Page 1

A

PROJECT REPORT ON

“TO UNDERSTAND THE USAGE PATTERN AND COMSUMER ATTITUDE TOWARDS

TOMATO SAUCES WITH MAGGI SAUCES AS A PRODUCT”

SUBMITTED IN THE PARTIAL FULFILLMENT OF THE REQUIREMENT OF TWO-YEAR FULL TIME COURSE OF BACHELOR’S DEGREE IN BUSINESS

ADMINISTRATION

Under the guidance of SUBMITTED BY:-Prof. Manoj Arora Pratik VohraAssistant Professor of Business Administration Class Roll no: 1629

Gobindgarh Public College1

Page 2

(Affiliated to Panjab University, Chandigarh)

CERTIFICATE

This is to certify that project entitled “TO UNDERSTAND THE USAGE PATTERN AND

COMSUMER ATTITUDE TOWARDS TOMATO SAUCES WITH MAGGI SAUCES AS A

PRODUCT” has been submitted to Punjab University, Chandigarh in the partial fulfillment of the

requirements for the degree of bachelor of business administration is a bonafide research work

carried out by PRATIK VOHRA under my supervision and that no part of his r project has been

submitted earlier to me.

The `assistance and help receiving during the course of investigation has been fully acknowledGED

Prof.

ACKNOWLEDGEMENT2

Page 3

I am highly indebted to Prof Manoj Arora, for his valuable inputs at the various stages of the project

and for providing valuable advice in designing and implementing various research tools to collect

relevant data.

I am thankful to those individuals who gave in their precious time in filling the questionnaire and

providing their immense cooperation without which the project would not have been possible.

I am very grateful to Prof. Rishi kesh Mourya (HOD) for having given me an opportunity to undertake

this project.

Finally, I would like to state that the project not only fulfilled an academic requirement, but would also

help me in future endeavors in the years to come.

]

DECLARATION

3

Page 4

I hereby declare that the project titled “TO UNDERSTAND THE USAGE PATTERN AND

COMSUMER ATTITUDE TOWARDS TOMATO SAUCES WITH MAGGI SAUCES AS A

PRODUCT” is an original piece of research work carried out by me under the guidance and

supervision of Mr. MANOJ ARORA. The information has been collected from genuine & authentic

sources. The work has been submitted in partial fulfillment of the requirement of bachelor of Business

Administration to Punjab University Chandigarh.

4

Page 5

PREFACE As MICHEL DE MONTAIGNE observed: --

“There never was in the world two opinions alike, no more than two hairs or two grains; the

most universal quality is diversity.”

The nineties are a celebration of diversities. Its people differ not only in usual ways- by age & gender,

by race & nationality, by education & occupation, by marital status & living arrangements but also in

their activities, their preferences, purchases, opinions & attitudes.

So, with all of the diversity that surrounds us, the profusion of goods & services offered to us &

freedom of choice available to us, one may wonder how individual marketers actually reach us with

their highly specific marketing messages. The answer lies in the fact that in spite of the diversities

amongst us there are many similarities amongst us - constants that can be found amongst many people

of the world.

One of the few common denominators amongst all of us, despite our differences, is that above all we

are consumers & for the marketers it is important to recognize -- why and how individuals make

their consumption decisions and what attitudes they possess about a particular brand.

So, this research has been organized to explore the attitude & behavior of the consumers towards

Maggi Tomato Sauces as a whole & further through analysis, suggestions are given.

INDEX5

Page 6

1 INTRODUCTION

2. PROJECT DESIGN

3. RESEARCH METHODOLOGY USED

4. DATA ANALYSIS

5. CONCLUSIONS AND SUGGESTIONS

6. SWOT ANALYSIS FOR MAGGI SAUCES

BIBLIOGRAPHY

ANNEXURE

6

Page 7

EXECUTIVE SUMMARY

This project aims to describe the usage pattern, attitude & behavior of the consumers towards Tomato

based sauces with special emphasis on Maggi Tomato Sauce as a whole.

The project has the following Research Questions:

Image perception of the brand & the product.

Usage Pattern of consumers (in different income groups) towards Maggi Sauces.

Efficacy of advertising of Maggi Sauces.

Purchase Behavior of Consumers.

Brand Loyalty towards Maggi Sauces.

Identifying purchaser-user relationship.

Identifying the barriers to the purchase of Maggi Sauces.

An insight about other players in Tomato Sauce market.

The data for different regions is a primary one which is being collected by surveying 200-230

households in Khanna market that included the survey of various female households in

different localities.

The survey method comprises of a structured questionnaire which helps to analyze the above

mentioned objectives on the basis of this data collected from different areas.

7

Page 8

HISTORY OF NESTLE

The history of Nestlé began in Switzerland in 1867 when Henri Nestlé, the pharmacist, launched his

product Farine Lactée Nestlé, a nutritious gruel for children. Henri used his surname, which means

‘little nest’, in both the company name and the logotype. The nest, which symbolizes security, family

and nourishment, still plays a central role in Nestlé’sprofile.

Since it began over 130 years ago, Nestlé’s success with product innovations and business acquisitions

has turned it into the largest Food Company in the world. As the years have passed, the Nestlé family

has grown to include chocolates, soups, coffee, cereals, frozen products, yogurts, mineral water and

other food products. Beginning in the 70s, Nestlé has continued to expand its product portfolio to

include pet foods, pharmaceutical products and cosmetics too.

Today, Nestlé markets a great number of products, all with one thing in common:

The high quality for which Nestlé has become renowned throughout the world.

1867- Henri Nestlé founded the company in Vevey, Switzerland.

1898-Nestlé purchases its first factory outside of Switzerland – Viking Melk factory in Norway.

1905- Nestlé merges with Anglo-Swiss Condensed Milk Company.

1929- Nestlé merges with Peter-Cailler-Kohler Chocolates Suisse’s S.A.

1938- Nestlé launches Nescafe – the world’s first instant coffee.

1947- Nestlé merges with Alimentana S.A. with the brand Maggi.

1962- Nestlé purchases Findus.

1974- Nestlé becomes a significant shareholder in the Cosmetics Company L’Oreal.

1977- Nestlé purchases Alcon, manufacturer of eye care products and kits.

8

Page 9

1985- Nestlé purchases the Food Company Carnation.

1988- Nestlé purchases the confectionary company Rowntree Mackintosh and the pasta company

Buitoni-Perugina.

1992- Nestlé purchases the mineral water Company Perrier.

1998- Nestlé purchases Spillers pet foods business.

1999- Nestlé acquires Preparadosy Congelados Alimenticios LA, La Cocinera, which produces ready-

made frozen meals, pizzas, snacks and refrigerated products under the La Cocinera and Fricongel

brand names.

2000- Nestlé sells the Findus brand in all countries except for Italy and Switzerland.

2001- Nestlé merges with Ralston Purina, the premier pet food Company in North America, and with

unique expertise in the dry dog food area.

9

Page 10

NESTLE IN INDIA:

Good Food, Good Life Since The Turn of The Century

NESTLE INDIA LIMITED

Nestle India Limited is a 51% subsidiary of Nestle S.A., Switzerland – a Company that can trace its

origins back to 1866. The original business of the Company was based on milk and dietetic foods for

children. Numerous other food products have since been added to the line: Chocolate, instant

beverages (the NESCAFE process was developed in 1938) culinary, refrigerated and frozen products,

ice cream, mineral water and pet foods to make Nestle the World Food Company of the 20th century

Nestle has been international from the very beginning with 509 factories today in 83 countries and

certain global brands such as NESCAFE available in over a 100 countries. Nestle is the most

multinational of all multinationals in every positive sense- only 2% of its turnover comes from the

local Swiss Company.

The Company is present in India with the following main brands

MILKMAID, EVERYDAY, CERELAC, NESTUM, LACTOGEN, NESTOGEN, MAGGI,

NESCAFE, NESCAFE SUNRISE, NESTEA, MILO, KITKAT, NESTLE CLASSIC, MILKY

BAR, CURNCH, ALLEN'S, POLO, NESTLE PURE MILK.

Local Sourcing Of Raw Materials: Nestle Factories in India

Nestle has been associated with India since the beginning of the century - importing and trading In

Condensed Milk and Infant Food. Manufacturing in India began in 1962, with the setting up of its First

factory at Moga, Punjab. Commissioned in 1992, the Samalkha Factory manufactures weaning cereals,

culinary products and milk products and water. Nestle does not own agricultural farms of in India, in

line with its international policy aimed at encouraging and benefiting the local farmer.

10

Page 11

Nestlé’s first unit at Moga, Punjab, deals with manufacturing of milk products, infant milk food and

weaning cereals, culinary products and beverages. This factory has since involved into one of Nestlé’s

ten largest Factories worldwide. Nestle has since contributed to all strengthening of the Indian

industrial Infrastructure by setting up state-of-the-art factories in Cherambadi (TamilNadu),

Nanjangud (Karnataka), Ponda (Goa) and Bicholim (Goa).

The second factory at Choladi, Tamilnadu to produce beverages (tea) was set up in 1967. To part-

finance this project NIL went public in 1968. The third plant at Nanjangud, Karnataka, set up in 1989,

manufactures instant coffee and health beverages. Nestle India Manufactures Liquid Milk, Sweetened

Condensed Milk, Milk Powder, Dairy Whitener, Dessert Mixes, Weaning Cereals, Infant Milk

Formulae, Junior Foods, Noodles, Sauces, Soups, Super Seasoning, Pickles Instant Coffee, Tea,

Health Beverages, Chocolates, Confectionary, Wafers and Waffles.

The Company depends on locally produced raw materials to manufacture world class quality foods by

applying state-of-the- art manufacturing and processing technology. As a consequence, Nestle has not

only got the best out of natural resources in the region where it operates but has helped to upgrade the

quality and quantity of milk, coffee and coca available, for the economic benefit of the farmer as well

as the health and nutrition of the consumer.

A sterling example is the Nestle Agricultural Services contribution to the upliftment of the Moga Milk

District in Punjab over three and a half decades.

Environmentally Conscious Company:

Nestle India puts over a hundred thousand tonnes of food in the marketplace every Year, marking its

presence in most value added segments of the Indian food industry. Liquid Milk, Milk products, Infant

Milk Formulae, Weaning Cereals, Culinary Products, Instant Coffee, Tea, Health Beverages,

Chocolates and Confectionery, Wafers and Waffles.

Solid Base for the future such responsible corporate citizenship has created goodwill for the Company

in every community where it operates. Nestle plans to build on this and continue to play a leading role

in the Indian Food Industry. Given Nestle India’s past performance, Nestle S.A. is confident that it can

11

Page 12

ably support Nestle India’s vision to reach a turnover of Rs. 10,000 Crores in the very first decade of

the 21st century.

12

Page 13

Nestle India Limited – A Brief Profile

PAST & PRESENT

1959: On 28th March, the Company was incorporated at Khanna. The company was promoted by

Nestle Alimentana S.A. through a wholly owned subsidiary, Nestle Holdings Ltd., Nassau, Bahama

Islands.

1978: During the period 4, 00,114 equity shares and 382,751 existing equity shares held by Nestlé’s

Holdings, Ltd., Nassau, Bahama Islands (Nestle) were offered to the resident Indian nationals at a

premium of Rs. 2.50 per share.

1987: During the year installation of a new factory at Nanjangud (Karnataka), for the manufacture of

instant coffee was in progress.

1989: The name of the company was changed from `Food Specialties Ltd.' to `Nestle India Ltd.'

on 24th March.

1990: During the year company entered into chocolate business by introducing Nestle premium

chocolates.

1993: Samalkha factory was commissioned during the year and underwent expansion for cereal based

products.

1994: During the year company launched a number of new products viz., Cerelac Soya, Milk maid,

Dessert Mixes, Maggo Tonit's Special Cooking Bases, Maggi 1-2-3 noodles, Contadina snack dressing

and the chocolate items, milky base marbles and bar one peanut. And also launched Bonus and Polo.

1995: During the year company commenced construction of a new factory at Bicholim, Goa. At the

same year, instant noodles factory was installed and commissioned at

Samalkha factory. - During the year company launched Kit Kat manufactures at the new factory at

Ponda, Goa.

13

Page 14

- During the same year the Nanjangud factory was commissioned and the unit was to manufacture

MILO - the World's Largest Selling Chocolate energy food drink.

- The Chennai-based Indian Food Fermentations tied up with Nestle India Ltd., to market its Dosa and

vada batter in consumer pack, in the country. The company has signed an agreement to this effect

recently. Nestle would sell the ready-to-use dosa, vada, sambhar and unique masala dosa batter in

consumer packs, under its own brand name in the country.

1996: During the year company launched MILO-Chocolate energy food drink in South India and a

range of culinary products like, Dosa and Sambhar mixes, pickles and new varieties of soups under the

brand "Maggi".

1997: NIL is one of the top players in the processed food & beverages industry and the largest

producer of instant coffee with a 49 per cent market share.

- After the success of Kit Kat and Polo, Nestle India had launched its first product in the hard boiled

sugar confectionery market, Allen's Splash.

- Nestlé’s wafer chocolate brand, Kit Kat, which created a major dent in the market with its launch, its

international milk drink brand Milo had garnered a mere three per cent share (value terms) in the Rs

500 crore market, a year after its launch in India.

- Nestle India Ltd. (NIL) leads the list of the country's top 15 coffee exporters for the ongoing calendar

year in terms of both quantum and value for the period January 1 - October 23.

1998: Nestle SA and the BM Khaitan group set up a joint venture, Nutritional Food Products India

Ltd, in 1990, which was amalgamated with NIL in 1993.

- Nestle had set up a parallel distribution network across the country.

1999: The Company has also set up a special cold chain for product distribution in select retail outlets.

- Nestle India entered into a 10-year agreement with Campco in February, 1990 for manufacture and

supply of bulk quantity of chocolates and cocoa products.

2000: Nestle entered the domestic bottled water business and launched the product under the brand

name `Pure Life'.

14

Page 15

- The Company launched its ultra heat treated liquid milk, `Nestle Pure Milk', in Bangalore, Chennai,

Hyderabad and Kochi.

- The Company launched Perrier and celebrated "Perrier Invitation Golf-2000".

- Nestle India Ltd. launched Nescafe Gold and Nescafe Gold Decaffeinated.

- Nestle India launched a range of gift packs under the Fox confectionery brand name for the festival

seasons.

The Company launched its second premium mineral water brand ‘San Pellegrino’ in India.

2001: Nestle India Ltd. launched `Pure Life', its mass-market bottled water, adding one more premium

brand to the already saturated Rs 600-crore bottled water segment.

- Nestle Bar-One was relaunched after renovating it to make it smoother, creamier and better meets

consumer needs.

2002: Nestle Group increased its holding in Nestle India to 53.27%

-Tied up with Nilgiris to co-brand various dairy products like dahi, paneer, ghee and possibly milk

-Launched a throat lozenge branded Acti-V to compete against Procter & Gamble's Vicks cough

drops.

-Regained top coffee exporter position in India.

2003: Rolled out Nestle Development Nutrition Plan for infant weaning and launched its infant food

CERELAC 123 as a range of products graded to the needs of infants in each stage of the plan

-Nestle SA, Switzerland, buys 1.01 million shares in its Indian arm 'Nestle India'. With this purchase,

the parent holding in its Indian arm goes up to 59.8 per cent from 58.7 per cent

-Signed a 100 per cent buyback pact with Bengal Nestor's India Ltd (BNIL) for its ultra heat treated

milk and other dairy products.

2004: Nestle India bags Tetra Pak's annual dairy and beverage industry award.

15

Page 16

Products/Projects/Important Brands:

Soluble coffee: Nescafe, Taster's Choice, Ricoré, Ricoffy

Roast & ground coffee: Nespresso, Bonka, Zoë gas, and Loumidis

Water: Nestlé Pure Life, Nestlé Aquarel, Perrier, Vittel, Contrex, S. Pellegrino, Valvert, Panna,

Levissima, Vera, First Bismarck, Viladrau, Arrowhead, Poland Spring, Zephyrhills, Santa Maria, La

Vie

Other beverages: Nestea, Nesquik, Nescau, Milo, Carnation, Libby's, Caro

Dairy products (shelf stable): Nestlé, Nido, Nespray, Ninho, Carnation, Milkmaid, La Lechera,

Moça, Klim, Gloria, Svelty, Molico, Nestlé Omega Plus, Bear Band, Coffee-mate / (chilled): Nestlé,

LC1, Chamyto, La Laitière, Sveltesse, Yoco, Svelty, Molico

Breakfast cereals: Nestlé

Infant foods: Nestlé, Nan, Lactogen, Beba, Nestogen, Cérélac, Neslac, Nestum, Guigoz

Performance nutrition: Power Bar

Clinical nutrition: Nutren, Peptamen, Modulen, Build-up, Nesvita

Culinary products (bouillons, soups, seasonings, prepared dishes, canned food, pasta, sauces):

Maggi, Buitoni, Crosse & Blackwell, Libby's, Thomy, Winiary

Frozen foods: Magi, Buitoni, Stouffer's

Ice cream: Nestlé, Frisco, Motta, Camy, Savory, Peters

Refrigerated products (yogurts, desserts, pasta, sauces): Nestlé, Buitoni, Herta

16

Page 17

Chocolate and confectionery: Nestlé, Crunch, Cailler, Galak/Milkybar, Kit Kat, Quality Street,

Smarties, Baci, After Eight, Baby Ruth, Butterfinger, Lion, Aero, Polo, Fruitips, etc.

Food Services and professional products: Chef, Davigel, Minor's, Santa Rica

Pet care: Friskies, Fancy Feast, Alpo, Mighty Dog, Gourmet, Mon Petit, Felix

Flavours for the food industry: Food Ingredients Specialties’ (FIS)

Pharmaceutical products: Alcon, Galderma

Cosmetics: L’Oreal (Nestle owns 49% of Gesparal, an investment vehicle 51% owned by the French

Bettencourt family, headed by Liliane Bettencourt. Gesparal in turn owns 53.7% of L'Oreal, with the

rest quoted on the Paris Bourse.)

17

Page 18

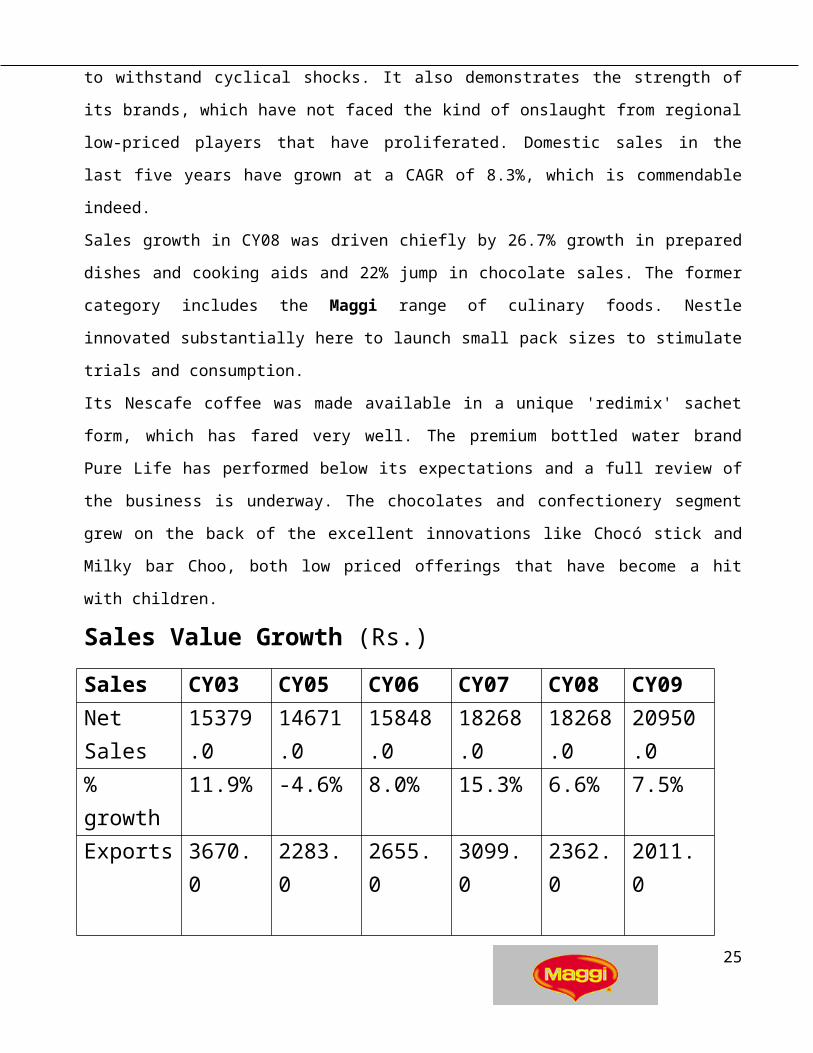

Financial Results and Operations

Nestle India Limited June 06, 2009

Domestic sales growth sustained

Nestle India's domestic sales have grown at a steady pace right through 2008 in the face of difficult

trading conditions. This proves yet again Nestlé’s portfolio's diversity and its resilience to withstand

cyclical shocks. It also demonstrates the strength of its brands, which have not faced the kind of

onslaught from regional low-priced players that have proliferated. Domestic sales in the last five years

have grown at a CAGR of 8.3%, which is commendable indeed.

Sales growth in CY08 was driven chiefly by 26.7% growth in prepared dishes and cooking aids and

22% jump in chocolate sales. The former category includes the Maggi range of culinary foods. Nestle

innovated substantially here to launch small pack sizes to stimulate trials and consumption.

Its Nescafe coffee was made available in a unique 'redimix' sachet form, which has fared very well.

The premium bottled water brand Pure Life has performed below its expectations and a full review of

the business is underway. The chocolates and confectionery segment grew on the back of the excellent

innovations like Chocó stick and Milky bar Choo, both low priced offerings that have become a hit

with children.

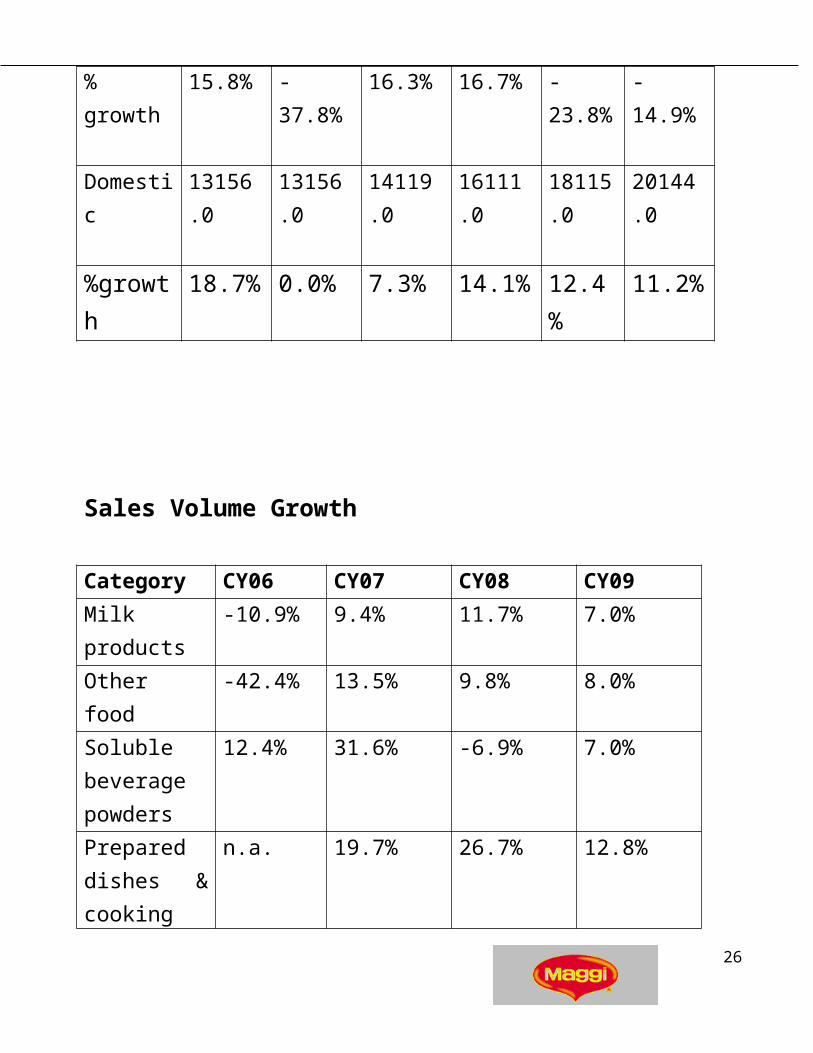

Sales Value Growth (Rs.)

Sales CY03 CY05 CY06 CY07 CY08 CY09Net Sales 15379.0 14671.0

15848.0 18268.0 18268.0 20950.0

% growth 11.9% -4.6% 8.0% 15.3% 6.6% 7.5%Exports 3670.0 2283.0 2655.0 3099.0 2362.0 2011.0

% growth 15.8% -37.8% 16.3% 16.7% -23.8% -14.9%

Domestic 13156.0 13156.0 14119.0 16111.0 18115.0 20144.0

%growth 18.7% 0.0% 7.3% 14.1% 12.4% 11.2%

18

Page 19

Sales Volume Growth

Category CY06 CY07 CY08 CY09Milk products

-10.9% 9.4% 11.7% 7.0%

Other food

-42.4% 13.5% 9.8% 8.0%

Soluble beverage powders

12.4% 31.6% -6.9% 7.0%

Prepared dishes & cooking aids

n.a. 19.7% 26.7% 12.8%

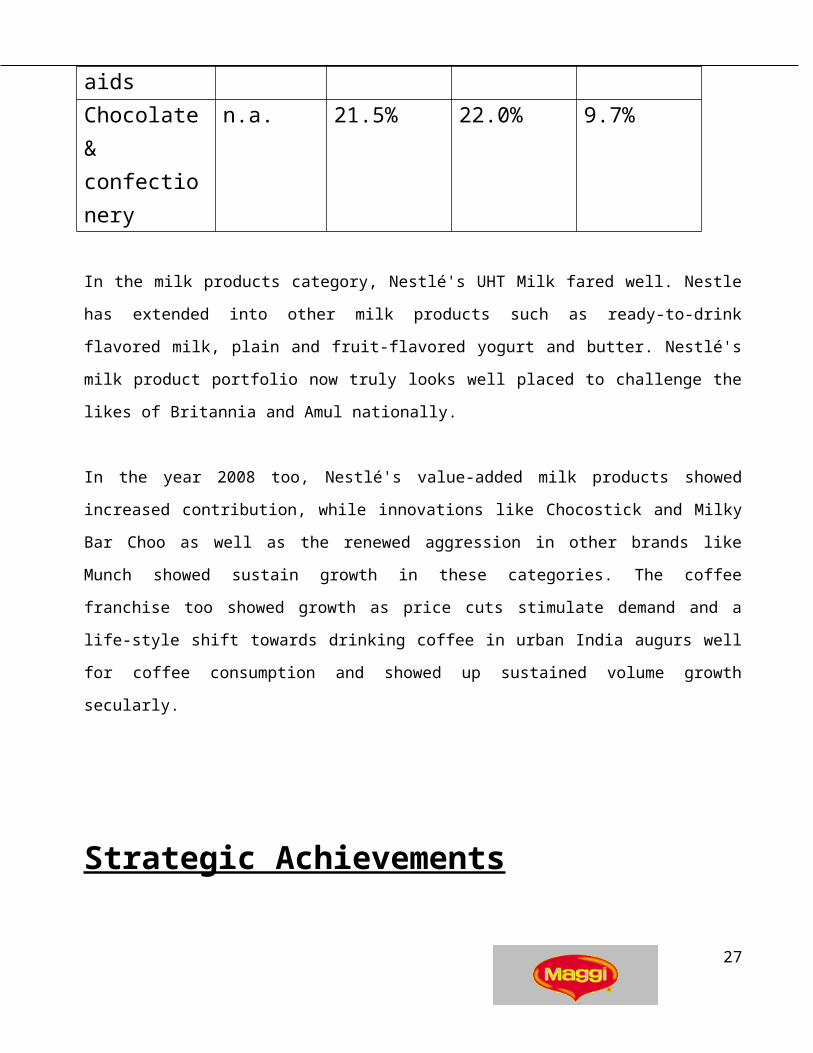

Chocolate & confectionery

n.a. 21.5% 22.0% 9.7%

In the milk products category, Nestlé's UHT Milk fared well. Nestle has extended into other milk

products such as ready-to-drink flavored milk, plain and fruit-flavored yogurt and butter. Nestlé's milk

product portfolio now truly looks well placed to challenge the likes of Britannia and Amul nationally.

In the year 2008 too, Nestlé's value-added milk products showed increased contribution, while

innovations like Chocostick and Milky Bar Choo as well as the renewed aggression in other brands

like Munch showed sustain growth in these categories. The coffee franchise too showed growth as

price cuts stimulate demand and a life-style shift towards drinking coffee in urban India augurs well

for coffee consumption and showed up sustained volume growth secularly.

19

Page 20

Strategic Achievements

Nestle has succeeded in emulating the success of other FMCG products into its portfolio, of offering

small pack-sizes and convenience of use as a USP at very affordable prices. This strategy has been

cast across product categories such as soups, coffee, flavored milk and chocolates.

To improve penetration and availability, it pushed the 'out-of-home' channel of sales of products like

Nestea, Nescafe Frappe, Italian Tomato Sauce mix, Maggi Hot Cup soups, and Nescafe vending

machines were the chief products driven through this channel. Much of the strong volume growth seen

in these categories is attributable to this change

in tack. According to company sources, Nestlé's early successes with its brand extensions and new

delivery channels will lead to sustained growth in the years to come.

Exports

Exports have tended to sputter last year and the performance in Q1CY09 is also not encouraging

enough to believe that Nestle wishes to turn things around. One of the chief causes for the decline in

exports is the 7.4% drop in sales volume. This was on account of

Discontinuation of tea exports and a higher base in CY08. Lower realization in instant coffee exports

to Russia (roughly three-fourth of its exports) on account of lower coffee prices also impacted sales

negatively.

20

Page 21

Benign raw material prices help, but for how long?

Nestle has benefited from benign raw material prices for the last few years. Observe that milk, (42% of

commodity material costs for Nestle) has seen prices decline by close to 10% in the last four years.

Green coffee, which is 12% of such costs, is down 60% in the same period, while other important

products like sugar and wheat flour are also down between 1% to 7%.Milk prices are apparently

already up this year and we suspect that commodities like coffee and cocoa may have seen their lows

in 2008.

The first quarter results reflect inflationary pressures straight away on the raw material front.

Marketing and distribution costs under check

Nestlé's advertising costs have moved down by 100 basis points in the last two years as a percentage

of sales while freight & distribution costs are down 70 basis points. S & D costs account for 13-14%

of net sales in the same period. Since these have remained flat in absolute terms in the last three years,

even as sales have grown by 23%, the accretion to the bottomline is about Rs.160mn in two years just

on this count. Continuous investment in IT infrastructure, supply chain efficiencies and optimum

logistics management has aided the company.

21

Page 22

Selling & Distribution costs

Particulars CY06 CY07 CY08 CY09A & P costs

8.3% 8.7% 7.9% 7.7%

Freight & Distr. Costs

5.5% 5.7% 5.1% 5.0%

Total S & D costs

13.8% 14.5% 13.0% 12.7%

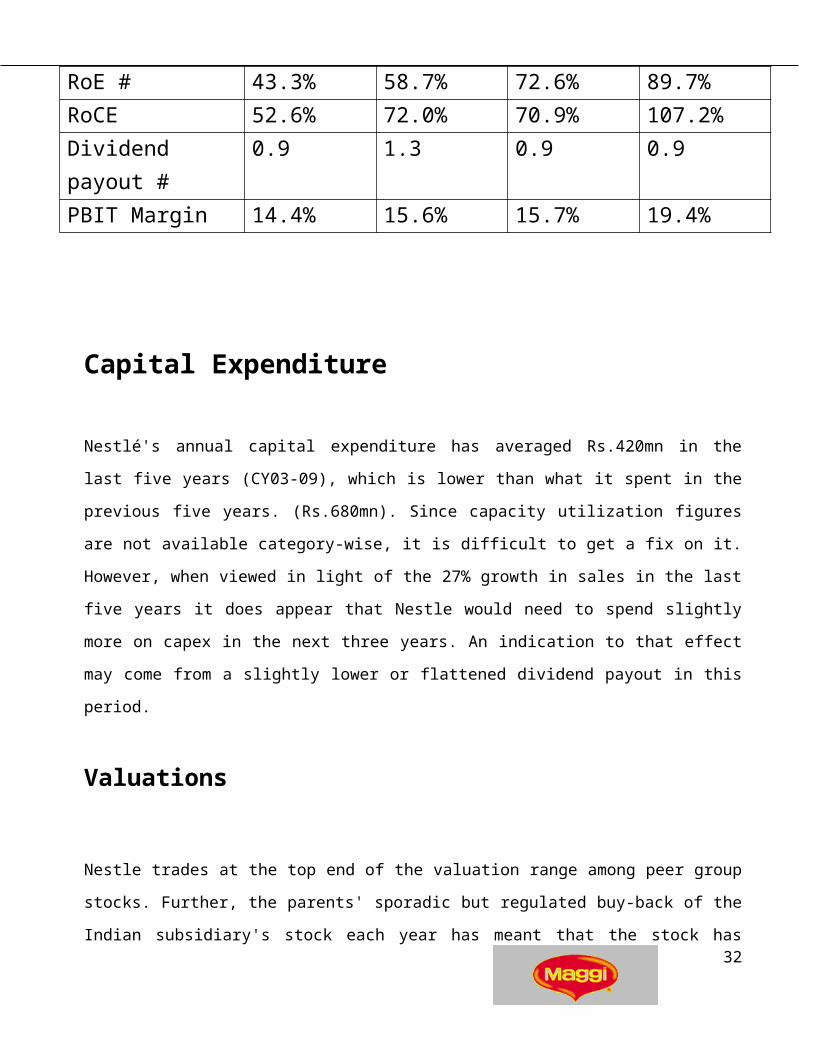

Capital efficiency remains exemplary

Nestlé's return ratios speak for themselves. The company has been able to grow the RoCE and RoEs

even from present high levels owing to continuing contraction of its balance sheet size. Sharp

reduction in working capital, low capital expenditures in relation to the growth in sales in the last three

years, has seen Nestlé's ROE almost double to 90% from an already healthy 43% in CY03. Since

Nestle provides perhaps excessively and aggressively for contingencies and write-offs, we believe the

net profit and PBIT before exceptional would offer true representation.

Ratios CY06 CY07 CY08 CY09RoE # 43.3% 58.7% 72.6% 89.7%RoCE 52.6% 72.0% 70.9% 107.2%Dividend payout # 0.9 1.3 0.9 0.9PBIT Margin 14.4% 15.6% 15.7% 19.4%

Capital Expenditure22

Page 23

Nestlé's annual capital expenditure has averaged Rs.420mn in the last five years (CY03-09), which is

lower than what it spent in the previous five years. (Rs.680mn). Since capacity utilization figures are

not available category-wise, it is difficult to get a fix on it. However, when viewed in light of the 27%

growth in sales in the last five years it does appear that Nestle would need to spend slightly more on

capex in the next three years. An indication to that effect may come from a slightly lower or flattened

dividend payout in this period.

Valuations

Nestle trades at the top end of the valuation range among peer group stocks. Further, the parents'

sporadic but regulated buy-back of the Indian subsidiary's stock each year has meant that the stock has

been well-supported by fundamental and technical factors. Given the obvious merits of its business,

the exemplary performance ratios and its resilience to the slow-down in the FMCG sector, impart high

durability, greater visibility and less volatility to its earnings and it is indeed worthy of its premium

valuations. Nestlé’s sales are targeted to grow by 7.5% in CY08 (taking into consideration some

inflationary pressures on raw materials and hence allowed margin expansion of just 60 basis points).

However this should be enough for the gross profit to grow by 23% and net profits before exceptionals

to rise by 27%. Nestlé’s EPS would rise to Rs.30.10.

23

Page 24

ABOUT THE BRAND

What exactly a brand is?

The brand is defined as a ‘name, term, sign, symbol, or design, or a combination of them, intended to

identify the goods or services of one seller or group of sellers and to differentiate them from those of

the competitors’.

In essence, a brand identifies the seller or maker. It can be a name, trademark, logo, or other symbol. It

is essentially a seller’s promise to deliver a specific set of features, benefits, and services consistently

to the buyers.

A Brand conveys upto six levels of meaning:-

Attributes

Benefits(functional and emotional benefits)

Values

Culture

Personality

User

Brand is basically a market term, a major selling tool & is one of the essential and most important

components of the total product personality. A brand name not only facilitates advertising and

promotion but also functions as demand stimulant.

Nowadays consumers have become extremely brand conscious and this may be attributed to the

intensive brand promotion undertaken by the marketers.

Nowadays when one goes in the market to buy Tomato Sauces, he/she would not ask for just one

tomato sauce but over the years due to the impact of the image created about the particular brand in the

mind of the consumers, they insist for the particular brand say Maggi, Kissan

Heinz, etc.

24

Page 25

Thus it is the image associated with the particular brand, in a way decides the success of the whole

gamut of the marketing and promotional efforts done by the company, as it helps in creating brand

loyality towards a brand.

So, a good brand name should be distinctive, easy to pronounce, recognize and remember. Above all it

should be appealing.

MAGGI – A BRAND DESCRIPTION

HISTORY OF MAGGI

ACHIEVEMENTS

MAGGI has become a household name in Singapore, synonymous with quality food as well as being a

leading culinary expert, boasting cooking aids that provide invaluable help to housewives in whipping

up tasty and convenient meal solutions for their families. Most have grown up with fond memories of

MAGGI 2-Minute Noodles. In fact, many can still recall the MAGGI 2-Minute Noodles commercial

on television years ago that depicted two school children running home to enjoy a bowl of scrumptious

MAGGI noodles. The jingle is still embedded deep in the minds of consumers -”Fast to cook, good to

eat” and has made MAGGI noodles a must for every home.

With the regional R&D Centre in Singapore focusing on development of Asian cuisine, MAGGI’s

portfolio of products can be developed at a faster pace to suit the needs of consumers. The MAGGI

range of products has evolved from noodles and sauces to include cooking aids and recipe mixes to

cater to the changing lifestyles of Singaporeans. These include products which are nutritious for health

conscious Singaporeans.

25

Page 26

HISTORY

Over a century ago, back in 1884, a genius called Julius Maggi invented a powdered pea and bean

soup, to provide nutritious, easy to prepare food for busy women who worked in factories and didn’t

have time to prepare healthy meals. This product was able to provide much needed nutrition for the

people. Julius Maggi followed this first MAGGI product two years later with the invention of ready-

to-use soups and liquid seasoning. Then Julius Maggi perfected bouillon concentrates, first in

capsules, followed by cubes.

Since then, the MAGGI range has extended substantially. In Singapore, the first products produced

were MAGGI Tomato Ketchup and Chilli Sauce, launched in 1969. This was followed two years

later with the popular MAGGI 2-Minute Noodles. Today, these three products are the market leaders

in their respective categories.

26

Page 27

THE PRODUCT

MAGGI offers a total experience in culinary delights to consumers - with authentic tasting products,

which are of the highest quality. The extensive MAGGI range includes MAGGI Noodles,

Bouillon/Chicken Stock in powder and liquid, Dipping and Cooking Sauces, Cooking Aids and Recipe

Mixes.

In the bag noodles segment, MAGGI dominates, enjoying a high penetration rate of 77 percent

in homes of Singaporeans while in the sauces category, MAGGI has almost 50 percent market

share.

The MAGGI Recipe Mixes include the MAGGI “Hari Hari Favorites” range which enables busy

adults and working mothers of today to cook up a mouth-watering feast of timeless culinary classics.

The variety of recipe mixes offered within the range is the ideal solution to creating authentic Malay

and Chinese favourites with ease and convenience.

In this way, MAGGI has also helped preserve the culinary heritage of traditional cuisine for people

to cook these dishes in their own homes any day of the week.

27

Page 28

RECENT DEVELOPMENTSIn 2002, MAGGI’s presence in the noodles category was strengthened by the launch of MAGGI Hot

Bowl Noodles and MAGGI Famous Cup Noodles to meet the increased demand for convenience.

MAGGI also caters to new trends with its range of vegetarian products - MAGGI 2-Minutes Noodles

in Vegetarian flavor and MAGGI Shiitake Mushroom Oyster Flavored Sauce. In the premium sauces

category, MAGGI launched the delicious MAGGI Thai Chilli Sauce and MAGGI Paste Mixes.

Another area of product portfolio expansion is the cooking aids segment, a growing segment relevant

to needs of today’s busy Singaporeans.

MAGGI is the first in the recipe mixes category in Singapore to obtain the Healthier Choice Symbol,

awarded by the Singapore Health Promotion Board. It boasts four tasty flavours; Sweet & Sour Fish,

Chilli Prawn, Braised Chicken Mushroom and Black Pepper Beef.

28

Page 29

PROMOTION

In 2002, MAGGI was an exhibitor at Food Expo, a major consumer of products from local food

companies or companies with local/Asian food offerings.

This event also served as a launch pad for MAGGI Hot Bowl Noodles, generating high trial and

awareness. MAGGI does both wet and dry sampling at high traffic outlets and locations using affinity

group targeting, especially for new products to drive awareness and trial e.g. sampling of MAGGI Hot

Bowl Noodles to tertiary students in hostels. Secondary schools are not left out – MAGGI sponsors

home economics classes and cooking competitions.

The objective is to teach students to prepare simple, yet tasty and nutritious meals at home. The

themes and recipes are carefully selected to ensure relevance to the needs of the various participants.

Recipe cards are produced and distributed during these sessions for easy reference, while MAGGI

sampling packs are given away after the sessions for participants to whip up some MAGGI magic at

home.

BRAND VALUES

MAGGI offers consumers simple solutions for today’s consumers who are under various pressures

such as time, budget, declining traditional cooking skills and the constant search for variety. The

MAGGI range has established a reliable bond with consumers by giving ideas and advice that makes it

easier to provide interesting meals. MAGGI products make providing tasty and interesting meals

simple and easy. They make food more of an enjoyable sensory experience.

29

Page 30

THINGS YOU DIDN’T KNOW ABOUT MAGGI

• The MAGGI brand is over 100 years old and is recognized worldwide for its culinary range of

products.

• The MAGGI brand traces its roots all the way back to Switzerland in 1836. In 1947, the MAGGI

Company merged with Nestlé. Nestlé strengthened the distribution and financial base of MAGGI

and enabled it to become a leading world food brand.

• The first product that Julius Maggi launched was MAGGI’S Leguminous Flour and then MAGGI

Seasoning, which is still available today.

• MAGGI’s presence in the noodles category was strengthened by the 2002 launch of MAGGI Hot

Bowl Noodles and MAGGI Famous Cup Noodles. MAGGI revitalized this segment with the

introduction of exciting, authentic local flavours adding a clean, springy bite to the product.

30

Page 31

MAGGI SAUCE– A BRIEF BRAND PROFILE

Maggi sauces manufactured by NESTLE INDIA LTD were launched in October 1985 and created

consumer history. For the first time, a food product was launched nationally across 300 countries.

Maggi sauces are available in 4 flavours:-

Maggi Tomato ketchup launched in 1985.

Maggi Hot n Sweet launched in 1985.

Maggi Chilli Garlic launched in 1986.

Maggi Masala Chilli launched in 1987.

Maggi Sauces are available in the following packings and with the following Price points:-

200g --25/- for penetration

600g -- 57/- is the core grammage a house wife ends us buying

1.2 kg --89/- for consumers to upgrade from 600g to 1.2kg at less than double the price

10g-- 2/- for penetration (Economy pack and the sachet)

31

Page 32

MARKET CHARACTERISITCS

MAJOR PLAYERS & PERFORMANCE TRENDS

RED HOT! THE KETCHUP WAR GETS SAUCIER

“India is primarily a dip-consuming nation, be it curd with parathas or chutney with dosas’.” The shift

from home-made dips to tomato ketchup in urban households appears to be a natural process. Urban

and semi-urban households are also showing a trend towards a breakfast habit of eggs, hence

augmenting the demand for ketchup (to be consumed along with the eggs).

According to research carried out by HLL, there is an increased usage of ketchup by younger adults

and teenagers -- and not just children -- both at home and outside.

The action in the Rs 1 billion tomato ketchup market in India is getting redder, hotter, and sweeter.

The Rs 250-crore category is currently dominated by multinationals like Nestle, HLL and Heinz.

While Nestle, HLL and Heinz are present in the Rs 120-crore ketchup category through their

brands Maggi, Kissan and Heinz respectively, HLL's Kissan is the only dominant branded player in

the Rs 100-crore jams’ category.

The tomato ketchup segment is currently witnessing a robust 20 to 25 per cent growth. Pegged to

see a 40 per cent growth over the next five years, the approximate size of the purees, jams and

sauces market in 2005 is projected at Rs 10 billion.

According to the new relief, all food preparations based on fruits and vegetables are exempt from

excise duty making wide range of products of common use like pickles, sauces, ketchup and juices

cheaper.

Even the rural markets are not left untouched. After years of growth derived primarily from the urban

markets, the FMCG companies have now realized that India lies in its rural villages. So much so that

32

Page 33

rural marketing has become the latest marketing mantra of most FMCG majors. With extensive

competition not only from MNCs but also from the numerous regional players and the lure of an

untapped market has driven the marketers to chalk out bold new strategies for targeting the rural

consumer in a big way.

FACTORS IMPACTING DEMAND

Demand for sauces is affected by a number of different factors. In the mayonnaise and sauce markets,

consumption and pricing of certain meats, chips, and vegetables influence manufacturers’ sales. The

state of the overall economy, which determines how much money consumers have in their wallets,

also has a significant impact on demand for dressings and sauces, in more ways than one. Economic

trends will not only dictate how much consumers can spend when shopping for their weekly groceries,

but also how often consumers will visit fast food and other restaurants.

33

Page 34

MAJOR PLAYERS IN SAUCE INDUSTRY

The companies that will be cooking up new recipes of growth include Hindustan Lever (HLL),

Nestle, Heinz and Nafed among others. Another player that has made a high impact in the sauces

segment is Tops Foods, which sells products such as pickles and sauces under the Tops brand.

Volfarm, a known and established name in this sector has been slowly wiped out after the introduction

of these new entrants in the particular segment.

HLL has increasingly made its Kissan tomato ketchup portfolio ethnic with variants like Kissan

Tomato Pudina, Kissan Tomchi, Kissan Tom-Imli and others, while competitor Nestlé’s Maggi tomato

ketchup has variants in chilli-garlic and hot-n-sweet.

34

Page 35

COMPETITION – PERFORMANCE TRENDS

According to an extensive retail audit conducted by Samsika for the organised ketchup market in July

1997, Maggi ketchups had a 53 per cent market share in Bombay, of which the plain ketchup (200 gm,

600 gm, 1,200 gm pack sizes) accounted for 36.5 per cent, the rest being with Maggi Hot & Sweet

(200 gm and 600 gm). (Nestle, claims a whopping 85 per cent market share in the Maggi Noodles

category).

KISSAN

HLL‘s Kissan, with all its variants, has a 48 per cent market share nationally, both in terms of

volume and value. HLL, however, puts the national volume at 17,000 tonnes

MAGGI

Nestle, for its part, claims a 53 per cent national share in what it says is the 13,000-tonne market.

HEINZ

In the tomato ketchup Foodservice market, Heinz holds a European market share of 30 to 45%. With

38,600 employees, the multinational operates 200 plants globally. The company’s products are

organized into six core businesses and among these ketchup, sauces, and condiments comprise of 27%

of fiscal year 2001 sales.

Ketchup and Condiments: - Ketchup has always been the company’s “flagship” brand. With global

ketchup sales in excess of $1.3 billion, Heinz has over 50% of the

domestic ketchup market and approximately 34% of the global market. However, Heinz ketchup

faces challenges from other brand name ketchups, private label ketchups, and salsa. The increased

35

Page 36

popularity of salsa and other ethnic condiments as well as the lower cost structures for private label

brands will threaten Heinz’s market share.

Tops, the Rs 15-crore company has a wide range of products ranging from 21 varieties of pickles to

jams, Chinese traditional noodles to juices and ketchups. We expect to double our growth figures this

year and aim at targeting about 20 per cent share of the Rs 250-crore jams and ketchup market.” The

company aspires to reach a target of Rs 100 crore by 2006 and is all out to focus entirely on the huge

domestic market.

36

Page 37

BRAND POSITIONING STRATEGY

According To Rosse Reaves

“Positioning is the art of selecting out a number of unique selling propositions, the one which

will get maximum sales.”

According Philips Kotler

“Market Positioning is arranging for a product to occupy a clear, distinctive and desirable place

in the market and in the minds of target customer.”

Thus, basic components of positioning can be referred to as:-

(1) Product class or the structure of the market in which the brand will compete.

(2) Consumer Segmentation

(3) Consumer Perception of Brand in relation to competitors.

37

Page 38

STRATEGY STATEMENT OF MAGGI SAUCES

TARGET MARKET: Upscale household (income 2500+) with particular emphasis on children.

POSITIONING PRODUCT LINE:

KETCHUP - : A Tasty, High Quality ketchup which goes best with all eats.

HOT AND SWEET, CHIILLI GARLIC, MASALA CHILLI: -

Uniquely spiced ketchup to suit the adult palate.

PRICE: At par with competitive brands.

DISTRIBUTION OUTLETS: All towns and all types of outlets both in urban and rural areas.

COMMUNICATION STRATEGY: Chahiye Yahi Chahiye is the last theme commercial run last

year on TV. Strategy is to raise preference for the brand vis a vis competition.

PROMOTION STRATEGY: Target kids via promos like water bottle, Tiffin pack or do value

promos including noodles free, extra grammage or price offs (5 or 10/- off on packs) for the

housewife.

RESEARCH & DEVELOPMENT: Done Internationally.

38

Page 39

OBJECTIVES OF THE STUDY

PROJECT AIM:

To understand the usage patterns and attitudes of the consumers towards the

Tomato based Sauces product category with focus on MAGGI SAUCES.

Objectives of the Study:

The present study was undertaken to describe the following objectives:--

1) To have a better understanding of the consumer attitude and behavior towards Maggi

Sauces.

2) To study the influence of Price, Quality, Availability, Promotional Schemes on the

purchase behavior of the consumers.

3) To study the image perception of the consumer towards Maggi Sauces.

4) To explore the impact of physical attribute of the Maggi Sauces on the

Consumer.

39

Page 40

Scope Of The Study

This study is conducted by the method of field survey of the females in the different zones, in the

Khanna market.

Since this study enables to discover the usage pattern and attitude of the consumers in the Khanna

market towards the Maggi Tomato Sauces, this is basically an exploratory, conclusive kind of a study.

40

Page 41

Limitations Of The Study:

As the questionnaire was quite comprehensive so respondents were often complaining that it

was taking a lot of time.

Time constraint because of which sample size has been restricted to just 200-250.

The study surrounded the Khanna city only.

The respondents were not ready to tell their actual income

The individuals were not ready to fill questionnaire due to lack of time

41

Page 42

Sampling Unit

The universe for this project was Khanna city. The decision to have number of samples/ respondents

had to be decided keeping in mind the following factors:--

The time available.

The objectives which are to be fulfilled through this study.

The type of target customers for research.

The respondents were selected randomly for the study purpose.

Data Collection

In this research, Primary data is collected by administering questionnaire to the respondents. The

consumer survey is conducted by calling upon the respondents door to door in all areas, in which the

survey is to be conducted.

Thus, a thorough field survey is done in this research study.

Sample Size

Keeping in mind the above stated factors; the sample size was kept between 200-230 respondents and

in order to have proper representation of the sample the 14 localities are chosen from khanna city, in

which survey is to be conducted. Out of this, around 200 responses have been used in the final

analysis.

42

Page 43

RESEARCH METHODOLOGY

The research was carried out in two phases:--

DATA COLLECTION: The first phase comprises of designing the instrument, i.e., designing the Questionnaire.

DESIGNING THE QUESTIONNAIRE

The decision about the format of the questionnaire was very important and crucial since it has to fulfill

all the research objectives, so that all the questions and problems are answered and at the same time

tabulation and analysis should be easier and subjective bias should be eliminated.

Following criteria was kept in mind while designing the questionnaire:--

1) The information sought should be clear and precise.

2) Use of multiple choice or five point ranking questions were used in the questionnaire, so that it is

easy to administer and less time consuming.

3) The wording of the questions was kept simple so that both researcher and the respondent can

understand easily.

4) The use of open ended questions along with the close ended questions were also introduced to have

the complete in-depth study of the consumer attitude can be made to the extent possible.

5) Proper scope has been provided in the questionnaire for the quantification of the results.

6) The time factor was also very important since the research has to be done in the stipulated time

along with the tabulation and analysis of the results.

43

Page 44

The questionnaire, which is used to conduct research, is a structured, non-disguised type of

questionnaire.

Advantages of using structured, non-disguised questionnaires are:-

It helps in gathering relevant information.

It can be administered easily.

The precise and specific information is collected.

44

Page 45

DATA - ANALYSIS

Profile of the respondents:-

Females in different age groups

Using Tomato based sauces having individual preferences for:-

Branded Sauces

Unbranded Sauces (brought from the market)

Unbranded Sauces (Home Made)

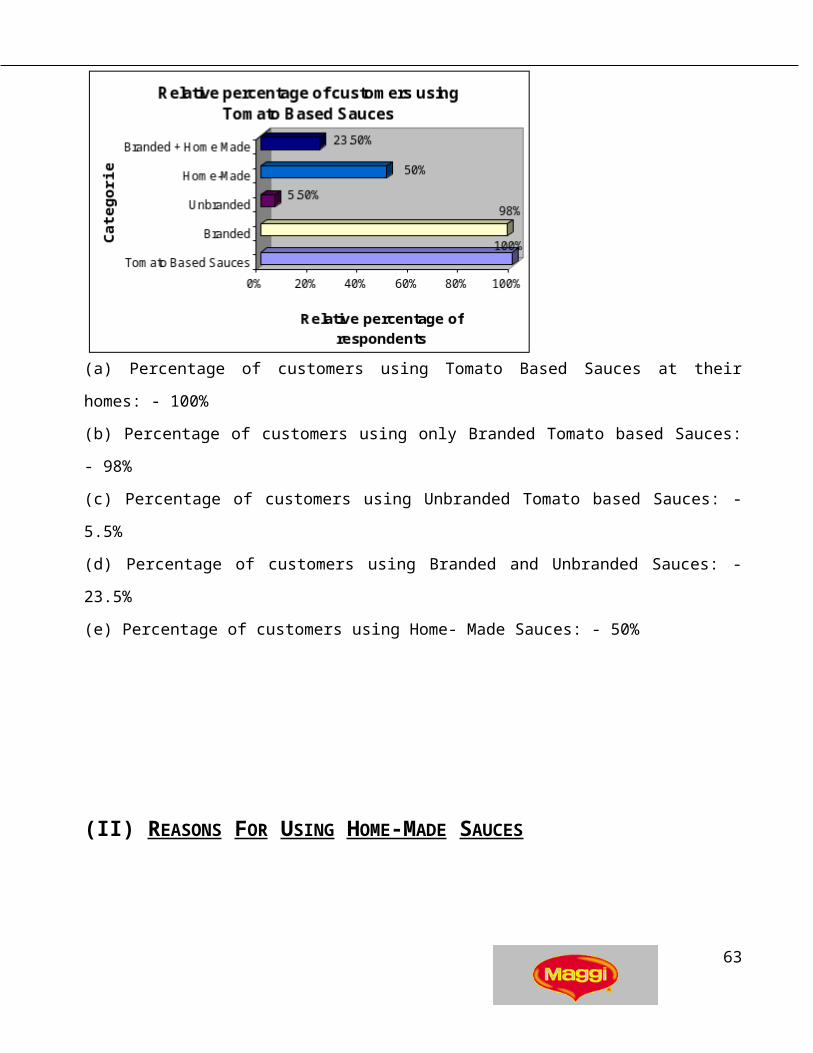

(I) USAGE PATTERN FOR SAUCES :-

1. TOMATO SAUCE USERS:-

Sample Size:-200

(a) Percentage of customers using Tomato Based Sauces at their homes: - 100%

(b) Percentage of customers using only Branded Tomato based Sauces: - 98%

(c) Percentage of customers using Unbranded Tomato based Sauces: - 5.5%

(d) Percentage of customers using Branded and Unbranded Sauces: - 23.5%

(e) Percentage of customers using Home- Made Sauces: - 50%

45

Page 46

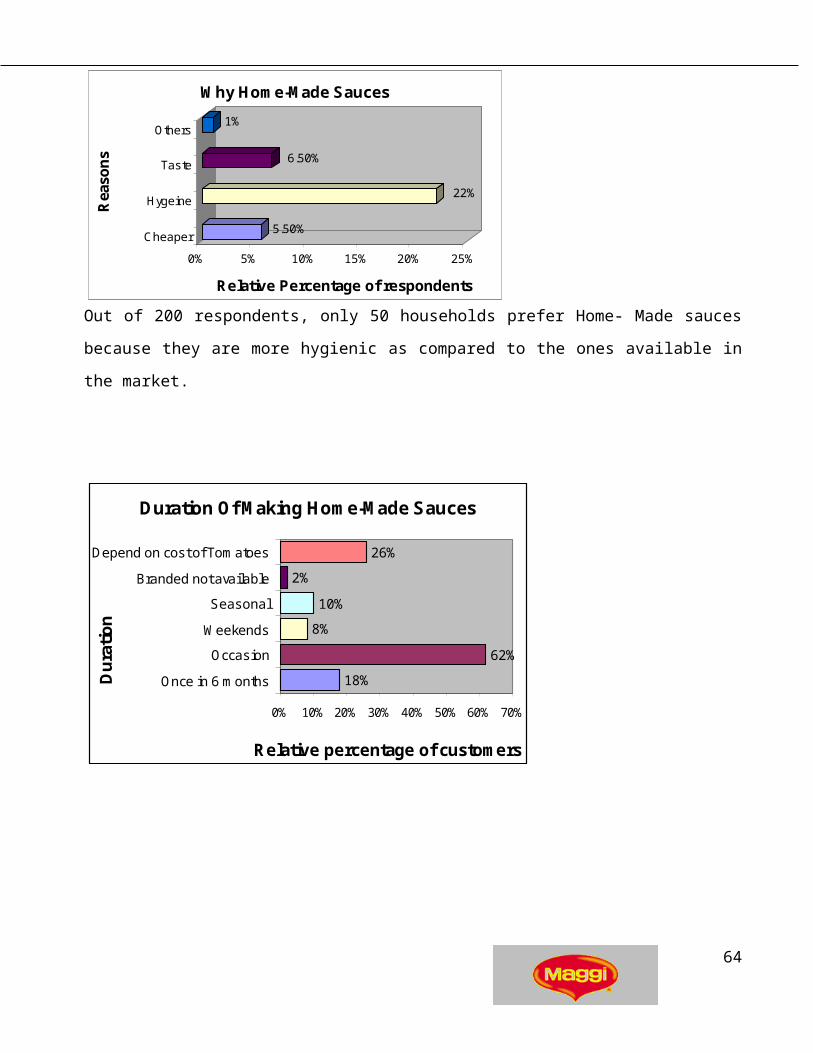

(II) REASONS FOR USING HOME-MADE SAUCES

5.50%

22%

6.50%

1%

0% 5% 10% 15% 20% 25%

Relative Percentage of respondents

Cheaper

Hygeine

Taste

Others

Rea

son

s

Why Home-Made Sauces

Out of 200 respondents, only 50 households prefer Home- Made sauces because they are more

hygienic as compared to the ones available in the market.

Duration Of Making Home-Made Sauces

18%

62%

8%

10%

2%

26%

0% 10% 20% 30% 40% 50% 60% 70%

Once in 6 months

Occasion

Weekends

Seasonal

Branded not available

Depend on cost of Tomatoes

Du

rati

on

Relative percentage of customers

46

Page 47

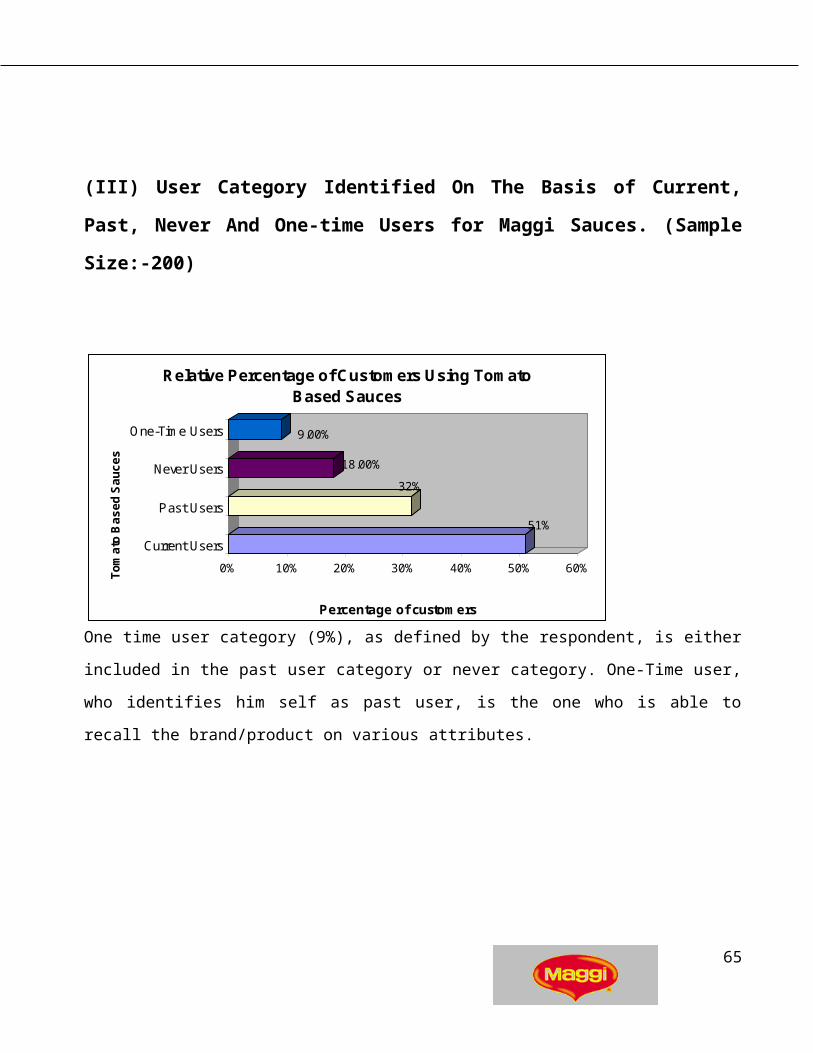

(III) User Category Identified On The Basis of Current, Past, Never And One-time

Users for Maggi Sauces. (Sample Size:-200)

51%

32%

18.00%

9.00%

0% 10% 20% 30% 40% 50% 60%

Percentage of customers

Current Users

Past Users

Never Users

One-Time Users

To

ma

to B

as

ed

Sa

uc

es

Relative Percentage of Customers Using Tomato Based Sauces

One time user category (9%), as defined by the respondent, is either included in the past user category

or never category. One-Time user, who identifies him self as past user, is the one who is able to recall

the brand/product on various attributes.

47

Page 48

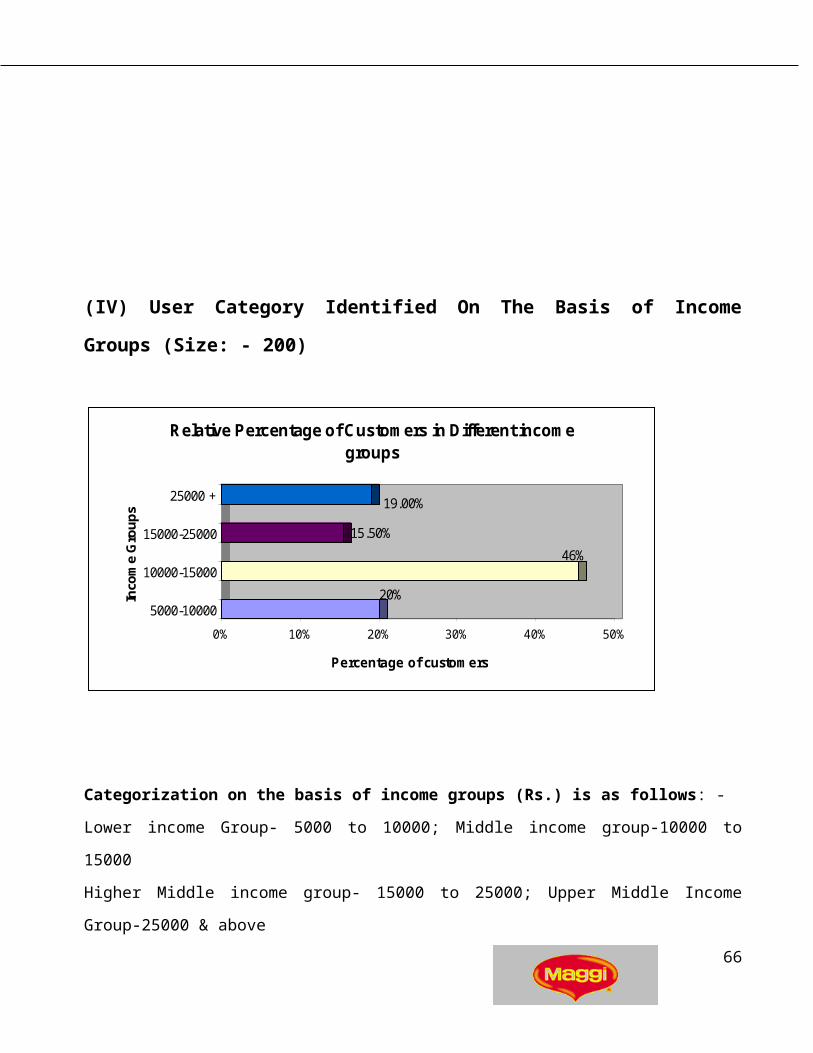

(IV) User Category Identified On The Basis of Income Groups (Size: - 200)

20%

46%

15.50%

19.00%

0% 10% 20% 30% 40% 50%

Percentage of customers

5000-10000

10000-15000

15000-25000

25000 +

Inco

me

Gro

up

s

Relative Percentage of Customers in Different income groups

Categorization on the basis of income groups (Rs.) is as follows: -

Lower income Group- 5000 to 10000; Middle income group-10000 to 15000

Higher Middle income group- 15000 to 25000; Upper Middle Income Group-25000 & above

48

Page 49

(V) RELATIVE AWARENESS OF DIFFERENT BRANDS AMONG THE RESPONDENTS IN

VARIOUS INCOME GROUPS (Sample Size:-200)

97%

97.50%39.50%

39.50%

14%

9%

0% 20% 40% 60% 80% 100%

Relative percentage

MAGGI

KISSAN

HEINZ

NAFED

TOPS

VOLFARM

BR

AN

Ds

AWARENESS LEVELS FOR VARIOUS BRANDS

Highest awareness is for Kissan as well as Maggi Sauces among the respondents.

49

Page 50

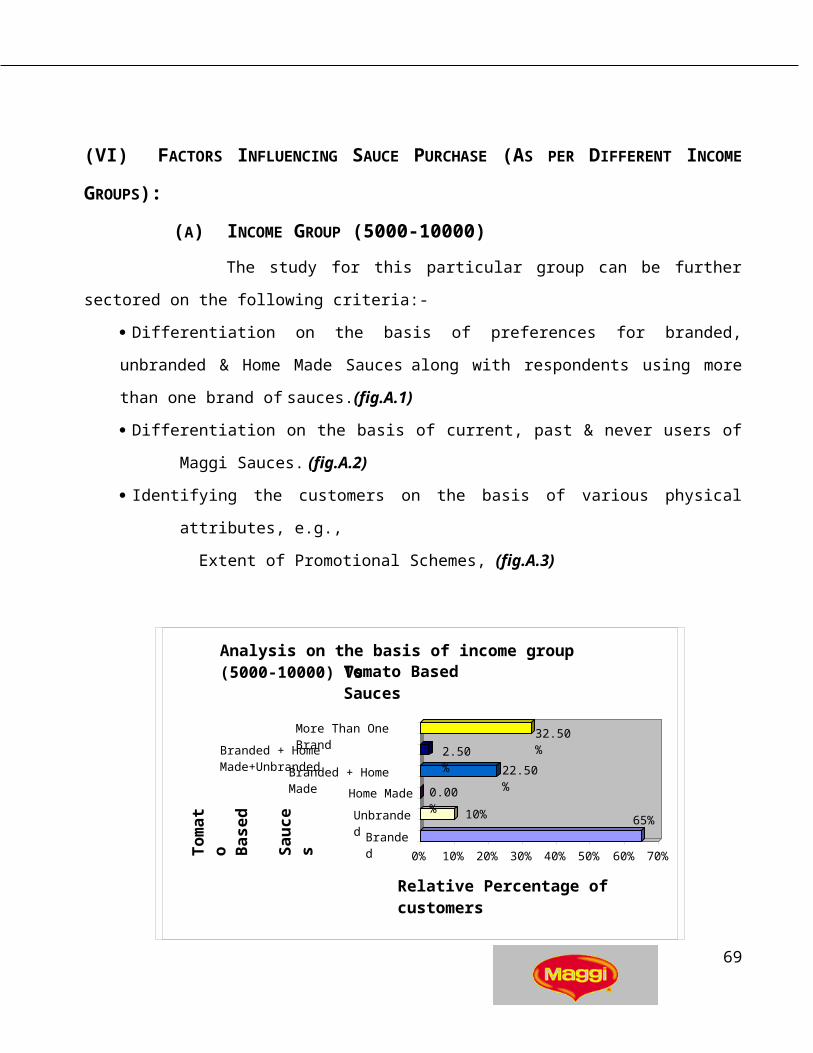

(VI) FACTORS INFLUENCING SAUCE PURCHASE (AS PER DIFFERENT INCOME

GROUPS):

(A) INCOME GROUP (5000-10000)

The study for this particular group can be further sectored on the following criteria:-

Differentiation on the basis of preferences for branded, unbranded & Home Made Sauces along

with respondents using more than one brand of sauces.(fig.A.1)

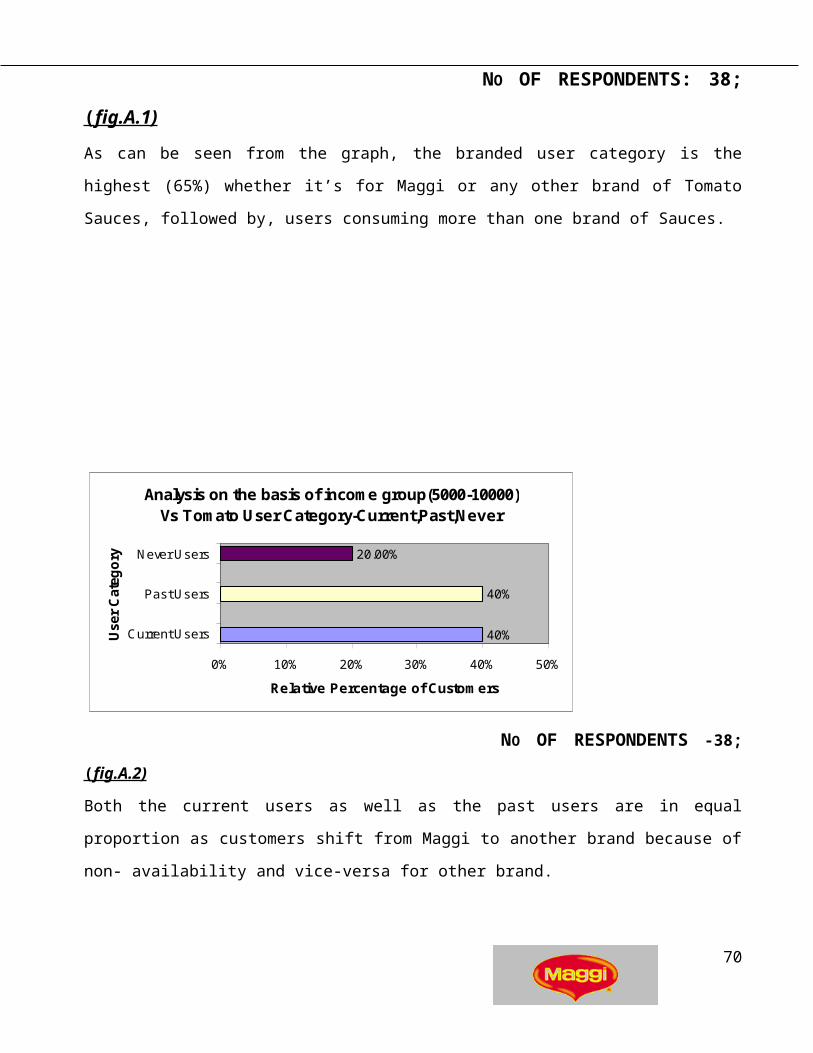

Differentiation on the basis of current, past & never users of Maggi Sauces. (fig.A.2)

Identifying the customers on the basis of various physical attributes, e.g.,

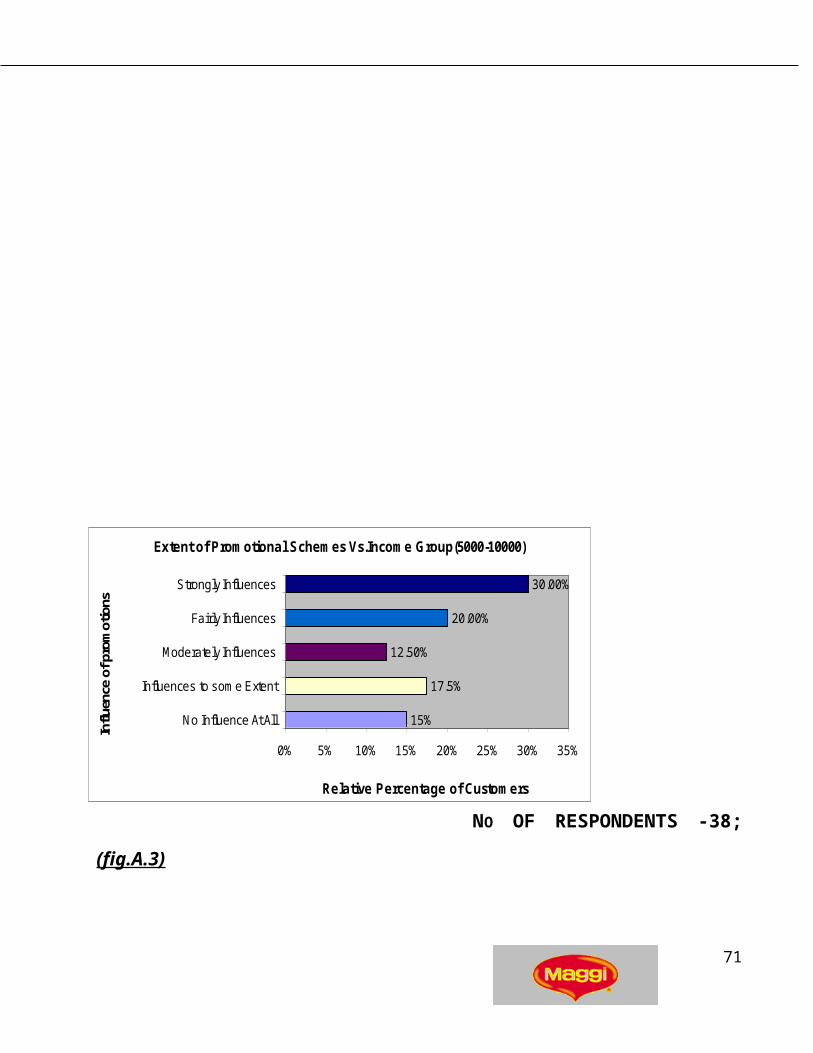

Extent of Promotional Schemes, (fig.A.3)

NO OF RESPONDENTS: 38;

( fig.A.1)

As can be seen from the graph, the branded user category is the highest (65%) whether it’s for Maggi

or any other brand of Tomato Sauces, followed by, users consuming more than one brand of Sauces.

65%10%

0.00%

22.50%

2.50%

32.50%

0% 10% 20% 30% 40% 50% 60% 70%

Relative Percentage of customers

Branded

Unbranded

Home Made

Branded + Home Made

Branded + Home Made+Unbranded

More Than One Brand

Tom

ato B

ased

Sau

ces

Analysis on the basis of income group (5000-10000) Vs Tomato Based Sauces

50

Page 51

Analysis on the basis of income group(5000-10000) Vs Tomato User Category-Current,Past,Never

40%

40%

20.00%

0% 10% 20% 30% 40% 50%

Current Users

Past Users

Never Users

Use

r C

ateg

ory

Relative Percentage of Customers

NO OF RESPONDENTS -38;

( fig.A.2)

Both the current users as well as the past users are in equal proportion as customers shift from Maggi

to another brand because of non- availability and vice-versa for other brand.

51

Page 52

Extent of Promotional Schemes Vs.Income Group(5000-10000)

15%

17.5%

12.50%

20.00%

30.00%

0% 5% 10% 15% 20% 25% 30% 35%

No Influence At All

Influences to some Extent

Moderately Influences

Fairly Influences

Strongly Influences

Influ

ence

of p

rom

otio

ns

Relative Percentage of Customers

NO OF RESPONDENTS -38;

(fig.A.3)

Promotional Schemes have a strong influence on the purchase of Sauces as a product.

52

Page 53

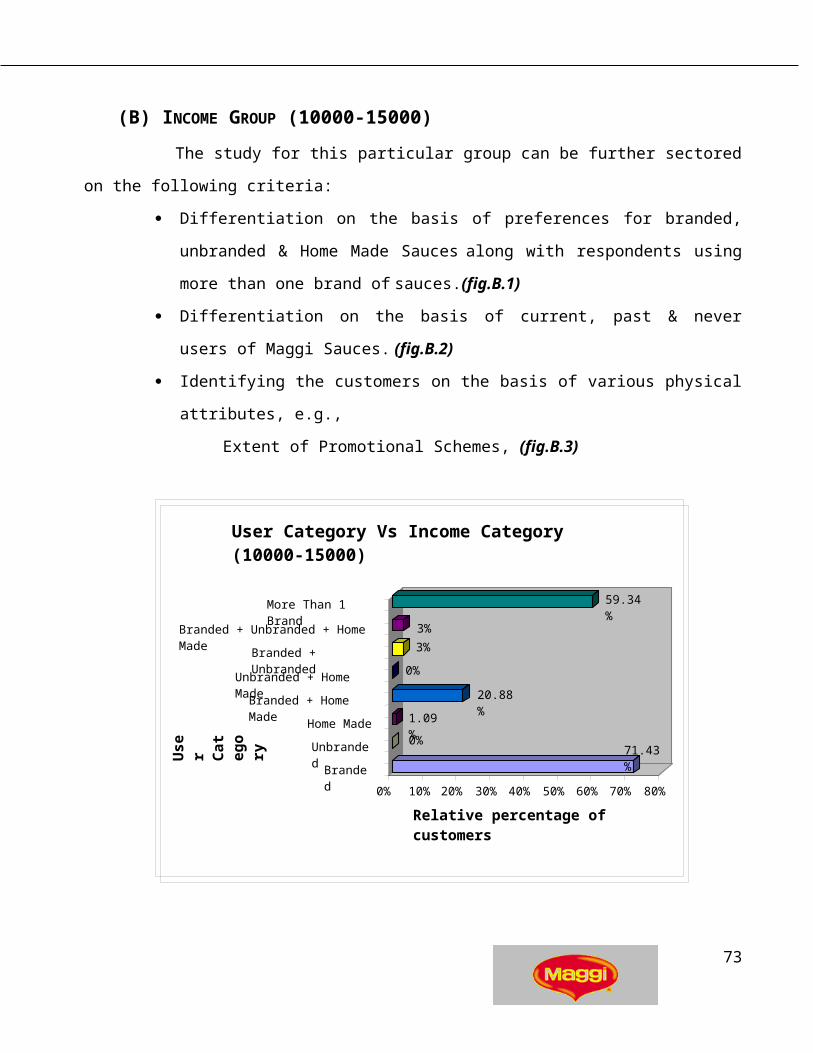

(B) INCOME GROUP (10000-15000)

The study for this particular group can be further sectored on the following criteria:

Differentiation on the basis of preferences for branded, unbranded & Home Made

Sauces along with respondents using more than one brand of sauces.(fig.B.1)

Differentiation on the basis of current, past & never users of Maggi Sauces. (fig.B.2)

Identifying the customers on the basis of various physical attributes, e.g.,

Extent of Promotional Schemes, (fig.B.3)

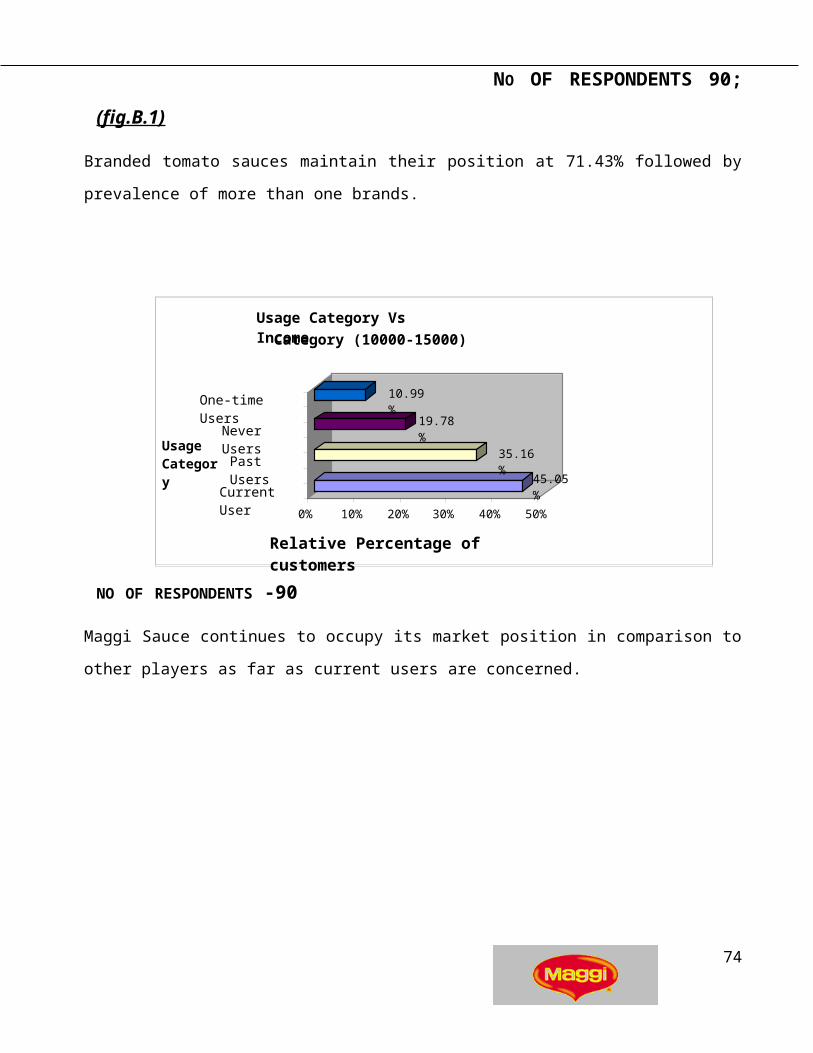

NO OF RESPONDENTS 90;

(fig.B.1)

Branded tomato sauces maintain their position at 71.43% followed by prevalence of more than one

brands.

71.43%0%

1.09%

20.88%

0%

3%

3%

59.34%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Relative percentage of customers

Branded

Unbranded

Home Made

Branded + Home Made

Unbranded + Home Made

Branded + Unbranded

Branded + Unbranded + Home Made

More Than 1 Brand

Use

r C

ate

go

ry

User Category Vs Income Category (10000-15000)

53

Page 54

NO OF RESPONDENTS -90

Maggi Sauce continues to occupy its market position in comparison to other players as far as current

users are concerned.

NO OF RESPONDENTS -90;

(fig.B.3)

The promotional Schemes have a strong influence on this category as well with a relative percent of

24.18%, however, this percentage is less as compared to the one in the income group of 5000-10000.

45.05%

35.16%

19.78%

10.99%

0% 10% 20% 30% 40% 50%

Relative Percentage of customers

Current User

Past Users

Never Users

One-time Users

Usage Category

Usage Category Vs Income

Category (10000-15000)

Extent of Promotional Schemes vs. Income Group (10000-15000)

16.48%

17.58%

15.38%

25.27%

24.18%

0% 5% 10% 15% 20% 25% 30%

No Influence at All

Influences to some Extent

Moderately Influences

Fairly Influences

Strongly Influences

Infl

uen

ce

of

P r o m o ti o n s

Relative Percentage of Customers

54

Page 55

(C) INCOME GROUP (15000-25000)

The study for this particular group can be further sectored on the following criteria:-

Differentiation on the basis of preferences for branded, unbranded & Home Made

Sauces along with respondents using more than one brand of sauces.(fig.C.1)

Differentiation on the basis of current, past & never users of Maggi Sauces. (fig.C.2)

Identifying the customers on the basis of various physical attributes, e.g.,

Extent of Promotional Schemes, (fig.C.3)

70.96%0%

0.00%

22.58%

0%

3.22%

3.22%

48.38%

0%

10 %

20%

30%

40%

50%

60%

70%

80%

Relative percentage of customers

Branded

Unbranded

Home Made

Branded + Home Made

Unbranded + Home Made

Branded + Unbranded

Branded + Unbranded + Home Made

More Than 1 Brand

Us

er

Ca

teg

ory

User Category Vs Income Category(15000-25000)

55

Page 56

NO OF RESPONDENTS: 30;

(fig.C.1)

Branded category of Sauces shows high prevalence followed by the usage of more than one brands.

56

Page 57

Usage Category Vs Income Group(15000-25000)

58.06%

32.26%

9.67%

0% 10% 20% 30% 40% 50% 60% 70%

Current User

Past Users

Never Users

Usa

ge C

ateg

ory

Relative Percentage of customers

NO OF RESPONDENTS: 30;

(fig.C.2)

Current users are higher with relative percentage of 58.06% followed by past users with 32.26%.

Extent of Promotional Schemes Vs.Income Group(15000-25000)

22.58%

12.90%

15.80%

16.12%

19.35%

0.00% 5.00% 10.00% 15.00% 20.00% 25.00%

No Influence At All

Influences to some Extent

Moderately Influences

Fairly Influences

Strongly Influences

Influ

ence

of

prom

otio

ns

Relative Percentage of Customers

NO OF RESPONDENTS 30;

(fig.C.3)

Price, here has no influence at all over this category, i.e. customers look forward to the quality rather

than the cost of the product.

57

Page 58

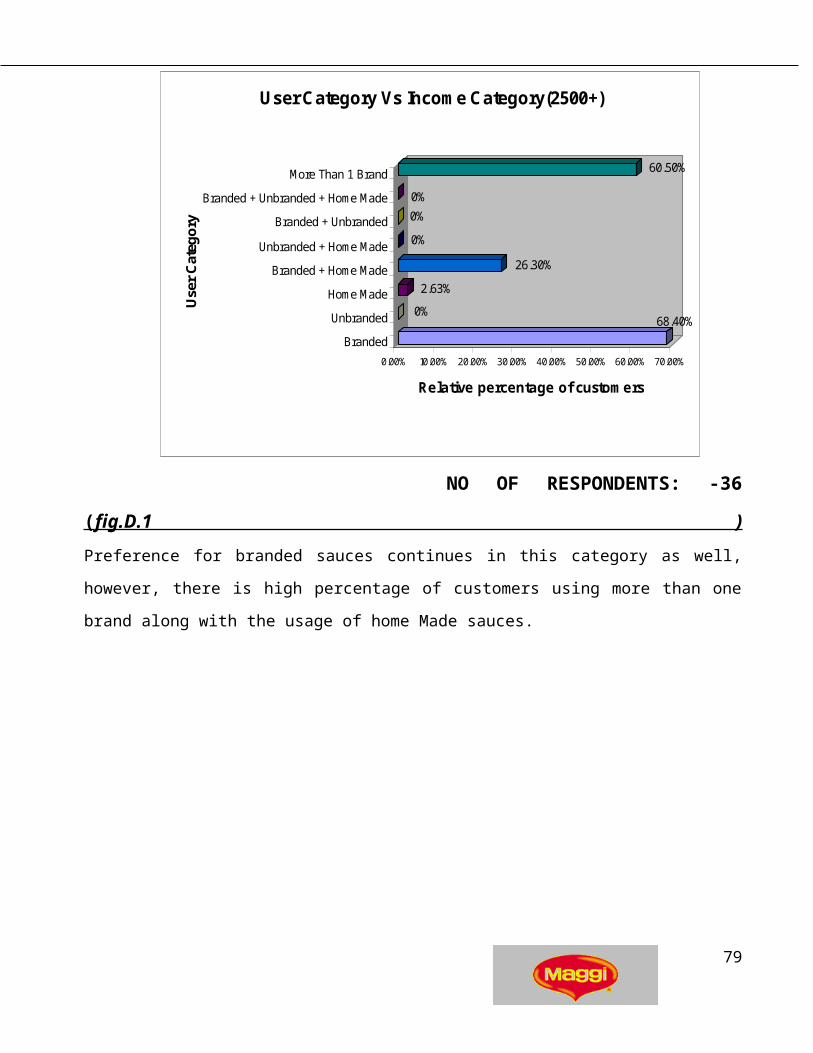

(D) INCOME GROUP (25000+)

The study for this particular group can be further sectored on the following criteria:-

Differentiation on the basis of preferences for branded, unbranded & Home Made

Sauces along with respondents using more than one brand of sauces (fig.D.1)

Differentiation on the basis of current, past & never users of Maggi Sauces. (fig.D.2)

Identifying the customers on the basis of various physical attributes, e.g.,

Extent of Promotional Schemes, (fig.D.3)

68.40%0%

2.63%

26.30%

0%

0%

0%

60.50%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00% 60.00% 70.00%

Relative percentage of customers

Branded

Unbranded

Home Made

Branded + Home Made

Unbranded + Home Made

Branded + Unbranded

Branded + Unbranded + Home Made

More Than 1 Brand

Use

r C

ateg

ory

User Category Vs Income Category(2500+)

NO OF RESPONDENTS: -36

( fig.D.1 ) Preference for branded sauces continues in this

category as well, however, there is high percentage of customers using more than one brand along

with the usage of home Made sauces.

58

Page 59

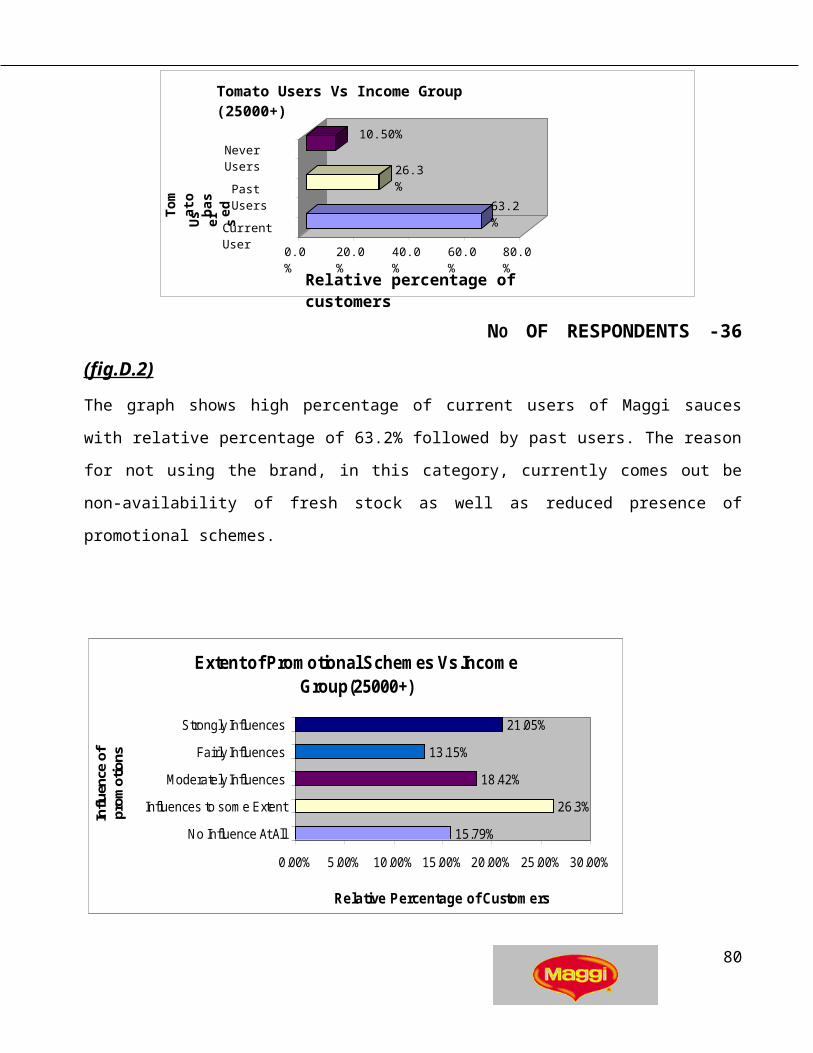

NO OF RESPONDENTS -36 (fig.D.2)

The graph shows high percentage of current users of Maggi sauces with relative percentage of 63.2%

followed by past users. The reason for not using the brand, in this category, currently comes out be

non-availability of fresh stock as well as reduced presence of promotional schemes.

Extent of Promotional Schemes Vs.Income Group(25000+)

15.79%

26.3%

18.42%

13.15%

21.05%

0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 30.00%

No Influence At All

Influences to some Extent

Moderately Influences

Fairly Influences

Strongly Influences

Influ

ence

of

prom

otio

ns

Relative Percentage of Customers

NO OF RESPONDENTS -36

63.2%

26.3%

10.50%

0.0% 20.0% 40.0% 60.0% 80.0%

Relative percentage of customers

Current User

Past Users

Never Users

To mat

o

bas

ed

Us

er sTomato Users Vs Income Group (25000+)

59

Page 60

Since there is reduced visibility of promotional schemes, therefore, these schemes influence to a

certain extent.

(VII) SCENARIO OVERALL KHANNA (in relation to category of Users)

NO. OF RESPONDENTS: 194

As can be seen from the graph, there is a strong favour for the branded category. Also, the

customers have the preference for more than one brand of sauces.

SCENARIO OVERALL KHANNA (in relation to category of Users - Current, Past

& never users)

60

Page 61

NO. OF RESPONDENTS: 194

Maggi Sauces are being used by majority of the households (51.03%).

One-Time users include those categories of sauce users who can now be included in the never user

Category

(VIII) INFLUENCE OF DIFFERENT ATTRIBUTES ON PURCHASE OF SAUCES .

(A)PRICE

51.03%35.05%

17.01%

5.15%

0% 10% 20% 30% 40% 50% 60%

Relative Percentage of Users

Current Users

Past Users

Never users

One-Time Users

Us

er

Ca

teg

or

y

Maggi Sauce Users

61

Page 62

NO. OF RESPONDENTS: 194

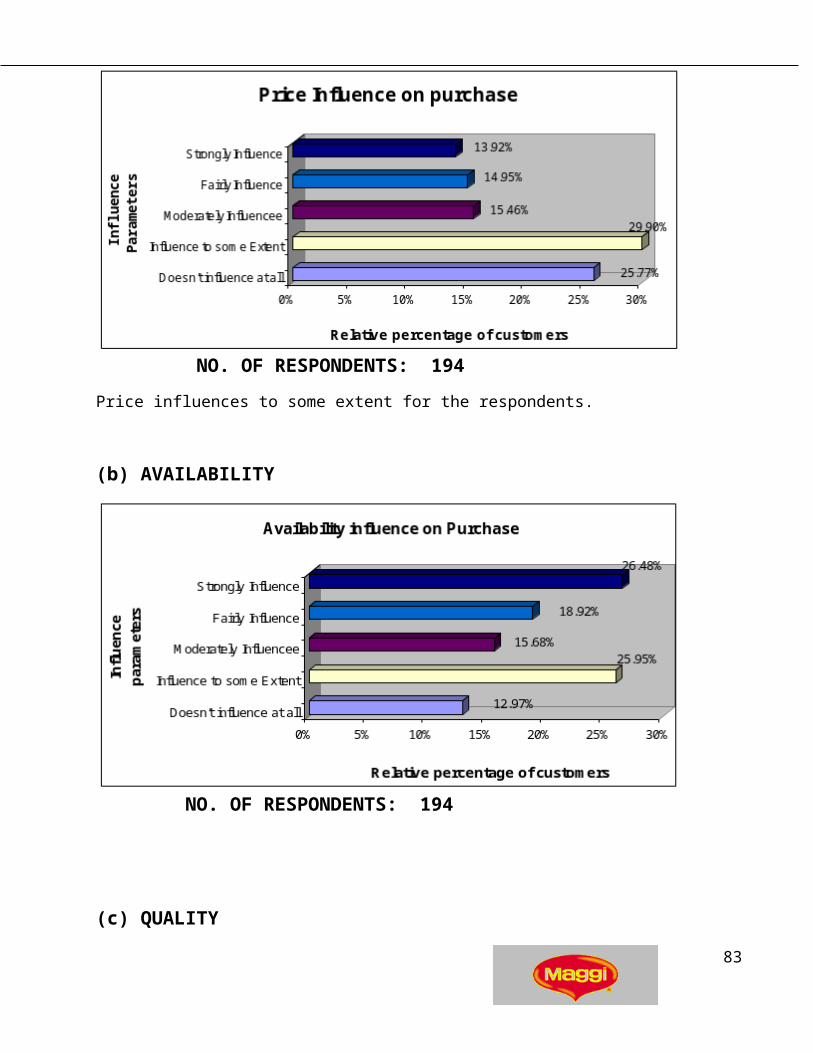

Price influences to some extent for the respondents.

(b) AVAILABILITY

NO. OF RESPONDENTS: 194

(c) QUALITY

62

Page 63

NO. OF RESPONDENTS: 194

Quality, as an attribute, has major contribution towards the selection of sauces as a product.

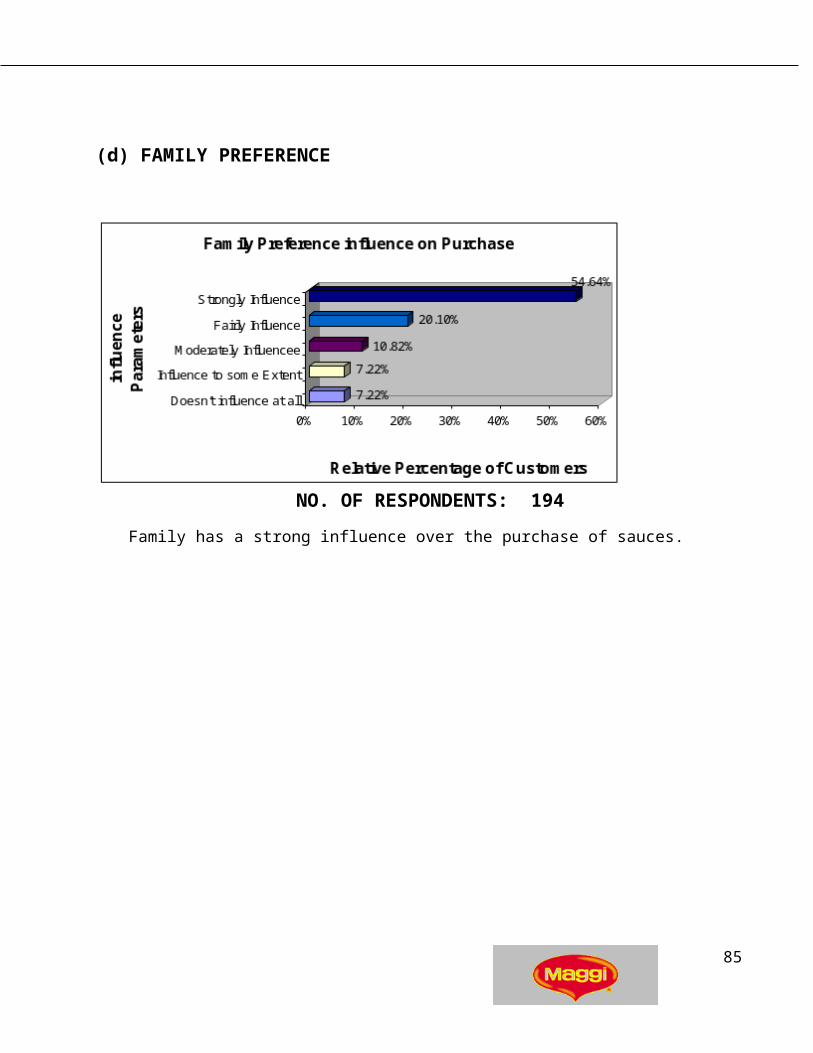

(d) FAMILY PREFERENCE

63

Page 64

NO. OF RESPONDENTS: 194

Family has a strong influence over the purchase of sauces.

64

Page 65

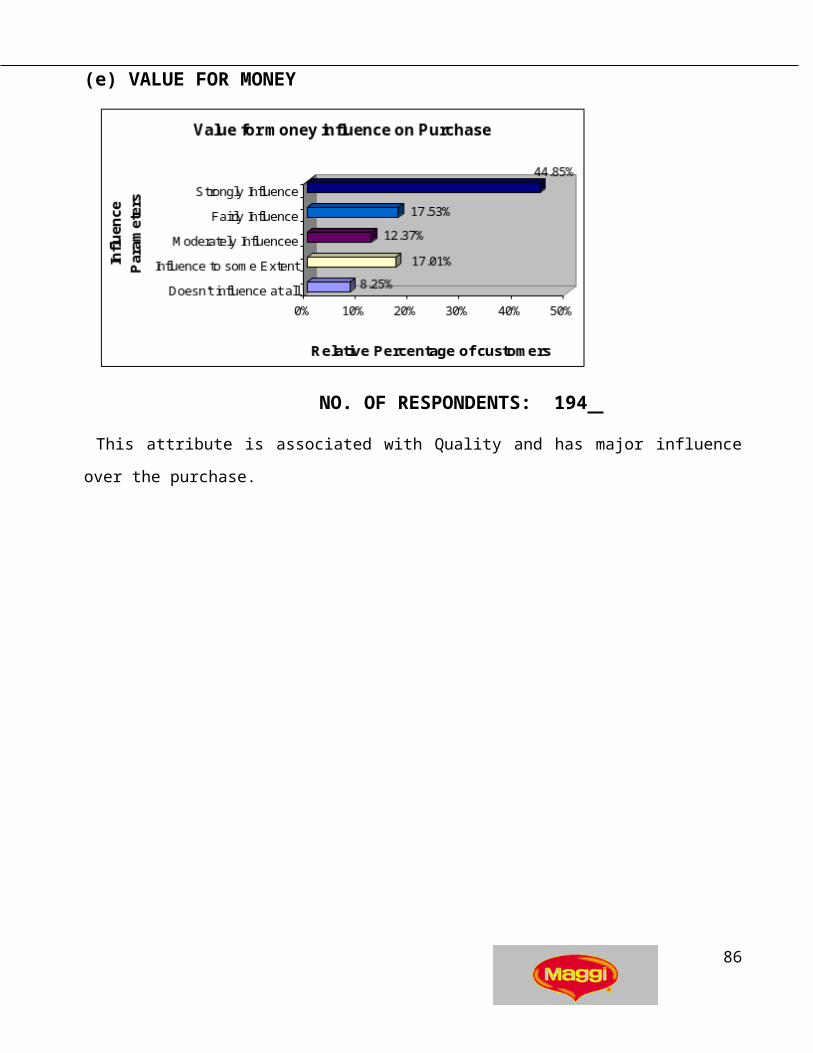

(e) VALUE FOR MONEY

NO. OF RESPONDENTS: 194 This attribute is associated with Quality and has major influence over the purchase.

65

Page 66

(IX) PERCEPTION OF BRANDS

ATTRIBUTE SCORE GIVEN TO MAGGI BY CURRENT USERS

NO. OF RESPONDENTS: 105

Maggi Sauces enjoys maximum market for its Taste and Quality (62.35% and72.38%) respectively.

Also, it has somewhat preference for its spiceness and sweetness

66

Page 67

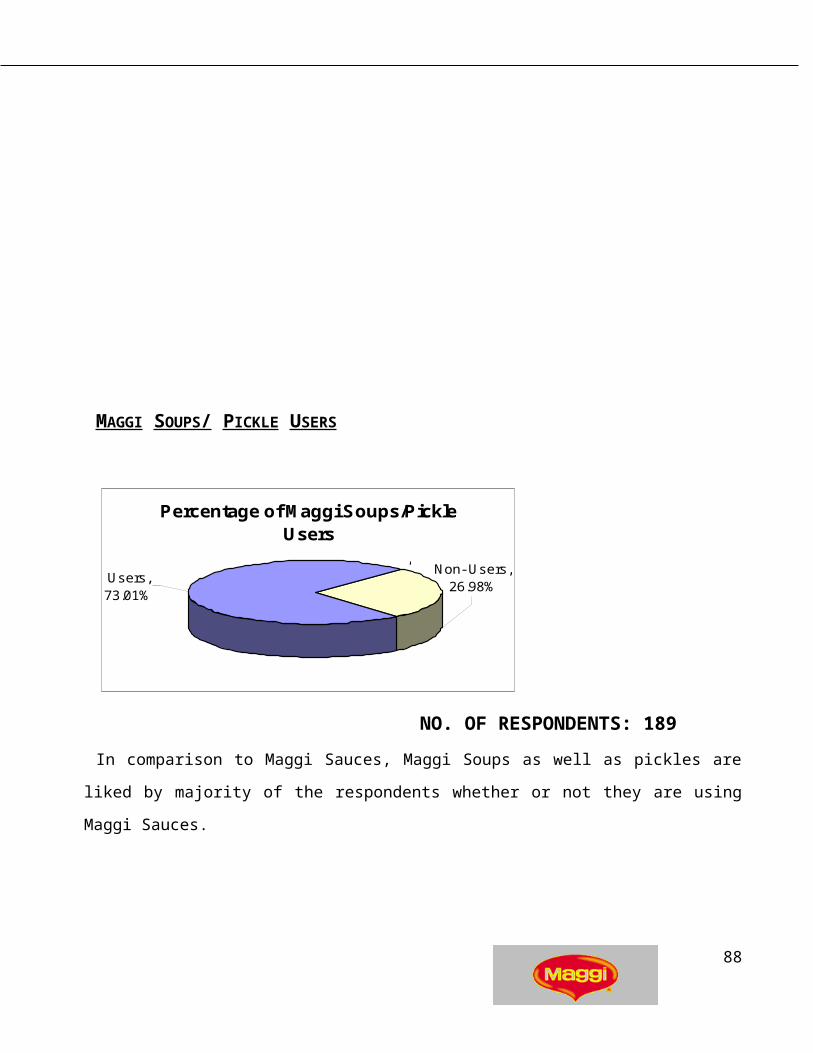

MAGGI SOUPS/ PICKLE USERS

Percentage of Maggi Soups/Pickle Users

,

Users, 73.01%

Non- Users, 26.98%

NO. OF RESPONDENTS: 189

In comparison to Maggi Sauces, Maggi Soups as well as pickles are liked by majority of the

respondents whether or not they are using Maggi Sauces.

67

Page 68

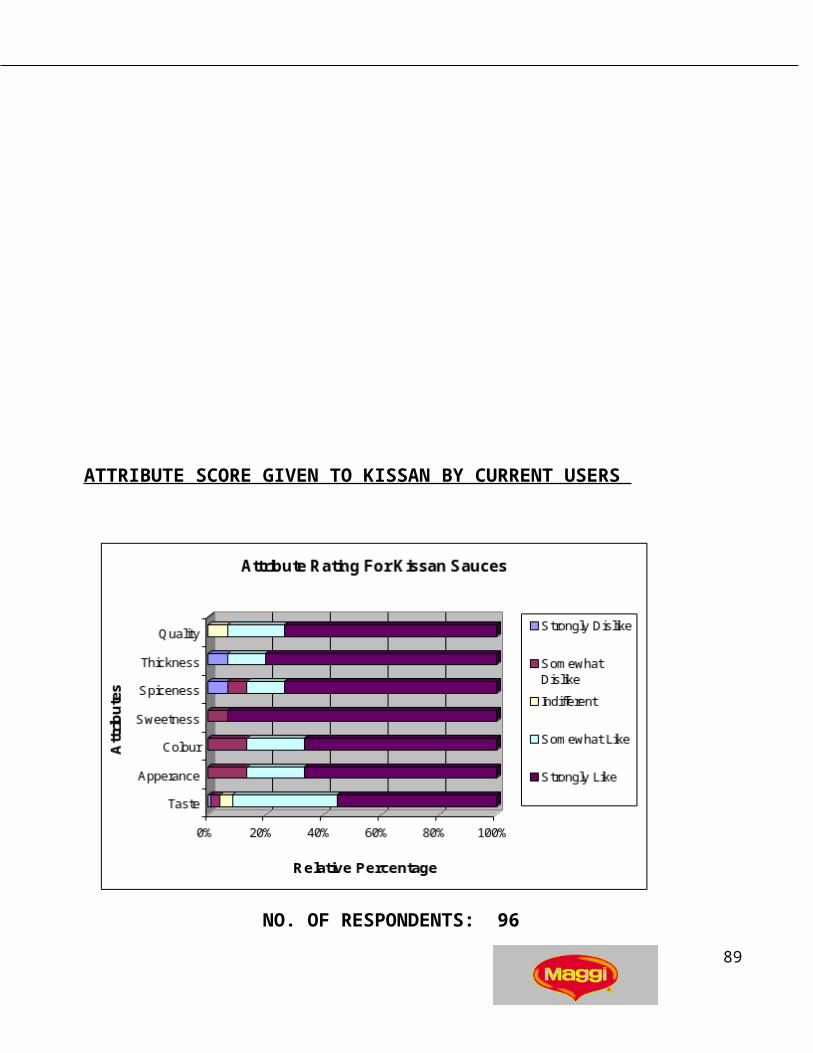

ATTRIBUTE SCORE GIVEN TO KISSAN BY CURRENT USERS

NO. OF RESPONDENTS: 96

Kissan, on the other hand, is liked by majority of the respondents on all of its aspects be it Quality,

Taste, Spiceness or Sweetness.

68

Page 69

KISSAN SQUASH/ JAM USERS

Percentage of Kissan Squash/Jam Users

, Users, 78.72% Non- Users,

21.27%

NO. OF RESPONDENTS: 188

Kissan squashes/ jams are also being consumed in maximum households when compared to Kissan

sauces. (According to the data obtained only 96 respondents agreed to the consumption of Kissan

sauces whereas Kissan squashes/ jams are being purchased by 188 respondents).

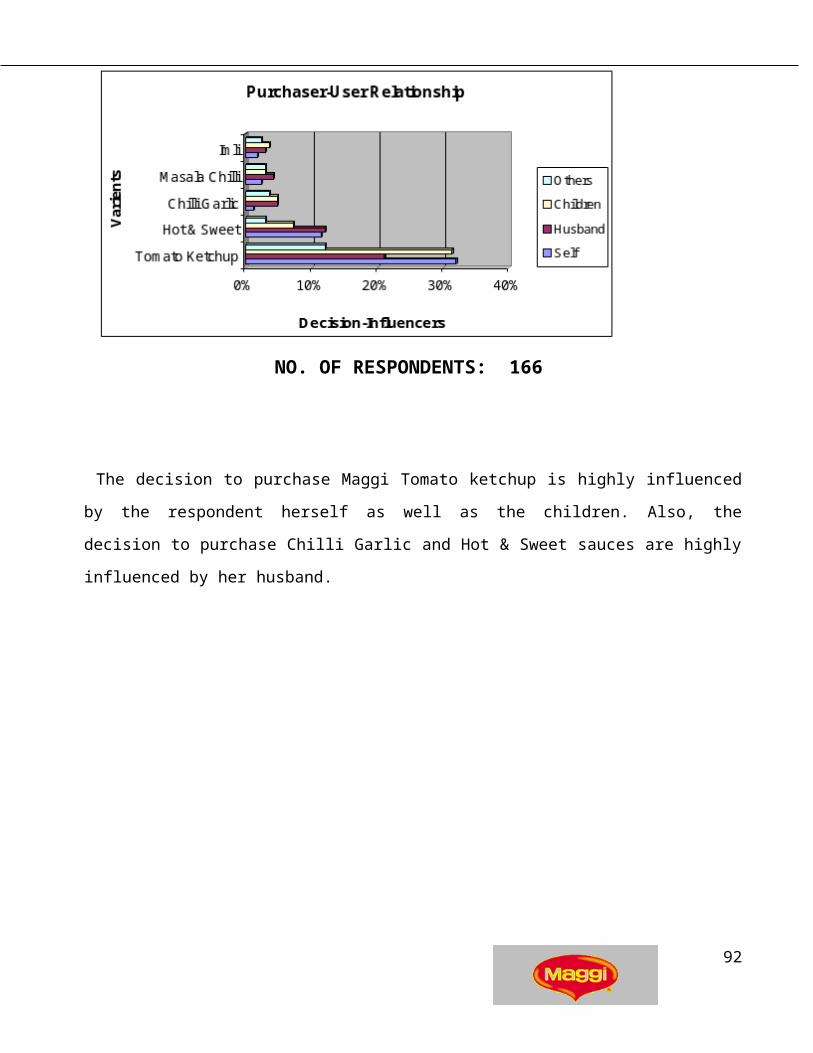

(X) INFLUENCE OF PURCHASER-USER RELATIONSHIP

69

Page 70

NO. OF RESPONDENTS: 166

The decision to purchase Maggi Tomato ketchup is highly influenced by the respondent herself as

well as the children. Also, the decision to purchase Chilli Garlic and Hot & Sweet sauces are highly

influenced by her husband.

70

Page 71

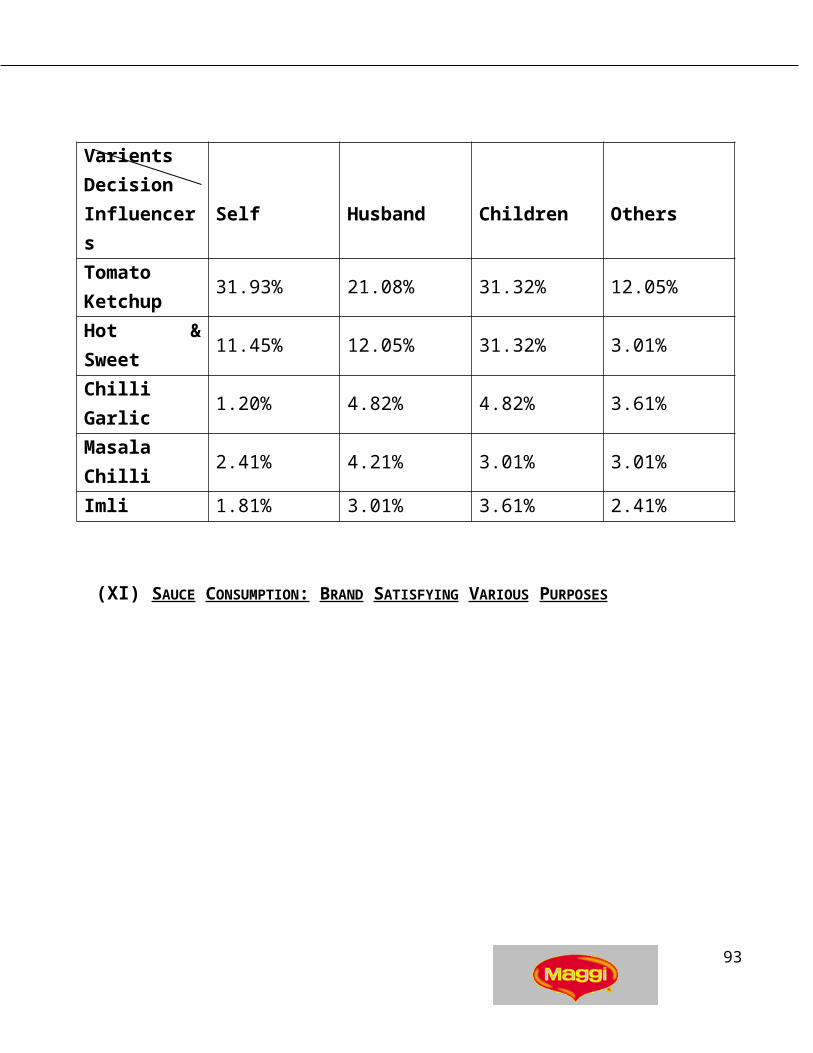

VarientsDecisionInfluencers Self Husband Children Others

Tomato Ketchup

31.93% 21.08% 31.32% 12.05%

Hot & Sweet 11.45% 12.05% 31.32% 3.01%Chilli Garlic 1.20% 4.82% 4.82% 3.61%Masala Chilli 2.41% 4.21% 3.01% 3.01%Imli 1.81% 3.01% 3.61% 2.41%

(XI) SAUCE CONSUMPTION: BRAND SATISFYING VARIOUS PURPOSES

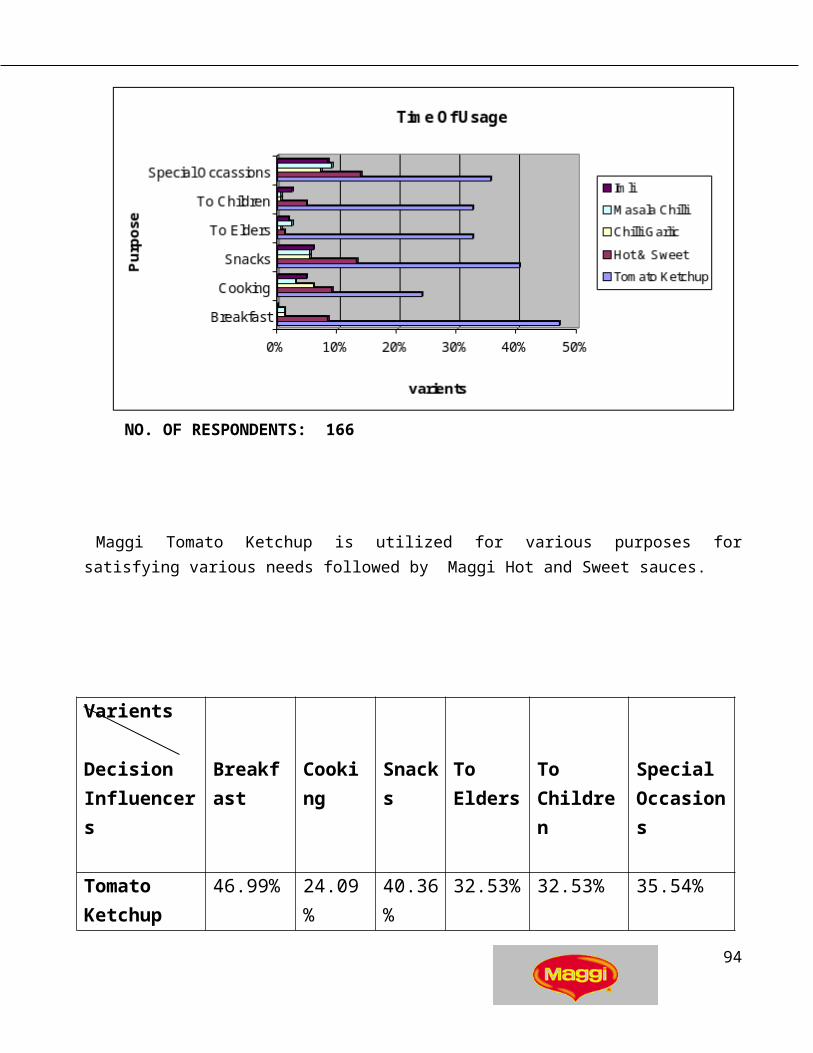

NO. OF RESPONDENTS: 166

Maggi Tomato Ketchup is utilized for various purposes for satisfying various needs followed by Maggi Hot and Sweet sauces.

71

Page 72

Varients

DecisionInfluencers

Breakfast

Cooking

Snacks To Elders

To Children

Special Occasions

Tomato Ketchup

46.99% 24.09%40.36%

32.53% 32.53% 35.54%

Hot & Sweet8.43% 9.04%

13.25%

1.20% 4.82% 13.85%

Chilli Garlic1.20% 6.02% 5.42% 0.60% 0.60% 7.23%

Masala Chilli1.20% 3.01% 5.42% 2.41% 0.60% 9.04%

Imli0% 4.82% 6.02% 1.81% 2.41% 8.43%

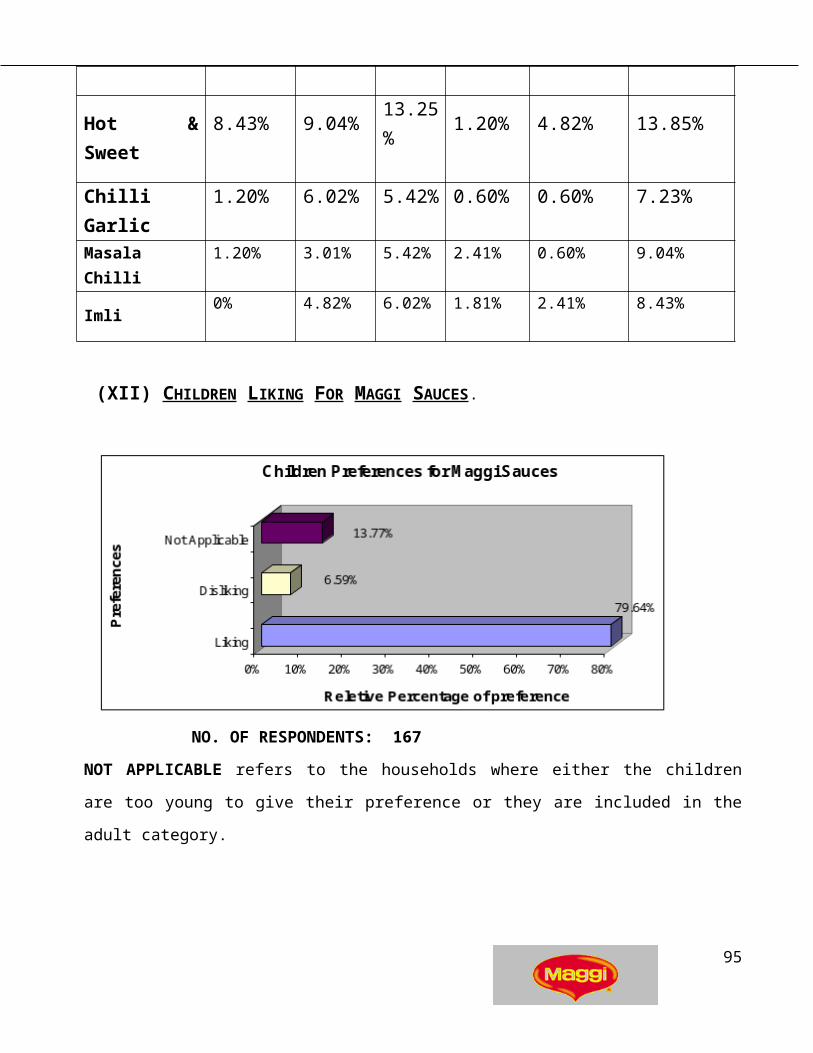

(XII) CHILDREN LIKING FOR MAGGI SAUCES .

NO. OF RESPONDENTS: 167

72

Page 73

NOT APPLICABLE refers to the households where either the children are too young to give their

preference or they are included in the adult category.

(XIII) REASONS FOR HAVING PREFERENCE TOWARDS MAGGI SAUCES

NO. OF RESPONDENTS: 167

Children prefer Maggi Sauces because they associate Maggi Sauces with Maggi Noodles whereas

68.26% like it because of its good taste.

(XIV) IMPACT OF ADVERTISEMENTS ON THE PURCHASE OF MAGGI SAUCES

73

Page 74

NO. OF RESPONDENTS: 167

Maggi advertisements are potential enough to leave an impression in the minds of the customers as

approximately 77% respondents are able to recall the advertisements.

(XV) PRODUCT RECALL: IMPACT OF THE ADVERTISEMENT

NO. OF RESPONDENTS: 167

Approximately 42% respondents recalled Maggi Tomato ketchup whereas 17% said it was the

advertisement for Maggi Hot & Sweet.

74

Page 75

(XVI) COMMUNICATION BY ADVERTISEMENTS: UNAIDED RECALL OF PUNCH LINE

NO. OF RESPONDENTS: 167

Though 77% of the respondents were able to recall the advertisements, 66 %( approx.)

Were not able to recall the communication made by that advertisement.

(XVII) SOURCES OF AWARENESS OF ADVERTISEMENTS

Punch-Line recall

,

Not Able to recall,

65.27%

Able to recall, 34.73%

75

Page 76

NO. OF RESPONDENTS: 167

Respondents who visualized the advertisement of Maggi sauces on TV are: - 84% (approx.)

Respondents who visualized the advertisement of Maggi sauces in Press are: - 7% (approx.)

Respondents who visualized the advertisement of Maggi sauces on Hoardings are: - 6% (approx.)

(XVIII) I MPACT OF THESE ADVERTISEMENTS

NO. OF RESPONDENTS: 167

Impact was favourable for the products, especially, Maggi Tomato Ketchup & Maggi Hot & Sweet

as 70% of the respondents agreed to buy more after seeing these advertisements.

Impact of Advertisements on Buying

,

Favourable, 69.46%

Unfavourable, 30.84%

76

Page 77

(XIX) PREFERENCE FOR VARIOUS PROMOTIONAL SCHEMES

NO. OF RESPONDENTS: 167

Discounts/ Price-off is the most worthy Promotional Scheme, as told by the respondents. Following

this is more quantity at same price.

(XX) INFLUENCE OF VARIOUS PROMOTIONAL SCHEMES ON PURCHASE

30.54%

49.70%

39.52%

0% 10% 20% 30% 40% 50%

Relative percentage of preference

Gifts

Discounts/price-off

More Quantity at same price

P r o m o ti o n a l

Sc

he

me

s

Preference for Promotional Schemes

77

Page 78

Influence of Promotional Schemes on Purchase

,

Buying More, 73.05%

Not Buying More,

26.95%

NO. OF RESPONDENTS: 167

The promotional Schemes have the favourable response on the respondents, as 73% of the

respondents agree to buy more.

(XXI) SOURCES OF AWARENESS OF PROMOTIONAL SCHEMES

89.82%40.72%

43.11%

13.17%

1.80%

4.19%

3.59%

0% 20% 40% 60% 80% 100%

Relative percentage of respondents

T.V.

Newspaper

Shopkeeper

Magazine

Hoarding

Radio

P.O.P

So

urc

es

Sources of Awareness of Promotional Schemes

NO. OF RESPONDENTS: 167

Approximately 90% of the respondents find TV as one of the most important promotional tool.

78

Page 79

Whereas, only 40% find newspaper as the informative promotional tool.

(XXII) BRAND LOYALITY TOWARDS MAGGI SAUCES

Percentage of Brand Loyals

,

Brand Loyal, 58.08%

Brand Switchers,

41.91%

NO. OF RESPONDENTS: 167

Maggi sauces continue to hold its position as 58% of the respondents continue to buy Maggi Sauces

even if there is a promotional scheme on some other brand. Also, the respondents who said that they

will be shifting to other brands because of the promotional schemes, will shift only if the other brand is

Kissan

79

Page 80

(XXIII) PRIDE ASSOCIATED WITH MAGGI SAUCES

Pride Associated with Maggi Sauces

,

,

Can't Say, 6.59%

Not feeling Pride, 18.56%

Respondents feeling Pride,

74.85%

NO. OF RESPONDENTS: 167

75% of the respondents feel pride in serving Maggi Sauces to their guests and associate

this with prestige issue.

80

Page 81

(XXIV) REASONS FOR NOT PURCHASING MAGGI SAUCES (AS GIVEN BY THE

NEVER USERS)

16.67%

16.67%

5%

33.30%16.67%

0%

3.33%

3.33%

6.66%

13.30%

6.66%

0% 5% 10% 15% 20% 25% 30% 35%

Relative percentage of respondents

Prices too high

Poor Quality

Non-Availability

Poor Taste

satisfied w ith Current brand

Never felt need of trying maggi

Not liked by family

Bad w ord of mouth

Thickness

No Specif ic reason

Its perfect

Rea

son

s

Reasons for not using maggi Sauces (as given by never users)

81

Page 82

Among the Never users and One-time users, 33% does not like the taste of Maggi Sauces (mainly

because of the presence of garlic and onions in it). Also, 17% feel it has poor packaging. (They

associate Quality with packaging) whereas 17% are satisfied with the current brand they use.

82

Page 83

REASONS FOR NOT PURCHASING MAGGI SAUCES (AS GIVEN BY THE PAST USERS)

37.50%12.50%

6.25%

12.50%

5%

2.50%

1%

2.50%

5%

12.50%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Relative percentage of respondents

Prices too high

Poor Quality

Non-Availability

Poor Taste

satisf ied w ith Current brand

Never felt need of trying maggi

Not liked by family

Bad w ord of mouth

Thickness

No Specif ic reason

Re

as

on

s

Reasons for Not Purchasing maggi Sauces(As given by past Users)

Among the Past Users, 38% feel that the prices of Maggi Sauces are too high in comparison to the

current brand they use whereas 7% have shifted because of the non-availability of Maggi Sauces.

83

Page 84

CONCLUSION

According to Marten Harper,

“To manage a business well is to manage its future, and to manage the future is to manage

information.”

In today’s competitive world, it is very difficult for the companies to sustain and in order to keep their

hands on the pulse of both business and consumers there is a strange need to have information. In the

fast moving consumer goods (FMCG) industry, it is not only difficult to get information but also very

important. The most crucial part is to manage this objective in mind, the research was conducted in the

14 localities of the D khanna market and the following conclusions are drawn from the study:-

There is a considerable degree of brand loyalty (almost 60%) towards Maggi Sauces that

in it indicates that people have strong admiration towards tastes and quality of Maggi

sauces.

The advertisement of Maggi Hot n Sweet Sauce has a strong recall in the minds of

consumers and the famous statement “Its Different” and “2-minutes”are still fresh in their

minds.

There is a very strong impact of the advertisements of Maggi on the minds of consumers

as approximately 100% consumers are aware of Maggi Sauces.

In case of preference for promotional schemes approximately half of the consumers have

stated their liking towards Price-Off followed by Gifts and Incentives.

It has been observed in most of the cases that the decision to purchase sauces is the joint

family decision whereby children are playing a major role for purchasing sauces.

Promotional Schemes have a strong degree of influence on the purchasing decision of

consumers in all the income groups.

84

Page 85

Kissan is a strong competitor for Maggi Sauces. Also, threat is posed off from some

domestic players on account of low price and more distribution and availability

Heinz repositioning strategy is also playing a major threat to Maggi Sauces.

There is an emerging trend among the consumers for using more than one brand of

sauces (as told by more than half of the respondents), one for household and other for

special occasions and consumers use Maggi Sauce for this purpose as its add to their

prestige.

75% consumers feel pride in serving Maggi sauces to their guests, a strong image for the

company.

Past Users of Maggi Sauces (35%) feel that Maggi sauces should be relaunched with

reduced prices, better packaging, and improved quality along with more no. of

promotional schemes.

85

Page 86

SUGGESTIONS

Market oriented thinking is a necessity in todays competitive world. In many places, there are too

many goods chasing too few customers. Most of the companies are competing to enlarge their share of

existing market. In the end, the companies’ best satisfy their customers will be winners. It is special

responsibility of marketers to understand the needs and wants of market place and to help their

companies translate them into solutions that win the customer’s approval. Today’s smart companies

are not merely looking for sales; they are investing in long term, mutually satisfying customer

relationships based on delivering quality, service and value. Keeping this objective in mind following

suggestions can be made: -

Nestle should stress more on advertising its products, i.e. Maggi Masala Chilli, Maggi Chilli Garlic

and Maggi Tomato Ketchup.

They should also improve the availability of their products; introduce the varients without onions

and garlic.

They can relaunch their products by reducing the prices supported with more of promotional

schemes, free-samples/sachets.

86

Page 87

SWOT ANALYSIS FOR MAGGI SAUCES

STRENGTHS

Strong brand identity among consumers; especially through Maggi Noodles.

Available in varieties of flavours.

WEAKNESSES

A low overall marketing effort.

Has placed its components at higher prices in comparison to Kissan which is the major threat

to Maggi Sauces.

Poor packaging

Less number of promotional schemes.

Non-availability of fresh stock in the market.

Price-Quantity trade-off is not taken care off.

87

Page 88

OPPORTUNITIES

Widely untouched rural market.

Associations with major fast food chains (MNCs)/food shows.

Associations with companies dealing in cooking ware, like, microwave oven.

Should introduce more flavours, like ones without onion and garlic.

Make the bottle handy with widened mouth so that it can become mobile.

Create more uses and more demands

THREATS

Loyality reducing among customers.

Threat from local and low priced entrants/substitutes.

Threat from Home Made Sauces.

Unable to create repeated purchases.

88

Page 89

QUESTIONNAIREOBJECTIVE: - To study the brand preference of Maggi Tomato Ketchup.

1. Name: …………………………………………

2. Sex:

Male

Female

3. Family Monthly Income:

5000-10000

10000-15000

15000-25000

25000 and above

4. Location: ……………………………………

5. Age:

15-25

25-35

35-45

45 and above

89

Page 90

6. Family type:

Joint

Nuclear

7. Do you consume tomato ketchup?

Yes

No

8. Which type of sauce do you prefer?

Branded

Home made

Unbranded

Branded+ home made

Tomato based sauces

9. Which brand you prefer the most?

Maggi

Kissan

Heinz

Tops

Volfram

10. Have you ever used Maggi Tomato Ketchup?

Yes

No

90

Page 91

11. If no, it is because:

Lack of awareness

Lack of availability

You find it expensive

You don’t like the product.