66

LIFE INSURANCE BUSINESS IN JAPAN The Life Insurance Association of Japan 2016-2017

LIFE INSURANCE BUSINESS

IN JAPAN

The Life Insurance Association of Japan

2016-2017

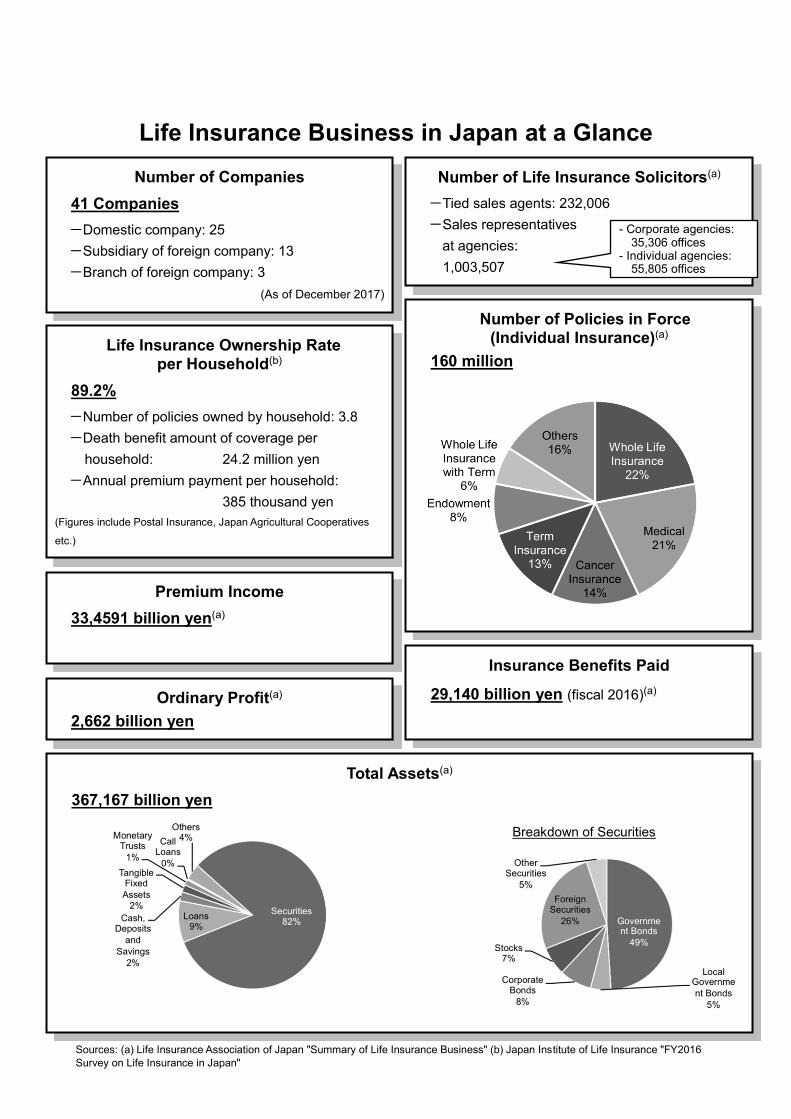

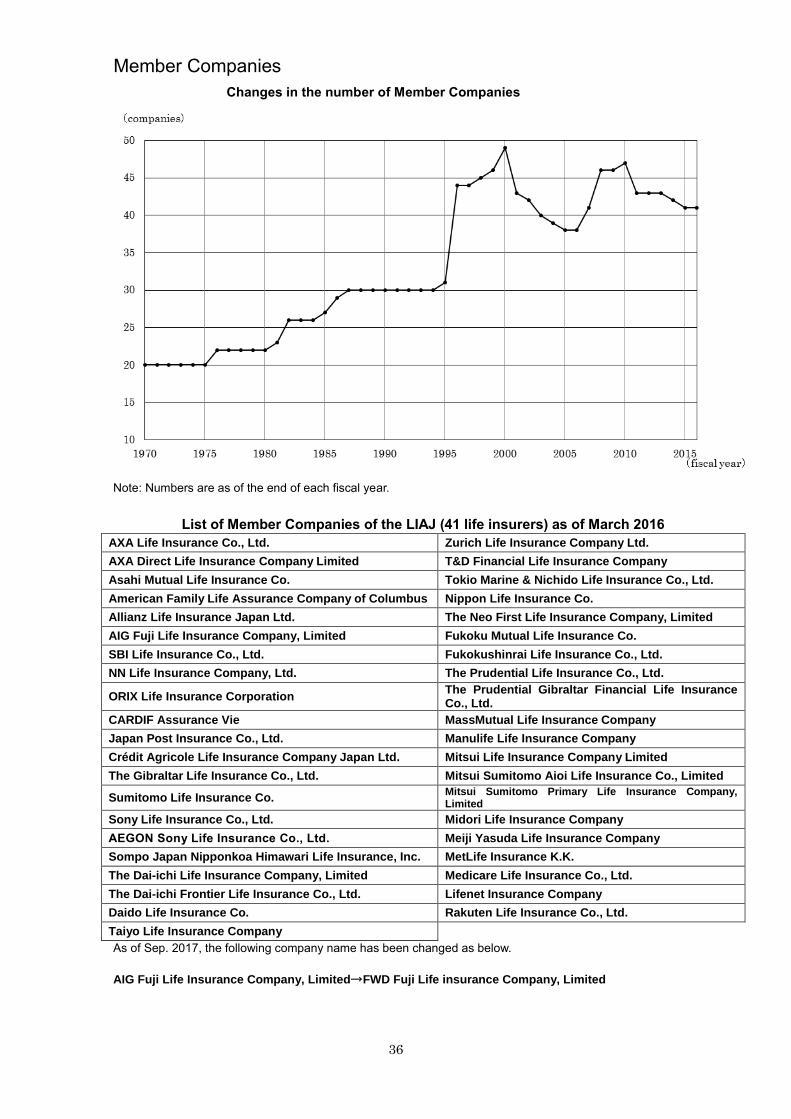

Life Insurance Business in Japan at a Glance

Number of Companies

41 Companies

-Domestic company: 25

-Subsidiary of foreign company: 13

-Branch of foreign company: 3

(As of December 2017)

Life Insurance Ownership Rate per Household(b)

89.2%

-Number of policies owned by household: 3.8

-Death benefit amount of coverage per

household: 24.2 million yen

-Annual premium payment per household:

385 thousand yen

(Figures include Postal Insurance, Japan Agricultural Cooperatives

etc.)

Ordinary Profit(a)

2,662 billion yen

Number of Life Insurance Solicitors(a)

-Tied sales agents: 232,006

-Sales representatives

at agencies:

1,003,507

Sources: (a) Life Insurance Association of Japan "Summary of Life Insurance Business" (b) Japan Institute of Life Insurance "FY2016

Survey on Life Insurance in Japan"

Premium Income

33,4591 billion yen(a)

Number of Policies in Force (Individual Insurance)(a)

160 million

Insurance Benefits Paid

29,140 billion yen (fiscal 2016)(a)

Total Assets(a)

367,167 billion yen

- Corporate agencies: 35,306 offices - Individual agencies: 55,805 offices

Breakdown of Securities

Table of Contents

Part 1 Life Insurance in Numbers ··································· 1

Part 2 The Life Insurance Association of Japan (LIAJ) ·

·················································································· 37

1. The LIAJ’s Topics for Fiscal 2016 ····························· 38

1. Promotion of Friendly Life Insurance Services for the Elderly ······ 38

2. Promotion of Insurance Education ······································ 39

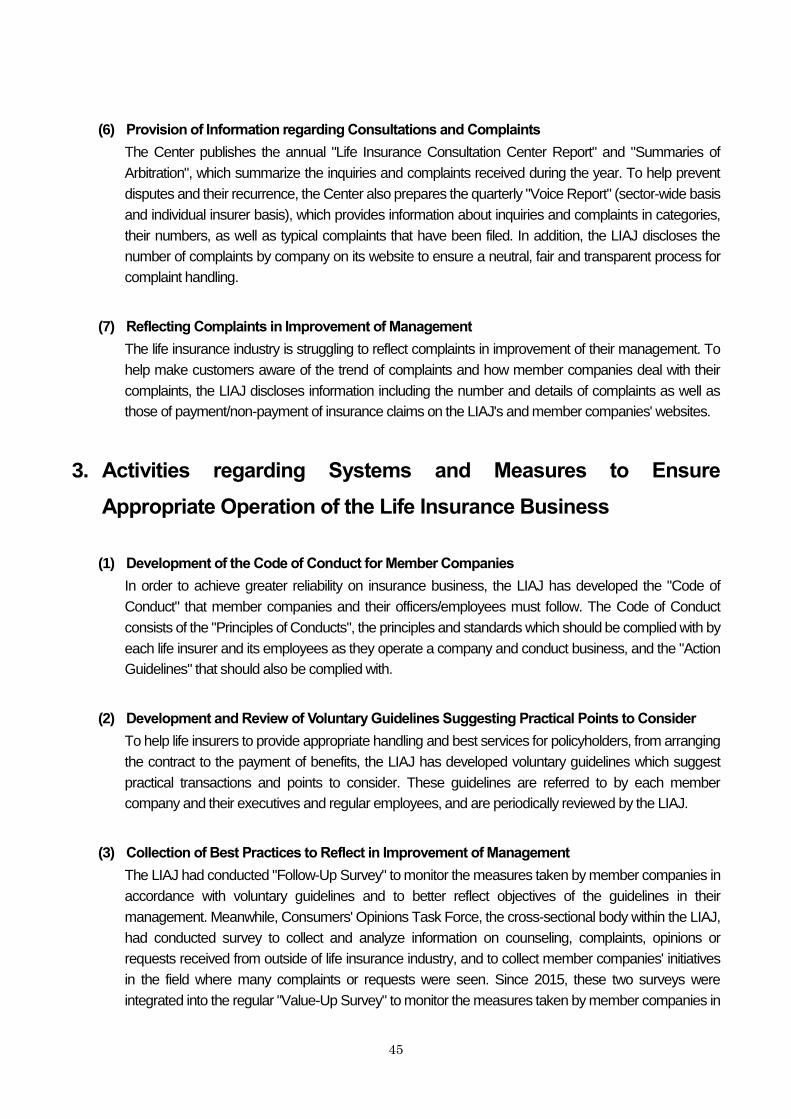

2. The LIAJ's Key Activities ········································ 42

1. Activities to Provide Information and Promote Understanding on

the Life Insurance Business ············································· 42

2. Consultation Services, Complaint Processing and Dispute

Resolution Operations regarding Life Insurance Business ········· 43

3. Activities regarding Systems and Measures to Ensure

Appropriate Operation of the Life Insurance Business ·············· 45

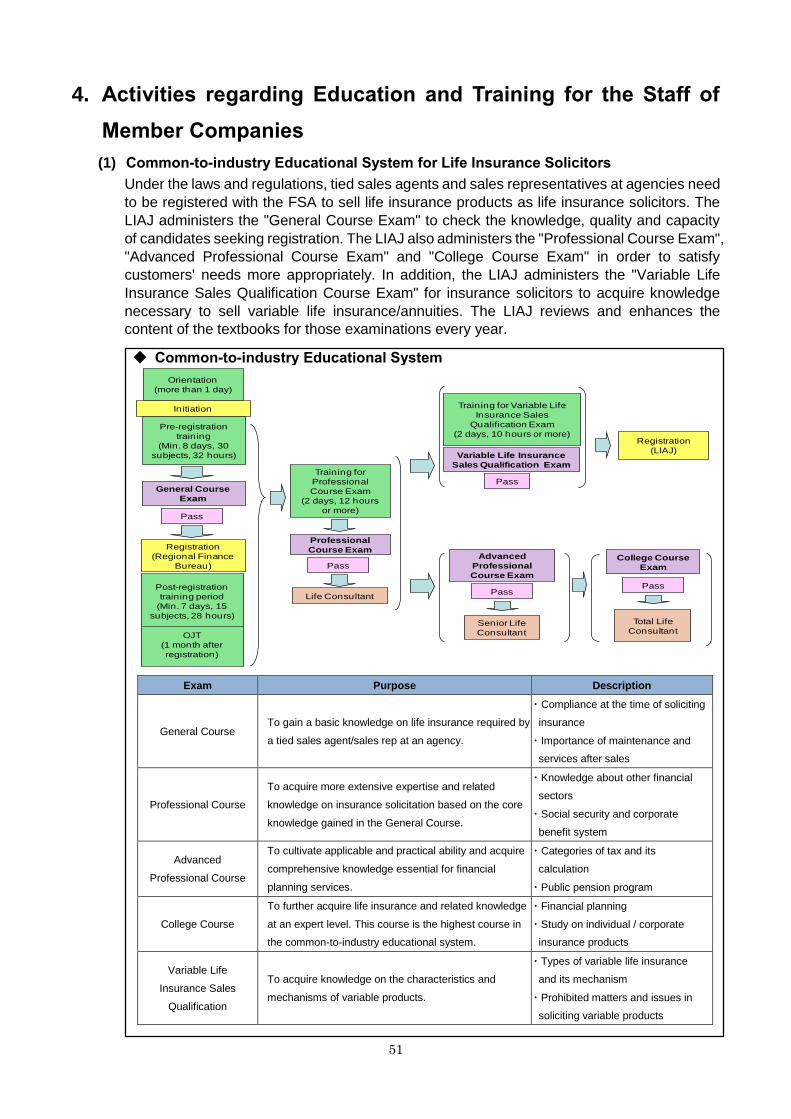

4. Activities regarding Education and Training for the Staff of

Member Companies ······················································· 51

5. Activities regarding Making Requests and Proposals to relevant

Authorities, Agencies and Organizations ······························ 52

6. Activities to Fulfill Social Responsibilities····························· 54

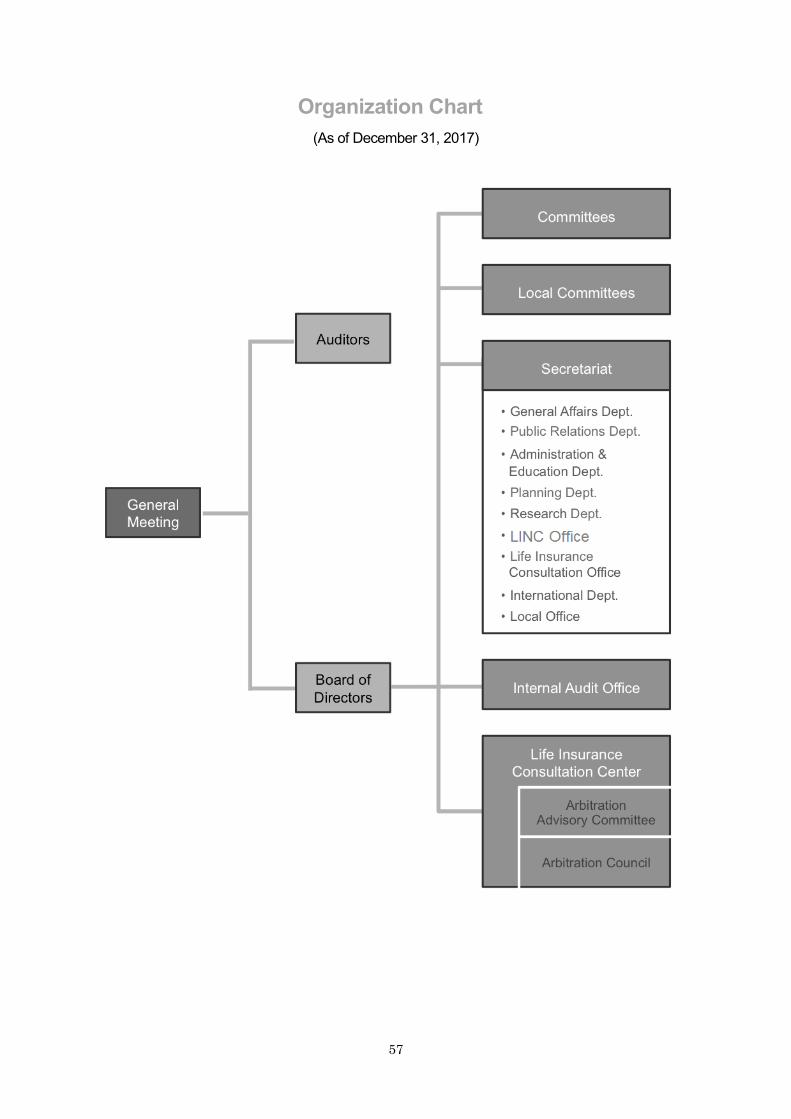

3. The LIAJ’s Organization Profile ································ 56

Note: In this document, the LIAJ's activities are categorized in accordance with its Business

Plan for Fiscal Year 2016. This “Life Insurance Business in Japan” does not specifically introduce (V) Research and study activities regarding the theory and practice of life insurance and (VIII) Other activities considered necessary to achieve the goals of the LIAJ.

1

Part 1

Life Insurance in Numbers

(Reprint of Life Insurance Fact Book 2017)

2

Introduction

The Life Insurance Fact Book summarizes key performance indicators of life

insurance companies operating in Japan. We hope that this report will provide a

better understanding of the life insurance business in Japan.

Please note that the data of Japan Post Insurance has been included in the

figures since fiscal 2008; therefore, some figures show the data excluding Japan

Post Insurance in order to maintain continuity with the previous data before its

inclusion. The data of Japan Post Insurance is not included in figures for fiscal

2007 and 2008 for the purpose of counting years (e.g. “for the Xth successive

years” or “for the first time in X years”).

In addition to this report, the LIAJ provides detailed statistical data of the life

insurance market in Japan; please refer to such data as necessary.

*The LIAJ is not responsible for any losses that may occur through the use of the

information contained in this CD-ROM.

3

Contents

Highlights of Business Results ································································ 4

I Underwriting Results ········································································ 6 1. Insurance Products for Individual ····················································· 6

(1) Individual Insurance ································································· 6 (2) Individual Annuity Insurance ···················································· 10 (3) Annualized Premium ······························································ 12 (4) Hospitalization and Surgery Protection ······································ 13 (5) Statistical Data by Gender, Age and Prefecture ··························· 14

2. Insurance Products for Groups ······················································ 19 (1) Group Insurance ··································································· 19 (2) Group Annuity Insurance ························································ 21

II Profit and Loss ············································································· 23

1. Insurance Related Profit and Loss ················································· 23 (1) Premium Income ··································································· 23 (2) Insurance Benefits Paid ·························································· 24

2. Investment Income and Expenses ················································· 26 3. Operating Expenses ···································································· 28 4. Ordinary Profits and Basic Profits ·················································· 28

III Investment Results ········································································ 29

1. Total Assets ··············································································· 29 2. Securities ·················································································· 30 3. Loans ······················································································· 31 4. Tangible Fixed Assets (Real Estate) ··············································· 33

IV Liabilities and Net Assets ································································ 33

Reference ························································································· 35

Distribution Channels and Sales Force ················································· 35 Member Companies ········································································· 36

4

Highlights of Business Results - The Trend of Individual Insurance Policies -

As of the end of fiscal 2016, the amount of policies in force (the amount of coverage for major protections such as death protection) for individual insurance was 862,905 billion yen (100.5% y/y) and increased from the previous year for the second successive year. The number of policies in force as of the end of fiscal 2016 was 167.72 million, increasing for the ninth successive year. Though the amount of new policies (including converted contracts) decreased from the previous year to 68,478 billion yen (98.8% y/y),decrease in lapses and surrenders owing to insurers’ efforts over the past years to maintain existing policies lead to the increase in policies in force. As to the type of new policies for individual policies in terms of amount (excluding converted contracts), suspension of savings-type products due to the lower domestic interest rates and consequent lower assumed interest rates for single-premium products resulted in the decreased sale particularly for whole life insurance from the previous year. Meanwhile, the sales of term insurance, which is largely protection-based, increased from the previous year to 35,977 billion yen (112.8%y/y). (See: pages 6 to 9) y/y)

As to the annualized premium (the amount of premium income which a life insurer would receive in one year, under the assumption that premium is equally divided and paid throughout the entire contract period) of policies in force, it amounted to 27.4 trillion yen (including 6.2 trillion yen for "third-sector") at the end of fiscal 2016, increasing steadily since fiscal 2006 when the record started. With small amount insurance products of policies increasing such as medical insurance, annualized premium is referred to as an additional indicator that supports the amount of policies.(See: page 12)

Note: The amount of annualized premium of "third-sector" includes the amount of premium to be allocated for paying medical coverage (e.g. benefits for hospitalization/surgery), living benefits (e.g. benefits for specified disease/long-term care), and premium waiver benefits (e.g. benefits due to specified disease or long-term care, but excluding disability).

19.2

31.8

4.9

2.4

16.6

35.9

5.1

1.5

0

5

10

15

20

25

30

35

40

Whole Life

Insurance

(Total)

Term

Insurance

Endowment

Insurance

Variable

Insurance

(trillion yen)Amount of newpolicies (fiscal2015)

Amount of newpolicies (fiscal2016)

Note: "Whole Life Insurance (Total)" includes whole life insurance, whole life with term rider and whole life with variable accumulation rate.

19.4 19.8 20.4 21.3 21.7 22.7 23.8 24.4 25.2 26.1 27.4

4.4 4.5 4.7 4.8 5.0 5.2 5.3 5.5 5.7 5.9 6.2

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

(trillion yen)Annualized Premium of Policies in Force

"Third-Sector"

Note: Including individual annuity insurance

861 857 862

0

20

40

60

80

100

120

140

160

180

0

100

200

300

400

500

600

700

800

900

1,000

2012 2013 2014 2015 2016

百万

Amount of Policies in Force

Number of Policies in Force

(million)

865 858

(trillion yen)

5

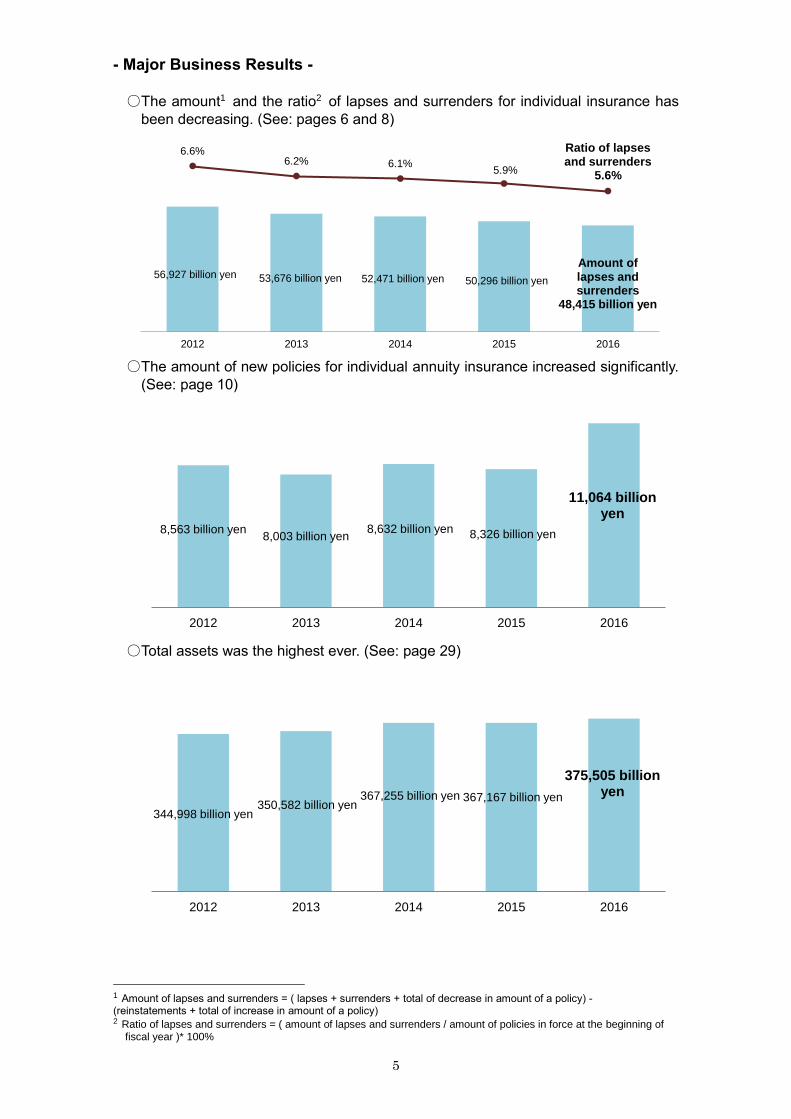

- Major Business Results - ○The amount1 and the ratio2 of lapses and surrenders for individual insurance has

been decreasing. (See: pages 6 and 8)

○The amount of new policies for individual annuity insurance increased significantly.

(See: page 10)

○Total assets was the highest ever. (See: page 29)

1 Amount of lapses and surrenders = ( lapses + surrenders + total of decrease in amount of a policy) - (reinstatements + total of increase in amount of a policy) 2 Ratio of lapses and surrenders = ( amount of lapses and surrenders / amount of policies in force at the beginning of

fiscal year )* 100%

56,927 billion yen 53,676 billion yen 52,471 billion yen 50,296 billion yen

Amount of lapses and surrenders

48,415 billion yen

6.6%6.2% 6.1%

5.9%

Ratio of lapses and surrenders

5.6%

2012 2013 2014 2015 2016

8,563 billion yen8,003 billion yen

8,632 billion yen 8,326 billion yen

11,064 billion yen

2012 2013 2014 2015 2016

344,998 billion yen350,582 billion yen

367,255 billion yen 367,167 billion yen

375,505 billion yen

2012 2013 2014 2015 2016

6

I Underwriting Results

1 Insurance Products for Individual3

(1) Individual Insurance

I. New Policies

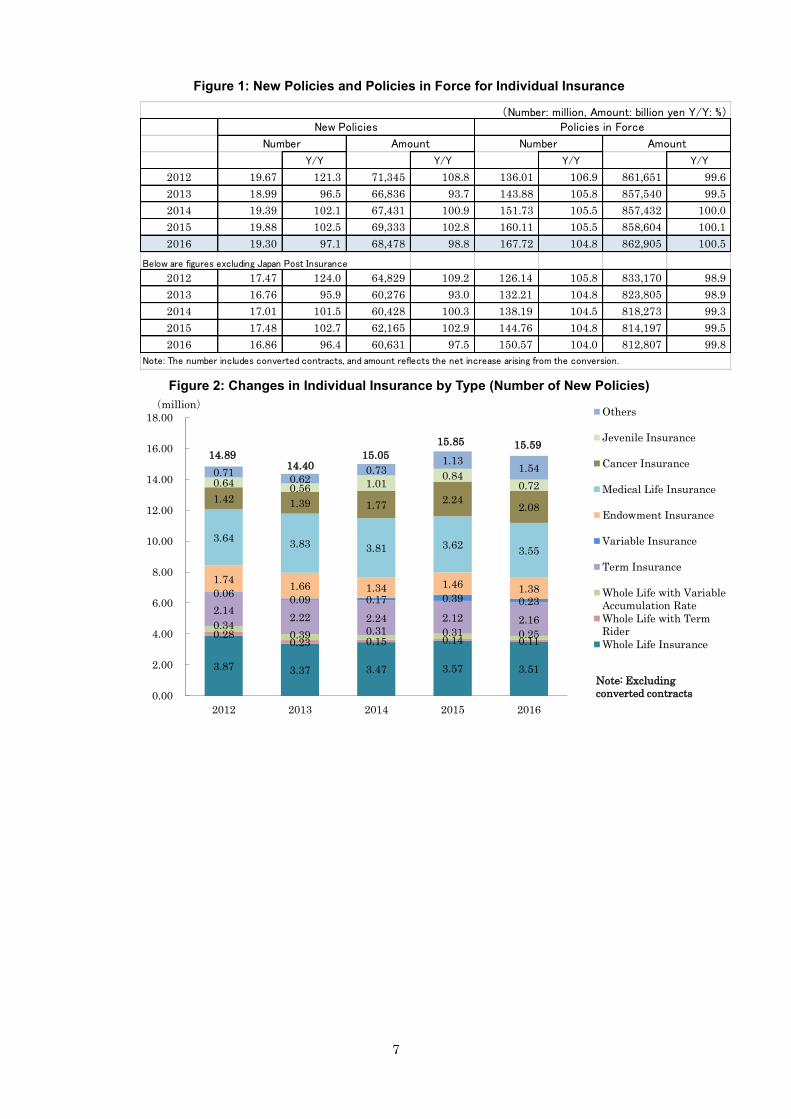

The number of new policies for individual insurance (including converted contracts) was 19.3 million (97.1% y/y), and the new policies amount4 (reflecting the net increase arising from the conversion) was 68,478billion yen (98.8% y/y). [Figure 1]

Both the number and the amount of new policies decreased from the previous year in fiscal 2016 notwithstanding the increase trend over the several years supported by increased sales of medical insurance and whole life insurance. This turn-around reflects the negative developments such as suspended sales of single premium payment products due to the reduction in the standard assumed interest rate for such products following the further downward shift of the yield in the domestic investment market.

By type of new policies for individual insurance (excluding converted contracts), medical insurance ranked top in number (3.55 million, 22.8% of the total), followed by whole life insurance (3.51 million, 22.5%), term insurance (2.16 million, 13.9%), cancer insurance (208 million, 13.4%), and endowment insurance (1.38 million, 8.9%), with the ranks switched between term insurance and cancer insurance from the previous year. [Figure 2]

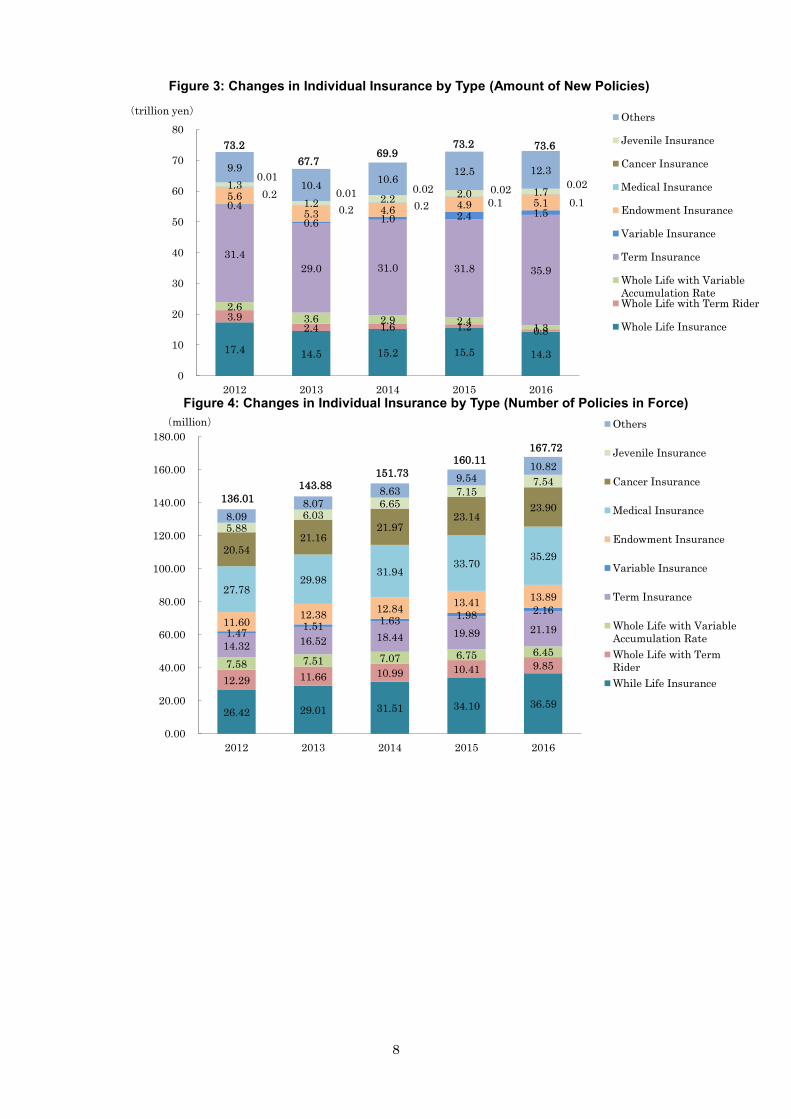

Of the total amount of new policies for individual insurance (excluding converted contracts), term insurance ranked top (35,977 billion yen, 48.9% of the total), followed by whole life insurance (14,377 billion yen, 19.5%), endowment insurance (5,194 billion yen, 7.1%), Juvenile insurance(1,781billion, 2.4%), variable insurance (1,558 billion, 2.1%), with Juvenile insurance moving up in the ranking. [Figure 3]

II. Policies in Force

The number of policies in force for individual insurance was 167.72 million (104.8% y/y), and the amount of policies in force was 862,905 billion yen (100.5% y/y). [Figure 1]

The number of policies in force increased for the ninth successive year. Despite the fact that the insured amount of policies in force had been decreasing due to the current trend of increasing medical protection while reducing death protection, it increased for the second successive year.

As for the number of policies in force for individual insurance, whole life insurance ranked top (36.59 million, 21.8% of the total), followed by medical insurance (35.29 million, 21.0%), cancer insurance (23.90 million, 14.3%), term insurance (21.19 million, 12.6%), endowment insurance (13.89 million, 8.3%) and whole life insurance with term rider (9.85 million, 5.9%). [Figure 4]

Of the total amount of policies in force for individual insurance, term insurance ranked top (268,940 billion yen, 31.2% of the total), followed by whole life insurance(176,659 billion yen, 20.5%), whole life insurance with term rider (120,368 billion yen, 13.9%), whole life insurance with variable accumulation rate (69,593 billion yen, 8.1%) and endowment insurance (45,407 billion yen, 5.3%). [Figure 5]

III. Lapses and Surrenders

The amount5 and the ratio6 of lapses and surrenders for individual insurance were 48,415 billion yen (96.3% y/y) and 5.6% (down by 0.3 points from the previous year). [Figure 6]

The amount and the ratio of lapses and surrenders decreased for the fifteenth successive year and eighth successive year, respectively.

3 The business result of individual insurance and individual annuity insurance includes those policies under which

policyholder is a corporate body and the insured is a member of the management (so-called "key person insurance"). 4 The amount of major protections such as a death protection. 5 Amount of lapses and surrenders = ( lapses + surrenders + total of decrease in amount of a policy) -

(reinstatements + total of increase in amount of a policy) 6 Ratio of lapses and surrenders = ( amount of lapses and surrenders / amount of policies in force at the beginning of

fiscal year )* 100%

7

Figure 1: New Policies and Policies in Force for Individual Insurance

Figure 2: Changes in Individual Insurance by Type (Number of New Policies)

Y/Y Y/Y Y/Y Y/Y

2012 19.67 121.3 71,345 108.8 136.01 106.9 861,651 99.6

2013 18.99 96.5 66,836 93.7 143.88 105.8 857,540 99.5

2014 19.39 102.1 67,431 100.9 151.73 105.5 857,432 100.0

2015 19.88 102.5 69,333 102.8 160.11 105.5 858,604 100.1

2016 19.30 97.1 68,478 98.8 167.72 104.8 862,905 100.5

Below are figures excluding Japan Post Insurance

2012 17.47 124.0 64,829 109.2 126.14 105.8 833,170 98.9

2013 16.76 95.9 60,276 93.0 132.21 104.8 823,805 98.9

2014 17.01 101.5 60,428 100.3 138.19 104.5 818,273 99.3

2015 17.48 102.7 62,165 102.9 144.76 104.8 814,197 99.5

2016 16.86 96.4 60,631 97.5 150.57 104.0 812,807 99.8

Note: The number includes converted contracts, and amount reflects the net increase arising from the conversion.

(Number: million, Amount: billion yen Y/Y: %)New Policies Policies in Force

Number Amount Number Amount

3.87 3.37 3.47 3.57 3.51

0.28 0.23 0.15 0.14 0.11

0.34 0.39 0.31 0.31 0.25

2.14 2.22 2.24 2.12 2.16

0.06 0.09 0.17 0.39 0.23

1.74 1.66 1.34 1.46 1.38

3.64 3.83 3.81 3.62

3.55

1.42 1.39 1.77 2.24

2.08

0.64 0.56 1.01

0.84 0.72

0.71 0.62

0.73 1.13

1.54

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

2012 2013 2014 2015 2016

(million)Others

Jevenile Insurance

Cancer Insurance

Medical Life Insurance

Endowment Insurance

Variable Insurance

Term Insurance

Whole Life with Variable

Accumulation Rate

Whole Life with Term

Rider

Whole Life Insurance

15.5914.89

14.4015.05

15.85

Note: Excluding

converted contracts

8

Figure 3: Changes in Individual Insurance by Type (Amount of New Policies)

Figure 4: Changes in Individual Insurance by Type (Number of Policies in Force)

17.4 14.5 15.2 15.5 14.3

3.9 2.4 1.6 1.2 0.8

2.6 3.6 2.9 2.4

1.3

31.4

29.0 31.0 31.8 35.9

0.4

0.6 1.0 2.4 1.5

5.6

5.3 4.6 4.9 5.1

0.2

0.2 0.2 0.1 0.1

0.01

0.01 0.02 0.02 0.02 1.3

1.2 2.2 2.0 1.7

9.9

10.4 10.6

12.5 12.3

0

10

20

30

40

50

60

70

80

2012 2013 2014 2015 2016

(trillion yen)Others

Jevenile Insurance

Cancer Insurance

Medical Insurance

Endowment Insurance

Variable Insurance

Term Insurance

Whole Life with Variable

Accumulation RateWhole Life with Term Rider

Whole Life Insurance

73.2 73.673.269.9

67.7

26.42 29.01 31.51 34.10 36.59

12.29 11.66 10.99 10.41 9.85 7.58 7.51 7.07 6.75 6.45 14.32 16.52 18.44 19.89 21.19 1.47

1.51 1.63

1.98 2.16

11.60 12.38

12.84 13.41

13.89 27.78

29.98 31.94

33.70 35.29

20.54 21.16

21.97 23.14

23.90

5.88

6.03 6.65

7.15 7.54

8.09

8.07 8.63

9.54 10.82

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

2012 2013 2014 2015 2016

(million) Others

Jevenile Insurance

Cancer Insurance

Medical Insurance

Endowment Insurance

Variable Insurance

Term Insurance

Whole Life with Variable

Accumulation Rate

Whole Life with Term

Rider

While Life Insurance

167.72

136.01

143.88151.73

160.11

9

Figure 5: Changes in Individual Insurance by Type (Amount of Policies in Force)

Figure 6: Changes in Amount and Ratio of Lapses and Surrenders of Individual Insurance

135 146 157 167 176

194 174 154 136 120

112 104 91 80 69

204 220 237 252 268

10 10 11 12 14

38 40 42 43 45 4 4 4 4 3

2 2 2 2 1

13 13 14 15 16 145 139 141 143 145

0

200

400

600

800

1,000

2012 2013 2014 2015 2016

(trillion yen)

Others

Jevenile Insurance

Cancer Insurance

Medical Insurance

Endowment Insurance

Variable Insurance

Term Insurance

Whole Life with Variable

Accumulation RateWhole Life with Term

Rider

862858857857861

56,927 53,676 52,471 50,296 48,415

6.66.2 6.1 5.9

5.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

0

20,000

40,000

60,000

80,000

100,000

2012 2013 2014 2015 2016

(%)(billion yen)

10

(2) Individual Annuity Insurance

IV. New Policies

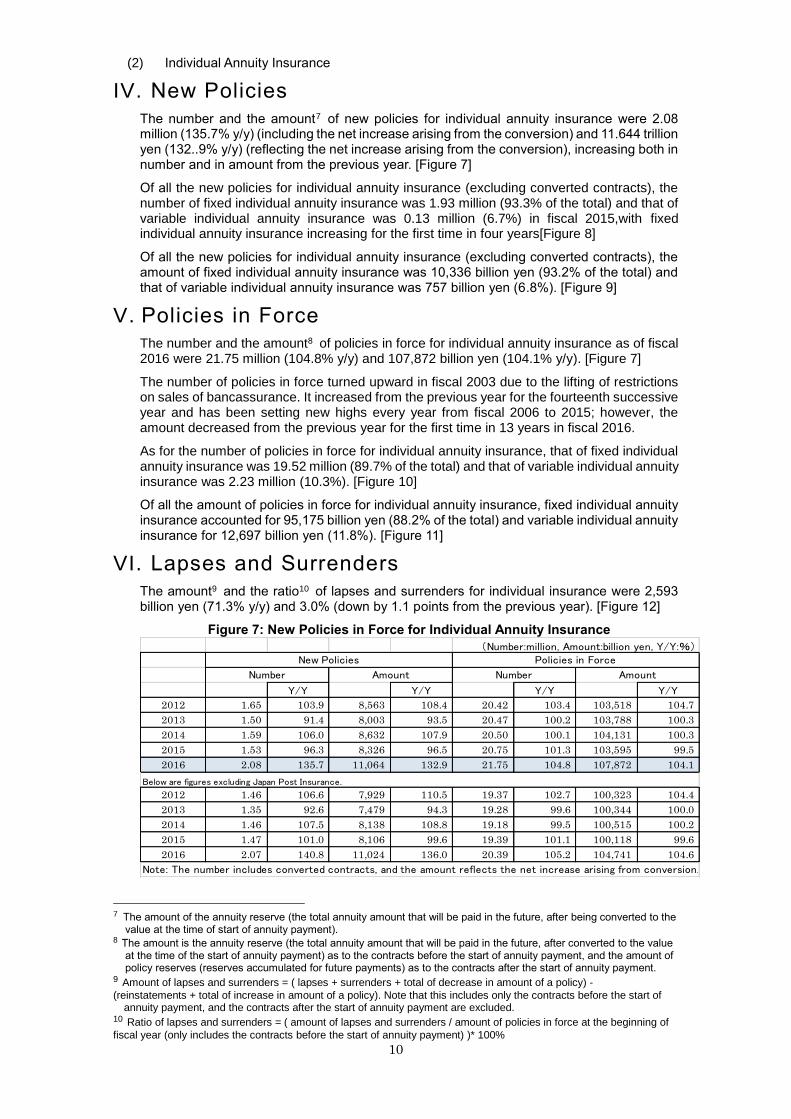

The number and the amount7 of new policies for individual annuity insurance were 2.08 million (135.7% y/y) (including the net increase arising from the conversion) and 11.644 trillion yen (132..9% y/y) (reflecting the net increase arising from the conversion), increasing both in number and in amount from the previous year. [Figure 7]

Of all the new policies for individual annuity insurance (excluding converted contracts), the number of fixed individual annuity insurance was 1.93 million (93.3% of the total) and that of variable individual annuity insurance was 0.13 million (6.7%) in fiscal 2015,with fixed individual annuity insurance increasing for the first time in four years[Figure 8]

Of all the new policies for individual annuity insurance (excluding converted contracts), the amount of fixed individual annuity insurance was 10,336 billion yen (93.2% of the total) and that of variable individual annuity insurance was 757 billion yen (6.8%). [Figure 9]

V. Policies in Force

The number and the amount8 of policies in force for individual annuity insurance as of fiscal 2016 were 21.75 million (104.8% y/y) and 107,872 billion yen (104.1% y/y). [Figure 7]

The number of policies in force turned upward in fiscal 2003 due to the lifting of restrictions on sales of bancassurance. It increased from the previous year for the fourteenth successive year and has been setting new highs every year from fiscal 2006 to 2015; however, the amount decreased from the previous year for the first time in 13 years in fiscal 2016.

As for the number of policies in force for individual annuity insurance, that of fixed individual annuity insurance was 19.52 million (89.7% of the total) and that of variable individual annuity insurance was 2.23 million (10.3%). [Figure 10]

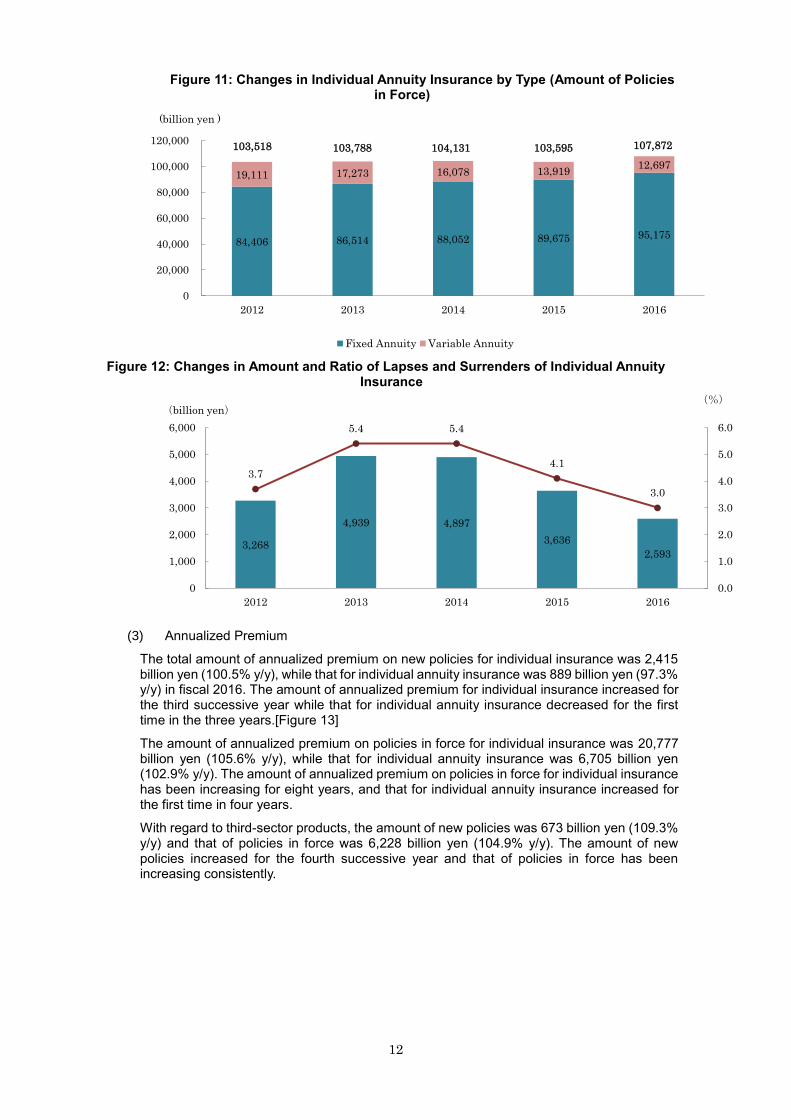

Of all the amount of policies in force for individual annuity insurance, fixed individual annuity insurance accounted for 95,175 billion yen (88.2% of the total) and variable individual annuity insurance for 12,697 billion yen (11.8%). [Figure 11]

VI. Lapses and Surrenders

The amount9 and the ratio10 of lapses and surrenders for individual insurance were 2,593 billion yen (71.3% y/y) and 3.0% (down by 1.1 points from the previous year). [Figure 12]

Figure 7: New Policies in Force for Individual Annuity Insurance

7 The amount of the annuity reserve (the total annuity amount that will be paid in the future, after being converted to the

value at the time of start of annuity payment). 8 The amount is the annuity reserve (the total annuity amount that will be paid in the future, after converted to the value

at the time of the start of annuity payment) as to the contracts before the start of annuity payment, and the amount of policy reserves (reserves accumulated for future payments) as to the contracts after the start of annuity payment.

9 Amount of lapses and surrenders = ( lapses + surrenders + total of decrease in amount of a policy) -

(reinstatements + total of increase in amount of a policy). Note that this includes only the contracts before the start of annuity payment, and the contracts after the start of annuity payment are excluded.

10 Ratio of lapses and surrenders = ( amount of lapses and surrenders / amount of policies in force at the beginning of

fiscal year (only includes the contracts before the start of annuity payment) )* 100%

(Number:million, Amount:billion yen, Y/Y:%)

Y/Y Y/Y Y/Y Y/Y

2012 1.65 103.9 8,563 108.4 20.42 103.4 103,518 104.7

2013 1.50 91.4 8,003 93.5 20.47 100.2 103,788 100.3

2014 1.59 106.0 8,632 107.9 20.50 100.1 104,131 100.3

2015 1.53 96.3 8,326 96.5 20.75 101.3 103,595 99.5

2016 2.08 135.7 11,064 132.9 21.75 104.8 107,872 104.1

2012 1.46 106.6 7,929 110.5 19.37 102.7 100,323 104.4

2013 1.35 92.6 7,479 94.3 19.28 99.6 100,344 100.0

2014 1.46 107.5 8,138 108.8 19.18 99.5 100,515 100.2

2015 1.47 101.0 8,106 99.6 19.39 101.1 100,118 99.6

2016 2.07 140.8 11,024 136.0 20.39 105.2 104,741 104.6

Below are figures excluding Japan Post Insurance.

Note: The number includes converted contracts, and the amount reflects the net increase arising from conversion.

New Policies Policies in Force

Number Amount Number Amount

11

Figure 8: Changes in Individual Annuity Insurance by Type (Number of New Policies)

Figure 9: Changes in Individual Annuity Insurance by Type

(Amount of New Policies)

Figure 10: Changes in Individual Annuity Insurance by Type (Number of Policies

in Force)

1.51.3 1.3 1.29

1.93

0.090.16 0.26 0.22

0.13

0

0.3

0.6

0.9

1.2

1.5

1.8

2.1

2.4

2012 2013 2014 2015 2016

(million)

Fixed Annuity Variable Annuity

2.07

1.521.561.471.6

8,023 7,054 7,001 6,964

10,336

526 919 1,653 1,390

757

0

2,000

4,000

6,000

8,000

10,000

12,000

2012 2013 2014 2015 2016

(billion yen)

Fixed Annuity Variable Annuity

11,094

8,3548,655

7,973

8,550

17.09 17.50 17.85 18.33 19.52

3.33 2.97 2.64 2.422.23

0.00

5.00

10.00

15.00

20.00

25.00

2012 2013 2014 2015 2016

(million)

Fixed Annuity Variable Annuity

21.7520.7520.5020.4720.42

Note: Excluding converted contracts

Note: Excluding converted contracts

12

Figure 11: Changes in Individual Annuity Insurance by Type (Amount of Policies

in Force)

Figure 12: Changes in Amount and Ratio of Lapses and Surrenders of Individual Annuity

Insurance

(3) Annualized Premium

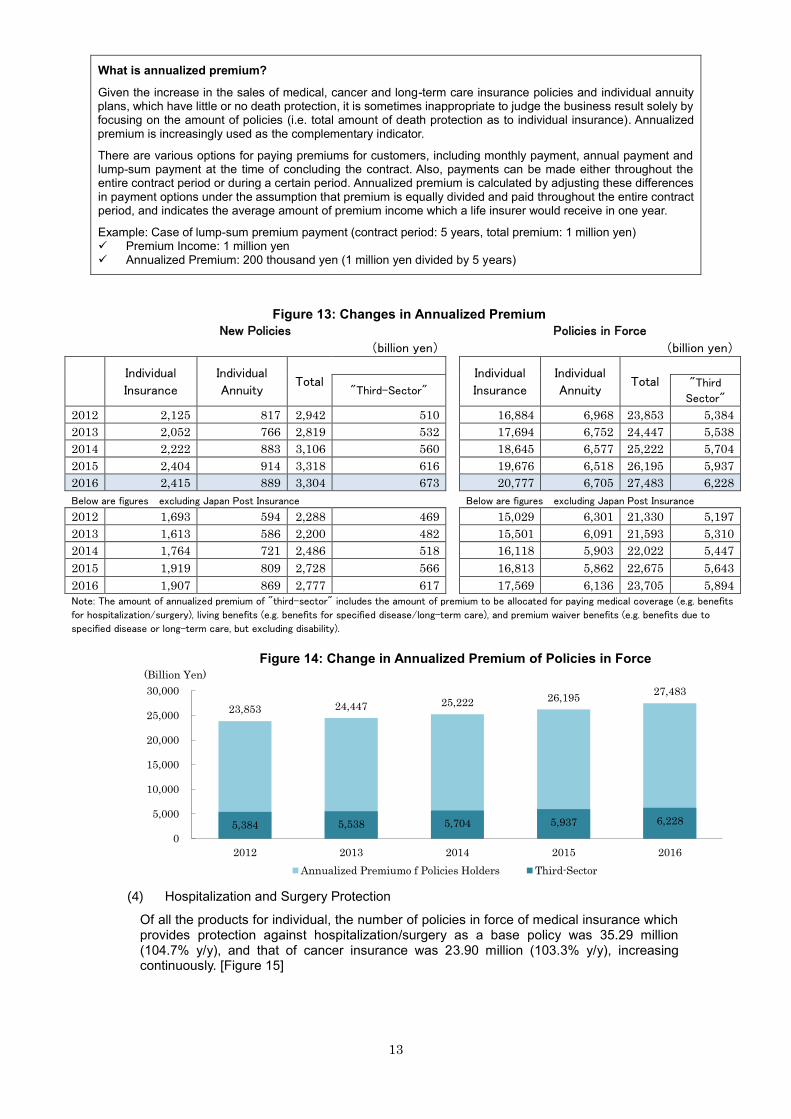

The total amount of annualized premium on new policies for individual insurance was 2,415 billion yen (100.5% y/y), while that for individual annuity insurance was 889 billion yen (97.3% y/y) in fiscal 2016. The amount of annualized premium for individual insurance increased for the third successive year while that for individual annuity insurance decreased for the first time in the three years.[Figure 13]

The amount of annualized premium on policies in force for individual insurance was 20,777 billion yen (105.6% y/y), while that for individual annuity insurance was 6,705 billion yen (102.9% y/y). The amount of annualized premium on policies in force for individual insurance has been increasing for eight years, and that for individual annuity insurance increased for the first time in four years.

With regard to third-sector products, the amount of new policies was 673 billion yen (109.3% y/y) and that of policies in force was 6,228 billion yen (104.9% y/y). The amount of new policies increased for the fourth successive year and that of policies in force has been increasing consistently.

84,406 86,514 88,052 89,675 95,175

19,111 17,273 16,078 13,919 12,697

0

20,000

40,000

60,000

80,000

100,000

120,000

2012 2013 2014 2015 2016

(billion yen )

Fixed Annuity Variable Annuity

103,788103,518 103,595104,131 107,872

3,268

4,939 4,897

3,636

2,593

3.7

5.4 5.4

4.1

3.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016

(%)(billion yen)

13

What is annualized premium?

Given the increase in the sales of medical, cancer and long-term care insurance policies and individual annuity plans, which have little or no death protection, it is sometimes inappropriate to judge the business result solely by focusing on the amount of policies (i.e. total amount of death protection as to individual insurance). Annualized premium is increasingly used as the complementary indicator.

There are various options for paying premiums for customers, including monthly payment, annual payment and lump-sum payment at the time of concluding the contract. Also, payments can be made either throughout the entire contract period or during a certain period. Annualized premium is calculated by adjusting these differences in payment options under the assumption that premium is equally divided and paid throughout the entire contract period, and indicates the average amount of premium income which a life insurer would receive in one year.

Example: Case of lump-sum premium payment (contract period: 5 years, total premium: 1 million yen) Premium Income: 1 million yen Annualized Premium: 200 thousand yen (1 million yen divided by 5 years)

Figure 13: Changes in Annualized Premium

New Policies Policies in Force

(billion yen) (billion yen)

Individual

Insurance

Individual

Annuity Total

Individual

Insurance

Individual

Annuity Total

"Third-Sector" "Third

Sector"

2012 2,125 817 2,942 510 16,884 6,968 23,853 5,384

2013 2,052 766 2,819 532 17,694 6,752 24,447 5,538

2014 2,222 883 3,106 560 18,645 6,577 25,222 5,704

2015 2,404 914 3,318 616 19,676 6,518 26,195 5,937

2016 2,415 889 3,304 673 20,777 6,705 27,483 6,228

Below are figures excluding Japan Post Insurance Below are figures excluding Japan Post Insurance

2012 1,693 594 2,288 469 15,029 6,301 21,330 5,197

2013 1,613 586 2,200 482 15,501 6,091 21,593 5,310

2014 1,764 721 2,486 518 16,118 5,903 22,022 5,447

2015 1,919 809 2,728 566 16,813 5,862 22,675 5,643

2016 1,907 869 2,777 617 17,569 6,136 23,705 5,894

Note: The amount of annualized premium of "third-sector" includes the amount of premium to be allocated for paying medical coverage (e.g. benefits

for hospitalization/surgery), living benefits (e.g. benefits for specified disease/long-term care), and premium waiver benefits (e.g. benefits due to

specified disease or long-term care, but excluding disability).

Figure 14: Change in Annualized Premium of Policies in Force

(4) Hospitalization and Surgery Protection

Of all the products for individual, the number of policies in force of medical insurance which provides protection against hospitalization/surgery as a base policy was 35.29 million (104.7% y/y), and that of cancer insurance was 23.90 million (103.3% y/y), increasing continuously. [Figure 15]

23,853 24,447 25,222 26,195 27,483

5,384 5,538 5,704 5,937 6,228

0

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015 2016

(Billion Yen)

Annualized Premiumo f Policies Holders Third-Sector

14

Figure 15: Changes in Medical and Cancer Insurance (Number of Policies in Force)

To provide medical protection, there are also other types of insurance policies which are served with medical riders. With respect to insurance policies with hospitalization and surgery coverage (the sum of riders and stand-alone medical insurance policies among individual life insurance and individual annuity insurance), the number of policies with accidental hospitalization riders in force was 76.75 million (102.1% y/y), those with sickness hospitalization riders in force was 77.33 million (102.4% y/y), and those with surgical benefit riders in force was 102.74 million (103.0% y/y). [Figure 16]

Figure 16: Changes in Medical Insurance for Hospitalization and Surgery

(Number of Policies in Force)

Note: Figures are the total of the numbers of protection under individual insurance policies and individual annuity contracts in force, both as a base policy and as a rider. Products with more than one protections are counted in each protection.

(5) Statistical Data by Gender, Age and Prefecture11

VII. By Gender

Comparing the number of new policies for individual insurance (excluding converted contracts) by gender of the insured, the ratio of females has been increasing recently to exceed that of males. In fiscal 2016, the ratio of males was slightly higher than that of the previous year. The ratio of females was 50.2%, slightly exceeding that of men at 49.8%, though the gap was narrowed. [Figure 17]

Comparing the number of new policies for individual insurance between each type of insurance product by gender of the insured in fiscal 2016, "others" including cancer insurance and medical insurance ranked top (more than 50% of the total) for male and female, followed by whole life insurance, term insurance and endowment insurance. [Figure 18]

11 Statistical data by gender, age and prefecture is based on the classification of the insured.

27.78 29.98

31.94 33.70

35.29

20.54 21.16 21.97 23.14 23.90

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

2012 2013 2014 2015 2016

(million)

Medical Insurance Cancer Insurance

70.8172.31 73.57

75.1576.75

70.4172.21

73.7175.53

77.33

92.0594.52

96.7399.74

50.00

60.00

70.00

80.00

90.00

100.00

2012 2013 2014 2015 2016

(million) 102.74

Hospitalization due to unforseen accidents Hospitalization due to sickness Surgery

15

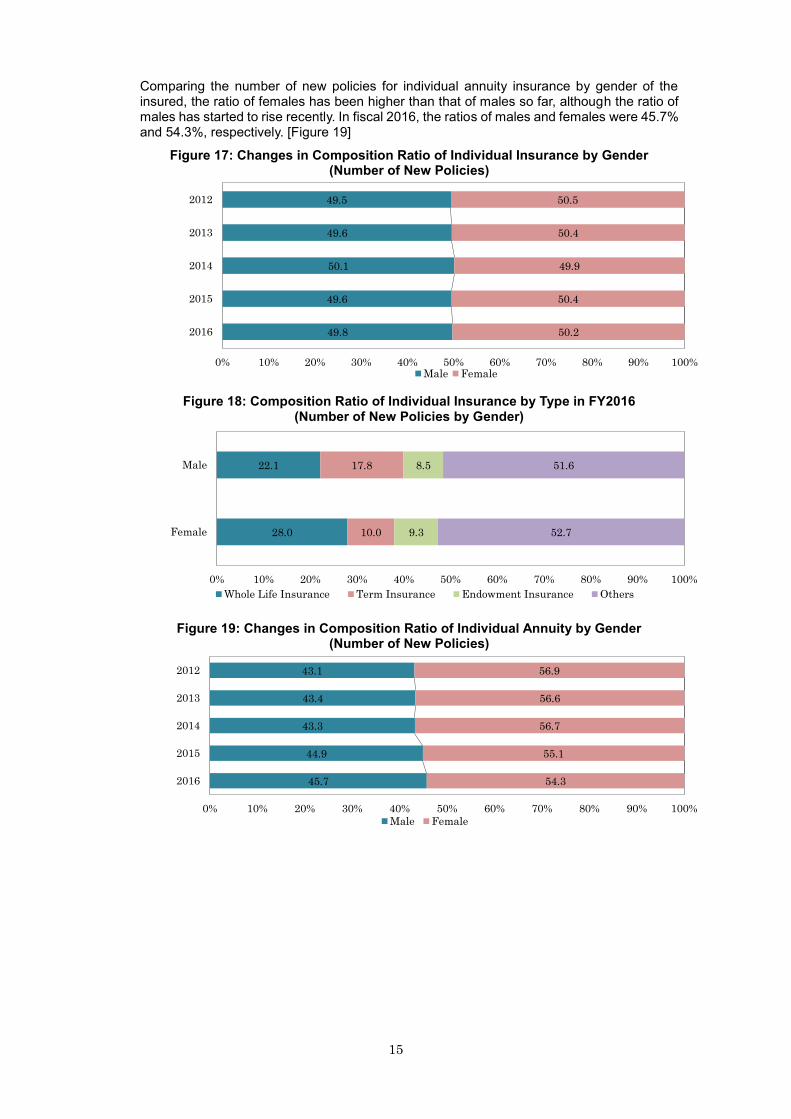

Comparing the number of new policies for individual annuity insurance by gender of the insured, the ratio of females has been higher than that of males so far, although the ratio of males has started to rise recently. In fiscal 2016, the ratios of males and females were 45.7% and 54.3%, respectively. [Figure 19]

Figure 17: Changes in Composition Ratio of Individual Insurance by Gender (Number of New Policies)

Figure 18: Composition Ratio of Individual Insurance by Type in FY2016 (Number of New Policies by Gender)

Figure 19: Changes in Composition Ratio of Individual Annuity by Gender (Number of New Policies)

49.5

49.6

50.1

49.6

49.8

50.5

50.4

49.9

50.4

50.2

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2012

2013

2014

2015

2016

Male Female

22.1

28.0

17.8

10.0

8.5

9.3

51.6

52.7

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Male

Female

Whole Life Insurance Term Insurance Endowment Insurance Others

43.1

43.4

43.3

44.9

45.7

56.9

56.6

56.7

55.1

54.3

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2012

2013

2014

2015

2016

Male Female

16

VIII. By Age

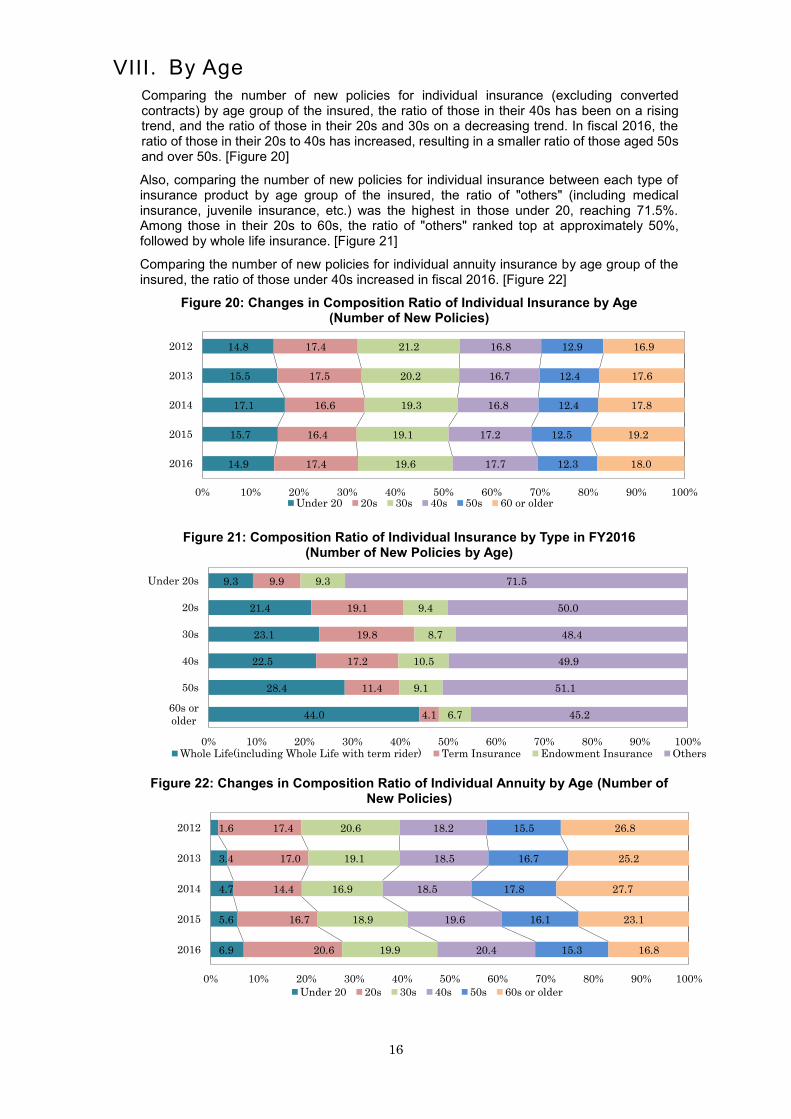

Comparing the number of new policies for individual insurance (excluding converted contracts) by age group of the insured, the ratio of those in their 40s has been on a rising trend, and the ratio of those in their 20s and 30s on a decreasing trend. In fiscal 2016, the ratio of those in their 20s to 40s has increased, resulting in a smaller ratio of those aged 50s and over 50s. [Figure 20]

Also, comparing the number of new policies for individual insurance between each type of insurance product by age group of the insured, the ratio of "others" (including medical insurance, juvenile insurance, etc.) was the highest in those under 20, reaching 71.5%. Among those in their 20s to 60s, the ratio of "others" ranked top at approximately 50%, followed by whole life insurance. [Figure 21]

Comparing the number of new policies for individual annuity insurance by age group of the insured, the ratio of those under 40s increased in fiscal 2016. [Figure 22]

Figure 20: Changes in Composition Ratio of Individual Insurance by Age (Number of New Policies)

Figure 21: Composition Ratio of Individual Insurance by Type in FY2016 (Number of New Policies by Age)

Figure 22: Changes in Composition Ratio of Individual Annuity by Age (Number of New Policies)

14.8

15.5

17.1

15.7

14.9

17.4

17.5

16.6

16.4

17.4

21.2

20.2

19.3

19.1

19.6

16.8

16.7

16.8

17.2

17.7

12.9

12.4

12.4

12.5

12.3

16.9

17.6

17.8

19.2

18.0

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2012

2013

2014

2015

2016

Under 20 20s 30s 40s 50s 60 or older

9.3

21.4

23.1

22.5

28.4

44.0

9.9

19.1

19.8

17.2

11.4

4.1

9.3

9.4

8.7

10.5

9.1

6.7

71.5

50.0

48.4

49.9

51.1

45.2

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Under 20s

20s

30s

40s

50s

60s or

older

Whole Life(including Whole Life with term rider) Term Insurance Endowment Insurance Others

1.6

3.4

4.7

5.6

6.9

17.4

17.0

14.4

16.7

20.6

20.6

19.1

16.9

18.9

19.9

18.2

18.5

18.5

19.6

20.4

15.5

16.7

17.8

16.1

15.3

26.8

25.2

27.7

23.1

16.8

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2012

2013

2014

2015

2016

Under 20 20s 30s 40s 50s 60s or older

17

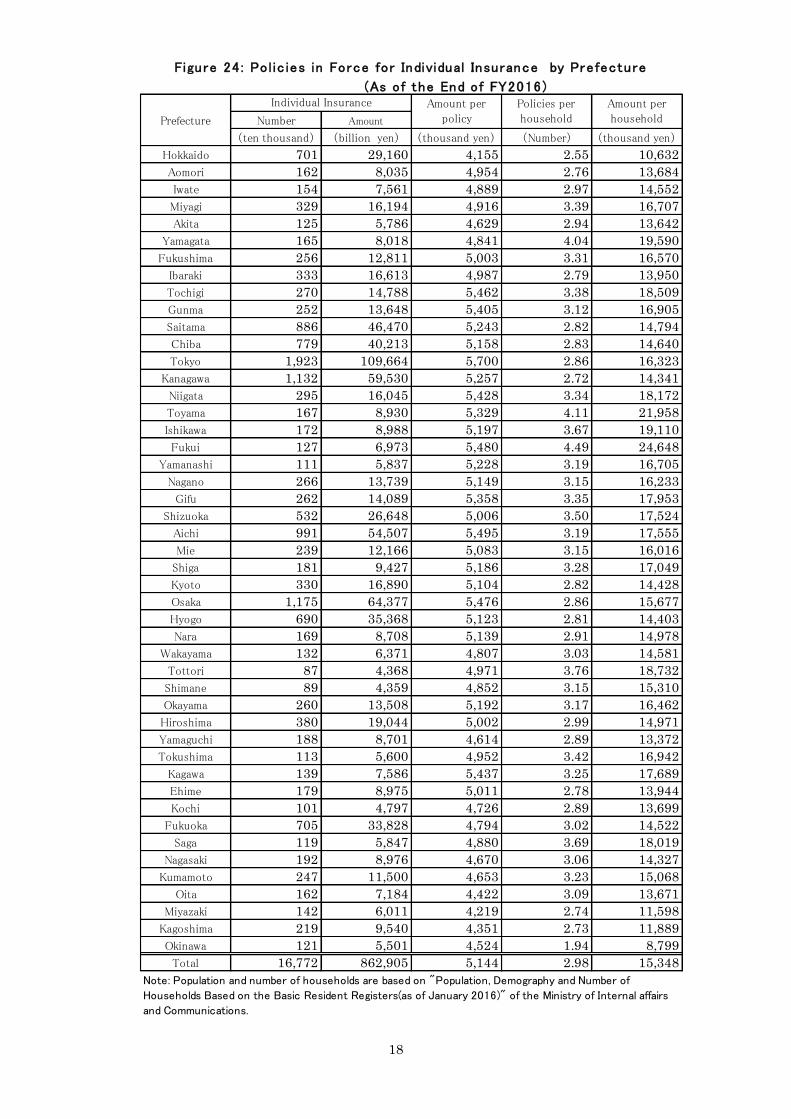

IX. By Prefecture

Regarding the details of individual insurance by each prefecture, Figure 23 provides the details of new policies (excluding converted contracts), and Figure 24 provides details of policies in force.

Prefecture Numver Amount

ten thousand (billion yen) (thousand yen) (Number) (thousand yen)(ten thousand)(ten thousand)

Hokkaido 67 2,503 3,709 0.24 912 534 274

Aomori 15 587 3,897 0.25 1,000 131 58

Iwate 14 610 4,178 0.28 1,175 127 51

Miyagi 30 1,353 4,484 0.31 1,396 230 96

Akita 11 432 3,672 0.27 1,020 102 42

Yamagata 15 631 4,056 0.38 1,541 111 40

Fukushima 23 1,094 4,686 0.30 1,415 192 77

Ibaraki 30 1,331 4,429 0.25 1,117 290 119

Tochigi 23 1,128 4,745 0.29 1,412 195 79

Gunma 21 1,087 4,696 0.27 1,346 194 80

Saitama 76 3,700 4,826 0.24 1,178 719 314

Chiba 67 3,123 4,633 0.24 1,137 615 274

Tokyo 200 10,596 5,275 0.29 1,577 1,304 671

Kanagawa 97 4,796 4,922 0.23 1,155 896 415

Niigata 25 1,227 4,737 0.29 1,390 228 88

Toyama 13 647 4,723 0.33 1,591 105 40

Ishikawa 15 718 4,599 0.33 1,527 114 47

Fukui 11 551 4,713 0.41 1,949 78 28

Yamanashi 10 457 4,416 0.29 1,308 83 34

Nagano 22 1,055 4,591 0.27 1,247 209 84

Gifu 23 1,157 4,985 0.29 1,474 201 78

Shizuoka 47 2,159 4,539 0.31 1,420 368 152

Aichi 88 4,699 5,289 0.28 1,513 731 310

Mie 22 1,013 4,571 0.29 1,334 179 75

Shiga 16 764 4,566 0.30 1,382 139 55

Kyoto 30 1,437 4,755 0.25 1,227 251 117

Osaka 111 5,799 5,201 0.27 1,412 864 410

Hyogo 61 3,025 4,884 0.25 1,231 550 245

Nara 14 683 4,671 0.25 1,175 136 58

Wakayama 12 521 4,219 0.28 1,193 97 43

Tottori 7 329 4,155 0.34 1,414 57 23

Shimane 8 339 4,072 0.29 1,192 68 28

Okayama 23 1,105 4,668 0.28 1,347 190 82

Hiroshima 35 1,710 4,814 0.27 1,344 281 127

Yamaguchi 17 742 4,213 0.27 1,140 139 65

Tokushima 11 461 4,179 0.33 1,397 75 33

Kagawa 12 636 4,927 0.30 1,484 98 42

Ehime 17 761 4,405 0.26 1,183 139 64

Kochi 9 372 4,003 0.26 1,065 72 35

Fukuoka 68 3,169 4,597 0.29 1,360 506 232

Saga 11 477 4,245 0.34 1,471 83 32

Nagasaki 18 1,051 4,129 0.30 1,239 138 62

Kumamoto 24 1,123 4,670 0.31 1,471 178 76

Oita 15 624 4,025 0.29 1,188 116 52

Miyazaki 15 576 3,798 0.29 1,111 111 51

Kagoshima 21 903 4,118 0.27 1,125 166 80

Okinawa 14 598 4,117 0.23 957 145 62

Total 1,559 73,607 4,719 0.27 1,309 12,558 5,622

3 the population does not include non-Japanese residents.

2.The figures are now policies excluding converted contracts.

Figure 23 : New Pol ic ies for Individual Insurance by Prefecture (FY2016)

Individual Insurance Amount per

policy

Policies per

household

Amount per

householdPopulation Household

* 1.Population and number of households are based on"Population, Demography, and Number of House holds based on the

Basic Resident Registers(as of 1 January 2016)" of the Ministry of Internal Affairs and Communications.

18

Prefecture Number Amount

(ten thousand) (billion yen) (thousand yen) (Number) (thousand yen)

Hokkaido 701 29,160 4,155 2.55 10,632

Aomori 162 8,035 4,954 2.76 13,684

Iwate 154 7,561 4,889 2.97 14,552

Miyagi 329 16,194 4,916 3.39 16,707

Akita 125 5,786 4,629 2.94 13,642

Yamagata 165 8,018 4,841 4.04 19,590

Fukushima 256 12,811 5,003 3.31 16,570

Ibaraki 333 16,613 4,987 2.79 13,950

Tochigi 270 14,788 5,462 3.38 18,509

Gunma 252 13,648 5,405 3.12 16,905

Saitama 886 46,470 5,243 2.82 14,794

Chiba 779 40,213 5,158 2.83 14,640

Tokyo 1,923 109,664 5,700 2.86 16,323

Kanagawa 1,132 59,530 5,257 2.72 14,341

Niigata 295 16,045 5,428 3.34 18,172

Toyama 167 8,930 5,329 4.11 21,958

Ishikawa 172 8,988 5,197 3.67 19,110

Fukui 127 6,973 5,480 4.49 24,648

Yamanashi 111 5,837 5,228 3.19 16,705

Nagano 266 13,739 5,149 3.15 16,233

Gifu 262 14,089 5,358 3.35 17,953

Shizuoka 532 26,648 5,006 3.50 17,524

Aichi 991 54,507 5,495 3.19 17,555

Mie 239 12,166 5,083 3.15 16,016

Shiga 181 9,427 5,186 3.28 17,049

Kyoto 330 16,890 5,104 2.82 14,428

Osaka 1,175 64,377 5,476 2.86 15,677

Hyogo 690 35,368 5,123 2.81 14,403

Nara 169 8,708 5,139 2.91 14,978

Wakayama 132 6,371 4,807 3.03 14,581

Tottori 87 4,368 4,971 3.76 18,732

Shimane 89 4,359 4,852 3.15 15,310

Okayama 260 13,508 5,192 3.17 16,462

Hiroshima 380 19,044 5,002 2.99 14,971

Yamaguchi 188 8,701 4,614 2.89 13,372

Tokushima 113 5,600 4,952 3.42 16,942

Kagawa 139 7,586 5,437 3.25 17,689

Ehime 179 8,975 5,011 2.78 13,944

Kochi 101 4,797 4,726 2.89 13,699

Fukuoka 705 33,828 4,794 3.02 14,522

Saga 119 5,847 4,880 3.69 18,019

Nagasaki 192 8,976 4,670 3.06 14,327

Kumamoto 247 11,500 4,653 3.23 15,068

Oita 162 7,184 4,422 3.09 13,671

Miyazaki 142 6,011 4,219 2.74 11,598

Kagoshima 219 9,540 4,351 2.73 11,889

Okinawa 121 5,501 4,524 1.94 8,799

Total 16,772 862,905 5,144 2.98 15,348

Note: Population and number of households are based on "Population, Demography and Number of

Households Based on the Basic Resident Registers(as of January 2016)" of the Ministry of Internal affairs

and Communications.

Figure 24 : Po l ic ies in Force for Individual Insurance by Prefecture

Individual Insurance Amount per

policy

Policies per

household

Amount per

household

(As of the End of FY2016)

19

2 Insurance Products for Groups

(1) Group Insurance

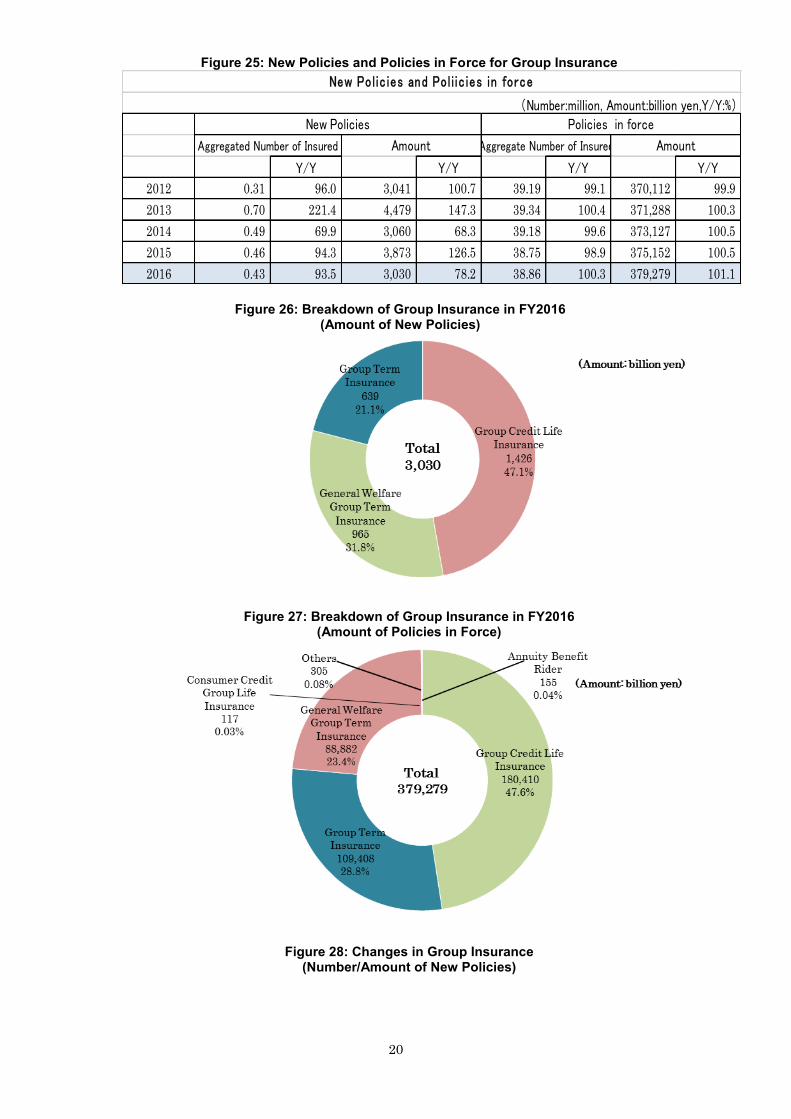

X. New Policies

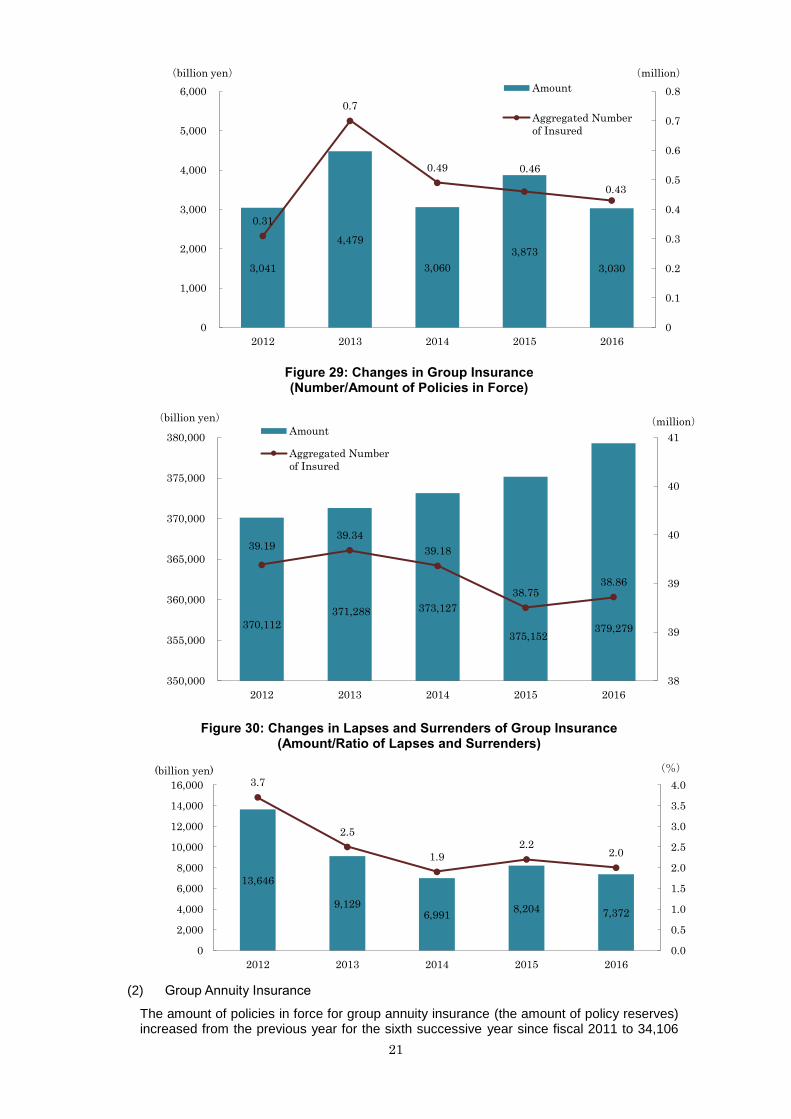

The aggregated number of the newly insured (the number after resolving double counting of insured of coinsurance undertaken by multiple insurers) and the amount of new policies for group insurance were 0.43 million (93.5% y/y) and 3,30 billion yen (78.2% y/y). [Figures 25 and 28]

Looking at the aggregated number of the newly insured, new policies for group insurance had been declining since some policies of the group term insurance existing at that time were switched to general welfare group term insurance in fiscal 1997. However, it has remained on the same level since fiscal 2006.

Of all the new policies, the amount of general welfare group term insurance ranked top (1,426 billion yen, 47.1% of the total), followed by group credit life insurance (965 billion yen, 31.8%) and group term insurance (639 billion yen, 21.1%). [Figure 26]

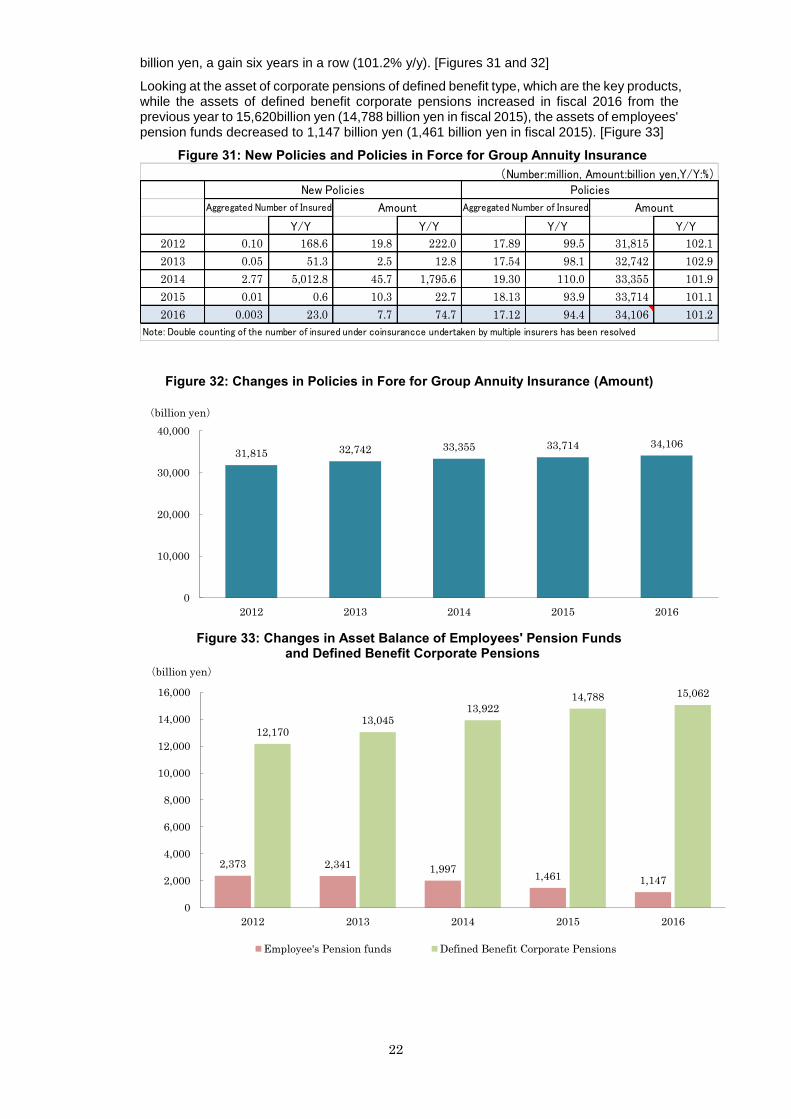

XI. Policies in Force

The number of the insured (aggregated) and the amount of policies in force were 38.86 million (100.3% y/y) and 379,279 billion yen (101.1% y/y). [Figures 25 and 29]

Of all the policies in force, the amount of group credit life insurance ranked top (180,410 billion yen, 47.6% of the total), followed by group term insurance (109,408 billion yen, 28.8%) and general welfare group term insurance (88,882 billion yen, 23.4%). [Figure 27]

XII. Lapses and Surrenders

The amount of lapses and surrenders of group insurance12 decreased from the previous year to 7,372 billion yen (89.9% y/y), and the ratio of lapses and surrenders13 also decreased to 2.0 (down by 0.2 points from the previous year). [Figure 30]

[Major Types of Group Insurance]

Group Term Insurance: A kind of voluntary insurance product companies introduce for the purpose of welfare for its members, under which the applicants become insured and pay insurance premium.

General Welfare Group Term Insurance: A kind of term insurance companies requires its all members to subscribe mandatorily in principle for the purpose of providing life security to the surviving relatives of the member. Contracts are renewed every year and the companies pay the premium.

Group Credit Life Insurance: A kind of insurance used for the conservation of loans such as housing loans, under which a debtor of the loan becomes the insured and credit providers (e.g. banks) or credit guarantee institutions become policyholders and beneficiaries. Under group credit life insurance, in case the debtor dies or become affected by prescribed state of disabilities, benefits equivalent to the amount of unpaid debts will be paid to the policyholder to clear the debt.

12 Amount of lapses and surrenders = ( lapses + surrenders + total of decrease in amount of a policy) -

(reinstatements + total of increase in amount of a policy) 13 Ratio of lapses and surrenders = ( amount of lapses and surrenders / amount of policies in force at the beginning of

fiscal year )* 100%

20

Figure 25: New Policies and Policies in Force for Group Insurance

Figure 26: Breakdown of Group Insurance in FY2016 (Amount of New Policies)

Figure 27: Breakdown of Group Insurance in FY2016 (Amount of Policies in Force)

Figure 28: Changes in Group Insurance (Number/Amount of New Policies)

Y/Y Y/Y Y/Y Y/Y

2012 0.31 96.0 3,041 100.7 39.19 99.1 370,112 99.9

2013 0.70 221.4 4,479 147.3 39.34 100.4 371,288 100.3

2014 0.49 69.9 3,060 68.3 39.18 99.6 373,127 100.5

2015 0.46 94.3 3,873 126.5 38.75 98.9 375,152 100.5

2016 0.43 93.5 3,030 78.2 38.86 100.3 379,279 101.1

New Pol ic ies and Pol i ic ies in force

(Number:million, Amount:billion yen,Y/Y:%)New Policies Policies in force

Aggregated Number of Insured Amount Aggregate Number of Insured Amount

21

Figure 29: Changes in Group Insurance (Number/Amount of Policies in Force)

Figure 30: Changes in Lapses and Surrenders of Group Insurance (Amount/Ratio of Lapses and Surrenders)

(2) Group Annuity Insurance

The amount of policies in force for group annuity insurance (the amount of policy reserves) increased from the previous year for the sixth successive year since fiscal 2011 to 34,106

3,041

4,479

3,060

3,873

3,030

0.31

0.7

0.49 0.46

0.43

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016

(million)(billion yen)

Amount

Aggregated Number

of Insured

370,112

371,288 373,127

375,152 379,279

39.19 39.34

39.18

38.75 38.86

38

39

39

40

40

41

350,000

355,000

360,000

365,000

370,000

375,000

380,000

2012 2013 2014 2015 2016

(million)(billion yen)Amount

Aggregated Number

of Insured

13,646

9,1296,991

8,204 7,372

3.7

2.5

1.92.2

2.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2013 2014 2015 2016

(%)(billion yen)

22

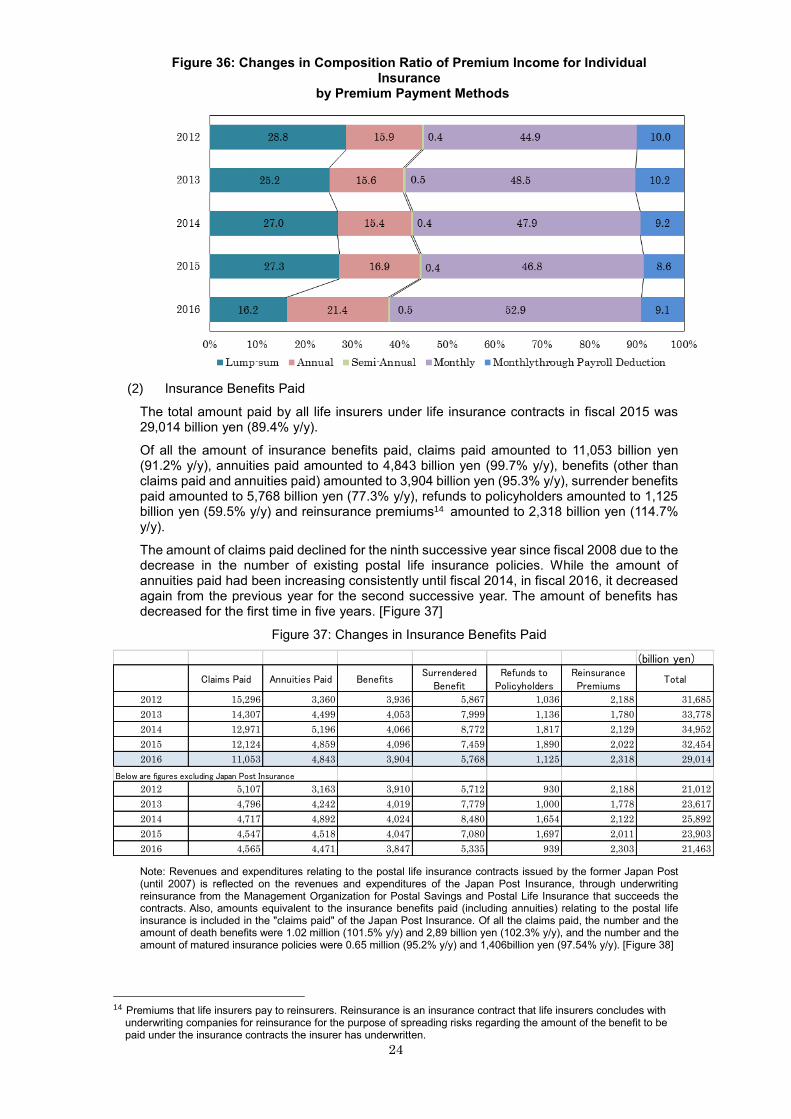

billion yen, a gain six years in a row (101.2% y/y). [Figures 31 and 32]

Looking at the asset of corporate pensions of defined benefit type, which are the key products, while the assets of defined benefit corporate pensions increased in fiscal 2016 from the previous year to 15,620billion yen (14,788 billion yen in fiscal 2015), the assets of employees' pension funds decreased to 1,147 billion yen (1,461 billion yen in fiscal 2015). [Figure 33]

Figure 31: New Policies and Policies in Force for Group Annuity Insurance

Figure 32: Changes in Policies in Fore for Group Annuity Insurance (Amount)

Figure 33: Changes in Asset Balance of Employees' Pension Funds and Defined Benefit Corporate Pensions

Y/Y Y/Y Y/Y Y/Y

2012 0.10 168.6 19.8 222.0 17.89 99.5 31,815 102.1

2013 0.05 51.3 2.5 12.8 17.54 98.1 32,742 102.9

2014 2.77 5,012.8 45.7 1,795.6 19.30 110.0 33,355 101.9

2015 0.01 0.6 10.3 22.7 18.13 93.9 33,714 101.1

2016 0.003 23.0 7.7 74.7 17.12 94.4 34,106 101.2

Note: Double counting of the number of insured under coinsurancce undertaken by multiple insurers has been resolved

(Number:million, Amount:billion yen,Y/Y:%)New Policies Policies

Aggregated Number of Insured Amount Aggregated Number of Insured Amount

31,815 32,742 33,355 33,714 34,106

0

10,000

20,000

30,000

40,000

2012 2013 2014 2015 2016

(billion yen)

2,373 2,341 1,9971,461 1,147

12,17013,045

13,92214,788 15,062

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2013 2014 2015 2016

(billion yen)

Employee's Pension funds Defined Benefit Corporate Pensions

23

II Profit and Loss

1 Insurance Related Profit and Loss

(1) Premium Income

The total amount of gross annual premium income was 33,459 billion yen (88.6% y/y) in Fiscal 2016. Though Gross annual premium income had trended upward in recent years, it decreased for the first time in three years in fiscal 2016, affected by the suspension of the sales of single-premium products due to the reduce in the assumed interest rates. [Figure 34]

As for results by type of business, individual insurance (23,611billion yen, 92.2% y/y), individual annuity insurance (4,340 billion yen, 91.8% y/y), group insurance (1,134 billion yen, 100.9% y/y), and group annuity insurance (3,057 billion yen, 67.0% y/y). [Figure 35]

By method of premium payments for individual insurance, monthly payment ranked top (52.9% of the total), followed by annual payment (21.4%), single-premium payment (16.2%) and monthly payment through payroll deduction (9.1%). The shares of single-premium payment and annual payment have significantly decreased from the previous year in fiscal 2016. [Figure 36]

Figure 34: Changes in Profit and Loss

Figure 35: Changes in Premium Income by Type

Ordinary

Revenue

s

Premium

Incomes and

Others

Premium

Income

Investmen

t Income

Interest

and

Dividend

Others

Ordinary

Expense

s

Insuranc

e

benefits

paid

Provision

for Policy

Reserves

Investme

nt

Expenses

Operatin

g

Expense

s

Other

s

2012 54,803 38,069 37,140 11,835 6,475 4,899 52,239 31,685 12,881 1,734 4,349 1,588 2,564

2013 53,215 35,784 34,738 11,326 6,877 6,105 50,113 33,778 9,108 1,345 4,389 1,491 3,101

2014 55,959 38,681 37,222 12,310 7,085 4,966 52,449 34,952 10,041 1,325 4,499 1,630 3,510

2015 52,305 38,962 37,748 8,291 7,111 5,051 49,537 32,454 8,361 2,473 4,706 1,541 2,768

2016 47,760 35,182 33,459 9,078 7,023 3,499 45,097 29,014 8,155 1,777 4,726 1,423 2,662

Below are figures excluding Japan Post Insurance

2012 42,968 31,587 30,658 10,274 4,975 1,106 40,933 21,012 12,872 1,705 3,836 1,507 2,034

2013 41,981 29,872 28,826 9,785 5,419 2,323 39,343 23,617 9,103 1,327 3,876 1,418 2,638

2014 45,790 32,724 31,267 10,850 5,720 2,215 42,773 25,892 10,040 1,314 3,986 1,538 3,016

2015 42,700 33,548 32,338 6,936 5,802 2,214 40,344 23,903 8,361 2,463 4,169 1,446 2,355

2016 39,101 30,141 28,424 7,710 5,797 1,250 36,717 21,463 8,155 1,617 4,166 1,314 2,383

(billion yen)Income Expenses

Ordinary

Profit

24,099 22,721 24,546 25,60723,611

4,3744,312

5,154 4,7294,340

1,1091,112

1,119 1,1241,134

3,6833,851

4,175 4,562

3,057

3,8742,739

2,226 1,723

1,314

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2012 2013 2014 2015 2016

(billion yen)

Individual Insurance Individual Annuity Insurance

Group Insurance Group Annuity Insurance

34,73837,222 37,748

33,459

37,140

24

Figure 36: Changes in Composition Ratio of Premium Income for Individual Insurance

by Premium Payment Methods

(2) Insurance Benefits Paid

The total amount paid by all life insurers under life insurance contracts in fiscal 2015 was 29,014 billion yen (89.4% y/y).

Of all the amount of insurance benefits paid, claims paid amounted to 11,053 billion yen (91.2% y/y), annuities paid amounted to 4,843 billion yen (99.7% y/y), benefits (other than claims paid and annuities paid) amounted to 3,904 billion yen (95.3% y/y), surrender benefits paid amounted to 5,768 billion yen (77.3% y/y), refunds to policyholders amounted to 1,125 billion yen (59.5% y/y) and reinsurance premiums14 amounted to 2,318 billion yen (114.7% y/y).

The amount of claims paid declined for the ninth successive year since fiscal 2008 due to the decrease in the number of existing postal life insurance policies. While the amount of annuities paid had been increasing consistently until fiscal 2014, in fiscal 2016, it decreased again from the previous year for the second successive year. The amount of benefits has decreased for the first time in five years. [Figure 37]

Figure 37: Changes in Insurance Benefits Paid

Note: Revenues and expenditures relating to the postal life insurance contracts issued by the former Japan Post (until 2007) is reflected on the revenues and expenditures of the Japan Post Insurance, through underwriting reinsurance from the Management Organization for Postal Savings and Postal Life Insurance that succeeds the contracts. Also, amounts equivalent to the insurance benefits paid (including annuities) relating to the postal life insurance is included in the "claims paid" of the Japan Post Insurance. Of all the claims paid, the number and the amount of death benefits were 1.02 million (101.5% y/y) and 2,89 billion yen (102.3% y/y), and the number and the amount of matured insurance policies were 0.65 million (95.2% y/y) and 1,406billion yen (97.54% y/y). [Figure 38]

14 Premiums that life insurers pay to reinsurers. Reinsurance is an insurance contract that life insurers concludes with

underwriting companies for reinsurance for the purpose of spreading risks regarding the amount of the benefit to be paid under the insurance contracts the insurer has underwritten.

(billion yen)

Claims Paid Annuities Paid BenefitsSurrendered

BenefitRefunds to

PolicyholdersReinsurancePremiums

Total

2012 15,296 3,360 3,936 5,867 1,036 2,188 31,685

2013 14,307 4,499 4,053 7,999 1,136 1,780 33,778

2014 12,971 5,196 4,066 8,772 1,817 2,129 34,952

2015 12,124 4,859 4,096 7,459 1,890 2,022 32,454

2016 11,053 4,843 3,904 5,768 1,125 2,318 29,014

Below are figures excluding Japan Post Insurance

2012 5,107 3,163 3,910 5,712 930 2,188 21,012

2013 4,796 4,242 4,019 7,779 1,000 1,778 23,617

2014 4,717 4,892 4,024 8,480 1,654 2,122 25,892

2015 4,547 4,518 4,047 7,080 1,697 2,011 23,903

2016 4,565 4,471 3,847 5,335 939 2,303 21,463

25

Figure 38: Changes in Number and Amount of Death/Maturity Benefit Payments

Of all the benefits paid, the number and the amount of hospitalization benefits increased to 6.66 million (102.9% y/y) and 693 billion yen (101.0% y/y), and also those of surgery benefits increased to 3.96 million (104.6% y/y) and 412 billion yen (103.0% y/y). [Figure 39]

Figure 39: Changes in Number and Amount of Hospitalization and Surgery Benefits

26

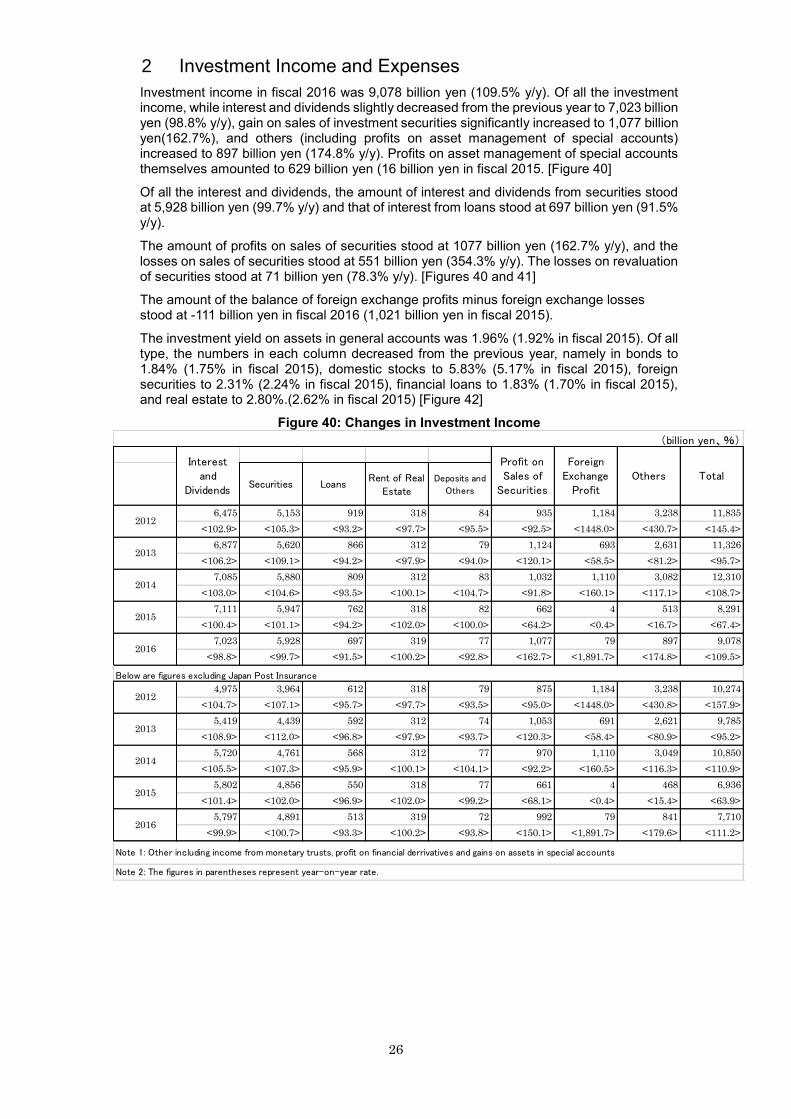

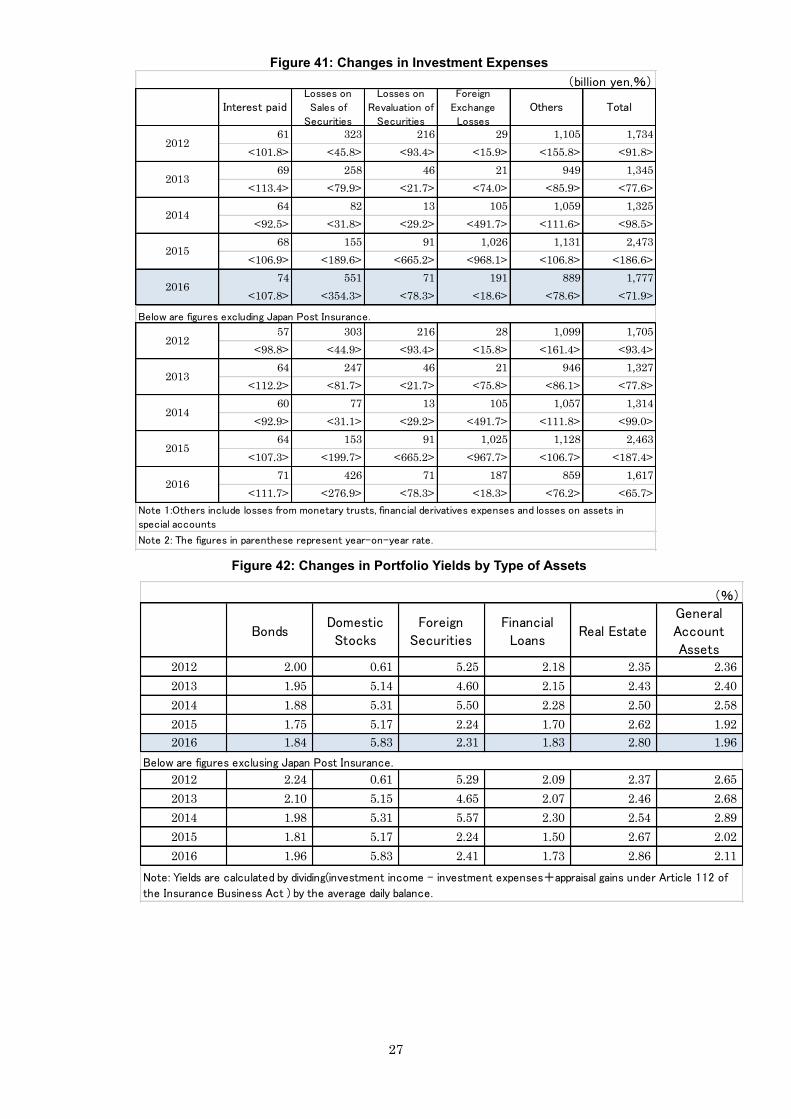

2 Investment Income and Expenses

Investment income in fiscal 2016 was 9,078 billion yen (109.5% y/y). Of all the investment income, while interest and dividends slightly decreased from the previous year to 7,023 billion yen (98.8% y/y), gain on sales of investment securities significantly increased to 1,077 billion yen(162.7%), and others (including profits on asset management of special accounts) increased to 897 billion yen (174.8% y/y). Profits on asset management of special accounts themselves amounted to 629 billion yen (16 billion yen in fiscal 2015. [Figure 40]

Of all the interest and dividends, the amount of interest and dividends from securities stood at 5,928 billion yen (99.7% y/y) and that of interest from loans stood at 697 billion yen (91.5% y/y).

The amount of profits on sales of securities stood at 1077 billion yen (162.7% y/y), and the losses on sales of securities stood at 551 billion yen (354.3% y/y). The losses on revaluation of securities stood at 71 billion yen (78.3% y/y). [Figures 40 and 41]

The amount of the balance of foreign exchange profits minus foreign exchange losses stood at -111 billion yen in fiscal 2016 (1,021 billion yen in fiscal 2015).

The investment yield on assets in general accounts was 1.96% (1.92% in fiscal 2015). Of all type, the numbers in each column decreased from the previous year, namely in bonds to 1.84% (1.75% in fiscal 2015), domestic stocks to 5.83% (5.17% in fiscal 2015), foreign securities to 2.31% (2.24% in fiscal 2015), financial loans to 1.83% (1.70% in fiscal 2015), and real estate to 2.80%.(2.62% in fiscal 2015) [Figure 42]

Figure 40: Changes in Investment Income

Securities LoansRent of Real

EstateDeposits and

Others

6,475 5,153 919 318 84 935 1,184 3,238 11,835

<102.9> <105.3> <93.2> <97.7> <95.5> <92.5> <1448.0> <430.7> <145.4>

6,877 5,620 866 312 79 1,124 693 2,631 11,326

<106.2> <109.1> <94.2> <97.9> <94.0> <120.1> <58.5> <81.2> <95.7>

7,085 5,880 809 312 83 1,032 1,110 3,082 12,310

<103.0> <104.6> <93.5> <100.1> <104.7> <91.8> <160.1> <117.1> <108.7>

7,111 5,947 762 318 82 662 4 513 8,291

<100.4> <101.1> <94.2> <102.0> <100.0> <64.2> <0.4> <16.7> <67.4>

7,023 5,928 697 319 77 1,077 79 897 9,078

<98.8> <99.7> <91.5> <100.2> <92.8> <162.7> <1,891.7> <174.8> <109.5>

4,975 3,964 612 318 79 875 1,184 3,238 10,274

<104.7> <107.1> <95.7> <97.7> <93.5> <95.0> <1448.0> <430.8> <157.9>

5,419 4,439 592 312 74 1,053 691 2,621 9,785

<108.9> <112.0> <96.8> <97.9> <93.7> <120.3> <58.4> <80.9> <95.2>

5,720 4,761 568 312 77 970 1,110 3,049 10,850

<105.5> <107.3> <95.9> <100.1> <104.1> <92.2> <160.5> <116.3> <110.9>

5,802 4,856 550 318 77 661 4 468 6,936

<101.4> <102.0> <96.9> <102.0> <99.2> <68.1> <0.4> <15.4> <63.9>

5,797 4,891 513 319 72 992 79 841 7,710

<99.9> <100.7> <93.3> <100.2> <93.8> <150.1> <1,891.7> <179.6> <111.2>

Total

(billion yen、%)

Interestand

Dividends

Profit onSales of

Securities

2014

ForeignExchange

ProfitOthers

2012

2013

Note 1: Other including income from monetary trusts, profit on financial derrivatives and gains on assets in special accounts

2016

2012

2015

2016

Below are figures excluding Japan Post Insurance

2015

2013

2014

Note 2: The figures in parentheses represent year-on-year rate.

27

Figure 41: Changes in Investment Expenses

Figure 42: Changes in Portfolio Yields by Type of Assets

61 323 216 29 1,105 1,734

<101.8> <45.8> <93.4> <15.9> <155.8> <91.8>

69 258 46 21 949 1,345

<113.4> <79.9> <21.7> <74.0> <85.9> <77.6>

64 82 13 105 1,059 1,325

<92.5> <31.8> <29.2> <491.7> <111.6> <98.5>

68 155 91 1,026 1,131 2,473

<106.9> <189.6> <665.2> <968.1> <106.8> <186.6>

74 551 71 191 889 1,777

<107.8> <354.3> <78.3> <18.6> <78.6> <71.9>

57 303 216 28 1,099 1,705

<98.8> <44.9> <93.4> <15.8> <161.4> <93.4>

64 247 46 21 946 1,327

<112.2> <81.7> <21.7> <75.8> <86.1> <77.8>

60 77 13 105 1,057 1,314

<92.9> <31.1> <29.2> <491.7> <111.8> <99.0>

64 153 91 1,025 1,128 2,463

<107.3> <199.7> <665.2> <967.7> <106.7> <187.4>

71 426 71 187 859 1,617

<111.7> <276.9> <78.3> <18.3> <76.2> <65.7>

Note 2: The figures in parenthese represent year-on-year rate.

(billion yen,%)Losses on

Sales of

Securities

Losses on

Revaluation of

Securities

Foreign

Exchange

Losses

Others Total

Note 1:Others include losses from monetary trusts, financial derivatives expenses and losses on assets in

special accounts

2016

2015

Interest paid

2016

Below are figures excluding Japan Post Insurance.

2012

2015

2013

2014

2012

2013

2014

BondsDomesticStocks

ForeignSecurities

FinancialLoans

Real EstateGeneralAccountAssets

2012 2.00 0.61 5.25 2.18 2.35 2.36

2013 1.95 5.14 4.60 2.15 2.43 2.40

2014 1.88 5.31 5.50 2.28 2.50 2.58

2015 1.75 5.17 2.24 1.70 2.62 1.92

2016 1.84 5.83 2.31 1.83 2.80 1.96

2012 2.24 0.61 5.29 2.09 2.37 2.65

2013 2.10 5.15 4.65 2.07 2.46 2.68

2014 1.98 5.31 5.57 2.30 2.54 2.89

2015 1.81 5.17 2.24 1.50 2.67 2.02

2016 1.96 5.83 2.41 1.73 2.86 2.11

Below are figures exclusing Japan Post Insurance.

Note: Yields are calculated by dividing(investment income - investment expenses+appraisal gains under Article 112 of

the Insurance Business Act ) by the average daily balance.

(%)

28

3 Operating Expenses

The total amount of operating expenses stood at 4,726 billion yen (100.4% y/y). The ratio of premium income to total operating expenses was 13.4% (up by 1.3points from the previous year). [Figure 43]

Figure 43: Changes in Operating Expenses

4 Ordinary Profits and Basic Profits

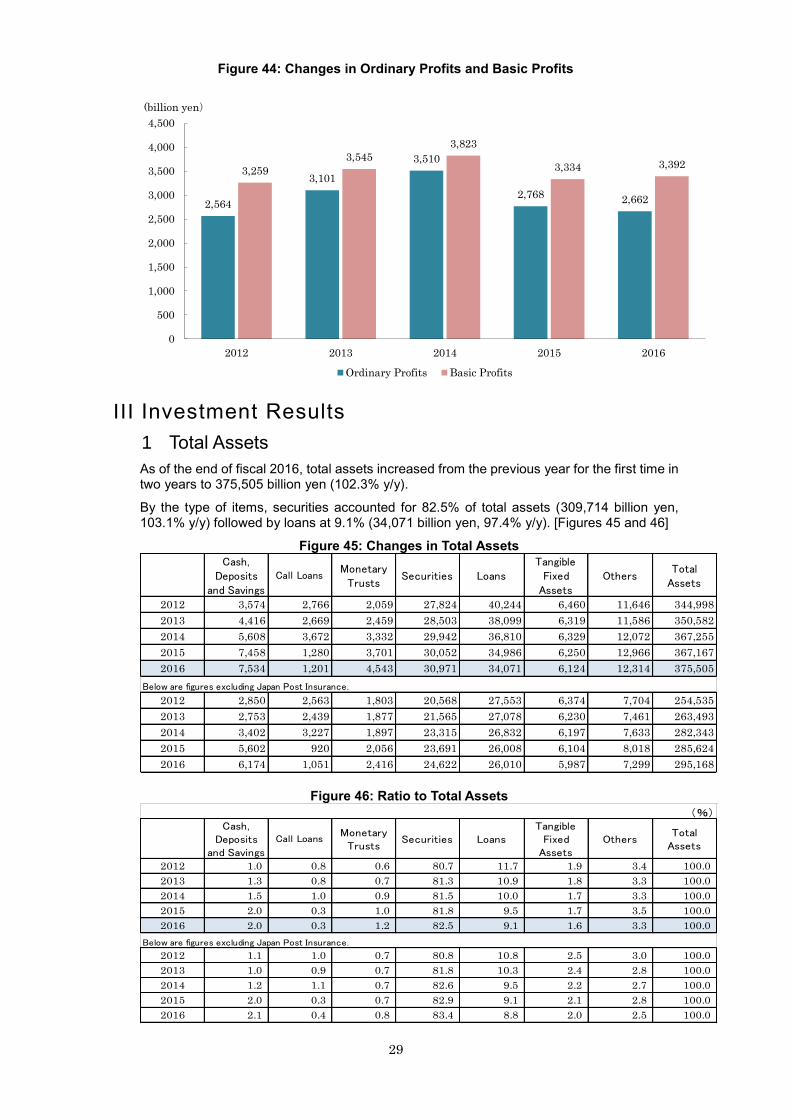

The total amount of ordinary profits decreased for the second successive year to 2,662billion yen (96.2% y/y) due to the decrease in premium income. The total amount of basic profits, which represents the profitability of the life insurance companies for the year, increased from the previous year to 3,392 billion yen (101.8% y/y) for the first time in six years. [Figure 44]

What is Basic Profit?

"Basic profit" is the indicator for the basic periodic profit/loss status of life insurers, comprised of income and expenditures for core insurance business (e.g. premium income, payments of insurance benefits and operating expenses) and income and expenditures for investment (mainly interest and dividends). The amount is calculated by deducting both "capital gains/losses" and "extraordinary gains/losses" (e.g. profits/losses on sales of securities) from the ordinary profits.

4,349 4,389 4,499 4,706 4,726

11.4

12.3 11.6

12.1

13.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0

1,000

2,000

3,000

4,000

5,000

6,000

2012 2013 2014 2015 2016

(%)(billion yen)

Operating Expenses

Ratio to Premium Income

29

III Investment Results

1 Total Assets

As of the end of fiscal 2016, total assets increased from the previous year for the first time in two years to 375,505 billion yen (102.3% y/y).

By the type of items, securities accounted for 82.5% of total assets (309,714 billion yen, 103.1% y/y) followed by loans at 9.1% (34,071 billion yen, 97.4% y/y). [Figures 45 and 46]

Figure 45: Changes in Total Assets

Figure 46: Ratio to Total Assets

2,564

3,101

3,510

2,7682,662

3,259

3,545

3,823

3,334 3,392

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2012 2013 2014 2015 2016

(billion yen)

Ordinary Profits Basic Profits

Cash,Deposits

and Savings

Call LoansMonetary

TrustsSecurities Loans

TangibleFixed

AssetsOthers

TotalAssets

2012 3,574 2,766 2,059 27,824 40,244 6,460 11,646 344,998

2013 4,416 2,669 2,459 28,503 38,099 6,319 11,586 350,582

2014 5,608 3,672 3,332 29,942 36,810 6,329 12,072 367,255

2015 7,458 1,280 3,701 30,052 34,986 6,250 12,966 367,167

2016 7,534 1,201 4,543 30,971 34,071 6,124 12,314 375,505

2012 2,850 2,563 1,803 20,568 27,553 6,374 7,704 254,535

2013 2,753 2,439 1,877 21,565 27,078 6,230 7,461 263,493

2014 3,402 3,227 1,897 23,315 26,832 6,197 7,633 282,343

2015 5,602 920 2,056 23,691 26,008 6,104 8,018 285,624

2016 6,174 1,051 2,416 24,622 26,010 5,987 7,299 295,168

Below are figures excluding Japan Post Insurance.

Cash,Deposits

and Savings

Call LoansMonetary

TrustsSecurities Loans

TangibleFixed

AssetsOthers

TotalAssets

2012 1.0 0.8 0.6 80.7 11.7 1.9 3.4 100.0

2013 1.3 0.8 0.7 81.3 10.9 1.8 3.3 100.0

2014 1.5 1.0 0.9 81.5 10.0 1.7 3.3 100.0

2015 2.0 0.3 1.0 81.8 9.5 1.7 3.5 100.0

2016 2.0 0.3 1.2 82.5 9.1 1.6 3.3 100.0

2012 1.1 1.0 0.7 80.8 10.8 2.5 3.0 100.0

2013 1.0 0.9 0.7 81.8 10.3 2.4 2.8 100.0

2014 1.2 1.1 0.7 82.6 9.5 2.2 2.7 100.0

2015 2.0 0.3 0.7 82.9 9.1 2.1 2.8 100.0

2016 2.1 0.4 0.8 83.4 8.8 2.0 2.5 100.0

Below are figures excluding Japan Post Insurance.

(%)

Figure 44: Changes in Ordinary Profits and Basic Profits

30

2 Securities

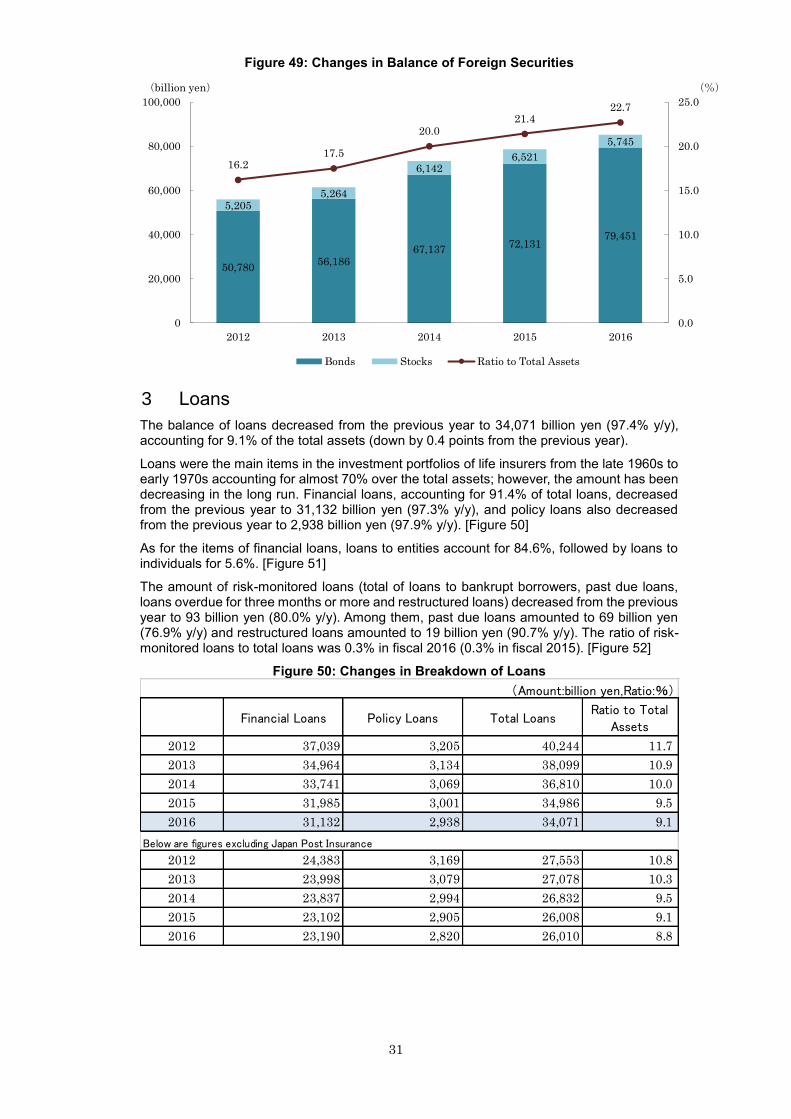

By the type of securities (309,714 billion yen in total), Japanese government bonds ranked top with 148,553 billion yen (99.99% y/y) accounting for 48.0% of the total securities, followed by foreign securities at 85,197 billion yen (108.3% y/y), corporate bonds at 25,824 billion yen (101.8% y/y), stocks at 21,514 billion yen (101.8% y/y) and local government bonds at 12,982 billion yen (96.0% y/y). [Figure 47]

Since the domestic interest rate remained low throughout fiscal 2016, financial resources were increasingly allocated to foreign securities etc., because of their comparatively higher interest rates. As a result, the amount of bonds (total of government bonds, local government bonds and corporate bonds) decreased for the third successive year (187,360 billion yen, 99.95% y/y). The amount of stocks increased for second successive year. Among the assets, the amount of bonds accounted for 49.9%, foreign securities for 22.7%, and stocks for 5.7% of the total in fiscal 2016. [Figures 48 and 49]

Of all the foreign securities, the amount of bonds (total of government bonds, local government bonds corporate bonds, and other foreign securities) stood at 79,451 billion yen (110.1% y/y), and the amount of stocks stood at 5,745 billion yen (88.1% y/y). [Figure 49]

Figure 47: Changes in Breakdown of Securities

Figure 48: Changes in Balance of Bonds and Stocks.

Total

Amount Ratio Amount Ratio Amount Ratio Amount Ratio Amount Ratio Amount Ratio Amount

2012 148,769 53.5 13,934 5.0 25,155 9.0 16,725 6.0 55,986 20.1 17,673 6.4 278,244

2013 149,815 52.6 14,008 4.9 24,895 8.7 18,029 6.3 61,450 21.6 16,830 5.9 285,031

2014 148,761 49.7 13,868 4.6 24,855 8.3 22,697 7.6 73,280 24.5 15,965 5.3 299,429

2015 148,568 49.4 13,517 4.5 25,363 8.4 19,813 6.6 78,653 26.2 14,607 4.9 300,523

2016 148,553 48.0 12,982 4.2 25,824 8.3 21,514 6.9 85,197 27.5 15,642 5.1 309,714

2012 92,296 44.9 5,236 2.5 18,671 9.1 16,724 8.1 55,084 26.8 17,673 8.6 205,686

2013 97,292 45.1 4,835 2.2 18,454 8.6 18,028 8.4 60,211 27.9 16,830 7.8 215,652

2014 100,675 43.2 4,312 1.8 18,202 7.8 22,696 9.7 71,299 30.6 15,965 6.8 233,152

2015 104,389 44.1 4,112 1.7 19,126 8.1 19,812 8.4 74,964 31.6 14,507 6.1 236,912

2016 105,821 43.0 3,755 1.5 20,125 8.2 21,455 8.7 80,845 32.8 14,225 5.8 246,228

Below are figures excluding Japan Post Insurance

GovernmentBonds

LocalGovernment

BondsCorporate Bonds Stocks Foreign SecuritiesOther Securities

(Amount:billion yen、Ratio:%)

31

Figure 49: Changes in Balance of Foreign Securities

3 Loans

The balance of loans decreased from the previous year to 34,071 billion yen (97.4% y/y), accounting for 9.1% of the total assets (down by 0.4 points from the previous year).

Loans were the main items in the investment portfolios of life insurers from the late 1960s to early 1970s accounting for almost 70% over the total assets; however, the amount has been decreasing in the long run. Financial loans, accounting for 91.4% of total loans, decreased from the previous year to 31,132 billion yen (97.3% y/y), and policy loans also decreased from the previous year to 2,938 billion yen (97.9% y/y). [Figure 50]

As for the items of financial loans, loans to entities account for 84.6%, followed by loans to individuals for 5.6%. [Figure 51]

The amount of risk-monitored loans (total of loans to bankrupt borrowers, past due loans, loans overdue for three months or more and restructured loans) decreased from the previous year to 93 billion yen (80.0% y/y). Among them, past due loans amounted to 69 billion yen (76.9% y/y) and restructured loans amounted to 19 billion yen (90.7% y/y). The ratio of risk-monitored loans to total loans was 0.3% in fiscal 2016 (0.3% in fiscal 2015). [Figure 52]

Figure 50: Changes in Breakdown of Loans

50,78056,186

67,13772,131

79,451

5,2055,264

6,1426,521

5,745

16.217.5

20.021.4

22.7

0.0

5.0

10.0

15.0

20.0

25.0

0

20,000

40,000

60,000

80,000

100,000

2012 2013 2014 2015 2016

(%)(billion yen)

Bonds Stocks Ratio to Total Assets

Financial Loans Policy Loans Total LoansRatio to Total

Assets

2012 37,039 3,205 40,244 11.7

2013 34,964 3,134 38,099 10.9

2014 33,741 3,069 36,810 10.0

2015 31,985 3,001 34,986 9.5

2016 31,132 2,938 34,071 9.1

2012 24,383 3,169 27,553 10.8

2013 23,998 3,079 27,078 10.3

2014 23,837 2,994 26,832 9.5

2015 23,102 2,905 26,008 9.1

2016 23,190 2,820 26,010 8.8

(Amount:billion yen,Ratio:%)

Below are figures excluding Japan Post Insurance

32

Figure 51: Changes in Financial Loans to Entities and Individuals

Note 1: Financial loans to entities include the loans to foreign entities in addition to the items described above. Note 2: Financial loans from Japan Post Insurance to SMEs include loans to Management Organization for Postal Savings and Postal Life Insurance. Note 3: The figures in parentheses represent year-on-year rate.

(Classification of Scale of Entities by the Type of Business)

Type of Business

① All Types of Business

Except for ② to ④ ② Retail and Eating and

Drinking Business ③ Service Business ④ Wholesale Business

Large Entities With more

than 300 employees and;

Capital of 1 billion yen or more With more

than 50 employees and;

Capital of 1 billion yen or more With more

than 100 employees and;

Capital of 1 billion yen or more With more

than 100 employees and;

Capital of 1 billion yen or more

Leading Medium-Sized Entities

Capital of more than 300 million yen and less than 1 billion yen

Capital of more than 50 million yen and less than 1 billion yen

Capital of more than 50 million yen and less than 1 billion yen

Capital of more than 100 million yen and less than 1 billion yen

SMEs With capital of 300 million yen or less or 300 or less full-time employees

With capital of 50 million yen or less or 50 or less full-time employees

With capital of 50 million yen or less or 100 or less full-time employees

With capital of 100 million yen or less or 100 or less full-time employees

Large EntitiesLeading

Medium-sizedEntities

SMEsHome

MortgagesConsumer

Loans

32,489 17,097 131 13,874 1,451 794

<94.5> <98.3> <85.4> <89.8> <92.4> <102.2>

30,443 16,594 139 12,104 1,400 808

<93.7> <97.1> <106.6> <87.2> <96.5> <101.7>

29,437 16,282 135 11,040 1,333 706

<96.7> <98.1> <97.3> <91.2> <95.2> <87.4>

27,798 15,659 156 9,989 1,251 646

<94.4> <96.2> <115.5> <90.5> <93.8> <91.6>

26,338 14,849 129 9,047 1,142 587

<94.7> <94.8> <82.8> <90.6> <91.3> <90.8>

20,286 16,881 131 1,888 1,451 794

<97.1> <98.0> <85.4> <89.2> <92.4> <102.2>

19,981 16,351 139 1,885 1,400 808

<98.5> <96.9> <106.6> <99.8> <96.5> <101.7>

20,067 16,027 135 1,925 1,333 706

<100.4> <98.0> <97.3> <102.1> <95.2> <87.4>

19,505 15,439 156 1,916 1,251 646

<97.2> <96.3> <115.5> <99.5> <93.8> <91.6>

19,067 14,673 129 1,951 1,142 587

<97.8> <95.0> <82.8> <101.8> <91.3> <90.8>

2013

2016

2015

2014

2015

2016

Below are figures exclusing Japan Post Insurance

2012

2014

Loans to Individuals

(billion yen, %)

2012

2013

Loans to Entities

33

Figure 52: Changes in Amount of Risk-Monitored Loans

4 Tangible Fixed Assets (Real Estate)

Of the total amount of tangible fixed assets (6,124 billion yen), the amount of real estate, which is the total amount of land, buildings and construction in process, was 6,027 billion yen (97.9% y/y). The total amount of tangible fixed assets accounts for 1.6% of the total assets for fiscal 2016.[Figures 45 and 53]

Figure 53: Changes in Balance of Real Estate

IV Liabilities and Net Assets

Total liabilities stood at 352,674 billion yen (102.6% y/y), accounting for 93.9% of gross capital (the total of liabilities and net assets). By the items of liabilities, insurance reserves account for 92.8% of total liabilities. Of all the insurance reserves, policy reserves, which are reserved for future insurance claim payments, account for 98.1% of total policy reserves. Other than that, reserves for policyholder dividends account for 1.3%, which are reserved for paying dividends on insurance contracts, and reserves for outstanding claims account for 0.7%, which are reserved for unclaimed insurance payable. [Figure 54 (upper panel)]

Meanwhile, total net assets were 22,830 billion yen (97.6% y/y), accounting for 6.1% of gross capital. It decreased from the previous year due to the decrease in "total valuation, translation adjustment, and others". [Figure 54 (lower panel)]

34

Figure 54: Liabilities and Net Assets

Breakdown of Liabilities (Billion、%)

Amount Ratio of Liabilities Ratio

327,298 92.8 87.2

Reserves for Outstanding Claims 2,180 0.6 0.6

Policy Reserves 321,021 91.0 85.5

Reserves for Policyholder Dividends 4,095 1.2 1.1

4,100 1.2 1.1

21,275 6.0 5.7

352,674 100.0 93.9

Amount Ratio of Net Assets Ratio

Total Foundation Funds and others or Total Stockholders' Equity10,684 46.8 2.8

Fund or Capital 2,840 12.4 0.8

Accumulated Redeemed Foundation Funds 2,376 10.4 0.6

Capital Surplus 1,872 8.2 0.5

Surplus or Retained Earnings 3,570 15.6 1.0

Others 24 0.1 0.0

12,146 53.2 3.2

0 0.0 0.0

22,830 100.0 6.1

37,550 - 100.0

Total Net Assets

Total Liabilities and Net Assets

Total Valuation, TranslationAdustment, and Others

Stock Acquisition Rights

Insurance Reserves

Reserves for Price Fluctuations

Others

Total Liablities

Breakdown of Net Assets

35

Reference

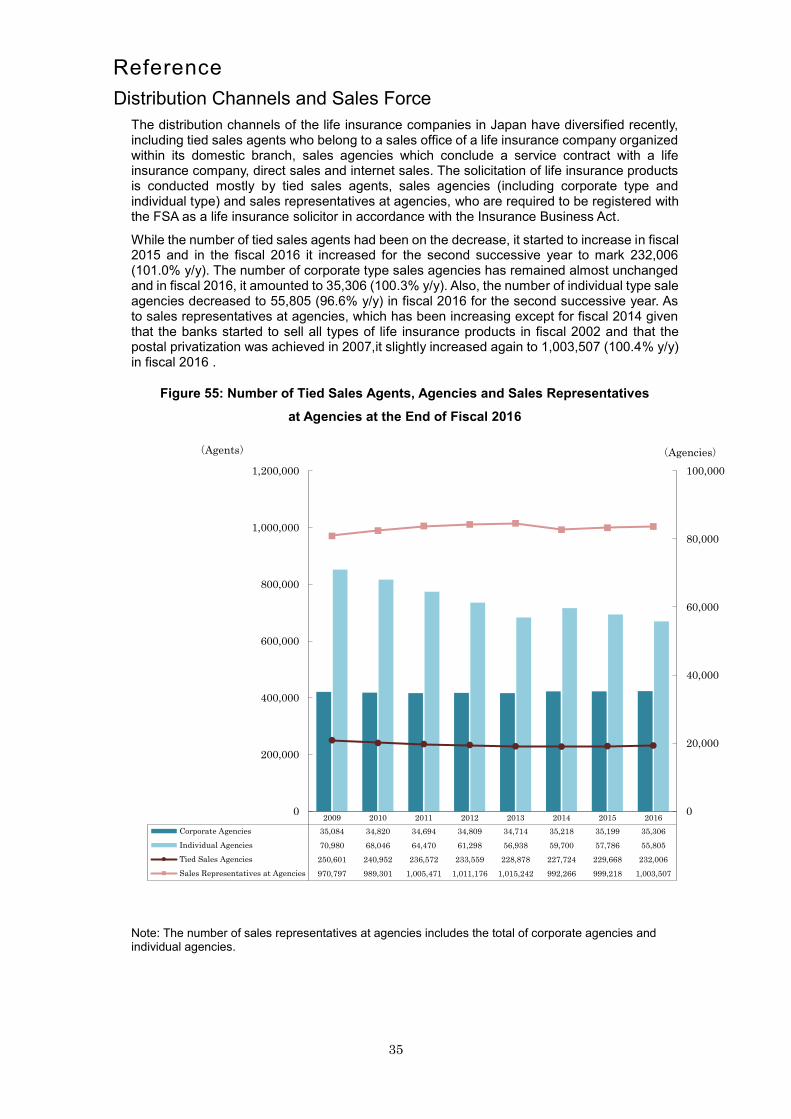

Distribution Channels and Sales Force

The distribution channels of the life insurance companies in Japan have diversified recently, including tied sales agents who belong to a sales office of a life insurance company organized within its domestic branch, sales agencies which conclude a service contract with a life insurance company, direct sales and internet sales. The solicitation of life insurance products is conducted mostly by tied sales agents, sales agencies (including corporate type and individual type) and sales representatives at agencies, who are required to be registered with the FSA as a life insurance solicitor in accordance with the Insurance Business Act.

While the number of tied sales agents had been on the decrease, it started to increase in fiscal 2015 and in the fiscal 2016 it increased for the second successive year to mark 232,006 (101.0% y/y). The number of corporate type sales agencies has remained almost unchanged and in fiscal 2016, it amounted to 35,306 (100.3% y/y). Also, the number of individual type sale agencies decreased to 55,805 (96.6% y/y) in fiscal 2016 for the second successive year. As to sales representatives at agencies, which has been increasing except for fiscal 2014 given that the banks started to sell all types of life insurance products in fiscal 2002 and that the postal privatization was achieved in 2007,it slightly increased again to 1,003,507 (100.4% y/y) in fiscal 2016 .