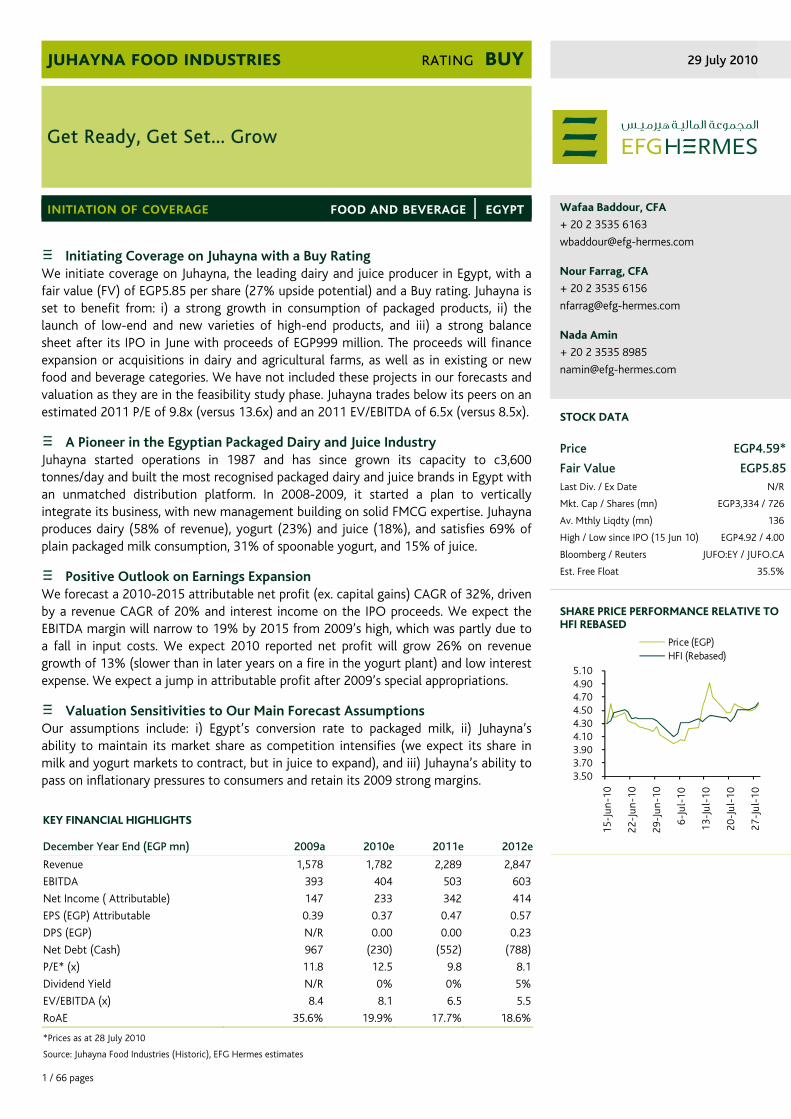

1 / 66 pages initiation of coverage Initiating Coverage on Juhayna with a Buy Rating We initiate coverage on Juhayna, the leading dairy and juice producer in Egypt, with a fair value (FV) of EGP5.85 per share (27% upside potential) and a Buy rating. Juhayna is set to benefit from: i) a strong growth in consumption of packaged products, ii) the launch of low-end and new varieties of high-end products, and iii) a strong balance sheet after its IPO in June with proceeds of EGP999 million. The proceeds will finance expansion or acquisitions in dairy and agricultural farms, as well as in existing or new food and beverage categories. We have not included these projects in our forecasts and valuation as they are in the feasibility study phase. Juhayna trades below its peers on an estimated 2011 P/E of 9.8x (versus 13.6x) and an 2011 EV/EBITDA of 6.5x (versus 8.5x). A Pioneer in the Egyptian Packaged Dairy and Juice Industry Juhayna started operations in 1987 and has since grown its capacity to c3,600 tonnes/day and built the most recognised packaged dairy and juice brands in Egypt with an unmatched distribution platform. In 2008-2009, it started a plan to vertically integrate its business, with new management building on solid FMCG expertise. Juhayna produces dairy (58% of revenue), yogurt (23%) and juice (18%), and satisfies 69% of plain packaged milk consumption, 31% of spoonable yogurt, and 15% of juice. Positive Outlook on Earnings Expansion We forecast a 2010-2015 attributable net profit (ex. capital gains) CAGR of 32%, driven by a revenue CAGR of 20% and interest income on the IPO proceeds. We expect the EBITDA margin will narrow to 19% by 2015 from 2009’s high, which was partly due to a fall in input costs. We expect 2010 reported net profit will grow 26% on revenue growth of 13% (slower than in later years on a fire in the yogurt plant) and low interest expense. We expect a jump in attributable profit after 2009’s special appropriations. Valuation Sensitivities to Our Main Forecast Assumptions Our assumptions include: i) Egypt’s conversion rate to packaged milk, ii) Juhayna’s ability to maintain its market share as competition intensifies (we expect its share in milk and yogurt markets to contract, but in juice to expand), and iii) Juhayna’s ability to pass on inflationary pressures to consumers and retain its 2009 strong margins. Wafaa Baddour, CFA + 20 2 3535 6163 [email protected]Nour Farrag, CFA + 20 2 3535 6156 [email protected]Nada Amin + 20 2 3535 8985 [email protected]STOCK DATA Price EGP4.59* Fair Value EGP5.85 Last Div. / Ex Date N/R Mkt. Cap / Shares (mn) EGP3,334 / 726 Av. Mthly Liqdty (mn) 136 High / Low since IPO (15 Jun 10) EGP4.92 / 4.00 Bloomberg / Reuters JUFO:EY / JUFO.CA Est. Free Float 35.5% SHARE PRICE PERFORMANCE RELATIVE TO HFI REBASED juhayna food industries rating buy 29 July 2010 Get Ready, Get Set... Grow food and beverage │ egypt KEY FINANCIAL HIGHLIGHTS December Year End (EGP mn) 2009a 2010e 2011e 2012e Revenue 1,578 1,782 2,289 2,847 EBITDA 393 404 503 603 Net Income ( Attributable) 147 233 342 414 EPS (EGP) Attributable 0.39 0.37 0.47 0.57 DPS (EGP) N/R 0.00 0.00 0.23 Net Debt (Cash) 967 (230) (552) (788) P/E* (x) 11.8 12.5 9.8 8.1 Dividend Yield N/R 0% 0% 5% EV/EBITDA (x) 8.4 8.1 6.5 5.5 RoAE 35.6% 19.9% 17.7% 18.6% *Prices as at 28 July 2010 Source: Juhayna Food Industries (Historic), EFG Hermes estimates 3.50 3.70 3.90 4.10 4.30 4.50 4.70 4.90 5.10 15-Jun-10 22-Jun-10 29-Jun-10 6-Jul-10 13-Jul-10 20-Jul-10 27-Jul-10 Price ( EGP) HFI ( Rebased)

Transcript

1 / 66 pages

initiation of coverage

Initiating Coverage on Juhayna with a Buy Rating We initiate coverage on Juhayna, the leading dairy and juice producer in Egypt, with a fair value (FV) of EGP5.85 per share (27% upside potential) and a Buy rating. Juhayna is set to benefit from: i) a strong growth in consumption of packaged products, ii) the launch of low-end and new varieties of high-end products, and iii) a strong balance sheet after its IPO in June with proceeds of EGP999 million. The proceeds will finance expansion or acquisitions in dairy and agricultural farms, as well as in existing or new food and beverage categories. We have not included these projects in our forecasts and valuation as they are in the feasibility study phase. Juhayna trades below its peers on an estimated 2011 P/E of 9.8x (versus 13.6x) and an 2011 EV/EBITDA of 6.5x (versus 8.5x).

A Pioneer in the Egyptian Packaged Dairy and Juice Industry Juhayna started operations in 1987 and has since grown its capacity to c3,600 tonnes/day and built the most recognised packaged dairy and juice brands in Egypt with an unmatched distribution platform. In 2008-2009, it started a plan to vertically integrate its business, with new management building on solid FMCG expertise. Juhayna produces dairy (58% of revenue), yogurt (23%) and juice (18%), and satisfies 69% of plain packaged milk consumption, 31% of spoonable yogurt, and 15% of juice.

Positive Outlook on Earnings Expansion We forecast a 2010-2015 attributable net profit (ex. capital gains) CAGR of 32%, driven by a revenue CAGR of 20% and interest income on the IPO proceeds. We expect the EBITDA margin will narrow to 19% by 2015 from 2009’s high, which was partly due to a fall in input costs. We expect 2010 reported net profit will grow 26% on revenue growth of 13% (slower than in later years on a fire in the yogurt plant) and low interest expense. We expect a jump in attributable profit after 2009’s special appropriations.

Valuation Sensitivities to Our Main Forecast Assumptions Our assumptions include: i) Egypt’s conversion rate to packaged milk, ii) Juhayna’s ability to maintain its market share as competition intensifies (we expect its share in milk and yogurt markets to contract, but in juice to expand), and iii) Juhayna’s ability to pass on inflationary pressures to consumers and retain its 2009 strong margins.

I. EXECUTIVE SUMMARY 3 INITIATING COVERAGE WITH A BUY RATING 3 JUHAYNA GOES PUBLIC 3 JUHAYNA, A LEADING DAIRY AND JUICE PRODUCER IN EGYPT 4 STRONG GROWTH IN THE EGYPTIAN PACKAGED MARKET… 5 …ATTRACTING NEW PLAYERS, INTENSIFYING COMPETITION 6 JUHAYNA DEVISES ITS NEW GROWTH-ORIENTED STRATEGY 6 EXPECT SOLID GROWTH IN NET PROFIT AND FCF 7 ASSUMPTION RISKS AND VALUATION SENSITIVITIES 9

II. VALUATION 10 A. DISCOUNTED CASH FLOW 10 B. UPSIDE AND DOWNSIDE RISKS 11 C. VALUATION SENSITIVITIES TO MAIN FORECAST ASSUMPTIONS 12 D. COMPARABLE VALUATION 14

III. PROFILE AND STRATEGY 19 BACKGROUND 19 EXPANSION STRATEGY 19 BUSINESS LINES AND SUPPORT FUNCTIONS 20

IV. FINANCIAL ANALYSIS AND FORECASTS 29 A. SUMMARY OF HISTORICAL FINANCIAL PERFORMANCE 29 B. REVENUE ANALYSIS AND FORECASTS 33 C. SEGMENTAL ANALYSIS OF REVENUE AND GROSS MARGIN 41 FINANCIAL STATEMENTS 47

V. INDUSTRY ANALYSIS 49 EGYPT’S DAIRY & JUICE MARKET 49 DAIRY AND JUICE INDUSTRY MARGINS 56 FACTORS AFFECTING CONSUMPTION OF PACKAGED DAIRY PRODUCTS 57 RAW MILK 60

VI. INDUSTRY CONSOLIDATION AND RECENT DEVELOPMENTS 64

3 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

I. EXECUTIVE SUMMARY

INITIATING COVERAGE WITH A BUY RATING

We initiate coverage on Juhayna Food Industries (Juhayna) with a fair value (FV) of EGP5.85 per share based on a five-year DCF valuation, implying an upside potential of 27%. We assign a Buy rating to Juhayna. The company is set to benefit from: i) a strong growth in consumption of packaged products, ii) the launch of low-end products and new varieties of high-end products, and iii) a strong balance sheet (2010 estimated net cash position of EGP230 million) following the IPO in June, with gross proceeds of EGP999 million scheduled to finance expansion or acquisitions in dairy and agricultural farms, as well as in existing or new food and beverage categories. The company will allocate approximately two-thirds of the IPO proceeds to the farms. These projects are in the feasibility study phase and accordingly, we have not included them in our forecasts and valuation. Juhayna trades below its peers on an estimated 2011 P/E of 9.8x (versus 13.6x) and an estimated 2011 EV/EBITDA of 6.5x (versus 8.5x).

JUHAYNA GOES PUBLIC

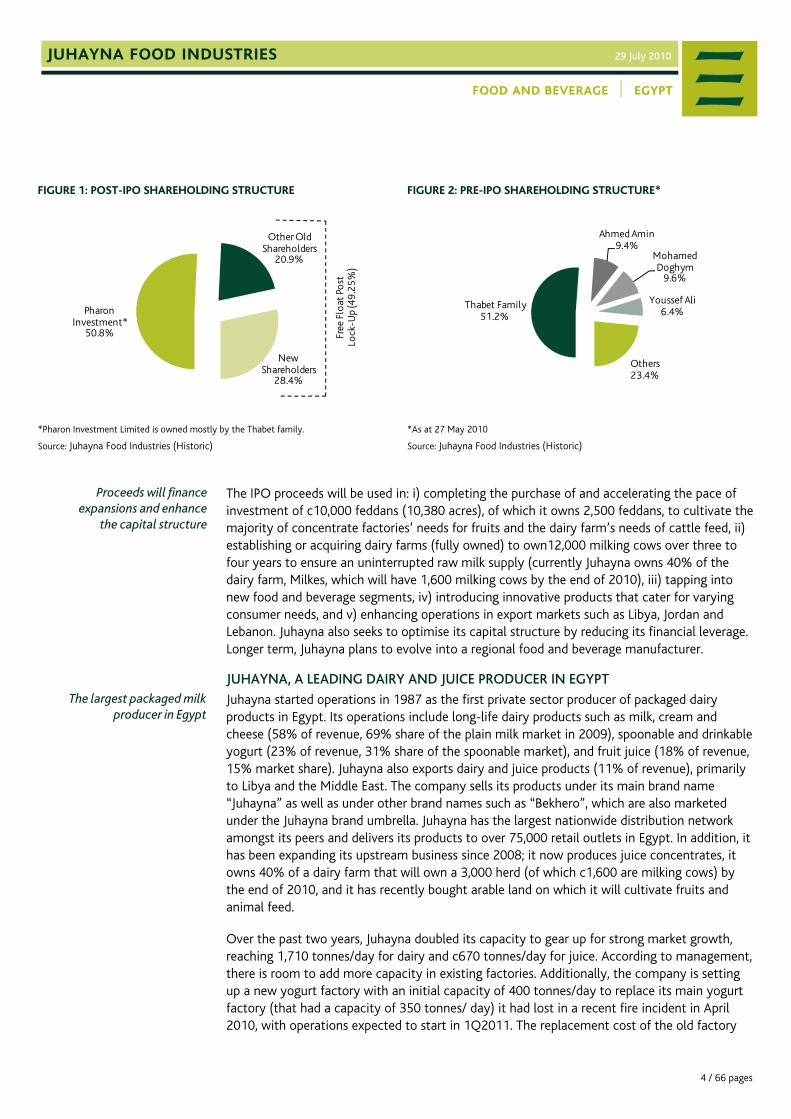

Juhayna was established in 1984 by Safwan Thabet (Chairman and CEO) and other founders as the first private sector producer of packaged dairy products in Egypt. In June 2010, Juhayna pursued an initial public offering (IPO); the founding shareholders (led by the Thabet family) sold c206 million shares. Of the shares sold, 80% were allocated in a private placement to institutions at a price of EGP4.90 per share and 20% to retail investors at a price of EGP4.66 per share. All IPO proceeds (EGP999 million) were injected into the company to fund a rights issue, with new shares dedicated to the selling shareholders, at a price of EGP4.85 per share (the weighted average price of the institution and retail tranches’ prices).

Following the IPO and the rights issue, Juhayna’s number of shares increased to 726.4 million from 520.4 million shares and its shareholding structure became: 50.75% Pharon Investment Limited (owned mostly by the Thabet family), 20.9% other old shareholders, and 28.35% new shareholders. Some 90% of shares owned by old shareholders are locked up for a period of 180 days following the start of trading (15 June) of the shares. Accordingly, we estimate Juhayna’s free float at 35.51% during the lock-up period and 49.25% afterwards. EFG Hermes Investment Banking was the global co-ordinator and sole book runner of the IPO.

IPO proceeds injected into the company

A free float of 49.25% post lock-up duration

4 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

FIGURE 1: POST-IPO SHAREHOLDING STRUCTURE

FIGURE 2: PRE-IPO SHAREHOLDING STRUCTURE*

*Pharon Investment Limited is owned mostly by the Thabet family.

Source: Juhayna Food Industries (Historic)

*As at 27 May 2010

Source: Juhayna Food Industries (Historic)

The IPO proceeds will be used in: i) completing the purchase of and accelerating the pace of investment of c10,000 feddans (10,380 acres), of which it owns 2,500 feddans, to cultivate the majority of concentrate factories’ needs for fruits and the dairy farm’s needs of cattle feed, ii) establishing or acquiring dairy farms (fully owned) to own12,000 milking cows over three to four years to ensure an uninterrupted raw milk supply (currently Juhayna owns 40% of the dairy farm, Milkes, which will have 1,600 milking cows by the end of 2010), iii) tapping into new food and beverage segments, iv) introducing innovative products that cater for varying consumer needs, and v) enhancing operations in export markets such as Libya, Jordan and Lebanon. Juhayna also seeks to optimise its capital structure by reducing its financial leverage. Longer term, Juhayna plans to evolve into a regional food and beverage manufacturer.

JUHAYNA, A LEADING DAIRY AND JUICE PRODUCER IN EGYPT

Juhayna started operations in 1987 as the first private sector producer of packaged dairy products in Egypt. Its operations include long-life dairy products such as milk, cream and cheese (58% of revenue, 69% share of the plain milk market in 2009), spoonable and drinkable yogurt (23% of revenue, 31% share of the spoonable market), and fruit juice (18% of revenue, 15% market share). Juhayna also exports dairy and juice products (11% of revenue), primarily to Libya and the Middle East. The company sells its products under its main brand name “Juhayna” as well as under other brand names such as “Bekhero”, which are also marketed under the Juhayna brand umbrella. Juhayna has the largest nationwide distribution network amongst its peers and delivers its products to over 75,000 retail outlets in Egypt. In addition, it has been expanding its upstream business since 2008; it now produces juice concentrates, it owns 40% of a dairy farm that will own a 3,000 herd (of which c1,600 are milking cows) by the end of 2010, and it has recently bought arable land on which it will cultivate fruits and animal feed.

Over the past two years, Juhayna doubled its capacity to gear up for strong market growth, reaching 1,710 tonnes/day for dairy and c670 tonnes/day for juice. According to management, there is room to add more capacity in existing factories. Additionally, the company is setting up a new yogurt factory with an initial capacity of 400 tonnes/day to replace its main yogurt factory (that had a capacity of 350 tonnes/ day) it had lost in a recent fire incident in April 2010, with operations expected to start in 1Q2011. The replacement cost of the old factory

Pharon Investment*

50.8%

Other Old Shareholders

20.9%

New Shareholders

28.4%

Free

Flo

at P

ost

Lock

-Up

(49

.25%

)

Thabet Family51.2%

Ahmed Amin9.4%

Mohamed Doghym

9.6%

Youssef Ali6.4%

Others23.4%

Proceeds will finance expansions and enhance

the capital structure

The largest packaged milk producer in Egypt

5 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

will be covered by insurance proceeds, according to management. Until the new factory becomes operational, the company is temporarily operating alternative yogurt capacities (old and new machines) in other dairy factories (with capacity expected to increase from 70 tonnes/day in May to 300 tonnes/day in August 2010 and 350 tonnes/day by early 2011). Due to seasonality, juice and yogurt capacity utilisation is usually higher during Ramadan and the summer months. Yogurt is the most seasonal product with its capacity utilisation reaching over 85% during Ramadan. Additionally, milk utilisation is higher in the winter because cow yields are higher than in the summer.

FIGURE 3: JUHAYNA’S MAIN OPERATIONAL INDICATORS BY SEGMENT (2009)

Segment Market Share

Capacity (Tonnes/Year) 1

Production (Tonnes/Year) Utilisation

Revenue(EGP mn)

% of Total

Gross Profit2

(EGP mn)

% of Total

Gross Profit Margin

EBITDA Margin

Dairy 496 158 32% 907 58% 328 55% 36% 23%

o/w Milk3 69% 479 150 31% 798 51% 283 47% 35%

o/w Cream4 N/A N/A 5 N/A 84 5% 43 7% 51%

o/w Cheese 7% 17 3 17% 25 2% 2 0% 8%

Yogurt3 31% 102 42 42% 364 23% 157 26% 43% 26%

Juice 15% 194 49 25% 287 18% 115 19% 40% 27%

1Annual capacity is calculated based on 290 days to adjust for use of machines in producing different types of products (i.e. flavoured products). 2Excluding depreciation from costs and before adding the export rebate. 3Market share is for plain milk and plain spoonable yogurt, which represents the majority of packaged consumption in Egypt. Juhayna’s yogurt factory was subject to a fire in April 2010 and is expected to be replaced by new capacity of 400 tonnes/day versus 350 tonnes/day of the old factory. 4Cream is a by-product of milk and has no specific capacity of its own.

The packaged dairy industry effectively began in the 1980s with the entrance of the private sector, with several major producers coming onto the scene. However, the industry has not yet reached maturity as loose products are still widely consumed. We expect that the packaged dairy and juice market will grow at double-digit rates over the medium term, driven by: i) a strong demographic profile: a large and young population with a high growth rate, ii) room for consumption per capita to grow from its relatively low levels, and, most importantly, iii) increased penetration as a result of a growing consumer trend away from loose products and towards healthier, packaged products.

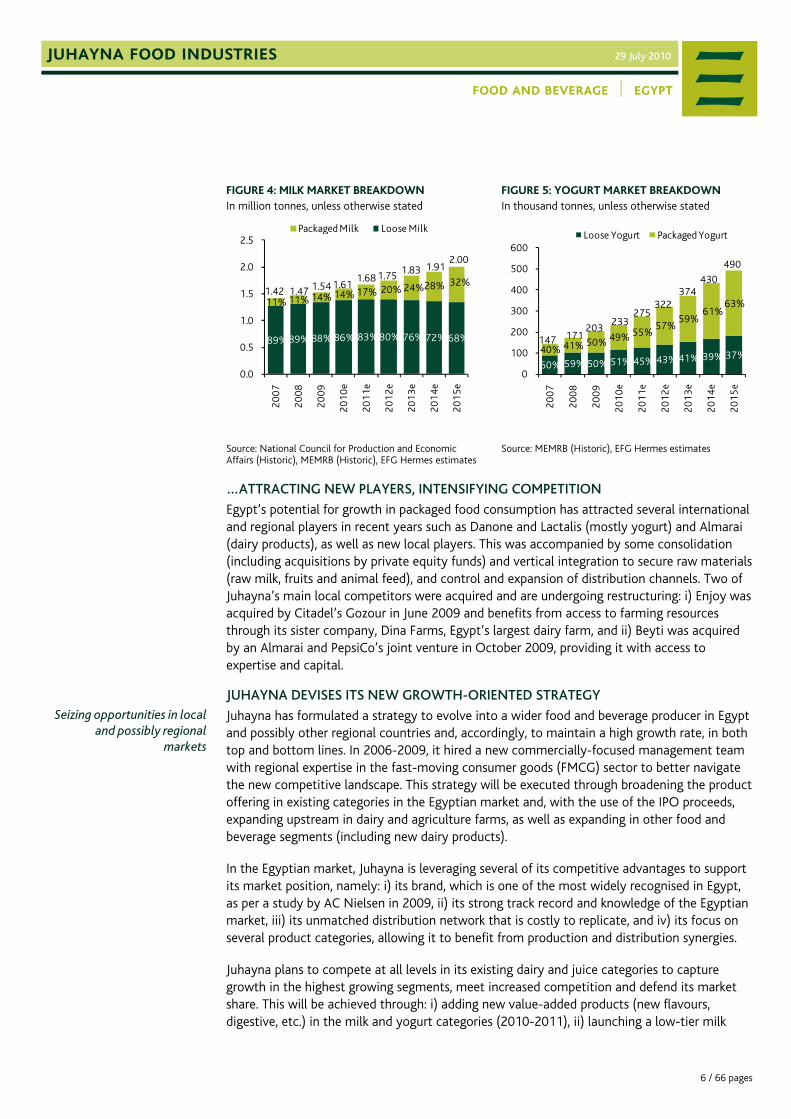

Packaged products’ contribution to milk consumption is low at 12%. It is expected to increase as dairy producers launch new brands for the lower-end range of the market and partner with the Ministry of Health (MoH) to educate the public on the health risks associated with loose milk. Industrial-packaged yogurt comprises a larger proportion of yogurt consumption at 50% as it has been growing at a faster rate than milk. This growth was encouraged by the similarity in price with loose (primitively packaged) yogurt as well as the entrance of international players (Danone and Lactel-Nestlé) who launched several advertising campaigns (to encourage yogurt consumption, which benefited the market at large) and brought new products to the market. Our forecasts assume a faster market conversion to packaged milk (from 12% to 32%) over our forecast period than yogurt (from 50% to 63%).

6 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

FIGURE 4: MILK MARKET BREAKDOWN In million tonnes, unless otherwise stated

Source: National Council for Production and Economic Affairs (Historic), MEMRB (Historic), EFG Hermes estimates

Source: MEMRB (Historic), EFG Hermes estimates

…ATTRACTING NEW PLAYERS, INTENSIFYING COMPETITION

Egypt’s potential for growth in packaged food consumption has attracted several international and regional players in recent years such as Danone and Lactalis (mostly yogurt) and Almarai (dairy products), as well as new local players. This was accompanied by some consolidation (including acquisitions by private equity funds) and vertical integration to secure raw materials (raw milk, fruits and animal feed), and control and expansion of distribution channels. Two of Juhayna’s main local competitors were acquired and are undergoing restructuring: i) Enjoy was acquired by Citadel’s Gozour in June 2009 and benefits from access to farming resources through its sister company, Dina Farms, Egypt’s largest dairy farm, and ii) Beyti was acquired by an Almarai and PepsiCo’s joint venture in October 2009, providing it with access to expertise and capital.

JUHAYNA DEVISES ITS NEW GROWTH-ORIENTED STRATEGY

Juhayna has formulated a strategy to evolve into a wider food and beverage producer in Egypt and possibly other regional countries and, accordingly, to maintain a high growth rate, in both top and bottom lines. In 2006-2009, it hired a new commercially-focused management team with regional expertise in the fast-moving consumer goods (FMCG) sector to better navigate the new competitive landscape. This strategy will be executed through broadening the product offering in existing categories in the Egyptian market and, with the use of the IPO proceeds, expanding upstream in dairy and agriculture farms, as well as expanding in other food and beverage segments (including new dairy products).

In the Egyptian market, Juhayna is leveraging several of its competitive advantages to support its market position, namely: i) its brand, which is one of the most widely recognised in Egypt, as per a study by AC Nielsen in 2009, ii) its strong track record and knowledge of the Egyptian market, iii) its unmatched distribution network that is costly to replicate, and iv) its focus on several product categories, allowing it to benefit from production and distribution synergies.

Juhayna plans to compete at all levels in its existing dairy and juice categories to capture growth in the highest growing segments, meet increased competition and defend its market share. This will be achieved through: i) adding new value-added products (new flavours, digestive, etc.) in the milk and yogurt categories (2010-2011), ii) launching a low-tier milk

Seizing opportunities in localand possibly regional

markets

7 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

brand “Halibo” to benefit from the expected acceleration of consumer conversion to packaged milk (May 2010), and iii) introducing juice drinks (that include 10% fruit concentrate) (end-2009-2010), which account for 41% of packaged juice consumption, instead of only focusing on juice nectars (that include at least 25% fruit concentrate) and pure juices (100% fruit concentrate). Additionally, the company is studying expanding into the fresh product segment, targeting the high-end consumer and selling only to large retailers who are equipped to sell fresh products. The fresh product segment is highly untapped in the Egyptian market.

EXPECT SOLID GROWTH IN NET PROFIT AND FCF

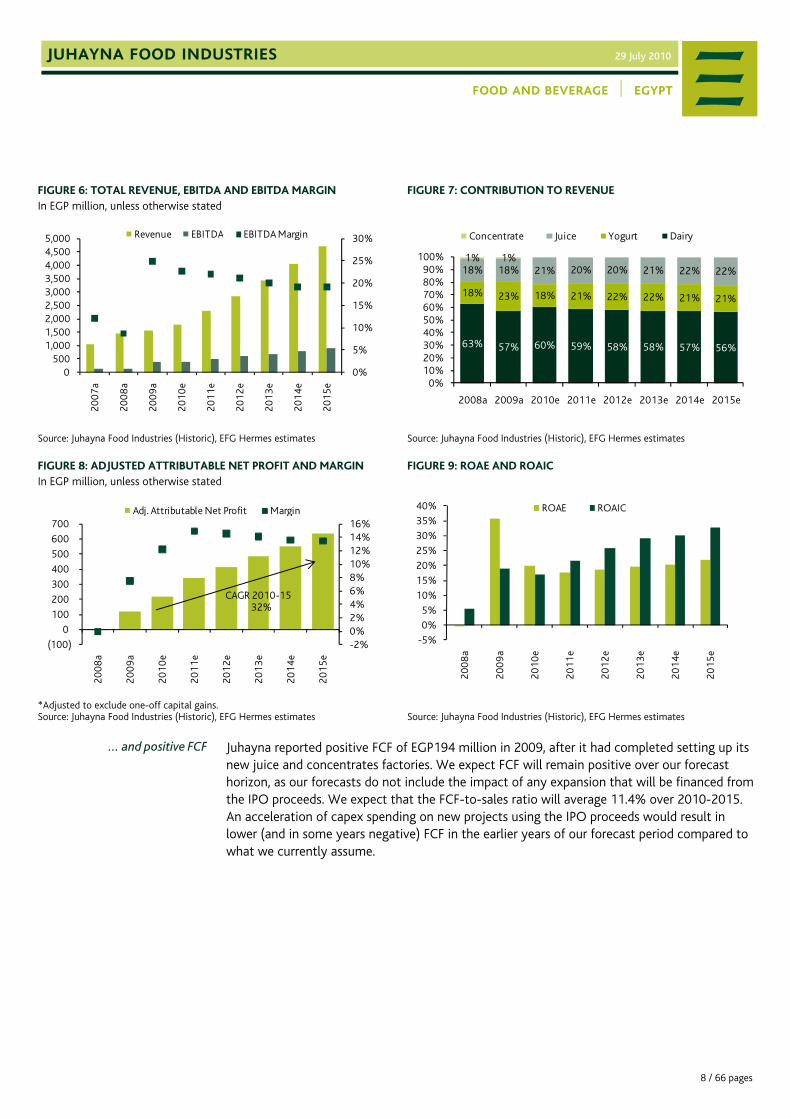

The company achieved a double-digit CAGR in revenue in 2008-2009 of 22%, driven by consumption growth in packaged milk, yogurt and juice, and price increases in 2008 that Juhayna applied to pass on rises in input costs. The EBITDA margin recovered significantly in 2009 to 25% from depressed levels in 2007 and 2008 as a result of a decline in raw material costs from their 2008 peak levels that was not passed onto consumers and savings from Juhayna’s 2008-2009 restructuring programme and resultant factory specialisation. Attributable net profit, accordingly, surged to EGP147 million (EGP119 million, excluding a one-off capital gain) from EGP37 million in 2007 and no profit in 2008.

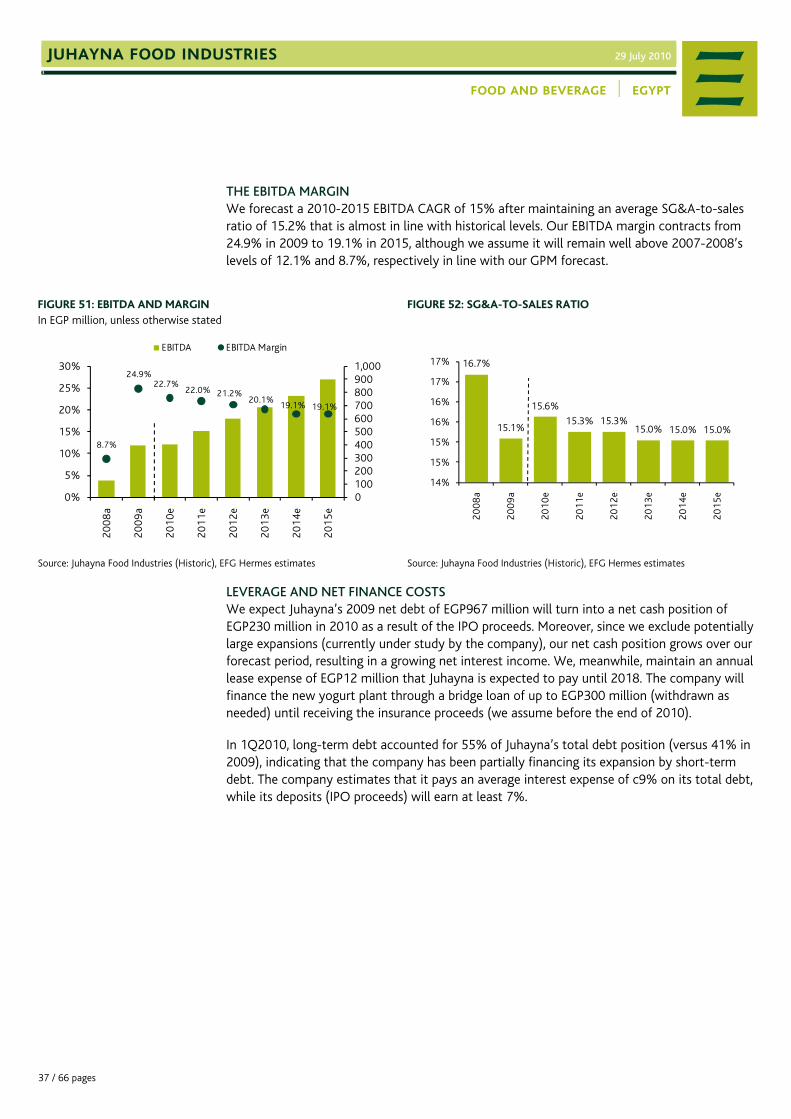

In 2010-2015, we forecast a total revenue CAGR of 20%, with a slower rate of 13% in 2010 to account for a decline in yogurt revenue. We conservatively assume that the EBITDA margin will gradually contract to 19.1% in 2015 from 24.9% in 2009, although we assume it will remain well above 2007-2008 levels of 12.1% and 8.7%, respectively. Our assumptions reflect our conviction that 2009 margins were higher than industry norms due to a sharp decline in raw material costs and a negative impact from competitive pressures on future margins. Our assumptions do not include any positive impact from the planned upstream expansion in dairy and agriculture farms, as these expansions are not yet included in our forecasts. In 2010, our attributable net profit (excluding 2009-2010’s one-off capital gains) surges 84% on lower net finance charges and appropriations (2009 included exceptional payments to employees and its board of directors - BoD). In 2011-2015, we forecast attributable net profit will grow at a 24% CAGR that is mainly driven by core operations (+21% CAGR in net operating profit), but also as interest income expands (on IPO proceeds).

Once Juhayna starts to use the IPO proceeds, this will result in a decline in interest income. Accordingly, our net profit estimates in earlier forecast years will be adjusted downward until new expansions start paying off.

Strong top and bottom linegrowth…

8 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

FIGURE 6: TOTAL REVENUE, EBITDA AND EBITDA MARGIN In EGP million, unless otherwise stated

Juhayna reported positive FCF of EGP194 million in 2009, after it had completed setting up its new juice and concentrates factories. We expect FCF will remain positive over our forecast horizon, as our forecasts do not include the impact of any expansion that will be financed from the IPO proceeds. We expect that the FCF-to-sales ratio will average 11.4% over 2010-2015. An acceleration of capex spending on new projects using the IPO proceeds would result in lower (and in some years negative) FCF in the earlier years of our forecast period compared to what we currently assume.

0%

5%

10%

15%

20%

25%

30%

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

200

7a

200

8a

200

9a

201

0e

201

1e

201

2e

201

3e

201

4e

201

5e

Revenue EBITDA EBITDA Margin

63% 57% 60% 59% 58% 58% 57% 56%

18% 23% 18% 21% 22% 22% 21% 21%

18% 18% 21% 20% 20% 21% 22% 22%1% 1%

0%10%20%30%40%50%60%70%80%90%

100%

2008a 2009a 2010e 2011e 2012e 2013e 2014e 2015e

Concentrate Juice Yogurt Dairy

-2%0%2%4%6%8%10%12%14%16%

(100)

0

100

200

300

400

500

600

700

2008

a

2009

a

2010

e

2011

e

2012

e

2013

e

2014

e

2015

e

Adj. Attributable Net Profit Margin

CAGR 2010-15 32%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

200

8a

200

9a

20

10e

20

11e

20

12e

20

13e

20

14e

20

15e

ROAE ROAIC

… and positive FCF

9 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

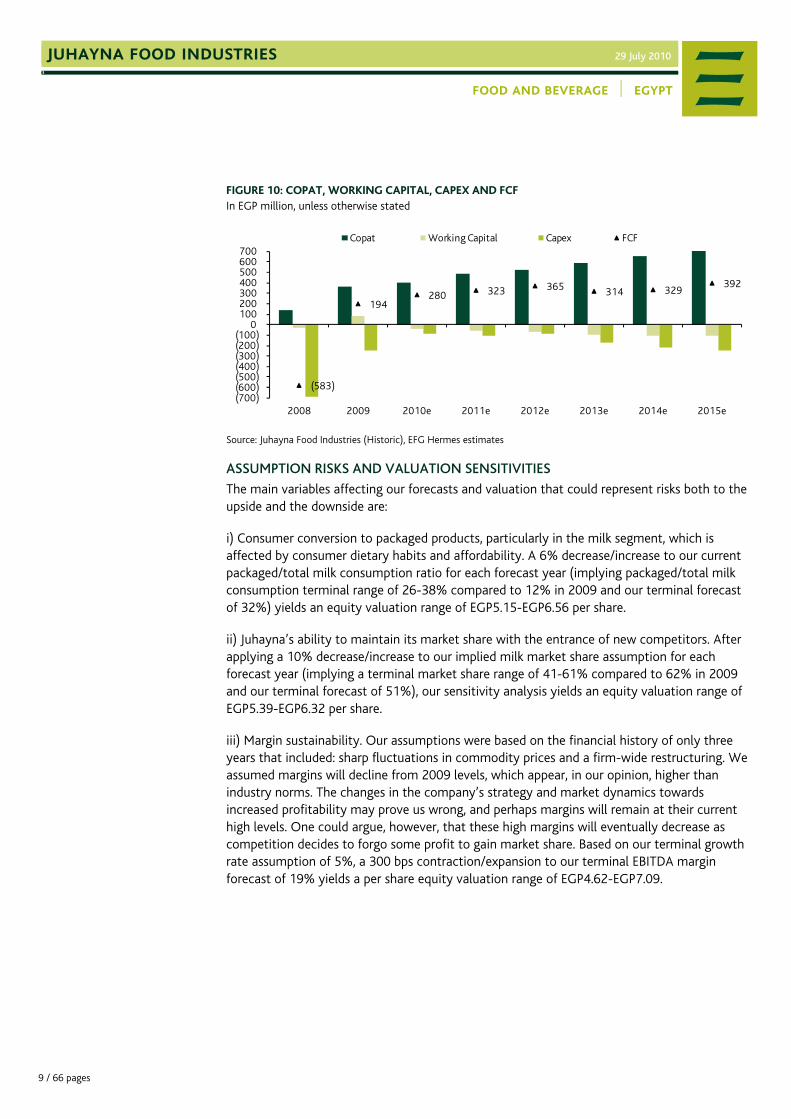

FIGURE 10: COPAT, WORKING CAPITAL, CAPEX AND FCF In EGP million, unless otherwise stated

The main variables affecting our forecasts and valuation that could represent risks both to the upside and the downside are:

i) Consumer conversion to packaged products, particularly in the milk segment, which is affected by consumer dietary habits and affordability. A 6% decrease/increase to our current packaged/total milk consumption ratio for each forecast year (implying packaged/total milk consumption terminal range of 26-38% compared to 12% in 2009 and our terminal forecast of 32%) yields an equity valuation range of EGP5.15-EGP6.56 per share.

ii) Juhayna’s ability to maintain its market share with the entrance of new competitors. After applying a 10% decrease/increase to our implied milk market share assumption for each forecast year (implying a terminal market share range of 41-61% compared to 62% in 2009 and our terminal forecast of 51%), our sensitivity analysis yields an equity valuation range of EGP5.39-EGP6.32 per share.

iii) Margin sustainability. Our assumptions were based on the financial history of only three years that included: sharp fluctuations in commodity prices and a firm-wide restructuring. We assumed margins will decline from 2009 levels, which appear, in our opinion, higher than industry norms. The changes in the company’s strategy and market dynamics towards increased profitability may prove us wrong, and perhaps margins will remain at their current high levels. One could argue, however, that these high margins will eventually decrease as competition decides to forgo some profit to gain market share. Based on our terminal growth rate assumption of 5%, a 300 bps contraction/expansion to our terminal EBITDA margin forecast of 19% yields a per share equity valuation range of EGP4.62-EGP7.09.

(583)

194 280 323 365 314 329

392

(700)(600)(500)(400)(300)(200)(100)

0 100 200 300 400 500 600 700

2008 2009 2010e 2011e 2012e 2013e 2014e 2015e

Copat Working Capital Capex FCF

10 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

II. VALUATION

Our fair value for Juhayna stands at EGP5.85 per share, using a five-year discounted cash flow (DCF) valuation. Additionally, we examine dairy and juice comparables in emerging and developed markets. The blended peer group trades on an average estimated 2010 P/E multiple of 15.1x and 2011 P/E multiple of 13.6x, and on an average estimated 2010 EV/EBITDA multiple of 9.5x and 2011 EV/EBITDA multiple of 8.5x. Juhayna trades lower than its peers on an estimated 2011 P/E of 9.8x and an estimated 2011 EV/EBITDA of 6.5x.

Our DCF fair value estimate is based on the existing business and does not account for any expansion using the IPO proceeds (i.e. vertical integration upstream and expansion in existing/new food and beverage products). We believe this may underestimate the value of the company as it does not take into account the value of any expansion and/or acquisitions Juhayna may undertake.

A. DISCOUNTED CASH FLOW We use a five-year DCF valuation to arrive at an equity value of EGP4.3 billion. Our DCF assumptions are as follows: i) a risk-free rate of 10% reflecting the T-bill yield, adjusted for tax and discretionary duration premium, ii) an equity risk premium (ERP) of 6.0% (we use 5.5-6.0% for our consumer companies), iii) a terminal debt-to-equity ratio of 1:1; and iv) a terminal growth rate (TGR) of 5.0%.

FIGURE 11: SUMMARY OF DCF VALUATION In EGP million, unless otherwise stated

2011e 2012e 2013e 2014e 2015e

COPAT 483 526 587 656 748

Working Capital (56) (70) (98) (108) (110)

Capex (104) (91) (175) (219) (246)

Net Cash Flow 323 365 314 329 392

PV of NCF 290 292 223 208 225

PV of Terminal Value 2,748

Terminal WACC 12.0%

Terminal Growth Rate 5.0%

EV 3,985

2010e Net Debt (cash) (230)

Equity Value of Consolidated Activities 4,214

Milkes BV 36

Total Equity Value 4,250

Shares Outstanding (mn) 726

Fair Value per Share (EGP) 5.85

Source: EFG Hermes estimates

Our DCF valuation yields a FVof EGP5.85/share

11 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

FIGURE 12: VALUATION SENSITIVITY TO OUR COST OF EQUITY, TGR ASSUMPTIONS In EGP, unless otherwise stated

Cost of Equity

Term

inal

Gro

wth

15.0% 15.5% 16.0% 16.5% 17.0%

4.0% 5.65 5.49 5.35 5.21 5.08

4.5% 5.92 5.75 5.58 5.43 5.28

5.0% 6.24 6.04 5.85 5.68 5.52

5.5% 6.61 6.38 6.16 5.96 5.78

6.0% 7.04 6.77 6.52 6.30 6.09

Source: EFG Hermes estimates B. UPSIDE AND DOWNSIDE RISKS Upside Risks - Use of the proceeds in investments that result in improved margins and/or returns.

- A faster-than-expected consumer shift to packaged food and beverage products, particularly milk that enlarges the market.

- Stability or expansion in Juhayna’s market shares, which comes in better than our forecast, as the company better utilises its new, commercially-oriented management team and benefits from more active R&D and marketing activities and the expansion of its product offerings to include a wider range of low-tier brands and fresh products.

- A faster development of the retail sector to become more industrialised, which will encourage dairy and juice companies to expand into fresh products on a large scale.

Downside Risks - Deterioration of economic conditions that negatively affects demand for dairy and juice products or slows consumer shift from loose to packaged food consumption.

- Slow development of the retail industry, which may hold back a wide expansion into industrial-packaged fresh dairy and juice products.

- Loss of market share to competitors as a result of limited revisions of product offerings to reflect changes in customer preferences or overcapacity if competitors decide to aggressively expand their capacities.

- Rising costs that are not matched with price increases. This includes a success of dairy farms lobbying to increase raw milk prices, increases in milk powder prices, and higher packaging costs. Increases in energy prices (in July 2010), set by the government, have a minor impact on margins since dairy and juice are non-energy intensive industries.

12 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

Risks to Margin Assumptions Although Juhayna has a long history and a reputable track record in the Egyptian consumer market, our assumptions were based on financial history of only three years that included: i) sharp fluctuations in commodity prices in 2008 and 2009 that had a considerable impact on input costs, with rises in costs mostly passed onto consumers while gains on declines in costs were retained by the company (and the consumer sector at large), ii) a firm-wide restructuring and cost rationalisation programme that included the discontinuation of low-margin sales and realignment/expansion of production lines to produce each product category in a specialised factory with ample capacity, and iii) a significant increase in debt levels, particularly in 2008, to finance expansions. This has resulted in significant fluctuations in margins and profitability, with an impressive performance in 2009 and 1Q2010.

In our forecasts we assumed margins will decline from 2009 and 1Q2010 levels, which appear, in our opinion, higher than industry norms, but will remain well above 2007 and 2008 depressed levels. The changes in the company’s strategy and market dynamics may prove us wrong and perhaps margins will remain at their high levels as Juhayna, and the consumer industry at large, take these margins and profitability as a base for a new, more profitable era. One could argue, however, that these high margins will eventually decrease, particularly with increased competition that may decide to forgo some profits to gain market share.

C. VALUATION SENSITIVITIES TO MAIN FORECAST ASSUMPTIONS The main variables affecting our forecasts and valuation include: i) the pace of shift by consumers to packaged products, particularly in the milk segment as it currently has a low contribution to milk consumption, mostly caused by consumer dietary habits and affordability, ii) Juhayna’s ability to maintain its market share with the entrance of new competitors, particularly in the packaged milk segment where it had a dominant market share of 69% in 2009, and iii) margin sustainability.

In the following tables we present the impact on our valuation from: i) the speed of conversion to packaged milk, and changes in Juhayna’s share of the milk market, and ii) changes in the company’s terminal EBITDA margin.

Implied Market Share and Packaged/Total Milk Consumption (Conversion Rate) After applying a 10% decrease/increase to our implied market share assumption for each forecast year (implying a market share range of 41-61% by our terminal year), our sensitivity analysis yields an equity valuation range of EGP5.39-EGP6.32 per share. Using the same methodology, a 6% decrease/increase to our current packaged/total milk consumption ratio for each forecast year (implying packaged/total milk consumption range of 26-38% by 2014) yields an equity valuation range of EGP5.15-EGP6.56 per share.

13 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

FIGURE 13: DCF* SENSITIVITY TO IMPLIED MILK MARKET SHARE AND CONVERSION RATIO In EGP, unless otherwise stated

Implied Market Share

-30.0% -20.0% -10.0% 0.0% 10.0% 20.0%Pa

ckag

ed /

Tot

al

-10.0% 3.89 4.15 4.41 4.67 4.94 5.20

-8.0% 4.00 4.30 4.61 4.91 5.21 5.52

-6.0% 4.11 4.46 4.80 5.15 5.49 5.83

-4.0% 4.23 4.61 5.00 5.38 5.77 6.15

-2.0% 4.34 4.77 5.19 5.62 6.04 6.47

0.0% 4.45 4.92 5.39 5.85 6.32 6.78

2.0% 4.57 5.07 5.58 6.09 6.59 7.10

4.0% 4.68 5.23 5.77 6.32 6.87 7.42

6.0% 4.79 5.38 5.97 6.56 7.15 7.73

8.0% 4.91 5.53 6.16 6.79 7.42 8.05

10.0% 5.02 5.69 6.36 7.03 7.70 8.37

*For the purpose of this exercise, DCF is based on a mid range cost of equity and terminal growth rate (as per Figure 13). Source: EFG Hermes estimates

*Implied market share is based on Juhayna’s production volumes divided by total market consumption volumes. Source: MEMRB (Historic market volumes), Juhayna Food Industries (Historic volumes), EFG Hermes estimates

Source: MEMRB (Historic), EFG Hermes estimates

Terminal EBITDA Margin and TGR Based on a terminal growth rate assumption of 5%, a 300 bps contraction/expansion to our terminal EBITDA margin forecast yields a fair value per share of EGP4.62-EGP7.09.

62%61%

62%

60%

57%

54%

51%

50%

53%

55%

58%

60%

63%

65%

2009

a

2010

e

2011

e

2012

e

2013

e

2014

e

2015

e

12%14% 14% 14%

17%

20%

24%

28%

32%

5%

10%

15%

20%

25%

30%

35%20

09a

2010

e

2010

e

2010

e

2011

e

2012

e

2013

e

2014

e

2015

e

14 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

FIGURE 16: DCF* SENSITIVITY TO EBITDA MARGIN In EGP, unless otherwise stated

FIGURE 17: EBITDA MARGIN BASE-CASE FORECAST

Terminal EBITDA Margin

13.1% 16.1% 19.1% 22.1% 25.1%

TGR

4.5% 3.27 4.43 5.58 6.74 7.89

5.0% 3.38 4.62 5.85 7.09 8.32

5.5% 3.50 4.83 6.16 7.49 8.82

*For the purpose of this exercise, DCF is based on a mid-range cost of equity of 16% Source: EFG Hermes estimates

D. COMPARABLE VALUATION Our peer group consists of 15 developed and emerging companies that have dairy and juice as main business lines. We note that: i) in terms of market choice, we include developed comparables due to the limited number of listed comparables in emerging markets, or the lack of consensus estimates for some of them, and ii) in terms of business lines, some comparables may have business lines that differ from those of Juhayna. The blended peer group trades on an average estimated 2010 P/E multiple of 15.1x and 2011 P/E multiple of 13.6x, and an average estimated 2010 EV/EBITDA multiple of 9.5x and 2011 EV/EBITDA multiple of 8.5x. Juhayna trades lower than both its emerging and developed peers on an estimated 2011 P/E of 9.8x and an estimated 2011 EV/EBITDA of 6.5x.

The emerging peer group trades on an average estimated 2010 P/E multiple of 15.9x and 2011 P/E multiple of 13.7x, and an average estimated 2010 EV/EBITDA multiple of 10.8x and 2011 EV/EBITDA multiple of 9.2x. On a P/E multiple basis, developing companies trade moderately above developed companies in 2010, but on par in 2011 and 2012. They, however, trade at a premium based on EV/EBITDA multiples.

There are only two comparable dairy and juice companies actively traded in the MENA region, Almarai Company (estimated 2010 P/E multiple of 17.2x and 2011 P/E multiple of 15.1x) and SADAFCO (estimated P/E of 8.4x in 2010 and 8.2x in 2011). Based on our estimates Almarai trades on higher multiples than the peer group average, which is partly justified by its expansion strategy, strong track record, high margins and high ROE.

12%

9%

25%23% 22% 21%

20% 19% 19%

5%

10%

15%

20%

25%

30%

2007

a

2008

a

2009

a

2010

e

2011

e

2012

e

2013

e

2014

e

2015

e

The blended peer group trades on an estimated 2010 P/E of 15.1x and 2011 P/E of

*Prices as at 28 July 2010 **EPS CAGR is calculated for years available between 2009-2012e. Source: Bloomberg, Reuters, Zawya Dow Jones, and EFG Hermes estimates

16 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

A SNAPSHOT OF COMPARABLE COMPANIES DEVELOPED MARKETS: Nestlé SA (Switzerland) is the holding company of the Nestlé Group, which has subsidiaries and joint ventures across the globe. Its main units are: i) food and beverages (75% of 2009 revenue), including dairy and confectionary products, powdered and liquid beverages, and prepared dishes and cooking aids; ii) Nestlé Nutrition (9%); iii) Nestlé Waters (8%); and iv) pharmaceutical operations (8%). Nestlé’s operations are international, with its North American operations contributing 46% of 2009 revenue, while European operations contributed 32%. Its operations in Africa, the Middle East and Asia contributed 23% to revenue last year. The company plans to double its sales in the ten largest emerging market countries by 2018. Some of its main consumer brands are Stouffer’s, Nescafe, Kit-Kat, Carnation, Perrier, Vittel and Pure Life.

Danone SA (France) is a food processor that divides its activities into: i) fresh dairy; ii) water; iii) baby nutrition; and iv) medical nutrition. Some of the company’s main brands include Danone, Activia, Danacol, Evian, Volvic and Bledina. In 2009, the dairy products division accounted for 57% of revenue, water 17%, baby nutrition 20% and medical nutrition 6%. Europe contributed the largest proportion to 2009’s revenue with c60%, while Asia, its second largest market, contributed 12.5%. The rest of the world contributed the remaining c28%. The company is expanding its market reach into high-potential emerging countries, including South Korea, China, Thailand, Mozambique, Syria, Lebanon, Colombia, Kazakhstan and Chile.

Saputo Inc. (Canada) divides its activities into two sectors: i) dairy products (97% of 2009 consolidated revenue); and ii) grocery products (3%). Its dairy operations are in Canada, the United States, Europe and Argentina, while its grocery operations are in the US and include a bakery division. Saputo is the largest dairy processor and snack-cake producer in Canada, the third largest dairy processor in Argentina and is amongst the top three cheese producers in the US.

Parmalat (Italy) is a major global producer and distributor of milk (58% of 2009 revenue), dairy products (31%, including yogurt, cream-based white sauces, desserts and cheese) and fruit-based drinks (8%). Its main markets include Canada (35% of 2009 revenue), Italy (25%), Central and South America (15%), Australia (13%) and Africa (9%). Its main brands are Parmalat and Santal, as well as Zymil, Fibresse, Omega3, and a number of local brands produced through its subsidiaries.

Dean Foods Company (US) is one of the largest processors of milk and dairy products in the US. Fresh milk comprised 71% of 2009 revenue, while ice cream accounted for 10%. It operates through its two divisions: i) Fresh Dairy Direct, which processes and distributes milk and other dairy products and sells under 50-plus local and regional brands and a number of private labels; and ii) WhiteWave-Morningstar, which offers branded soybean-based beverages and food products in Europe.

17 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

Morinaga Milk Industry Co. Ltd (Japan) has two segments: i) food, which includes the processing, manufacturing and selling of liquid milk (29% of 2009 revenue), powdered milk (10%), yogurt (12%), ice cream and frozen products (10%), cheese and butter (9%), and desserts (5%); and ii) other products (24% of revenue), which includes the purchase and sale of animal feed, plant equipment design and construction, and real estate leasing. Its operations are mainly in Japan, but through its subsidiaries and joint ventures Morinaga’s market extends to China, France, Germany and the United States.

Emmi AG (Switzerland) produces a range of dairy and cream products, including milk, butter, margarine, cream, yogurt, cheese, chilled coffee drinks, desserts and ice cream. Dairy products accounted for 29% of 2009’s total revenue, while fresh products accounted for 22% and cheese and other products accounted for 35%. The company derived 74% of its 2009 revenue from Switzerland and, through its subsidiaries; it operates in the rest of Europe, the United States and Canada.

EMERGING MARKETS: Almarai Company (Saudi Arabia) is the GCC region’s largest producer of dairy products (c30% market share) and a major manufacturer of juices, baked goods and poultry products. Its dairy segment covers all supply chain activities (farming, processing and distribution). Almarai has a JV with PepsiCo, where it holds 48%, that focuses on dairy and juice activities outside the GCC region. The JV currently owns dairy and juice companies in Egypt (100% of Beyti) and Jordan (75% of Teeba). In 2009, dairy accounted for 58% of sales, cheese and butter for 19%, juice for 11%, baked goods for 11%, and poultry and agriculture for 1%.

Nestlé Berhad (Malaysia) is a subsidiary of the Nestlé Group. It produces a range of products, including coffee, culinary aids/prepared foods, milk, liquid drinks, junior foods, breakfast cereals, chilled dairy products, ice cream, chocolate and confectionery, healthcare nutrition, performance nutrition. It exports its products mainly to South East Asia and the Middle East.

China Mengniu Dairy Company Limited (China) manufactures and distributes dairy products in China through its subsidiaries. Products include ultra-high temperature milk (UHT) milk (55% of 2009 revenue), milk beverages (24%), yogurt (8%), ice cream (11%), and milk powder and other products (2%).

Wimm-Bill-Dann Foods OJSC (WBD) (Russia) manufactures dairy and juice products and divides its operations into: i) dairy (74% of 2009 revenue); ii) beverages (17%); and iii) baby nutrition (9%). The company has 37 manufacturing facilities in Russia, the Ukraine, Kyrgyzstan, Uzbekistan and Georgia.

American Dairy, Inc (China) is mainly involved in the production and distribution of milk powder, soybean milk powder, and related dairy products. Milk powder comprised 90% of 2009’s revenue and the company holds a 6.4% market share in China’s infant formula market. Operations are mainly in China through subsidiaries that collectively own over 200 milk collection stations, two dairy farms and seven production facilities. The company and its subsidiaries has a daily milk powder production capacity of c1,234 tonnes.

18 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

Vietnam Dairy Products Joint Stock Company (Vinamilk) (Vietnam) manufactures and distributes a number of dairy products. Powdered milk and infant cereals (20% of 2009 revenue) are sold in Vietnam and exported to the Middle East, while condensed milk (25%) is sold locally and exported to Cambodia and the Philippines. Liquid milk (35% of 2009 revenue) is sold only to the local market, as is yogurt, ice-cream and cheese (17%), as well as fruit juice, soybean milk, purified water and coffee (3%). The company purchases c60% of all cow milk produced in Vietnam.

Saudi Arabian Dairy and Food Company (Sadafco) (Saudi Arabia) is a dairy and food processor with subsidiaries across the GCC region and Jordan. Dairy products (c70% of 2009 revenue) include long-life milk, dry milk, cheese and cream. It also produces ice cream (8% of 2009 revenue), and other products (22%). Its flagship brand is “Saudia”. The company has a c6% market share in the GCC region’s dairy products market.

Imlek (Serbia) is a dairy producer with products that include fresh and processed milk, butter, white cheese, yogurt, cream, cheese spread, fruit beverages and desserts. Its main operations are in Macedonia, Bosnia and Herzegovina, and Montenegro through a number of subsidiaries.

19 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

III. PROFILE AND STRATEGY

BACKGROUND

Juhayna Food Industries (Juhayna) is a leading Egyptian packaged dairy and fruit juice manufacturer and distributor. Production began in 1987, and today its operations include long-life dairy products (58% of revenue), yogurt (23%), and fruit juice (18%). The company sells under its main brand name “Juhayna” as well as under other brand names, such as “Bekhero”. These other brands are marketed under the Juhayna brand umbrella, however, to build on Juhayna’s brand equity. Juhayna has the largest nationwide distribution network amongst its peers and delivers its products to over 75,000 retail outlets in Egypt. In addition, Juhayna has been expanding its upstream business since 2008; it now produces juice concentrates, it owns a dairy farm that will have a 3,000 herd (of which c1,600 are milking cows) by the end of 2010, and it has recently bought arable land on which it will cultivate fruits and animal feed.

Selling over 150 SKUs (stock keeping units, different product types such as different flavours or sizes), Juhayna has a dominant 69% share of Egypt’s packaged plain milk market, 31% of the spoonable yogurt market, and a 15% share of the fruit juice market, during 2009 through to December. It also exports dairy and juice products (11% of revenue), primarily to Libya (73%) and the Middle East. In the medium to long term, Juhayna plans to evolve from a local dairy and juice manufacturer into a wider food and beverage manufacturer.

FIGURE 19: CONTRIBUTION TO REVENUE* (2009) In EGP million, unless otherwise stated

FIGURE 20: NUMBER OF SKUS*

FIGURE 21: MARKET SHARE BY SEGMENT (2009)

*Dairy includes milk, soft white cheese and cream. Source: Juhayna Food Industries

*As at end-March 2010. Source: Juhayna Food Industries

*Soft white cheese. Source: MEMRB

EXPANSION STRATEGY

Egypt’s favourable demographics (young and growing population), combined with the under-penetration of the dairy and juice segment by organised producers, have attracted several international and regional players in recent years. This has changed the market’s competitive landscape. Existing players have found their market share threatened, especially as they had not been very active in the past in offering new products/flavours to the market.

Dairy, 907 , 58%

Yogurt, 364 , 23%

Juice, 287 , 18%

Concen-trates,

20 , 1%

Total Revenue = EGP1,578 million

55

52

46

40 45 50 55 60

Dairy

Juice

Yogurt 69%74%

31%

86%

55%

20%15% 7%

0%

20%

40%

60%

80%

100%

Plai

n

Flav

ou

red

S poo

nab

le

Dri

nkab

le

Pure

Nec

tar

Ble

nde

d

Che

ese*

Milk JuiceYogurt

The largest packaged milk producer in Egypt…

…benefiting from first mover advantage

Plans to evolve into an integrated food and

beverage producer

20 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

Juhayna is leveraging several of its competitive advantages to support its market position, namely: i) its brand, which is one of the most widely recognised in Egypt, as per a study by AC Nielsen in 2009, ii) its strong track record and knowledge of the Egyptian market, iii) its unmatched distribution network that is costly to replicate, and iv) its focus on several product categories, allowing it to benefit from production and distribution synergies.

The company has formulated a strategy to maintain a high growth rate that consists of the following:

i) Improving its cost structure by a further vertical integration upstream (dairy and agricultural farms) and downstream (distribution), as well as a further diversification of its supplier base.

ii) The company is also considering tapping into other food categories in Egypt to leverage its distribution network (under consideration).

iii) Expanding its product portfolio in its existing dairy and juice categories. Juhayna plans to compete at all levels in its existing product categories to meet increased competition and defend its market share. This includes expanding its product range (for example by adding new flavours for milk and yogurt, or different types of packaging for juice) to cater to changing consumer preferences, as well as broadening its coverage across all income brackets (for example, by adding a new low-tier milk brand).

iv) Longer term, possibly expanding regionally by replicating its business model in other MENA countries.

BUSINESS LINES AND SUPPORT FUNCTIONS

Juhayna separates its activities into four, 99.9% owned business lines: i) dairy products, ii) yogurt products, iii) juice products, and iv) juice concentrates. These products are manufactured in six factories located in the Sixth of October City. The company has rearranged its production lines to allow each factory to become specialised in one product segment. Additionally, Juhayna has two support functions: i) a wide distribution arm under the name Tiba (99.9% owned), and ii) agriculture (99.9% owned) and dairy farming (40% owned) activities.

21 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

FIGURE 22: BUSINESS SEGMENTS*

*The Kamel family owns the remainder 60% of Milkes Dairy.

Source: Juhayna Food Industries The timetable below summarises the important milestones in Juhayna’s history.

FIGURE 23: MILESTONES

Source: Juhayna Food Industries

DAIRY PRODUCTS (58% OF REVENUE)

Dairy products include long-life milk (with a shelf life of six months), cream and soft cheese. Production takes place at two factories, Juhayna and Masreya, with a capacity of 1,650 tonnes/day for milk and 60 tonnes/day for cheese. Juhayna splits its milk products into two main types: plain milk and flavoured milk. Plain milk products include its top-tier “Juhayna” brand and mid-tier “Bekhero” brand, with a combined market share of 69% in 2009. Bekhero targets mid- to low-income consumers and accounts for almost 50% of the company’s plain milk sales volume. Flavoured milk products include the brands “Mix” and the smaller-sized pack “Jino”, both of which target children and had a combined market share of 74% in 2009.

Business-to-business (B2B) accounts for 10% of the company’s dairy product sales. B2B customers include hotels, airlines, restaurants and fast food chains (including brands such as McDonalds, Chili’s, Burger King and Starbucks). Exports account for 17% of the segment’s revenue, of which 85% is from milk. Libya and the Middle East are the largest export markets. Juhayna estimates its market share in the Libyan packaged milk market was approximately 20% in 2009.

Juhayna

Dairy

Juhayna Food Industries

Masreya Dairy & Juice Co.

(99.9%)

Yogurt

Egyptian Food Industries Co.

(99.9%)

Juice

Int'l Co. for Modern Food

Industries (99.9%)

Concentrates

El Marwa Food Industries Co.

(99.9%)

Modern Concentrate Co. (99.9%)

Support

Distribution Activities

Tiba for Trading &

Distribution (99.9%)

Farming Activities

Al Enmaa for Agricultral

Development (99.9%)

Milkes Dairy Co. (40.0%)

1984-2002

Established 1984- Start of operations 1987

Strategic alliance with TetraPak 1985

Start of Exports 1988

Start of B2B activitiy 1994

2007

Acquisition of El Masreya 2005

Setting up Tiba for Trading & Distribution Co. 2007

2008

Setting up Modern Concentrate

Setting up Milkes Dairy and El Dawleya

Acquisition of El Marwa Concentrate

Conracting Combibloc to supply juice packaging

2009

Setting up El Enmaa for Agri. Dev.

2010

Increasing paid up capital to EGP520 million in 1Q2010

IPO (June); increasing paid up capital to EGP726 million

22 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

Juhayna recently introduced/plans to introduce three new milk products in the near future: i) a low-tier plain milk brand, “Halibo” (May 2010), to target the large low-income bracket population, which generally consumes “loose” milk - fresh, unpasteurised milk. This segment has recently been tapped by other players offering products at prices close to loose milk prices, ii) “Bekhero” skimmed milk, targeting the mid- to low-income consumers, and iii) honey and sugar “Mix” flavoured milk, both of which are additions aimed at children’s consumption.

The company is also planning on becoming a more active player in the cheese market. In addition, it is considering a possible entry into the fresh milk market segment, targeting the high-end consumer. This will likely be sold only in hypermarkets and large supermarkets as most of the retail sector in Egypt is dominated by individually owned stores, which are not equipped to sell fresh dairy products.

Yogurt products include spoonable and drinkable yogurt, both of which have a short life span of two weeks and are accordingly sold entirely to the local market. Spoonable yogurt accounts for 71% of the segment’s revenue and had a 31% market share in 2009 through its Juhayna-branded plain, light, and fruit yogurts. Foreign brands have recently entered the spoonable yogurt market, with a variety of new value-added products (such as new flavours) and, as a result, the market has expanded. To benefit from this expansion and to better compete with foreign brands, Juhayna widened its product offering in 2009-2010 to include flavoured, sweetened and digestive yogurt. Juhayna was the first to introduce drinkable yogurt products to Egypt (known in the GCC region as Laban) in 1990. Drinkable yogurt is sold under the brand names “Rayeb” (plain) and “Zabado” (fruit).

Yogurt used to be produced at the Egyfood factory, which had a capacity of c350 tonnes/day. Juhayna lost this factory in a fire in April 2010 and, accordingly, it is currently replacing it by building a new factory that it anticipates will be operational in 1Q2011. The new factory will have an initial capacity of 400 tonnes/day and the company estimates its capex at EGP275 million. According to the company, the old factory was fully insured with a value equivalent to EGP299 million in case of total loss. The company estimates the replacement cost of the factory at EGP240 million. Juhayna will finance the new factory’s capex through a bridge loan of up to EGP300 million (withdrawn as needed) until it receives the insurance proceeds. Until

Milk 88%

Cream 9%

Cheese 3%

Total Revenue: EGP907.3 million

Local Market 83%

Libya 12%

Africa 1%

Middle East 3%

EU & USA 1%

Exports17%

Becoming more active at the lower end of the milk market

Successfully rebuilding its lost yogurt capacity

23 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

the new factory starts operations, the company is operating yogurt production lines (old machines, as well as new machines that will become operational between July 2010 and early 2011) at its Juhayna and Masreya factories. This has resulted in a combined yogurt capacity of around 70 tonnes/day in May that will increase to 300 tonnes/day in August (c85% of the old factory’s capacity) and will further grow to 350 tonnes/day by early 2011 (100% of the old factory's capacity). The reduction in capacity will mean that Juhayna’s market share will decline in 2010; we estimate to 25-26% from 31% in 2009.

FIGURE 26: YOGURT REVENUE BREAKDOWN (2009)

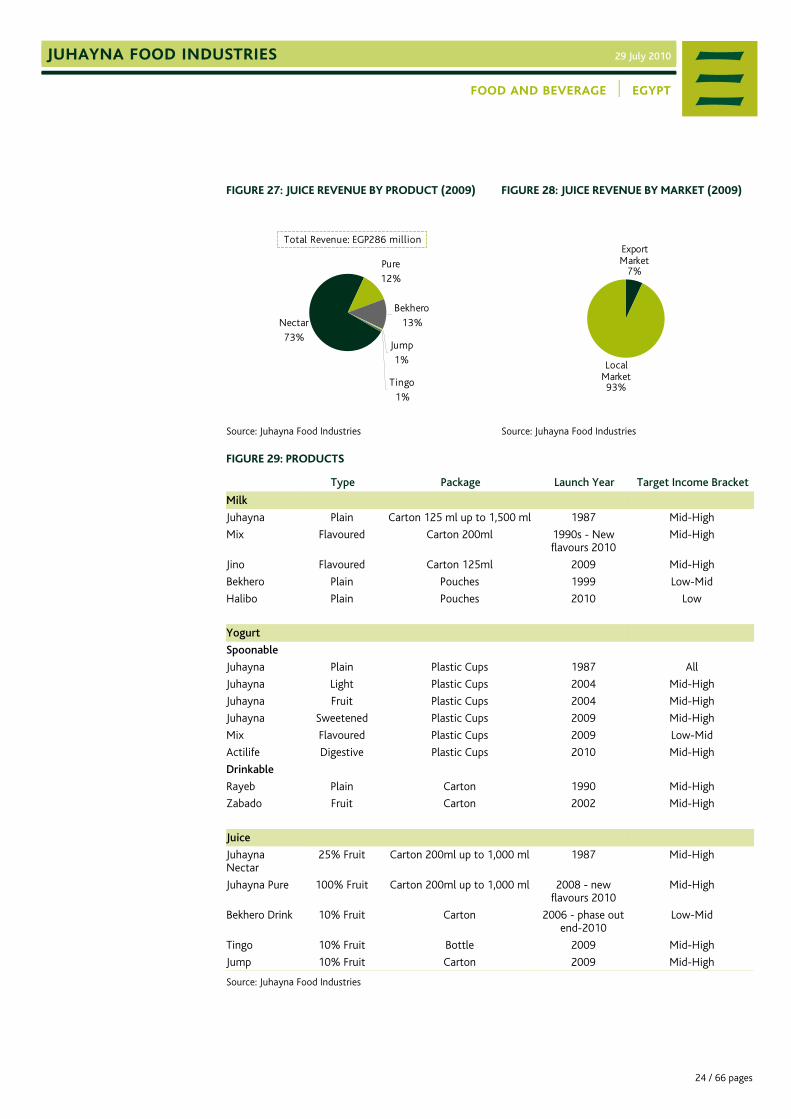

Source: Juhayna Food Industries JUICE PRODUCTS (18% OF REVENUE)

In 2008, Juhayna established its El Dawleya factory to expand and centralise its juice production in one factory. The factory has a filling capacity of 667 tonnes/day. Juice products include: i) “Juhayna Nectar” (74% of juice revenue), which has a minimum fruit content of 25%, ii) “Juhayna Pure”, a premium product with 100% fruit content and no sugar added, iii) “Bekhero” juice drink, which has a minimum fruit content of 10%, and iv) other juice drinks under two recently introduced brands, “Jump” and “Tingo”.

Although, Juhayna had a sizeable market share in the nectar (20%) and pure juice (55%) categories in 2009, its blended market share in the packaged juice market was small at 15%. This is because it previously mostly sold juice nectar, while juice drinks account for 41% of the market. Additionally, it used to sell in carton packaging, while bottles and pouches account for 57% of the market. However, the company has recently launched its first bottled juice drink brand, “Tingo” as well as “Jump” juice drink in carton. It is also considering entering into the pouch market, which has significant potential in the low-income bracket. Additionally, to expand sales of its higher margin “Juhayna Pure”, the company intends to add four new flavours to its offering in 2010 (carrot and orange, mango, guava, and pineapple).

1To control value ingredients and bacteria count in the milk. 2Ultra-High Temperature; sterilisation before packaging, then filling into pre-sterilised containers in a sterile atmosphere. Milk is processed this way using temperatures exceeding 135° C. 3Yogurt is made by fermenting milk with friendly bacteria (Lactobacillus bulgaricus and Streptococcus thermophilus). Milk sugar (lactose) is fermented by these bacteria to lactic acid, which causes the characteristic curd to form. 4An automated system that maximises the stability of the pallets during transportation. 5The pulp/juice is heat treated and then certain products are concentrated in an evaporator.

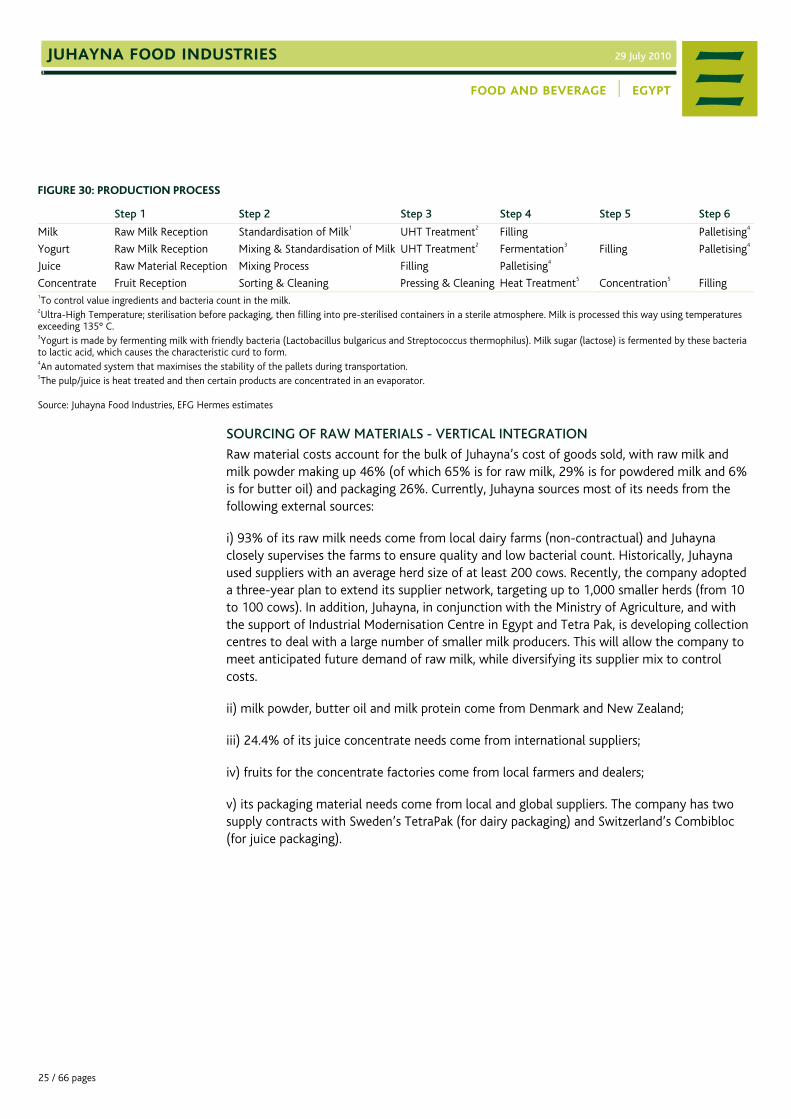

Raw material costs account for the bulk of Juhayna’s cost of goods sold, with raw milk and milk powder making up 46% (of which 65% is for raw milk, 29% is for powdered milk and 6% is for butter oil) and packaging 26%. Currently, Juhayna sources most of its needs from the following external sources:

i) 93% of its raw milk needs come from local dairy farms (non-contractual) and Juhayna closely supervises the farms to ensure quality and low bacterial count. Historically, Juhayna used suppliers with an average herd size of at least 200 cows. Recently, the company adopted a three-year plan to extend its supplier network, targeting up to 1,000 smaller herds (from 10 to 100 cows). In addition, Juhayna, in conjunction with the Ministry of Agriculture, and with the support of Industrial Modernisation Centre in Egypt and Tetra Pak, is developing collection centres to deal with a large number of smaller milk producers. This will allow the company to meet anticipated future demand of raw milk, while diversifying its supplier mix to control costs.

ii) milk powder, butter oil and milk protein come from Denmark and New Zealand;

iii) 24.4% of its juice concentrate needs come from international suppliers;

iv) fruits for the concentrate factories come from local farmers and dealers;

v) its packaging material needs come from local and global suppliers. The company has two supply contracts with Sweden’s TetraPak (for dairy packaging) and Switzerland’s Combibloc (for juice packaging).

26 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

FIGURE 31: BREAKDOWN OF COSTS (2009)*

*Raw milk and powder includes 65% raw milk, 29% powdered milk and 6% butter oil.

Source: Juhayna Food Industries Juhayna has been taking major steps since 2008 to control the supply of its raw materials and reduce costs, taking advantage of vertical integration possibilities:

i) It entered into a JV to establish Milkes (located in Cairo-Alexandria Road), of which it owns 40%, to set up and operate a modern dairy farm. This took place in 2008 after the government removed the ban on milking cow imports. The farm will have a 3,000 herd by the end of 2010 (of which c1,600 are milking cows with an average yield per cow of 35 litres/day), purchased from Europe. Milkes currently covers 7% of Juhayna’s raw milk needs. In the medium term, the company plans to be increasingly self sufficient in milk, sourcing about half of its raw milk needs internally. To help it achieve this aim, Juhayna plans to develop a further 4,000 feddans (4,152 acres) to expand its dairy farming activities. Management believes owning efficient modern farms will allow it to source a greater proportion of its raw milk needs at cheaper prices than the market averages. Egypt’s annual yield per cow is only c1,000-1,600 litres compared with modern farms’ 9,000-12,000 litres (or 30-40 litres per day).

ii) It now produces 76% of its juice concentrate needs, selling the excess production to third parties, both local (such as Isis and Beyti) and export customers.

iii) It has recently bought 2,500 feddans (2,595 acres, located in the Oasis) and plans to buy another 7,500 feddans (7,785 acres) of arable land, which it will use to cultivate fruits for its concentrate factories (with the excess sold to local and export markets) and animal feed for its dairy farms.

In addition to the aforementioned upstream expansion, Juhayna has also been focusing on its downstream processes to ensure that its products are distributed at a guaranteed quality to consumers across Egypt.

DISTRIBUTION

Juhayna has 20 distribution centres that are spread across Egypt, from Alexandria in the North to Aswan in the South, and two key distributors. The distribution segment employs c43% of Juhayna’s total workforce of 2,844 employees. It distributes to c25,000 outlets directly through its fleet of 523 vans (294 vans adapted for dry goods and 229 for chilled goods - the latter can carry dry goods as well), and to a further c50,000 outlets through sub-distributors. In particular, the company uses four sub-distributors to reach remote areas. According to MEMRB, Juhayna covers 94% of weighted retailers in the dairy segment, 75% in the yogurt segment, and 44% in the juice segment. Major chains and large supermarkets account for

Packaging 26%

Manufacturing 13%

Other15%

Raw milk & powder

46%

Moving upstream

A nationwide distribution network

27 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

about 18% of the company’s sales. With the exception of a small number of larger supermarkets, Juhayna sales terms require cash payment by retailers at the time of delivery.

Juhayna is also setting up a mega-distribution centre on an area of 55,000 sqm beside its factories in the Sixth of October City. This is expected to be completed by mid-2012 and will act as a supplier to the existing smaller distribution centres. It will free up space in Juhayna’s factories, thus enabling new product lines to be easily added in the future. The company intends to acquire an additional two land plots for the same purpose (c33,000 sqm in Upper Egypt and possibly another c30,000 sqm in Alexandria). Additionally, the company will contract a further 100 small rural sub-distributors to reach deep rural areas and small villages.

FIGURE 32: DISTRIBUTION

Source: Juhayna Food Industries

28 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

BOX 1: ORGANISATION STRUCTURE AND MANAGEMENT

In 2006-2009, Juhayna hired a new management team with strong experience in the consumer sector to better handle expansion, marketing and commercial aspects and face the new competitive environment.

FIGURE 33: ORGANISATION STRUCTURE AND MANAGEMENT

Source: Juhayna Food Industries

Chairman & CEO

Sawfan Thabet

Commercial Operations

Division

Nabil Skaria

Manufacturing Division

Niels Thomson

Finance Division

Ehab A. Hamid

Supply Chain Division

Ahmed Labib

Agricultral Sector

Hany Kamel

Admisitration Division

Hisham Zaki

Deputy CEO

Nabil Skaria

29 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

IV. FINANCIAL ANALYSIS AND FORECASTS

A. SUMMARY OF HISTORICAL FINANCIAL PERFORMANCE Revenue Juhayna’s revenue grew 38% in 2008 to EGP1.5 billion, driven by consumption growth in packaged milk, yogurt and juice, and price increases that Juhayna applied to pass on rises in input costs. Revenue growth decelerated in 2009 to 8%, mainly after Juhayna discontinued or reduced sales of some low-margin businesses (for example milk school tenders). Its average prices grew slightly, we believe, mainly on a better sales mix. The 2008-2009 revenue CAGR was 22%.

Gross Profit Juhayna almost maintained its gross profit margin (including export rebate) in 2008 at 25.4% (versus 26.7% in 2007), after it increased prices to offset a rise in input costs, particularly raw milk and packaging materials. Cost of production fell in 2009, mostly due to a decline in raw milk prices as global commodity prices fell and, according to Juhayna’s management, partly due to savings from the company’s 2008-2009 restructuring and resultant factory specialisation. Juhayna, in line with the industry, refrained from cutting its prices, which combined with its improved sales mix, has significantly improved its gross profit margin to 40%. Gross profit grew 31% in 2008 and 70% in 2009 to EGP631 million.

Juhayna reported export rebates, representing on average 10% of its total export revenues in 2007-2009. In 2008-2009, the rebate included a temporary increase that the government had passed as part of a broader incentive scheme.

EBITDA In 2007 and 2009, the SG&A expense to sales ratio was roughly stable at 14.6% and 15.1%, respectively. In 2008, the ratio peaked at 16.7% mainly as a result of a one-off cost item (excluding this EGP23 million one-off cost, SG&A expense/sales stood at 15.1%). Variable costs account for approximately 70% of SG&A and fixed for 30%.

The 2008-2009 EBITDA CAGR was strong at 75%, with EBITDA reaching EGP393 million in 2009. The EBITDA margin also expanded strongly to 24.9% in 2009 from 12.1% in 2007 and an exceptionally depressed 8.7% in 2008.

Net Profit Reported net profit achieved a 2008-2009 CAGR of 108% to EGP185 million (from EGP5 million in 2008 and EGP43 million in 2007). Core operations drove most of 2009’s net profit growth, although Juhayna also booked EGP35 million (gross) one-off gains from the sale of 50% of its stake in its real estate investment Bonian. Depreciation and interest expenses meanwhile also surged 72% to EGP97 million and 144% to EGP125 million, respectively, in 2009, following the series of investments that Juhayna undertook in 2008 and 2009 that were mostly debt financed.

It is worth pointing out that Juhayna’s effective tax rate is less than half of Egypt’s flat 20% corporate tax rate at c7%, as a result of the tax exemptions that a number of its factories currently enjoy. Some of these exemptions will expire in 2012 and the rest in 2018.

*Includes board allowance. **Includes lease expense. ***Net of related tax expense in 2009 and 1Q10.

Source: Juhayna Food Industries, EFG Hermes

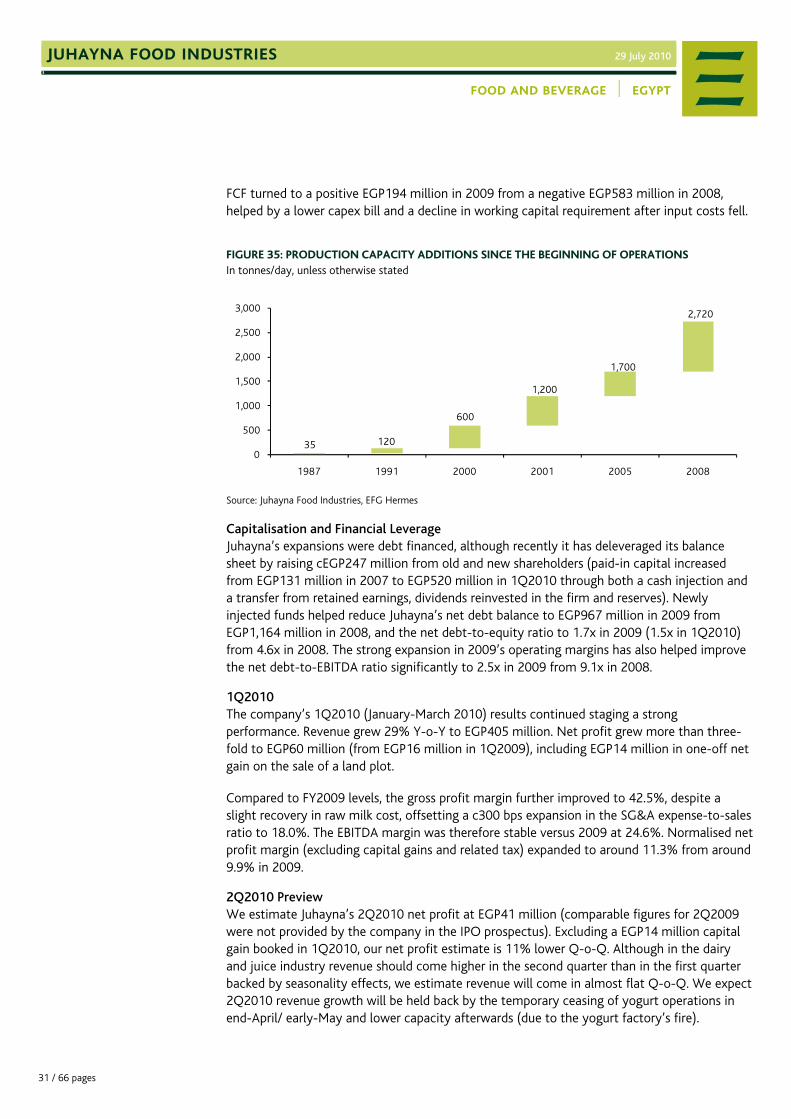

Working Capital, Capex and FCF Between its start of operations in 1987 and 2008, Juhayna’s total production capacity (excluding concentrate) grew from 35 tonnes/day to 2,730 tons/day (3,610 tons/day, including its juice concentrate capacity). This was achieved through both organic growth and a series of acquisitions.

In 2008, Juhayna spent significant capex of just below EGP700 million, most of which to build its new state-of-the-art juice factory (El Dawleya) and associated concentrate plants.

To support its operations, Juhayna has grown through a

series of capacity additions anda number of acquisitions

31 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

FCF turned to a positive EGP194 million in 2009 from a negative EGP583 million in 2008, helped by a lower capex bill and a decline in working capital requirement after input costs fell.

FIGURE 35: PRODUCTION CAPACITY ADDITIONS SINCE THE BEGINNING OF OPERATIONS In tonnes/day, unless otherwise stated

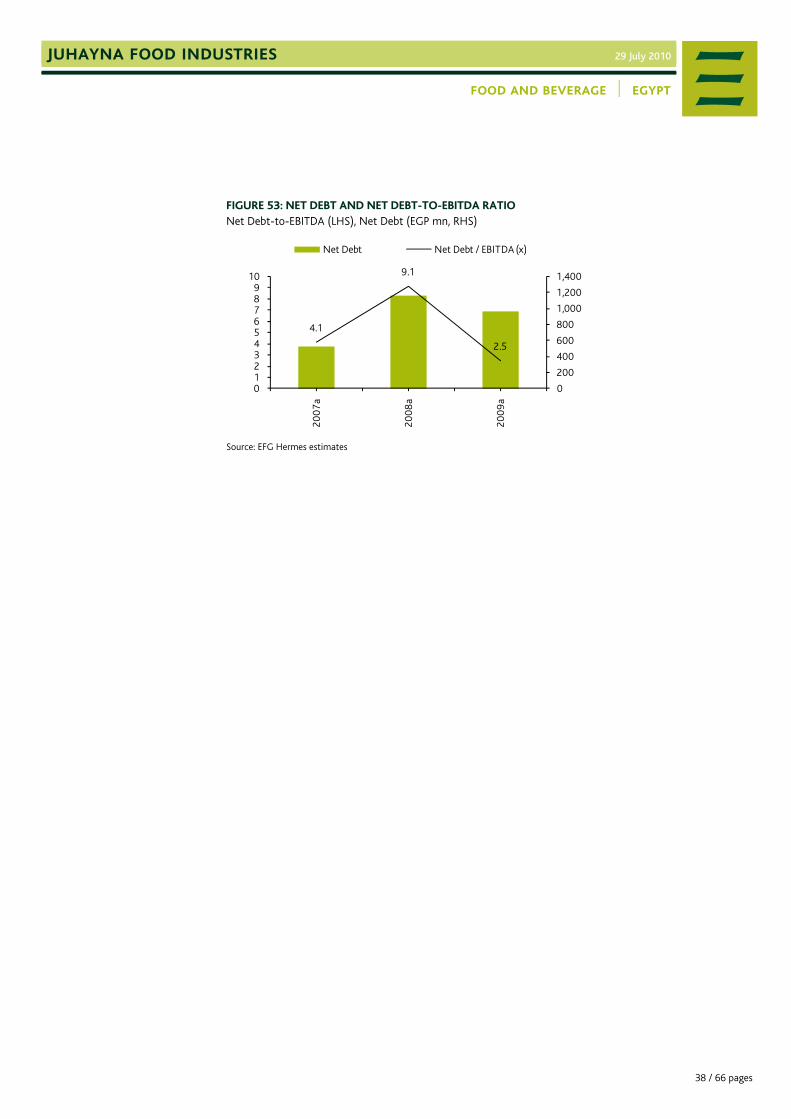

Source: Juhayna Food Industries, EFG Hermes Capitalisation and Financial Leverage Juhayna’s expansions were debt financed, although recently it has deleveraged its balance sheet by raising cEGP247 million from old and new shareholders (paid-in capital increased from EGP131 million in 2007 to EGP520 million in 1Q2010 through both a cash injection and a transfer from retained earnings, dividends reinvested in the firm and reserves). Newly injected funds helped reduce Juhayna’s net debt balance to EGP967 million in 2009 from EGP1,164 million in 2008, and the net debt-to-equity ratio to 1.7x in 2009 (1.5x in 1Q2010) from 4.6x in 2008. The strong expansion in 2009’s operating margins has also helped improve the net debt-to-EBITDA ratio significantly to 2.5x in 2009 from 9.1x in 2008.

1Q2010 The company’s 1Q2010 (January-March 2010) results continued staging a strong performance. Revenue grew 29% Y-o-Y to EGP405 million. Net profit grew more than three-fold to EGP60 million (from EGP16 million in 1Q2009), including EGP14 million in one-off net gain on the sale of a land plot.

Compared to FY2009 levels, the gross profit margin further improved to 42.5%, despite a slight recovery in raw milk cost, offsetting a c300 bps expansion in the SG&A expense-to-sales ratio to 18.0%. The EBITDA margin was therefore stable versus 2009 at 24.6%. Normalised net profit margin (excluding capital gains and related tax) expanded to around 11.3% from around 9.9% in 2009.

2Q2010 Preview We estimate Juhayna’s 2Q2010 net profit at EGP41 million (comparable figures for 2Q2009 were not provided by the company in the IPO prospectus). Excluding a EGP14 million capital gain booked in 1Q2010, our net profit estimate is 11% lower Q-o-Q. Although in the dairy and juice industry revenue should come higher in the second quarter than in the first quarter backed by seasonality effects, we estimate revenue will come in almost flat Q-o-Q. We expect 2Q2010 revenue growth will be held back by the temporary ceasing of yogurt operations in end-April/ early-May and lower capacity afterwards (due to the yogurt factory’s fire).

0

500

1,000

1,500

2,000

2,500

3,000

1987 1991 2000 2001 2005 2008

35

2,720

1,700

1,200

600

120

32 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

Management indicated that export revenue declined Y-o-Y in 1H2010, but expects 2H2010 exports to show Y-o-Y (and H-o-H) growth. We expect strong (double-digit) growth in local milk and juice sales. The EBITDA margin is forecast to come under pressure at 22.3% versus 24.3% in 1Q2010, partly due to the use of higher-cost alternative yogurt production lines in other dairy factories.

Management indicated that the yogurt factory loss will be recorded in 2Q2010 income statement, but it will be completely netted against part of the insurance proceeds.

FIGURE 36: SUMMARY OF INCOME STATEMENT In EGP million, unless otherwise stated

Seasonality Sales of dairy and juice products peak during the summer season, and whatever period that coincides with Ramadan. In 2007-2009, Juhayna generated on average 57% of its annual revenue during the second half of the year. Within Juhayna’s product range, yogurt is the most seasonal, with approximately 45 days of production for Ramadan traditionally representing more than 30% of Juhayna’s annual yogurt production volume.

FIGURE 37: QUARTERS' CONTRIBUTION TO FY REVENUE

Source: Juhayna Food Industries

18%

23%

30% 29%

20%

25%

30%

25%

20%

24%

29%27%

10%

15%

20%

25%

30%

35%

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

33 / 66 pages

juhayna food industries 29 July 2010 [

food and beverage │ egypt

B. REVENUE ANALYSIS AND FORECASTS REVENUE AND GROSS PROFIT MARGIN Revenue and Market Share In 2010-2015, we forecast a total revenue CAGR of 20%. In 2010, we project a decline in yogurt revenue, but expect strong growth from milk and juice to more than compensate, and that Juhayna’s total 2010 revenue will actually grow 13% to EGP1.8 billion. Juhayna has indicated that its milk and juice sales volumes have increased significantly shortly after the fire in the yogurt factory, after it distributed the two products’ SKUs using yogurts’ specialised/chilled fleet.

We, meanwhile, expect the revenue contribution from milk and juice exports to decline over our forecast period, as Juhayna directs its production capacity to meet the high-growth and more profitable domestic demand.

FIGURE 38: HISTORICAL AND PROJECTED REVENUE CAGR BY SEGMENT

We assume Juhayna’s volumes growth will be supported by a solid dairy and juice consumption growth outlook, and more importantly, by consumers’ anticipated conversion to packaged products, particularly milk. We expect Juhayna will grow at a lower rate than the packaged market, especially in our later forecast years, for milk and yogurt, on increased competition. We, meanwhile, assume that Juhayna’s juice market share will expand, owing to the company’s strategy of taping into new, sizable market segments, which it already started implementing in January 2010.

Our forecasts assume a faster conversion to packaged milk (from 12% to 32%) over our forecast period than yogurt (from 50% to 63%), as industrialised packaged yogurt’s contribution to yogurt consumption had a steep increase in recent years. Additionally, packaged milk growth should be boosted by milk producers and the Ministry of Health efforts to encourage packaged milk consumption through educational campaigns and the launching of new low-tier brands.

16%

41%

17%22%

20% 19%

24%20%

0%5%

10%15%20%25%30%35%40%45%

Dairy Yogurt Juice Total

2008a-2009a 2010e-2015e

Volumes to grow; market shares to eventually decline on increased

competition

34 / 66 pages

juhayna food industries 29 July 2010

food and beverage │ egypt

FIGURE 39: MILK VOLUME CAGR

FIGURE 40: YOGURT VOLUME CAGR

FIGURE 41: JUICE VOLUME CAGR

Source: Juhayna Food Industries (Historic),

EFG Hermes estimates

Source: Juhayna Food Industries (Historic),

EFG Hermes estimates

Source: Juhayna Food Industries (Historic),

EFG Hermes estimates Revenue mix We expect dairy’s (mostly milk) revenue contribution to remain the group’s largest at 56% by 2015. We expect the contribution from yogurt to contract to 21% from 23%, while the contribution from juice should expand to 22% from 18%.

FIGURE 42: REVENUE AND CAGR In EGP million, unless otherwise stated

FIGURE 43: PRODUCT CONTRIBUTION TO REVENUE

Source: Juhayna Food Industries (historic), EFG Hermes estimates Source: Juhayna Food Industries (historic), EFG Hermes estimates Pricing Juhayna’s ability to pass rising production costs onto consumers has been generally intact. We nonetheless assume a relatively moderate annual price increase of 4-5% for milk, yogurt, and juice, which means that our revenue growth forecast is mostly volume driven.

Our conservative price increase is slightly dented by the scheduled introduction of low-end products, mainly for milk and juice, and, for 2010 only, by the absence of high value-added yogurt production for few months as a result of the fire incident.

THE GROSS PROFIT MARGIN Although we assume that Juhayna’s gross profit margin (GPM) will fall from 2009’s exceptionally strong levels, we forecast that for all the three main business lines (milk, yogurt and juice) the GPM will remain well above 2007-2008’s pre-restructuring levels over our forecast period.

In general, our expected GPM compression is driven by: i) a recovery in raw material prices (feed and imported milk powder price that already started increasing in 2010) from 2009’s depressed levels, and ii) our assumption of Juhayna’s inability to entirely pass on increases in its production cost on tougher competition (we believe competition will initially focus on product differentiation, but eventually on price).