57

Larsen & Toubro Investor Presentation – H1 FY16 October 30, 2015

Larsen & Toubro

Investor Presentation – H1 FY16October 30, 2015

Disclaimer

This presentation contains certain forward looking statements concerning L&T’s future

business prospects and business profitability, which are subject to a number of risks

and uncertainties and the actual results could materially differ from those in such

forward looking statements.

The risks and uncertainties relating to these statements include, but are not limited to,

risks and uncertainties regarding fluctuations in earnings, our ability to manage growth,

competition (both domestic and international), economic growth in India and the

target countries for exports, ability to attract and retain highly skilled professionals,

time and cost over runs on contracts, our ability to manage our international

operations, government policies and actions with respect to investments, fiscal

deficits, regulations, etc., interest and other fiscal costs generally prevailing in the

economy. Past performance may not be indicative of future performance.

The company does not undertake to make any announcement in case any of these

forward looking statements become materially incorrect in future or update any

forward looking statements made from time to time by or on behalf of the company.2

3

Presentation Outline

L&T Overview

Business Overview

Group Performance

SectoralOpportunities

& Outlook

4

Presentation Outline

L&T Overview

Business Overview

Group Performance

SectoralOpportunities

& Outlook

L&T - At a Glance

Professionally Managed Company

FY 15 Group Revenues: `920 Bn

(approx.

US$ 15 Bn)

Market Cap (30th Oct’15):

₹1313 Bn

(approx.

US$ 20 Bn)

Credit Ratings CRISIL:

AAA/Stable ICRA:

AAA(Stable)

5

India’s largest E&C company with interests in Projects, Infrastructure

Development, Manufacturing, IT & Financial Services

6

L&T - At a Glance

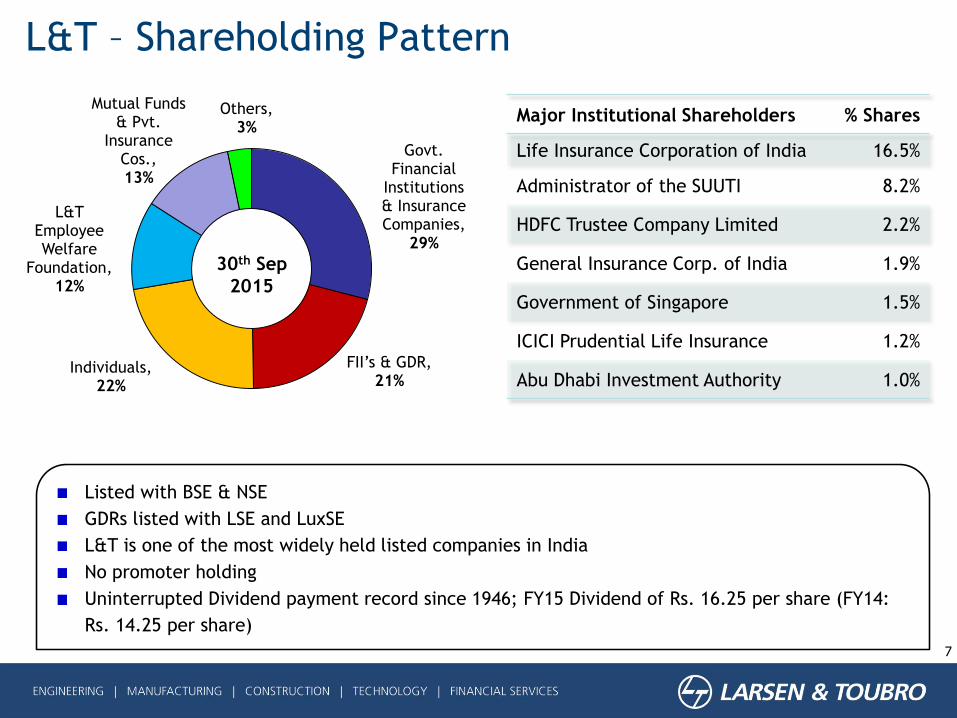

L&T – Shareholding Pattern

Listed with BSE & NSE

GDRs listed with LSE and LuxSE

L&T is one of the most widely held listed companies in India

No promoter holding

Uninterrupted Dividend payment record since 1946; FY15 Dividend of Rs. 16.25 per share (FY14:

Rs. 14.25 per share)

Major Institutional Shareholders % Shares

Life Insurance Corporation of India 16.5%

Administrator of the SUUTI 8.2%

HDFC Trustee Company Limited 2.2%

General Insurance Corp. of India 1.9%

Government of Singapore 1.5%

ICICI Prudential Life Insurance 1.2%

Abu Dhabi Investment Authority 1.0%

7

Govt. Financial

Institutions & Insurance Companies,

29%

FII’s & GDR, 21%

Individuals,22%

L&T Employee Welfare

Foundation,12%

Mutual Funds & Pvt.

Insurance Cos., 13%

Others,3%

30th Sep

2015

Experienced Management Team

8

A M Naik

Group Executive Chairman

BE [Mech]

Joined L&T in March 1965

Diverse and vast experience in general management, Technology and E&C

S. N. Subrahmanyan

Deputy Managing Director & President

B.SC ENGG (CIVIL), MBA (Finance)

Joined L&T in November 1984

Vast experience in Design & Build (D&B) Contracts, PPP Projects, Engineering and Construction Industry

R Shankar Raman

Whole-time Director &Chief Financial Officer

B.Com, ACA, CWA

Joined L&T Group in November 1994

Vast experience in Finance, Taxation, Insurance, Risk Management, Legal and Investor Relations

Shailendra Roy

Whole-time Director & Sr. Executive Vice President (Power, Heavy Engg. & Defence)

BE (Tech)

Joined L&T in 2004

Vast experience in Thermal Power Business

D. K. Sen

Whole-time Director & Sr. Executive Vice President (Infrastructure)

B.SC ENGG (CIVIL), MBA (Finance)

Joined L&T in 1989

Vast experience in Design & Engineering, Business Development, Tendering and construction.

Corporate Governance

9

Four-tier Governance Structure

L&T’s essential character revolves around values based on transparency, integrity, professionalism and accountability

Board

of Directors

Executive Management Committee (EMC)

Independent Company (IC) Board

Strategic Business Group (SBG) / Business Unit (BU)

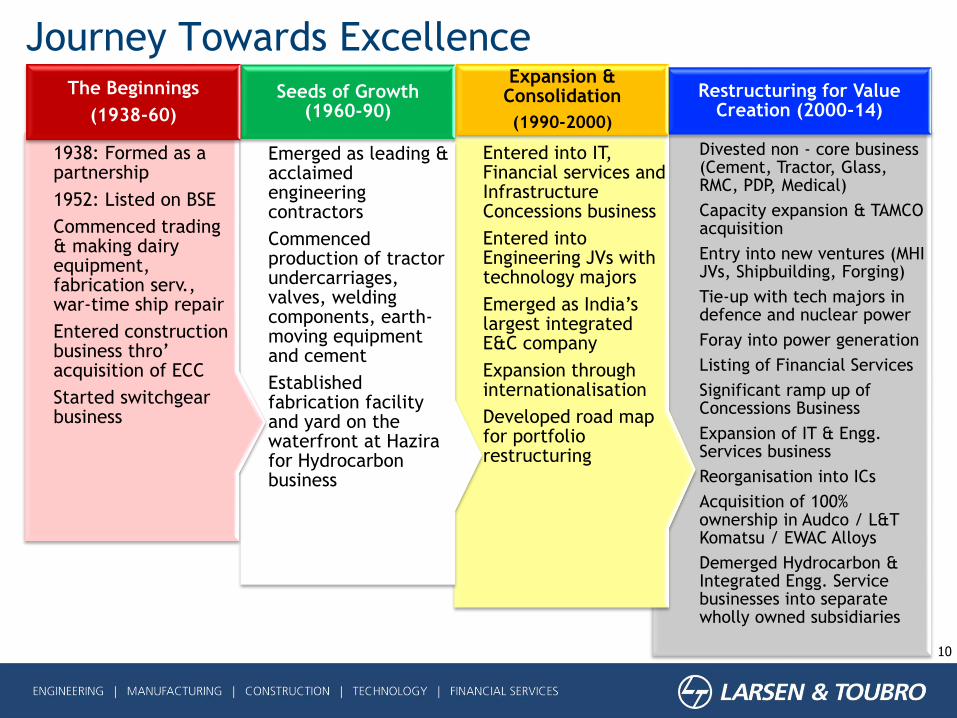

Journey Towards Excellence

10

Divested non - core business (Cement, Tractor, Glass, RMC, PDP, Medical)

Capacity expansion & TAMCO acquisition

Entry into new ventures (MHI JVs, Shipbuilding, Forging)

Tie-up with tech majors in defence and nuclear power

Foray into power generation

Listing of Financial Services

Significant ramp up of Concessions Business

Expansion of IT & Engg. Services business

Reorganisation into ICs

Acquisition of 100% ownership in Audco / L&T Komatsu / EWAC Alloys

Demerged Hydrocarbon & Integrated Engg. Service businesses into separate wholly owned subsidiaries

Restructuring for Value Creation (2000-14)

Entered into IT, Financial services and Infrastructure Concessions business

Entered into Engineering JVs with technology majors

Emerged as India’s largest integrated E&C company

Expansion through internationalisation

Developed road map for portfolio restructuring

Expansion & Consolidation

(1990-2000)

Emerged as leading & acclaimed engineering contractors

Commenced production of tractor undercarriages, valves, welding components, earth-moving equipment and cement

Established fabrication facility and yard on the waterfront at Hazira for Hydrocarbon business

Seeds of Growth (1960-90)

1938: Formed as a partnership

1952: Listed on BSE

Commenced trading & making dairy equipment, fabrication serv., war-time ship repair

Entered construction business thro’ acquisition of ECC

Started switchgear business

The Beginnings

(1938-60)

L&T’s Sustainability InitiativeThe L&T Sustainability Report 2014 is a ‘GRI Checked’ , Externally Assured, Application Level A+ report.

Climate Change Carbon footprint

mapping

Energy Conservation

Water Conservation

Material Management

Community

Sustainability Thrust Areas

Safety

Accolades

One of the eight Indian

companies featuring in Dow

Jones Sustainability

Emerging Markets Indices

One of the only five Indian

Companies to feature in the

Global ‘A’ list for its Carbon

Performance – CDP 2014

Ranked Asia’s 2nd Most

Sustainable Company in

Industrial Sector in Channel

NewsAsia’s Sustainability

Rankings 2014

L&T Ranks In Top 10

Companies for CSR – The

Economic Times

Sustainability – Environment & Social

12

Green Buildings

L&T’s own – 2.1 million sq. ft.

Constructed for Clients – 43.02 million sq. ft.

All 28 L&T Campuses are zero wastewater discharge

5 Campuses are water positive

2012-13 2013-14

1,6

1,4

67

2,0

7,3

68

Energy Conservation (GJ)

Renewable power contributes 7.9 % of indirect energy

Food waste processing plants for

treatment of organic waste

Aligned with

National Action Plan on Climate Change

and

UN Millennium Development Goals

Thrust Areas No. of Beneficiaries (2013-14)

Education 242,024

Skill Building 45,209

Healthcare-Mother and Child

517,837

Total 805,070

Education - Over two lakh children impacted

Skill Building - 8 construction skills training institutes empowering more than 13,000 people

Healthcare: Mother & Child - 8 community health centres provide state-of-the-art diagnostic health

services

Parameter Values

Energy Consumption(GJ/Employee)

132.82

Direct GHG Emissions (Tons/Employee)

7.80

Water Consumption(m3/employee)

155.81

13

Presentation Outline

L&T Overview

Business Overview

Group Performance

SectoralOpportunities

& Outlook

Builders to the nation

14

Wankhede Stadium, Mumbai

Baha’i Temple, Delhi

Maruti Manesar (Haryana) Expansion 88m Rail Bridge Jammu Udhampur1320 MT FCC Regenerator – for RIL

Oil & Gas Offshore PlatformsMumbai International Airport 3rd Narmada High

ITC Grand Chola Hotel, Chennai Sri Sathya sai Whitefield Hospital Srinagar Hydro Electric Plant

2x384 MW CCPP, Vemagiri, A.P. Transmission Lines in Himachal Water Treatment Plant, Barmer300 mtr Minerva Tower, Mumbai

Kakrapar Nuclear Power Plant, Guj

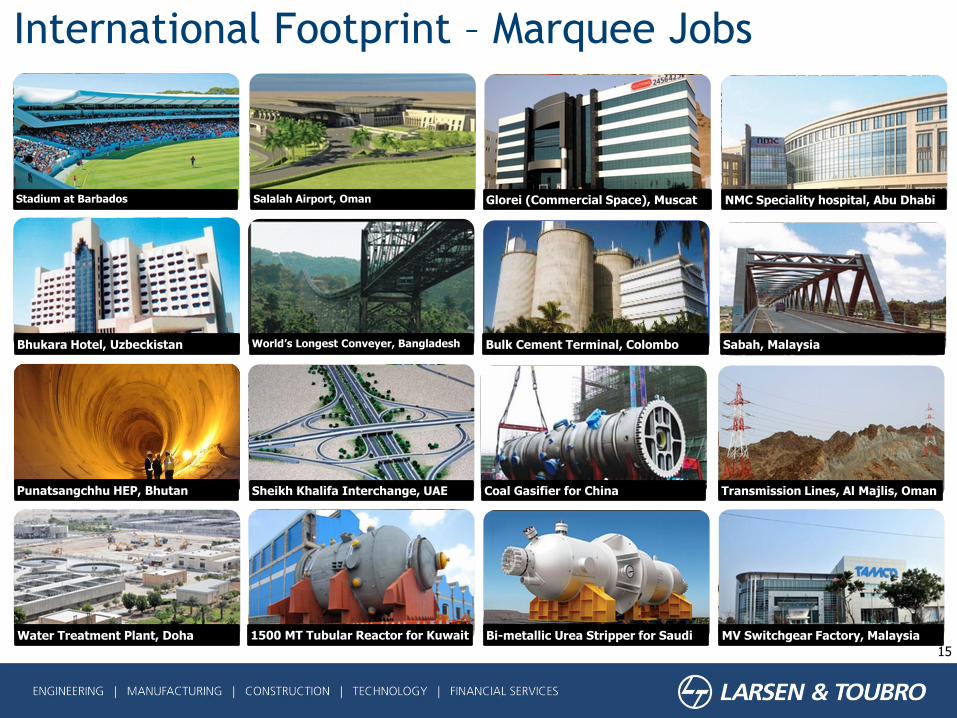

International Footprint – Marquee Jobs

15

NMC Speciality hospital, Abu Dhabi

Bhukara Hotel, Uzbeckistan

Stadium at Barbados Glorei (Commercial Space), MuscatSalalah Airport, Oman

Sabah, Malaysia

Sheikh Khalifa Interchange, UAE Coal Gasifier for China Transmission Lines, Al Majlis, Oman

1500 MT Tubular Reactor for Kuwait Bi-metallic Urea Stripper for Saudi MV Switchgear Factory, MalaysiaWater Treatment Plant, Doha

Punatsangchhu HEP, Bhutan

World’s Longest Conveyer, Bangladesh Bulk Cement Terminal, Colombo

E&C Delivery Platform

16Single point responsibility for turnkey solutions

Design

&

Engineering

Manufacture

&

Fabrication

EPC Projects

Construction

One of Asia’s largest vertically integrated E&C Companies

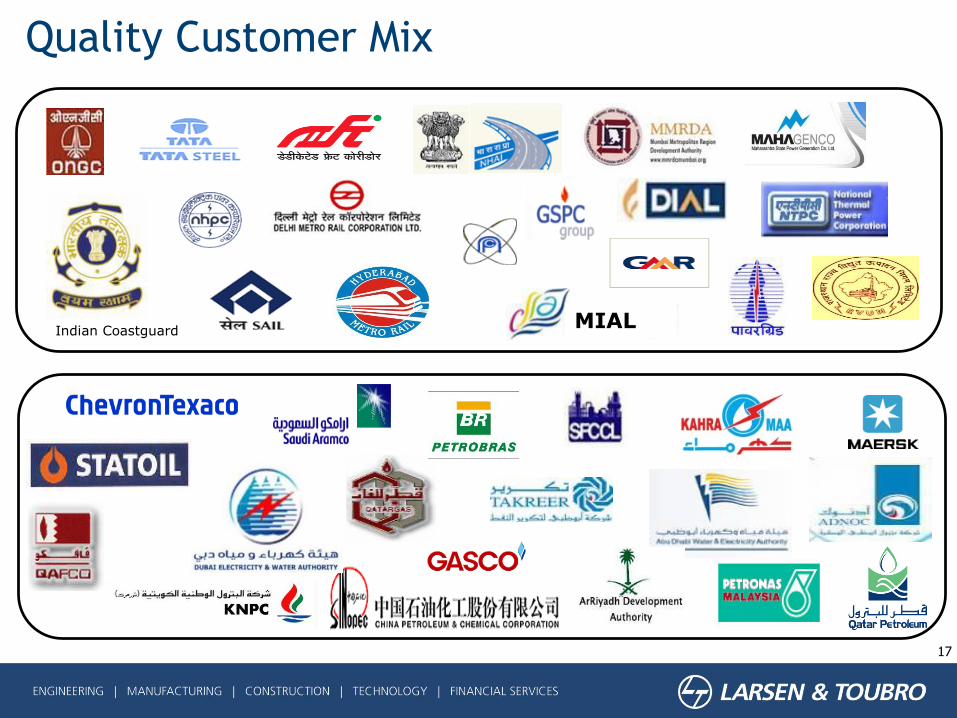

Quality Customer Mix

17

MIALIndian Coastguard

Multiple Alliances & Joint Ventures

18

Alliances

Pre qualifications

Note: Some of these are project specific alliances & pre qualifications

Joint Ventures

Befula Investments

L&T’s Business StructureLARSEN & TOUBRO LTD.

BUSINESS VERTICALSSUBSIDIARIES &

ASSOCIATES

BUILDINGS & FACTORIES

TRANSPORTATION INFRASTRUCTURE

METALLURGICAL & MATERIAL HANDLING

POWER T&D

HEAVY ENGINEERING

SHIPBUILDING

ELECTRICAL & AUTOMATION

POWER

FINANCIAL SERVICES

IT & TECHNOLOGY SERVICES

INFRASTRUCTURE SPVs (BOTs)

MHPS JVs (Boilers & Turbine Mfg.)

HEAVY CIVIL INFRASTRUCTURE

WATER, SMART WORLD & COMM.

OTHER MANUFACTURING & FABRICATION SUBSIDIARIES

SERVICES AND OTHER SUBSIDIARIES & ASSOCIATES

19

L&T HYDROCARBON ENGINEERING

20

Presentation Outline

L&T Overview

Business Overview

Group Performance

SectoralOpportunities

& Outlook

FY 12 FY 13 FY 14 FY 15

88.8

99.3 107.3

EBITDA

Four Year Performance

21

`B

illi

on

FY 12 FY 13 FY 14 FY 15

643 745

851

Net Sales

`B

illi

on

`B

illi

on

FY 12 FY 13 FY 14 FY 15

1,450 1,648

1,815

Order Book

`B

illi

on

920

2,327113.4

FY 12 FY 13 FY 14 FY 15

1,554

793

Order Inflow

`B

illi

on

1272

1029

`B

illi

on

22

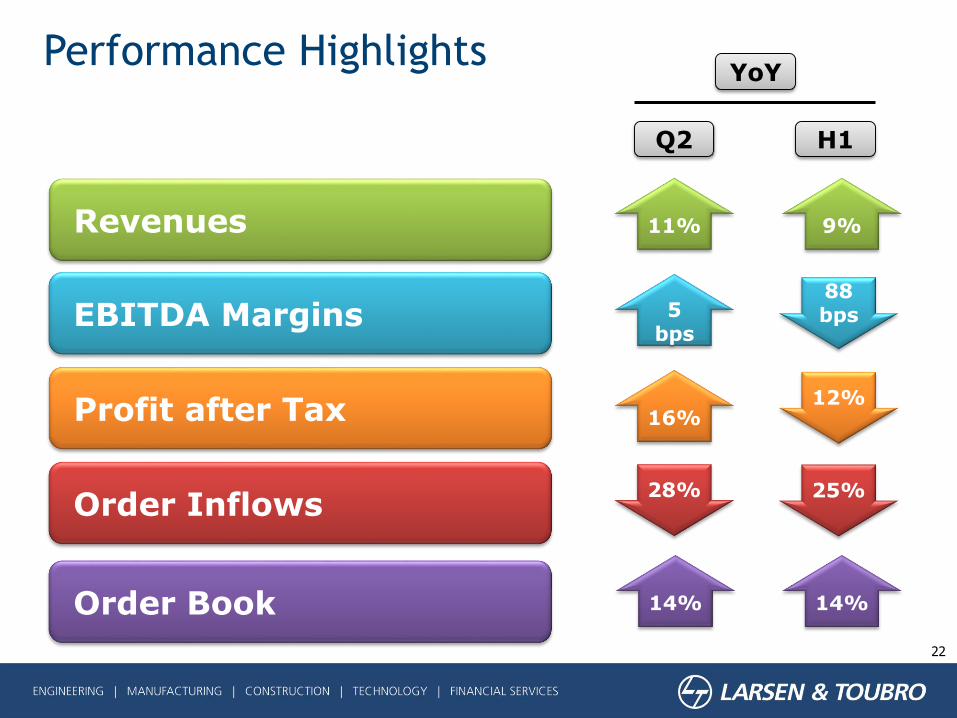

Performance Highlights

Order Inflows

Revenues

Order Book

EBITDA Margins

Profit after Tax

Q2 H1

28%

9%11%

14%

16%

14%

25%

88bps5

bps

12%

YoY

Sep'14 Sep'15

Order Book

2144

2441

Group level Order Inflow & Order Book

23

Amount in ` Bn

14%

Order Inflow Order Book

65%72%

35% 28%

Geographical Breakup

Domestic International

Investment momentum in domestic market yet to gather pace

Excess capacity restrains industrial capex and private sector investment

Middle East Capex witnessing slowdown due to low oil prices

International business powered mainly by Infra segment

H1

FY16

FY15 FY16

334 264

398

286

Order Inflow

Q1 Q2

-25%

732

550

Group Performance – Sales & Costs

24

Infra, Power and Services businesses contribute to Revenue growth

MCO charge in line with level of operations

Staff cost increase due to manpower augmentation, normal revisions and increased

level of international operations

Increase in SGA expenses reflects higher business development expenses and warranty

provisions

Q2 FY15 Q2 FY16 % Change ` Billion H1 FY15 H1 FY16 %

Change FY15

211.59 233.93 11%Net Sales / Revenue from

Operations 401.34 436.45 9% 920.05

64.21 76.58 19% ----International Sales 112.71 142.66 27% 259.26

30% 33% 3% % of Sales 28% 33% 5% 28%

153.69 169.96 11% Mfg, Cons. & Opex (MCO) 286.95 314.76 10% 672.55

22.62 24.33 8% Staff Costs 40.20 45.32 13% 79.98

11.94 13.72 15% Sales, adm. & other Exp. (SGA) 25.78 27.55 7% 54.17

188.25 208.02 10% Total Opex 352.93 387.64 10% 806.71

Performance Summary – Operational Costs & Profitability

Material cost,

42.4%(37.0%)

Subcontracting

charges,15.6%

(16.4%)

Other

Opex, 14.7%(19.2%)

Staff Costs,

10.4%(10.7%)

Sales, adm. &

other Exp., 5.9%(5.6%)

EBITDA,

11.1%(11.0%)

Q2 FY16

25

Material cost,

36.5%(34.1%)

Subcontracting

charges,17.8%

(18.0%)

Other

Opex, 17.8%(19.4%)

Staff Costs,

10.4%(10.0%)

Sales, adm. &

other Exp., 6.3%(6.4%)

EBITDA,

11.2%(12.1%)

H1 FY16

Figures in brackets indicate corresponding period of the Previous Year

Group Performance Summary Extracts

26

Composite margins holding steady

Increase in interest expenses due to decline in G-Sec rates and operationalization of 3

road SPVs

Increase in depreciation charge due to revisions under Companies Act and

operationalization of road SPVs

Other income mainly comprises treasury gains

Q2 FY15 Q2 FY16 % Change ` Billion H1 FY15 H1 FY16 %

Change FY15

23.34 25.92 11% EBITDA 48.41 48.82 1% 113.33

11.03% 11.08% 0.1% EBITDA Margin 12.1% 11.2% -0.9% 12.3%

(6.91) (8.28) 20% Interest Expenses (14.61) (15.35) 5% (28.51)

(5.49) (6.94) 26% Depreciation (13.56) (13.16) -3% (26.23)

2.15 2.19 2% Other Income 4.92 4.76 -3% 10.10

(4.69) (4.94) 5% Provision for Taxes (9.18) (10.39) 13% (22.53)

8.62 9.96 16% PAT after Minority Interest 18.29 16.02 -12% 47.65

Group Balance Sheet

27

Gross D/E: 2.33

Net Working Capital (excl. Fin. Serv.) : 24% of Sales

` Billion Sep-15 Mar-15Incr /

(Decr)

Net Worth 421.85 409.09 12.76

Minority 60.48 49.99 10.49

Borrowings (Fin. Serv.) 462.06 430.10 31.96

Other Non-Current Liabilities 485.51 406.76 78.75

Other Current Liabilities 713.25 642.07 71.18

Total Sources 2,143.15 1,938.01 205.14

Net Fixed Assets 587.55 475.16 112.39

Goodwill on consolidation 21.85 22.15 (0.30)

Loans & Advances (Fin. Serv.) 490.83 454.26 36.57

Other Non- Current Assets 158.47 156.31 2.16

Cash and Cash Equivalents 150.46 138.21 12.25

Other Current Assets 733.99 691.92 42.07

Total Applications 2,143.15 1,938.01 205.14

Group Cash Flow (Summarised)

28* included under Net Cash from operations under statutory financial statements

` Billion Q1 FY16 Q2 FY16 H1 FY16 Q1 FY15 Q2 FY15 H1 FY15

Operating Profit 23.62 27.68 51.30 23.70 23.89 47.60

Direct Taxes (Paid) / Refund - Net (5.61) (8.33) (13.94) (5.21) (8.54) (13.75)

Changes in Working Capital (6.34) (10.25) (16.59) (6.02) (17.21) (23.23)

Net Cash from Operations (A) 11.68 9.10 20.78 12.48 (1.86) 10.62

Investments in Fixed Assets (Net) (15.90) (8.31) (24.21) (18.29) (15.26) (33.55)

Net Purchase of Long Term & Curr. Inv. (28.00) 6.90 (21.11) (16.13) 10.96 (5.18)

Loans/Deposits made with Associate Cos. (0.01) 0.02 0.01 6.37 0.14 6.51

Interest & Div. Received and Others 3.29 1.30 4.58 1.00 2.21 3.22

Net Cash from/(used in) Invest. Act. (B) (40.63) (0.10) (40.73) (27.05) (1.95) (29.00)

Issue of Share Capital / Minority 6.26 5.72 11.98 5.01 1.89 6.91

Net Borrowings 42.05 28.97 71.02 18.49 44.47 62.96

Disbursements towards financing activities* (19.06) (17.51) (36.57) (6.44) (16.14) (22.58)

Interest & Dividend paid (6.56) (27.14) (33.70) (8.79) (20.64) (29.43)

Net Cash from Financing Activities (C) 22.69 (9.97) 12.72 8.28 9.58 17.86

Net (Dec) / Inc in Cash & Bank (A+B+C) (6.26) (0.96) (7.23) (6.29) 5.77 (0.52)

29

Segment Performance Analysis

30

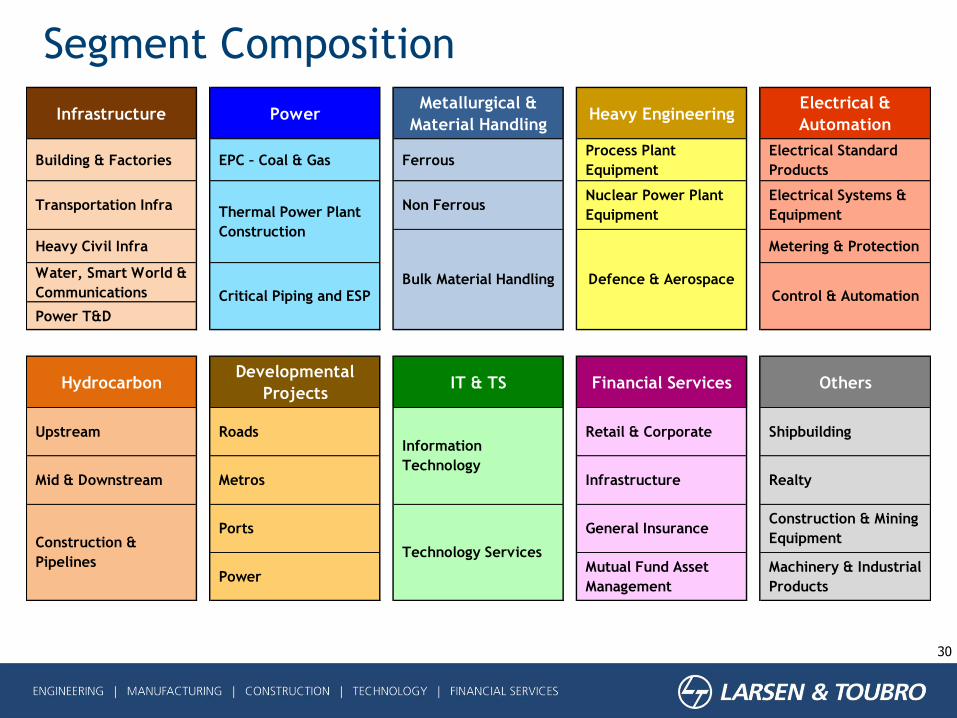

Segment Composition

Infrastructure PowerMetallurgical &

Material HandlingHeavy Engineering

Electrical &

Automation

Building & Factories EPC – Coal & Gas FerrousProcess Plant

Equipment

Electrical Standard

Products

Transportation Infra Non FerrousNuclear Power Plant

Equipment

Electrical Systems &

Equipment

Heavy Civil Infra Metering & Protection

Water, Smart World &

Communications

Power T&D

HydrocarbonDevelopmental

ProjectsIT & TS Financial Services Others

Upstream Roads Retail & Corporate Shipbuilding

Mid & Downstream Metros Infrastructure Realty

Ports General InsuranceConstruction & Mining

Equipment

Power Mutual Fund Asset

Management

Machinery & Industrial

Products

Construction &

Pipelines

Control & AutomationCritical Piping and ESPDefence & Aerospace

Technology Services

Information

Technology

Bulk Material Handling

Thermal Power Plant

Construction

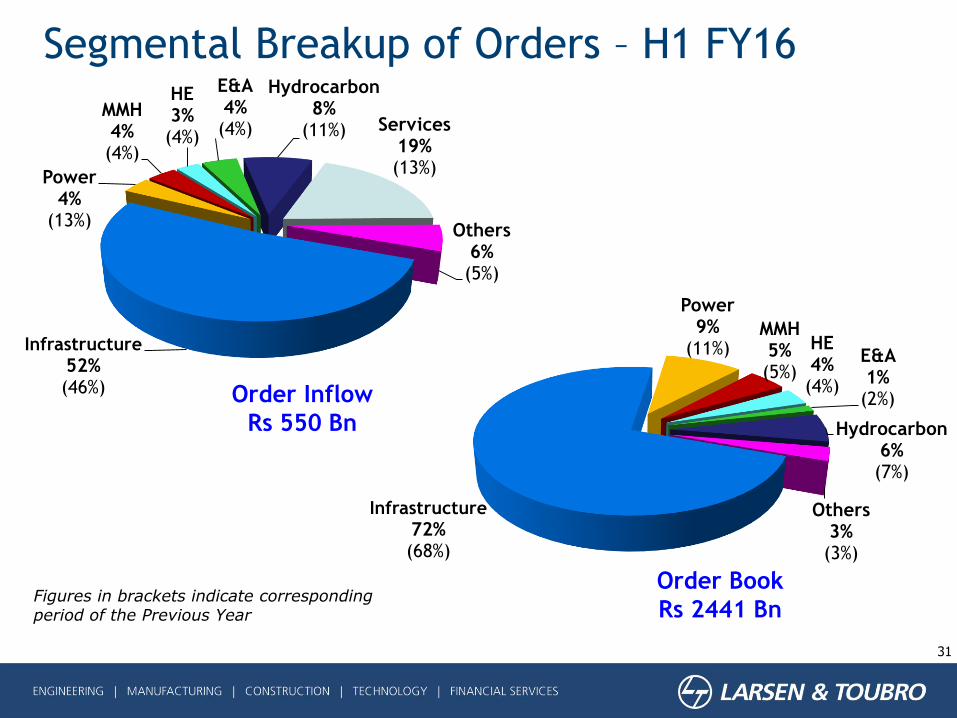

Infrastructure

72%(68%)

Power9%

(11%)MMH5%(5%)

HE4%(4%)

E&A 1%(2%)

Hydrocarbon6%(7%)

Others3%(3%)

Order Book

Rs 2441 Bn

31

Segmental Breakup of Orders – H1 FY16

Infrastructure

52%(46%)

Power4%

(13%)

MMH4%(4%)

HE3%(4%)

E&A4%(4%)

Hydrocarbon8%

(11%) Services19%(13%)

Others6%(5%)

Figures in brackets indicate corresponding period of the Previous Year

Order Inflow

Rs 550 Bn

68%

32%

Geographical breakup

Domestic International

Infrastructure43%

MMH2%

Power6%

HE3%

Hydrocarbon10%

IT & TS10% Fin. Services

8%

Devl. Proj.6%

Others7%

Segmental Breakup

32

Revenue Breakup – H1 FY16

E&A

5%

Infrastructure Segment

33

Amount in ` Bn

Revenues reflect in-line progress of execution

International business growth contributed by previous years’ order wins

Margin variation primarily due to job mix status

Revenues & Margin

Power Segment

34

Amount in ` Bn

High competitive intensity for fresh orders from State Utilities/PSUs

Revenue growth due to execution progress on opening Order Book

Margin variation due to job mix

Revenues & Margin

Revenue decline due to low sectorial investments and reduced Order Book

Margin drop arising from under utilisations and cost overruns

35

Amount in ` Bn

Metallurgical & Material Handling (MMH) Segment

Revenues & Margin

Oil price drop, muted global growth and excess capacity adversely impacting

business opportunity and profitability

Declining revenues arising out of depleted order book

Margin drop due to volume shrinkage and cost provisions

36

Amount in ` Bn

Heavy Engineering Segment

Revenues & Margin

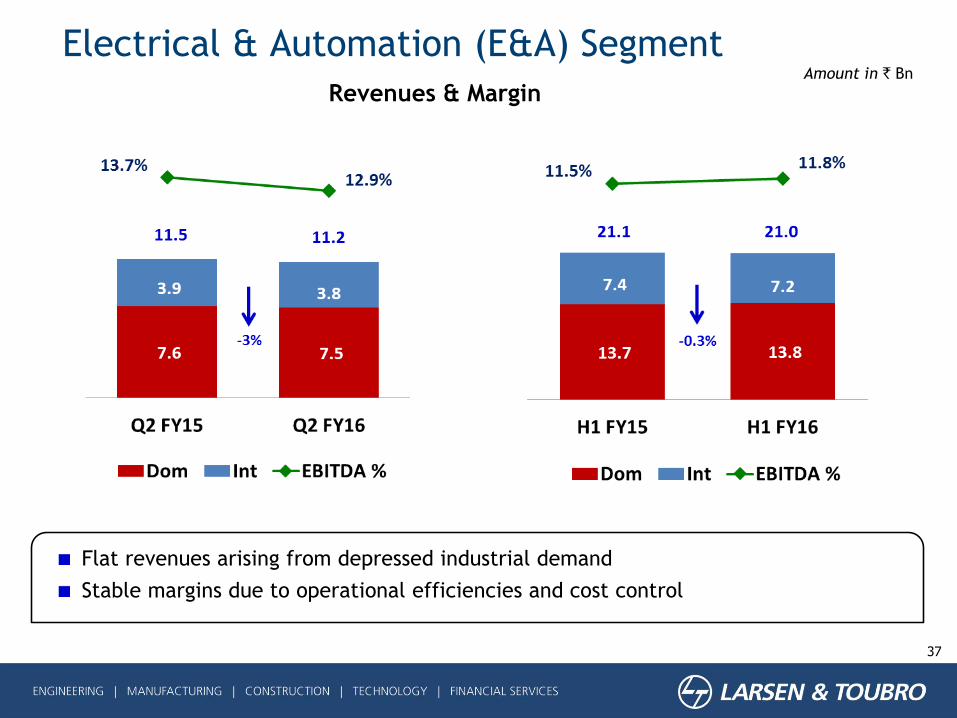

Flat revenues arising from depressed industrial demand

Stable margins due to operational efficiencies and cost control

37

Amount in ` Bn

Electrical & Automation (E&A) Segment

Revenues & Margin

Challenged legacy Middle East projects nearing execution completion

Middle East Hydrocarbon Capex undergoing curtailment due to oil price decline

Reduced level of international operations giving rise to under-recovery of overheads

Leadership team being strengthened

38

Hydrocarbon SegmentAmount in ` Bn

Revenues & Margin

Growth in end-markets seen across sectors except energy and utilities

Favourable currency movement aiding top line and margins

39

Amount in ` Bn

IT & Technology Services Segment

Revenues & Margin

Revenue growth driven by Realty, Valves and Industrial Machinery businesses

Margins largely arising from Realty business

40

Amount in ` Bn

Others Segment

Revenues & Margin

Increase in revenues and margins (excl. Dhamra) driven by operationalization of Nabha 2nd

Unit and 3 Road SPVs

41

Amount in ` Bn

Developmental Projects Segment

Revenues EBITDA

Balance Equity Commitment (Sep 2015): ` 44 Bn

Total Project Cost (Sep 2015): ` 561 Bn

Equity Invested (Sep 2015): ` 89 Bn

42

Roads and Bridges:

Portfolio: 16 projects (1721 Km); 14 Operational

Project Cost: `178 Bn

Power:

Portfolio: 5 projects (2270 MW); 1 Operational

Project Cost: `178 Bn

Ports:

Portfolio: 2 projects (18 MTPA) - Operational

Project Cost: `21 Bn

Metros:

Portfolio: 1 project (71.16 Km) – Under-implementation

Project Cost: `170 Bn

Transmission Lines:

Portfolio: 1 project (482 Km) – Under-implementation

Project Cost: `14 Bn

Concessions Business Portfolio – 25 SPVs

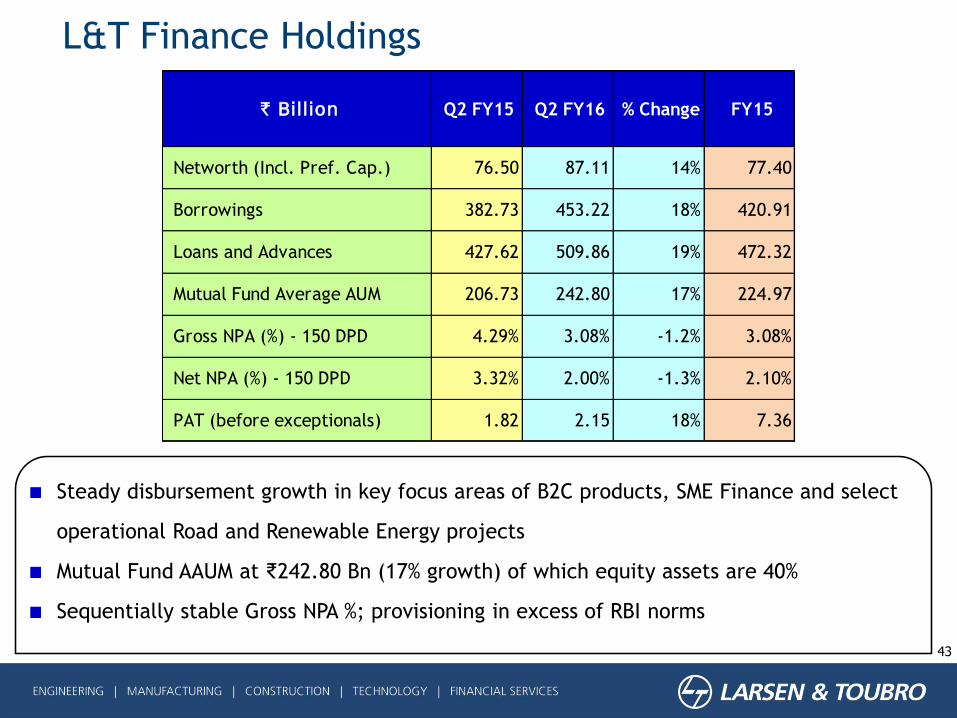

Steady disbursement growth in key focus areas of B2C products, SME Finance and select

operational Road and Renewable Energy projects

Mutual Fund AAUM at ₹242.80 Bn (17% growth) of which equity assets are 40%

Sequentially stable Gross NPA %; provisioning in excess of RBI norms

43

L&T Finance Holdings

` Billion Q2 FY15 Q2 FY16 % Change FY15

Networth (Incl. Pref. Cap.) 76.50 87.11 14% 77.40

Borrowings 382.73 453.22 18% 420.91

Loans and Advances 427.62 509.86 19% 472.32

Mutual Fund Average AUM 206.73 242.80 17% 224.97

Gross NPA (%) - 150 DPD 4.29% 3.08% -1.2% 3.08%

Net NPA (%) - 150 DPD 3.32% 2.00% -1.3% 2.10%

PAT (before exceptionals) 1.82 2.15 18% 7.36

44

Presentation Outline

L&T Overview

Business Overview

Group Performance

SectoralOpportunities

& Outlook

Infrastructure Segment – Urban Infra

45

Opportunities:

High end residential projects by cash rich developers

Affordable housing projects by Urban Authorities with

focus on Housing For All targets

Office space build-out by IT majors

Healthcare capacity expansion in India & Middle East

Greenfield Airports and Brownfield expansions

Thrust on Education facility expansion by Gov’t

International urban infra prospects in Oman, UAE,

Qatar, KSA

Presence :

Residential & Commercial Buildings, IT & Office Space,

Hospitals, Shopping Malls, Educational Institutions,

Luxury Hotels, Airport Terminals, and Factory

Buildings

Infrastructure Segment – Transportation Infra

46

Opportunities:

Increased road build-out by NHAI with current focus on

EPC projects

Expressway projects by State Governments

Elevated corridors and Ring Roads in major cities

Dedicated Freight Corridor program

Track modernisation and expansion by Indian Railways

Airport runways

International opportunities in Oman, UAE, Qatar and

KSA

Presence :

Roads, Elevated Corridors, Railway Construction &

Airport Runways,

Infrastructure Segment – Heavy Civil Infra

47

Opportunities:

Metro & Mono Rail projects planned in multiple cities

across India (to decongest urban traffic)

Build out of Hydel Plants in Nepal, Bhutan and NE

States

Thrust being given by Govt on increasing nuclear

power installed base

Thrust on connectivity to hilly states (J&K,

Arunachal, Himachal) with Tunnels and Border Roads

Increased spends on infrastructure facilities for

armed forces

Presence :

Metro Railways, Monorails, Hydel Power Plant

construction, Nuclear (civil) plant construction,

Defence Infrastructure, Special Bridges and Tunnels

Infrastructure Segment – Water & Communication

48

Opportunities:

Thrust on water infrastructure due to falling water

tables across the country

Waste water treatment plants from municipalities

Thrust on river water pollution prevention including

Namami Gange program

Defence sector fibre optic connectivity projects

Smart cities: Security solutions and inter-city

telecom connectivity

Effluent treatment plants in Industrial units/clusters

Presence :

Bulk transmission of water, water treatment, waste

water treatment, sewage rehabilitation, effluent

treatment, telecom infrastructure and security

systems

Infrastructure Segment – Power T&D

49

Opportunities:

Thrust on Grid Strengthening programs with

increasing loads

Thrust on Expansion of T&D grids with growing

generation capacities as well as demand

Transmission efficiency enhancement programs

Feeder Separation scheme and other Rural programs

Dedicated Green Energy Transmission Corridors

Thrust on Solar Power capacity addition

T&D expansion in Oman, UAE, Qatar, Kuwait and KSA

Presence :

Sub-stations, Transmission Lines, Solar Power projects

Infrastructure Segment – Challenges

50

Major Challenges in Infrastructure:

Investment constraints

Lending capacity of Banking system

Government Funding

Lack of private sector interest in PPP projects

Land acquisition

Environmental Clearances

Slow evolution of policy frameworks

Pace of awards and execution

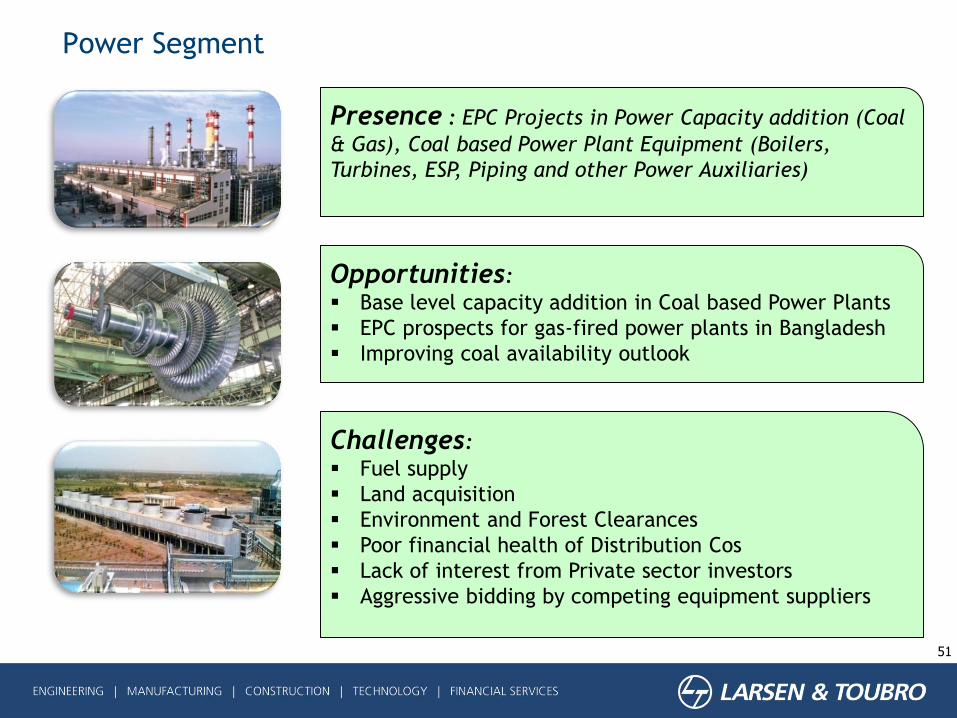

Power Segment

51

Presence : EPC Projects in Power Capacity addition (Coal

& Gas), Coal based Power Plant Equipment (Boilers,

Turbines, ESP, Piping and other Power Auxiliaries)

Challenges:

Fuel supply

Land acquisition

Environment and Forest Clearances

Poor financial health of Distribution Cos

Lack of interest from Private sector investors

Aggressive bidding by competing equipment suppliers

Opportunities:

Base level capacity addition in Coal based Power Plants

EPC prospects for gas-fired power plants in Bangladesh

Improving coal availability outlook

Heavy Engineering & Defence

52

Opportunities: Oil & Gas equipment supply opportunities in India, Middle

East, Far East, Russia, Europe and USA

Nuclear Power Plant equipment in India

Indigenisation thrust for Defence equipment

Interceptor Boats, Naval vessels and Submarines for

Indian Navy and Coastguard

Artillery guns and other equipment for Indian Army

Components for Indian Space Program

Presence : Equipment for process plants (mainly for oil

and gas), Nuclear power plant equipment, Defense (mainly

for navy and army) and Aerospace

Challenges:

Shrinking spends on Oil & Gas with low Crude price

Reduced prospect base of nuclear power equipment post-

Fukushima and consequent on civil liability overhang

Very long prospect-to-award timelines and dominance of

Public Sector and foreign OEMs in Defense orders

Hydrocarbon Segment

53

Opportunities: Select International prospects – Upstream / Mid &

Downstream

Opportunities from ONGC Capex – Upstream / Mid &

Downstream

Opportunities for Fertilizer EPC

Regasification terminals and Pipelines

‘Clean fuel’ projects

Presence : Offshore Platforms, Subsea pipelines,

Floating Systems, Subsea installations, Onshore Oil & Gas

installations, Refineries, Petrochemical and Fertiliser

Plants (EPC), Onshore pipelines, Regasification Terminals

Challenges:

Reduced Capex in Middle East in low Crude price

scenario

Long bid-to-award timelines

Aggressive competition in Domestic and GCC markets

Project execution in international markets

Outlook – Wide circles of influence

Thank You

55

Annexure-1: Group Profit & Loss

56* Includes Insurance Business

H1 FY16 H1 FY15 %

Change

Revenue from Operations 43.88 36.46 25.53 330.58 436.45 401.34 9%

EBITDA 9.22 5.47 6.61 27.52 48.82 48.41 1%

Interest Expenses (0.05) (0.17) (6.78) (8.35) (15.35) (14.61) 5%

Depreciation (1.18) (0.61) (2.11) (9.26) (13.16) (13.56) -3%

Other Income 0.09 0.96 0.02 3.69 4.76 4.92 -3%

Exceptional Items - - - 3.10 3.10 2.49

Provision for Taxes (1.55) (1.87) (0.37) (6.61) (10.39) (9.18) 13%

PAT from Ordinary Activites 6.53 3.78 (2.62) 10.08 17.78 18.47 -4%

Share in profit of Associates - 0.01 0.01 (0.01) 0.01 0.02

Adjustments for Minority

Interest(0.00) (1.77) 0.25 (0.25) (1.77) (0.21)

Profit After Tax 6.53 2.03 (2.36) 9.82 16.02 18.29 -12%

` Billion IT & TS Fin.

Services *

Devl.

Projects

L&T &

Others (Incl.

Eliminations)

L&T Group

Annexure 2: Group Balance Sheet

57

* Includes Insurance Business

^ Partly netted off from Capital Employed in Reported Segment

Sep-15 Mar-15Inc /

(Dec)

Net Worth (Excl. Pref. Cap.) 24.3 35.9 61.4 300.2 421.9 409.1 12.8

Minority Interest 0.0 43.2 10.4 7.0 60.5 50.0 10.5

Borrowings 6.9 462.1^ 296.7^ 216.9 982.6 905.7 77.0

Deferred Payment Liabilities - - 111.0 - 111.0 30.3 80.7

Other Current & Non-Current Liab. 17.5 27.1 31.1 491.4 567.1 542.9 24.2

Total Sources 48.8 568.2 510.7 1,015.5 2,143.2 1,938.0 205.1

Net Segment Assets 48.8 568.2 510.7 1,015.5 2,143.2 1,938.0 205.1

Total Applications 48.8 568.2 510.7 1,015.5 2,143.2 1,938.0 205.1

L&T Group

` Billion IT & TS Fin.

Services *

Devl.

Projects

L&T &

Others (Incl.

Eliminations)