41

#WorldInCommon AGENCE FRANÇAISE DE DÉVELOPPEMENT | FRENCH DEVELOPMENT AGENCY Investors presentation March 2018

| Date post: | 18-May-2018 |

| Category: |

Documents |

| Upload: | nguyenkien |

| View: | 218 times |

| Download: | 3 times |

#WorldInCommon AGENCE FRANÇAISE DE DÉVELOPPEMENT | FRENCH DEVELOPMENT AGENCY

Investors presentation

March 2018

2 March 2018 Investors presentation

AFD at a glance

3

AFD: the French Development Agency AFD at a glance

March 2018 Investors presentation

Established in 1941, Agence Française de Développement (“AFD”) is the

bilateral Development Bank of France:

AFD’s missions consist in financing infrastructure and urban development, water and sanitation, agriculture,

education, health, environment and natural resources, private sector development

AFD’s activities are aimed at:

Reducing poverty and

inequalities

Promoting sustainable economic growth

Reducing negative climate change impacts

Promoting biodiversity, social and environmental responsibility

AFD :

Is 100% owned by the French State

Is an EPIC subject to Banking Regulation

Is AA rated by Fitch and

S&P

Is qualified as “Advanced” by Vigeo and is rated Prime Status by Oekom

4

A fresh impetus to French development policy

French Government relies on AFD to conduct and strengthen Public Aid :

End of 2016, French State strengthened AFD’s capital by turning EUR 2.4Bn subordinated loans (Tier

2) into Core Tier One capital

From 2016, an increase of commitments of EUR 1Bn/y until 2020, to reach a target of a EUR 4Bn

increase per year

From EUR 8.3Bn/y in total in 2015 to EUR 12.5Bn/y in total in 2020. In 2016, EUR 9.4Bn were approved

President Macron set for French public aid the objective to reach 0.55% of GDP by 2022

Commitments have been taken to support sustainable development and fight against climate

change

With climate as the top priority :

France hosted in 2015 the COP 21, Its commitments to support sustainable development and fight

against climate were confirmed during the last One Planet Summit in Paris on December 12th, 2017

Large part of French commitments in contribution to reduce green house gases will be provided

by AFD in the coming years

Half of the increase of AFD’s commitments will concern Climate projects (mitigation, adaptation

and budget support)

From EUR 3Bn/y in 2015 to EUR 5Bn/y of Climate projects in 2020. In 2016, EUR 3.58Bn were

approved

March 2018 Investors presentation

AFD at a glance

5

AFD operates in most of the emerging and emerged markets

AFD operates also in French overseas territories

(1.6bn€ in 2016, representing 17% of the commitments of AFD group)

March 2018 Investors presentation

AFD at a glance

6

AFD and its foreign partners

March 2018 Investors presentation

AFD at a glance

Partnerships with IBRD, EIB, KFW, ADB, …

AFD is a recognized institution amongst Development Banks

Since October 2017, our CEO Remy Rioux

has had the honour to lead the IDFC* which

brings together 23 development banks.

With USD 630 bn of commitments per year,

they are trying to reach ambitious goals in terms of sustainable

development.

It makes this worldwide organization the main

provider of public

finance for development.

* International Development

Finance Club

7 March 2018 Investors presentation

Status & Credit profile

8

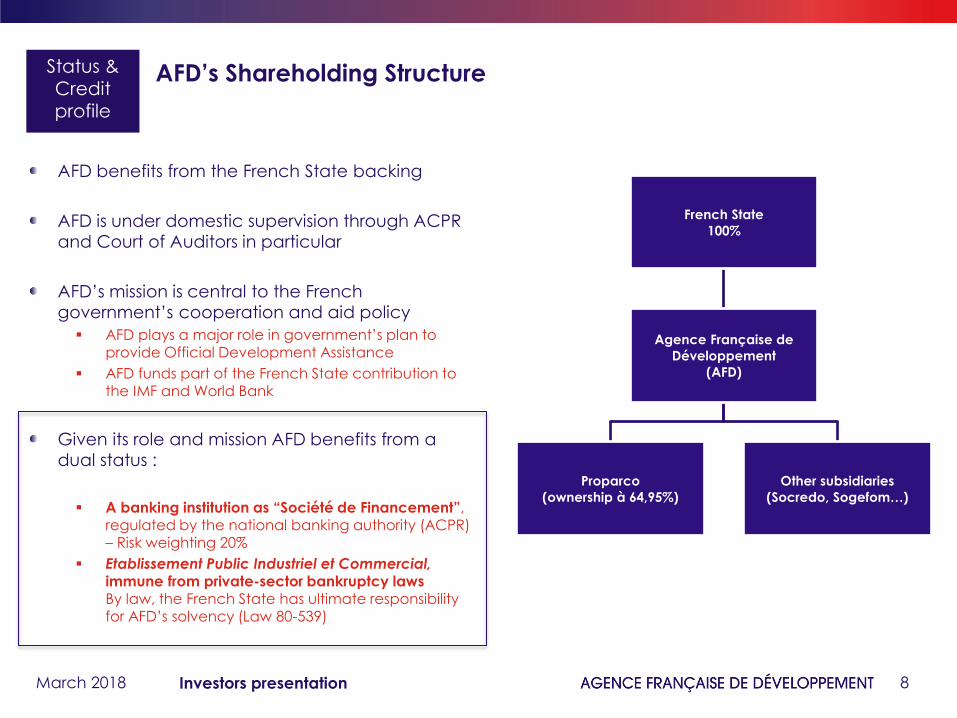

AFD’s Shareholding Structure

AFD benefits from the French State backing

AFD is under domestic supervision through ACPR

and Court of Auditors in particular

AFD’s mission is central to the French

government’s cooperation and aid policy

AFD plays a major role in government’s plan to

provide Official Development Assistance

AFD funds part of the French State contribution to the IMF and World Bank

Given its role and mission AFD benefits from a

dual status :

A banking institution as “Société de Financement”, regulated by the national banking authority (ACPR) – Risk weighting 20%

Etablissement Public Industriel et Commercial, immune from private-sector bankruptcy laws By law, the French State has ultimate responsibility for AFD’s solvency (Law 80-539)

March 2018 Investors presentation

Status & Credit

profile

French State

100%

Agence Française de

Développement

(AFD)

Proparco

(ownership à 64,95%)

Other subsidiaries

(Socredo, Sogefom…)

9

AFD benefits from High Quality Ratings

March 2018 Investors presentation

Status & Credit profile

AA/Outlook Stable

Short-Term A-1+

AA/Outlook Stable

Short-Term F1+

04/10/2017

“AFD ratings are aligned with those of the French state, reflecting its strong legal status as an EPIC, strategic importance to France, strong control by the French state and, to a lesser degree, integration with the state.”

“EPIC status reflects the ultimate responsibility of

the French state for AFD’s solvency and liquidity under the law of 16 July 1980. “

“recent change of status does not affect the EPIC

status“

“Because AFD has EPIC status, we view the French government as ultimately responsible for AFD's solvency.”

“We therefore equalize our long-term rating on AFD with our long-term sovereign rating on

France.”

AA/AA rating linked to dual-entity status and public nature of AFD’s mission

22/02/2017

10

AFD : a recognized Corporate Responsibility

March 2018 Investors presentation

Status & Credit profile

AFD is rated by two of the world’s leading rating agencies in the segment of sustainable investments

Last update: september 2017

AFD 2nd in the panel of 15 Specific Purpose Banks & Agencies

11 March 2018 Investors presentation

Financial Performance

& Risk Management

12

Key figures

March 2018 Investors presentation

Financial perf. RIsk manag.

IFRS (€ million) 2014 2015 2016

Total balance sheet 31,243 35,834 37,749

Consolidated capital 5,484 5,561 5,860

Loan outstanding 24,570 27,504 30,146

Net banking income 508 594 724

Operating profit 141 188 283

Pre-tax income 146 199 292

Net income 120 173 246

13

AFD Boasts Strong Capitalisation

AFD benefits from a

strong capitalisation,

well above the

regulatory minimums

Conversion of €2,4 Bn

of T2 into CET1 in 2016

March 2018 Investors presentation

Financial perf. RIsk manag.

AFD: Capital ratios

Regulatory capital ratios 2014 2015 2016

Capital adequacy ratio 19.05% 16.72% 16.82%

Minimum regulatory level 8% 8% 8.625%

T1 Ratio 8.71% 9.42% 16.82%

Minimum regulatory level 5.5% 6% 6.625%

CET1 Ratio 9.69% 8.70% 15.22%

Minimum regulatory level 4% 4.5% 5.125%

14

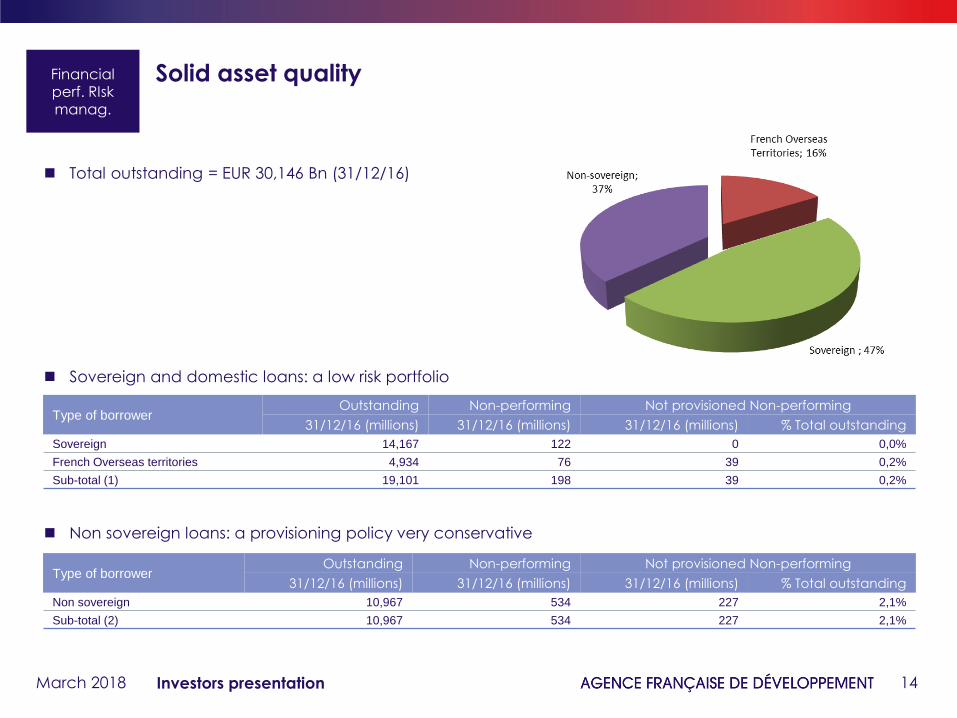

Solid asset quality

March 2018 Investors presentation

Financial perf. RIsk manag.

Total outstanding = EUR 30,146 Bn (31/12/16)

Sovereign and domestic loans: a low risk portfolio

Non sovereign loans: a provisioning policy very conservative

Type of borrower Outstanding Non-performing Not provisioned Non-performing

31/12/16 (millions) 31/12/16 (millions) 31/12/16 (millions) % Total outstanding

Non sovereign 10,967 534 227 2,1%

Sub-total (2) 10,967 534 227 2,1%

Type of borrower Outstanding Non-performing Not provisioned Non-performing

31/12/16 (millions) 31/12/16 (millions) 31/12/16 (millions) % Total outstanding

Sovereign 14,167 122 0 0,0%

French Overseas territories 4,934 76 39 0,2%

Sub-total (1) 19,101 198 39 0,2%

15

Conservative Risk Management

Exchange and interest rate risk All issues and loans swapped into Euros Single currency exposure < 1% of Consolidated

Capital Global forex position < 2% of Consolidated Capital No speculative trading

Liquidity risk Treasury ≥ 3 months of cash outflows (current treasury

equivalent to around 7,15 months of cash outflows) A CD and BMTN issue program of EUR 2Bn each A EUR 550 mn investment portfolio (100% ≥ AA)

eligible to repo market (5 to 7 years duration) A EUR 1,163 bn dynamic portfolio (2 to 3 years

duration)

Counterparty risk Minimum A1/P1 for short term investments, except

through UCITS (limited to 35% A2/P2) AAA/AA SSA euro zone for the investment portfolio

with small limit until BBB rating for dynamic portfolio Weekly ratings monitoring and collateral contracts

(move to daily margining on track) Clearing IRS under EMIR regulation, trades are

currently being onboard

March 2018 Investors presentation

Financial perf. RIsk manag.

Investment & LCR portfolio of € 1,93Bn c. Last update 28Feb2018

16 March 2018 Investors presentation

Capital Markets Activities

17

Capital Market Highlights

An increasing trend towards funding :

An increase in the commitments of EUR 1Bn per year until 2020 will impact disbursements

Upward trend to support disbursements growth

Amortization of older loans will partly finance this growth

March 2018 Investors presentation

Capital

Markets

AFD's disbursements (loans) (EUR millions)

Funding program (EUR millions)

Forecast Forecast

4 800 5 100 4 892

6 233 6 770

6 400 6 600

5 700

6 700

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2014 2015 2016 2017 2018 2019 2020 2021 2022

4 200

3 400

4 463

5 597 5 800 5 300

5 900

6 700

7 300

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2014 2015 2016 2017 2018 2019 2020 2021 2022

18

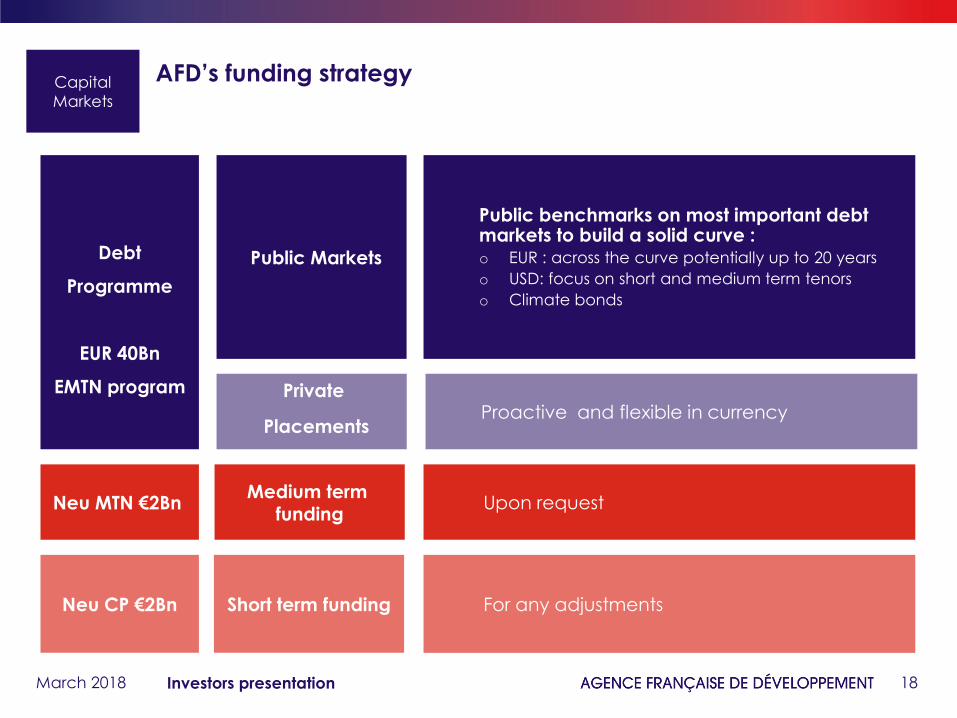

AFD’s funding strategy

March 2018 Investors presentation

Capital

Markets

Public Markets

Medium term funding

Private

Placements

Debt

Programme

EUR 40Bn

EMTN program

Short term funding

Neu CP €2Bn

Neu MTN €2Bn

Public benchmarks on most important debt markets to build a solid curve :

o EUR : across the curve potentially up to 20 years

o USD: focus on short and medium term tenors

o Climate bonds

Proactive and flexible in currency

Upon request

For any adjustments

19

AFD’s funding strategy

3 main axes will feed the development of volumes :

1. Explore less sollicited segments of the curve

o Short end (1 to 3 years)

o Long end (>12 years)

2. More active approach of the private placements market

o More frequent prices on PPs

o Non-vanilla coupon structures

3. Green bond

o New framework is currently being studied

o More frequent issuances

March 2018 Investors presentation

Status & Credit profile

20

2017 funding program

March 2018 Investors presentation

Capital

Markets

2018 funding program : EUR 6,77 Bn

• 60% to 80 %:

EUR public issues (1Y => 15Y)

USD public issues (2Y => 5Y)

• 20% to 40%:

Private placements

Bloomberg ticker : AGFRNC

Issue date Amount (m) Currency Coupon Tenor Maturity Type

1 400 EUR 1% 10Y janv-28 Public

2018 50 EUR 1,593% 20Y janv-38 Private

200 EUR 0% 2Y janv-20 Private

TOTAL 1 650 EUR Mn eq.

200 USD FRN 1,8Y sept-19 Tap

100 EUR 1,112% 13,5Y juin-31 Private

750 EUR 0,125% 6Y nov-23 Public

205 EUR 1,715% 20Y oct-37 Private

500 USD FRN 2Y sept-19 Private

150 EUR 1,375% 15Y juil-32 Tap

1 250 USD 1,875% 3Y sept-20 Public

350 EUR 1,375% 15Y juil-32 Tap

2017 50 AUD 3,538% 10Y juil-27 Private

300 USD FRN 2Y juil-19 Private

1 000 EUR 1,375% 15Y juil-32 Public

250 EUR 0,375% 7Y avr-24 Tap

1 500 EUR 0,125% 5Y avr-22 Public

TOTAL 6 233 EUR Mn eq.

1 000 EUR 0,13% 5Y avr-21 Public

150 EUR 0,00% 2,5Y déc-18 Private

50 EUR FRN 2Y févr-18 Tap

2016 200 USD FRN 2Y mars-18 Private

250 EUR 0,875% 15Y juin-31 Private

1 500 EUR 0,25% 10Y juil-26 Public

1 000 USD 1,375% 3Y août-19 Public

850 EUR 0,375% 7Y avr-24 Public

TOTAL 4 892 EUR Mn eq.

2015

250 USD 1,625% 5Y janv-20 Tap

250 GBP 0,75% 2Y mars-17 Public

1 000 EUR 0,875% 16Y mai-31 Public

500 USD FRN 3Y févr-18 Public

500 EUR 2,25% 6Y févr-21 Tap

1 000 USD 1,625% 5Y janv-20 Public

65 EUR 2,125% 6Y févr-21 Tap

20 EUR 2,125% 6Y févr-21 Tap

100 EUR 3,625% 5Y avr-20 Tap

100 EUR 3,625% 5Y avr-20 Tap

500 USD 1,375% 3Y août-18 Public

50 AUD 3,630% 10Y sept-25 Private

1 000 EUR 0,500% 7Y oct-22 Public

21

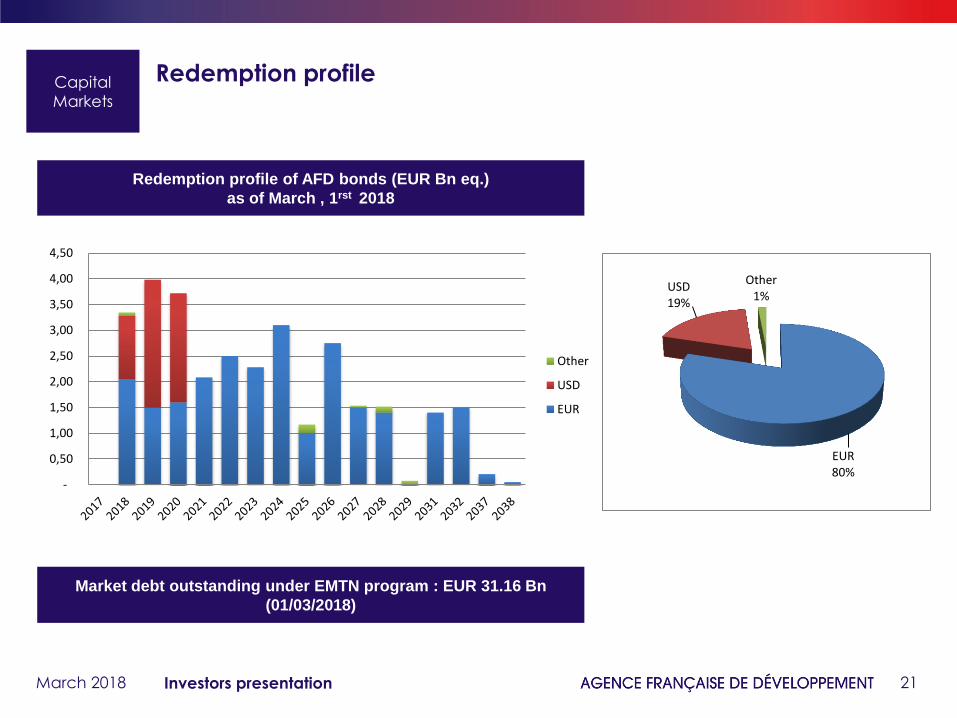

Redemption profile

March 2018 Investors presentation

Capital

Markets

Market debt outstanding under EMTN program : EUR 31.16 Bn

(01/03/2018)

Redemption profile of AFD bonds (EUR Bn eq.)

as of March , 1rst 2018

-

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

4,50

Other

USD

EUR

EUR 80%

USD 19%

Other 1%

22

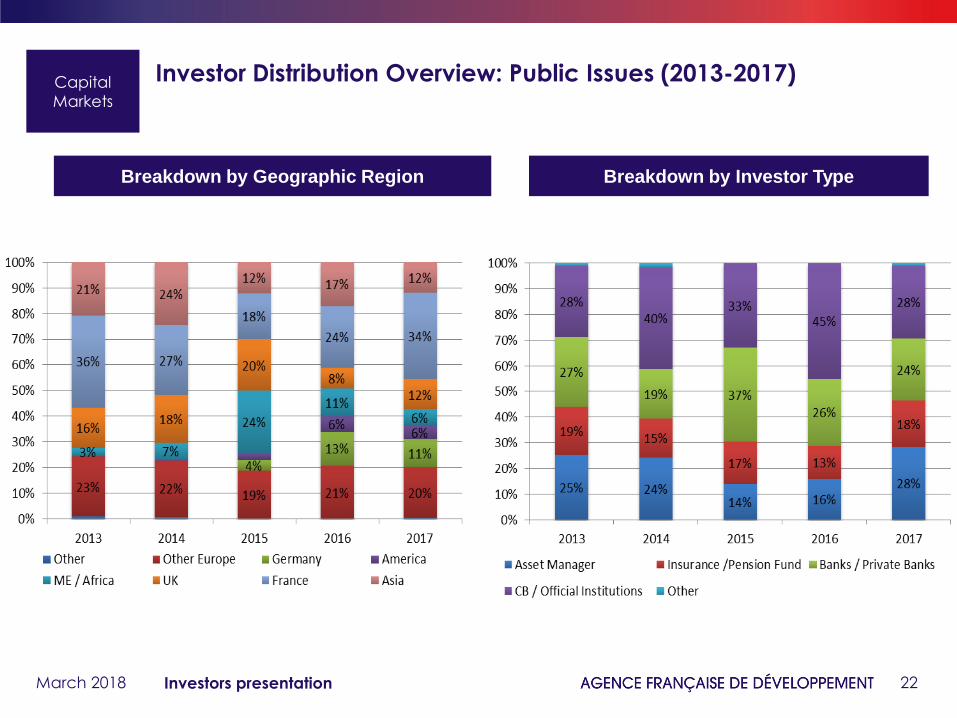

Investor Distribution Overview: Public Issues (2013-2017)

March 2018 Investors presentation

Capital

Markets

Breakdown by Geographic Region Breakdown by Investor Type

23 March 2018 Investors presentation

New climate bond framework

24

New ambition – New approach

Programatic approach

o Creation of a persistent framework

o The broadening of the asset pool and the governance for it have been part of the framework

Ensuring a more frequent presence on the green bond market

o Benchmark size

o Different tenors

o Every 12 to 18 month minimum

Keeping the bond specifics in line with AFD climate strategy,

But better reflecting the nature, variety and complexity of AFD underlying

business

o Mitigation

o But also adaptation, credit lines, potentially budget support

March 2018 Investors presentation

Climate

bond

Framework

25

The framework is fully aligned with the Green Bond Principles

AFD is a member of the GBP

The framework has been designed in accordance with the 4 GBP

components :

1. Use of procceds

2. Process for project evaluation and selection

3. Management of proceeds

4. Reporting

Also follows the recommendation on external review

o Second party opinion : Cicero + annual review by auditors

March 2018 Investors presentation

Climate

bond

Framework

26

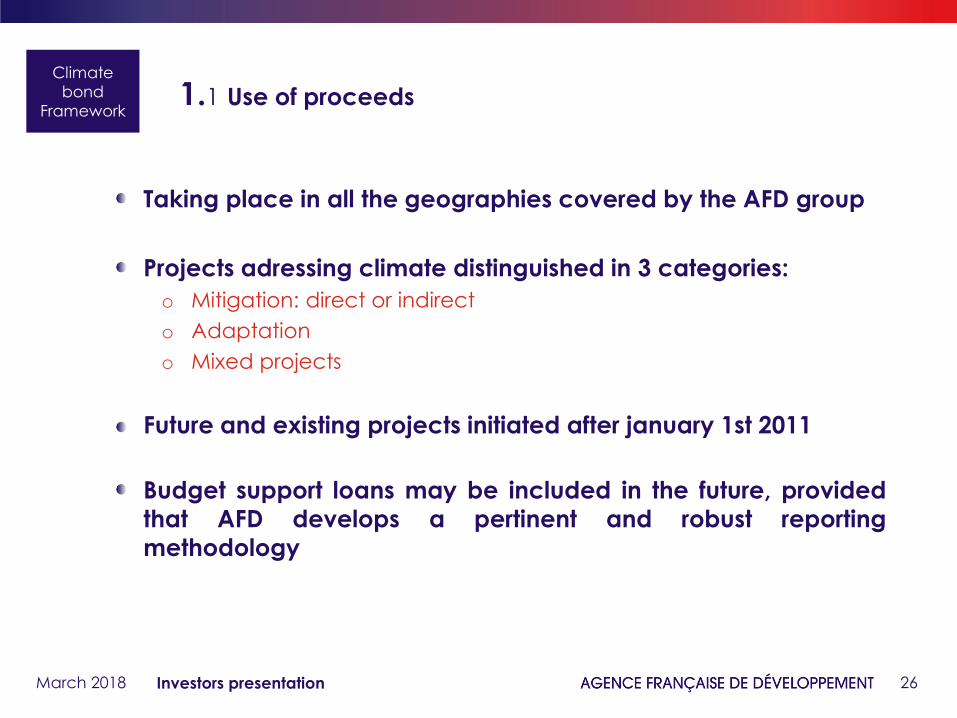

1.1 Use of proceeds

Taking place in all the geographies covered by the AFD group

Projects adressing climate distinguished in 3 categories:

o Mitigation: direct or indirect

o Adaptation

o Mixed projects

Future and existing projects initiated after january 1st 2011

Budget support loans may be included in the future, provided

that AFD develops a pertinent and robust reporting

methodology

March 2018 Investors presentation

Climate

bond

Framework

27

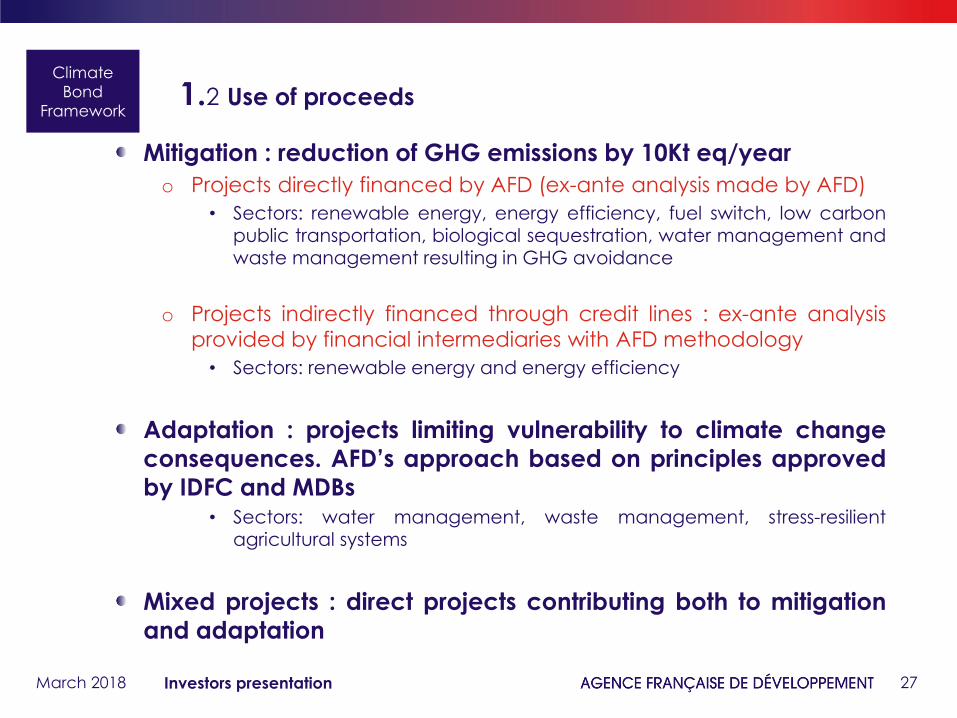

1.2 Use of proceeds

Mitigation : reduction of GHG emissions by 10Kt eq/year

o Projects directly financed by AFD (ex-ante analysis made by AFD)

• Sectors: renewable energy, energy efficiency, fuel switch, low carbon public transportation, biological sequestration, water management and waste management resulting in GHG avoidance

o Projects indirectly financed through credit lines : ex-ante analysis

provided by financial intermediaries with AFD methodology

• Sectors: renewable energy and energy efficiency

Adaptation : projects limiting vulnerability to climate change

consequences. AFD’s approach based on principles approved

by IDFC and MDBs • Sectors: water management, waste management, stress-resilient

agricultural systems

Mixed projects : direct projects contributing both to mitigation

and adaptation

March 2018 Investors presentation

Climate

Bond

Framework

28

1.3 Use of proceeds

Mitigation examples – projects directly financed by AFD

o Renewable energy :

AFD participated in the cofinancing of Ouarzazate’s solar program (total power of more than 500MW, among a Moroccan plan of 2 000MW) through two AFD loans totalizing EUR 150M, whose impact is evaluated at 1 200 Ktons eq / year.

https://www.afd.fr/fr/la-plus-grande-centrale-solaire-du-monde-ouarzazate

o Low carbon public transportation :

Namma metro in Bengalore: A USD 1.3 billion program to build about 100 kilometers

of railway. AFD loaned EUR 110M toward the program, which is co-financed by Japan (JICA) and the Asian Development Bank. After completion, the metro will carry 1.5 million passengers per day. Impact : reduction of CO2 emissions by 230 Ktons eq / year

http://www.afd.fr/base-projets/consulterProjet.action?idProjet=CIN1062

Mitigation examples – projects financed through credit lines

o A 100M€ loan to Halkbank in Turkey, supporting private investments in renewable energy and efficiency to 104 sub-projects

https://www.sunref.org/en/projet/turkish-smes-key-stakeholders-for-a-sustainable-use-of-energy-in-

turkey/

March 2018 Investors presentation

Climate

Bond

Framework

29

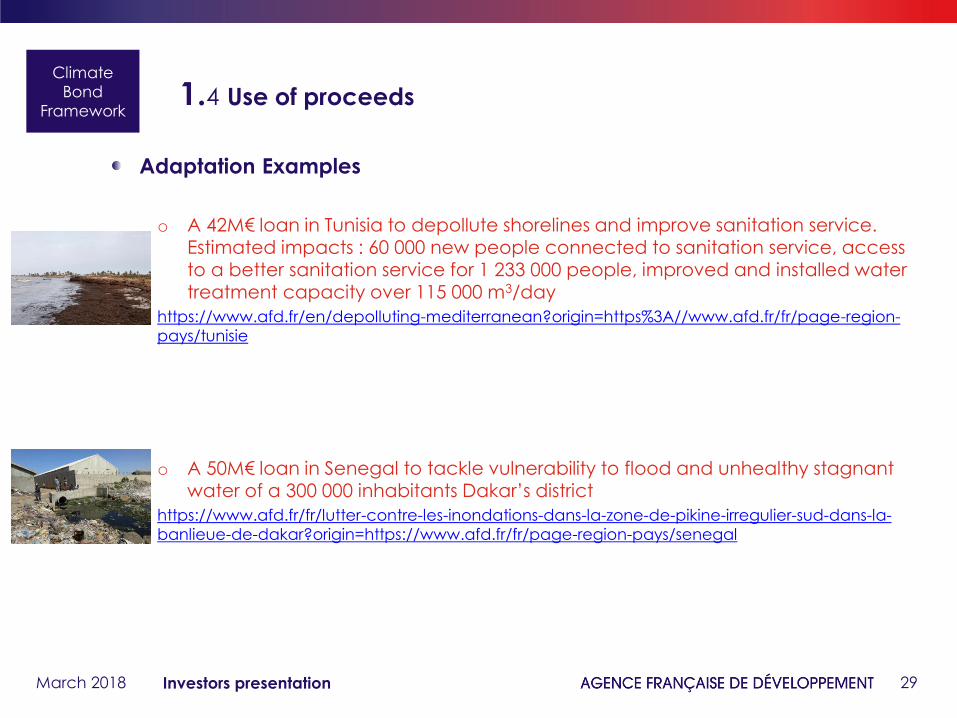

1.4 Use of proceeds

Adaptation Examples

o A 42M€ loan in Tunisia to depollute shorelines and improve sanitation service. Estimated impacts : 60 000 new people connected to sanitation service, access to a better sanitation service for 1 233 000 people, improved and installed water treatment capacity over 115 000 m3/day

https://www.afd.fr/en/depolluting-mediterranean?origin=https%3A//www.afd.fr/fr/page-region-

pays/tunisie

o A 50M€ loan in Senegal to tackle vulnerability to flood and unhealthy stagnant water of a 300 000 inhabitants Dakar’s district

https://www.afd.fr/fr/lutter-contre-les-inondations-dans-la-zone-de-pikine-irregulier-sud-dans-la-

banlieue-de-dakar?origin=https://www.afd.fr/fr/page-region-pays/senegal

March 2018 Investors presentation

Climate

Bond

Framework

30

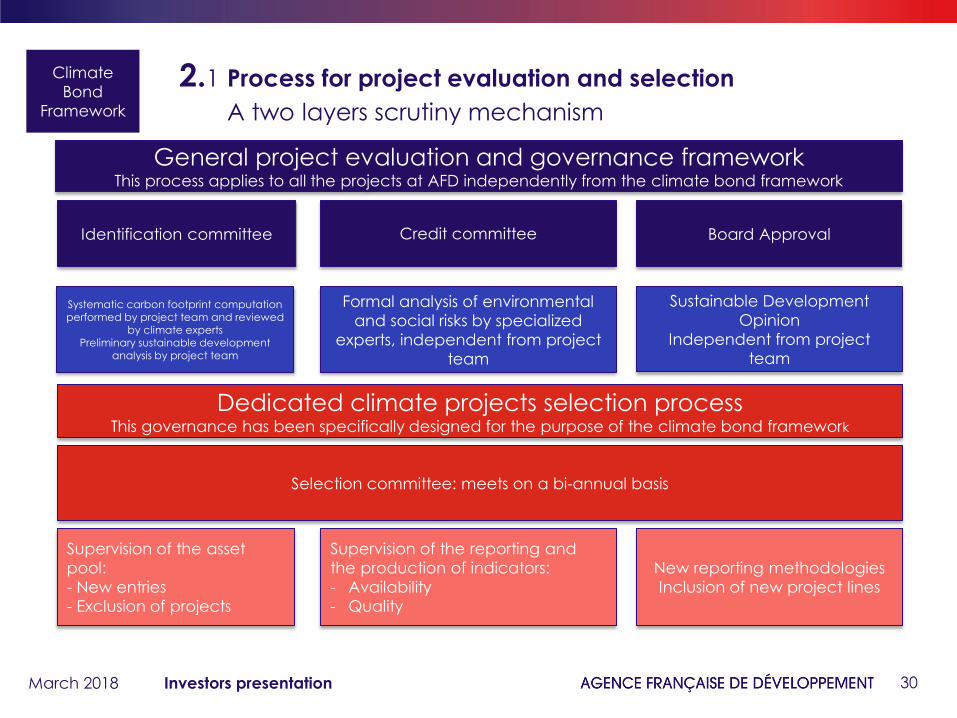

2.1 Process for project evaluation and selection

A two layers scrutiny mechanism

March 2018 Investors presentation

Climate

Bond

Framework

General project evaluation and governance framework This process applies to all the projects at AFD independently from the climate bond framework

Identification committee

Sustainable Development

Opinion

Independent from project

team

Credit committee Board Approval

Systematic carbon footprint computation performed by project team and reviewed

by climate experts Preliminary sustainable development

analysis by project team

Formal analysis of environmental

and social risks by specialized

experts, independent from project

team

Dedicated climate projects selection process This governance has been specifically designed for the purpose of the climate bond framework

Selection committee: meets on a bi-annual basis

New reporting methodologies

Inclusion of new project lines

Supervision of the asset

pool:

- New entries

- Exclusion of projects

Supervision of the reporting and

the production of indicators:

- Availability

- Quality

31

2.2 Process for project evaluation and selection

Carbon footprint methodology

March 2018 Investors presentation

Climate

bond

Framework

Gases measured :

o Carbon Dioxide (CO2), which results primarily from combusting fossil fuels and from

producing aluminium, steel, cement and glass.

o Methane (CH4), which results from burning and/or decomposing biomass (organic material) and

from producing and/or refining gasoline and natural gas.

o - Nitrous Oxide (N2O), which results from incinerating solid waste, spreading fertilizers, and/or

various transportation means.

o Hydrofluorocarbons (HFC), which occur as a by-product of industrial processes making insulation,

refrigeration and air conditioning.

o Perfluorocarbons (PFC), which occur as a by-product of aluminium production.

o Sulphur hexafluoride (SF6), which is used for insulation and current interruption in electricity

transmission and distribution equipment and electronic systems.

CO2 equivalent: a common measurement unit for GHG impacts

Sources of emissions

o Project ‘Construction Phase’ emissions sources

o Project ‘Operating Phase’ emissions sources

32

2.2 Process for project evaluation and selection

Carbon footprint methodology

March 2018 Investors presentation

Climate

Bond

Framework

Scope o Scope 1 = Direct GHG emissions, from sources directly related to a project’s activity, e.g.,

combustion, etc.

o Scope 2 = Electricity indirect GHG emissions, from the generation of purchased electricity

and/or heat needed for the project’s activity.

o Scope 3 = Other indirect GHG emissions, from the production of materials purchased from other

parties and used in the project’s activity, e.g., production and/or extraction of purchased materials,

waste disposal, and use of sold products and services.

The methodology used to measure the GHG emissions of AFD-financed projects accounts for

direct and indirect emissions, both up- and downstream from a project, as per Scopes 1, 2 and 3.

Project lifetime o The standard lifetimes are set as:

• 50 years for dams

• 30 years for transportation infrastructure

• 20 years for other projects

Reference situation o The standard reference situation represents a situation without the project

o EXCEPT for renewables, where the reference situation represents the country’s energy

mix.

33

2.3 Process for project evaluation and selection

E & S risk management process

March 2018 Investors presentation

Climate

bond

Framework

Step 1 – Identification of the projects:

o Exclusion list

o Criteria for sustainable development (positive impacts of the projects)

• Sustainable and resilient growth

• Social well-being and inequalities reduction

• Gender equality and empowerment of women and girls

• Biodiversity protection and natural resources management

• Transition to a low carbon development (mitigation)

• Resilience to Climate Change (adaptation)

• Governance and lost lasting effects of the project

o E&S categorization that reflects the "level of E&S risk" of the project based on the nature of the operation, location and

sensitivity of the affected area, the severity of the potential E&S risks and impacts, client’s capacity to manage them

• Category A [High Risks]: Negative impacts may extend beyond the area of infrastructure right-of-way or extend

beyond the period of construction and operation.

• Category B + [Significant risks]: Negative impacts may extend beyond the area of infrastructure right-of-way or

extend beyond the period of construction and operation but be easily identified and mitigated by appropriate

measures.

• Category B [Moderate Risks]: Negative environmental or social impacts that are potentially reversible, or limited in

space and time, and whose sensitivity to the environment is less. They can be easily identified and mitigated by

appropriate measures.

• Category C [Low Risk]: Potential negative environmental or social impacts are minimal or non-existent

34

2.3 Process for project evaluation and selection

E & S risk management process

March 2018 Investors presentation

Climate

bond

Framework

Step 2 – Evaluation of the project :

o E&S Due-diligences and standards depending on the categorization:

• Different tools for the E&S assessment: E&S Impact Assessment, Resettlement Action Plan, E&S audit, and specific

studies depending on the risks (gender action plan, biodiversity plan, vulnerability study…)

• In line with local regulations and World Bank Standards for A/B+ projects

• In coordination with the feasibility studies

• Before financing approval

o E&S risk management process reducing the risks and improving the quality of the projects

Step 3 – Loan agreement

o E&S clauses => compliance with regulation and standards, reporting…

o E&S Commitment Plan for A/B+/B projects; will define specific E&S clauses to mitigate negative impacts, based on the gaps identified during the Due-Diligence

Step 4 – Monitoring during the execution of the project

o Based on E&S reports, E&S audits, AFD E&S experts’ visits

o To ensure effective implementation of the defined measures of the ESMP, RAP and ESCP

o To identify any unforeseen event (accident, complaint…)

o To adapt if needed the E&S management system of the project

o To support the beneficiary in improving the E&S performances of the project

o Complaint mechanism

35

3. Management of proceeds

Assets and liabilities perspective

Volume of issues ≤ 75% Asset pool

Insures immediate use of the sums invested

Enables to substitute some assets in the pool, in case of

controversies, or if data are insufficient for example

Very flexible approach in terms of tenors and volume

March 2018 Investors presentation

Climate

bond

Framework

36

4.1 Reporting

Reporting is published on a yearly basis

In order to provide the investors with some context, it is embbeded into the corporate social responsibility report

Report on assets and liabilities

For mitigation projects : Carbon footprint by sectors and by regions + examples

For adaptation : examples + output measures when available and relevant

March 2018 Investors presentation

Climate

Bond

Framework

Budget support projects included in the pool if and only if reporting methodology (still to be designed) is deemed sound enough by the selection committee

37

4.2 Reporting

March 2018 Investors presentation

Climate

Bond

Framework

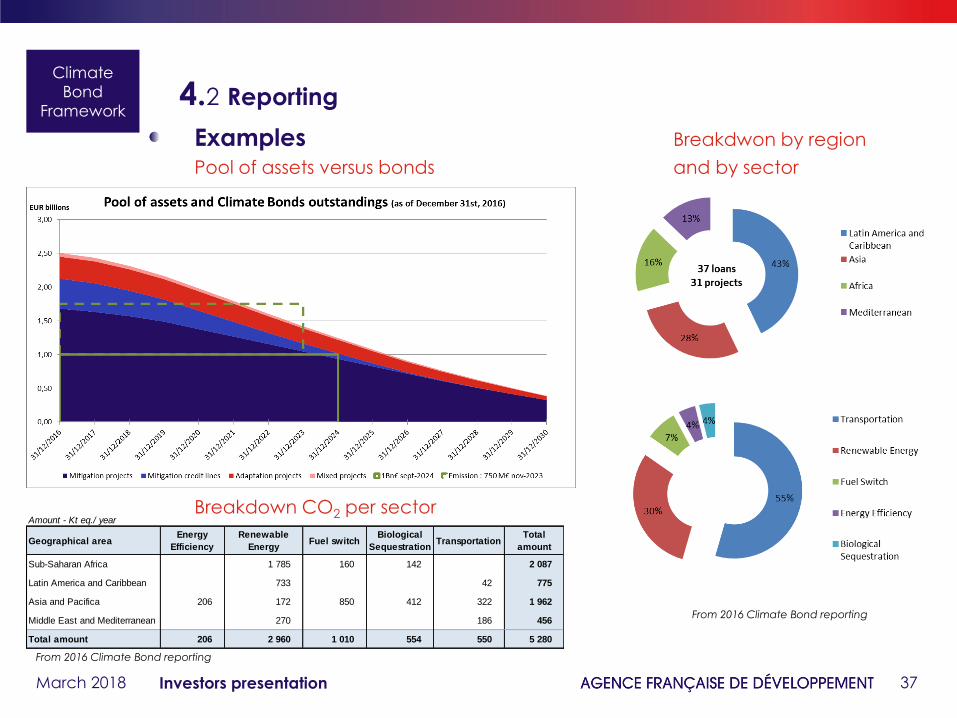

Examples Breakdwon by region

Pool of assets versus bonds and by sector

Breakdown CO2 per sector

From 2016 Climate Bond reporting

From 2016 Climate Bond reporting

Amount - Kt eq./ year

Geographical areaEnergy

Efficiency

Renewable

EnergyFuel switch

Biological

SequestrationTransportation

Total

amount

Sub-Saharan Africa 1 785 160 142 2 087

Latin America and Caribbean 733 42 775

Asia and Pacifica 206 172 850 412 322 1 962

Middle East and Mediterranean 270 186 456

Total amount 206 2 960 1 010 554 550 5 280

38

External review

AFD’s Climate Bond Framework

https://www.afd.fr/sites/afd/files/2017-10/afd-climate-bond-framework.pdf

Climate Bond Framework reviewed by Cicero

o Overall assessment : « medium green »

o According to Cicero’s rating sectors, 66% of AFD’s projects in the 2016

Climate Bond reporting would have been « dark green »

o Strong governance structure

o Link : https://www.afd.fr/sites/afd/files/2017-10/cicero-second-opinion-

afd-climate-bond-framework.pdf

Annual reporting certificated by AFD’s auditors

March 2018 Investors presentation

Climate

bond

Framework

39

AFD Highlights

The French bilateral aid agency

o Established in 1941, entirely state-owned and controlled by the State, AFD benefits from the EPIC status

o Fulfil the ODA and Climate Change government policy

o Activity boosted with adding EUR 4Bn per year of commitments from 2020

Fully regulated by the ACPR (Autorité de Contrôle Prudentiel et de Résolution)

o Strong Basel II Capital Adequacy Ratio at 16,82%

o Strong Tier One ratio at 15,22%

AA / AA ratings by Fitch and S&P

o Conservative credit risk and provisioning policy backed by French State guarantees for non-

performing sovereign loans

o Prudent market risk management framework

Recurrent EUR and USD Benchmark Issuer

o 20% risk weighting under Basel II

o Euro transactions are ECB eligible as “Recognised Agency” https://www.ecb.europa.eu/ecb/legal/pdf/oj_jol_2016_014_r_0006_en_txt.pdf; https://www.ecb.europa.eu/mopo/assets/standards/marketable/html/index.en.html)

“Advanced” overall CSR performance by Vigeo and “Prime status” by Oekom

Climate Bond Framework assessed “medium green” by Cicero

March 2018 Investors presentation

40

Contacts

March 2018 Investors presentation

Funding team contact : [email protected]

Agence Française de Développement

5, rue Roland Barthes

75598 PARIS CEDEX 12

Internet : //www.afd.fr

Françoise Lombard CFO

Thibaut Makarovsky Head of Funding and Market Operations

Demba Tandia & Margaux Adida Funding Officers

Bokar Cherif Head of Treasury and Capital Markets

Samia Ben Mebarek Deputy Head of Funding and Market Operations

41 March 2018

Disclaimer These materials have been prepared by and are the sole responsibility of AFD (the “Company”) and have not been verified,

approved or endorsed by any lead manager, bookrunner or underwriter retained by the Company.

These materials are provided for information purposes only and do not constitute, or form part of, any offer or invitation to underwrite, subscribe for or otherwise acquire or dispose of, or any solicitation of any offer to underwrite, subscribe for or otherwise acquire or dispose of, any debt or other securities of the Company (“securities”) and are not intended to provide the basis for any credit or any other third party evaluation of securities. If any such offer or invitation is made, it will be done so pursuant to separate and distinct documentation in the form of a prospectus, offering circular or other equivalent document (a "prospectus") and any decision to purchase or subscribe for any securities pursuant to such offer or invitation should be made solely on the basis of such prospectus and not these materials.

These materials should not be considered as a recommendation that any investor should subscribe for or purchase any securities. Any person who subsequently acquires securities must rely solely on the final prospectus published by the Company in connection with such securities, on the basis of which alone purchases of or subscription for such securities should be made. In particular, investors should pay special attention to any sections of the final prospectus describing any risk factors. The merits or suitability of any securities or any transaction described in these materials to a particular person’s situation should be independently determined by such person. Any such determination should involve, inter alia, an assessment of the legal, tax, accounting, regulatory, financial, credit and other related aspects of the securities or such transaction.

These materials may contain projections and forward looking statements. Any such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the Company’s actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Any such forward-looking statements will be based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future. Further, any forward-looking statements will be based upon assumptions of future events which may not prove to be accurate. Any such forward-looking statements in these materials will speak only as at the date of these materials and the Company assumes no obligation to update or provide any additional information in relation to such forward-looking statements.

These materials are confidential, are being made available to selected recipients only and are solely for the information of the such recipients. These materials and must not be reproduced, redistributed or passed on to any other person or published, in whole or in part, for any purpose without the prior written consent of the Company.

This document and the information contained herein are not an offer of securities for sale in the United States and are not for publication or distribution to persons in the United States (within the meaning of Regulation S under the United States Securities Act of 1933, as amended (the Securities Act). The securities proposed to be offered by the Issuer have not been and will not be registered under the Securities Act and may not be offered or sold in the United States in reliance on exemption from, or as a transaction not subject to, the registration requirements of the Securities Act.

Investors presentation