110

Investing in Argentina Industry Approach Financial Advisory Services Argentina November 2017

Investing in ArgentinaIndustry Approach

Financial Advisory Services Argentina

November 2017

© 2017 Deloitte & Co. S.A. All rights reserved.

Content

• Argentina – Country’s Overview

• Industry Snapshot

• Consumer Goods & Retail: Food, Beverages & Tobacco

• Financial Services

• Agribusiness

• Telecommunications, Media & Technology

• Energy

ArgentinaCountry’s Overview

Politic Regime

ArgentinaPolitic Regime

Source: National Investment and Trade Promotion Agency information.

System of Government: Federal republic with three branches of government. Executive (President), Legislative (Congress) and Judiciary(Supreme and Lower Courts).

Congress: Divided into two houses: the Senate and the House of Representatives. Members are elected by popular vote. In the case of the Senate, members are elected for six-year terms. In the House, members are elected for four-year terms.

Federal Government:The country is divided into 23 provinces plus the autonomous city of Buenos Aires. Provinces have their own constitutions and executive, legislative and judicial branches of government.

Politics & Government

Executive (President)

Legislative (Congress)

Judiciary (Supreme & Lower

Courts)

Representatives/Members

President - Senate: 72 (3 per Province + 3 for the Buenos Aires City)

- House of Representatives: 257

Supreme Court: 5 members

Elections Every four years based on a two-round system: the candidate

wins if he receives either 45% of the vote

or 40% and is 10% ahead of the second candidate. If not, a run-off takes place.

- Senate: mandateslast 6 years. Elections are held every 2 years

in which 1/3 of the Senate is voted.

- House of Representatives:

mandates last 4 years. Elections are held every 2 years in which half of the chamber is voted.

Selected by the president, with the Senate approval,

and remain in charge as long as

they have the right conduct.

When a member turns 75 years old,

his is re-named every 5 years, as

long as his is able to comply with the

charge’s responsibilities.

Government Regime

© 2017 Deloitte & Co. S.A. All rights reserved.

Macroeconomic Factors

ArgentinaMacroeconomic Factors (1/2)

GDP Real Growth (%)

-1

2,4

-2,5

2,6

-2,2

2,7 3,3 2,7 2,7 3,4

-4

-2

0

2

4

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Average Exchange Rate (AR$/US$)

4,54 5,468,08 9,23

14,76 16,619,07 20,81 22,22 23,6

0

10

20

30

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Inflation Index (%)

25,3 23,4

38,1

26,5

41,4

26,217

10,8 7,9 6,3

0

20

40

60

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Source: EIU and BCRA (Central Bank).

National Reserves (US$ Bn)

43,2

30,5 31,425,5

38,4

54,5

0

20

40

60

2012 2013 2014 2015 2016 2017F

© 2017 Deloitte & Co. S.A. All rights reserved.

Country Risk (%)

Fiscal Deficit/GDP (% of GDP)

Trade Balance (US$)

9,910,7

7,9

5,94,8

3,6

0

2

4

6

8

10

12

2012 2013 2014 2015 2016 2017

15

5 6

0

5

-5 -6 -7 -6 -5-10

-5

0

5

10

15

20

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Source: Deloitte’s analysis based on EIU, Ambito Financiero, INDEC.

-2,1 -1,9-2,7

-4,8

-5,9-6,3 -6,4

-6-5,3

-3,4

-7

-6

-5

-4

-3

-2

-1

0

2012 2013 2014 2015 2017 2017F 2018F 2019F 2020F 2021F

© 2017 Deloitte & Co. S.A. All rights reserved.

ArgentinaMacroeconomic Factors (2/2)

Total Foreign Debt (US$ Bn)

Debt Interest Payments/GDP (% of GDP)

Total Public Debt/GDP (% over GDP)

137,0 147,0 145,0160,0

190,0 201,4 210,0 222 233 245 256

0

50

100

150

200

250

300

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F

36,7 39,4 41,3

54,0 54,5 54,4 54,7 56 57,9 57,2 56,4

0

10

20

30

40

50

60

70

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F

Source: Deloitte’s analysis based on EIU, Ambito Financiero, INDEC.

1,9

1,31,6

2,11,6

2,1

3,23,7 3,7

2,5

0,0

1,0

2,0

3,0

4,0

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

© 2017 Deloitte & Co. S.A. All rights reserved.

ArgentinaMacroeconomic Factors (2/2)

Economic Sectors

Regional Main Activities

Source: Deloitte’s analysis based on EIU, INDEC.

GDP by Activity (2015)

PatagoniaOil & GasFishFruits

PampasAgricultureCattle RaisingIndustry

NortheastAgricultureForestry

NorthwestAgricultureMiningGas

CuyoMiningWinery

17%

13%

10%

8%7%4%

4%

4%

3%

3%

3%2%

2%

20%

Manufacturing Wholesale, Reatail & Repairs

Real Estate Logistics

Agriculture Financial Services

Public Administration & Defense Education

Health Services Mining

Construction Leisure

Electricity, Gas & Water Other

Argentina has a highly diversified economy. It's key sectors are: agribusiness, pharmaceuticals, automobiles, energy & resources and biotechnology. Argentina is world leading producer of foodstuffs: third producer of soybean, fourth producer of sunflower and between the largest beef producers. In addition, it has the world’s fourth-biggest shale oil reserves and the second-biggest shale gas reserves. It is very rich in terms of mining resources: gold, cooper, silver and lithium –world’s third largest reserves, behind Bolivia and Chile.

The leading industrial sectors are: food processing, beverages, chemicals & pharmaceuticals, oil refining, motor vehicles and auto parts.Regarding services, the main sectors are wholesale, retail, transport and communications. The service sector is the largest job creator.

ArgentinaEconomic Sectors

© 2017 Deloitte & Co. S.A. All rights reserved.

Investment Activity & Foreign Trade

ArgentinaInvestment Activity

Foreign Direct Investment Stock (US$ B)

Source: INDEC and National Investment & Trade Promotion Agency.

99,0088,00 90,00

80,0072,00

83,0095,00

109,00123,00

137,00

-

20

40

60

80

100

120

140

160

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Identified Investment Opportunities (US$ B)

The National Government has identified investment opportunities for approximately US$ 240B across multiple sectors as described below:

Transportation & Infrastructure

+ US$ 80B

Federal Infrastructure &

Public Works+ US$ 60B

Power & Renewable Energy

+ US$ 35B

Mining+ US$ 30B

Oil & Gas+ US$ 25B

RE & Urban Development

+ US$ 5B

Agribusiness+ US$ 2B

Telecom & High Technology

+ US$ 2B

Tourism+ US$ 1B

© 2017 Deloitte & Co. S.A. All rights reserved.

Year Target Acquirer Acquirer Origin

Deal Ticket (US$ M)

2016 Petrobras Argentina

Pampa Energía Argentina 897

2016 Telecom Argentina

Fintech Group Mexico 812

2016 Grupo Mabe Ontex Group Belgium 444

2016 Nextel Comunicaciones

Grupo Clarín Argentina 178

2016 Campo Austral BRF Brazil 85

91 78 6856

77 71

0

50

100

2012 2013 2014 2015 2016 2017YTD

Deal Volume

Acquirer’s Origin – 2016 (Volume)

North America12%

Latin America70%

Asia & Oceania6%

Europe12%

Recent Deals

Source: Deloitte’s analysis based on Mergermarket & Thompson Reuters information.

ArgentinaRecent M&A Activity

© 2017 Deloitte & Co. S.A. All rights reserved.

65 7162 57 53

62 66 70 74 78 83

0

50

100

2012 2013 2014 2015 2016 2017F2018F2019F2020F2021F2022F

Imports FOB (US$ B)

2014 2015 2016

Brazil 1° 1° 1°

China 2° 2° 2°

US 3° 3° 3°

Germany 4° 4° 4°

Mexico 6° 5° 5°

Imports Ranking

80 7668

57 58 57 60 63 68 73 80

0

50

100

2012 2013 2014 2015 2016 2017F2018F2019F2020F2021F2022F

Exports FOB (US$ B)

2014 2015 2016

Brazil 1° 1° 1°

China 2° 2° 2°

US 3° 3° 3°

Chile 4° 4° 4°

Spain 6° 6° 5°

Exports Ranking

24%

19%

13%5%

3%3%

3%2%2%

26%

Brazil

China

US

Germany

Mexico

France

Italy

Japan

Spain

Rest

Imports by Partner

Exports by Partner

16%

8%

8%

4%3%2%2%2%2%

53%

Brazil

China

US

Chile

Spain

Germany

Netherlands

Canada

Uruguay

RestSource: EIU, INDEC.

ArgentinaForeign Trade

© 2017 Deloitte & Co. S.A. All rights reserved.

Demographics

Source: Deloitte analysis based on INDEC information.

Population:43.6M inhabitants

Population density:10.7 persons/km2

Age distribution:25.5% under 1564.3% between 15-6510.2% over 65

Literacy rate: 98%

English proficiency: High (19th in the World –Education First English Proficiency Index)

GDP per capita:US$ 21,430

Official Language:Spanish

Population Characteristics

Age Distribution (in Millions)

5,195

12,654

1,674

5,027

13,135

2,43

-15 -10 -5 0 5 10 15

0-14

15-65

65+

Millions

Men Women

© 2017 Deloitte & Co. S.A. All rights reserved.

ArgentinaPopulation Characteristics & Age Distribution

Unemployment (%)

Source: EIU, INDEC

7,2 7,1 7,3

6,5

8,5 8,68,1

7,87,5 7,4 7,2

0

1

2

3

4

5

6

7

8

9

10

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F 2022F

Average Wage (US$ per month)

902938

842

957

777

868931 955 978 992

0

200

400

600

800

1.000

1.200

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

ArgentinaEmployment

© 2017 Deloitte & Co. S.A. All rights reserved.

Analphabetic Index – 2010 Social Census (%)

Source: INDEC, EF EPI

English Level (EF EPI over 72 countries)

19 19

15 15

19

0

2

4

6

8

10

12

14

16

18

20

2012 2013 2014 2015 2016

#1 in LATAM (14 countries)

9,8 average years of education

Expense in Education: 15% of GDP

1,41,2 1,2 1,3

1,6

3,14,2

10,8 0,8 0,9

1,3

2,8

4,7

0

1

2

3

4

5

10-14 15-17 18-24 25-29 30-49 50-64 65 +

%

Male Female

ArgentinaEducation

© 2017 Deloitte & Co. S.A. All rights reserved.

Infrastructure

Source: INDEC, IGN.

Autonomous City of Buenos Aires Mendoza City

Cordoba City Rosario City

Location: NE of Buenos Aires ProvincePopulation:12,8 Million (32% of total)International Airports: 2Ports: Yes

Location: N of Mendoza ProvincePopulation: 0,9 Million (2,3% of total)International Airports: 1Ports: None

Location: NW of Córdoba ProvincePopulation: 1,4 Million (3,6% of total)Population: International Airports: 1Ports: None

Location: SE of Santa Fe ProvincePopulation: 1,2 Million (3,1% of total)International Airports: 1Ports: Yes

ArgentinaMain Cities

© 2017 Deloitte & Co. S.A. All rights reserved.

Source: Ministerio de Transporte, Red Vial Argentina, Aeropuertos 2000

Airports

- +50 airport terminals along the country- Most of them are managed by Aeropuertos2000 – private operator- +30M passengers per year

Ports

- +40 ports along the country- Main ports: Buenos Aires City and Rosario- Water flow throught the Río de la Plata, Paraná, and Uruguay rivers and Mar Argentino

Railway System

- 50,000kms of railway network- Largest in Latin America- Connected with limit countries- Buenos Aires City network has 7 different lines

Roads & Highways

- +500,000kms of roads- 35,000kms are national roads- +5,000kms of highways- Less than 35% are paved roads

ArgentinaCountry’s Overview: Transport Infrastructure

© 2017 Deloitte & Co. S.A. All rights reserved.

Source: Ministerio de Transporte, Aeropuertos 2000, Aduana Argentina

Airport Terminals

Ports

Key

ArgentinaAirport and Port System

© 2017 Deloitte & Co. S.A. All rights reserved.

Source: National Investment & Trade Promotion Agency.

The New Administration presented an US$ 80Bn investment plan in transportation to develop nationwide improvement in road/highways,

railways, ports and airports infrastructure.

5,6

1,5

1,4

3,2

8,5

15

48

Other

BA Port

Metropolitan BA Subway

Rolling Stock

Passenger Rail

Freight Rail

Roads

Transport Infrastructure Investment Plan (US$ Bn)

Concession and construction opportunities for 43,000kms of roads and highways.

Recovery of national freight railway so as to be able to transport up to 100M tns per year.

Improve the metropolitan railway network of 241 stations.

Maintain and expand the fleet of passenger rail cars.

Modernize three lines and build a new one to improve the Buenos Aires metro area subway.

Modernize, expand and operate the Buenos Aires Port – largest in the country.

Investment opportunities to improve and expand airports and ports and increase urban mobility across the country.

ArgentinaNational Transport Infrastructure Plan

© 2017 Deloitte & Co. S.A. All rights reserved.

Business Types, Regulatory Framework & Tax System

Source: National Investment & Trade Promotion Agency.

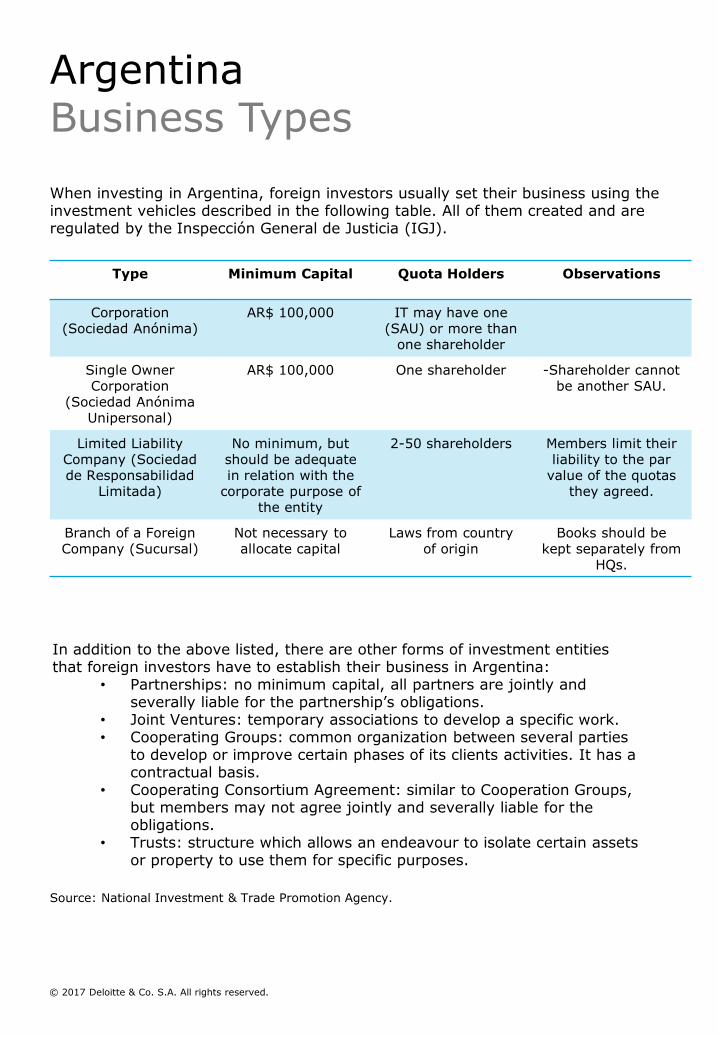

Type Minimum Capital Quota Holders Observations

Corporation (Sociedad Anónima)

AR$ 100,000 IT may have one (SAU) or more than

one shareholder

Single Owner Corporation

(Sociedad AnónimaUnipersonal)

AR$ 100,000 One shareholder -Shareholder cannot be another SAU.

Limited Liability Company (Sociedadde Responsabilidad

Limitada)

No minimum, but should be adequate in relation with the

corporate purpose of the entity

2-50 shareholders Members limit their liability to the par

value of the quotas they agreed.

Branch of a Foreign Company (Sucursal)

Not necessary toallocate capital

Laws from country of origin

Books should be kept separately from

HQs.

When investing in Argentina, foreign investors usually set their business using the investment vehicles described in the following table. All of them created and are regulated by the Inspección General de Justicia (IGJ).

In addition to the above listed, there are other forms of investment entities that foreign investors have to establish their business in Argentina:

• Partnerships: no minimum capital, all partners are jointly and severally liable for the partnership’s obligations.

• Joint Ventures: temporary associations to develop a specific work.• Cooperating Groups: common organization between several parties

to develop or improve certain phases of its clients activities. It has a contractual basis.

• Cooperating Consortium Agreement: similar to Cooperation Groups, but members may not agree jointly and severally liable for the obligations.

• Trusts: structure which allows an endeavour to isolate certain assets or property to use them for specific purposes.

ArgentinaBusiness Types

© 2017 Deloitte & Co. S.A. All rights reserved.

Source: National Investment & Trade Promotion Agency.

Financial Activities(FEA No 21,526)

The Central Bank (BCRA) is responsible for regulating and supervising financial institutions, authorizing the operation,

merger or transfer of activities and authorizing the establishment of

foreign bank branches or representative offices in Argentina.

Insurance Activities(Law No 12,988 & 20,091)

Only issuers authorized by the Superintendence of Insurances (SNN)

may perform insurance activities. Only Corporations incorporated in

Argentina, branches with assigned local capital and SOEs can perform

insurance activities.

Capital Markets Regulations

- Law No 17,811 (as amended by Law No 26,831): enacts the rules for the

public offering regime.- CNV (Argentine Securities

Commission) states the regulatory framework – all agents and issuers

have to be authorized and comply with requirement determined by CNV.

Oil & GasLaw No 17,319: Exploration

and production regulation, as well as the hydrocarbons exploration, development and production.

Hydrocarbon operation needs a Federal concession or permit.

Law No 13,660: Downstream regulation.

Exploration should be approved by the E&M ministry through a biding process.

Mining(Mining Code – Law No 1,919)

A concession is needed to develop mining activity, in which the

concessionaire must pay an annual royalty to Federal/Provincial

Government. Mining activities have tax incentives which should be analysed before the

investment.

Energy & Resources(Law No 24,065, 26,190

& 27,191)

Legal framework divides the sector in: generation, transmission, distribution

and demand.New regulation for the Renewable

Sources of Energy (RSE) which states tax benefits for the ones in charge of projects – need to be certified by RSE

Program.

ArgentinaRegulatory Framework

© 2017 Deloitte & Co. S.A. All rights reserved.

Source: National Investment & Trade Promotion Agency and Deloitte own analysis based on AFIP.

Federal Taxes Provincial & Municipal Taxes

Income TaxValue Added Tax

Minimum Presumed Income TaxPersonal Assets Tax

Tax on Financial TransactionsCustoms Duties

Turnover TaxReal Estate Tax

Stamp DutyTax on Vehicles

Tax on Public AdvertisingOthers

The Argentine tax system is composed of Federal, Provincial and Municipal taxes. It is a self-assessment system (or enterprise) and its period it’s the calendar year.

Main Business Taxes

Corporate Income Tax• Rate: 35% flat• Territoriality: for resident companies, worldwide income is taxable. Branches

must keep a separate book for its operation in Argentina.• Period: it is reported and paid annually.Value Added Tax (VAT)• Rate: general is 21% - 27% for electricity, natural gas and water supply and

10,5% is applied to some activities.• Territoriality: Argentinian transactions except for exports which pay zero rate –

imports VAT can be recovered through tax refunds.• Period: it is reported and paid monthly.Minimum Presumed Income Tax• Rate: 1% flat (minimum value of assets in the country: AR$ 200k)• Territoriality: all assets in Argentina and abroad owned by local companies. • Period: it is reported and paid annually.• Observations: it complements income tax whenever the income tax liability does

not exceed the minimum presumed income tax.

© 2017 Deloitte & Co. S.A. All rights reserved.

ArgentinaTax System

Industry SnapshotConsumer Goods & Retail: Food, Beverage & Tobacco

Industry Highlights

Industry Subsector Main Players

Non-Perishable Food

Ready Meals

Dairy

Bakery, Biscuits & Snacks

Non-AlcoholcBeverages

Alcoholic Beverages

Tobacco

Industry Subsectors

Source: The Economist Intelligence Unit

The Argentine Consumer Goods industry is the largest in the region after Brazil and Mexico. Yet, the high levels of inflation and the weak economic growth that thecountry experiences since the consumer spending boom halted in 2012 has nothelped the industry develop. Furthermore, Cambiemos’ economic policy making has not helped reactivate the sector and combined with a local-currency depreciation, the retail market in 2016 is smaller than it was in 2012 in US-dollar terms.

The Economist Intelligence Unit forecasts that retail sales will rise sharply in nominal, local-currency terms to US$130bn by 2020, but this will mostly be explained by high levels of inflation pushing up prices. Instead, the real retail sales growth will average 2.20% in 2016-20 in US-dollar terms, as consumer confidence improves and inflation subsides.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Overview

The 4 firm Herfindahl-HirschmanIndex of market concentration:

PerfectCompetition

10.000

1

Monopolist

2.500

1.000

= =

Current Market

Concentration2.446

Moderate

High

Low

Molinos Río de la Plata is the leadingand dominant firm in the Non-Perishable food subsector as its portfolio companies account for approximately 49% of the market. Other competitors that fall behind the market leader are Molinos Ala (5%), Unilever (4%) and Dos Hermanos (2%).

Molinos Río de la Plata’s swide variety of brands in different price bands allows them to be the most important company within the category.

Source: Euromonitor Intelligence 2017, International Pasta Organization.

The market for non-perishable food in Argentina is significant. Argentines eat an average of 9,1 kilograms of pasta per year, and remain as the sixth nation that consumes more dry pasta in the world according to the International Pasta Organization. It is also estimated that each Argentine national eats an average of 10 kilograms of rice per year. Hence, the focus of the Non-Perishable subsector will focus on its biggest segment: Rice, Pasta and noodles.In 2016, Euromonitor Intelligence estimated that the market for rice, pasta and noodles grew 4% in retail volume terms and 24% in current value growth, thus reaching a value of ARS17,100 million. Companies have reinvented the consumption of dried pasta to boost consumption, while rice registers the highest growth of 7% in retail volume terms in 2016. However, the high levels of inflation have made the average unit price of the standard unit in the industry rise by 19%.

Lead Players Market Concentration Ratio

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Brief: Non-Perishable Food

Company OriginFootprint in Argentina

BrandsMarket ShareRice, Pasta &

Noodles

Alicorp Argentina Production <1%

CV Trading ArgentinaImport &

Distribution2%

Dos Hermanos ArgentinaProduction & Distribution

2%

El Sol de BellaVista

Argentina Production <1%

GualtieriHermanos

Argentina Production <1%

La Cachuera Argentina Production <1%

La Salteña

(General Mills)

US Production 2%

Ladislao Popelkay Cia

Argentina Production <1%

Lee Kwon Chan ArgentinaImport &

Distribution<1%

Liu Li Wei ArgentinaImport &

Distribution<1%

Molino Arrocero Milenum

ArgentinaProduction & Distribution

1%

Molinos Ala ArgentinaProduction & Distribution

5%

Molinos Río de la Plata

ArgentinaProduction & Distribution

49%

OblimarArgentina Production <1%

Sagemuller Argentina Production<1%

Unilever

UK-Netherland

sProduction & Distribution

4%

Villa d’Agri Argentina Production <1%

Source: Euromonitor Intelligence 2017.© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Non-Perishable Food

The ready meals market in Argentina is considered by many as an under-developed niche. According to Nielsen Consulting, the market revenues reaches AR$1200 million and has a potential grow significantly, as the argentina per capita average consumption is of 1,6 kilograms, 60% less than Chile’s and Brazil's per capita demand for the products in the segment.Yet, in 2016 the ready meals market declined by 8% in retail volume terms but increased by 34% in current value terms to reach ARS986 million. Dried ready meals registers the worst performance with a fall of 10% in retail volume terms in 2016. The rationale behind lower levels of consumption for these product-types is that homemade meals have been substituting ready meals as a result of the economic crisis.

The 4 firm Herfindahl-HirschmanIndex of market concentration:

PerfectCompetition

10.000

1

Monopolist

2.500

1.000

= =

Current Market

Concentration2.565

Moderate

High

Low

Molinos Río de la Plata is the leading firm in the Ready Meals food subsector as its portfolio companies account for approximately 46% of the market.

Other competitors that fall behind the market leader are McCain (16%), Unilever (12%) and Buenos Aires Food (7%).

In the past years Molinos Río de la Plata increased its retail value share in ready meals by 15 percentage points. This excellent performance was down to the repositioning of its brand Gallo in dried ready meals, which pushed the Knorrbrand from Unilever into second place.

Source: Euromonitor Intelligence 2017, Nielsen Consulting Report 2016.

Lead Players Market Concentration Ratio

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Brief: Ready Meals

Company OriginFootprint in Argentina

Brands

MarketShareReady Meals

Buenos Aires Food (Dr Oetker)

Germany Production 7%

Carrefour France Distribution <1%

Family Group Argentina Production <1%

Coto Argentina Distribution <1%

Día Spain Distribution <1%

General Mills USProduction & Distribution 4%

Jumbo (Grupo Cencosud)

Chile Distribution <1%

Molinos Rìo de la Plata

ArgentinaProduction & Distribution

46%

McCain USProduction & Distribution

16%

BRF BrazilProduction & Distribution

4%

Unilever UK-NetherlandsProduction & Distribution

12%

Walmart US Distribution <1%

Source: Euromonitor Intelligence 2017.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Ready Meals

In 2016, the annual per capita quantity of pasteurized, UHT and Chocolate milk consumed in Argentina was of 40,10 liters, and represented a 10% decrease with respect with 2015, according to the Ministerio de Agroindustria.The drinking Milk Products category remained relatively constant in terms of retail volume in 2016. The increasing demand of drinking yogurt combined with the rise in cost per average unit has had a negative impact on the performance of the dairy products.Mastellone Hnos leads the market with a retail value share of 41% in 2016. The second most important player is Sancorwith 16% of market share.

The 4 firm Herfindahl-HirschmanIndex of market concentration:

PerfectCompetition

10.000

1

Monopolist

2.500

1.000

= =

Yoghurt & Sour Milk5.079

High

Low

Other Diaries2.072

Drinking Milk Products2.022

The Market for Other Dairy remained the unchanged in terms of retail volume in 2016. Euromonitor international estimates that the market value for this segment can be estimated at ARS 10,700 million. Danone is leading the market with a retail value share of 36%. Other industry key players are Sancor and Mastellone Hnos that through their brands hold 22% and 16% of the market share for the segment.

The Yoghurt and Sour Milk market declined by 3% in 2016. The current value of the market is about ARS 13,200 million. The drinking yoghurt market declined by 1% compared with a 35% rise in the average unit price in the segment. This suggests the strong consumer preferences for Yoghurt and Sour Milk in Argentina.Danone continues to dominate yoghurt and sour milk products in 2016 with a market share of 69%. The second market share position is detained by Sancor with 17%.

Source: Euromonitor Intelligence 2017, Ministerio de Agroindustria 2017.

Drinking Milk Products

Yoghurt and Sour Milk Other Milk Products

Market Concentration Ratio

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Brief: Diaries

Company OriginFootprint

in Argentina

Brands

MarketShare

Drinking Milk

Products

MarketShare

Youghurtand Sour

Milk

MarketShareOther Diary

Carrefour France Distribution <1% N/A <1%

CencoSud Chile Distribution <1% N/A <1%

Coto Argentina Distribution <1% N/A <1%

Danone FranceProduction & Distribution

3% 69% 36%

Día Argentina Distribution <1% <1% 2%

La Sibila ArgentinaProduction & Distribution

<1% N/A N/A

LácteosConoSur

ArgentinaProduction & Distribution

<1% 1% 1%

Mastellone ArgentinaProduction & Distribution 41% N/A 16%

Milkaut ArgentinaProduction & Distribution

3% 2% 1%

NestléSwitzerlan

dProduction & Distribution

5% N/A <1%

RPB SA ArgentinaProduction & Distribution

<1% N/A N/A

SanCorCooperativas

ArgentinaProduction & Distribution

16% 17% 22%

Sucesores de Alfredo Williner

ArgentinaProduction & Distribution

7% 5% 6%

The Coca-Cola Company

USProduction & Distribution

6% N/A N/A

Veronica SA ArgentinaProduction & Distribution

<1% N/A <1%

Wal-Mart US Distribution <1% N/A <1%

Source: Euromonitor Intelligence 2017.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Dairy

The 4 Firm Herfindahl-HirschmanIndex of market concentration:

PerfectCompetition

10.000

1

Monopolist

2.500

1.000

= =

Salty Snacks Market6.508

Biscuit Market2.670

Sweet Snacks Market2.742

Moderate

High

Low

Alfajores Market1.566

Consumers in Argentina buy 7kgs of biscuits per year, according to Kantar Worldpanel. The overall market value of the Argentinean biscuits market grew by 7.21% totaling to 310.88 Million Kgs in 2016. Arcor is the leading firm in Biscuit segment with 49% of the market, followed by Mondelez with 16%, Granix with 4%, and Don Satur with 3%.

The annual per capita consumption of Salty Snacks in Argentina is of 1 kg, and remains relatively low when compared to that of Uruguay (1,6kg), and Chile (2,3 kg). Even though consumption has fallen considerably in the past few quarters, the segment is considered an interesting niche by several players eager to expand.Pepsico is the leading and dominant firm in this segment with 80% of the market, followed by 5 Hispanos with 10%.

Consumers in Argentina buy 24 alfajores per year, according to study conducted by CCR in 2015.Kids and teen-agers, raging from 8 to 18, account for 80% of the demand of the product in Argentina. Arcor is the leading firm in this segmentwith 30% of the market, followed byMondelez with 19%, Jorgito with 17%,and Guaymallén with 4%.The sweet snacks market is lead byArcor, whose brands account for the46% of the market. Mondelez followsthe lead with 24%, and Ferrero andBonafide have mantained a good part ofthe market with 5% each.

Market Concentration RatioAlfajores & Sweet Snacks Products

BiscuitsSalty Snacks Products

Source: Euromonitor Intelligence 2017, Kantar World Panerl, CCR 2015, El Cronista.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Brief: Biscuits & Snacks

CompanyFootprint in Argentina

Origin BrandsMarket ShareBiscuits

Market Share

Alfajores

MarketShareSweet Snacks

MarketShare

Salty Snacks

5 HispanosProduction & Distribution

Argentina N/A N/A N/A 10%

Arcor S.AProduction & Distribution

Argentina 49% 30% 46% <2%

Bonafide Production Argentina N/A <1% 5% N/A

CachafazProduction & Distribution

Argentina <1% <1%<1%

N/A

Don SaturProduction & Distribution

Argentina 3% N/A N/A N/A

FantocheProduction & Distribution

Argentina N/A <1% <1% N/A

Fel FortProduction & Distribution

Argentina N/A <1% <1% N/A

Ferrero S.A. Production Italy N/A N/A 5% N/A

Guaymallén Production Argentina N/A 4% N/A N/A

GranixProduction & Distribution

Argentina 4% N/A N/A N/A

HavannaProduction & Distribution

Argentina N/A <1% 5% N/A

Jorgito Production Argentina <1% 17% N/A N/A

La Nirva Production Argentina N/A <1% N/A N/A

Molinos Río de la Plata

Production & Distribution

Argentina <1% <1% <1% <2%

Mondelez S.A

Production & Distribution

USA 16% 19% 24% <2%

Pepsico

Production & Distribution USA <1% <1% N/A 80%

Tia MarucaProduction & Distribution

Argentina 2% N/A N/A N/A

Source: Euromonitor Intelligence 2017.© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Biscuits & Snacks

Company OriginFootprint in Argentina

Brands Market Position

Balcarce Argentina Production National Bakery

Breviss Argentina Production National Bakery

Carrefour France Dist. & Retail 2nd Brand Product

Cencosud Chile Dist. & Retail 2nd Brand Product

Coto Argentina Dist. & Retail 2nd Brand Product

Doña Noly Argentina Production National Bakery

Grupo Bimbo Mexico Production Regional Leader

La Perla Argentina Production National Bakery

Molinos Cañuelas Argentina Production & Dist. National Bakery

Riera Argentina Production National Bakery

Walmart USA Dist. & Retail 2nd Brand Producs

In the past years, wheat flour production dropped due to draught conditions suffered during the 2013 harvest, which caused an exorbitant price hike of more than 30% in artisanal/unpackaged bread. Consequently consumers switched to lower-priced bakery products, in which biscuits was the main beneficiary.Artisanal bread is an important element of the Argentinean consumer’s food basket, which over the last years has been left behind due to the trend towards healthy, natural food.

Highly Concentrated Industry:

• Grupo Bimbo is the leading firm in this sub-industry with a significant foothold on the market as it is estimated that its portfolio brands account for approximately 80% of the market.

• The 25% left of the market can be traced back to national bakeries and 2nd brand products.

10.000

1

An estimation of the Herfindahl-Hirschman Index of market

concentration is:

Monopolist

PerfectCompetition

2.500

1.000

= =

Current Market

Concentration

Moderate

High

Low

Source: Euromonitor Intelligence 2017.

Industry Highlights Market Concentration Ratio

Main Players

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Bakery

Carbonates sees volume decline of 1% in 2016 to reach 6,300 million liters. The growth of inferior brands given economic uncertainty catapulted Manaos as the new star Brand in the sector. Coca-Cola FEMSA is the leading firm in the Carbonate Beverages sub-industry as its portfolio brands account for approximately 51% of the market, followed by Pepsico and the argentine-national RefresNow which account for 13% and 7%, respectively.

The Herfindahl-Hirschman Indexof market concentration:

PerfectCompetition

10.000

1

Monopolist

2.500

1.000

= =

Bottled Water (4-Firm HHI)675

Carbonate Beverages

(4-Firm HHI)2.855

Sport Drinks

(2-Firm HHI)4.993

Moderate

High

Low

In 2016, the market total volume sales grew 2% to reach 5.2 billion litres. During 2016 the total sales of second-brands accelerated significantly. The bottled water market in Argentina is a competitive market led by Grupo Danone’s portfolio companies accounting for the 21% of the market share. The group has one of the widest distribution networks in the country.The argentine IVESS follows the lead with 11% of the market volume. Coca Cola Femsa’s (7%), Nestlé’s (6%) and Pepsico’s (3%) fall behind another Argentine water-supplier, Cimes, that falls third according to Euromonitor with 8% of the bottled water market volume.

Sports Drinks saw a total volume growth of 4% and reached 87 million liters in 2016. Pepsico’s Gatorade leads the much smaller market of Isotonic Beverages with 63% of the market share, followed by Coca-Cola’s Powerade with 32%. It is noteworthy to mention that Powerade has been experiencing strong growth as its market share rose from 21% in 2013 to the actual level in 2016.

Sports Drinks

Bottled Water Market Concentration Ratio

Carbonate Beverages

Source: Euromonitor Intelligence 2017.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Brief: Non-Alcoholic Beverages

CompanyIndustry Position

(Lead-Mid-Small)

Footprint in Arg.

Brands

Market ShareBottled Water

Market ShareSportsDrinks

Market Share

CorbanateDrinks

Coca-Cola FEMSA

Leader Production 7% 32% 51%

Nestlé S.A. LeaderProduction & Distribution

6% N/A N/A

Pepsico S.A.I.C. Leader

Production & Distribution

by third party (CerveceríaQuillmes)

3% 63% 13%

Grupo Danone Leader

Production & Distribution done by 3rd

Party

21% N/A N/A

Refres Now MediumProduction & Distribution

N/A N/A 7%

Prodea MediumProduction & Distribution

N/A N/A 4%

Cimes MediumProduction & Distribution

8% N/A N/A

IVESS MediumProduction & Distribution

11% N/A N/A

NutrecoAlimentos

MediumProduction & Distribution

1% N/A N/A

Pritty SA SmallProduction & Distribution

<1% N/A 6%

CarrefourNot focused on the Segment

Distribution <1% N/A 3%

CotoNot focused on the Segment

Distribution <1% N/A 2%

Source: Euromonitor Intelligence 2017.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Non-Alcoholic Beverages

Argentina is traditionally a wine-drinking country but, the total consumption of wine has been declining in the past few years. Beer has been gaining popularity and since 2012 has beaten all other alcoholic beverages with a per capita consumption of 44,7 liters.The Beer industry appears to be highlyconcentrated specially after AbInbev’smerger with SABMiller. Recent studiesshow that AbInbev accounts for 71% ofthe market followed by CCU and Isenbeckwhich account for 22% and 4%,respectively.

10.000

1

The Herfindahl-Hirschman Index of marketconcentration:

Monopolist

PerfectCompetition

2.500

1.000

High= =

Beer Market

(3 Firm HHI)5.541

Low

Spirits Market

(4 Firm HHI)1.319

Wine Market

(4 Firm HHI)1.319

In 2016 the wine industry is recovering from a decline in 2015, registering total volume growth of 5% to reach sales of 1.1 billion liters. The industry is predicted to post a total volume CAGR of 2% until 2021.FeCoViTa is the leading firm in wine segment with 26% of the market. The Grupo Peñaflor follows the lead with 22% of the market volume. LicoresArgentinos (7%) and Bodegas y ViñedosGarbin (7%) fall behind RPB, that accounts for 8% of the wine market voiume.

The Spirits market exhibits a more competitive environment than the beer market, given the high levels of product differentiation across its actors. Within this sub-industry, the Fernet is the product with the strongest foothold. Fratelli Branca accounts for 50% of the Fernet market, while Grupo Cepasfollows the lead with 15% of it. The argentine Fratelli Branca sets the lead with 27% of the spirit market volume and accounts for 50% of the Fernet sales in the country. Pernod Ricard occupies the second place with 21%, Sabia Campari with 10%, and Grupo Cepas with 7% of the market volume.

Source: Euromonitor Intelligence 2017.

Wine

Spirits Drinks

Beer

Market Concentration Ratio

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoIndustry Brief: Alcoholic Beverages

Company OriginFootprint in Argentina

Brands

Market

ShareBeer

Market

Share

Spirits

MarketShare

Wine

AB InBev BelgiumProduction & Distribution

71% N/A N/A

Grupo Cepas ArgentinaProduction & Distribution

N/A 7% 3%

Compañía de Cervecerías

Unidas

ChileProduction & Distribution

22% N/A N/A

FratelliBranca

ArgentinaProduction & Distribution

N/A 27% N/A

PernodRicard

FranceProduction & Distribution

N/A 21% N/A

Diageo UKProduction & Distribution

N/A 6% N/A

Sabia Campari

ArgentinaProduction & Distribution

N/A 10% N/A

Grupo Peñaflor

ArgentinaProduction & Distribution

N/A N/A 22%

Cervecería Argentina Isenbeck

ArgentinaProduction & Distribution

4% N/A N/A

FeCoViTaCoop

ArgentinaProduction & Distribution

N/A N/A 26%

RPB ArgentinaProduction & Distribution N/A N/A 9%

Bodegas y Viñedos Garbin

ArgentinaProduction & Distribution

N/A N/A 6%

Bodegas ValentínBianchi

ArgentinaProduction & Distribution

N/A N/A 3%

MoetHennessy

FranceProduction & Distribution

N/A N/A 3%

Licores Argentinos

ArgentinaProduction & Distribution

N/A N/A 7%

Llorente y Compañía

ArgentinaProduction & Distribution

N/A N/A 2%

Source: Euromonitor Intelligence 2017.

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Alcoholic Beverages

Company Origin Industry Position(Lead-Mid-Small)

Footprint in Argentina

Brands MarketShare

MassalinParticulares

Phillip Morris International

US Leader Production70% (aprox.)

British American Tobacco

UK Leader Production27% (Aprox.)

According to data from the Ministerio de Salud, besides the fact that 21% of women and 30% of men in Argentina smoked in 2013, the annual per capita consumption of argentines aged 15 or older is 1.014 cigarettes.Prices remain low, in spite of the recent introduction of a new regulatory framework in the industry. Yet, health warnings are compulsory, advertising directed at younger generations is prohibited and marketing is banned from television between 8 am and 10 pm.

Highly Concentrated Industry:

• Phillip Morris International is the leading firm in this sub-industry with a quasi-monopoly on the market as two of its portfolio brands account for approximately 70% of the market.

• The other main player is British American Tobacco that accounts for27% of the Argentine Market of Tobacco.

Source: Euromonitor Intelligence 2017, Ministerio de Salud.

Industry Highlights

Main Players

10.000

1

The 2-firm Herfindahl-HirschmanIndex of market concentration:

Monopolist

PerfectCompetition

2.500

1.000

= =

Current Market

Concentration5.629

Moderate

High

Low

Market Concentration Ratio

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoMain Players: Cigarettes

Source: Deloitte’s elaboration based on Mergermarket & Thompson Reuters information.

Year Target Acquirer Acquirer Origin Deal Ticket

2017 Dilexis S.A. Tía Maruca Argentina N/D

2017 PotigianGolosinas

Private Investor Argentina N/D

2016 Sancor(Youghurt & Dessert Production Unit)

Vicentín SAIC Argentina 100 Million

2016 Viña Cobos SA Molinos Río de la Plata

Argentina 12 Million

2016 Main Process Agrana Austria N/D

Deal Volume & Value

Acquirer’s Origin – 2016 (Volume)

North America8%

Latin America65%

Asia & Oceania5%

Europe19%

Recent DealsUnknown: 3%

0%

10%

20%

30%

0

10

20

30

2012 2013 2014 2015 2016 2017

Deal Volume Deal Volume

© 2017 Deloitte & Co. S.A. All rights reserved.

Consumer: Food, Beverage & TobaccoRecent M&A Activity

Industry SnapshotFinancial Services

In Argentina, the financial services industry -under the category “financial intermediation and other services” – accounted for 3,8% of GDP in 2015, according to the Instituto Nacional de Estadística y Censos (INDEC). Currently, the industry employs about 164,000 workers, or 2,5% of the registered labour force, in line with the Ministry of Labour.There is scope for substantial growth in banking in the country in the medium term given a population of just over 43M, high per-head incomes (by comparison with much of the rest of Latin America) and very low level of private-sector credit as a percentage of GDP.

Source: BCRA, World Bank, EIU.

Argentina in the Region - 2016

Argentina Brazil Chile Colombia Mexico Peru

Deposits/ GDP

29,2 109 54,4 35,6 28,1 74,6

Loans 75.034 921.988 217.894 146.558 201.163 70.161

Financial Assets/

GDP

105,2 669,6 568,9 336,2 262,3 211,4

Deposits over GDP

0,0

20,0

40,0

60,0

80,0

100,0

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Argentina Brazil Chile Colombia México Perú

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesIndustry Overview

Source: BCRA, EIU.

Financial Assets over GDP (% of GDP)

Industry Subsectors

AmountMain Players

Foreign Domestic

Financial Entities

83

Insurance Companies

184

Asset Managers 814 (funds)

Specialty Financing Companies

200 aprox.

Financial Regulation

Argentina has multiple regulators for different types of financial firms:• The Banco Central de la República Argentina (BCRA) is responsible for the

oversight of Banks and finance companies. In addition it is responsible for the monetary policy, the payment system, overall financial stability and the issuance of notes and coins.

• The Superintendencia de Seguros de la Nación (SSN) provides oversight for primary insurers, reinsurers and agents.

• The Comisión Nacional de Valores (CNV), supervises securities and derivate markets, brokers and investment funds.

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F 2021F

Argentina Brazil Chile Colombia México Perú

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesIndustry Overview

A programme of policy adjustment is ongoing and will reduce economic distortions. However, up to now, banks are still affected by a weak economy and high nominal interest rates. Credit remains low as a percentage of GDP, at an estimated 13% over GDP in 2015.Growth in credit to private sector remains high in nominal terms, and negative in real terms due to high inflation registered in October 2016. Personal lending had also rapid growth (44% year to year) from Ahora 12, an Interest-free 12-month credit plan announced in 2015. Currently revamped into Ahora 18 in order to boost consumption.

Argentinians are modest users of bank accounts. Around 50% of the adult population had an individual or shared account at a formal financial institution in 2014, according to the World Bank.Even though 19% of those surveyed, reported that they had borrowed money, just 8% received loans from financial institution while another 6% had borrowed from family. In the same way though 23% of respondents said that they had saved money, only 4% did so at a financial institution.

Total Loans (US$ Bn) Total Deposits (US$ Bn)

Source: BCRA. IMF, EIU.

14,117,1

24 24,9

31,2

25,8

16,5

0

5

10

15

20

25

30

35

Lending Interest Rate (%)

12

14,9

20,4 21,2

24,3

18,816,5

0

5

10

15

20

25

30

2012 2013 2014 2015 2016 2017F2018F

Deposit Interest Rate (%)

0

20

40

60

80

100

ST Loans LT Loans

0

50

100

150

200

2014 2015 2016 2017F 2018F 2019F 2020F

Time & Savings DepositsCurrent-Account Deposits

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesFinancial Entities

0 10.000 20.000 30.000 40.000 50.000 60.000 70.000 80.000 90.000100.000

Santander Río

Galicia y Buenos Aires

Francés SA

Macro SA

HSBC Bank

Credicoop Coop.

Patagonia SA

Industrial

Citibank

Hipotecario

Superville SA

Prov. De Córdoba

Nuevo Santa Fe SA

San Juan SA

Itau Argentina

Comafi SA

La Pampa SEM

Nuevo Entre Ríos

Banco Industria

Santiago del Estero SA

Otros

Ranking

Main Players

Concentration in the banking sector is high. By the end of 2015, the top five Banks represented over 55% of the market in terms of deposits. The top ten Banks over 70%.In terms of assets, the largest domestic Banks are the state-owned: Banco de la Nación Argentina, which accounts 25,5% of total assets, the private Banco de Galicia y Buenos Aires (7,5%) and the Buenos Aires province-owned Banco de la Provincia de Buenos Aires (7,4%).The main foreign Banks are Spanish-owned Banco Santander Río (8,3% of total assets) and BBVA Banco Francés (5,9%), HSBC (UK, 3,8%), Banco Patagonia (Brazil 3,2%), Industrial and Commercial Bank of China (China, 3,2%), Citibank (US, 3,2%) –recently acquired by Santander Río -, and Banco Itaú (Brazil, 1,2%).While the new government focuses on ironing out some of the macroeconomic distortions, there will be significant scope for M&A activity.

Source: BCRA.

Assets

Loans

Deposits

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesFinancial Entities

The insurance market is still small and remains highly fragmented. There were 186 insurance companies in service by the end of 2016. The high levels of GPD per head in the past decade have improved penetration of insurance services in the local market.There has been rapid growth in premiums in recent years, according to the Superinendencia de Seguros de la Nación (SSN): premiums rose to AR$211.000M in June 2016, representing year-on-year growth of 38%. As share of GDP, premiums represent around 3%, which is well below the OECD average of 8% of GDP and suggests significant scope for catch-up with mature markets.

Source: Superintendencia de Seguros de la Nacion.

Main Subsectors

Property Insurance

Personal Insurance

Life InsuranceRetirement Insurance

Issued Premiums per Subsector (Q of Premiums)

0

50.000

100.000

150.000

200.000

250.000

300.000

2010 2011 2012 2013 2014 2015 2016

Millions

Property Personal Life Retirement

33.39645.006

59.388

80.626

108.913

153.321

211.027

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesInsurance Companies

32.613

3.533

3.559

3.588

3.746

3.767

3.960

4.366

4.463

4.841

5.326

6.306

6.628

7.066

9.481

13.946

-5.000 5.000 15.000 25.000 35.000

Others

MAPFRE

Royal & Sun Alliance

Meridional

Nación

Provincia

Mercantil Andina

Zurich

Segunda

QBE Bs As

B. Rivadavia

San Cristobal

Allianz

Sancor

Caja Generales

Fed. Patronal

Millions

Source: Superintendencia de Seguros de la Nacion.

7.788

539

586

628

657

664

752

1.191

1.311

1.473

1.784

1.862

1.964

2.074

2.199

2.224

0 10.000 20.000 30.000

Others

Opción

Fed. Patronal

Caruso

Assurant

ACE

CNP

Zurich Santander

BBVA Consolidar

Provincia

Sancor

Nación

Cardif

Galicia

Caja Generales

MetLife

Millions

Personal Insurance Companies – 2016 (by Premium in AR$)

Property Insurance Companies – 2016 (by Premium in AR$)

Total Premiums: AR$ 117.189 M

Amount of Companies: 109

Top15 Share: 72%

Total Premiums: AR$ 27.696 M

Amount of Companies: 84

Top15 Share: 72%

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesInsurance Companies

438

153

157

170

254

294

299

305

357

509

577

660

846

935

977

1.383

-5.000 5.000 15.000 25.000 35.000

Others

Tres Provincias

Mañana

Plenaria

Qualia

Segunda Personas

Instituto Salta

Provincia Vida

Binaria Vida

MAPFRE Vida

SMG Vida

Origenes Vida

Zurich International Life

HSBC Vida

Prudential

BHN Vida

Millions

Source: Superintendencia de Seguros de la Nacion.

0

1

4

5

24

39

52

90

136

144

225

337

2.524

-5.000 5.000 15.000 25.000 35.000

Galicia Retiro

Fed. Patronal Retiro

SMG Retiro

MetLife Retiro

Credicoop Retiro

Inst. Entre Ríos Retiro

Binaria Retiro

San Cristobal Retiro

HSBC Retiro

Segunda Retiro

Orígenes Retiro

Nación Retiro

Estrella Retiro

Millions

Retirement Insurance Companies – 2016 (by Premium in AR$)

Life Insurance Companies - 2016 (by Premium in AR$)

Total Premiums: AR$ 8.314 M

Amount of Companies: 36

Top15 Share: 95%

Total Premiums: AR$ 3.581 M

Amount of Companies: 13

Top15 Share: 100%

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesInsurance Companies

449

384

822

943

3.812

4.029

5.458

7.664

9.319

10.105

10.905

-5.000 5.000 15.000 25.000 35.000

Others

Liderar ART

Omint ART

Berkley ART

Swiss Medical ART

Segunda ART

Asociart ART

Experta ART

Provincia ART

Galeno ART

Prevención ART

Millions

Source: Superintendencia de Seguros de la Nacion.

Labour Risk Insurance Companies - 2016 (by Premium in AR$)

Total Premiums: AR$ 53.889 M

Amount of Companies: 12

Top15 Share: 100%

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesInsurance Companies

Argentina’s fund-management industry was busted by the 2001-2002 crisis, and afterwards, in 2008, by the time the government nationalized the system of private pension funds.The Argentinian mutual-fund segment is smaller than the now-extinct pension-fund market: around U$S17Bn under management - much less than in other Latin American countries. Only around 150k Argentines (over a 43-million population) invest in mutual funds, compared with 20M investors in Brazil. Most investments are in money-market and bond funds, with only a short percentage of assets dedicated to shares.

Top Ten Mutual Fund Managers in Argentina

Source: Deloitte’s analysis based on EIU and CNV.

Bancarized Non-Bancarized

Lo

cal

Fo

reig

n

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesAsset Management

AgencyNumber of operations

Libres Cambio S.A. 13,861

Andina Internacional Cambio y Turismo S.A. 13,859

Transatlántica S.A. 11,161

Cambio García Navarro, Ramaglio y Cía S.A. 10,726

Cambio, Excursiones, Turismo Columbus S.A. 9,281

Montevideo Cambio y Turismo S.A. 9,035

Tourfé S.A. 6,942

Valuar S.A. Agencia de Cambio 6,707

Thaler Agencia de Cambio S.A. 6,659

García Navarro y Cía S.A. 6,204

Others 74,820

Top ten change agencies2014

AgencyNumber of credit

cards

Debt > 90days

Tarjeta Naranja S.A 7.034.800 9,46%

CMR Falabella S.A 1.712.420 5,57%

Cencosud S.A 1.322.979 5,86%

American Express Argentina S.A 908.343 1,08%

Tarjetas Cuyanas S.A 718.609 12,06%

Tarshop S.A 491.270 18,48%

Gramit S.A 377.840 7,83%

Tarjetas del Mar S.A 321.985 9,4%

Italcred S.A 293.550 51,72%

Sistema de Crédito de Entre Ríos S.A 278.324 1,84%

Others 2.238.414 -

Top ten credit cards emisors2014

Source: BCRA.

6,2

6,7

6,7

6,9

9,0

9,3

10,7

11,2

13,9

13,9

2,2

0,3

0,3

0,3

0,4

0,5

0,7

0,9

1,3

1,7

7,0

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesSpecialty Financing Entities

Source: Deloitte’s analysis based on Mergermarket & Thompson Reuters information.

Year Target Acquirer Acquirer Origin

Deal Ticket (US$ M)

2017 Banco Interfinanzas

Investor Group Argentina N/D

2016 Citi Argentina (Retail Bank)

Santander Río Spain

2016 RSA InsuranceLatin America

Suramericana Colombia 615

2016 Tarjetas del Mar

Investor Group Argentina 15

2016 MBA Lazard Asset Mgmt

Lazard France N/D

1410

47

10

3

0%

20%

40%

0

10

20

2012 2013 2014 2015 2016 2017 Q1Deal Volume Participation on Period Activity

Deal Volume

Acquirer’s Origin – 2016 (Volume)

North America10%

Latin America80%

Europe10%

Recent Deals

© 2017 Deloitte & Co. S.A. All rights reserved.

Financial ServicesRecent M&A Activity

Industry SnapshotAgribusiness

AgribusinessIndustry OverviewIndustry Highlights

Argentina is one of the leading countries in the commercialization of soybeans, wheat and meat. In addition to that, Argentina is also an important producer of wool and wine. Nevertheless, the major part of wine consumption is done domestically.- In Argentina, 20.3 million of hectares are devoted to the production of soybeans.

The states where the majority of the this commodity is grown the regions of Buenos Aires, Cordoba and santa Fe.

- Sugarcane and citrus plantations are also largely present in Argentina. Indeed, the citrus were generally introduced as a protection against the instability of the sugar market. The Jujuy and Salta provinces are largely used to the growth tobacco. Moreover, The west of the Paraña River is mainly utilized to cultivate cotton.

- Livestock are traditionally reared in the Pampas province, it is the most renowned and valuable commodities in Argentina. Indeed, the local producers have been able to adapt quickly and accurately to the riskiness of the market. They switched between breeds when one has a better yield and change their way of feeding their production by substituting the Alfalfa feed with sorghum grain to have a better meat.

- Additionally, Corrientes and Entre Ríos are also know for their cattle raising production following those of the pampas. The Criollo cattle is manly reared in the Chaco province. Finally, the majority of the sheep are produced in Patagonia, the south region of Argentina.

Source: Global Economy.

Activity Main Players

Cereals & Oilseeds

production

Soybean, corn, wheat,

barley, sunflower, sorghum, peanut

Animal Raising &

Animal Protein

Production

Animal raising and animal

protein production

Fruit Production

Apples, Pears & Citric

Animal Feed

Nutritional products for animal feed

SugarSugar

production

Industry Subsectors

© 2017 Deloitte & Co. S.A. All rights reserved.

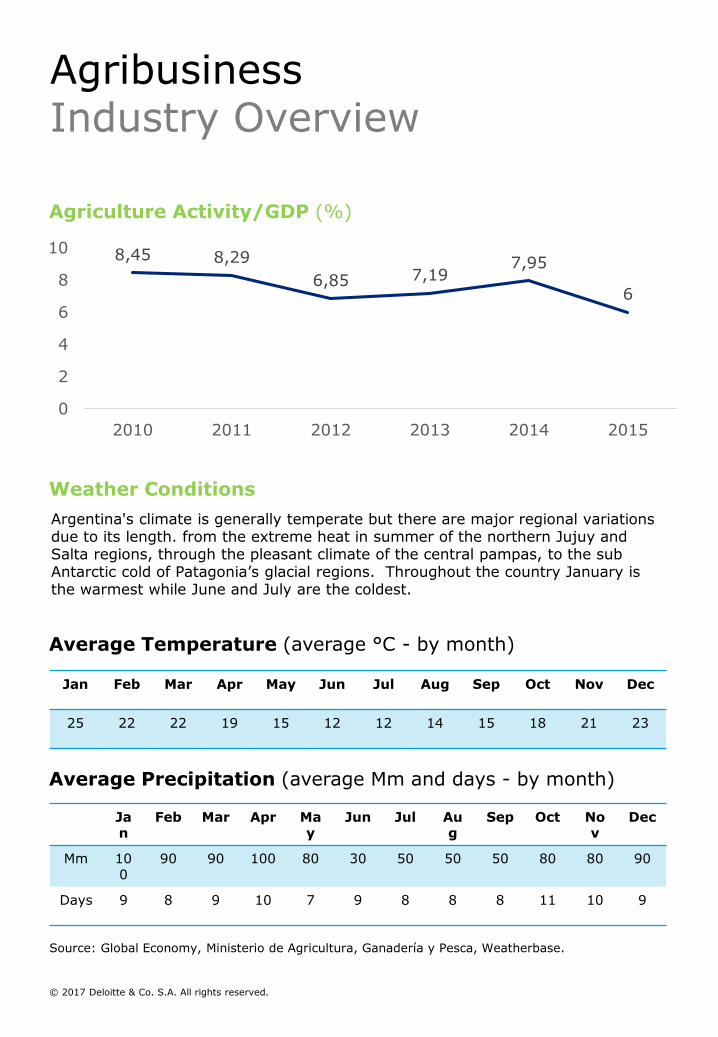

Agriculture Activity/GDP (%)

8,45 8,29

6,85 7,197,95

6

0

2

4

6

8

10

2010 2011 2012 2013 2014 2015

Source: Global Economy, Ministerio de Agricultura, Ganadería y Pesca, Weatherbase.

Weather Conditions

Argentina's climate is generally temperate but there are major regional variations due to its length. from the extreme heat in summer of the northern Jujuy and Salta regions, through the pleasant climate of the central pampas, to the sub Antarctic cold of Patagonia’s glacial regions. Throughout the country January is the warmest while June and July are the coldest.

Average Temperature (average °C - by month)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

25 22 22 19 15 12 12 14 15 18 21 23

Average Precipitation (average Mm and days - by month)

Jan

Feb Mar Apr May

Jun Jul Aug

Sep Oct Nov

Dec

Mm 100

90 90 100 80 30 50 50 50 80 80 90

Days 9 8 9 10 7 9 8 8 8 11 10 9

© 2017 Deloitte & Co. S.A. All rights reserved.

AgribusinessIndustry Overview

Cereals & Oilseeds Production

Production (M of Tns)

Source: USDA.

Yield (000 Tns/Ha)

0

50

100

Argentina Brazil Paraguay Peru Uruguay

0,0

1,0

2,0

3,0

Argentina Brazil Paraguay Peru Uruguay

0

20

40

60

Argentina Brazil Paraguay Peru Uruguay

Exports (M of Tns)

Growth

AR: 1,2x

BR: 4,0x

PY: 2,5x

PE: -

UY: 212x

2017 Yield

AR: 2,9

BR: 3,3

PY: 2,8

PE: 1,5

UY: 2,5

Growth

AR: 2,0x

BR: 2,8x

PY: 2,9x

PE: 1,0x

UY: 117x

© 2017 Deloitte & Co. S.A. All rights reserved.

Cereals & Oilseeds ProductionSoybean

Production (M of Tns)

Source: USDA.

Yield (000 Tns/Ha)

0,0

1,0

2,0

3,0

4,0

Argentina Brazil Paraguay Peru Uruguay

0

5

10

Argentina Brazil Paraguay Peru Uruguay

Exports (M of Tns)Growth

AR: 0,9x

BR: 466x

PY: 6,7x

PE: 4,3

UY: 55x

2017 Yield

AR: 3,3

BR: 3,2

PY: 1,9

PE: 1,5

UY: 3,7

0

5

10

15

20

Argentina Brazil Paraguay Peru Uruguay

Growth

AR: 0,9x

BR: 4,1x

PY: 2,9x

PE: 1,0x

UY: 2,5x

© 2017 Deloitte & Co. S.A. All rights reserved.

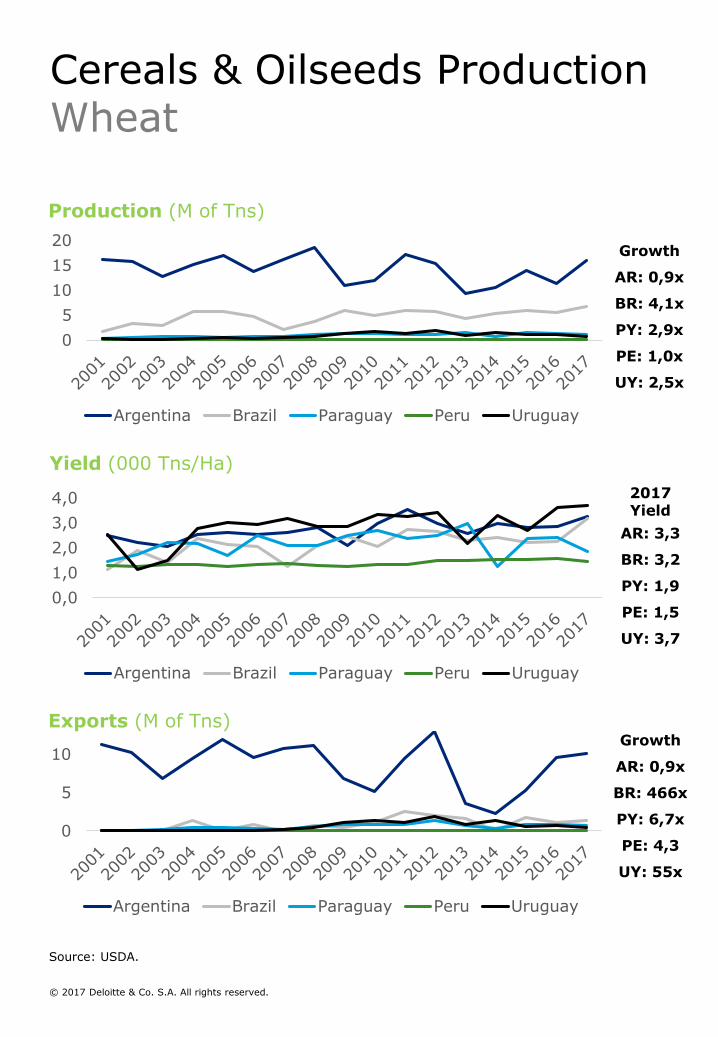

Cereals & Oilseeds ProductionWheat

Production (M of Tns)

Source: USDA.

Yield (000 Tns/Ha)

0

2

4

6

8

10

Argentina Brazil Paraguay Peru Uruguay

0

10

20

30

Argentina Brazil Paraguay Peru Uruguay

Exports (M of Tns) Growth

AR: 2,7x

BR: 5,1x

PY: 4,1x

PE: 2,5x

UY: 17,5x

2017 Yield

AR: 8,4

BR: 5,4

PY: 4,6

PE: 3,2

UY: 5,2

0

20

40

60

80

100

Argentina Brazil Paraguay Peru Uruguay

Growth

AR: 2,5x

BR: 2,3x

PY: 2,7x

PE: 1,2x

UY: 1,7x

© 2017 Deloitte & Co. S.A. All rights reserved.

Cereals & Oilseeds ProductionCorn

Cereals & Oilseeds ProductionMain Players

Source: USDA.

Company OriginFootprint in Argentina

Brands

Industry Position

(Lead-Mid-Small)

CargillUnited-States

Grains/Oilseeds/ Flour

Lead

BungeUnited-States

Wheat/ Soybean/ Corn/

SunflowerLead

Louis Dreyfus Company

France

Grains/Oilseeds/

Dairy/ RiceLead

Archer Daniels Midland

United-States

Beans/ Proteins/ Rice/

SoyMiddle

Nidera (COFCO) ChinaCrop/ Oilseeds/

OilMiddle

Adecoagro ArgentinaCrops/ Rice/

DairyLead

Cresud ArgentinaCrops/

Sugarcane/ Dairy

Middle

Grupo Los Grobo

ArgentinaCorn/ Soy/ Sunflower/

CropMiddle

Molinos Juan Semino S.A

Argentina Starch/ Flour Small

MorixeHermanos S.A

Argentina Wheat/ Cereals Small

Lartirigoyen y Cía

Argentina Crop/ Oilseeds Medium

Asociación de CooperativasArgentinas

ArgentinaCrop/ Oilseeds/

StorageMedium

AgricultoresFederadosArgentinos

ArgentinaCrop/ Oilseeds/

StorageMedium

© 2017 Deloitte & Co. S.A. All rights reserved.

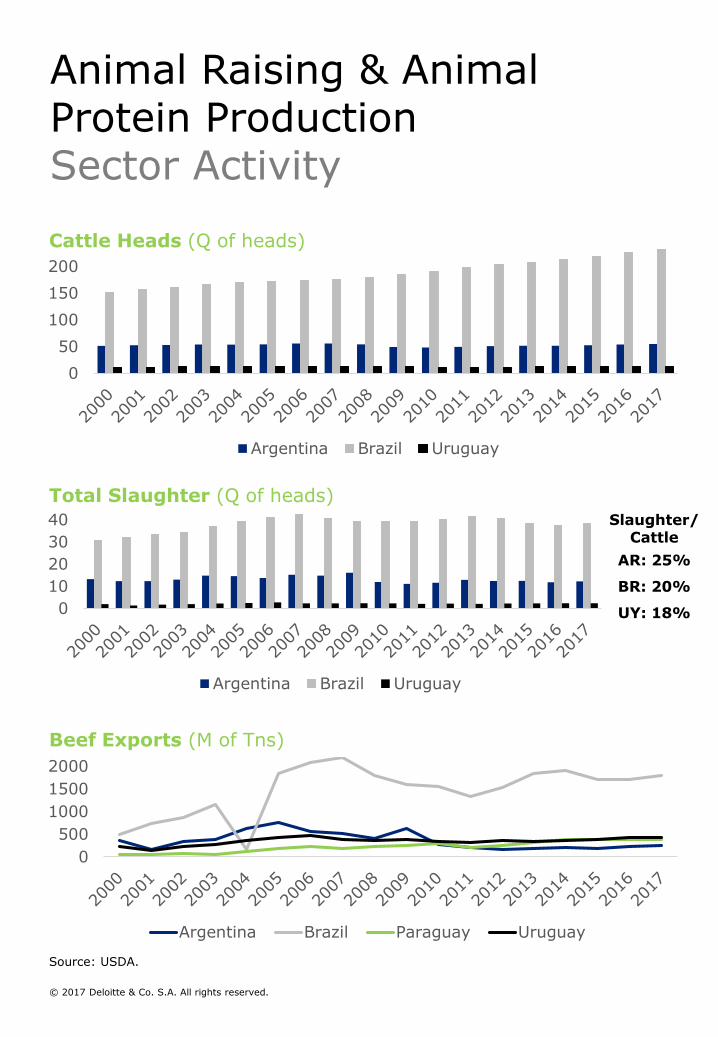

Animal Raising & Animal Protein Production

Source: USDA.

Cattle Heads (Q of heads)

0

50

100

150

200

Argentina Brazil Uruguay

Total Slaughter (Q of heads)

0

10

20

30

40

Argentina Brazil Uruguay

Slaughter/ Cattle

AR: 25%

BR: 20%

UY: 18%

0

500

1000

1500

2000

Argentina Brazil Paraguay Uruguay

Beef Exports (M of Tns)

© 2017 Deloitte & Co. S.A. All rights reserved.

Animal Raising & Animal Protein Production Sector Activity

Source: USDA, BMI, EMIS.

Beef Production & Consumption (000 of Tns)

0500

10001500200025003000

Beef Production Beef Consumption

Pork Production & Consumption (000 of Tns)

0

100

200

300

400

500

Pork Production Pork Consumption

Poultry Production & Consumption (000 of Tns)

0500

10001500200025003000

Poultry Production Poultry Consumption

DriversProd: slow growth because producers will try to grow their herds in the ST to increase output and take advantage of export market.Cons: declining due to health trend and increases in price.

DriversProd: growth to the expanding of the domestic market –less imported product.Cons: it is expected to outperform poultry levels – which gained market due to lower prices.

DriversProd: will growth as it is the cheaper meat, it can benefit from the beef consumption slow down.Cons: it will benefit from high beef prices.

© 2017 Deloitte & Co. S.A. All rights reserved.

Animal Raising & Animal Protein Production Sector Activity

Animal Raising & Animal Protein Production Main Players

Source: Company’s Website.

Company OriginFootprint in Argentina

Brands

Industry Position

(Lead-Mid-Small)

Inversora Juramento S.A INVJ

ArgentinaLivestockraising

Lead

Carlos Casado S.AArgentina

Livestock raising

Middle

Cabaña Pilagá ArgentinaLivestock raising/ Breeding

Middle

Cresta Roja Argentina PoultryProcessing

Lead

RioPlatense ArgentinaMeat (Beef) Processing

Lead

Frigorífico Gorina ArgentinaMeat (Beef) Processing

Lead

BRF BrazilMeat (Beef) Processing

Lead

Ciaber (Compñía Bernal) ArgentinaMeat (Beef) Processing

Middle

JBS Brazil

Meat (Beef) Processing –Hamburger/

Sausage Producer

Lead

Frigorífico Rydhans Argentina

Meat (Pork) Processing –

Sausage Producer

Lead

Paladini Argentina

Meat (Pork) Processing –

Sausage Producer

Lead

Arre Beef ArgentinaMeat (Beef) Processing

Lead

© 2017 Deloitte & Co. S.A. All rights reserved.

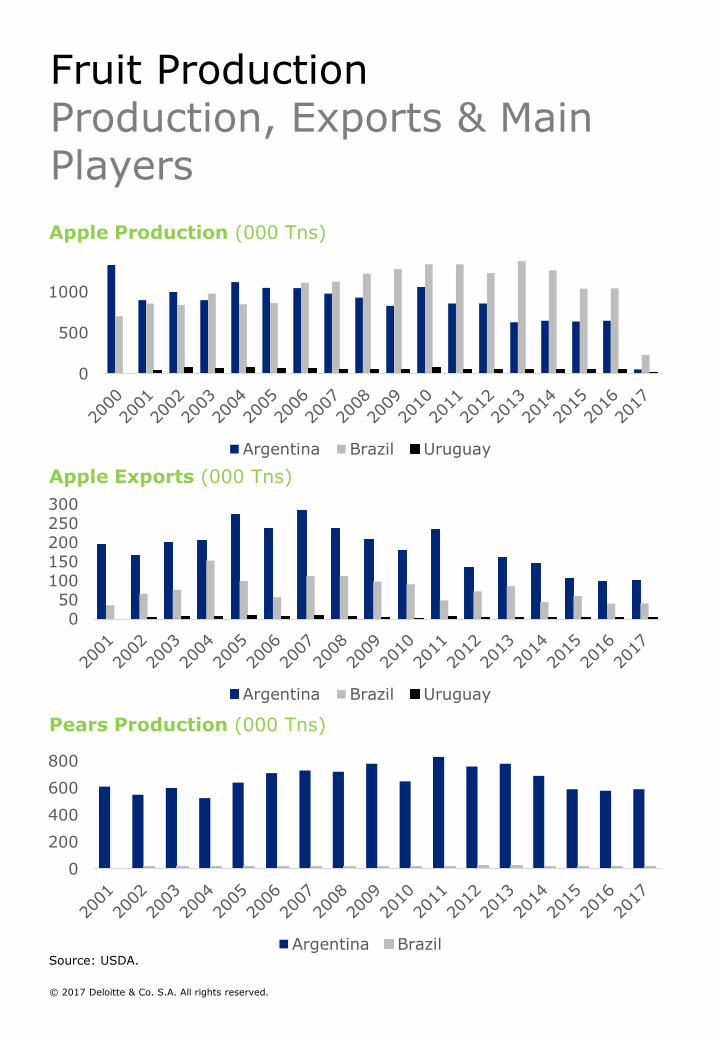

Fruits Production

Source: USDA.

Apple Production (000 Tns)

0

500

1000

Argentina Brazil Uruguay

Apple Exports (000 Tns)

050

100150200250300

Argentina Brazil Uruguay

Pears Production (000 Tns)

0

200

400

600

800

Argentina Brazil

© 2017 Deloitte & Co. S.A. All rights reserved.

Fruit ProductionProduction, Exports & Main Players

Source: USDA.

Pears Exports (000 Tns)

0

100

200

300

400

500

Argentina

Lemons Production (000 Tns)

Lemons Exports (000 Tns)

0

300

600

900

1200

1500

Argentina

0

100

200

300

400

Argentina

© 2017 Deloitte & Co. S.A. All rights reserved.

Fruit ProductionProduction, Exports & Main Players

Fruit ProductionProduction, Exports & Main Players

Source: Company’s Website.

Company OriginFootprint in Argentina

BrandsIndustry Position(Lead-Mid-Small)

San Miguel Argentina Citrus Lead

Costa Limay Argentina Apple/ Pear Middle

Cosur S.A.Grupo Battaglio

Argentina Apple/ PearMiddle

Cofrutas SA Argentina Fruits/ Flowers Middle

ArgesaArgentina

Argentina Citrus/ Fruits Middle

Dole Nat S.A. United States Fruits Lead

Canale Group ArgentinaFruits/

vegetablesSmall

SA Veracruz Argentina Fruits/ Citrus Small

Tres Ases SA Argentina Peache/ Apple Middle

Via Frutta SA Argentina Apple Middle

Expofrut ArgentinaApple/ Citrics/Pear/ Grapes/ Onion/ Garlic

Lead

Ecofrut Spain Apple/ Pear Middle

San FormerioS.R.L

ArgentinaApple/ Pears/

PeachesMiddle

Patagonian Fruits Trade

S.A.Argentina Apple Middle

Moño Azul Argentina Apple Middle

Los Juanes S.A. Argentina Apple/ Pear Middle

Kleppe S.A. Argentina Apple/ Pear Middle

© 2017 Deloitte & Co. S.A. All rights reserved.

Animal Feed

Company Origin Footprint in Argentina

Main Brands Industry Position(Lead-Mid-Small)

Provimi USARuminants, Swine

& PoultryMiddle

Alltech ArgentinaRuminants, Swine,

Pet & PoultryMiddle

Biofarma ArgentinaRuminants, Swine

& PoultryLeader

Brouwer ArgentinaRuminants &

SwineSmall

Ceres Argentina Ruminants Middle

Cladán ArgentinaRuminants, Swine,

Pet & PoultrySmall

DSMHolandesa

Ruminants, Swine, Pet & Poultry

Middle

Ensol ArgentinaSwine, Pet &

PoultryMiddle

Nutrefeed, Argentina Ruminants Small

Nutriser ArgentinaRuminants, Swine

& PoultrySmall

Vetifarma ArgentinaRuminants, Swine

& PoultryMiddle

Metrive Argentina Pet & Ruminant Middle

Royal Canin(Grupo Mars)

USA Pet food Leader

Purina (Nestlé) Switzerland Pet food Leader

Gepsa Argentina Pet food Middle

Agroindustrias Baires SA

Argentina Pet food Middle

Garay SRL Argentina Ruminants Middle

AgrocerealesArgentina SRL

Argentina Swine/ Ruminants Middle

© 2017 Deloitte & Co. S.A. All rights reserved.

Animal FeedMain Players

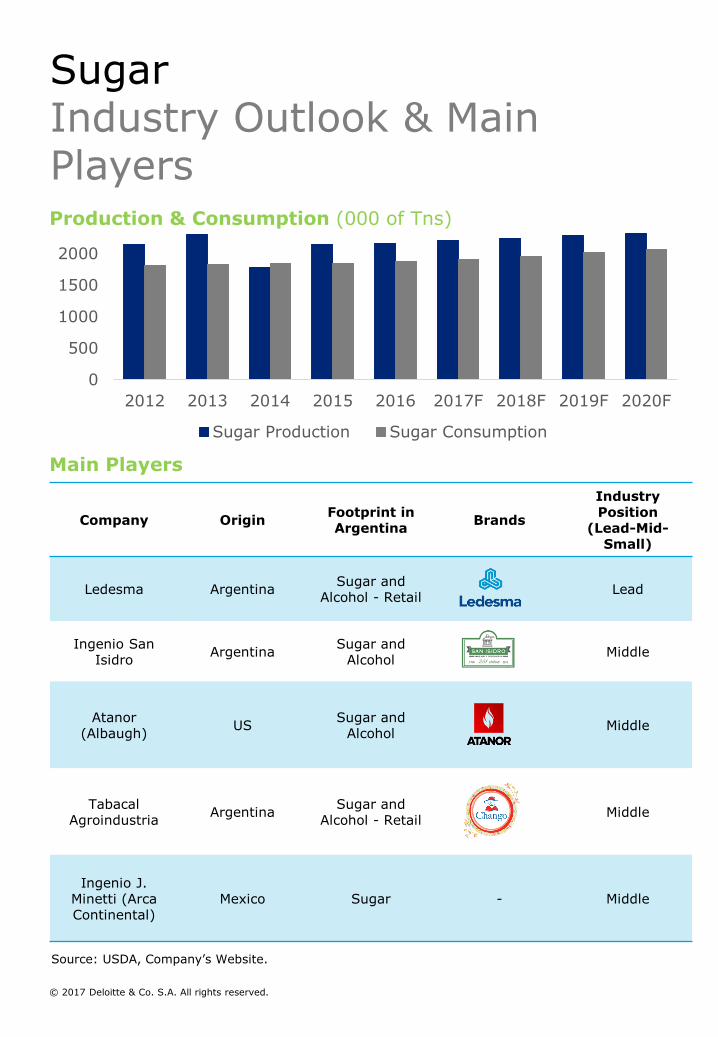

Sugar

Source: USDA, Company’s Website.

Production & Consumption (000 of Tns)

0

500

1000

1500

2000

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F

Sugar Production Sugar Consumption

Main Players

Company OriginFootprint in Argentina

Brands

Industry Position

(Lead-Mid-Small)

Ledesma ArgentinaSugar and

Alcohol - RetailLead

Ingenio San Isidro

ArgentinaSugar and

AlcoholMiddle

Atanor(Albaugh)

USSugar and

AlcoholMiddle

TabacalAgroindustria

ArgentinaSugar and

Alcohol - RetailMiddle

Ingenio J. Minetti (ArcaContinental)

Mexico Sugar - Middle

© 2017 Deloitte & Co. S.A. All rights reserved.

SugarIndustry Outlook & Main Players

Source: Deloitte’s elaboration based on Mergermarket & Thompson Reuters information.

Year Target AcquirerAcquirer Origin

Deal Ticket(US$ M)

2017AceiteraMartinez

Bunge Ltd US N/D

2016Grupo Los

GroboVSAP

Agriservices LPArgentina 75

2016 Rasic Hnos Proteinsa Argentina 121

2016Marfrig (One

Asset)

Black Bamboo (ForesunGroup)

China 75

2016 LDC Semillas Galba SA Argentina N/D

6

9

5

24

1

0%

10%

20%

0

5

10

2012 2013 2014 2015 2016 2017 Q1Deal Volume Participation over Period Activity

Deal Volume & Value

Acquirer’s Origin - 2016 (Volume)

Latin America75%

Asia & Oceania25%

Recent Deals

© 2017 Deloitte & Co. S.A. All rights reserved.

AgribusinessRecent M&A Activity

Industry SnapshotTelecommunications, Media & Technology

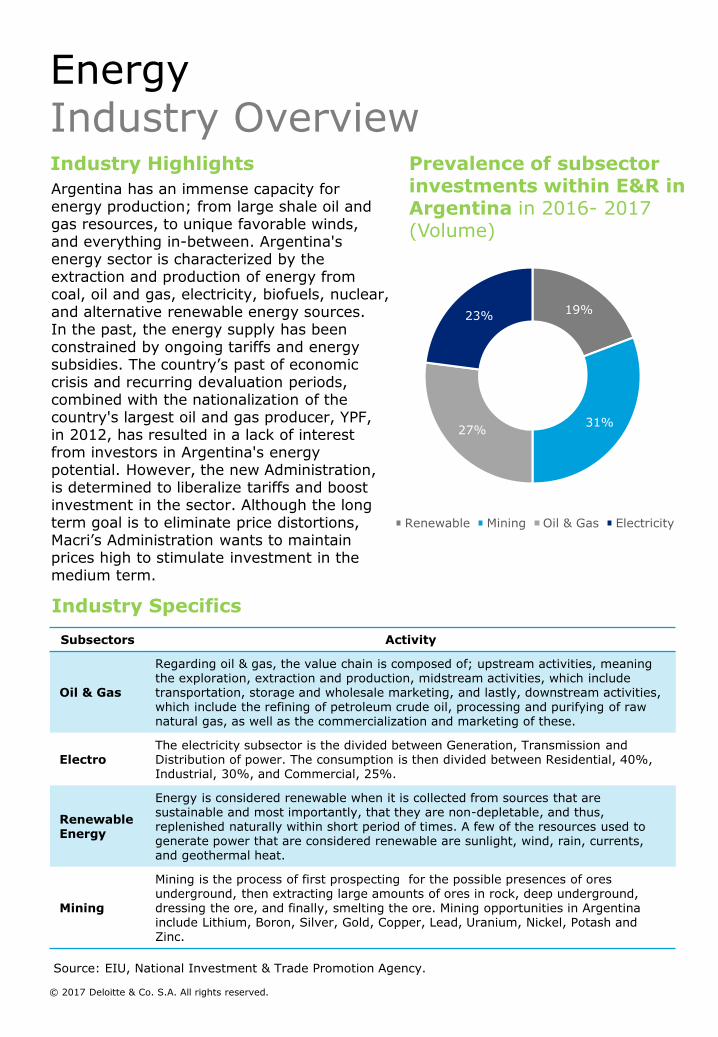

Industries Highlights

Industries Subsectors

IndustryMain Players

Foreign Domestic

Telecomunications

Media

Technology

Telecommunications:Although Argentina’s telecommunications infrastructure is generally developed, opportunities to increase coverage and speed remain:• Argentina has nationwide broadband access but internet speeds are 15% lower

than those of regional peers.• Argentina’s mobile phone penetration is high (141%) but coverage is not

uniform across the country and is often poor due to insufficient cell tower coverage.

The government has made cell and internet access expansion development a priority which is opening a number of opportunities for private investmentMedia:Argentina in one of the leaders in the South America media market, under favorable legislation, the industry has consolidated and a large number of companies have appeared.Technology:• The software and IT services sector in Argentina is made of 3,800 firms, ranging

from globally consolidated multinationals to a growing network of highly innovative small and medium-sized local enterprises. Argentine companies’ global projection in this sector is expanding as one quarter of its production is exported to international markets.

• As Latin America is becoming one of the most attractive E-commerce acceptance market around the world, the E-commerce sector in Argentina is growing rapidly and the country is expected to become a regional leader in this area.

Source: National Investment & Trade Promotion Agency.

© 2017 Deloitte & Co. S.A. All rights reserved.

Telecommunications, Media & TechnologyIndustries Overview

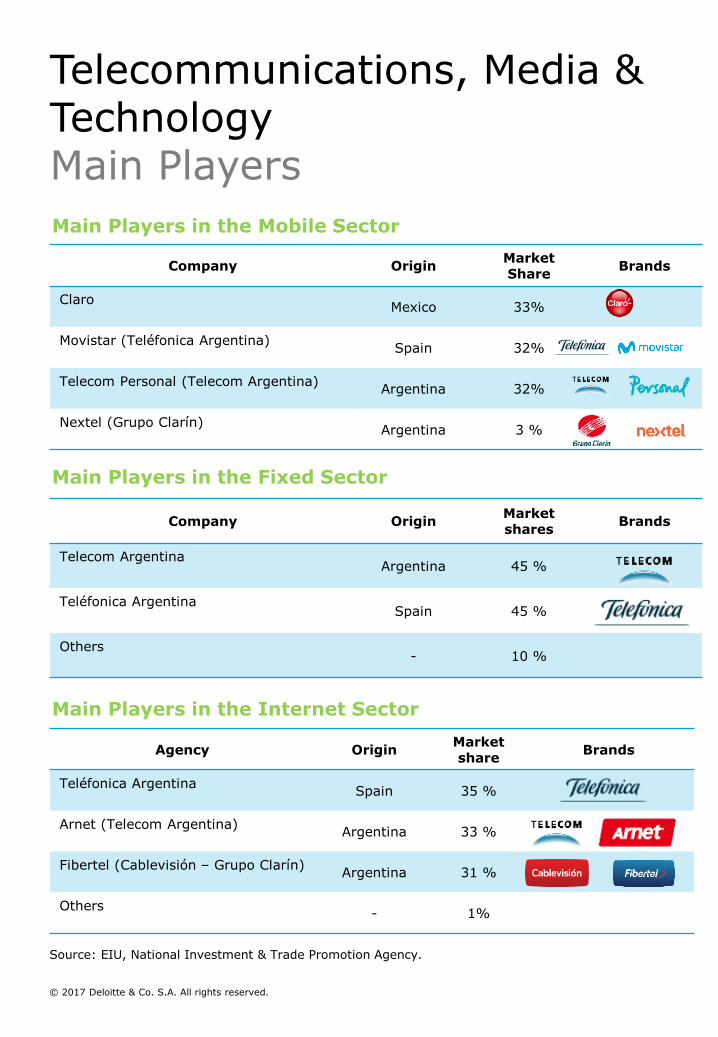

Telecommunications

• The expansion of Argentina’s cell coverage presents a USD 2 billion investment opportunity.

• There are three top players in the mobile telephony segment—Claro (owned by Mexico's América Movil), Telecom Personal (a subsidiary of Telecom Argentina), and Movistar (owned by Spain's Telefónica). Each operator holds about one-third of market share.

• Telecoms investment are expected to grow at an average rate of 12.9% a year during the five-year forecast period, to reach AR$ 64.7 billion (or US$ 2.8bn) by 2021.

• Mobile revenue growth will also be supported by strong growth of the smartphone market in Argentina. In 2016, only 37% of the population owns a smartphone – considerably low against the region.

• In Argentina there are approximately 15,000 active cell sites (mobile towers), this number is meant to double in order to ensure an acceptable quality of service. The Government will facilitate this development.

• There is ample room for Neutral Infrastructure Operators (tower builders/operators) to enter this market as neutral operators own 62% of cell sites worldwide vs. 0% in Argentina.

• Growth in mobile telephony will be led by data transmission and mobile broadband. Substantial investments have been undertaken by telecoms companies to allow them to develop their value-added services, including mobile data, and, ultimately, increase average revenue per user.

65,000

jobs

directly

supported

by mobile

ecosystem

Mobile

industry

contributes

to

3.7%of GDP

12.9%Average

expected

growth rate

per year

during the

next 5 years

Source: EIU, National Investment & Trade Promotion Agency, GSMA Intelligence.

Mobile Subscriptions (per 100 people)

Deployment Mobile Coverage

0

20

40

60

80

100

120

140

160

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F

© 2017 Deloitte & Co. S.A. All rights reserved.

TelecommunicationsMobile Telecommunications

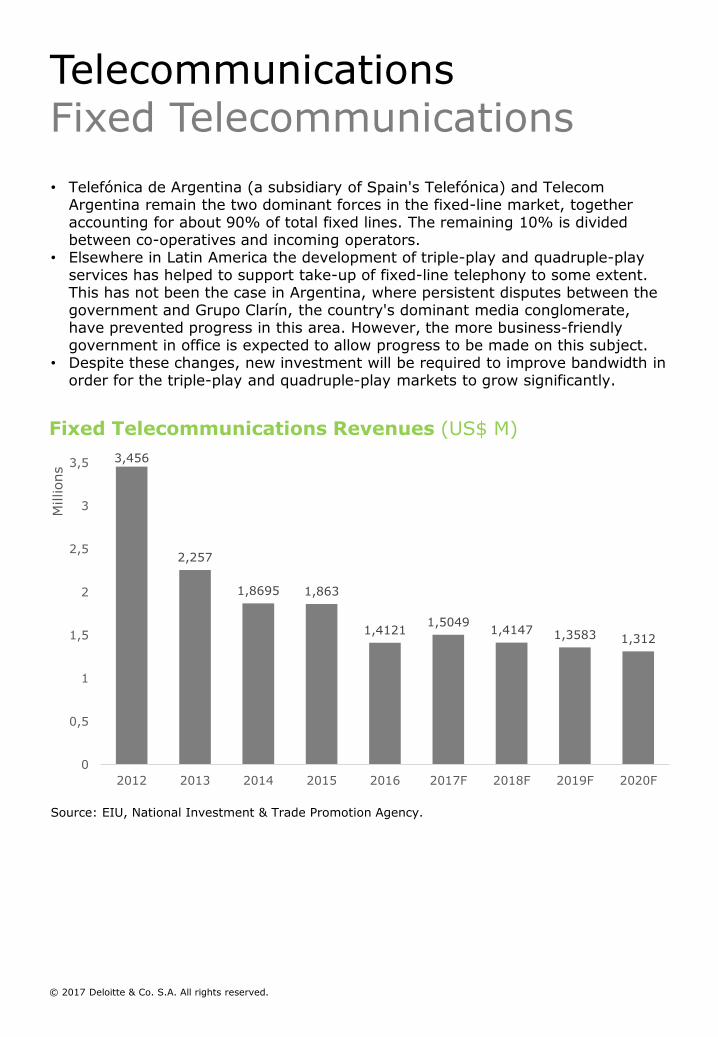

• Telefónica de Argentina (a subsidiary of Spain's Telefónica) and Telecom Argentina remain the two dominant forces in the fixed-line market, together accounting for about 90% of total fixed lines. The remaining 10% is divided between co-operatives and incoming operators.

• Elsewhere in Latin America the development of triple-play and quadruple-play services has helped to support take-up of fixed-line telephony to some extent. This has not been the case in Argentina, where persistent disputes between the government and Grupo Clarín, the country's dominant media conglomerate, have prevented progress in this area. However, the more business-friendly government in office is expected to allow progress to be made on this subject.

• Despite these changes, new investment will be required to improve bandwidth in order for the triple-play and quadruple-play markets to grow significantly.

Source: EIU, National Investment & Trade Promotion Agency.

3,456

2,257

1,8695 1,863

1,41211,5049

1,4147 1,3583 1,312

0

0,5

1

1,5

2

2,5

3

3,5

2012 2013 2014 2015 2016 2017F 2018F 2019F 2020F

Millions

Fixed Telecommunications Revenues (US$ M)

© 2017 Deloitte & Co. S.A. All rights reserved.

TelecommunicationsFixed Telecommunications

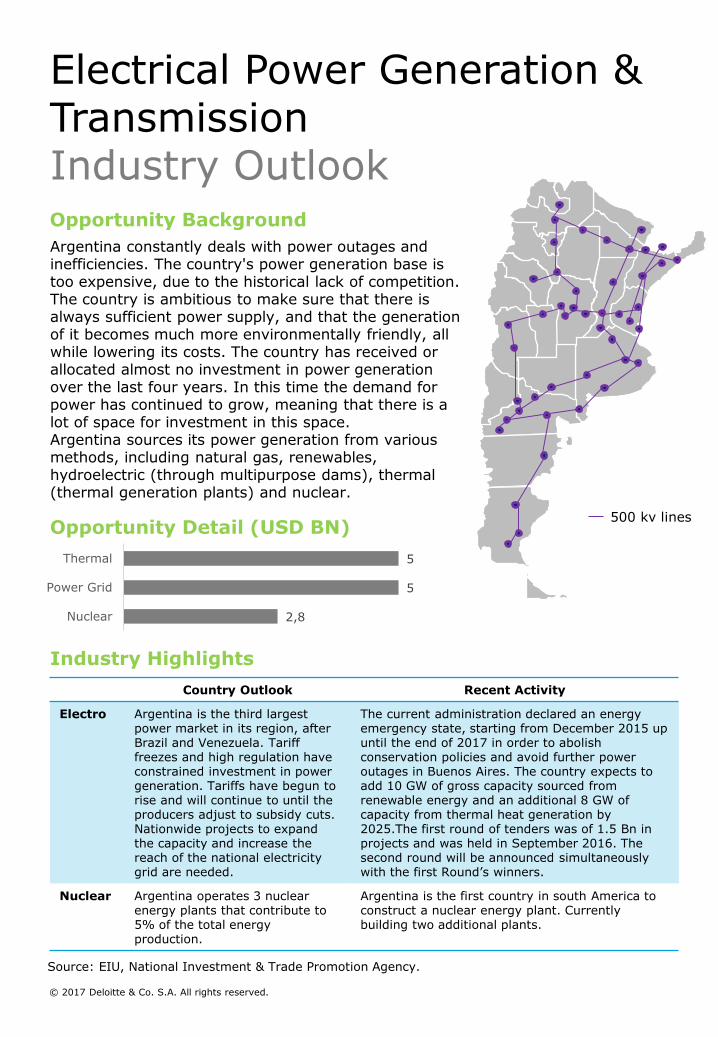

• The expansion of Argentina’s fiber optic network over the next 2 years presents a US$ 307 M investment opportunity: