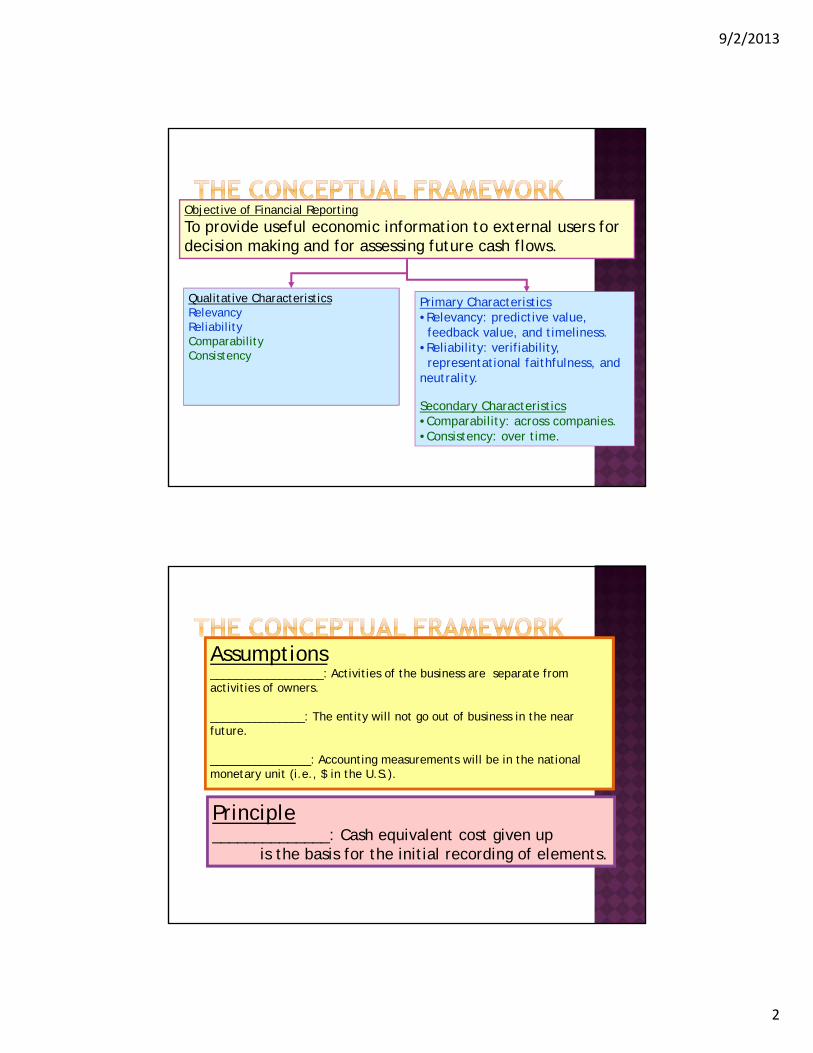

feedback value, and timeliness.•Reliability: verifiability,

representational faithfulness, and neutrality.

Secondary Characteristics•Comparability: across companies.•Consistency: over time.

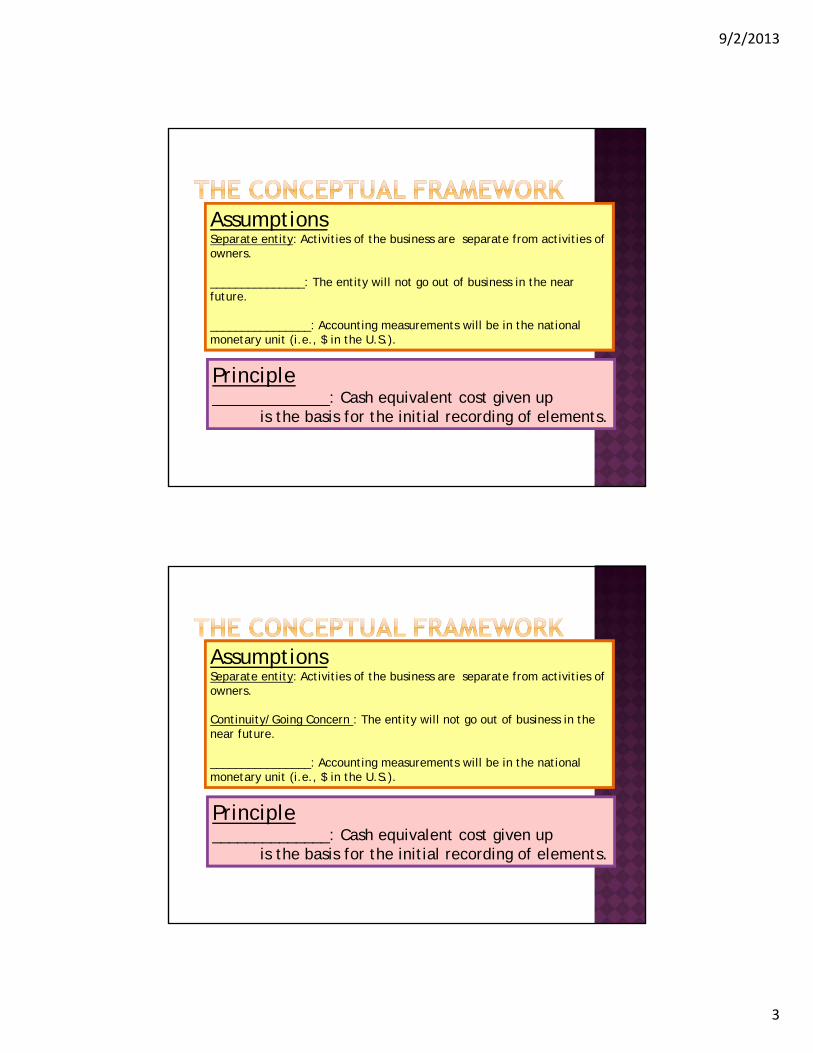

Assumptions__________________: Activities of the business are separate from activities of owners.

_______________: The entity will not go out of business in the near future.

________________: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

Principle______________: Cash equivalent cost given up

is the basis for the initial recording of elements.

9/2/2013

3

AssumptionsSeparate entity: Activities of the business are separate from activities of owners.

_______________: The entity will not go out of business in the near future.

________________: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

Principle______________: Cash equivalent cost given up

is the basis for the initial recording of elements.

AssumptionsSeparate entity: Activities of the business are separate from activities of owners.

Continuity/Going Concern : The entity will not go out of business in the near future.

________________: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

Principle______________: Cash equivalent cost given up

is the basis for the initial recording of elements.

9/2/2013

4

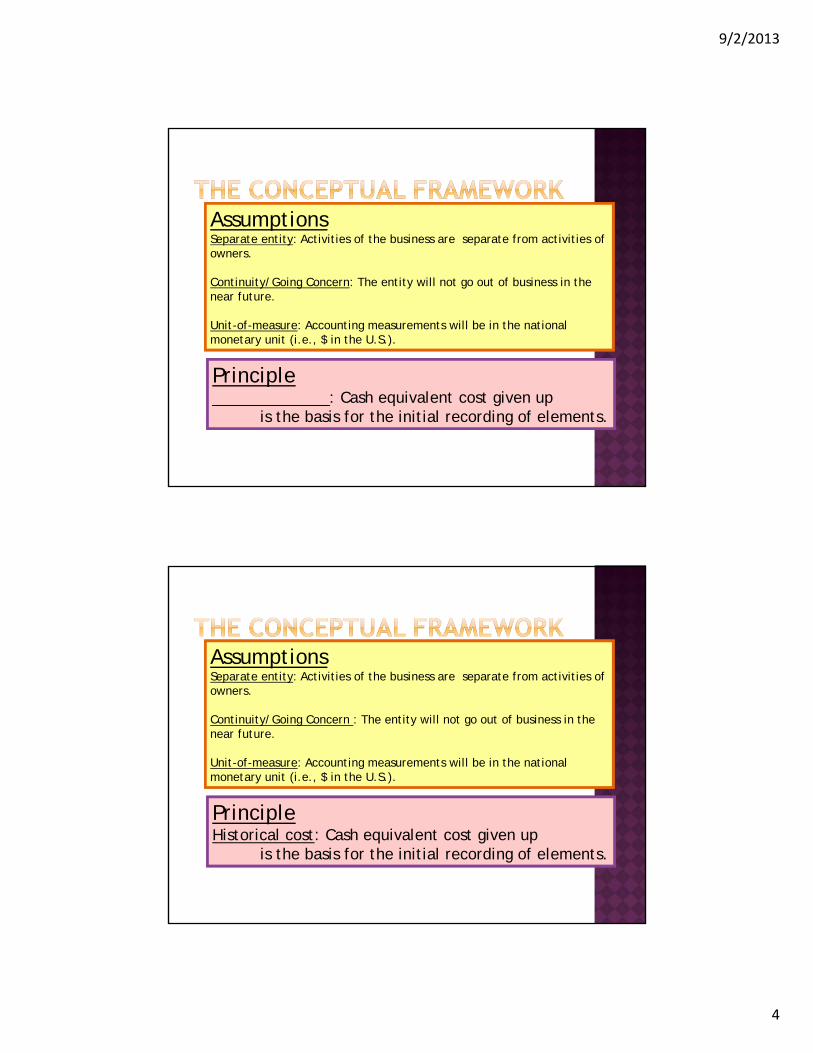

AssumptionsSeparate entity: Activities of the business are separate from activities of owners.

Continuity/Going Concern: The entity will not go out of business in the near future.

Unit-of-measure: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

Principle______________: Cash equivalent cost given up

is the basis for the initial recording of elements.

AssumptionsSeparate entity: Activities of the business are separate from activities of owners.

Continuity/Going Concern : The entity will not go out of business in the near future.

Unit-of-measure: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

PrincipleHistorical cost: Cash equivalent cost given up

is the basis for the initial recording of elements.

9/2/2013

5

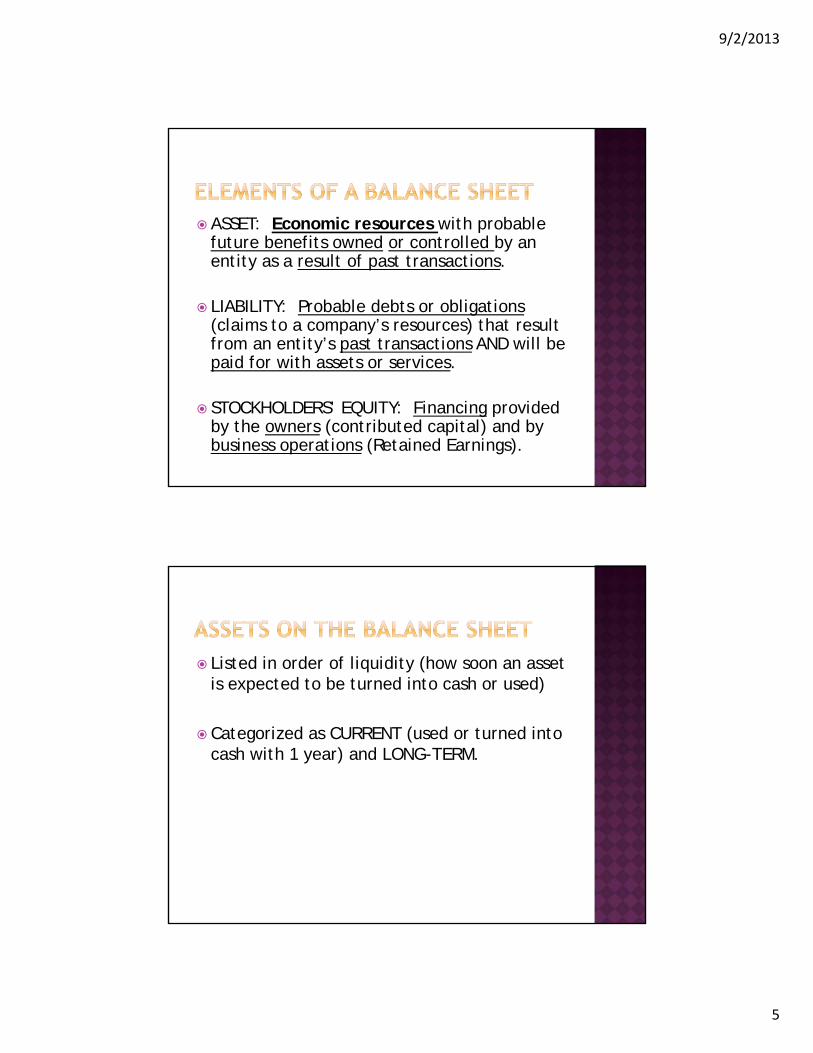

ASSET: Economic resources with probable future benefits owned or controlled by an entity as a result of past transactions.

LIABILITY: Probable debts or obligations (claims to a company’s resources) that result from an entity’s past transactions AND will be paid for with assets or services.

STOCKHOLDERS’ EQUITY: Financing provided by the owners (contributed capital) and by business operations (Retained Earnings).

Listed in order of liquidity (how soon an asset is expected to be turned into cash or used)

Categorized as CURRENT (used or turned into cash with 1 year) and LONG-TERM.

9/2/2013

6

Listed in order of maturity (how soon the obligation will be paid)

Classified as CURRENT or LONG-TERM

For simplicity, usually only includes two accounts: Contributed Capital and Retained Earnings

Will get more complex later in the semester.

9/2/2013

7

External events: exchanges of assetsand liabilities between the businessand one or more other parties.

Borrow cash

from the bank

Internal events: not an exchange betweenthe business and other parties, but havea direct effect on the accounting entity.

Loss due to fire damage.

9/2/2013

8

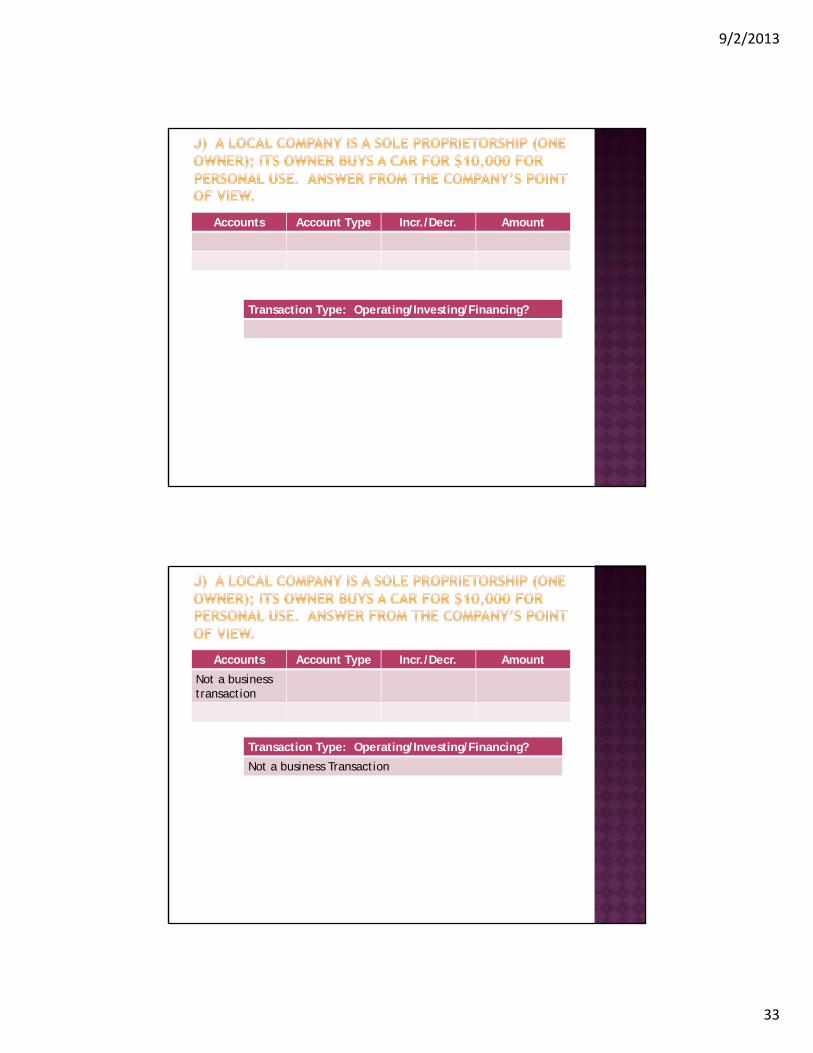

Dittman Company purchased a machine that it paid for by signing a note payable. _______

Dittman Company purchased a machine that it paid for by signing a note payable. __YES__

9/2/2013

9

The founding owner, Megan Dittman, purchased additional stock in another company. _______

The founding owner, Megan Dittman, purchased additional stock in another company. __NO___

9/2/2013

10

The company borrowed $1,000,000 from a local bank._______

The company borrowed $1,000,000 from a local bank.__YES___

9/2/2013

11

Six investors in Dittman Company sold their stock to another investor. ________

Six investors in Dittman Company sold their stock to another investor. ___NO___

9/2/2013

12

The company lent $150,000 to a member of the board of directors. _______

The company lent $150,000 to a member of the board of directors. ___YES___

9/2/2013

13

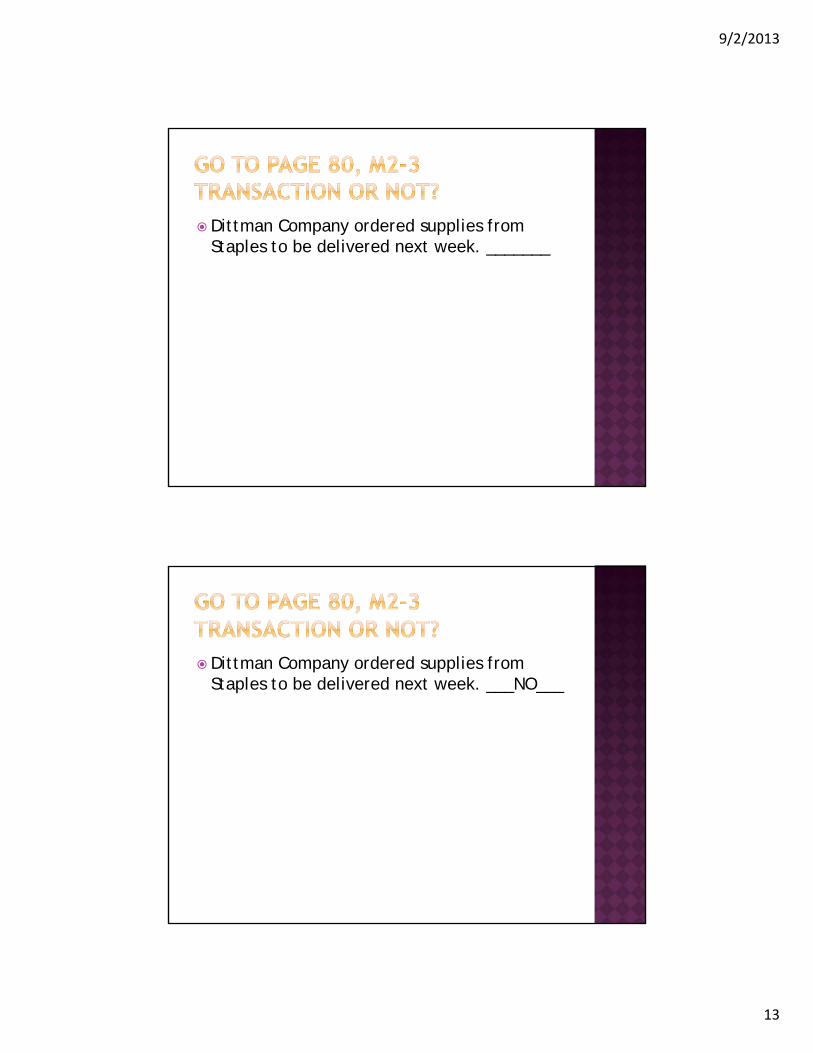

Dittman Company ordered supplies from Staples to be delivered next week. _______

Dittman Company ordered supplies from Staples to be delivered next week. ___NO___

9/2/2013

14

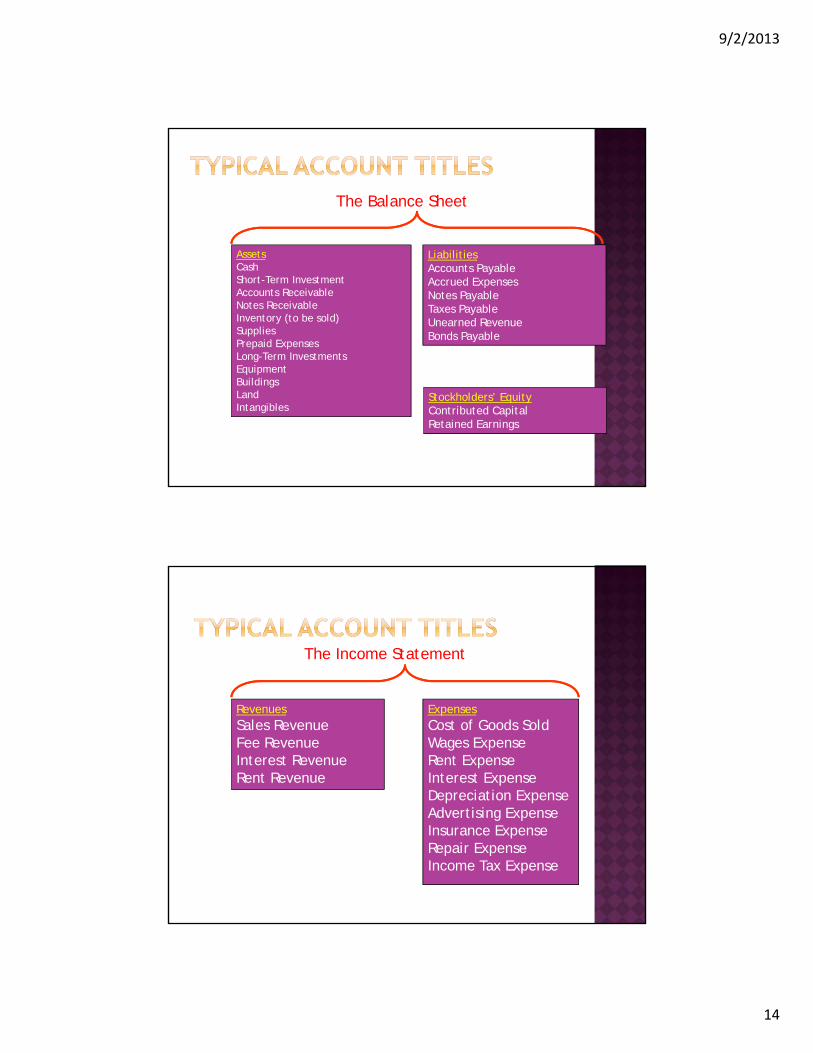

AssetsCashShort-Term InvestmentAccounts ReceivableNotes ReceivableInventory (to be sold)SuppliesPrepaid ExpensesLong-Term InvestmentsEquipmentBuildingsLandIntangibles

Every transaction affects at least twoaccounts (duality of effects).The accounting equation must remain in

balance after each transaction.

A = L + SE(Assets) (Liabilities) (Stockholders’

Equity)

Most transactions with external parties involve an exchange where the business entity gives up something but receivessomething in return.

9/2/2013

16

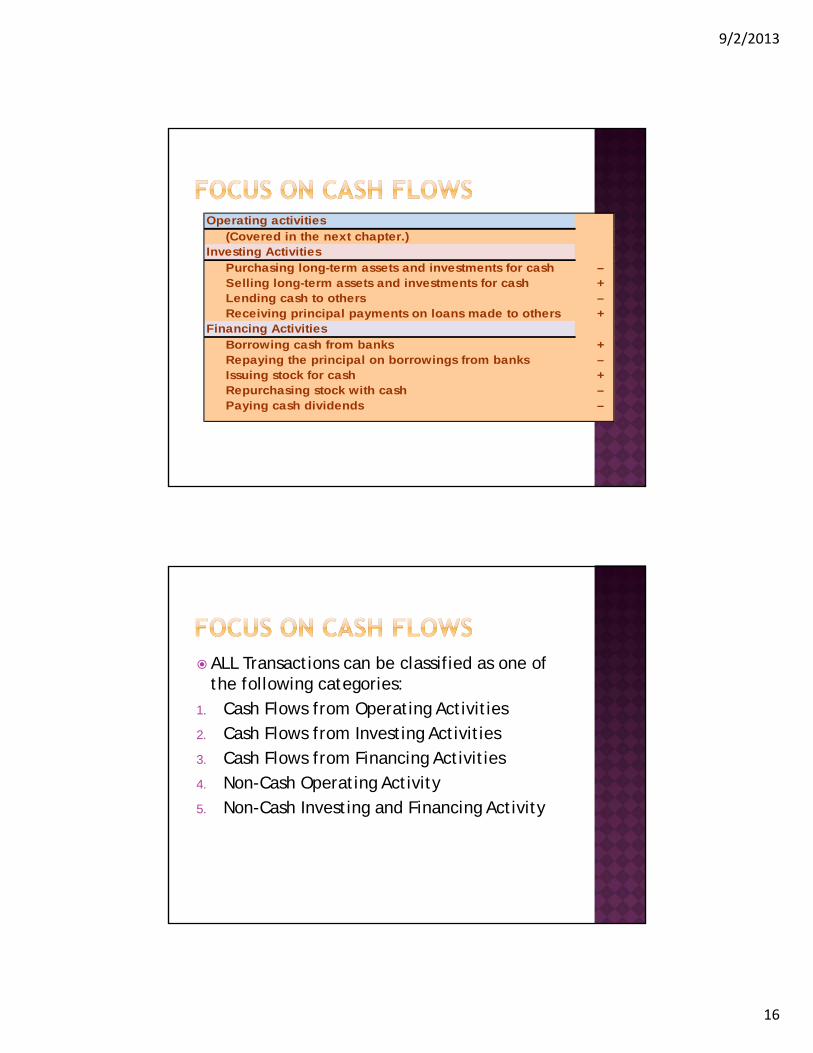

Operating activities (Covered in the next chapter.)Investing Activities Purchasing long-term assets and investments for cash – Selling long-term assets and investments for cash + Lending cash to others – Receiving principal payments on loans made to others +Financing Activities Borrowing cash from banks + Repaying the principal on borrowings from banks – Issuing stock for cash + Repurchasing stock with cash – Paying cash dividends –

ALL Transactions can be classified as one of the following categories:

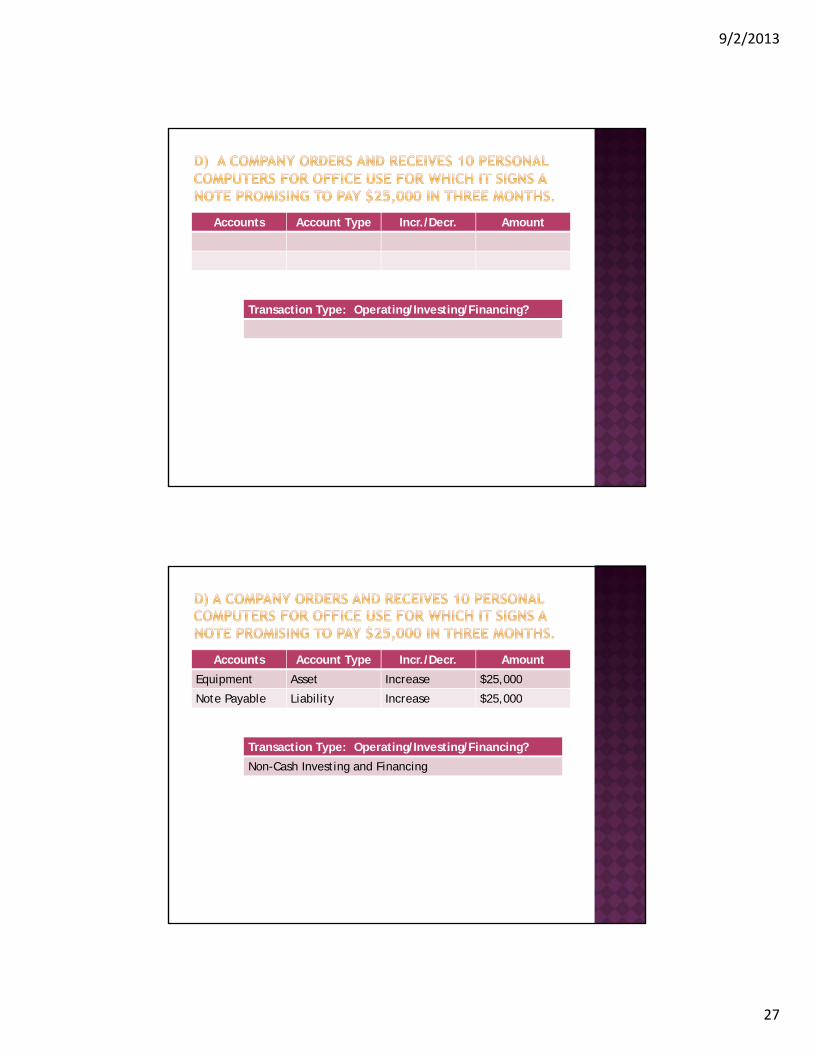

1. Cash Flows from Operating Activities2. Cash Flows from Investing Activities3. Cash Flows from Financing Activities4. Non-Cash Operating Activity5. Non-Cash Investing and Financing Activity

9/2/2013

17

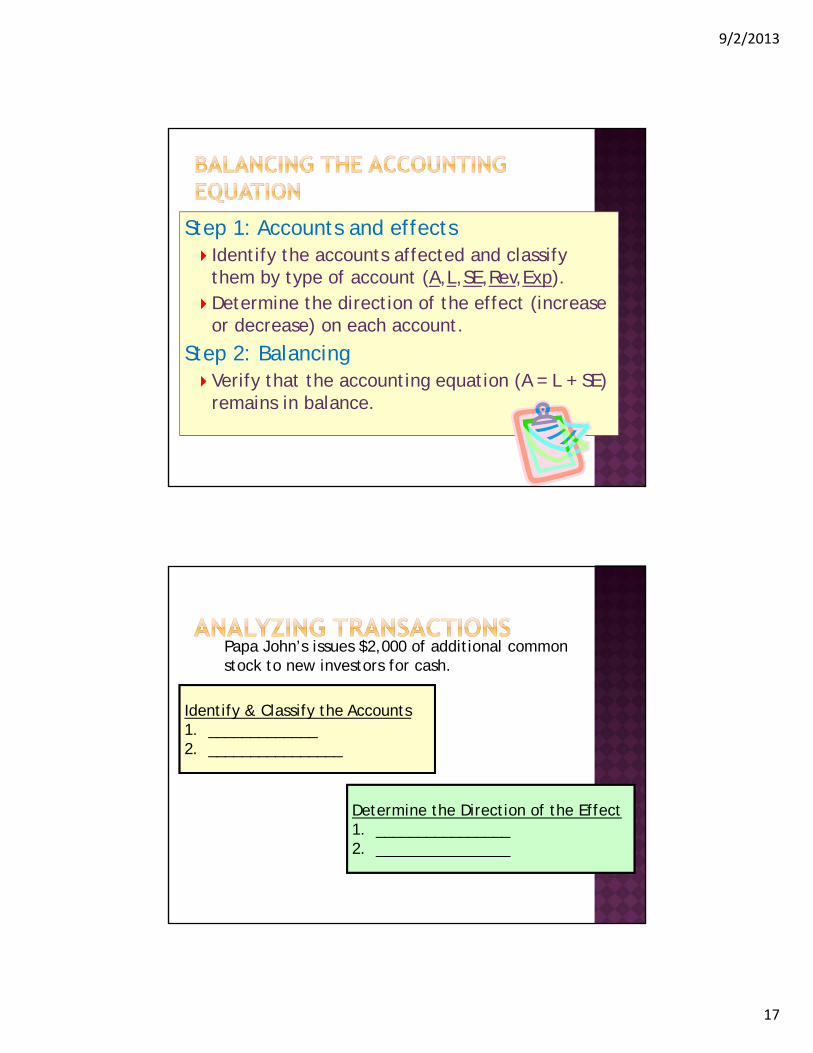

Step 1: Accounts and effects Identify the accounts affected and classify

them by type of account (A,L,SE,Rev,Exp). Determine the direction of the effect (increase

or decrease) on each account.

Step 2: Balancing Verify that the accounting equation (A = L + SE)

remains in balance.

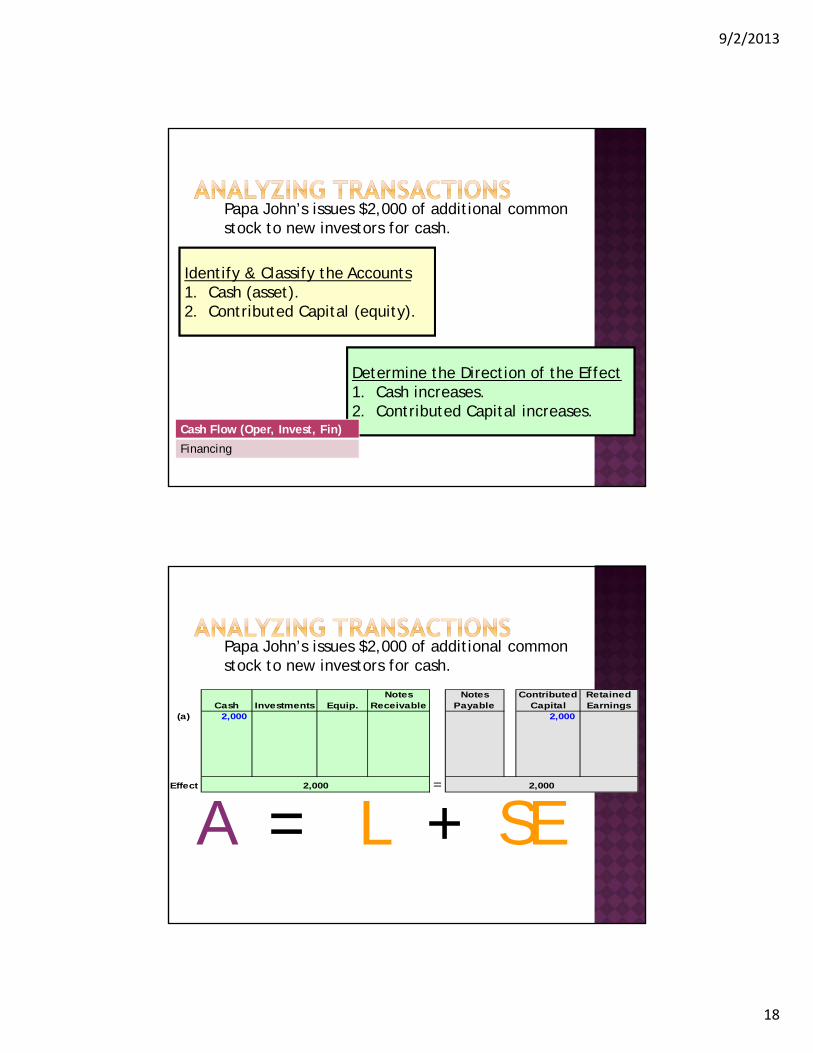

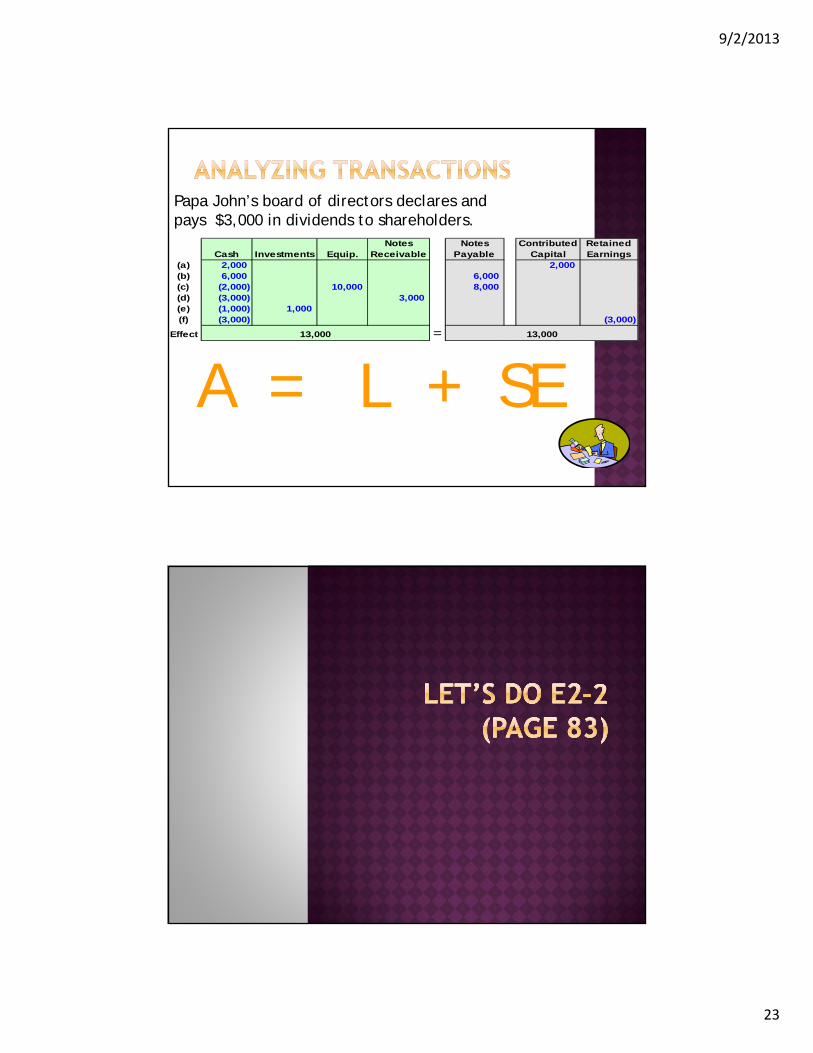

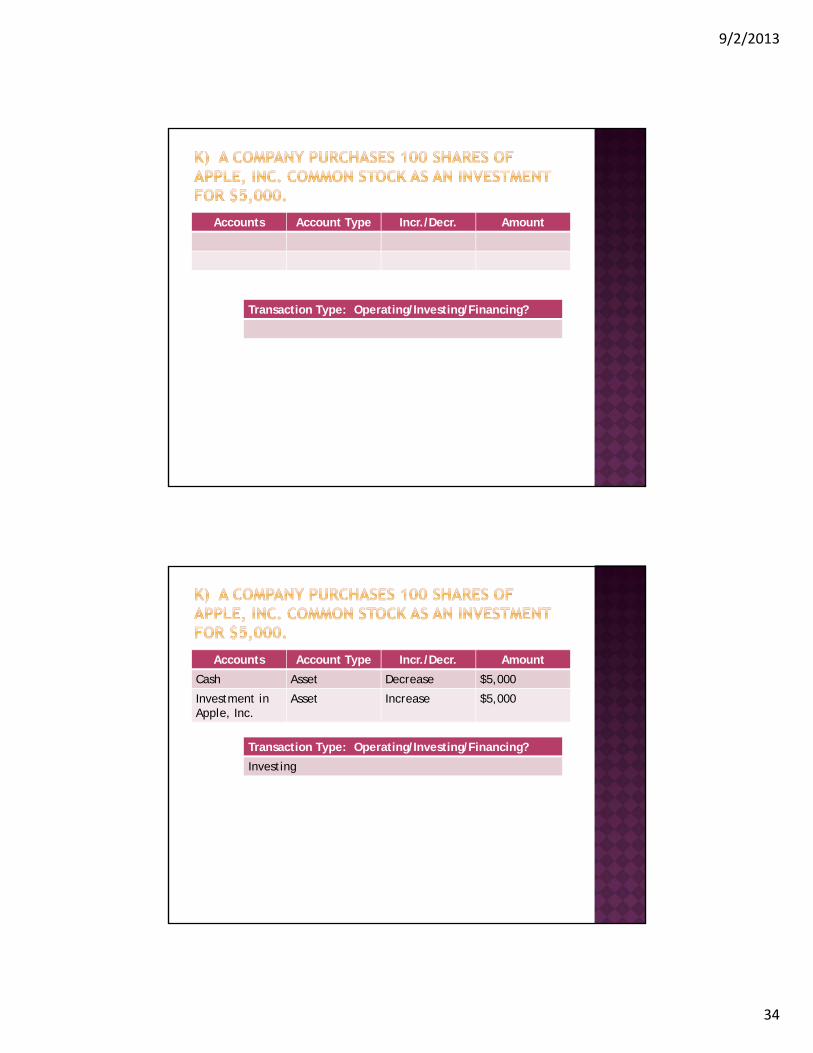

Papa John’s issues $2,000 of additional common stock to new investors for cash.

Identify & Classify the Accounts1. _____________2. ________________

Determine the Direction of the Effect1. ________________2. ________________

9/2/2013

18

Papa John’s issues $2,000 of additional common stock to new investors for cash.

Identify & Classify the Accounts1. Cash (asset).2. Contributed Capital (equity).

Determine the Direction of the Effect1. Cash increases.2. Contributed Capital increases.

Cash Flow (Oper, Invest, Fin)

Financing

A = L + SE

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000

Effect =2,000 2,000

Papa John’s issues $2,000 of additional common stock to new investors for cash.

9/2/2013

19

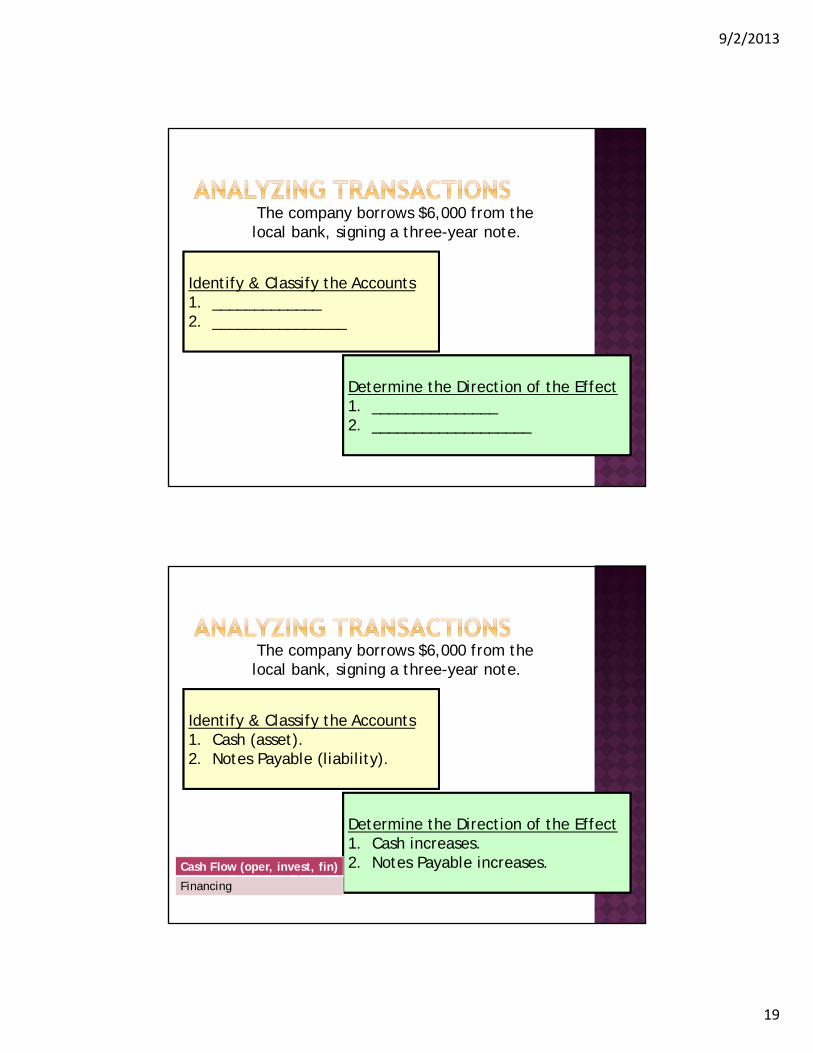

The company borrows $6,000 from the local bank, signing a three-year note.

Identify & Classify the Accounts1. _____________2. ________________

Determine the Direction of the Effect1. _______________2. ___________________

The company borrows $6,000 from the local bank, signing a three-year note.

Identify & Classify the Accounts1. Cash (asset).2. Notes Payable (liability).

Determine the Direction of the Effect1. Cash increases.2. Notes Payable increases.Cash Flow (oper, invest, fin)

Financing

9/2/2013

20

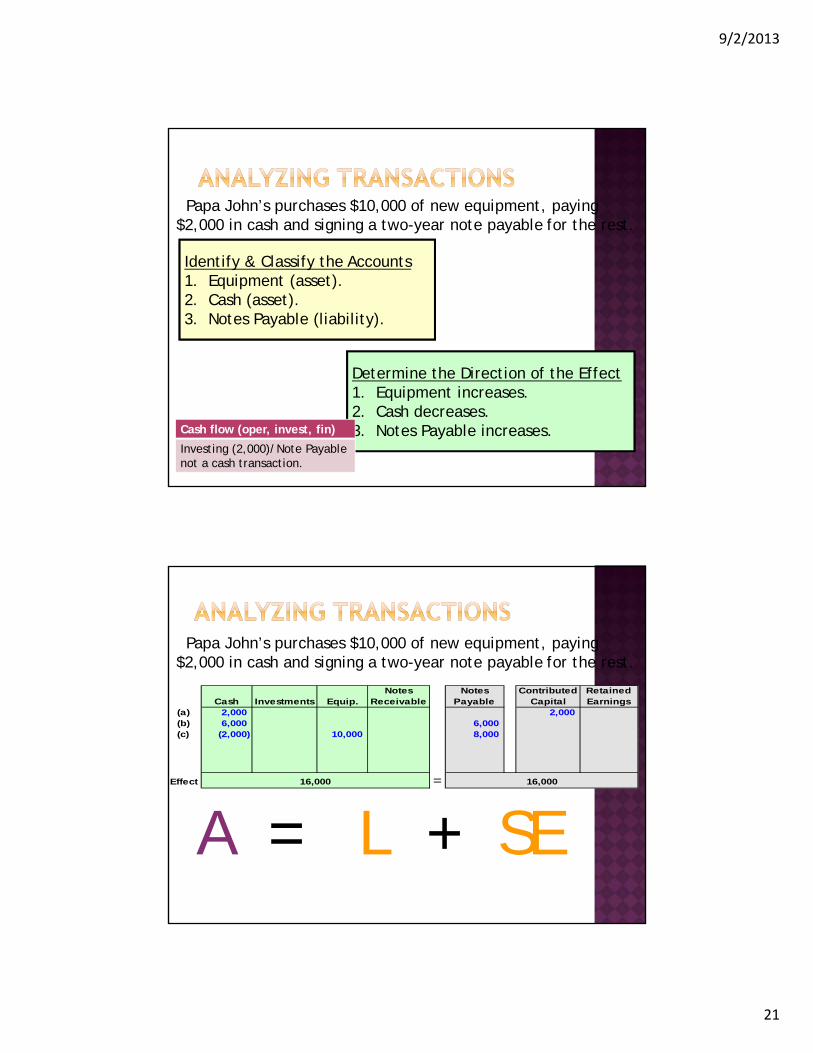

A = L + SE

Cash Investments Equip.Notes

ReceivableNotes

PayableContributed

CapitalRetained Earnings

(a) 2,000 2,000 (b) 6,000 6,000

Effect =8,000 8,000

The company borrows $6,000 from the local bank, signing a three-year note.

Papa John’s purchases $10,000 of new equipment, paying $2,000 in cash and signing a two-year note payable for the rest.

Identify & Classify the Accounts1. __________________2. ___________________3. ___________________

Determine the Direction of the Effect1. _______________2. ________________3. __________________

9/2/2013

21

Papa John’s purchases $10,000 of new equipment, paying $2,000 in cash and signing a two-year note payable for the rest.