Page 1

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

ech

apte

rth

irtee

nConcept PreviewAfter reading this chapter, you should be able to:

Competitive and Distributive Forces

Competitive and Distributive Forces

1. explain why international competition has increased among the U,S., Japan, the EU, and Asian nations

2. understand the purpose of the keiretsu in Japanese industry

3. know the areas in which the US remains vulnerable to foreign competition according the Council on Competitiveness

4. describe the responsibilities of government, management, labor, and consumers in maintaining the international competitiveness of the U.S

Page 2

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

ech

apte

rth

irtee

nConcept Preview continued After reading this chapter, you should be able to:

Competitive and Distributive Forces

Competitive and Distributive Forces

5. explain the competitive environment in Japan., EU, and the developing nations, including the NIE’s

6. appreciate the magnitude and danger of product counterfeiting

7. understand the importance of industrial espionage

8. describe the sources of competitive information

9. discuss the channel members available to companies that export indirectly or directly or manufacture overseas

10. explain the structural trends in wholesaling and retailing

Page 3

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eCompetitive and Distribution Forces

Macro-level national competitiveness

Analysis of competitive forces Distributive forces

13-3

Page 4

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eIntratriad Trade, 1995 (billions of dollars)13-4 Figure 13.1

UnitedStatesUnitedStates

JapanJapanEUEU

$133.7billion

$116.3billion

$61.0billion

$122.0billion

$70.5billion

$42.5billion

Source: United Nations, Monthly Bulletin of Statistics, June 1997, pp. 266-71.

Page 5

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eNational Competitiveness-U.S.

1970’s overvaluation of the US dollar US Government threats to retaliate to open foreign

markets Japan, Brazil, India

Super 301 “hit list” Keiretsu vertically integrated—informal trade

barriers Competitive Policy Council—government must do

more Industrial targeting

assist selected industries to grow Management

increase product quality and productivity Labor long term view accept looser work rules

13-5

Page 6

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e13-6 Large U.S. Acquisitions by Foreign Companies

ValueTarget Acquirer Date ($ billions)

Carnation Nestle (Swiss) 1984 3.00

Cheeseborough-Pond’s Unilever (UK-Dutch) 1986 3.10

Firestone Bridgestone (Japan) 1987 2.65

Standard Oil British Petroleum (UK) 1987 7.40

Celanese Hoechst (Germany) 1987 2.72

Pillsbury Grand Metropolitan (UK) 1988 5.76

Columbia Pictures Sony Corp (Japan) 1989 3.45

Holiday Inn Bass (UK) 1989 2.00

MCA Matsushita Electric (Japan) 1990 6.60

Table 13.1

Page 7

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

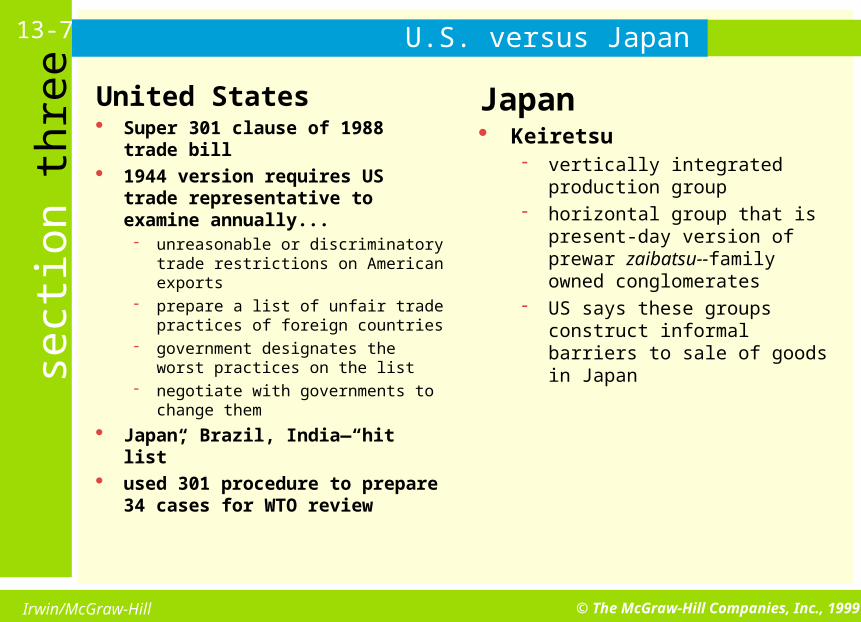

eU.S. versus Japan

United States Super 301 clause of 1988 trade

bill 1944 version requires US trade

representative to examine annually... unreasonable or discriminatory

trade restrictions on American exports

prepare a list of unfair trade practices of foreign countries

government designates the worst practices on the list

negotiate with governments to change them

Japan, Brazil, India—“hit list” used 301 procedure to prepare

34 cases for WTO review

13-7

Japan Keiretsu

vertically integrated production group

horizontal group that is present-day version of prewar zaibatsu--family owned conglomerates

US says these groups construct informal barriers to sale of goods in Japan

Page 8

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e13-8 Government and U.S. Competitiveness

Stricter enforcement of dumping laws Improvement of US national education

system Complete deregulation of industry—

intrastate trucking regulations Lower the federal budget deficit Eliminate double taxation of dividends Reduce the double taxation of

corporate retained earnings

Page 9

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

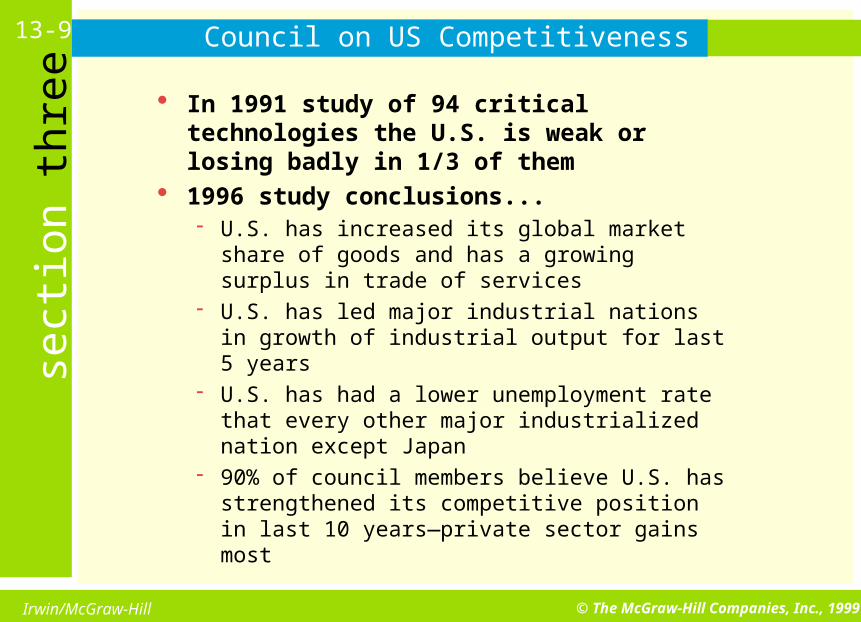

eCouncil on US Competitiveness

In 1991 study of 94 critical technologies the U.S. is weak or losing badly in 1/3 of them

1996 study conclusions... U.S. has increased its global market share of

goods and has a growing surplus in trade of services

U.S. has led major industrial nations in growth of industrial output for last 5 years

U.S. has had a lower unemployment rate that every other major industrialized nation except Japan

90% of council members believe U.S. has strengthened its competitive position in last 10 years—private sector gains most

13-9

Page 10

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eCouncil on U.S. Competitiveness

Among areas where the U.S. remain vulnerable low national savings rate—has increased

nation’s reliance on foreign capital real U.S. investment in plant and equipment has

declined since 1985…net capital stock to continue productivity improvements has slowed

small national productivity gains less than 1% (1985-95) the lowest rate among major industrialized nations

U.S. leads all nations on R&D spending—long term investment as % of GDP is falling while increasing in other countries

U.S. outspends all other nations in education and leads in % graduations from secondary schools and universities

13-10

Page 11

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eU.S. Competitiveness13-11 Figures 13.3

Average annual growth of U.S. net capital stock

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1981-1985 1986-1990 1991-1994

Growth of Net Capital Stock

Growth of Net Capital Stock minusInformation Processing

0.9

2.2

1.82.0

1.9

2.3

0.9

0.0

0.5

1.0

1.5

2.0

2.5

Compound annual growth innational productivity, 1985-1995

U.S.A. Japan Germany France U.K. Italy Canada

Source: Council on Competitiveness. Competitiveness Index (Washington D.C. Council on Competitiveness, 1996), p. 19.

Page 12

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e13-12 Table 13.3Who is the Head of the Class?

Country Mathematics Science

Singapore 643 (1) 607 (1)South Korea 607 (2) 565 (4)Japan 605 (3) 571 (3)Hong Kong 588 (4) 522 (24)Czech Republic 564 (6) 574 (2)France 564 (13) 498 (28)Russia 535 (15) 538 (14=)Ireland 527 (17) 538 (14=)Thailand 522 (20=) 525 (22)Israel 522 (20=) 524 (23)UK 506 (25) 552 (10)USA 500 (28) 534 (17)Spain 487 (31) 517 (26)Romania 482 (34) 486 (31)Portugal 454 (37) 480 (33)Iran 428 (38) 470 (37)Colombia 385 (40) 411 (40)South Africa 354 (41) 326 (41)

Source: The Mexico City News, December 12, 1996, p.6.

Page 13

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eCompound Annual Growth in Manufacturing 1895-199513-13 Table 13.3

2.9

4.3

2.5

3.2

4.0

3.5

1.6

3.2

4.54.1

2.12.3

1.1

-0.2

-1

0

1

2

3

4

5

U.S.A. Japan Germany France U.K. Italy Canada

1985-1995 1996

Source: Council on Competitiveness, Competitiveness Index 1996 (Washington, D.C.: Council on Competitiveness, 1996) p. 31; and Bureau of Labor Standards, “International Comparisons of Manufacturing Productivity and Unit Labor Cost Trends, 1996,”ftp://146.142.4.23/pub/news.release/prod4.txt (January 24, 1998).

Page 14

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

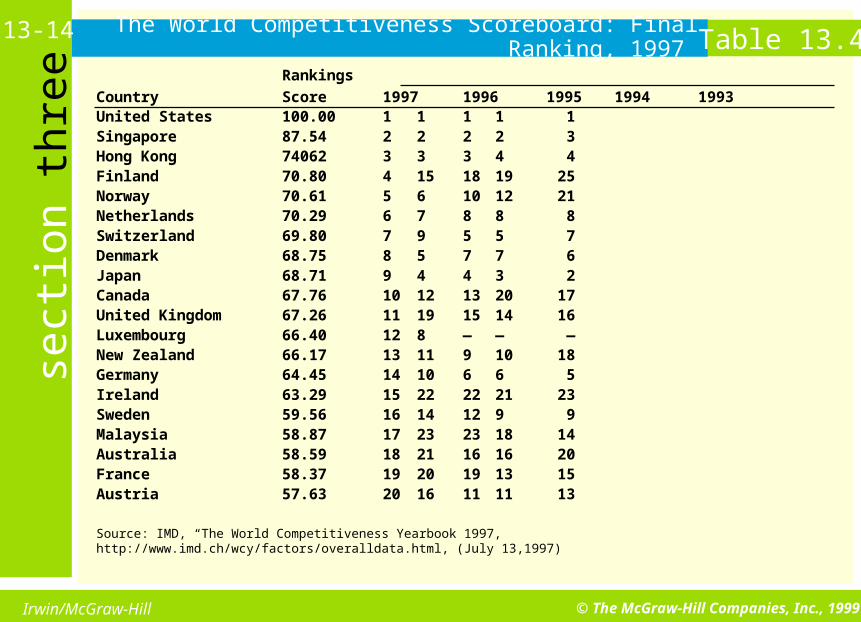

eThe World Competitiveness Scoreboard: Final Ranking, 1997

Rankings

Country Score 1997 1996 1995 1994 1993United States 100.00 1 1 1 1 1Singapore 87.54 2 2 2 2 3Hong Kong 74062 3 3 3 4 4Finland 70.80 4 15 18 19 25Norway 70.61 5 6 10 12 21Netherlands 70.29 6 7 8 8 8Switzerland 69.80 7 9 5 5 7Denmark 68.75 8 5 7 7 6Japan 68.71 9 4 4 3 2Canada 67.76 10 12 13 20 17United Kingdom 67.26 11 19 15 14 16Luxembourg 66.40 12 8 — — —New Zealand 66.17 13 11 9 10 18Germany 64.45 14 10 6 6 5Ireland 63.29 15 22 22 21 23Sweden 59.56 16 14 12 9 9Malaysia 58.87 17 23 23 18 14Australia 58.59 18 21 16 16 20France 58.37 19 20 19 13 15Austria 57.63 20 16 11 11 13

Source: IMD, “The World Competitiveness Yearbook 1997, http://www.imd.ch/wcy/factors/overalldata.html, (July 13,1997)

Table 13.413-14

Page 15

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eLabor Costs in Europe

Higher in 11 European countries than inthe U.S.

Hourly rates of 9 European countries are higher than Japan

Complaint: Europe’s workers are overpaid, overprotected and get too many holidays

Holidays 43 days in Germany 21 days in the U.S. 22 days in Japan

13-15

Page 16

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eGrowth in Volume of World Merchandise Trade

by Selected Regions, 1990-1995 (Annual Change in Percentage)

Exports ImportsAverage, Average,1990-96 1995 1996 1990-96 1995 1996

5.5 8.5 4.0 World 6.0 8.5 4.5

7.0 9.5 5.5 North America (US & CN) 7.0 8.0 5.5

8.5 12.0 11.0 Latin America 11.0 3.0 10.5

5.0 7.5 4.0 Western Europe 4.0 6.5 3.0

5.0 8.0 4.0 European Union (15) 4.0 6.0 2.5

3.5 14.5 3.5 Transition Economies 2.5 11.5 12.07.0 9.5 2.5 Asia 9.5 14.0 4.51.0 3.5 -0.5 Japan 6.0 12.5 2.5

10.0 14.5 3.5 Six East Asian traders* 10.5 15.5 4.0

*Hong Kong, the Republic of Malaysia, Singapore, Taiwan, and Thailand.Source: World trade Organization, “International Trade,” April 4, 1997, http://www.wto.org/intltrad/intlorg.htm (July 9, 1997).

Table 13.513-16

Page 17

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eTable 13.613-17 Total Japanese Investment in the EU

percentage of total

Cumulative Investment, FY 1951-94

United Kingdom Netherlands Germany

33.8 19.4 8.1

Luxembourg France Spain

6.0 6.4 3.0

Belgium Italy Ireland

3.2 1.8 1.6

Portugal Greece Denmark

0.3 NA NA

Source: JETRO. “EU-Japan Investments.” http:www.jetro.go.jp/FACTS/EU-Handbook/DETAIL/t14html (Jan. 30, 1998)

Page 18

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eNational Competitiveness-Japan

Weak economy in 1997 more than 16,000 companies sought bankruptcy protection bankruptcies of small and midsize firms reduced Japan’s GNP

by more than 2 percent estimated that bankruptcies caused a 10 % loss of the GDP over

5-year period government aggravated situation by reducing spending and

increased taxes by over $80 billion faces a possible recession

Competition from the U.Ss Japanese consumers are more price-conscious U.S. has forced the opening of the Japanese distribution system American automakers are making inroads in the Japanese

market Japanese firms have moved their production facilities to

other Asian countries Japanese firms close production facilities and become

marketing organizations for foreign producers

13-18

Page 19

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e1994 and 1996 Sales and 2000 Sales Projections

of U.S. Car Brands in Japan (in units)

General Motors Ford Chrysler

1994 Sales

Imports 39,500 15,000 14,208*

Japanese-made 0 32,000 0

1996 Sales

Imports 71,500 21,000 16,170

Japanese-made 0 31,000 0

2000 Sales (projected)

Imports 100,000 100,000 100,000

Japanese-made 0 100,000 0

*Includes 1,000 gray market cars, discussed later in this chapter.

Source: Telephone conversations with Chrysler, General Motors, and Ford representatives.

Table 13.713-19

Page 20

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eNational Competitiveness-NIC’s

Korea competes worldwide Counterfeiting

use of well-known names on products that are copies close copies with different names reproductions that not exact copies imitations that are cheap copies and fool no one piracy

copying of trade-related intellectual property protected by patents, copyrights, and trademarks South Korea China—CD's Hong Kong Thailand

Industrial espionage spying on a competitor to lean its trade and

production secrets reverse engineering-dismantling a competitor's

product to learn everything possible about it

13-20

Page 21

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eTable 13.813-21 Average Annual Increases in Merchandise Exports

for Selected Countries, 1980-1995

Average Annual Growth Rate*1990-95 (%) 1980-90 (%) Value in 1995

World 6.0% 4.7% $5,145.0 Hong Kong 15.4 15.3 173.8Thailand 14.3 21.6 56.5Singapore 12.2 16.2 118.3Taiwan 11.6 5.9 111.6Malaysia 11.5 17.8 74.0Indonesia 21.3 5.3 45.4China 14.3 11.4 148.8Gambia 26.9 2.3 0.1Zambia 26.9 -3.5 0.8Panama 23.3 2.6 0.6Mexico 14.7 12.2 79.5Greece 11.9 5.1 9.4Japan 0.4 5.0 443.1Germany 2.2 4.6 523.7United States 5.6 3.6 584.7

*Service exports not included.Source: World Development Indicators, 1997 (Washington D.C.: World Bank, 1997), pp. 154-56, 158-60.

Page 22

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e13-22 Analysis of Competitive Forces

Competitor intelligence need for more in-depth

knowledge gather data and analyze

Sources of information within the firm published materials benchmarking suppliers/customers direct observation benchmarking employees

Benchmarking Stages:

management examines its firm for the aspects of the business that need improving

looks for companies that are work leaders in performing similar processes

determines how those companies perform so well

Which companies to use as a benchmark internal—one operation in the firm with

another competitive—compare with a direct

competitor functional—compare similar function in

broadly defined industry generic-compare operations in totally

unrelated industries

Page 23

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e13-23 Distribution Forces

Channel member selection depends on method of market entry indirect exporting

exporters that buy and sell for their own account Export merchants (export distributors) buy and sell in

their own names Cooperative exporters (piggyback) also handle

products for other firms sell for the manufacturer buy for their overseas customers purchase on behalf of foreign or middlemen or

users Webb-Pomerene Associations-competing firms join

together for export

Page 24

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

e13-24 Distribution Forces

Channel member selection depends on method of market entry direct exporting

four types of middlemen manufacturers’ agents--residents in foreign

markets who trade in company’s name distributors-wholesale importers who buy for

their own account-may have exclusive rep. retailers frequently are direct importers trading companies import a wide range of

goods (can be state trading companies) foreign production

wholesale institutions retail institutions

Page 25

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eRetailers and Wholesalers per 1,000 population Figure 13.1413-25

3.67

1.60 2.00

12.80

6.17 6.00

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Wholesalers Retailers

Japan United States United Kingdom

Source: European Marketing Data and Statistics, 1995; and International Marketing Data and Statistics, 1995

Page 26

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

ePassenger Car Distribution Channels in Japan Figure 13.1513-26

Imported Cars

Domestic Cars

Foreignmaker

Foreignmaker ImporterImporter Import

dealerImportdealer

Dealershipbranch

Dealershipbranch

SubdealerSubdealer ConsumerConsumer

Foreigndealer

Foreigndealer

ParallelimporterParallelimporter

10%

80%

10%

30%

70%

Domesticmaker

Domesticmaker

Salescompany

Salescompany DealerDealer Dealership

branchDealership

branch

SubdealerSubdealer ConsumerConsumer

Page 27

Irwin/McGraw-Hill © The McGraw-Hill Companies, Inc., 1999

sect

ion

thre

eEuropean Food Distribution

by Type of Organization (Percent of Market)

Retailer-ControlledCountry Co-ops Chains Voluntary Assns Independents Others*

Austria 15% 44% 36% — 5%

Belgium — 23 30 36% 30

Finland 16 — 50 5 50

France — 25 27 18 27

Italy 8 12 25 45 —

Netherlands — 54 — 39 7

Norway 23 37 33 7 —

Portugal 1 10 — 86 3

Sweden 21 8 44 — 27

Switzerland 34 — 14 34 18

United Kingdom 12 58 — — 30

West Germany — 80 — — 20

*Refers to specialty shops and department stores.

Source: European Marketing Data & Statistics, 1995 (London: Euromonitor, 1995), p. 317.

Table 13.913-27