36

Investment Evaluation 1 INVESTMENT EVALUATION Professor Tim Thompson Kellogg School of Management

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | khalid-vorse |

| View: | 221 times |

| Download: | 0 times |

Investment Evaluation 1

INVESTMENT EVALUATIONProfessor Tim Thompson

Kellogg School of Management

Investment Evaluation 2

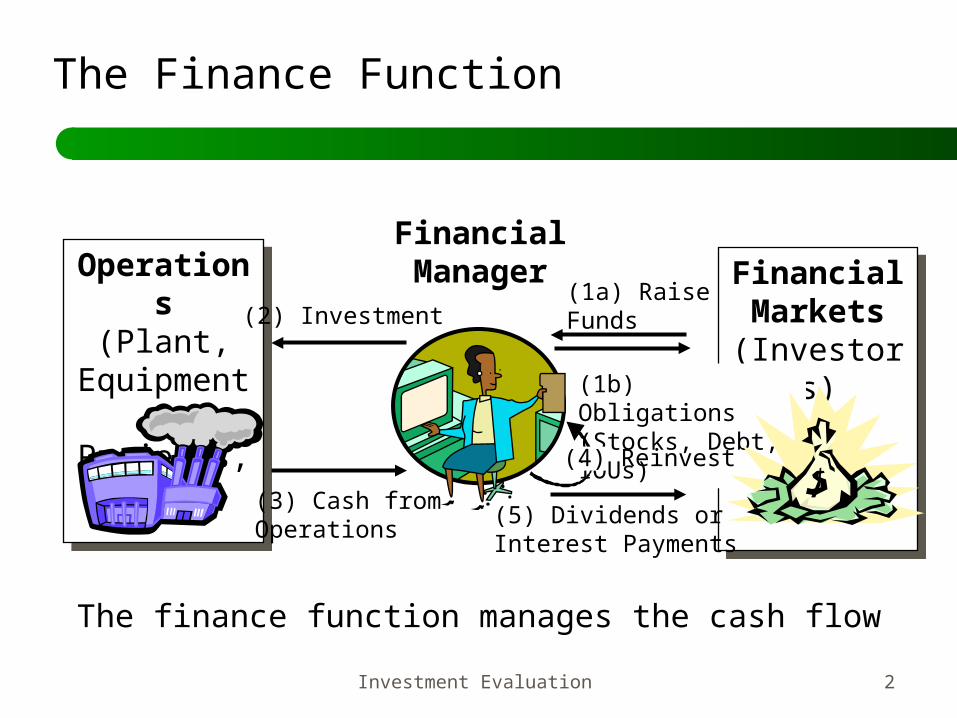

The Finance Function

Financial Markets

(Investors)

Financial Markets

(Investors)

Operations

(Plant, Equipment, Projects,

etc.)

Operations

(Plant, Equipment, Projects,

etc.)

FinancialManager

(1a) RaiseFunds

(1b) Obligations(Stocks, Debt, IOUs)

(2) Investment

(3) Cash fromOperations

(5) Dividends orInterest Payments

The finance function manages the cash flow

(4) Reinvest

Investment Evaluation 3

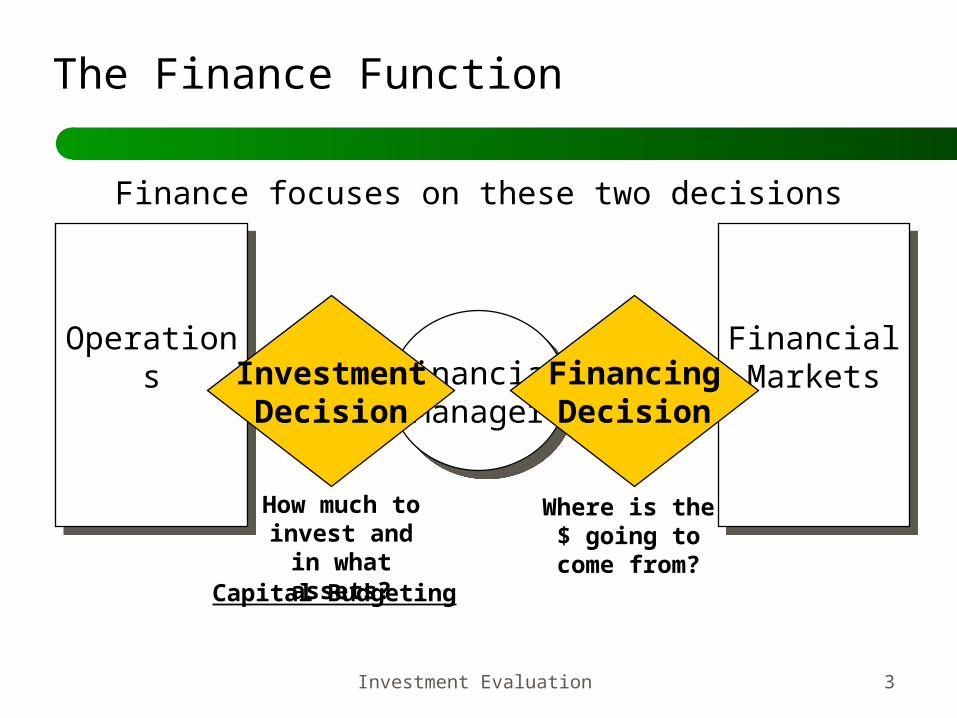

The Finance Function

Financial Markets

Financial Markets

Operations

Operations Financial

ManagerFinancialManager

InvestmentDecision

FinancingDecision

How much to invest and in what assets?

Where is the $ going to

come from?Capital Budgeting

Finance focuses on these two decisions

Investment Evaluation 4

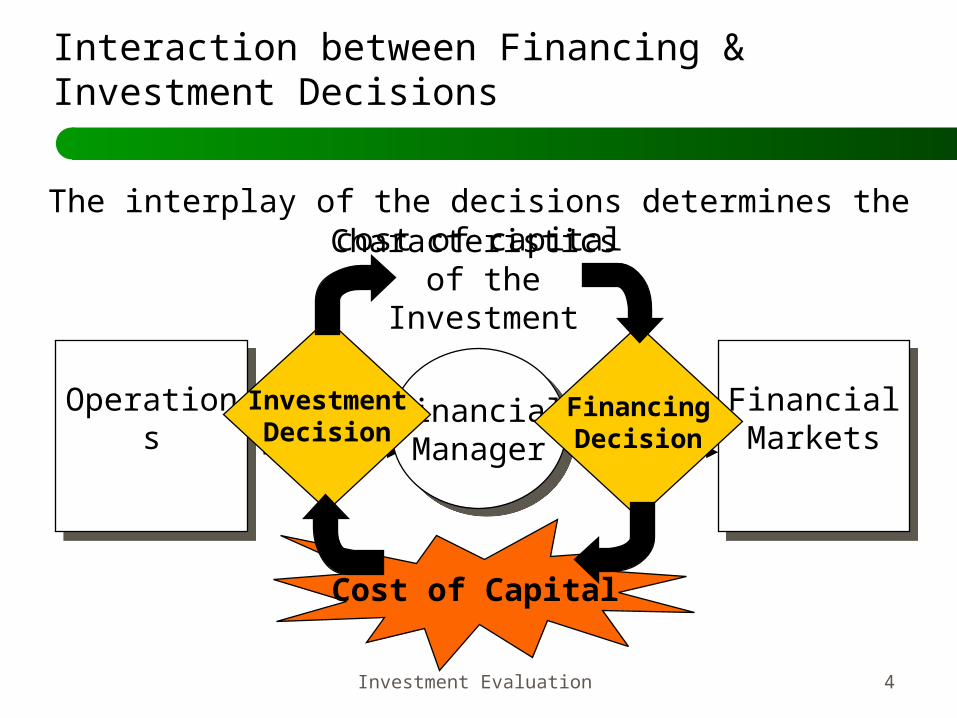

Interaction between Financing & Investment Decisions

Financial Markets

Financial Markets

Operations

Operations

FinancialManagerFinancialManager

InvestmentDecision

FinancingDecision

The interplay of the decisions determines the cost of capital

Cost of Capital

Characteristics of the

Investment

Investment Evaluation 5

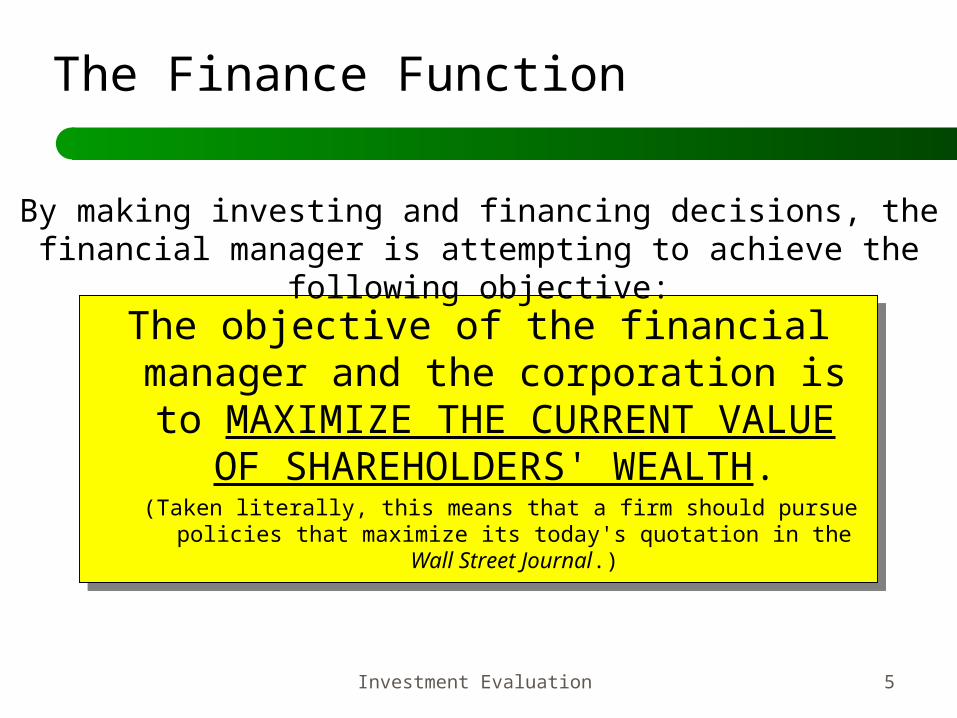

The Finance Function

The objective of the financial manager and the corporation is to MAXIMIZE THE CURRENT VALUE OF

SHAREHOLDERS' WEALTH.(Taken literally, this means that a firm should pursue policies

that maximize its today's quotation in the Wall Street Journal.)

The objective of the financial manager and the corporation is to MAXIMIZE THE CURRENT VALUE OF

SHAREHOLDERS' WEALTH.(Taken literally, this means that a firm should pursue policies

that maximize its today's quotation in the Wall Street Journal.)

By making investing and financing decisions, the financial manager is attempting to achieve the following objective:

Investment Evaluation 6

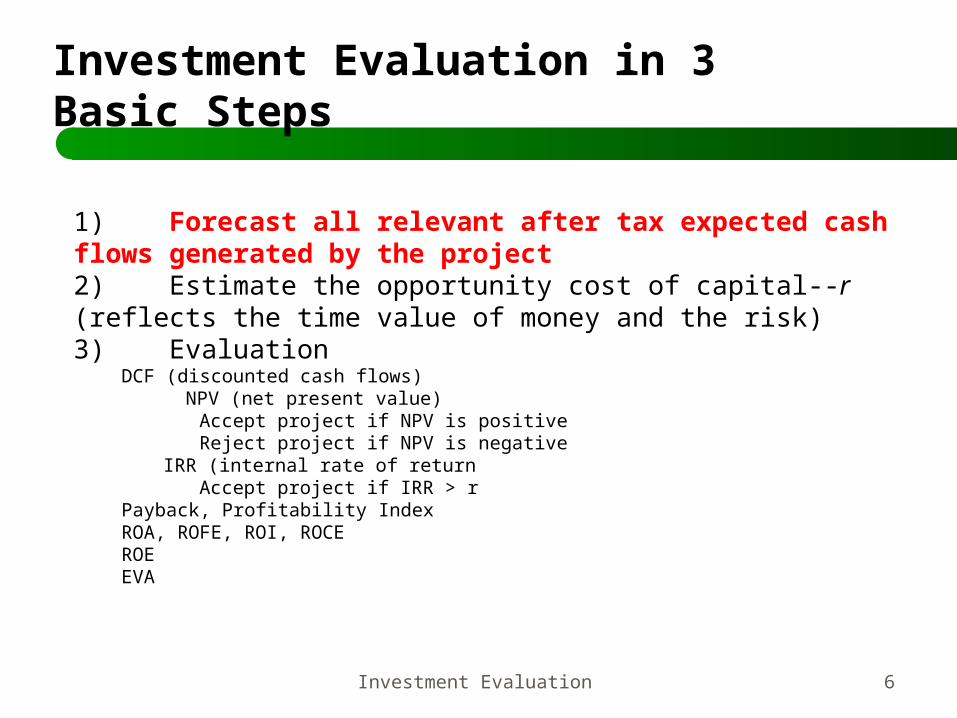

Investment Evaluation in 3 Basic Steps

1) Forecast all relevant after tax expected cash flows generated by the project2) Estimate the opportunity cost of capital--r (reflects the time value of money and the risk)3) Evaluation

DCF (discounted cash flows) NPV (net present value)

Accept project if NPV is positiveReject project if NPV is negative

IRR (internal rate of returnAccept project if IRR > r

Payback, Profitability IndexROA, ROFE, ROI, ROCEROEEVA

Investment Evaluation 7

Forecasting Cash Flows

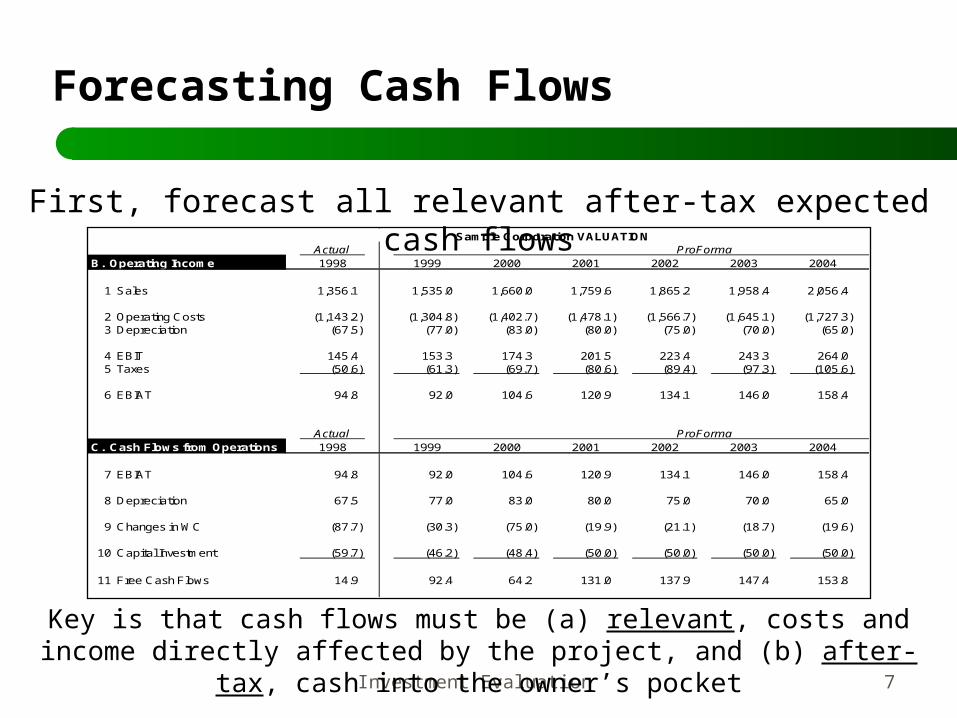

First, forecast all relevant after-tax expected cash flowsActual

B. Operating Income 1998 1999 2000 2001 2002 2003 2004

1 Sales 1,356.1 1,535.0 1,660.0 1,759.6 1,865.2 1,958.4 2,056.4

2 Operating Costs (1,143.2) (1,304.8) (1,402.7) (1,478.1) (1,566.7) (1,645.1) (1,727.3) 3 Depreciation (67.5) (77.0) (83.0) (80.0) (75.0) (70.0) (65.0)

4 EBIT 145.4 153.3 174.3 201.5 223.4 243.3 264.0 5 Taxes (50.6) (61.3) (69.7) (80.6) (89.4) (97.3) (105.6)

6 EBIAT 94.8 92.0 104.6 120.9 134.1 146.0 158.4

ActualC. Cash Flows from Operations 1998 1999 2000 2001 2002 2003 2004

7 EBIAT 94.8 92.0 104.6 120.9 134.1 146.0 158.4

8 Depreciation 67.5 77.0 83.0 80.0 75.0 70.0 65.0

9 Changes in WC (87.7) (30.3) (75.0) (19.9) (21.1) (18.7) (19.6)

10 Capital Investment (59.7) (46.2) (48.4) (50.0) (50.0) (50.0) (50.0)

11 Free Cash Flows 14.9 92.4 64.2 131.0 137.9 147.4 153.8

ProForma

ProForma

Sample Corporation VALUATION

Key is that cash flows must be (a) relevant, costs and income directly affected by the project, and (b) after-tax, cash into the

owner’s pocket

Investment Evaluation 8

Forecasting Cash Flows

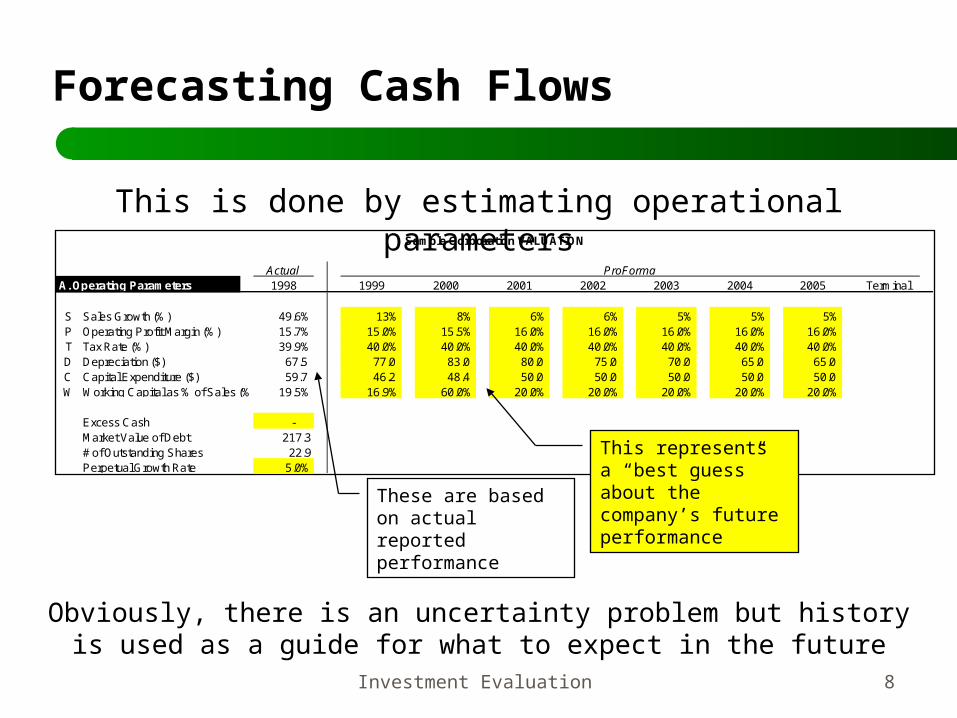

This is done by estimating operational parameters

ActualA. Operating Parameters 1998 1999 2000 2001 2002 2003 2004 2005 Terminal

S Sales Growth (%) 49.6% 13% 8% 6% 6% 5% 5% 5%P Operating Profit Margin (%) 15.7% 15.0% 15.5% 16.0% 16.0% 16.0% 16.0% 16.0%T Tax Rate (%) 39.9% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%D Depreciation ($) 67.5 77.0 83.0 80.0 75.0 70.0 65.0 65.0 C Capital Expenditure ($) 59.7 46.2 48.4 50.0 50.0 50.0 50.0 50.0 W Working Capital as % of Sales (%) 19.5% 16.9% 60.0% 20.0% 20.0% 20.0% 20.0% 20.0%

Excess Cash - Market Value of Debt 217.3# of Outstanding Shares 22.9Perpetual Growth Rate 5.0%

Sample Corporation VALUATION

ProForma

These are based on actual reported performance

This represents a “best guess” about the company’s future performance

Obviously, there is an uncertainty problem but history is used as a guide for what to expect in the future

Investment Evaluation 9

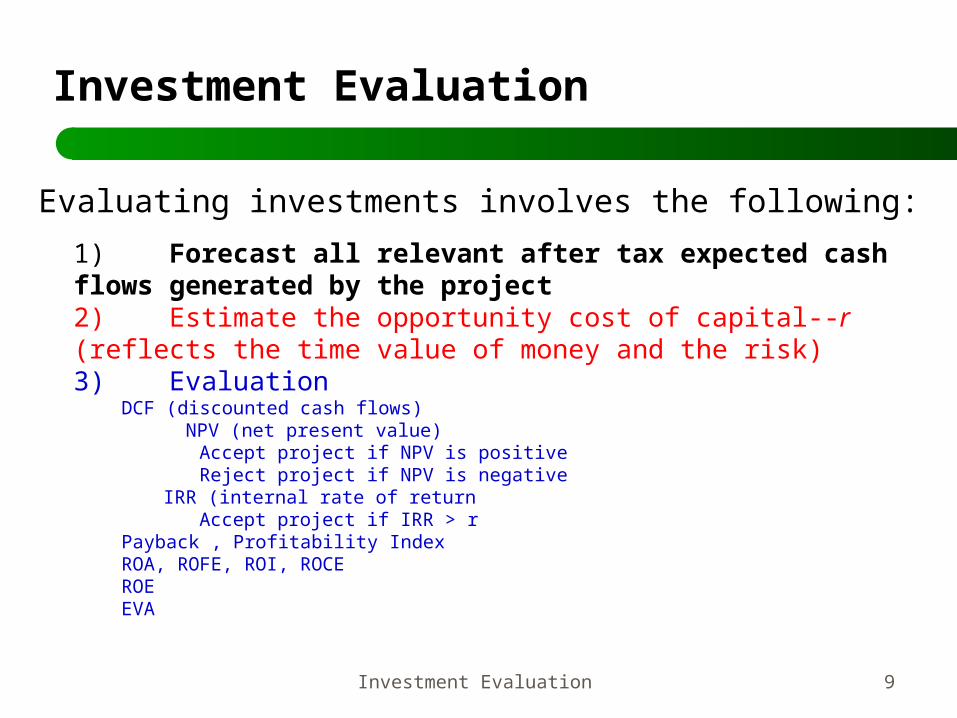

Investment Evaluation

Evaluating investments involves the following:

1) Forecast all relevant after tax expected cash flows generated by the project2) Estimate the opportunity cost of capital--r (reflects the time value of money and the risk)3) Evaluation

DCF (discounted cash flows) NPV (net present value)

Accept project if NPV is positiveReject project if NPV is negative

IRR (internal rate of returnAccept project if IRR > r

Payback , Profitability IndexROA, ROFE, ROI, ROCEROEEVA

Investment Evaluation 10

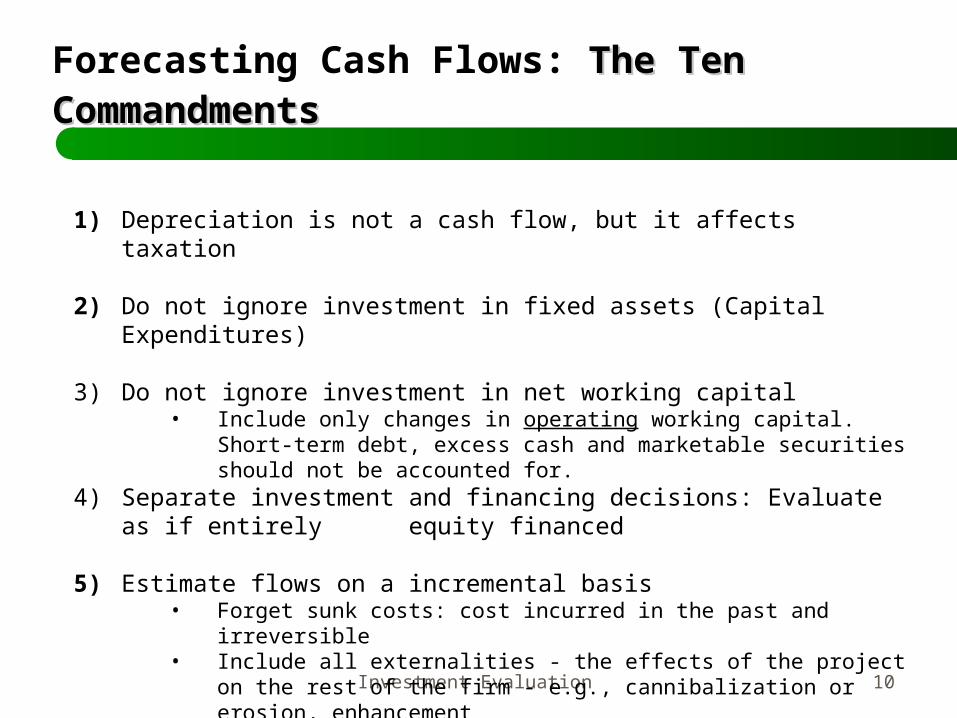

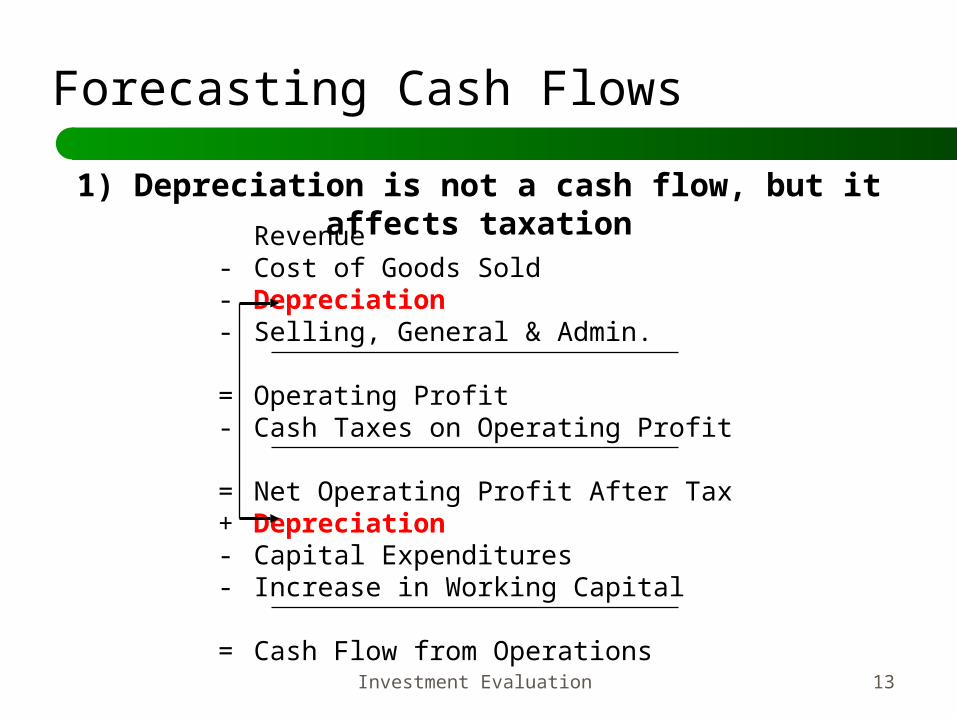

1) Depreciation is not a cash flow, but it affects taxation

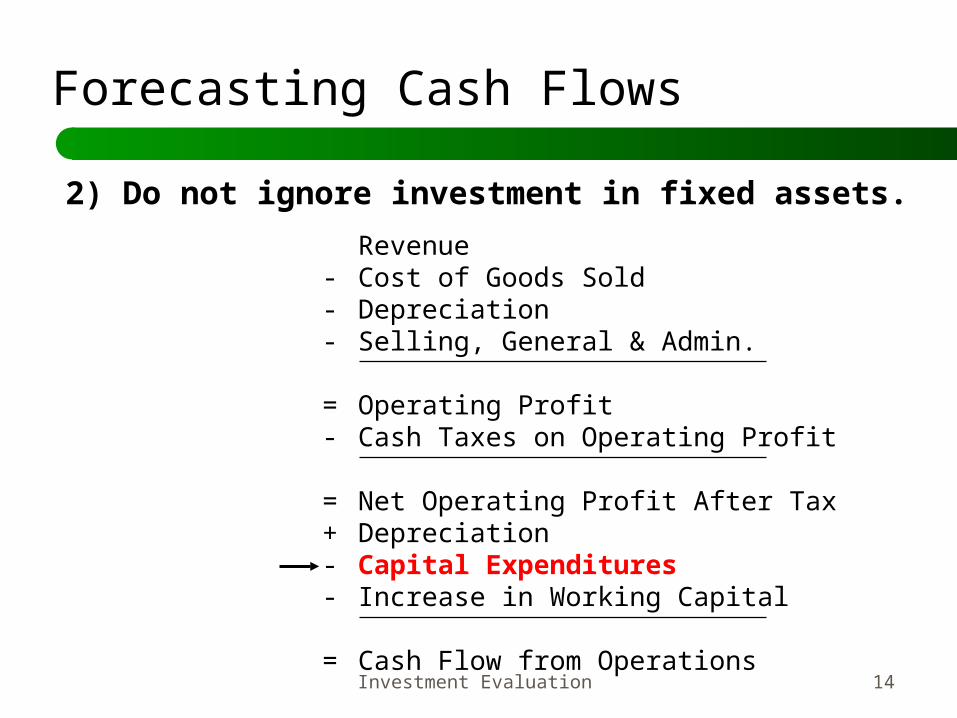

2) Do not ignore investment in fixed assets (Capital Expenditures)

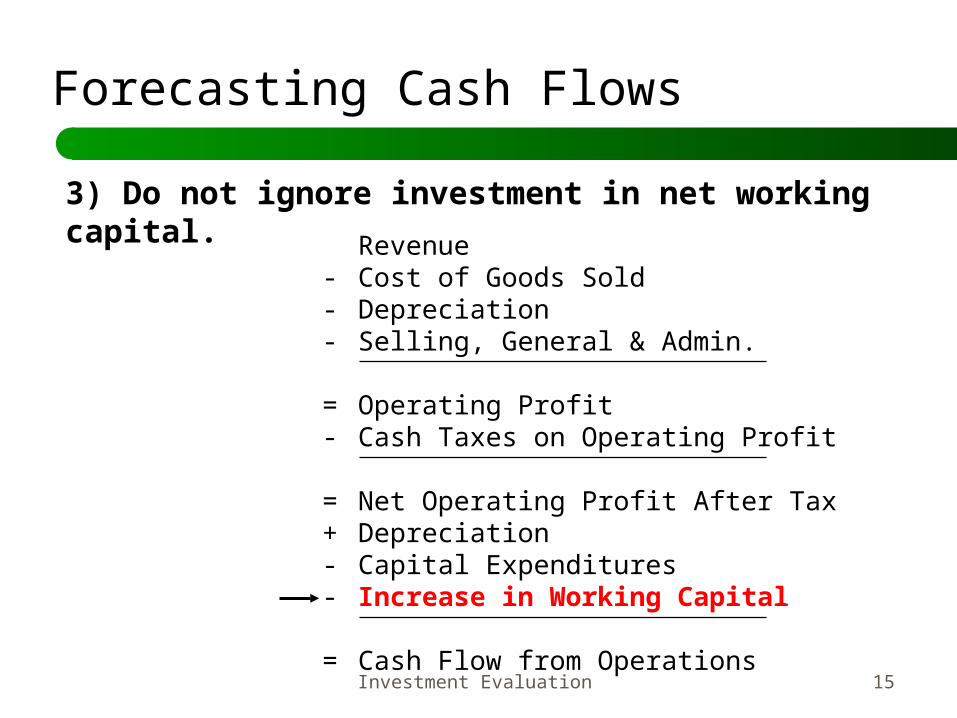

3) Do not ignore investment in net working capital• Include only changes in operating working capital. Short-term

debt, excess cash and marketable securities should not be accounted for.

4) Separate investment and financing decisions: Evaluate as if entirely equity financed

5) Estimate flows on a incremental basis• Forget sunk costs: cost incurred in the past and irreversible• Include all externalities - the effects of the project on the rest of

the firm - e.g., cannibalization or erosion, enhancement

6) Opportunity costs cannot be ignored

Forecasting Cash Flows: The Ten The Ten CommandmentsCommandments

Investment Evaluation 11

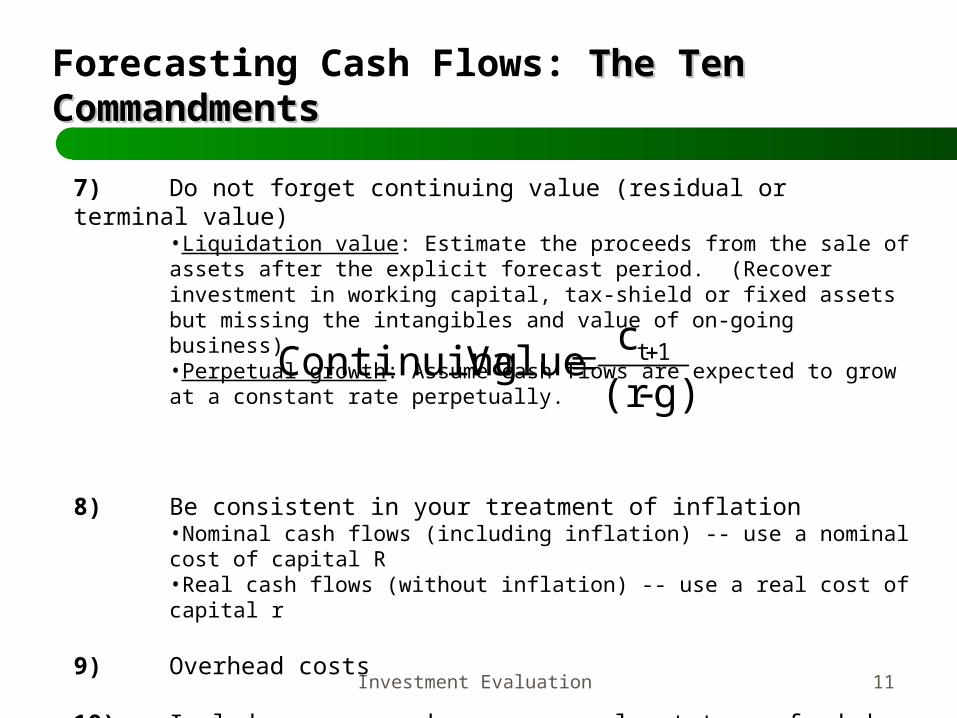

7) Do not forget continuing value (residual or terminal value)•Liquidation value: Estimate the proceeds from the sale of assets after the explicit forecast period. (Recover investment in working capital, tax-shield or fixed assets but missing the intangibles and value of on-going business)•Perpetual growth: Assume cash flows are expected to grow at a constant rate perpetually.

8) Be consistent in your treatment of inflation•Nominal cash flows (including inflation) -- use a nominal cost of capital R•Real cash flows (without inflation) -- use a real cost of capital r

9) Overhead costs

10) Include excess cash, excess real estate, unfunded (over-funded) pension fund, large stock option obligations, and other relevant off balance sheet items.

Forecasting Cash Flows: The Ten The Ten CommandmentsCommandments

g)-(r

c Value Continuing 1t

Investment Evaluation 12

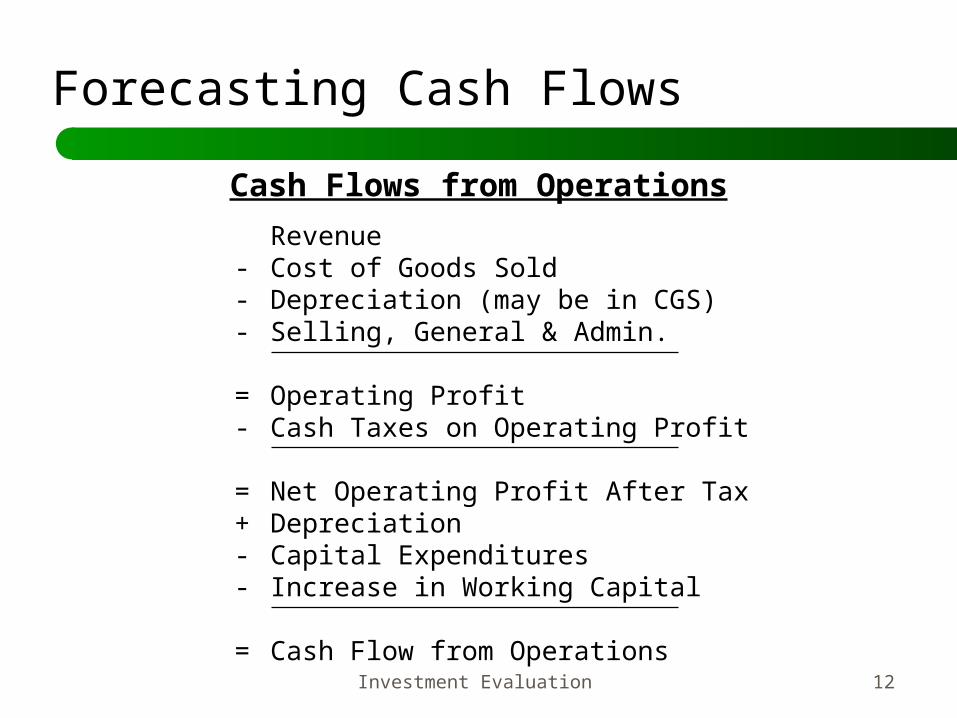

Forecasting Cash Flows

Cash Flows from Operations

Revenue- Cost of Goods Sold- Depreciation (may be in CGS)- Selling, General & Admin.

= Operating Profit- Cash Taxes on Operating Profit

= Net Operating Profit After Tax+ Depreciation- Capital Expenditures- Increase in Working Capital

= Cash Flow from Operations

Investment Evaluation 13

Forecasting Cash Flows

1) Depreciation is not a cash flow, but it affects taxationRevenue

- Cost of Goods Sold- Depreciation- Selling, General & Admin.

= Operating Profit- Cash Taxes on Operating Profit

= Net Operating Profit After Tax+ Depreciation- Capital Expenditures- Increase in Working Capital

= Cash Flow from Operations

Investment Evaluation 14

Forecasting Cash Flows

2) Do not ignore investment in fixed assets.

Revenue- Cost of Goods Sold- Depreciation- Selling, General & Admin.

= Operating Profit- Cash Taxes on Operating Profit

= Net Operating Profit After Tax+ Depreciation- Capital Expenditures- Increase in Working Capital

= Cash Flow from Operations

Investment Evaluation 15

Forecasting Cash Flows

3) Do not ignore investment in net working capital. Revenue

- Cost of Goods Sold- Depreciation- Selling, General & Admin.

= Operating Profit- Cash Taxes on Operating Profit

= Net Operating Profit After Tax+ Depreciation- Capital Expenditures- Increase in Working Capital

= Cash Flow from Operations

Investment Evaluation 16

Forecasting Cash Flows

There is an important distinction between the accounting definition of working capital and the economic/finance definition relevant to cash flows forecast. The distinction is a direct result of the

4th commandment above: We need the operating working capital, not the operating and financial working capital.

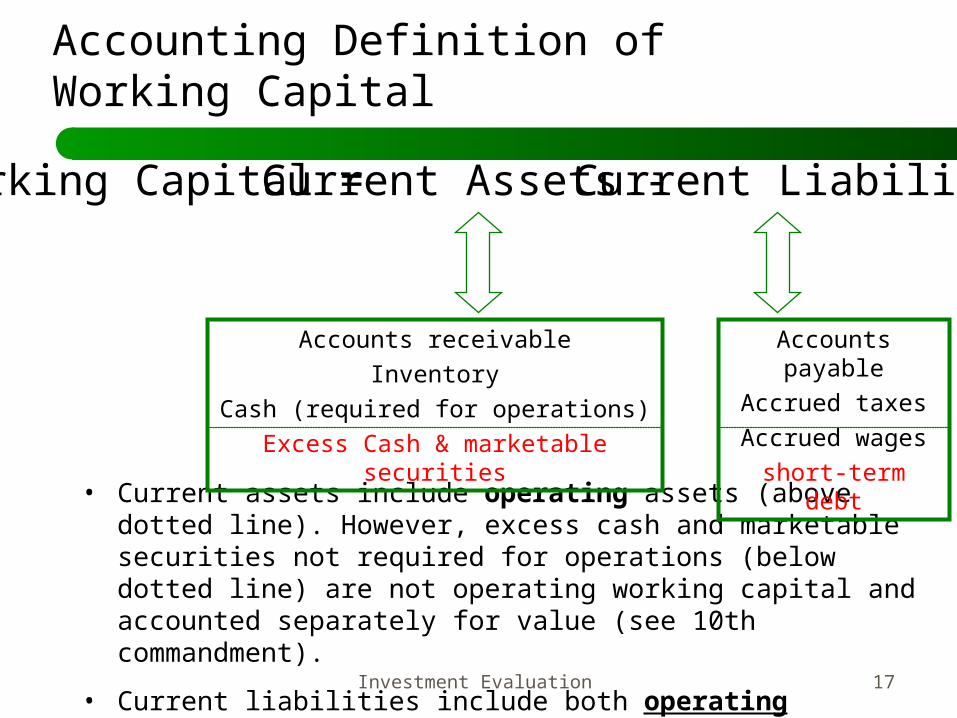

Investment Evaluation 17

• Current assets include operating assets (above dotted line). However, excess cash and marketable securities not required for operations (below dotted line) are not operating working capital and accounted separately for value (see 10th commandment).

• Current liabilities include both operating liabilities (above the dotted line) and non-operating short-term debt (below the dotted line).

Accounting Definition of Working Capital

Accounts receivable

Inventory

Cash (required for operations)

Excess Cash & marketable securities

Accounts payable

Accrued taxes

Accrued wages

short-term debt

Working Capital = Current Assets - Current Liabilities

Investment Evaluation 18

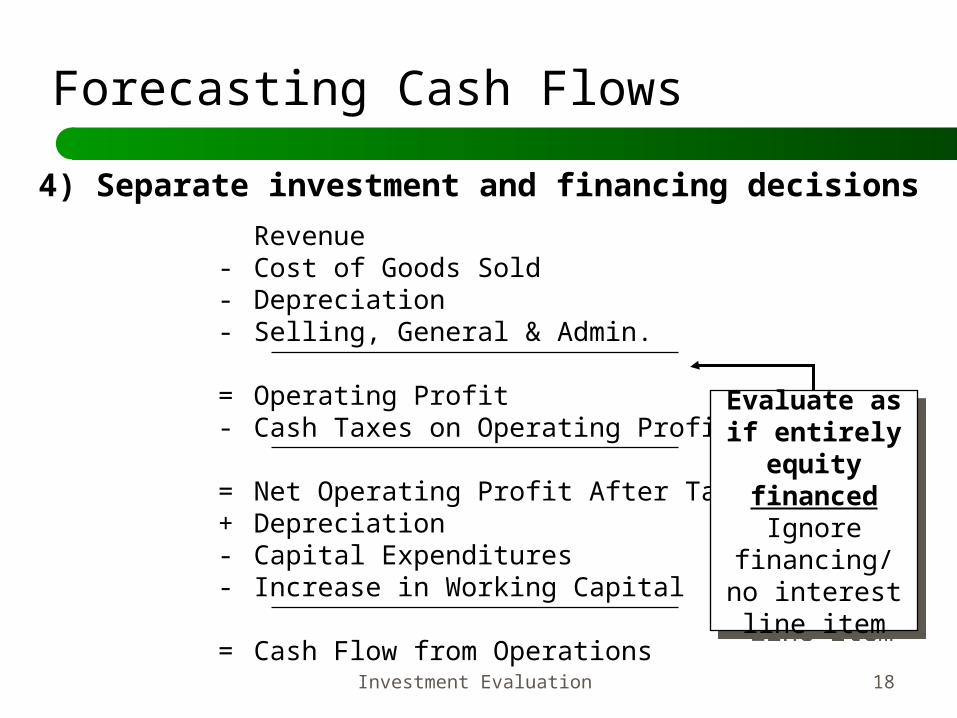

Forecasting Cash Flows

4) Separate investment and financing decisions

Revenue- Cost of Goods Sold- Depreciation- Selling, General & Admin.

= Operating Profit- Cash Taxes on Operating Profit

= Net Operating Profit After Tax+ Depreciation- Capital Expenditures- Increase in Working Capital

= Cash Flow from Operations

Evaluate as if entirely

equity financed

Ignore financing/no interest line item

Evaluate as if entirely

equity financed

Ignore financing/no interest line item

Investment Evaluation 19

Forecasting Cash Flows

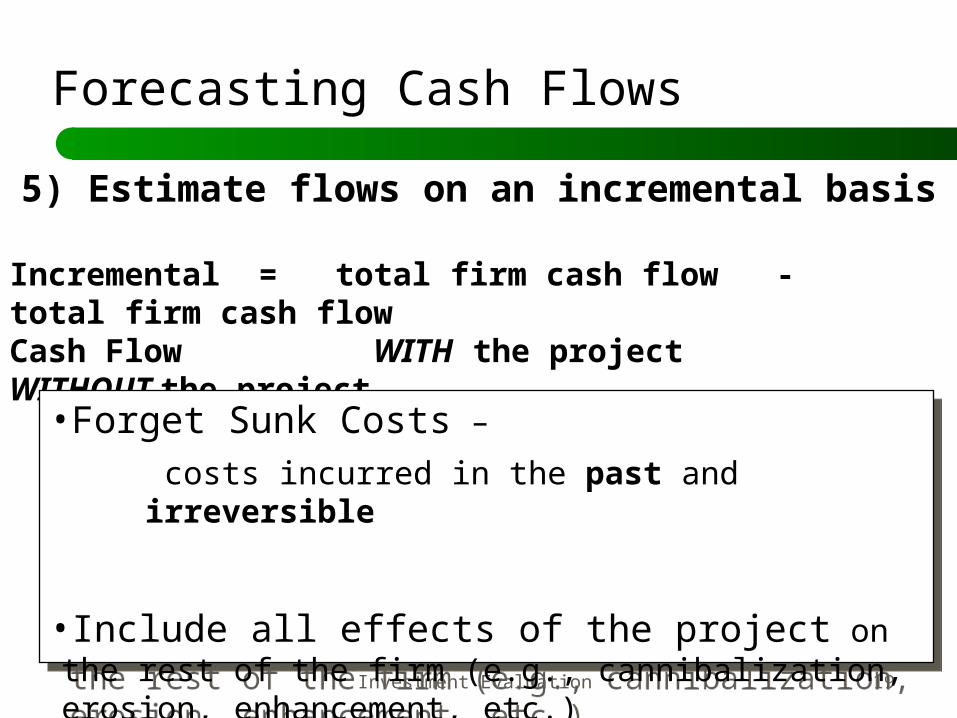

5) Estimate flows on an incremental basis

Incremental = total firm cash flow - total firm cash flow Cash Flow WITH the project WITHOUT the project

•Forget Sunk Costs –

costs incurred in the past and irreversible

•Include all effects of the project on the rest of the firm (e.g., cannibalization, erosion, enhancement, etc.)

•Forget Sunk Costs –

costs incurred in the past and irreversible

•Include all effects of the project on the rest of the firm (e.g., cannibalization, erosion, enhancement, etc.)

Investment Evaluation 20

Forecasting Cash Flows

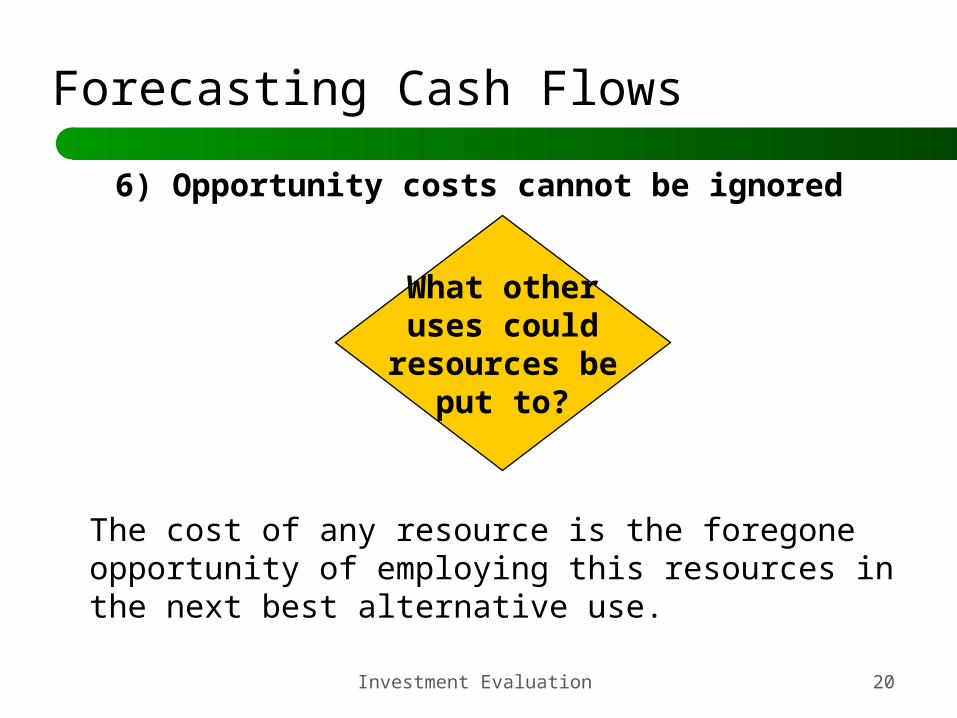

6) Opportunity costs cannot be ignored

What otheruses could

resources beput to?

The cost of any resource is the foregone opportunity of employing this resources in the next best alternative use.

Investment Evaluation 21

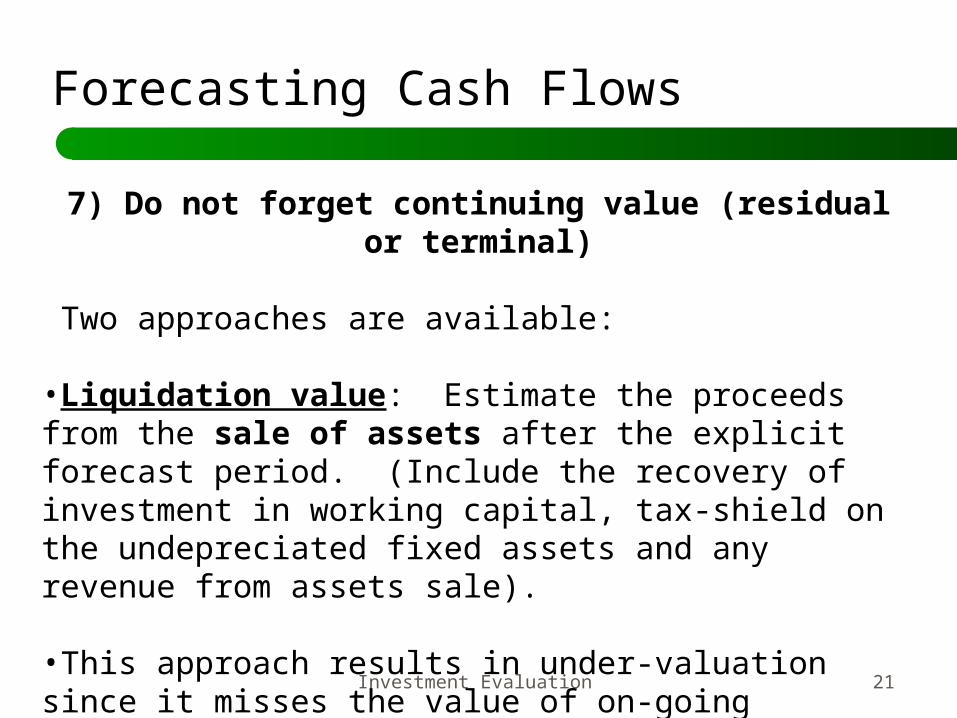

Forecasting Cash Flows

7) Do not forget continuing value (residual or terminal)

Two approaches are available:

•Liquidation value: Estimate the proceeds from the sale of assets after the explicit forecast period. (Include the recovery of investment in working capital, tax-shield on the undepreciated fixed assets and any revenue from assets sale). •This approach results in under-valuation since it misses the value of on-going business. It ignores the value of intangibles.

Investment Evaluation 22

Forecasting Cash Flows

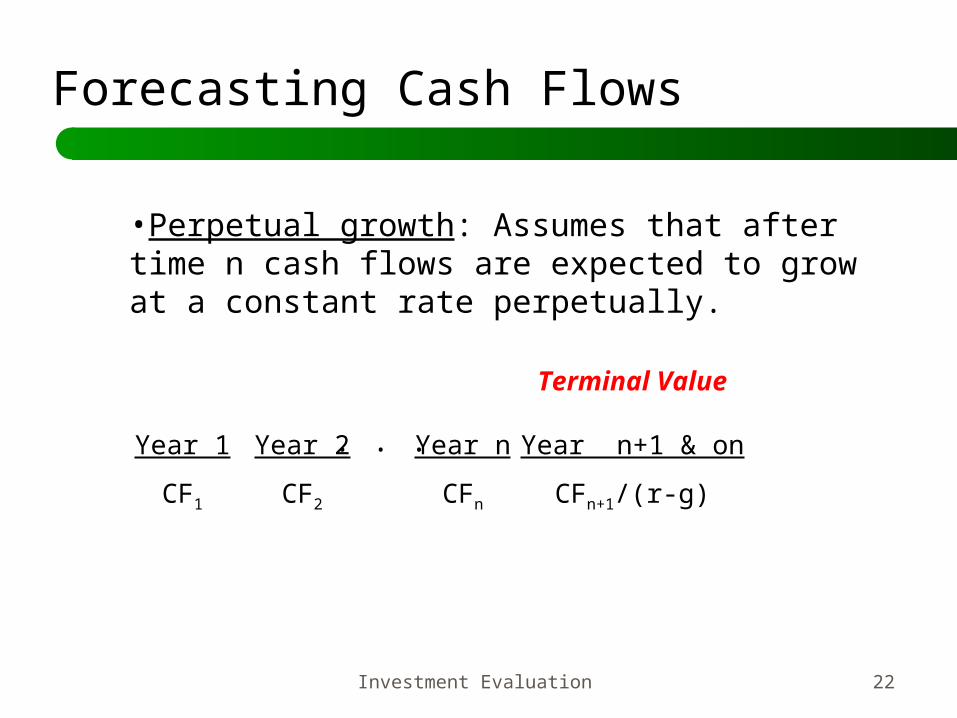

•Perpetual growth: Assumes that after time n cash flows are expected to grow at a constant rate perpetually.

Year 1

CF1

Year 2

CF2

Year n

CFn

. . .

Terminal Value

Year n+1 & on

CFn+1/(r-g)

Investment Evaluation 23

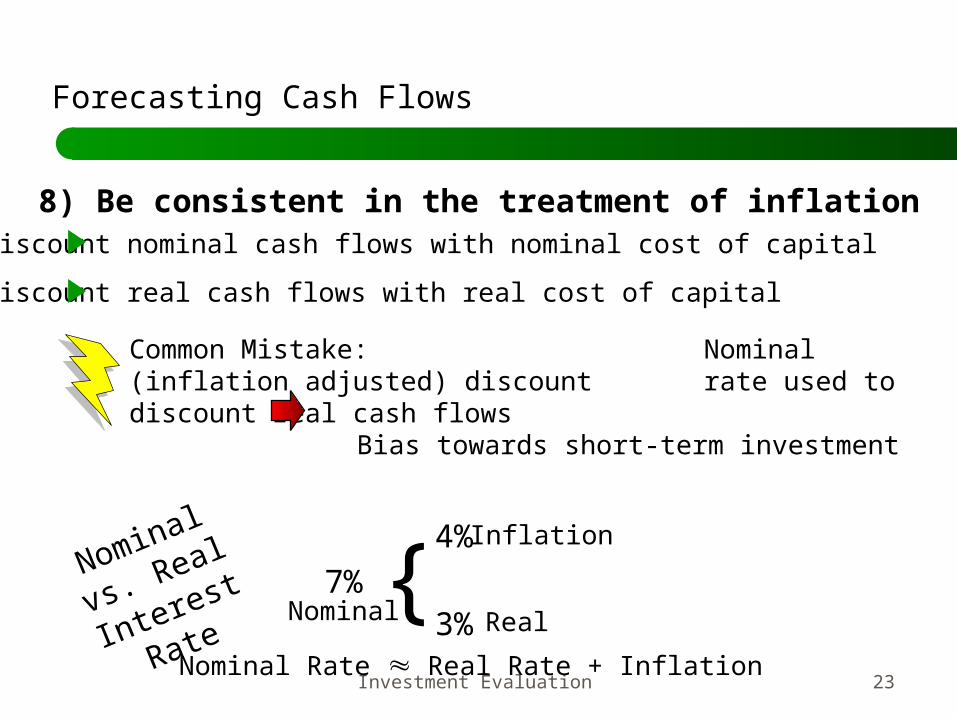

8) Be consistent in the treatment of inflationDiscount nominal cash flows with nominal cost of capital

Discount real cash flows with real cost of capital

Nominal Rate Real Rate + Inflation

Common Mistake: Nominal (inflation adjusted) discount rate used to discount real cash flows

Bias towards short-term investment

Nominal vs.

Real Interest

Rate7%

4%

3%Nominal

Inflation

Real{

Forecasting Cash Flows

Investment Evaluation 24

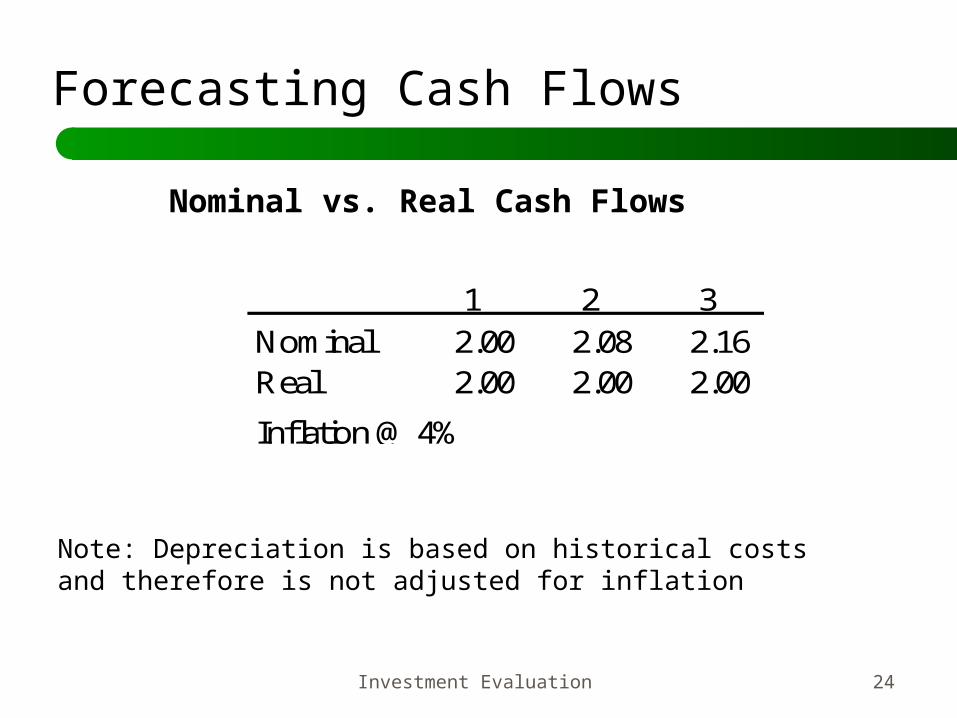

1 2 3Nominal 2.00 2.08 2.16 Real 2.00 2.00 2.00

Inflation @ 4%

Nominal vs. Real Cash Flows

Note: Depreciation is based on historical costs and therefore is not adjusted for inflation

Forecasting Cash Flows

Investment Evaluation 25

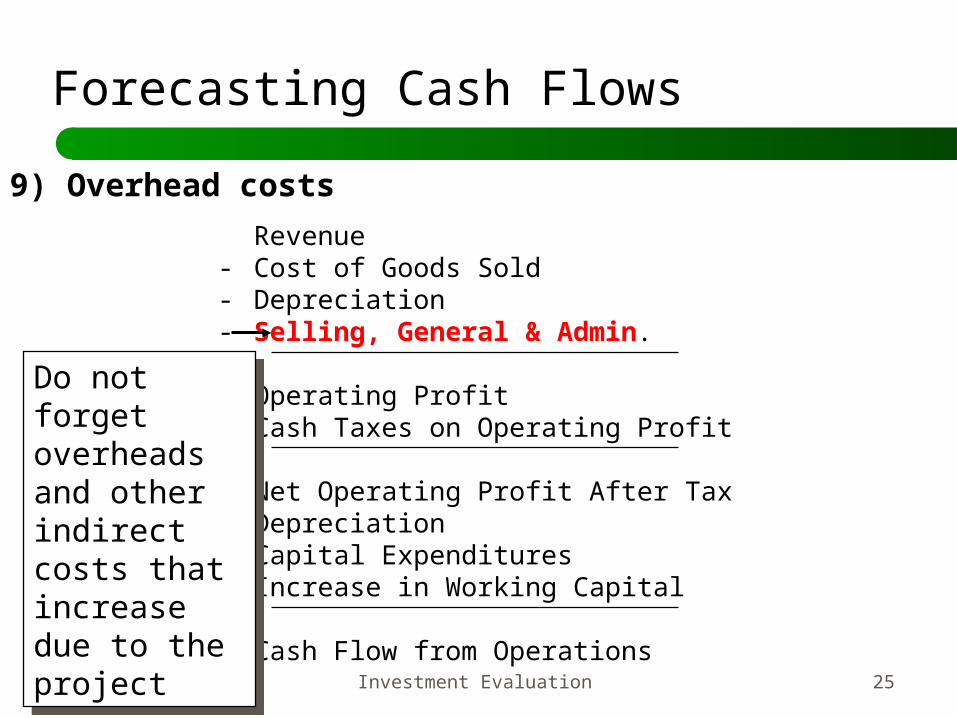

Forecasting Cash Flows

9) Overhead costs

Revenue- Cost of Goods Sold- Depreciation- Selling, General & Admin.

= Operating Profit- Cash Taxes on Operating Profit

= Net Operating Profit After Tax+ Depreciation- Capital Expenditures- Increase in Working Capital

= Cash Flow from Operations

Do not forget overheads and other indirect costs that increase due to the project

Do not forget overheads and other indirect costs that increase due to the project

Investment Evaluation 26

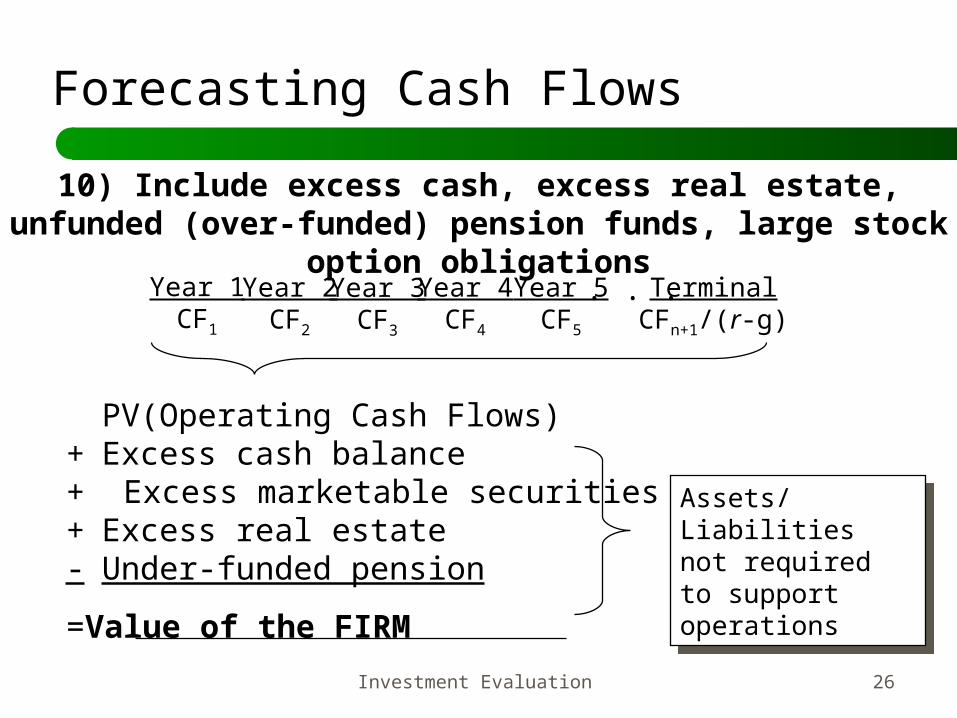

Forecasting Cash Flows

10) Include excess cash, excess real estate, unfunded (over-funded) pension funds, large stock

option obligationsYear 1

CF1

Year 2CF2

Year 3CF3

Year 4CF4

Year 5CF5

TerminalCFn+1/(r-g)

. . .

PV(Operating Cash Flows)+ Excess cash balance+ Excess marketable securities+ Excess real estate- Under-funded pension

=Value of the FIRM

Assets/Liabilities not required to support operations

Assets/Liabilities not required to support operations

Investment Evaluation 27

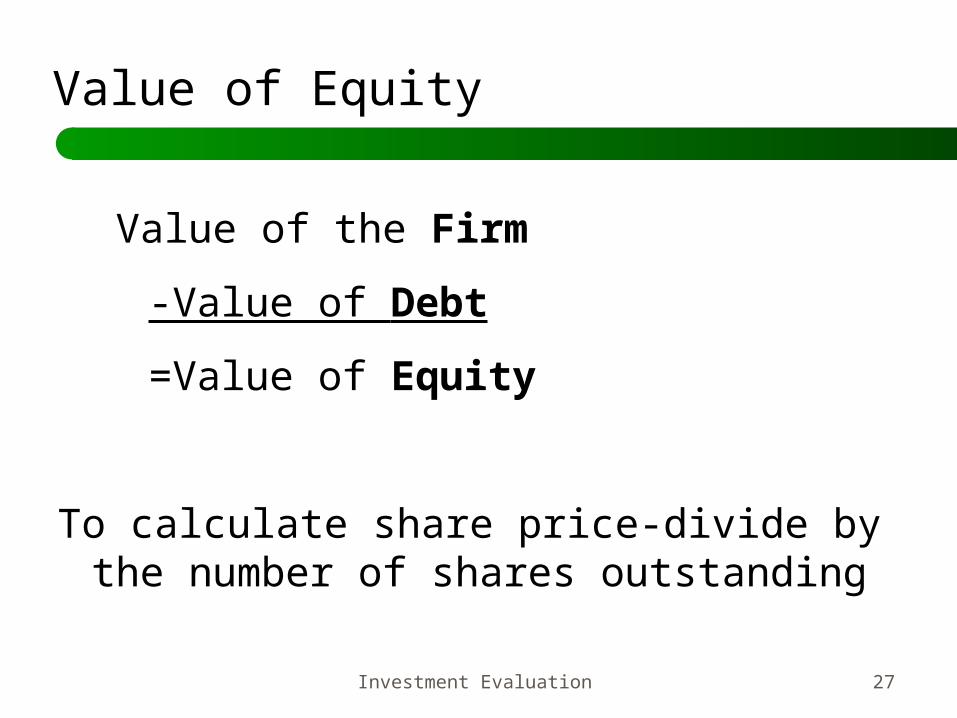

Value of the Firm

-Value of Debt

=Value of Equity

To calculate share price-divide by the number of shares outstanding

Value of Equity

Investment Evaluation 28

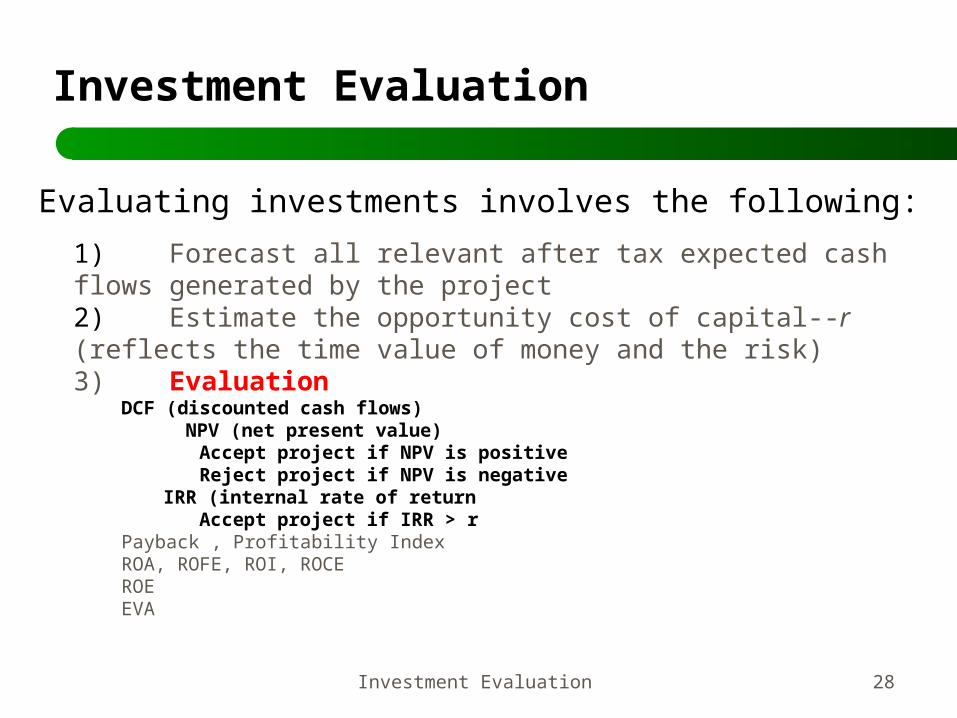

Investment Evaluation

Evaluating investments involves the following:

1) Forecast all relevant after tax expected cash flows generated by the project2) Estimate the opportunity cost of capital--r (reflects the time value of money and the risk)3) Evaluation

DCF (discounted cash flows) NPV (net present value)

Accept project if NPV is positiveReject project if NPV is negative

IRR (internal rate of returnAccept project if IRR > r

Payback , Profitability IndexROA, ROFE, ROI, ROCEROEEVA

Investment Evaluation 29

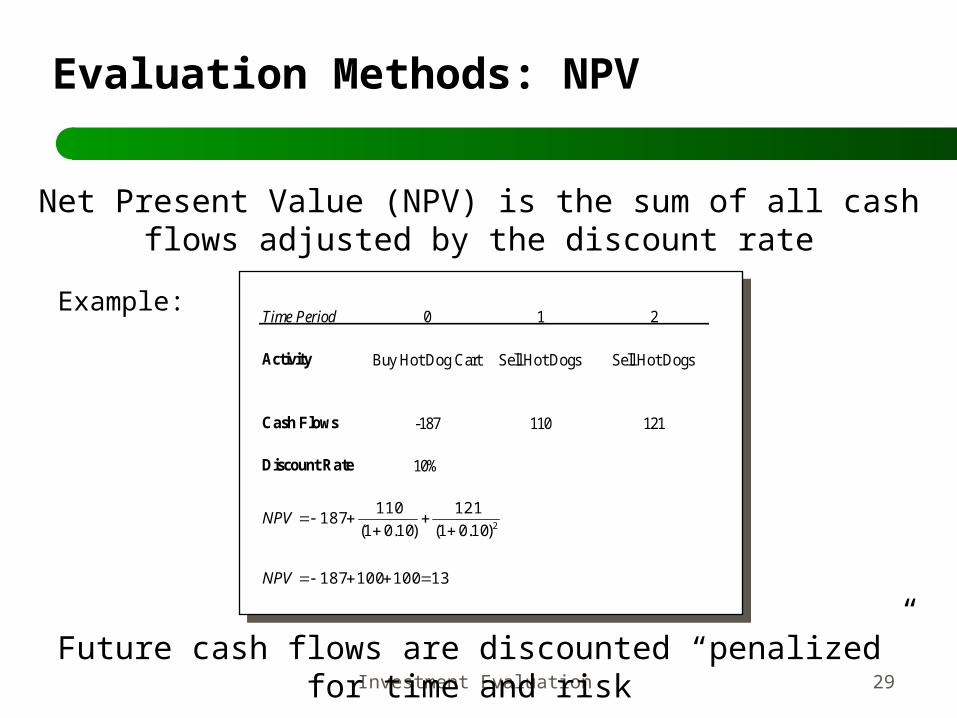

Evaluation Methods: NPV

Net Present Value (NPV) is the sum of all cash flows adjusted by the discount rate

Example: Time Period 0 1 2

Activity Buy Hot Dog Cart Sell Hot Dogs Sell Hot Dogs

Cash Flows -187 110 121

Discount Rate 10%

13100100187

)10.01(

121

)10.01(

110187

2

NPV

NPV

Future cash flows are discounted “penalized” for time and risk

Investment Evaluation 30

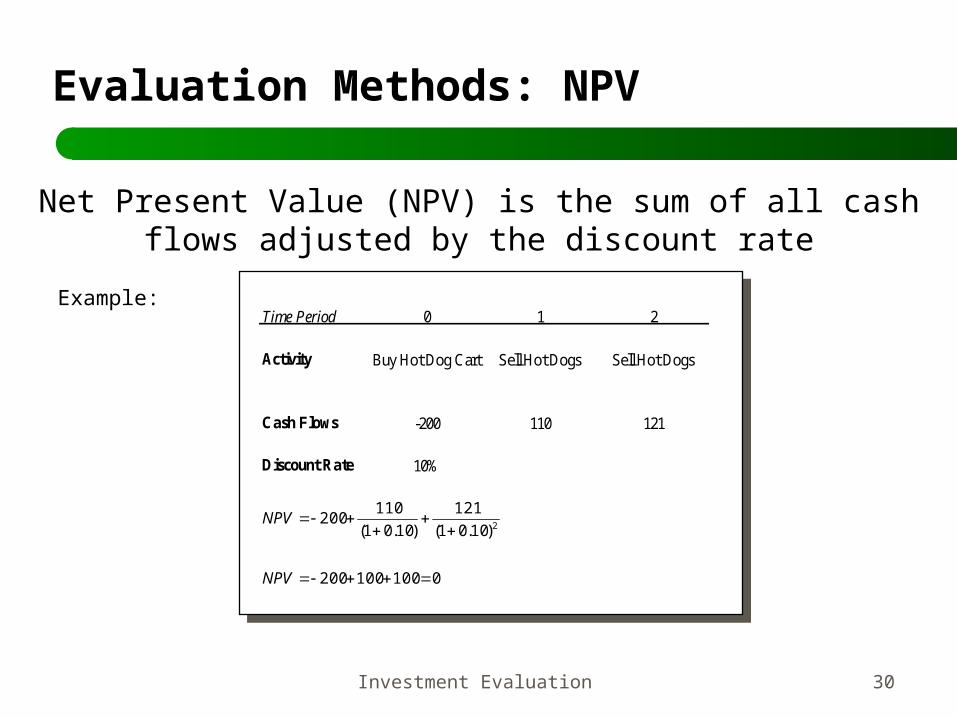

Evaluation Methods: NPV

Net Present Value (NPV) is the sum of all cash flows adjusted by the discount rate

Example:Time Period 0 1 2

Activity Buy Hot Dog Cart Sell Hot Dogs Sell Hot Dogs

Cash Flows -200 110 121

Discount Rate 10%

0100100200

)10.01(

121

)10.01(

110200

2

NPV

NPV

Investment Evaluation 31

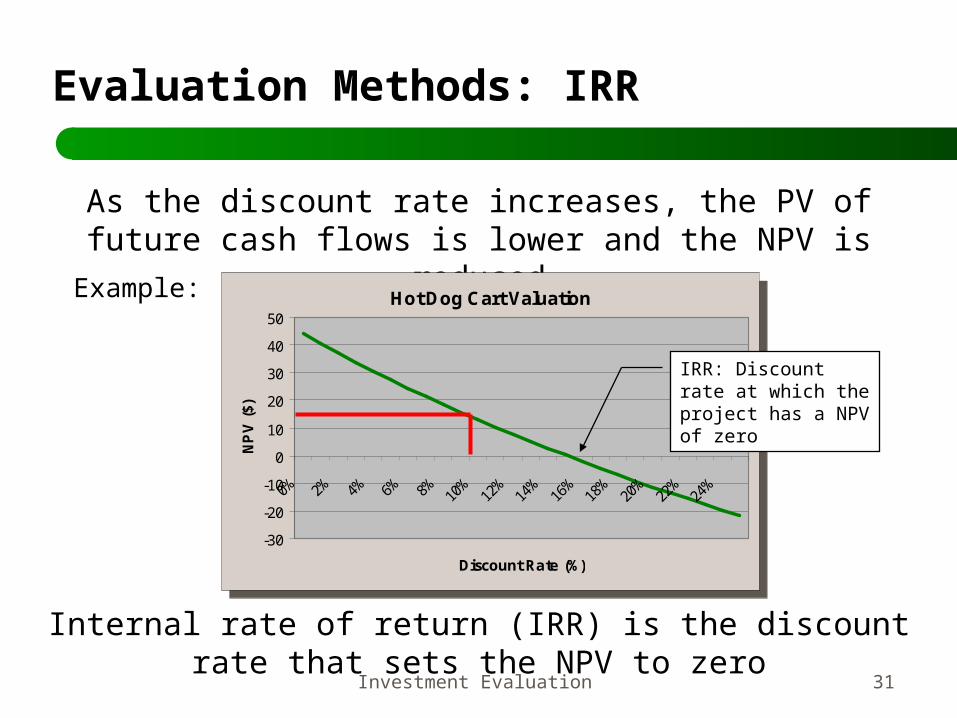

Evaluation Methods: IRR

As the discount rate increases, the PV of future cash flows is lower and the NPV is reduced

Example:Hot Dog Cart Valuation

-30

-20

-10

0

10

20

30

40

50

0% 2% 4% 6% 8% 10%

12%

14%

16%

18%

20%

22%

24%

Discount Rate (%)

NP

V (

$)

Hot Dog Cart Valuation

-30

-20

-10

0

10

20

30

40

50

0% 2% 4% 6% 8% 10%

12%

14%

16%

18%

20%

22%

24%

Discount Rate (%)

NP

V (

$)

Internal rate of return (IRR) is the discount rate that sets the NPV to zero

IRR: Discount rate at which the project has a NPV of zero

Investment Evaluation 32

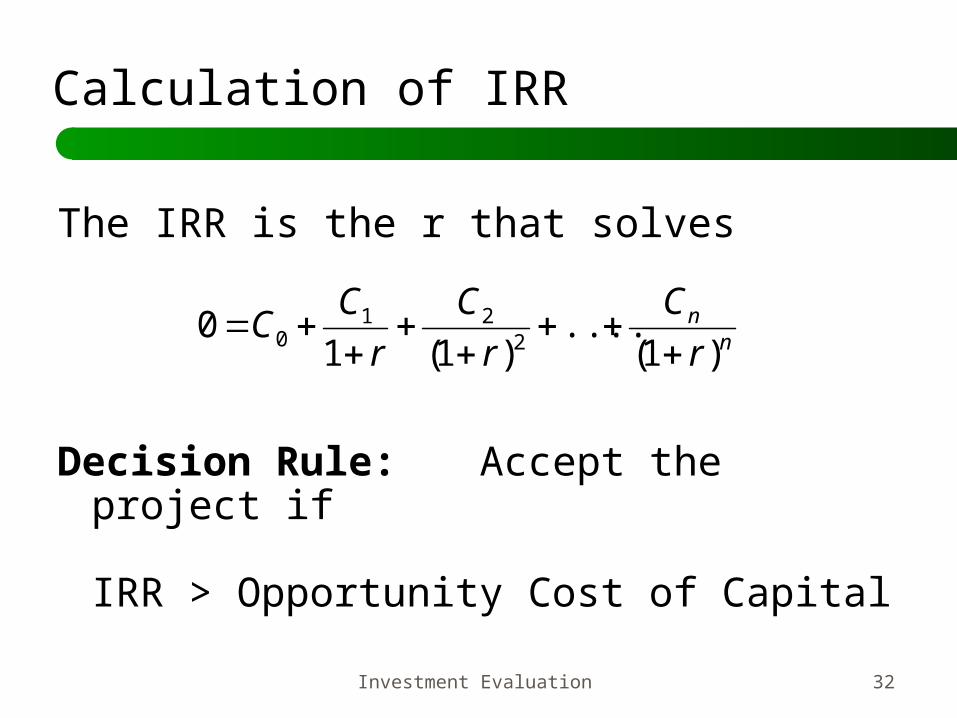

Calculation of IRR

The IRR is the r that solves

Decision Rule: Accept the project if

IRR > Opportunity Cost of Capital

nn

r

C

r

C

r

CC

)1(....

)1(10

221

0

Investment Evaluation 33

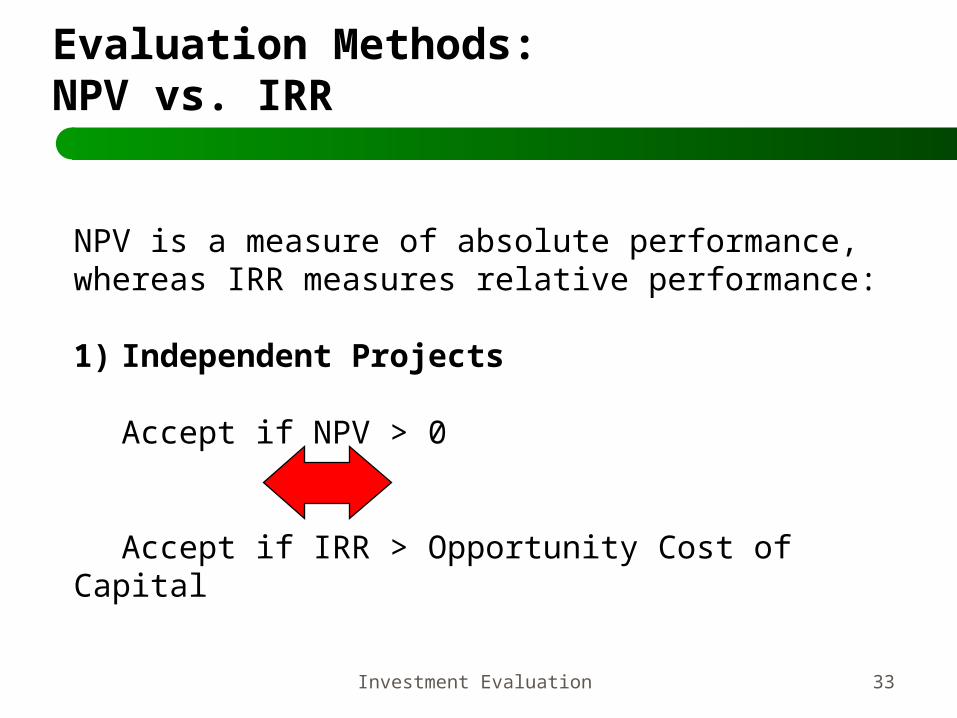

Evaluation Methods: NPV vs. IRR

NPV is a measure of absolute performance, whereas IRR measures relative performance:

1) Independent Projects

Accept if NPV > 0

Accept if IRR > Opportunity Cost of Capital

Investment Evaluation 34

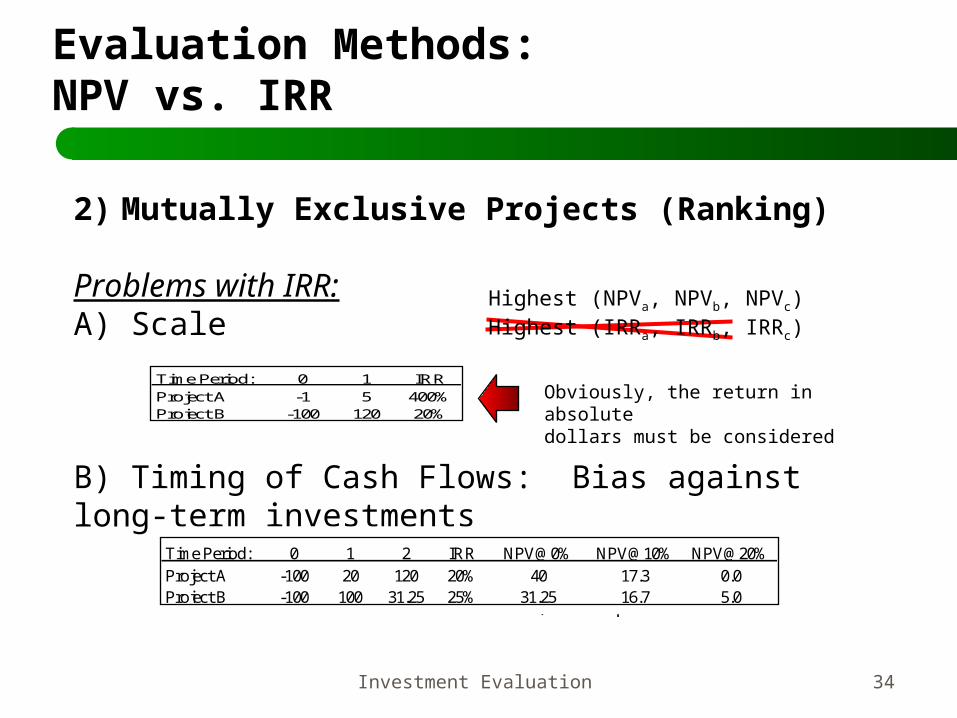

Evaluation Methods: NPV vs. IRR

2) Mutually Exclusive Projects (Ranking)

Problems with IRR:A) Scale

B) Timing of Cash Flows: Bias against long-term investments

Time Period: 0 1 IRRProject A -1 5 400%Project B -100 120 20%

Highest (NPVa, NPVb, NPVc)Highest (IRRa, IRRb, IRRc)

Obviously, the return in absolutedollars must be considered

Preference for CF early!But, it depends.

Time Period: 0 1 2Project A -100 20 120Project B -100 100 31.25

Time Period: 0 1 2 IRR NPV@0% NPV@10% NPV@20%Project A -100 20 120 20% 40 17.3 0.0Project B -100 100 31.25 25% 31.25 16.7 5.0

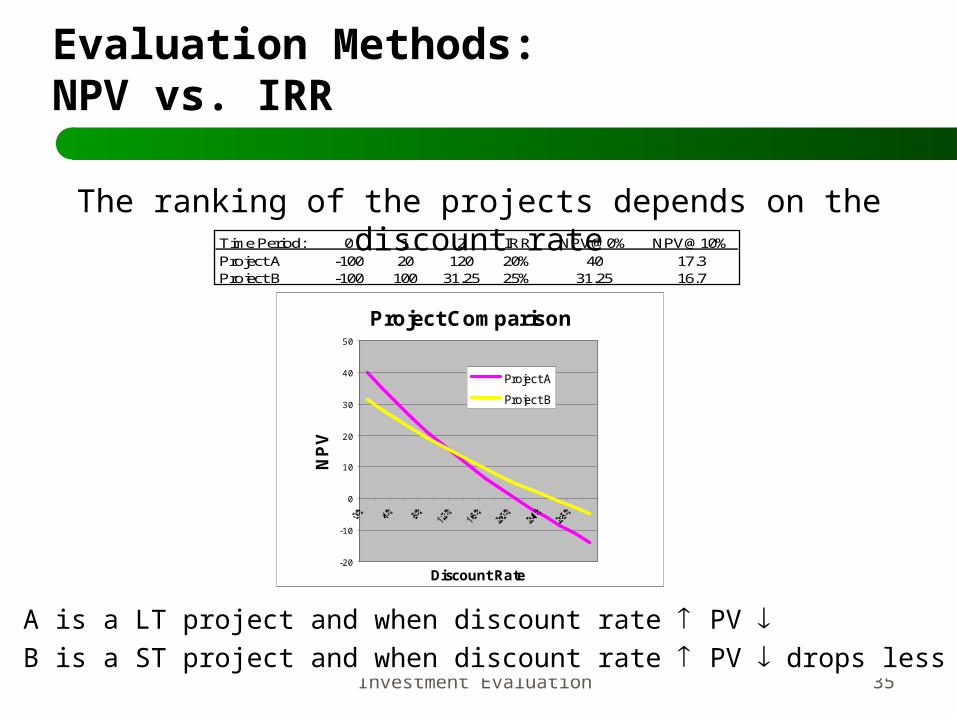

Investment Evaluation 35

The ranking of the projects depends on the discount rateTime Period: 0 1 2 IRR NPV@0% NPV@10%

Project A -100 20 120 20% 40 17.3Project B -100 100 31.25 25% 31.25 16.7

Project Comparison

-20

-10

0

10

20

30

40

50

Discount Rate

NP

V

Project A

Project B

A is a LT project and when discount rate PVB is a ST project and when discount rate PVdrops less

Evaluation Methods: NPV vs. IRR

Investment Evaluation 36

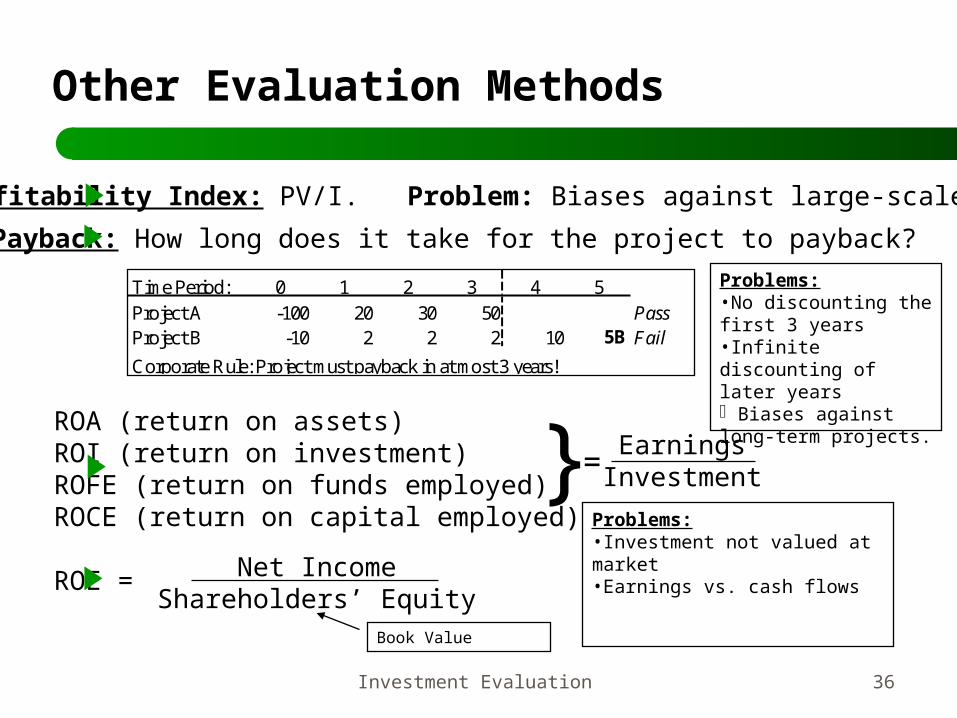

Other Evaluation Methods

Payback: How long does it take for the project to payback?

Time Period: 0 1 2 3 4 5Project A -100 20 30 50 PassProject B -10 2 2 2 10 5B Fail

Corporate Rule: Project must payback in at most 3 years!

Problems:•No discounting the first 3 years•Infinite discounting of later years Biases against long-term projects.ROA (return on assets)

ROI (return on investment)ROFE (return on funds employed)ROCE (return on capital employed)

ROE =

} EarningsInvestment=

Problems:•Investment not valued at market•Earnings vs. cash flows

Net IncomeShareholders’ Equity

Book Value

Profitability Index: PV/I. Problem: Biases against large-scale projects.