26

Local Internet interconnection Simon Hampton AOL Europe

Local Internet interconnection

Simon Hampton

AOL Europe

Overview

� The need for flat rate

� Network costs & interconnection models�Per-user pricing

� capacity-based pricing

� Local and regional interconnection

� Non-discrimination: is it any use?

The need for flat rate

� Increases Internet penetration 30%

� Address the usage gap:�EU: 30% of households for 15 mins a day

�US: 50% of households for 70 mins a day

� Increases "e-confidence" and thus boosts e-commerce

� Reaches the entire country today

� Provides an affordable "taste" of theInternet – stimulates demand forbroadband (fixed & mobile)

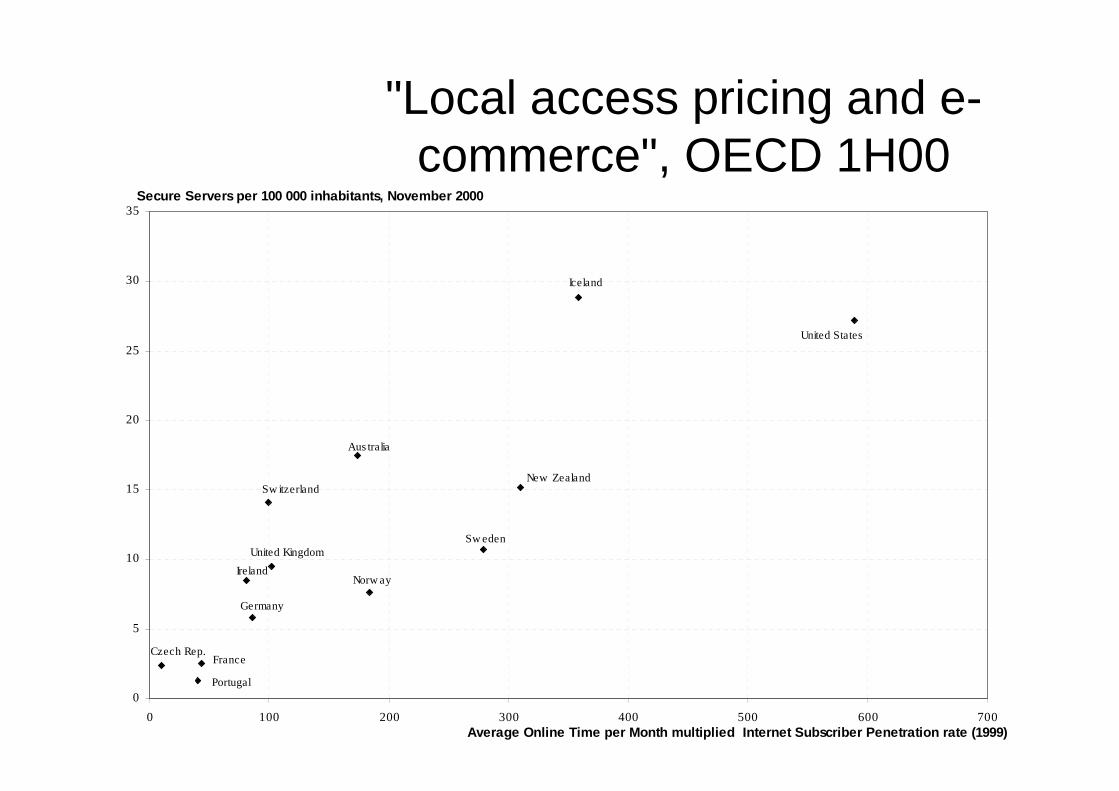

"Local access pricing and e-commerce", OECD 1H00

Sw eden

Aus tralia

Czech Rep.France

Germany

Iceland

Ireland

New Zealand

Norw ay

Portugal

Sw itzerland

United Kingdom

United States

0

5

10

15

20

25

30

35

0 100 200 300 400 500 600 700

Secure Servers per 100 000 inhabitants, November 2000

Average Online Time per Month multiplied Internet Subscriber Penetration rate (1999)

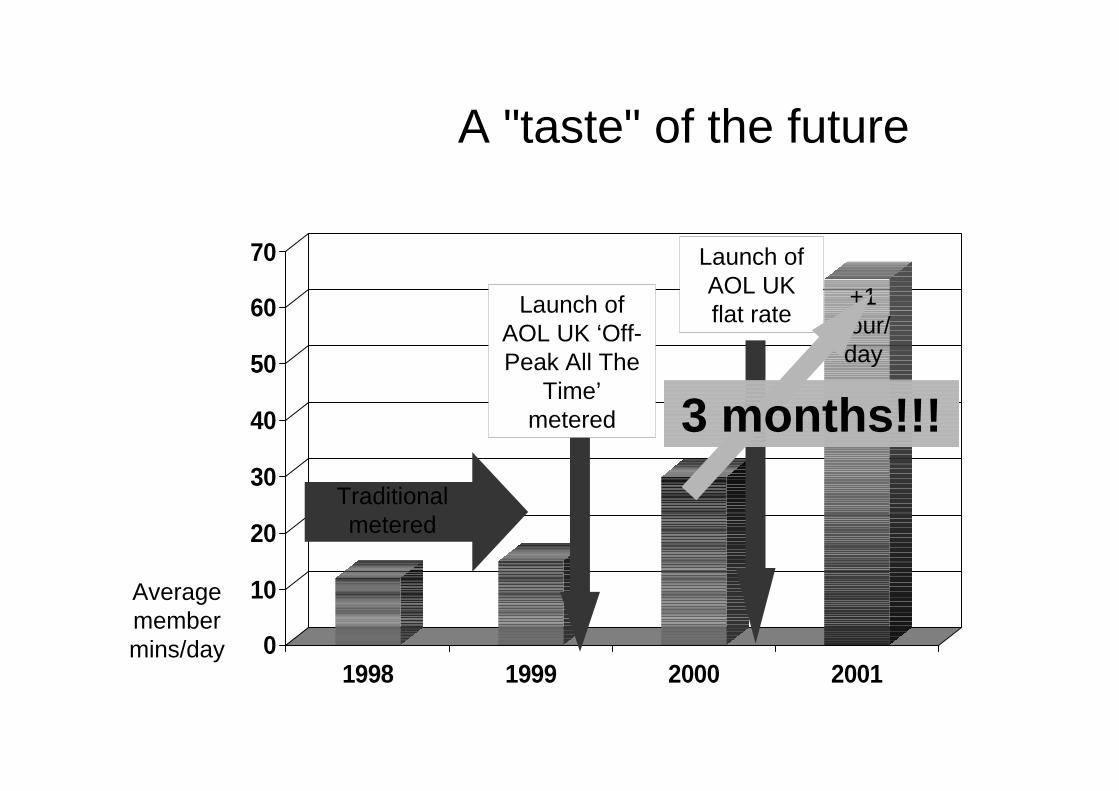

A "taste" of the future

0

10

20

30

40

50

60

70

1998 1999 2000 2001

Traditionalmetered

Launch ofAOL UK ‘Off-Peak All The

Time’metered

Launch ofAOL UKflat rate

Averagemembermins/day

+1hour/day

3 months!!!

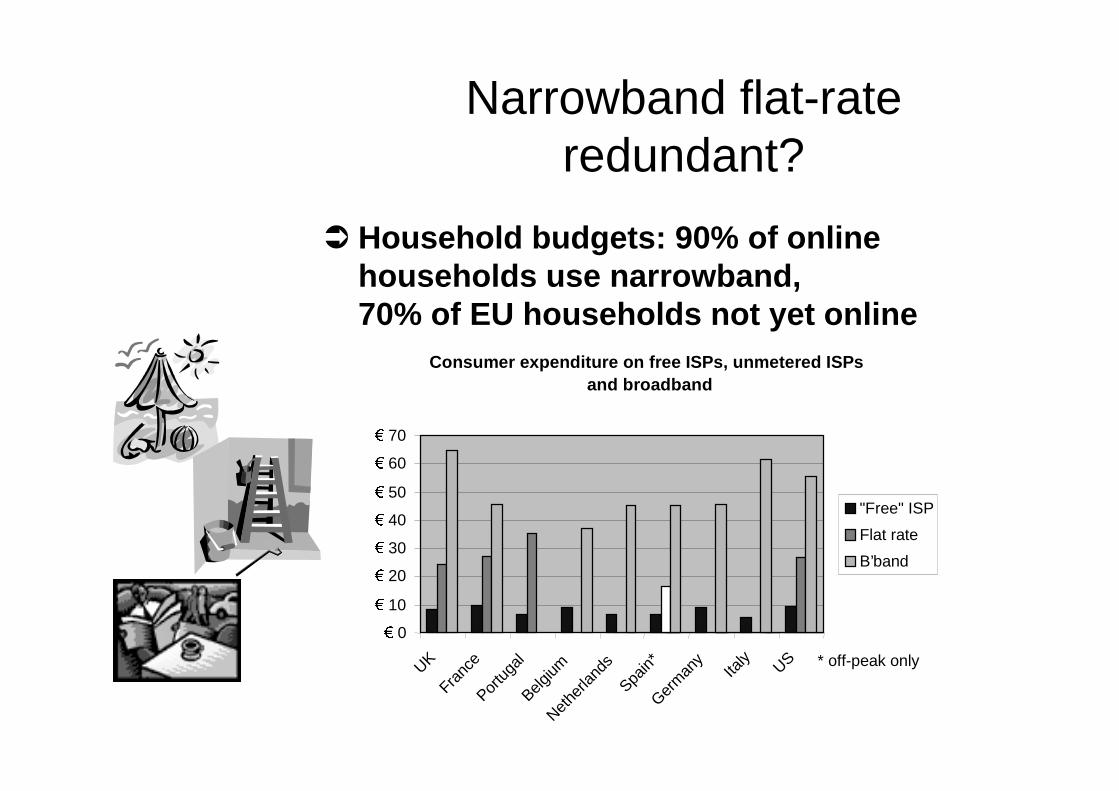

Narrowband flat-rateredundant?

� Household budgets: 90% of onlinehouseholds use narrowband,70% of EU households not yet online

Consumer expenditure on free ISPs, unmetered ISPs and broadband

0

10

20

30

40

50

60

70

UKFra

nce

Portu

gal

Belgium

Nethe

rland

sSpa

in*Ger

man

y

Italy US

"Free" ISP

Flat rate

B’band

* off-peak only

Narrowband flat-rateredundant?

Per-userprice

Time

Early adopters

Mass market

Broadband

FRIACO based narrowband"Heavy users"mean limitedcircuit sharing

Remaininglighter userspermit greatercircuit sharing

Network costs and pricing

Fixed costs:line rental or

LLU

Costs driven by number ofsimultaneous callers,

but charged by the minute!

Costs driven bysimultaneousdata volumes

PSTN IP

ISPPoint of

interconnect

Local loop Mo

dem

s

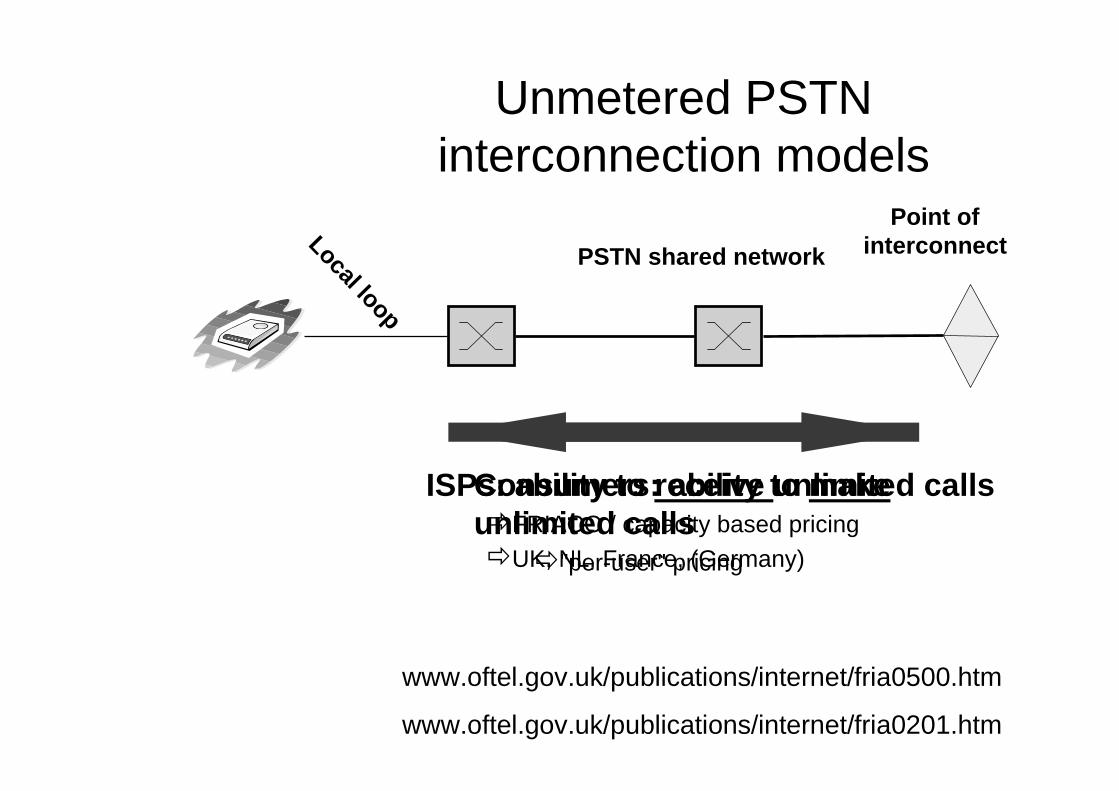

Unmetered PSTNinterconnection models

Consumers: ability to makeunlimited calls

�"per-user" pricing

ISPs: ability to receive unlimited calls�FRIACO / capacity based pricing

�UK, NL, France, (Germany)

www.oftel.gov.uk/publications/internet/fria0500.htm

www.oftel.gov.uk/publications/internet/fria0201.htm

PSTN shared network

Point ofinterconnectLocal loop

Per-user pricing

� Lump sum interconnection charge�Termination model: Spain

�Origination model: Portugal, Japan ISDN

� Per-call (’set-up’) charge�Australia

� Unlimited call service� Japan analogue, Brazil

� "Free" – included in line rental�US, Canada

�Mexico: 100 calls�New Zealand: residential only

Per-user pricing &capacity management

� “Flat rate pricing means people will stayonline all day and blow up incumbents’network”

� Consumers pay for PSTN usage directlyto incumbent

� ISPs - running IP networks - are largelyindifferent to when, and for how long,consumers are online

� Trouble brewing…? Maybe not!

Capacity based pricingFlat Rate Internet Access Call Origination

� ISPs buy capacity to receive calls, andmust use it efficiently

�The more users share a circuit, the lower the per-user cost

� ISPs’ scope to stagger demand�Price

�Content�Quality of service!

� Political benefit: privatise the "evening-peak" problem

Endorsements

"In an ideal situation … capacity basedcharging would be the most efficientinterconnect pricing rule."

(Commission Recommendation, 1997)

"Daher eigne sich internetverkehr besser fürkapazitätsbezogene Preise"

(RegTP, November 2000)

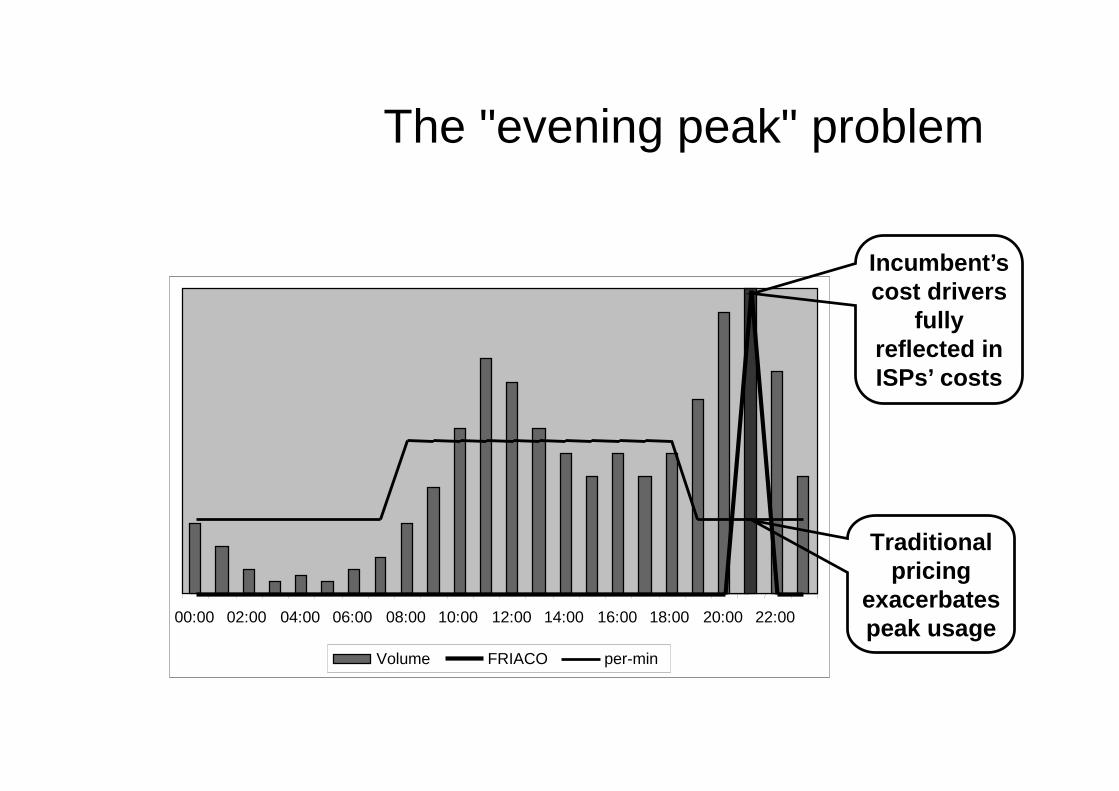

00:00 02:00 04:00 06:00 08:00 10:00 12:00 14:00 16:00 18:00 20:00 22:00

Volume FRIACO per-min

The "evening peak" problem

Traditionalpricing

exacerbatespeak usage

Incumbent’scost drivers

fullyreflected inISPs’ costs

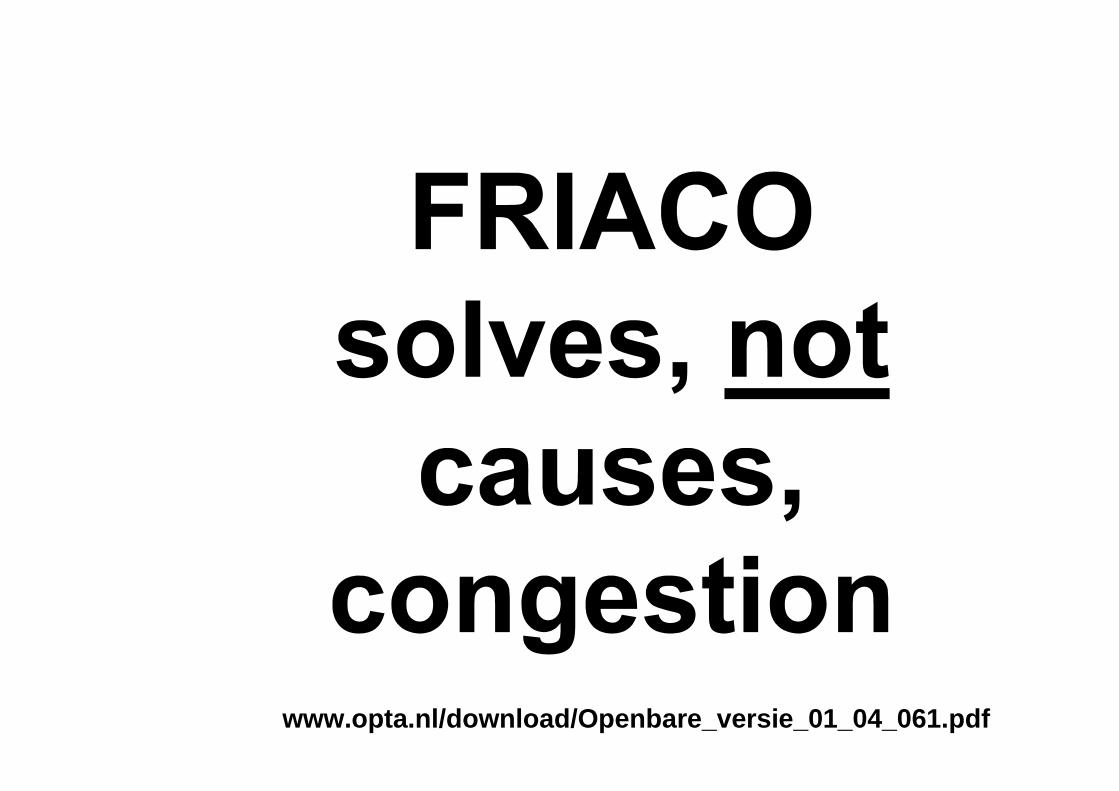

www.opta.nl/download/Openbare_versie_01_04_061.pdf

Interconnect benchmarks

0200400600800

100012001400160018002000

( p

er y

ear)

BT FT

KPN DTTele

fonic

a* PTPer user IC

Regional FRIACO

Local FRIACO

* Telefonica is off-peak only

Local/regional interconnect

� ISP innovation depends on calltermination competition

�Kickbacks�Call & access bundled offers�Carrier selection + Internet access bundle, etc

� Liberalisation just 3 years’ old�OLOs interconnected at regional level

� Variety of origination products used�Retail minus termination outpayment� Indirect access�0800�Special Internet pre-fix, and…�… FRIACO

Policy balance

� "Internet call origination traffic should betaken off the PSTN as early as possible"

�Strategic advantage for incumbent, as they are inevery local exchange already

- Need modem co-location at LEX

�Higher OLO termination costs- Potentially inefficient investment in digging to LEX

� Preserve call termination competition�OFTEL "Single Tandem FRIACO", Feb 2001

� "IP interconnect"�Could extend local access dominance to modems

and backhaul

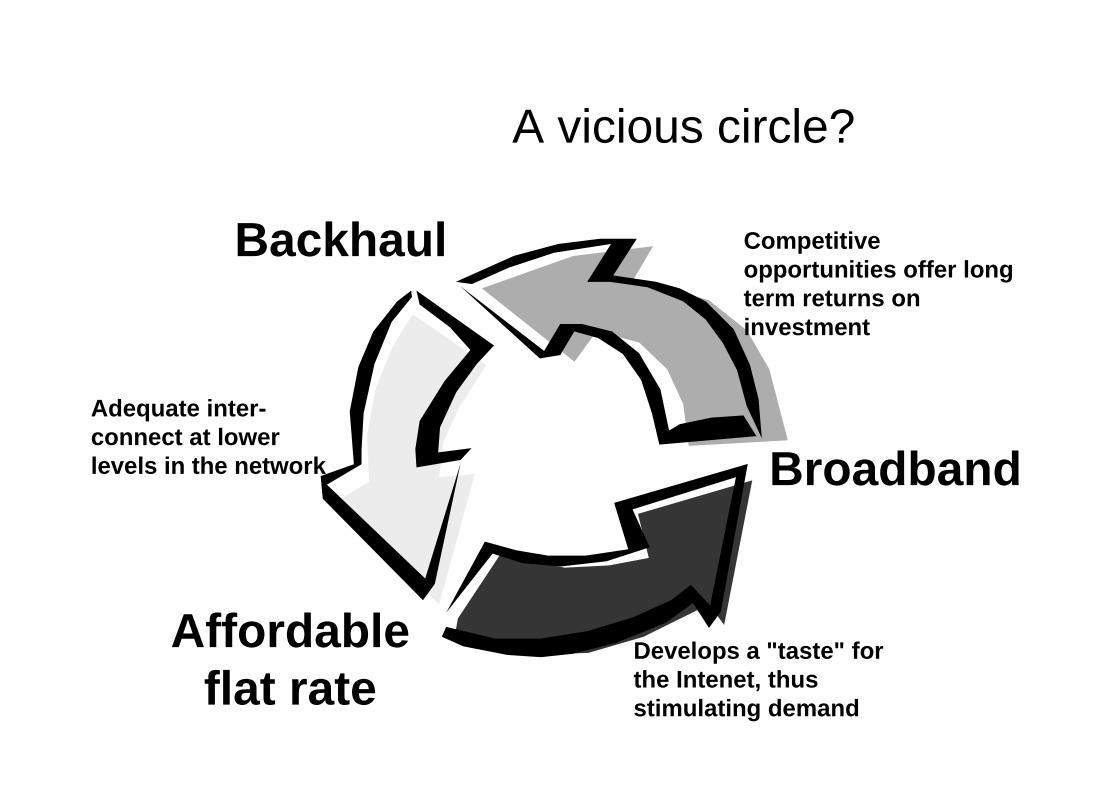

A vicious circle?

Backhaul

Affordableflat rate

Broadband

Competitiveopportunities offer longterm returns oninvestment

Adequate inter-connect at lowerlevels in the network

Develops a "taste" forthe Intenet, thusstimulating demand

Non-discrimination

� WTO commitments

� Anti-trust obligation on dominantcompanies

� EU interconnection Directive�Basis for German RegTP action

� "Reasonable request"�Basis for action in UK and NL

- OFTEL prodded into faster action because of BT flatrate

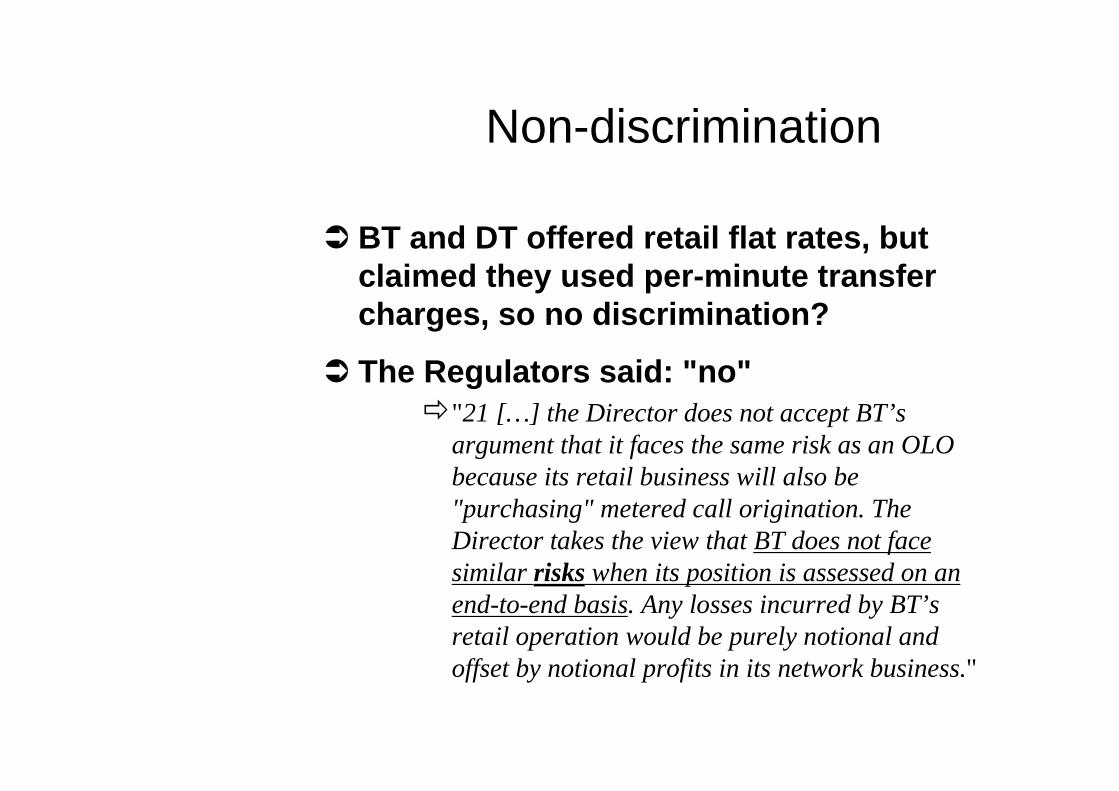

Non-discrimination

� BT and DT offered retail flat rates, butclaimed they used per-minute transfercharges, so no discrimination?

� The Regulators said: "no"�"21 […] the Director does not accept BT’s

argument that it faces the same risk as an OLObecause its retail business will also be"purchasing" metered call origination. TheDirector takes the view that BT does not facesimilar risks when its position is assessed on anend-to-end basis. Any losses incurred by BT’sretail operation would be purely notional andoffset by notional profits in its network business."

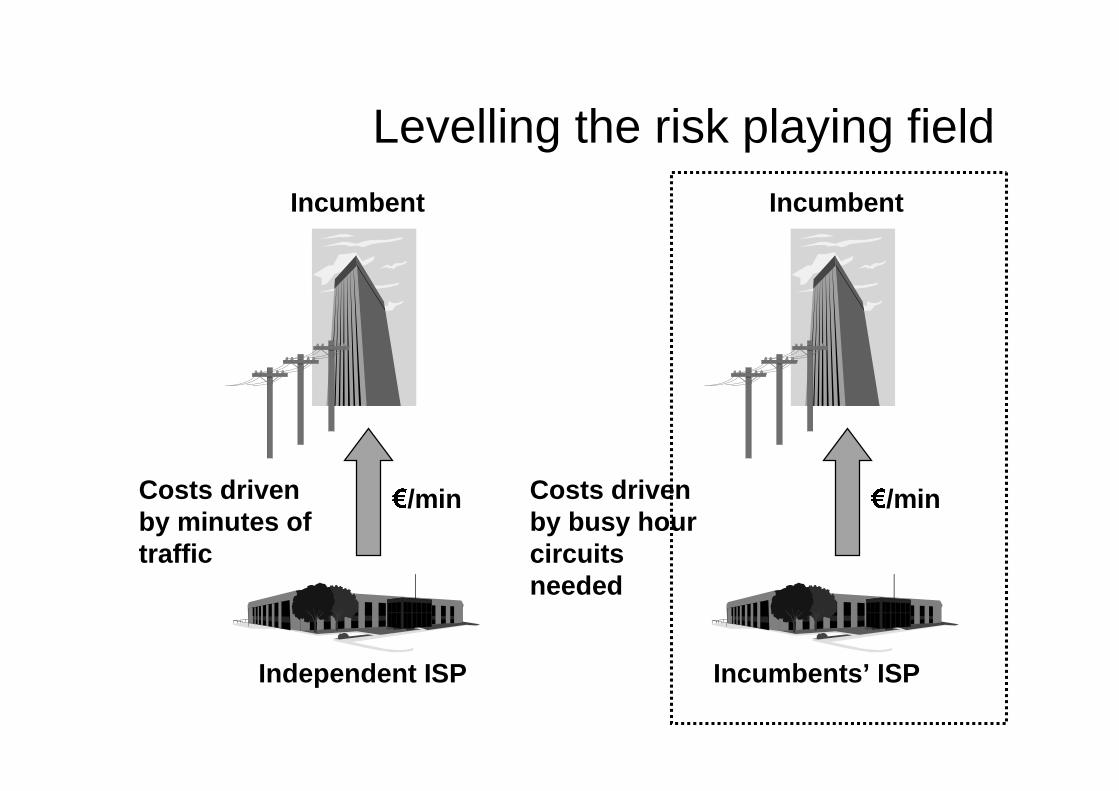

Levelling the risk playing field

Costs drivenby busy hourcircuitsneeded

/min

Incumbents’ ISP

Incumbent

/min

Independent ISP

Incumbent

Costs drivenby minutes oftraffic

Non-discrimination

� TOL withdrew its flat-rate prices, andjudge threw out RegTP’s decision

�RegTP had linked need for flat rate interconnectprices from DT to TOL flat rate retail prices

� Incumbents’ costs are inherently capacitybased, irrespective of transfer and/orretail prices

�option of capacity based interconnection prices isalways necessary

�Failure to provide is implicit discrimination

Other shared networks

� Costs driven by simultaneous usage

� Local access network�SMS, GPRS, UMTS

�Cable TV networks

�NOT DSL

� All IP backbones

� Main issue is vertical integration, and alazy carry-over of retail models intowholesale pricing

Conclusions

� Flat rate is key stepping stone tobroadband on the demand side

� PSTN traditionally mis-priced – what willhappen to off-peak pricing?

� FRIACO�Key ingredient for flat-rate consumer prices

�Addresses congestion issues head-on�Both regional and local interconnection needed

� Capacity-based pricing needed to ensurereal non-discrimination