35

VALUE SOURCING BV Hans Dijkhuis Maastricht, June 19, 2013 Ketensamenwerking in de bouw ASML: Samenwerken in de keten voor de klanten van de de semicon industrie

VALUE SOURCING BV

Hans Dijkhuis

Maastricht, June 19, 2013

Ketensamenwerking in de bouw

ASML: Samenwerken in de keten voor de klanten van de de semicon industrie

VALUE SOURCING BV Introduction:

Public

Slide 2

Creating customer value by suppliers

June 19, 2013

VALUE SOURCING BV

ASML: introduction in the semicon market

Meeting our customer’s requirements

How we got it done

Agenda June 19, 2013

Public

Slide 3

VALUE SOURCING BV ASML: leading manufacturer of chip-making equipment

Public

Slide 4

June 19, 2013

VALUE SOURCING BV ASML

Public

Slide 5

June 19, 2013

VALUE SOURCING BV ASML

Public

Slide 6

June 19, 2013

VALUE SOURCING BV This too is Moore’s law

June 19, 2013

Public

Slide 7

Note: data iSupply, March 2009. High quality Flash

VALUE SOURCING BV ASML:

Public

Slide 8

• One of the world’s leading manufacturers of chip-making equipment and a key supplier to the chip industry

• A global company founded in 1984, headquarters in Veldhoven, The Netherlands

• A public company traded on both Euronext Amsterdam and Nasdaq stock exchanges

FY2012:

Net sales: 4.732 M€

Net income: 1.146 M€

# of systems sold: 170

# of employees 8.497(FTE)

June 19, 2013

VALUE SOURCING BV Great Supply Chain Performance in bad times

Public

Slide 9

629 949 919

184

742

1452 1252

942

930 844

277

1069

1529

1228 958

934 697

555

1176

1459

1229 1053 955

919

581

1521

1211

1023

0

1000

2000

3000

4000

5000

6000

2006 2007 2008 2009 2010 2011 2012

3,582 3,768 3379

1,597

4,508

Q1

Q2

Q3

Q4

5.651

4.732

Net sa

les (

mill

ion

eu

ro)

• The entire ASML Supply Chain was

able to cope

• No business drop outs

• 2nd tier chain remained in tact

• The entire ASML Supply Chain

recovered timely

• 2010: Highest sales ever: 4.508 M€

• 2011: Exceeding 2010: 5.651 M€

• 2012: Higher than record year 2010:

4.732 M€

08Q4-09Q1: production: minus 85%

ASML buys 90% of production cost

Thanks to market robust suppliers!

M€

June 19, 2013

VALUE SOURCING BV Great Supply Chain Performance in bad times

Public

Slide 10

629 949 919

184

742

1452 1252

942

930 844

277

1069

1529

1228 958

934 697

555

1176

1459

1229 1053 955

919

581

1521

1211

1023

0

1000

2000

3000

4000

5000

6000

2006 2007 2008 2009 2010 2011 2012

3,582 3,768 3379

1,597

4,508

Q1

Q2

Q3

Q4

5.651

4.732

Net sa

les (

mill

ion

eu

ro)

• How did ASML achieve this ?

• What was the role of Procurement?

ASML Procurement

ASML buys 90% of production cost

Thanks to market robust suppliers!

M€

June 19, 2013

VALUE SOURCING BV

Public

Slide 11

1400

2600

1600

629 949 919

184

742

1452 1252

942

930 844

277

1069

1529

1228 958

934 697

555

1176

1459

1229 1053 955

919

581

1521

1211

1023

0

1000

2000

3000

4000

5000

6000

1999 2000 2001 2006 2007 2008 2009 2010 2011 2012

3,582 3,768 3379

1,597

4,508

Q1

Q2

Q3

Q4

Net sa

les (

mill

ion

eu

ro)

5.651

4.732

Great Supply Chain Performance in bad times thanks to lessons learned in 2001

June 19, 2013

VALUE SOURCING BV Bad times in 2001, great lessons:

Public

Slide 12

1400

2600

1600

0

1000

2000

3000

4000

5000

6000

1999 2000 2001

Net sa

les (

mill

ion

eu

ro)

March 2001: order board plunged

• Year 2k: Consumers bought electronics before y2000

• High Inventory at our customers: no additional capacity

• Order board: March 328 systems; Year end 168 of which 28

of March

• Sourcing value dropped by 50%

• Firm fixed orders for at least 1.5y

• 40% of total buy in radius of 40km

• ASML at many suppliers over 80% of T.O.

• Supply Base not prepared for this 38% market decrease

• Historically: continuous grow: 20-15% per year

• No flexibility in cost: direct hit in P&L: L

‒ No flex in 2nd tier supply chain

‒ No flex in manpower: fixed FTE, very limited temp.

June 19, 2013

VALUE SOURCING BV Such a market decrease might happen again!

Public

Slide 13

Source: IMF, VLSI research, Gartner

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

1985

1986

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

YoY

gro

wth

Gross Domestic Product

Electronics Revenue

IC Revenue

Lithography Revenue

June 19, 2013

VALUE SOURCING BV ASML is the supplier of the supplier of the supplier of

the customer Public

Slide 14

June 19, 2013

VALUE SOURCING BV

ASML: introduction in the semicon market

Meeting our customer’s requirements

How we got it done

Agenda June 19, 2013

Public

Slide 15

VALUE SOURCING BV ASML: Customer focused outsourcing:

Buying customer value, delivering supplier value Public

Slide 16

1. Clear on reasons for outsourcing

2. Customer requirements translated into long term supplier

performance

3. Integration of the supply chain in each phase of the life cycle

4. Relationship management

5. Contracting

6. Vendor rating

4. Sourcing is responsible for the cross functional sourcing function

5. Risk assessment on actual supplier performance

6. Continuously working with the supplier on improvements

1. Market investigation

2. Supply Base Development

3. Supplier development

6 Sourcing Core

Activities

June 19, 2013

VALUE SOURCING BV 1. Clear on reasons for outsourcing

ASML focuses on high value-added integration role • Total product competence

• Shorten cycle times

Subsystem suppliers have specialized competencies • More efficient and dedicated operations

• Focus on reducing cost, increasing capability and quality

Subsystem suppliers serve also other customers • Share and spread the risks of the market cycles

• Increased flexibility and competitive cost structure

Creating access to the best competencies available • Time to Market

• Most advanced technology

Public

Slide 17

June 19, 2013

VALUE SOURCING BV 2. Customer requirements translated into long term supplier

performance requirements

June 19, 2013

Public

Slide 18

>98 % Tool Availability

Focus on Sustainability

Towards 3 months

Customer Lead Time ASML

Relentless R&D Investment

Fast Time to Market

Adequate Cost Reduction

Creating Value-of-Ownership

Having a Functional, Reliable and

Sustainable Product

Coping with market cycles

Realizing the Semiconductor

Technology Roadmap

Being World Wide

competitive in all life cycles

ASML corporate strategy Customer Requirements

From Customer Market Requirements into Performance Criteria

VALUE SOURCING BV … leading to the ASML Supply Strategy ….

June 19, 2013

Public

Slide 19

>98 % Tool Availability

Focus on Sustainability

Towards 3 months

Customer Lead Time ASML

Relentless R&D Investment

Fast Time to Market

Adequate Cost Reduction

Creating Value-of-Ownership

ASML corporate strategy ASML Supply Strategy

The ASML Supplier accepts and adapts to the (changing)

ASML Customer requirements

Long Term supplier relationships, profitable over the ASML

market cycle and contributing to the Supplier’s business

strategy

QLTC Performance management in all phases of the life

cycle:

• integral and cross functional managed

• Continuously measured

• Continuously improved

World Wide competitiveness

VALUE SOURCING BV … thus resulting in ASML Supply Chain Performance

requirements:

June 19, 2013

Public

Slide 20

>98 % Tool Availability

Focus on Sustainability

Towards 3 months

Customer Lead Time ASML

Relentless R&D Investment

Fast Time to Market

Adequate Cost Reduction

Creating Value-of-Ownership

ASML corporate strategy ASML Supply Base strategy

Qualified Production Processes

Product (Design) Qualification

Short Lead Times

Capacity and Flexibilty

Advanced Technology

Efficient Operations

Integrated Supplier Network

Competive Pricing

Sharing Market Dynamics

in Risks and Rewards

Value Sourcing: managing Supplier Value

Quality – Logistics – Technology - total Cost

VALUE SOURCING BV Supplier Profile:

Measuring performance in each phase of the life cycle: QLTC

Public

Slide 21

Pre-Dev. R&D Engineering

Proto

Engineering Pilot

Ramp-Up Volume Service

Supplier Profile

Overall Vendor ratingSupplier name + number

M+W Products GmbH

1 2 3 4 5 Status

Material Quality Performance (MQP) - Q1 G

FSD's exclusive DOA’s / DOI’s - Q2 G

DOA and DOI Parts at End-ustomers - Q3

Complaint Handling - Q4

Warranty Claims - Q5

Introduction of new products - Q6

Process control of the production process - Q7 G

Version control and archiving - Q8

Supplier selection criteria throughout the supply chain - Q9

Environmental Performance - Q10

Health & Safety Performance - Q11

Corporate Social Responsibility (CSR) - Q12

Quality performance of 2nd tier - Q13

Customer focus and craftsmanship - Q14

To be made specific if relevant - Q15

Order fulfilment flexibility & Delivery reliability - L1 G

Material Availability & Stock Out Ratio - L2

Just In Time replenishment - L3

Authorized Replenishment Call - L4

Order Time - L5

Repair Cycle Time performance - L6 G

Order management - L7

Flexibility Requirement - L8

Proto Flexibility - L9

Cycle Time performance - L10

Process Control: ERP-system - L11

Logistic performance of 2nd tier - L12

Customer focus and craftsmanship - L13

To be made specific if relevant - L14

Structured product development - T1

Structured production process technology development - T2

Structured product- and production design process -T3

Generic Design competence - T4

Specific Design competence -T5

Investments on development -T6

Continuous learning organization for NPI product development -T7

Continuous learning organization for NPI production process tech development - T8

Continuous learning organization for Product defects - T9

Technical Support during total product lifecycle - T10

Early manufacturing / engineering involvement - T11 G

Engineering Change (EC) Management and configuration management - T12 G

Supplier’s product and production process technology roadmap alignment -T13

Cleanliness Control - T14

Technology performance of 2nd tier - T15

Customer focus and craftsmanship - T16

To be made specific if relevant - T17

Market Conformity (PP3) - C1

Open costing - C2

total Cost Reduction Programs - C3

Customer portfolio - C4

Market portfolio - C5

Payment Terms - C6

Warranty according to ASML Customer expectation - C7

Lean maturity level - C8

total Cost performance of 2nd tier - C9

Customer focus and craftsmanship - C10

To be made specific if relevant - C11

Definition action status:

Actual matches Requirement (or better)

Action according to plan Legend Vendor rating:

Action not according to plan; corrective actions started, confidence in rehabilitation 95.0% 87.5% 75.0% 50.0% < 50%

Gap identified, agreed low priority, no plan yet A B C D E

Action not according to plan; no confidence in realization

V 7.1 - Company Secret - page 1 of 1

(1) SoW is UCC> done > SOW signed off 11wk11 (2) EPS UPW mk3 needs to be frozen and accepted 11wk16.3; EPS is frozen at M+W, Arjan needs to confirm week 11.17, final check by M+W week 11.18 (done ?)(3) 3D Drawing shared (Jens Done)(4) HerH will check current status EPS

Integrate in IP/EC Bridging project. Jens to give input to Thomas. Show plan in SATmeeting 11wk17.4: Plan in place; target implementation August 2011(2) Monitor till end UPW NTX mk3 project (Q4 2011)

Organizational change has been implemented , includes extension of team; results in more and better focus on the repair handling. Additional actions implemented to speed-up Cycle Time. Improvements already visible (july performance) Back on target in Q3/Q4 2011

Rootcause analysis done. Repairs mainly cause for decreased performance. Increased performance Q4 2011 visible.

A

Agreed improvement projects

Align or work towards X ≤ 1% using SMART ** action and proposed enddate ** use template in this profileUpdate action plan before next SAT meeting 11wk36 (TWOE)

Analysis report expected 11wk15.5 A.Gross (done); review data together and draw up conclusion, HerH, week 19 (done); discuss with ASML CS-EE, HerH, week 20 (done), IP has been rejected

(1) Align or work towards Target of 98% using SMART action, plan to be delivered on 11wk16.3 (done)(2) Update on UPW and ACC (11wk30 TWOE)

tota

l C

ost

B

B

A

Q

ua

lity

L

og

isti

cs

T

ec

hn

olo

gy

ARevision Date:

1001008 06 Sep 2011

actual required

Supplier XYZ

Quality

Logistics

Technology

Total Cost

Quality

Logistics

Technology

Total Cost

June 19, 2013

VALUE SOURCING BV ASML: Customer focused outsourcing:

Buying customer value, delivering supplier value Public

Slide 22

1. Clear on reasons for outsourcing

2. Customer requirements translated into long term supplier

performance

3. Integration of the supply chain in each phase of the life cycle

4. Relationship management

5. Contracting

6. Vendor rating

4. Sourcing is responsible for the cross functional sourcing function

5. Risk assessment on actual supplier performance

6. Continuously working with the supplier on improvements

1. Market investigation

2. Supply Base Development

3. Supplier development

June 19, 2013

VALUE SOURCING BV 3. Integration of the supply chain in each phase of the life

cycle

Public

Slide 23

At ASML, the pace of Innovation prevents switching to other suppliers

Supplier Selection and Contracting are crucial for success

New Product Development

Pre-Dev. R&D Engineering

Proto

Engineering Pilot

Ramp-Up Volume Service

Sustaining

Feasibility

Agreement on PERFORMANCE: the supplier as Engineer, the supplier as manufacturer for many years. Long Term Supply Agreement

Supplier: fit for the entire product life cycle: >15 years

June 19, 2013

VALUE SOURCING BV Why would a Supplier chose such customer?

Public

Slide 24

What is the Value for having such a Customer?

Product delivery

Product related Services

Business related Services

Payment at lowest ASML Total cost:

Paying in Euro’s: cash out

&

Paying in perceived value by the supplier

Supplier Delivery Supplier

Delivery Supplier Delivery

VALUE

VALUE

VALUE VALUE VALUE € Supplier

Delivery

Strategic alignment between

Supplier Business Strategy and Supply Base Strategy

June 19, 2013

t

VALUE SOURCING BV Cross functional Supply Management

Public

Slide 25

Supplier strategy

Supplier strategy

Preferred Supplier Strategy

ASML Technology Road map

ASML Customer and

supplier market

characteristics

ASML Strategy

Part category

Part category

Preferred Supply Base

per Part category

SPFT SPFT SPFT SPFT SPFT SAT SAT SAT

Yearly Risk Assessment

57 Supplier Account Teams

197 representatives from our suppliers

148 representatives from ASML

487 QLTC improvement programs:

Q: 160 L: 143 T: 111 C: 73

9 Strategic Product Family Teams

Internal ASML: D&E, IE, F, Sales, Q., L, Manu,

Sourcing

104 Supply Base improvement programs:

June 19, 2013

VALUE SOURCING BV Supply Risk:

June 19, 2013

Public

Slide 26

1. Does the product or service we’d

like to outsource effect our

competitiveness?

2. Is there a QLTC competitive supply

base where these specific products

or services can be bought?

3. Won’t ASML become too dependent

of this supplier?

Yes: Do it yourself

No: Consider outsourcing

No: Do it yourself

Yes: Consider outsourcing

No: take the risk

Assess risk and mitigate

Make- Buy Board

Product Family Team

Supplier Account Team

Mitigation by x-functional teams

VALUE SOURCING BV Make-Buy is not always obvious

June 19, 2013

Public

Slide 27

• ASML is the only source with sufficient competence on this activity • Knowledge (IP) or competence for this activity may not be leaked to customer or

competition • ASML cannot ensure future control over litho roadmap (technology performance),

ramp-up/ramp-down capabilities, service-levels towards customers, cost levels • ASML cannot get legal agreements in place to control margins/IP/Logistics (LTA)

and on SLA • Activity requires customer contact and this might endanger ASML control towards

customer on service-levels (uptime)/pricing/image • Activity is perceived by customer as core activity for ASML Outsourcing would

reduce image and market position • Requirement definition is not possible (complex interfacing) • Supplier is not able to cope with semicon market demands regarding ramp-

up/ramp down • ASML is able to develop, manufacture or integrate at lower total cost (including QLT

requirements) over the market cycle (price, investment, factory cost, ramp up/down)

• Financial impact of outsourcing would not be beneficial for ASML: largest part of earnings over the market cycle should be retained at ASML

• ASML might lose critical mass of competences and skills needed for tool integration development and manufacturing

• To build competence to increase VoO (uptime, wph, etc.) at customer • Foreseen risk mitigation of QLTC performance is not acceptable for ASML • Performing the activity at ASML generates competence needed for a roadmap on

beyond-Litho markets • There is no profitable business case for the supplier

Why developing or manufacturing yourself? Why being forced to buy? • The Supplier is the only source with sufficient competence

on this activity in order to execute ASML’s technology roadmap within required Time to Market

• The Supplier owns required development-IP and does not allow ASML using it.

• The Supplier is able to develop, manufacture or integrate at lower total cost over the market cycle ( price, investment, factory cost, ramp up/down) because the supplier:

• Is specialist on the specific competence and therefore more efficient

• Is vertically integrated and/or serves other product-markets to leverage and develop the activity

• ASML financial risk exposure is unacceptable: large investments should be spread over several suppliers, reducing risk for ASML over the market cycle (including infrastructure investments, WIP investments and risks for push-out and obsolescence)

• Combined development & manufacturing activity at supplier is needed to yield best performance on design for manufacturability, service-ability and total cost

• Supplier has more knowledge and better access to lower tier competencies and supply chain

VALUE SOURCING BV Yearly Risk Assessment: Facts on Acts & Act on Facts

- Company Secret -

Company Profile 0Revision Date

Supplier Number CEO Mobile phone

SAT Chairman Plant Manager Mobile phone

LTA signed 0 Expiration date 0 Account Manager Mobile phone

NDA signed 0 Expiration date 0 Part of Holding 0 Name holding

SPFT SPFT co-Chairmen Proc DEV

SAT Members: Applicable Sourcing models

Q

L

T

C

Financial & performance data*

Total net sales holding (Meur)

Total ASML net sales Holding (Meur)

Total net profit holding (Meur)

Number of Employees holding

Dependency holding on ASML (%)

Dependency holding on Semicon Market (%)

Total net sales supplier (Meur)

ASML net sales supplier (Meur)

Accounts Receivable (Meur)

Equity supplier (Meur)

Total Liability and Equity (Meur)

Interest supplier (Meur)

Total net profit supplier (Meur)

Number of Employees supplier

Solvability supplier

Interest coverage supplier

Days Sales Outstanding (DSO)

Financial Z-score supplier

Supplier’s dependency on ASML

Net sales supplier per employee (Keur)

Vendor rating supplier (end of every year)

Remarks:

Main ASML products at supplier (P latform): Pred.**

Markets (%) 2010 2011 est. 2011 est.

Medical 0% #DIV/0! #DIV/0!

Competitors of supplier: Defense 0% #DIV/0! #DIV/0!

Aerospace 0% #DIV/0! #DIV/0!

Automotive 0% #DIV/0! #DIV/0!

Top-5 Customers Supplier (% of net sales): Semicon 0% #DIV/0! #DIV/0!

Engineering 0% #DIV/0! #DIV/0!

Energy 0% #DIV/0! #DIV/0!

Top-5 Customers Holding (% of net sales): Others 0% #DIV/0! #DIV/0!

Total 0% #DIV/0! #DIV/0!

Turnover 2011 (Supplier est. base 2010) 0%

Platform Turnover (Meur) 2008 2009 2010 est. 2011 est. 2012 est. Turnover 2011 (ASML est. base 2010) 0%

XT 0 0 0 0 0 These estimates are on Supplier level

NXT 0 0 0 0 0

NXE 0 0 0 0 0

Others (e.g. D&E, service) 0 0 0 0 0

Total 0 0 0 0 0

Supplier risk overview Position ASML in supplier customer portfolio Virtual integration level

Leverage Strategic Exploitable Core Unique Dual

€ € With transparency

Routine Bottelneck Nuisance Development Single Dual

Without transparency

Risk Attractiveness Single sourced Dual Sourced

Supplier

Holding*

* Holding data in case applicable

** Calcution based on ASML market development expectations V 3.06

0.0

0.0

0.0%

0

0.0

0.0 0.0 0.0

0.0

0.0

0.0 0.0

0% 0%

0.0

0.0%0.0%

Supplier

0

0

0

0.0

0.0

0.0

0.0 0.0 0.0

0.0 0.0

0.0%

0% 0%

0.0 0.0

0.0 0.00.0

0.0 0.0 0.0

2011 est.

0.0

2012 est.

0.0

0.0

0.0

0.0

0%

0.0

0

0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0 0

0.0

0.0

0.0%

2009

0.0

0

0

2010

Supplier

0.0

0 0

0.0

0

0

0

2008

0

0

0

ASML

0

0

0.0

0.0

0.0

0.0

0.0

0.0

0 0

Vir

tual in

tegra

tion

Product 1 (XT/NXT), Product 2 (EUV)

Competitor 1, Competitor 2

Customer 1 (30%), Customer 2 (15%), etc.

Customer 1 (30%), Customer 2 (15%), etc.

0

0

0.0

0.0

0

0

0

0

00 0

0.0

Overall Risk status Timing all Risk mitigated Legend overall risk status:

Risk mitigation in place H2.2013 At Risk

Risk mitigation in place

Risk Contained

No Risk

0.0

2.0

4.0

6.0

8.0

10.0Dependency

Technology Ownership

Virtual Integration level

Strategic Alignment

Transfer barriers

2nd tier ManagementMaterial availability service parts

Sustainability

Financial

Disaster Contingency plans

Flexibility

Risk Identification Risk Threshold

Long term riskShort term risk

Performance risk

Mover Rate risk

Public

Slide 28

June 19, 2013

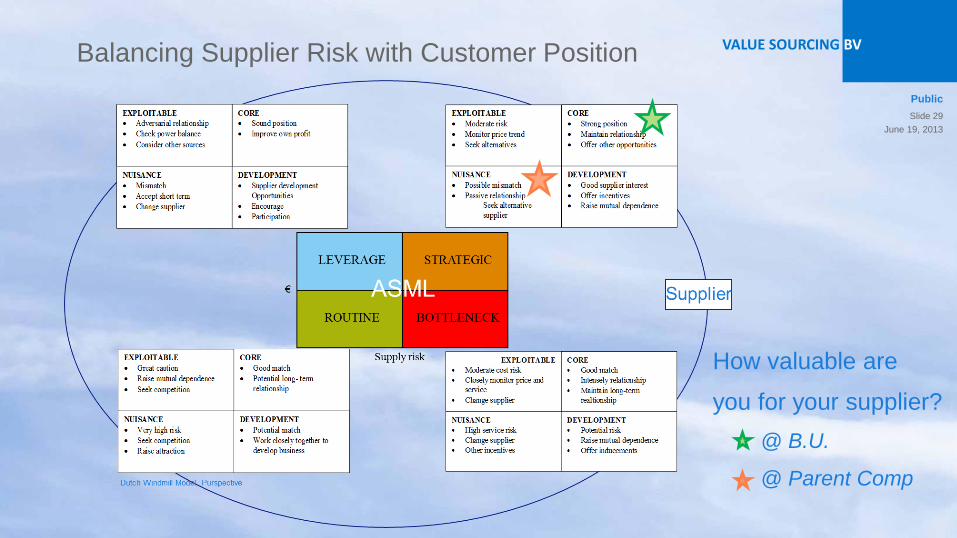

VALUE SOURCING BV Balancing Supplier Risk with Customer Position

Public

Slide 29

How valuable are

you for your supplier?

@ B.U.

@ Parent Comp

June 19, 2013

VALUE SOURCING BV

ASML: introduction in the semicon market

Meeting our customer’s requirements

How we got it done

Agenda June 19, 2013

Public

Slide 30

VALUE SOURCING BV Getting started: well organized, great expectation

June 19, 2013

Public

Slide 31 a route, a goal A team,

We started in 2002

VALUE SOURCING BV

June 19, 2013

Public

Slide 32

But our way to success was painful, and at dear cost

VALUE SOURCING BV

June 19, 2013

Public

Slide 33

Did we organize it?

Did we create the infrastructure?

Did we provide the necessities?

We had to steer on fit!

a route, a goal A team,

Content Fit Organizational Fit People Fit

Steering

culture fit

Is it clear what to

do, where to go

and when to

arrive?

Can I do it and

do I want it?

Am I willing to

pay the prize?

Why? We were not fit enough!

VALUE SOURCING BV Summary Lessons Learned ASML

June 19, 2013

Public

Slide 34

• Translate the customer’s expectation into measurable supplier performance criteria. QLTC supply base and supplier strategies

• What performance requires the customer, the internal organization? • Know what you need, know what you’re buying!

• Be part of the supplier’s future, as they are yours. • What’s your value now, will you remain valuable?

• Everyone who works with suppliers is part of the Procurement Function

• Actively involve your colleagues into the Procurement Function • Manage corrective action plans. • Integrity, ethics and respect are the foundation for trust.

Co

nte

nt

Org

an

iza

tio

n

Pe

op

le

• Organize for long term suppliers relations: improve QLTC in stead of relocate.

• Measure performance, report structurally • Provide a future for your people

March 21, 2013

Public Slide 35