22

Sector Outlook: How Will Mexico’s Industries Fare in the Global Recovery? Mark Killion, CFA Managing Director, World Industry Group IHS Global Insight July 21, 2010

| Date post: | 21-Feb-2017 |

| Category: |

Documents |

| Upload: | mark-killion-cfa |

| View: | 67 times |

| Download: | 1 times |

Sector Outlook: How Will Mexico’s Industries Fare in the Global Recovery?

Mark Killion, CFAManaging Director, World Industry Group IHS Global Insight

July 21, 2010

Copyright © 2009 IHS Global Insight. All Rights Reserved.2

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Outline of Presentation

• Themes Shaping the Outlook for Industries

• Rank Sectors by Their Growth Outlooks• Mexico, U.S, and World

• Industry Impact in Mexico from Exports, Competitiveness

• Global Industry Growth Forecast for Key Countries:• Electronics and Automotive, Aircraft and Shipbuilding• Energy and Metals• Construction and Related Materials, Wood, Paper, Chemicals• Retail, Tourism and Leisure, Consumer Staples• Telecommunications and Utilities• Financials and Real Estate, Business and IT Services• Public Administration, Defense and Education

Copyright © 2009 IHS Global Insight. All Rights Reserved.3

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-12

-7

-2

3

8

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Construction Manufacturing Services

-12

-7

-2

3

8

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

World TotalMexico

Delve into the Supply Side of Macro Economic GrowthAnnual Growth Rate of Inflation Adjusted Value Added

Copyright © 2009 IHS Global Insight. All Rights Reserved.4

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Key Factors Affecting Pace of Sector Recovery

ü “De-synchronization”, Uneven Pace of Growth Across Countries & Industries:Ø Emerging Asia outpacing rest of globe, Latin America faring well Ø Europe faces slow growth due to fiscal drag and Euro zone issues

Ø The United States is in between… a vibrant technology sector and resurgent industry is leading a recovery, but deteriorating public finances, credit-restrained private sector and a further de-leveraging of the household and financial sectors are a drag on growth

Ø Growth rates of “domestic” sectors reflect the country-based patterns… such as in Construction, Real Estate and Consumer oriented industries

ü Balance sheet repair continues to reverberate in, and from, the financial sectorü Manufacturing Rebound Began in late 2009 but has slowed in recent months

Ø Huge adjustment to the previously sharp declines: Commodities, Metals, AutosØ Electronics and Technology are leading drivers for growth

ü Impact from injections and withdrawals of economic stimulus programs

ü Roll out of infrastructure in emerging market countries such as in Transportation, Communications and Utilities

Copyright © 2009 IHS Global Insight. All Rights Reserved.5

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Ranking of Sectors by Their Growth Outlooks

Copyright © 2009 IHS Global Insight. All Rights Reserved.6

Copyright © 2009 IHS Global Insight. All Rights Reserved.

-8

-4

0

4

8

12

16

20

Oil &

Gas

Indu

stry

Met

als

&M

inin

gFo

od &

Beve

rage

Che

mic

als

Indu

stria

lM

achi

nery

Auto

s

Airc

raft

Elec

troni

cs

Con

stru

ctio

n

Tran

spor

tatio

nSe

rv.

Bank

ing

&Fi

nanc

e

Bus

Serv

ices

Publ

ic A

dmin

. &

Def

ense

2010 2011 2012

Sales Growth in Mexico for Key Sectors

Sector Sales Growth (Inflation Adjusted), Mexico

37.3

Copyright © 2009 IHS Global Insight. All Rights Reserved.7

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Profile of Mexico’s Export Sectors

5

23

4

16

13

10

2

97

16

21 20

3

12

3

1617 17

0

5

10

15

20

25

Agriculture EnergyMining

Textiles &Apparel

IndustrialMachinery

&Appliances

Electronics MotorVehicles &

Parts

1990 2000 2009

Distribution of Mexico’s Merchandise (Goods) Exports 2009

Others7%

Textiles & Apparel

3%

Agriculture3% Energy

Mining12%

Metal Mining1%Food,

Beverages & Tobacco

4%

Printing & Publishing

3%

Mineral-based

Products1%

Chemicals5%

Basic & Fabricated

Metals7%

Machinery, Equipment, Appliances

9%

Electrical Industries

28%

Motor Vehicles &

Parts17%

Evolution of Sector Shares of Mexico’s Exports from 1990, 2000 and 2009

Copyright © 2009 IHS Global Insight. All Rights Reserved.8

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Profile of Industry Competitiveness in Mexico: Industry Winners

Comparative Advantage IndexShare in “All

Goods” ExportsAverage Value of Comparative

Advantage IndexIndustries are ranked by CAI *

(First is the Highest CAI) 1990 20091990-2000

2000-2006

2007-2009

Recent Change

1.Semiconductors, Circuit Boards, LCD 4.1 9.1 3.11 2.56 2.612. Beverages 0.8 1.2 1.59 2.01 2.123. Electric Industrial Machinery 3.7 4.0 1.98 1.88 1.944. Motor Vehicles and Parts 9.3 17.5 1.81 1.98 1.995. Machinery for Mining & Construction 1.0 1.4 2.44 2.90 2.696. Furniture 1.2 1.7 2.06 2.38 1.887. Receivers, Players, Sound, Systems, Transmitters, Routers, Telephony 2.5 8.1 1.39 1.20 1.678. Medical & Measuring Equipment 1.3 3.8 1.38 1.55 1.689. Domestic Appliances 0.8 1.7 1.19 1.28 1.5910. Medical, Precision and Optical 1.5 4.2 1.08 1.22 1.4

* Comparative Advantage Index: (Value of Mexico exports of good i divided by value of exports of All Mexico goods) / (Value of World exports of good i divided by value of exports of All World goods)

Copyright © 2009 IHS Global Insight. All Rights Reserved.9

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Comparative Advantage Index Share in “All Goods” Exports

Average Value of Comparative Advantage Index

Industries are Ranked by CAI *(First is the Lowest CAI) 1990 2009 1990-

20002000-2006

2006-2009

Recent Change

1. Shipbuilding 0.1 0.1 0.04 0.05 0.072. Aircraft and Spacecraft 0.1 0.2 0.05 0.03 0.093. Wood Products (Excl. Furniture), Paper and Pulp 0.8 0.6 0.26 0.27 0.28

4. Pharma: Drugs and Medicines 0.3 0.6 0.24 0.23 0.195. Basic Chemicals and Fertilizers 2.4 1.4 0.45 0.35 0.396. Specialty Chemicals (excl. Pharma) 1.8 2.5 0.49 0.46 0.517. Food Products 2.7 1.9 0.44 0.41 0.478. Textiles 1.0 0.7 0.58 0.62 0.559. Mineral-based Products (excl. Glass) 0.6 0.5 0.69 0.72 0.6010. Basic Metals and Fabricated Metals 6.2 5.9 0.7 0.7 0.68

Profile of Industry Competitiveness in Mexico: Industry Losers

* Comparative Advantage Index: (Value of Mexico exports of good i divided by value of exports of All Mexico goods) / (Value of World exports of good i divided by value of exports of All World goods)

Copyright © 2009 IHS Global Insight. All Rights Reserved.10

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Electronics & Automotives

0

5

10

15

20

25

Chi

na

Taiw

an

Japa

n

U.S

.

Indi

a

Mex

ico

Indo

nesi

a

S. K

orea

M. E

ast

Mal

aysi

a

Thai

land

Bra

zil

Rus

sia

Aus

tral

ia

Afr

ica

EM

U

Wor

ld

Computers & Communication Electronics Motor Vehicles

Forecast Growth in Real Sales (2010–11 CAGR) ü Autos growth rebounding in US,

Japan and Russia but output remains below pre-recession highs

ü Chinese autos growth set to decelerate in 2011-2012 after withdrawal of stimulus and incentives

ü Electronics recovery is more widely dispersed and fundamentally based

ü Technology and electronics have already regained most of their former high water marks

ü Strong connection with Software and Communications sectors

ü Mexico achieved recent gains in comparative advantage in Electronics and Autos, stemming a long decline

Copyright © 2009 IHS Global Insight. All Rights Reserved.11

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Aircraft and Shipbuilding

0

2

4

6

8

10

12

Indi

a

Chi

naTh

aila

ndTa

iwan

Bra

zil

S. K

orea

Mal

aysi

aM

exic

oIn

done

sia

Sin

gapo

reR

ussi

aE

MU

M. E

ast

Aus

tral

iaJa

pan

Afr

ica

U.S

.

Wor

ld

Aicraft & Spacecraft Shipbuilding

Forecast Growth in Real Sales (2010–11 CAGR) ü Airlines in the U.S. and Europe remain

cautious about purchasing aircraft but by 2011 many aircraft orders are scheduled to be delivered

ü The global shipbuilding industry remains supported mainly by order backlogs. IN 2009 the number of vessels delivered was the highest ever

ü Ship deliveries should now progressively decline in the years ahead and ordering this year is expected to remain rather depressed

ü Asian shipyards will again experience the highest growth in 2010–2011, but players in Brazil and the Middle East are making their way to the top in the performers’ list, because of proximity to local sources of demand (particularly in the energy and metals sectors)

Copyright © 2009 IHS Global Insight. All Rights Reserved.12

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Energy and Metals Complex

0

2

4

6

8

10

12

14

16

Chi

naIn

dia

Thai

land

Bra

zil

Taiw

anA

ustr

alia

Mal

aysi

aIn

done

sia

Kor

eaA

fric

a

Japa

nM

. Eas

tR

ussi

aU

SE

MU

Mex

ico

Wor

ld

Energy Complex Metals & Related Mining

Forecast Growth in Real Sales (2010–11 CAGR) ü World oil demand is growing again after

the 2008–09 pullback, but upside is limited… and the downstream oil sector remains bogged down by overcapacity, especially in the OECD markets

ü Scrutiny of industry operational and safety practices and the industry costs to find and develop new oil and gas will increase due in part to the deepwater well blowout in the Gulf of Mexico

ü The Metals complex has bounced back from steep production cuts and de stocking in 2008–09 to lead economic growth rates

ü High growth is being seen in Mexico’s Metals sectors. For example Grupo Mexico plans to double capacity over the next two years after a 3-year strike

Copyright © 2009 IHS Global Insight. All Rights Reserved.13

Copyright © 2009 IHS Global Insight. All Rights Reserved.

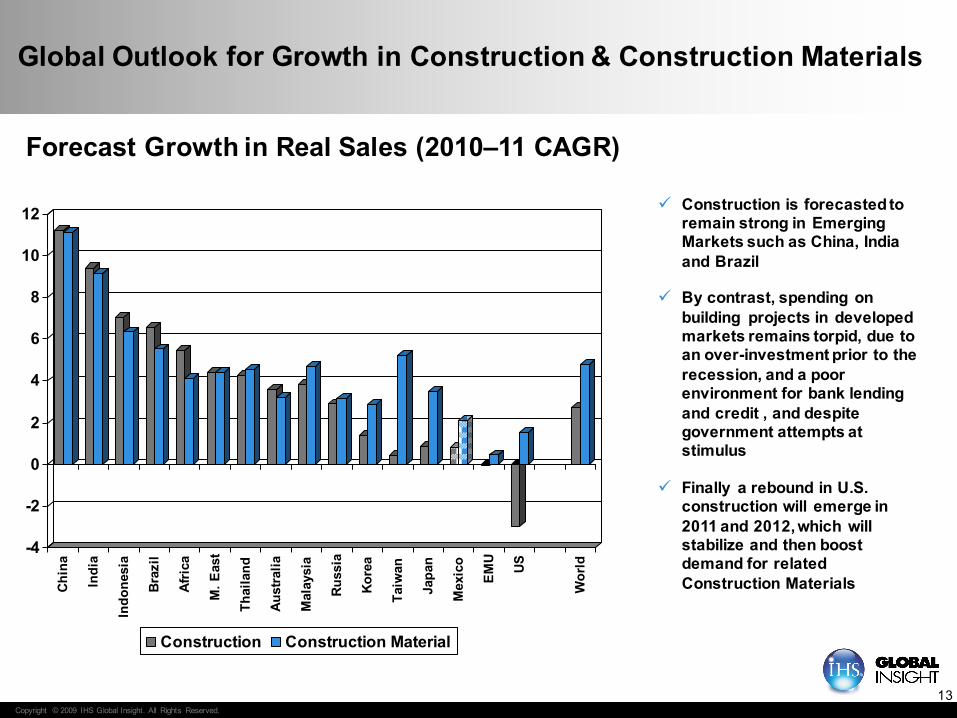

Global Outlook for Growth in Construction & Construction Materials

-4

-2

0

2

4

6

8

10

12

Chin

a

Indi

a

Indo

nesi

a

Braz

il

Afric

a

M. E

ast

Thai

land

Aust

ralia

Mal

aysi

a

Russ

ia

Kore

a

Taiw

an

Japa

n

Mex

ico

EMU

US

Wor

ld

Construction Construction Material

Forecast Growth in Real Sales (2010–11 CAGR)

ü Construction is forecasted to remain strong in Emerging Markets such as China, India and Brazil

ü By contrast, spending on building projects in developed markets remains torpid, due to an over-investment prior to the recession, and a poor environment for bank lending and credit , and despite government attempts at stimulus

ü Finally a rebound in U.S. construction will emerge in 2011 and 2012, which will stabilize and then boost demand for related Construction Materials

Copyright © 2009 IHS Global Insight. All Rights Reserved.14

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Wood & Paper Industries

-2

0

2

4

6

8

10

12

14

Chi

na

Indi

a

Indo

nesi

a

Mal

aysi

a

US

M. E

ast

Thai

land

Taiw

an

Bra

zil

Japa

n

Rus

sia

Afr

ica

Kor

ea

Aus

tral

ia

EM

U

Mex

ico

Wor

ld

Wood Products Paper & Pulp

Forecast Growth in Real Sales (2010–11 CAGR) ü The global outlook for the wood

and paper industry is turning positive

ü Demand in the Far East, especially China, recovered well in late 2009, driving global growth in the paper industry

ü However, the trend is clearly downward over the long term due to expectations of high energy and transportation costs and advanced the usage of electronic communication

ü The Wood industry follows closely activity in construction and so is lagging the economic recovery, will remain flat in 2010, but see 4–5% growth by 2011–12

Copyright © 2009 IHS Global Insight. All Rights Reserved.15

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Chemicals

0

2

4

6

8

10

12

Chin

a

Indi

a

Japa

n

Mal

aysi

a

Thai

land

Taiw

an

Indo

nesi

a

Kore

a US

M. E

ast

Braz

il

Afric

a

Mex

ico

Russ

ia

EMU

Aust

ralia

Wor

ld

Basic Chemicals Specialty Chemicals excl. Pharma

Forecast Growth in Real Sales (2010–11 CAGR) ü Growth in Chemicals output

should outperform the overall economy in countries such as the U.S. and Japan

ü Emerging markets will drive the global trend as manufacturers expand production to meet local sources of demand

ü Growth is boosted in developed markets by manufacturers rebuilding inventories, after depleting stocks in the recession

ü Poor performance in U.S. construction and consumer segments will mute sales of specialty chemicals

Copyright © 2009 IHS Global Insight. All Rights Reserved.16

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Telecommunications & Utilities

0

2

4

6

8

10

12

14

16

Ind

ones

ia

Chi

na

Ind

ia

Bra

zil

Mex

ico

M. E

ast

Taiw

an U.S

.

Mal

aysi

a

Rus

sia

Aus

tral

ia

Thai

land

Afr

ica

S. K

orea

Japa

n

EM

U

Wor

ld

Telecommunications Utilities

Forecast Growth in Real Sales (2010–11 CAGR) ü Telecoms and Utilities will benefit

from one of the major themes in emerging markets—increases in infrastructure spending

ü Developing economies will witness the strongest growth in telecom sales due to their lower saturation rates and faster macro economic growth

ü Telecoms infrastructure is increasingly focused on wireless

ü Utilities sales will rebound in 2010–11, led by strong demand growth from both the industrial sectors

ü Capacity additions should generally lead sales in Europe and North America, and continue to be focused on renewables, gas-fired and nuclear generation

Copyright © 2009 IHS Global Insight. All Rights Reserved.17

Copyright © 2009 IHS Global Insight. All Rights Reserved.

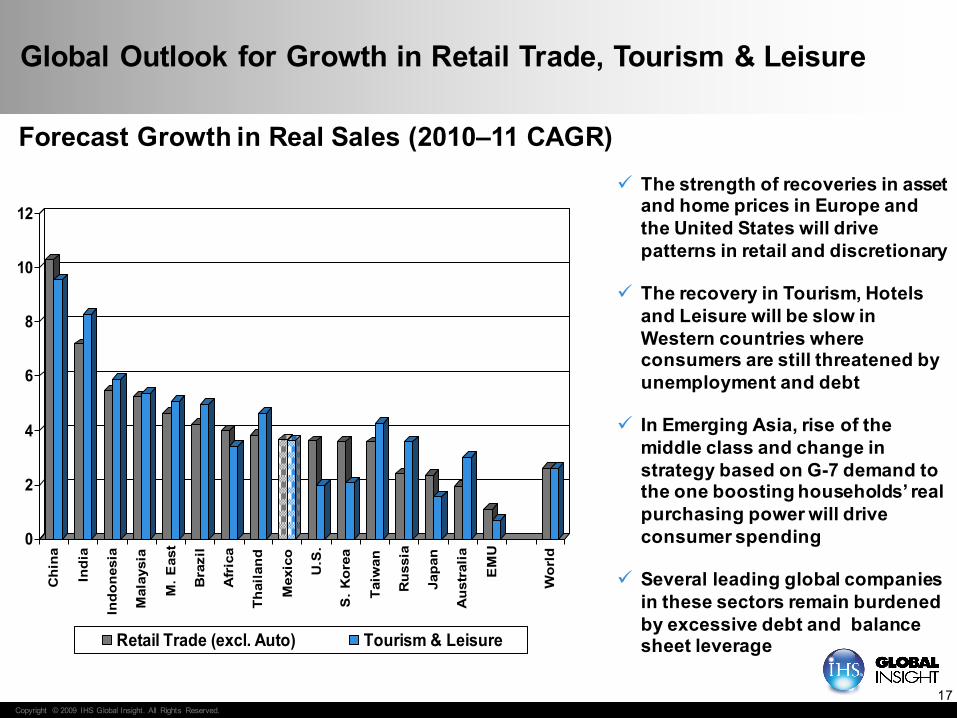

Global Outlook for Growth in Retail Trade, Tourism & Leisure

0

2

4

6

8

10

12

Chi

na

Indi

a

Indo

nesi

a

Mal

aysi

a

M. E

ast

Bra

zil

Afr

ica

Thai

land

Mex

ico

U.S

.

S. K

orea

Taiw

an

Rus

sia

Japa

n

Aus

tral

ia

EM

U

Wor

ld

Retail Trade (excl. Auto) Tourism & Leisure

Forecast Growth in Real Sales (2010–11 CAGR) ü The strength of recoveries in asset

and home prices in Europe and the United States will drive patterns in retail and discretionary

ü The recovery in Tourism, Hotels and Leisure will be slow in Western countries where consumers are still threatened by unemployment and debt

ü In Emerging Asia, rise of the middle class and change in strategy based on G-7 demand to the one boosting households’ real purchasing power will drive consumer spending

ü Several leading global companies in these sectors remain burdened by excessive debt and balance sheet leverage

Copyright © 2009 IHS Global Insight. All Rights Reserved.18

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Consumer Staples Sectors

-4

-2

0

2

4

6

8

10

12

14

Chi

na

Thai

land

Indo

nesi

a

Mal

aysi

a

Indi

a

Taiw

an

Bra

zil

M. E

ast

Kor

ea

Afr

ica

Japa

n

US

Rus

sia

EMU

Mex

ico

Aus

tral

ia

Wor

ld

Food, Beverages, Tobacco Textile & Apparel

Forecast Growth in Real Sales (2010–11 CAGR) ü Food, Beverages, Tobacco

sales are forecasted to see positive growth across the globe

ü Mexico maintains a solid comparative advantage position in the Beverage industry but faces poorer prospects in other parts of the Food complex

ü Textile & Apparel sales will follow a similar trend, driven by trends in local consumer spending

ü The Apparel industry in North America and Europe has lost comparative advantage to China and other lower income locations

Copyright © 2009 IHS Global Insight. All Rights Reserved.19

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Financials & Real Estate

0

2

4

6

8

10

12

14

16

Ch

ina

Ind

ia

Bra

zil

Ind

on

esia

Mal

aysi

a

Tai

wan

M.

Eas

t

Ko

rea

Afr

ica

Ru

ssia

Th

aila

nd

Mex

ico

Au

stra

lia

US

EM

U

Jap

an

Wo

rld

Banking & Related Financials Real Estate

Forecast Growth in Real Sales (2010–11 CAGR) ü Bank lending is still contracting or is

tepid in the U.S. and West Europe, but is flowing more freely in BRIC countries and Mexico

ü Banks in the United States and Europe are also under pressure from expected major reforms that will lead to significantly tougher oversight and limits on capital and compensation

ü In China and many emerging countries more focus is on regulating the lending in order to limit the risks of excessive credit and asset price bubbles

ü Mexico’s Banking sector has “safe” (robust) capitalization levels and solvency ratios. Growth of new credit is driven by corporate demand, but banks continue to show declines in their consumer credit portfolios

Copyright © 2009 IHS Global Insight. All Rights Reserved.20

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Business and IT Services including R&D

0

2

4

6

8

10

12

14

Chi

na

Indi

a

Mal

aysi

a

Indo

nesi

a

Bra

zil

Thai

land

Taiw

an

M. E

ast

Rus

sia

Afr

ica

Aus

tral

ia

U.S

.

Mex

ico

S. K

orea

EM

U

Japa

n

Wor

ldBusiness Services Information Technology Services

Forecast Growth in Real Sales (2010–11 CAGR)

ü IT services, R&D and technical business skills are among the best performing sectors during the recession

ü These are major beneficiaries of new developments in computing technology, communication and hardware

ü These have also ranked highly among the sources of growth in employment

ü Several of the influential companies in this sector enjoy healthy balance sheets and much cash, are looking for growth via M&A and penetration of new markets

Copyright © 2009 IHS Global Insight. All Rights Reserved.21

Copyright © 2009 IHS Global Insight. All Rights Reserved.

Global Outlook for Growth in Public Administration, Defense & Education

-2

0

2

4

6

8

10

Indi

a

Chin

a

M. E

ast

Afric

a

Mal

aysi

a

Indo

nesi

a

Braz

il

Thai

land

Aust

ralia

Russ

ia

Taiw

an

Mex

ico

Kore

a US

EMU

Japa

n

Wor

ld

Public Administration & Defence Education

Forecast Growth in Real Sales (2010–11 CAGR) ü As a result of the crisis, countries have increased public expenditure to strengthen aggregate demand, limit the depth of the recession and ensure a faster recovery

ü Now, with public finances strained, many governments will need to consider how to unwind the stimulus and seriously cut back on spending

ü Key developmental goals of the stimulus are: energy and construction, other infrastructure, expanding education and health services, providing funding for technological research and development

Thank youMark Killion, CFAManaging Director, World Industry Group, IHS Global [email protected]

For more information, please see our public Web sites:http://www.ihsglobalinsight.com/WorldIndustry

Download a copy of this presentation at:www.ihsglobalinsight.com/events/MexConf_July2010_presentations