46

APLA - Annual Regional Conference 19-23 rd October 2015 LOTTERY INDUSTRY UPDATES : PDJ

APLA - Annual Regional Conference 19-23rd October 2015

LOTTERY INDUSTRY

UPDATES : PDJ

APLA - Annual Regional Conference 19-23rd October 2015

SAIL WITH KOREA WAVE !

APLA - Annual Regional Conference 19-23rd October 2015

SURF WITH POLYNESIA WAVE !

PRESENTATION

1. THE LOCAL CONTEXT (POLYNESIA & POLYNESIANS)

2. THE COMPANY (SALES, NETWORK & GAMING MODEL)

3. OUR CHALLENGES (SPORTS BETTING & INTERNET)

Thierry GABARRET

Chief Executive Officer - La Pacifique des Jeux, French Polynesia International Relations Director - La Française des Jeux, France Executive Board Member of Internationale des Jeux, France Vice-President of Beijing Zhongcai Printing, China

APLA - Annual Regional Conference 19-23rd October 2015

1. THE LOCAL CONTEXT

WHAT IS FRENCH POLYNESIA ?

Society Islands

Marquesas Islands

Tuamotu Archipelago

Austral Islands

Gambier Islands 9,763 miles from Paris

6,606 miles from Seoul

5,897 miles from Tokyo

4,104 miles from L.A.

3,808 miles from Sydney

1767 : descovered by Captain Samuel Wallis

1959 : became a « French Overseas Territory »

1984 : Status of « Internal Autonomy »

Which history ?

Where is it ?

What geography ?

2014 : A long-lasting crisis (since 2008)

WHO ARE THE POLYNESIANS ?

Split of population by cultural make up

Ma’ohi : 66%

Chinese : 5%

Europeans : 12%

Mixed Tahitians : 17%

WHAT ARE THE RELIGIONS ?

Split of population by religion

Protestants : 54%

No religion : 6%

Others : 10%

Roman Catholics : 30%

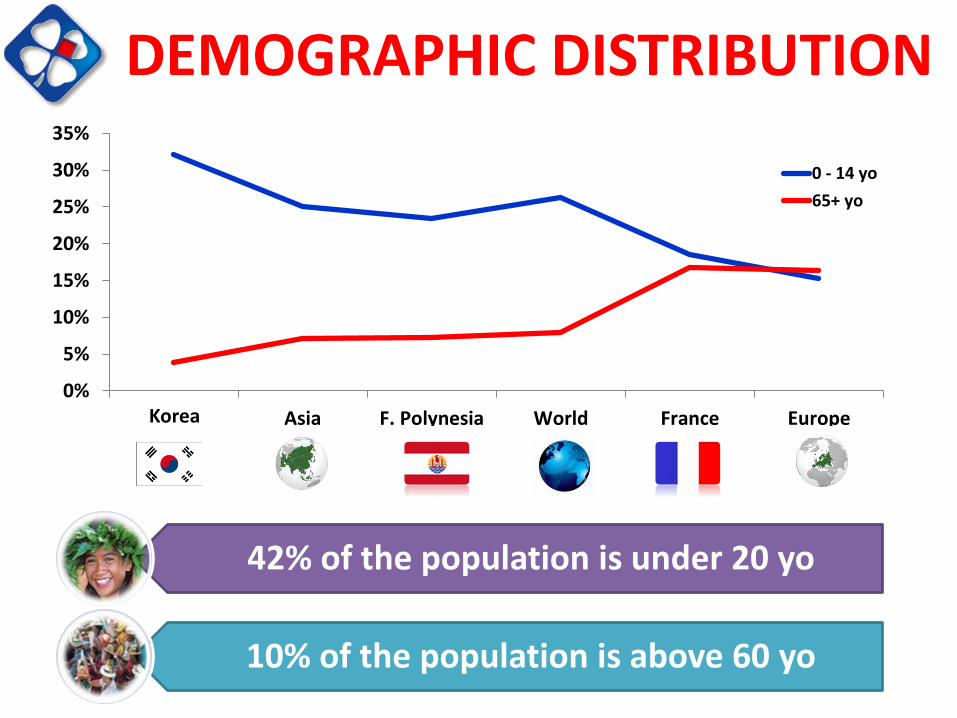

DEMOGRAPHIC DISTRIBUTION

0%

5%

10%

15%

20%

25%

30%

35%

Cambodia Asia F. Polynesia World France Europe

0 - 14 yo

65+ yo

42% of the population is under 20 yo

10% of the population is above 60 yo

Korea

SCOPE OF THE LOCAL MARKET

Cock

Va’a

Poker

Kikiri

Casino

Horses

Instant

games

Draw

games

Amigo

Sport betting

Illegal betting Under question PDJ monopoly

SPECIFIC CULTURAL MAKE UP

Weight of religion Weight of tradition Role of superstition

Necessity to deal with these issues

2. THE COMPANY

Total sales 2014 : €42 M i.e. 0.3% of FDJ total sales (€12.99 bn)

5 draw based games 15 scratch games

KEY FIGURES

100% subsidiary of FDJ (under specific agreement with Polynesian government)

No sports betting

No digital lottery

140 POS over a territory as wide as Europe (0,4% FDJ)

165,000 players (88% of adult pop.)

20 direct employees (137 indirect)

Hinano FREDRIKSEN

Finance & Accounting Manager

Vaiana CONAN

Retail Accounting

Magali TIHONI

General Accounting

Thomas SONNENTRUCKER

Logistics Manager

Caroline PEREZ Mereana VANAA Hinano MANA Thérèse AHINI

Sales Assistants

Patrick GASSION

IT & Security Manager

Orama MONFOUGA Vanessa BISIAUX Manolios CHANG Chantal RERE

Sales Promoters

Myrna LY Noémi TUAIRAU

Control

Thierry GABARRET

Chief Executive Officer

Didier PAUTRAT

Deputy General Manager

Valérie VEDEL

Executive Assistant

Guillaume REYNAUD

Commercial & Marketing Manager

Nastasia LAW

Product Manager

ORGANIZATION CHART

PDJ SALES AND NETWORK Points of sale

TAHITI = 73%

ISLV + BORA = 13%

MOOREA = 7%

TUAMOTU = 4%

AUSTRALES = 2%

MARQUESAS = 1%

1991-1995 1996-2000 2001-2005 2006-2010 31/12/2012

23.5

27.7

37.7

42.7 43,7

Average sales per period of time

In M€

FDJ

PDJ

POS

1991-1995 1996-2000 2001-2005 2006-2010 2011-2014

140 POS compared to 32,700 retailers for FDJ (0.4%)

Sales 2014 : € 42 M compared to € 13 bn for FDJ (0.3%)

PHYSICAL NETWORK

3 POINTS DE VENTE

2 POINTS DE VENTE

9 POINTS DE VENTE

1 POINT DE VENTE

9 POINTS DE VENTE 97 POINTS DE VENTE

3 POINT DE VENTE

2 POINTS DE VENTE

1 POINT DE VENTES

5 POINTS DE VENTE

73% 13%

4% 1%

2%

7%

10%

60%

90%

100% sell scratch

games

SPLIT BY GAMES

GEOGRAPHICAL DISTRIBUTION

Lottery signs

OUTDOOR SIGNAGE

Signage material

Jackpot display Promotional posters

INSIDE EQUIPMENT

Dedicated counter

Dedicated Gaming Modulo

player’s space

Promotional posters

Winners’ promotion

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

46 914 K€

39 846 K€ 42 006 K€

EVOLUTION OF SALES

SCRATCH GAMES

LOTO + SUPER LOTO JOKER+

RAPIDO KENO

EURO MILLIONS OXO

AMIGO

Draw based games : 86% Scratch Games 14%

STAKES PER TYPE OF GAME

16%

2%

25%

16%

27%

14%

REPARTITION DU C.A. TOTALau 31/03/2015

LOTO

JOKER +

KENO

AMIGO

EURO MILLIONS

GRATTAGE

TOTAL SALES 2015 half-year

5 draw based games (all FDJ’s games) 15 scratch games (5 launching a year)

23%

47%

30%

DETAIL GAMME GRATTAGE au 31/03/15

100 F

200 F

500 F

SCRATCH GAMES 2015 half-year

Out of scope 1 Out of scope 2

18%

34%

16% 20% 24%

12% 12% 10% 18%

13%

75%

60%

75% 64%

68%

54% 51% 50%

54%

46%

7% 6% 8%

4%

3%

1%

13% 5%

34% 37% 39%

28%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

SCRATCH GAMES FOCUS

100 F

200 F

500 F

Evolution by segment (15 games on 3 price segments)

Players

Territory

FDJ+PDJ

Retailers 0

5,000

10,000

15,000

20,000

25,000

30,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

REDISTRIBUTION OF STAKES

Players : 55% - Polynesian Territory : 22%

Retailers : 5% - PDJ + FDJ : 18%

8.5 M€

7.5 M€

2.1 M€

23.9 M€

Total 2014 : € 40 million were redistributed

Since 1991 : € 0.8 bn to the local economy

FDJ REDISTRIBUTION

Total 2014 : € 12.3 bn (+5,8% vs 2013)

Equivalent jobs : 29,250 (current min wage)

95% of stakes redistributed to the players, the distribution network and the community

The network (physical or not)

The community

The players

Winners

65%

Public Finance

24%

Distribution network 6%

FDJ’s operations

5%

INTEGRITY DEVELOPMENT RESPONSABILITY SECURITY PROXIMITY

…

few players who play a lot !

More players who play less is better than …

PDJ GAMING MODEL

PLAYER’S PROFILE

Social Solitary

Interactive

Ambitious

Opportunist

Ordinary people

SUPERSTITIOUS

Gender Age

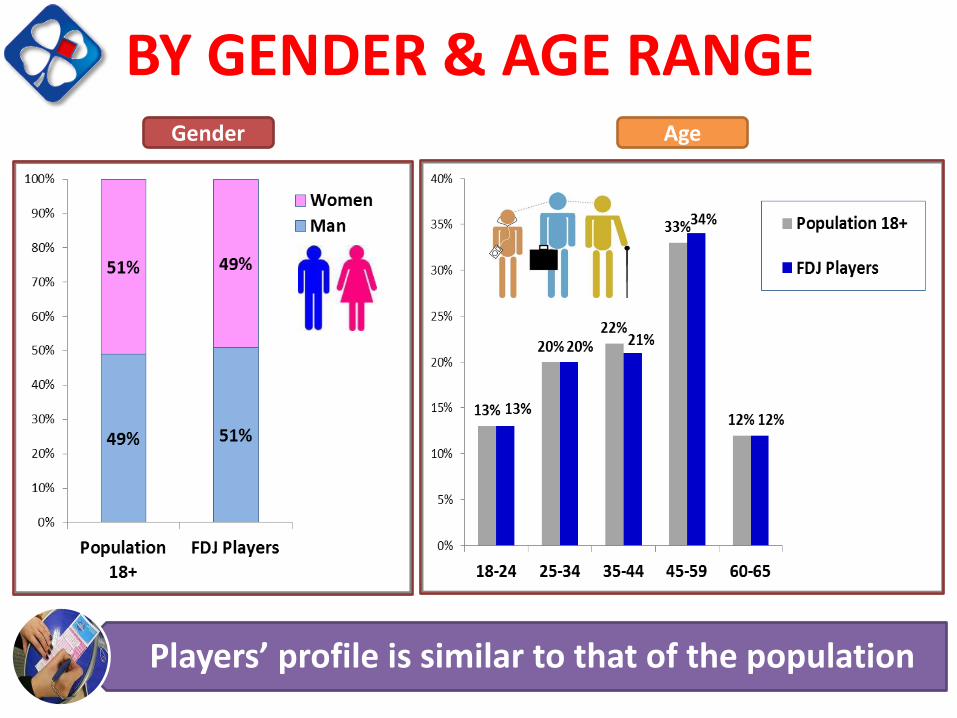

BY GENDER & AGE RANGE

Players’ profile is similar to that of the population

Socio-Professional category Monthly Revenue

BY SOCIO-DEMO & REVENUE

Players’ profile is similar to that of the population

SPENDING PER INHABITANT

86,941

74,002

59,695

36,562 34,432

32,814 30,831 30,802

25,544 24,860 22,995

19,910 19,720 19,455 18,667 17,661

In F.CFP per year

Moderate level of annual spending

High penetration rate : 88%

MAIN TASKS

Legal

Regulatory

Contractual Ethical

Procedural

“Ensure the integrity and the security of game operations …”

AC

CES

S TO

GA

MES

PR

IZE PAIY

MEN

TS

RULES

IMPLEMENT CONTROL

1 • Corporate Governance

2 • Responsible Gaming

3 • Customer Satisfaction

4 • Community Involvement

5 • Environmental Impact

6 • Partner Relations

7 • Human Resources

7 COMMITMENTS IN KEY AREAS

6 VALUES THAT GIVE SENSE

Integrity Fairness

Proximity Optimism Solidarity

Inventiveness

GAMES’ SUCCESS

Promote a safe and regulated model

Give benefit to the general interest

VALUES & COMMITMENTS

CERTIFICATIONS

PDJ has been a member of APLA since 2005

Certified ISO 27001 in June 2015 Certified WLA SCS in Sept 2015

3. THE CHALLENGES

0

10

5

15

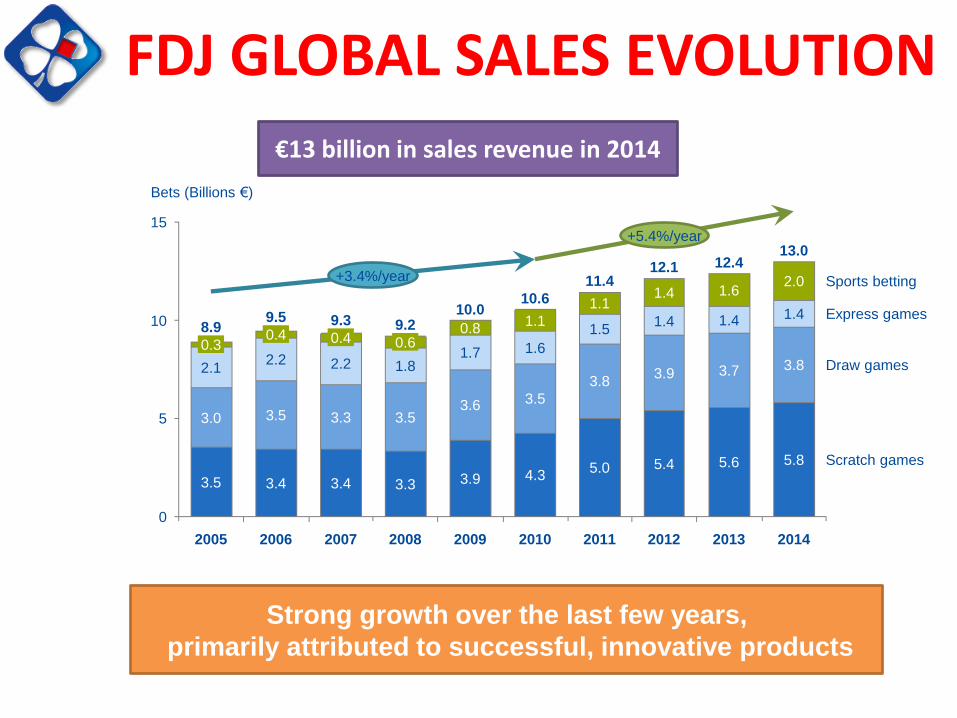

Bets (Billions €)

2005 2006 2007

13.0

9.5

12.1

10.0 9.2 9.3

8.9 Express games

2010 2008

1.1

1.1

1.7

1.5 0.6 1.6

0.8

1.4

1.4

1.6

1.4

2.0

1.4

3.5 3.4 3.4 3.3 3.9 4.3 5.0 5.4

3.8 3.9 3.7 3.8

+3.4%/year

2011 2012 2013 2014

Scratch games

2.1

Sports betting

2.2

2009

+5.4%/year

Draw games 1.8

10.6

11.4

12.4

5.8

0.4 0.3

5.6

0.4

3.5 3.6 3.5 3.3 3.5 3.0

2.2

Strong growth over the last few years,

primarily attributed to successful, innovative products

€13 billion in sales revenue in 2014

FDJ GLOBAL SALES EVOLUTION

FDJ SALES PER RANGE

15,2%

44,8%

29,4%

10,6%

+20%

+1,7%

+4,8%

-1% GLOBAL GROWTH

DUE TO :

- New option EUML

- Soccer World Cup

- Instant tickets

FDJ SPORTS BETTING

23 different sports

available

Paris Mutuel since 1985 :Loto Foot

Oddset betting since 2003 : “ParionsSport”

Internet betting since 2009 : “ParionsSport”

Mobile app launched in 2013 on iOS (250,000 downloads)

15.2% of total sales for Sports betting (+20% vs 2013)

N°1 IN EUROPE FOR SPORTS BETTING

49%

79%

51%

21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Population 18-65 Sports Betting

ManWomen

Gender Age

13%

20% 22%

33%

12%

25%

28% 26%

8%

0%

5%

10%

15%

20%

25%

30%

35%

18-24 25-34 35-44 45-59 60-65

Population 18-65

Sports Betting

SPORTS BETTING PLAYERS

Mainly male and much more age cluster 25-44

7,540

6,070

2,357

1,978

1,511

868 597

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1ChinaSportsChine

2HKJC

Hong Kong

3Sports Toto

Corée du Sud

4FDJ

France

5OPAPGrèce

6Lottomatica

Italie

7Svenska Spel

Suède

2014 ranking Sales in M€

FDJ remains n°1 in Europe. All the lotteries take benefit from the Soccer World Cup : China Sports (+82%), HKJC (+24%), FDJ (+20%), OPAP (+20%)

N°1

N°4

SPORTS BETTING WORLDWIDE

0.00%

1.00%

2.00%

3.00%

4.00%

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014

Online sales

% of total sales

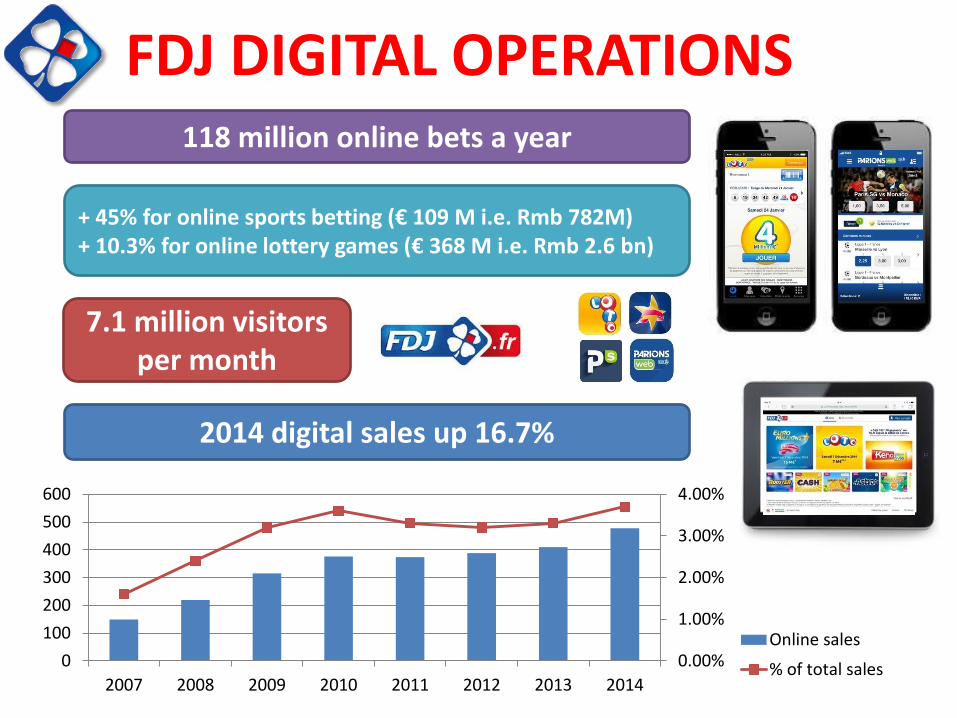

FDJ DIGITAL OPERATIONS

+ 45% for online sports betting (€ 109 M i.e. Rmb 782M) + 10.3% for online lottery games (€ 368 M i.e. Rmb 2.6 bn)

7.1 million visitors per month

118 million online bets a year

2014 digital sales up 16.7%

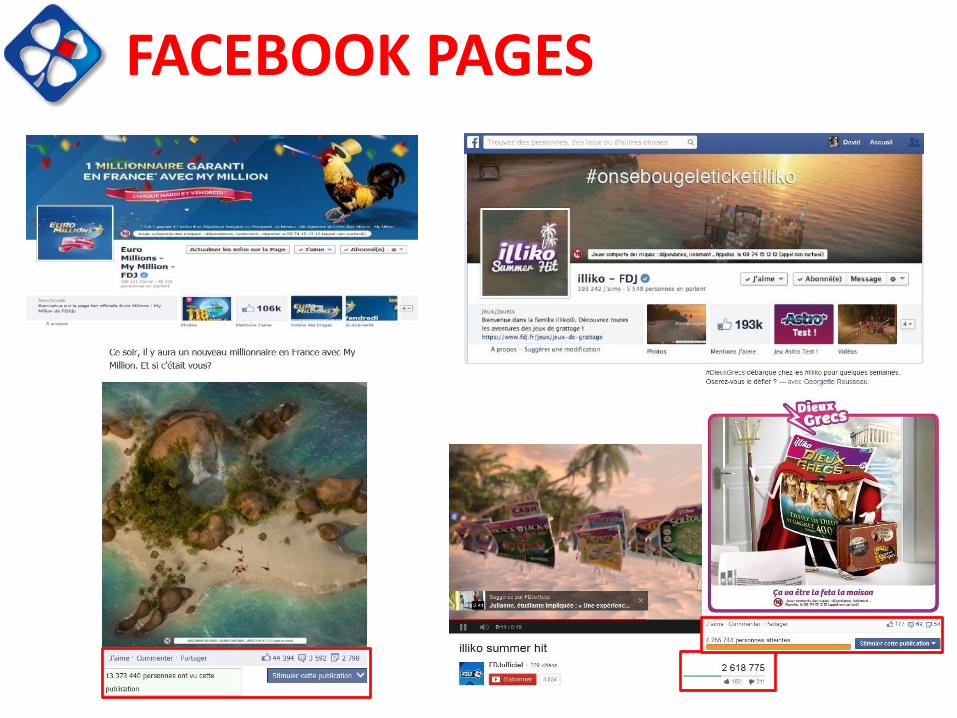

SOCIAL NETWORKS TOTAL FDJ

CHALLENGES

Increase the audience and the coverage of the brands

Participate in chats and develop proximity

Listen, moderate and watch the e-reputation

Groupe

Fondation

Eté FDJ

Equipe FDJ

Parions Sport

Parions Web

Illiko

LOTO

EUML

2 434 3 782 5 432

143 620

127 942

131 247

341 278

5 760 9 151 26 526

3 538

33 638

62 746

571

31 707

133

45 401 followers

874 217 fans

FACEBOOK PAGES

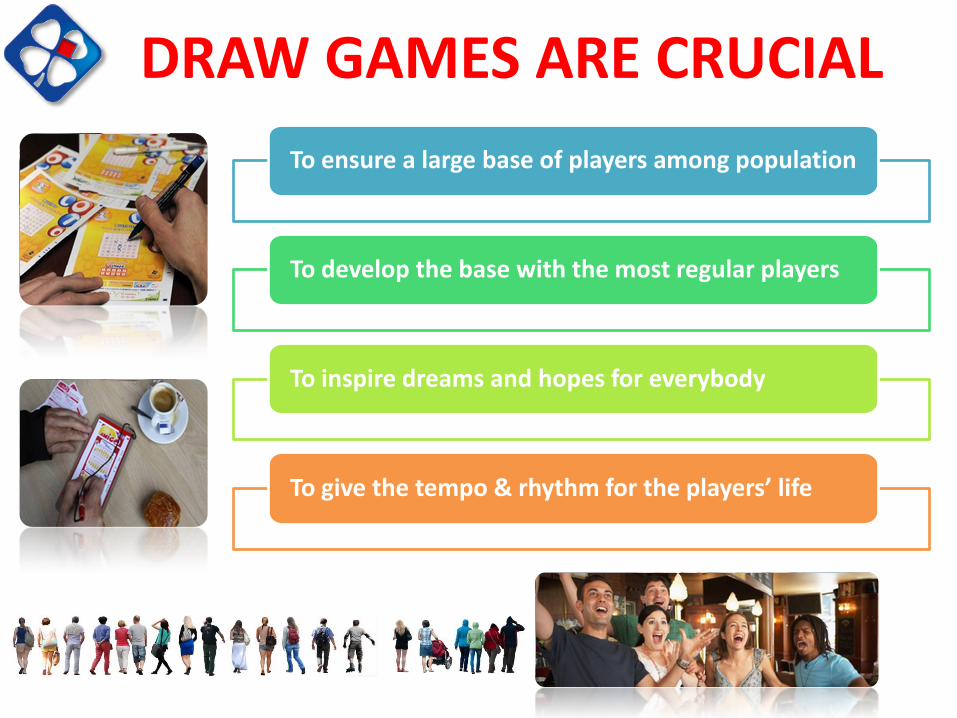

DRAW GAMES ARE CRUCIAL

To ensure a large base of players among population

To develop the base with the most regular players

To inspire dreams and hopes for everybody

To give the tempo & rhythm for the players’ life

INSTANTS ARE ESSENTIAL

To give access to gaming to the largest population

To grant a winning experience to players (pay outs)

To bring permanent novelties to the market

To enable to recruit new players (1st price segment)

OTHERS AS OPPORTUNITIES

● satisfy much lower players base than the core range ● create a niche or a complement to attract new players

ENRICH THE PORTFOLIO IN ORDER TO :

● enable new practices and recruit new players ● reach the motivations, needs & hopes of the players

● permanent entries and departures create a need to recruit permanently to ensure a consistent development ● trust and confidence of people are fragile

Present moves

Products

Retail

Digital

International

CSR

Security

Integrity

STRENGHTEN THE MODEL

1 • Recruit new players

2 • Enhance proximity

3 • Responsible Gaming

4 • Security and Integrity

5 • Higher performance

6 • Corporate image

Coming challenges

… RUN THE BUSINESS SMARTER SELL BETTER = SELL MORE !

APLA - Annual Regional Conference 19-23rd October 2015

« SELL WITH KOREA WAVE ! »

APLA - Annual Regional Conference 19-23rd October 2015