32

TECHNOLOGY A wake-up call for Europe IT sector competitiveness INFORMATION, COMMUNICATIONS & ENTERTAINMENT

TECHNOLOGY

A wake-up call for EuropeIT sector competitiveness

INFORMATION, COMMUNICATIONS & ENTERTAINMENT

Introduction 1

Executive summary 3

How European IT players stack up 5

Some strengths, more weaknesses 7

A tough road ahead 15

Conclusion 19

Appendix: Survey results 21

Contents

On behalf of KPMG’s Information, Communications and Entertainmentpractice, we are pleased to introduce this review of Europe’s technologysector. Produced in co-operation with the Economist Intelligence Unit,the aim of this study is to analyze the strengths and weaknesses ofEurope’s information technology firms in a global context.

Europe’s IT firms face very difficult challenges. Only a handful currentlyenjoy the scale of their North American rivals, while lower cost Asianfirms are improving their performance in areas such as innovation.European suppliers’ traditional strengths, the technical excellence of theirproducts and services, and their ability to build strong customer andpartner relationships, will stand them well in the global competition tocome. This report makes clear, however, that addressing their lack ofcompetitiveness in pricing is a matter of urgency.

Europe’s technology sector enjoys another potential advantage –concerted policymaker attention at the EU level. The strategies developedby the European Union to foster the development of an informationsociety, if followed through, have the promise of strengthening thesector’s long-term competitiveness.

KPMG’s Information, Communications and Entertainment practice aimscontinuously to provide our firms’ with informed perspectives on criticalindustry issues. The following analysis not only highlights the depth of industry knowledge available from KPMG firms, but also demonstratesan on-going commitment to turning knowledge into value for the benefitof our global network’s clients, people, and the capital markets.

European IT Competitiveness 1

Introduction

Gary MatuszakGlobal Chair, KPMG’s Technology practiceKPMG in the U.S.

Crispin O’BrienUK ChairKPMG’s Technology practiceKPMG in the U.K.

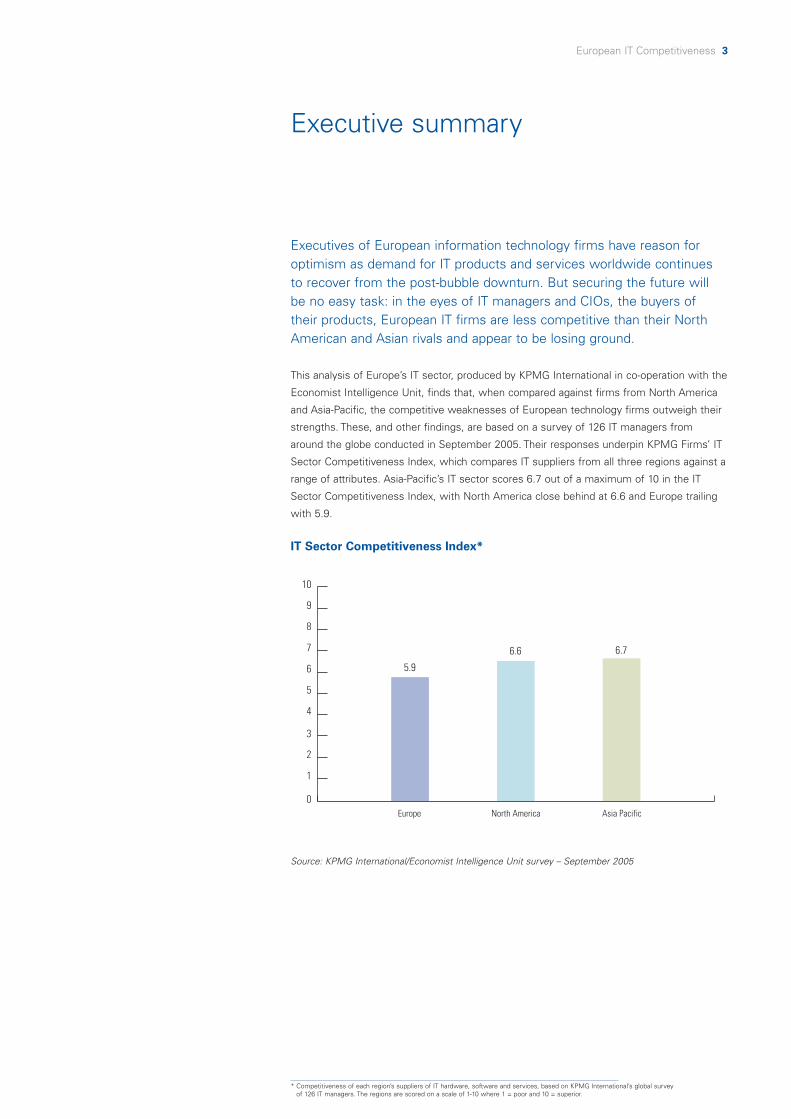

Executives of European information technology firms have reason foroptimism as demand for IT products and services worldwide continuesto recover from the post-bubble downturn. But securing the future will be no easy task: in the eyes of IT managers and CIOs, the buyers of their products, European IT firms are less competitive than their NorthAmerican and Asian rivals and appear to be losing ground.

This analysis of Europe’s IT sector, produced by KPMG International in co-operation with the

Economist Intelligence Unit, finds that, when compared against firms from North America

and Asia-Pacific, the competitive weaknesses of European technology firms outweigh their

strengths. These, and other findings, are based on a survey of 126 IT managers from

around the globe conducted in September 2005. Their responses underpin KPMG Firms’ IT

Sector Competitiveness Index, which compares IT suppliers from all three regions against a

range of attributes. Asia-Pacific’s IT sector scores 6.7 out of a maximum of 10 in the IT

Sector Competitiveness Index, with North America close behind at 6.6 and Europe trailing

with 5.9.

European IT Competitiveness 3

* Competitiveness of each region’s suppliers of IT hardware, software and services, based on KPMG International’s global survey of 126 IT managers. The regions are scored on a scale of 1-10 where 1 = poor and 10 = superior.

Executive summary

IT Sector Competitiveness Index*

0

1

2

3

4

5

6

7

8

9

10

Europe North America Asia Pacific

5.9

6.6 6.7

Source: KPMG International/Economist Intelligence Unit survey – September 2005

Other key findings from our analysis include the following:

• High prices and a perception of less value for money are the major weaknesses in

European IT firms’ competitive armor. They perform well, on the other hand, in the areas

of technical excellence and strength of customer and partner relationships. If price and

value for money are factored out, Europe performs on a par with Asia and reduces the gap

with North America. But of course price cannot be ignored.

• IT managers will expect continued concessions on pricing from their suppliers, as well

as greater flexibility in structuring contracts, but a large number doubt the ability of

European suppliers to deliver in these areas. It is here that European IT firms can be

most vulnerable to Asian competitors, not only in international markets but potentially

also at home.

• All parts of Europe’s IT industry are not equal. Suppliers of IT services, hardware, desktop

software and microelectronics are seen to be losing ground in competition with firms

from other regions. Producers of mobile devices, applications and enterprise software,

however, score high marks, and IT managers believe these firms are becoming more

competitive vis-à-vis their American and Asian rivals.

• Europe’s technology firms have clear options to help improve competitiveness. Some will

innovate with pricing strategies, or make better use of off-shoring to help reduce costs

and improve service delivery. Others may also acquire rivals in order to broaden portfolios

and gain economies of scale. All will have to address perceived value for money.

In its ‘i2010’ strategy, the European Commission aims to redress the weaknesses in

Europe’s technology sector by, among other things, focusing national efforts to expand

IT research and development and fostering other components of the digital economy.

Reaching these objectives will be welcome: the EU currently devotes three percent of its

annual budget to supporting research and innovation, compared to 37 percent that goes to

supporting agriculture. But in the final analysis, the fortunes of Europe’s IT sector will hinge

on the business acumen that its firms’ leaders, employees and owners are able to muster

for the challenge ahead.

4 European IT Competitiveness

What is a European IT firm?European IT firms are defined here as

suppliers of IT hardware, software and

services whose birthplace is Europe.

Country or region of origin is important to

this analysis as, in our view, it is the

business environment which can

determine the ability of entrepreneurs

and their firms to emerge and grow.

Thus, although they have a major

presence in Europe and dominate many

corners of Europe’s IT market, firms such

as IBM, Microsoft, Oracle, HP and others

are considered as U.S. firms, products as

they are of America’s particular business

and technology crucible. Likewise, few

would argue that Asia-headquartered

firms and European technology

companies, wherever they operate,

exhibit unique management, operational

or cultural features that set them apart

from their counterparts elsewhere.

The 2005 survey on Europe’s ITcompetitivenessIn September 2005, KPMG and the

Economist Intelligence Unit polled 126

CIO’s, IT managers and directors for their

views on IT sector competitiveness.

The survey was cosmopolitan, covering

more than 20 countries in three regions.

A range of industries was represented,

with manufacturing, healthcare, financial

services, telecoms and IT accounting

for the majority of respondents.

The companies represented in the

survey were of substantial scale: 58

percent earn more than US$500 million

in annual revenue, and 44 percent earn

over US$1 billion.

Geographic distribution of survey respondents

Western Europe

Middle East & Africa

Asia Pacific

Latin America

North America

Eastern Europe

38%

2%25%

6%

23%

6%

Source: KPMG International/Economist Intelligence Unit survey – September 2005

When it comes to serving multinational corporations (MNCs) with IThardware, software and services, European-headquartered suppliers haveoften struggled to compete against their North American counterparts.

Andy Green, CEO of BT Global Services, which targets MNCs for the provision of

‘networked IT services’, illustrates starkly how far European IT firms are perceived by large

enterprises to lag behind. “Fortune 1000 companies want to be confident of enterprise-

wide [global] delivery from their suppliers of traditional IT services,” he says. “But of the

European players, only CapGemini – at a stretch – is seen as capable of providing that

reach. From the U.S., on the other hand, CSC, EDS, HP, IBM and Accenture all have

that capability.”

Adding to the competitive pressures is the growing strength of Asia-based suppliers.

ABN Amro’s recent awarding of IT outsourcing contracts worth €300 million to Tata

Consulting Services and Infosys is a good example of how far Indian-based IT players have

come to be trusted by large enterprise customers headquartered in Europe and who

operate on a global scale.

Not just a problem of scaleA dissimilar potential to leverage economies of scale is often used to explain the

competitive imbalance between North American and European IT firms. U.S. firms play in a

large and homogenous domestic market, so this argument goes, whereas Europe’s multiple

cultures, languages and operating environments constrain cross-border growth for home-

grown IT players.

Europe’s IT players are not just innocent victims of geographical circumstance however.

In particular, IT buyers view them as unable to meet their demands for lower prices and

inflexible on how they structure contracts. This suggests a lack of commercial innovation

on behalf of the European IT players, which is hardly a function of geographical location.

The top Asia-based players, meanwhile, appear to be mastering the art of providing

attractive pricing to MNCs around the globe without falling competitively short of

meeting local IT needs.

The difficult position that Europe’s IT suppliers find themselves in vis-à-vis competitors

from other regions is manifested in the IT Sector Competitiveness Index, developed for

this report and based on KPMG International’s global survey of 126 IT managers conducted

in September 2005. Overall, the surveyed executives rate IT suppliers from the Asia-Pacific

region as slightly more competitive than their rivals from North America, and a good deal

more than those from Europe.

European IT Competitiveness 5

How European IT players stack up

IT Sector Competitiveness Index*

6 European IT Competitiveness

* Competitiveness of each region’s suppliers of IT hardware, software and services, based on a global survey

of 126 IT managers. The regions are scored on a scale of 1-10 where 1 = poor and 10 = superior.

Overall competitivenessCompetitiveness criteriaInnovationTechnical excellenceAttention to localneeds/tastesScope for customizationPrice competitivenessValue for moneyCustomerservice/product support

Europe5.9

6.16.7

6.26.24.75.5

6.0

North America6.6

7.57.4

5.76.36.46.4

6.5

Asia-Pacific6.7

6.56.7

5.96.38.07.4

5.8

Scratching below the surface reveals a more complex picture than the overall score

suggests. If price and value for money are factored out, Europe performs on a par with Asia

in our index and reduces the gap with North America. And while some corners of Europe’s

technology sector are weak in global context, others outperform their global rivals.

In the next section, we take a closer look at the gaps in performance between European,

North American and Asian technology suppliers as perceived by the executives who buy

their products. In the last section we provide examples of how some European IT firms are

striving to remain competitive, and highlight a few areas where Europe’s IT sector should

be able to strengthen its armor.

Explaining the IT SectorCompetitiveness Index In order to help gauge the relative

strengths and weaknesses of European,

Asian and North American information

technology firms, KPMG International

and the Economist Intelligence Unit

polled 126 IT managers and CIOs from

around the globe. The survey results

underpin the “IT Sector Competitiveness

Index,” which is discussed throughout

this white paper. Respondents were

asked to rate suppliers of IT hardware,

software and services from each region

against seven criteria: innovation;

technical excellence; attention to local

needs; scope for customization;

customer service and product support;

price competitiveness; and value for

money. Ratings were assigned on a scale

of one to five, with one denoting ‘poor’

and five denoting ‘superior’. The index

model then converted the ratings from all

respondents to weighted-average scores

on a 10-point scale. In addition to scores

for each criterion, the model also

generated an overall competitiveness

score for each region’s IT sector.

Source: KPMG International/Economist Intelligence Unit survey – September 2005

European IT firms deliver well in many areas when compared withcompetitors from other regions. Nonetheless, the verdict of the ITexecutives in our survey appears to be that European IT suppliers’weaknesses currently outweigh their strengths, and as a result they arebecoming less competitive than their Asian and North American rivals.

Strength in mobilityIt would be misleading to assign this verdict to all parts of Europe’s IT industry. Not

surprisingly, IT managers in our survey give low ratings to Europe-based suppliers of IT

hardware, where U.S. and Asian producers have long dominated the field, and desktop

software, the realm of Microsoft. And, despite the presence of a few strong players,

European microelectronics firms are also seen to be fighting an uphill battle.

European suppliers of mobile devices and applications have been trailblazers in their

respective product areas, and enterprise purchasers of IT deem them highly competitive.

In the realm of devices, the Nordic giants, Nokia and Ericsson, set the pace of handset

design and marketing early on, with a handful of smaller producers also establishing strong

market positions. Their activity helped also to spawn a strong mobile software community.

Applications from firms such as Webraska, Zed and Aspiro operate not only in the devices

and networks of European suppliers but also those of their Asian and North American

competitors. Nearly half the IT managers in our survey feel that European mobile

applications providers are gaining in strength vis-à-vis competitors from other regions,

and another 30 percent believe they are at least holding their ground.

Jorgen Behrens, Vice President Strategy & Product Management at Symbian, the Nokia-led

venture whose operating system powers the current generation of smartphones,

acknowledges the strength of his Asian rivals. “Japan and Korea are still the world’s leaders

in mobile application innovation,” he says, “but the European application developers are

rapidly catching up. In the U.S., where mobile markets are least developed, mobile

application development lags behind.”

Another European leader in the field in U.K.-based LogicaCMG, which provides messaging

software used by mobile operators. According to Chris McDermott, CEO of the company’s

global telecom division, the firm's strongest competitive challenge currently emanates from

the U.S., but he sees a growing threat as well from low-cost Chinese vendors. Yet he

expects the competitive wars to be fought on more than just price. “Experience and

expertise in specialist areas will be an important asset; in this context, a weakness of the

Chinese vendors may be the breadth of their product portfolios,” argues Mr McDermott.

European IT Competitiveness 7

Some strengths, more weaknesses

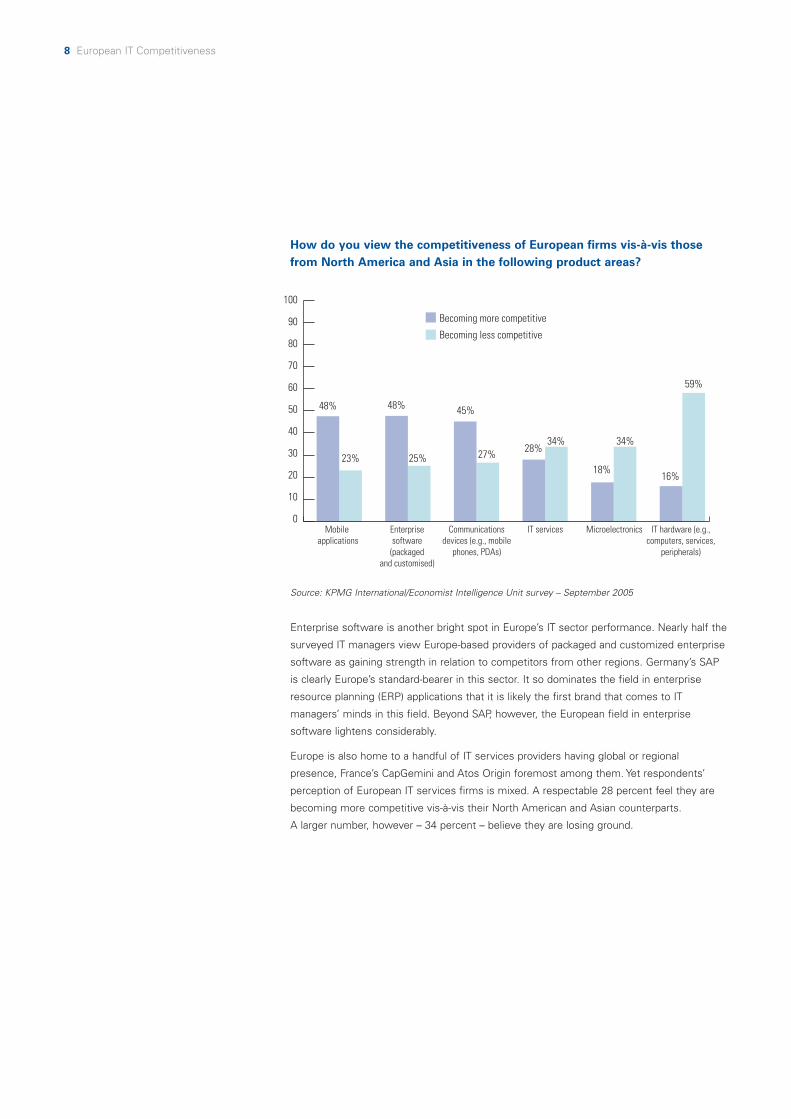

How do you view the competitiveness of European firms vis-à-vis thosefrom North America and Asia in the following product areas?

8 European IT Competitiveness

0

10

20

30

40

50

60

70

80

90

100

Mobile applications

Enterprise software (packaged

and customised)

Communications devices (e.g., mobile

phones, PDAs)

Becoming more competitive

Becoming less competitive

48%

IT services Microelectronics IT hardware (e.g., computers, services,

peripherals)

23%

48%

25%

45%

27% 28%34%

18%

34%

16%

59%

Source: KPMG International/Economist Intelligence Unit survey – September 2005

Enterprise software is another bright spot in Europe’s IT sector performance. Nearly half the

surveyed IT managers view Europe-based providers of packaged and customized enterprise

software as gaining strength in relation to competitors from other regions. Germany’s SAP

is clearly Europe’s standard-bearer in this sector. It so dominates the field in enterprise

resource planning (ERP) applications that it is likely the first brand that comes to IT

managers’ minds in this field. Beyond SAP, however, the European field in enterprise

software lightens considerably.

Europe is also home to a handful of IT services providers having global or regional

presence, France’s CapGemini and Atos Origin foremost among them. Yet respondents’

perception of European IT services firms is mixed. A respectable 28 percent feel they are

becoming more competitive vis-à-vis their North American and Asian counterparts.

A larger number, however – 34 percent – believe they are losing ground.

The strength of American IT service providers such as IBM and EDS, and the rise of Asia’s

outsourcing giants, may help to explain such perceptions. Alexandre Steiner, Vice President

of global portfolio and marketing at Netherlands based Getronics a supplier of managed IT

and communications services, acknowledges that the big U.S. based firms have made

significant inroads into Europe’s IT outsourcing markets. He argues, however, that it is their

greater marketing muscle – rather than intrinsically better solutions – that has been a major

driver of this trend. “When we go up against the big boys to build, deploy and manage an

enterprise’s ICT infrastructure, there is a perception in the market that we can’t do it as well

they can,” he says. “We have to fight against that perception.”

This may also help to explain an apparent ambivalence by European enterprises towards

local suppliers: nearly as many European respondents (30 percent) believe local IT service

providers are becoming less competitive as those (33 percent) who hold the opposite view.

Our survey suggests that there is a natural loyalty towards local players but, in the

provision of IT services, it is being seriously tested by not only North American but also

by Asian players.

Quality in products and relationshipsEurope’s technology leaders rightly view the high quality and technical superiority of their

products as their chief competitive edge in the global marketplace. IT managers confirm

this perception: European IT firms earn a score of 6.7 on ‘technical excellence’ in the IT

Sector Competitiveness Index, behind North American suppliers but ahead of their

Asian rivals.

IT managers in Asia-Pacific have a particularly high regard for the quality of European

solutions, with 65 percent saying their technical level is competitive or superior.

Three-quarters of Asian respondents cite product quality as European IT firms’

greatest strength.

European IT Competitiveness 9

How would you assess European suppliers of IT hardware, software andservices on technical excellence? (Responses of IT managers from differentregions)

0%

10%

20%

30%

40%

50%

60%

Generally uncompetitive Average Competitive Superior

European IT managers

North American IT managers

Asia Pacific IT managers

Source: KPMG International/Economist Intelligence Unit survey – September 2005

European firms also pride themselves on the strength of the relationships they have built

with customers and partners. Technology firms are no exception, and global IT managers

agree that European suppliers excel in this area. In the IT Sector Competitiveness Index,

European IT firms outperform both Asian and North American competitors in their attention

to local needs. Strength of partnerships – in marketing, research and development, supply

chain and other areas – is also regarded as a key European strength.

These advantages will continue to fare European firms well in markets close to home and,

for some companies, in North America. Asia will prove a tougher challenge: IT managers

there value European quality, but are not (at least yet) impressed with the level of local

attention received from European suppliers. The latter have done a commendable job at

incorporating local customers’ needs into their product offerings at home and in North

America, but their inability to achieve the same in Asia bodes ill for their prospects in this

rapidly expanding marketplace. Neither should their advantages be taken for granted

at home.

10 European IT Competitiveness

How would you assess European suppliers of IT hardware, software andservices on attention to local needs? (Responses of IT managers fromdifferent regions)

0%

10%

20%

30%

40%

50%

60%

Poor Generally uncompetitive

Average Competitive Superior

European IT managers

North American IT managers

Asia Pacific IT managers

Source: KPMG International/Economist Intelligence Unit survey

European purchasers of technology profess a high degree of regional loyalty. As discussed

earlier, nine in 10 would prefer to find local or regional suppliers for IT products and

services, all things being equal. A majority also say that they would require a significant

price differential to persuade them to trade with an IT supplier from another region. But a

significant price differential appears to exist, particularly when comparing European and

Asian players. It is not inconceivable that customers will forego some ‘local understanding’

in exchange for dramatic cost savings.

The pricing challengeAcross the globe, IT managers expect the prices they pay for technology products and

services to continue declining. They also expect their vendors to provide greater flexibility

in pricing and structuring of contracts. European suppliers fare poorly in these areas in

comparison with their North American and especially their Asian competitors. This explains

the yawing gap between European and Asian suppliers in the IT Competitiveness Index in

the area of pricing: Europe scores 4.7 on price competitiveness, easily its lowest mark out

of the seven categories, while Asia notches up 8.0, its single highest score.

Few IT managers in any region deem European firms to be competitive on price, but Asian

customers are particularly critical of their performance. This underscores how difficult it may

be for European IT firms to expand into Asia as enterprises there increasingly have the

option of turning to local and more price competitive IT firms.

European IT Competitiveness 11

How would you assess European suppliers of IT hardware, software andservices on price competitiveness? (Responses of IT managers fromdifferent regions)

0%

10%

20%

30%

40%

50%

60%

Generally uncompetitive

Poor Average Competitive Superior

European IT managers

North American IT managers

Asia Pacific IT managers

Source: KPMG International/Economist Intelligence Unit survey – September 2005

Just as alarming is the perception that European suppliers are unable to redress the pricing

imbalance. Forty-three percent of IT managers in the survey say that they see no change in

European price performance, while 40 percent see deterioration.

LogicaCMG’s Mr McDermott attributes some of the pressure on pricing to the increasing

power of customers. “Consolidation in different industry sectors has meant that the

negotiating power of customers has increased,” he observes. At the same time, he detects

a changing set of priorities among IT spenders: “In the telecoms industry, for example,

reduction in costs has been their dominant motivation in the past, but they are now giving

greater priority to innovation.”

If this is the case, it could work in European firms’ favor, as IT managers believe European

suppliers are improving on innovation, even though North American and Asian firms

currently outperform Europe in the Index on this competitive attribute. Of course, the larger

problem is that customers are unwilling to pay a sufficient premium for European quality.

The perception of high prices is only one part of the pricing problem for European IT firms,

lack of pricing flexibility is the other. Less than 20 percent of global IT managers believe that

pricing flexibility is a strength of European suppliers in comparison to IT firms from other

regions. This is a concern because pricing flexibility is exactly what IT buyers are

demanding. An overwhelming majority of survey respondents – 82 percent – expect to see

significant changes over the next two years in how suppliers structure the pricing of

software and services.

Value for money?Europe’s IT leaders acknowledge the perception among customers that their products

carry high price tags. In response they tend to stress the extra value and ‘total cost of

ownership’ benefits that their more expensive offerings bring to customers. “We sell our

applications at a premium to the competition because our products are superior,” says

Stefan Gruber, head of investor relations at SAP.

Mr Gruber acknowledges that the German firm is facing “a lot of pricing pressure” and that

it will most likely look at new contract structuring models. (See next section.) But overall,

there will not be much change. “Due to the quality of our products, we believe we can

sustain our prices,” says Mr Gruber.

As a global leader in the provision of enterprise software, SAP arguably has the market

power to achieve this. Few other European firms are likely to be able to pull it off, however.

No more than a quarter of IT managers in the survey say that European IT firms are

‘competitive’ or ‘superior’ in delivering value for money, with the remainder judging them to

be ‘average’ or ‘generally uncompetitive’. By contrast, 46 percent of respondents deem

North American IT suppliers as ‘competitive’ or ‘superior’ on value for money, while a

staggering 69 percent believe the same of Asian suppliers.

12 European IT Competitiveness

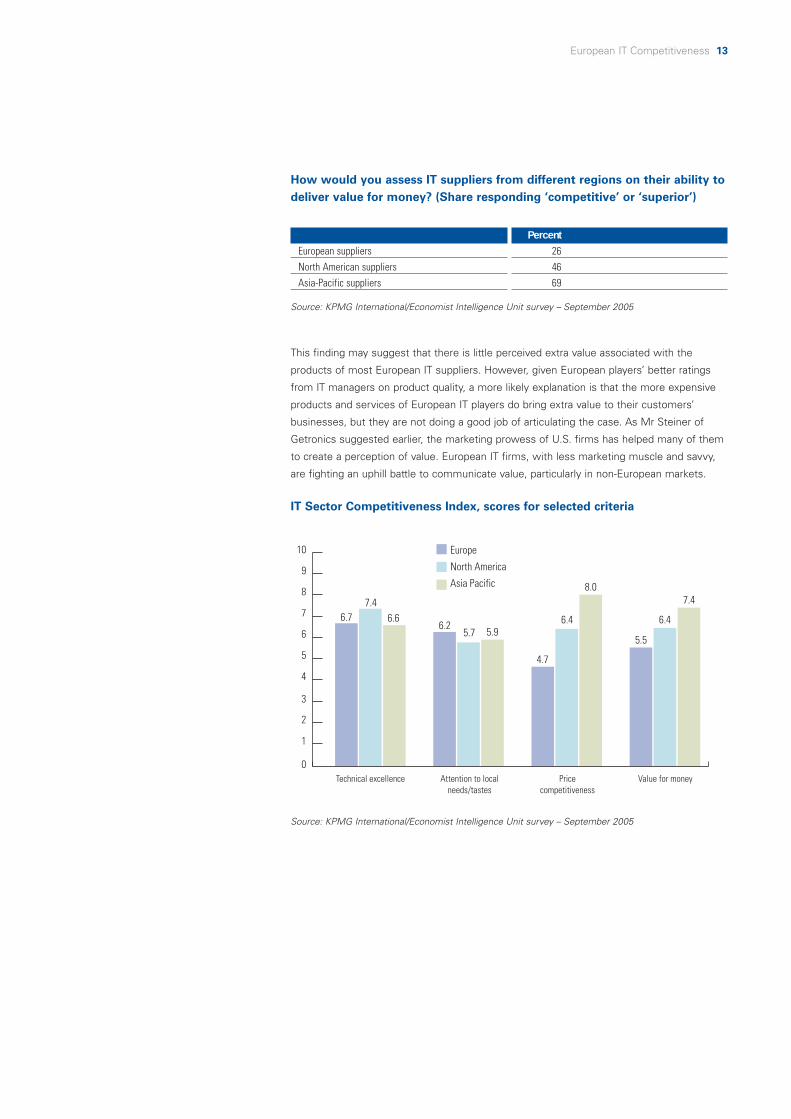

This finding may suggest that there is little perceived extra value associated with the

products of most European IT suppliers. However, given European players’ better ratings

from IT managers on product quality, a more likely explanation is that the more expensive

products and services of European IT players do bring extra value to their customers’

businesses, but they are not doing a good job of articulating the case. As Mr Steiner of

Getronics suggested earlier, the marketing prowess of U.S. firms has helped many of them

to create a perception of value. European IT firms, with less marketing muscle and savvy,

are fighting an uphill battle to communicate value, particularly in non-European markets.

European IT Competitiveness 13

How would you assess IT suppliers from different regions on their ability todeliver value for money? (Share responding ‘competitive’ or ‘superior’)

European suppliersNorth American suppliersAsia-Pacific suppliers

Percent264669

IT Sector Competitiveness Index, scores for selected criteria

0

1

2

3

4

5

6

7

8

9

10

Technical excellence Attention to local needs/tastes

Price competitiveness

Value for money

6.77.4

6.66.2

5.7 5.9

4.7

6.4

8.0

5.5

6.4

7.4

Europe

North America

Asia Pacific

Source: KPMG International/Economist Intelligence Unit survey – September 2005

Source: KPMG International/Economist Intelligence Unit survey – September 2005

There is good news and bad for European firms as they look at demandfor IT products and services over the next two years. Industry analystspaint a relatively bright picture for IT spending in Europe. The U.S.research firm IDC sees new investment by West European firms in IThardware, software and services expanding by over five percent perannum between now and 2007 (about the same clip as in Asia-Pacificand slightly higher than in North America). It sees IT spending growingeven faster in Eastern Europe over the same period, at about 12 percent per annum. Similarly, EITO (the European Information TechnologyObservatory Report 2005) projects European Union-wide investment in ITand telecommunications equipment and services to expand by 4.2percent in 2006, with slower telecoms spending growth a drag on therest of the sector.

European IT Competitiveness 15

A tough road ahead

Western Europe IT market size and growth, 2005-2007 (U.S.$bn)

0

50

100

150

200

250

300

350

400

2005 2006 2007

Hardware

Software

Services+5%+5.2%

+5.5%

Source: IDC – Market Research (2005)

European software and IT services firms should benefit from this modest upsurge in

demand after the post-bubble downturn of 2001-2003. About three-quarters of IT managers

in our survey say they expect to maintain or boost their spending with European suppliers

of software and services over the next two years. This sentiment is strongest among IT

managers based in Europe. It weakens considerably, though, among North American and

Asian respondents.

Historically, European IT players have found it difficult to compete against their North

American and Asian counterparts outside their home territories. While North American and

Asian players have made their presence felt strongly in Europe, European IT players – with

the noticeable exception of SAP – have not been able to make anywhere near a similar

impact in North America and Asia. And even the German software giant has found it tough

going. “The U.S. is a far more challenging market for us than Europe,” says SAP’s

Mr Gruber, although he points out the firm has gained significant market share there in

competition with its big US peers in the past two years.

Is your firm likely to spend more, the same or less with European suppliersof IT hardware, software and services over the next two years?

16 European IT Competitiveness

European suppliers of IThardwareEuropean suppliers ofsoftwareEuropean suppliers of ITservices

More

21%

29%

27%

About the same

52%

48%

48%

Less

27%

23%

25%

Source: KPMG International/Economist Intelligence Unit survey – September 2005

Judging by our survey, it is a situation that looks set to continue until at least 2007. Less

than 15 percent of North American respondents, for example, say they plan to spend more

with European suppliers on either hardware or software, although the picture for IT services

is somewhat brighter.

Asia looks the most unattractive market for European IT firms on this evidence. An average

of about 35 percent of Asian IT managers say they’ll spend less with European suppliers

over the next two years. With a growing and competitively priced supply of IT products and

services on their doorstep, many Asian customers appear comfortable reducing their spend

with European firms.

How can they compete more effectively?The demand outlook notwithstanding, our analysis paints a sobering picture for Europe’s

technology firms, of deteriorating competitiveness in the global marketplace. Much of this

is down to price levels, an area where European companies, based in higher-cost

environments than their U.S. and Asian rivals, have little room to manoeuvre.

There are no easy fixes for European firms, but there are a few areas in which they can

respond more effectively to the ‘less value for money’ perception.

Flexibility of pricing. Cutting prices may be difficult, but European suppliers can do more

to embrace more flexible approaches to structuring prices and contracts. Examples of

practices that are already common among North American suppliers include on-demand

pricing and revenue-sharing, where the provider shares the risk of investment with the

customer. LogicaCMG applies the latter model in contracts with some operators. Rather

than pay upfront for its mobile messaging software, the operator shares a portion of the

revenue generated by the messaging service. “We expect to see the structure of contracts

change to encompass more risk sharing,” says Mr McDermott.

Not all European technology firms are convinced that the structure of contracts for

enterprise customers will change radically. Says SAP’s Mr Gruber: “I can’t see the licence-

fee-per-user-model going away. “At the same time, he accepts that the way software is

delivered may need to evolve to meet changing customer demand, and he relates that SAP

will launch an on-demand CRM initiative in early 2006.

European IT firms have not employed off-shoring with nearly the same gusto as North

American competitors. Cultural and political considerations militate against this in many

European countries, but companies that do take the plunge should create greater room for

manoeuvre for themselves in pricing. IT service providers can also employ the practice to

compete more effectively on pricing for IT outsourcing, and to provide a means of serving

enterprises on a global scale without sacrificing on serving local needs.

European IT services firms would do well to develop a ‘blended’ off-shoring and near-

shoring service delivery model. Over half of our survey respondents say they expect to

expand the outsourcing of IT services to off-shore providers in the next two years, while 52

percent say they are attracted to the concept of near-shoring to help enable outsourcing to

take place in similar time zones.

Mr McDermott of LogicaCMG recognizes that the competitive gauntlet has been laid down

on service delivery and claims that LogicaCMG, for one, is responding in kind. “We are

focused on a blended model: a mixture of on-shore, near-shore and off-shore,” he says.

“If you outsource everything to, say, India, you can risk diluting your relationship with the

customer. The client needs people near them who are knowledgeable about their business,

possess industry understanding and have techical excellence, wherever they may be

physically located – you need to have a flexible model in terms of delivery."

Dutch IT services firm Getronics has adopted a similar approach but with a nuance. It set

up in 2004 three ‘global service centers’ with the aim of reaping cost economies and

enabling more responsive service delivery to local customers. But they are based in

Mexico, Budapest and Singapore rather than the more familiar offshoring locations in Asia.

“If we try just to compete on price we’re dead,” says Alexandre Steiner, Vice President of

global portfolio and marketing. “While we will use India as a base for back-office tasks to

lower our costs, the location of our global service centers is influenced by other factors: the

ability of people, from both a language and cultural perspective, to deal with our customers’

support requirements directly.”

Build scale, with caution. Another potential response to pricing pressure is to build

economies of scale through acquisition. America’s IT giants have embraced this approach

with passion, feeding a wave of consolidation over the past year, particularly in the software

market. LogicaCMG and Getronics are two European firms that are following suit, having

made recent purchases of rivals in France and the Netherlands, respectively.

European IT Competitiveness 17

Mr McDermott of LogicaCMG firmly believes that inorganic growth is the answer to achieve

scale. “We will continue to look for acquisitions,” he says. “As an IT services company,

we want to be in the world’s top ten and to do that, we will have to make acquisitions.

That includes, eventually, making purchases in North America.” Getronics’ Mr Steiner

believes that building scale is a prerequisite to expanding globally. “If you are strong in

your home market it puts you in a better position to go after the international markets,” he

argues. “You have greater credibility.”

But the M&A strategy is not a sure winner. There will be inevitable product integration

hurdles to overcome and – in the case of LogicaCMG and Getronics – it is still uncertain

how far a greater presence in their home country markets will be enough to make them

significantly more competitive on the international stage.

SAP’s Mr Gruber also has a warning for software companies seeking growth by acquisition.

“An organic growth strategy is a superior one,” he says. “Integration takes time and always

leads to a deterioration of product quality. There are also enormous costs in stitching

together disparate software code bases following a large acquisition in the software

industry, not to mention the challenge of integrating different corporate cultures.”

Building scale through M&A, then, is not for everyone. Those IT suppliers embarking on an

acquisition will therefore need to make every effort to reassure their existing customers

that product quality and development will not be compromised. Firms that opt to grow

organically, on the other hand, will need to be able to partner extremely effectively in order

to project strength in North American or Asian markets. Mr Steiner points out that such

partnerships with Asian competitors can also help European firms in other areas: “Asian

players are very strong on technology development, and there is a good argument for us to

establish more partnerships with them to pool our respective strengths.”

18 European IT Competitiveness

European technology firms are going to have to fight hard against a perception – generally

felt by enterprises around the globe – that North American and Asian suppliers will be the

natural choice for their IT services and products in the future. Looking ahead to 2007, IT

managers in the KPMG International/EIU survey are convinced that the United States will

remain home to some of the world’s strongest suppliers of hardware, software and

services. This should be no surprise to executives of Europe’s IT firms. What should be

more worrying to them is the expectation among global purchasers of IT that India and

China will not be far behind.

Compared with their global peers, European IT managers assume less prominence for

Asian countries as home to IT industry leaders and more for the likes of Germany and the

United Kingdom. To the extent that this reflects broader corporate thinking in Europe

overall, it should be considered alarming as it points to an underestimation of the threat

emanating from Asia.

European IT Competitiveness 19

Conclusion

In your opinion, which countries will be home to the strongest suppliers ofIT hardware, software or services in two years’ time? (Top ten countries)

United StatesIndiaChinaGermanyUnited KingdomJapanSouth KoreaFinlandRussiaSingapore

%84726440332521171110

Europe’s policymakers have a role to play in helping its technology firms meet the

challenge. The i2010 strategy adopted by the European Commission in June 2005 aims to

“modernize and deploy all EU policy instruments to encourage the development of the

digital economy: regulatory instruments, research and partnerships with industry.” A central

plank of the strategy addresses one of the areas where European IT firms are currently

outperformed by global rivals: improving innovation through stronger research and

development. Achieving the i2010 goal of boosting R&D spending in the technology

sector by 80 percent will help. But is this agenda sufficiently far-reaching?

Europe’s technology firms have reason to be proud of their successes and the reputations

they have earned for quality and strong customer relationships. But to remain competitive

on a global scale, like so many other industries before them, they need to address their

shortcomings as a matter of urgency.

Source: KPMG International/Economist Intelligence Unit survey – September 2005

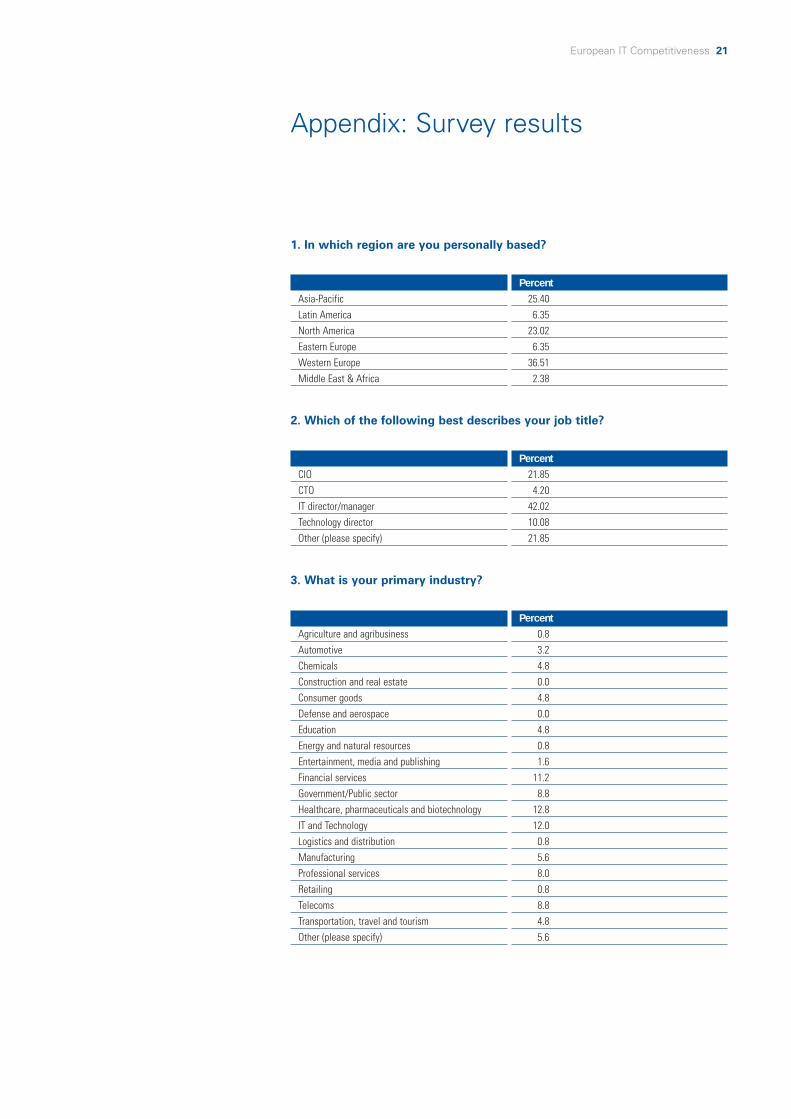

1. In which region are you personally based?

European IT Competitiveness 21

Appendix: Survey results

Asia-PacificLatin AmericaNorth AmericaEastern EuropeWestern EuropeMiddle East & Africa

Percent25.406.35

23.026.35

36.512.38

2. Which of the following best describes your job title?

CIOCTOIT director/managerTechnology directorOther (please specify)

Percent21.854.20

42.0210.0821.85

3. What is your primary industry?

Agriculture and agribusinessAutomotiveChemicalsConstruction and real estateConsumer goodsDefense and aerospaceEducationEnergy and natural resourcesEntertainment, media and publishingFinancial servicesGovernment/Public sectorHealthcare, pharmaceuticals and biotechnologyIT and TechnologyLogistics and distributionManufacturingProfessional servicesRetailingTelecomsTransportation, travel and tourismOther (please specify)

Percent0.83.24.80.04.80.04.80.81.6

11.28.8

12.812.00.85.68.00.88.84.85.6

22 European IT Competitiveness

4. What are your organization’s global annual revenues in U.S. dollars?

$500 million or less$500 million to $1 billion$1 billion to $5 billion$5 billion to $10 billion$10 billion or more

Percent41.9414.5215.325.65

22.58

5. Is your firm likely to spend more, the same or less with Europeansuppliers of IT hardware, software and services over the next two years?

European suppliers of IT hardwareEuropean suppliers of softwareEuropean suppliers of IT services

6. How would you assess European suppliers of IT hardware, software andservices against the following criteria?

InnovationTechnicalexcellenceAttention tolocal needs/tastesScope forcustomizationPricecompetitivenessValue for moneyCustomerservice/productsupport

Poor2.38%

0.0%

4.8%

3.2%

4.8%0.0%

0.0%

Generallyuncompetitive

13.49%

8.8%

14.40%

15.20%

40.0%27.20%

20.63%

Average39.68%

35.20%

32.80%

36.80%

41.60%46.40%

42.06%

Competitive42.06%

45.60%

36.80%

36.00%

12.00%23.2%

30.95%

Superior2.38%

10.40%

11.20%

8.80%

1.60%3.20%

6.35%

More21.43%28.57%26.98%

About the same52.38%48.41%47.62%

Less26.19%23.02%25.40%

European IT Competitiveness 23

7. In your view, how is the performance of European suppliers changingagainst these criteria?

InnovationTechnical excellenceAttention to local needs/tastesScope for customizationPrice competitivenessValue for moneyCustomer service/product support

8. How would you assess North American suppliers of IT hardware,software and services against the following criteria?

InnovationTechnicalexcellenceAttention tolocal needs/tastesScope forcustomizationPricecompetitivenessValue for moneyCustomerservice/productsupport

Poor1.61%

0.81%

0.81%

2.44%

0.81%1.61%

0.0%

Generallyuncompetitive

1.61%

2.42%

27.42%

11.38%

14.63%8.87%

10.48%

Average24.19%

28.23%

41.94%

35.77%

30.89%43.55%

43.55%

Competitive51.61%

50.81%

20.97%

46.34%

48.78%41.94%

37.9%

Superior20.97%

17.74%

8.87%

4.07%

4.88%4.03%

8.06%

Improving44.80%45.97%32.80%29.60%17.74%18.55%27.20%

Deteriorating15.20%12.90%13.60%16.0%

39.52%29.03%17.60%

No change40.0%

41.13%53.60%54.40%42.74%52.42%55.20%

24 European IT Competitiveness

9. How would you assess Asian suppliers of IT hardware, software andservices against the following criteria?

10. When comparing the competitive attributes of IT suppliers fromdifferent regions, what do you view as the main strengths of Europe’s IThardware, software and services suppliers?

InnovationTechnicalexcellenceAttention tolocal needs/tastesScope forcustomizationPricecompetitivenessValue for moneyCustomerservice/productsupport

Poor3.23%

1.61%

4.07%

0.81%

1.61%0.81%

1.63%

Generallyuncompetitive

12.1%

9.68%

17.89%

14.63%

4.03%3.23%

21.14%

Average37.10%

37.90%

39.84%

38.21%

12.90%27.42%

42.28%

Competitive32.26%

38.71%

30.89%

36.59%

43.55%46.77%

27.64%

Superior15.32%

12.10%

7.32%

9.76%

37.90%21.77%

7.32%

ScaleGeographic reachAbility to innovateProduct qualityBreadth of product portfolioPricing flexibilityMarketing and sales effectivenessStrength of partnerships

Percent23.3954.0329.8458.8721.7716.9424.1958.06

European IT Competitiveness 25

11. How do you view the competitiveness of European firms vis-à-vis thosefrom North America and Asia in the following product areas?

IT hardware (eg., computers, servers,peripherals)Enterprise software (packaged andcustomized)Desktop softwareIT servicesCombined portfolio of hardware, softwareand/or servicesConsumer electronics devicesCommunications devices (eg., mobilephones, PDAs)Mobile applicationsMicroelectronics

12. Please indicate whether you agree with the following statements aboutIT suppliers in general.

All things being equal, we would prefer to find localor regional suppliers for at least some IT productsand servicesWe require a significant price differential topersuade us to trade with an IT supplier fromanother region

Agree

82.40%

60.80%

Disagree

13.60%

32.80%

Don’t know

4.00%

6.40%

13. Please indicate whether you agree with the following statements aboutthe supply of IT software and services.

We expect to see reductions in prices of softwareand services over the next two yearsWe expect to see significant changes over the nexttwo years in how suppliers structure the pricing ofsoftware and servicesWe expect to see IT services increasingly beingsupplied by hardware, software,telecommunications or other providers

Agree

78.57%

81.60%

64.80%Disagree

Disagree

19.84%

8.80%

19.20%

Don’t know

1.59%

9.60%

16.00%

Becoming morecompetitive

15.87%

47.58%16.00%27.78%

25.40%28.80%

44.80%48.00%17.6%

Becoming lesscompetitive

58.73%

25.00%47.20%34.13%

33.33%46.40%

27.20%23.20%33.60%

Remaining about the same

25.40%

27.42%36.80%38.10%

41.27%24.80%

28.00%28.80%48.80%

26 European IT Competitiveness

14. Please indicate whether you agree with the following statements aboutthe outsourcing of IT services.

15. In your opinion, which countries will be home to the strongest suppliersof IT hardware, software or services in two years’ time?

We expect to begin or increase the outsourcing of ITservices to off-shore providers in the next two yearsWe expect at least some of our off-shore providersof IT services to move on-shore within the next two yearsWe are attracted to the concept of “near-shoring” to enable our outsourcing to take place in similartime zones

Agree

52.80%

42.40%

52.00%

Disagree

36.00%

30.40%

24.00%

Don’t know

11.20%

27.20%

24.00%

United StatesUnited KingdomGermanyFranceNetherlandsSwedenFinlandItalyRussiaChinaIndiaJapanSouth KoreaAustraliaSingaporeOther

Percent84.1333.3340.486.358.737.94

16.671.59

11.1164.2972.2224.6

20.633.179.52

10.32

16. Please indicate whether you agree with the following statement: “The threat of terrorism in all its forms will lead to a significant increase in IT spending by firms in my region.”

AgreeDisagreeDon’t know

Percent40.8038.4020.80

kpmg.com

© 2005 KPMG International. KPMG International is aSwiss cooperative of which all KPMG firms aremembers. KPMG International provides no servicesto clients. Each member firm is a separate andindependent legal entity and each describes itself as such. All rights reserved. Printed in the United Kingdom.KPMG and the KPMG logo are registered trademarksof KPMG International, a Swiss cooperative.Designed and produced by KPMG LLP (U.K.)’s Design ServicesPublication name: A wake up call for EuropePublication number: 214-675 Publication date: November 2005

KPMG International is a Swiss cooperative that serves as a coordinating entity for a network of independent memberfirms. KPMG International provides no audit or other client services. Such services are provided solely by memberfirms in their respective geographic areas. KPMG International and its member firms are legally distinct and separateentities. They are not and nothing contained herein shall be construed to place these entities in the relationship ofparents, subsidiaries, agents, partners, or joint venturers. No member firm has any authority (actual, apparent,implied or otherwise) to obligate or bind KPMG International or any member firm in any manner whatsoever or vice versa.The information contained herein is of a general nature and is not intended to address the circumstances of anyparticular individual or entity. Although we endeavor to provide accurate and timely information, there can be noguarantee that such information is accurate as of the date it is received or that it will continue to be accurate in thefuture. No one should act on such information without appropriate professional advice after a thorough examinationof the particular situation.

Contact us

For further information about the services offered by KPMG’s Technology practice,please contact us:

Gary MatuszakKPMG LLP (U.S.)Silicon Valley+1 650 404 [email protected]

Crispin O'Brien KPMG LLP (U.K.)London+44 20 7311 [email protected]

Bruno WallrafKPMG LLP (Germany)Düsseldorf +49 211 475 [email protected]

Wouter van de BuntKPMG LLP (Netherlands)Amsterdam+31 20 656 [email protected]

Frédéric QuélinKPMG LLP (France)Paris+33 1 55 68 70 [email protected]