194

TPO LENDER TRAINING Kentucky Housing Corporation

| Date post: | 22-Jun-2018 |

| Category: |

Documents |

| Upload: | truongmien |

| View: | 215 times |

| Download: | 0 times |

TPO LENDER TRAINING

Kentucky Housing Corporation

SECONDARY MARKET

KHC Funding Source

Lender Relationship

Third Party Originator Lender.

Originate, process, KHC credit and compliance underwrites for ALL loans, KHC prepares closing package and handles any post closing issue.

Compensation and fees.

2.0% of total loan amount.

UW fee of $495 paid to KHC on all loans.

Administration Fee of $125 paid to KHC on all loans.

Program Guides

All KHC Program Guides

are Date Sensitive

Secondary Market Funding Source

Applicants Income Only.

Income Limits ($103,600 - $137,025 Range).

Based on County of property location.

Purchase Price & Refinance Limit $301,294.

First time and Repeat Homebuyers Statewide.

Secondary Market Income Limits

Secondary Market Applicant’s Income

ONLY:

Jefferson: $125,025

Fayette: $122,675

Northern KY:$137,025

Program

Guides & Quick

Reference

Cards

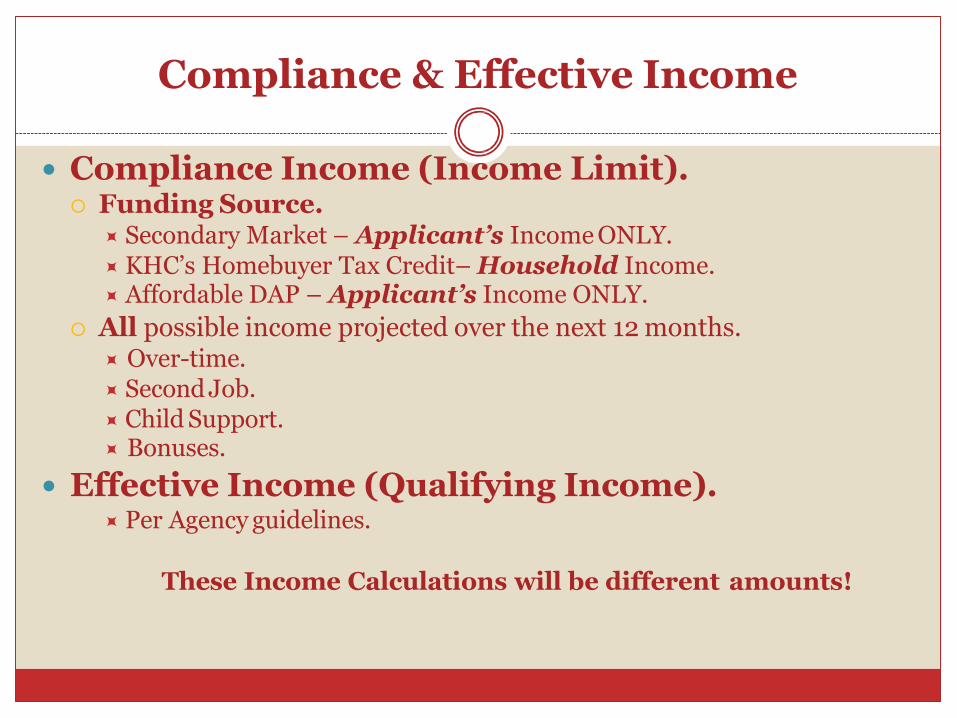

Compliance & Effective Income

Compliance Income (Income Limit). Funding Source.

Secondary Market – Applicant’s Income ONLY. KHC’s Homebuyer Tax Credit– Household Income. Affordable DAP – Applicant’s Income ONLY.

All possible income projected over the next 12 months. Over-time. Second Job. Child Support. Bonuses.

Effective Income (Qualifying Income). Per Agency guidelines.

These Income Calculations will be different amounts!

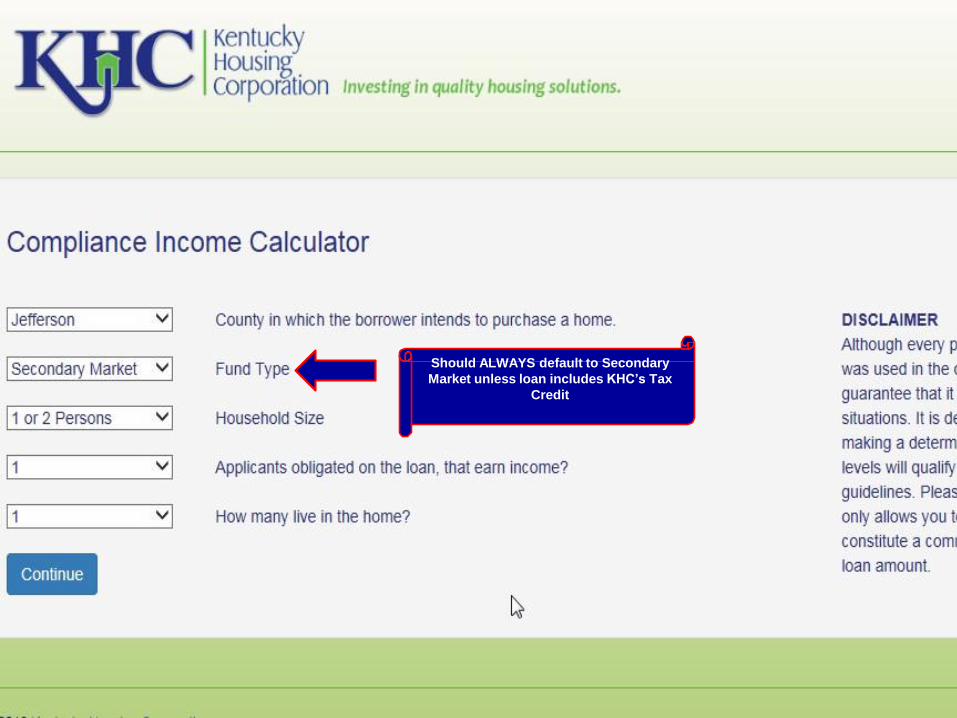

KHC’s Income Calcuator

Items needed to complete Income Calculator.

Verbal VOE with a Start Date.

Most recent 30-days worth of paystubs.

Should ALWAYS default to Secondary

Market unless loan includes KHC’s Tax

Credit

Check the income sources

that apply to your applicant or

household if KHC’s

Homebuyer Tax Credit.

The start date automatically defaults to

January 1st of the current year. You only

need to change it if their employment

start date was later in the year.

KHC’s income calculator compares

your applicant’s income to all the

other income limits. Place your final

version of this calculator in the file.

$125,025.00

Income Tips

Compliance Income. When in doubt count it!

The following should be counted in Compliance Income:Base Pay.

Overtime.

Bonuses.

Commission.

Child Support/Alimony.

Profit Sharing.

Tip Income.

Non-taxable Income (SSI, Disability).

Car Allowances.

Schedule C or E Income.

Income Tips

Compliance Income.

If Child Support is not consistent then average over 12 months.

Conventional – exception – must be consistent.

One Time Payments – Do NOT count for Compliance.

Performance Bonus.

Enlistment Bonus.

Inheritance.

Insurance Settlement.

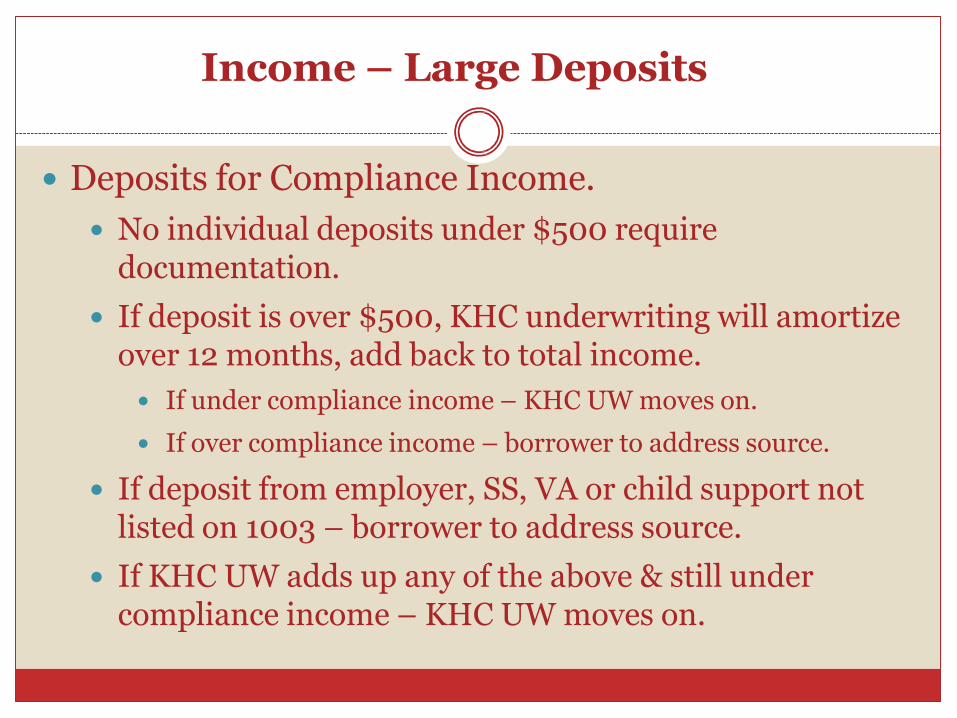

Income – Large Deposits

Deposits for Compliance Income.

No individual deposits under $500 require documentation.

If deposit is over $500, KHC underwriting will amortize over 12 months, add back to total income.

If under compliance income – KHC UW moves on.

If over compliance income – borrower to address source.

If deposit from employer, SS, VA or child support not listed on 1003 – borrower to address source.

If KHC UW adds up any of the above & still under compliance income – KHC UW moves on.

KHC First Mortgage Programs

First Mortgage Purchase Programs

Purchase. FHA. VA. RHS.

If NOT set up with GUS: All individuals needing access to GUS needs to sign up for RHS

Security Access Level 1 at this link: https://identitymanager.eems.usda.gov/registration/selfRegistrationForm.aspx?level=1

Need e-Authentication ID – KHC can add as a Lender Agent.

If already setup with GUS: Need e-Authentication ID – KHC can add as Lender Agent.

Conventional No MI Program. Conventional With MI Program.

Reduced Charter Coverage.

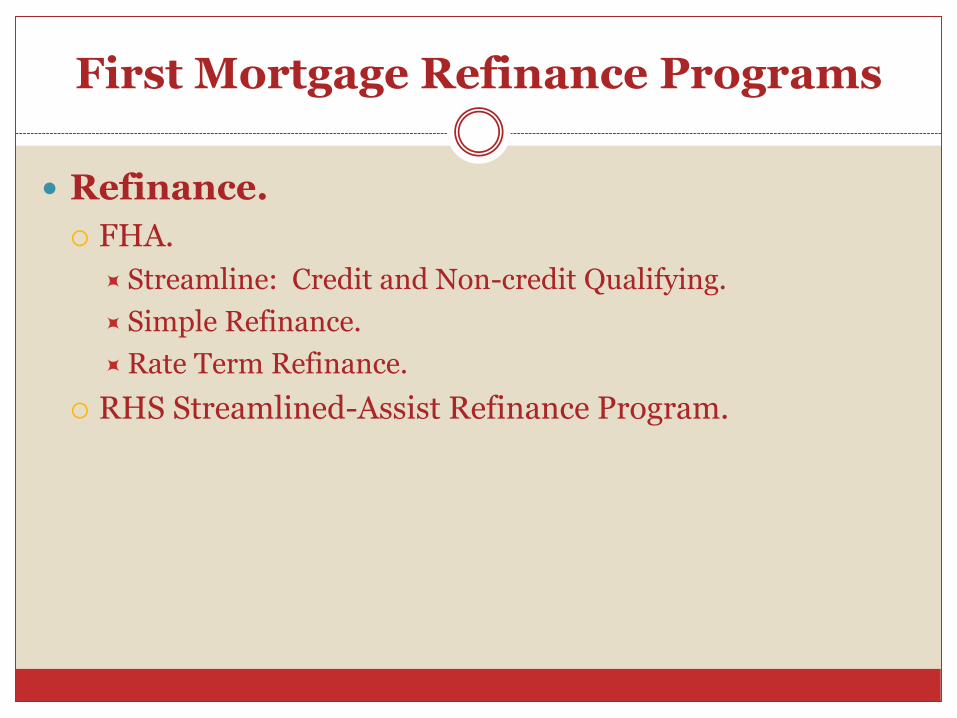

First Mortgage Refinance Programs

Refinance.

FHA.

Streamline: Credit and Non-credit Qualifying.

Simple Refinance.

Rate Term Refinance.

RHS Streamlined-Assist Refinance Program.

Property Guidelines

Single family, 1-unit, owner occupied in KY.

New & existing property.

Manufactured Housing. FHA/VA New & Existing.

RHS – New.

Conventional – 95% LTV / 105% CLTV.

Can ignore findings that state exceed CLTV if Approve/Ineligible.

Affidavit of Conversion to Real Estate.

Condominiums.

Agency Guidelines.

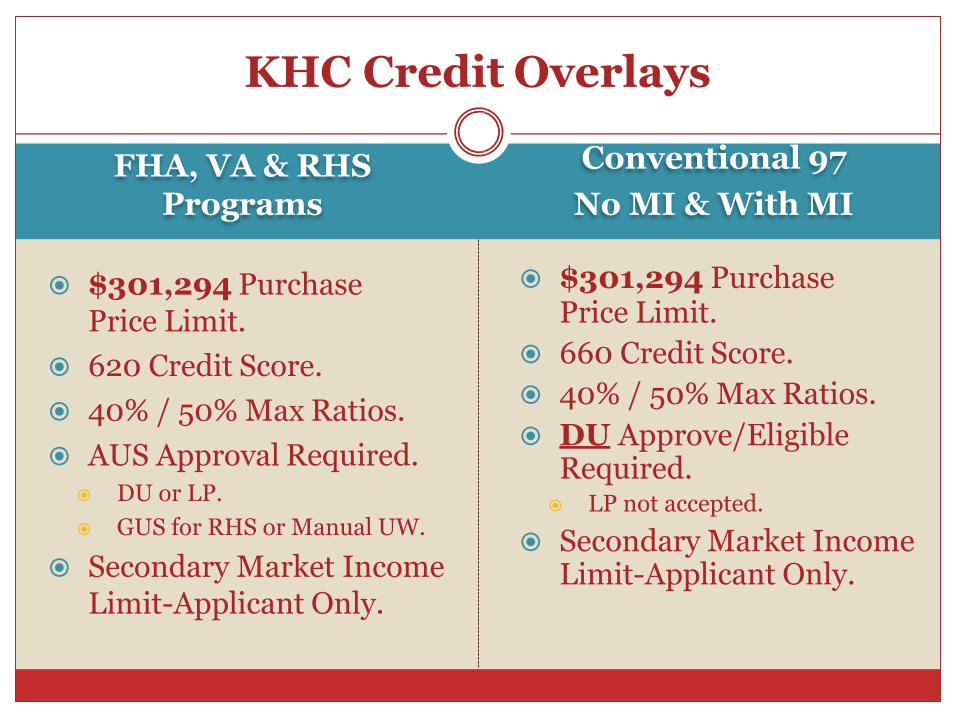

FHA, VA & RHSPrograms

$301,294 Purchase Price Limit.

620 Credit Score.

40% / 50% Max Ratios.

AUS Approval Required. DU or LP.

GUS for RHS or Manual UW.

Secondary Market Income Limit-Applicant Only.

Conventional 97

No MI & With MI

$301,294 PurchasePrice Limit.

660 Credit Score.

40% / 50% Max Ratios.

DU Approve/Eligible Required. LP not accepted.

Secondary Market Income Limit-Applicant Only.

KHC Credit Overlays

SPECIAL DESIGNATIONS

Conventional Programs

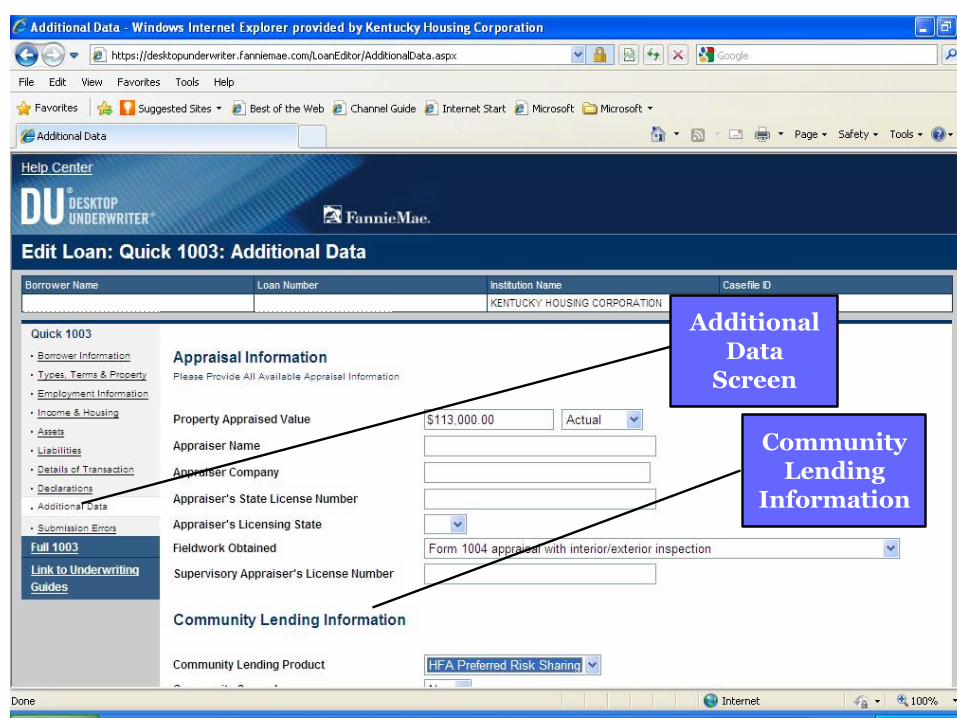

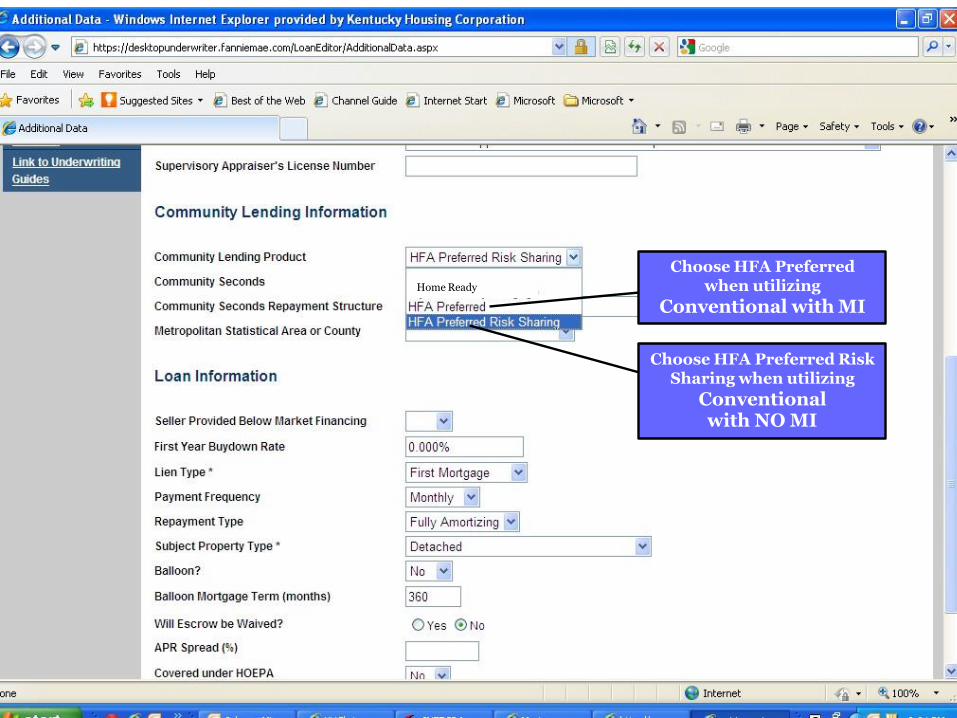

Entering Conventional with & withoutMI Program in DU

In DU select Additional Data Screen.

Under Community Lending Information

› Choose “HFA Preferred Risk Sharing” for Conventional without MI.

› Special Feature Code: 820.

› Choose “HFA Preferred” for Conventional with MI.

› Special Feature Code: 741.

› Community Seconds: HHF, Regular or Affordable DAP.

› Special Feature Code: 118.

Additional Data

Screen

Community Lending

Information

Choose HFA Preferred Risk Sharing when utilizing

Conventionalwith NO MI

Choose HFA Preferred when utilizing

Conventional with MIHome Ready

Homebuyer EducationConventional Only

Follow your DU findings.

First time homebuyers.

At least one borrower complete pre-purchase counseling.

Online session, workshop, telephone, or classroom.

MGIC or other MI Companies – Free.

DU – Request KHC as SponsorConventional Only

Fannie Mae’s Website.

Get set up with DU.

Request KHC as sponsor.

Institution ID: a0239 (lower case).

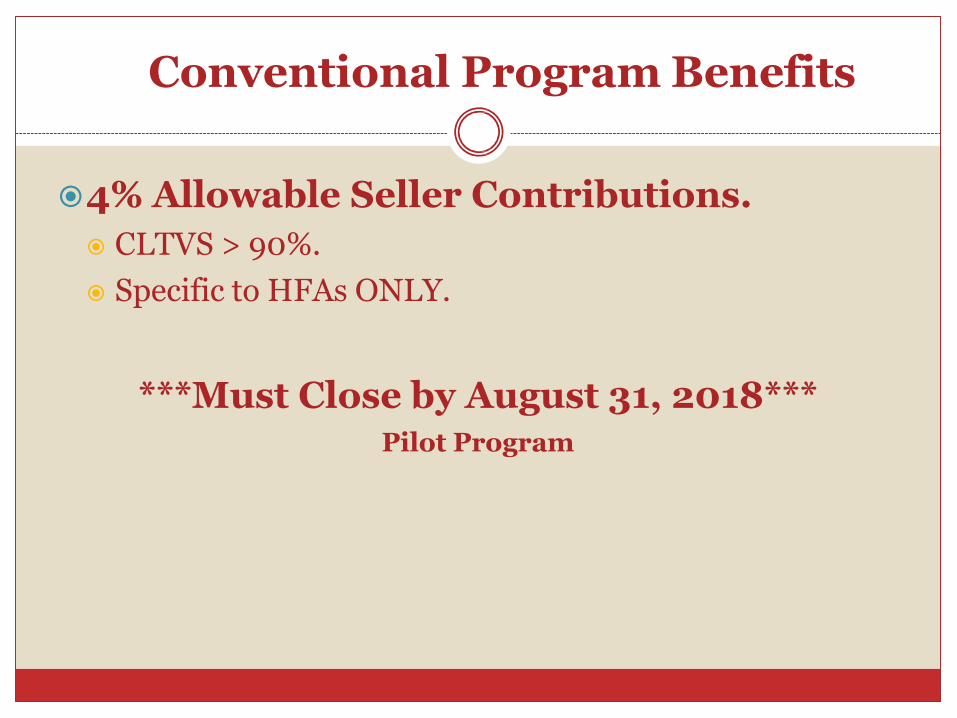

Conventional Program Benefits

4% Allowable Seller Contributions.

CLTVS > 90%.

Specific to HFAs ONLY.

***Must Close by August 31, 2018***Pilot Program

HFA Preferred & Preferred Risk Sharing

✓ Higher Income Limits.

✓ Secondary Market 175% AMI.

✓ DAP access.

✓ No MI option.

✓ Lower MI payments.

✓ 4% Allowable Seller.Contributions (CLTVs > 90%).

Home Ready

✓ Lower Income Limits.

✓ 100% AMI.

✓ No DAP.

✓ Higher MI payments.

✓ 3% Allowable Seller.Contributions (CLTVs> 90%).

KHC Conventional vs. Home Ready

Mortgage Insurance

MI Companies. Arch MI

Essent

Genworth

MGIC

Charter Coverage. 97 – 95.01% = 18%

95 – 90.01% = 16%

90 – 85.01% = 12%

85 – 81% = 6%

Single Pay Premium – Upfront. Borrower Paid

DAP

Terms FHA

Conventional

Preferred (with MI)

Conventional

Preferred Risk

(with NO MI)

Interest Rate 5.25% 5.25% 5.75%

Base First Mortgage $144,750 $145,500 $145,500

Financed MI $2,533 N/A N/A

Total First Mortgage

Amount

$147,283 $145,500 $145,500

Monthly MI $102.53 $50.15 N/A

Monthly Payment $915.53 $853.15 $849.00

Monthly Savings N/A $62.38 Savings $66.53 Savings

Based on $150,000 purchase price and 30 year fixed interest rate

Down Payment Assistance ProgramsDAP

Regular DAP

Affordable

DAP

HHF DAP(when available)

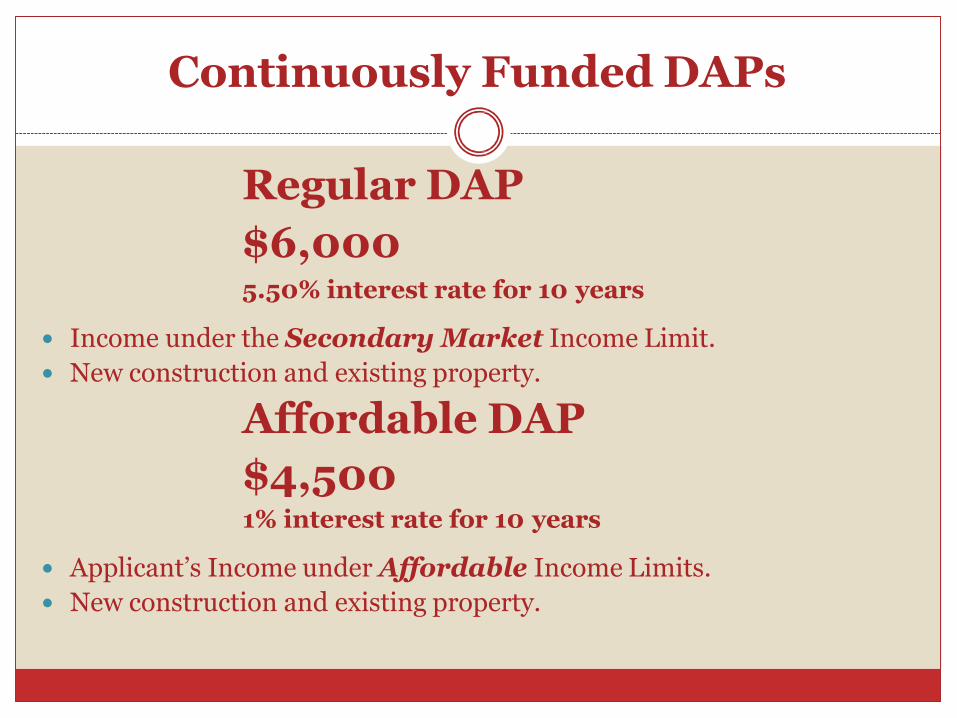

Continuously Funded DAPs

Regular DAP

$6,0005.50% interest rate for 10 years

Income under the Secondary Market Income Limit.

New construction and existing property.

Affordable DAP

$4,5001% interest rate for 10 years

Applicant’s Income under Affordable Income Limits.

New construction and existing property.

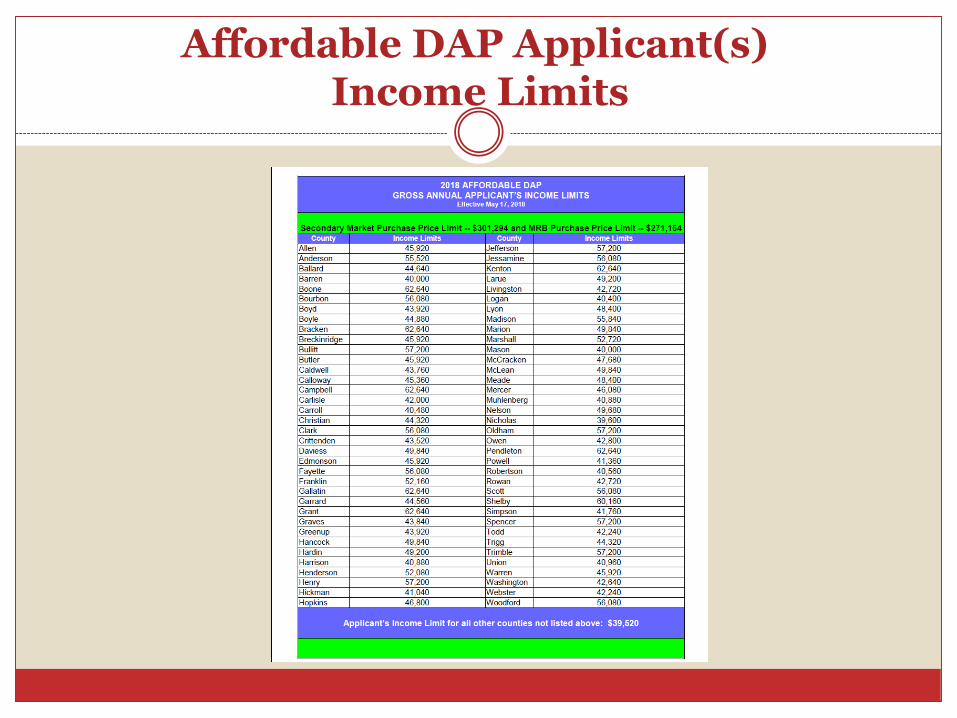

Affordable DAP Applicant(s) Income Limits

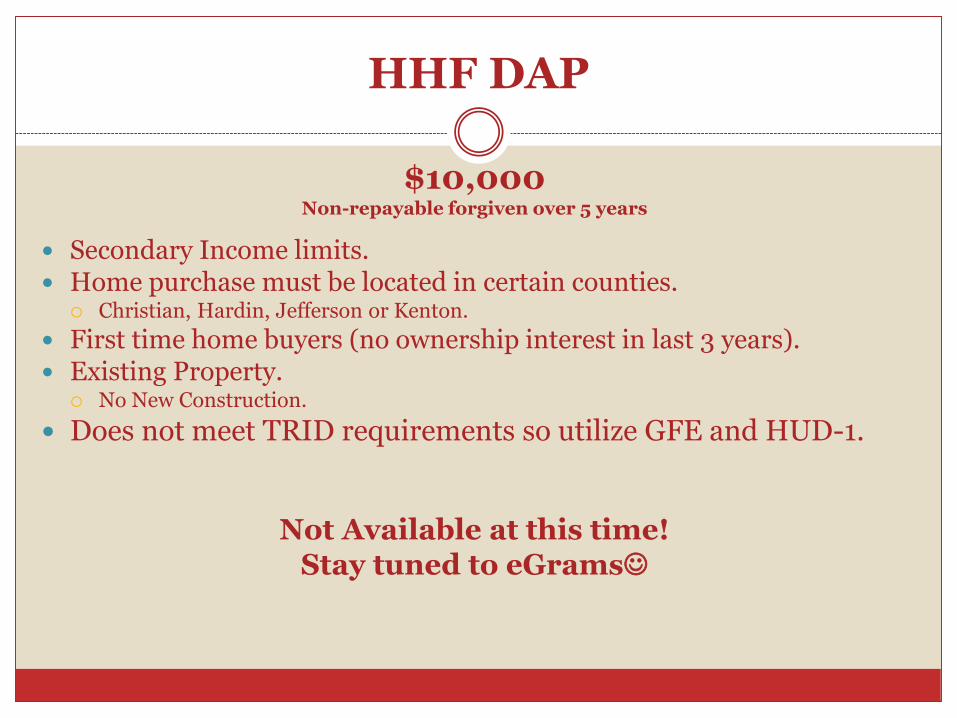

HHF DAP

$10,000Non-repayable forgiven over 5 years

Secondary Income limits. Home purchase must be located in certain counties.

Christian, Hardin, Jefferson or Kenton.

First time home buyers (no ownership interest in last 3 years). Existing Property.

No New Construction.

Does not meet TRID requirements so utilize GFE and HUD-1.

Not Available at this time!Stay tuned to eGrams☺

KHC DAPs

All take a second lien position.

DAPs can be used with:

Non-KHC DAPs.

As long as KHC’s DAP stays in 2nd Lien position.

Non-KHC DAP must meet agency guidelines.

Welcome Home Funds.

Seller Paid Closing Costs.

Gifts.

Borrower’s own funds.

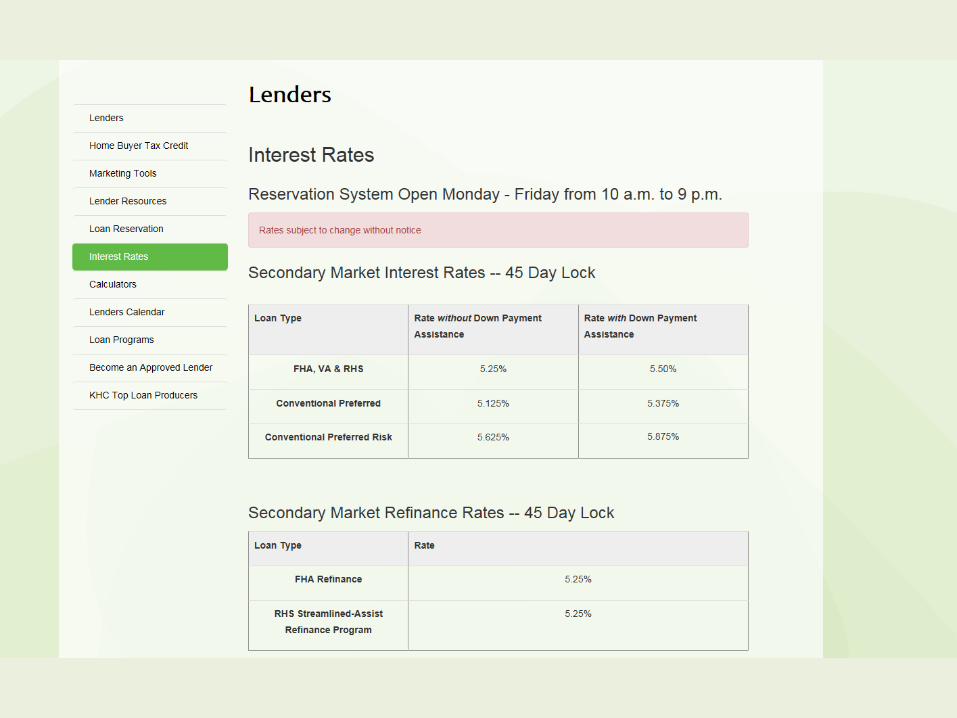

PRICED WITH & WITHOUT DAP

45 DAY LOCK

Interest Rates

Scroll down to

the bottom of

KHC’s Home

Page

Changes to Loan Reservation

Change/Extend/Cancel

7 days at .125%.

15 days at .25%.

30 days at .50%.

Email: [email protected] to change the following: Address.

Social Security Number.

First Mortgage Loan Type.

Loan Amount or Purchase Price.

Addition/Deletion of DAP.

Duplicate Loan.

Worse Case Pricing after 30 day extension.

502-564-7630 ext. 291

Ordering Appraisal for FHA, RHS & Conventional

FHA – Complete a Case Number Request.

Electronically upload through KHC’s Reservation System.

TPO Lender orders the appraisal.

Pay for this service at time of request with credit card.

MDIA.

$495 FHA/RHS & $425 Conventional.

Track progress of the appraisal online.

NEVER upload the appraisal.

KHC receives directly from ARIVS.

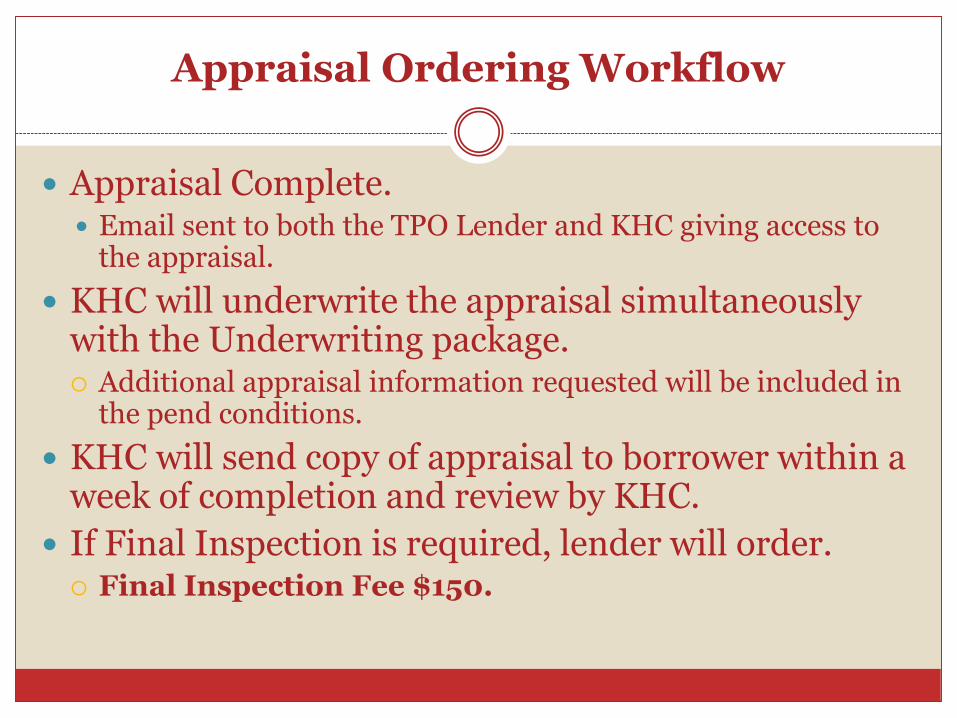

Appraisal Ordering Workflow

Appraisal Complete. Email sent to both the TPO Lender and KHC giving access to

the appraisal.

KHC will underwrite the appraisal simultaneously with the Underwriting package. Additional appraisal information requested will be included in

the pend conditions.

KHC will send copy of appraisal to borrower within a week of completion and review by KHC.

If Final Inspection is required, lender will order. Final Inspection Fee $150.

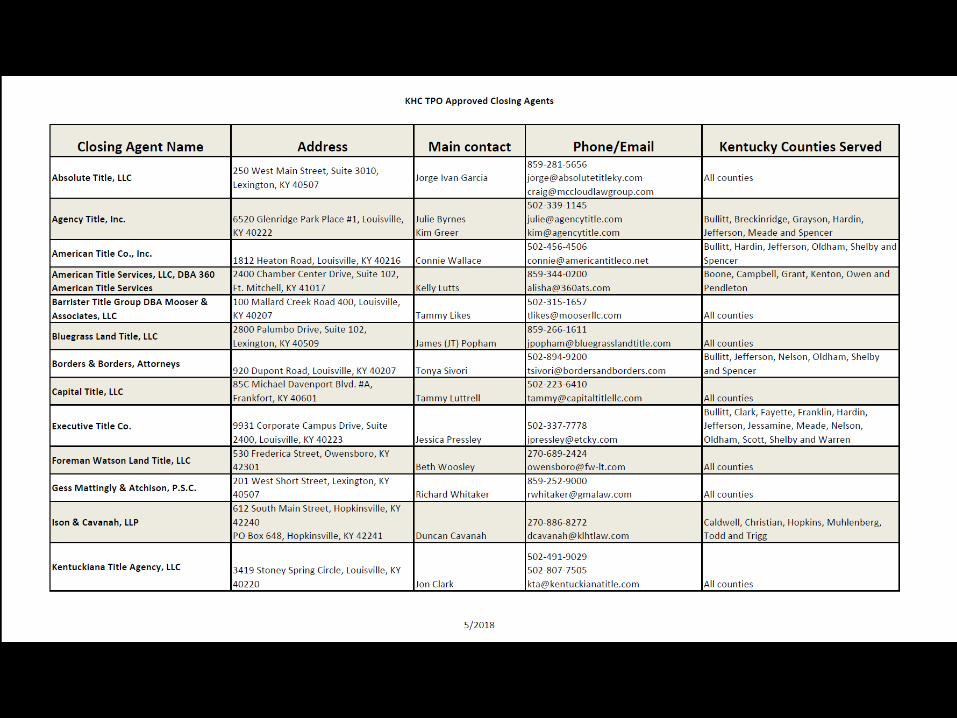

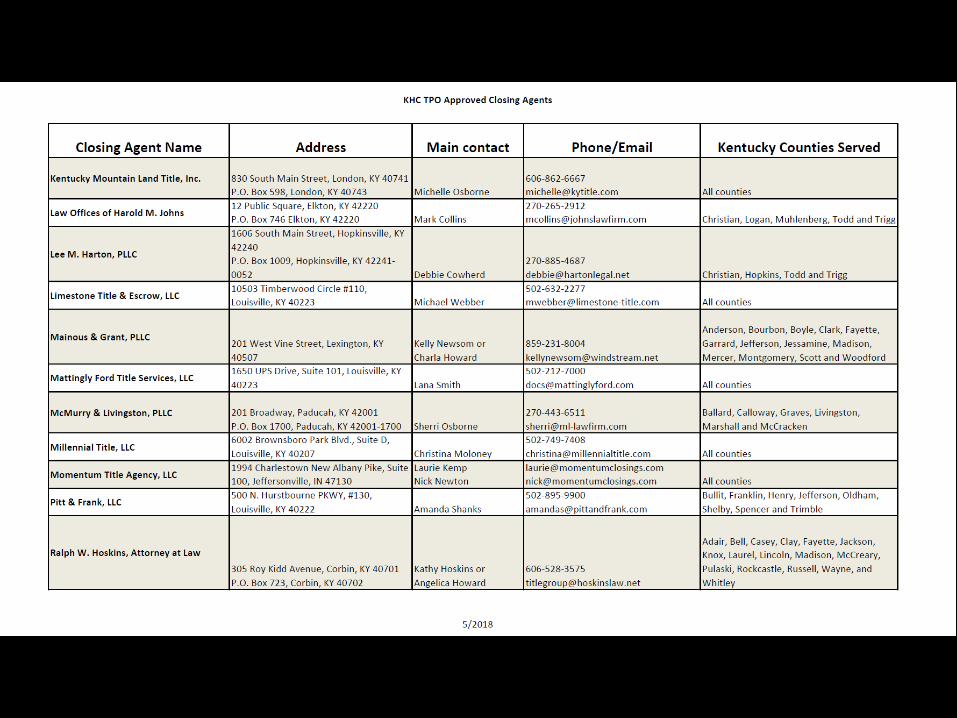

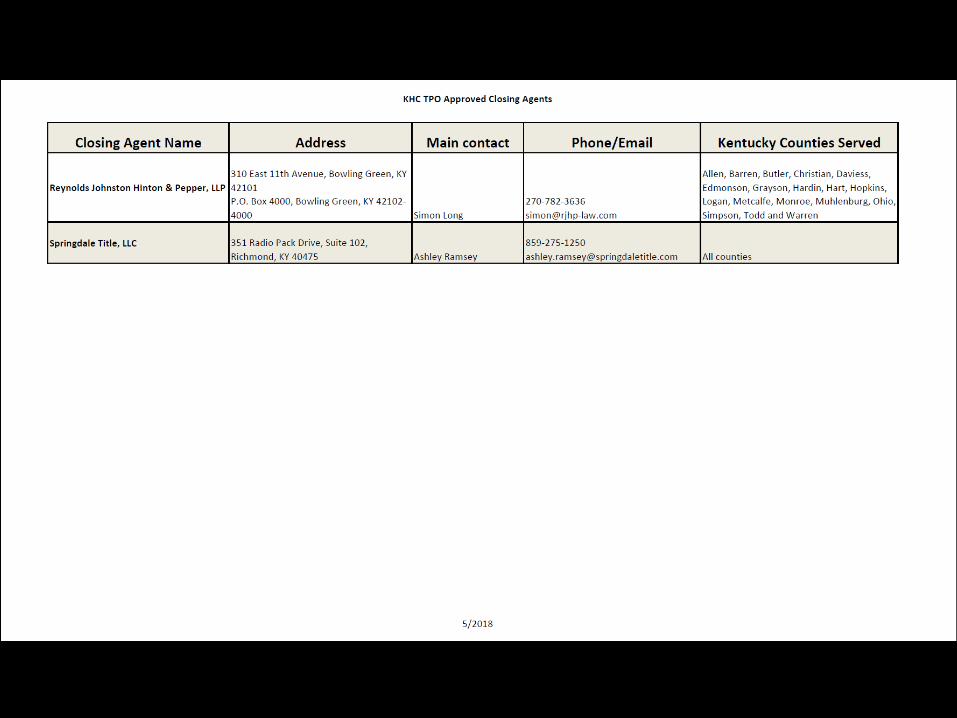

Approved TPO Closing Agents

Approved Closing Agents

Absolute Title, LLC Agency Title, INC. American Title Company, INC. American Title Services, LLC.,

DBA 360 American Title Services

Barrister Title Group DBA Mooser & Associates, LLC

Bluegrass Land Title, LLC. Borders & Borders, Attorneys Capital Title, LLC. Executive Title Company Foreman Watson Land Title,

LLC. Gess Mattingly & Atchison,

P.S.C. Kentuckiana Title Agency, LLC

Kentucky Mountain Land Title, INC.

Law Offices of Harold M. Johns Lee M. Harton, PLLC Limestone Title & Escrow, LLC. Mainous & Grant, PLLC. Mattingly Ford Title Services,

LLC. McMurry & Livingston, PLLC. Millennial Title, LLC Momentum Title Agency, LLC Pitt & Frank, LLC Ralph Hoskins, Attorney at Law Reynolds, Johnston, Hinton &

Pepper, LLP. Springdale Title, LLC.

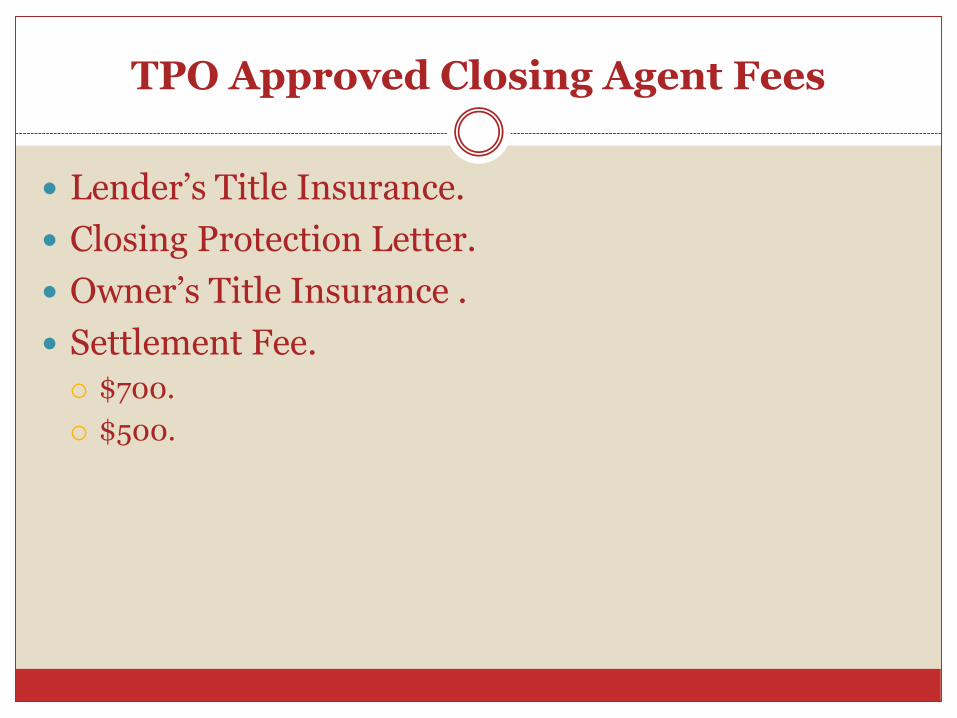

TPO Approved Closing Agent Fees

Approved Closing Agents Settlement Fee.

Title Policy provided by Closing Agent = $500.

Title Policy NOT provided by Closing Agent = $700.

Settlement Fee includes any:

Courier Fee.

Wire Fee.

Travel Fee.

Notary Fee.

Processing Fee.

TPO Approved Closing Agent Fees

Lender’s Title Insurance.

Closing Protection Letter.

Owner’s Title Insurance .

Settlement Fee.

$700.

$500.

KHC’s Loan Reservation System

RESERVE FIRST MORTGAGE

AND DAP

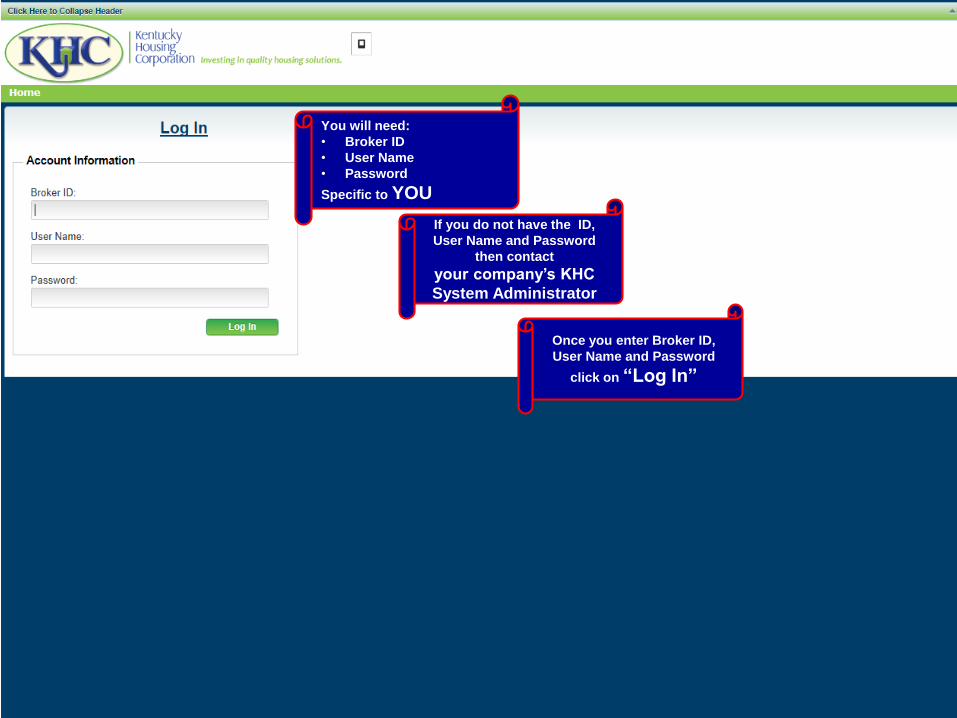

Click on “Log In”

If you do not have the ID,

User Name and Password

then contact

your company’s KHC

System Administrator

You will need:

• Broker ID

• User Name

• Password

Specific to YOU

Once you enter Broker ID,

User Name and Password

click on “Log In”

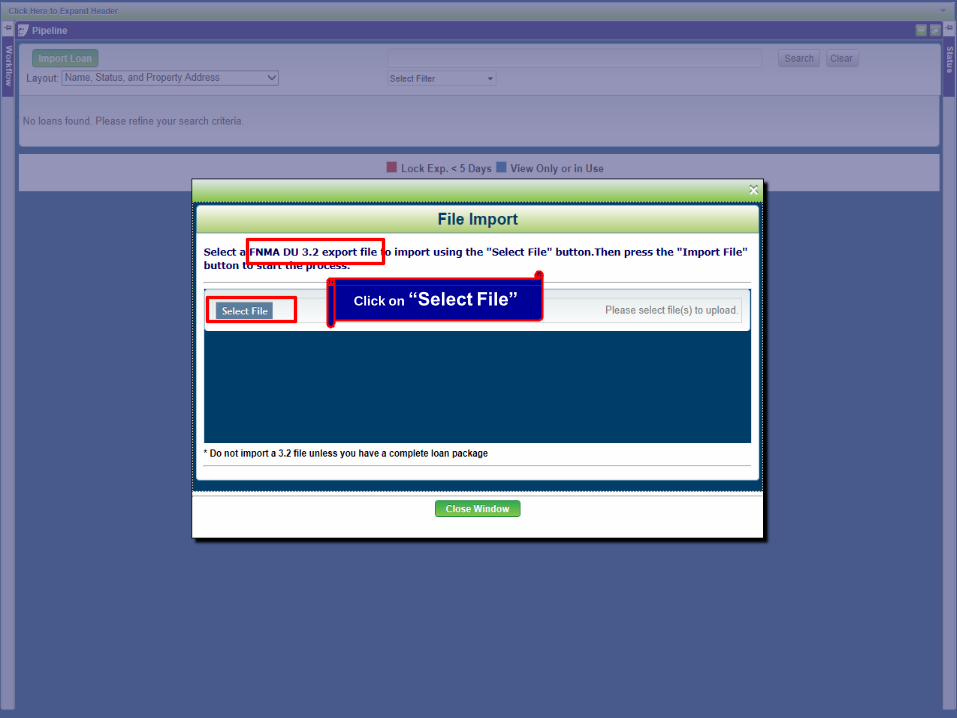

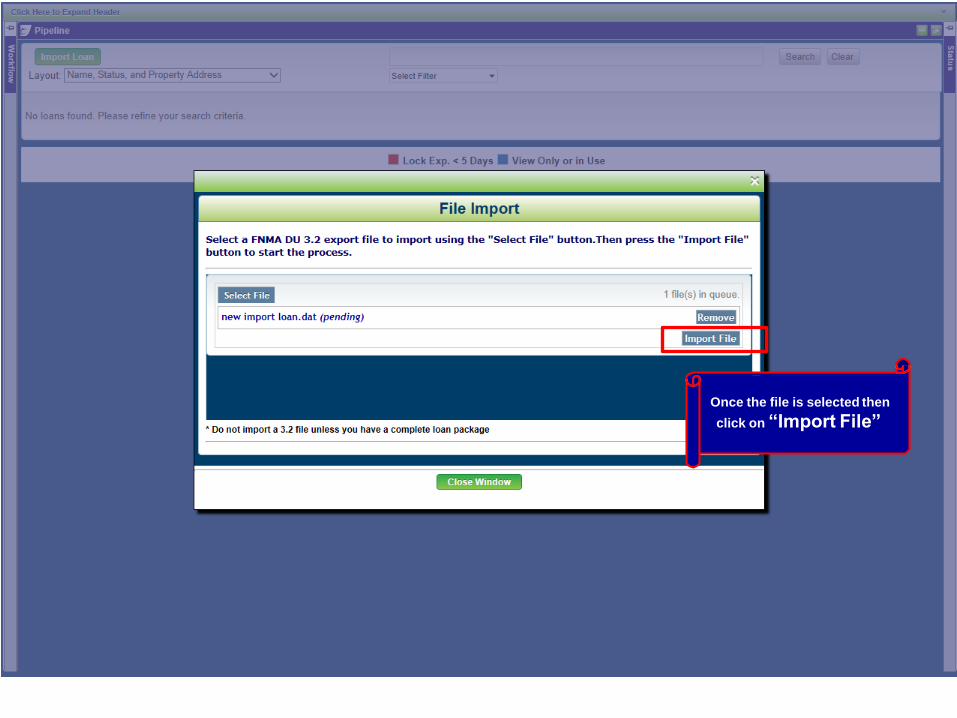

Click on “Import Loan”

Click on “Select File”

Select the file to upload

Once the file is selected then

click on “Import File”

You can follow status

Once the file is imported then

the Loan Review Screen

will appear

Wherever you see the

“Thumbnail” you can

open or collapse

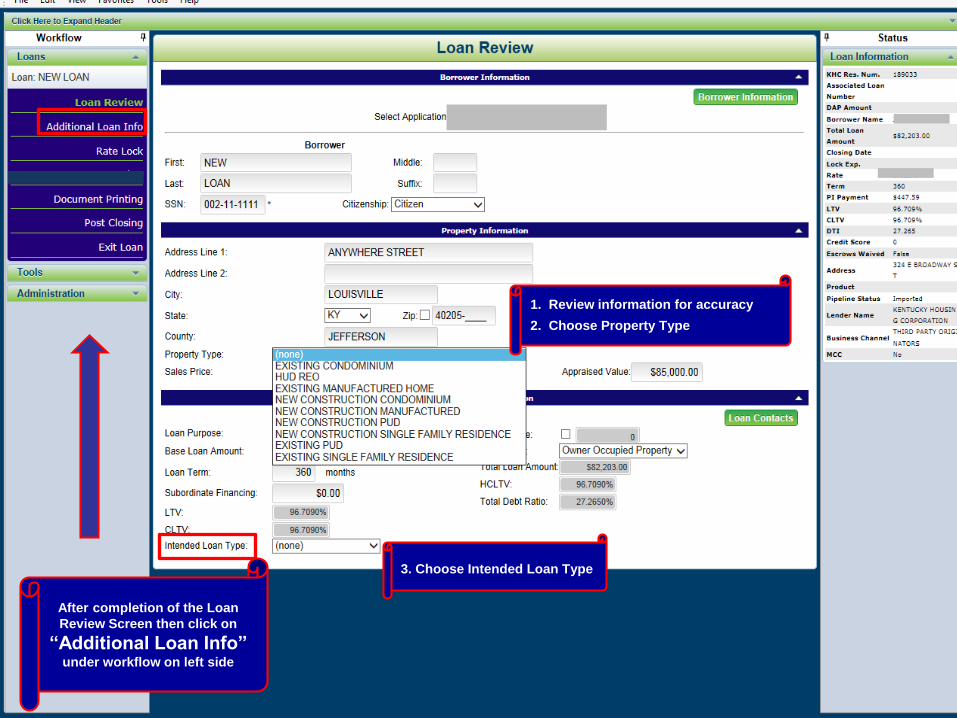

1. Review information for accuracy

2. Choose Property Type

3. Choose Intended Loan Type

After completion of the Loan

Review Screen then click on

“Additional Loan Info” under workflow on left side

Choose Loan Officer

AUS

Choose Loan Processor

All fields with an

“Asterisk” need to be

completed

These are the people that will be

contacted electronically when file is

underwritten

Input credit score &

select Repository

AUS

Complete ALL fields

with an Asterisk

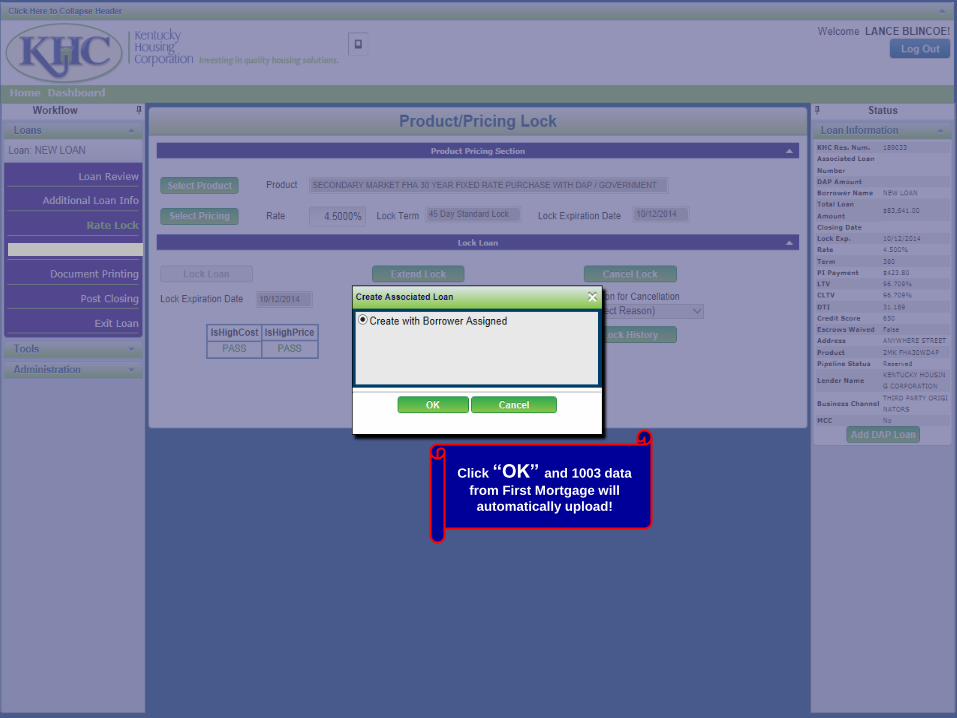

Attaching a DAP?

Closing Agent Question

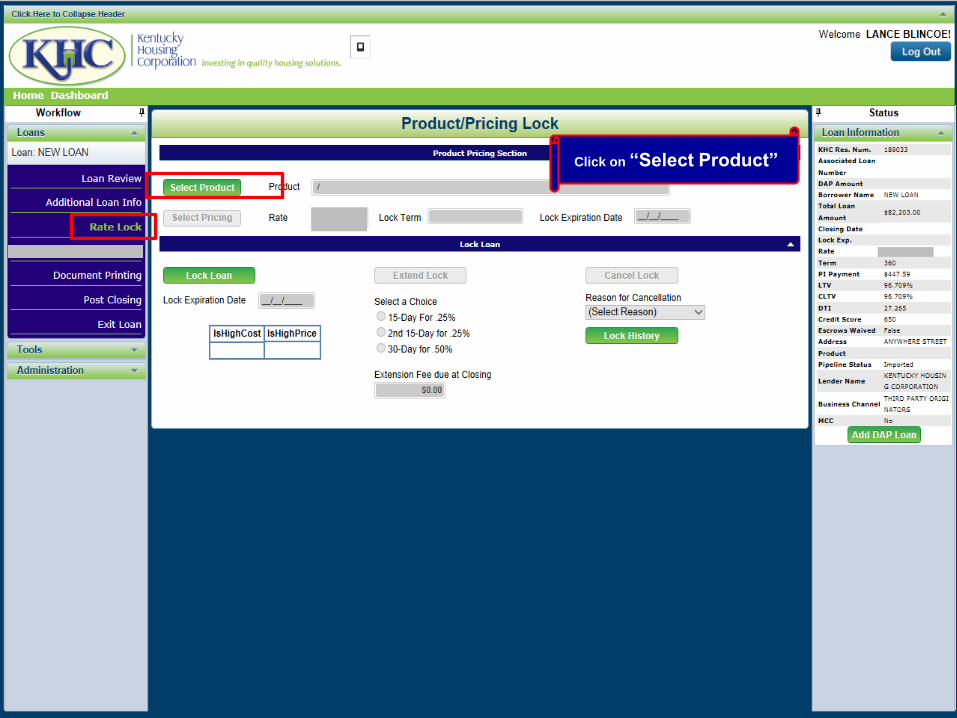

When complete click

on “Rate Lock”

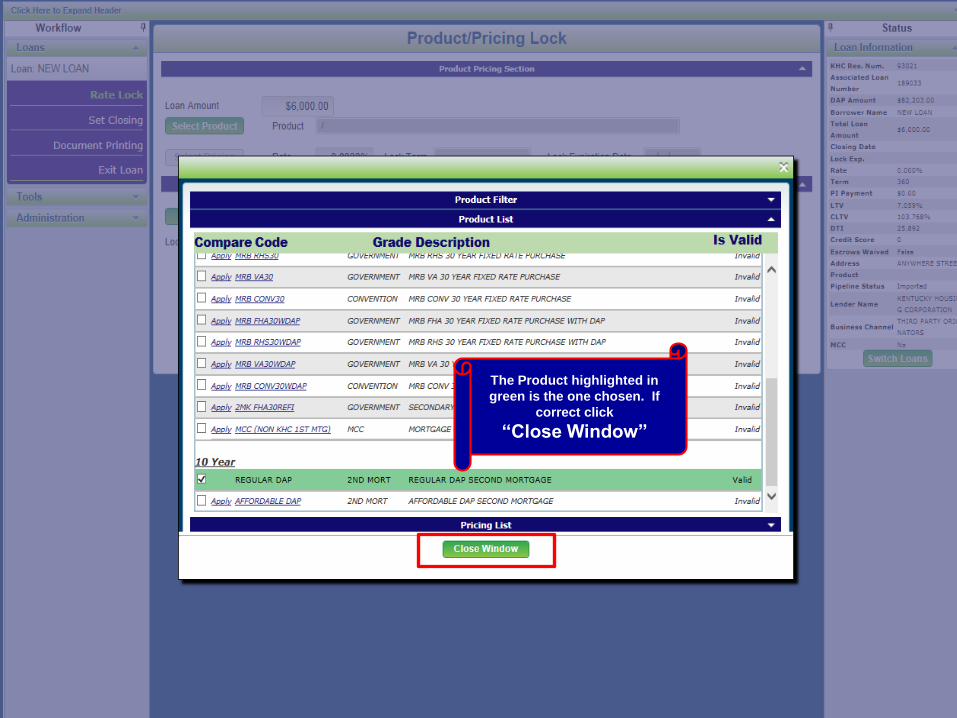

Click on “Select Product”

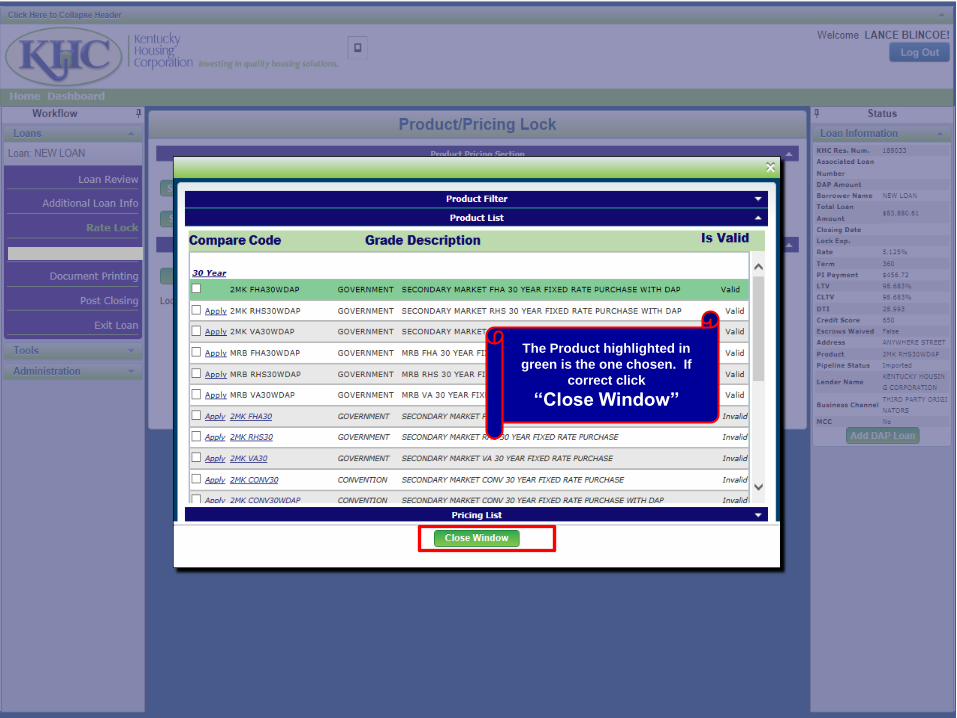

Check Product and

click on “Apply”

The Product highlighted in

green is the one chosen. If

correct click

“Close Window”

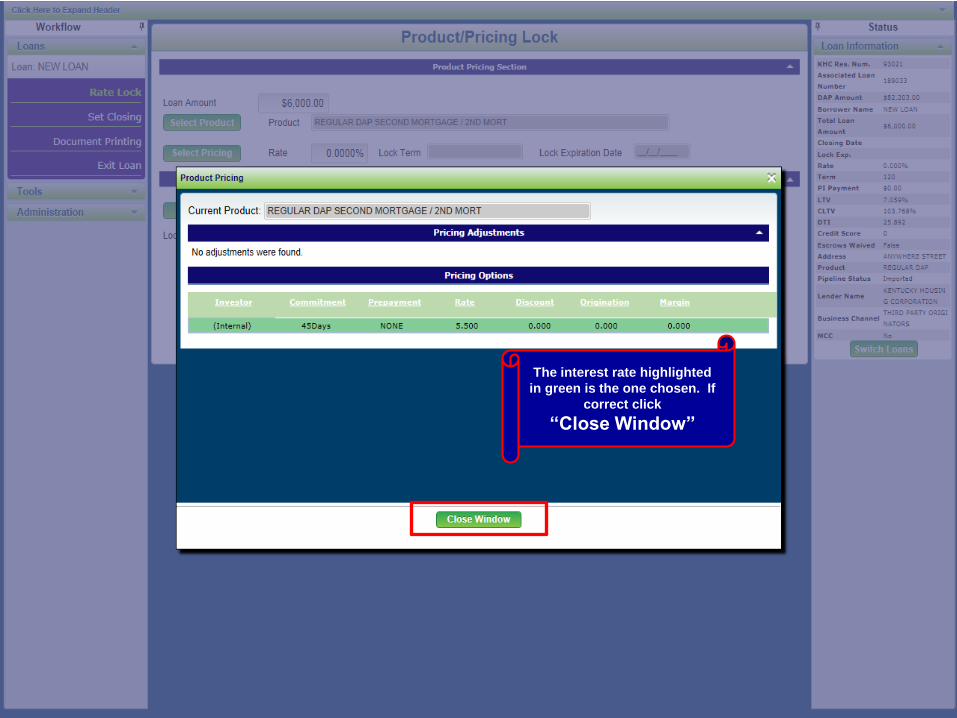

Click on

“Select Pricing”

Click on “Apply”

The interest rate highlighted

in green is the one chosen. If

correct click

“Close Window”

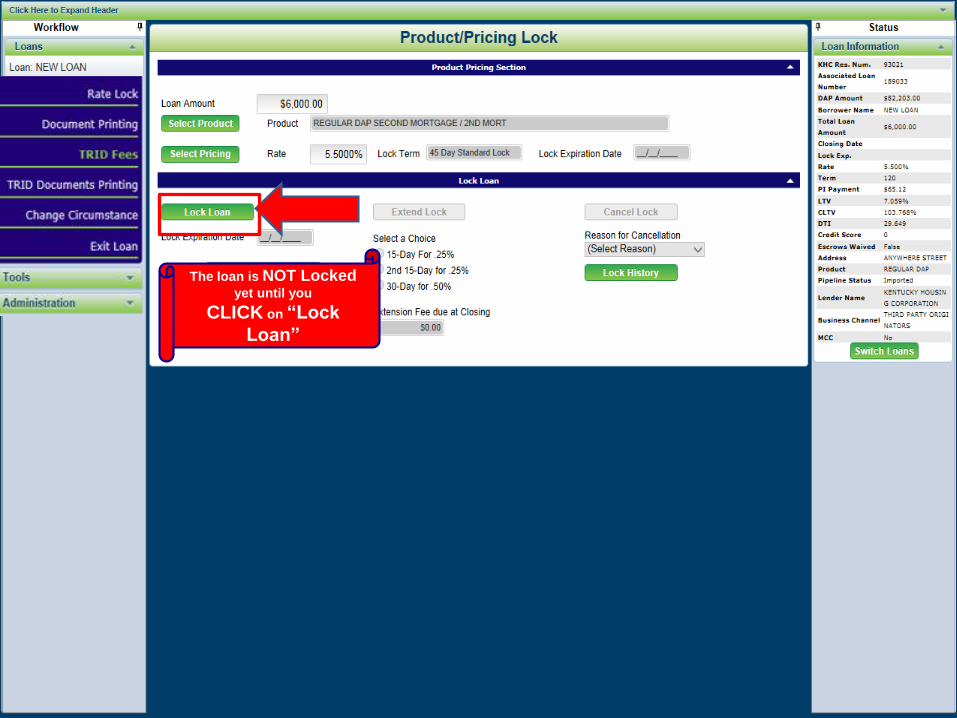

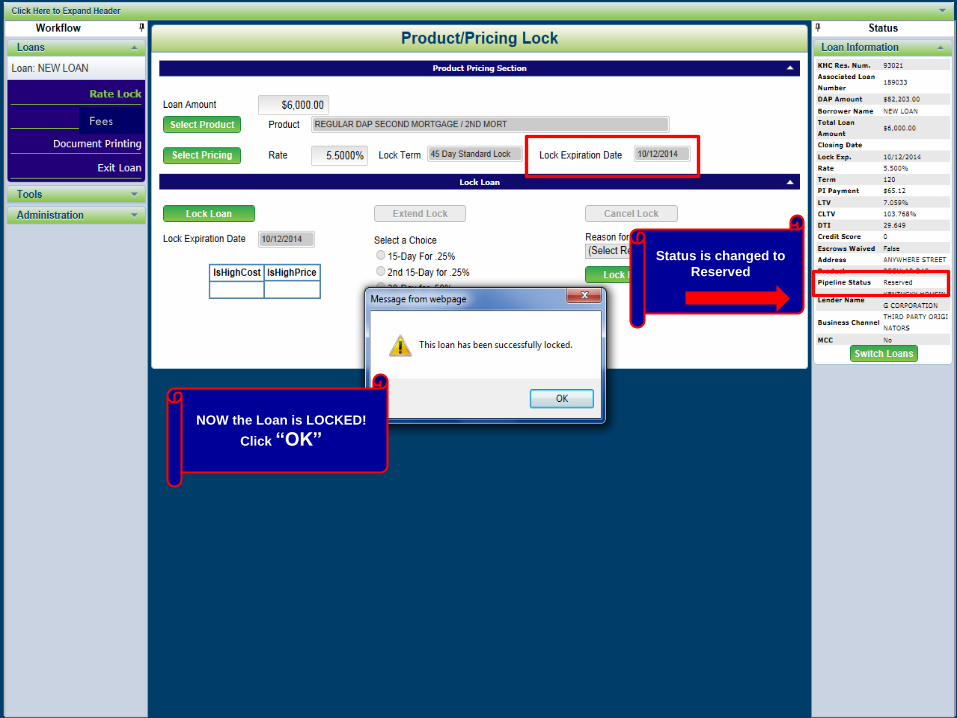

The loan is NOT Locked yet until you

CLICK on “Lock

Loan”

NOW the Loan is LOCKED!

See Lock Expiration

Date.

Click “OK”

Status is changed to

Reserved

Since this loan has a DAP

then you will need to click

on “Add DAP Loan”

Click “OK” and 1003 data

from First Mortgage will

automatically upload!

Click “OK” unless you do

NOT need the DAP

Since a second loan (DAP) has

been created you now need to

Click on “Switch Loan”

Type in DAP Loan Amount –

Round-up to Nearest $100

Click on

“Select Product”

Scroll down to bottom -- Check

Product and click on “Apply”. HHF DAP will show up here when

available

The Product highlighted in

green is the one chosen. If

correct click

“Close Window”

Click on

“Select Pricing”

Click on “Apply”

The interest rate highlighted

in green is the one chosen. If

correct click

“Close Window”

Fees

The loan is NOT Locked yet until you

CLICK on “Lock

Loan”

NOW the Loan is LOCKED!

Click “OK”

Status is changed to

Reserved

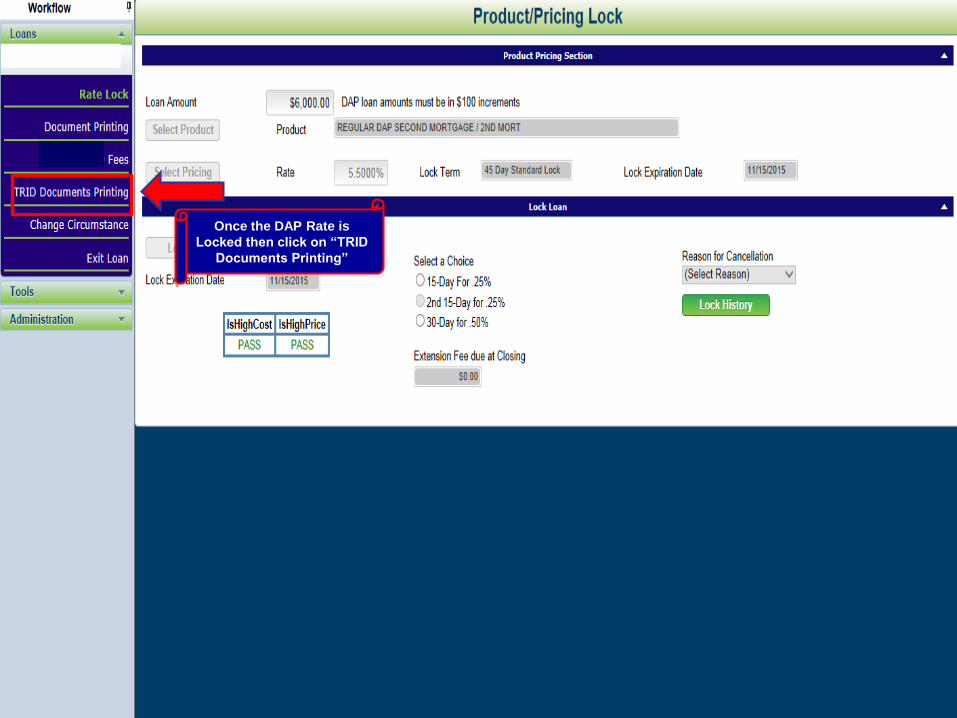

Fees

Once the DAP Rate is

Locked then click on “TRID

Documents Printing”

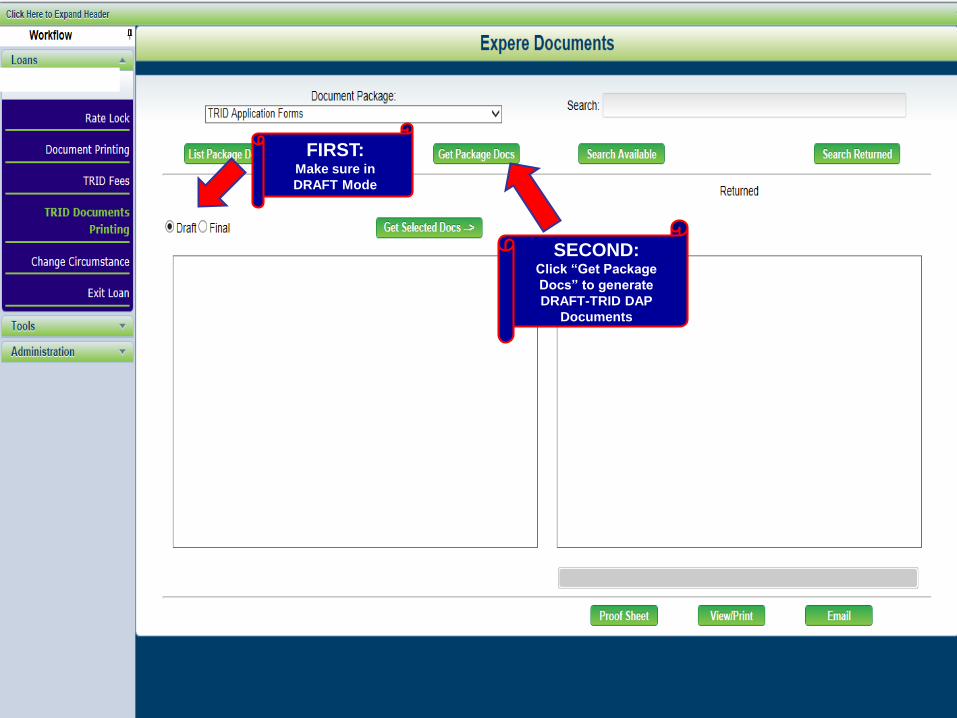

FIRST: Make sure in

DRAFT Mode

SECOND: Click “Get Package

Docs” to generate

DRAFT-TRID DAP

Documents

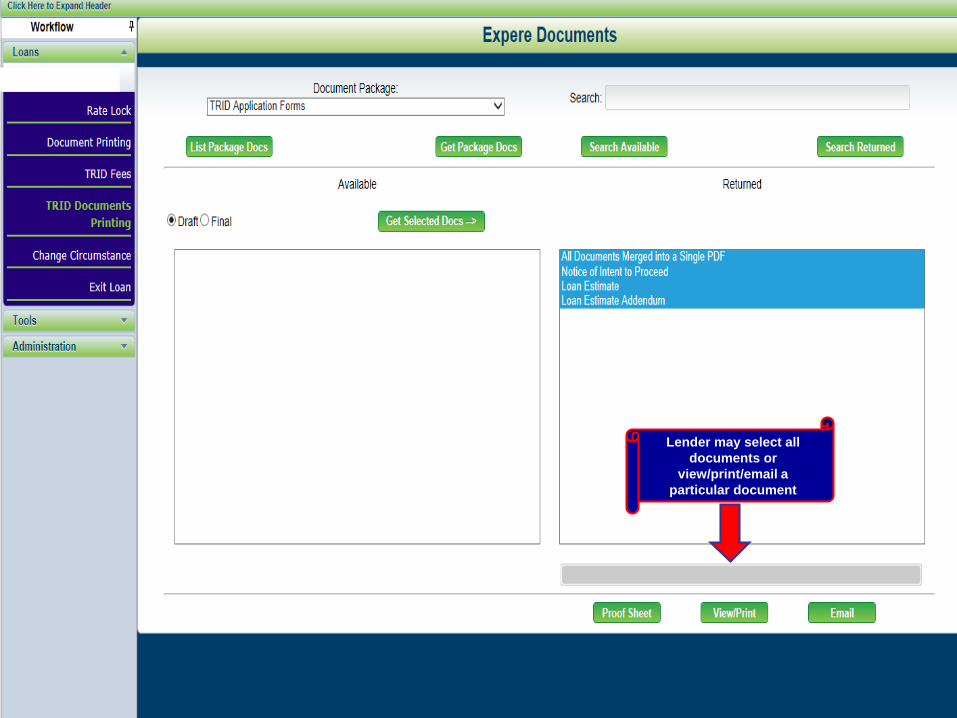

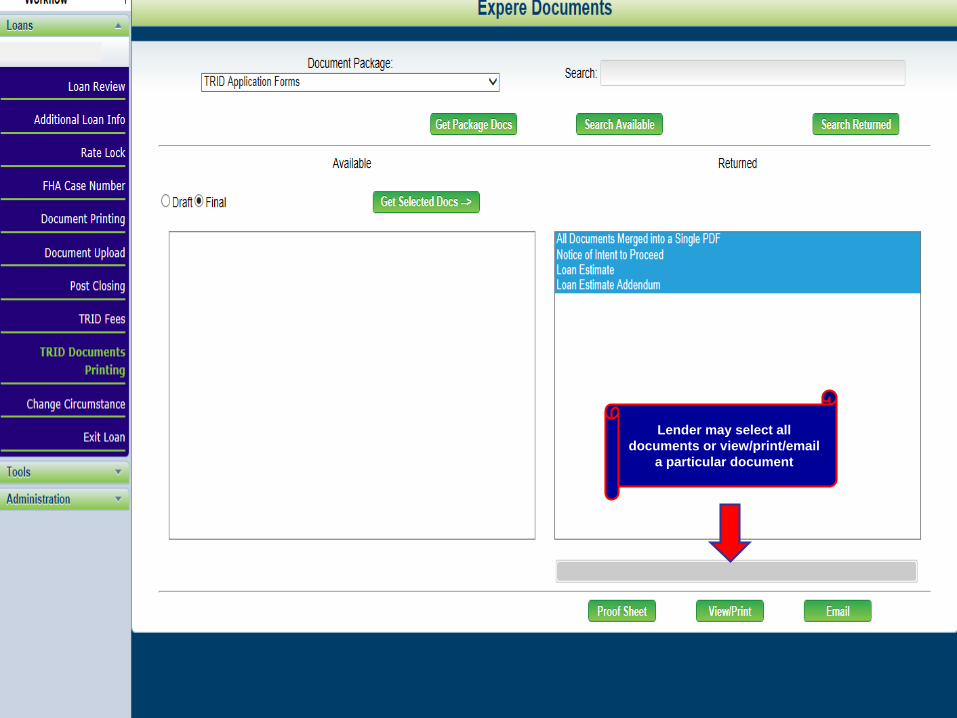

Lender may select all

documents or

view/print/email a

particular document

DRAFT DAP LE

Fees are already hard coded

($26 Recording Fee & $50

Doc Prep to Closing Agent)

DRAFT watermark

FIRST:

When ready to FINALIZE:Be sure all fees are correct,

because once the mode is changed

to FINAL the fees are locked down

unless a change of circumstance

occurs.

SECOND: Click “Get Package

Docs” to generate

FINAL-TRID

Documents

Click View/Print

Finalized Initial DAP LE

without the DRAFT

watermark

Click on “SWITCH LOAN” to

go back to the first

mortgage

Fees

Conventional Preferred Loans

Mortgage Insurance Tab

Choose MI Company from drop-down.

Enter MI Rate to flow over to First Mortgage LE.

Must be done PRIOR to Fees Tab for First Mortgage LE.

Or MI will not disclose on LE.

Tolerance Cure.

Mortgage Insurance If Loan is Conventional

“PREFERRED” with MI then need

to go to Mortgage Insurance

page before FEEs for LE

These fields need to be completed or

the MI will not show up on First

Mortgage LE. Your company will be

responsible for Tolerance Cure.

Fees

CLICK on “Fees”

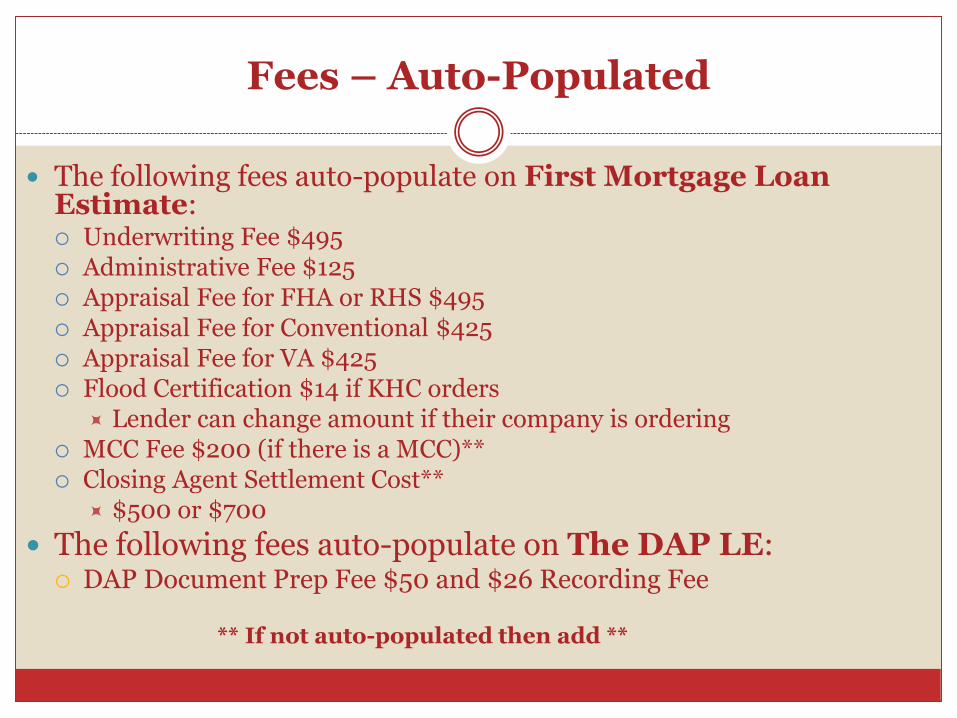

Fees – Auto-Populated

The following fees auto-populate on First Mortgage Loan Estimate: Underwriting Fee $495 Administrative Fee $125 Appraisal Fee for FHA or RHS $495 Appraisal Fee for Conventional $425 Appraisal Fee for VA $425 Flood Certification $14 if KHC orders

Lender can change amount if their company is ordering MCC Fee $200 (if there is a MCC)** Closing Agent Settlement Cost**

$500 or $700

The following fees auto-populate on The DAP LE: DAP Document Prep Fee $50 and $26 Recording Fee

** If not auto-populated then add **

Additional Fees – Non-PopulatedIf Applicable

Credit Report

VOE Fee

DU/LP Fee

Extension Fee

When interest rate extended in KHC’s Loan Reservation System then it will auto-populate.

A Changed Circumstance and new Loan Estimate will need to be printed

Flood Insurance

Final Inspection - $150 ( if required)

Termite Inspection

Structural Engineer Inspection

Home Inspection

Survey

Hazard Insurance

Premium Tax and CPL

Owner’s Title Insurance

Lender’s Title Insurance

One line item for all additional title services

Loan Estimate Buckets

Easier to use the Buckets A thru J and Calculating Cash to Close A – Origination Charges

B – Services You Cannot Shop For

C – Services You Can Shop For

D – Total Loan Costs (A+B+C)

E – Taxes and Other Government Fees

F – Prepaids

G – Initial Escrow Payment at Closing

H – Other

I – Total Other Costs (E+F+G+H)

J – Total Closing Costs

Easiest way to

navigate – by the

buckets

To edit a

fee click

on the

button

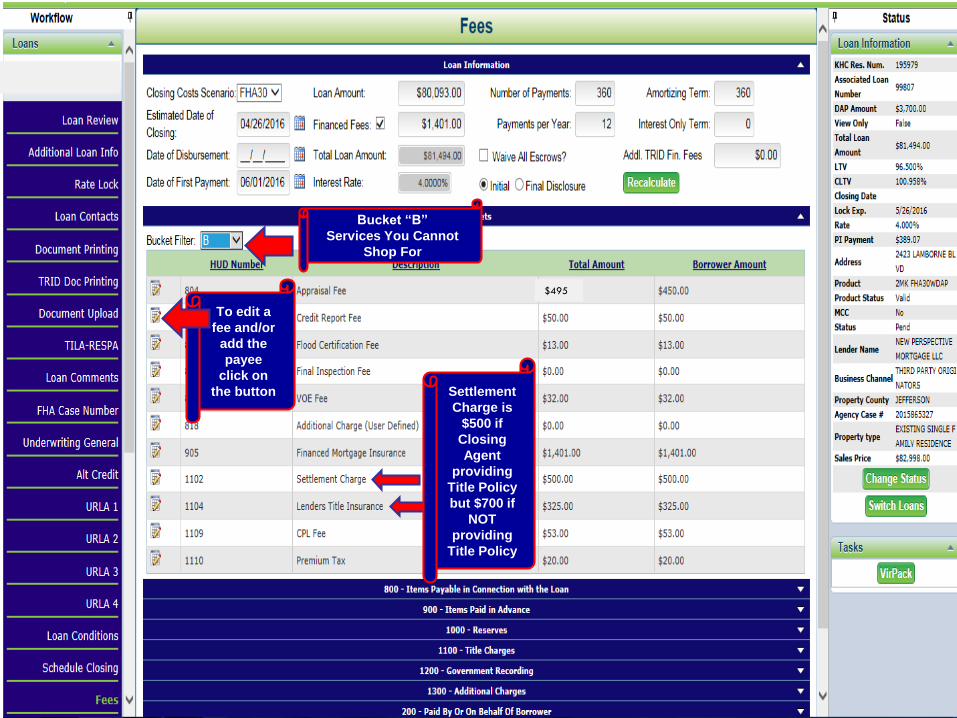

Bucket “A”

Origination Charges

$125

Bucket “B”

Services You Cannot

Shop For

Settlement

Charge is

$500 if

Closing

Agent

providing

Title Policy

but $700 if

NOT

providing

Title Policy

To edit a

fee and/or

add the

payee

click on

the button

$495

Add Provider Name

and then click “OK”

Click “OK”

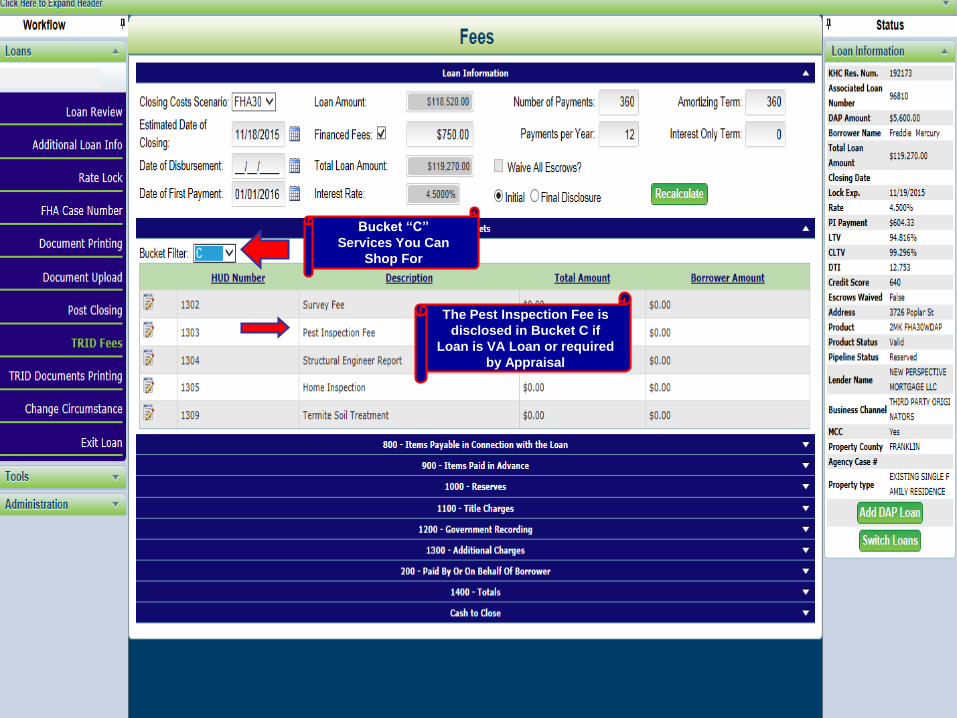

Bucket “C”

Services You Can

Shop For

The Pest Inspection Fee is

disclosed in Bucket C if

Loan is VA Loan or required

by Appraisal

Bucket “E”

Taxes & Other

Government Fees

Bucket “F”

Prepaids

Enter Annual Hazard

Insurance Premium. Interest

automatically calculates at 15

days

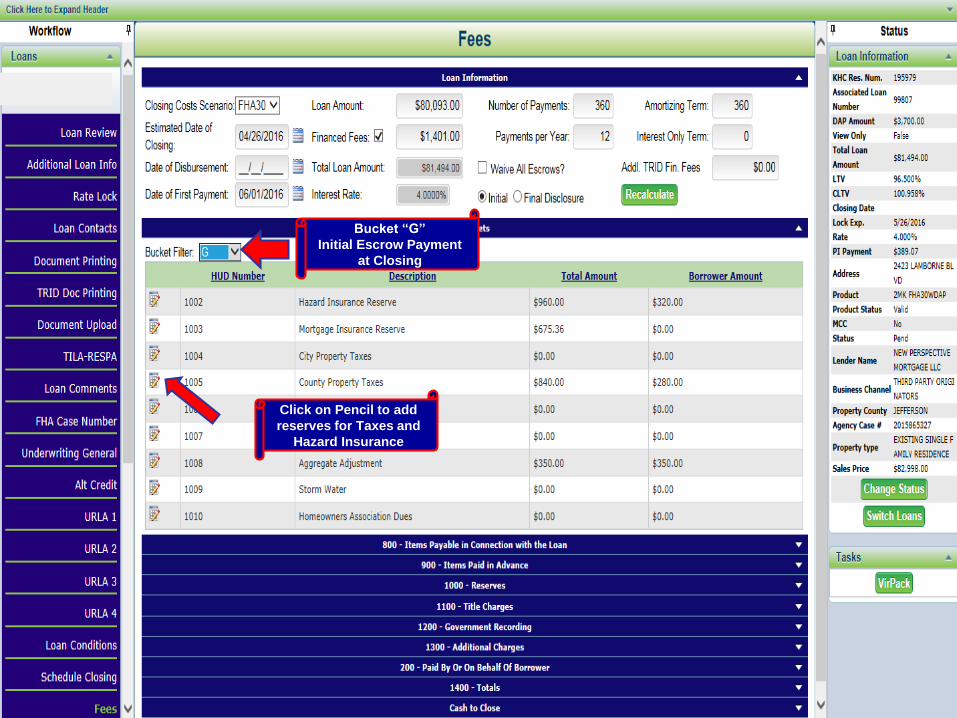

Bucket “G”

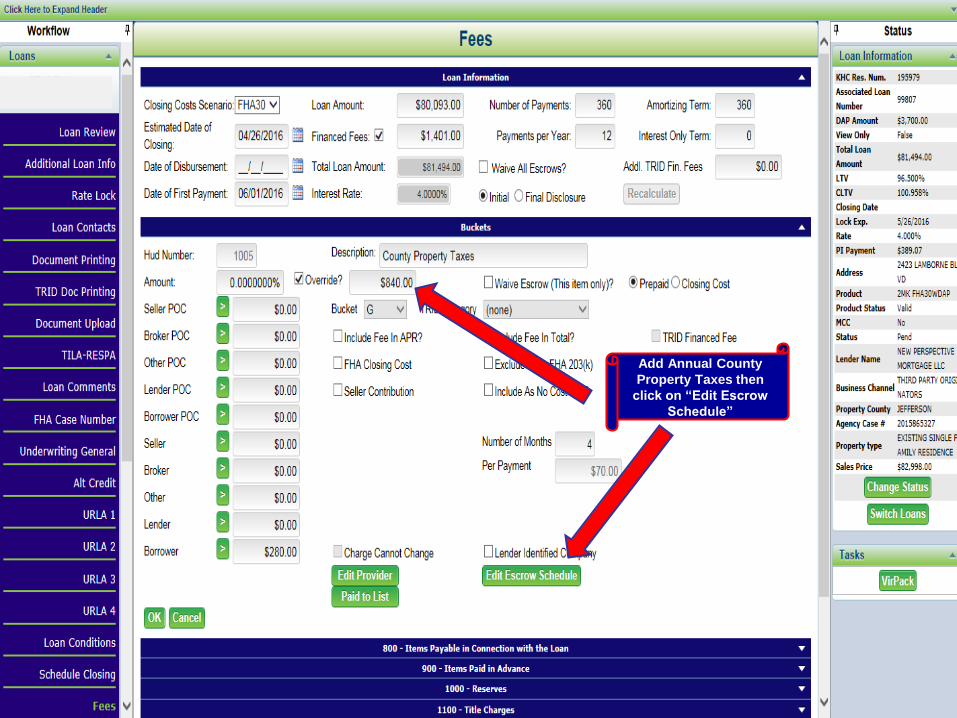

Initial Escrow Payment

at Closing

Click on Pencil to add

reserves for Taxes and

Hazard Insurance

Add Annual County

Property Taxes then

click on “Edit Escrow

Schedule”

Check the Month this

payment is disbursed

(it defaults to October

for Taxes)– system will

automatically calculate

the number of required

months in reserves

then Click “OK”

Click “OK”

The County Property

Tax Reserve is

populated

Do the same for Hazard

Insurance Reserve

Do NOT override Aggregate

Adjustment or Mortgage Insurance

Reserve – does not disclose on LE

but does on CD

Bucket “H”

Other

Must disclose cost

The Pest

Inspection Fee

is disclosed in

Bucket H if not

a VA Loan or

not required by

the Appraiser

Bucket “J”

Only used by TPO for a

Tolerance Cure

Bucket “K” – Do NOT need to go

into this bucket—it is for CD

Seller Paid Closing Costs

DAP –

automatically

flows from

lock

GIFT

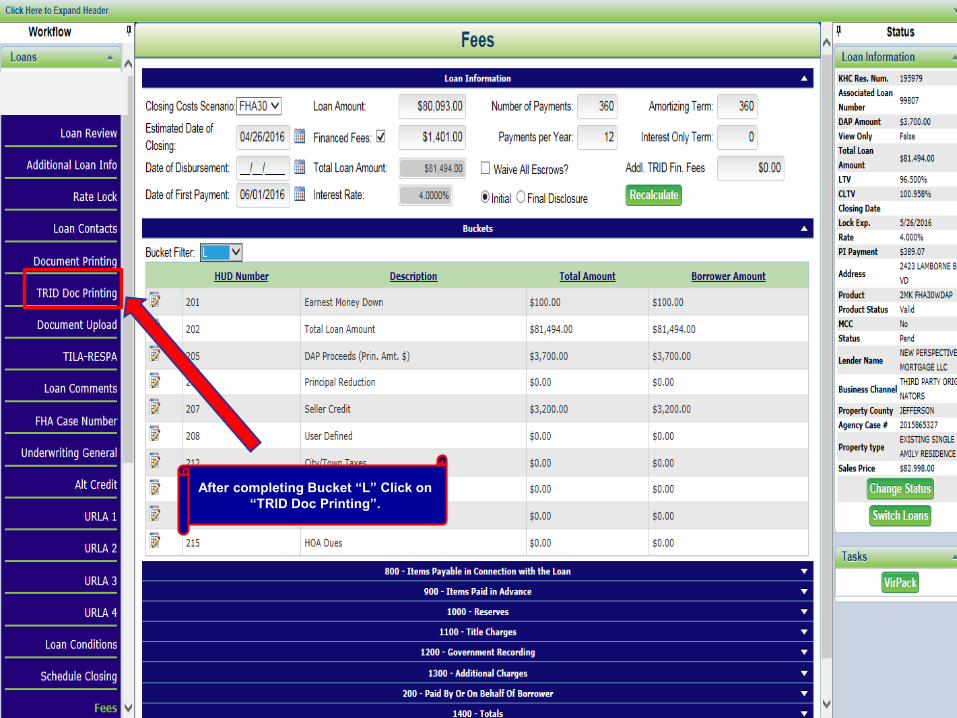

Bucket “L”

Calculating Cash to

Close

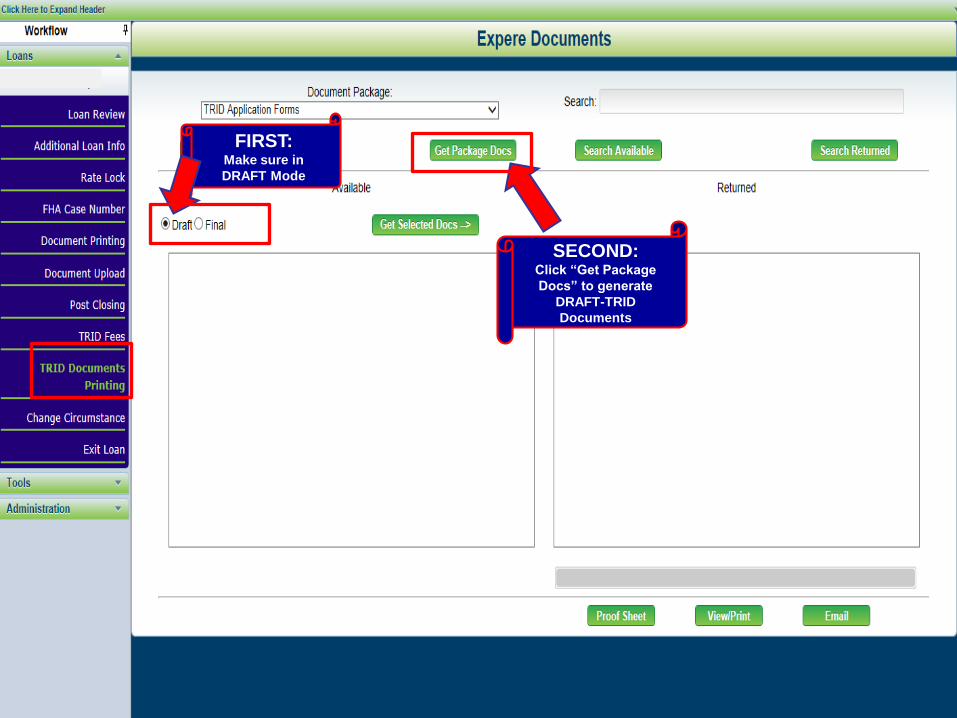

After completing Bucket “L” Click on

“TRID Doc Printing”.

SECOND: Click “Get Package

Docs” to generate

DRAFT-TRID

Documents

FIRST: Make sure in

DRAFT Mode

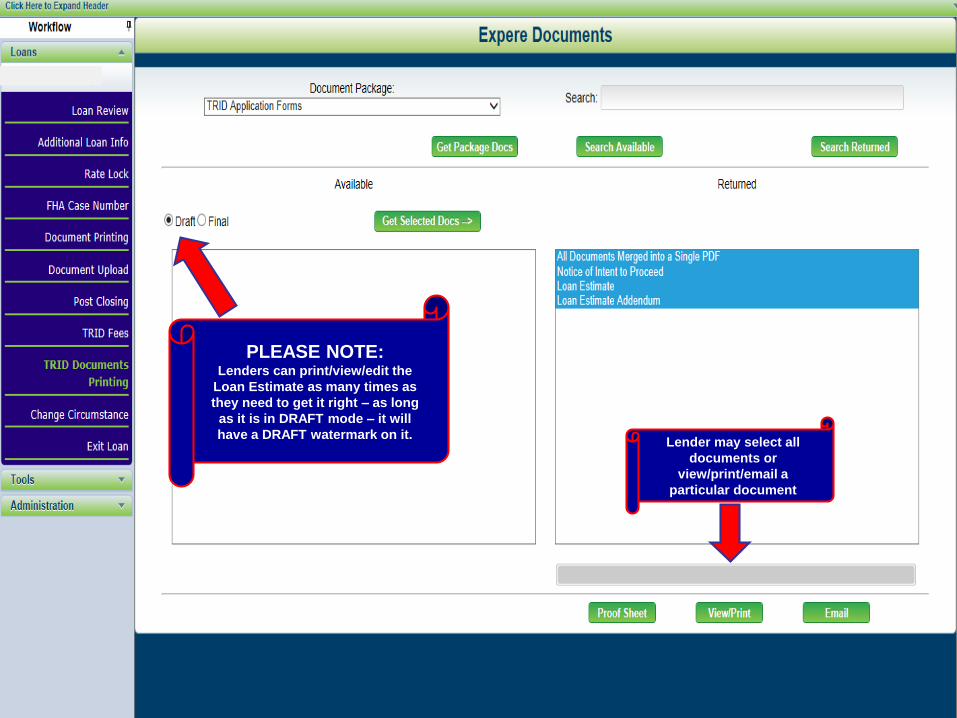

PLEASE NOTE:Lenders can print/view/edit the

Loan Estimate as many times as

they need to get it right – as long

as it is in DRAFT mode – it will

have a DRAFT watermark on it. Lender may select all

documents or

view/print/email a

particular document

FIRST:

When ready to FINALIZE:Be sure all fees are correct,

because once the mode is changed

to FINAL the fees are locked down

unless a change of circumstance

occurs.

SECOND: Click “Get Package

Docs” to generate

FINAL-TRID

Documents

Lender may select all

documents or view/print/email

a particular document

Loan Estimate

Print and change as many times in DRAFT mode.

Final mode -- cannot make any changes unless a valid Change of Circumstance.

The date of the LE will be the date the LE is finalized.

Needs to be within the 3 days of application date, OR

An earlier LE from your system.

So review, review, review to ensure you have all fees correct.

***Any cost to cure will be collected from the TPO Lender***

Common Errors

Double check Closing Agent Title Fees.

Most tolerance cures for this fee.

Owner’s Title Insurance cost not entered.

Escrow Setups.

Be sure to print out and review before finalizing the Loan Estimate.

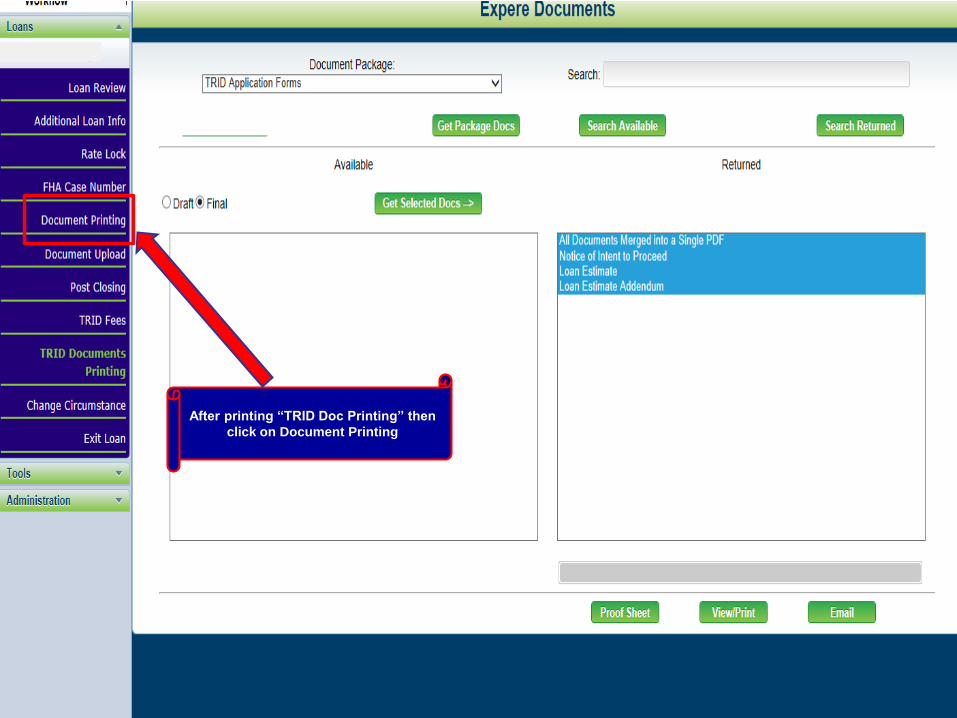

After printing “TRID Doc Printing” then

click on Document Printing

KHC Underwriting Checklist

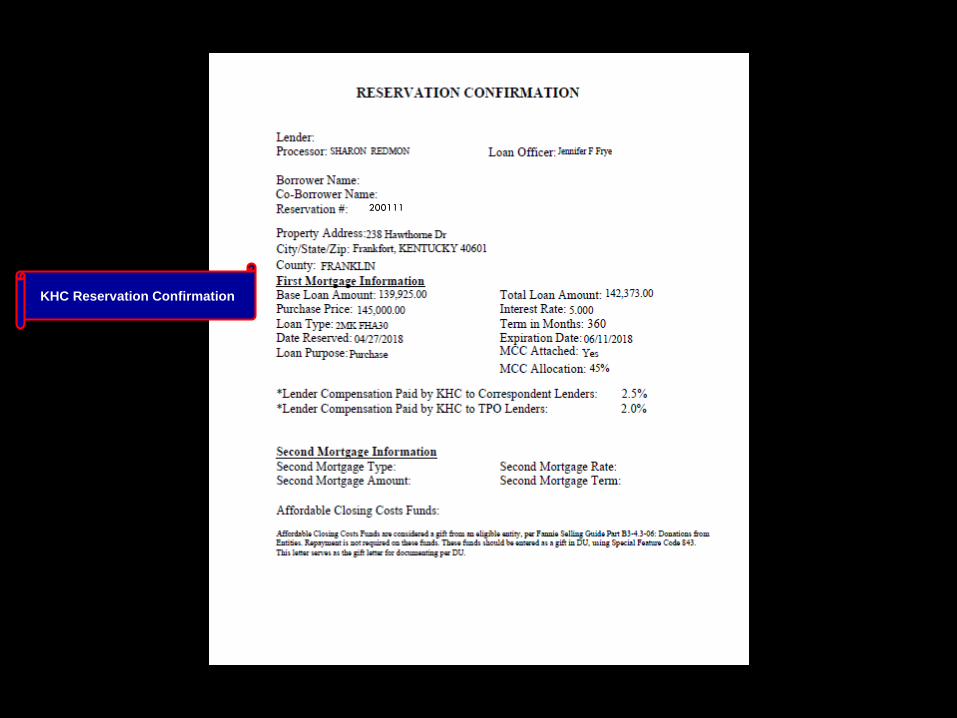

KHC Reservation Confirmation

200111

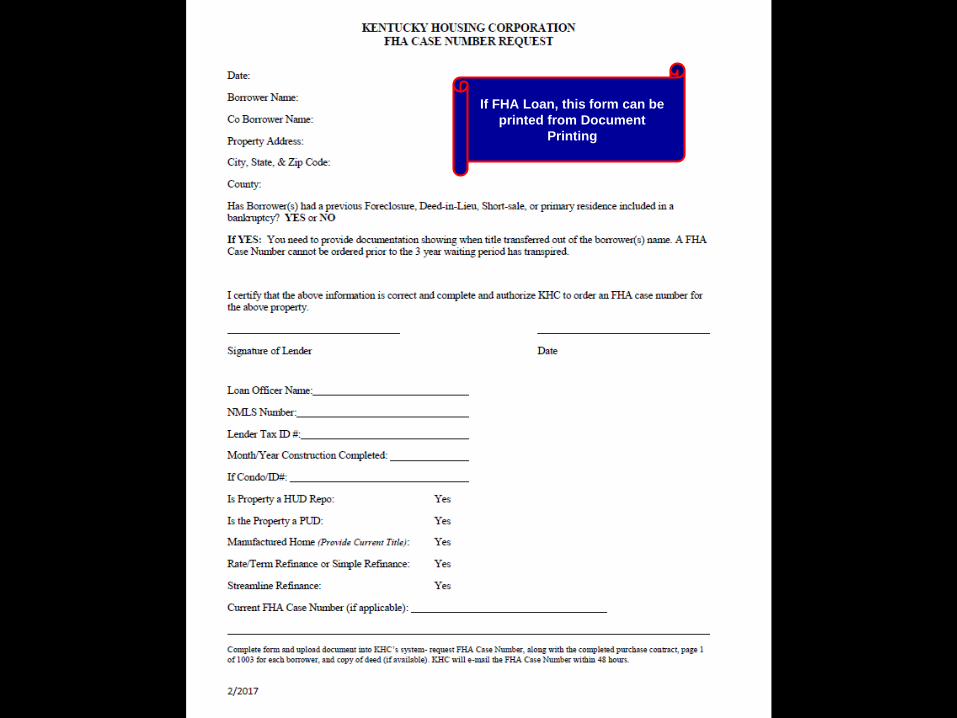

If FHA Loan, this form can be

printed from Document

Printing

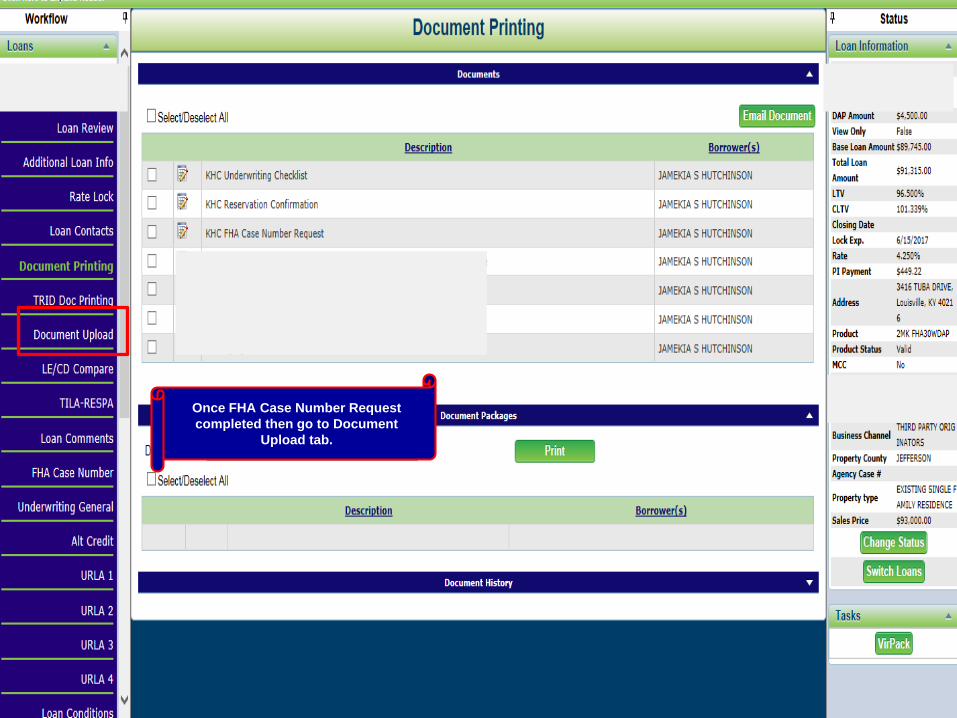

Requesting FHA Case Number

Once FHA Case Number Request

completed then go to Document

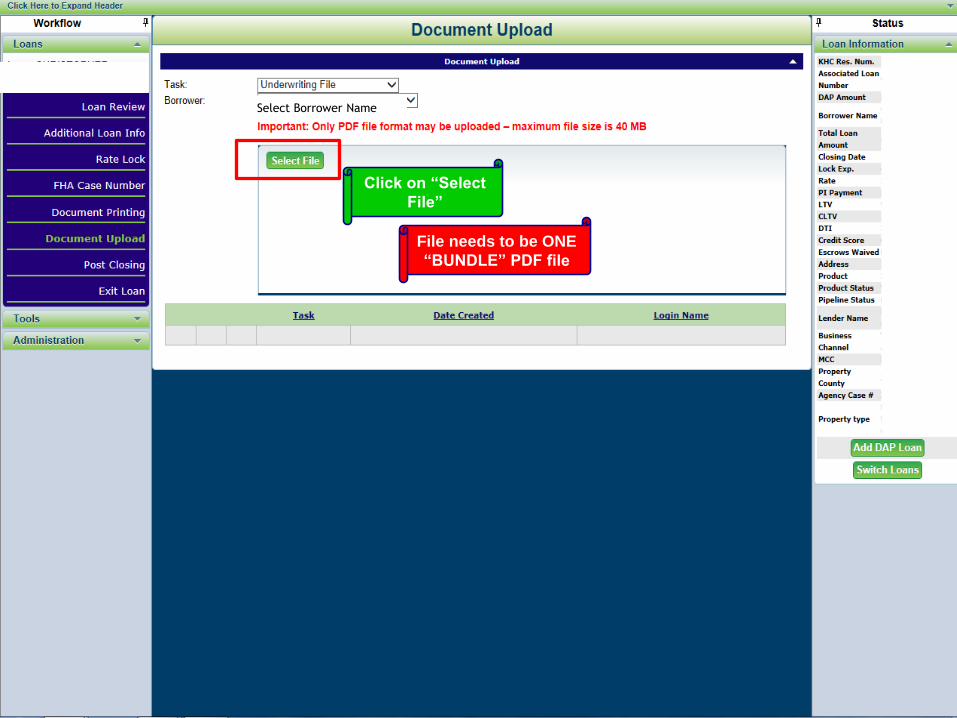

Upload tab.

Click on “Select

File”

File needs to be ONE

“BUNDLE” PDF file

Select Borrower Name

FHA Case Number Request Select FHA Case

Number Request

Upload FHA Case Number

Request, all pages of purchase

contract and page one of 1003

Once file has been

selected then click on

“UPLOAD” button

FHA Case Number Request

FHA Case Number Request

FHA Case Number

Within 24 - 48 hours the FHA Case Number is entered on the FHA Case Number Tab.

An email notification is sent to the Loan Officer/Processor listed in Additional Loan Data screen notifying them it is available.

05/15/2018

203(b)A123456789

FHA Case Number,

Borrower and Co-

borrower CAIVR#s

2012222222222

KHC’s Loan Reservation System

CHANGES TO RESERVED LOAN

Changes to Reservation

Loan Amount and Purchase Price can all be changed while in RESERVED status ONLY.

Once Underwriting File is uploaded then ONLY extension to interest rate or cancellation of reservation is available.

If other changes need to be made then email [email protected]

Once you enter Broker ID,

User Name and Password

click on “Log In”

Most changes to the

reservation can be made by

the lender

Choose applicable loan

To make changes to the

Expiration Date click on

“RATE LOCK”

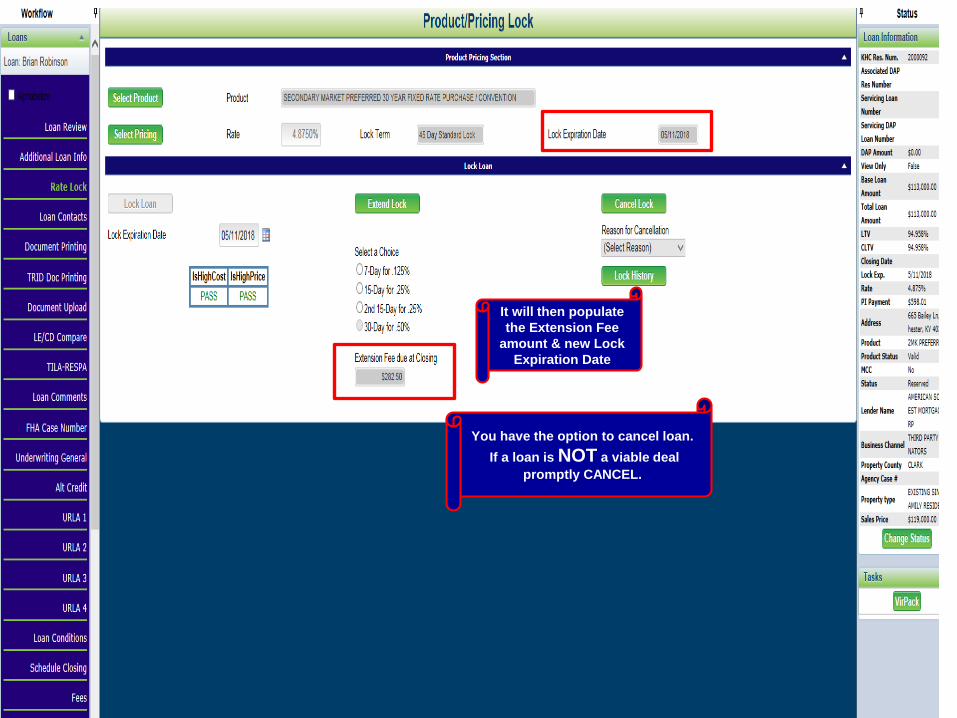

You can extend for a total of 7

days, 15 days, 30 days

intervals or all at once)—see

applicable fees

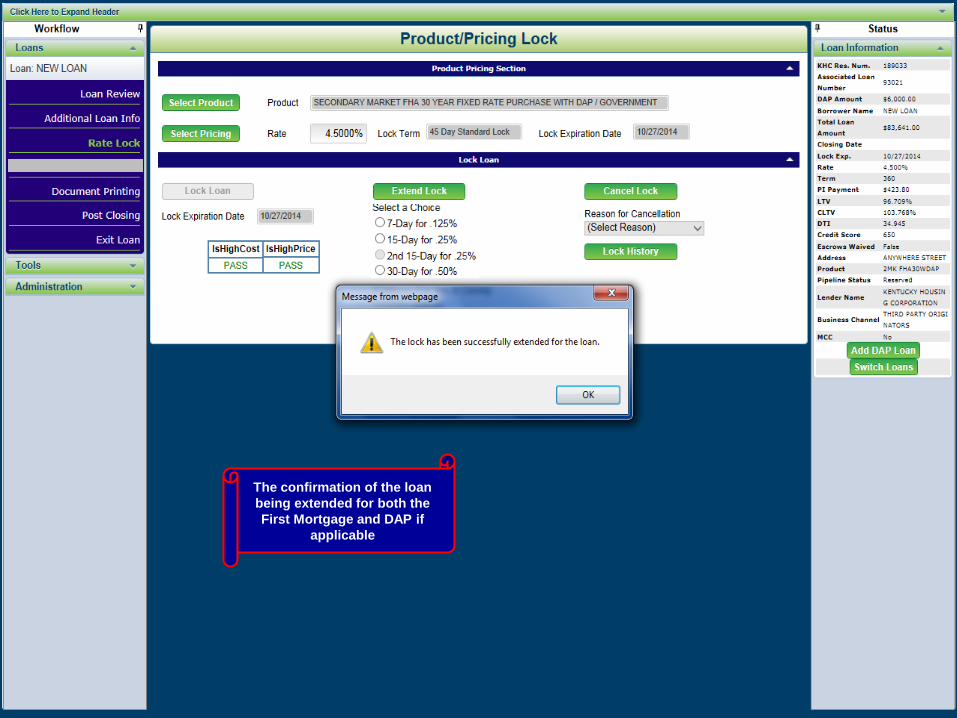

The confirmation of the loan

being extended for both the

First Mortgage and DAP if

applicable

It will then populate

the Extension Fee

amount & new Lock

Expiration Date

You have the option to cancel loan.

If a loan is NOT a viable deal

promptly CANCEL.

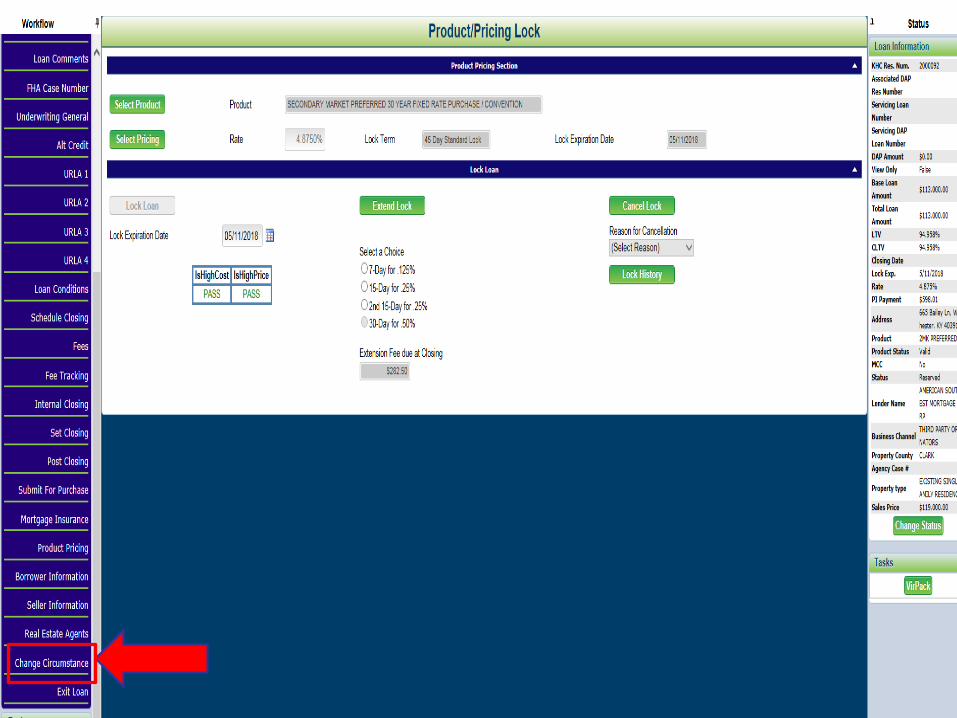

Change of Circumstance

EXTENSION FEEPAID BY THE BORROWER

Change of Circumstance

HOW TO ADD THE EXTENSION FEE TO THE LE

Change of Circumstance

Once rate is extended in Rate Lock Screen…

Click on Change of Circumstance Tab.

Choose “Extension Fee”.

Ensure Latest Disclosure date matches COC date.

Choose Change Circumstance Reason from dropdown.

Click the “Push Current to LE” button on the right side of the screen to flow to the TRID documents.

Click Ok.

Click on Document Printing.

Print the COC Form.

Click on TRID Documents Printing.

Print the updated Loan Estimate.

Make sure the Date of

Latest Disclosure

Matches the date of

COC

Select Change of Circumstance Reason:• Lock Extension

• Not a Valid Reason

• Property Type Change

• Legal Address Error

• Property Value Change

• Borrower Requested Change in Loan

Terms/Product

• Credit Qualify Change Due to New Info Received

Push Current to LE and then

click “OK”. Then go to TRID

Documents Printing

SECOND:Click “Get Package Docs”

to generate DRAFT TRID

Documents and Change

of Circumstance Form

FIRST: Make sure in

DRAFT Mode

FIRST: Make sure in FINAL

Mode

SECOND:Click “Get Package Docs” to

generate FINAL TRID

Documents and Change of

Circumstance Form and

click on the View/Print

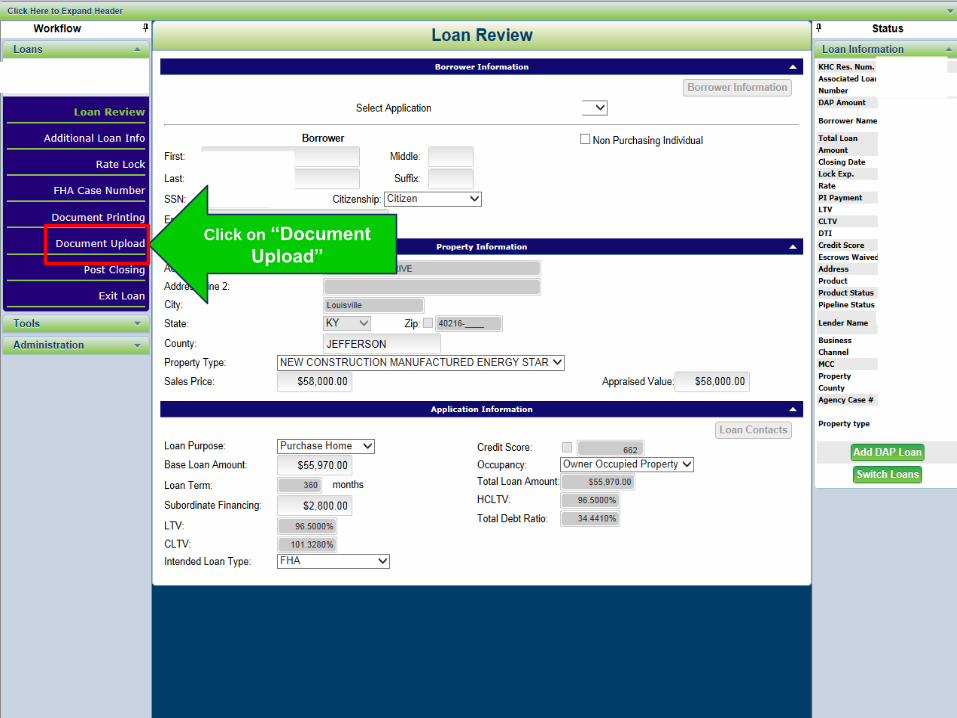

Electronic Upload

KHC’S RESERVATION SYSTEM

Document Upload

For Multi‐Function Devices and scanners the below settings will need to be made standard so that the quality of scanned files is optimal: 300 dpi.

Black & White (not grayscale as that will create significantly larger image files.

Auto-Sense Page Size.

No Page Scaling.

Don’t Compress or Zip Files.

If you have questions please contact your technical support staff.

Document UploadOnly one “BUNDLE” PDF File

“BUNDLE” Underwriting checklist prints when reservation is made.

TPO Lenders: Upload:

FHA Case Number Request.

Underwriting File.

Underwriting Pend Conditions.

TPO Pre-closing Package.

Electronic Upload

UNDERWRITING FILE

Click on “Document

Upload”

Select Underwriting

File

Click on “Select

File”

File needs to be ONE

“BUNDLE” PDF file

Select Borrower Name

Once file has been

selected then click on

“UPLOAD” button

Once the UW File is listed

under Task then file has been

successfully uploaded!

You can go into this tab –

Document Upload to view

specifically what has been

uploaded at any given time.

Workflow

KHC UNDERWRITING

KHC Underwriting

Credit and Compliance Underwrite.

FHA, VA, RHS and Conventional.

Typically 3-4 business day turn-time.

If item(s) are left out of initial electronic Underwriting File upload AND the file has not been underwritten by KHC then send those items to [email protected].

Loan Status Changes

After initial underwriting review Loan Officer and Loan Processor (the ones selected in Additional Data Screen) will receive email notification .

“The status on the above referenced loan has been changed, please log into KHC website for details”.

Lender will go to Document Printing to print the Pend Letter, Commitment Letter or Denial Letter.

Electronically Upload the Underwriting Pend Conditions of specific loan in KHC’s Loan Reservation System.

Underwriting Pend Conditions.

Clearing Pend ConditionsGNMA & MRB Funding Sources

1. Follow KHC’s Underwriting Checklist.1. Submit complete file.

2. Do not submit multiple copies of forms.

3. Do not submit items if not requested.

2. Review what is being submitted.

3. Potential issue/situation, ask questions before submitting file.

4. Pended Loans -- submit all conditions at same time.1. Upload to Underwriting Pend Conditions

5. All forms are completed/signed by all applicable parties.

6. FHA loans only need first two pages of Initial 92900-A.

7. Income Calculator – include a completed version

Underwriting TipsGNMA & MRB Funding Sources

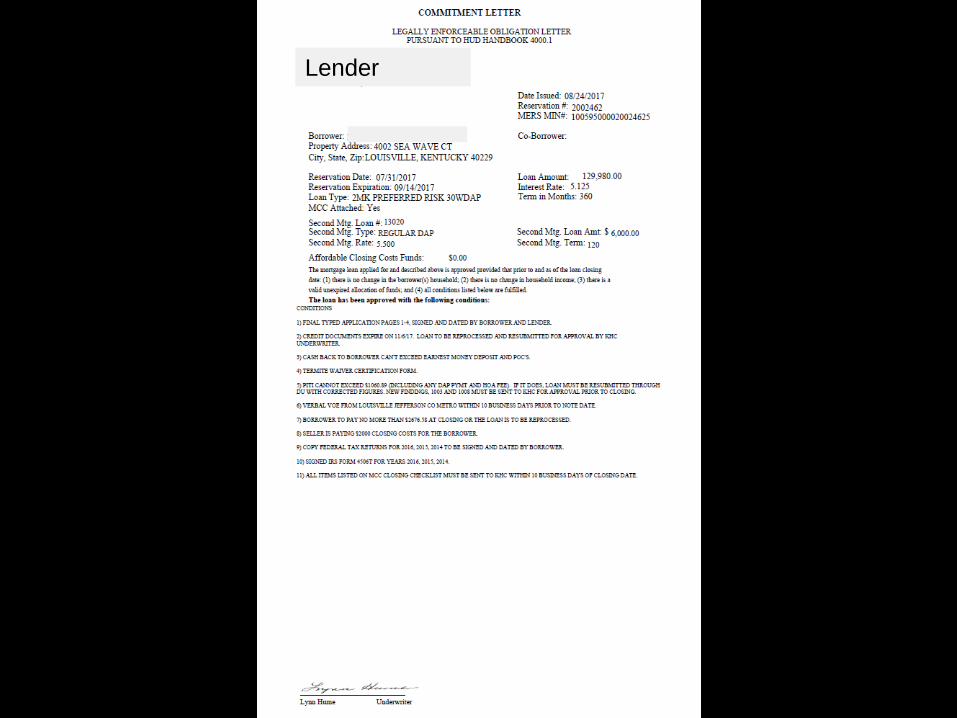

Approved Loan

KHC’S COMMITMENT LETTER

Click on “Document Printing”

to print Commitment Letter

Fee Sheet

Lender

Approved Loan

SCHEDULE CLOSING

Closing Disclosure

Provided to consumers at least three business days before consummation of the loan.

Does include Saturday in the counting of the 3 business days.

KHC is NOT open on Saturday so no mailings or closings can occur on a Saturday.

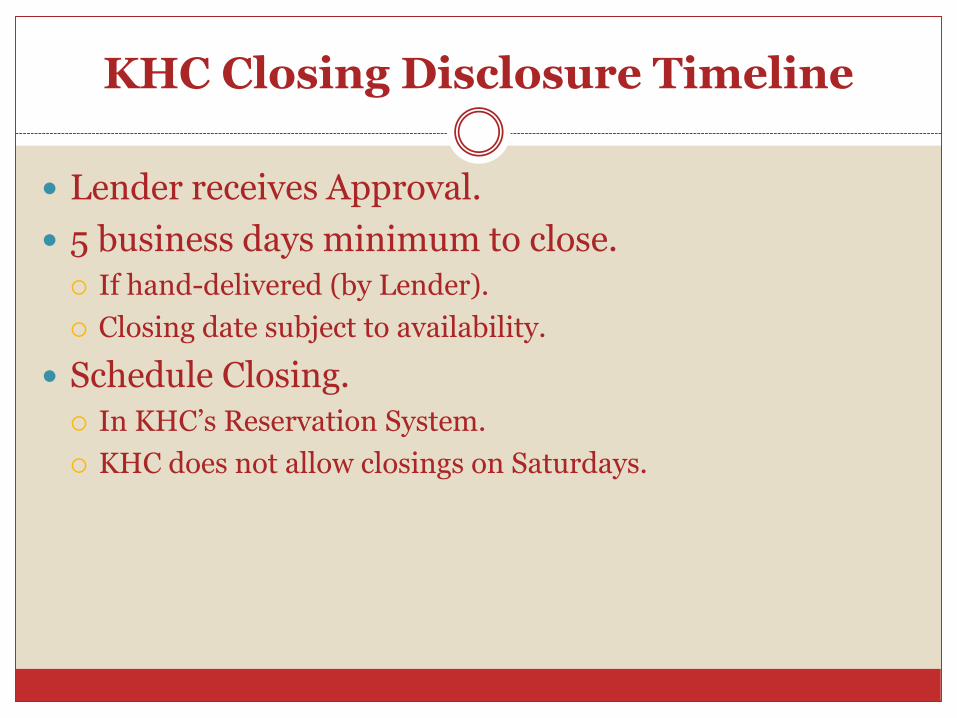

KHC Closing Disclosure Timeline

Lender receives Approval.

5 business days minimum to close.

If hand-delivered (by Lender).

Closing date subject to availability.

Schedule Closing.

In KHC’s Reservation System.

KHC does not allow closings on Saturdays.

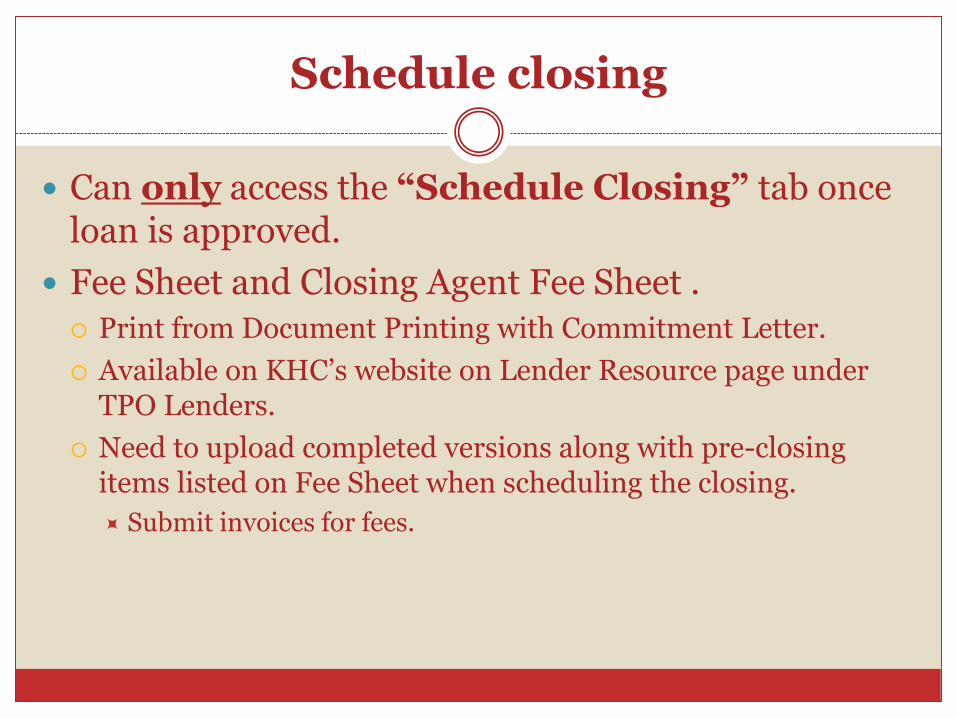

Schedule closing

Can only access the “Schedule Closing” tab once loan is approved.

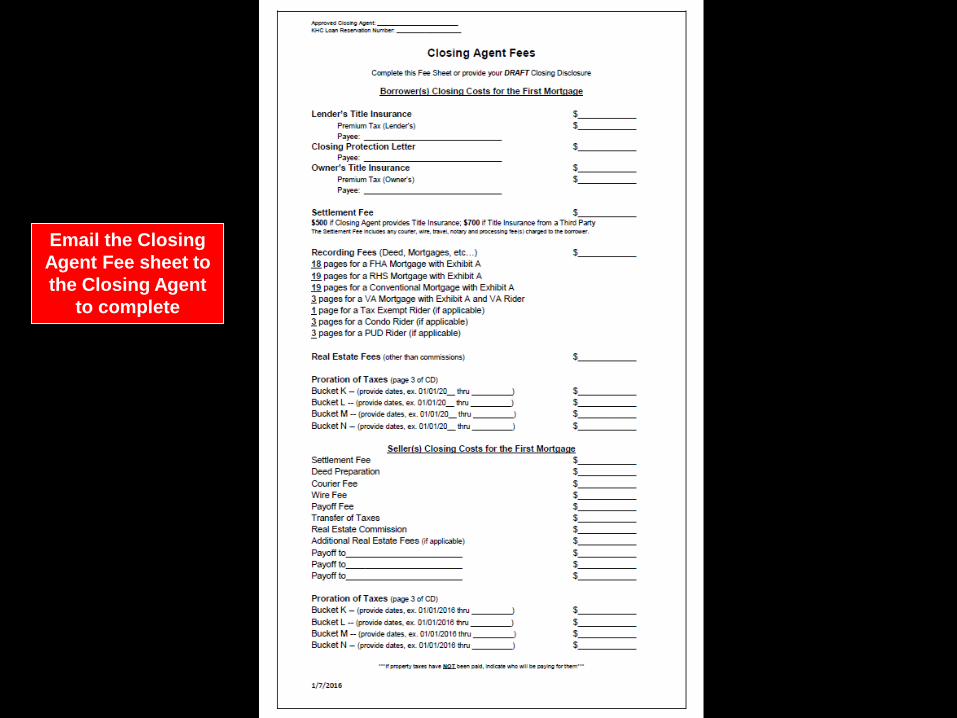

Fee Sheet and Closing Agent Fee Sheet .

Print from Document Printing with Commitment Letter.

Available on KHC’s website on Lender Resource page under TPO Lenders.

Need to upload completed versions along with pre-closing items listed on Fee Sheet when scheduling the closing.

Submit invoices for fees.

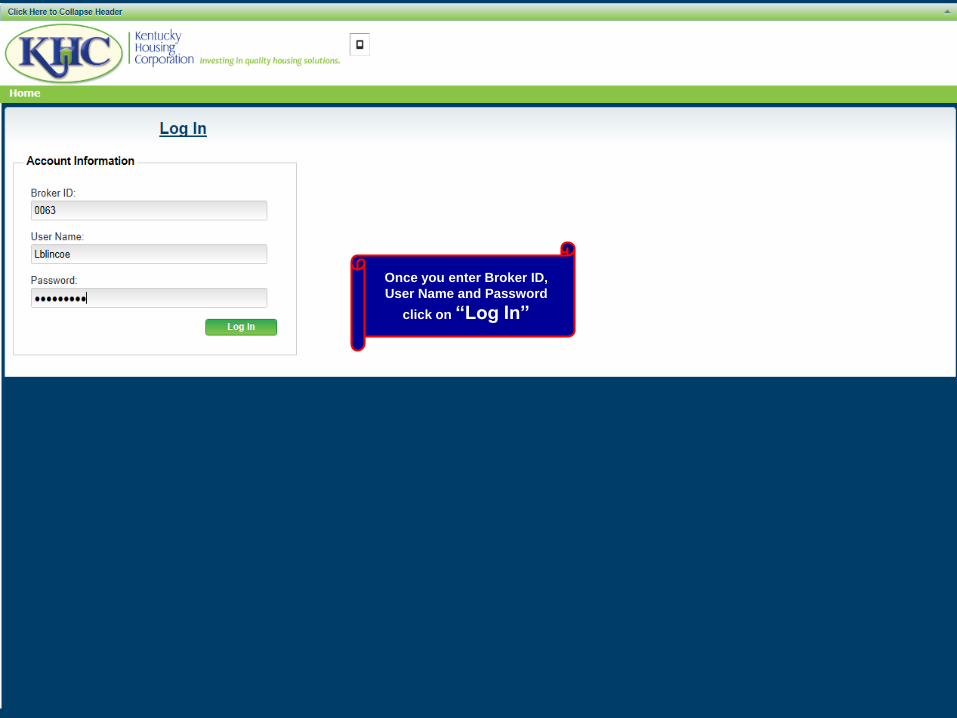

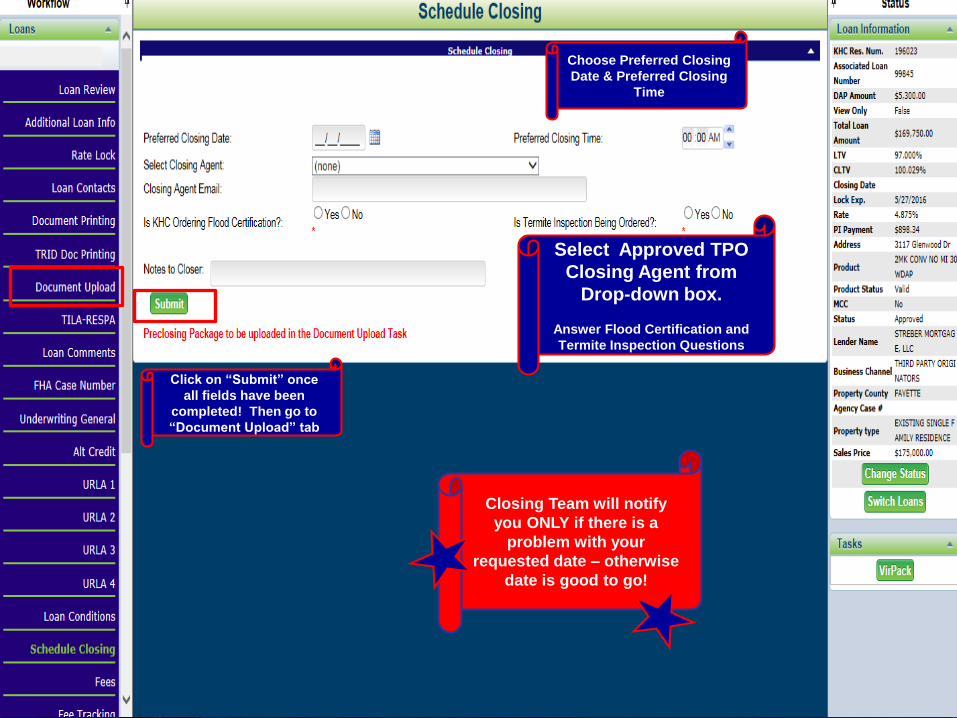

Once you enter Broker ID,

User Name and Password

click on “Log In”

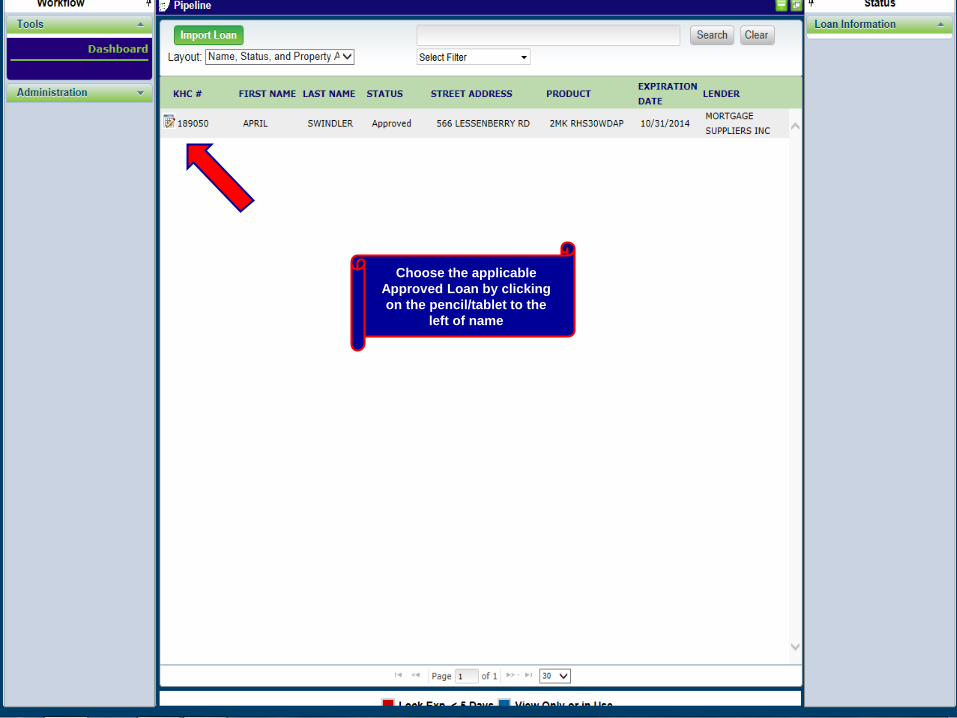

Choose the applicable

Approved Loan by clicking

on the pencil/tablet to the

left of name

Select Approved TPO

Closing Agent from

Drop-down box.

Answer Flood Certification and

Termite Inspection Questions

Choose Preferred Closing

Date & Preferred Closing

Time

Closing Team will notify

you ONLY if there is a

problem with your

requested date – otherwise

date is good to go!

Click on “Submit” once

all fields have been

completed! Then go to

“Document Upload” tab

TPO Pre-Closing Package

Upload ALL Pre-closing Items – this may include but not limited to:

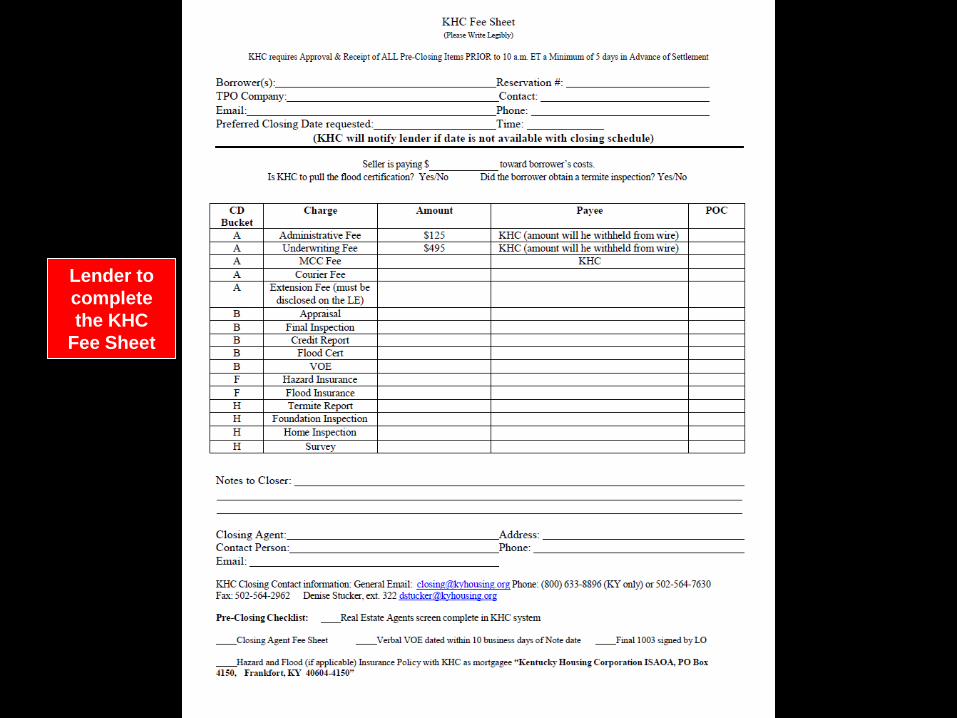

KHC Fee Sheet.

Closing Agent Fee Sheet.

Final 1003 signed by Loan Officer.

Underwriting Approval Conditions.

Final Inspection(s).

RHS Conditional Commitment.

Hazard Insurance with KHC as Mortgagee.

Title Commitment.

Verbal VOE dated within 10 business days of note date.

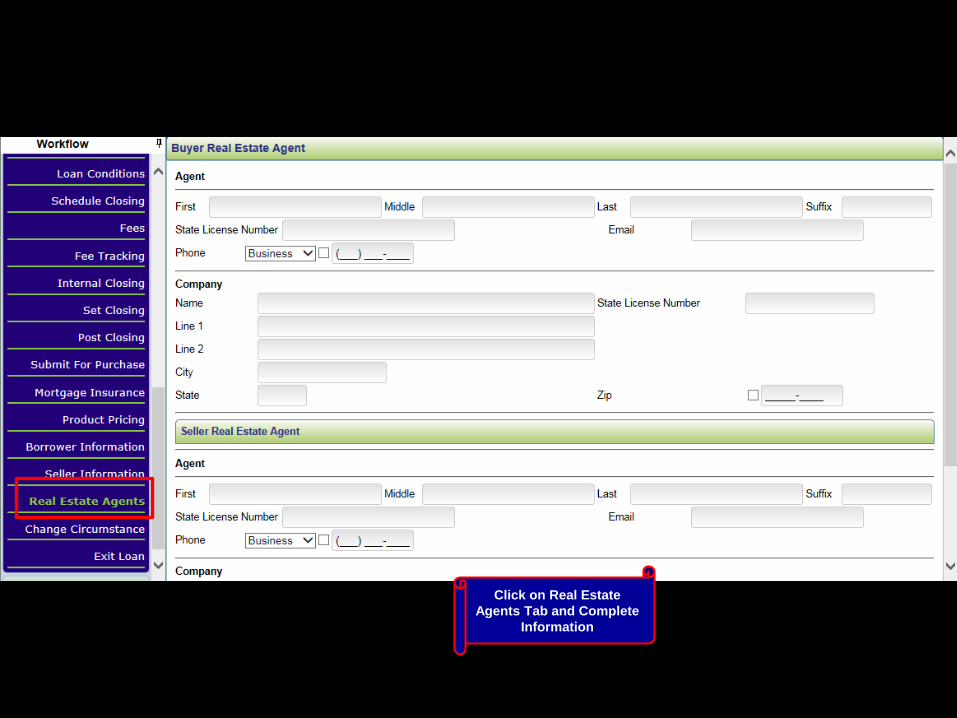

Click on Real Estate

Agents Tab and Complete

Information

Lender to

complete

the KHC

Fee Sheet

Email the Closing

Agent Fee sheet to

the Closing Agent

to complete

Choose TPO Pre-

closing Package

Select File and upload

“ONE PDF Bundle”

KHC Closing Team Workflow

Review all pre-closing items uploaded by Lender.

Email Lender changes that need to be made.

Email initial Closing Disclosure to Lender and Closing Agent for review.

Upon completion of revisions, a final version of the Initial CD will be emailed to Lender and Closing Agent.

Signed Initial CD is to be returned to KHC to ensure the 3 days delivery for TRID compliance.

Email Closing Package to the Closing Agent and request the funds for closing.

After the Loan Closes

Closing Agent will deliver Closed Loan Package along with Original First Mortgage Note and DAP Note to KHC.

Within 90 days KHC should receive the original recorded documents with final title policy.

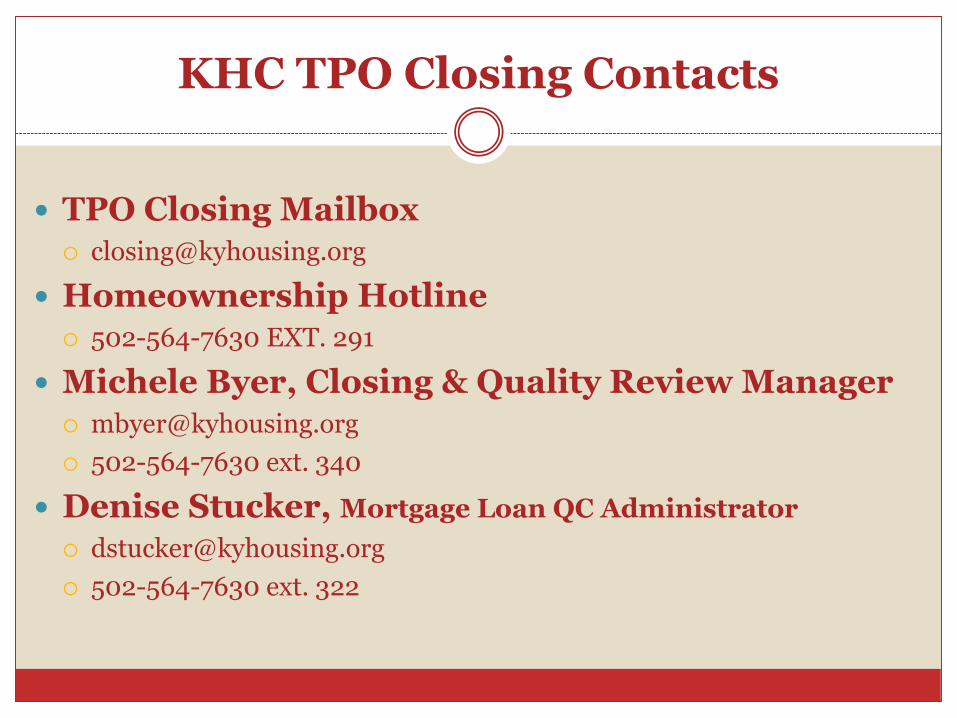

KHC TPO Closing Contacts

TPO Closing Mailbox [email protected]

Homeownership Hotline 502-564-7630 EXT. 291

Michele Byer, Closing & Quality Review Manager [email protected]

502-564-7630 ext. 340

Denise Stucker, Mortgage Loan QC Administrator

502-564-7630 ext. 322

KHC Contacts

KHC Underwriting Mailbox [email protected]

Homeownership Hotline 502-564-7630 EXT. 291

Jamie Swindler, Mortgage Production Administrator

502-564-7630 ext. 329

Cindy Bradley, Mortgage Production Administrator

502-564-7630 ext. 347

Thank You