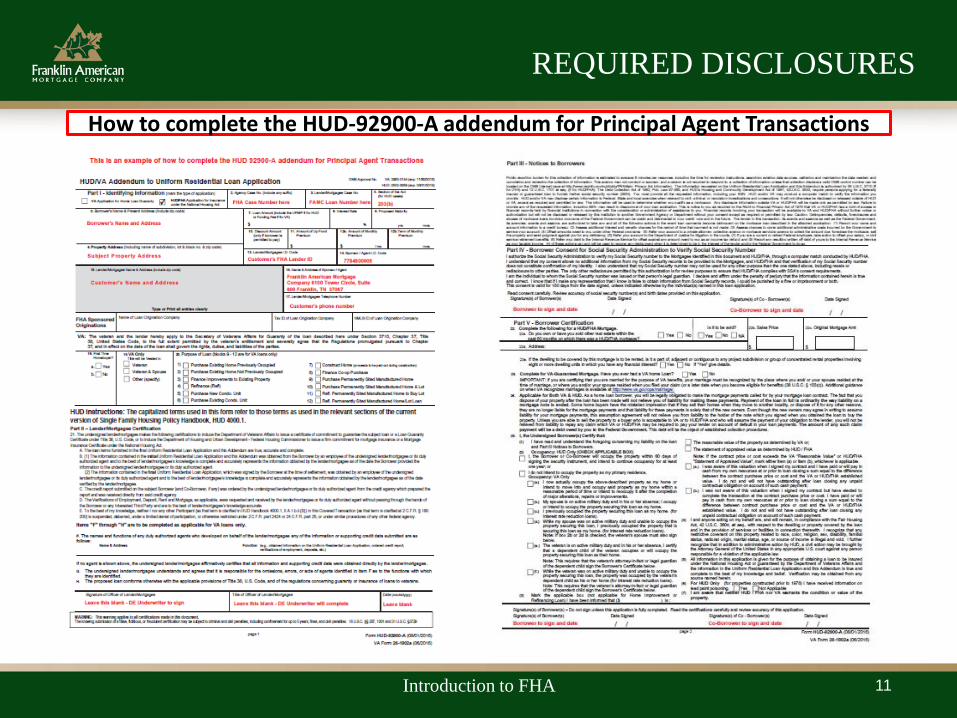

How to complete the HUD-92900-A addendum for Principal Agent Transactions

REQUIRED DISCLOSURES

Introduction to FHA 12

Important Notice to Homebuyers

REQUIRED DISCLOSURES

Introduction to FHA 13

REQUIRED DISCLOSURES

Introduction to FHA 14

Informed Consumer Choice Disclosure

CAIVRS All borrowers must be screened using CAIVRS (Credit Alert Interactive Voice Response System), except for

streamline refinances. CAIVRS is a Federal government-wide repository of information on those individuals

with delinquent or defaulted federal debt, or who have had an FHA or VA insurance claim paid on a previous

mortgage loan.

Delinquent Federal Debts Delinquent Federal Non-Tax Debt

Borrowers are ineligible for an FHA insured mortgage with delinquent federal non-tax debt, including

deficiencies and other debt associated with past FHA-insured mortgages.

• Any debt that is confirmed as valid and in delinquent status must be resolved in order for a borrower to

become eligible

• Documentation must be included in the file from the creditor agency to support the verification and

resolution of the debt. A clear CAIVRS report is required for all debt reported through CAIVRS.

If a borrower is currently delinquent on an FHA-insured mortgage, they are ineligible for a new FHA-insured

mortgage unless the delinquency is resolved.

CAIVRS AND DELINQUENT DEBT

Introduction to FHA 15

Delinquent Federal Debts, continued Delinquent Federal Tax Debt

Borrowers with delinquent federal tax debt and no valid repayment agreement in place are ineligible.

Tax liens may remain unpaid if:

• The borrower has entered into a valid repayment agreement with the federal agency owned to make

regular payments, AND

• The borrower has made at least three of the scheduled payments on time. The borrower cannot prepay

scheduled payments in order to meet the required minimum of three months of payments.

• Verification that the borrower does not have a lien against their property for a debt owed to the federal

government. If a lien is in place, the lien holder must subordinate the tax lien to the new FHA-insured

mortgage.

• Documentation from the IRS evidencing the repayment agreement and verification of payments made

must be included in the file.

• The payment amount must be included in the DTI ratio.

CAIVRS AND DELINQUENT DEBT

Introduction to FHA 16

LDP/SAM

Suspended and Debarred Individuals

The following entities must be checked against HUD's Limited Denial of Participation (LDP) list at

http://portal.hud.gov/hudportal/HUD?src=/topics/limited_denials_of_participation or the System for Award

Management (SAM) Excluded Party List https://www.sam.gov/. Any entity noted on either of the LDP or SAM

lists will cause the loan to be ineligible.

• Borrower(s)

• Seller(s)

• Loan Officer

• Loan Processor

• Loan Underwriter

• Listing Agent

• Selling Agent

• Appraiser

• Settlement Agent

NOTE: FAMC is responsible for checking the LDP/SAM list on all entities.

LDP/SAM

Introduction to FHA 17

Requesting a Case Number

When can I request a Case Number?

The loan must first be locked or registered with FAMC and a copy of the URLA/1003 must be provided.

Remember to also account for any Compliance-related waiting periods before ordering the appraisal.

How do I request a Case Number?

The FHA Case Number Request Form for SOs must be fully completed and sent to FAMC via email.

Where do I send my Case Number request?

A specific FHA Case Number Request email address has been created for each Operations Center. Please

submit your request to the corresponding office for that loan file.

California Operations Center: [email protected]

Massachusetts Operations Center: [email protected]

Tennessee Operations Center: [email protected]

Texas Operations Center: [email protected]

Pennsylvania Operations Center: [email protected]

CASE NUMBER REQUEST

Introduction to FHA 18

Requesting a Case Number, Continued Who is eligible for this service?

We will provide this service to any of our business partners that are Sponsored Originators.

When should I expect to receive my Case Number?

If a fully completed request form is received by 4:00 PM local time, it will be processed the same day. However

it is very important to note that FAMC will not provide the Case Number Assignment until the following

business day, as the request must first pass FHA’s overnight validation process and be returned clear of any

warning messages.

Requests received after 4:00 PM local time will be treated as next day submissions.

Incomplete request forms will be processed once all necessary information is received, according to the

timeframe stated above.

How will the Case Number be returned to me?

FAMC will email the Case Number Assignment to the email address provided on the request form.

REQUESTING A CASE NUMBER

Introduction to FHA 19

Automated Underwriting

TOTAL is HUD’s proprietary credit evaluation system, used within an Automated Underwriting System (AUS)

to evaluate the borrower’s credit history and other application variables, and return either an

accept/approve recommendation or refer the loan for traditional underwriting. TOTAL is automatically

accessed when an FHA loan is submitted for underwriting via previously-approved AUS products, including

Freddie Mac's Loan Prospector (LP) and Fannie Mae’s Desktop Underwriter (DU) system. All FHA loans must

be scored through TOTAL with the exception of Streamline Refinance Transactions.

On-line Resources

HUD's "Home Page" links to a broad variety of HUD-related topics. HUD’s “Lenders Page” links to specific

FHA lending information, including mortgagee letters, mortgage limits, program descriptions, HUD contacts,

phone numbers, e-mail addresses, etc.

HUD Home Page: http://www.hud.gov/

Lenders Page: http://www.hud.gov/groups/lenders.cfm

Mortgagee Letters: http://www.hud.gov/offices/adm/hudclips/letters/mortgagee/

RESOURCES AND TECHNOLOGY

Introduction to FHA 20

Resources and Technology The best way to stay up to date with FHA requirements is to sign up for HUD’s Housing E-mail list:

http://portal.hud.gov/hudportal/HUD?src=/subscribe

FHA Resource Center: search online knowledge base: http://portal.hud.gov/hudportal/HUD?src=/library

HUD Handbook 4000.1 is a consolidated, consistent, and comprehensive single source for FHA Single Family

Housing Policy.

Handbook is accessible via HUD Clips:

http://portal.hud.gov/hudportal/HUD?src=/program_offices/administration/hudclips/handbooks/hsgh

FAMC Wholesale Lending Website:

Handy links to the above and many other sources of industry information can be accessed at FAMC’s

website under “Resources”

https://www.franklinamerican.com/ext/wholesale?npage=wholesaleHome

RESOURCES AND TECHNOLOGY

Introduction to FHA 21

Helpful Links Please refer to the Franklin American Mortgage website under Resources for more

information.

http://www.hud.gov/ – HUD web address

http://portal.hud.gov/hudportal/HUD?src=/FHAFAQ – FHA Frequently Asked Questions Site

http://portal.hud.gov/hudportal/HUD?src=/program_offices/administration/hudclips – HUD clips where

you can find handbooks, mortgagee letters, and other processing and underwriting guidance

https://www5.hud.gov/Ecpcis/main/ECPCIS_List – HUD LDP list (must be checked for all parties to the

transaction including real estate agents, buyer, seller, appraiser, etc.)

https://entp.hud.gov/idapp/html/condlook.cfm – FHA approved condominium search (all condominiums

must be approved and listed on FHA’s list of approved condos)

https://entp.hud.gov/idapp/html/hicostlook.cfm – FHA maximum mortgage limits (check the maximum

mortgage limit for are in which you are lending. Limits are set based on state and county location)

HELPFUL FHA LINKS

Introduction to FHA 22

http://www.hud.gov/localoffices.cfm – List of HUD field offices

http://portal.hud.gov/hudportal/documents/huddoc?id=92900-lt.pdf

FORMS: FHA Loan Underwriting and Transmittal Summary

http://portal.hud.gov/hudportal/documents/huddoc?id=92800-5b.pdf

FORMS: Conditional Commitment

Resources to help struggling FHA homeowners learn their options to avoid foreclosure and scams:

• National Servicing Center:

http://portal.hud.gov/hudportal/HUD?src=/program_offices/housing/sfh/nsc

• HUD Approved Counseling Agencies: http://www.hud.gov/offices/hsg/sfh/hcc/hcs.cfm

• Customer-focused websites: http://portal.hud.gov/hudportal/HUD?src=/topics/avoiding_foreclosure

HELPFUL FHA LINKS

Introduction to FHA 23

Helpful Links, Continued

Sections of the Act

FHA Loan Programs come under the jurisdiction of HUD (the Department of Housing and Urban

Development). HUD has numerous loan programs known as "Titles."

• The home loan programs offered by FAMC and covered in this manual fall under the "Title II" program.

• FHA loan programs are known as "Sections", and each Section is associated with a number. Below is an

overview of these Sections.

203 (b) Description – Regular

• Fixed Rate or ARM

• Can be used for 1-4 unit properties

• Used for condos and PUDs

• Requires Upfront Mortgage Insurance Premiums (UFMIP) and Monthly Mortgage Insurance Premium (MIP)

• Most widely-used section

• Energy Efficient Mortgage (EEM)

FHA PROGRAMS (“SECTIONS”)

Introduction to FHA 24

Closing Costs

HUD allows FHA borrowers to pay reasonable and customary closing costs and fees that are

necessary to close the mortgage.

Non-Allowable Closing Costs

Federal, state, local regulations and predatory lending rules apply. Check your local and state

guidelines, they could be more restrictive.

Additional Closing Cost Guidelines

• Commitment (lock-in) fees require a written guarantee of the interest rate

and discount points (if any) for at least 15 days.

• Third-party fees may not be “marked up” (includes credit report, appraisal, title, etc.).

• Origination fee not limited to 1%.

CLOSING COSTS INFORMATION

Introduction to FHA 25

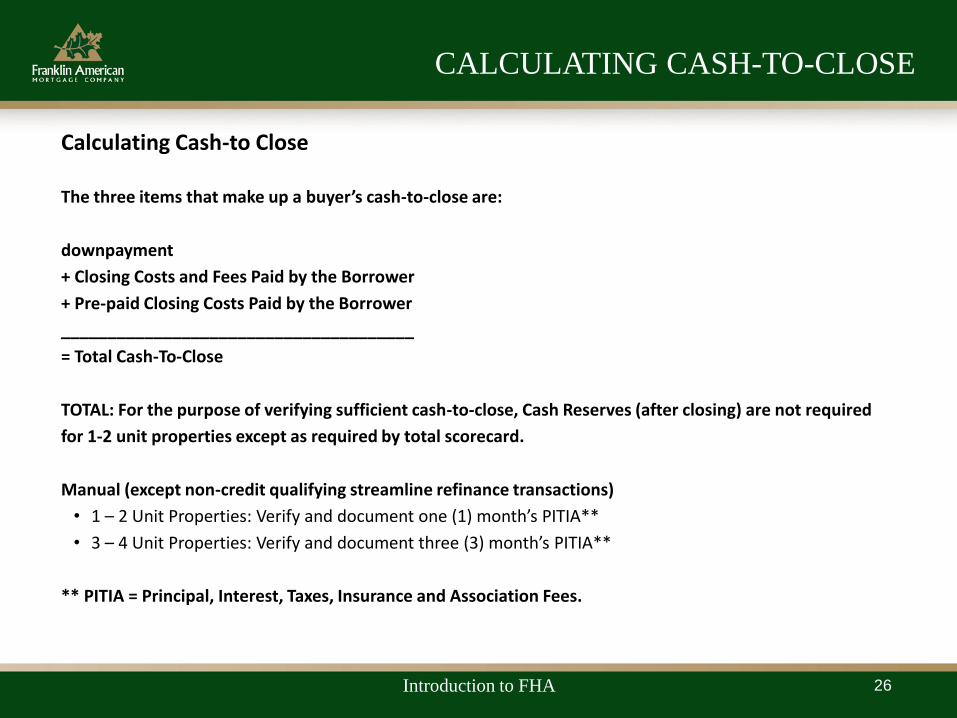

Calculating Cash-to Close

The three items that make up a buyer’s cash-to-close are:

downpayment

+ Closing Costs and Fees Paid by the Borrower

+ Pre-paid Closing Costs Paid by the Borrower

______________________________________

= Total Cash-To-Close

TOTAL: For the purpose of verifying sufficient cash-to-close, Cash Reserves (after closing) are not required

for 1-2 unit properties except as required by total scorecard.

Manual (except non-credit qualifying streamline refinance transactions)

• 1 – 2 Unit Properties: Verify and document one (1) month’s PITIA**

• 3 – 4 Unit Properties: Verify and document three (3) month’s PITIA**

** PITIA = Principal, Interest, Taxes, Insurance and Association Fees.

CALCULATING CASH-TO-CLOSE

Introduction to FHA 26

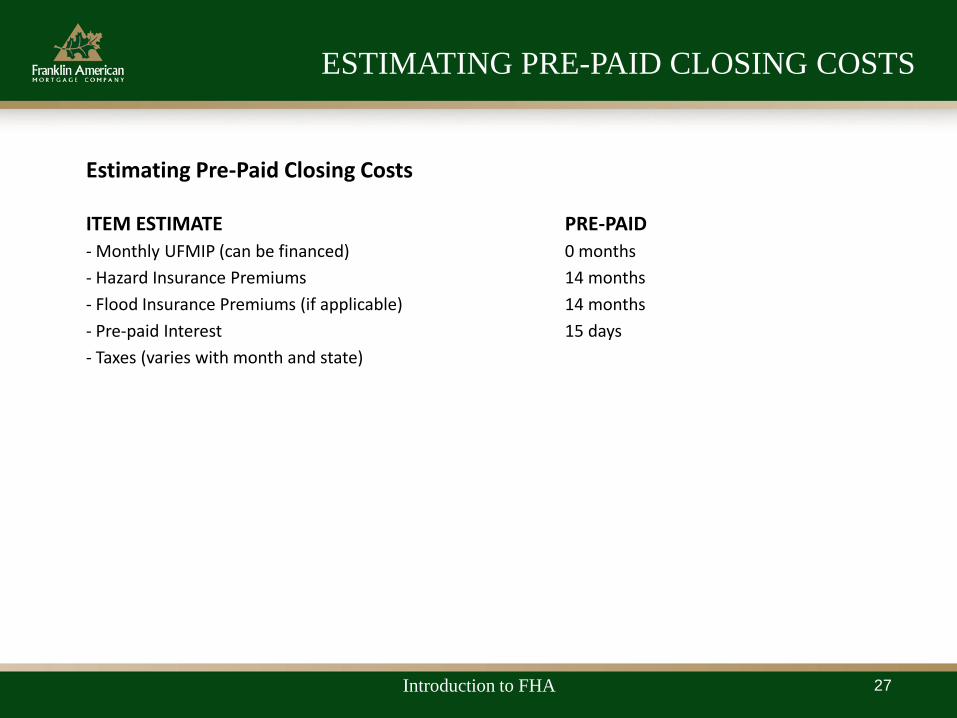

Estimating Pre-Paid Closing Costs

ITEM ESTIMATE PRE-PAID

- Monthly UFMIP (can be financed) 0 months

- Hazard Insurance Premiums 14 months

- Flood Insurance Premiums (if applicable) 14 months

- Pre-paid Interest 15 days

- Taxes (varies with month and state)

ESTIMATING PRE-PAID CLOSING COSTS

Introduction to FHA 27

Upfront Mortgage Insurance Premium An Upfront Mortgage Insurance Premium (UFMIP) is required on all FHA mortgage programs offered by

Franklin American Mortgage Company. The maximum mortgage may never exceed the statutory limits,

except by the amount of financed UFMIP.

Monthly Mortgage Insurance Premium FHA mortgages require an additional Mortgage Insurance Premium (MIP) that is collected monthly. The

percentage amount of the monthly premium varies by program, LTV, and loan term.

FHA Simple and Streamline submissions MUST include a copy of the “Refinance Authorization/Credit

Query” documenting the original endorsement date (see below).

UPFRONT /ANNUAL MORTGAGE

INSURANCE PREMIUMS

Introduction to FHA 28

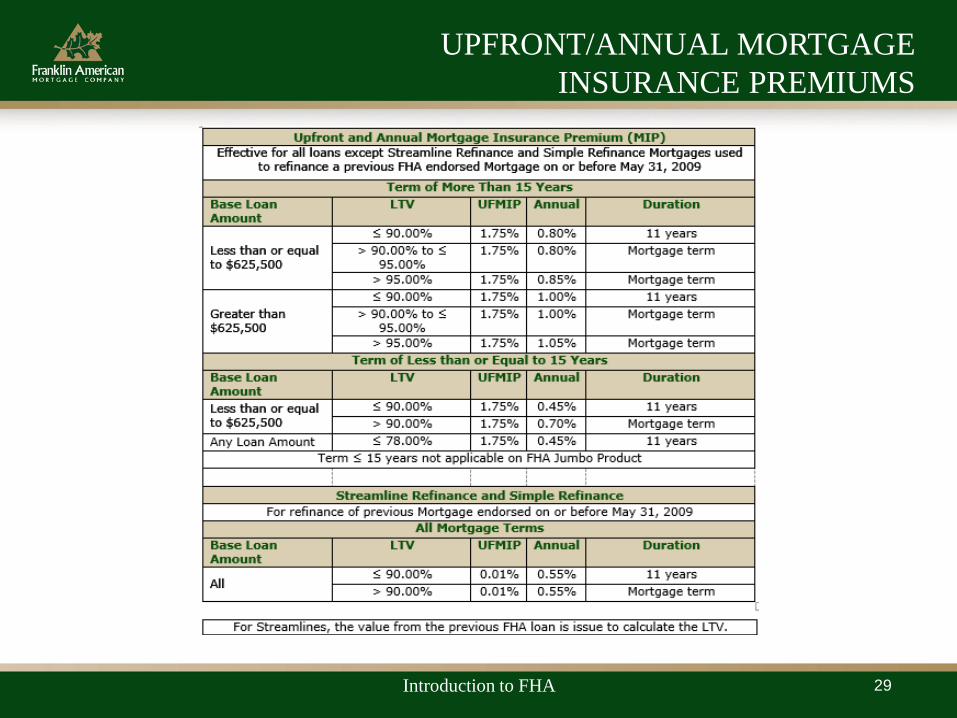

UPFRONT/ANNUAL MORTGAGE

INSURANCE PREMIUMS

Introduction to FHA 29

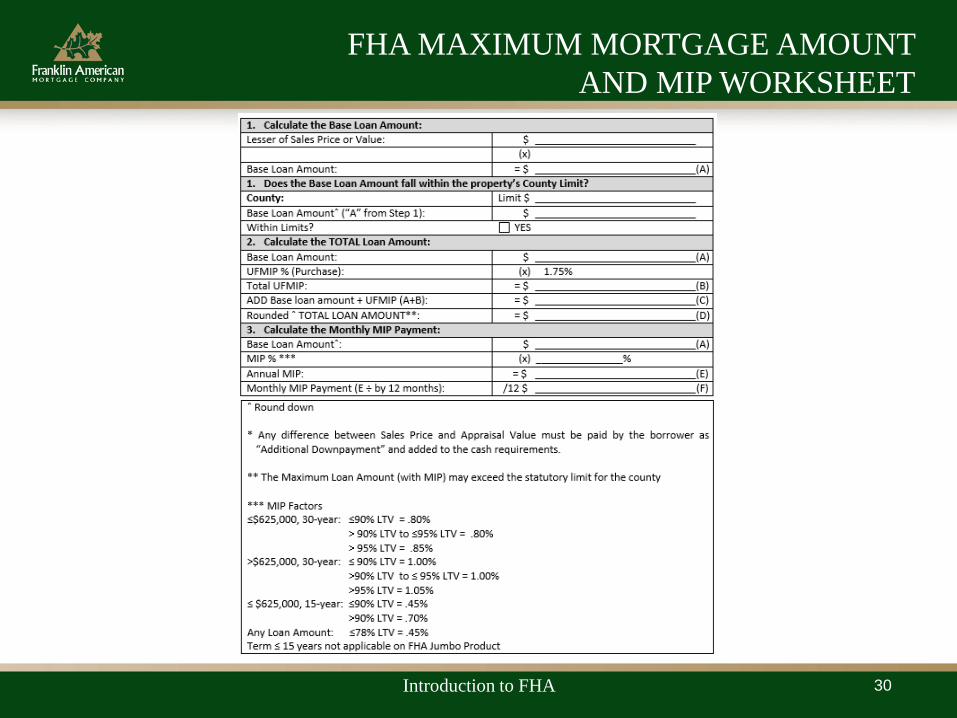

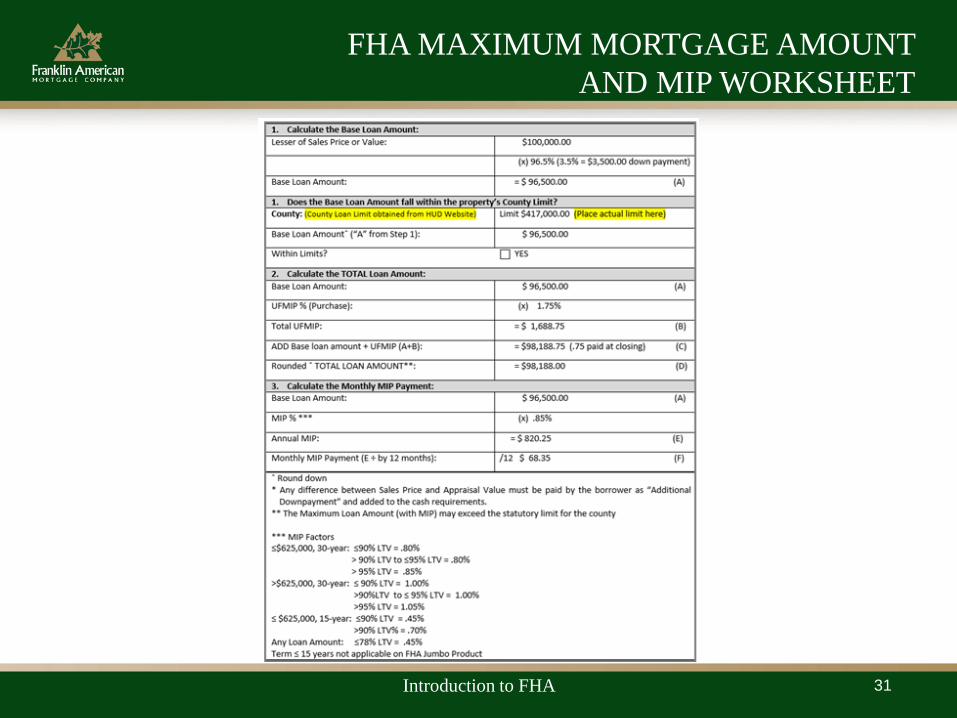

FHA MAXIMUM MORTGAGE AMOUNT

AND MIP WORKSHEET

Introduction to FHA 30

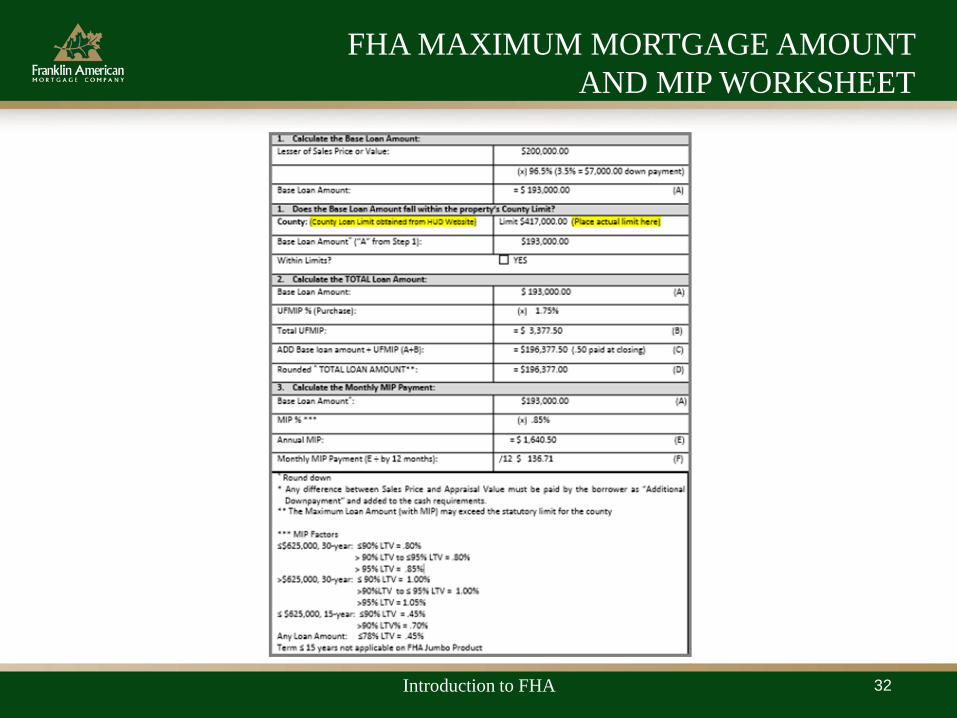

FHA MAXIMUM MORTGAGE AMOUNT

AND MIP WORKSHEET

Introduction to FHA 31

FHA MAXIMUM MORTGAGE AMOUNT

AND MIP WORKSHEET

Introduction to FHA 32

Restrictions to Maximum FHA Amounts Certain types of loan transactions affect the amount of financing available and the calculation of the

maximum mortgage amount.

These include: Identity-of-Interest, Non-Occupying Co-Borrowers, and additional FHA loans.

Identity of Interest Transactions

Identity-of-Interest is defined by HUD as a sales transaction between parties with a family or business

relationship. These transactions are usually restricted to a maximum loan-to-value of 85%. However,

maximum financing is permissible under the following circumstances:

• A family member purchasing another family member's home as a principal residence. The home must be the seller’s primary residence.

• An employee of a builder purchasing one of the builder's new homes as a principal residence.

• A corporation transferring an employee out of an area, purchasing the transferred employee's home, and reselling to another employee.

• A current tenant purchasing the property that he or she has rented for at least six (6) months immediately predating the sales contract. A lease or other written evidence must be submitted to verify occupancy.

RESTRICTIONS TO MAXIMUM

FHA LOAN AMOUNTS

Introduction to FHA 33

RESTRICTIONS TO MAXIMUM

FHA AMOUNTS

Introduction to FHA 34

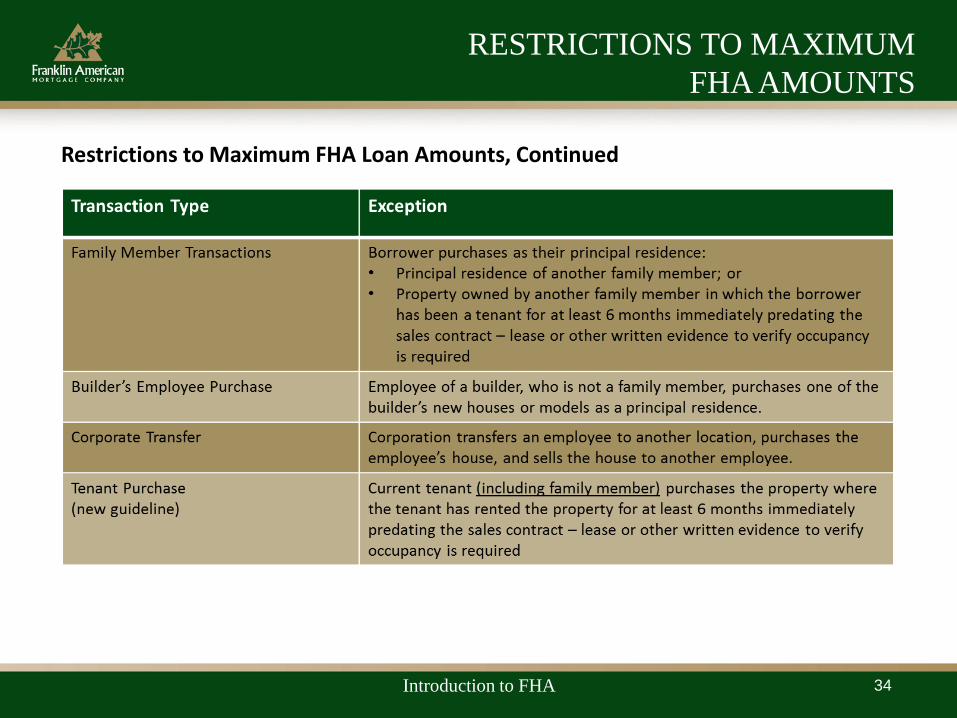

Restrictions to Maximum FHA Loan Amounts, Continued

Restrictions to Maximum FHA Loan Amounts, Continued Family Member is defined as follows:

• Child, parent, or grandparent;

o Child is defined as son, stepson, daughter, or stepdaughter;

o Parent or grandparent includes a step-parent/grandparent or foster parent/grandparent

• Spouse or domestic partner

• Legally adopted son or daughter, including a child who is placed with the borrower by an authorized agency

• for legal adoption

• Foster child

• Brother, stepbrother

• Sister, stepsister

• Uncle

• Aunt

• Son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law of the borrower

Note: This applies to identity-of-interest and gift funds.

RESTRICTIONS TO MAXIMUM

FHA AMOUNTS

Introduction to FHA 35

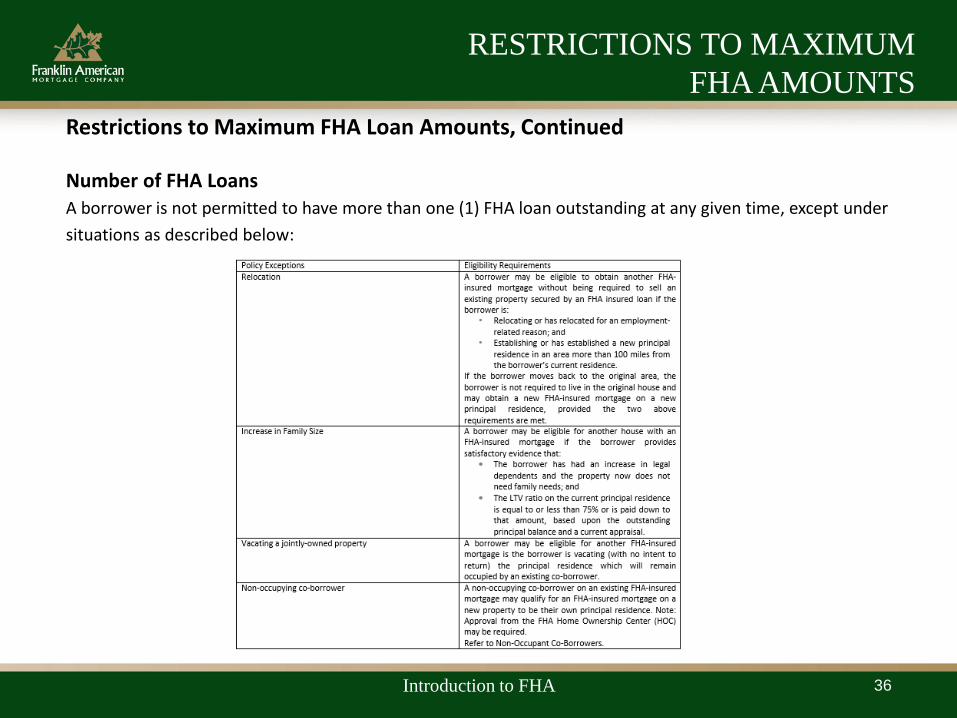

Restrictions to Maximum FHA Loan Amounts, Continued Number of FHA Loans

A borrower is not permitted to have more than one (1) FHA loan outstanding at any given time, except under

situations as described below:

RESTRICTIONS TO MAXIMUM

FHA AMOUNTS

Introduction to FHA 36

Please refer to the FAMC Wholesale Lending Guide for complete Borrower Eligibility guidelines at: Underwriting Guidelines>FHA>Borrower Eligibility Non-Occupant Co-Borrowers

For non-occupying co-borrower transactions, the maximum LTV is limited to 75% LTV.

The LTV can be increased to a maximum of 96.5% if the borrowers are family members, provided the

transaction does not involve the following:

• A family member selling to a family member who will be a non-occupying co-borrower.

• A transaction on a two- to four-unit property.

Non-Borrowing Spouse or Domestic Partner:

A non-borrowing spouse or domestic partner is a person who has an ownership interest in the security property.

Non-borrowing spouses or domestic partners are required to sign the security instrument and other

applicable documentation in order to perfect a lien in accordance with the governing state law. The option to

waive any property right by virtue of being the owner’s spouse or domestic partner must be in accordance

with applicable state law. CAIVRS is not required for non-borrowing spouses or domestic partners in

community property states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and

Wisconsin).

The following guidelines apply for non-borrowing spouses or domestic partners in community property states:

• Debts of a non-borrowing spouse must be counted in the borrower’s qualifying ratios.

• The non-borrowing spouse or domestic partner’s credit performance and credit score is generally not

a consideration.

BORROWER ELIGIBILITY

Introduction to FHA 37

Borrower's Cash Investment

The cash investment in the property must equal the difference between the amount of the insured mortgage,

excluding any upfront MIP, and the total cost to acquire the property including pre-paid expenses and closing

costs. All funds for the borrower's investment in the property must be verified and documented from

acceptable sources.

Minimum Downpayment Requirements

A downpayment is the difference between the sale price of real estate and the base loan amount which is

paid by the borrower.

On purchase transactions, a minimum downpayment of 3.5% (Minimum Required Investment (MRI), based

on the lesser of the sales price or appraised value is required. The MRI must be clearly documented and may

come from the following sources:

• From the borrower’s own funds:

• An acceptable gift source (refer to gifts), or

• An acceptable secondary financing source, refer to secondary/subordinate financing.

• When the borrower’s minimum required investment is provided by a source other than the borrower, clear

documentation must be obtained to support the permissible nature of those funds.

Closing costs paid by the borrower are not permitted to be used as a source of funds towards the 3.5%

minimum required investment (MRI).

Seller’s real estate tax proration to be received or credited at closing may not be considered at the time of

underwriting as the source of the applicant’s required funds to close.

FUNDS TO CLOSE

Introduction to FHA 38

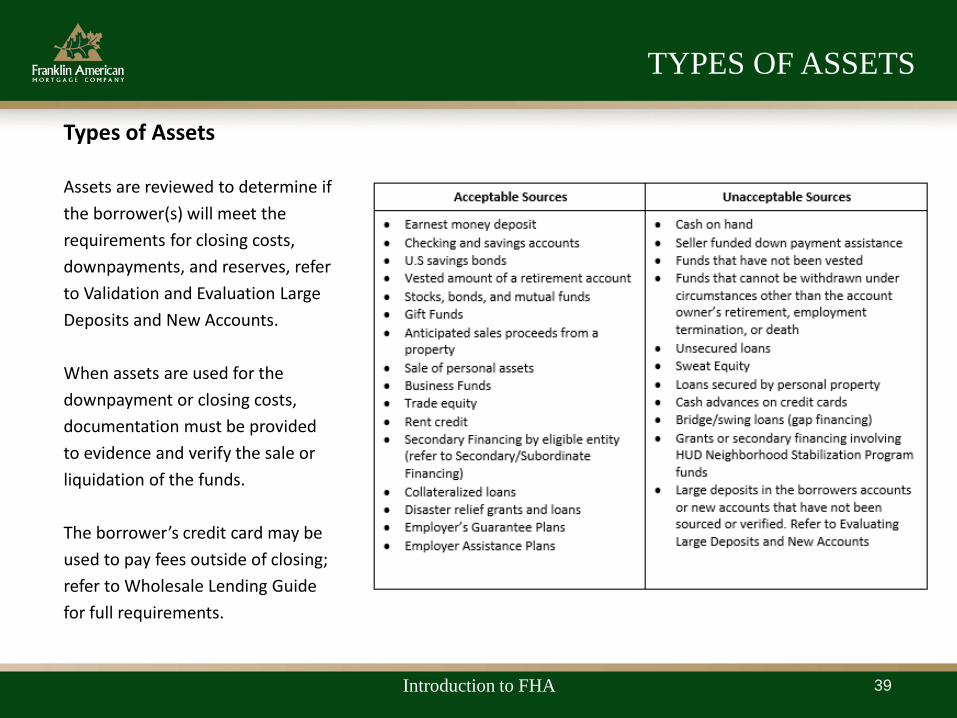

Types of Assets

Assets are reviewed to determine if

the borrower(s) will meet the

requirements for closing costs,

downpayments, and reserves, refer

to Validation and Evaluation Large

Deposits and New Accounts.

When assets are used for the

downpayment or closing costs,

documentation must be provided

to evidence and verify the sale or

liquidation of the funds.

The borrower’s credit card may be

used to pay fees outside of closing;

refer to Wholesale Lending Guide

for full requirements.

TYPES OF ASSETS

Introduction to FHA 39

TYPES OF ASSETS

Introduction to FHA 40

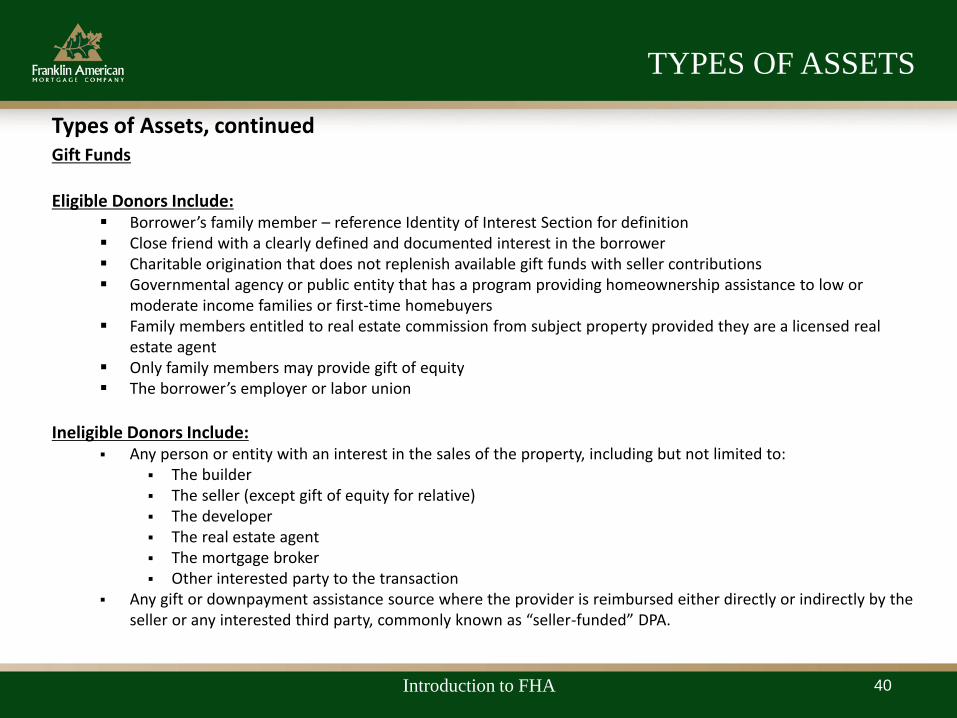

Types of Assets, continued Gift Funds

Eligible Donors Include:

Borrower’s family member – reference Identity of Interest Section for definition Close friend with a clearly defined and documented interest in the borrower Charitable origination that does not replenish available gift funds with seller contributions Governmental agency or public entity that has a program providing homeownership assistance to low or

moderate income families or first-time homebuyers Family members entitled to real estate commission from subject property provided they are a licensed real

estate agent Only family members may provide gift of equity The borrower’s employer or labor union

Ineligible Donors Include:

Any person or entity with an interest in the sales of the property, including but not limited to: The builder The seller (except gift of equity for relative) The developer The real estate agent The mortgage broker Other interested party to the transaction

Any gift or downpayment assistance source where the provider is reimbursed either directly or indirectly by the seller or any interested third party, commonly known as “seller-funded” DPA.

TYPES OF ASSETS, CONTINUED

Introduction to FHA 41

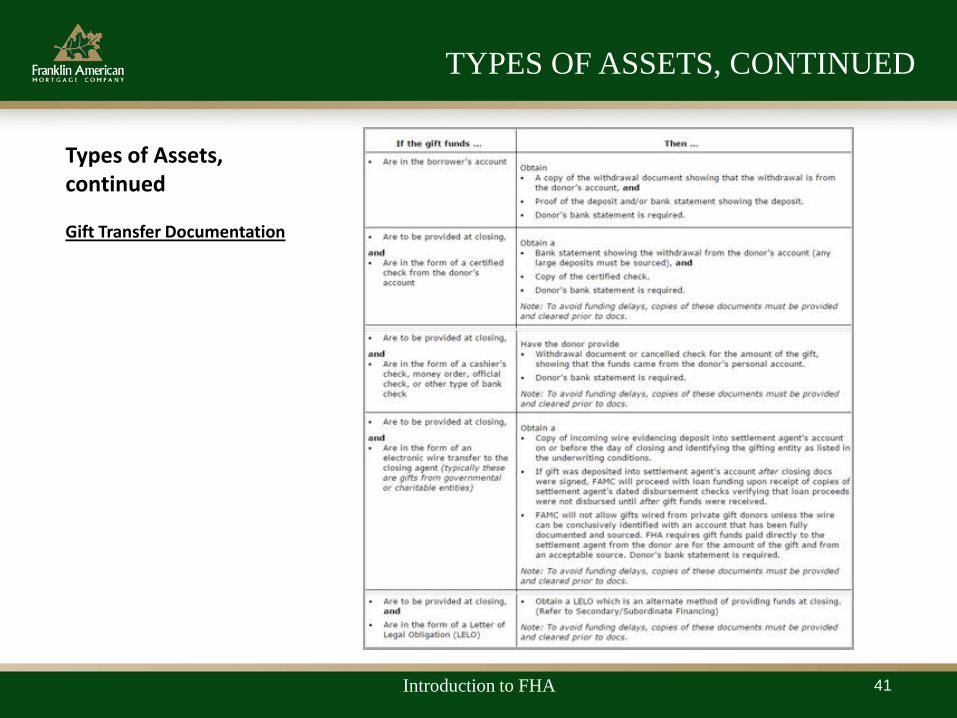

Types of Assets, continued Gift Transfer Documentation

LIABILITIES

Introduction to FHA 42

Please refer to the FAMC Wholesale Lending Guide for a complete list of liabilities guidelines at: Underwriting Guidelines>FHA>General Underwriting Guidelines>Liabilities

Installment Accounts Closed-end installment debts do not have to be included if: They will be paid off within 10 months; AND

The cumulative payments are less than or equal to 5% of the borrower’s gross monthly income. The borrower may not pay down the balance in order to meet the 10-month requirement

Student Loans All student loans must be included in the borrower’s DTI, regardless of the status of the loan or payment type. • Loans in deferment or forbearance may not be excluded. • One of the following two options are required for determining the qualifying payment.

• Utilize the greater of: o 1% of the outstanding loan balance, OR o The monthly payment reflected on the credit report.

• The actual payment only if it is fixed and fully amortized. o Written documentation from the student loan provider is required.

Example 1: Credit report reflects a $25,000 balance and a payment of $100.00. Written documentation indicates non-fixed plan. Qualifying payment must be $250.00.

Example 2: Credit report reflects a balance of $30,000 and a payment of zero. Written documentation indicates a fixed and fully amortized payment of $200.00 to begin in 18 months. Qualifying payment is $200.00.

LIABILITIES

Introduction to FHA 43

Non-Borrowing Spouse • Obtain SSA-89 for non-borrowing spouse and validate social security number (required if the subject

property is in a community property state or the non-borrowing spouse currently resides in a community property state.)

• If non-borrowing spouse does not have SSN:

• Verify lack of SSN with the Social Security Administration or one of their authorized service providers.

• Where an SSN does not exist for a non-borrowing spouse, a manual credit report must be provided and contain, at a minimum, the non-borrowing spouse’s full name, date of birth, and previous addresses for the last two years.

• Apply all of the following when a community property state applies:

• Community property state applies when: o Subject property is located in a community property state; OR o Borrowers current residence is located in a community property state (Arizona, California,

Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin). • Obtain credit report for non-borrowing spouse:

o Except non-credit qualifying streamline refinance • Debts must be included in borrower’s qualifying ratios, except for obligations excluded

by state law. • Credit performance and credit score is generally not a consideration.

LIABILITIES

Introduction to FHA 44

Obligations not to be considered: Medical collections Federal, state, and local taxes, if not delinquent and no payments

are required Automatic deductions from savings, when not associated with another type

of obligation Federal Insurance Contributions Act (FICA) and other retirement

contributions, such as 401(k) accounts Collateralized loans secured by depository accounts Utilities Child care Commuting costs Union dues Insurance, other than property insurance Open accounts with zero balances Voluntary deductions when not associated with another type of obligation

EMPLOYMENT AND INCOME

Introduction to FHA 45

Please refer to the FAMC Wholesale Lending Guide for a complete list of Employment and Income guidelines at: Underwriting Guidelines>FHA>General Underwriting Guidelines>Employment and Income

Employment History and Continuance

Establishing stable monthly income is based on the type of income received, the length of time received, and

whether or not the income is likely to continue.

• The borrower's employment must be documented for the most recent two (2) years. • Gaps of employment:

o Two year work history must be documented prior to gap in employment o Gaps of six (6) months or more (1 month or more for AUS Refer loans) must be fully explained by

the borrower

• Documentation of time spent in college or military service can be included to make up the two (2) year period. Time spent in high school cannot be used as part of borrower’s 2-year employment history

• Frequent changes in employment

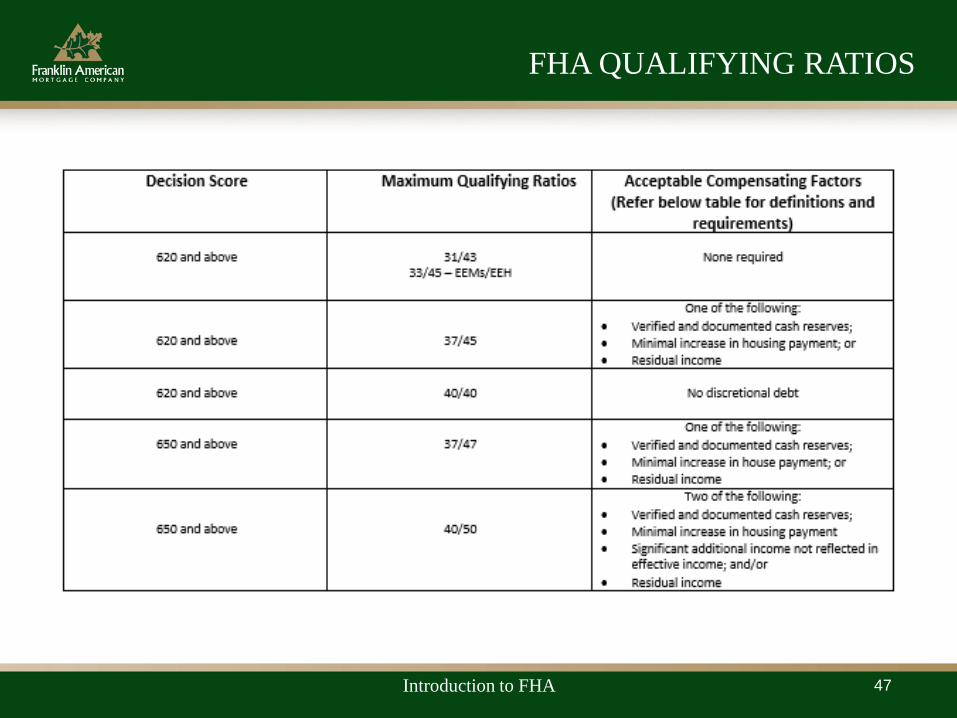

FHA QUALIFYING RATIOS

Introduction to FHA 46

Please refer to the FAMC Wholesale Lending Guide for a complete list of Ratio guidelines at: Underwriting Guidelines>FHA>General Underwriting Guidelines>Ratios and Compensating Factors

"Top Ratio": The total mortgage payment to effective income-to-income (also known as “front”) ratio is calculated

by dividing total monthly housing expenses for the financed property by the effective monthly income.

"Bottom Ratio”: The total fixed payment ratio (also known as DTI or “back”) ratio is calculated by dividing the total

of all monthly obligations by the effective monthly income. These ratios may only be exceeded with an AUS-Accept

recommendation that meets published FAMC credit guidelines (see FAMC FHA Product Description for full details).

TOTAL: o FICO < 650: DTI cannot exceed 45%, regardless of AUS results. o FICO > 650: As per AUS

Manual: o Refer to Ratios and Compensating Factors in FAMC Wholesale Lending Guide

for complete requirements.

Refer to EEM Program for qualifying guidelines on energy efficient mortgages. For new construction properties, borrowers must be qualified using the estimated real estate taxes based upon the completed property improvements, not the unimproved lot taxes.

FHA QUALIFYING RATIOS

Introduction to FHA 47

CREDIT POLICIES AND ANALYSIS

Introduction to FHA 48

Please refer to the FAMC Wholesale Lending Guide for a complete list of Credit guidelines at: Underwriting Guidelines>FHA>General Underwriting Guidelines>Credit Analysis

Automated Underwriting

AUS Requirements

An FHA TOTAL Scorecard recommendation is required for all FHA loans except for streamline refinance transactions. The loan must be underwritten to the applicable standards and guidelines in accordance with AUS findings and modified by Franklin American Mortgage Company's Product Descriptions. All terms and conditions of the loan and underwriting information must match the data on which the AUS Findings are based.

AUS Acceptability

30-year FHA loans which meet FAMC minimum credit requirements and receive an AUS-Approve recommendation and are

successfully validated by FAMC, will be approved upon successful validation if they meet these FHA requirements:

• The data entered into the AUS meets FHA guidelines and is true, complete, accurate, AND

• The loan does not contain characteristics that would require a downgrade to manual underwriting (see below),

AND

• The entire loan package meets all other FHA requirements except for those specifically not required because the

loan was evaluated by an AUS, AND

• There is no indication of fraudulent loan documentation.

Any loan with a term of less than 30 years will be accepted with an AUS approval as long as it also receives a 30-year term

AUS approval, which will be run internally by FAMC.

CREDIT POLICIES AND ANALYSIS

Introduction to FHA 49

Manual Downgrades

HUD requires the underwriter to manually downgrade an AUS-Accept recommendation to “Refer” and

perform a complete manual underwrite based on standard FHA guidelines if any of the following

conditions exist:

• Delinquent Federal Debt: As revealed by public records, credit information or CAIVRS, including:

– Federally-guaranteed student loans.

– Federal taxes (if in accepted repayment agreement, must be current).

– FHA and VA loans.

– Small Business Administration (SBA) loans.

– Liens placed against borrower’s property for a debt owed to the US Government.

• Foreclosure: Foreclosure, Deed-In-Lieu of Foreclosure or Pre-Foreclosure Sale, Short Sale

completed within three years of the case number assignment date.

• Bankruptcy: The date of the borrower’s bankruptcy discharge as reflected on bankruptcy

documents is within two (2) years from the date of the case number assignment.

CREDIT POLICIES AND ANALYSIS

Introduction to FHA 50

Manual Downgrades, continued

• The borrower has undisclosed mortgage debt

• The mortgage payment history by transaction type requires a manual downgrade (refer to

Credit History section in the applicable Product Description)

• Additional information not considered in the AUS recommendation that affects the overall

insurability of the loan (refer to Inaccuracy in Debt Consideration)

• Business Income shows a greater than 20% decline over the analysis period

• The borrower has disputed derogatory accounts with a cumulative balance of $1,000 or more

• The file contains information or documentation that cannot be entered into or evaluated by

TOTAL Mortgage Scorecard

Manual Overrides of AUS-Refer

Loans receiving an AUS-Refer must receive a loan transmittal or second review and signature. If manually

approved, the Underwriting Manager must note with detailed reasons for approving the loan, including

compensating factors.

Compensating factors, as listed in FAMC Wholesale Lending Guide>FHA General Underwriting Ratios and

Compensating Factors, must be carefully considered by the Underwriting Manager for their applicability

to the individual circumstances and whether or not they are relevant, appropriate, and sufficient to

overcome the AUS-Refer recommendation and the particular risk factors of the individual file.

CREDIT POLICIES AND ANALYSIS

Introduction to FHA 51

Inquiries

All inquiries within the past 90 days must be reviewed to ensure that all debts, including any new

payments resulting from material inquiries listed on the credit report are used to calculate the debt

ratios. If an inquiry results in a debt, regardless of the amount of time passed since the inquiry was

made, the payment must be included and the debt must be considered in the AUS results.

The Underwriter must also determine that any recent debts were not incurred to obtain any part of

the borrower’s required funds to close on the subject property.

NOTE: If credit report contains inquiries beyond 90 days, those debts must be reviewed and considered.

Credit History and Credit Scores

Credit history and credit scores are required for each borrower on the application. Non-traditional credit is not permitted. Minimum credit score is 620, regardless of AUS.

• Streamline refinance transactions require a minimum 640 credit score. Maximum Number of Financed Properties There are no restrictions on the number of financed properties owned by the borrower(s) for Standard Loan Amounts. Refer to Product Description for FHA Jumbo. Number of Borrowers per Transaction The number of borrowers per loan transaction is restricted to four (4) borrowers.

PROPERTY ELIGIBILITY

Introduction to FHA 52

Ineligible Properties • Any property where the seller is not the owner of record.

• Properties being re-sold within 90 days of the seller's acquisition

date (refer to Property Flipping in FAMC Lending Guide).

• Properties which are not primarily residential in nature and use

(see FAMC Lending Guide for full requirements).

• Manufactured or mobile housing.

• Leasehold condominium.

• Spot condominium.

• Multi-unit condominium.

• Co-ops.

• Dome homes.

• Builder Trade Equity.

• Any property that does not meet HUD’s minimum property

requirements and minimum property standards.

• Properties with individual water purification systems required to

make the water safe for human consumption

• Fraternity and sorority houses

• Vacation homes

• Properties subject to Private Transfer Fee Covenants • Properties that do not meet HUD minimum property requirements

and standards

Please refer to the FAMC Wholesale Lending Guide for a complete list of Property guidelines at: Underwriting Guidelines>Property Eligibility>FHA

Eligible Properties Individual programs and products may have more restrictive

guidelines. Refer to the individual product description to

determine property eligibility.

• 1-4 unit attached or detached primary residence

including condominiums and PUDs.

• Condominiums must be FHA-approved, refer to

Condominium and PUD projects.

• 3-4 unit properties are subject to an additional “self-

sufficiency” test. See the Maximum/Minimum Loan

Amount section of the product description.

• REO properties. These include properties owned by HUD,

Fannie Mae, Freddie Mac, VA, USDA, and banking

institutions.

• Log homes.

• Modular homes (must have 2nd level review

in Underwriting).

• Mixed-use properties.

• Age-restricted properties (with completed Age Restricted

Properties Form).

• New Construction – refer to New Construction.

PROPERTY ELIGIBILITY

Introduction to FHA 53

Condominium and PUD Projects

• Site condominiums are single-family detached dwellings encumbered by a declaration of condominium

covenants or condominium form of ownership. Condominium project approval is not required for site

condominiums; however, the condominium rider must be included in the FHA case binder submitted for

insurance endorsement, and the loan closed under Section 203(b).

• Condominiums must be FHA-approved. The project must be listed on FHA's approved condominium

project list at https://entp.hud.gov/idapp/protect/condlook.cfm

• If a project is no longer approved or foes not meet Lender Certification Criteria, then only an FHA-

to-FHA streamline refinance without an appraisal is permitted.

• PUDs do not require FHA approval.

Leasehold Estates

• A leasehold estate is a way of holding title to real estate in which the mortgagor does not actually own

the property and instead has a recorded long-term lease. Generally, leasehold estates are eligible. The

appraisal must indicate market acceptance of leasehold estates as well as meet all HUD documentation

requirements for leasehold estates.

• For 1-4 unit properties, including a one (1) family unit in a condominium project, the mortgage must be

a real estate held on leasehold under:

• A lease having a term of not less than 10 years beyond the maturity date of

the mortgage OR

• A lease of not less than 99 years which is renewable.

APPRAISAL

Introduction to FHA 54

FHA Appraisals All appraisals must be ordered with strict adherence to Franklin American Mortgage Company’s guidelines for Appraiser Independence Requirements (AIR). The appraiser’s status must be verified within FHA Connection under Single Family FHA/Single Family Origination/FHA Approval Lists/Appraisers. The effective date of the appraisal cannot be before the case number assignment date. Requirements in the Product Description must be followed.

Second Appraisals Franklin American Mortgage Company must order all second appraisals. A second case number is not to be used. Appraisal, value, and payment requirements:

Form 2055 is permitted. The value from the second appraisal must be used for LTV calculation if it exceeds 5% less than

the value from the first appraisal (only applies for property flipping). If the second appraisal value is higher than the initial appraisal, the value from the second

appraisal may not be used. The borrower may not be charged for the second appraisal.

PROPERTY INSPECTION

Introduction to FHA 55

Termite, Well, and Septic Inspections

Properties under one (1) year old require mandatory inspection, treatment, and testing, even if previously occupied.

See FHA New Construction Guidelines in FAMC Wholesale Lending Guide for more information.

For existing properties over one (1) year old, inspection and/or testing is only required if:

• The appraisal indicates there may be a problem or that problems are common in the area.

• Mandated by the state or local jurisdiction (see below) • Required by the sales contract • A water purification system is present. If the water supply does not test safe without

the purification system, the property is ineligible because of the required maintenance escrow.

• When utilities (water, gas, electric) are NOT on at the time of appraisal the appraiser must condition for further inspection to determine if the utilities are in proper working order.

Shared Well Appraiser must obtain a copy of the shared well report and indicate any readily observable deficiencies:

• A copy of the shared well agreement must be included with the appraisal report

For properties with wells and other water systems, refer to: http://portal.hud.gov/hudportal/HUD?src=/FHAFAQ

For properties with septic systems, refer to http://portal.hud.gov/hudportal/HUD?src=/FHAFAQ

REFINANCE TRANSACTIONS

Introduction to FHA 56

Please refer to the FAMC Wholesale Lending Guide for complete Refinance guidelines at: Underwriting Guidelines>FHA>Mortgage Eligibility>Refinance Transactions

Refinance Transactions

A refinance transaction is a mortgage loan used to payoff an existing real estate obligation on the same property

for borrower(s) with legal title to the subject property. Not all borrowers have to be obligated on the loan being

paid off.

The types of refinance transactions available are:

• Rate/term refinances (limited cash out): A no cash-out refinance of any mortgage in which all proceeds

are used to pay off eligible existing liens on the subject property and eligible costs associated with the

transaction.

• Simple refinance: A no cash-out refinance of an existing FHA-insured mortgage in which all proceeds are

used to pay off the existing FHA-insured mortgage on the subject property and eligible costs associated

with the transaction. An appraisal is required.

• Streamline refinances without appraisals: A refinance of an existing FHA-insured loan, with no appraisal

required. There are two options available:

• Credit Qualifying

• Non-Credit Qualifying

• Cash-out refinances: A refinance of any mortgage to take additional proceeds not limited to a specific

purpose or a withdrawal of equity when there is no existing mortgage.

NEW CONSTRUCTION

Introduction to FHA 57

Please refer to the FAMC Wholesale Lending Guide for a complete list of New Construction guidelines at: Underwriting Guidelines>Property Eligibility>FHA>New Construction New Construction Categories

The first step in determining the correct documentation for FHA new construction cases is to determine the construction category. The category is determined by the stage of construction at the time the appraisal is performed and noted under “General Description” in the “Improvements” section of the appraisal. The categories are:

Existing Less Than 1-Year Old: Property is 100% complete the issuance of the Certificate of Occupancy or equivalent was less than one year prior to the date of the appraisal. The property must have never been occupied.

Under Construction: The period from the first placement of permanent material through 100% completion with no Certificate of Occupancy or equivalent.

Proposed Construction: Property where no concrete or permanent material has been placed. Digging of footing and placement of rebar is not considered permanent.