101

Learn to Earn : Investment 101 Mar 7 th , 2018 Picture credit: http://www.telegraph.co.uk/

Learn to Earn : Investment 101

Mar 7th, 2018Picture credit: http://www.telegraph.co.uk/

Audiences/Assumptions/Objectives

Audiences

New Young LA , ผทยงไมไดลงทนอยางจรงจง

Assumptions- สามารถออมเงนเพอลงทนในระยะยาวได- อยากเพมผลตอบแทนจากการลงทน ภายใตความเสยงระดบหนงท

ยอมรบไดObjectives

เปนแนวทางเบองตนส าหรบการลงทน (สวนบคคล) อยางสมาเสมอในระยะยาว เพอผลตอบแทนทดในระดบความเสยงทเหมาะสม

3

“วชาหนงทสาคญทสดในโลกซงโรงเรยนมธยมในอเมรกาไมไดสอน คอ ”

“หลกการเงนเปนหลกทแสนธรรมดาและเขาใจงาย ขอแรกกคอ เงนออมเทากบเงนลงทน เงนในกระปกออมสนหรอในขวดโหลของคณไมนบเปนการลงทน ทวาเมอใดทคณนาเงนนนไปฝากธนาคาร ซอพนธบตร หรอซอหนบรษท เมอนนคณกาลงลงทน”

“คณคงไดยนหลายตอหลายคนทพร าบอกคณวา การศกษาเปนสงส าคญ เรยนดๆ ตอไปจะไดมหนาทการงานทด มเงนเดอนสงๆ แตสงทพวกเขาไมไดบอกคณกคอ ในระยะยาวแลวการท าเงนไดมากเทาใด ไมใชตวก าหนดวาคณจะมงคงหรอร ารวยหรอไมในอนาคต แตมนอยทวาคณสามารถใชใหเงนเหลานน ทางานใหคณไดอยางไรจากการออมและการลงทน”

การลงทน

4

Peter Lynch ‘s past performance

http://www.morssglobalfinance.com/tiger-woods-and-investment-gurus-lose-their-touch-question-do-they-ever-get-it-back/

https://thepfengineer.com/2016/07/18/deconstructing-peter-lynch/

Annualized

return 29.06%

Annualized

return 15.52%

Session 1

Break

Session 2

Q&A

1. Hr 10

Mins

10

Mins

30

Mins

Investment

Stock

Investing1. Hr 10

Mins

Work shop 1

• อนาคตอยากเปนอะไร แผนระยะสน/กลาง/ยาวเชน 15 ป แรก / 15 ป ถดไป

• สงทคาดหวงจากการสมมนาในครงน

7

https://www.slideshare.net/Anjiyaa/speculation-vs-investment

Investing vs

Speculating

https://archieyuki30.wordpress.com/author/archieyuki30/page/5/

Is this an investment?

Why do we need to invest?

Real Return = Nominal Return - Inflationhttp://1077thejewel.com/inflation-rate-dummies-101-think/

ฝากเงน bank ได 1.8% - เงนเฟอ 2.0% = ผลตอบแทนทแทจรงตดลบ 0.2%

1. Key Factors for

Successful Investment

2. Investment Framework3. Asset Allocation

Personal Investment

12

Investment

Warren Buffett

http://www.businessinsider.com/warren-buffett-berkshire-hathaway-vs-sp-500-2016-2

http://awealthofcommonsense.com/2015/03/buffetts-performance-by-decade/

“Word of Wisdoms”

15

http://www.azquotes.com/quote/1420708

17

http://izquotes.com/quote/26798

1. Key Factors for

Successful Investment

2. Investment Framework3. Asset Allocation

Personal Investment

18

Investment

Investment Analysis and Portfolio Management : Reilly & Brown

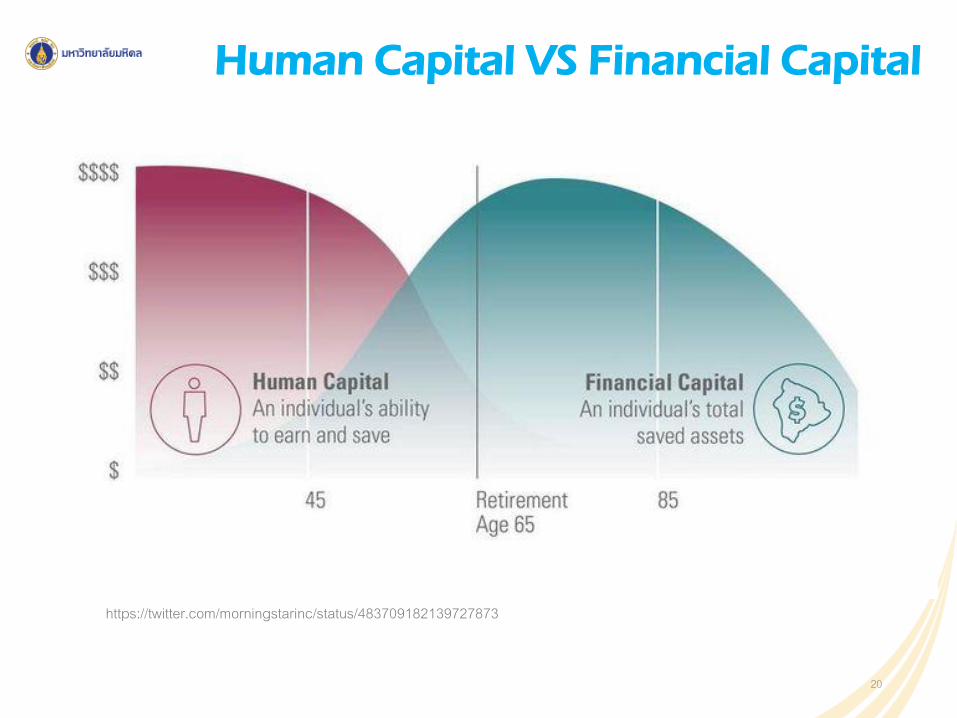

Human Capital VS Financial Capital

20

https://twitter.com/morningstarinc/status/483709182139727873

Life Cycle Investment Goals

1. Near-term high –priority goals >> Not high-risk investments• House / Car / A Trip / College exp

2. Long- term high – priority goals >> Higher-risk investments• Financial Independence (retire at a certain age)

3. Lower-priority goals >> well-developed policy• Purchase a new car every few years.

• Redecorate the home with expensive furnishings.

• Luxurious vacation

การควบคมอารมณ/ วนยในการลงทน

Investment Framework

ความ เขาใจ

รจกตนเอง รจกตลาด

พลงของแกว 3ประการ

Asset Allocation

Product Selection-กองทนตางๆ

Morning Star

»LTF/RMF»กองทนตรา

สารทนอน

เลนหน

-Emergency Liquidity-Human Capital Asset »Earning

Ability»Stability

-Risk/Return Objectives-Constraints

-Markets/ Products (Equity/ Fixed Income)-Risk/Return

Amount / Return / Time

(Greed/Fear; Mr Market)22

ความเขาใจ ตนเอง และ ตลาด

-Risk/Return Objectives-Constraints

-Markets/Products-Risk/Return

LiquidityTime HorizonTaxesUnique Circumstances

EquityFixed IncomeAlternatives

23

High risk, High expected return

https://www.thewealthwisher.com/2017/01/03/compounding-8th-wonder-world/

พลงของแกว 3 ประการ

FV = PV(1+i)t

FV = คาเงนในอนาคตPV = คาเงนปจจบนหรอเงนตน (ขนอยกบความสามารถและบญกรรมทม)i = อตราดอกเบย (ขนอยกบความสามารถและวนยในการลงทน)t = งวดเวลา (ทกคนมเทากน)

25

“1”

“2”

“3”

พลงของแกว 3 ประการ

(308,416)

60,000

(544,993)

17, 1,478,725

34, 4,359,133

17, 1,794,339

34, 6,626,087

(9,000,000)

(7,000,000)

(5,000,000)

(3,000,000)

(1,000,000)

1,000,000

3,000,000

5,000,000

7,000,000

9,000,000

(1,000,000)

(800,000)

(600,000)

(400,000)

(200,000)

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1 2 3 4 5 6 7 8 9 10111213141516171819202122232425262728293031323334353637383940414243444546474849505152535455

Cu

m W

ealt

h (

Bah

t)

Year

ly C

ash

flo

w (

Bah

t)

Year

(i=4%) CF (Baht) LH (i=6%) CF (Baht) LH (i=4%) Cum Wealth (Baht) RH (i=6%) Cum Wealth (Baht) RH

Invest 60K yearly for 34 yrs (5K monthly) => Withdraw yearly for 20 yrs

6%

4%

25,701/m

45,416/m

26

พลงของแกว 3 ประการ

Invest 120K yearly for 34 yrs (10K monthly) => Withdraw yearly for 20 yrsfor retirement

(616,832)

120,000

(1,089,986)

17, 3,588,678

34, 13,252,174

(14,000,000)

(9,000,000)

(4,000,000)

1,000,000

6,000,000

11,000,000

(2,800,000)

(1,800,000)

(800,000)

200,000

1,200,000

2,200,000

1 2 3 4 5 6 7 8 9 101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354

Cu

m W

ealt

h (

Bah

t)

Year

ly C

ash

flo

w (

Bah

t)

Year

(i=4%) CF (Baht) LH (i=6%) CF (Baht) LH (i=4%) Cum Wealth (Baht) RH (i=6%) Cum Wealth (Baht) RH

51,402/m

90,832/m

6%

4%

-1,089,986/year=>90,832/monthif i=6%, Principal = 13.2M

-Should also consider inflation

27

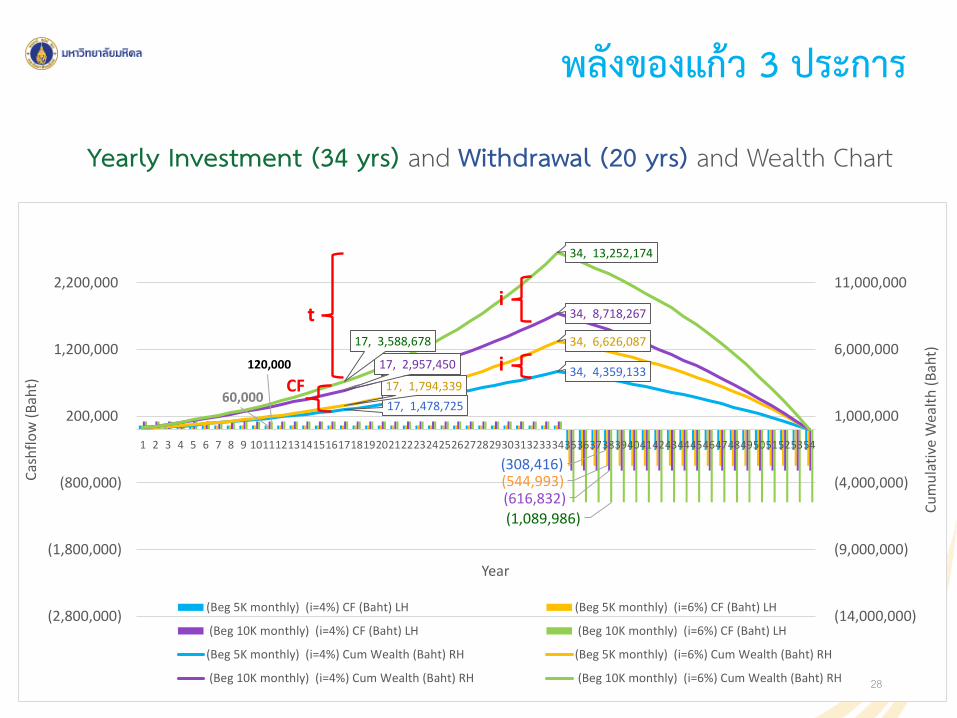

พลงของแกว 3 ประการ

(308,416)

60,000

(544,993)(616,832)

120,000

(1,089,986)

17, 1,478,725

34, 4,359,133 17, 1,794,339

34, 6,626,087

17, 2,957,450

34, 8,718,267

17, 3,588,678

34, 13,252,174

(14,000,000)

(9,000,000)

(4,000,000)

1,000,000

6,000,000

11,000,000

(2,800,000)

(1,800,000)

(800,000)

200,000

1,200,000

2,200,000

1 2 3 4 5 6 7 8 9 101112131415161718192021222324252627282930313233343536373839404142434445464748495051525354

Cu

mu

lati

ve W

ealt

h (

Bah

t)

Cas

hfl

ow

(B

aht)

Year

(Beg 5K monthly) (i=4%) CF (Baht) LH (Beg 5K monthly) (i=6%) CF (Baht) LH

(Beg 10K monthly) (i=4%) CF (Baht) LH (Beg 10K monthly) (i=6%) CF (Baht) LH

(Beg 5K monthly) (i=4%) Cum Wealth (Baht) RH (Beg 5K monthly) (i=6%) Cum Wealth (Baht) RH

(Beg 10K monthly) (i=4%) Cum Wealth (Baht) RH (Beg 10K monthly) (i=6%) Cum Wealth (Baht) RH

Yearly Investment (34 yrs) and Withdrawal (20 yrs) and Wealth Chart

t

CFi

i

28

“ควรลงทนตงแตอายยง

นอย”

1. Key Factors for

Successful Investment

2. Investment Framework3. Asset Allocation

30

Investment

Equity

Debt

Asset

หน PTT• ปนผลแตละป 3%• มลคาเพมของราคาหน 18%

IPO 35฿ ป 2544ปจจบน ราคา 550฿

หนก PTT• ดอกเบยตาม

สญญา 4-5%

ผลตอบแทนรวม 21% ตอป• Limited downside• Unlimited upside

• Limited downside• Limited upside

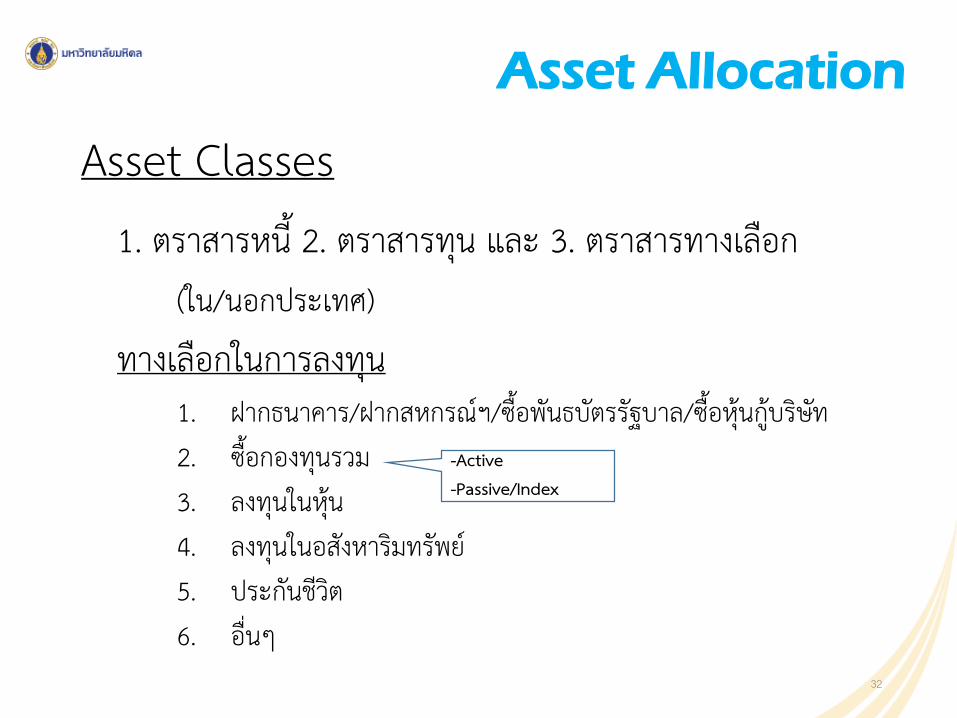

Asset Allocation

Asset Classes1. ตราสารหน 2. ตราสารทน และ 3. ตราสารทางเลอก

(ใน/นอกประเทศ)

ทางเลอกในการลงทน1. ฝากธนาคาร/ฝากสหกรณฯ/ซอพนธบตรรฐบาล/ซอหนกบรษท2. ซอกองทนรวม3. ลงทนในหน4. ลงทนในอสงหารมทรพย5. ประกนชวต6. อนๆ

-Active-Passive/Index

32

1. บญชออมทรพย ตราสารเงน ตราสารหน

ระยะสน

ขอเสยอตราดอกเบยต ามาก / นอยกวาเงนเฟอ

คาแนะนาเหมาะแกการพกเงน/สะสมเงนจนกวาจะมเงนมากพอไปลงทนอยางอน แตในระยะยาวไมท าประโยชนแกคณมากเทาใด

ขอดมดอกเบย / ไดเงนคนคอนขางเรว / โอกาสขาดทนนอยมาก

ขอด-ขอเสยของการลงทนพนฐาน 5 วธ (1)

33

2. ของสะสมมคา

ขอดความสขทางใจ

ขอเสยอาจสญหาย ถกขโมยและช ารดเสยหาย /ตองอาศยความเชยวชาญสง

คาแนะนาของสะสมมคามอะไรมากมายทตองเรยนร บางอยางคณหาไดจากหนงสอ แตสวนใหญมกจะไดมาอยางเจบปวดจากประสบการณ

ขอด-ขอเสยของการลงทนพนฐาน 5 วธ (2)

34

3. บานและทอยอาศย

ขอดคณอยไดขณะทรอใหราคาขน / ซอไดดวยเงนก

ขอเสยเงนเกบอาจเหลอนอยกวา (การเชาบาน) ในชวงแรก

คาแนะนาเปนการออมในรปแบบหนงทคนไมคอยนกถง

ขอด-ขอเสยของการลงทนพนฐาน 5 วธ (3)

35

4. เงนฝาก พนธบตรหรอหนกระยะยาว

ขอดมดอกเบยชดเจน / รก าหนดวาจะไดเงนตนคนเมอใด / โอกาสขาดทนนอย

ขอเสยอาจบาดเจบจากการขายกอนก าหนด/ ผลตอบแทนอาจนอยกวาเงนเฟอ / อาจโดนเบยวหน

คาแนะนาในระยะยาวผลตอบแทนทแทจรงอาจเปนศนย

ขอด-ขอเสยของการลงทนพนฐาน 5 วธ (4)

36

5. หน

ขอดในระยะยาวจะใหผลตอบแทนทดเสมอ

ขอเสยไมเหมาะกบการลงทนระยะสน

คาแนะนาหนนาจะเปนการลงทนทดทสดทคณท าไดนอกจากบาน

ขอด-ขอเสยของการลงทนพนฐาน 5 วธ (5)

37

Asset Allocation

Asset

Liquidity Fixed Income

Equity Alternatives

-Emergency Liquidity

-Human Cap Asset => Earning Stability/Ability

-Expected Return

38

• New Young LA สามารถทา Asset Allocation ของสนทรพยบางประเภทผาน Mutual Fund ได เชน ลงทนกองทนรวมพนธบตร กองทนรวมหน กองทนทองค า

• แลวท าไมตองลงทนในหน???

1. ในระยะยาวจะใหผลตอบแทนทดเสมอ

2. ชนะเงนเฟอ

3. กระจายความเสยง***หนนาจะเปนการลงทนทดทสดทคณท าไดนอกจากบาน***

Recommendation

39

Stock Investing

1. Stock investingA. Introduction

B. Cap gain vs Dividend

C. Fundamental vs Technical

2. Key Ideas

3. Case Study : KISS Investing

4. Ponzi Scheme

High Risk High Expected Return

Asian crisis -87%

Hamburger crisis -53%

European crisis -25%

Introduction :Primary Market (IPO) vs Secondary Market

• ตลาดหน• Brokers

http://marketbusinessnews.com/financial-glossary/primary-market/

Introduction :SET Index vs individual stock

Stock Index

C

B A

• Criteria >> Value or Growth , Big or Mid or

Small

• Method >> Mkt weight or Price weight

SET >> SET50 >> SET100

G.P.A. Average

height of

students

Stock Investing

1. Stock investingA. Introduction

B. Cap gain vs Dividend

C. Fundamental vs Technical

2. Key Ideas

3. Case Study : KISS Investing

4. Ponzi Scheme

Cap gain vs Dividend

Total Return = <Capital Gain/Loss> + <Dividend>

CAGR 14y

11%

CAGR

14y 7%

11% 4%7%

นลท. ก ไดรบ ตลาดหนจาย?? บรษทจาย

Investing Diagram

Stock Investing

Equity Funds

Passive Style / Index / ETF

Active Style

Individual Stocks

Fundamental Technical

Active vs Passive : 1 years

Active vs Passive : 5 years

Active vs Passive : 10 years

Stock Investing

1. Stock investingA. Introduction

B. Cap gain vs Dividend

C. Fundamental vs Technical

2. Key Ideas

3. Case Study : KISS Investing

4. Ponzi Scheme

Fundamental vs Technical

• Value calculated

using various

economic factors

• Buy when price

falls below

intrinsic value

• Uses price movements

and patterns on charts

to predict future price

movements

• Buy when trader sees a

price formation that has

a high probability of

moving into profit in the

near future.

คนวนของหนงหมนชม.“เราทกคนสามารถทจะมความเชยวชาญในดานใดดานหนงได หากเราใชเวลากบมนอยางต า 10,000 ชวโมง หนงหมนชวโมงน ไมไดหมายความวาท า 1 หนงชวโมงเเลวนอนทบมนอก 9999 ชวโมง 10,000 ชวโมงนหมายความวา คณตองท ามนใหครบ

10,000 ชวโมง ไมวาจะในเรองของ ดนตร กฬา ภาษา คอมพวเตอร การวาดรป คณตศาสตร หรอ การเงน การลงทน”

ถาหากเราทมเทฝกฝนกบสงนนวนละกชวโมงและจะตองใชเวลากป

ฝกวนละ 1 ชม. ใชเวลา 10000 วน หรอ 27 ปกวาๆฝกวนละ 2 ชม. ใชเวลา 5000 วน หรอ ราว 14 ปฝกวนละ 4 ชม. ใชเวลา 2500 วน หรอ ประมาณ 7 ปฝกวนละ 8 ชม. ใชเวลา 1250 วน หรอ เกอบๆ 4 ปฝกวนละ 12 ชม. ใชเวลา 833 วน หรอ ประมาณ 2 ป

http://www.unigang.com/Article/18731

Stock Investing

1. Stock investingA. Introduction

B. Cap gain vs Dividend

C. Fundamental vs Technical

2. Key Ideas

3. Case Study : KISS Investing

4. Ponzi Scheme

https://www.pinterest.com/pin/382102349626516521/

Key Ideas (for success in long term investing)

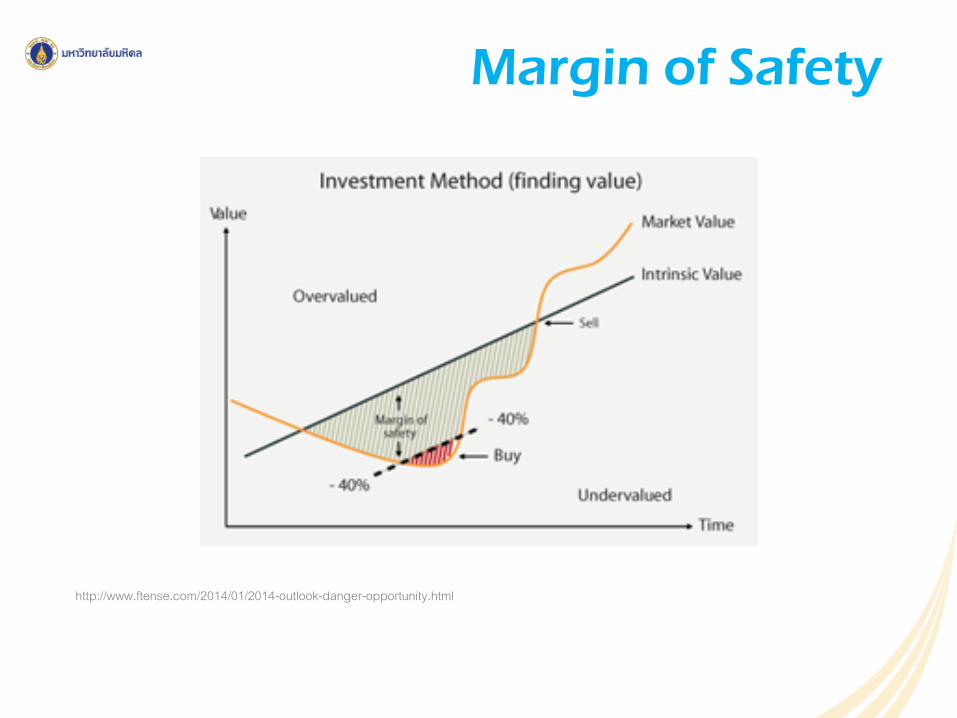

1.Margin of Safety

2.Mr. Market

Margin of Safety

http://www.ftense.com/2014/01/2014-outlook-danger-opportunity.html

ttps://www.safalniveshak.com/value-investing-course-margin-of-safety/

M.O.S.

http://www.netnethunter.com/benjamin-graham-still-relevant-or-a-complete-waste-of-time/

Mr. Market

Greed

Fear

MrMarket

Stock Investing

1. Stock investingA. Introduction

B. Cap gain vs Dividend

C. Fundamental vs Technical

2. Key Ideas

3. Case Study : KISS Investing

4. Ponzi Scheme

Case Study : KISS Investing

K I S SKeep It Simple & Stupid

Investor A was born in 1982

https://pantip.com/topic/36363380

Nintendo

When he was 12 years old

Barbies

Walt Disney

When he was 15 years old

Nike

McDonalds

When he was 18 years old

Louis Vuitton

Nokia

https://www.sbs.com.au/topics/science/fundamentals/explainer/great-science-behind-terrifying-history-atomic-bomb

Amazon

When he was 23 years old

Amazon

When he was 23 years old

https://www.rd.com/advice/saving-money/13-things-lottery-winners/

Chevron

Apple

When he was 27 years old

https://www.rd.com/advice/saving-money/13-things-lottery-winners/

STARBUCKS

https://www.rd.com/advice/saving-money/13-things-lottery-winners/

Black Berry

https://www.sbs.com.au/topics/science/fundamentals/explainer/great-science-behind-terrifying-history-atomic-bomb

Coach

When he was 30 years old

https://www.sbs.com.au/topics/science/fundamentals/explainer/great-science-behind-terrifying-history-atomic-bomb

Honda

When he was 32 years old

When he was 33 years old

http://www.businessinsider.com/foab-vs-moab-bomb-damage-2017-4

No. Year Stock BGNEND 2018

HPRAnn

ReturnIndex BGN END HPR

Ann Return

Better than index

1 1994 Nintendo 100 756 656% 9% Nikkei 100 107 7% 0% 9%2 1994 Mattel 100 100 0% 0% S&P 100 585 485% 8% -8%3 1997 Disney 100 418 318% 7% S&P 100 340 240% 6% 1%4 1997 Nike 100 729 629% 10% S&P 100 340 240% 6% 4%5 2000 MCD 100 494 394% 9% S&P 100 200 100% 4% 5%6 2000 LV 100 356 256% 7% S&P 100 200 100% 4% 3%7 2000 Nokia 100 8 -92% -13% S&P 100 200 100% 4% -17%8 2005 Amazon 100 4,194 4094% 33% S&P 100 222 122% 6% 27%9 2005 Chevron 100 184 84% 5% S&P 100 222 122% 6% -2%

10 2009 Apple 100 1,451 1351% 35% S&P 100 398 298% 17% 18%11 2009 Star Buck 100 1,363 1263% 34% S&P 100 398 298% 17% 17%

12 2009Black berry

100 34 -66% -11% S&P 100 398 298% 17% -28%

13 2012 Coach 100 65 -35% -7% S&P 100 198 98% 12% -19%14 2014 Honda 100 97 -3% -1% Nikkei 100 144 44% 10% -10%15 2015 Twitter 100 72 -28% -10% S&P 100 130 30% 9% -20%

Total 1,500 10,321 588% 1,500 4,082 172%

The Outcome

Durable competitive advantage Companies

Price with high M.O.S.

Great return in the long

run99.99%Mr.

Market

Full time investor

Discipline

Stock Investing

1. Stock investingA. Introduction

B. Cap gain vs Dividend

C. Fundamental vs Technical

2. Key Ideas

3. Case Study : KISS Investing

4. Ponzi Scheme

Ponzi Scheme / แชรลกโซ

https://decentralize.today/bitcoin-is-the-total-opposite-of-a-ponzi-scheme-heres-why-4d795f0ed?gi=d102c12ae6b9http://englishbookgeorgia.com/blogebg/interesting-words-and-expressions-theres-no-such-thing-as-a-free-lunch/

101

Q & A

Mahidol University

Asset Management CenterTel 02-849-6069, 96