LmE Week: inconsistent picture of the aluminium market developmentG. Djukanovic, Podgorica

London Metal Exchange – The LME Week, the premier event in the global commodities business calendar, was held at a time when metal prices were on the decline and forecasts for the coming year rather downgraded. The annual gathering of traders, producers, brokers, analysts and other professionals of the metals community is a unique opportunity to meet industry experts, hear first-hand news and exchange information. Most of the events this year occurred between 20-23 October, with the traditional LME Seminar on the first day in the morning and the Macquarie Bank Seminar in the afternoon. The following day started with the CRU Breakfast & Seminar, followed by the Standard Bank London Buffet Lunch and Commerzbank’s Metals Pre-sentation, INTL FC Stone Cocktails and the LME Annual Diner in the evening. Those were the most interesting meetings in the author’s view.

At the LME Seminar Matthew Chamberlain, head of Business Development, said that after a period of transition the LME is looking to move forward and develop its business along multiple axes. Bought by Hong Kong Exchang-es and Clearing for USD2.2bn in 2012, the LME now wants to capitalise on its purchase, espe-cially its ability to expand into main-land China, the largest consumer and producer of most metals. The LME announced the launch of Asian mini-contracts for aluminium, zinc and copper in Hong Kong, trad-ing of which will start in December, in Chinese Ren-minbi. The ‘minis’ will offer lots of 5 tonnes rather than the standard 25 tonnes, and are expected to target China’s numerous retail investors who already trade heavily on

domestic futures exchanges. There will be no floor trading, with traders shouting orders from the Ring, as is the case in London – the last open-outcry trading floor in Europe. The LME accounts for about 80% of overall global futures and options trade in base metals.

Most base metals prices started rising during or immediately after the LME Week. The aluminium price jumped above the USD 2,000/t hurdle again – not because the LME Week has overcome the prevailing bearish mood on the markets, but rather due to posi-tive signals from China and Japan.

opposite views on aluminium balance

Two well known analysts from two renowned banks expressed opposite views on the alu-minium market balance at the LME Seminar: one claiming a market deficit, the other a surplus. This shows that statistical figures, es-pecially those about production in China, are far from accurate and reliable but rather a matter of free estimation and guessing.

David Wilson, director of Metals Research and Strategy at Citigroup, disputed that the market was in a major deficit. He pointed out that there had not been any significant closure since March this year, while temporary clo-sures in China this summer have been more

than compensated by new smelters in west-ern provinces. “Prices have done very well through the third quarter,” he said. “The key

driver of the rally was algorithm CTA activity – the trend followers and the technical follow-ers.” Wilson stated that the surplus would be expected to remain at least until 2017.

In contrast Nic Brown, head of Commodi-ties Research at Natixis bank, sees a supply-demand deficit of some 300,000 tonnes for aluminium this year. He expects this deficit to increase further, at least in the next two to three years. A shortage of bauxite, coupled with increased aluminium demand, would push the average price to USD2,070/t in 2015 and USD2,240/t in 2016, he said, adding that Chinese producers were “very dependent” on Indonesian bauxite, of which there is “a lack”. According to Brown Chinese smelters would feel the shortage of bauxite in 2015 and that the surge in aluminium production in the past years was nearly over. He expects the alumin-ium demand to grow some 5% annually in the coming years.

In conclusion: a deficit according to Brown, and one that will steadily increase over the next two years. A surplus according to Wilson, with no sign of deficit at least until 2017.

metals outlook from financial institutions

Below, a summary of economic and metals outlooks by participants at the LME Week.

CRU: The Chi-nese real estate sector is currently facing severe dif-ficulties with sales down 8% this year. However, ‘favoured’ sectors are growing, with investments in social housing up 31% and in rail up 21%. The big-gest single issue for metals demand this year has been the downturn in Chinese real es-tate, which CRU views as the most

serious risk to world metals markets. CRU pointed out that factors on the sup-

demand that drives the metals price cycle, it is the supply that sorts the winners and losers. The metals with the strongest demand growth have historically shown the worst price per-formance. Just think of aluminium: its his-torically weak price compared with growth in demand is all down to supply-side factors.

CRU expects the aluminium demand to grow by 7% annually and the aluminium price to grow gradually to USD2,200/t in 2016, on average.

Standard Bank London: The aluminium market is much tighter this year than the bank initially expected. While growth in demand has remained strong, the supply side has seen a series of capacity curtailments. The global supply looks set to expand by only 3.6% this year – the weakest increase since 2009. This is down from the bank’s original 7% forecast of world production for 2014. The bank ex-pects 2014 to post a deficit (of 806,000 t) for the first time in seven years. The deficit for 2015 is expected to double to 1.27m tonnes. Taking the four-year time period of 2014 to 2017, the bank expects the overall deficit to accumulate to 3.3m tonnes. By contrast, there was an estimated 5.5m tonnes surplus over the time period of 2008 to 2013.

Given record physical premiums, it seems that the bulk of metal leaving LME ware- houses is most likely going into off-warrant storage deals rather than to consumers. As such, and with the LME aluminium inventory still making up over 17% of market open in-terest, bouts of tightness will remain a feature of the market as this inventory overhang is subject to specula-tive interest.

The rate of change in interest rates will be key to what happens to the financing deals, as will the success or failure of the LME’s premium hedging contract. As regards the in-terest rates, there is scope for euro-de-nominated financ-ing should euro vs. dollar interest rates diverge too much.

Meanwhile, al-though a premium hedging tool has generally been looked at from a consumer’s viewpoint, it actually also stands to benefit metal financiers. Rather than take a punt on

premiums when locking into a finance deal, with the concern that premiums might col-lapse, financiers may be able to lock in physi-cal premiums at the time of the deal. There would then be no need to panic and dump material into the market at the first sign of softening physical demand. The premium hedging contract may therefore in fact serve to prolong the disconnection between LME cash prices and the all-in price of aluminium.

SBL estimates that the global loss of pro- duction capacity since December 2011 amounts to 3.284m tonnes and there is addi-tional ‘at-risk’ capacity that could lift the figure close to 4m tonnes by year-end.

Aluminium consumption globally has grown at an average annual rate of 8.7% since the 2008/09 financial crisis. This compares with 4-5% for copper, zinc and lead, for ex-ample, and even less for tin. The bank expects the aluminium demand to grow by 6-7% this and next year and by 5% in 2016 and 2017, which is a cautious forecast.

Overall, the bank is neutral as regards the price prospects in the short and medium term. In the longer term the bank expects the aluminium price to recover; however, at the expense of premiums as the physical market slowly normalises and LME warehouse queues subside. SBL predicts an average aluminium price of USD1,858/t in 2014 and increas-ing slightly over the years to USD2,300/t in 2017.

Citi bank: Premiums are still being driven by financing demand for physical metal rather than by load-out queues. Financing has be-

come a challenge for using metal in LME ware-houses given the flattening contango spreads and high LME rents, and non-LME financing

has surged. The rental deals are being struck in non-LME sheds for ¢5-10/t/d versus LME rates of ¢45/t/d. With the imminent prospect of interest rate hikes in the US, the bank ex-pects even non-LME financing will become challenging, prompting a release of metal in 2015.

The demand outlook for aluminium is per-haps the most positive of the base metals com-plex with the auto sector the driving force. Citi bank expects annual demand to grow close to 6% on average until 2020.

Whilst production has been curtailed at a number of Brazilian smelters, no new cap-acity cuts have been announced since the first quarter of 2014, apart from the final shut- down of Point Henry in Australia in July. The closure of Alcoa’s Portovesme smelter was somewhat misleading as the smelter ceased production in 2012. Unsurprisingly, the full aluminium price including premiums is above USD2,500/t. As the bank noted in its last quar-terly report, smelter production has been ac-celerating in the Middle East and China. The bank expects smelter production to speed up in 2014, up 6.1% vs 4.5% in 2013.

Citi bank expects that the appeal court rul-ing in the Rusal vs. LME case in October will have little effect on the aluminium price or premiums, given that warehouses are behav-ing as if the LME’s proposed rule changes have already been implemented.

The aluminium market is regarded as be-ing in global surplus. Rising borrowing costs in 2015 could reverse this situation. The bank expects an LME aluminium price of USD

1,995/t on average in 2015.

INTL FC Stone: Apart from the USA, all major economies are de-celerating despite zero interest rates. Such a synchro-nised slowdown has not been seen since the financial crisis in 2008/09, and the fact that it could affect the US economy is now of rising concern. Against this back-ground INTL FC Stone thinks the 2015 metals land-

scape will be very similar to what we have seen this year, namely relatively reduced vol-atility and trading ranges.

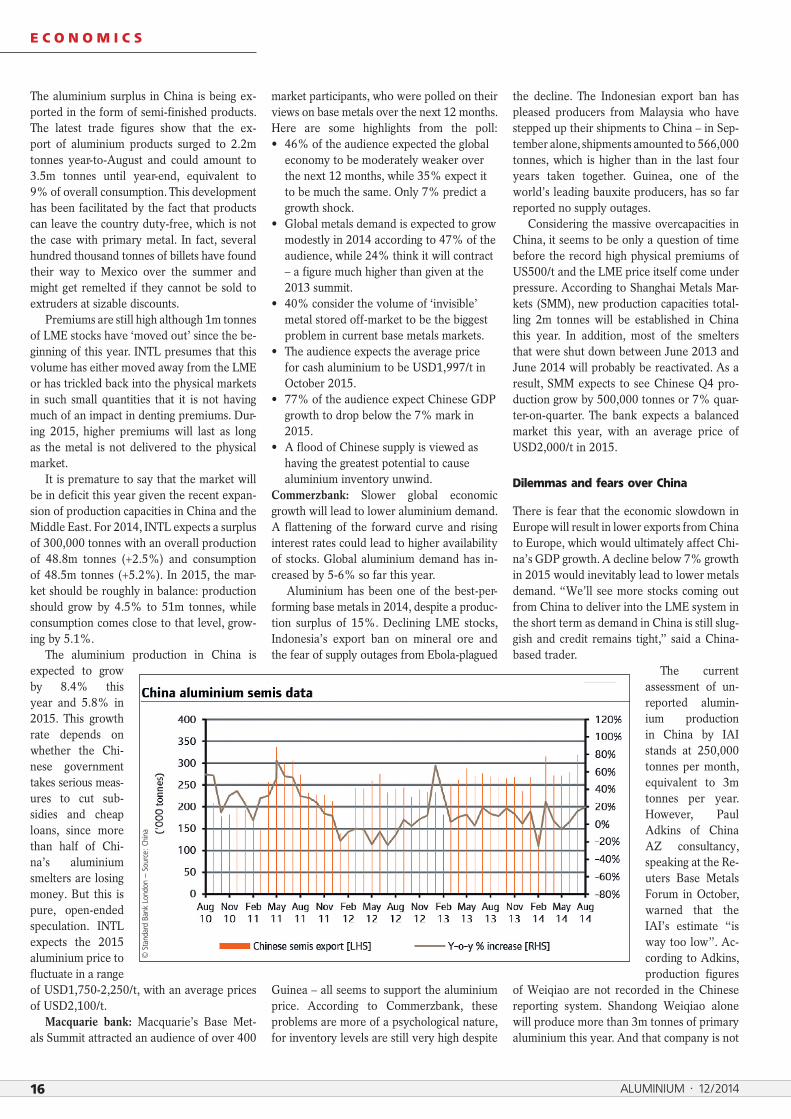

The aluminium surplus in China is being ex-ported in the form of semi-finished products. The latest trade figures show that the ex-port of aluminium products surged to 2.2m tonnes year-to-August and could amount to 3.5m tonnes until year-end, equivalent to 9% of overall consumption. This development has been facilitated by the fact that products can leave the country duty-free, which is not the case with primary metal. In fact, several hundred thousand tonnes of billets have found their way to Mexico over the summer and might get remelted if they cannot be sold to extruders at sizable discounts.

Premiums are still high although 1m tonnes of LME stocks have ‘moved out’ since the be-ginning of this year. INTL presumes that this volume has either moved away from the LME or has trickled back into the physical markets in such small quantities that it is not having much of an impact in denting premiums. Dur-ing 2015, higher premiums will last as long as the metal is not delivered to the physical market.

It is premature to say that the market will be in deficit this year given the recent expan-sion of production capacities in China and the Middle East. For 2014, INTL expects a surplus of 300,000 tonnes with an overall production of 48.8m tonnes (+2.5%) and consumption of 48.5m tonnes (+5.2%). In 2015, the mar-ket should be roughly in balance: production should grow by 4.5% to 51m tonnes, while consumption comes close to that level, grow-ing by 5.1%.

The aluminium production in China is expected to grow by 8.4% this year and 5.8% in 2015. This growth rate depends on whether the Chi-nese government takes serious meas- ures to cut sub-sidies and cheap loans, since more than half of Chi-na’s aluminium smelters are losing money. But this is pure, open-ended speculation. INTL expects the 2015 aluminium price to fluctuate in a range of USD1,750-2,250/t, with an average prices of USD2,100/t.

Macquarie bank: Macquarie’s Base Met-als Summit attracted an audience of over 400

market participants, who were polled on their views on base metals over the next 12 months. Here are some highlights from the poll:• 46% of the audience expected the global economy to be moderately weaker over the next 12 months, while 35% expect it to be much the same. Only 7% predict a growth shock.• Global metals demand is expected to grow modestly in 2014 according to 47% of the audience, while 24% think it will contract – a figure much higher than given at the 2013 summit.• 40% consider the volume of ‘invisible’ metal stored off-market to be the biggest problem in current base metals markets.• The audience expects the average price for cash aluminium to be USD1,997/t in October 2015.• 77% of the audience expect Chinese GDP growth to drop below the 7% mark in 2015.• A flood of Chinese supply is viewed as having the greatest potential to cause aluminium inventory unwind.Commerzbank: Slower global economic growth will lead to lower aluminium demand. A flattening of the forward curve and rising interest rates could lead to higher availability of stocks. Global aluminium demand has in-creased by 5-6% so far this year.

Aluminium has been one of the best-per-forming base metals in 2014, despite a produc-tion surplus of 15%. Declining LME stocks, Indonesia’s export ban on mineral ore and the fear of supply outages from Ebola-plagued

Guinea – all seems to support the aluminium price. According to Commerzbank, these problems are more of a psychological nature, for inventory levels are still very high despite

the decline. The Indonesian export ban has pleased producers from Malaysia who have stepped up their shipments to China – in Sep-tember alone, shipments amounted to 566,000 tonnes, which is higher than in the last four years taken together. Guinea, one of the world’s leading bauxite producers, has so far reported no supply outages.

Considering the massive overcapacities in China, it seems to be only a question of time before the record high physical premiums of US500/t and the LME price itself come under pressure. According to Shanghai Metals Mar-kets (SMM), new production capacities total-ling 2m tonnes will be established in China this year. In addition, most of the smelters that were shut down between June 2013 and June 2014 will probably be reactivated. As a result, SMM expects to see Chinese Q4 pro-duction grow by 500,000 tonnes or 7% quar-ter-on-quarter. The bank expects a balanced market this year, with an average price of USD2,000/t in 2015.

Dilemmas and fears over china

There is fear that the economic slowdown in Europe will result in lower exports from China to Europe, which would ultimately affect Chi-na’s GDP growth. A decline below 7% growth in 2015 would inevitably lead to lower metals demand. “We’ll see more stocks coming out from China to deliver into the LME system in the short term as demand in China is still slug-gish and credit remains tight,” said a China-based trader.

The current assessment of un-reported alumin-ium production in China by IAI stands at 250,000 tonnes per month, equivalent to 3m tonnes per year. However, Paul Adkins of China AZ consultancy, speaking at the Re-uters Base Metals Forum in October, warned that the IAI’s estimate “is way too low”. Ac-cording to Adkins, production figures

of Weiqiao are not recorded in the Chinese reporting system. Shandong Weiqiao alone will produce more than 3m tonnes of primary aluminium this year. And that company is not

the only Chinese producer not making it into the official figures.

The impact of Chinese oversupply on the rest of the world can be assessed by using Chi-na’s customs export figures for aluminium, to be precise the export of semi-fabricated prod-ucts. This has been in constant growth over the last seven to eight years and may reach almost 4m tonnes this year. Semis exports of 340,000 tonnes in September matched the all-time high recorded in May 2011, while year-to-date export growth is 10% above 2013 levels. Many analysts do not consider that those exports, since they are products, have an influence on the global primary aluminium balance.

However, Citi’s analyst David Wilson claims that China’s exports cause a double-count in the global consumption calculation because of the differing methodologies used in different countries. In China they are counted as first-use consumption. However, if they are then exported to a country, e.g. the United States, where better data allows the construction of a bottom-up demand calcula-tion, they get counted again. Moreover, there is growing concern among analysts about the nature of some of these exports. Is it possi-ble that some Chinese players are performing minimal transformation of primary metal into basic ‘products’ to skip through China‘s export tax regime? The primary exports are hit with a 15% tax, while product exports qualify for a partial VAT refund.

Arthur Fan, CEO of Boci Global Commodi-ties, said that a slowdown in China, caused by transition from an investment-based to a con-sumption-based economy, and financial re-forms and more interaction with international markets would affect commodity markets. “In the next years we will see quite a significant change in the impact of China on the global metals market,” he said.

author’s final remarks

It is questionable how much conclusions from this and similar events are used by big mar-ket participants (traders, funds, etc.) to plan their business strategy and make profits on developments quite the opposite of what is expected by most players on the market. It has been seen more than once that the prices of certain commodities moved in the opposite direction from the consensus of analysts. For instance, copper has the worst prospects of all base metals as regards price development in 2015, while some leading institutions expect China’s imports of copper to fall significantly in 2015. What if market participants in China,

or whoever, start buying copper for stockpil-ing and financing deals, in expectation that the price will rise again in three to four years from now? Then the price would not fall; it would maybe even rise, despite the expected surplus on the market.

In line with such assumptions, the ques-tion is whether the aluminium price can re-main at around USD2,000/t and premiums at a record high (around USD500/t in Europe) if China’s economy continues to slow down. Most analysts would give a negative answer. However, stagnant and even weaker economic growth in China may result in less and smaller bank loans, less investments, and finally less exports of semi-finished aluminium products from China. The export of products from China in recent years was the main cause of oversupplied western and world markets and consequently capped the aluminium price. In explicit words: despite high and even rising demand, the aluminium price cannot move much higher with a constant surplus on the market due to the exports from China. The export of semi-finished products may reach 4m tonnes this year, while at the same time China’s primary aluminium production may surpass demand by 1m tonnes.

This is the reason why it is not appropriate to talk of a market deficit, even outside China. Despite an obvious production deficit outside China, the global market surplus will remain until China exports more products than the world market (outside China) can consume. This is because granted the amount of products exports from China, there is correspondingly less demand from extruders and rolling mills for primary aluminium from world smelters (ex China). In conclusion, in the event that China’s exports of products (presuming pri-mary aluminium exports would remain mini-mal too) decrease to 1m tonnes per year, or less, even with a weakening Chinese economy, the aluminium price would remain at current levels or even rise slightly.

Demand from the automotive and aero-space industries will remain high and even grow (above all in the USA) so the main risk for the price development is and will remain China’s export of products. If we, for instance, compare the situation with copper, the price is high because China imports some 3m tonnes of refined copper per year. The decrease in imports this year has already been reflected in lower LME copper prices and any further decrease of imports in 2015 will also be re-flected in the price. What would happen with the aluminium price if China turns into a net importer either of primary aluminium or semi-finished products, some 3-4m tonnes per year,

instead of exporting that much?Unfortunately for smelters (ex China),

but fortunately for end consumers (automo-tive, aerospace), this will not happen in the next two to three years at least. The current total aluminium price including premiums at USD2,500/t may be considered as an optimum (state of equilibrium) for the aluminium indus-try, satisfying all market participants: on the one hand most primary aluminium producers are profitable and on the other hand, the price is affordable for downstream producers and end consumers. Growth towards USD3,000/t would slow future aluminium applications and demand, while a decline to USD1,800/t or less would force many primary aluminium producers to close. In the long term, stable prices are important for supporting substantial growth in demand and new applications. This is the reason why many consumers request long-term contracts with fixed price and de-livery quantities.

Another point where analysts disagree is aluminium premiums. Many expect them to fall next year, after LME rules for metal deliv-ery out of warehouses are implemented. Also, eventually a rise of interest rates and frequent backwardation (when the price for prompt de-livery is higher than the 3-month price, etc.) will lead to the cancellation of financing deals, allowing metal from warehouses to enter the market. However, it is more likely that these process will develop gradually over several years and will not necessarily result in a flood of metal onto the market and significant fall of premiums in 2015. Metal from LME ware-houses may be transferred to other warehous-es, both registered and non-registered ones, instead of arriving on the market immediately. It is more likely that big traders and funds, who hold most of the metal in financing deals at warehouses (Glencore, Goldman Sachs), will not allow large amounts of metal to reach customers at once, but gradually, in smaller amounts over a longer period of time. With high and still rising demand, aluminium (and other metals) premiums may remain at current record high levels, or a little lower, in 2015. Finally, Standard Bank London argued that premium hedging contracts may also support and prolong high premiums.

author

Goran Djukanovic is an aluminium market analyst. He is located in Podgorica, Montenegro. Email: [email protected].