Page 1 Copyrighted Material. All rights reserved. The McLean Group, LLC M&A Trends: Tech & Government Contracting Deal Dynamics, Valuation, Drivers and Markets in an Era of Uncertainty Presented by: Greg Boucher Managing Director The McLean Group [email protected]Direct: 410.799.2053 September 25, 2012

Transcript

Page 1 Copyrighted Material. All rights reserved. The McLean Group, LLC

M&A Trends: Tech & Government

Contracting Deal Dynamics, Valuation, Drivers and Markets in an Era of Uncertainty

Alternatives for granting equity awards to key employees:

1. Restricted Stock

2. Restricted Stock Units

3. Stock Options

Incentive Stock Options (ISOs)

Nonqualified Stock Options (NQSOs)

4. Stock Appreciation Rights

5. Phantom Stock

Awards may be used in whole or in part to carry-out a succession plan

32

Restricted Stock

A grant of shares of stock with limitations on transferability; may be subject to vesting requirements or other “substantial risk of forfeiture”

May be awarded for no consideration as a stock bonus or recipient may pay all or a portion of stock’s FMV

May be subject to repurchase restrictions that require the resale of stock to the company at some predetermined or formula price upon certain triggering events

Not treated as “non-qualified deferred compensation” (NQDC) under the American Jobs Creation Act (AJCA)

33

Restricted Stock

Tax Overview

Governed by IRC § 83 – taxation of “property” transferred “in

connection with the “performance of services”

Taxed upon vesting of the award (i.e., when stock is no longer

subject to a substantial risk of for forfeiture)

If no substantial risk of forfeiture, taxed at time of award

Substantial Risk of Forfeiture (IRC § 83)

Exists where rights in property are conditioned upon future

performance of substantial services by any person, or the

occurrence of a condition related to a purpose of the transfer

Section 83(b) election is available.

34

Stock Options

Represent a right to buy stock during a specified period at a

fixed purchase price

Types:

Incentive Stock Options (ISOs)

Non-qualified Stock Options (NQSOs)

Generally not deemed to be “property” for income tax purposes

(IRC § 83)

35

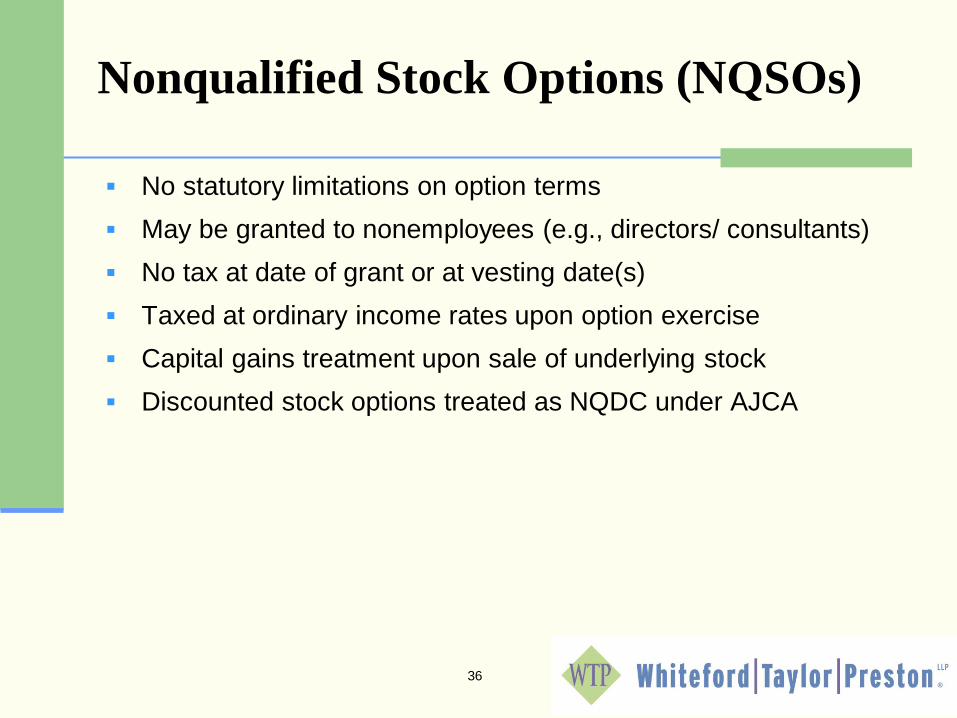

Nonqualified Stock Options (NQSOs)

No statutory limitations on option terms

May be granted to nonemployees (e.g., directors/ consultants)

No tax at date of grant or at vesting date(s)

Taxed at ordinary income rates upon option exercise

Capital gains treatment upon sale of underlying stock

Discounted stock options treated as NQDC under AJCA

36

Incentive Stock Options (ISOs)

Plan Requirements: Written Plan

Must specify aggregate number of shares subject to Plan

May limit all awards under omnibus plan or may limit ISO

awards only

“Net” share counting permitted (i.e., forfeited shares and shares

issued to satisfy exercise price can be reissued under Plan)

Must identify eligible Employees or class of Employees

Stockholder approval required within 12 months of adoption of Plan

No additional stockholder approval required for ISOs assumed

in a corporate transaction

ISOs are not subject to AJCA

ISO grant terms are subject to numerous special requirements

under the IRC.

37

Other Types of Equity Awards

Phantom Stock

Employee granted units equivalent to (but not actual) shares of Employer stock

Stock Appreciation Rights

Represent right to be paid spread between grant price and FMV of stock at exercise date

Restricted Stock Units Units representing shares of common stock settled by delivery of

shares at vesting or later payout

38

Equity Compensation –

Employee Tax Summary

NQSO ISO Phantom

Stock

SARs Restricted

Stock

Restricted Stock

Units

Grant Date No tax impact No tax

impact

No tax

impact

No tax

impact

No tax impact1 No tax impact

Vesting Date No tax impact No tax

impact

No tax

impact

No tax

impact

Ordinary

income1

Ordinary income2

Exercise

Date

Ordinary

income on

spread

No tax

impact3

Ordinary

income on

FMV of unit

Ordinary

income on

spread

N/A N/A

Sale Date Capital gain on

appreciation

post exercise

Capital Gain4 N/A N/A Capital gain on

appreciation1

Capital Gain on

appreciation

1 Assumes substantial risk of forfeiture exists and that recipient does not make a §83(b) election. 2 RSU may provide for deferral of payout after vesting – subject to AJCA deferral requirements. 3 AMT may be applicable. 4 Absent “disqualifying disposition.”

39

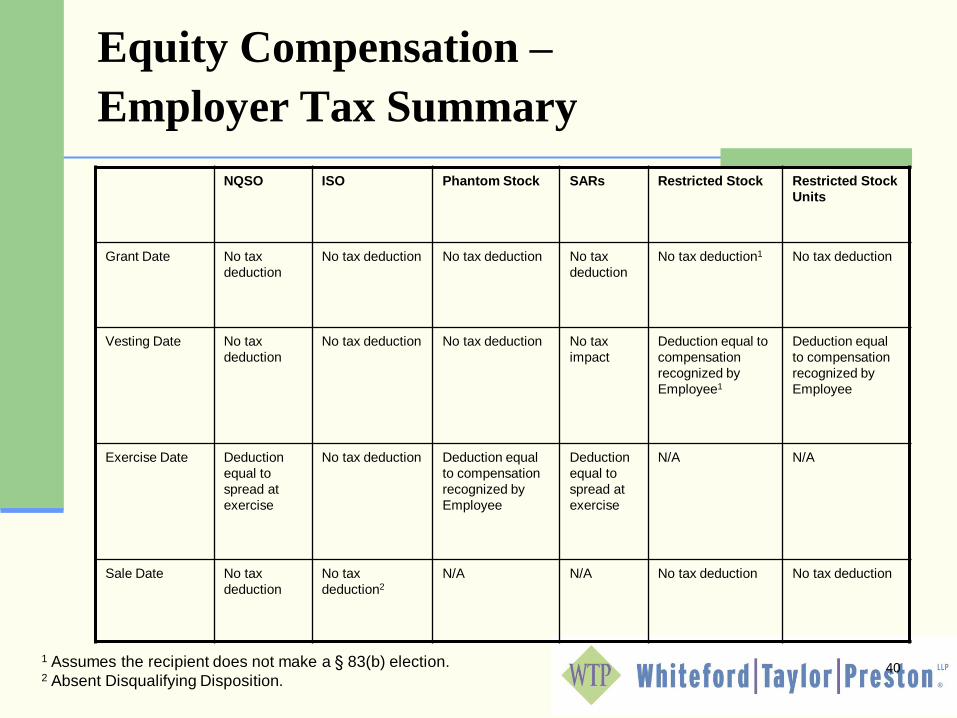

Equity Compensation –

Employer Tax Summary

NQSO ISO Phantom Stock SARs Restricted Stock Restricted Stock

Units

Grant Date No tax

deduction

No tax deduction No tax deduction No tax

deduction

No tax deduction1 No tax deduction

Vesting Date No tax

deduction

No tax deduction No tax deduction No tax

impact

Deduction equal to

compensation

recognized by

Employee1

Deduction equal

to compensation

recognized by

Employee

Exercise Date Deduction

equal to

spread at

exercise

No tax deduction Deduction equal

to compensation

recognized by

Employee

Deduction

equal to

spread at

exercise

N/A N/A

Sale Date No tax

deduction

No tax

deduction2

N/A N/A

No tax deduction No tax deduction

1 Assumes the recipient does not make a § 83(b) election. 2 Absent Disqualifying Disposition.

40

Basic Types of Exit Strategies:

41

1. Company Stock Redemption

2. Management Led Buyout

3. Third Party Sale

4. Sale to an ESOP

This Presentation is focused on a sale of target to a third-party

Buyer

M&A Risks for Seller

Disruption of business, loss of key employees, etc.

Loss of ownership/control

Confidentiality issues and risks

Unless an “all cash” deal, Buyer’s stock

Substantial costs and negotiation time

Earn-outs and contingent consideration

Escrow, holdbacks and indemnities

Failure to integrate and execute successfully

Affect on customers/suppliers if deal doesn’t go through

42

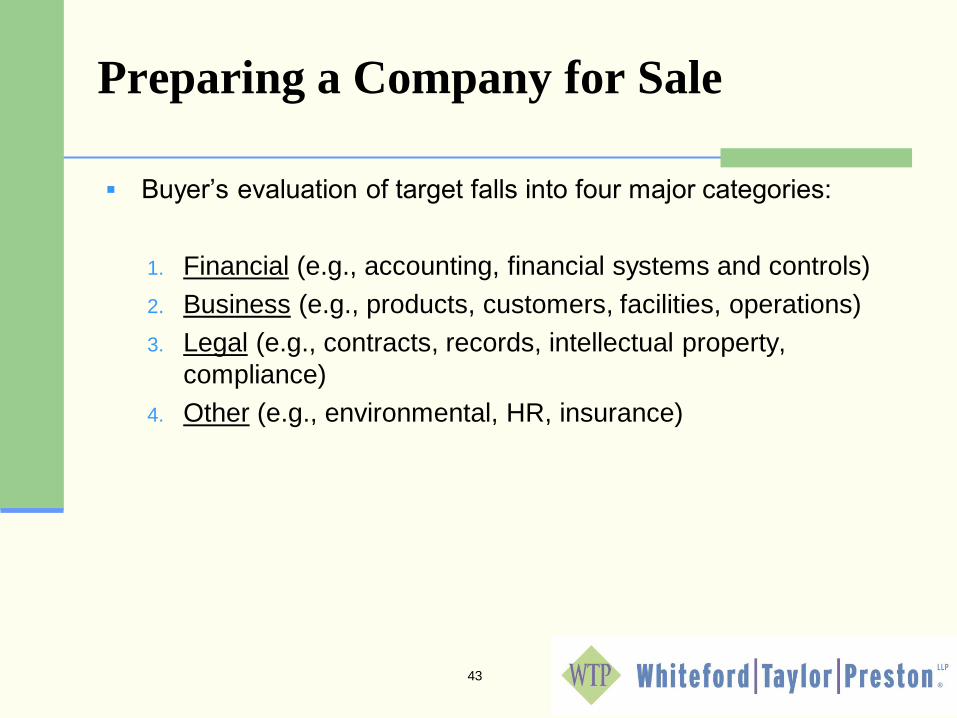

Preparing a Company for Sale

Buyer’s evaluation of target falls into four major categories:

1. Financial (e.g., accounting, financial systems and controls)

2. Business (e.g., products, customers, facilities, operations)

Analyze the impact of the deal structure on the owner’s ability to meet lifetime financial

goals and objectives

Explore advantages of wealth transfer planning pre-transaction

From P&L to Portfolio Bernstein.com 60

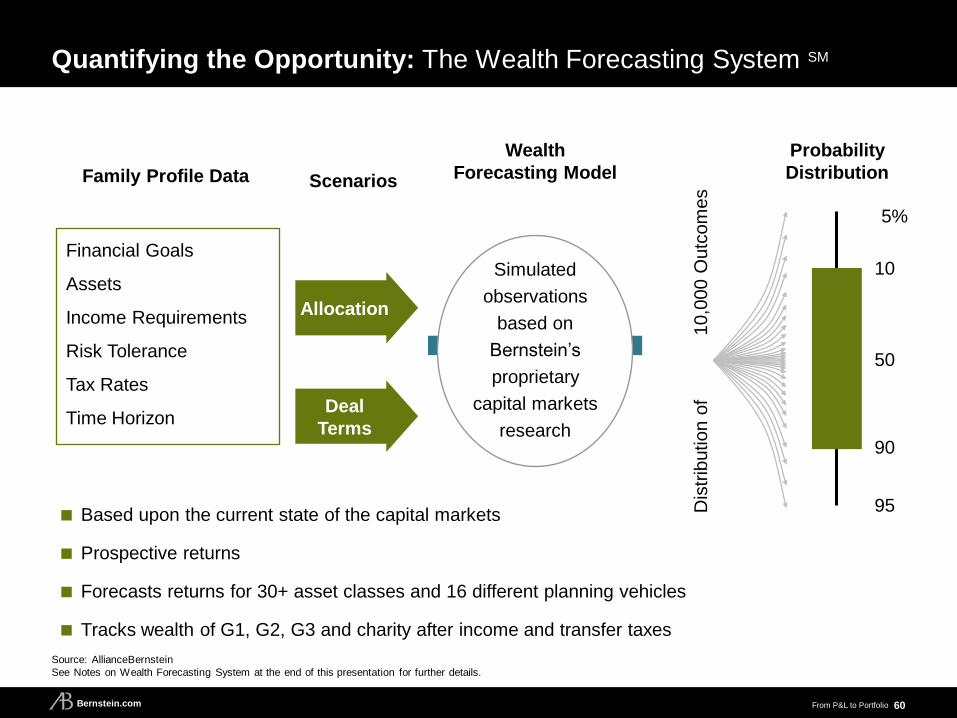

Quantifying the Opportunity: The Wealth Forecasting System SM

Based upon the current state of the capital markets

Prospective returns

Forecasts returns for 30+ asset classes and 16 different planning vehicles

Tracks wealth of G1, G2, G3 and charity after income and transfer taxes

Family Profile Data

Wealth

Forecasting Model

Probability

Distribution

Financial Goals

Assets

Income Requirements

Risk Tolerance

Tax Rates

Time Horizon

Dis

trib

ution o

f 10,0

00 O

utc

om

es

Simulated

observations

based on

Bernstein’s

proprietary

capital markets

research

5%

50

90

10

95

Scenarios

Allocation

Deal

Terms

Source: AllianceBernstein

See Notes on Wealth Forecasting System at the end of this presentation for further details.

From P&L to Portfolio Bernstein.com

Evaluating What You Need and What You Want

61

How much?

To whom?

How quickly?

What techniques?

Excess Capital

Amount that can be

transferred

How much do you spend?

What is your age?

What is your risk tolerance?

Core Capital

Amount to ensure spending

needs are met

Calculated at 90% level of

confidence

Charity

Capital for Next

Venture

Extra Spending

Children and

Grandchildren

Personal Reserve

Lifestyle

Spending

From P&L to Portfolio Bernstein.com

How does their risk tolerance affect their decision?

Which offer should the couple take so that they can retire confidently today?

Case Study: Retiring Securely

Married couple, age 60, wants to sell their technology company and retire

Investment assets of $1.25 million of which $250,000 is in a qualified retirement plan

Currently spending $240,000 per year

Evaluating two term sheets:

(More Upfront) The first provides $10 million total—$8 million upfront and an annual earnout of

$400,000 for five years

(Less Upfront) The other provides $12 million total—$4 million upfront and an annual earnout of

$1.6 million for five years

62

From P&L to Portfolio Bernstein.com

$12.6

$9.5

$8.2 $7.7

0/100 20/80 40/60 60/40

$4.5 Mil. (Less Upfront)

$7.7 Mil. (More Upfront)

Current Assets**

What Is the Couple’s Core Portfolio?

63

Amount Needed to Fund Core Portfolio Today Spend $240,000 (Real)

($ Millions)*

*Based on Bernstein’s estimate of returns for the applicable capital markets over the applicable time horizon. Data do not represent past performance and are not a promise of

actual or a range of future results. Core capital calculated at 90% level of confidence assuming adjusted joint life expectancy. Variations in actual income, spending, applicable

tax rates, life span and market returns may substantially impact the likelihood that a core-capital estimate will be sufficient to provide for future expenses.

**Current assets are the sum of the beginning portfolio assets plus the after-tax sale proceeds in the first year of the analysis. A combined 19.25% state and federal capital gains tax

rate was assumed.

***“Asset Allocation” refers to the proportion of assets invested in stocks and the proportion invested in bonds over the next 35 years. Assumes globally diversified stocks (21% US

value, 21% US growth, 21% US diversified, 7% US small and mid cap, 22.5% developed international and 7.5% emerging markets); bonds are assumed to be intermediate term

with municipal bonds in the taxable portfolio and taxable bonds in the tax-deferred portfolio. See Notes on Wealth Forecasting System at the end of this presentation for further

details.

Source: AllianceBernstein

Asset Allocation (Stocks/Bonds)***

From P&L to Portfolio Bernstein.com

What Is the Couple’s Investment Risk?

42%

32%

69%

93%

2% 2%11%

46%

2% 2% 2%

12%

0/100 20/80 40/60 60/40

10% Loss 20% Loss 30% Loss

64

Probability of Peak-to-Trough Losses over 40

years*

Data do not represent past performance and are not a promise of actual or a range of future results.

*Data indicate the probability of a peak-to-trough decline in pretax, pre-cash-flow cumulative returns of 10%, 20% or 30% over the next 40 years. Because the Wealth Forecasting

System uses annual capital markets returns, the probability of peak-to-trough losses measured on a more frequent basis (such as daily or monthly), may be understated. The

probabilities depicted above include an upward adjustment intended to account for the incidence of peak-to-trough losses that do not last an exact number of years.

**“Asset Allocation” refers to the proportion of assets invested in stocks and the proportion invested in bonds over the next 40 years. Assumes globally diversified stocks (21% US

value, 21% US growth, 21% US diversified, 7% US small and mid cap, 22.5% developed international and 7.5% emerging markets); bonds are assumed to be intermediate term

with municipal bonds in the taxable portfolio and taxable bonds in the tax-deferred portfolio. See Notes on Wealth Forecasting System at the end of this presentation for further

details.

Source: AllianceBernstein

Asset Allocation (Stocks/Bonds)**

From P&L to Portfolio Bernstein.com

94% 96% 96% 98%

40/60 60/40 40/60 60/40

Both Deals Meet Spending Plan—If They Get 100% of Earnouts

65

35th Year—Probability of Maintaining Spending* Spending $240,000 (Real)

100% Earnout**

Asset Allocation (Stocks/Bonds)***

*“Probability of Maintaining Spending” represents the probability of having assets greater than $0 at the end of the 35th year. Based on Bernstein’s estimate of returns for the

applicable capital markets over the next 35 years. Data do not represent past performance and are not a promise of actual or a range of future results.

**Assumes the couple receives each annual payout in its entirety as described previously.

***“Asset Allocation” refers to the proportion of assets invested in stocks and the proportion invested in bonds over the next 35 years. Assumes globally diversified stocks (21% US

value, 21% US growth, 21% US diversified, 7% US small and mid cap, 22.5% developed international and 7.5% emerging markets); bonds are assumed to be intermediate term

with municipal bonds in the taxable portfolio and taxable bonds in the tax-deferred portfolio. See Notes on Wealth Forecasting System at the end of this presentation for further

details.

Source: AllianceBernstein

More Upfront

Less Upfront

From P&L to Portfolio Bernstein.com

If Earnouts Are Less Certain, Asset Allocation Can Help

66

35th Year—Probability of Maintaining Spending* Spending $240,000 (Real)

60% Earnout**

*“Probability of Maintaining Spending” represents the probability of having assets greater than $0 at the end of the 35th year. Based on Bernstein’s estimate of returns for the

applicable capital markets over the next 35 years. Data do not represent past performance and are not a promise of actual or a range of future results.

**Assumes the couple receives an earnout of only $240,000 per year in the “More Upfront” scenarios and $960,000 per year in the “Less Upfront” scenarios.

***“Asset Allocation” refers to the proportion of assets invested in stocks and the proportion invested in bonds over the next 35 years. Assumes globally diversified stocks (21% US

value, 21% US growth, 21% US diversified, 7% US small and mid cap, 22.5% developed international and 7.5% emerging markets); bonds are assumed to be intermediate term

with municipal bonds in the taxable portfolio and taxable bonds in the tax-deferred portfolio. See Notes on Wealth Forecasting System at the end of this presentation for further

details.

Source: AllianceBernstein

91% 94%

84% 89%

40/60 60/40 40/60 60/40

Asset Allocation (Stocks/Bonds)***

More Upfront

Less Upfront

From P&L to Portfolio Bernstein.com

0

23

45

68

90

$3.3$1.1

What Is the Impact on the Couple’s Future Wealth?

67

$45.9

$14.1

$26.7

$8.7

$62.5

$20.5

$36.9

$13.5

Range of Wealth Values, Year 35* After Taxes and Cash Flows, Nominal

60% Earnout**

$ M

illio

ns

*Based on Bernstein’s estimate of returns for the applicable capital markets over the next 35 years. Data do not represent past performance and are not a promise of actual or

a range of future results.

Asset values represent the estimated market value; if the assets were liquidated, additional capital gains or losses would be realized that are not reflected here.

**Assumes the couple receives an earnout of only $240,000 per year in the “More Upfront” scenarios and $960,000 per year in the “Less Upfront” scenarios.

***“Asset Allocation” refers to the proportion of assets invested in stocks and the proportion invested in bonds over the next 35 years. Assumes globally diversified stocks (21% US

value, 21% US growth, 21% US diversified, 7% US small and mid cap, 22.5% developed international and 7.5% emerging markets); bonds are assumed to be intermediate term

with municipal bonds in the taxable portfolio and table bonds in the tax-deferred portfolio. See Notes on Wealth Forecasting System at the end of this presentation for further details.

Source: AllianceBernstein

40/60 60/40 40/60 60/40

Asset Allocation (Stocks/Bonds)***

More Upfront Less Upfront

5%

10

50

90

95

Level of

Confidence

From P&L to Portfolio Bernstein.com

Case Study: Excess Planning—Client Situation

68

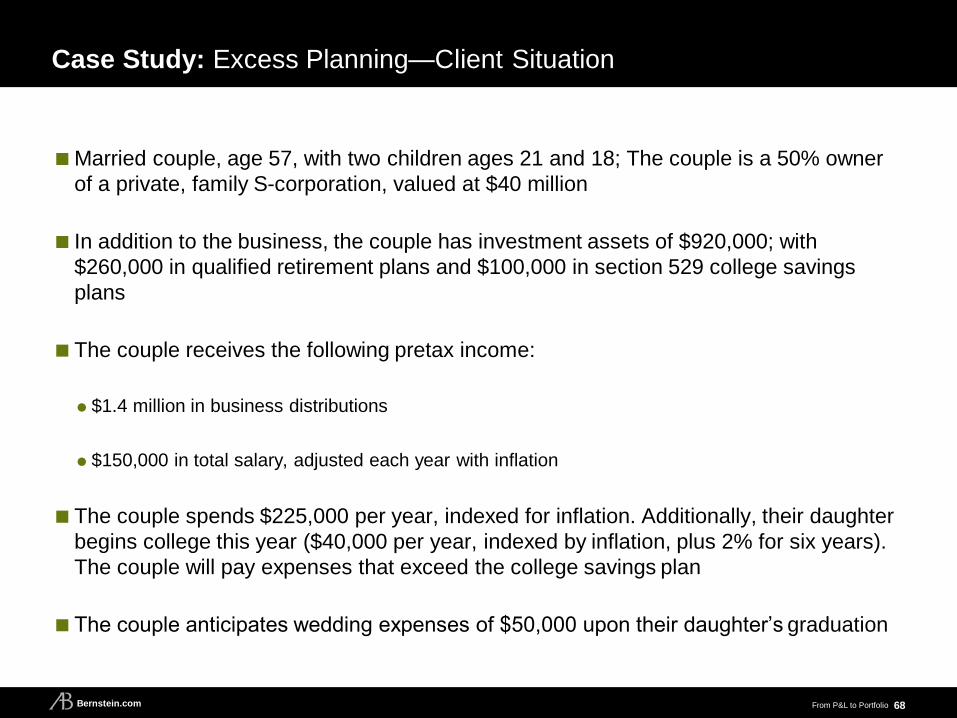

Married couple, age 57, with two children ages 21 and 18; The couple is a 50% owner

of a private, family S-corporation, valued at $40 million

In addition to the business, the couple has investment assets of $920,000; with

$260,000 in qualified retirement plans and $100,000 in section 529 college savings

plans

The couple receives the following pretax income:

$1.4 million in business distributions

$150,000 in total salary, adjusted each year with inflation

The couple spends $225,000 per year, indexed for inflation. Additionally, their daughter

begins college this year ($40,000 per year, indexed by inflation, plus 2% for six years).

The couple will pay expenses that exceed the college savings plan

The couple anticipates wedding expenses of $50,000 upon their daughter’s graduation

From P&L to Portfolio Bernstein.com

Case Study: Excess Planning—Business Facts

69

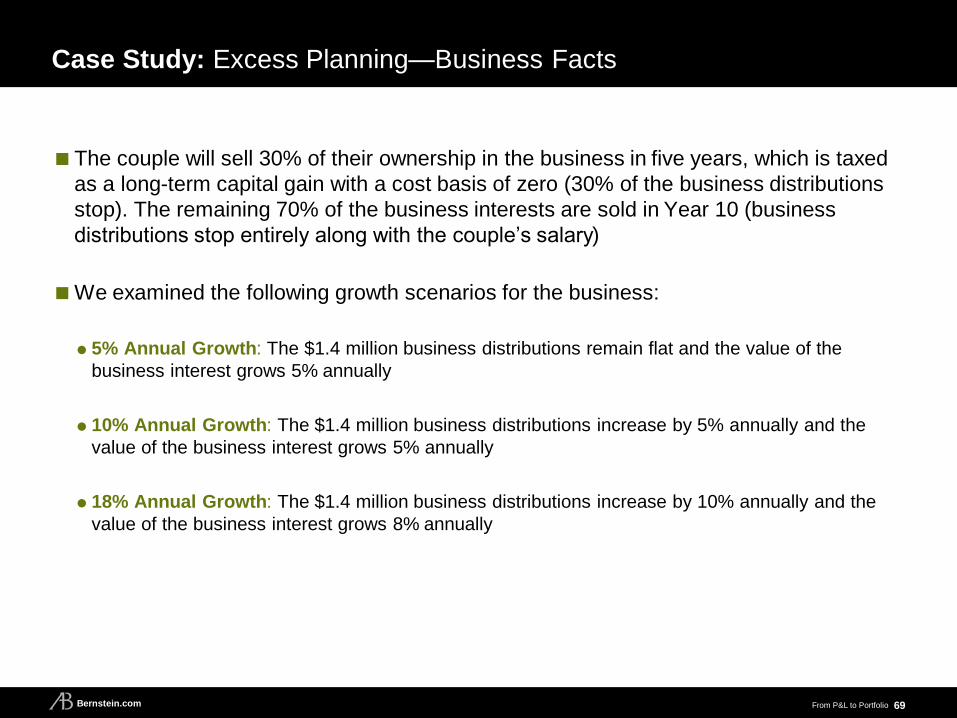

The couple will sell 30% of their ownership in the business in five years, which is taxed

as a long-term capital gain with a cost basis of zero (30% of the business distributions

stop). The remaining 70% of the business interests are sold in Year 10 (business

distributions stop entirely along with the couple’s salary)

We examined the following growth scenarios for the business:

5% Annual Growth: The $1.4 million business distributions remain flat and the value of the

business interest grows 5% annually

10% Annual Growth: The $1.4 million business distributions increase by 5% annually and the

value of the business interest grows 5% annually

18% Annual Growth: The $1.4 million business distributions increase by 10% annually and the

value of the business interest grows 8% annually

From P&L to Portfolio Bernstein.com

No Wealth Transfer: Distribution of 40-Year Family Wealth*

40/60 Portfolio for G1 After Spending and Taxes in Typical Markets (Nominal)

Bernstein is not a legal, tax or estate advisor. Investors should consult with professionals in those areas as appropriate before making any decisions.

*Median results. Assumes the grantor’s assets are invested 40% globally diversified stocks and 60% intermediate term bonds. Assumes that the spouses die in the same year, and

that $5 million, indexed for inflation, per person, is exempt from estate taxes less any gifts made during life. The remaining estate is taxed using a 35% estate tax rate. See Notes on

Estate Transfer and Taxation at the end of this presentation for further details. Based on Bernstein estimates of the range of returns for the applicable capital markets over the

duration of the analysis. Data do not represent past performance and are not a promise of actual or a range of future results. See Notes on Wealth Forecasting System at the

You’re Kidding, Right? There Has to Be a Better Way

71

Couple makes an $8 million gift of interests in their business to an irrevocable grantor

trust for the benefit of their children

Pro: Couple has a combined $10.24 million applicable lifetime exclusion in 2012 and can

comfortably make gifts without jeopardizing their core portfolio; immediately removes the present

value of the growth of the business from their estate

Con: Uncertainty about future gift and estate tax policies

Other Strategies to Consider:

Discounted sale to children or a trust for their benefit in exchange for a promissory note

Pro: Uses little or no gift tax exclusion and requires little to no gift taxes to be paid; the applicable

federal rates are near historic lows

Con: The principal value of the note remains in the grantor’s estate

Discounted transfer to a grantor retained annuity trust (GRAT)

Pro: Requires no gift tax exclusion to be used when GRAT is zeroed out; Section 7520 rates are

near historic lows

Con: Mortality risk; frequent valuations required

From P&L to Portfolio Bernstein.com

Gift/Estate Strategies Benefit from a Discount

72

Capitalize on the valuation discount, due to illiquidity and lack of control

Assuming transfer of a minority interest. Bernstein does not advise on the value of any discounts; information on discounts was provided by clients’ tax and legal teams.

Source: AllianceBernstein

Grantor

Value of Gift for

Transfer Tax Purposes Discount

$8.0 Million

$6.0 Million

$8 Million

Pre-

Transaction

Gift

$5.2 Million 35%

25%

0%

The couple’s deal team advises them to use a 25% valuation discount, due to illiquidity and lack of marketability

From P&L to Portfolio Bernstein.com

Planning: Distribution of 40-Year Family Wealth*

73

40/60 Portfolio for G1; 80/20 Portfolio for G2** After Spending and Taxes in Typical Markets (Nominal)

Bernstein is not a legal, tax or estate advisor. Investors should consult with professionals in those areas as appropriate before making any decisions.

*Median results. Assumes G1 assets are invested 40% globally diversified stocks and 60% intermediate-term bonds, and G2 assets are invested 80% global stocks and 20% bonds.

Assumes that the spouses die in the same year, and that $5 Million, indexed for inflation, per person, is exempt from estate taxes less any gifts made during life. The remaining

estate is taxed using a 35% estate tax rate. See Notes on Estate Transfer and Taxation at the end of this presentation for further details.

**G2 portfolio is assumed to be an irrevocable grantor trust for the first 10 years, at which time the trust pays its own taxes. Based on Bernstein estimates of the range of returns for

the applicable capital markets over the duration of the analysis. Data do not represent past performance and are not a promise of actual or a range of future results. See

Notes on Wealth Forecasting System at the end of this presentation for further details.