81

Investment Community Presentation

| Date post: | 23-Mar-2018 |

| Category: |

Documents |

| Upload: | nguyendiep |

| View: | 216 times |

| Download: | 2 times |

Investment Community Presentation

04

11

23

41

49

55

65

Enbridge and Spectra Merger

Strategic Overview

Liquids Pipelines

Gas Pipelines & Processing

Gas Distribution

Power, International & Energy Services

Corporate Finance

Appendix

Project Status Update

Maps

73

Contents

75

76

Legal NoticeThis presentation includes certain forward looking information (FLI) to provide Enbridge shareholders and potential investors with information about Enbridge and management’s assessment of its future plans and operations, which may not be appropriate for other purposes. FLI is typically identified by words such as “anticipate”, “expect”, “project”, “estimate”, “forecast”, “plan”, “intend”, “target”, “believe” and similar words suggesting future outcomes or statements regarding an outlook. All statements other than statements of historical fact may be forward-looking statements. In particular, this Presentation may contain forward-looking statements pertaining to the following: expectations regarding, and anticipated impact of, the Transaction, dividend payout policy and dividend payout expectations; adjusted earnings per share guidance, available cash flow from operations (ACFFO) guidance; satisfaction of closing conditions and the obtaining of consents and

approvals required to complete the Transaction; effect, results and perceived benefits of the Transaction, including with respect to the consideration to be received by the Company; expected timing and completion of Transaction; future equity and debt offerings and financing requirements and plans; expected future sources and costs of financing; and future growth opportunities and the allocation and impact thereof.

Although we believe that our FLI is reasonable based on the information available today and processes used to prepare it, such statements are not guarantees of future performance and you are cautioned against placing undue reliance on FLI. By its nature, FLI involves a variety of assumptions, risks, uncertainties and other factors which may cause actual results, levels of activity and achievements to differ materially from those expressed or implied in our FLI. Material assumptions include assumptions about: expected timing and terms of the Transaction; anticipated completion of the Transaction; adoption of the dividend policy; satisfaction of all closing conditions and receipt of regulatory, shareholder and third party consents and approvals with respect to the Transaction; impact of the Transaction and dividend policy on the Company’s future cash flows and capital project funding; impact of the Transaction and dividend policy on the Company’s credit ratings; expected earnings/(loss) or adjusted earnings/(loss); expected earnings/(loss) or adjusted earnings/(loss) per share; expected future cash flows and expected future ACFFO; estimated future dividends; debt and equity market conditions; expected supply and demand for crude oil, natural gas and natural gas liquids; prices of crude oil, natural gas and natural gas liquids; expected exchange rates; inflation; interest rates; availability and price of labour and pipeline construction materials; operational reliability; anticipated in-service dates and weather. Due to the interdependencies and correlation of these macroeconomic factors, the impact of any one assumption on FLI cannot be determined with certainty, particularly with respect to expected earnings and associated per unit or per share amounts, or estimated future distributions or dividends.

Our FLI is subject to risks and uncertainties pertaining to the Transaction, dividend policy, adjusted earnings guidance, ACFFO guidance, operating performance, regulatory parameters, weather, economic conditions, exchange rates, interest rates and commodity prices, including but not limited to those discussed more extensively in our filings with Canadian and US securities regulators. The impact of any one risk, uncertainty or factor on any particular FLI is not determinable with certainty as these are interdependent and our future course of action depends on management’s assessment of all information available at the relevant time. Except to the extent required by law, we assume no obligation to publicly update or revise any FLI, whether as a result of new information, future events or otherwise. All FLI in this presentation is expressly qualified in its entirety by these cautionary statements.

You should be cautioned that there is no assurance that the Transaction will be completed in the manner contemplated, or at all, or that the current market conditions and Enbridge’s assumptions and forecasts based on such market conditions will not materially change.

This presentation will make reference to non-GAAP measures including adjusted earnings and ACFFO, together with respective per share amounts. These measures are not measures that have a standardized meaning prescribed by U.S. GAAP and may not be comparable with similar measures presented by other issuers. Additional information on the Company’s use of non-GAAP measures can be found in Management’s Discussion and Analysis available on the Company’s website and www.SEDAR.com and the news release.

Enbridge Inc. and Spectra Energy Corp. Combine to Create North America’s Premier Energy Infrastructure Company

Investment Community Presentation January 2017

1

This presentation includes certain forward looking statements and information (FLI) to provide Enbridge and Spectra Energy shareholders and potential investors with information about Enbridge, Spectra Energy and their respective subsidiaries and affiliates, including each company’s management’s respective assessment of Enbridge, Spectra Energy and their respective subsidiaries’ future plans and operations, which FLI may not be appropriate for other purposes. FLI is typically identified by words such as “anticipate”, “expect”, “project”, “estimate”, “forecast”, “plan”, “intend”, “target”, “believe”, “likely” and similar words suggesting future outcomes or statements regarding an outlook. All statements other than statements of historical fact may be FLI. In particular, this news release contains FLI pertaining to, but not limited to, information with respect to the following: the Transaction; the combined company’s scale, financial flexibility and growth program; future business prospects and performance; annual cost, revenue and financing benefits; the expectation that the Transaction will be neutral to expected ACFFO per share growth guidance through 2019 and additive to the growth rate beyond that timeframe; future shareholder returns; annual dividend growth and anticipated dividend increases; payout of distributable cash flow; financial strength and ability to fund capital program and compete for growth projects; run-rate and tax synergies; leadership and governance structure; and head office and business center locations.

Although we believe that the FLI is reasonable based on the information available today and processes used to prepare it, such statements are not guarantees of future performance and you are cautioned against placing undue reliance on FLI. By its nature, FLI involves a variety of assumptions, which are based upon factors that may be difficult to predict and that may involve known and unknown risks and uncertainties and other factors which may cause actual results, levels of activity and achievements to differ materially from those expressed or implied by these FLI, including, but not limited to, the following: the timing and completion of the Transaction, including receipt of regulatory and shareholder approvals and the satisfaction of other conditions precedent; interloper risk; the realization of anticipated benefits and synergies of the Transaction and the timing thereof; the success of integration plans; the focus of management time and attention on the Transaction and other disruptionsarising from the Transaction; expected future ACFFO; estimated future dividends; financial strength and flexibility; debt and equity market conditions, including the ability to access capital markets on favourable terms or at all; cost of debt and equity capital; potential changes in the Enbridge share price which may negatively impact the value of consideration offered to Spectra Energy shareholders; expected supply and demand for crude oil, natural gas, natural gas liquids and renewable energy; prices of crude oil, natural gas, natural gas liquids and renewable energy; economic and competitive conditions; expected exchange rates; inflation; interest rates; tax rates and changes; completion of growth projects; anticipated in-service dates; capitalproject funding; success of hedging activities; the ability of management of Enbridge, its subsidiaries and affiliates to execute key priorities, including those in connection with the Transaction; availability and price of labour and construction materials; operational performance and reliability; customer, shareholder, regulatory and other stakeholder approvals and support; regulatory and legislative decisions and actions; public opinion; and weather. We caution that the foregoing list of factors is notexhaustive. Additional information about these and other assumptions, risks and uncertainties can be found in applicable filings with Canadian and U.S. securities regulators, including any proxy statement, prospectus or registration statement to be filed in connection with the Transaction. Due to the interdependencies and correlation of these factors, as well as other factors, the impact of any one assumption, risk or uncertainty on FLI cannot be determined with certainty.

Except to the extent required by law, we assume no obligation to publicly update or revise any FLI, whether as a result of new information, future events or otherwise. All FLI in this news release is expressly qualified in its entirety by these cautionary statements.

This presentation makes reference to non-GAAP measures, including ACFFO and ACFFO per share. ACFFO is defined as cash flow provided by operating activities before changes in operating assets and liabilities (including changes in environmental liabilities) less distributions to non-controlling interests and redeemable non-controlling interests, preference share dividends and maintenance capital expenditures, and further adjusted for unusual, non-recurring or non-operating factors. Management of Enbridge believes the presentation of these measures gives useful information to investors and shareholders as they provide increased transparency and insight into the performance of Enbridge. Management of Enbridge uses ACFFO to assess performance and to set its dividend payout target. These measures are not measures that have a standardized meaning prescribed by generally accepted accounting principles in the United States of America (U.S. GAAP) and may not be comparable with similar measures presented by other issuers. Additional information on Enbridge’s use of non-GAAP measures can be found in Enbridge’s Management’s Discussion and Analysis (MD&A) available on Enbridge’s website and www.sedar.com.

Enbridge will file with the U.S. Securities and Exchange Commission (SEC) a registration statement on Form F-4, which will include a proxy statement of Spectra Energy that also constitutes a prospectus of Enbridge, and any other documents in connection with the Transaction. The definitive proxy statement/prospectus will be sent to the shareholders of Spectra Energy. INVESTORS AND SHAREHOLDERS OF SPECTRA ENERGY ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS, AND ANY OTHER DOCUMENTS FILED OR TO BE FILED WITH THE SEC IN CONNECTION WITH THE TRANSACTION WHEN THEY BECOME AVAILABLE, AS THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT Enbridge, Spectra Energy, THE TRANSACTION AND RELATED MATTERS. The registration statement and proxy statement/prospectus and other documents filed by Enbridge and Spectra Energy with the SEC, when filed, will be available free of charge at the SEC's website at www.sec.gov. In addition, investors and shareholders will be able to obtain free copies of the proxy statement/prospectus and other documents which will be filed with the SEC by Enbridge on Enbridge’s website at www.Enbridge.com or upon written request to Enbridge’s Investor Relations department, 200, 425 First St. SW, Calgary, AB T2P 3L8 or by calling 800.481.2804 within North America and 403.231.5957 from outside North America, and will be able to obtain free copies of the proxy statement/prospectus and other documents filed with the SEC by Spectra Energy upon written request to Spectra Energy, Investor Relations, 5400 Westheimer Ct. Houston, TX 77056 or by calling 713.627.4610. You may also read and copy any reports, statements and other information filed by Spectra Energy and Enbridge with the SEC at the SEC public reference room at 100 F Street N.E., Room 1580, Washington, D.C. 20549. Please call the SEC at 800.732.0330 or visit the SEC's website for further information on its public reference room. This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to appropriate registration or qualification under the securities laws of such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the U.S. Securities Act of 1933, as amended.

This communication is not a solicitation of proxies in connection with the Transaction. However, Enbridge, Spectra Energy, certain of their respective directors and executive officers and certain other members of management and employees, under SECrules, may be deemed to be participants in the solicitation of proxies in connection with the Transaction. Information about Enbridge’s directors and executive officers may be found in its Management Information Circular dated March 8, 2016 available on its website at www.Enbridge.com and at www.sedar.com. Information about Spectra Energy's directors, executive officers and other members of management and employees may be found in its 2015 Annual Report on Form 10-K filed with the SEC on February 25, 2016, and definitive proxy statement relating to its 2016 Annual Meeting of Shareholders filed with the SEC on March 16, 2016. These documents can be obtained free of charge from the sources indicated above. Additional information regarding the interests of such potential participants in the solicitation of proxies in connection with the Transaction will be included in the proxy statement/prospectus and other relevant materials filed with the SEC when they become available.

Legal Disclaimer

Investment Community Presentation January 2017

2

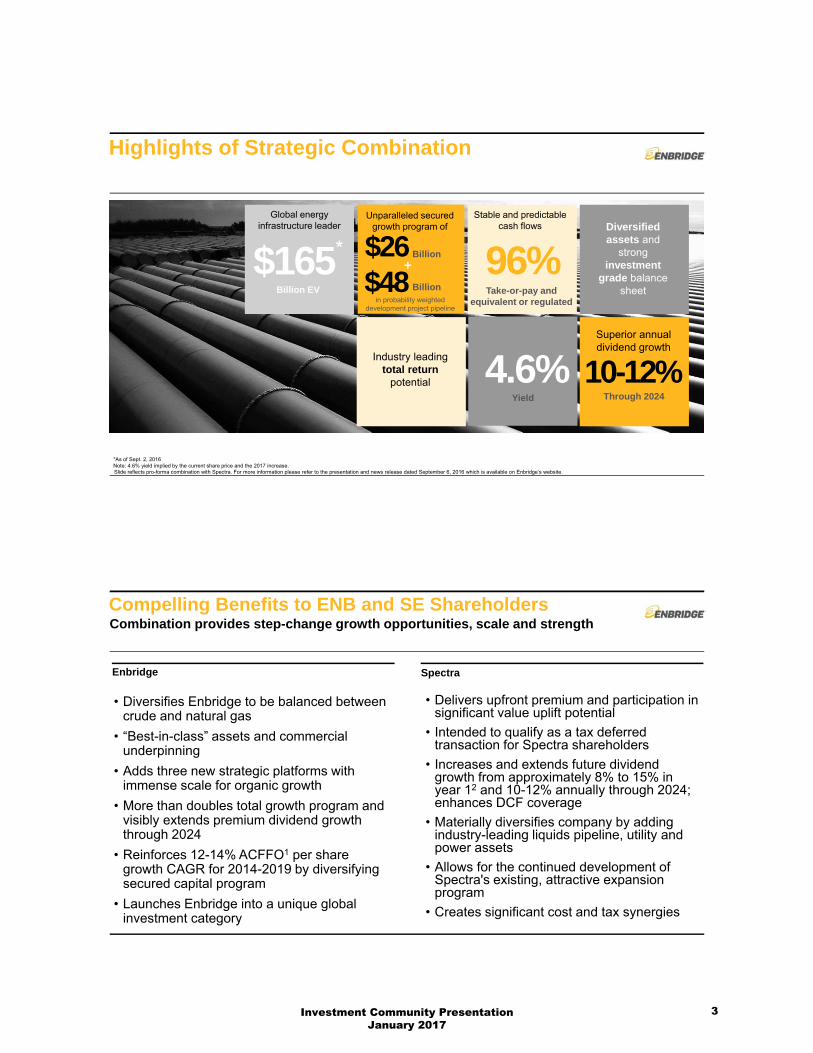

Highlights of Strategic Combination

$165Billion EV

10-12% Through 2024

Global energy infrastructure leader

Superior annual dividend growth

Unparalleled secured growth program of

$26Billion

Industry leading total return

potential

96%Take-or-pay and

equivalent or regulated

Stable and predictable cash flows

Yield

4.6%

Diversified assets and

strong investment

grade balance sheet$48 Billion

in probability weighted development project pipeline

+

*As of Sept. 2, 2016Note: 4.6% yield implied by the current share price and the 2017 increase.Slide reflects pro-forma combination with Spectra. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

*

Compelling Benefits to ENB and SE ShareholdersCombination provides step-change growth opportunities, scale and strength

Enbridge Spectra

• Diversifies Enbridge to be balanced between crude and natural gas

• “Best-in-class” assets and commercial underpinning

• Adds three new strategic platforms with immense scale for organic growth

• More than doubles total growth program and visibly extends premium dividend growth through 2024

• Reinforces 12-14% ACFFO1 per share growth CAGR for 2014-2019 by diversifying secured capital program

• Launches Enbridge into a unique global investment category

• Delivers upfront premium and participation in significant value uplift potential

• Intended to qualify as a tax deferred transaction for Spectra shareholders

• Increases and extends future dividend growth from approximately 8% to 15% in year 12 and 10-12% annually through 2024; enhances DCF coverage

• Materially diversifies company by adding industry-leading liquids pipeline, utility and power assets

• Allows for the continued development of Spectra's existing, attractive expansion program

• Creates significant cost and tax synergies

Investment Community Presentation January 2017

3

• $165B enterprise value

• Highest quality liquids and natural gas franchises

• Low-risk business model

• Strong balance sheet and access to capital

• $26B combined secured growth program

• 12-14% CAGR ACFFO/share growth (2014-2019)

• $48B development project pipeline drives 10-12% annual dividend growth through 2024

Premier North American Energy Infrastructure AssetsHighly compelling combination

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Processing plants

Terminals / storage

Liquids long-haul

Gas long-haul

G&P pipelines

Wind assets

Geothermal power

Gas distribution

Solar assets

Enbridge

Processing plants

Propane terminals

Gas long-haul

NGL storage

Crude storage

Gas storage facility

Gas Distribution

Liquids long-haul

Spectra

G&P pipelines

Power transmission

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

North American Energy InfrastructureEnterprise Value

Global Energy CompaniesMarket Capitalization

Canadian Listed CompaniesEnterprise Value

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

En

brid

ge P

F

DU

K

KM

I

NE

E

En

brid

ge

ET

E

EP

D

TR

P

ET

P

WM

B

WP

Z

Sp

ectr

a

$-

$20

$40

$60

$80

$100

$120

$140

RY

TD

BN

S

En

brid

geP

F CN

R

SU

BM

O

BC

E

En

brid

ge

CN

Q

BA

M

CM

TR

I

Largest North American energy infrastructure company

One of the largest energy companies globally

One of the largest publicly listed Canadian companies

Source: Market Data from FactSet as at 09/02/2016. Based on spot FX rate as of 09/02/2016.

Enhanced financial flexibility and access to capitalScale Enhances Competitive Position

$-

XO

M

CV

X

Pe

troC

hina

RD

SB

BR

Pet

ro.

Tot

al BP

Sin

opec

En

brid

ge P

F

SL

B

DU

K

KM

I

En

brid

ge

EP

D

$600

$300

$150

$-

Investment Community Presentation January 2017

4

80

116

Residential/ Commercial

Industrial

Coal/ Nuclear Retirements

PowerDemand

Exports byLNG andPipeline

0

1,000

2,000

3,000

4,000

5,000

6,000

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Fundamentals Support Sustainable Long Term Cash Flow and Efforts to Extend and Diversify Growth

Natural Gas: Steady long term growth from demand pull assets into US Northeast, Southeast and Gulf Coast

Liquids: Highly stable and growing base cash flows with further upside optionality in an oil recovery scenario

WCSB Takeaway Capacity vs Supply (kbpd)

WCSB short >500 kbpd pipeline capacity by 2021

Western Canadian refineries

Other existing pipelines

Enbridge

Sources of demand (Bcf/d)

Significant expansion potential

2016 2025

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Multiple Strategic Growth Platforms

Positioned for sustained demand-pull organic growth for the foreseeable future

Positioned on a combined basis to compete with Canada’s leading midstream players on gas and NGL midstream infrastructure

Positioned to provide integrated gas/liquids midstream services across the hydrocarbon chain

Highly predictable growing cash flows with significant further

upside optionality

Utilities deliver significant customer and shareholder

benefits; Compelling platform for

extension to electric utilities

Spectra U.S. presence and utility customer base enhances growth

opportunities for Enbridge’s top-10 North American position

Canadian Midstream

North American

GasPipelines

Utilities

Renewable Power

U.S.Midstream

Enbridge Platforms for Growth Spectra Platforms for Growth

North American Liquids

Pipelines

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Investment Community Presentation January 2017

5

Strong Commercial Underpinning

Low Risk Business Model Limited Commodity Price Risk Investment Grade Customers

96% of cash flow underpinned by long term commercial agreements (Take-or-pay or

equivalent1 contracts)

<5% of combined EBITDA is commodity price exposed

93%2 of revenue from investment grade or equivalent customers

Maintains Enbridge’s low risk and capital discipline for unparalleled resilience in all market cycles

Investment grade or equivalent 93%

Sub investment grade 7%

Fee-based >95%

Not fee-based <5%

Take-or-pay or equivalent 96%

Volumetric risk 4%

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

(1) Equivalent includes cost of service, Competitive Tolling Settlement and fee for service.(2) Excludes low risk regulated distribution utility revenues.

Significant and Highly Visible Combination Synergies

Full run-rate cost synergies expected to be achieved by end of 2018:

• Identifiable and achievable cost synergies; conservative estimates

•Potential to optimize funding / financing synergies (not included)

•Extends Spectra Energy’s current favorable cash tax position beyond 2018

•Assumes no benefits from future commercial and structuring synergies

Significant value created through operating and financial synergies

Forecast annual run rate synergies by 2018

$540 Million

General O&A costs 75%

Supply chain optimization 13%

Other costs 12%

Multiple synergy opportunities

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Investment Community Presentation January 2017

6

Industry Leading GrowthWell balanced organic growth opportunities across six platforms

North American Liquids

Pipelines

North American Gas PipelinesUtilities

Midstream

Renewable Power

Unrivaled pro-forma secured expansion program1

2017 – 2019 ISDs ($ billions)Large, diverse opportunity set ($ billions)

$6 $8

$13

$17

$23

$26

WMBEPDETPKMITRPPro FormaEnbridge

100% in execution

$48Billion

Probability weighted development projects

Major Components of Risked Capital2, 3

• De-bottlenecking liquids pipelines / market access

• Northeast gas pipelines expansion / extension

• Southeast gas pipeline capacity

• Gas pipelines for exports

• EDF – Offshore wind

• Other offshore wind

• Utility organic growth

• Organic midstream expansion

• Others

Note: KMI, ETP, EPD and WMB secured expansion capex figures converted to CAD using a 1.28 USD to CAD F/X rate.(1) Secured growth capital program reflects only publicly announced secured projects entering into service between 2017 and 2019.(2) Probability weighted development growth capital.(3) Capital spending (predominantly post-2020) will further extend growth beyond the next decade

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Diversifies and De-risks 2017–2019 Growth Guidance

Capital in service (2017 – 2019)

$5.9

$1.4

$8.2

$7.0

$2.6

$0.4

0

2

4

6

8

10

12

14

2017 2018 2019

$26B in projects to come online between 2017 and 2019

Diversity of secured growth programs by:• Commodity type• Expenditure profile

• Geography• Project size

Enbridge

Spectra Energy

$13$13

$4$4

$9$9

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Investment Community Presentation January 2017

7

Supports, De-risks and Enhances Current Plan

$3.02

$3.72

2014A 2015A 2016E 2017E 2018E 2019E

$5.50

$6.00

$3.80

$4.50

ACFFO per share outlook through 2019 intact

ACFFO per Share Outlook (2014-2019)

2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E

Enbridge Spectra Energy Combination –Visible Organic Dividend Growth with Upside Potential

Dividend per Share Outlook (2017-2024)

$2.12

• 15% dividend increase in 20171

• 10-12% annual dividend growth (2018 through 2024)

• Conservative payout ratio of 50% - 60%

Dividend growth beyond 2019 supported by:

• Embedded growth / tilted returns

• $48B in probability-weighted development

project pipeline

• Potential to gradually increase payout within

50-60% range

1 Pro-rated based on transaction close date.Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Dividend growth through 2019 supported by:

• $26B secured growth program in execution

• Embedded growth / tilted returns

Investment Community Presentation January 2017

8

No Requirements for Follow-on Enbridge Inc. Equity

Uses Sources

Immediate and strengthening financial flexibility

Enbridge Group Funding Requirements2017e – 2019e

Debt maturities $10 JV Contributions $2

Capital expenditures $23 DRIP/Sponsored Investments/Monetizations

$8

Debt issuances $9

Internal cash flow, net of dividends $14

Ample sources of alternative equity financing

• $8B of alternative sources of equity capital:

• Spectra Energy Partners ATM

• Enbridge Income Fund Common Equity

• Enbridge Energy Partners PIK

• Enbridge Inc. DRIP

• Hybrids

• Planned monetization of ~$2B in non-core assets over next 12 months

• Other identified asset monetizations could provide an incremental $5-$6B of capital

Significant free cash flow generation beyond 2019

• Cumulative $14 to $18B free cash flow1 enables company to grow organically, acquire assets, and raise dividends without equity issuance at corporate level

• More competitive in capturing new organic opportunities

1 Cumulative free cash flow (net of dividends and maintenance capital) generated between 2020e and 2024e from commercially secured growth.

Balance Sheet StrengthCommitted to strong, investment grade credit ratings

Key Credit Metrics and TargetsStrong Credit Metrics

Significant Balance Sheet Strengthening by 2018Projected Pro Forma Debt to EBITDA

Credit Metric Target

FFO / Debt ≥15%

Debt / EBITDA ≤5.0x

6.2x5.5x

5.1x4.3x

2016 2017 2018 2019

5.0x

• Increased size, scale and asset diversity significantly enhances the credit profile of the combined entity

• Debt to EBITDA naturally improves as high quality projects under construction are placed into service and begin generating cash flows

• Committed to achieving targeted improvement in credit metrics and maintaining credit ratings across the family of companies as new projects are pursued

Slide reflects pro-forma combination with Spectra. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Investment Community Presentation January 2017

9

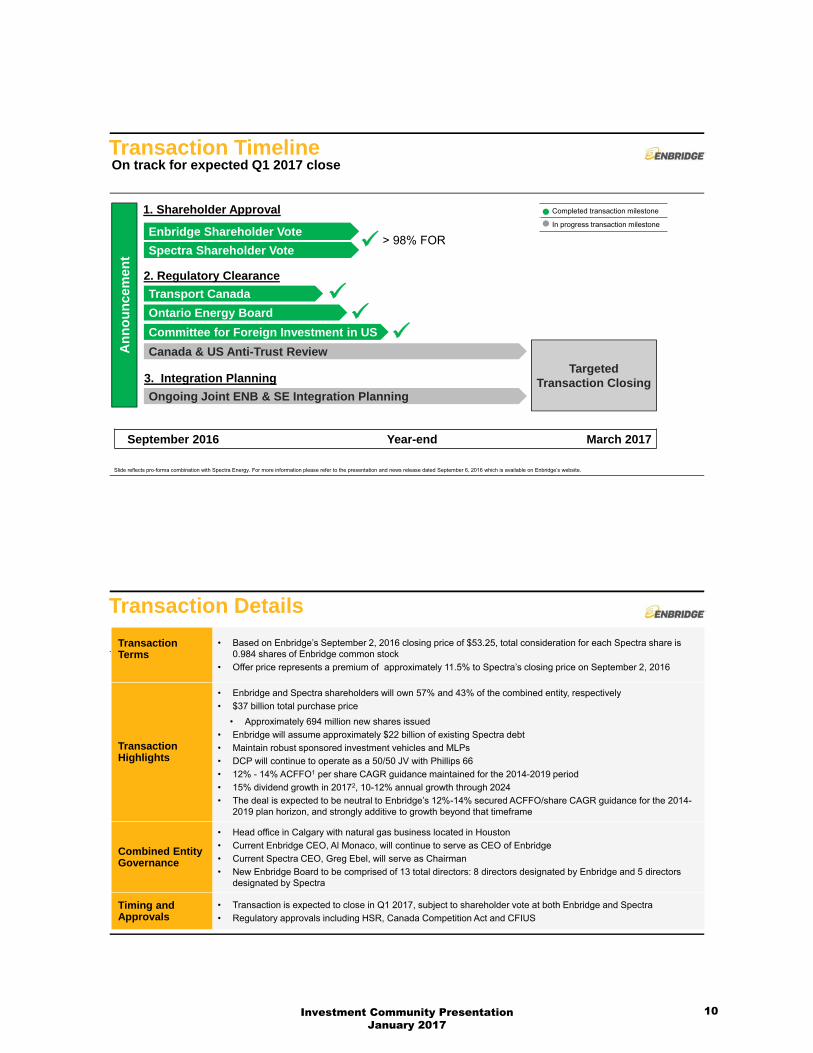

Transaction TimelineOn track for expected Q1 2017 close

Enbridge Shareholder Vote

An

no

un

cem

ent

Targeted Transaction Closing

September 2016 Year-end March 2017

Completed transaction milestone

In progress transaction milestone

Slide reflects pro-forma combination with Spectra Energy. For more information please refer to the presentation and news release dated September 6, 2016 which is available on Enbridge’s website.

Obtain Transport Canada and CFIUS clearance

Spectra Shareholder Vote

Transport Canada

Ontario Energy Board

Committee for Foreign Investment in US

Canada & US Anti-Trust Review

Ongoing Joint ENB & SE Integration Planning

1. Shareholder Approval

2. Regulatory Clearance

3. Integration Planning

> 98% FOR

Transaction Terms

• Based on Enbridge’s September 2, 2016 closing price of $53.25, total consideration for each Spectra share is 0.984 shares of Enbridge common stock

• Offer price represents a premium of approximately 11.5% to Spectra’s closing price on September 2, 2016

Transaction Highlights

• Enbridge and Spectra shareholders will own 57% and 43% of the combined entity, respectively

• $37 billion total purchase price

• Approximately 694 million new shares issued

• Enbridge will assume approximately $22 billion of existing Spectra debt

• Maintain robust sponsored investment vehicles and MLPs

• DCP will continue to operate as a 50/50 JV with Phillips 66

• 12% - 14% ACFFO1 per share CAGR guidance maintained for the 2014-2019 period

• 15% dividend growth in 20172, 10-12% annual growth through 2024

• The deal is expected to be neutral to Enbridge’s 12%-14% secured ACFFO/share CAGR guidance for the 2014-2019 plan horizon, and strongly additive to growth beyond that timeframe

Combined Entity Governance

• Head office in Calgary with natural gas business located in Houston

• Current Enbridge CEO, Al Monaco, will continue to serve as CEO of Enbridge

• Current Spectra CEO, Greg Ebel, will serve as Chairman

• New Enbridge Board to be comprised of 13 total directors: 8 directors designated by Enbridge and 5 directors designated by Spectra

Timing and Approvals

• Transaction is expected to close in Q1 2017, subject to shareholder vote at both Enbridge and Spectra

• Regulatory approvals including HSR, Canada Competition Act and CFIUS

Transaction Details

Investment Community Presentation January 2017

10

Strategic Overview

Investment Community Presentation January 2017

11

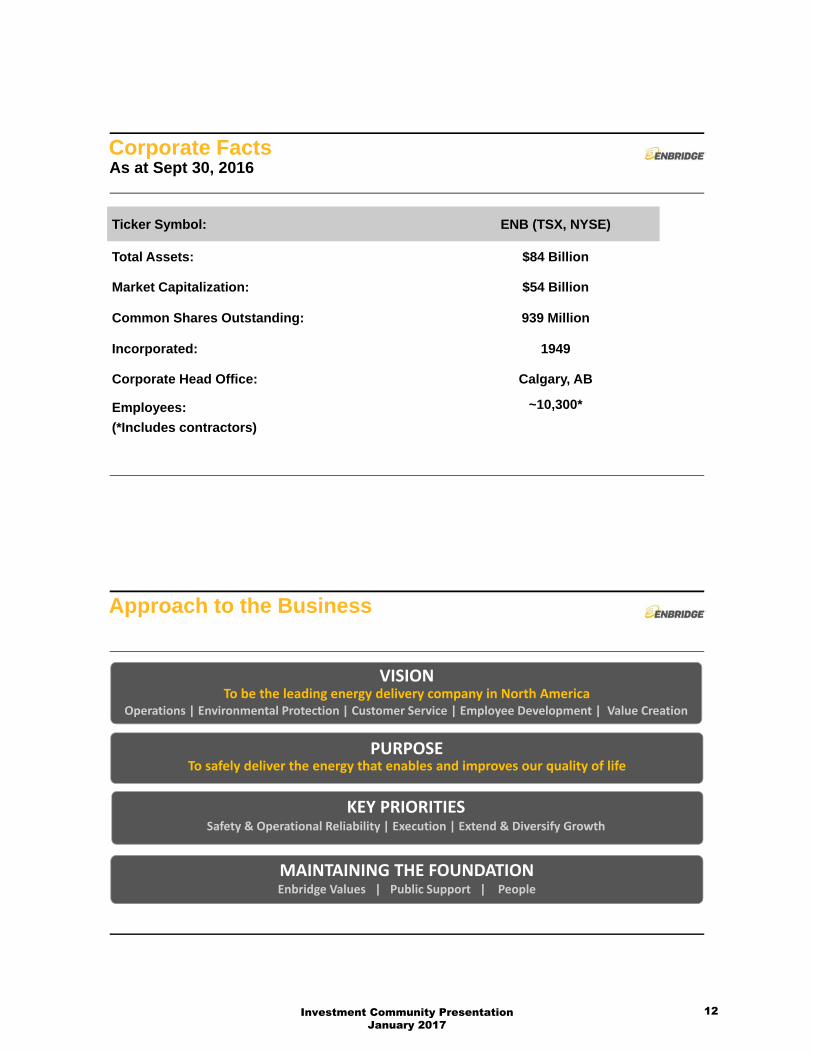

Corporate Facts

Ticker Symbol: ENB (TSX, NYSE)

Total Assets: $84 Billion

Market Capitalization: $54 Billion

Common Shares Outstanding: 939 Million

Incorporated: 1949

Corporate Head Office: Calgary, AB

Employees:

(*Includes contractors)

~10,300*

As at Sept 30, 2016

Approach to the Business

PURPOSETo safely deliver the energy that enables and improves our quality of life

KEY PRIORITIESSafety & Operational Reliability | Execution | Extend & Diversify Growth

MAINTAINING THE FOUNDATIONEnbridge Values | Public Support | People

VISION

Operations | Environmental Protection | Customer Service | Employee Development | Value CreationTo be the leading energy delivery company in North America

Investment Community Presentation January 2017

12

Strategically Positioned AssetsLiquids

• 27,600 km of pipeline

• 2.85 mmbpd mainline capacity

• 3.5 mmbpd market connected

Gas Distribution

• 2.1 million customers

• 420 bcf distributed

• 115 bcf gas storage

Gas Pipelines & Processing

• 24,800 km of pipeline

• 12 bcf/d pipeline capacity

• 107,000 bpd fractionation

• 4 bcf/d G&P capacity

Power & Energy Services

• 23 renewable projects

• 1,776 MW capacity (net)

• Marketing & refining supply

Shareholder Value Proposition

Industry Leading GrowthStrategic Asset Positioning ● Strong Fundamentals ●

Extend & Diversify Growth

Reliable Business ModelConservative Commercial Structures ● Minimal Commodity Exposure ●

Disciplined Capital Allocation

Significant Dividend Income4.0% yield ●10-12% growth

Superior Shareholder Returns=

+

+

14% 13%

2%4%

11% 11%

5 Year 10 Year

Enbridge Inc. S&P/TSX Composite Index Peer Average

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Dividend Per Share

Annualized Total Shareholder Return Dec 31, 2015

Investment Community Presentation January 2017

13

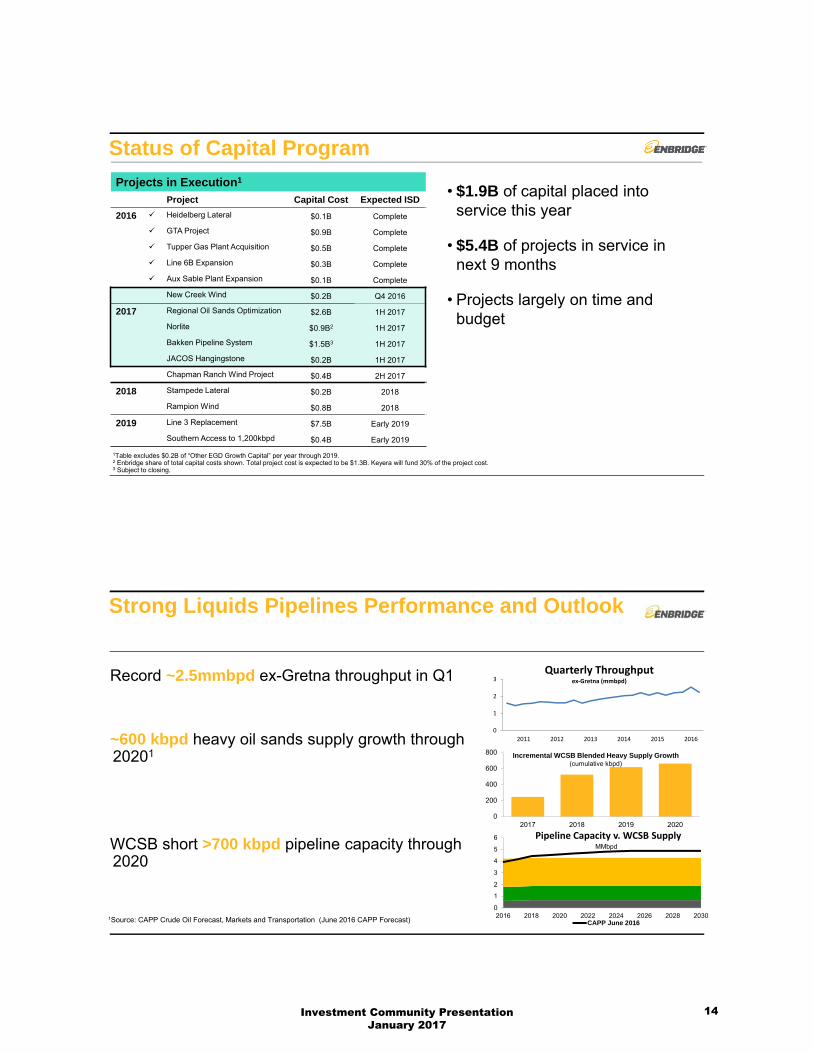

Status of Capital Program

Projects in Execution1

Project Capital Cost Expected ISD

2016 Heidelberg Lateral $0.1B Complete

GTA Project $0.9B Complete

Tupper Gas Plant Acquisition $0.5B Complete

Line 6B Expansion $0.3B Complete

Aux Sable Plant Expansion $0.1B Complete

New Creek Wind $0.2B Q4 2016

2017 Regional Oil Sands Optimization $2.6B 1H 2017

Norlite $0.9B2 1H 2017

Bakken Pipeline System $1.5B3 1H 2017

JACOS Hangingstone $0.2B 1H 2017

Chapman Ranch Wind Project $0.4B 2H 2017

2018 Stampede Lateral $0.2B 2018

Rampion Wind $0.8B 2018

2019 Line 3 Replacement $7.5B Early 2019

Southern Access to 1,200kbpd $0.4B Early 2019

1Table excludes $0.2B of “Other EGD Growth Capital” per year through 2019.2 Enbridge share of total capital costs shown. Total project cost is expected to be $1.3B. Keyera will fund 30% of the project cost.3 Subject to closing.

• $1.9B of capital placed into service this year

• $5.4B of projects in service in next 9 months

• Projects largely on time and budget

0

200

400

600

800

2017 2018 2019 2020

Strong Liquids Pipelines Performance and Outlook

1Source: CAPP Crude Oil Forecast, Markets and Transportation (June 2016 CAPP Forecast)

Pipeline Capacity v. WCSB Supply

0

1

2

3

4

5

6

2016 2018 2020 2022 2024 2026 2028 2030

MMbpd

CAPP June 2016

0

1

2

3

2011 2012 2013 2014 2015 2016

Quarterly Throughputex‐Gretna (mmbpd)

Incremental WCSB Blended Heavy Supply Growth(cumulative kbpd)

Record ~2.5mmbpd ex-Gretna throughput in Q1

~600 kbpd heavy oil sands supply growth through 20201

WCSB short >700 kbpd pipeline capacity through 2020

Investment Community Presentation January 2017

14

Liquids Business Competitive Position & Market Reach

*USD per barrel of heavy crude from Hardisty to Chicago

MARKET CAPACITY(KBPD)

Mainline ConnectedRefineries

1,900

Mainline Connected Markets (Pipelines)

PADD II 200

Cushing/USGC 775

Quebec/Ontario 300

Patoka 300

Total Pipeline Access 1,575

Grand Total 3,475

Stable, competitive tolls Stable, competitive tolls

$0

$2

$4

$6

2012 2013 2014 2015 2016

Strong Financial Position Strong credit ratings provide ready access to debt capital to fund growth program

Strong credit ratings supported by:

• Low business risk (rated “A” by Moody’s; “Excellent” by S&P)

• Minimal commodity price risk; strong counterparties

• Stable and predictable cash flows

• Project execution track record

• Strong dividend coverage

• Substantial standby liquidity; access to multiple sources of capital

EPI EGD ENB FUND EEP

DBRS A ABBB

(High)BBB

(High) BBB

Outlook Stable Stable Stable Stable Stable

Moody’s - - Baa2 Baa2 Baa3

Outlook - - Negative Negative Negative

S&P BBB+ BBB+ BBB+ - BBB

Outlook Stable Stable Stable - Stable

Investment Community Presentation January 2017

15

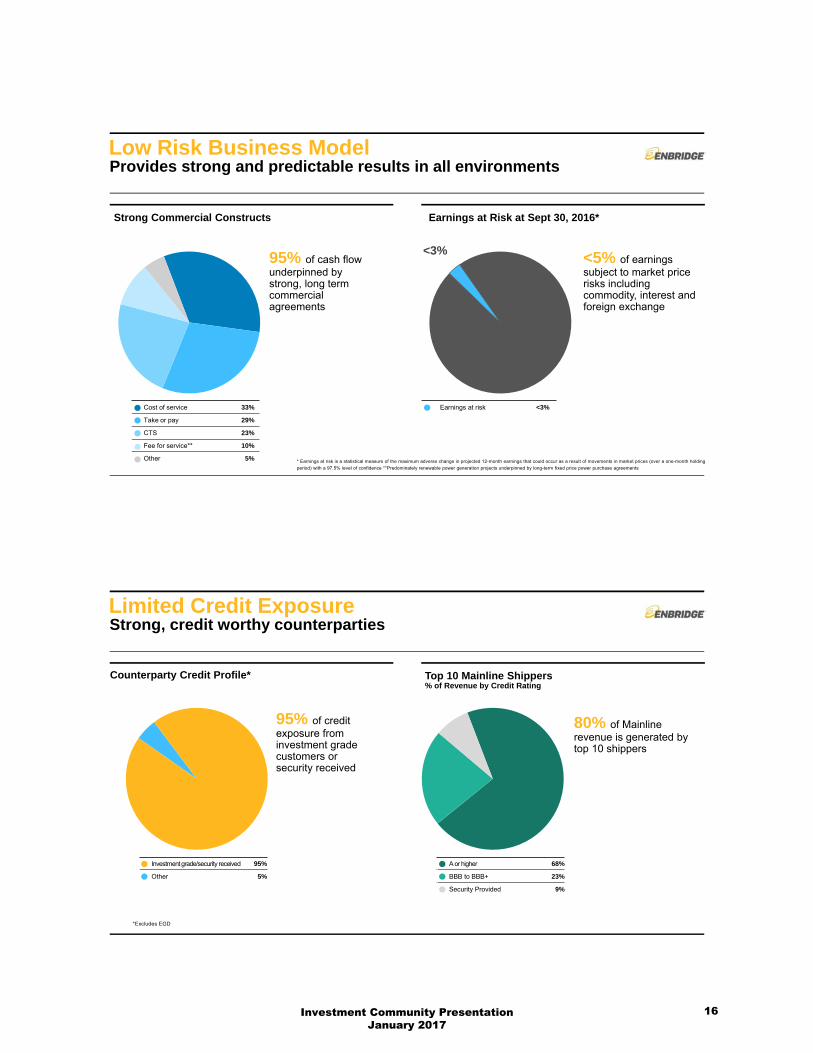

Low Risk Business Model

Strong Commercial Constructs

Provides strong and predictable results in all environments

Earnings at Risk at Sept 30, 2016*

Earnings at risk <3%Cost of service 33%

Take or pay 29%

CTS 23%

Fee for service** 10%

Other 5%

95% of cash flow underpinned by strong, long term commercial agreements

<5% of earnings subject to market price risks including commodity, interest and foreign exchange

<3%

* Earnings at risk is a statistical measure of the maximum adverse change in projected 12-month earnings that could occur as a result of movements in market prices (over a one-month holding

period) with a 97.5% level of confidence **Predominately renewable power generation projects underpinned by long-term fixed price power purchase agreements

Limited Credit Exposure Strong, credit worthy counterparties

Counterparty Credit Profile* Top 10 Mainline Shippers% of Revenue by Credit Rating

Investment grade/security received 95%

Other 5%

A or higher 68%

BBB to BBB+ 23%

Security Provided 9%

95% of credit exposure from investment grade customers or security received

80% of Mainline revenue is generated by top 10 shippers

*Excludes EGD

Investment Community Presentation January 2017

16

Strong Counterparty Credit Profile Major liquids pipeline systems underpinned by strong, investment grade customers

MAINLINE TOP 10 SHIPPERS

Shipper 1: Integrated AA+/Aaa

Shipper 2: Integrated A-/NR

Shipper 3: Refiner BBB/Baa2

Shipper 4: Integrated A-/Baa1

Shipper 5: Refiner AA-/A1

Shipper 6: Refiner A/Aa2

Shipper 7: Integrated BBB/Baa2

Shipper 8: Midstream B-/B3 (security provided)

Shipper 9: Refiner BBB-/Baa3

Shipper 10: Refiner BB/Ba3 (security provided)

REGIONAL OIL SANDS TOP 10 SHIPPERS

Shipper 1: Integrated A-/Baa1

Shipper 2: Integrated AA+/NR

Shipper 3: Producer BBB/Ba2

Shipper 4: Integrated BBB+/Baa2

Shipper 5: Producer A-/Baa2

Shipper 6: Producer BBB- (internal rating)

Shipper 7: Producer Credit enhancement to investment grade

Shipper 8: Integrated A+/Aa3

Shipper 9: Producer BBB+/NR

Positioned for Low Commodity Price Environment

Power & Energy Services

Gas Distribution Gas Pipelines & Processing

•WCSB volume growth through 2019

•Well capitalized customers with strong credit ratings

•Largest producers integrated with downstream operations

•Long term take-or-pay contracts

•Diversified businesses, connecting to premium markets

•Optimizing cost structure (MEP)

•No commodity price exposure

•Regulated business with throughput protection

•Highly competitive fuel source

•Long term PPAs with contracted power prices

•Diversified wind and solar resources

•Physical market arbitrage (Energy Services)

Liquids Pipelines

Investment Community Presentation January 2017

17

Corporate Priorities

1. Focus on safety andoperational reliability

2. Execute the growthcapital program

3. Extend and diversify growth

Priority 1: Focus on Safety & Operational ReliabilityOur goal is to lead the industry in six key areas of safety and operational reliability

Operational Risk Management

2011 2012 2013 2014 2015 2019E

Maintenance and Integrity Spending*(enterprise wide)

Technology Advancements

*Includes core maintenance capital and non-growth enhancements

Investment Community Presentation January 2017

18

Priority 2: Execute the Capital ProgramEnbridge has developed a strong major projects execution capability that provides a competitive advantage

Challenging Environment• Securing regulatory approval

• Cost and schedule risk

Project Management Expertise• Disciplined processes

• Supply chain management

• Capacity, skills, resources

Engaging Communities • Safety and environmental protection

• Demonstrate flexibility

• Build coalitions of support

0%

20%

40%

60%

80%

100%

Priority 2: Cost and Supply Chain Management

Key Inputs Secured• Favourable pricing and terms

⎯ Pipe

⎯ Mainline construction

⎯ Engineered equipment

• Capital Management

⎯ Supply chain cost initiatives

⎯ Scalable workforce

⎯ Productivity enhancements

• Capacity Optimization

⎯ Regional Oil Sands Optimization

⎯ $400 million savings

⎯ Mainline optimization

Enbridge Pipe vs. Market Pricing(USD/Short Ton)

Canadian Pipe

U.S. Pipe

Mainline Contracting

Land/ROW Acquisition

Enbridge Pricing

Market Pricing

0

400

800

1,200

1,600

2,000

Jan‐12 Nov‐12 Sep‐13 Jul‐14 May‐15 Mar‐16

Investment Community Presentation January 2017

19

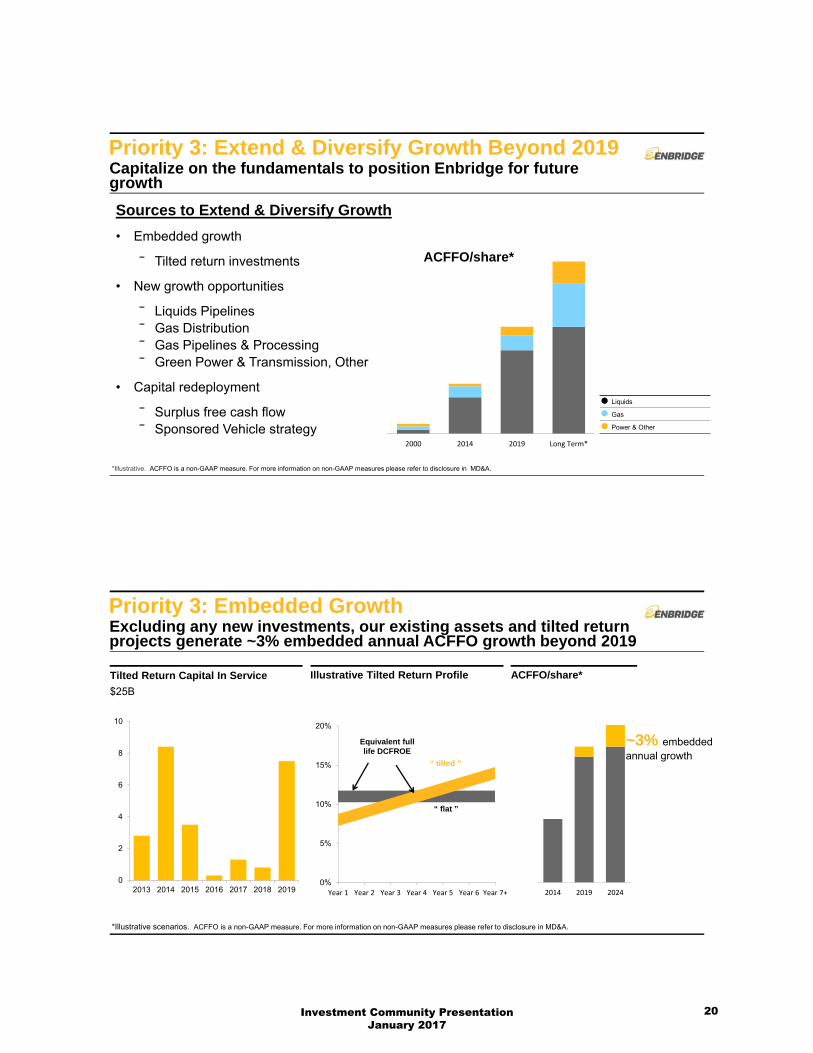

Priority 3: Extend & Diversify Growth Beyond 2019Capitalize on the fundamentals to position Enbridge for future growth

2000 2014 2019 Long Term*

ACFFO/share*

Sources to Extend & Diversify Growth

• Embedded growth

⎯ Tilted return investments

• New growth opportunities

⎯ Liquids Pipelines⎯ Gas Distribution⎯ Gas Pipelines & Processing⎯ Green Power & Transmission, Other

• Capital redeployment

⎯ Surplus free cash flow⎯ Sponsored Vehicle strategy

*Illustrative. ACFFO is a non-GAAP measure. For more information on non-GAAP measures please refer to disclosure in MD&A.

Liquids

Gas

Power & Other

Priority 3: Embedded Growth

*Illustrative scenarios. ACFFO is a non-GAAP measure. For more information on non-GAAP measures please refer to disclosure in MD&A.

Excluding any new investments, our existing assets and tilted return projects generate ~3% embedded annual ACFFO growth beyond 2019

ACFFO/share*Tilted Return Capital In Service

$25B

Illustrative Tilted Return Profile

~3% embedded annual growth

0

2

4

6

8

10

2013 2014 2015 2016 2017 2018 20190%

5%

10%

15%

20%

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7+

Equivalent full life DCFROE

“ tilted ”

“ flat ”

2014 2019 2024

Investment Community Presentation January 2017

20

Priority 3: Opportunities to Extend & Diversify Growth Substantial opportunity set drives growth beyond secured outlook

Gas Distribution• Retail, commercial, industrial load growth• System renewal and expansion• Storage and transportation

Gas Pipelines & Processing• Canadian midstream • Offshore USGC• Expand gas footprint

New Platforms• Power generation and transmission• Energy Services• International

Liquids Pipelines• Low-cost mainline expansion programs• Market access expansions/extensions• USGC regional infrastructure

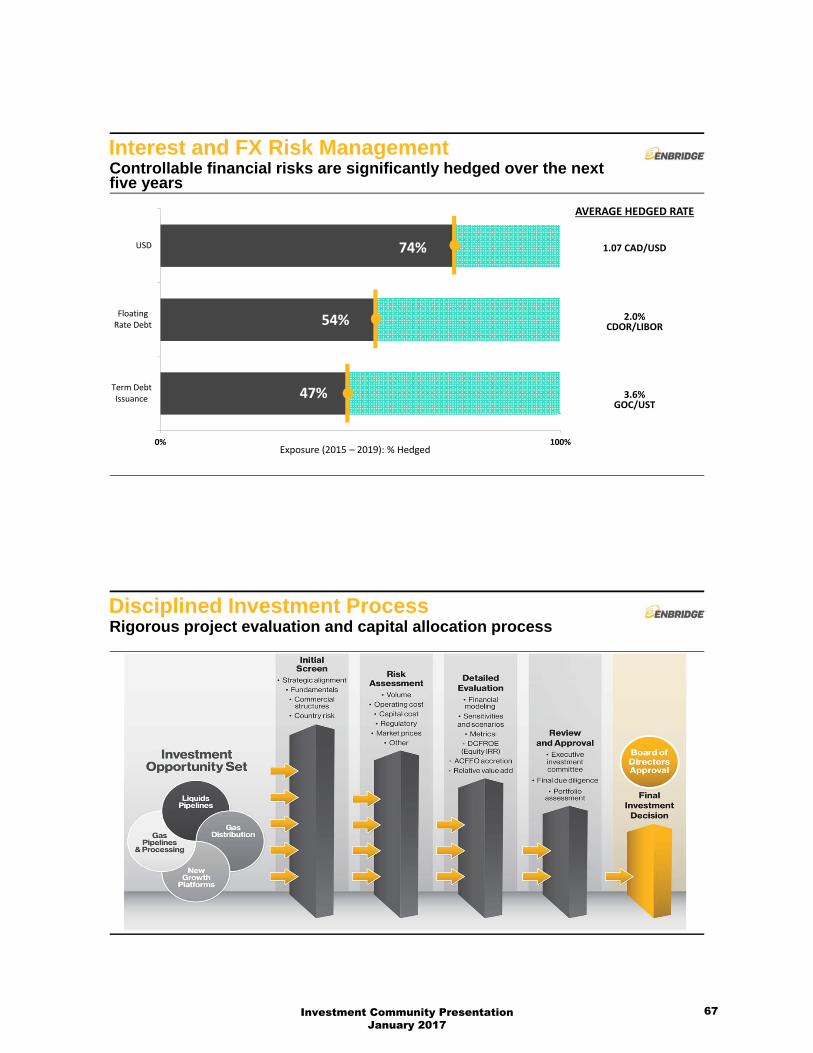

Key investment criteria

• Strategic alignment

• Solid fundamentals

• Strong commercial underpinning

• Premium return to cost of capital

• Readily financeable

Priority 3: Capital RedeploymentGrowing ACFFO will be redeployed based on our capital allocation framework and strength of redeployment opportunities

ACFFO Growth*(secured program)

Capital Allocation Parameters

• Consistent with value proposition

• Strategic alignment

• Dividend payout policy

Redeployment Opportunities

• Organic investments

• Bolt-on asset acquisitions

• Expand strategic footprint

• Return capital to shareholders*ACFFO is a non-GAAP measure. For more information on non-GAAP measures please refer to disclosure in MD&A. Growth rate reflects secured program only; unsecured development pipeline provides further upside.

$3.02

2014 2019

12-14%+ CAGR12-14%+ CAGR

Investment Community Presentation January 2017

21

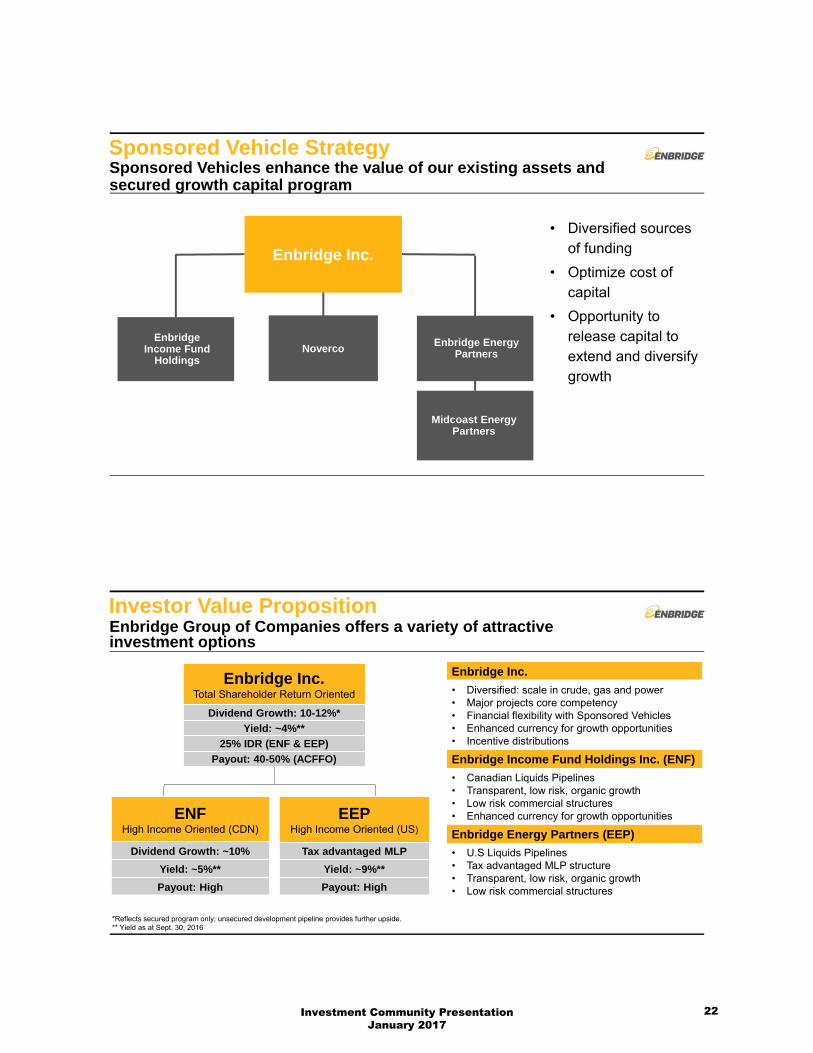

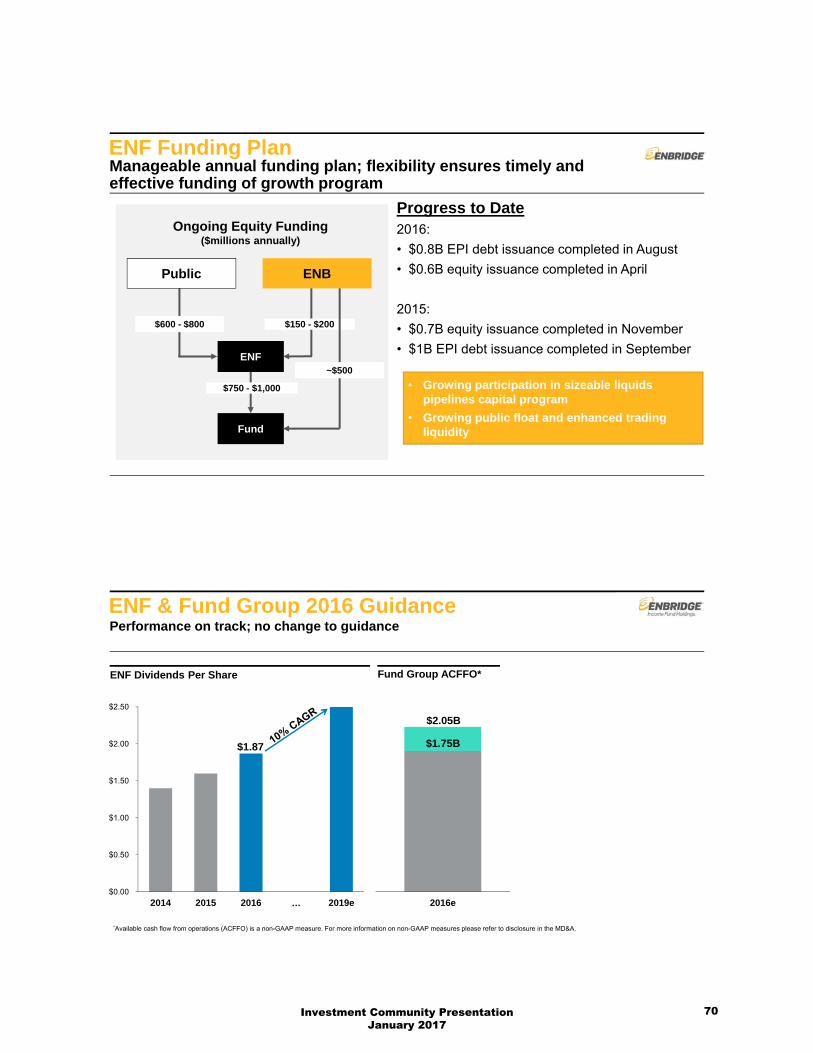

Sponsored Vehicle StrategySponsored Vehicles enhance the value of our existing assets and secured growth capital program

Enbridge Income Fund

HoldingsNoverco

Enbridge EnergyPartners

Enbridge Inc.

Midcoast Energy Partners

• Diversified sources of funding

• Optimize cost of capital

• Opportunity to release capital to extend and diversify growth

Investor Value Proposition

Enbridge Inc.Total Shareholder Return Oriented

Dividend Growth: 10-12%*

Yield: ~4%**

25% IDR (ENF & EEP)

Payout: 40-50% (ACFFO)

ENFHigh Income Oriented (CDN)

Dividend Growth: ~10%

Yield: ~5%**

Payout: High

EEPHigh Income Oriented (US)

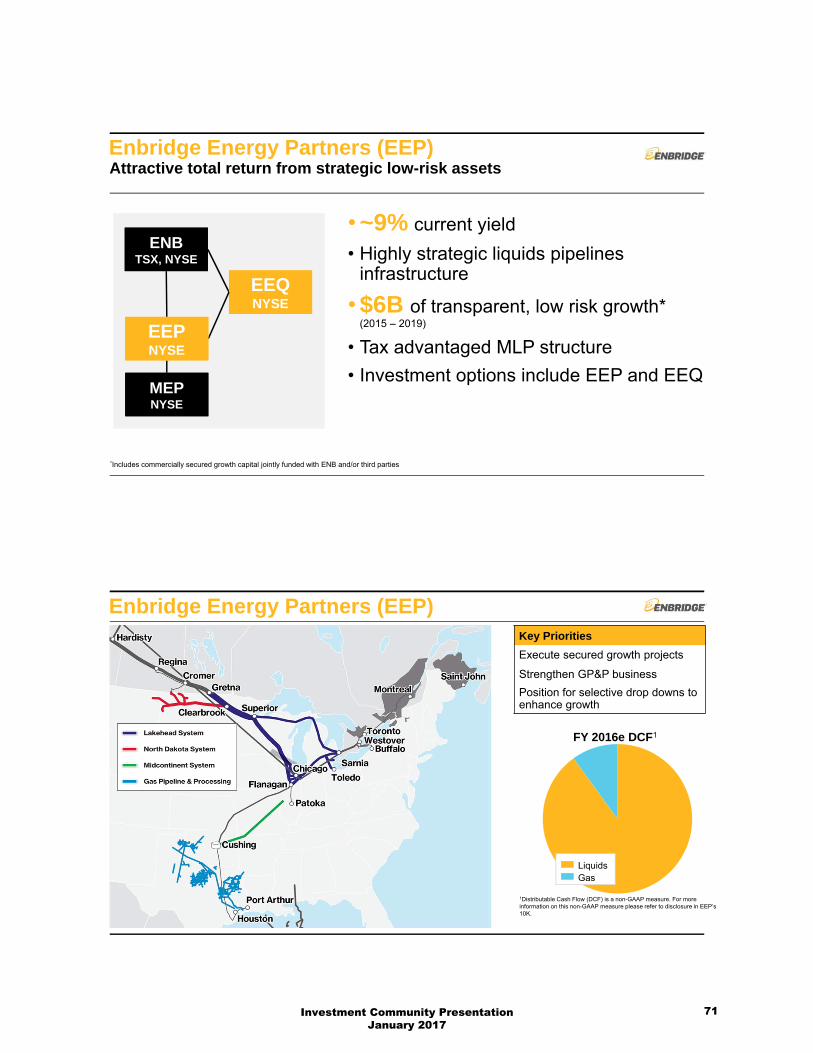

Tax advantaged MLP

Yield: ~9%**

Payout: High

Enbridge Group of Companies offers a variety of attractive investment options

Enbridge Inc.

• Diversified: scale in crude, gas and power• Major projects core competency• Financial flexibility with Sponsored Vehicles• Enhanced currency for growth opportunities• Incentive distributions

Enbridge Income Fund Holdings Inc. (ENF)

• Canadian Liquids Pipelines• Transparent, low risk, organic growth• Low risk commercial structures• Enhanced currency for growth opportunities

Enbridge Energy Partners (EEP)

• U.S Liquids Pipelines• Tax advantaged MLP structure• Transparent, low risk, organic growth• Low risk commercial structures

*Reflects secured program only; unsecured development pipeline provides further upside.** Yield as at Sept. 30, 2016

Investment Community Presentation January 2017

22

Liquids Pipelines

Investment Community Presentation January 2017

23

Current System Overview

• Low-cost and stable tolls

• Market access optionality

• Crude slate and capacity optimization

• Unparalleled terminal and operational flexibility

Regional Oil Sands

Mainline System

North Dakota System

Lakehead System

Spearhead/Flanagan South

Investment Community Presentation January 2017

24

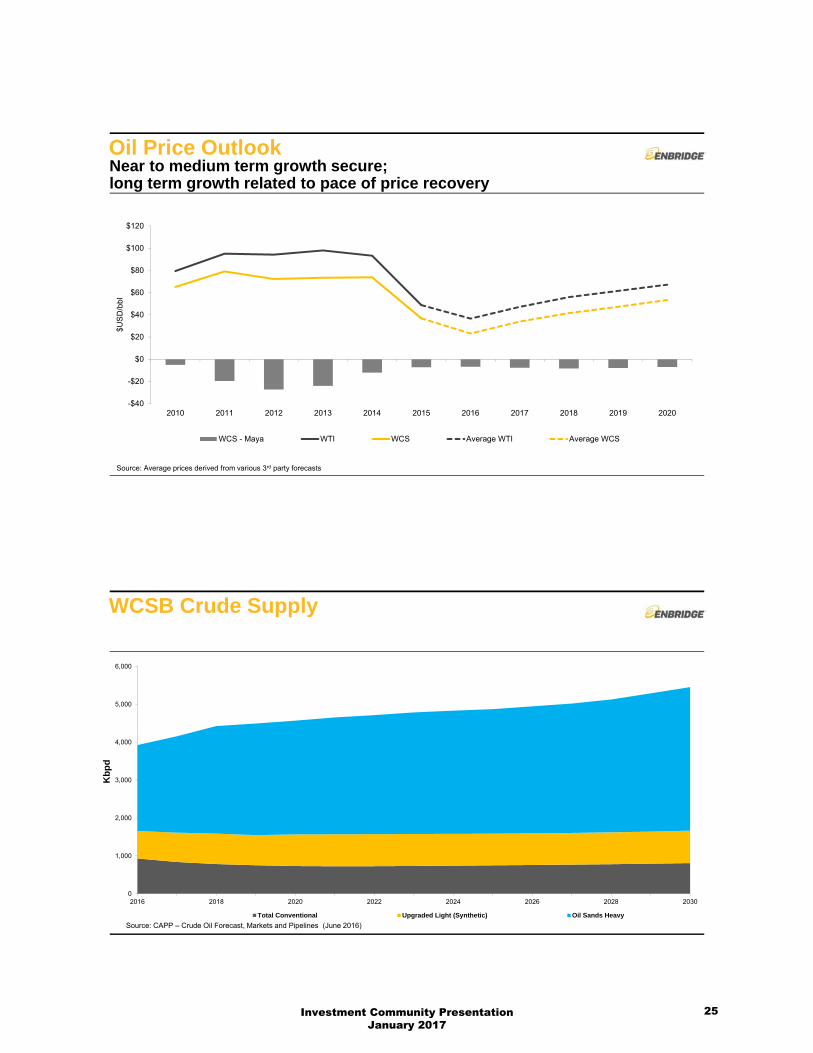

Oil Price OutlookNear to medium term growth secure; long term growth related to pace of price recovery

Source: Average prices derived from various 3rd party forecasts

-$40

-$20

$0

$20

$40

$60

$80

$100

$120

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

$U

SD

/bb

l

WCS - Maya WTI WCS Average WTI Average WCS

WCSB Crude Supply

Source: CAPP – Crude Oil Forecast, Markets and Pipelines (June 2016)

0

1,000

2,000

3,000

4,000

5,000

6,000

2016 2018 2020 2022 2024 2026 2028 2030

Kb

pd

Total Conventional Upgraded Light (Synthetic) Oil Sands Heavy

Investment Community Presentation January 2017

25

Oil Sands Blended Supply OutlookHighly transparent supply outlook drives growth

“Syncrude production averaged 85,000barrels per day (Imperial’s share), the second highest quarterly production inits nearly 40-year history, reflecting ongoing efforts to improve the reliabilityof operations.”

Imperial Oil 3nd Quarter Results Release Oct 28, 2016

“The Sunrise Energy Project has resumed itsramp up following the restart of operations after the Fort McMurray wildfires.”

Husky Energy 3th Quarter Results Release Oct 27, 2016

“Surmont fully recovered from wildfire impacts and continues to ramp upwith gross production exceeding 100 MBOED in mid-October.”

ConocoPhillips 3rd Quarter 2016 Results Oct 27, 2016

“The Fort Hills project is more than 70% complete at the end of the thirdquarter of 2016, with the majority of the remaining work based in Alberta.”

Suncor Energy Inc. 3rd Quarter 2016 Results Oct 26, 2016

1Source: CAPP Crude Oil Forecast, Markets and Transportation (June 2015 Operating & In Construction)

“Current production volumes at Horizon are approximately175,000 bbl/d as the Phase 2B expansion start-up was executed in earlyOctober, slightly ahead of the targeted start-up date.”

Husky Energy 3nd Quarter Results Release Nov 3, 2016

0

100

200

300

400

500

600

700

2017 2018 2019 2020

Incremental WCSB Blended HeavySupply Growth

(cumulative kbpd)

Takeaway Capacity vs. Supply Outlook

Other Existing Pipelines

Western Canadian Refineries

Source: CAPP – Crude Oil Forecast, Markets and Pipelines (June 2016)

Near term optimization: +60 – 80 kbpd

0

1

2

3

4

5

6

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Takeaway Capacity vs. Supply Outlook(mmbpd)

CAPP June 2016

Enbridge

Other Existing Pipelines

Western Canadian Refineries

Investment Community Presentation January 2017

26

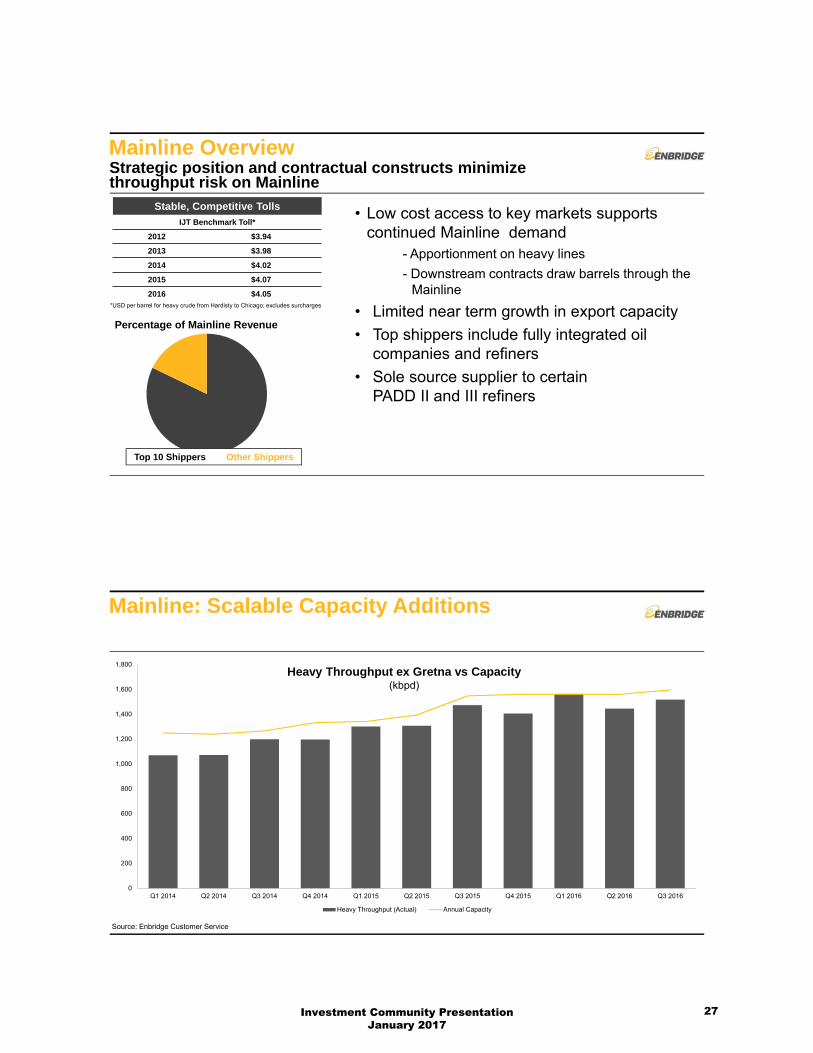

Mainline OverviewStrategic position and contractual constructs minimize throughput risk on Mainline

• Low cost access to key markets supports continued Mainline demand

- Apportionment on heavy lines

- Downstream contracts draw barrels through the Mainline

• Limited near term growth in export capacity

• Top shippers include fully integrated oil companies and refiners

• Sole source supplier to certain PADD II and III refiners

Stable, Competitive Tolls

IJT Benchmark Toll*

2012 $3.94

2013 $3.98

2014 $4.02

2015 $4.07

2016 $4.05

Top 10 Shippers Other Shippers

Percentage of Mainline Revenue

*USD per barrel for heavy crude from Hardisty to Chicago; excludes surcharges

Mainline: Scalable Capacity Additions

Source: Enbridge Customer Service

Heavy Throughput ex Gretna vs Capacity(kbpd)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016

Heavy Throughput (Actual) Annual Capacity

Investment Community Presentation January 2017

27

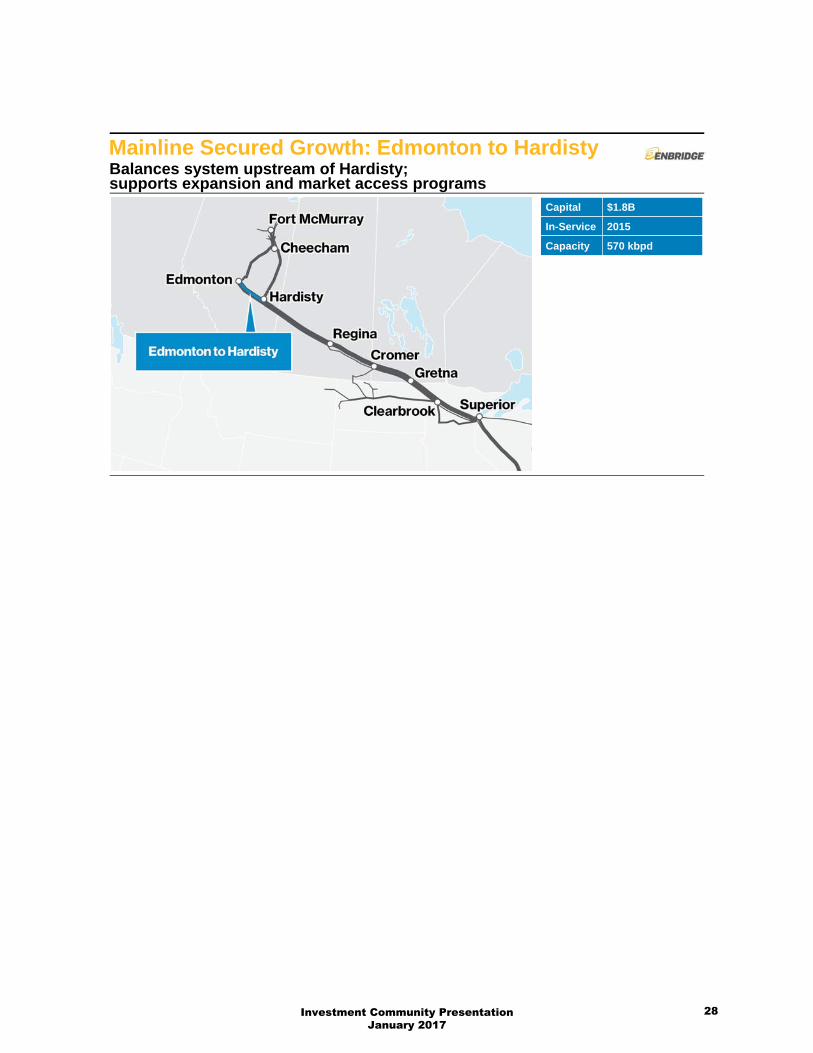

Mainline Secured Growth: Edmonton to HardistyBalances system upstream of Hardisty;supports expansion and market access programs

Capital $1.8B

In-Service 2015

Capacity 570 kbpd

Investment Community Presentation January 2017

28

Mainline Secured Growth: Line 3 Replacement

Capital $7.5B

In-Service Early 2019

CapacityRestore capacity to 760 kbpd

Project details• Replace all remaining segments of Line 3 between Hardisty and Superior• Restores line capacity to 760 kbpd• Expected in-service date: Early 2019• Shipper support (CAPP/RSG)• 15 year toll surcharge

Investment attributes• Solid return on significant incremental investment• Supports secured capital ACFFO growth profile• Avoids $1.1 billion in maintenance capital through 2017 and mounting thereafter

Benefits• Supports our #1 priority: safety and operational reliability• Provides high reliability and assurance to key markets• Reduced scheduling impacts of future maintenance• Increased scheduling flexibility• Improved line balancing

Mainline Secured Growth: Line 3 Replacement

Investment Community Presentation January 2017

29

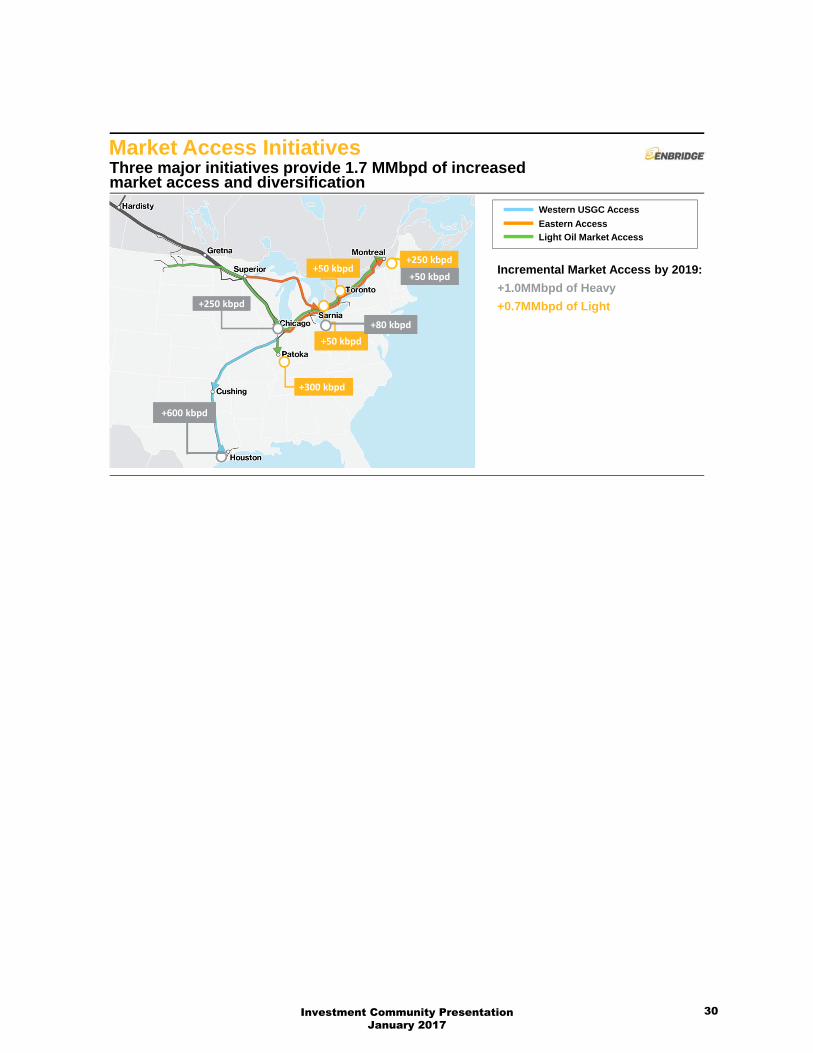

Market Access InitiativesThree major initiatives provide 1.7 MMbpd of increased market access and diversification

Eastern Access

Western USGC Access

Light Oil Market Access

Incremental Market Access by 2019:

+1.0MMbpd of Heavy

+0.7MMbpd of Light

+600 kbpd+600 kbpd

+300 kbpd

+250 kbpd+250 kbpd

+50 kbpd+50 kbpd+250 kbpd

+50 kbpd

+250 kbpd

+50 kbpd

+50 kbpd+50 kbpd

+80 kbpd+80 kbpd

Investment Community Presentation January 2017

30

Associated Mainline Expansions• Alberta Clipper to 800 kbpd • Southern Access to 560 kbpd

Flanagan South Pipeline • $2.9B capital project• In service: Q4 2014• Long term commercial agreements

(10 – 20 year terms)• Initial capacity: 600 kbpd, expandable to 800 kbpd

Seaway Pipeline Acquisition & Reversal • $1.2B purchase of 50% interest from

ConocoPhillips• $0.1B reversal and lateral to ECHO Terminal in

Houston completed Q2 2012• $0.1B capacity expansion completed in Q1 2013• 50/50 joint venture with Enterprise Products

Partners, L.P.

Seaway Pipeline Twin & Lateral • $1.2B capital project• In service: Q4 2014• Long term commercial agreements

(5 – 20 year terms)• Initial capacity: 450 kbpd, expandable to 600 kbpd

Market Access: Western US Gulf Coast Access

Market Access: Eastern AccessLine 9A Reversal • Reversal to access refineries in Ontario• Capacity: 240 kbpd• In service: 2013Line 9B Reversal • $0.7B capital project• Reversal to access refineries in Ontario

and Quebec• Capacity: 240 kbpd• In service: Q4 2015Line 5 Expansion • Capacity: 50 kbpd into Sarnia• In service: 2013Spearhead North Expansion • Capacity: 105 kbpd• In service: 2013Line 6B Replacement • Capacity: Increase of 260 kbpd into Sarnia

(Total line capacity of 500kbpd)• In service: 2014Toledo • Capacity: 80 kbpd• In Service: 2013

Investment Community Presentation January 2017

31

Market Access: Light Oil Market Access

Still need an update

Associated Mainline Expansions⎯ Canadian Mainline System Terminal Flexibility

and Connectivity ⎯ Southern Access Expansion

⎯ 560 kbpd to 950 kbpd: In service Q3 2015 ⎯ 950 kbpd to 1,200 kbpd: In service early 2019

Line 9 Capacity Expansion ⎯ $0.1B capital project⎯ Capacity: + 60 kbpd⎯ In service: Q4 2015

Line 6B Expansion (Pump stations and upgrades) ⎯ $0.3B capital project⎯ Capacity: +70 kbpd⎯ In service: 1H 2016

Southern Access Extension ⎯ $0.6B capital project (Enbridge cost)⎯ Capacity: 300 kbpd⎯ In service: December 2015⎯ Marathon named anchor shipper and equity partner, will fund 35%

of the project ($0.3B)

Line 62 Twin (Line 78 Chicago Connectivity)(36” pipeline from Flanagan to Griffith) ⎯ $0.5B capital project⎯ Capacity: 570 kbpd⎯ In service: Q4 2015

Market Access: Light Oil Market Access

Investment Community Presentation January 2017

32

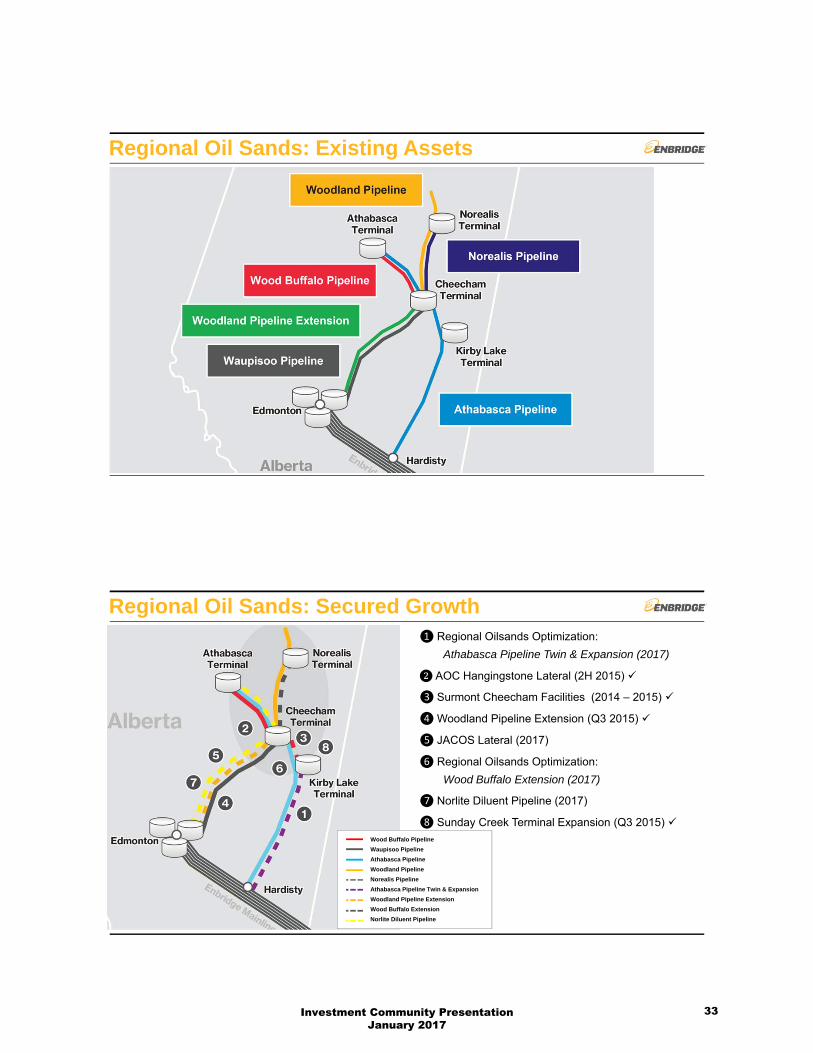

Regional Oil Sands: Existing Assets

❶ Regional Oilsands Optimization:

Athabasca Pipeline Twin & Expansion (2017)

❷ AOC Hangingstone Lateral (2H 2015)

❸ Surmont Cheecham Facilities (2014 – 2015)

❹ Woodland Pipeline Extension (Q3 2015)

❺ JACOS Lateral (2017)

❻ Regional Oilsands Optimization:

Wood Buffalo Extension (2017)

❼ Norlite Diluent Pipeline (2017)

❽ Sunday Creek Terminal Expansion (Q3 2015)

Regional Oil Sands: Secured Growth

Wood Buffalo Pipeline

Waupisoo Pipeline

Athabasca Pipeline

Woodland Pipeline

Norealis Pipeline

Athabasca Pipeline Twin & Expansion

Woodland Pipeline Extension

Wood Buffalo Extension

Norlite Diluent Pipeline

Investment Community Presentation January 2017

33

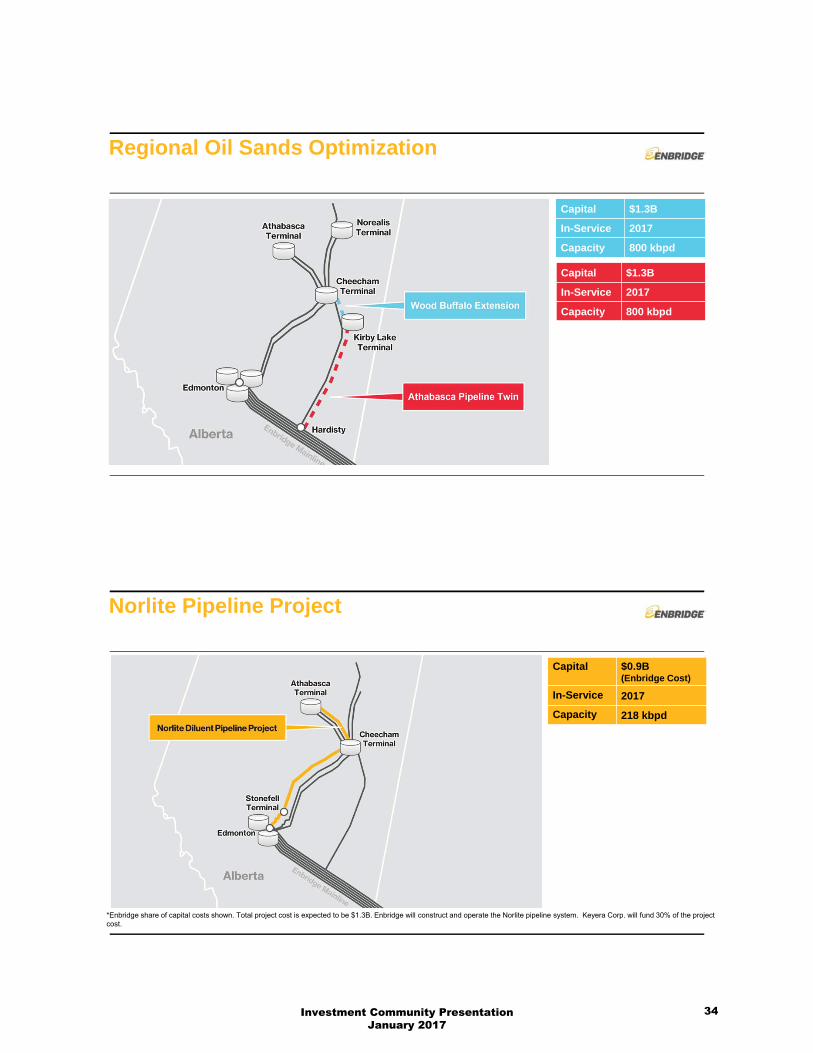

Regional Oil Sands Optimization

Capital $1.3B

In-Service 2017

Capacity 800 kbpd

Capital $1.3B

In-Service 2017

Capacity 800 kbpd

Norlite Pipeline Project

Capital $0.9B(Enbridge Cost)

In-Service 2017

Capacity 218 kbpd

*Enbridge share of capital costs shown. Total project cost is expected to be $1.3B. Enbridge will construct and operate the Norlite pipeline system. Keyera Corp. will fund 30% of the project cost.

Investment Community Presentation January 2017

34

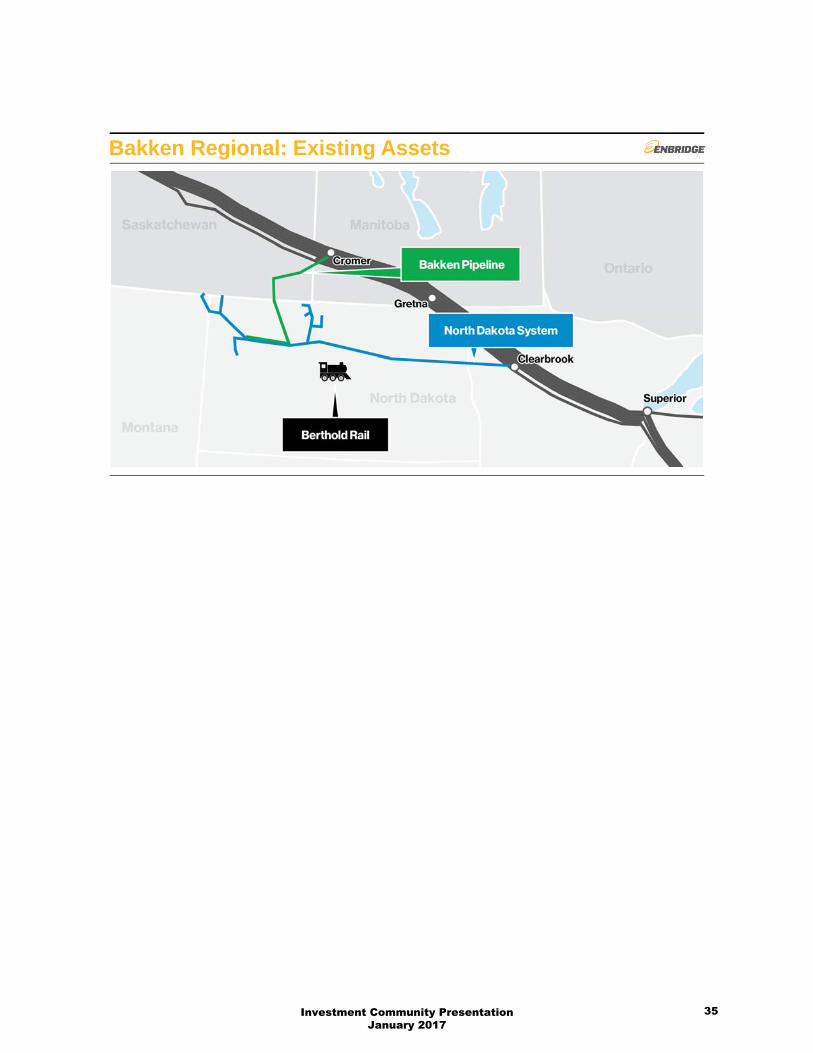

Bakken Regional: Existing Assets

*

Investment Community Presentation January 2017

35

Acquired Interest in Bakken Pipeline SystemSystem extends from the Bakken to USGC

Project Details

Assets:Bakken Pipeline System consists of Dakota Access Pipeline (DAPL) and Energy Transfer Crude Oil Pipeline (ETCO)

Capital: $1.5B

In-Service: 1H 2017

Capacity: ~470kbpd expandable to 570kbpd

Effective

Ownership: 27.6%

Expected Close: TBD

EEP MPC ETP SXL

Enbridge/Marathon Joint Venture

Bakken Holdings Company

Bakken Pipeline Investments

PSX

DAPL ETCO

75% 25% 60% 40%

49% 51%

75% 75%

25% 25%

PSX

Bakken Pipeline System Acquisition anticipated to close 2H 2016

Strategic Fit

• Offers customers competitive tolls between the Bakken and USGC

• Joint toll opportunity with Enbridge mainline

• Highly contracted: secured by long-term take-or-pay commitments

• High credit quality counterparties: >90% investment grade

• Expansion opportunities

Project Details

Capital: US $1.5B

In-Service: 1H 2017

Capacity: ~470 kbpd expandable to 570 kbpd

Effective

Ownership: 27.6%

Expected Close: TBD

Investment Community Presentation January 2017

36

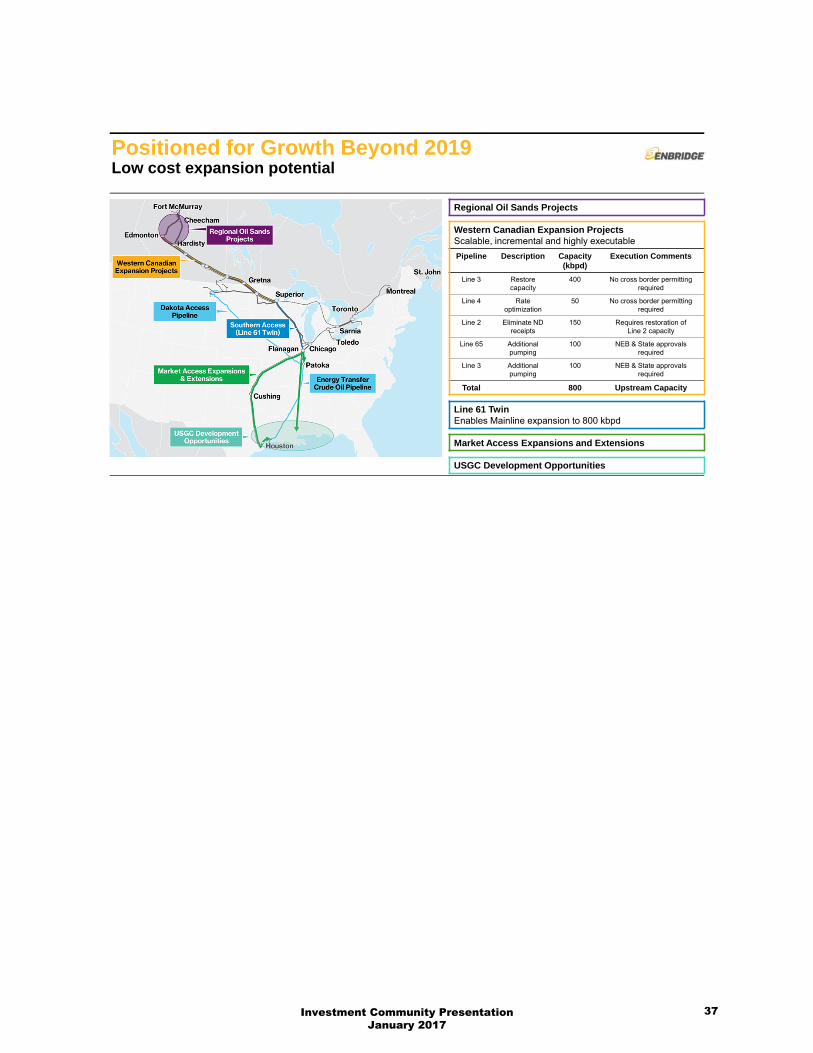

Regional Oil Sands Projects

Western Canadian Expansion ProjectsScalable, incremental and highly executable

Pipeline Description Capacity (kbpd)

Execution Comments

Line 3 Restore capacity

400 No cross border permitting required

Line 4 Rate optimization

50 No cross border permitting required

Line 2 Eliminate ND receipts

150 Requires restoration of Line 2 capacity

Line 65 Additionalpumping

100 NEB & State approvals required

Line 3 Additionalpumping

100 NEB & State approvals required

Total 800 Upstream Capacity

Line 61 TwinEnables Mainline expansion to 800 kbpd

Market Access Expansions and Extensions

USGC Development Opportunities

Positioned for Growth Beyond 2019Low cost expansion potential

Investment Community Presentation January 2017

37

Positioning for Growth Beyond 2019: Line 61 Twin

• Western Canadian Expansion will create a bottleneck at Superior

• Line 61 Twin relieves bottleneck and positions for market access growth

• Coordinating early development activities

Project Details

Scope Up to 42” twin of existing Line 61

Capital $3.5B - $4B

In-Service Date

TBD

Capacity Enables full Mainline expansion by 800 kbpd

Positioning for Growth Beyond 2019: Market Access

• Participation in ETCO can provide full path solution for Canadian producers to eastern USGC

• Positioned for a range of expansions and opportunities‒ Seaway/Flanagan South

‒ Southern Access Extension

‒ Eastern Gulf Coast Access

• Stable, competitive toll outlook

• Strong USGC market provides attractive netbacks

Investment Community Presentation January 2017

38

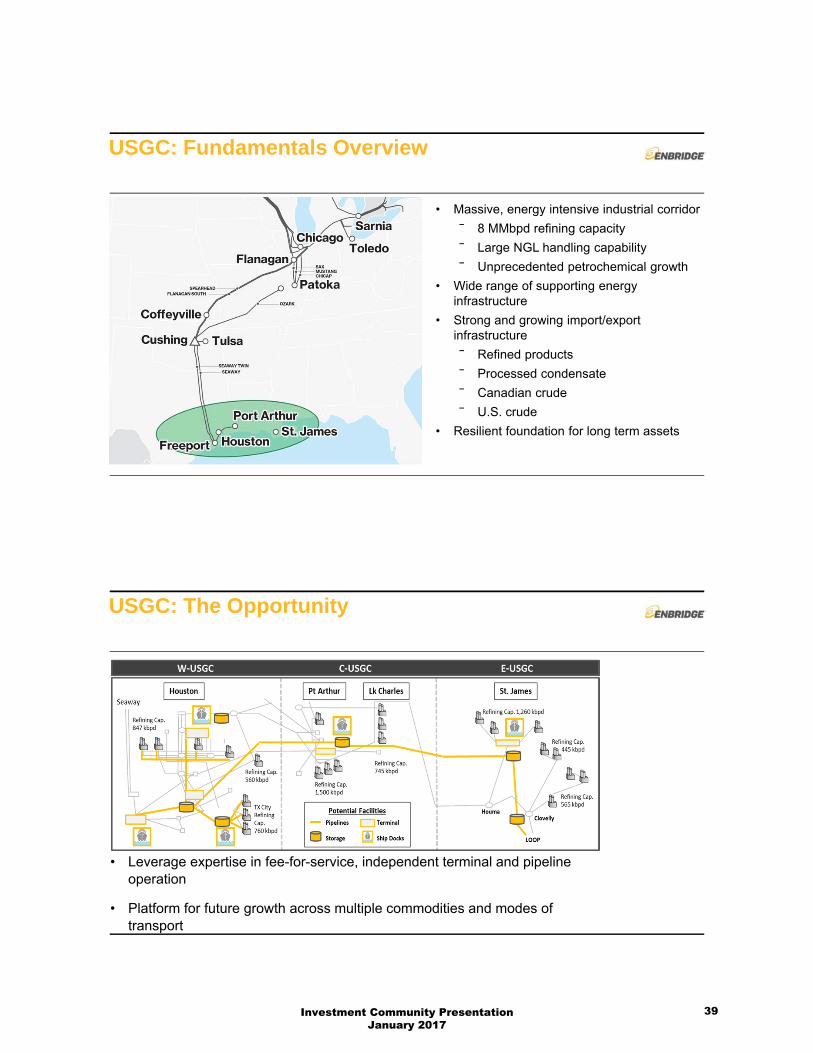

USGC: Fundamentals Overview

• Massive, energy intensive industrial corridor

⎯ 8 MMbpd refining capacity

⎯ Large NGL handling capability

⎯ Unprecedented petrochemical growth

• Wide range of supporting energy infrastructure

• Strong and growing import/export infrastructure

⎯ Refined products

⎯ Processed condensate

⎯ Canadian crude

⎯ U.S. crude

• Resilient foundation for long term assets

USGC: The Opportunity

• Leverage expertise in fee-for-service, independent terminal and pipeline operation

• Platform for future growth across multiple commodities and modes of transport

Investment Community Presentation January 2017

39

Investment Community Presentation January 2017

40

Gas Pipelines& Processing

Investment Community PresentationJanuary 2017

41

OverviewCurrent Position

• Strong regional positions

• Highly contracted

• Industry leading operations and integrity performance

Strategic Objectives

• Grow current footprint

• Build optionality

• Establish demand pull positions

Canadian Midstream

Alliance

US Gathering & Processing

Offshore

Aux Sable

Vector

Investment Community Presentation January 2017

42

Natural Gas Demand Growth

Source: IEA 2014 World Energy Outlook; ENB Gas & NGL Fundamentals

0

100

200

300

400

500

2012 2020 2025

Asia & Asia Oceania Middle East & Africa E. Europe/Eurasia

Europe Americas

Global natural gas demand (Bcf/d)

North American natural gas demand(Bcf/d)

0

20

40

60

80

100

120

140

2014 2025

Sources of demand Bcf/d

Residential/Commercial +1

Industrial +8

Coal/ Nuclear Retirements

+7

Power Demand +5

LNG +13

Mexico Exports +2

Natural Gas Supply Growth

0

2

4

6

8

10

12

14

16

18

20

2014 2016 2018 2020 2022 2024

Horn River Duvernay Montney Conventional

Source: Wood Mackenzie; ENB Gas & NGL Fundamentals

40

50

60

70

80

90

100

110

120

2014 2016 2018 2020 2022 2024

U.S. gas production(Bcf/d)

WCSB gas production(Bcf/d)

Investment Community Presentation January 2017

43

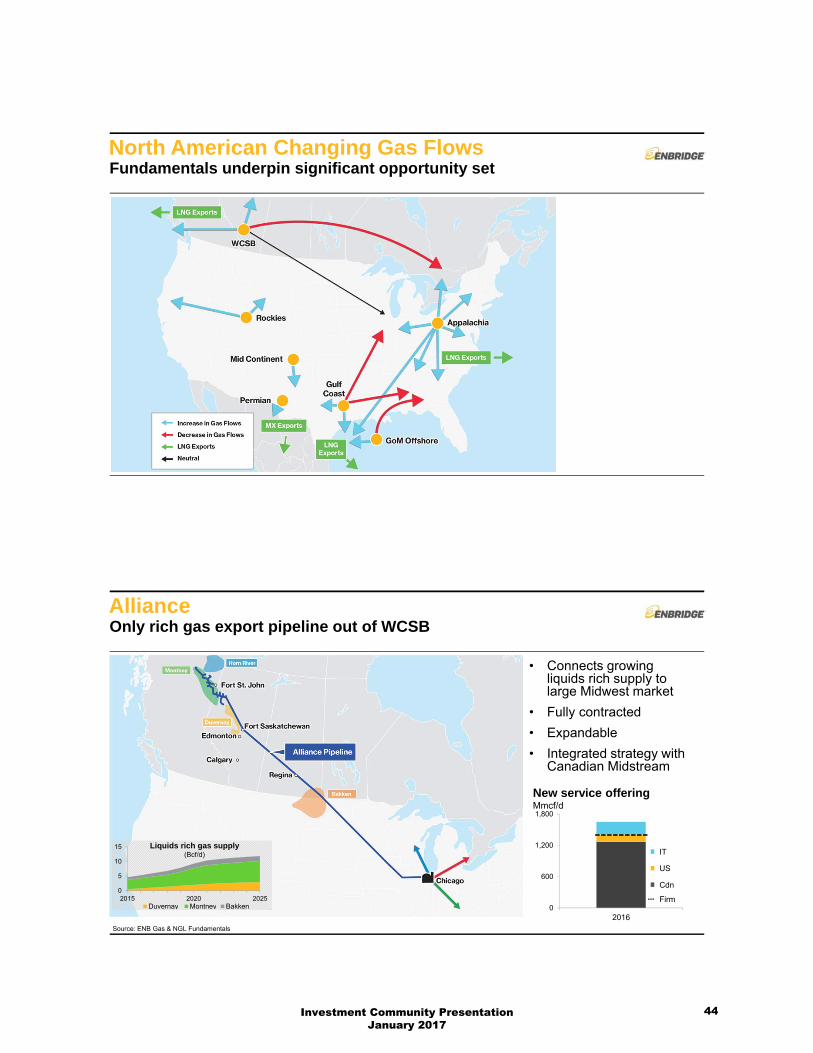

North American Changing Gas FlowsFundamentals underpin significant opportunity set

AllianceOnly rich gas export pipeline out of WCSB

• Connects growing liquids rich supply to large Midwest market

• Fully contracted

• Expandable

• Integrated strategy with Canadian Midstream

0

600

1,200

1,800

2016

New service offeringMmcf/d

IT

US

Cdn

Firm0

5

10

15

2015 2020 2025Duvernay Montney Bakken

Liquids rich gas supply(Bcf/d)

Source: ENB Gas & NGL Fundamentals

Investment Community Presentation January 2017

44

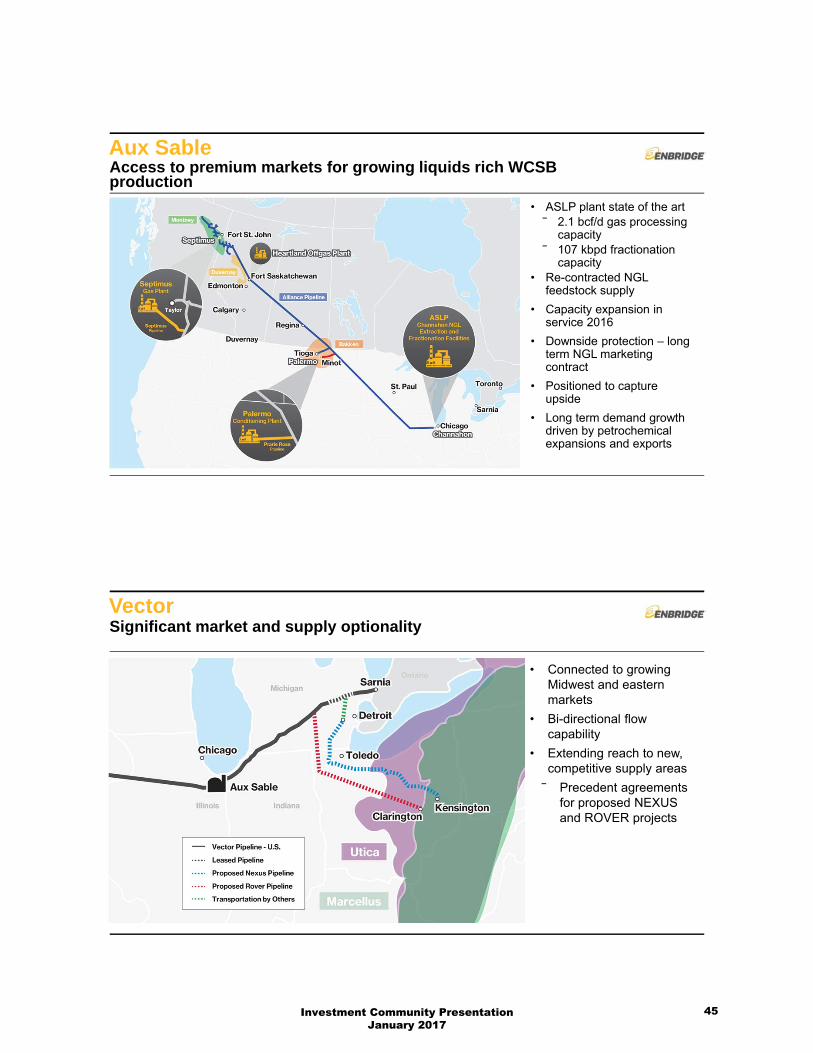

Aux SableAccess to premium markets for growing liquids rich WCSB production

• ASLP plant state of the art⎯ 2.1 bcf/d gas processing

capacity⎯ 107 kbpd fractionation

capacity• Re-contracted NGL

feedstock supply

• Capacity expansion in service 2016

• Downside protection – long term NGL marketing contract

• Positioned to capture upside

• Long term demand growth driven by petrochemical expansions and exports

VectorSignificant market and supply optionality

• Connected to growing Midwest and eastern markets

• Bi-directional flow capability

• Extending reach to new, competitive supply areas

⎯ Precedent agreements for proposed NEXUS and ROVER projects

Investment Community Presentation January 2017

45

US Gathering & ProcessingAsset optimization provides foundation for future growth

• Realign cost structure

• Rationalize portfolio

• Evolve commercial constructs to more fee based

• Extend reach in prolific and economic basins

• Expand service offerings

Opportunities in Growing Supply BasinsSignificant pipeline opportunities as growing supply expected to outpace regional demand

0

10

20

30

40

Demand Supply Demand Supply

Northeast Gas Supply & Regional Demand (Bcf/d)

2015 2025

MWMW

MA

MANE

NE

Utica Marcellus

Investment Community Presentation January 2017

46

OffshoreProven execution capabilities provide competitive advantage

• Robust long term outlook for deep water developments

• Commercial constructs aligned with reliable business model

• Recent project selections:⎯ Heidelberg⎯ Stampede⎯ Under negotiation: $0.6B

development

Canadian MidstreamFoundational assets provide optionality for large-scale development

• Develop customer gathering, processing and market access

• Strong producer interest in new 300 kbpd NGL pipeline & fractionator

• Limited Alberta C2/C3 market provides opportunities for NGL aggregation and export

Investment Community Presentation January 2017

47

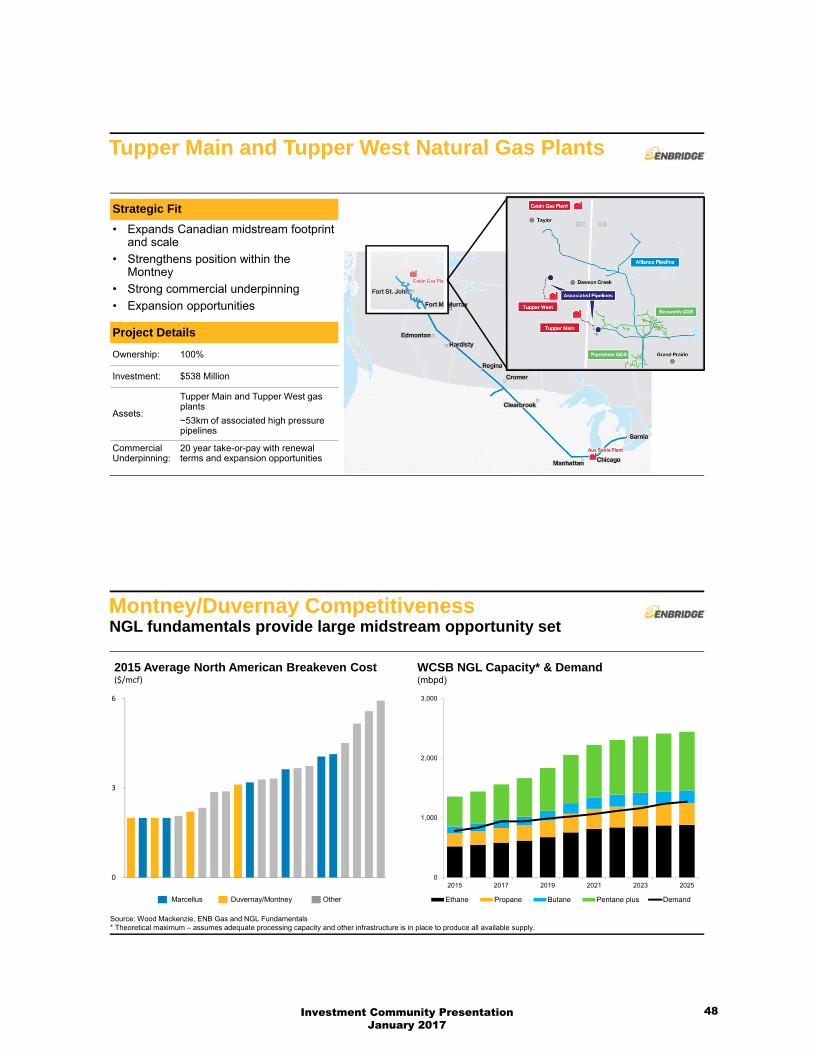

Tupper Main and Tupper West Natural Gas Plants

Strategic Fit

• Expands Canadian midstream footprint and scale

• Strengthens position within the Montney

• Strong commercial underpinning

• Expansion opportunities

Project Details

Ownership: 100%

Investment: $538 Million

Assets:

Tupper Main and Tupper West gas plants

~53km of associated high pressure pipelines

Commercial Underpinning:

20 year take-or-pay with renewal terms and expansion opportunities

Montney/Duvernay CompetitivenessNGL fundamentals provide large midstream opportunity set

0

3

6

Marcellus

2015 Average North American Breakeven Cost($/mcf)

0

1,000

2,000

3,000

2015 2017 2019 2021 2023 2025

Ethane Propane Butane Pentane plus Demand

WCSB NGL Capacity* & Demand(mbpd)

Duvernay/Montney Other

Source: Wood Mackenzie, ENB Gas and NGL Fundamentals* Theoretical maximum – assumes adequate processing capacity and other infrastructure is in place to produce all available supply.

Investment Community Presentation January 2017

48

Gas Distribution

Investment Community Presentation January 2017

49

Gas Distribution FootprintLargest gas distribution franchise in Canada;Serving over 2 million customers

Strategic PositioningStable low-risk business delivers strong risk-adjusted returns and foundation for growth

0%

6%

12%

2008 2009 2010 2011 2012 2013 2014 2015

Formula ROE ROE Premium

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014 2015

• Stable, predictable earnings and cash flow

• Low risk commercial model⎯ Regulated return

⎯ No direct commodity exposure

• $3 billion capital investment approved under current model⎯ Largest Canadian franchise

⎯ Strong population growth

• Foundational asset base supports broader energy strategy

Historical ROE Historical Rate Base$Billion

Investment Community Presentation January 2017

50

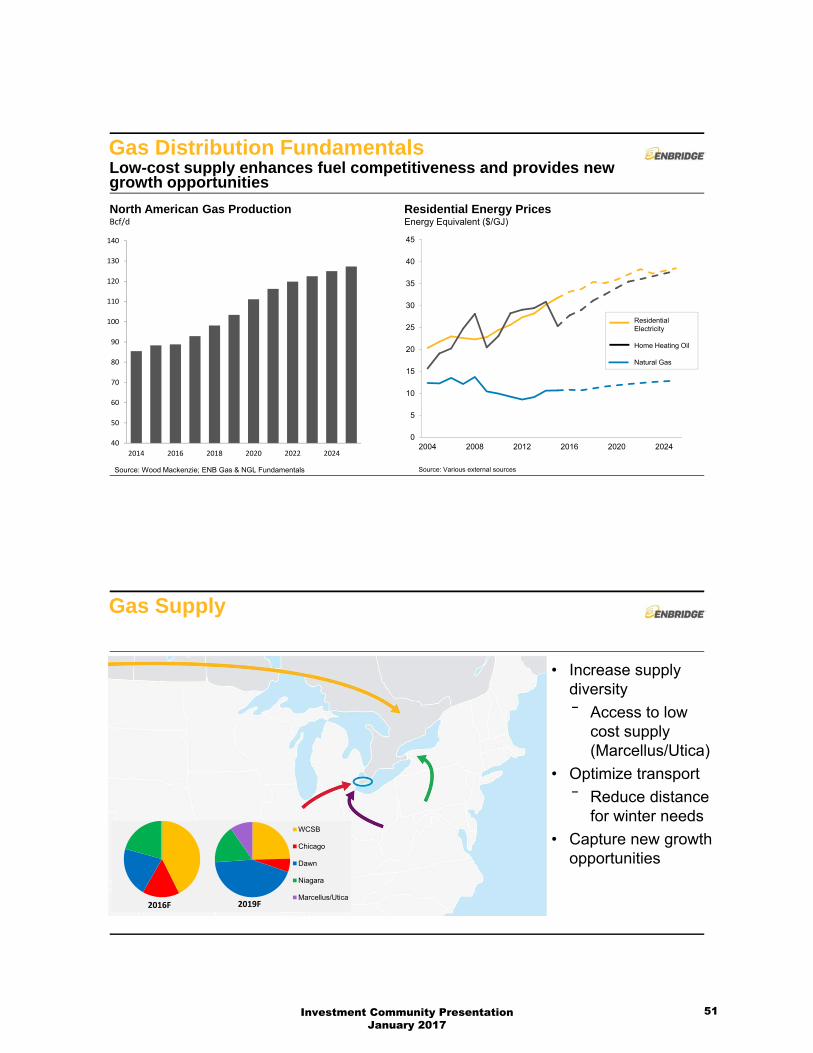

Gas Distribution FundamentalsLow-cost supply enhances fuel competitiveness and provides new growth opportunities

0

5

10

15

20

25

30

35

40

45

2004 2008 2012 2016 2020 202440

50

60

70

80

90

100

110

120

130

140

2014 2016 2018 2020 2022 2024

Source: Wood Mackenzie; ENB Gas & NGL Fundamentals Source: Various external sources

Residential Electricity

Home Heating Oil

Natural Gas

North American Gas ProductionBcf/d

Residential Energy PricesEnergy Equivalent ($/GJ)

Gas Supply

WCSB

Chicago

Dawn

Niagara

Marcellus/Utica2019F2016F

• Increase supply diversity

⎯ Access to low cost supply (Marcellus/Utica)

• Optimize transport

⎯ Reduce distance for winter needs

• Capture new growth opportunities

Investment Community Presentation January 2017

51

Custom Incentive RegulationInnovative model provides strong risk-adjusted returns with $3B approved capital investment

0%

2%

4%

6%

8%

10%

12%

2015 2016 2018

ROE Premium

Formula ROE

Board Approved Forecast

Current ROE Forecasts2015 - 2018• Annual ROE reset

protects against rising interest rates

• Upside sharing

• $3B approved capital investment required to meet customer needs

• No direct commodity exposure

Core Customer Growth

0

400

800

1,200

201

4

201

5

201

6

201

7

201

8

201

9

1.5

2.0

2.5

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

ForecastActual

• One of the fastest growing natural gas distribution companies in North America

• Consistently add 35k+ customers per year

• Ontario government supports rural community expansion

Average Number of Customers$ Million

Forecast Capital$ Million

Investment Community Presentation January 2017

52

System Renewal and Expansion: GTA ProjectLargest single capital investment in Gas Distribution history

• Increases capacity and reliability in the GTA and downtown Toronto

• Leverages additional supply and basin optionality

• Serves growing customer base through additional infrastructure

Project Details

Scope: Eastern Segment:23 km of 36” pipeWestern Segment:27 km of 42” pipe

In-Service Date: Q1 2016

Total Cost

$900M

Gas Storage OpportunitiesStorage investment reduces gas price volatility

• Storage is fundamental to support reliable, low cost supply

• Infrastructure renewal opportunities

⎯ Coincides with changing supply chain patterns

• Opportunity to position storage investments for long term growth

Investment Community Presentation January 2017

53

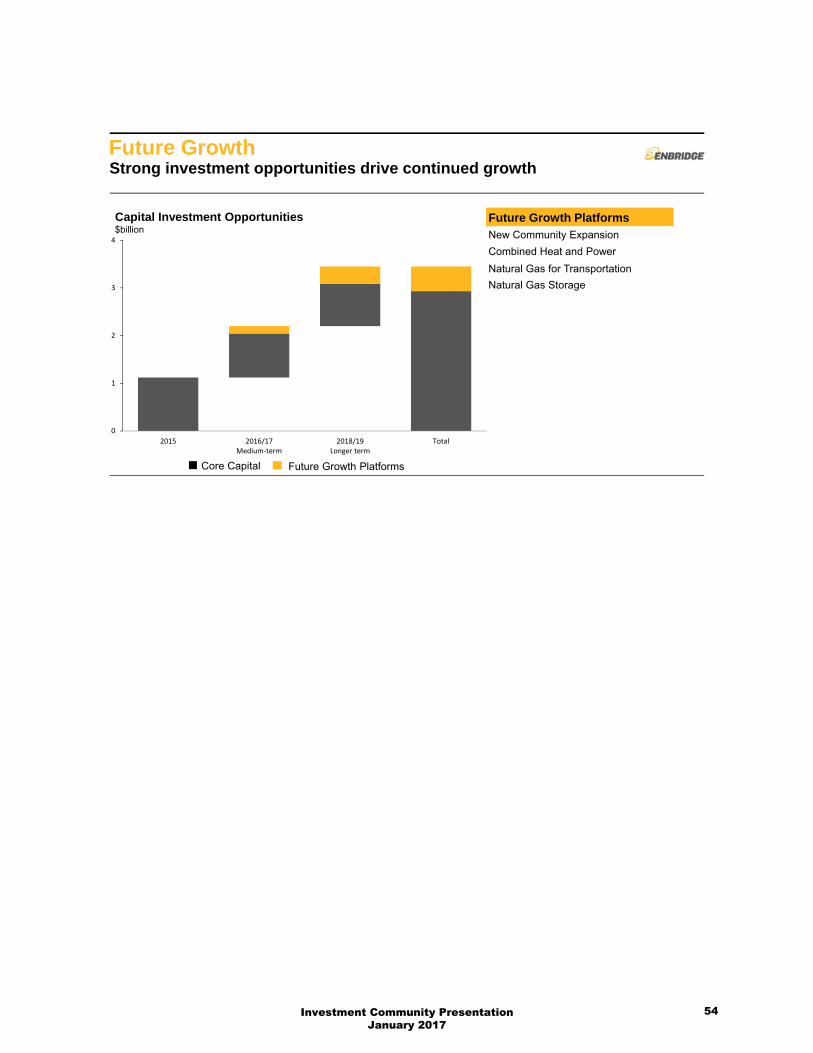

Future GrowthStrong investment opportunities drive continued growth

0

1

2

3

4

2015 2016/17Medium‐term

2018/19Longer term

Total

Future Growth PlatformsNew Community Expansion

Combined Heat and Power

Natural Gas for Transportation

Natural Gas Storage

Core Capital Future Growth Platforms

Capital Investment Opportunities$billion

Investment Community Presentation January 2017

54

Power, International and Energy Services

Investment Community PresentationJanuary 2017

55

Power Generation & Transmission Footprint

2010 2015 2019e

2010 2015 2019e

1,776

Net Generating Capacity MWs

Total Investment $ billion

4.6

0

50

100

2014-20 2021-25

Power FundamentalsAttractive fundamentals support accelerated growth

0

250

500

North America Europe

Gas Other Renewables

Forecast Generation Growth - 20251

GWsNorth American Transmission Investment3

US$ billions

1Source: International Energy Agency World Energy Outlook 20142Source: Energy International Administration (U.S.); Siemens (Europe). Europe combines data for UK and Germany.3Source: International Energy Agency

Investment Community Presentation January 2017

56

-

500

1,000

1,500

Current PositioningOne of Canada’s largest renewable power producers; opportunity for growth in U.S.

-

4,000

8,000

12,000

ENB

ENB

Top Wind & Solar GeneratorsCanada (MWs)

…

Top Wind & Solar GeneratorsNorth America (MWs)

Accelerated GrowthIntegrated model will help extend and accelerate growth

Operating Model Primarily outsourced Operator

Project Development External Internal & External

Portfolio Mix Primarily wind & solar Wind, solar, hydro, gas fired, transmission

Geographic Location North America North America & Europe

Investment Community Presentation January 2017

57

051015202530

2020 2014

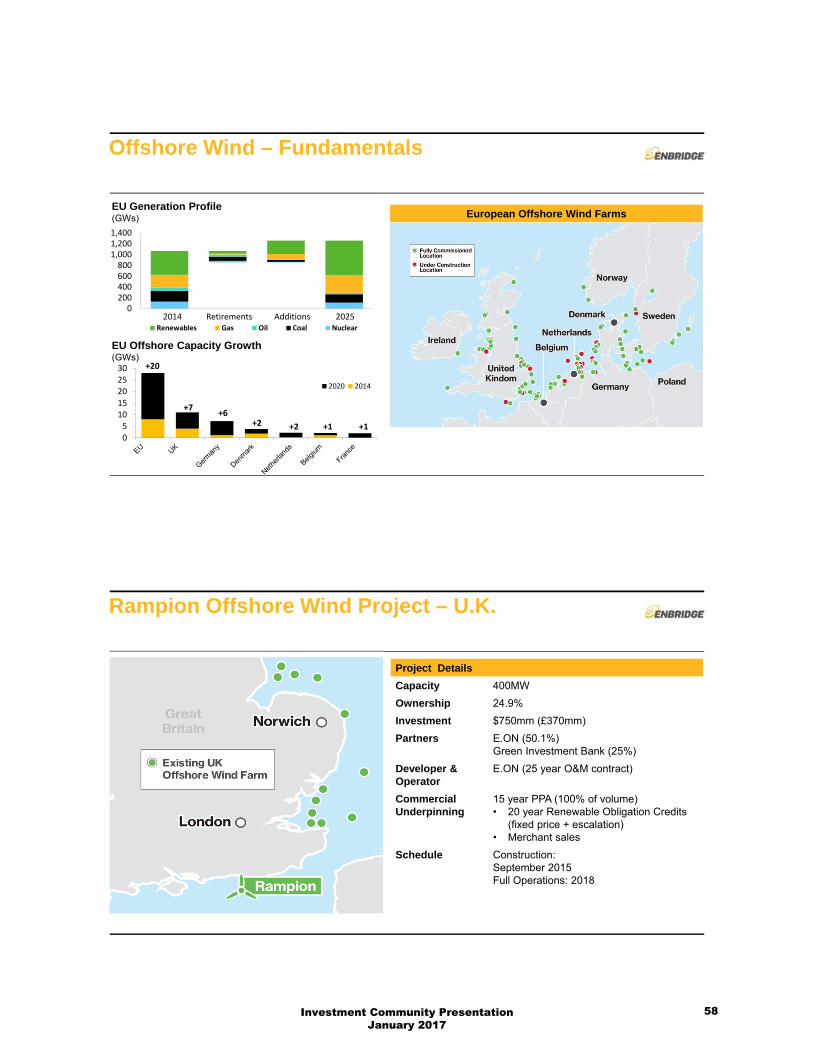

Offshore Wind – Fundamentals

EU Offshore Capacity Growth(GWs)

0200400600800

1,0001,2001,400

Renewables Gas Oil Coal Nuclear

EU Generation Profile(GWs)

2014 2025Retirements Additions

European Offshore Wind Farms

+20

+7+6

+2 +2 +1 +1

Rampion Offshore Wind Project – U.K.

Project Details

Capacity 400MW

Ownership 24.9%

Investment $750mm (£370mm)

Partners E.ON (50.1%)Green Investment Bank (25%)

Developer & Operator

E.ON (25 year O&M contract)

Commercial Underpinning

15 year PPA (100% of volume) • 20 year Renewable Obligation Credits

(fixed price + escalation)• Merchant sales

Schedule Construction:September 2015Full Operations: 2018

Investment Community Presentation January 2017

58

Investment in Offshore Wind DeveloperÉolien Maritime France (“EMF”)

Project MWAnticipated

ConstructionExpected

ISD

Eoliennes Offshore des HautesFalaises

498 2017 2020

Eoliennes Offshore du Calvados 450 2018 2021

Parc du Banc de Guerande 480 2019 2022

• Investment Summary:‒ 50% co-development

‒ 3 advanced stage projects (1,400 MWs)

‒ 20 year fixed price PPA (offtake: EDF)

‒ Advanced permitting, capital estimate

• Value Proposition:‒ Large investment opportunity ($4.5B)

‒ Individual project sanctioning

‒ Attractive returns

‒ Strong partner

New Creek Wind Project

Project Details

Capacity 102MW

Ownership 100%

Investment $0.1 billion

Developer EverPower Wind Holdings

Operator Gamesa/Enbridge

Commercial Underpinning

12 year fixed price agreement Merchant sales

Schedule Construction: March 2016Full Operations: December 2016

Investment Community Presentation January 2017

59

Chapman Ranch Wind Project

Project DetailsCapacity 249 MW

Ownership 100%

Investment $0.4 billion

Developer Apex Clean Energy

Operator Acciona/Enbridge

Commercial Underpinning 12 year fixed volume agreement

Schedule Construction: September 2016Full Operations: Q3 2017

Disciplined Investment CriteriaPower investments align with reliable business model

Liquids Projects Power Projects

Strong market fundamentals Attractive low risk returns Low capital cost risk Strong commercial underpinnings No commodity price risk

Investment Community Presentation January 2017

60

Power Opportunity SetActively pursuing over 2,000 MWs of attractive projects

0

500

1,000

1,500

2,000

2,500

2016Near Term

2017/2018Medium Term

2019Longer Term

Total

Growth Opportunities(MWs)

International Focus

Investment Criteria

Australia

• Stable political environment and hedgeable currency

• Significant infrastructure deficit

Colombia

• Favourable business environment

• Operations history (OCENSA)

Areas of Focus

Investment Community Presentation January 2017

61

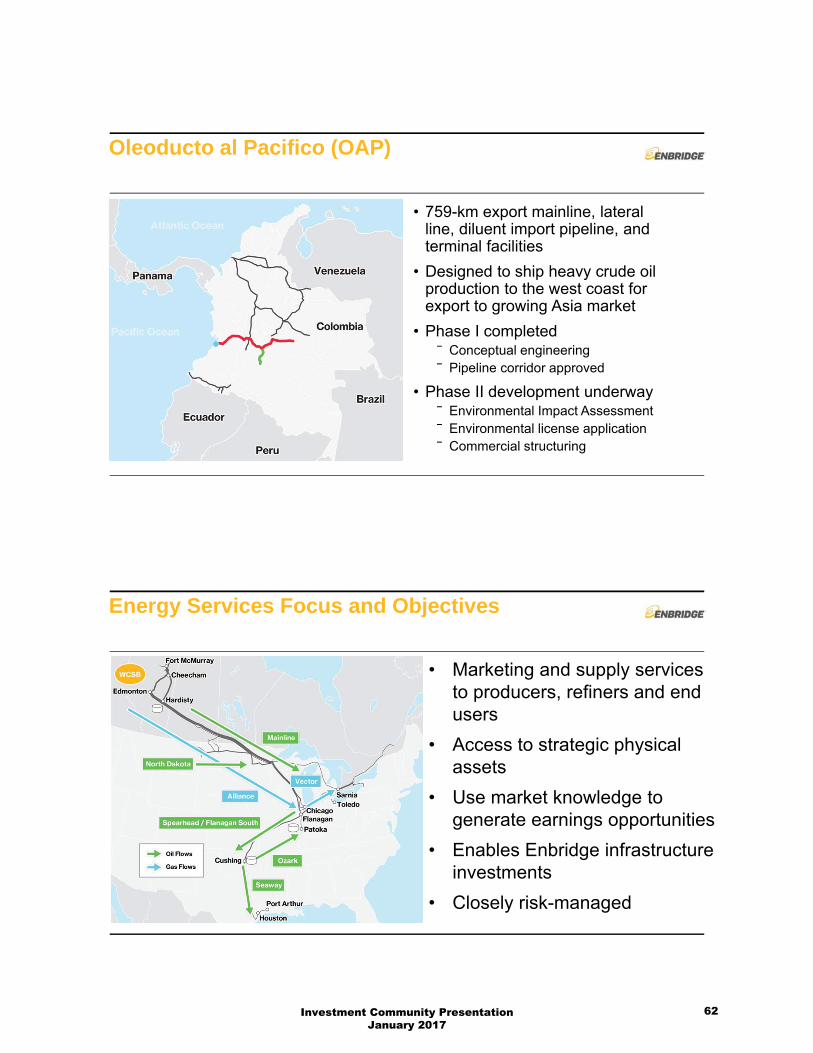

Oleoducto al Pacifico (OAP)

• 759-km export mainline, lateral line, diluent import pipeline, and terminal facilities

• Designed to ship heavy crude oil production to the west coast for export to growing Asia market

• Phase I completed ⎯ Conceptual engineering⎯ Pipeline corridor approved

• Phase II development underway⎯ Environmental Impact Assessment⎯ Environmental license application⎯ Commercial structuring

Proposed OAP Lateral

Proposed OAP Mainline

Proposed OAP Terminal

Existing Pipelines

Energy Services Focus and Objectives

• Marketing and supply services to producers, refiners and end users

• Access to strategic physical assets

• Use market knowledge to generate earnings opportunities

• Enables Enbridge infrastructure investments

• Closely risk-managed

Investment Community Presentation January 2017

62

Energy Services Business Strategies

A Buy WCS @ Edmonton, (35)Tariffs and TVM (6)

B Sell WCS @ Cushing 44Margin 3

A Buy DOM @ Midland (48)Tariffs and TVM (2)

B Sell DOM @ Longview 52Refinery Supply Margin 2

• Customer focus – fee for service solutions to producers and end users• Support Enbridge assets, profitably• Minimal commodity and basis spread exposure• Use physical assets to generate incremental optimization based earnings

Buy - February

($50)/bbl

Sell - March

$52/bbl

Investment Community Presentation January 2017

63

Investment Community Presentation January 2017

64

Corporate Finance

Investment Community PresentationJanuary 2017

65

Financial Highlights

1Available cash flow from operations (ACFFO), adjusted earnings before interest and taxes (adjusted EBIT) and adjusted earnings are non-GAAP measures. For more information on non-GAAP measures please refer to disclosure in the MD&A. Adjusted EBIT is not presented on a $/share basis.*Incremental impact if Alberta Wildfires had not occurred.

Adjusted EBIT1

$ MillionsACFFO1

$ Millions, except per share amounts

Adjusted Earnings1