2009 Global Forecasting & Marketing 2009 Global Forecasting & Marketing Conference Conference Hilton Orlando Hilton Orlando Orlando Orlando , FL , FL Manufacturing Outlook for the Manufacturing Outlook for the Orthopedic Device Market Orthopedic Device Market Consulting™ Global Forecasting & Marketing Conference – October 21-22, 2009 – Orlando, FL

Transcript

2009 Global Forecasting & Marketing2009 Global Forecasting & Marketing ConferenceConference

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic Market The Orthopedic Market --

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

FactsFactsMusculoskeletal conditions (150 diseases) are among the most costly illnesses to treat ($254 billion in the U.S.)One in 5 adults in the U.S and one in 10 Canadians suffer with osteoarthritis (OA)Knee osteoarthritis is as disabling as any cardiovascular disease (except stroke)More than 50 million fractures occur worldwide every year32% of people over 18 are limited in their activity due to chronic back painCost to treat back pain conditions exceed $100 billion/year worldwide

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Marketplace vs. DemographicsMarketplace vs. Demographics

Consulting™

US-Europe-JapanROW

US-Europe-JapanROW

Population Market Distribution

82%

18%

82%

18%

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

DemographicsDemographics: volume : volume –– worldwide, life style (worldwide, life style (““Baby Baby ZoomersZoomers””))New Products / TechnologiesNew Products / Technologies: US, Europe, Japan: US, Europe, JapanNew Surgical TechniquesNew Surgical Techniques: US, Europe, Japan (MIS, CAS, : US, Europe, Japan (MIS, CAS, Robotics)Robotics)New MaterialsNew MaterialsRevision SurgeryRevision Surgery: (mostly Western World): (mostly Western World)Spinal SurgerySpinal Surgery: huge demand worldwide: huge demand worldwideTraumaTrauma: regular growth: regular growth““GlobesityGlobesity””Availability of informationAvailability of information: Web, DTC Ads,: Web, DTC Ads,Rapid development of certain countriesRapid development of certain countries (China, India, etc.)(China, India, etc.)

Consulting™

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Cost ContainmentCost Containment pressure on healthcare systems worldwidepressure on healthcare systems worldwideUncertainties around Uncertainties around availability and increasing cost of raw availability and increasing cost of raw materialsmaterialsPreventive measures and prescription of Preventive measures and prescription of nonnon--surgical surgical treatments treatments reduce number of procedures reduce number of procedures Uncertainty in Uncertainty in reimbursement of new products/technologiesreimbursement of new products/technologiesCost of R&D and regulatory constraintsCost of R&D and regulatory constraints impedes/delay the impedes/delay the introduction of new productsintroduction of new productsIntense competitionIntense competition requires a high level of product requires a high level of product differentiation and shorten product life cycledifferentiation and shorten product life cycle

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

2008 Worldwide Sales ($billion) by Segment & Region2008 Worldwide Sales ($billion) by Segment & Region

Consulting™

SegmentSegment U.S.U.S. ExEx--U.S.U.S. TotalTotal Change Change vs. 2007vs. 2007

Total MarketTotal Market $21.7$21.7 $14.0$14.0 $35.7$35.7 9.9%9.9%

Change vs. 2007Change vs. 2007(Source: Orhoworld Inc.)

9.4%9.4% 10.6%10.6% 9.9%9.9%

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

--

Growth by SegmentGrowth by Segment

Consulting™

0

2

4

6

8

10

12

14

16

1999

2001

2003

2005

2007

2009

2011

Reconstruction

Trauma

Spinal

Arthro/Soft Tissuerepair

Orthobiologics

Others

CAGR:13.3%

Source: JP Consulting/Orthoworld

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

(1)(1) Spine/CMF OnlySpine/CMF Only(2)(2) Includes Soft Tissue RepairIncludes Soft Tissue Repair(3)(3) Excludes DentalExcludes Dental(4)(4) Excludes non Ortho ProductsExcludes non Ortho Products

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Others: Includes more than 100 companies

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

2008 Worldwide Joint Reconstruction Sales 2008 Worldwide Joint Reconstruction Sales Revenue by Segment ($ Million)Revenue by Segment ($ Million)

Consulting™

Knees 6,500Hips 5,400

Other Joints 300

Shoulders500

KneesHipsShouldersOther Joints

Source: Knowledge Enterprises

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Trends by SegmentTrends by Segment

ReconstructionReconstructionMature market Mature market (except for shoulder and upper extremity)(except for shoulder and upper extremity)Will enjoy steady growth Will enjoy steady growth (7 (7 –– 9% CAGR) over next 5 years9% CAGR) over next 5 yearsHip and Knees becoming commodity products Hip and Knees becoming commodity products Knees: Outpacing Hips Knees: Outpacing Hips (driven by (driven by ““GlobesityGlobesity””))Pressure on prices worldwidePressure on prices worldwideMajor consolidation process Major consolidation process is (almost) overis (almost) overMore and more need for differentiation More and more need for differentiation on the on the manufacturer side, but based upon existing technologiesmanufacturer side, but based upon existing technologiesMIS difficult to implement MIS difficult to implement due to type/size of implantsdue to type/size of implantsCAS/Robotic will boost number of surgeries CAS/Robotic will boost number of surgeries helping helping surgeon trainingsurgeon training

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

2008 Joint Reconstruction Procedures by Product & Region2008 Joint Reconstruction Procedures by Product & Region

Other JointsOther Joints 121,000121,000 29,00029,000 45,00045,000 35,00035,000 12,00012,000

Source: Medtech Insight / JP Consulting

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

2008 Worldwide Joint Reconstruction Sales 2008 Worldwide Joint Reconstruction Sales History & 3 Year ForecastHistory & 3 Year Forecast

Consulting™

Source: Knowledge Enterprises/JP Consulting

02468

10121416

1999 2001 2003 2005 2007 2009 2011

$Billion$Billion

CAGR: 12.2%

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Joint Reconstruction SegmentsJoint Reconstruction Segments U.S Forecast (Units in 000) 2008U.S Forecast (Units in 000) 2008--20122012

Consulting™

Source: Medtech Insight

6029

6836

7641

8445

9351

0

100

200

300

400

500

600

700

800

900

1000

2008 2009 2010 2011 2012

HipsKneesShouldersSmall Joints

Global CAGR:7.40%

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

2008 Worldwide Trauma Sales by Segment ($ MM)2008 Worldwide Trauma Sales by Segment ($ MM)

Consulting™

940 (19.2%)378 (7.8%)

1,220 (24.9%)

1,350 (27.5%)1,012 (20.6%)

External Fixation

Plates/Screws

IM Nails

Hip Screws (Fractures)

Pins/Screws (small bones)

Source: JP Consulting

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

$4.9Billion

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Trends by SegmentTrends by SegmentTraumaTrauma

Mature market Mature market Many implants have been commodity Many implants have been commodity products for a long products for a long timetimeInnovation Innovation in the upper extremity segment (small bones)in the upper extremity segment (small bones)Advancements in plates Advancements in plates (locking plates)(locking plates) and nailsand nailsDevelopment of nonDevelopment of non--metal implants: metal implants: bioresorbable bioresorbable (Polylactic(Polylactic--polyglycolic), composites, polymers (PEEK)polyglycolic), composites, polymers (PEEK)Will enjoy growth in the low double digit range for the Will enjoy growth in the low double digit range for the next 5 years next 5 years (Osteoporosis, China boosting # of traffic (Osteoporosis, China boosting # of traffic accidents)accidents)Pressure on prices Pressure on prices will continuewill continue

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

ExEx--US and U.S. Trauma Procedures / ForecastUS and U.S. Trauma Procedures / Forecast Procedures (000) / $ (MM)Procedures (000) / $ (MM)

Consulting™Source: Windhover Information / JP Consulting

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

US-Procedures

US ($) Ex-US-Procedures

Ex-US ($)

200720082009201020112012

CAGR: 4.2% CAGR: 4.2%

CAGR: 7.3%

CAGR: 7.3%

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

2008 Worldwide and US Spine Procedures2008 Worldwide and US Spine Procedures

Source: Windhover Information / JP Consulting~1MM Procedures

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

US and ExUS and Ex--US Spine Procedures ForecastUS Spine Procedures Forecast

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

ExEx--US and U.S. Spine Sales Forecast ($MM)US and U.S. Spine Sales Forecast ($MM)

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Trends by SegmentTrends by SegmentSpineSpine

Growing MarketGrowing MarketWill enjoy growth in the double digit range Will enjoy growth in the double digit range for the next 5 for the next 5 years (the most prevalent medical disorder in years (the most prevalent medical disorder in industrialized societies)industrialized societies)Prices will remain high Prices will remain high although slightly decliningalthough slightly decliningIncreased adoption of MIS/CAS. Increased adoption of MIS/CAS. Future growth will come with 2Future growth will come with 2ndnd generation discs generation discs (non (non metal nucleus replacement), revision products, facet metal nucleus replacement), revision products, facet replacementreplacementDevelopment of nonDevelopment of non--metal implants: metal implants: bioresorbable bioresorbable (Polylactic(Polylactic--polyglycolic), composites, polymers (PEEK), polyglycolic), composites, polymers (PEEK), biogels biogels

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic MarketThe Orthopedic Market

Main Players by Segment / Market ShareMain Players by Segment / Market Share

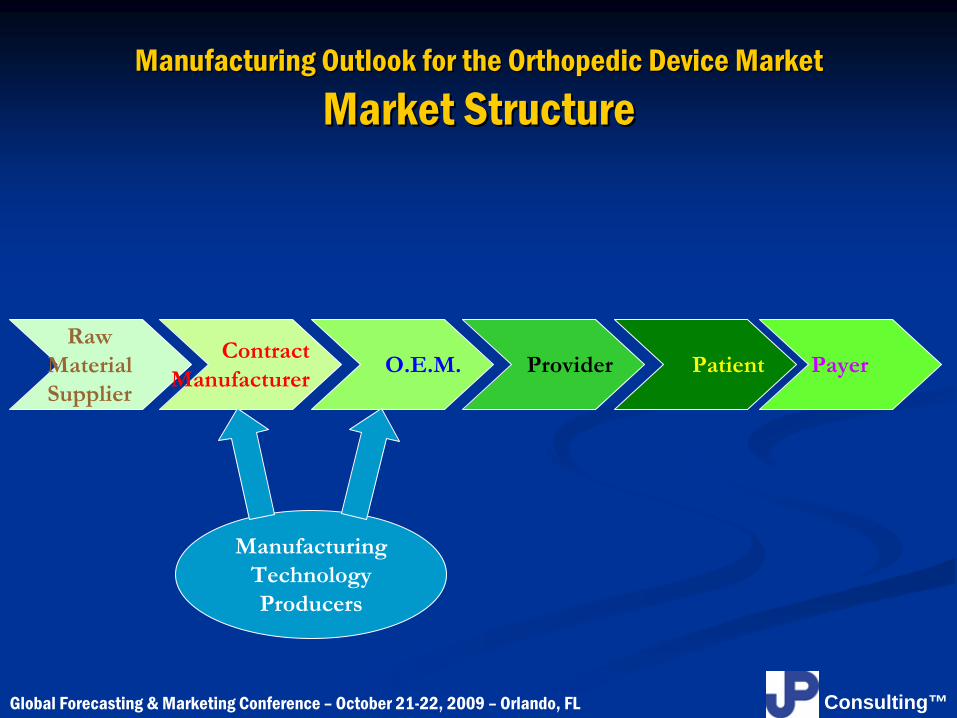

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Market StructureMarket Structure

Consulting™

RawMaterialSupplier

ContractManufacturer

O.E.M. PayerProvider Patient

ManufacturingTechnologyProducers

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic IndustryThe Orthopedic Industry

FDA would enforce compliance with QSR (former GMPs) FDA would enforce compliance with QSR (former GMPs) with both with both OEMs and Contract ManufacturersOEMs and Contract ManufacturersISO would also enforce compliance ISO would also enforce compliance with bothwith both

After 2007After 2007FDA is enforcing compliance with QSR FDA is enforcing compliance with QSR with OEMs onlywith OEMs onlyOEMs are held responsible OEMs are held responsible for compliance of their suppliers with QSRfor compliance of their suppliers with QSRISO keeps enforcing compliance ISO keeps enforcing compliance with both OEMs and Supplierswith both OEMs and SuppliersOEMs have been strongly pushing suppliers to comply with the samOEMs have been strongly pushing suppliers to comply with the same e level of compliance as their own, leading for example most suppllevel of compliance as their own, leading for example most suppliers iers to comply with ISO 13485to comply with ISO 13485

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market The Orthopedic IndustryThe Orthopedic Industry

Implant ManufacturingImplant ManufacturingSome processes are mostly outsourcedSome processes are mostly outsourced(Forging, Casting, Coating, Sterilization, etc.)(Forging, Casting, Coating, Sterilization, etc.)

Some OEMs tend to retain a maximum of work in house Some OEMs tend to retain a maximum of work in house (Synthes, Biomet) whereas some, like DePuy, Medtronic tend (Synthes, Biomet) whereas some, like DePuy, Medtronic tend to outsource more and more and sell plants to suppliers (4 to outsource more and more and sell plants to suppliers (4 recently)recently)Less offLess off--shore low labor cost outsourcing shore low labor cost outsourcing compared to compared to instruments instruments Main Processes: Main Processes: Forging, Casting, Milling, Coating, Polishing, Forging, Casting, Milling, Coating, Polishing, Grinding, Wire EDMGrinding, Wire EDMProprietary processes are of course Proprietary processes are of course performed in houseperformed in house25% are outsourced by OEMs25% are outsourced by OEMs

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Example of Hip ComponentsExample of Hip Components

Consulting™

Modular Hip Stem

Ceramic-CeramicAcetabular Cup

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Knee ComponentsExamples of Knee Components

Consulting™

Total Knee

Patella

Unicondylar

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Tibial Tray

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Upper & Lower Extremities ImplantsExamples of Upper & Lower Extremities Implants

Consulting™

Shoulder Elbow

Ankle

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Small Bones ImplantsExamples of Small Bones Implants

Consulting™

Wrist

Radial Head

Finger Joint

Great Toe Joint

Staple

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Trauma ImplantsExamples of Trauma Implants

Consulting™

External FixatorCortical Screw

Cancellous ScrewCranial Mesh

Locking PlatePlate for Wrist Fracture

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Spinal ImplantsExamples of Spinal Implants

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market NonNon--Metal Components / ImplantsMetal Components / Implants

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Instruments ManufacturingInstruments Manufacturing

Many types of instrumentsMany types of instrumentsProcedure Related: Procedure Related: Impactors, Cutting Guides, Alignment Impactors, Cutting Guides, Alignment Guides, Screw Drivers, Sizing Guides, Rod Cutters, Holders, Guides, Screw Drivers, Sizing Guides, Rod Cutters, Holders, Planers, Templates, etcPlaners, Templates, etcOrthopedic Surgery Related: Orthopedic Surgery Related: Mallets, Handles, Reamers, Mallets, Handles, Reamers, Broaches, Blades, Awls, Drill bits, Taps, Bone Mills, Rongeurs, Broaches, Blades, Awls, Drill bits, Taps, Bone Mills, Rongeurs, Osteotomes, Chucks, etc.Osteotomes, Chucks, etc.General Instruments: General Instruments: Retractors, Distractors, Scissors, Retractors, Distractors, Scissors, Forceps, Curettes, Spreaders, Clamps, etcForceps, Curettes, Spreaders, Clamps, etcPower Instrument Systems: Power Instrument Systems: Drills, SawsDrills, Saws

55% are outsourced by OEMs55% are outsourced by OEMs

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of InstrumentsExamples of Instruments

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of InstrumentsExamples of Instruments

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of InstrumentsExamples of Instruments

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Power Instrument SystemsExamples of Power Instrument Systems

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Delivery SystemsDelivery Systems

Trays and ContainersTrays and ContainersFunction: Deliver sterilized instruments/certain Function: Deliver sterilized instruments/certain implants to the O.R.implants to the O.R.Materials: aluminum, various polymersMaterials: aluminum, various polymersMain Mfg Processes: metal forming, molding, Main Mfg Processes: metal forming, molding, extrusion, ink jet printing, assemblyextrusion, ink jet printing, assembly90% are outsourced by OEMs90% are outsourced by OEMs

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Examples of Delivery SystemsExamples of Delivery Systems

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Major Manufacturing Processes in OrthopedicsMajor Manufacturing Processes in Orthopedics

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Common Raw Materials used in OrthopedicsCommon Raw Materials used in Orthopedics

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market More Recent Materials used in OrthopedicsMore Recent Materials used in Orthopedics

Manufacturing Outlook for the Orthopedic Device Market Manufacturing Outlook for the Orthopedic Device Market Manufacturing Spending (2008)Manufacturing Spending (2008)

Consulting™

$6,50073%

$2,43027%

OEMs

ContractManufacturers

In-House

Outsourced

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Capital ExpenditureCapital Expenditure

Consulting™

Company YearCompany Year 20082008 20072007 20062006 20052005

(*) Capital Expenditures may not consist of purchased manufacturing equipment, research and testing equipment only; They may include computer systems, office furniture and equipment, and plant improvement.

Source: Annual Reports

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market CAPEX TrendsCAPEX Trends

Largest investments in equipment are in the US and Europe Largest investments in equipment are in the US and Europe (Ireland, Switzerland, UK, Germany, France)(Ireland, Switzerland, UK, Germany, France)Both OEM and Suppliers also investing Both OEM and Suppliers also investing in China and Indiain China and IndiaNature of the business (medical), and need for automation Nature of the business (medical), and need for automation require acquisition of require acquisition of most sophisticated and expensive most sophisticated and expensive equipment and renew them often (every 5 equipment and renew them often (every 5 --7 years?)7 years?)Market size assumption: 3 to 4% of Sales? Market size assumption: 3 to 4% of Sales? ($1.0 to ($1.0 to 1.5billion in 2008?)1.5billion in 2008?)Impact of worldwide economy Impact of worldwide economy slow down in 2009 and slow down in 2009 and further on?further on?

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Outsourcing and OEMsOutsourcing and OEMs

Consulting™

Outsourcing is proving to be a vital strategic tool to Outsourcing is proving to be a vital strategic tool to OEMs which core competencies are OEMs which core competencies are R&D, Marketing, R&D, Marketing, and Sales, by:and Sales, by:

Reducing or eliminating investments Reducing or eliminating investments in new production in new production capacity and in employees capacity and in employees Providing manufacturing flexibility enhancing speed to Providing manufacturing flexibility enhancing speed to

market and generating cost reductionmarket and generating cost reductionProviding access to Providing access to highly skilled laborhighly skilled laborProviding access to services and technologies Providing access to services and technologies in the areas of in the areas of

delivery systems and specialized processesdelivery systems and specialized processes

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the OrthopedicManufacturing Outlook for the Orthopedic

Device MarketDevice Market Outsourcing by SegmentsOutsourcing by Segments

Consulting™

0% 20% 40% 60% 80% 100%

Implants

Instruments

Delivery SystemsOutsourcedInsourced

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Outsourcing TrendsOutsourcing Trends

Market expected to increase Market expected to increase from 26% of OEM production from 26% of OEM production costs in 2007 to 33% by 2012costs in 2007 to 33% by 2012Contract Manufacturers are Contract Manufacturers are adding capacity and adding capacity and capabilitiescapabilitiesGradually transforming Gradually transforming into OEMinto OEM’’s strategic partnerss strategic partnersOnOn--going consolidation resulting going consolidation resulting in larger firms that in larger firms that dominate the marketdominate the marketCompetition intensifying Competition intensifying within the US and with low labor within the US and with low labor countries (China, India, Vietnam, Malaysia, etc.)countries (China, India, Vietnam, Malaysia, etc.)Attracting attention and capital Attracting attention and capital from private investorsfrom private investorsVendor consolidation trend is onVendor consolidation trend is on--going going (OEMs reducing (OEMs reducing their vendor basis)their vendor basis)

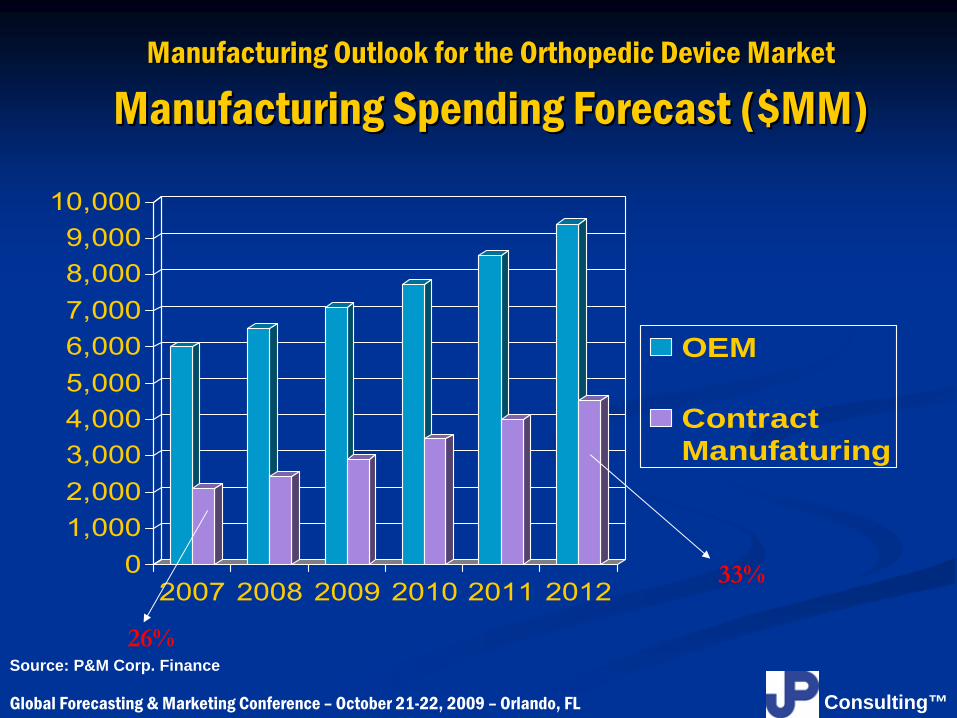

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Manufacturing Spending Forecast ($MM)Manufacturing Spending Forecast ($MM)

Consulting™

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,000

2007 2008 2009 2010 2011 2012

OEM

ContractManufaturing

26%

33%

Source: P&M Corp. Finance

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Outsourcing Market Value by Capabilities ($MM)Outsourcing Market Value by Capabilities ($MM)

Consulting™

255

115

105

1020115

115

105

140

345

115 Forging

Casting

Texturing/Coating

Forming/Machining

Assembly

Polishing

Polymer Machining

Screws

Delivery Systems

Packaging/Ster.

Source: JP Consulting

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Threats to Traditional ManufacturingThreats to Traditional Manufacturing

Slow but progressive replacement of Slow but progressive replacement of metal by new metal by new materialsmaterialsDevelopment of Development of Cartilage transplantCartilage transplantResurfacing of partially damaged cartilage Resurfacing of partially damaged cartilage (Copolymers with (Copolymers with similar properties like UHMWPE + polysaccharidesimilar properties like UHMWPE + polysaccharide

Potential cure for Potential cure for Osteoporosis Osteoporosis (New drugs)(New drugs)

Development of Development of Tissue EngineeringTissue EngineeringDevelopment of Development of Bone SubstitutesBone SubstitutesPotential cure for Potential cure for Osteoarthritis Osteoarthritis (New drugs)(New drugs)

Replacement of machined components Replacement of machined components by molded ones by molded ones (P.E., ceramics, M.I.M,)(P.E., ceramics, M.I.M,)

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Change in ManufacturingChange in Manufacturing

Most facilities have implemented and will continue to Most facilities have implemented and will continue to implement implement cell / lean manufacturingcell / lean manufacturingProcessing new materials Processing new materials (PEEK, Ca/P ceramics, PLLA(PEEK, Ca/P ceramics, PLLA--PGLA, Bone (machined allografts)PGLA, Bone (machined allografts)Highly (mirror) polished implants: Highly (mirror) polished implants: MetalMetal--on Metal and on Metal and Resurfacing heads and cups, Co/Cr bearings (knee, disc, Resurfacing heads and cups, Co/Cr bearings (knee, disc, ankle)ankle)Processing new porous materials: Processing new porous materials: porous Ti, porous porous Ti, porous Tantalum Tantalum with implications on possible debriswith implications on possible debrisProcessing more smaller implants for Processing more smaller implants for MIS, Spine, Small MIS, Spine, Small BonesBones

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Change in ManufacturingChange in Manufacturing

More and more CNC Machining Centers:More and more CNC Machining Centers:Implementing more automation to cut on labor cost Implementing more automation to cut on labor cost and compete with off shore manufacturing and compete with off shore manufacturing competitioncompetitionUnattended / Lights out manufacturing, MultiUnattended / Lights out manufacturing, Multi--Tasking, DoneTasking, Done--inin--One MachiningOne MachiningPalletization, Automatic Feeders and Part CatchersPalletization, Automatic Feeders and Part CatchersHigh Capacity Tool Magazine (240 tools)High Capacity Tool Magazine (240 tools)

Development of Robotics: Development of Robotics: Forging, PolishingForging, Polishing

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Impact of New Materials / New Technologies Impact of New Materials / New Technologies

on Manufacturingon Manufacturing

Introduction of manufacturing processes Introduction of manufacturing processes uncommon in this industry until recentlyuncommon in this industry until recently

Vapor DepositionVapor DepositionNano TechnologiesNano TechnologiesRapid Metal manufacturing (EBM)Rapid Metal manufacturing (EBM)Application of AntiApplication of Anti--Bacterial CoatingsBacterial CoatingsImplementation of Radio Frequency Identification Implementation of Radio Frequency Identification (instruments)(instruments)

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Impact of New Materials / New Technologies Impact of New Materials / New Technologies

on Manufacturingon ManufacturingIncorporation of sensors, microIncorporation of sensors, micro--electronics into implants electronics into implants (discs, rods)(discs, rods)

ee--DiscDisc™™ from from ThekenTheken (Integra)(wirelessly transmits forces of (Integra)(wirelessly transmits forces of motion and loads applied to the disc in postmotion and loads applied to the disc in post--recovery period)recovery period)

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Impact of New Materials / New Technologies Impact of New Materials / New Technologies

on Manufacturingon Manufacturing

Incorporation of sensors, microIncorporation of sensors, micro--electronics into implants electronics into implants (discs, rods)(discs, rods)

Monitoring of the progress of spinal fusion via a sensor placed Monitoring of the progress of spinal fusion via a sensor placed on an implanted metal rod to measure strain (OrthoData) (in on an implanted metal rod to measure strain (OrthoData) (in development)development)

Combination of Polymers and Metals (Composites)Combination of Polymers and Metals (Composites)

Consulting™

Epoch™

stem from Zimmer

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Impact of New Materials / New Technologies Impact of New Materials / New Technologies

on Manufacturingon ManufacturingCAD to Metal (Rapid Metal Manufacturing by Electron Beam CAD to Metal (Rapid Metal Manufacturing by Electron Beam Melting of Metal Powder (ARCAM AB, Sweden)Melting of Metal Powder (ARCAM AB, Sweden)

Consulting™

1. The part is designed in a 3D CAD program.

2. The part is built up in the Electron Beam Melting (EBM) process.

3. The result is a solid metal part.

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Impact of New Materials / New Technologies Impact of New Materials / New Technologies

on Manufacturingon ManufacturingReplacement of metal implants by Ceramic ones Replacement of metal implants by Ceramic ones (Zirconia)(Zirconia)

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market Impact of New Materials / New Technologies Impact of New Materials / New Technologies

on Manufacturingon Manufacturing

Machining of Allograft (Processed Human Bone) or Machining of Allograft (Processed Human Bone) or Xenograft (Animal Bone)Xenograft (Animal Bone)

Machined/Freeze-dried “Biocleansed”/low irradiatedSpinal Fusion Cage and Dowel (from human femur and tibia)Machined Interference

Screw from Bovine Bone

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Consulting™

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market OEMs OEMs ––

Contract Manufacturers Contract Manufacturers ––

MachineMachine--

Tool ProducersTool Producers

M.T ProducersM.T Producers

OEMsOEMs

Contract Contract ManufacturersManufacturers

No consultation between OEM andNo consultation between OEM andSuppliers in the acquisition of M.T.Suppliers in the acquisition of M.T.

Do not forget: OEMs and Suppliers are Do not forget: OEMs and Suppliers are also competitors (mfg costs, knowalso competitors (mfg costs, know--how, etc)how, etc)

Protection of trade secret and proprietaryProtection of trade secret and proprietaryprocesses is essential on both sidesprocesses is essential on both sides

. . . . . . . . . . . . . . . . . . . . .

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market ConclusionConclusion

Orthopedics continues to be Orthopedics continues to be the most dynamic and the most dynamic and fast growing segment of the medical device industryfast growing segment of the medical device industryA highly capital intensive industry A highly capital intensive industry avid of new avid of new technologytechnologyRequires more and more sophisticated, diversified Requires more and more sophisticated, diversified and automated equipment and automated equipment to cut labor cost and to cut labor cost and implement new processes to deal with new implement new processes to deal with new specifications, tolerances and materialsspecifications, tolerances and materials

Manufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market ConclusionConclusion

Consulting™

US and European markets for equipment are US and European markets for equipment are negatively impacted negatively impacted by off shore manufacturingby off shore manufacturing

Technology shifts can be swift especially in terms Technology shifts can be swift especially in terms of of new materials and processes used in implantsnew materials and processes used in implants

Consolidation on both sides (OEMs / Suppliers) Consolidation on both sides (OEMs / Suppliers) generating generating quick changes in the players landscapequick changes in the players landscape

Long term: pharma drugs, tissue engineering and Long term: pharma drugs, tissue engineering and Stem Cell technologies Stem Cell technologies may reduce need for may reduce need for implantsimplants

Global Forecasting & Marketing Conference –

October 21-22, 2009 –

Orlando, FL

Consulting™

Thank You for your Attention!Thank You for your Attention!

2009 Global Forecasting & Marketing Conference2009 Global Forecasting & Marketing Conference Hilton OrlandoHilton Orlando

OrlandoOrlando, FL, FLManufacturing Outlook for the Orthopedic Device MarketManufacturing Outlook for the Orthopedic Device Market