Page 1

Iran steel export: perspectives and competitiveness in the MENA region

2nd Iran Steel Export Perspectives ConferenceSeptember 4, 2015, Istanbul, Turkey

Andrey Pupchenko,Deputy Managing Director,Metal Expert

Page 2

Contents I. Iran’s export in post-sanctions era

II. Square billet as the most promising product now

III. Competitiveness in the MENA region

Page 3

I. Iran’s export in post-sanctions era

Page 4

Iran in post-sanctions era – steel export opens first

Now depressed domestic demand, limited export activity

1st stage Iranian banks get access to SWIFT

2nd stagenew players get access to international markets, export is the top priority, as weak currency made export very competitive, earn money first!

3rd stage oil & gas industry recovery provides solid demand for tubes and sheet products at home

4th stage economy speed up with massive improvements in construction industry and steel demand

5th stage import of downstream value-added products grows

© Metal Expert

Page 5

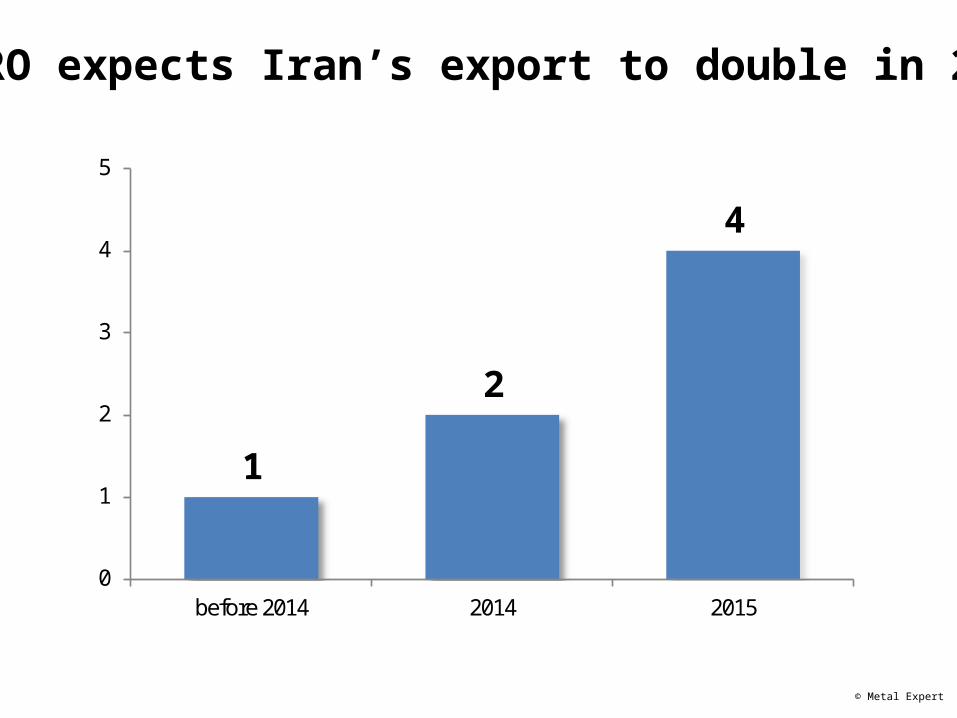

IMIDRO expects Iran’s export to double in 2015

1

2

4

0

1

2

3

4

5

before 2014 2014 2015

© Metal Expert

Page 6

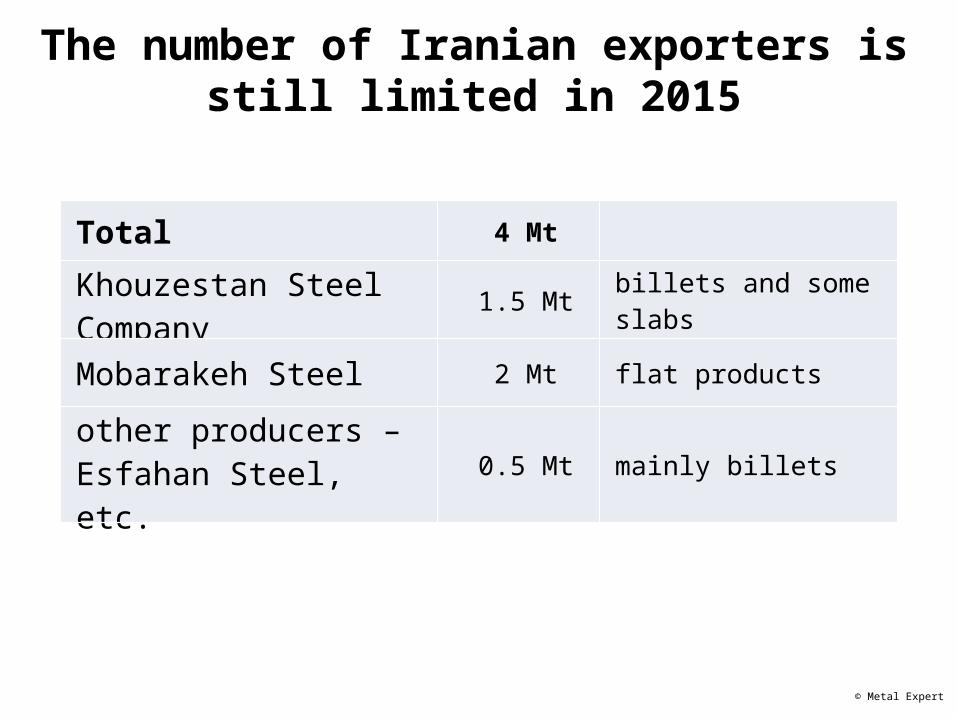

in million t

Total 4 Mt

Khouzestan Steel Company 1.5 Mt billets and some slabs

Mobarakeh Steel 2 Mt flat products

other producers – Esfahan Steel, etc. 0.5 Mt mainly billets

The number of Iranian exporters is still limited in 2015

© Metal Expert

Page 7

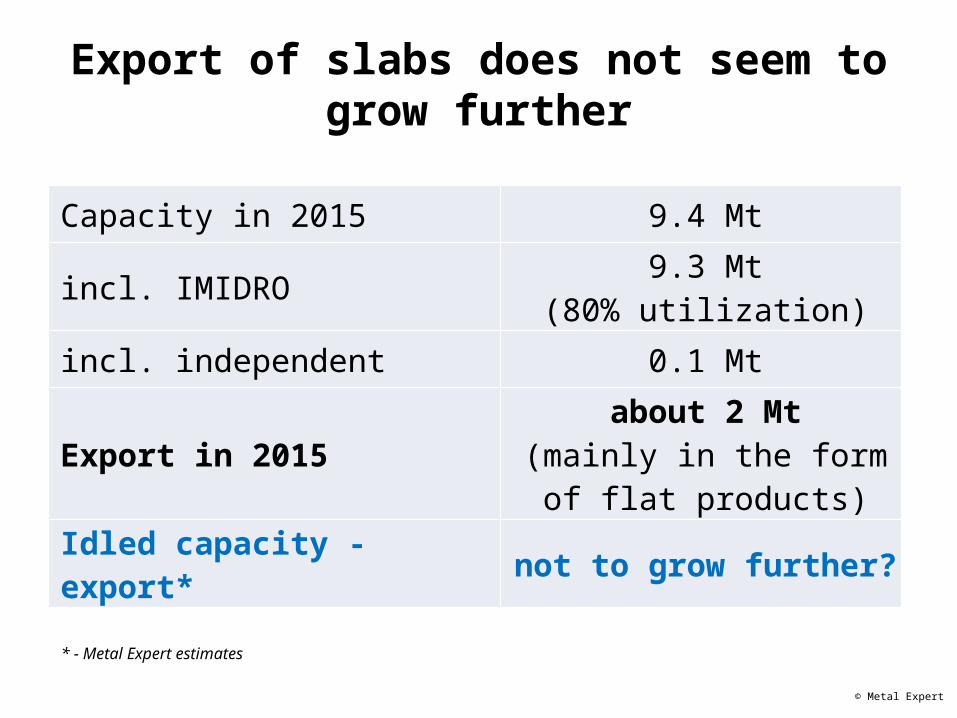

Capacity in 2015 9.4 Mt

incl. IMIDRO 9.3 Mt(80% utilization)

incl. independent 0.1 Mt

Export in 2015about 2 Mt

(mainly in the form of flat products)

Idled capacity - export* not to grow further?

Export of slabs does not seem to grow further

* - Metal Expert estimates

© Metal Expert

Page 8

Capacity in 2015 14.5 Mt

incl. IMIDRO 6.3 Mt (80% utilization)

incl. independent/private 8.2 Mt (about 50% utilization)

Export in 2015 less than 2 Mt

Idled capacity - export potential* around 4 Mt

Square billets in Iran – there is some potential here

* - Metal Expert estimates

© Metal Expert

Page 9

© Metal Expert

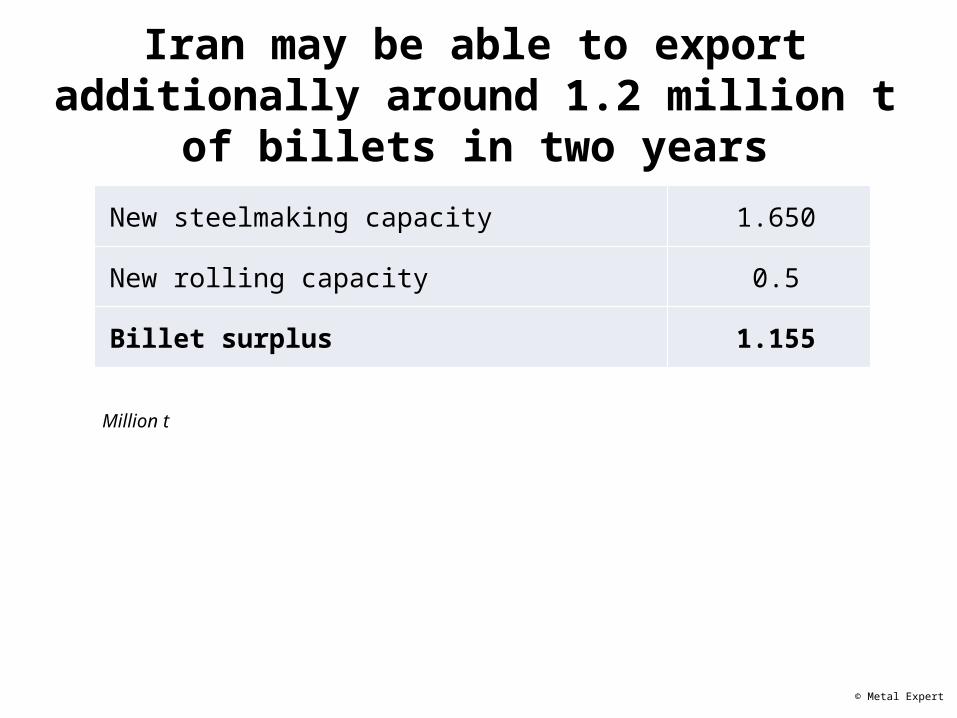

New steelmaking capacity 1.650

New rolling capacity 0.5

Billet surplus 1.155

Million t

Iran may be able to export additionally around 1.2 million t of billets in two years

Page 10

II. Square billet as the most promising product now – fundamental shift

Page 11

What creates new opportunities and disadvantages in global billet market?

• The end of 'super cycle' era

• Scrap price decreased much less comparing to iron ore

• Chinese billet export considerably increased

Page 12

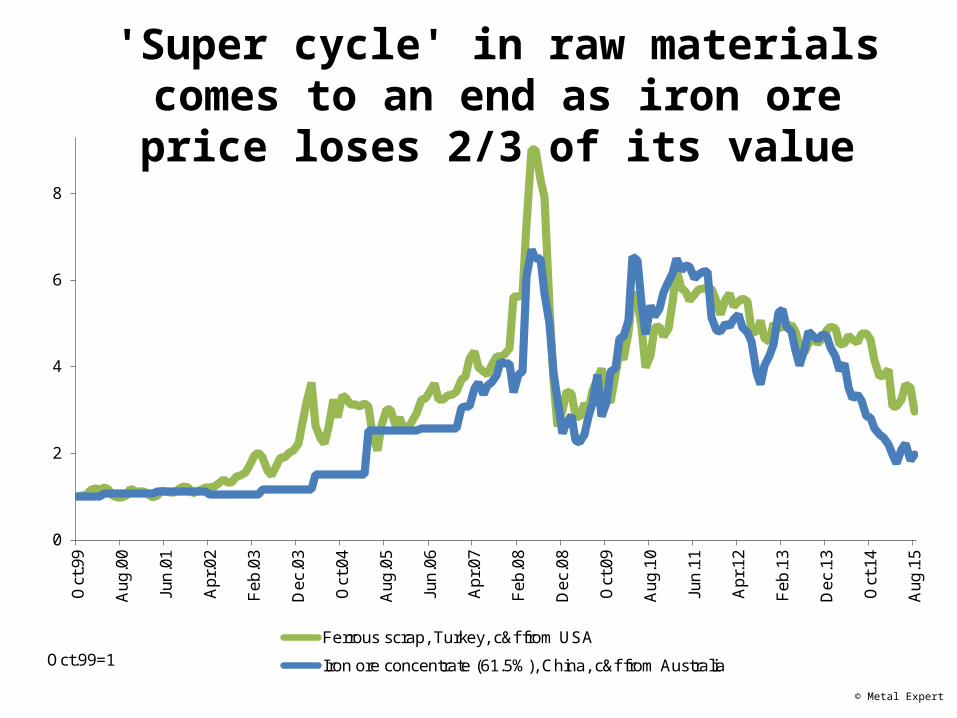

'Super cycle' in raw materials comes to an end as iron ore price loses 2/3 of its value

© Metal Expert

0

2

4

6

8

Oct

.99

Au

g.0

0

Jun

.01

Ap

r.02

Fe

b.0

3

De

c.0

3

Oct

.04

Au

g.0

5

Jun

.06

Ap

r.07

Fe

b.0

8

De

c.0

8

Oct

.09

Au

g.1

0

Jun

.11

Ap

r.12

Fe

b.1

3

De

c.1

3

Oct

.14

Au

g.1

5

Ferrous scrap, Turkey, c&f from USA

Iron ore concentrate (61.5%), China, c&f from AustraliaOct.99=1

Page 13

Scrap price decreased much less comparing to iron ore as recyclers overinvested

© Metal Expert

Page 14

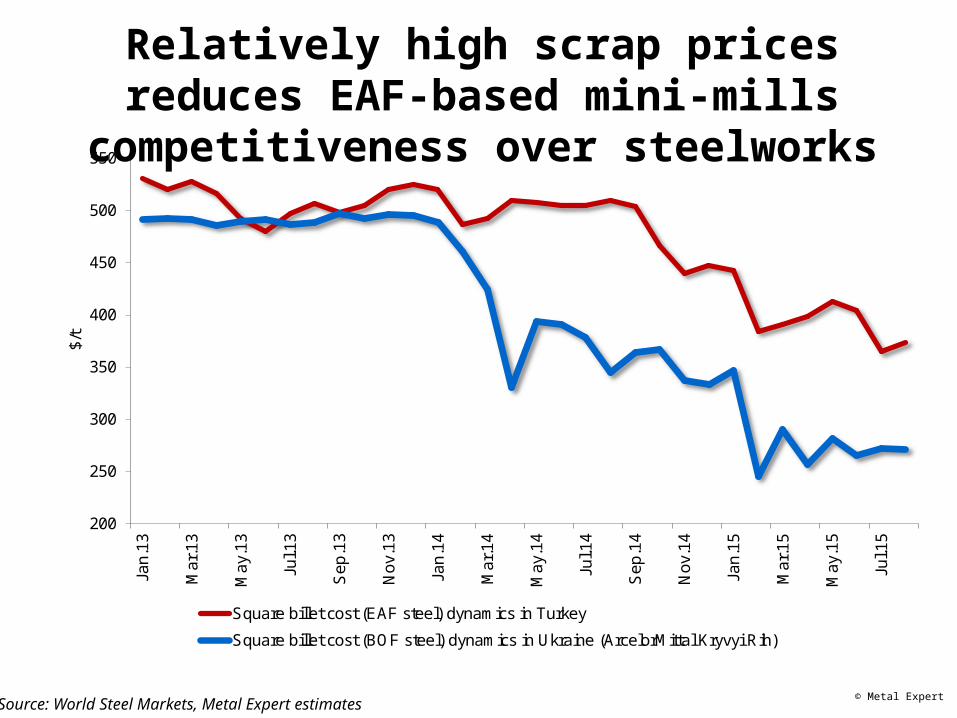

Relatively high scrap prices reduces EAF-based mini-mills competitiveness over steelworks

© Metal ExpertSource: World Steel Markets, Metal Expert estimates

200

250

300

350

400

450

500

550Ja

n.13

Mar

.13

May

.13

Jul.1

3

Sep

.13

Nov

.13

Jan.

14

Mar

.14

May

.14

Jul.1

4

Sep

.14

Nov

.14

Jan.

15

Mar

.15

May

.15

Jul.1

5

$/t

Square billet cost (EAF steel) dynamics in Turkey

Square billet cost (BOF steel) dynamics in Ukraine (ArcelorMittal Kryvyi Rih)

Page 15

Weak local market forces Chinese steel companies to boost exports

© Metal Expert

0

20

40

60

80

100

2013 2014 2015*

mill

ion

t

long products flat products steel pipe

* - Metal Expert's forecast

Page 16

III. Competitiveness in the MENA region

Page 17

2 major trends in billet market:

I. Mini-mills install EAFs (as heritage of old strategies – before 'super cycle' came to an end)

II. Square billet replaces ferrous scrap at existing mills, i.e. billet consumption rapidly expands

© Metal Expert

Page 18

© Metal Expert

Billet demand estimated by Metal Expert (on the assumption of 100% rolling capacity utilization); million t

Merchant billet market to expand in MENA

Source: World Steel Markets, Metal Expert estimates

2014 2015 billet market expansion

new billet capacity

2016

Total 8.6 11.2 2.6 0.1 11.1

Turkey 3 5.3 2.3 1.0 4.3

North Africa 3.4 3.7 0.3 -0.9 4.6

GCC 1.2 1.2 0 [3] 1.2

Other 1.0 1.0 0 [1.4] 1.0

Page 19

Turkey47%

North Africa33%

GCC11%

Others9%

Turkey35%

North Africa39%

GCC14%

Others12%

In 2014 billet import was 8.6 Mt

In 2015 billet import is expected to be

11.2 Mt

© Metal Expert

Turkey's billet import to grow this year

Page 20

Square billet replaces ferrous scrap in Turkey

© Metal Expert

200

220

240

260

280

300

320

340

360

380

400

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%A

ug.1

4

Sep

.14

Oct

.14

Nov

.14

Dec

.14

Jan.

15

Feb

.15

Mar

.15

Apr

.15

May

.15

Jun.

15

Jul.1

5

Aug

.15

Sep

.15

from scrap from imported billet imported scrap prices

Page 21

Square billet (rebar) production costs of main suppliers in MENA

© Metal Expert

0

200

400

Russian from local iron ore/DRI

(at $31/t)

Iranian from local iron ore/DRI (at

$48/t)

Ukrainian from local iron

ore/BOF (at $18/t)

Iranian from local DRI (at $176/t)

Chinese from iron ore/BOF (at

$60/t)

UAE from iron ore/DRI ($95/t)

Iranian from scrap (at $230/t)

Turkish from USA scrap (at $240/t)

$/t

Page 22

Conclusion

• After sanctions removal, Iran will begin to expand export, mainly square billets

• Billet demand from mini-mills is growing around the world and in MENA, in particular, due to overvalued scrap prices

• Iranian steel companies, with its own DRI, has the lowest cost in the region

Page 23

What it is about• New billet importers in the region, changes in market structure

• Estimates of billet consumption in the whole region, by countries and by new re-rollers

• Competitiveness analysis: comparison of billet production costs of main exporters into the region and local suppliers

• Comparison of rebar cost produced from different semis and raw materials (i.e. CIS-origin billets, Chinese-origin billets, the US and European scrap, HBI/DRI)

• Forecast of billet export into the region by CIS and Chinese producers

• Three-month price forecasts for billets in main importing countries (Turkey, Saudi Arabia, Egypt)

Metal Expert provides exclusive data and analysis in new report MENA Billet Markets

Subscription fee - $1350

Subscription department+38 056 239 88 50, +38 056 370 12 06, +38 056 370 12 [email protected] MENA Billet Markets is published twice a month

Exclusive statistics• Steel-melting and re-rolling capacities in

MENA

• Square billet export by CIS plants

• Turkey billet market structure

• GCC billet market structure

• Egypt billet market structure

Page 24

Thank you for your attention