[email protected]Vice President, e-Business Development Dubai United Nations Conference on Trade & Development Conference on Electronic Commerce Strategies for Development Tunis June 20 th 2003 E-Payments – New Opportunities

United Nations Conference on Trade & DevelopmentConference on Electronic Commerce Strategies for Development TunisJune 20th 2003

E-Payments – New Opportunities

Electronic Commerce – % of Total TransactionsEC GDV Activity Continues to Grow

Source: MasterCard Data Warehouse

1.6

2

2.5

1 2.9

3

3.1

3

3.1

5 3.5

6

3.3

2 3.8

8

3.9

3.9

8

00.5

1

1.52

2.5

33.5

4

EC% of Total Volume

Agenda•E-Commerce, The Challenges•E-Commerce, The Solution

– PC Authentication Program

– Chip Authentication Program

– MasterCard 3-D Secure Implementation

•MasterCard Internet Gateway Service (MIGS)

E-Commerce Market Challenges

•Fear of fraud remains barrier to converting online browsers to online shoppers

•Consumer Internet purchases generally restricted to domestic marketplaces

Consumers

Merchants and Acquirers

E-Commerce Market Challenges

• No guarantee of payment for merchant

– Online chargebacks growing – Bears all risk for non-signature

based transactions– Online fraud losses mounting

• Lack of consistent mechanism toauthenticate the buyer to the seller

– Privacy laws restrict use of authentication tools

– High accountholder decline rate – limits activity, especially for cross-border transactions

Findings •Reason Code 37 represents:

– 58% for all chargebacks

– 70% of EC chargebacks

•Decline rates are:– 5% for all transactions

– 16% for EC transactions (same as MO/TO)

Note: Based on MasterCard records.

What is it?MasterCard SecureCode is MasterCard’s consumer and merchant facing program name/identifier for our guaranteed payment solutions

MasterCard SecureCode offers issuers flexibility with choice of authentication technology including both browser-based and applet-based solutions.

MasterCard SecureCode accommodates MasterCard credit and debit including Maestro

Chip Authentication Program

PC Authenticatio

n Program

MasterCard 3-D Secure

Implementation

EMV SPA SPA

Hidden Fields -and- Merchant Plug-In

UCAF DataTransport

MerchantRequirement

IssuerPlatform

Algorithm

Solution Structure

Issuer Choice: PC Authentication Program•PC Authentication Program -- A download

implementation of MasterCard's Secure Payment Application, based on the detailed specifications released 6/ 2001, and has been amended 8/2002 which fully interoperates with the UCAF hidden fields supported by participating merchants.

– This specification has been licensed to more than 84 technology vendors and involves the use of a small downloaded applet by the cardholder that works on his or her PC.

PC Authentication Program

Merchant

AcquirerUCAF passed to Issuer in authorization transaction. Issuer matches to original

and returns positive authorisation

UCAFwith AAV

Merchant Website

Cardholder sees….

Cardholder browses Merchant website

HiddenFields

UCAF

IssuerSPA

Server

Download detects Hidden Fields on Checkout Page and contacts Issuer SPA

Server

Download

PaymentDetails

Download uses hidden fields on merchant website to populate UCAF on merchant

website

AAV

Cardholder sees….Cardholder sees….

PINPINPINPINPINPINPIN

BankWindowCardholder

authenticated by Issuer

S C

Issuer Choice: Chip Authentication Program•Chip Authentication Program --

Designed to integrate the ease of use and security of an EMV-compliant smart card for authentication through a user's PC.

•This solution is designed to interoperate with the UCAF hidden fields specifications and is supported by both connected and un-connected smart card readers.

•Evaluating Clientless alternative

Chip Authentication Program

UCAFwith EMV Dynamic

Cryptogram

Merchant

AcquirerUCAF passed to Issuer in

authorization transaction including EMV cryptogram

Merchant Website

Cardholder sees….

Cardholder browses Merchant website

HiddenFieldsUCAF

IssuerAuthorization

System

Download detects Hidden Fields on Checkout Page

Download

PaymentDetails

Download uses hidden fields on merchant website to populate UCAF on merchant

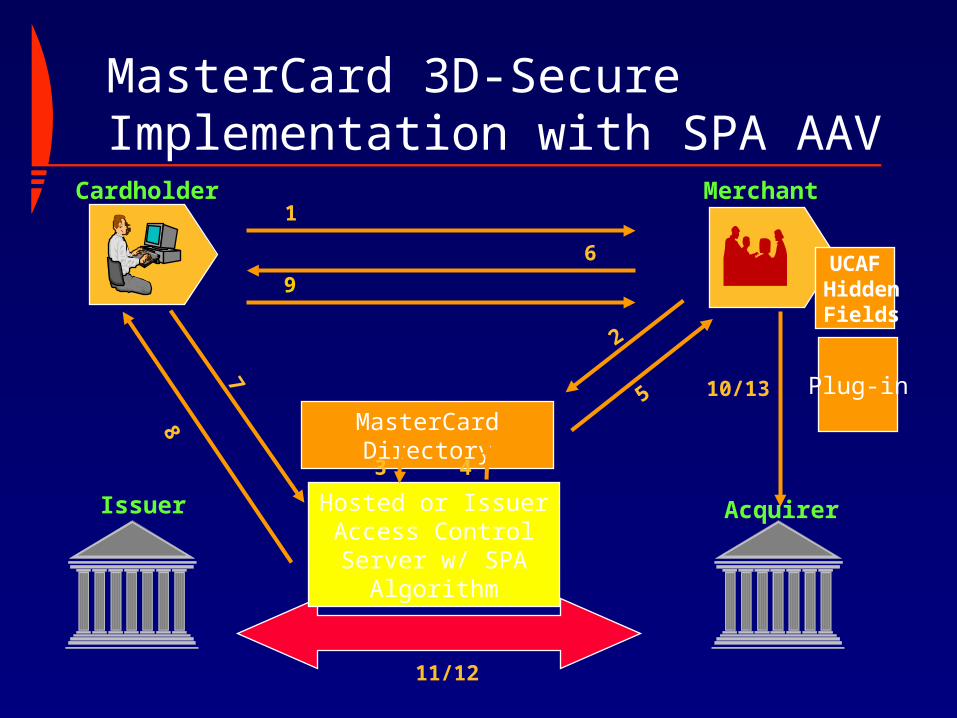

The MasterCard implementation of 3-D Secure includes support for the SPA algorithm and UCAF with no changes to the core 3-D Secure protocol. This implementation becomes the client-less (no cardholder download) authentication solution.

•MasterCard has licensed our SPA algorithm to vendors for use within their 3-D Secure version 1.02 implementations for MasterCard issuers.

MasterCard 3D-Secure Implementation with SPA AAV

Acquirer

MerchantCardholder

Issuer

MasterCard Directory

11/12

10/13

6

1

9

2

5

7

8

Hosted or Issuer Access Control Server w/ SPA

Algorithm

UCAF Hidden Fields

Plug-in

3 4

MIGS is a turn key, internet payment gateway, that significantly reduces the complexity and costs of acquiring, enabling, supporting and processing for EC merchants.

MIGS leverages the Bank’s existing transaction processing connectivity to MasterCard’s Banknet® Global Network.

What is MIGS?

Why MIGS for the Member Bank ?

• Banks lack business case yet face losing Merchants

• MIGS takes investment risk away from Member Bank

• Outsourcing with benefits of in-house and more

• MIGS is quicker to market (4 months instead of 12)

• Much lower cost and off balance sheet!

Easy Integration, Known costs, Low Risk

• MIGS requires minimal Systems development to integrate

• MIGS takes investment risk away from Member Bank

• MIGS cost advantage compared to In-House Infrastructure

• MIGS strengthens relationship between Bank and Merchant

• MIGS provides payment solutions for multiple segments

• MIGS strengthens the Bank’s Acquiring Business

Member BenefitsA Low Risk Strategy

Call Centre/IVR Credit Card

Purchase Card

E-CommerceCredit CardPIN’ed Debit

Loyalty Points RedemptionE-Cash (Mondex)

MIGS

Corporate (B2B)Purchase CardFunds Transfer

LC / Escrow

EBPPCredit CardPIN’ed Debit

E-Cash (Mondex)Funds Transfer

POS Credit CardPIN’ed Debit

E-Cash (Mondex)

M-CommerceCredit CardPIN’ed Debit

Loyalty Points RedemptionE-Cash (Mondex)

Payment Solutions - Multiple Segments

Benefits for African Countries

•New Export Potential•Merchants can Market Directly To