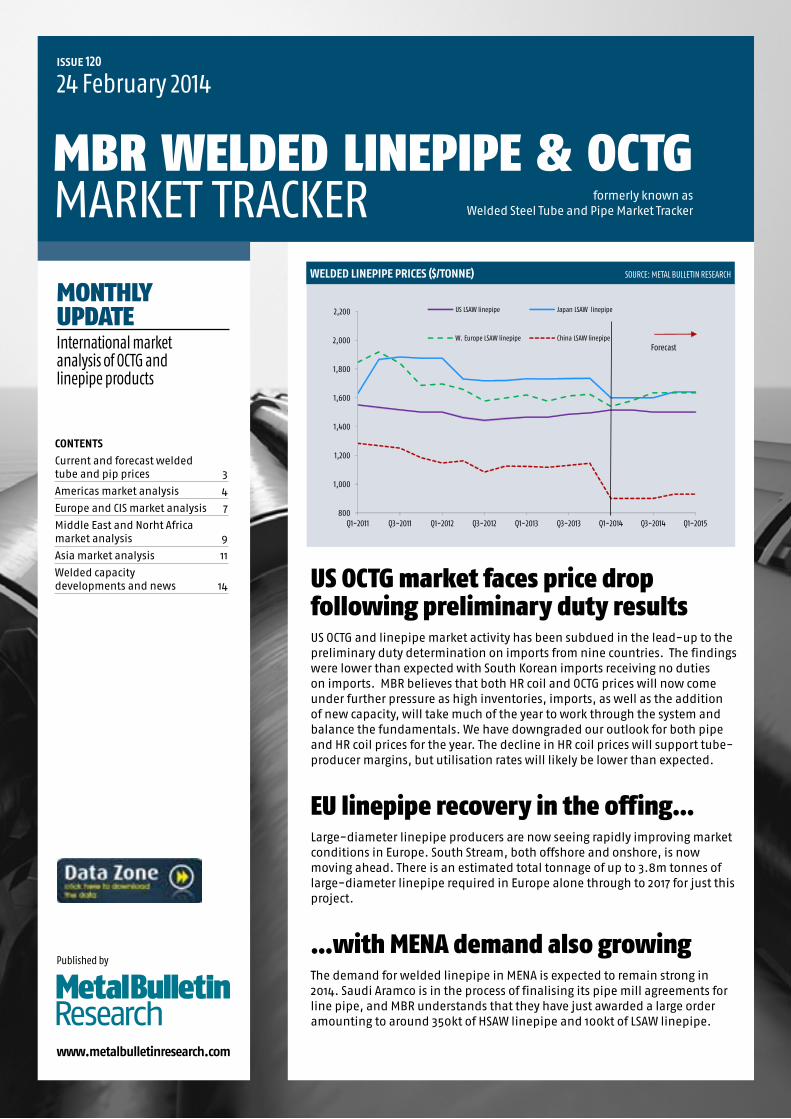

Published by www.metalbulletinresearch.com MONTHLY UPDATE International market analysis of OCTG and linepipe products MBR WELDED LINEPIPE & OCTG MARKET TRACKER ISSUE 120 24 February 2014 WELDED LINEPIPE PRICES ($/TONNE) SOURCE: METAL BULLETIN RESEARCH 800 1,000 1,200 1,400 1,600 1,800 2,000 2,200 Q1-2011 Q3-2011 Q1-2012 Q3-2012 Q1-2013 Q3-2013 Q1-2014 Q3-2014 Q1-2015 US LSAW linepipe Japan LSAW linepipe W. Europe LSAW linepipe China LSAW linepipe Forecast CONTENTS Current and forecast welded tube and pip prices 3 Americas market analysis 4 Europe and CIS market analysis 7 Middle East and Norht Africa market analysis 9 Asia market analysis 11 Welded capacity developments and news 14 US OCTG market faces price drop following preliminary duty results US OCTG and linepipe market activity has been subdued in the lead-up to the preliminary duty determination on imports from nine countries. The findings were lower than expected with South Korean imports receiving no duties on imports. MBR believes that both HR coil and OCTG prices will now come under further pressure as high inventories, imports, as well as the addition of new capacity, will take much of the year to work through the system and balance the fundamentals. We have downgraded our outlook for both pipe and HR coil prices for the year. The decline in HR coil prices will support tube- producer margins, but utilisation rates will likely be lower than expected. EU linepipe recovery in the offing… Large-diameter linepipe producers are now seeing rapidly improving market conditions in Europe. South Stream, both offshore and onshore, is now moving ahead. There is an estimated total tonnage of up to 3.8m tonnes of large-diameter linepipe required in Europe alone through to 2017 for just this project. …with MENA demand also growing The demand for welded linepipe in MENA is expected to remain strong in 2014. Saudi Aramco is in the process of finalising its pipe mill agreements for line pipe, and MBR understands that they have just awarded a large order amounting to around 350kt of HSAW linepipe and 100kt of LSAW linepipe. formerly known as Welded Steel Tube and Pipe Market Tracker

Transcript

Published by

www.metalbulletinresearch.com

MONTHLYUPDATEInternational marketanalysis of OCTG and linepipe products

MBR WELDED LINEPIPE & OCTGMARKET TRACKER

Issue 120

24 February 2014

Welded lInepIpe prIces ($/tonne) Source: Metal Bulletin reSearch

W. europe lSaW linepipe china lSaW linepipeForecast

contents

Current and forecast welded tube and pip prices 3

Americas market analysis 4

Europe and CIS market analysis 7

Middle East and Norht Africa market analysis 9

Asia market analysis 11

Welded capacity developments and news 14 US OCTG market faces price drop

following preliminary duty resultsUS OCTG and linepipe market activity has been subdued in the lead-up to the preliminary duty determination on imports from nine countries. The findings were lower than expected with South Korean imports receiving no duties on imports. MBR believes that both HR coil and OCTG prices will now come under further pressure as high inventories, imports, as well as the addition of new capacity, will take much of the year to work through the system and balance the fundamentals. We have downgraded our outlook for both pipe and HR coil prices for the year. The decline in HR coil prices will support tube-producer margins, but utilisation rates will likely be lower than expected.

EU linepipe recovery in the offing…Large-diameter linepipe producers are now seeing rapidly improving market conditions in Europe. South Stream, both offshore and onshore, is now moving ahead. There is an estimated total tonnage of up to 3.8m tonnes of large-diameter linepipe required in Europe alone through to 2017 for just this project.

…with MENA demand also growingThe demand for welded linepipe in MENA is expected to remain strong in 2014. Saudi Aramco is in the process of finalising its pipe mill agreements for line pipe, and MBR understands that they have just awarded a large order amounting to around 350kt of HSAW linepipe and 100kt of LSAW linepipe.

formerly known as Welded Steel Tube and Pipe Market Tracker

Current and Forecast Price data is only available to

paying subscribers.

To subscribe, or for a preview of our data,

please contact our sales department on:

+44 (0) 20 7779 7999

MBR WEldEd liNEpipE ANd OCTG MarKet tracKer FeBruarY 2014 WWW.MetalBulletinreSearch.coM

4 aMerIcas MarKet analYSiS

SOURCE: MBR

us erW octG (under 16” od) imports (y/y % change)

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

Feb11

May11

aug11

nov11

Feb12

May12

aug12

nov12

Feb13

May13

aug13

nov13

SOURCE: MBR

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan12

Mar12

May12

Jul12

Sep12

nov12

Jan13

Mar13

May13

Jul13

Sep13

nov13

Peru chile

Imports of large od linepipe in chile and peru (tonnes)

ERW OCTG prices slip modestly ahead of duty resultsWelded tube and pipe prices came under pressure in early February, as a result of declining raw materials and HR coil prices. ERW OCTG prices are now down to around $1,455/tonne for API 5CT J/K55 casing at distributors, a decline of about $10/tonne from January pricing. February scrap prices in the domestic US market fell $30/l.ton and are vulnerable to another cut in March. Meanwhile, HR coil prices are slipping through February with prices falling about $15-20/ton through the first half of the month and down $20-25/ton from four weeks ago. Much of the market was quiet through the first half of the month as buyers and sellers waited for the duty results on imported OCTG from nine countries, as many felt that once the duties were announced, prices would have room to eventually rise. OCTG duties fall short of expectationsThe results, however, did not come in favor of US producers. The US Department of Commerce International Trade Administration (US ITA) found that imports from South Korea – the country with the highest import share – were not sold below the cost of steel and, therefore, received no duties in the preliminary duty determination. The following are the preliminary duties for the nine countries investigated: India – 0 to 55.29%; South Korea – 0%; Philippines – 8.9%; Saudi Arabia – 2.92%; Taiwan – 2.65%; Thailand – 118.32%; Turkey – 0 to 4.87%; Ukraine – 5.31%; Vietnam – 9.57 to 111.47%.

In the case of the critical circumstances complaint, negative critical circumstances were determined for exporters from South Korea, Philippines, Turkey and Ukraine. In those cases, no retroactive duties will be imposed. Critical circumstances were found for exports from Jindal SAW in India, but for no other Indian exporter. In Vietnam, critical circumstances were found for all entities except SeAH Steel VINA Corporation. Critical circumstances complaints were not filed against Saudi Arabia, Taiwan, and Thailand.

Following the preliminary duty determination, all companies with duties will now be required to submit cash deposits based on the rates listed above for all OCTG tonnage entering the country. These will be required until final duty determinations are completed on or about 7 July.

Market participants will point to the findings as just preliminary, stating that final duties in the past have come out much higher than in the preliminary findings. The lack of any duty at all for South Korean material, however, is worrisome to those affected as Commerce determined that transaction prices were not below the cost of steel and therefore not subject to duty. MBR surmises, then, that the lack of any duty and the determination of no dumping would suggest that there would be limited scope for steep duties – enough to affect import offers – in the final determination. South Korean ERW producers have been stating all along that they have been purchasing their substrate from Posco at market prices. The prices

prices will be affected by duty determination

MBR Outlook US ERW and seamless OCTG producers will continue to face strong competitive pressure from importers as the preliminary duty determination resulted in zero or minimal duties placed on some of the most active players in the import market. We estimate that about 1.3m tonnes of imported OCTG as part of the suit against nine countries received minimal or zero duties. This ruling, while preliminary and subject to change, will affect market participants along the value chain. MBR believes that both HR coil and OCTG prices will come under further pressure as the overhang of material in the market along with import pressure as well as the addition of new capacity, will take much of the year to work through the system. As a result, we have downgraded our outlook for both pipe and HR coil prices for the year. Declining HR coil prices will support tube-producer margins, but at the expense of utilization rates.

13001350140014501500155016001650

Q12012

Q32012

Q12013

Q32013

Q12014

Q32014

Q12015

$/to

n

us erW J/K55 casInG prIces

Source: MBr

WWW.MetalBulletinreSearch.coM FeBruarY 2014 MBR WEldEd liNEpipE ANd OCTG MarKet tracKer

5aMerIcas MarKet analYSiS

Apparent consumption of welded pipes in key American countriesCountry 2011 2012 Q3 2013 Oct-13 year-to-date y-o-y % chgUSA LSAW line pipe 275 429 81 29 304 -12%HSAW line pipe 761 406 106 45 362 4%ERW line pipe 1023 1297 321 82 1074 -4%ERW OCTG 2792 3149 781 324 2676 -1%Canada LSAW line pipe 116 173 62 8 234 54%HSAW line pipe 203 139 42 3 200 86%ERW line pipe 252 271 49 14 141 -36%ERW OCTG 597 571 153 55 454 -1%Mexico LSAW line pipe 79 156 26 9 100 -28%HSAW line pipe 0 15 0 0 16 114%ERW line pipe 53 86 31 10 69 1%ERW OCTG 59 46 19 6 63 83%BrazilLSAW line pipe 14 105 25 6 124 48%HSAW line pipe 0 0 0 0 0 150%ERW line pipe 15 7 -1 1 4 -11%PeruLSAW line pipe 11 19 0 0 0 -100%HSAW line pipe 0 0 0 0 0 -100%ERW line pipe 53 14 0 0 2 -88%ChileLSAW line pipe 0 0 0 0 0 -HSAW line pipe 1 0 0 0 0 -ERW line pipe 53 67 15 2 39 -41%ArgentinaLSAW line pipe 41 26 1 3 6 -77%HSAW line pipe 0 0 0 0 0 -ERW line pipe 3 4 2 1 7 114%EcuadorLSAW line pipe 0 0 0 0 0 -HSAW line pipe 0 0 0 0 0 -ERW line pipe 1 9 0 0 0 -Source: Customs Statistics, ISSB, Metal Bulletin Research estimates

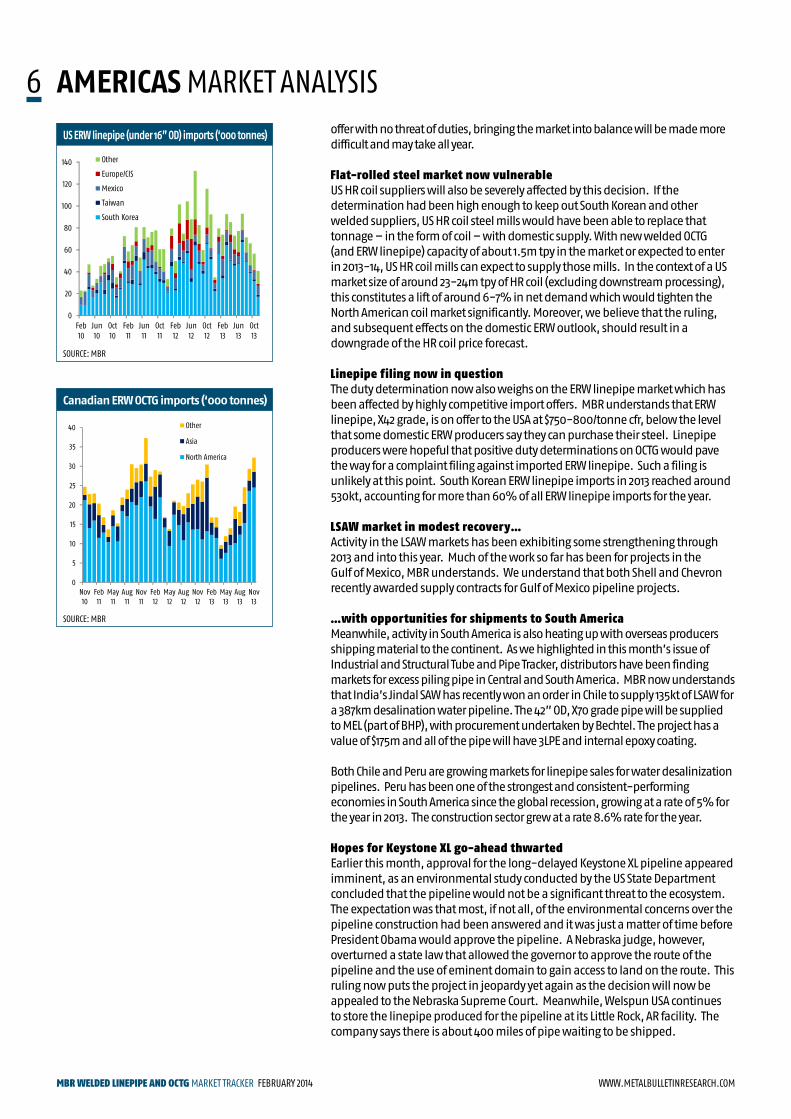

paid are low enough that even with conversion and freight costs, offers to the USA are highly competitive. Indeed, low steel prices in the South Korean market point to a structural steel oversupply which is now pressuring the global tube markets.

MBR’s price outlook now downgraded as a result of the dutiesNevertheless, the lack of duties on South Korean-origin OCTG has dealt the domestic US OCTG market a blow as it was expected that the displaced South Korean imports would be replaced by supplies from domestic producers. South Korea accounted for around 895kt of OCTG imports to the USA in 2013, up from nearly 790kt in 2012. We estimate that imports of welded OCTG from countries cited in the filing, but with zero or minimal duties were 1.3m tonnes in 2012 and 2013 out of total imports of 1.6-1.7m tonnes.

With nearly 3m tpy of rated capacity entering or planned for the US market, there is plenty of domestic material to meet prevailing demand. In the near-term, prices will suffer as the market absorbs this tonnage as well as presumed continued imports.

MBR has now downgraded its 2014 price forecast to account for sustained import competition as well as the inclusion of new OCTG capacity in North America. While we expect OCTG demand to climb in tandem with increased drilling rates over the coming years, as a result of rising energy consumption as well as expected LNG exports, the market is still dealing with an overhang of high distributor inventories that were built up in expectation of a successful filing. Estimated to be as high as five months on hand, much of this tonnage will need to be worked through the market before prices are able to climb. That said, with competitive material remaining on

Apparent consumption data is only available to paying

subscribers.

To subscribe, or for a preview of our data,

please contact our sales department on:

+44 (0) 20 7779 7999

MBR WEldEd liNEpipE ANd OCTG MarKet tracKer FeBruarY 2014 WWW.MetalBulletinreSearch.coM

6 aMerIcas MarKet analYSiSoffer with no threat of duties, bringing the market into balance will be made more difficult and may take all year.

Flat-rolled steel market now vulnerableUS HR coil suppliers will also be severely affected by this decision. If the determination had been high enough to keep out South Korean and other welded suppliers, US HR coil steel mills would have been able to replace that tonnage – in the form of coil – with domestic supply. With new welded OCTG (and ERW linepipe) capacity of about 1.5m tpy in the market or expected to enter in 2013-14, US HR coil mills can expect to supply those mills. In the context of a US market size of around 23-24m tpy of HR coil (excluding downstream processing), this constitutes a lift of around 6-7% in net demand which would tighten the North American coil market significantly. Moreover, we believe that the ruling, and subsequent effects on the domestic ERW outlook, should result in a downgrade of the HR coil price forecast.

Linepipe filing now in questionThe duty determination now also weighs on the ERW linepipe market which has been affected by highly competitive import offers. MBR understands that ERW linepipe, X42 grade, is on offer to the USA at $750-800/tonne cfr, below the level that some domestic ERW producers say they can purchase their steel. Linepipe producers were hopeful that positive duty determinations on OCTG would pave the way for a complaint filing against imported ERW linepipe. Such a filing is unlikely at this point. South Korean ERW linepipe imports in 2013 reached around 530kt, accounting for more than 60% of all ERW linepipe imports for the year.

LSAW market in modest recovery…Activity in the LSAW markets has been exhibiting some strengthening through 2013 and into this year. Much of the work so far has been for projects in the Gulf of Mexico, MBR understands. We understand that both Shell and Chevron recently awarded supply contracts for Gulf of Mexico pipeline projects.

…with opportunities for shipments to South AmericaMeanwhile, activity in South America is also heating up with overseas producers shipping material to the continent. As we highlighted in this month’s issue of Industrial and Structural Tube and Pipe Tracker, distributors have been finding markets for excess piling pipe in Central and South America. MBR now understands that India’s Jindal SAW has recently won an order in Chile to supply 135kt of LSAW for a 387km desalination water pipeline. The 42” OD, X70 grade pipe will be supplied to MEL (part of BHP), with procurement undertaken by Bechtel. The project has a value of $175m and all of the pipe will have 3LPE and internal epoxy coating.

Both Chile and Peru are growing markets for linepipe sales for water desalinization pipelines. Peru has been one of the strongest and consistent-performing economies in South America since the global recession, growing at a rate of 5% for the year in 2013. The construction sector grew at a rate 8.6% rate for the year.

Hopes for Keystone XL go-ahead thwartedEarlier this month, approval for the long-delayed Keystone XL pipeline appeared imminent, as an environmental study conducted by the US State Department concluded that the pipeline would not be a significant threat to the ecosystem. The expectation was that most, if not all, of the environmental concerns over the pipeline construction had been answered and it was just a matter of time before President Obama would approve the pipeline. A Nebraska judge, however, overturned a state law that allowed the governor to approve the route of the pipeline and the use of eminent domain to gain access to land on the route. This ruling now puts the project in jeopardy yet again as the decision will now be appealed to the Nebraska Supreme Court. Meanwhile, Welspun USA continues to store the linepipe produced for the pipeline at its Little Rock, AR facility. The company says there is about 400 miles of pipe waiting to be shipped.

SOURCE: MBR

us erW linepipe (under 16” od) imports (‘000 tonnes)

0

20

40

60

80

100

120

140

Feb10

Jun10

oct10

Feb11

Jun11

oct11

Feb12

Jun12

oct12

Feb13

Jun13

oct13

other

europe/ciS

Mexico

taiwan

South Korea

SOURCE: MBR

0

5

10

15

20

25

30

35

40

nov10

Feb11

May11

aug11

nov11

Feb12

May12

aug12

nov12

Feb13

May13

aug13

nov13

other

asia

north america

canadian erW octG imports (‘000 tonnes)

WWW.MetalBulletinreSearch.coM FeBruarY 2014 MBR WEldEd liNEpipE ANd OCTG MarKet tracKer

7europe and cIs MarKet analYSiS

Recovery arriving in the large-diameter pipe marketsEurope/CIS LSAW market set to see a pick-up in demandThe European and CIS large-diameter linepipe markets received the news for which producers have all been waiting. Following a dismal year in 2013 when many of the region’s LSAW mills posted their lowest utilisation rates on record, the pipe suppliers for the first string of the offshore section of South Stream have now been announced to the market.

API plate prices… As demand from the large-diameter pipeline projects begin to ramp-up, the API plate substrate market is also gaining support. Current European plate prices for non-sour API X65 are around €600/tonne. This has been the bottom of pricing in Europe. Germany’s Dillinger Hütte, one of the world’s leading API plate suppliers (who in October of 2013 started making cost savings in the company of €120 million and further savings of €10m were announced in January 2014 due to falling demand) have now announced an increase in plate prices from April onwards. Dillinger is leading the way by increasing plate prices by €30/tonne. We have heard of similar plate price increases also being announced by Russian plate mills.

…and LSAW pipe prices are expected to increaseDillinger has cited the improving pipe plate market as the reason for this price increase. The company has explained that plate prices have been stable and at extremely low levels for a long-time, and expected rising demand is increasing prices. As a result, in the second quarter we believe that API 5L X65 LSAW pipe prices in Europe will move up to around €850-1,150/tonne depending on the wall thickness and diameter from around a current level of around €820-1,130/tonne.

Offshore South Stream pipe tender announced…In late January, South Stream Transport B.V headquarters in Amsterdam hosted the signing of contracts to supply the first offshore string for South Stream. This offshore pipeline will be 931km in length using LSAW pipe at a diameter of 813mm (32”), grade API 5L X65 and wall thickness of 39mm, with a total tonnage of 670kt. The pipe will be laid at a water depth of over 2,200m and at a pressure greater than 200bars. There are a total of four offshore strings that will need to be constructed for the project.

…to Europipe, OMK and Severstal...Germany’s Europipe won 50% of the contract, Russia’s OMK and Severstal received a 35% and 15% share, respectively. This pipeline will begin construction in the autumn of 2014 with completion expected in December 2015. MBR understands that the pipe, which is technically challenging to provide a perfect geometric circle at this diameter and wall thickness, will

SOURCE: ISSB and MBR

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Jan12

Mar12

May12

Jul12

Sep12

nov12

Jan13

Mar13

May13

Jul13

Sep13

nov13

eu other asia central asia

russian lsaW exports (tonnes)

SOURCE: ISSB and MBR

German lsaW exports (‘000 tonnes)

MBR Outlook Large-diameter linepipe producers, suffering from the worst demand decline throughout 2013 in Europe and Russia, are now seeing rapidly improving market conditions in Europe. South Stream is now moving, both offshore and onshore. There is an estimated total tonnage of up to 3.8Mt of large-diameter linepipe required in Europe alone through to 2017 for just this project.

As utilisation rates increase at LSAW mills across the region, plate prices are set to pick-up in Q2 and with this we expect LSAW pipe prices to move up by around €30-40/tonne into the second half of this year. If other key projects in the region such as TAP and TANAP get the go-ahead this year we believe that large-diameter pipe mill utilisation rates will recover to stable levels quickly which could support further price increases in contracts that they tender for in H2 of this year.

640660680700720740760780800820

Q12012

Q32012

Q12013

Q32013

Q12014

Q32014

Q12015

euro

/ton

european erW lInepIpe prIces

Source: MBr

0

20

40

60

80

100

120

140

160

180

Jan12

Mar12

May12

Jul12

Sep12

nov12

Jan13

Mar13

May13

Jul13

Sep13

nov13

roW eastern europe/ciS Western europe

German exports will pick up sharply to Eastern Europe

MBR WEldEd liNEpipE ANd OCTG MarKet tracKer FeBruarY 2014 WWW.MetalBulletinreSearch.coM

8 europe and cIs MarKet analYSiSbe manufactured starting in April this year by Europipe for its share of the sections. Europipe will produce the pipe from its Mullheim plant in Germany.

…with the second string expected to be awarded by the end of Q1 2014The tender for the second offshore pipeline in this series will be awarded by the end of the first quarter of 2014. Therefore another 630kt of LSAW will be tendered for this. Tenders have not yet been placed by South Stream for the 3rd and 4th offshore strings. However, we learn that the offshore pipelines can be laid with some overlap and with the whole offshore pipeline series wanted to be completed by the end of 2017, the 3rd and 4th tenders could come quickly.

South Stream onshore in Europe is also set to moveMeanwhile, announcements in the next 6 weeks, will begin to be made for the supply of the European onshore section of South Stream. The total length of the European onshore section of South Stream is 1,500km with the required linepipe being at 56” OD and with an average wall thickness of 21.6mm. We estimate that the total tonnage of steel that will be required for this pipeline is around 1.1Mt. This pipeline will run from the coast of Bulgaria to Italy. However, this pipeline will not come in one single tender – each EU member is responsible for tendering for their section of the pipe line, with the counties involved being Bulgaria, Serbia, Hungary, Slovenia and Italy. HSAW is also set to compete for this line as well as LSAW.

Apparent consumption of welded pipes in key European countries by product ('000 tonne)Country 2011 2012 Q3 2013 Oct-13 year-to-date y-o-y % chgRussia LSAW line pipe 3507 1681 555 179 1810 30%HSAW line pipe 180 105 30 10 100 -7%ERW line pipe 765 815 242 81 810 20%ERW OCTG 375 407 113 38 363 8%Kazakhstan LSAW line pipe 46 263 88 0 191 -28%HSAW line pipe 8 20 37 0 118 608%ERW line pipe 7 130 3 0 1 -99%ERW OCTG 2 6 2 0 8 48%UkraineLSAW line pipe 90 48 18 19 23 207%ERW line pipe 80 45 11 3 37 4%Germany LSAW line pipe 280 44 109 13 43 -153%HSAW line pipe 70 40 7 0 6 -72%ERW line pipe 68 69 18 6 59 3%FranceLSAW line pipe 40 116 28 5 34 -47%ERW line pipe 31 11 2 0 10 7%UK LSAW line pipe 96 34 35 28 41 -42%HSAW line pipe 4 4 1 0 2 -43%ERW line pipe 21 21 5 1 16 13%ItalyLSAW line pipe 236 227 27 20 97 -50%HSAW line pipe 2 3 0 0 1 -52%ERW line pipe 6 8 1 0 3 -56%SpainHSAW line pipe 78 66 12 5 40 -24%ERW line pipe 7 5 1 0 2 2%Source: Customs Statistics, ISSB, Metal Bulletin Research estimates

Apparent consumption data is only available to paying

subscribers.

To subscribe, or for a preview of our data,

please contact our sales department on:

+44 (0) 20 7779 7999

WWW.MetalBulletinreSearch.coM FeBruarY 2014 MBR WEldEd liNEpipE ANd OCTG MarKet tracKer

9MIddle east and north afrIca MarKet analYSiS

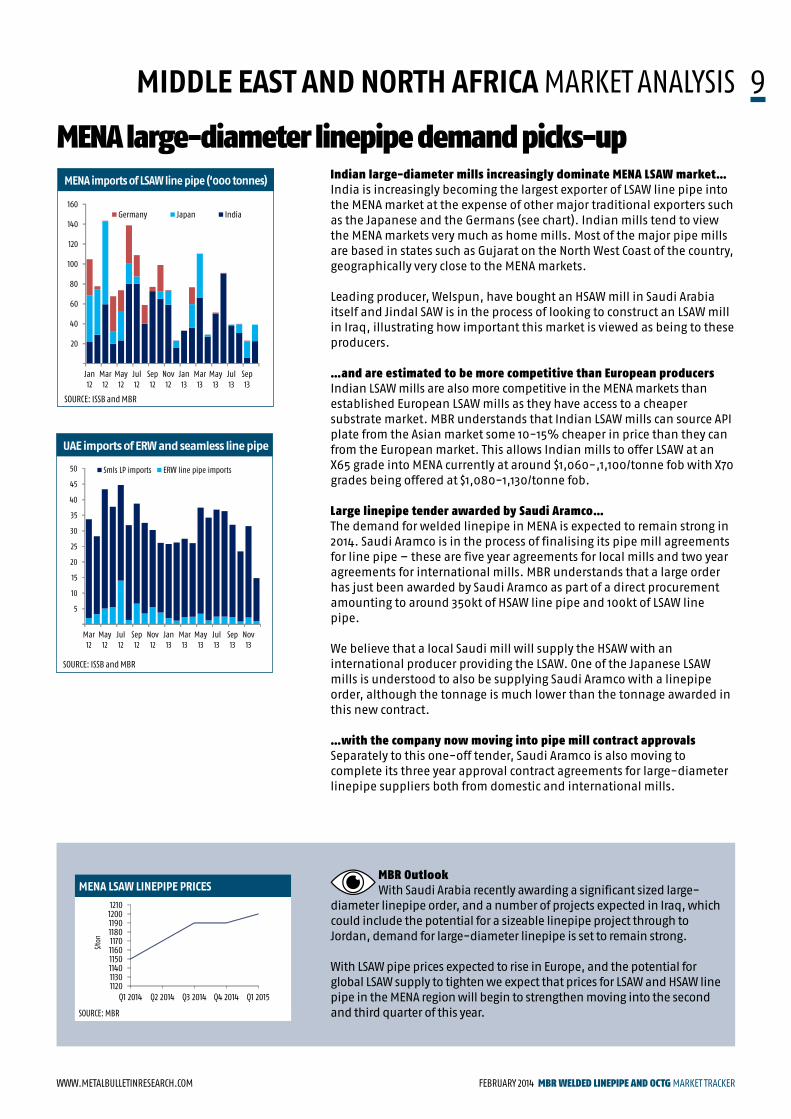

MENA large-diameter linepipe demand picks-upIndian large-diameter mills increasingly dominate MENA LSAW market…India is increasingly becoming the largest exporter of LSAW line pipe into the MENA market at the expense of other major traditional exporters such as the Japanese and the Germans (see chart). Indian mills tend to view the MENA markets very much as home mills. Most of the major pipe mills are based in states such as Gujarat on the North West Coast of the country, geographically very close to the MENA markets.

Leading producer, Welspun, have bought an HSAW mill in Saudi Arabia itself and Jindal SAW is in the process of looking to construct an LSAW mill in Iraq, illustrating how important this market is viewed as being to these producers.

…and are estimated to be more competitive than European producersIndian LSAW mills are also more competitive in the MENA markets than established European LSAW mills as they have access to a cheaper substrate market. MBR understands that Indian LSAW mills can source API plate from the Asian market some 10-15% cheaper in price than they can from the European market. This allows Indian mills to offer LSAW at an X65 grade into MENA currently at around $1,060-,1,100/tonne fob with X70 grades being offered at $1,080-1,130/tonne fob.

Large linepipe tender awarded by Saudi Aramco…The demand for welded linepipe in MENA is expected to remain strong in 2014. Saudi Aramco is in the process of finalising its pipe mill agreements for line pipe – these are five year agreements for local mills and two year agreements for international mills. MBR understands that a large order has just been awarded by Saudi Aramco as part of a direct procurement amounting to around 350kt of HSAW line pipe and 100kt of LSAW line pipe. We believe that a local Saudi mill will supply the HSAW with an international producer providing the LSAW. One of the Japanese LSAW mills is understood to also be supplying Saudi Aramco with a linepipe order, although the tonnage is much lower than the tonnage awarded in this new contract.

…with the company now moving into pipe mill contract approvalsSeparately to this one-off tender, Saudi Aramco is also moving to complete its three year approval contract agreements for large-diameter linepipe suppliers both from domestic and international mills.

SOURCE: ISSB and MBR

Mena imports of lsaW line pipe (‘000 tonnes)

20

40

60

80

100

120

140

160

Jan12

Mar12

May12

Jul12

Sep12

nov12

Jan13

Mar13

May13

Jul13

Sep13

Germany Japan india

SOURCE: ISSB and MBR

uae imports of erW and seamless line pipe

5

10

15

20

25

30

35

40

45

50

Mar12

May12

Jul12

Sep12

nov12

Jan13

Mar13

May13

Jul13

Sep13

nov13

Smls lP imports erW line pipe imports

MBR Outlook With Saudi Arabia recently awarding a significant sized large-diameter linepipe order, and a number of projects expected in Iraq, which could include the potential for a sizeable linepipe project through to Jordan, demand for large-diameter linepipe is set to remain strong.

With LSAW pipe prices expected to rise in Europe, and the potential for global LSAW supply to tighten we expect that prices for LSAW and HSAW line pipe in the MENA region will begin to strengthen moving into the second and third quarter of this year.

1120113011401150116011701180119012001210

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015

$/to

n

Mena lsaW lInepIpe prIces

Source: MBr

MBR WEldEd liNEpipE ANd OCTG MarKet tracKer FeBruarY 2014 WWW.MetalBulletinreSearch.coM

10 MIddle east and north afrIca MarKet analYSiSStrong LSAW demand expected in IraqIraq also remains a hot-spot for LSAW line pipe demand. MBR understands that in Iraq there are currently three tenders out for LSAW that combined amount to 250kt of large-diameter line pipe. Another potential large-diameter pipe project could come from Jordan through to Iraq. Government officials from both countries have been holding discussions about the pipeline which would be 1,700km in length and cost $18billion and allow Iraq to export 1Mbpd of oil.

Further afield in the wider Middle East and North Africa, linepipe suppliers have been explaining to us that projects that were put on hold due to the Arab Spring, in the Middle East and North Africa are now starting up again.

New LSAW mill arriving in KuwaitLocal capacity does continue to ramp-up in the region. Ten years ago there was only one LSAW mill in operation on the Arabian Peninsular, NPC in Saudi Arabia. Since this time, two more LSAW mills have started up in Saudi – Arabian Pipe Company in 2008, and this year the new Global Pipe Company has also began ramping up. We believe that

another Saudi LSAW mill being built by China’s PCK, could also enter the market. In Kuwait, KPIOS is also now in the process of building a new LSAW pipe mill. The company already owns a shareholding in the first LSAW mill that was built in the UAE, Al Jazzera. A second LSAW mill has also already been built in the UAE, owned by South Korea’s Seah.

Low levels of ERW linepipe being traded in the regionERW linepipe is a much smaller market in the MENA region, and the product is not actively traded to the same degree as seamless linepipe. MBR understands material that is currently being traded to a grade of API 5L X65 at a 10” od diameter is being sold from stockists in Jebel Ali at around $1,000/tonne fob.

As can be seen by the chart, seamless linepipe dominates all small-diameter linepipe imports into Jebel Ali. ERW line pipe accounted for just 7% of all small-diameter linepipe imports into the UAE in 2013 (as shown in the chart on Page 8). The use of ERW for small-diameter linepipe applications in the region appears to be declining. In 2012, ERW linepipe accounted for nearly 14% of all small-diameter linepipe imports at 56kt compared to 24kt in 2013.

Apparent consumption of welded pipes in key Middle East countries by product ('000 tonne)

LSAW line pipe 10 8 12 11 45 527% ERW line pipe 65 107 30 11 119 34%

ERW OCTG 11 14 5 3 14 13%

Iran

LSAW line pipe 585 819 150 56 456 -38% ERW line pipe 109 110 29 9 91 -1%

HSAW line pipe 254 224 51 17 177 -7%

Iraq

LSAW line pipe 270 388 80 38 249 -24% ERW line pipe 31 23 15 1 36 145%

HSAW line pipe 10 11 0 0 9 -11%

Algeria

LSAW line pipe 9 4 0 0 23 691% ERW line pipe 150 153 69 14 156 62%

HSAW line pipe 173 141 43 10 127 17%

Egypt

LSAW line pipe 95 93 27 8 108 39% ERW line pipe 37 28 10 1 35 52%

Source: Customs Statistics, ISSB, Metal Bulletin Research estimates

Apparent consumption data is only available to paying

subscribers.

To subscribe, or for a preview of our data,

please contact our sales department on:

+44 (0) 20 7779 7999

11

WWW.MetalBulletinreSearch.coM FeBruarY 2014 MBR WEldEd liNEpipE ANd OCTG MarKet tracKer

asIa MarKet analYSiS

to download full data sets please click here

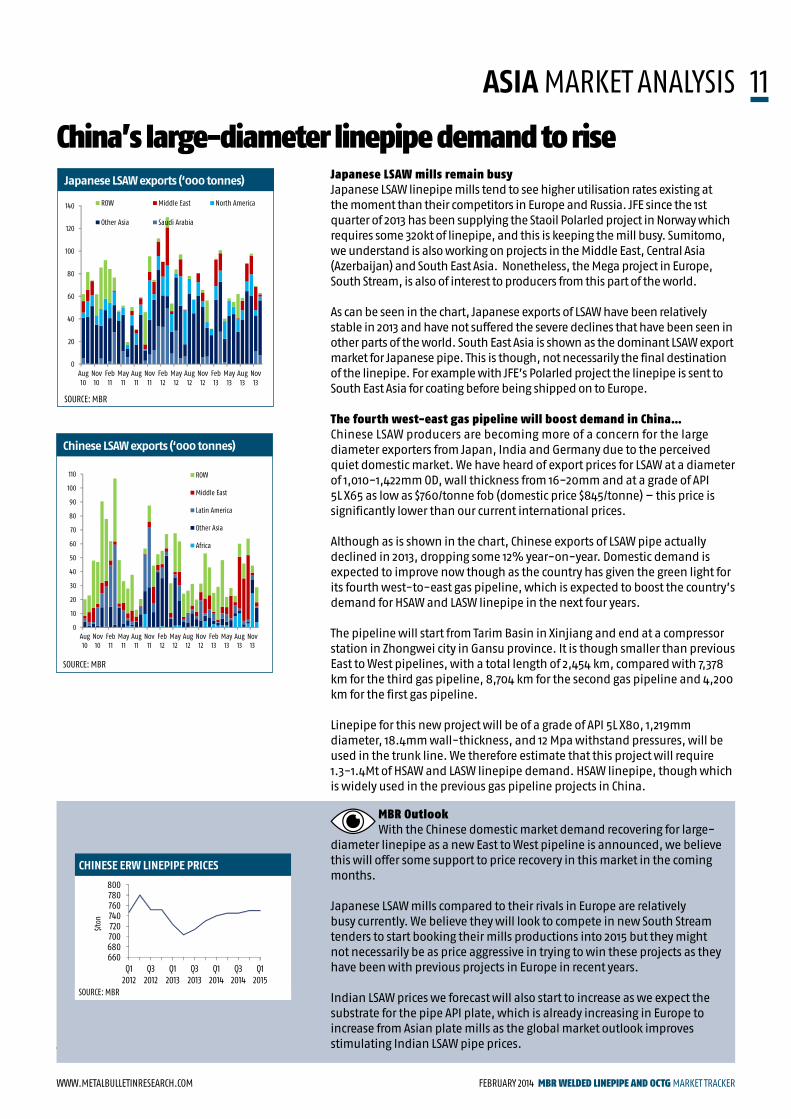

China’s large-diameter linepipe demand to riseJapanese LSAW mills remain busyJapanese LSAW linepipe mills tend to see higher utilisation rates existing at the moment than their competitors in Europe and Russia. JFE since the 1st quarter of 2013 has been supplying the Staoil Polarled project in Norway which requires some 320kt of linepipe, and this is keeping the mill busy. Sumitomo, we understand is also working on projects in the Middle East, Central Asia (Azerbaijan) and South East Asia. Nonetheless, the Mega project in Europe, South Stream, is also of interest to producers from this part of the world.

As can be seen in the chart, Japanese exports of LSAW have been relatively stable in 2013 and have not suffered the severe declines that have been seen in other parts of the world. South East Asia is shown as the dominant LSAW export market for Japanese pipe. This is though, not necessarily the final destination of the linepipe. For example with JFE’s Polarled project the linepipe is sent to South East Asia for coating before being shipped on to Europe.

The fourth west-east gas pipeline will boost demand in China…Chinese LSAW producers are becoming more of a concern for the large diameter exporters from Japan, India and Germany due to the perceived quiet domestic market. We have heard of export prices for LSAW at a diameter of 1,010-1,422mm OD, wall thickness from 16-20mm and at a grade of API 5L X65 as low as $760/tonne fob (domestic price $845/tonne) – this price is significantly lower than our current international prices.

Although as is shown in the chart, Chinese exports of LSAW pipe actually declined in 2013, dropping some 12% year-on-year. Domestic demand is expected to improve now though as the country has given the green light for its fourth west-to-east gas pipeline, which is expected to boost the country’s demand for HSAW and LASW linepipe in the next four years.

The pipeline will start from Tarim Basin in Xinjiang and end at a compressor station in Zhongwei city in Gansu province. It is though smaller than previous East to West pipelines, with a total length of 2,454 km, compared with 7,378 km for the third gas pipeline, 8,704 km for the second gas pipeline and 4,200 km for the first gas pipeline.

Linepipe for this new project will be of a grade of API 5L X80, 1,219mm diameter, 18.4mm wall-thickness, and 12 Mpa withstand pressures, will be used in the trunk line. We therefore estimate that this project will require 1.3-1.4Mt of HSAW and LASW linepipe demand. HSAW linepipe, though which is widely used in the previous gas pipeline projects in China.

SOURCE: MBR

Japanese lsaW exports (‘000 tonnes)

0

20

40

60

80

100

120

140

aug10

nov10

Feb11

May11

aug11

nov11

Feb12

May12

aug12

nov12

Feb13

May13

aug13

nov13

roW Middle east north america

other asia Saudi arabia

SOURCE: MBR

chinese lsaW exports (‘000 tonnes)

0

10

20

30

40

50

60

70

80

90

100

110

aug10

nov10

Feb11

May11

aug11

nov11

Feb12

May12

aug12

nov12

Feb13

May13

aug13

nov13

roW

Middle east

latin america

other asia

africa

MBR Outlook With the Chinese domestic market demand recovering for large-diameter linepipe as a new East to West pipeline is announced, we believe this will offer some support to price recovery in this market in the coming months.

Japanese LSAW mills compared to their rivals in Europe are relatively busy currently. We believe they will look to compete in new South Stream tenders to start booking their mills productions into 2015 but they might not necessarily be as price aggressive in trying to win these projects as they have been with previous projects in Europe in recent years.

Indian LSAW prices we forecast will also start to increase as we expect the substrate for the pipe API plate, which is already increasing in Europe to increase from Asian plate mills as the global market outlook improves stimulating Indian LSAW pipe prices.

MBR WEldEd liNEpipE ANd OCTG MarKet tracKer FeBruarY 2014 WWW.MetalBulletinreSearch.coM

12 asIa MarKet analYSiS…with CNPC’s Baoji expected to be a major supplierThere is little doubt that CNPC’s steel tube producers, especially Baoji, will be among the major suppliers of the linepipes in the fourth gas pipeline. Moreover, we believe Baosteel, which has already invested in the third gas pipeline project, will continue to play an important role in the new project.

CNPC is the major investor of west-to-east gas pipeline projects, and will start the four-year construction of the latest gas pipeline in 2014. Meanwhile, the third west-to-east gas pipeline is still under construction, and is expected to come into operation in 2015. This third line was also API 5L X80 grade and 1,219/1,016 mm diameter. In addition, China is also planning its fifth project, and is expected to get the approval in the coming year.

CNPC also critical to the future of Power of SiberiaCNPC is also involved in the wider Asian market in major linepipe projects. The company is a critical partner in Gazprom’s Power of Siberia and/or Altai pipeline projects. The two companies signed an MOU in March 2013 which determines the parameters to provide a 30 year gas supply framework from Russia to China,

which included the Power of Siberia and Altai project. At the end of January, we understand that the head of Gazprom metwith the head of CNPC to discuss Russian gas supplies to the Chinese market. They agreed that by May they will prepare a contract which could be signed during the visit of President Putin to China. This will provide a final decision on whether the Power of Siberia and/or the Altai pipeline will be constructed.

Both projects would be Mega pipeline projects. The Power of Siberia would use LSAW at a 1,4200mm OD, for a total length of 4,000km consuming up to 3Mt of large-diameter pipe travelling from Yakutia in Siberia to Vladivostok on the Russian Pacific coast. Altai is an alternative pipeline route to bring gas from Russia to China travelling from Siberia down through Central Russia to enter China between Mongolia and Kazakhstan.

Export prices edged downChina’s export prices of ERW API linepipe slipped in February as a reflection of enhanced international competition. ERW line-pipe with grade X52 API is selling at $730/tonne fob, down $10 from a month ago, while ERW line-pipe with grade X65 also moved down by the same amount to $840/tonne fob.

Apparent consumption of welded pipes in key Asian countries by product ('000 tonne)Country 2011 2012 Q3 2013 Oct-13 year-to-date y-o-y % chgChina LSAW line pipe 1112 1221 285 76 994 -2%HSAW line pipe 1556 1825 348 144 1102 -27%ERW line pipe 442 355 111 43 341 25%ERW OCTG 486 498 135 44 434 5%IndiaLSAW line pipe 302 227 55 29 60 -68%HSAW line pipe 174 271 98 32 256 13%ERW line pipe 96 50 40 12 110 155%ERW OCTG 2 9 2 0 8 -3%IndonesiaLSAW line pipe 67 204 10 1 272 142%HSAW line pipe 43 62 13 4 44 -7%ERW line pipe 9 26 4 1 17 -15%MalaysiaLSAW line pipe 33 25 48 49 97 20%HSAW line pipe 14 9 1 0 1 -88%ERW line pipe 5 25 6 3 1 -30%AustraliaLSAW line pipe 161 240 74 3 315 62%ERW line pipe 31 99 10 3 55 -33%Source: Customs Statistics, ISSB, Metal Bulletin Research estimates

Apparent consumption data is only available to paying

subscribers.

To subscribe, or for a preview of our data,

please contact our sales department on:

+44 (0) 20 7779 7999

WWW.MetalBulletinreSearch.coM FeBruarY 2014 MBR WEldEd liNEpipE ANd OCTG MarKet tracKer

13Welded lInepIpe & octG MarKet tracKer

Subscribe today

unlock the most extensive database of current, historical and forecast prices available anywhere

As well as this monthly report subscribers will also receive downloadable Excel data:

z Welded tube and pipe prices as well as plate and coil with three-year history and one-year forecast.

z North and South American apparent consumption of welded pipe by product with extensive historical data.

z Middle East and North African apparent consumption of welded pipe by product with three-year history.

z Asian welded tube consumption data by product and major country.

z European and CIS welded tube apparent consumption data by product by major country.

MBR WEldEd liNEpipE ANd OCTG MarKet tracKer FeBruarY 2014 WWW.MetalBulletinreSearch.coM

14 Welded capacIty develoPMentS and neWS

dIsclaIMer – IMportantplease read carefully

This Disclaimer is in addition to our Terms and Conditions as available on our website and shall not supersede or otherwise affect these Terms and Conditions.

Prices and other information contained in this publication have been obtained by us from various sources believed to be reliable. This information has not been independently verified by us. Those prices and price indices that are evaluated or calculated by us represent an approximate evaluation of current levels based upon dealings (if any) that may have been disclosed prior to publication to us. Such prices are collated through regular contact with producers, traders, dealers, brokers and purchasers although not all market segments may be contacted prior to the evaluation, calculation, or publication of any specific price or index. Actual transaction prices will reflect quantities, grades and qualities, credit terms, and many other parameters. The prices are in no sense comparable to the quoted prices of commodities in which a formal futures market exists.

Evaluations or calculations of prices and price indices by us are based upon certain market assumptions and evaluation methodologies, and may not conform

to prices or information available from third parties. There may be errors or defects in such assumptions or methodologies that cause resultant evaluations to be inappropriate for use. Your use or reliance on any prices or other information published by us is at your sole risk. Neither we nor any of our providers of information make any representations or warranties, express or implied as to the accuracy, completeness or reliability of any advice, opinion, statement or other information forming any part of the published information or its fitness or suitability for a particular purpose or use. Neither we, nor any of our officers, employees or representatives shall be liable to any person for any losses or damages incurred, suffered or arising as a result of use or reliance on the prices or other information contained in this publication, howsoever arising, including but not limited to any direct, indirect, consequential, punitive, incidental, special or similar damage, losses or expenses.

We are not an investment advisor, a financial advisor or a securities broker. The information published has been prepared solely for informational and educational purposes and is not intended for trading purposes or to address your particular requirements. The information provided is not an offer to buy or sell or a solicitation of an offer to buy or sell any security, commodity, financial product, instrument or other investment or to participate in any particular trading

strategy. Such information is intended to be available for your general information and is not intended to be relied upon by users in making (or refraining from making) any specific investment or other decisions. Your investment actions should be solely based upon your own decisions and research and appropriate independent advice should be obtained from a suitably qualified independent advisor before making any such decision.

Unauthorised and/or unlicensed copying of any part of this publication is in violation of copyright law. Violators may be subject to legal proceedings and liable for substantial monetary damages per infringement as well as costs and legal fees.

For information about copyright licenses please contact Simon Gates on COPYWATCH in the UK on +44 (0) 20 7827 6481. Brief extracts may be used for the purposes of publishing commentary or review only provided that the source is acknowledged.

this issue was published on 23 february 2014. the next issue will be published on 23 March 2014.

Tejas Tubular announces plans for Nebraska OCTG millEarlier this month, Tejas Tubular and the governor of Nebraska announced plans for Tajas to build a 150,000 tpy welded OCTG facility in Norfolk, Nebraska. Construction is scheduled to begin this year on the 350,000 sq. ft. plant which will produce casing, drill pipe and linepipe. The company already has a strategic partnership with Nucor to supply steel substrate to the plant. The project is receiving $5m in state and local grants and expects to apply for further business development incentives which are intended to promote job growth.

Tejas is also in the process of building a 72,000 tpy OCTG processing facility in New Carlisle, Indiana. It is intended to focus on heavy-walled production casing for sizes 4 ½ - 9 5/8” OD. The facility will offer both semi-premium and premium threading.

Friedman Industries adding processing facilityFriedman Industries is planning to build a $9.2m pipe threading and processing plant adjacent to its existing ERW pipe mills in Lone Star, Texas. The plant will also offer testing and inspection services. Friedman’s Texas Tubular Products division operates a distribution center and two ERW tube lines which produce API 5CT and 5L as well as ASTM A500B and A53B.

Russian capacity risingRussian welded tube producer Uraltrubprom based in Pervouralsk, Sverdlovsk region is planning to launch a new ERW OCTG production line in the 1Q 2014. The production range will include diameters from 146 to 324mm, API 5CT and GOST P 53366 in grades from H40 to P110. In house threading line is capable of making buttress, STC, LTC as well as GOST – OTTM and OTTG threads.

Published monthly by Metal Bulletin Research (MBR), the research and forecasting division of Metal Bulletin Ltd.

editor Kim Leppold, [email protected]+1 610 404 0801head of tubular consultingJames [email protected]+44 207 827 6443 consultantRoman [email protected]+44 207 827 6443contributorsXiaolei Xu, Analyst head of researchAlistair Ramsay

MBr directorPhilip ManleyMetal Bulletin ResearchNestor House Playhouse YardLondon EC4V 5EX

- The Five Year outlook for the Global OCTG industry

- Strategic Prospects for the Global Transmission Linepipe Market by type, size, range and grade

- The Five Year Outlook for the Small-diameter Linepipe Market (under 16” OD)

- A Strategic Outlook for the OCTG Heat Treatment, Threading, Coupling and Premium Connection Sectors out to 2020

- Steel Weekly Market Tracker

- Galvanised Steel and Tinplate Market Tracker

- Stainless Steels Monthly Tracker

to receive a free sample of any of the above reports please email your details to: [email protected]

MBr Welded lInepIpe & octG MARKET TRACKER

WWW.MetalBulletinreSearch.coM FeBruarY 2014 MBR WEldEd liNEpipE ANd OCTG MarKet tracKer

15

Subscribe today

The information you provide on this form will be used by Euromoney Institutional Investor PLC and its group companies (“we” or “us”) to process your order and/or deliver relevant products/services and content. We may also monitor your use of our website(s), including information you post and actions you take, to improve our services to you and track compliance with our terms of use. Except to the extent you indicate your objection below, we may also use your data (including data obtained from monitoring) (a) to keep you informed of our products and services; (b) occasionally to allow companies outside our group to contact you with details of their products/services; or (c) for our journalists to contact you for research purposes. As an international group, we may transfer your data on a global basis for the purposes indicated above, including to countries which may not provide the same level of protection to personal data as within the European Union. By submitting your details, you will be indicating your consent to the use of your data as identified above. Further information on our use of your personal data is set out in our privacy policy, which is available at www.euromoneyplc.com or can be provided to you separately upon request. If you object to contact as identified above by telephone ̈ , fax ̈ , or email ̈ , or post ̈ , please tick the relevant box. If you do not want us to share your information with our journalists ̈ , or other companies ̈ please tick the relevant box.

I want to subscribe to MBR’s Welded Linepipe & OCTG Market Tracker