45

Investment Themes in Optical Networking September 2001 Bill Magill – Optical Components & Systems

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | whitney-hines |

| View: | 216 times |

| Download: | 0 times |

Investment Themes in Optical Networking

September 2001

Bill Magill – Optical Components & Systems

2

Overview

Optical networking: defining the ecosystem

State of the industry

Looking forward: the bad and the good

Identifying the pain

Relieving the pain

Hot growth opportunities

Creating a Metric Of Interest

Investment summary

3

Defining The Ecosystem

4

Man

ufac

turi

ng S

ervi

ces

Man

ufac

turi

ng E

quip

men

t

Test

& M

easu

rem

ent E

quip

men

t

Food Chain In The Optical Networking Industry

Materials & Methods: Wafers, Fiber Preforms, Processes

Discrete components: passives, actives, planar

Modules & Subsystems: amplifiers, switches, ADMs, transponders

Systems: access, metro, long haul

Kigre Glass

5

Optical Networking Means Transparent Optical Solutions

STS-1 grooming:

Ciena CoreDirector

Sycamore SN16000

Corvis CorWave OCS

switching:

Calient DiamondWave

Lucent LambdaRouter

Corvis CorWave ON

O-ADM ring/mesh management:

Opthos IW 1000

Movaz RAYstar

Matisse D2WDM

OSP (amp, disp comp, DGE):

NP Photonics

Yafo

ZettaLight

MSPP, aggregation:

Cisco ONS 15454

Astral Point ON 7000

Ciena MetroDirector K2

LH Core

MetroCoreMetro

Access

mux & termination:

Ciena MultiWave

PhotonEx PX Ultra

Nortel OPTera

access:

AllOptic GigaForce

Paceon BPon

Quantum Bridge QB

6

The Optics Ecosystem – Systems & Subsystems

True Optical Switches

Calient Movaz

Lucent GlimmerGlass

Naynav Corvis Alcatel

Cinta Nortel Tellium

Optical Switch Plans?

Ciena

Sycamore Tellabs

Optical Add-Drops

Opthos

Matisse

AcceLight

WDM Terminals

Calient Lucent

Nortel Cisco

Alcatel Hitachi

Fujitsu NEC

Siemens Sycamore

Tellabs Reversi

Ultra Long-Haul

Corvis Innovance

Solinet Nortel

PhotonEx

O-ADM, OXC

OXC

WDMTerminals

OSP

OSPs

NP Photonics Optellios

Teem Photonics Phaethon

Zettalight Yafo

Xtera JDS Uniphase

Southampton Ph Corning

Optical Access

AllOptic Eluminent

Marconi Paceon

Optical Solutions OKI

Quantum Bridge

Siara TeraWave

PON

7

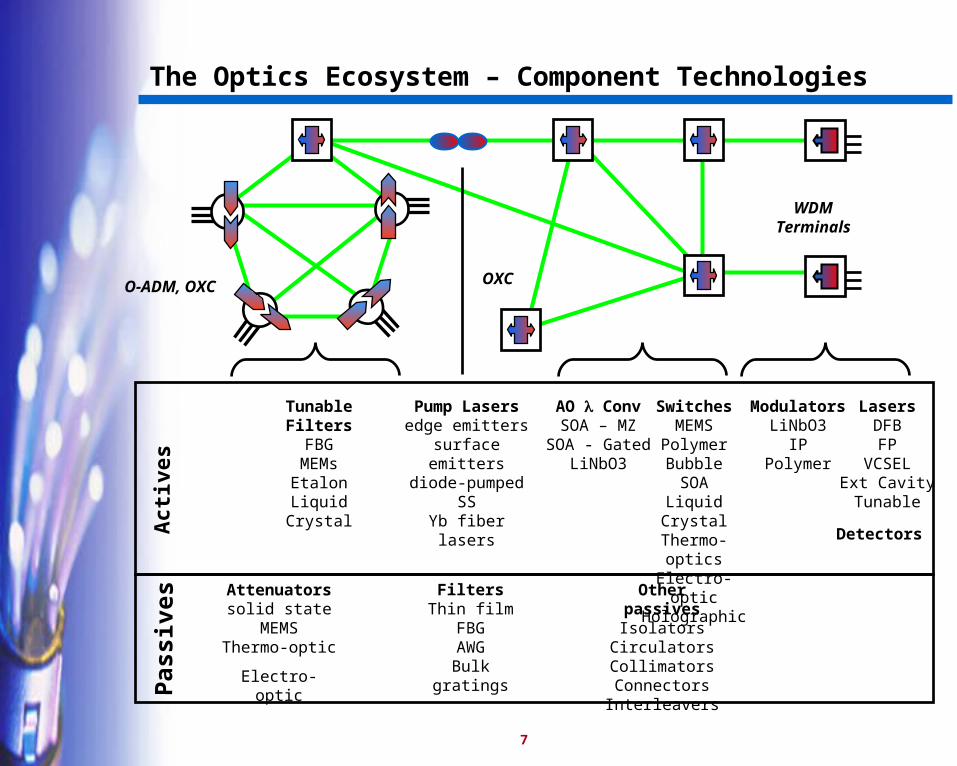

The Optics Ecosystem – Component Technologies

O-ADM, OXC OXC

WDMTerminals

LasersDFBFP

VCSELExt CavityTunable

ModulatorsLiNbO3

IPPolymer

Detectors

SwitchesMEMS

PolymerBubbleSOA

Liquid CrystalThermo-opticsElectro-opticHolographic

AO ConvSOA – MZ

SOA - GatedLiNbO3

Tunable FiltersFBG

MEMsEtalon

Liquid Crystal

Pump Lasersedge emitters

surface emittersdiode-pumped SS

Yb fiber lasers

Act

ives

Pas

sive

s Attenuatorssolid state

MEMSThermo-optic

Electro-optic

FiltersThin film

FBGAWG

Bulk gratings

Other passivesIsolators

CirculatorsCollimatorsConnectorsInterleavers

8

Select Companies Developing Active Components and Subsystems

Broadview, 9/01

9

Select Companies Developing Passive Components and Subsystems

Broadview, 9/01

10

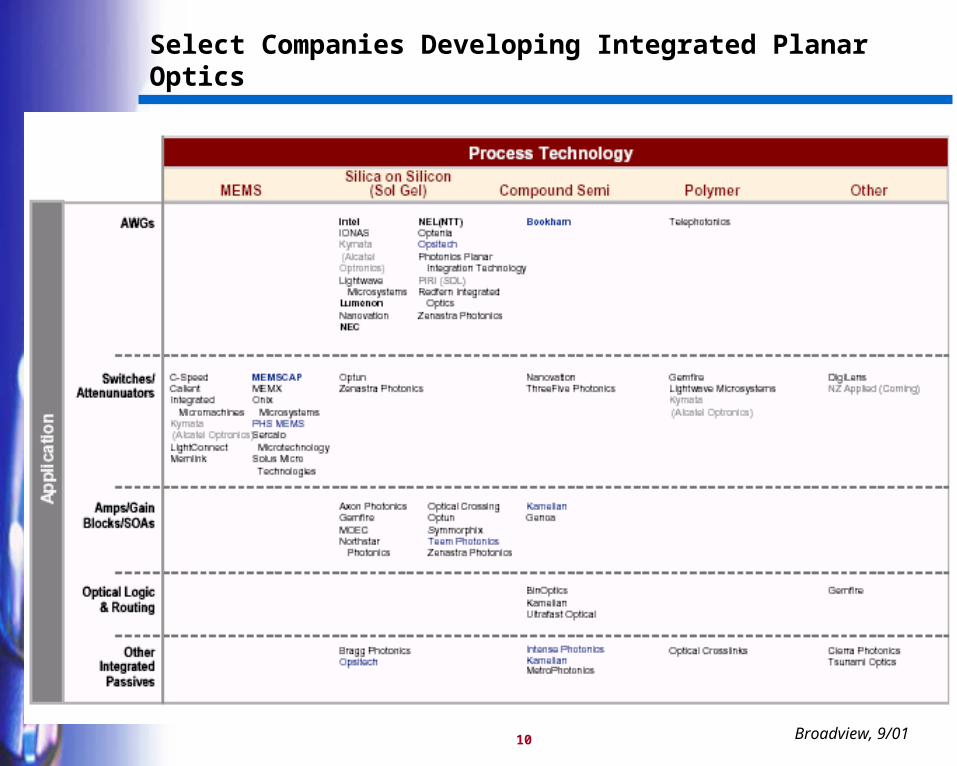

Select Companies Developing Integrated Planar Optics

Broadview, 9/01

11

State Of The Industry

12

Internet Traffic Growth Has Slowed

60%

80%

100%

120%

140%

160%

180%

200%

1999 2000 2001 2002 2003 2004

An

nu

al G

row

th

Recovery

Soft Landing

Contraction

RHK, 5/01

13

Carriers Over-invested Into The Slowing Growth

Carrier Spending Ratios

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1996 1997 1998 1999 2000 2001

Averaged Carrier Revenues Divided By Average Capex

14

System Suppliers Have Seen Demand Dry Up …

TTM CY01E % Change % Ch. 00/99Ciena 1,520 1,611 6 98Alcatel 27,101 23,760 -12 36Lucent 24,800 23,200 -6 naNortel 26,500 22,400 -15 31ONI 160 250 56 1,866

Revenue Growth Comparison ($M)

15

… And The Market Outlook Revised Down, …

Recovery

Soft Landing

Contraction

$18

$23

$28

$33

$38

$43

$48

$53

2000 2001 2002 2003 2004

Bill

ion

sNov '00

RHK cuts NA Optical Transport Market Outlook by ~25% in May.

16

… And Down Further …

RHK Forecast Revision: NA Optical Transport Market

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2000 2001 2002

$ B

illi

on

May 01 Fcst Range

Sept 01 Fcst Revision

RHK cuts NA Optical Transport Market Outlook by another 40% in September.

17

… And Inventories Build Up

On March 1 2 Year Avg % DifferenceAlcatel 145.0 103.4 40Ciena 108.5 86.1 26Cisco 80.9 58.6 38Lucent 102.8 102.4 0Nortel 87.8 78.0 13

Days of Inventory

18

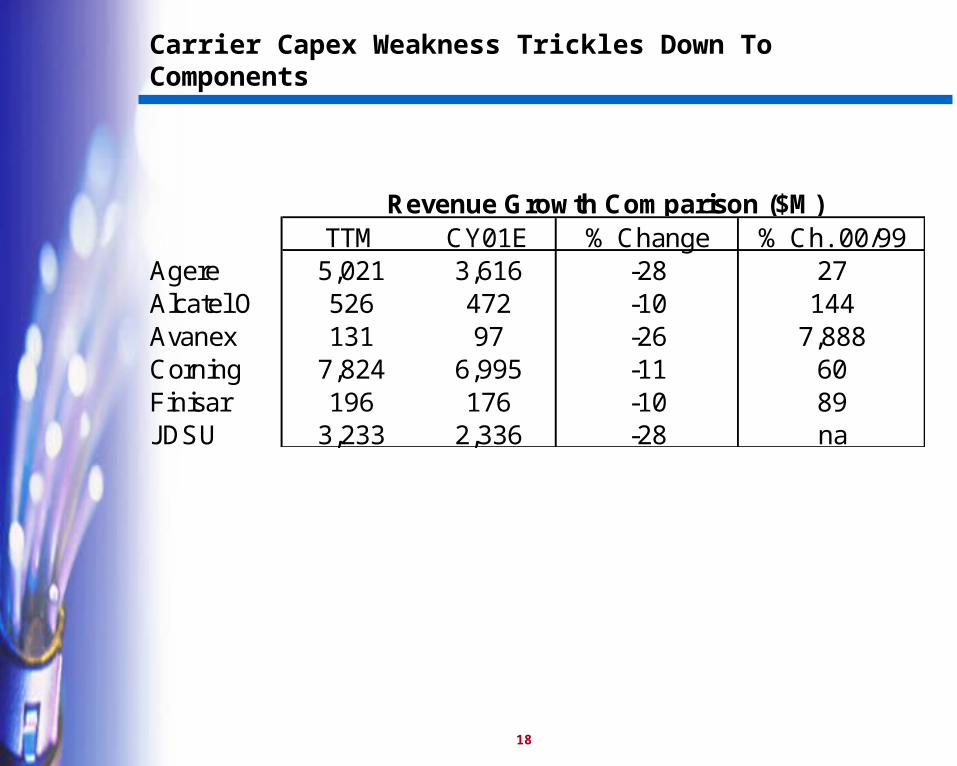

Carrier Capex Weakness Trickles Down To Components

TTM CY01E % Change % Ch. 00/99Agere 5,021 3,616 -28 27Alcatel O 526 472 -10 144Avanex 131 97 -26 7,888Corning 7,824 6,995 -11 60Finisar 196 176 -10 89JDSU 3,233 2,336 -28 na

Revenue Growth Comparison ($M)

19

Optical Equipment Stocks Have Been Hammered in 2001

Since January 2001:

JPM Equipment Index down 60%. (Includes all major telecom equipment suppliers.)

JPM Component Index down 55%. (Includes all major telecom optical and electronic component suppliers.)

Nasdaq off 25%

20

Everyone Is Unhappy

Carriers – Service spending by enterprise customers in a slump.

System OEMs – Carrier demand is slow.

Components Suppliers – OEM customers are sick.

Investment Banks – No equity market for IPOs. Little equity power for M&A, and everyone hoarding cash.

VCs – Where are the exits?

21

Looking Forward

22

The Bad And The Good

The Bad:– Aggregate carrier spending could be flat to down for next 1-4 years, due to recent

capex/revenue imbalance– Aggregate long-haul spending will be flat to down given over-investment and capacity glut – No catalyst (killer application or economic recovery) on near term horizon to re-accelerate

spending

The Good:– Optical networking helps improve the capex/revenue imbalance– Carriers’ restrained spending will favor optical networking equipment– No capacity glut in access or metro– Inventory overhang should dissipate by mid-02– Long-term outlook remains unchanged: unyielding bandwidth expansion and shifting traffic

dynamics will force the adoption of an optical networking model– Installed base of optical systems at early stage of technology maturity curve

23

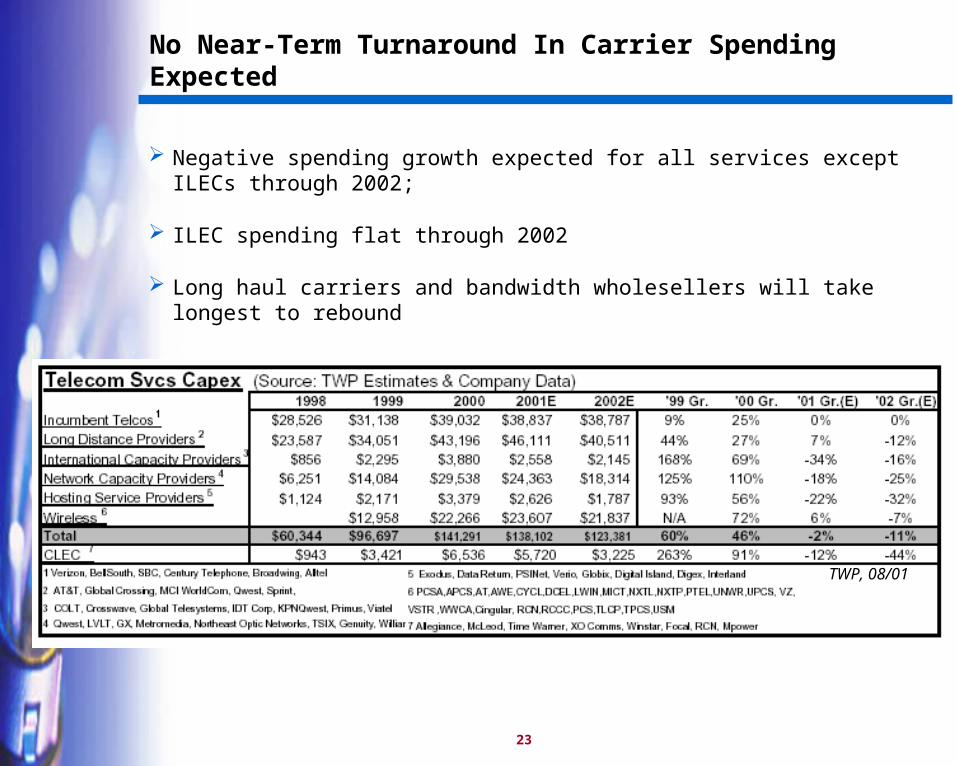

No Near-Term Turnaround In Carrier Spending Expected

Negative spending growth expected for all services except ILECs through 2002;

ILEC spending flat through 2002

Long haul carriers and bandwidth wholesellers will take longest to rebound

TWP, 08/01

24

Carriers Will Work Capex/Sales Ratios Down To Previous Levels

25

No Catalyst On Near Term Horizon To Re-accelerate Spending

Internet traffic volumes still double annually, but growth down by more than 40% from 2000.

Video-on-demand too expensive

Interactive gaming too slow, too expensive

DSL, cable modem deployment growth plodding

Bundled services and distributed storage the next killer apps??

26

Gauging The Timing Of A Recovery

2001 2002 2003 2004

Enterprise, Residence

Service Providers

Equipment Vendors

Component Vendors

Global market demand recovers: manufacturing, servicesCorporate profits improveCorporate hiring improves/stabilizesInterest rates remain lowCapex spending rebounds

Enterprise spending recoversNew differentiated services emergeRevenue/Capex ratio stabilizes. ROI improvesCapital markets open upRegulation eases

Carrier’s financial health improvesMetro bottleneck inhibits carrier revenue growthCapacity glut in long haul begins to dissipateNext gen solutions are rolled out, selectedCarriers re-initiate spending programs

System OEM’s health improvesInventory overhang dissipates – weak impactDemand for next gen components increases - strong impactIncreased integration strengthens margins

Sept 01

Rebound in components market could be more

than 2 year out.

27

The Good: Optical Networking Helps Improve the Capex/Revenue Imbalance …

Lowers the hardware cost/bit by 50% or more over legacy SONET gear, which represented 80% of transmission equipment spending in 2000 (CIBC, 7/01).

Provides a scalable platform - pay as you go – that lowers first installed cost.

Promises to lower operating costs by simplifying provisioning and maintenance

CIBC 7/01

28

… While Future-Proofing The Network

Scales in step with growing capacity needs

Transparent, so accommodates any transmission format and service type, including wavelength services

Reduces need for overlay networks

29

Carrier Spending Is Slowing, But The Distribution Will Slant Towards Optical Networking

Global Capex Spending

Annual Growth Rates

2000 2001

Total

Optical

$306B

$370B

$47B $64B

Total Capex Optical Capex

21%

36%

RHK, 2/01

30

Top Down Forecast Suggests Long-Term Market Growth Remains Robust …

CSFB, 09/01

With these updated numbers, redo chart on next slide. 9-17-01

31

… Even By More Conservative Forecasting Assumptions

Service growth held flat through 2004

Capex held to 19-20% of revenue through 2006, not 23%

Optics percent of total capex held to 30% by 2006, not 35%

Top Down Forecast of Optical Networking Markets ($B)

0

10

20

30

40

50

60

70

2000 2001 2002 2003 2004 2005 2006

Sys

tem

s M

arke

t

0

2

4

6

8

10

12

14

16

Co

mp

on

ents

Mar

ket

Systems

Components

32

Optical Networking Still In Its Infancy

Optical Networking Still In Its Early YearsOptical Networking Still In Its Early Years

1950 1960 1970 1980 1990 2000Semiconductors

IBM 1400 Computer

Apple I Computer

Intel 4004Intel 286

MS Windows

Netscape Navigator

Optical components 1990 2000 2010 2020 2030 2040

Ciena MW 1600

33

Venture Investors Continue To See Strong Potential In Optical Networking

1998 1999 2000 2001 YTD

Number of Investments 22 39 110 73

Aggregate Value of Investments ($M) $138 $479 $2,626 $1,907

Median Size of Investment ($M) $5 $12 $19 $13

Aggregate Value of Venture Investments

Broadview, 8/01

34

Identifying The Pain

35

To Lower Costs, Carriers Need To Simplify Their Networks

Existing networks are expensive:

To design: multiple protocols to support: ATM, IP, TDMTo provision: multiple layers to interface and manageTo maintain: large footprint and high box countTo operate: Each O/E/O interface and box interconnect provides a failure point

Transparent networks should be less expensive:

To design: single protocol – wavelengthsTo provision: single physical layerTo maintain – low box countTo operate - no O/E/O conversions

Shift To Transparency

What Is Needed?True optical switching devicesAdaptive, intelligent solutionsModular, scalable systemsManageable optical architecturesLow cost, high-volume, automated manufacturing

36

The Impact Of Network Simplification On Hardware Cost

Network Element Legacy SONET/WDM

System

Next-Gen SONET/WDM

System

Opaque Optical Networking System

DCSONSOC-192 terminalsWDM terminalsNG DCS/ADMsSpacePower

150

1,92030

03,930 sq ft

8.0 MW

000

30960

505 sq ft1.5 MW

015

030

0105 sq ft150 kW

Total Initial Cost $300m $160m $90m

Typical vendors Alcatel, Fujitsu, Nortel, Lucent, NEC

Ciena/Cyras, Cisco/Cerent, White Rock

Ciena, Sycamore, Tellium, Brightlink

JP Morgan, 5/01

Consider a theoretical LH core network with 15 nodes, populated with 64-channel DWDM systems; each channel at OC-192.

37

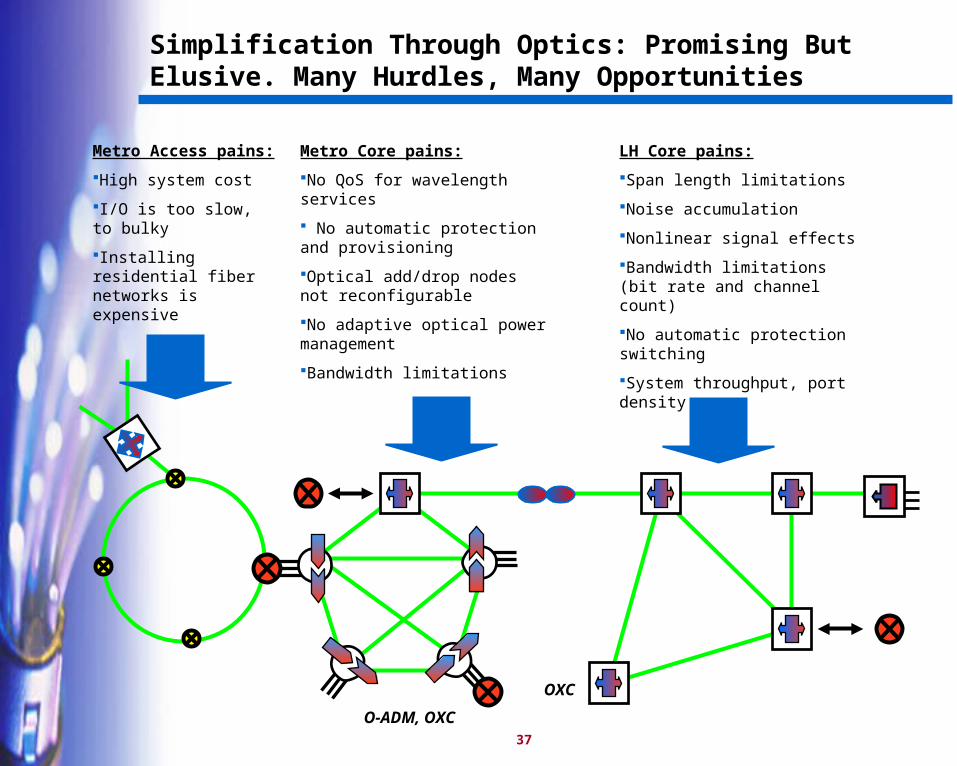

Simplification Through Optics: Promising But Elusive. Many Hurdles, Many Opportunities

O-ADM, OXC

OXC

LH Core pains:

Span length limitations

Noise accumulation

Nonlinear signal effects

Bandwidth limitations (bit rate and channel count)

No automatic protection switching

System throughput, port density

Metro Core pains:

No QoS for wavelength services

No automatic protection and provisioning

Optical add/drop nodes not reconfigurable

No adaptive optical power management

Bandwidth limitations

Metro Access pains:

High system cost

I/O is too slow, to bulky

Installing residential fiber networks is expensive

38

Points Of Pain – The Transition To Optics In Long Haul

Where it hurts The prescription Complication

Span limitations(600 km)

Next generation amplifiers, involving higher powers and distributed amplification. Higher sensitivity receivers. New modulation formats.

Specialty fiber and pump laser technologies immature. High-sensitivity receivers expensive.

Channel limitations(80 channels)

Tighter channel spacing and wide band accessibility

Filter technology slow to improve and wider band amplifiers immature

Noise accumulation Adaptive dispersion compensation Adaptive algorithms slow, devices expensive, large, and lossy

Optical power management is not adaptive

Dynamic gain equalization and management

Adaptive algorithms slow, devices expensive, large, lossy, requiring muxing/remuxing

Non-linear signal interaction

Solutions supporting lower peak and average transmission signal power

Specialty fiber and pump laser technologies immature

Bit rate limitations(10 Gb/s)

Higher speed transceivers High speed optics and driver chips immature, as are alternative modulation solutions

No automatic protection switching

High-speed optical performance monitoring, network management, and optical switching

Commercial solutions for OPM not available. Optical switches remain large and expensive.

Channel blocking due to assignment conflicts

Tunable lasers and all-optical wavelength converters

Low yields, low power, limited tuning range, expensive

System throughput, port density

Transparent optical switching systems and components

Switching engines are tough to manufacture, qualify

39

Points Of Pain – The Transition To Optics In Metro Core And Access

Where it hurts The prescription Complication

No QoS for lambda services High-speed optical performance monitoring

Commercial solutions for OPM not available. Optical switches remain large and expensive.

No automatic protection switching

OPM, plus integrated network management

Commercial solutions not available

Add/drop nodes are not reconfigurable

Low cost wavelength selective switches and tunable filters. Tunable lasers.

Technologies are immature: lossy, power hungry, expensive, low yield, unreliable

Optical power management is not adaptive

Dynamic gain equalization and management

Adaptive algorithms slow, devices expensive, large, lossy, requiring muxing/remuxing

Optical multiplexing is expensive

Lower cost filter assemblies The filters are cheap, the assembly is expensive

Transmitters/receivers are too expensive, too bulky

Tunable lasers and low cost, hot swappable transmitters

Price points are difficult to hit, based on low yields for tunables

Cost/bit of high reliability circuit-based solutions remains expensive for access

Migrate to LAN-originated protocols like Ethernet

Reliability of packet solutions is not carrier class

40

Relieving The Pain

41

Pain Relief

Network Needs Technology Responses

Next generation amplifiers, including higher power amps, lower-cost amplets, wider band amplifying, and distributed amplification

Higher power EDFAsHigher power pump lasers

Lower power EDFA ampletsSOAs

Raman amplifiers and lasersOptical pulse reshaping and retiming

Dynamic gain equalization and management

Dynamic gain equalizersAmplifier arrays

High sensitivity receivers APDs

Enhanced modulation formats Soliton & other ULH solutionsO-TDM solutions

Multilevel transmission solutions

Tighter channel spacing 25-50 GHz WDM filters

Adaptive dispersion compensation Adaptive dispersion compensators (chromatic and PMD)

Higher speed transceivers 40 Gb/s modulators40 Gb/s transceivers

High-speed optical performance monitoring, network management

Optical performance monitoringnetwork management

Tunable lasers and all-optical wavelength converters

Long reach tunable lasersoptical wavelength converters

42

Pain Relief (cont.)

Network Needs Technology Responses

Optical switching systems Optical cross-connect systemsOptical add/drop systems

High-speed, high finesse optical performance monitoring

Optical performance monitoring

Optical switches and tunable filters

MEMs, FBGs, bubble, liquid crystal, EO and TO devices, SOAs, other

technologies

Lower cost filter assemblies CWDM/TFF, AWGs, bulk gratings

Tunable lasers and low cost, hot swappable transmitters

Shorter reach tunable lasersShort and long wavelength VCSELs

SR and VSR transceivers, transponders

43

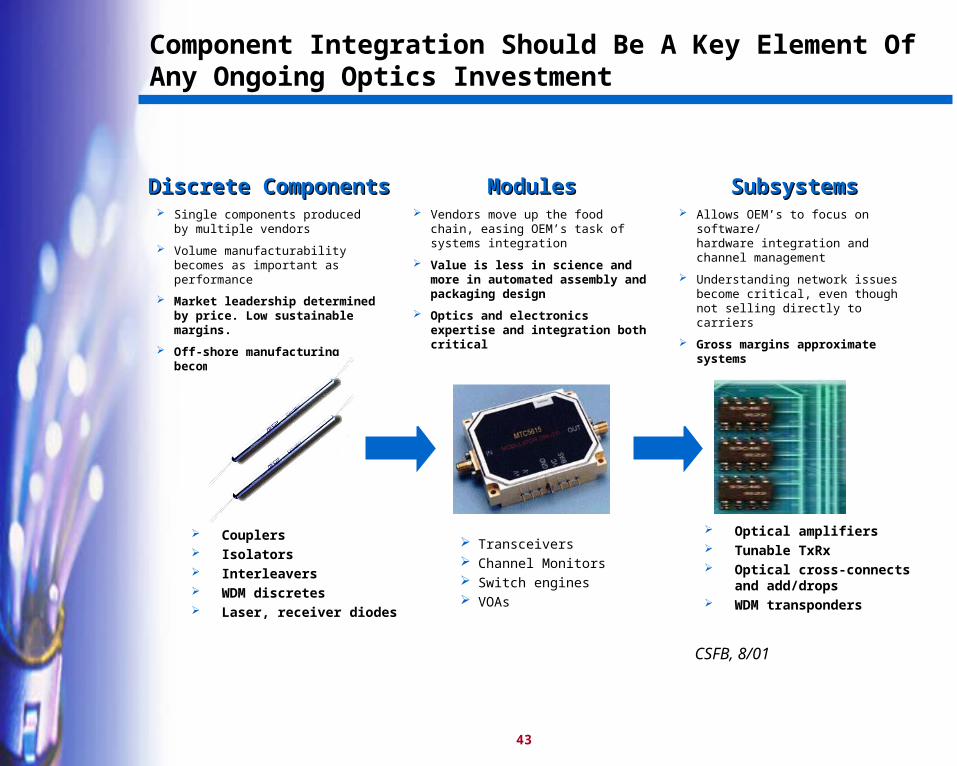

Component Integration Should Be A Key Element Of Any Ongoing Optics Investment

Discrete ComponentsDiscrete Components ModulesModules SubsystemsSubsystems

Transceivers Channel Monitors Switch engines VOAs

Single components produced by multiple vendors

Volume manufacturability becomes as important as performance

Market leadership determined by price. Low sustainable margins.

Off-shore manufacturing becomes norm

Vendors move up the food chain, easing OEM’s task of systems integration

Value is less in science and more in automated assembly and packaging design

Optics and electronics expertise and integration both critical

Allows OEM’s to focus on software/hardware integration and channel management

Understanding network issues become critical, even though not selling directly to carriers

Gross margins approximate systems

Optical amplifiers Tunable TxRx Optical cross-connects

and add/drops WDM transponders

Couplers Isolators Interleavers WDM discretes Laser, receiver diodes

CSFB, 8/01

44

The Impact Of Market Timing On Investment Decisions

Carriers slow spending

Work through inventory

Focus on risk aversion

Little appetite for new gen systems

Little demand for new gen components

Carriers spending re-bounds

Inventory of older gen equipment has been exhausted

New gen solutions will enable dramatic boost to network performance, drop in cost/bit

Opportunity for novel new component technologies. Incremental upgrades to older technologies won’t keep up.

2000 2001 2002 2003 2004 2005 2006

Systems

Components

Market dominated by:

static systems

discrete components

Market dominated by:

Dynamic, automated systems

Integrated, tunable components

Winter of Despair Spring of Hope

45

Investment Conclusions

Invest selectively now for the Spring of Hope

Focus on early stage companies that provide new approaches to network optimization:– Low cost– Integration– Tunable, adaptive– Automated operation– High bandwidth– Transparency

Avoid later-stage companies that provide incremental improvements to older generation equipment. If budget assumes substantial ramp in 2002, 2003 revenue, be wary.– Give little weight to OEM penetration, given the uncertainty of equipment markets and

players

Survive the Winter of Despair– See funding well into 2003– Keep burn low– Avoid high capitalization companies that are vulnerable to extended Winter