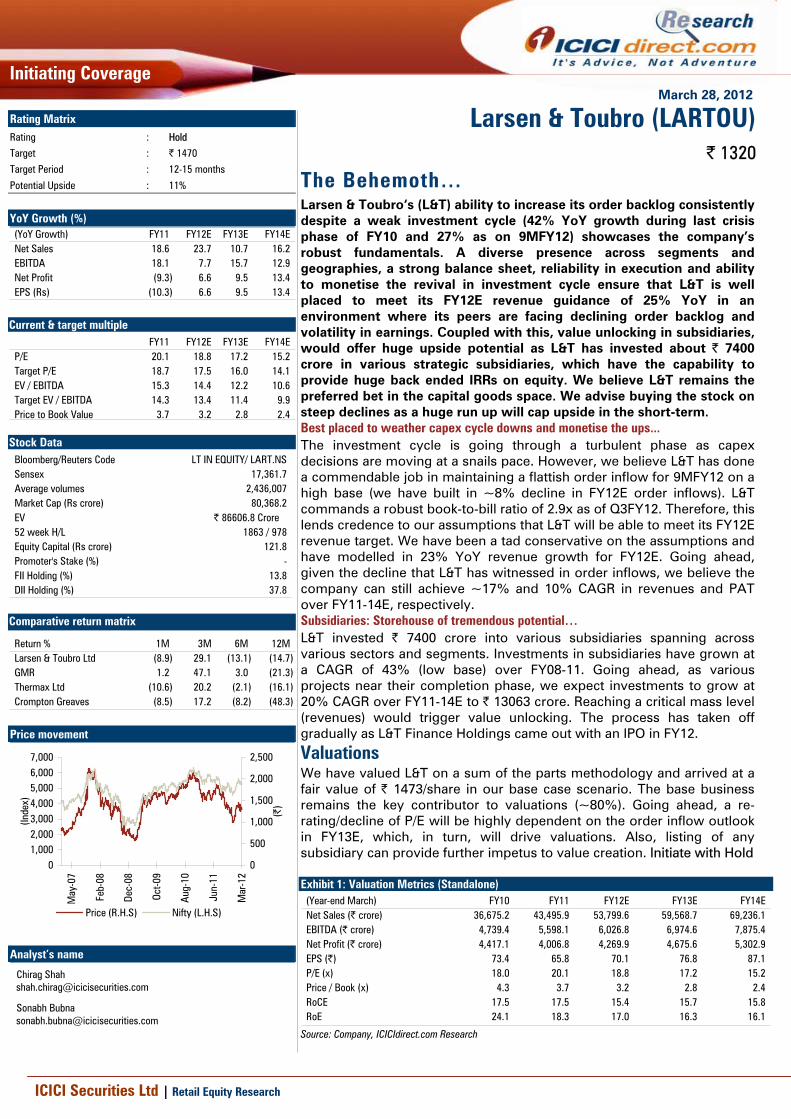

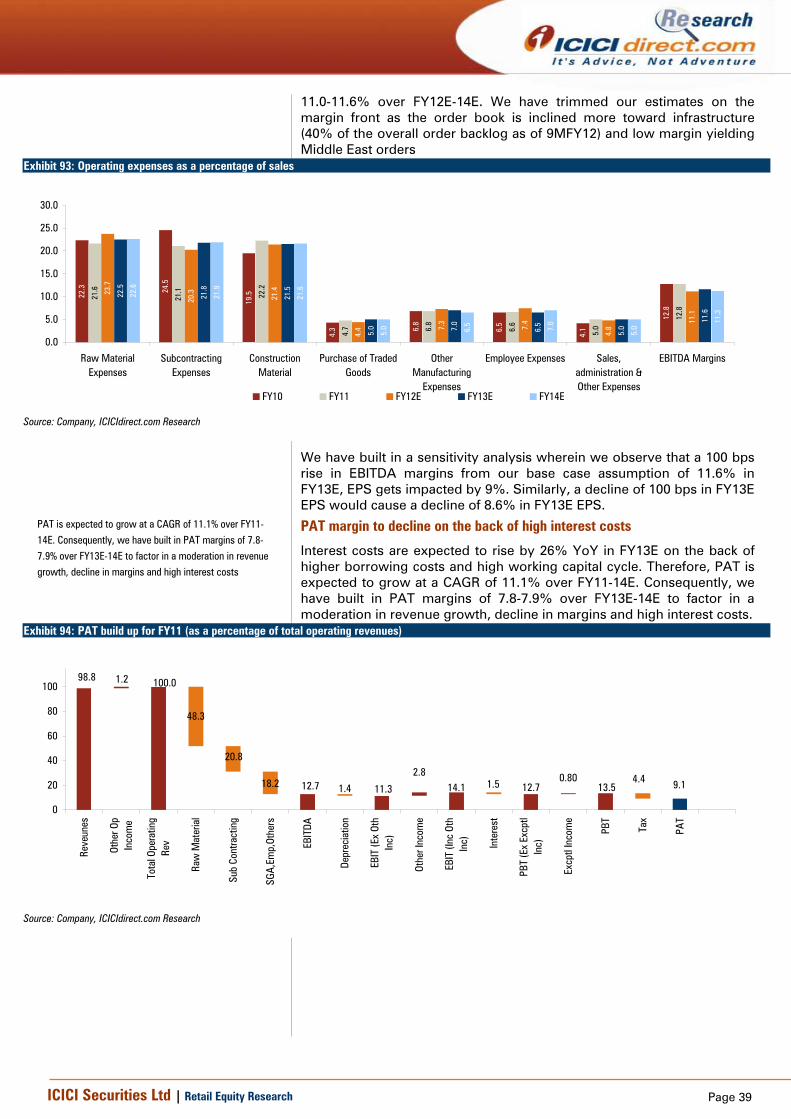

March 28, 2012 Initiating Coverage ICICI Securities Ltd | Retail Equity Research The Behemoth… Larsen & Toubro‘s (L&T) ability to increase its order backlog consistently despite a weak investment cycle (42% YoY growth during last crisis phase of FY10 and 27% as on 9MFY12) showcases the company’s robust fundamentals. A diverse presence across segments and geographies, a strong balance sheet, reliability in execution and ability to monetise the revival in investment cycle ensure that L&T is well placed to meet its FY12E revenue guidance of 25% YoY in an environment where its peers are facing declining order backlog and volatility in earnings. Coupled with this, value unlocking in subsidiaries, would offer huge upside potential as L&T has invested about | 7400 crore in various strategic subsidiaries, which have the capability to provide huge back ended IRRs on equity. We believe L&T remains the preferred bet in the capital goods space. We advise buying the stock on steep declines as a huge run up will cap upside in the short-term. Best placed to weather capex cycle downs and monetise the ups... The investment cycle is going through a turbulent phase as capex decisions are moving at a snails pace. However, we believe L&T has done a commendable job in maintaining a flattish order inflow for 9MFY12 on a high base (we have built in ~8% decline in FY12E order inflows). L&T commands a robust book-to-bill ratio of 2.9x as of Q3FY12. Therefore, this lends credence to our assumptions that L&T will be able to meet its FY12E revenue target. We have been a tad conservative on the assumptions and have modelled in 23% YoY revenue growth for FY12E. Going ahead, given the decline that L&T has witnessed in order inflows, we believe the company can still achieve ~17% and 10% CAGR in revenues and PAT over FY11-14E, respectively. Subsidiaries: Storehouse of tremendous potential… L&T invested | 7400 crore into various subsidiaries spanning across various sectors and segments. Investments in subsidiaries have grown at a CAGR of 43% (low base) over FY08-11. Going ahead, as various projects near their completion phase, we expect investments to grow at 20% CAGR over FY11-14E to | 13063 crore. Reaching a critical mass level (revenues) would trigger value unlocking. The process has taken off gradually as L&T Finance Holdings came out with an IPO in FY12. Valuations We have valued L&T on a sum of the parts methodology and arrived at a fair value of | 1473/share in our base case scenario. The base business remains the key contributor to valuations (~80%). Going ahead, a re- rating/decline of P/E will be highly dependent on the order inflow outlook in FY13E, which, in turn, will drive valuations. Also, listing of any subsidiary can provide further impetus to value creation. Initiate with Hold Exhibit 1: Valuation Metrics (Standalone) (Year-end March) FY10 FY11 FY12E FY13E FY14E Net Sales (| crore) 36,675.2 43,495.9 53,799.6 59,568.7 69,236.1 EBITDA (| crore) 4,739.4 5,598.1 6,026.8 6,974.6 7,875.4 Net Profit (| crore) 4,417.1 4,006.8 4,269.9 4,675.6 5,302.9 EPS (|) 73.4 65.8 70.1 76.8 87.1 P/E (x) 18.0 20.1 18.8 17.2 15.2 Price / Book (x) 4.3 3.7 3.2 2.8 2.4 RoCE 17.5 17.5 15.4 15.7 15.8 RoE 24.1 18.3 17.0 16.3 16.1 Source: Company, ICICIdirect.com Research Larsen & Toubro (LARTOU) | 1320 Rating Matrix Rating : Hold Target : | 1470 Target Period : 12-15 months Potential Upside : 11% YoY Growth (%) (YoY Growth) FY11 FY12E FY13E FY14E Net Sales 18.6 23.7 10.7 16.2 EBITDA 18.1 7.7 15.7 12.9 Net Profit (9.3) 6.6 9.5 13.4 EPS (Rs) (10.3) 6.6 9.5 13.4 Current & target multiple FY11 FY12E FY13E FY14E P/E 20.1 18.8 17.2 15.2 Target P/E 18.7 17.5 16.0 14.1 EV / EBITDA 15.3 14.4 12.2 10.6 Target EV / EBITDA 14.3 13.4 11.4 9.9 Price to Book Value 3.7 3.2 2.8 2.4 Stock Data Bloomberg/Reuters Code LT IN EQUITY/ LART.NS Sensex 17,361.7 Average volumes 2,436,007 Market Cap (Rs crore) 80,368.2 EV | 86606.8 Crore 52 week H/L 1863 / 978 Equity Capital (Rs crore) 121.8 Promoter's Stake (%) - FII Holding (%) 13.8 DII Holding (%) 37.8 Comparative return matrix Return % 1M 3M 6M 12M Larsen & Toubro Ltd (8.9) 29.1 (13.1) (14.7) GMR 1.2 47.1 3.0 (21.3) Thermax Ltd (10.6) 20.2 (2.1) (16.1) Crompton Greaves (8.5) 17.2 (8.2) (48.3) Price movement 0 500 1,000 1,500 2,000 2,500 Mar-12 Jun-11 Aug-10 Oct-09 Dec-08 Feb-08 May-07 (|) 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 (Index) Price (R.H.S) Nifty (L.H.S) Analyst’s name Chirag Shah [email protected]Sonabh Bubna [email protected]

Transcript

March 28, 2012

Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

The Behemoth… Larsen & Toubro‘s (L&T) ability to increase its order backlog consistently despite a weak investment cycle (42% YoY growth during last crisis phase of FY10 and 27% as on 9MFY12) showcases the company’s robust fundamentals. A diverse presence across segments and geographies, a strong balance sheet, reliability in execution and ability to monetise the revival in investment cycle ensure that L&T is well placed to meet its FY12E revenue guidance of 25% YoY in an environment where its peers are facing declining order backlog and volatility in earnings. Coupled with this, value unlocking in subsidiaries, would offer huge upside potential as L&T has invested about | 7400 crore in various strategic subsidiaries, which have the capability to provide huge back ended IRRs on equity. We believe L&T remains the preferred bet in the capital goods space. We advise buying the stock on steep declines as a huge run up will cap upside in the short-term. Best placed to weather capex cycle downs and monetise the ups... The investment cycle is going through a turbulent phase as capex decisions are moving at a snails pace. However, we believe L&T has done a commendable job in maintaining a flattish order inflow for 9MFY12 on a high base (we have built in ~8% decline in FY12E order inflows). L&T commands a robust book-to-bill ratio of 2.9x as of Q3FY12. Therefore, this lends credence to our assumptions that L&T will be able to meet its FY12E revenue target. We have been a tad conservative on the assumptions and have modelled in 23% YoY revenue growth for FY12E. Going ahead, given the decline that L&T has witnessed in order inflows, we believe the company can still achieve ~17% and 10% CAGR in revenues and PAT over FY11-14E, respectively. Subsidiaries: Storehouse of tremendous potential… L&T invested | 7400 crore into various subsidiaries spanning across various sectors and segments. Investments in subsidiaries have grown at a CAGR of 43% (low base) over FY08-11. Going ahead, as various projects near their completion phase, we expect investments to grow at 20% CAGR over FY11-14E to | 13063 crore. Reaching a critical mass level (revenues) would trigger value unlocking. The process has taken off gradually as L&T Finance Holdings came out with an IPO in FY12.

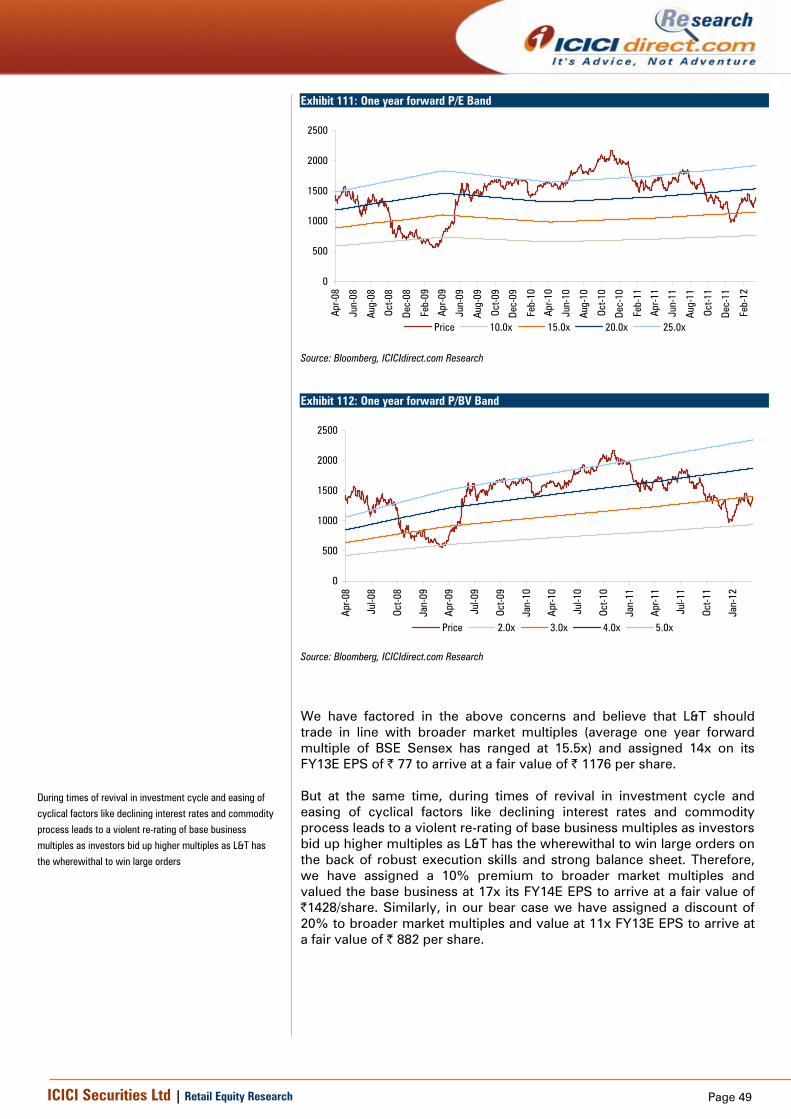

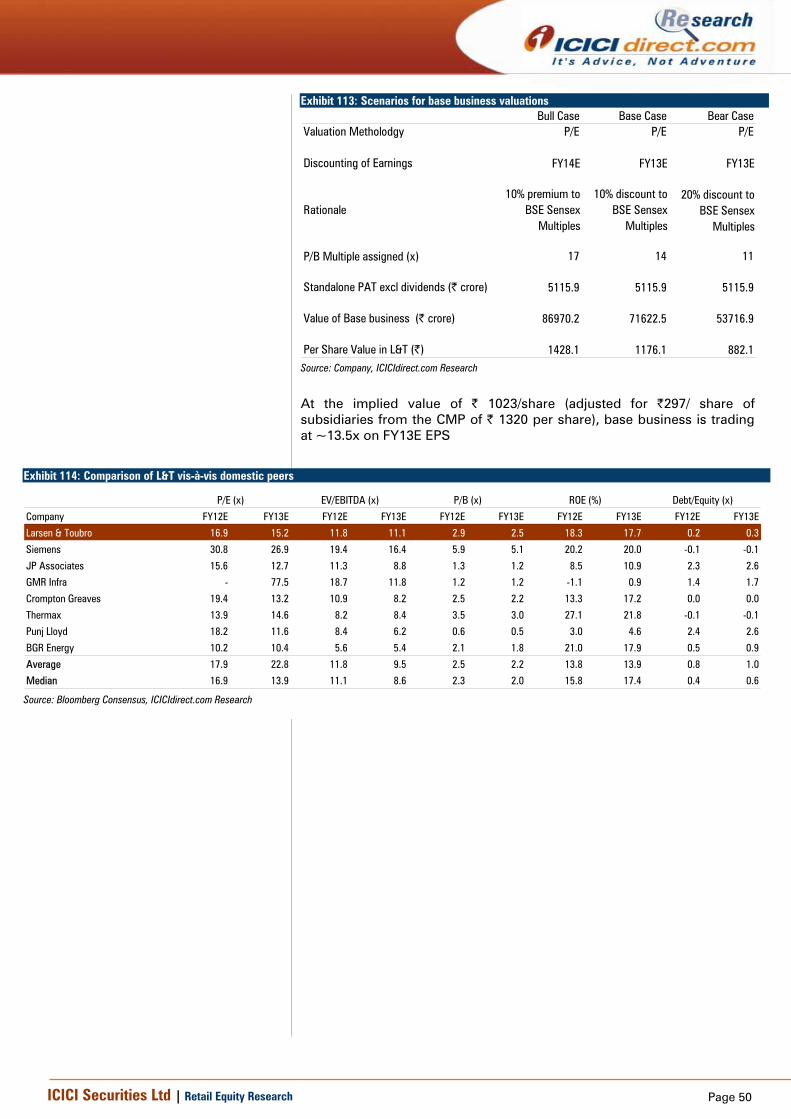

Valuations We have valued L&T on a sum of the parts methodology and arrived at a fair value of | 1473/share in our base case scenario. The base business remains the key contributor to valuations (~80%). Going ahead, a re-rating/decline of P/E will be highly dependent on the order inflow outlook in FY13E, which, in turn, will drive valuations. Also, listing of any subsidiary can provide further impetus to value creation. Initiate with Hold

Page 2ICICI Securities Ltd | Retail Equity Research

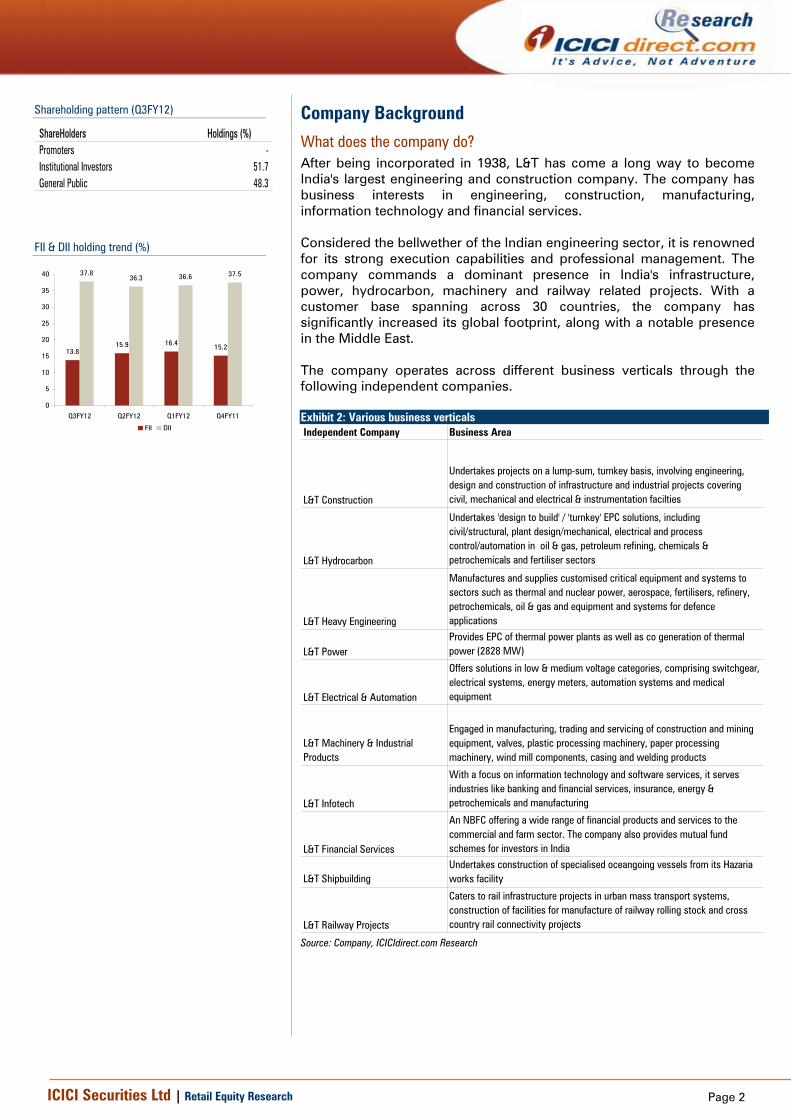

Company Background What does the company do? After being incorporated in 1938, L&T has come a long way to become India's largest engineering and construction company. The company has business interests in engineering, construction, manufacturing, information technology and financial services. Considered the bellwether of the Indian engineering sector, it is renowned for its strong execution capabilities and professional management. The company commands a dominant presence in India's infrastructure, power, hydrocarbon, machinery and railway related projects. With a customer base spanning across 30 countries, the company has significantly increased its global footprint, along with a notable presence in the Middle East. The company operates across different business verticals through the following independent companies. Exhibit 2: Various business verticals Independent Company Business Area

L&T Construction

Undertakes projects on a lump-sum, turnkey basis, involving engineering, design and construction of infrastructure and industrial projects covering civil, mechanical and electrical & instrumentation facilties

L&T Hydrocarbon

Undertakes 'design to build' / 'turnkey' EPC solutions, including civil/structural, plant design/mechanical, electrical and process control/automation in oil & gas, petroleum refining, chemicals & petrochemicals and fertiliser sectors

L&T Heavy Engineering

Manufactures and supplies customised critical equipment and systems to sectors such as thermal and nuclear power, aerospace, fertilisers, refinery, petrochemicals, oil & gas and equipment and systems for defence applications

L&T PowerProvides EPC of thermal power plants as well as co generation of thermal power (2828 MW)

L&T Electrical & Automation

Offers solutions in low & medium voltage categories, comprising switchgear, electrical systems, energy meters, automation systems and medical equipment

L&T Machinery & Industrial Products

Engaged in manufacturing, trading and servicing of construction and mining equipment, valves, plastic processing machinery, paper processing machinery, wind mill components, casing and welding products

L&T Infotech

With a focus on information technology and software services, it serves industries like banking and financial services, insurance, energy & petrochemicals and manufacturing

L&T Financial Services

An NBFC offering a wide range of financial products and services to the commercial and farm sector. The company also provides mutual fund schemes for investors in India

L&T ShipbuildingUndertakes construction of specialised oceangoing vessels from its Hazaria works facility

L&T Railway Projects

Caters to rail infrastructure projects in urban mass transport systems, construction of facilities for manufacture of railway rolling stock and cross country rail connectivity projects

Source: Company, ICICIdirect.com Research

Shareholding pattern (Q3FY12)

ShareHolders Holdings (%)Promoters -Institutional Investors 51.7 General Public 48.3

FII & DII holding trend (%)

13.815.9 16.4 15.2

37.836.3 36.6 37.5

0

5

10

15

20

25

30

35

40

Q3FY12 Q2FY12 Q1FY12 Q4FY11

FII DII

Page 3ICICI Securities Ltd | Retail Equity Research

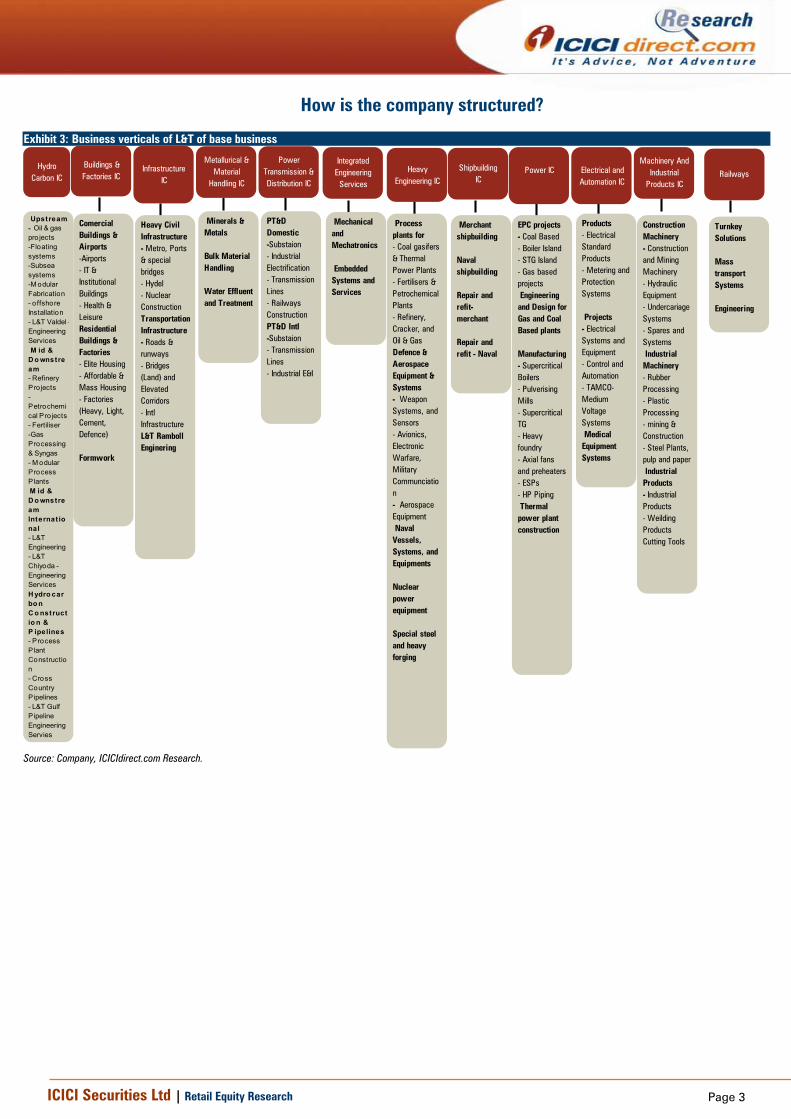

How is the company structured?

Exhibit 3: Business verticals of L&T of base business

Hydro Carbon IC

Upstream- Oil & gas pro jects-Floating systems-Subsea systems-M odular Fabrication- o ffshore Installation- L&T Valdel -Engineering Services M id & D o wnstream- Refinery Pro jects- Petrochemical Pro jects- Fertiliser-Gas Processing & Syngas - M odular Process Plants M id & D o wnstream Internat ional- L&T Engineering- L&T Chiyoda - Engineering ServicesH ydro carbo n C o nstructio n & P ipelines- Process Plant Construction - Cross Country Pipelines- L&T Gulf Pipeline Engineering Servies

Buildings & Factories IC

Comercial Buildings & Airports-Airports- IT & Institutional Buildings- Health & LeisureResidential Buildings & Factories- Elite Housing- Affordable & Mass Housing- Factories (Heavy, Light, Cement, Defence)

Heavy Civil Infrastructure- Metro, Ports & special bridges- Hydel- Nuclear ConstructionTransportationInfrastructure- Roads & runways- Bridges (Land) and Elevated Corridors- Intl InfrastructureL&T Ramboll Enginering

Metallurical & Material

Handling IC

Minerals & Metals

Bulk Material Handling

Water Effluent and Treatment

Shipbuilding IC

Merchant shipbuilding

Naval shipbuilding

Repair and refit- merchant

Repair and refit - Naval

Integrated Engineering

Services

Mechanical and Mechatronics

Embedded Systems and Services

Heavy Engineering IC

Process plants for - Coal gasifers & Thermal Power Plants- Fertilisers & Petrochemical Plants- Refinery, Cracker, and Oil & GasDefence & Aerospace Equipment & Systems- Weapon Systems, and Sensors- Avionics, Electronic Warfare, Military Communciation- Aerospace Equipment Naval Vessels, Systems, and Equipments

Nuclear power equipment

Special steel and heavy forging

Power IC

EPC projects- Coal Based- Boiler Island- STG Island- Gas based projects Engineering and Design forGas and Coal Based plants

Manufacturing- Supercritical Boilers- Pulverising Mills- Supercritical TG- Heavy foundry- Axial fans and preheaters- ESPs- HP Piping Thermal power plant construction

Electrical and Automation IC

Products- Electrical Standard Products- Metering and Protection Systems

Projects- Electrical Systems and Equipment- Control and Automation- TAMCO- Medium Voltage Systems Medical Equipment Systems

Machinery And Industrial

Products IC

Construction Machinery- Construction and Mining Machinery- Hydraulic Equipment- Undercariage Systems- Spares and Systems Industrial Machinery- Rubber Processing- Plastic Processing- mining & Construction- Steel Plants, pulp and paper Industrial Products- Industrial Products- Weilding ProductsCutting Tools

Railways

Turnkey Solutions

Mass transport Systems

Engineering

Source: Company, ICICIdirect.com Research.

Page 4ICICI Securities Ltd | Retail Equity Research

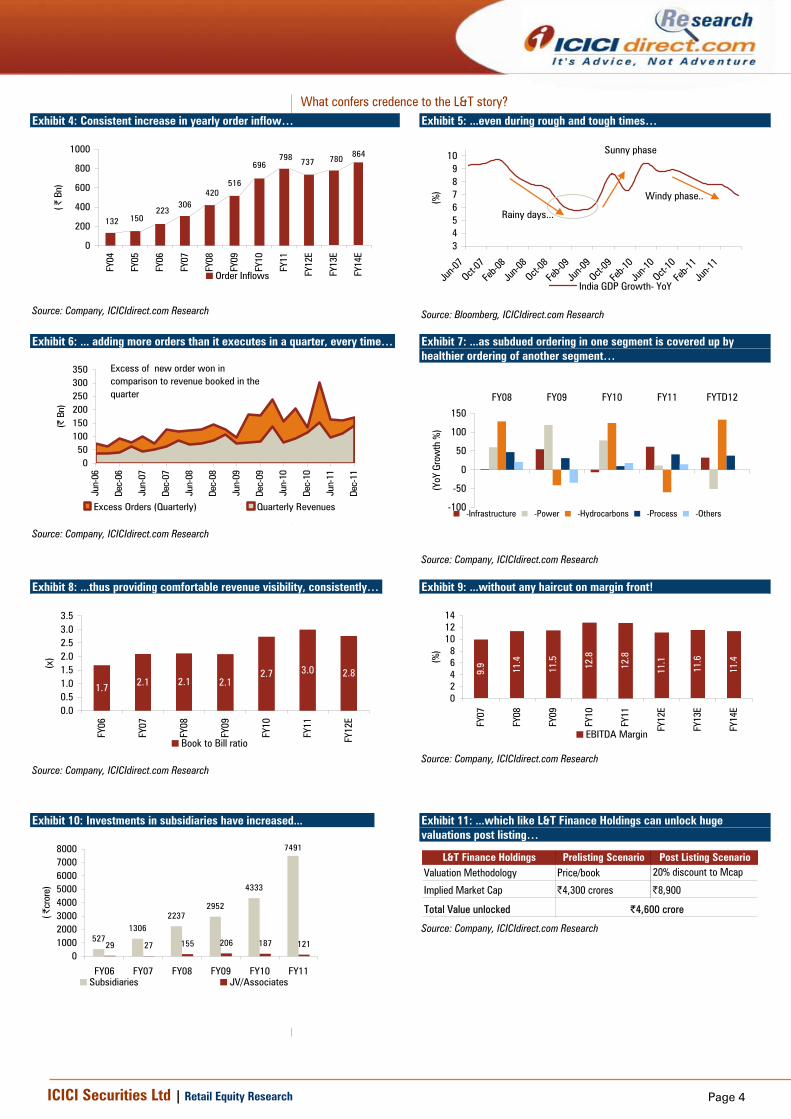

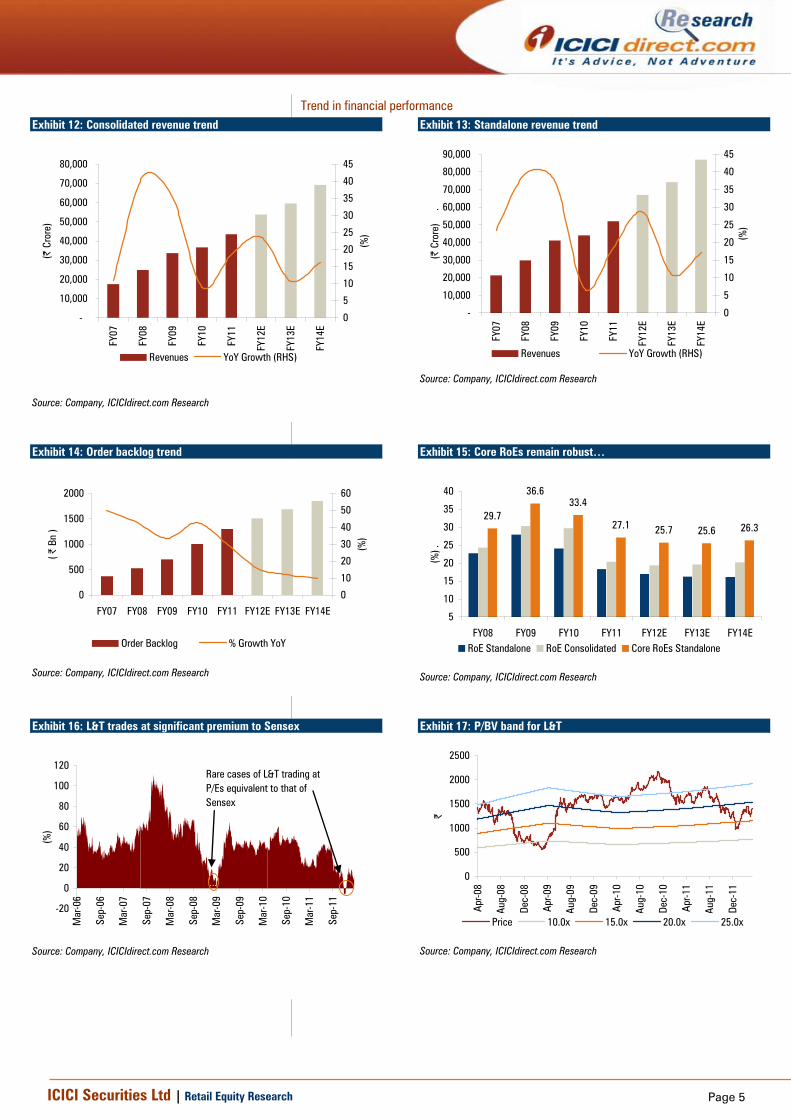

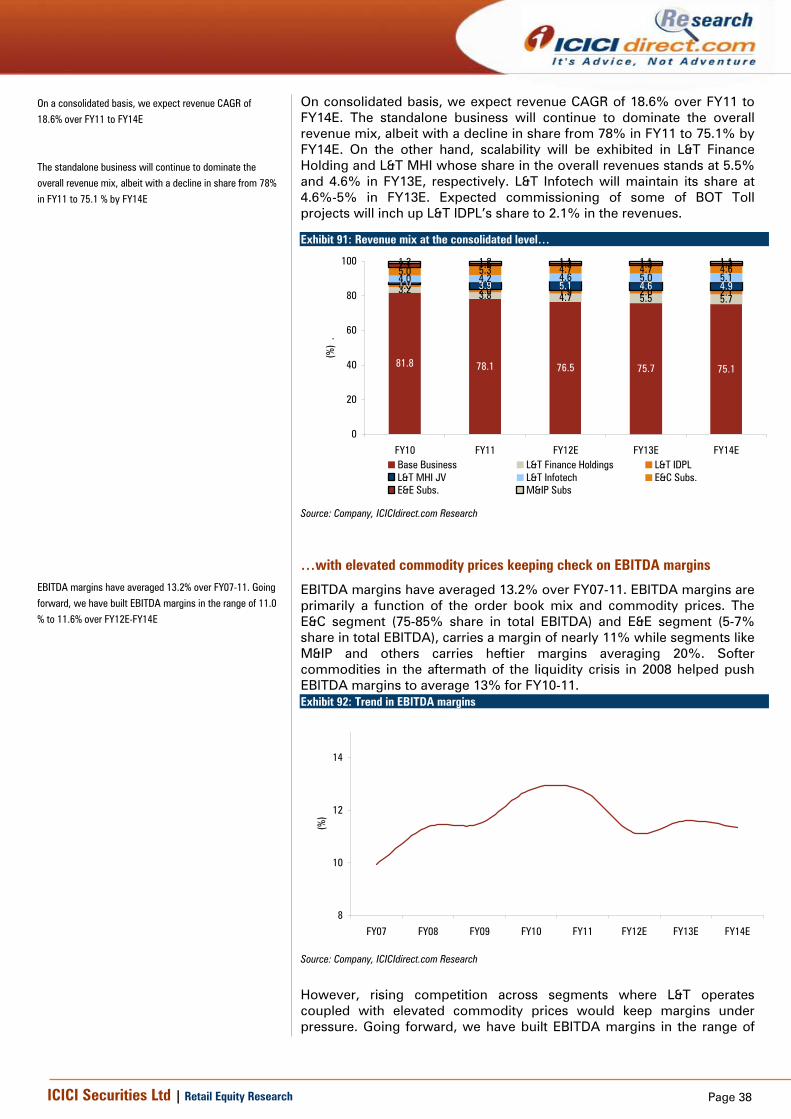

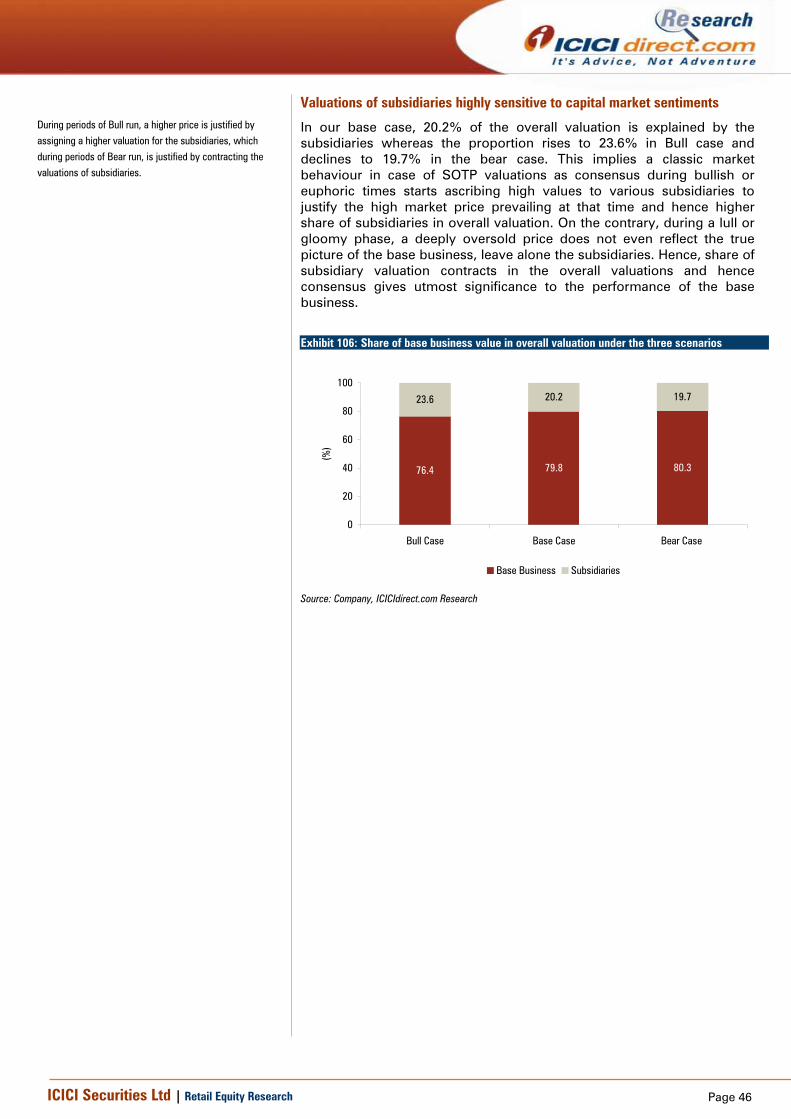

What confers credence to the L&T story? Exhibit 4: Consistent increase in yearly order inflow…

737

132 150223

306420

516

696798 780

864

0

200

400

600

800

1000

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

E

FY13

E

FY14

E

( | B

n)

Order Inflows

Source: Company, ICICIdirect.com Research

Exhibit 5: ...even during rough and tough times…

3456789

10

Jun-0

7Oct-

07

Feb-0

8

Jun-0

8Oct-

08

Feb-0

9

Jun-0

9Oct-

09

Feb-1

0

Jun-1

0Oct-

10

Feb-1

1

Jun-1

1

(%)

India GDP Growth- YoY

Rainy days...

Sunny phase

Windy phase..

Source: Bloomberg, ICICIdirect.com Research

Exhibit 6: ... adding more orders than it executes in a quarter, every time…

050

100150200250300350

Jun-

06

Dec-

06

Jun-

07

Dec-

07

Jun-

08

Dec-

08

Jun-

09

Dec-

09

Jun-

10

Dec-

10

Jun-

11

Dec-

11

(| B

n)

Excess Orders (Quarterly) Quarterly Revenues

Excess of new order won in comparison to revenue booked in the quarter

Source: Company, ICICIdirect.com Research

Exhibit 7: ...as subdued ordering in one segment is covered up by healthier ordering of another segment…

Exhibit 16: L&T trades at significant premium to Sensex

-20

0

20

40

60

80

100

120

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

(%)

Rare cases of L&T trading at P/Es equivalent to that of Sensex

Source: Company, ICICIdirect.com Research

Exhibit 17: P/BV band for L&T

0

500

1000

1500

2000

2500

Apr-0

8

Aug-

08

Dec-

08

Apr-0

9

Aug-

09

Dec-

09

Apr-1

0

Aug-

10

Dec-

10

Apr-1

1

Aug-

11

Dec-

11

|

Price 10.0x 15.0x 20.0x 25.0x

Source: Company, ICICIdirect.com Research

Page 6ICICI Securities Ltd | Retail Equity Research

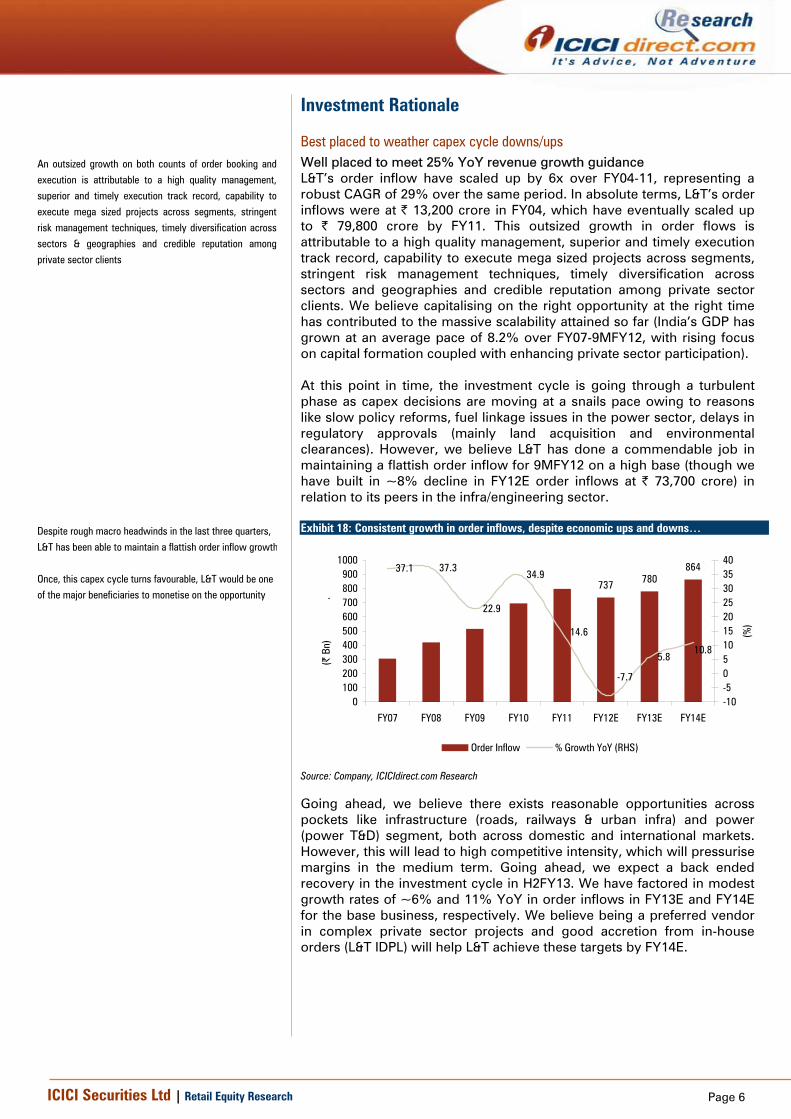

Investment Rationale

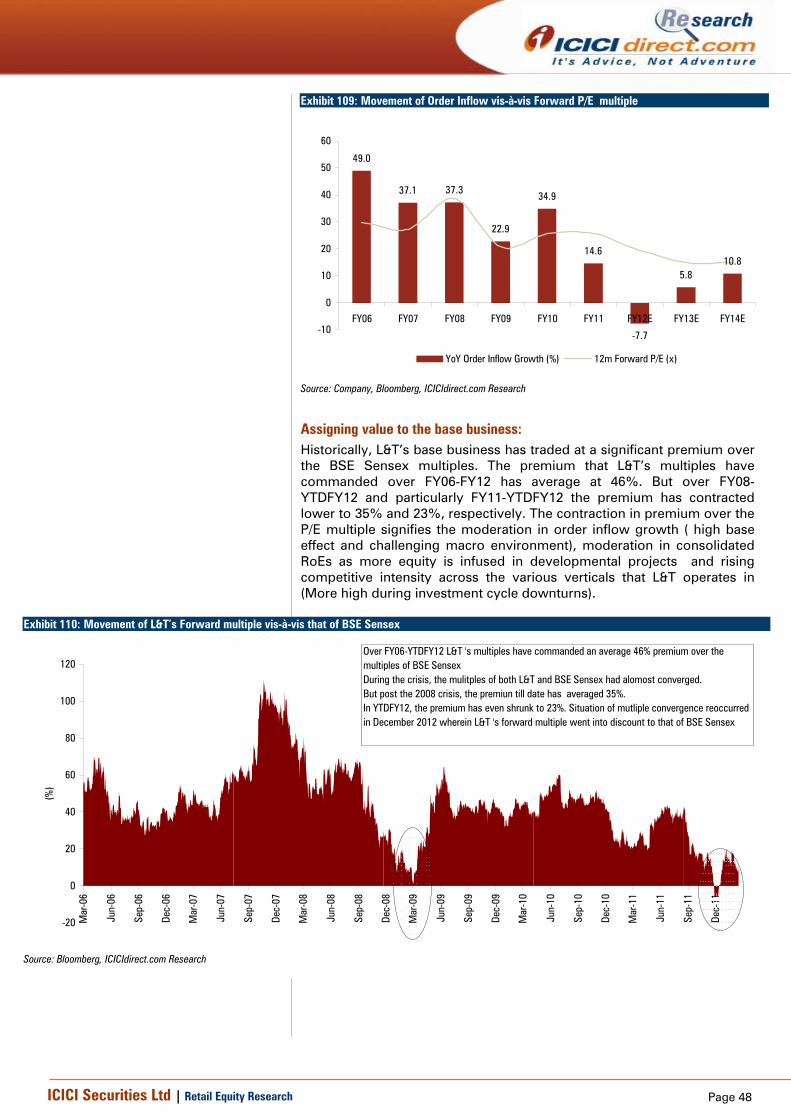

Best placed to weather capex cycle downs/ups Well placed to meet 25% YoY revenue growth guidance L&T’s order inflow have scaled up by 6x over FY04-11, representing a robust CAGR of 29% over the same period. In absolute terms, L&T’s order inflows were at | 13,200 crore in FY04, which have eventually scaled up to | 79,800 crore by FY11. This outsized growth in order flows is attributable to a high quality management, superior and timely execution track record, capability to execute mega sized projects across segments, stringent risk management techniques, timely diversification across sectors and geographies and credible reputation among private sector clients. We believe capitalising on the right opportunity at the right time has contributed to the massive scalability attained so far (India’s GDP has grown at an average pace of 8.2% over FY07-9MFY12, with rising focus on capital formation coupled with enhancing private sector participation). At this point in time, the investment cycle is going through a turbulent phase as capex decisions are moving at a snails pace owing to reasons like slow policy reforms, fuel linkage issues in the power sector, delays in regulatory approvals (mainly land acquisition and environmental clearances). However, we believe L&T has done a commendable job in maintaining a flattish order inflow for 9MFY12 on a high base (though we have built in ~8% decline in FY12E order inflows at | 73,700 crore) in relation to its peers in the infra/engineering sector. Exhibit 18: Consistent growth in order inflows, despite economic ups and downs…

780737

86437.1 37.3

22.9

34.9

14.6

5.810.8

-7.7

0100200300400500600700800900

1000

FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(| B

n)

.

-10-50510152025303540

(%)

Order Inflow % Growth YoY (RHS)

Source: Company, ICICIdirect.com Research

Going ahead, we believe there exists reasonable opportunities across pockets like infrastructure (roads, railways & urban infra) and power (power T&D) segment, both across domestic and international markets. However, this will lead to high competitive intensity, which will pressurise margins in the medium term. Going ahead, we expect a back ended recovery in the investment cycle in H2FY13. We have factored in modest growth rates of ~6% and 11% YoY in order inflows in FY13E and FY14E for the base business, respectively. We believe being a preferred vendor in complex private sector projects and good accretion from in-house orders (L&T IDPL) will help L&T achieve these targets by FY14E.

An outsized growth on both counts of order booking and

execution is attributable to a high quality management,

superior and timely execution track record, capability to

execute mega sized projects across segments, stringent

risk management techniques, timely diversification across

sectors & geographies and credible reputation among

private sector clients

Despite rough macro headwinds in the last three quarters,

L&T has been able to maintain a flattish order inflow growth

Once, this capex cycle turns favourable, L&T would be one of the major beneficiaries to monetise on the opportunity

Page 7ICICI Securities Ltd | Retail Equity Research

Exhibit 19: Book to bill ratio of 2.8x to ensure high double digit revenue growth into FY14E

1.72.1 2.1 2.1

2.7 3.0 2.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY06

FY07

FY08

FY09

FY10

FY11

FY12

E

(x)

Book to Bill ratio

Source: Company, ICICIdirect.com Research

Exhibit 20: Order backlog indicative of revenue growth over FY11-FY14E.

369526.8

703

1002.39

1302.17

15081686

1850

0

200

400

600

800

1000

1200

1400

1600

1800

2000

FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(| B

n)

.

0.0

10.0

20.0

30.0

40.0

50.0

60.0

(%)

.

Order Backlog Growth YoY

Source: Company, ICICIdirect.com Research

L&T commands a book-to-bill ratio of 2.9x as of Q3FY12 and, therefore, lends credence to our assumptions that L&T will be able to meet its FY12E revenue target of 25% YoY. We have been a tad conservative on the assumptions and have modelled in 23% YoY revenue growth for FY12E. Going ahead, given the tepid decline that L&T would witness in order inflows for FY12E coupled with a modest rise in FY13E and FY14E, we have modelled in growth at 11.4% and 16.2% in the base business revenues in FY13E and FY14E, respectively.

Exhibit 21: History of L&T’s guidance vs. achievement

Order Inflow Growth (%) Base Business Revenue Growth (%) EBITDA Margin (%)

Source: Company, ICICIdirect.com Research, Figures marked in Red indicated ICICIdirect Estimates for FY12E(standalone)

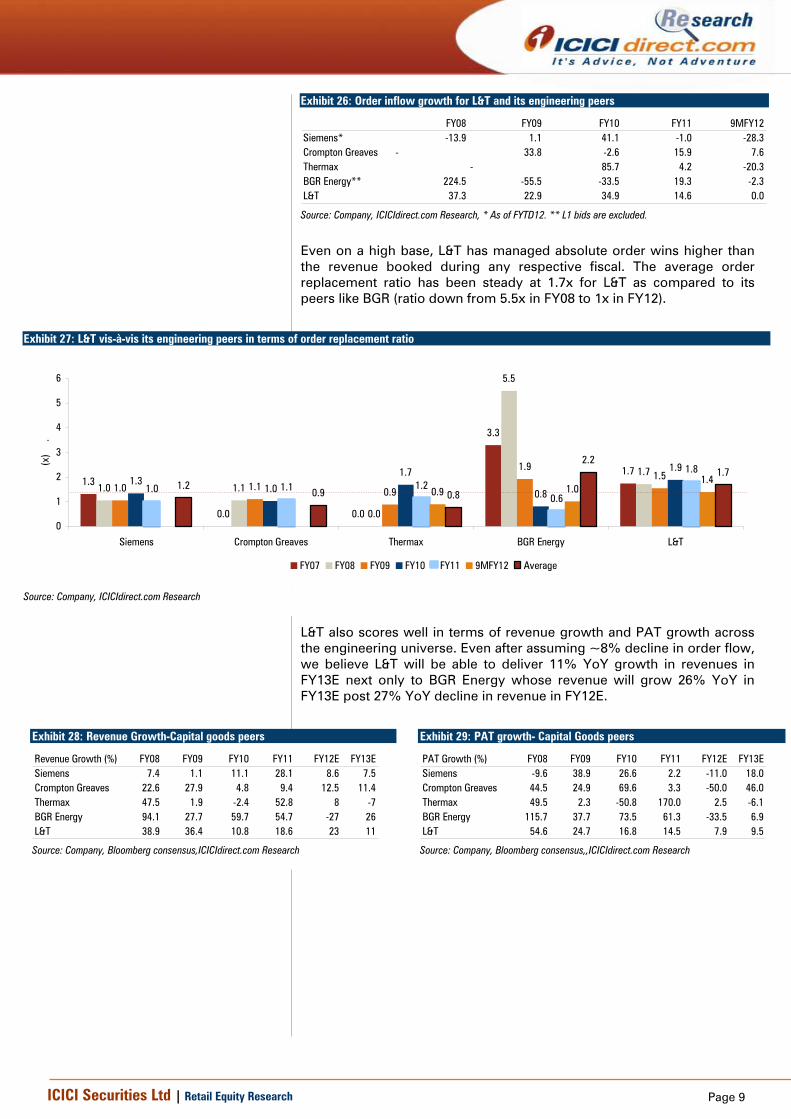

Stands tall across parameters vis-à-vis construction/engineering peers Looking at the various operating matrices of L&T and its construction/engineering peers, we observe that L&T is far superior across parameters such as order inflow growth, revenue growth and working capital management across business cycles. Hence, clearly premium multiples, especially during investment cycle downturns are sustained for L&T vis-à-vis its peers. We have analysed data from FY07-9MYTDFY12, which clearly supports our argument as order inflow growth for players like IVRCL infra, NCC, Simplex and HCC is too lumpy wherein L&T’s order inflows exhibits low lumpiness and, thereby, consistent revenue visibility and growth (refer Exhibit 22 and Exhibit 23).

Page 8ICICI Securities Ltd | Retail Equity Research

Exhibit 22: Order inflow growth for L&T and its construction peers

Even among engineering firms, L&T exhibits consistent operating matrices. The most significant among these parameters are the order inflow growth and order replacement ratio (refer Exhibit 26 and Exhibit 27). Though at absolute levels, inflow growth has declined, the volatility in inflow growth is less compared to peers like BGR Energy, Crompton Greaves and Siemens as degree of business diversification of L&T is significantly higher than its peers, thereby diffusing macro risks in a better way.

Cycles of downturn further exhibit a robust business

model and strong balance sheet of L&T. This is clearly

indicated in the NWC ratio as percentage of sales.

During downturns, L&T’s NWC as percentage of sales

hovers between 16% and 17% whereas peers like

IVRCL, NCC, Simplex and HCC have NWCs ranging

between 30% and 60%

Quality of earnings and growth rates are better for L&T

when compared to its peers (Refer Exhibit 25)

Page 9ICICI Securities Ltd | Retail Equity Research

Exhibit 26: Order inflow growth for L&T and its engineering peers

Source: Company, ICICIdirect.com Research, * As of FYTD12. ** L1 bids are excluded.

Even on a high base, L&T has managed absolute order wins higher than the revenue booked during any respective fiscal. The average order replacement ratio has been steady at 1.7x for L&T as compared to its peers like BGR (ratio down from 5.5x in FY08 to 1x in FY12).

Exhibit 27: L&T vis-à-vis its engineering peers in terms of order replacement ratio

1.3

0.0 0.0

3.3

1.7

1.0 1.1

0.0

5.5

1.7

1.0 1.1 0.9

1.91.51.3

1.0

1.7

0.8

1.9

1.0 1.1 1.20.6

1.8

0.9 1.01.41.2

0.9 0.8

2.21.7

0

1

2

3

4

5

6

Siemens Crompton Greaves Thermax BGR Energy L&T

(x)

.

FY07 FY08 FY09 FY10 FY11 9MFY12 Average

Source: Company, ICICIdirect.com Research

L&T also scores well in terms of revenue growth and PAT growth across the engineering universe. Even after assuming ~8% decline in order flow, we believe L&T will be able to deliver 11% YoY growth in revenues in FY13E next only to BGR Energy whose revenue will grow 26% YoY in FY13E post 27% YoY decline in revenue in FY12E.

Source: Company, Bloomberg consensus,,ICICIdirect.com Research

Page 10ICICI Securities Ltd | Retail Equity Research

Diversified operations provide good hedge during capex downturns L&T’s current order backlog of | 146000 crore (Q3FY12) is highly diversified across segments. Out of the current backlog, the infrastructure segment (roads, buildings & factories, urban infra, airports) comprises 40% of the backlog whereas power (generation & T&D) and process (metals & material handling) segment’s share stands at 29% and 15%, respectively. Hydrocarbons and others (defence, shipbuilding and electronic products), on the other hand, constitute 11% and 5% of the backlog, respectively.

Exhibit 30: Segment wise business activities of L&T

Infrastructure Power Hydrocarbons Process Others

Roads and bridge Power generation Upstream Minerals and metals Shipbuilding

Ports and harbours Power plant equipment Mid and downstream Bulk material handling Defence & aerospace

AirportsElectrification/transmission and

distribution Pipelines Construction and mining equipment

Railways Fertilisers Electronic Products

Buildings and factories Valves Technology service

Urban infra

Water

Source: Company, ICICIdirect.com Research

Comparing the current break up of backlog, the share of the power and infrastructure segment has made significant gains of 18% and 5% to 29% and 40%, respectively, when compared to the average share (FY04-YTDFY12) of 11% and 35%, respectively. On the other hand, the share of hydrocarbons and other segments has faced a loss of 7% and 9% when compared to historical averages (FY04-YTDFY12).

Going ahead, we expect the share of infrastructure to rise to 42% in FY14E from 40% in FY12E (pick-up in road project awards, opportunities in metro projects and mega projects such as DFC and urban infra) as other segments like power (fuel linkage issues, delays in environmental clearances and high competitive intensity though domestic and international T&D projects provide reasonable scope) and process (low capacity utilisations) are going through a rough patch.

Total 70% of the current backlog comes from the infra and power

segments. Going ahead, we expect the share of infrastructure to rise to 42% in FY14E from 40% in FY12E

Page 11ICICI Securities Ltd | Retail Equity Research

Exhibit 31: Trend in share of segment in order backlog

39 36 41 33 36 40 41 42

16 1622 30 32 29 27 25

19 2314 15 12 11 11 12

12 14 16 16 16 15 15 1514 11 7 6 4 5 6 6

0102030405060708090

100

FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(%) .

Infrastructure Power Hydrocarbons Process Others

Source: Company, ICICIdirect.com Research

From a seasonality perspective, order inflows in the infrastructure projects segment have remained relatively consistent as compared to the power and hydrocarbons space where lumpiness in order flows is high. Over FY08-YTD FY12 (18 quarters), segments such as power and hydrocarbons have posted negative quarterly order inflow growth (YoY) seven and nine times, respectively. On the other hand, consistency of infra segment order flows is explained by 14 quarters of positive order inflow growth out of 18 counts.

Exhibit 32: Degree of cyclicality in the various segments with respect to order inflows over FY10-YTDFY12

Though power order inflows had been down in recent quarters, one big EPC order win could make up for lost quarters...

A higher dgree of lumpiness for hydrocarbons orders as capex plans are sensitive to oil prices

Sensitive to overall capex sentiments..

Emerging segments (like defence) for L&T..

Source: Company, ICICIdirect.com Research

Different segments are displaying different sensitivities,

with the infrastructure projects segment remaining

relatively consistent as compared to the power and hydrocarbons space where lumpiness in order flows is high

Page 12ICICI Securities Ltd | Retail Equity Research

Exhibit 33: Positive/negative order inflow growth for segment across Q1FY08-Q3FY12

47

95

9

1412 9

139

02468

101214161820

Infrastructure Power Hydrocarbons Process Others

(No

of Q

uarte

rs)

.Negative growth Positive growth

Source: Company, ICICIdirect.com Research

Our second argument for consistency in segmental order flows is reflected in the slow moving orders in the backlog (10-12% of the backlog as of Q3FY12), which are mainly related to the power and process segments. Hence, with rising thrust on the infrastructure segment in the overall order book, we expect moderation in execution rate to be limited and to keep the growth rate in standalone revenues at 16.8% CAGR over FY11-FY14E.

Exhibit 34: Some slow moving orders in current order backlog (as of 9MFY12) Order Segment Size (| crore) CommentsNabha Power Power Pending fuel linakgesKarchana Power Land acquisition delaysHyderabad Metro Infrastructure - Land acquisition delaysBlast furnace Process

Source: Company, ICICIdirect.com Research

Page 13ICICI Securities Ltd | Retail Equity Research

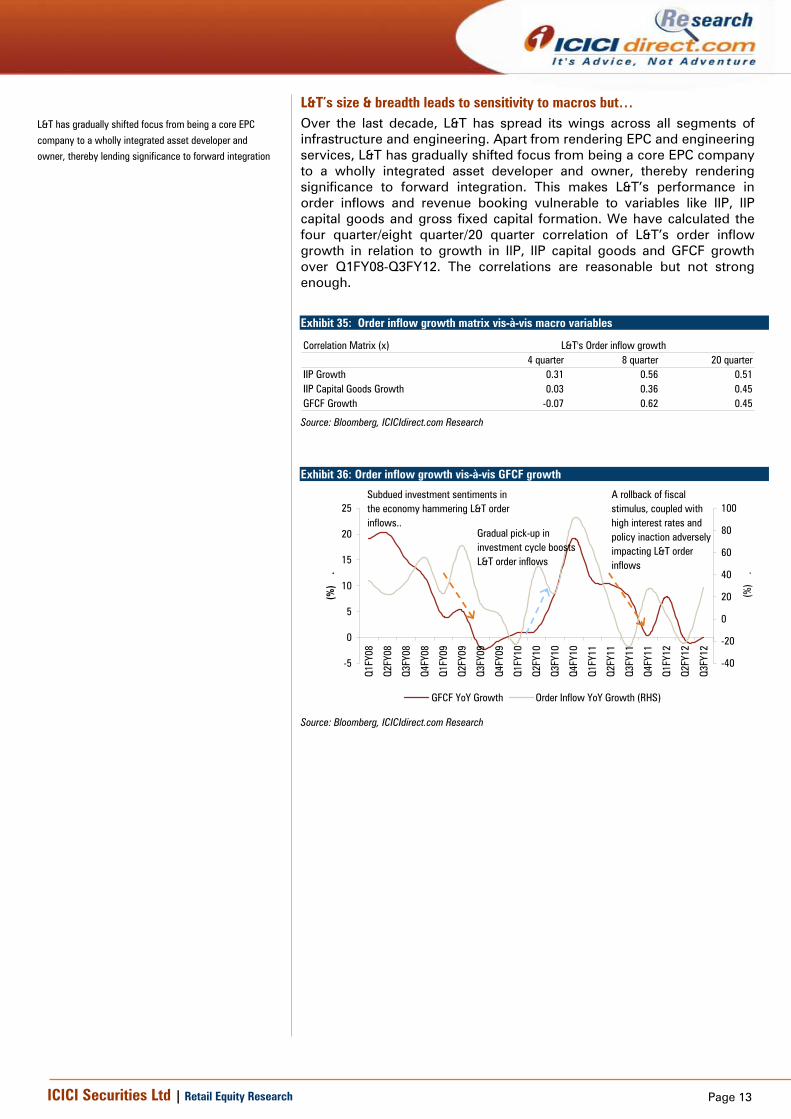

L&T’s size & breadth leads to sensitivity to macros but… Over the last decade, L&T has spread its wings across all segments of infrastructure and engineering. Apart from rendering EPC and engineering services, L&T has gradually shifted focus from being a core EPC company to a wholly integrated asset developer and owner, thereby rendering significance to forward integration. This makes L&T’s performance in order inflows and revenue booking vulnerable to variables like IIP, IIP capital goods and gross fixed capital formation. We have calculated the four quarter/eight quarter/20 quarter correlation of L&T’s order inflow growth in relation to growth in IIP, IIP capital goods and GFCF growth over Q1FY08-Q3FY12. The correlations are reasonable but not strong enough.

Exhibit 35: Order inflow growth matrix vis-à-vis macro variables

Exhibit 36: Order inflow growth vis-à-vis GFCF growth

-5

0

5

10

15

20

25

Q1FY

08

Q2FY

08

Q3FY

08

Q4FY

08

Q1FY

09

Q2FY

09

Q3FY

09

Q4FY

09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11

Q1FY

12

Q2FY

12

Q3FY

12

(%)

.

-40

-20

0

20

40

60

80

100

(%)

.

GFCF YoY Growth Order Inflow YoY Growth (RHS)

Subdued investment sentiments in the economy hammering L&T order inflows..

Gradual pick-up in investment cycle boosts L&T order inflows

A rollback of fiscal stimulus, coupled with high interest rates and policy inaction adversely impacting L&T order inflows

Source: Bloomberg, ICICIdirect.com Research

L&T has gradually shifted focus from being a core EPC

company to a wholly integrated asset developer and owner, thereby lending significance to forward integration

Page 14ICICI Securities Ltd | Retail Equity Research

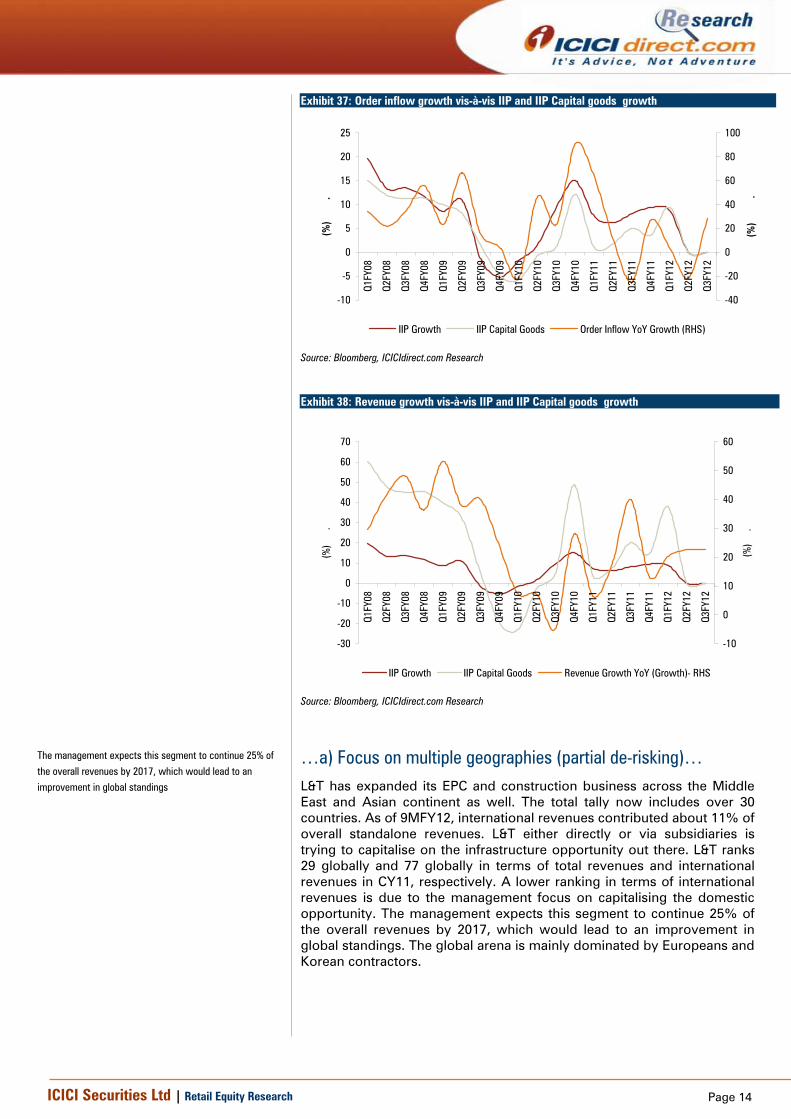

Exhibit 37: Order inflow growth vis-à-vis IIP and IIP Capital goods growth

-10

-5

0

5

10

15

20

25

Q1FY

08

Q2FY

08

Q3FY

08

Q4FY

08

Q1FY

09

Q2FY

09

Q3FY

09

Q4FY

09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11

Q1FY

12

Q2FY

12

Q3FY

12

(%)

.

-40

-20

0

20

40

60

80

100

(%)

.

IIP Growth IIP Capital Goods Order Inflow YoY Growth (RHS)

Source: Bloomberg, ICICIdirect.com Research

Exhibit 38: Revenue growth vis-à-vis IIP and IIP Capital goods growth

-30

-20

-10

0

10

20

30

40

50

60

70

Q1FY

08

Q2FY

08

Q3FY

08

Q4FY

08

Q1FY

09

Q2FY

09

Q3FY

09

Q4FY

09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11

Q1FY

12

Q2FY

12

Q3FY

12

(%)

.

-10

0

10

20

30

40

50

60

(%)

.

IIP Growth IIP Capital Goods Revenue Growth YoY (Growth)- RHS

Source: Bloomberg, ICICIdirect.com Research

…a) Focus on multiple geographies (partial de-risking)…

L&T has expanded its EPC and construction business across the Middle East and Asian continent as well. The total tally now includes over 30 countries. As of 9MFY12, international revenues contributed about 11% of overall standalone revenues. L&T either directly or via subsidiaries is trying to capitalise on the infrastructure opportunity out there. L&T ranks 29 globally and 77 globally in terms of total revenues and international revenues in CY11, respectively. A lower ranking in terms of international revenues is due to the management focus on capitalising the domestic opportunity. The management expects this segment to continue 25% of the overall revenues by 2017, which would lead to an improvement in global standings. The global arena is mainly dominated by Europeans and Korean contractors.

The management expects this segment to continue 25% of

the overall revenues by 2017, which would lead to an improvement in global standings

Page 15ICICI Securities Ltd | Retail Equity Research

Exhibit 39: Global ranking of contractors in terms of international revenues

Company Name Company Rank in 2011 Rank in 2010HOCTIEF Germany 1 1VINCI France 2 2Bechtel US 3 4BOUGYES France 4 5Skanska Sweden 5 6Saipem Italy 6 7Flour Corp US 7 9Larsen & Toubro India 77 62

Source: McGraw Hill Construction,, ICICIdirect.com Research

Exhibit 40: Global ranking of contractors in terms of overall revenues

Company Name Company Rank in 2011 Rank in 2010China Railway Cons. China 1 1China Railway group China 2 2China state cons. China 3 6VINCI France 4 3China communications China 5 5BOUGYES France 6 4China Metallurgical grou China 7 8Larsen & Toubro India 29 34

Source: McGraw Hill Construction, ICICIdirect.com Research

Opportunity is huge in the Middle East markets

Exhibit 41: Opportunity in Saudi Arabia over 2009-2014

7 8 10 13

25

35

59

92

105 7 10

0102030405060708090

100

2009 2014 2019 2024

($ B

n)

.

Public Sector Private Industrial Oil Sector

Source: Ministry of economy and planning (Kingdom of Saudi Arabia), ICICIdirect.com Research

Exhibit 42: Opportunity in Oman over 8th five year plan (2010-2015)

4.33.2

1.3 1.2 1.20.40

2

4

6

Airp

orts

Road

s

Seap

orts

Wat

er

Hous

ing

Othe

rs

($ B

n)

Source: Ministry national economy (Oman), ICICIdirect.com Research

Key initiatives taken to step up international business opportunities …

• Setting up of modular fabrication facility in Oman • Also, setting up a switchboard manufacturing facility in Saudi Arabia • A system integration facility in Jebel Ali to capitalise on the drive automation business

… Efforts start to become visible..

Exhibit 43: Major orders announced in International markets by L&T across various segments. Order Details Client Year Order size (| Crore) SegmentT&D order in Oman Public FY12 170 PowerOrder of 132/11 KV substation system in Kuwait Public FY12 320 PowerSubstation and Transmission line order in Kuwait Public FY12 185 Power Order from Qatar General Electric and Water Corporation for 13 EHV Substaion Public FY12 1210 PowerEPC of 225 km transmission line for Saudi Construction Company Public FY12 597 PowerOrder from Petroleum Development Oman, LLC for 3 MMSCMD grenfield gas project Public FY12 700 HydrocarbonsEPC of 123 km pipleline order from GASCO: Abu Dhabhi, Public FY12 $189 mn HydrocarbonsOrder for four wellhead towers and one mainhead tower platform from ADNOC, UAE Public FY12 $450 mn HydrocarbonsOrder for three wellhead and associated works for PTT Public Ltd Co Public FY12 $250 mn HydrocarbonsTwo major roads orders in Oman (first big road orders) Public FY12 875 Infrastructure

Public FY11 2200 InfrastructureConstruction of New Salah International Aiport (Oman), to be done in 30 months (L&T's share in total order is |2,200)

Source: Company, ICICIdirect.com Research

Page 16ICICI Securities Ltd | Retail Equity Research

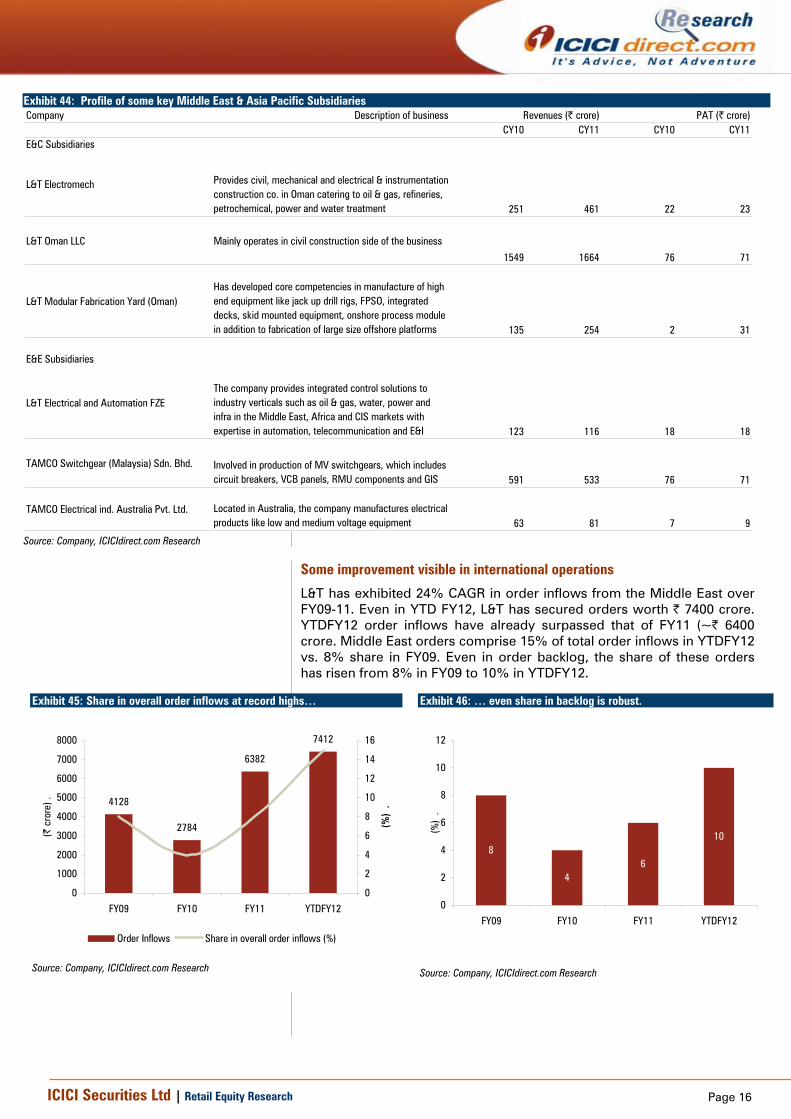

Exhibit 44: Profile of some key Middle East & Asia Pacific Subsidiaries Company Description of business

CY10 CY11 CY10 CY11E&C Subsidiaries

L&T Electromech Provides civil, mechanical and electrical & instrumentation construction co. in Oman catering to oil & gas, refineries, petrochemical, power and water treatment 251 461 22 23

L&T Oman LLC Mainly operates in civil construction side of the business

1549 1664 76 71

L&T Modular Fabrication Yard (Oman)Has developed core competencies in manufacture of high end equipment like jack up drill rigs, FPSO, integrated decks, skid mounted equipment, onshore process module in addition to fabrication of large size offshore platforms 135 254 2 31

E&E Subsidiaries

L&T Electrical and Automation FZEThe company provides integrated control solutions to industry verticals such as oil & gas, water, power and infra in the Middle East, Africa and CIS markets with expertise in automation, telecommunication and E&I 123 116 18 18

TAMCO Switchgear (Malaysia) Sdn. Bhd. Involved in production of MV switchgears, which includes circuit breakers, VCB panels, RMU components and GIS 591 533 76 71

TAMCO Electrical ind. Australia Pvt. Ltd. Located in Australia, the company manufactures electrical products like low and medium voltage equipment 63 81 7 9

Revenues (| crore) PAT (| crore)

Source: Company, ICICIdirect.com Research

Some improvement visible in international operations

L&T has exhibited 24% CAGR in order inflows from the Middle East over FY09-11. Even in YTD FY12, L&T has secured orders worth | 7400 crore. YTDFY12 order inflows have already surpassed that of FY11 (~| 6400 crore. Middle East orders comprise 15% of total order inflows in YTDFY12 vs. 8% share in FY09. Even in order backlog, the share of these orders has risen from 8% in FY09 to 10% in YTDFY12.

Exhibit 45: Share in overall order inflows at record highs…

4128

2784

6382

7412

0

1000

2000

3000

4000

5000

6000

7000

8000

FY09 FY10 FY11 YTDFY12

(| c

rore

) .

0

2

4

6

8

10

12

14

16

(%)

.

Order Inflows Share in overall order inflows (%)

Source: Company, ICICIdirect.com Research

Exhibit 46: … even share in backlog is robust.

8

46

10

0

2

4

6

8

10

12

FY09 FY10 FY11 YTDFY12

(%)

.

Source: Company, ICICIdirect.com Research

Page 17ICICI Securities Ltd | Retail Equity Research

…b) Traction in captive orders: L&T IDPL enhancing portfolio… L&T is also aiming to house significant infrastructure assets portfolio via its subsidiary L&T IDPL, which houses about 17 projects costing over | 75500 crore. Given the backward integration of L&T (strong EPC business), ordering for the developmental assets do come to the base business, thereby proving a good opportunity for the base business. As of YTDFY12, in-house orders contributed 14% of the overall backlog and commanded ~13% of the order inflows in Q3DY12. Going ahead, many infrastructure projects (mainly in power T&D, roads and Railways) will be ordered out on a BOT basis, where L&T will be a key bidder. Hence, this will provide visibility to the base business in terms of securing further in-house orders from L&T IDPL. Exhibit 47: Share of In house orders in backlog and order inflows

0

5

10

15

20

FY08

FY09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11

Q1FY

12

Q2FY

12

Q3FY

12

(%)

.

0

10

20

30

40

(%)

.

Share in order backlog Share in order inflows(RHS)

Source: Company, ICICIdirect.com Research

…c) Preferred bidder in complex private sector projects

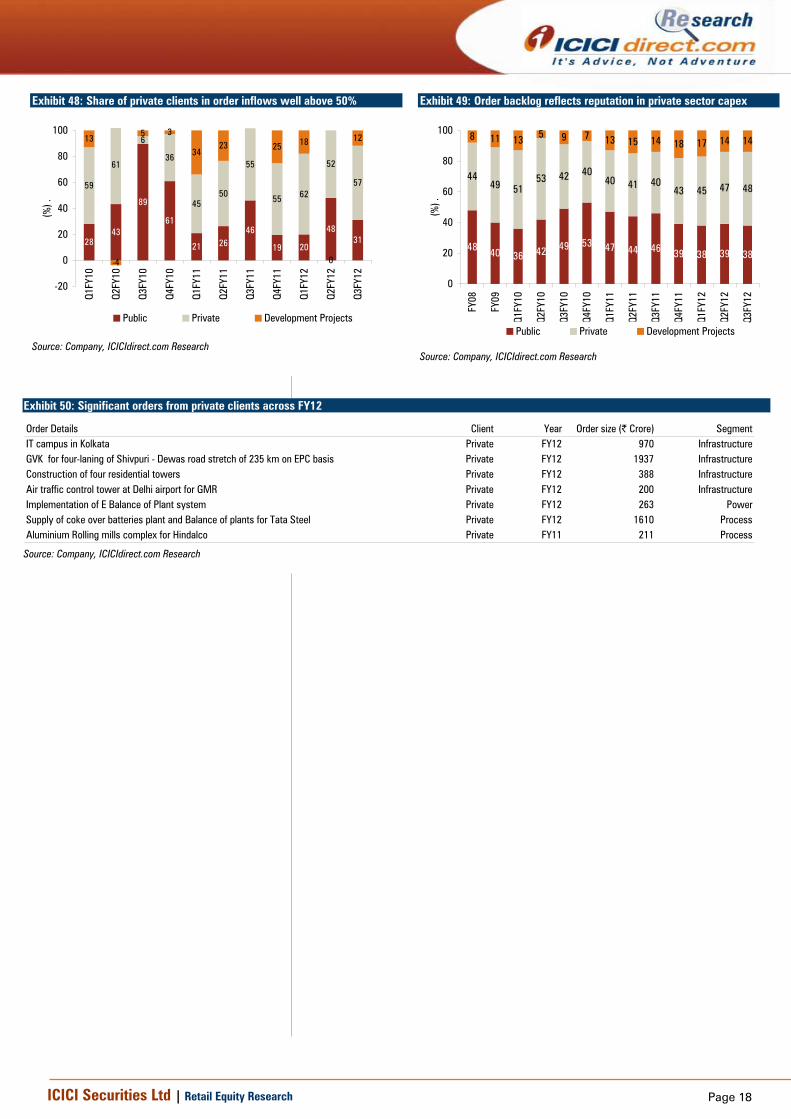

Another reason why L&T‘s sensitivity to macro variables has relatively come down may be due to the fact that in large complex negotiated orders, L&T scores well above its peers as L&T has robust execution skills, an integrated business model and timely delivery schedules to handle large complex projects as private sector projects are more time bound ones. This is clearly visible in the private clients’ share in order inflows over FY10-YTDFY12 as the average share during the period stood at 50%. Even in the backlog, average share of private clients stood at 45% over FY08-YTDFY12.

Opportunities in India’s five year plan also will help L&T, going ahead, as private sector participation in the Eleventh and Twelfth Five Year Plan is expected to rise to 33% and 50%, respectively. Hence, we believe once the tough macro conditions trough and private sector capex resumes, L&T will benefit immensely from the same.

L&T scores well above its peers in private sector orders as

it has robust execution skills, an integrated business model

and timely delivery schedules to handle large complex projects as the same are more time bound projects

Page 18ICICI Securities Ltd | Retail Equity Research

Exhibit 48: Share of private clients in order inflows well above 50%

2843

89

61

21 2646

19 20

4831

59

61

6

36

4550

55

55 62

52

57

13

-4

5 3

3423 25 18

0

12

-20

0

20

40

60

80

100

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11

Q1FY

12

Q2FY

12

Q3FY

12

(%) .

Public Private Development Projects

Source: Company, ICICIdirect.com Research

Exhibit 49: Order backlog reflects reputation in private sector capex

48 40 36 42 49 53 47 44 46 39 38 39 38

4449 51

53 42 4040 41 40

43 45 47 48

8 11 13 5 9 7 13 15 14 18 17 14 14

0

20

40

60

80

100

FY08

FY09

Q1FY

10

Q2FY

10

Q3FY

10

Q4FY

10

Q1FY

11

Q2FY

11

Q3FY

11

Q4FY

11

Q1FY

12

Q2FY

12

Q3FY

12

(%) .

Public Private Development Projects

Source: Company, ICICIdirect.com Research

Exhibit 50: Significant orders from private clients across FY12

Order Details Client Year Order size (| Crore) SegmentIT campus in Kolkata Private FY12 970 InfrastructureGVK for four-laning of Shivpuri - Dewas road stretch of 235 km on EPC basis Private FY12 1937 InfrastructureConstruction of four residential towers Private FY12 388 InfrastructureAir traffic control tower at Delhi airport for GMR Private FY12 200 InfrastructureImplementation of E Balance of Plant system Private FY12 263 PowerSupply of coke over batteries plant and Balance of plants for Tata Steel Private FY12 1610 ProcessAluminium Rolling mills complex for Hindalco Private FY11 211 Process

Source: Company, ICICIdirect.com Research

Page 19ICICI Securities Ltd | Retail Equity Research

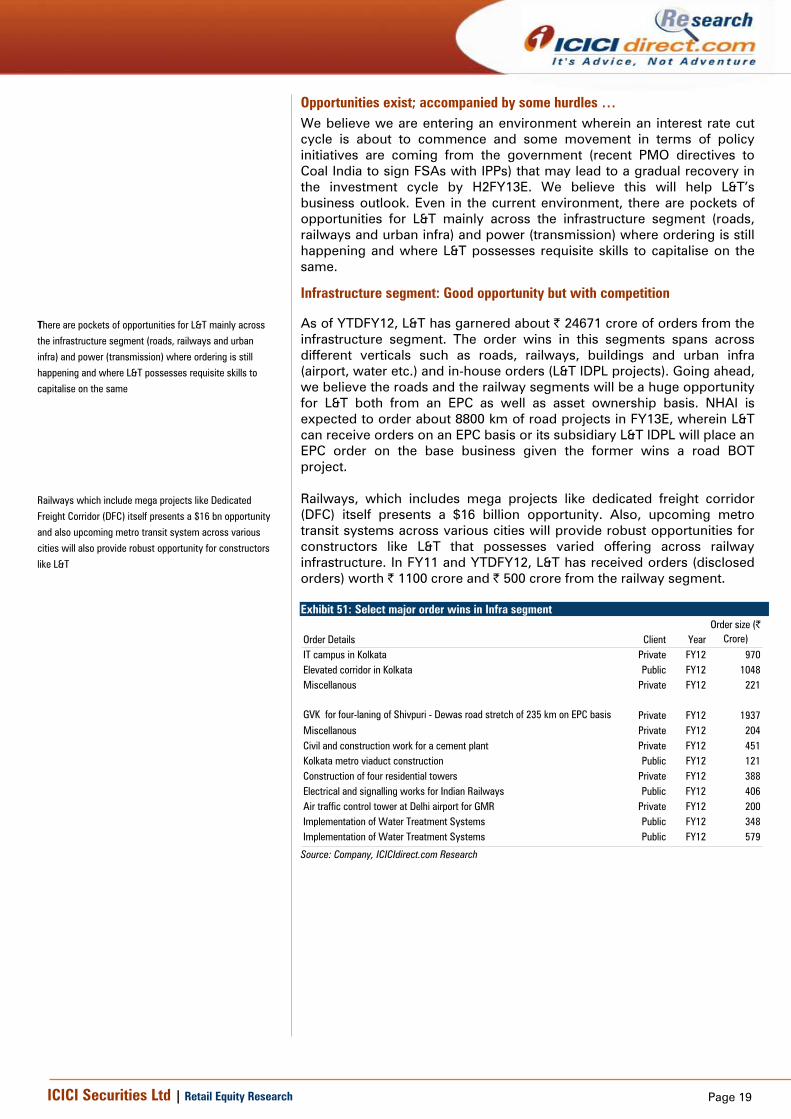

Opportunities exist; accompanied by some hurdles … We believe we are entering an environment wherein an interest rate cut cycle is about to commence and some movement in terms of policy initiatives are coming from the government (recent PMO directives to Coal India to sign FSAs with IPPs) that may lead to a gradual recovery in the investment cycle by H2FY13E. We believe this will help L&T’s business outlook. Even in the current environment, there are pockets of opportunities for L&T mainly across the infrastructure segment (roads, railways and urban infra) and power (transmission) where ordering is still happening and where L&T possesses requisite skills to capitalise on the same.

Infrastructure segment: Good opportunity but with competition

As of YTDFY12, L&T has garnered about | 24671 crore of orders from the infrastructure segment. The order wins in this segments spans across different verticals such as roads, railways, buildings and urban infra (airport, water etc.) and in-house orders (L&T IDPL projects). Going ahead, we believe the roads and the railway segments will be a huge opportunity for L&T both from an EPC as well as asset ownership basis. NHAI is expected to order about 8800 km of road projects in FY13E, wherein L&T can receive orders on an EPC basis or its subsidiary L&T IDPL will place an EPC order on the base business given the former wins a road BOT project. Railways, which includes mega projects like dedicated freight corridor (DFC) itself presents a $16 billion opportunity. Also, upcoming metro transit systems across various cities will provide robust opportunities for constructors like L&T that possesses varied offering across railway infrastructure. In FY11 and YTDFY12, L&T has received orders (disclosed orders) worth | 1100 crore and | 500 crore from the railway segment. Exhibit 51: Select major order wins in Infra segment

Order Details Client YearOrder size (|

Crore)IT campus in Kolkata Private FY12 970Elevated corridor in Kolkata Public FY12 1048Miscellanous Private FY12 221

GVK for four-laning of Shivpuri - Dewas road stretch of 235 km on EPC basis Private FY12 1937Miscellanous Private FY12 204Civil and construction work for a cement plant Private FY12 451Kolkata metro viaduct construction Public FY12 121Construction of four residential towers Private FY12 388Electrical and signalling works for Indian Railways Public FY12 406Air traffic control tower at Delhi airport for GMR Private FY12 200Implementation of Water Treatment Systems Public FY12 348Implementation of Water Treatment Systems Public FY12 579

Source: Company, ICICIdirect.com Research

There are pockets of opportunities for L&T mainly across

the infrastructure segment (roads, railways and urban

infra) and power (transmission) where ordering is still

happening and where L&T possesses requisite skills to capitalise on the same

Railways which include mega projects like Dedicated

Freight Corridor (DFC) itself presents a $16 bn opportunity

and also upcoming metro transit system across various

cities will also provide robust opportunity for constructors

like L&T

Page 20ICICI Securities Ltd | Retail Equity Research

Roads vertical: NHAI expected to award 8800 Kms of road projects in FY13E Exhibit 52: Ordering opportunity for L&T in the roads segment

Balance length for award - 420 2,572 3,023 1,000 659 276 12,250 19,924 - 20 20,220

percentage left for awarding - 6 21 47 100 94 71 83 41 - 1 40

NHDP Phase III

NHDP Phase V

NHDP Phase VI Others

PortConnectivityGQ Total by NHAI

NHDP Phase VII

NHDP

SARDP -NE

NHDP Phase IV

NHDP Total

NS -EW Ph. I & II

Source: NHAI, ICICIdirect.com Research

Exhibit 53: Road ordering by NHAI till FY13E

500

1500

2500

3500

4500

5500

6500

7500FY

07

FY08

FY09

FY10

FY11

FY12

E*

FY13

E**

(km

)

.

Source: NHAI, Budget Document, ICICIdirect.com Research. * Expected ordering in FY12E ** Ordering target for Fy13E

Dedicated Freight Corridor The dedicated freight corridor (DFC) is a mega project and the completion cost as per the business plan is | 77630 crore. Railways is expected to award 1,000 km route contracts for DFC in FY13 and work with respect of RFP and RFQ processes for phase 1 of the western and eastern corridor has already commenced. The completion of this project is expected to happen by 2017-2018.

The dedicated freight corridor (DFC) is a mega project and

the completion cost as per the Business Plan is | 77630

Crore. Railways is expected to award 1,000 km route

contracts for DFC in FY13

Page 21ICICI Securities Ltd | Retail Equity Research

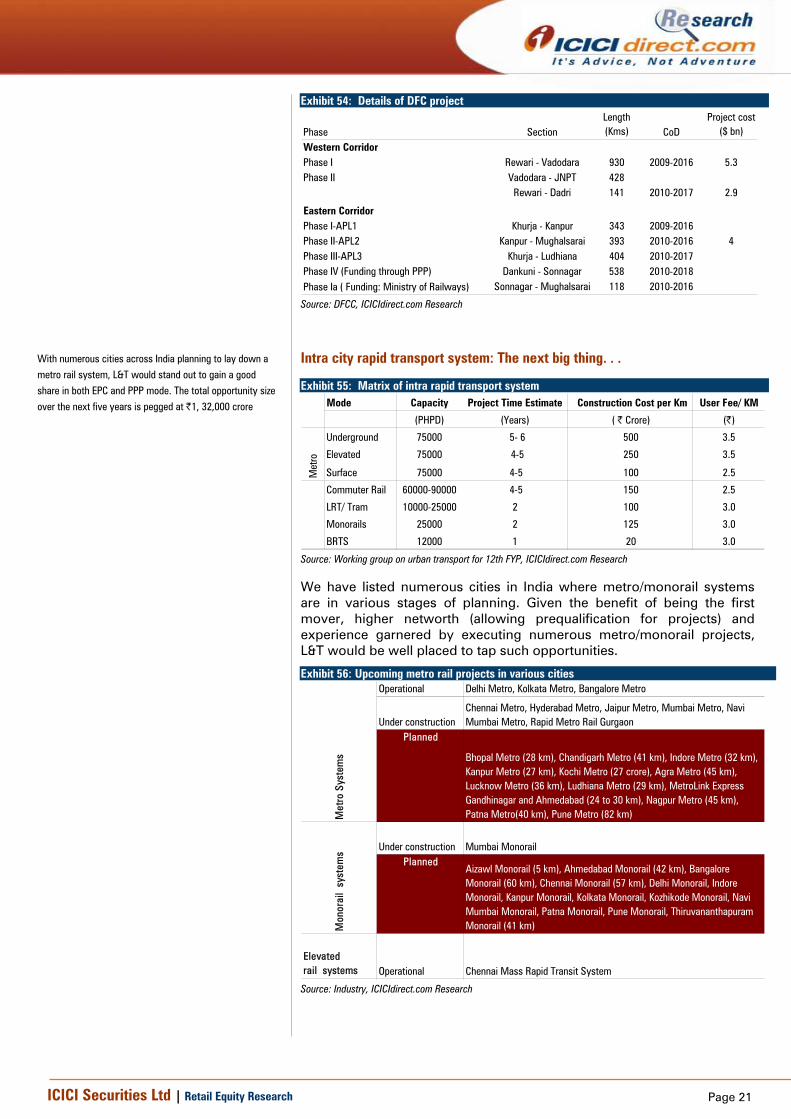

Exhibit 54: Details of DFC project

Phase SectionLength (Kms) CoD

Project cost ($ bn)

Western CorridorPhase I Rewari - Vadodara 930 2009-2016 5.3Phase II Vadodara - JNPT 428

Intra city rapid transport system: The next big thing. . .

Exhibit 55: Matrix of intra rapid transport system Mode Capacity Project Time Estimate Construction Cost per Km User Fee/ KM

(PHPD) (Years) ( | Crore) (|)

Underground 75000 5- 6 500 3.5

Elevated 75000 4-5 250 3.5

Surface 75000 4-5 100 2.5

Commuter Rail 60000-90000 4-5 150 2.5

LRT/ Tram 10000-25000 2 100 3.0

Monorails 25000 2 125 3.0

BRTS 12000 1 20 3.0

Met

ro

Source: Working group on urban transport for 12th FYP, ICICIdirect.com Research

We have listed numerous cities in India where metro/monorail systems are in various stages of planning. Given the benefit of being the first mover, higher networth (allowing prequalification for projects) and experience garnered by executing numerous metro/monorail projects, L&T would be well placed to tap such opportunities.

Exhibit 56: Upcoming metro rail projects in various cities Operational

Under constructionPlanned

Under construction Mumbai MonorailPlanned

Elevated rail systems Operational Chennai Mass Rapid Transit System

Met

ro S

yste

ms

Mon

orai

l sy

stem

s

Delhi Metro, Kolkata Metro, Bangalore Metro

Chennai Metro, Hyderabad Metro, Jaipur Metro, Mumbai Metro, Navi Mumbai Metro, Rapid Metro Rail Gurgaon

Bhopal Metro (28 km), Chandigarh Metro (41 km), Indore Metro (32 km), Kanpur Metro (27 km), Kochi Metro (27 crore), Agra Metro (45 km), Lucknow Metro (36 km), Ludhiana Metro (29 km), MetroLink Express Gandhinagar and Ahmedabad (24 to 30 km), Nagpur Metro (45 km), Patna Metro(40 km), Pune Metro (82 km)

With numerous cities across India planning to lay down a metro rail system, L&T would stand out to gain a good share in both EPC and PPP mode. The total opportunity size over the next five years is pegged at |1, 32,000 crore

Page 22ICICI Securities Ltd | Retail Equity Research

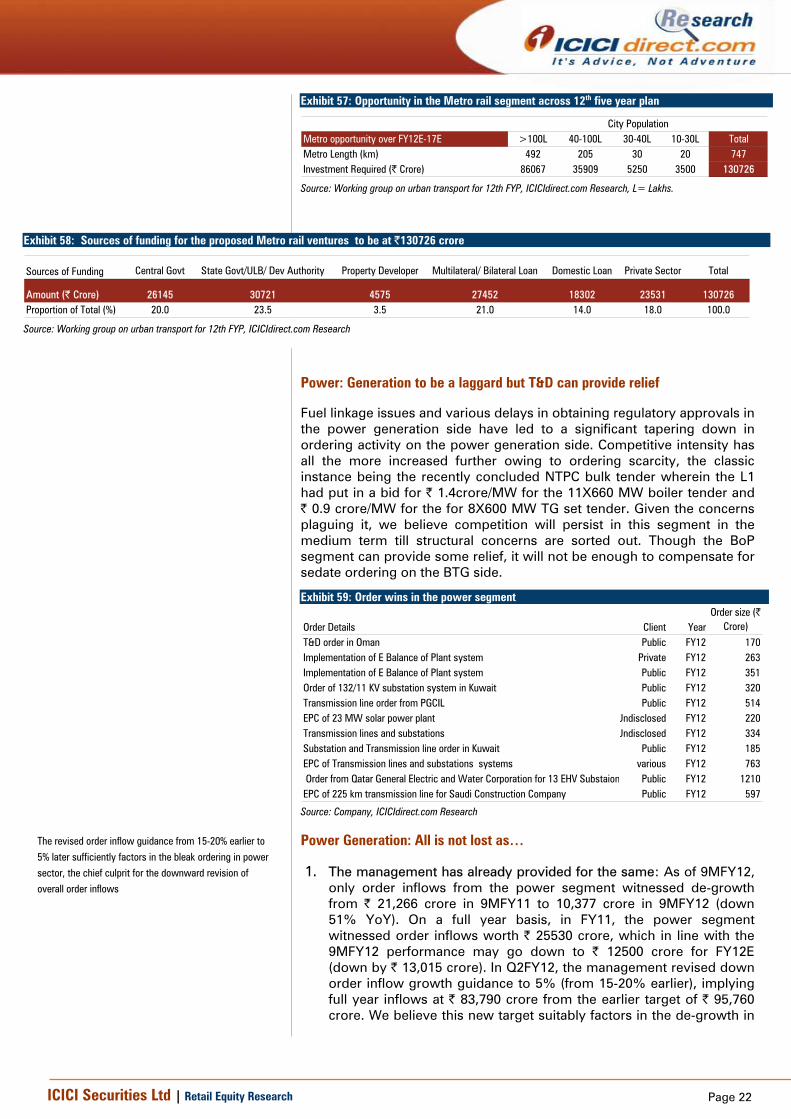

Exhibit 57: Opportunity in the Metro rail segment across 12th five year plan

Source: Working group on urban transport for 12th FYP, ICICIdirect.com Research, L= Lakhs.

Exhibit 58: Sources of funding for the proposed Metro rail ventures to be at |130726 crore

Sources of Funding Central Govt State Govt/ULB/ Dev Authority Property Developer Multilateral/ Bilateral Loan Domestic Loan Private Sector Total

Amount (| Crore) 26145 30721 4575 27452 18302 23531 130726Proportion of Total (%) 20.0 23.5 3.5 21.0 14.0 18.0 100.0

Source: Working group on urban transport for 12th FYP, ICICIdirect.com Research

Power: Generation to be a laggard but T&D can provide relief

Fuel linkage issues and various delays in obtaining regulatory approvals in the power generation side have led to a significant tapering down in ordering activity on the power generation side. Competitive intensity has all the more increased further owing to ordering scarcity, the classic instance being the recently concluded NTPC bulk tender wherein the L1 had put in a bid for | 1.4crore/MW for the 11X660 MW boiler tender and | 0.9 crore/MW for the for 8X600 MW TG set tender. Given the concerns plaguing it, we believe competition will persist in this segment in the medium term till structural concerns are sorted out. Though the BoP segment can provide some relief, it will not be enough to compensate for sedate ordering on the BTG side.

Exhibit 59: Order wins in the power segment

Order Details Client YearOrder size (|

Crore)T&D order in Oman Public FY12 170Implementation of E Balance of Plant system Private FY12 263Implementation of E Balance of Plant system Public FY12 351Order of 132/11 KV substation system in Kuwait Public FY12 320Transmission line order from PGCIL Public FY12 514EPC of 23 MW solar power plant Undisclosed FY12 220Transmission lines and substations Undisclosed FY12 334Substation and Transmission line order in Kuwait Public FY12 185EPC of Transmission lines and substations systems various FY12 763 Order from Qatar General Electric and Water Corporation for 13 EHV Substaion Public FY12 1210EPC of 225 km transmission line for Saudi Construction Company Public FY12 597

Source: Company, ICICIdirect.com Research

Power Generation: All is not lost as…

1. The management has already provided for the same: As of 9MFY12, only order inflows from the power segment witnessed de-growth from | 21,266 crore in 9MFY11 to 10,377 crore in 9MFY12 (down 51% YoY). On a full year basis, in FY11, the power segment witnessed order inflows worth | 25530 crore, which in line with the 9MFY12 performance may go down to | 12500 crore for FY12E (down by | 13,015 crore). In Q2FY12, the management revised down order inflow growth guidance to 5% (from 15-20% earlier), implying full year inflows at | 83,790 crore from the earlier target of | 95,760 crore. We believe this new target suitably factors in the de-growth in

The revised order inflow guidance from 15-20% earlier to 5% later sufficiently factors in the bleak ordering in power sector, the chief culprit for the downward revision of overall order inflows

Page 23ICICI Securities Ltd | Retail Equity Research

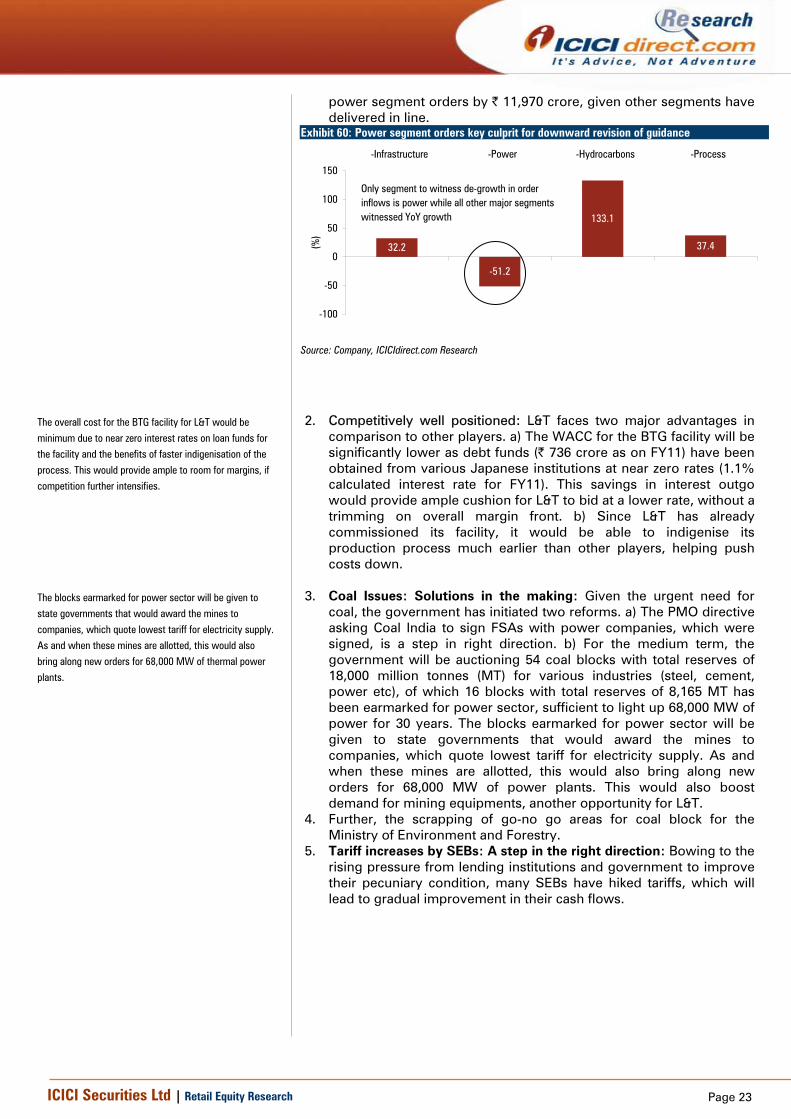

power segment orders by | 11,970 crore, given other segments have delivered in line.

Exhibit 60: Power segment orders key culprit for downward revision of guidance

32.2

-51.2

133.1

37.4

-100

-50

0

50

100

150

-Infrastructure -Power -Hydrocarbons -Process

(%)

Only segment to witness de-growth in order inflows is power while all other major segments witnessed YoY growth

Source: Company, ICICIdirect.com Research

2. Competitively well positioned: L&T faces two major advantages in

comparison to other players. a) The WACC for the BTG facility will be significantly lower as debt funds (| 736 crore as on FY11) have been obtained from various Japanese institutions at near zero rates (1.1% calculated interest rate for FY11). This savings in interest outgo would provide ample cushion for L&T to bid at a lower rate, without a trimming on overall margin front. b) Since L&T has already commissioned its facility, it would be able to indigenise its production process much earlier than other players, helping push costs down.

3. Coal Issues: Solutions in the making: Given the urgent need for

coal, the government has initiated two reforms. a) The PMO directive asking Coal India to sign FSAs with power companies, which were signed, is a step in right direction. b) For the medium term, the government will be auctioning 54 coal blocks with total reserves of 18,000 million tonnes (MT) for various industries (steel, cement, power etc), of which 16 blocks with total reserves of 8,165 MT has been earmarked for power sector, sufficient to light up 68,000 MW of power for 30 years. The blocks earmarked for power sector will be given to state governments that would award the mines to companies, which quote lowest tariff for electricity supply. As and when these mines are allotted, this would also bring along new orders for 68,000 MW of power plants. This would also boost demand for mining equipments, another opportunity for L&T.

4. Further, the scrapping of go-no go areas for coal block for the Ministry of Environment and Forestry.

5. Tariff increases by SEBs: A step in the right direction: Bowing to the rising pressure from lending institutions and government to improve their pecuniary condition, many SEBs have hiked tariffs, which will lead to gradual improvement in their cash flows.

The overall cost for the BTG facility for L&T would be minimum due to near zero interest rates on loan funds for the facility and the benefits of faster indigenisation of the process. This would provide ample to room for margins, if competition further intensifies.

The blocks earmarked for power sector will be given to state governments that would award the mines to companies, which quote lowest tariff for electricity supply. As and when these mines are allotted, this would also bring along new orders for 68,000 MW of thermal power plants.

Page 24ICICI Securities Ltd | Retail Equity Research

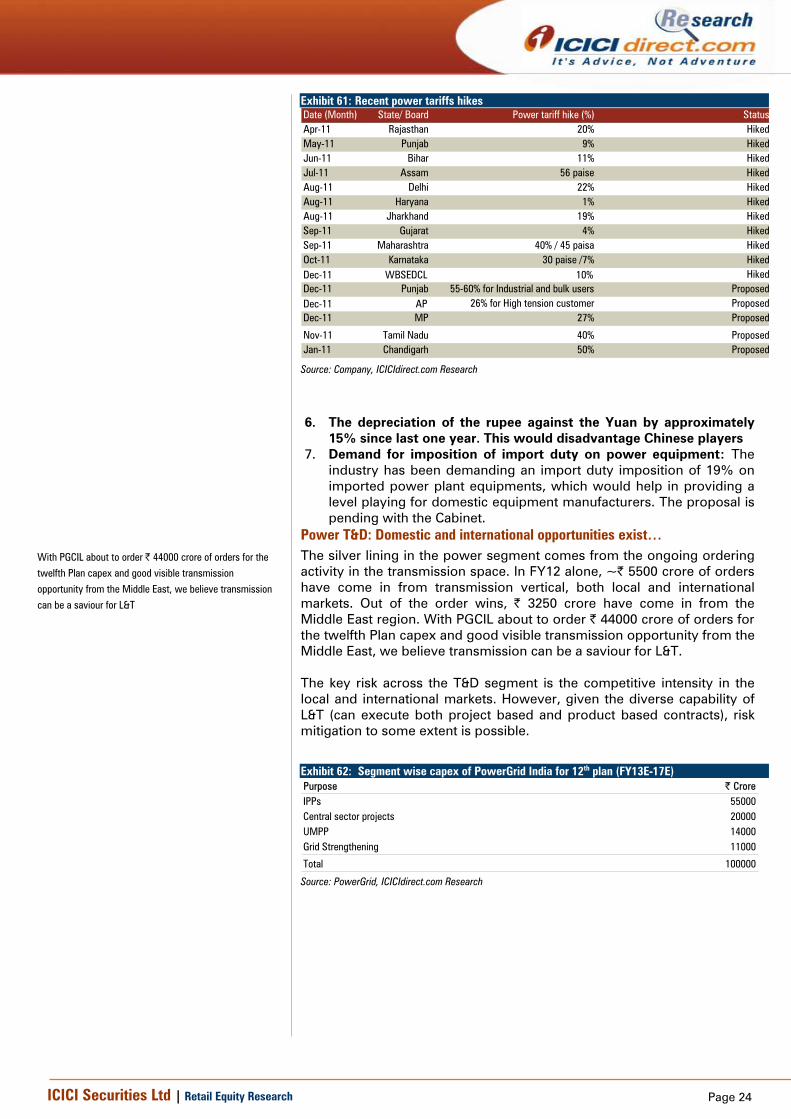

Exhibit 61: Recent power tariffs hikes Date (Month) State/ Board Power tariff hike (%) StatusApr-11 Rajasthan 20% HikedMay-11 Punjab 9% HikedJun-11 Bihar 11% HikedJul-11 Assam 56 paise HikedAug-11 Delhi 22% HikedAug-11 Haryana 1% HikedAug-11 Jharkhand 19% HikedSep-11 Gujarat 4% HikedSep-11 Maharashtra 40% / 45 paisa HikedOct-11 Karnataka 30 paise /7% HikedDec-11 WBSEDCL 10% HikedDec-11 Punjab 55-60% for Industrial and bulk users ProposedDec-11 AP 26% for High tension customer ProposedDec-11 MP 27% Proposed

Nov-11 Tamil Nadu 40% ProposedJan-11 Chandigarh 50% Proposed

Source: Company, ICICIdirect.com Research

6. The depreciation of the rupee against the Yuan by approximately

15% since last one year. This would disadvantage Chinese players 7. Demand for imposition of import duty on power equipment: The

industry has been demanding an import duty imposition of 19% on imported power plant equipments, which would help in providing a level playing for domestic equipment manufacturers. The proposal is pending with the Cabinet.

Power T&D: Domestic and international opportunities exist… The silver lining in the power segment comes from the ongoing ordering activity in the transmission space. In FY12 alone, ~| 5500 crore of orders have come in from transmission vertical, both local and international markets. Out of the order wins, | 3250 crore have come in from the Middle East region. With PGCIL about to order | 44000 crore of orders for the twelfth Plan capex and good visible transmission opportunity from the Middle East, we believe transmission can be a saviour for L&T. The key risk across the T&D segment is the competitive intensity in the local and international markets. However, given the diverse capability of L&T (can execute both project based and product based contracts), risk mitigation to some extent is possible.

Exhibit 62: Segment wise capex of PowerGrid India for 12th plan (FY13E-17E) Purpose | CroreIPPs 55000Central sector projects 20000UMPP 14000Grid Strengthening 11000

Total 100000

Source: PowerGrid, ICICIdirect.com Research

With PGCIL about to order | 44000 crore of orders for the

twelfth Plan capex and good visible transmission

opportunity from the Middle East, we believe transmission

can be a saviour for L&T

Page 25ICICI Securities Ltd | Retail Equity Research

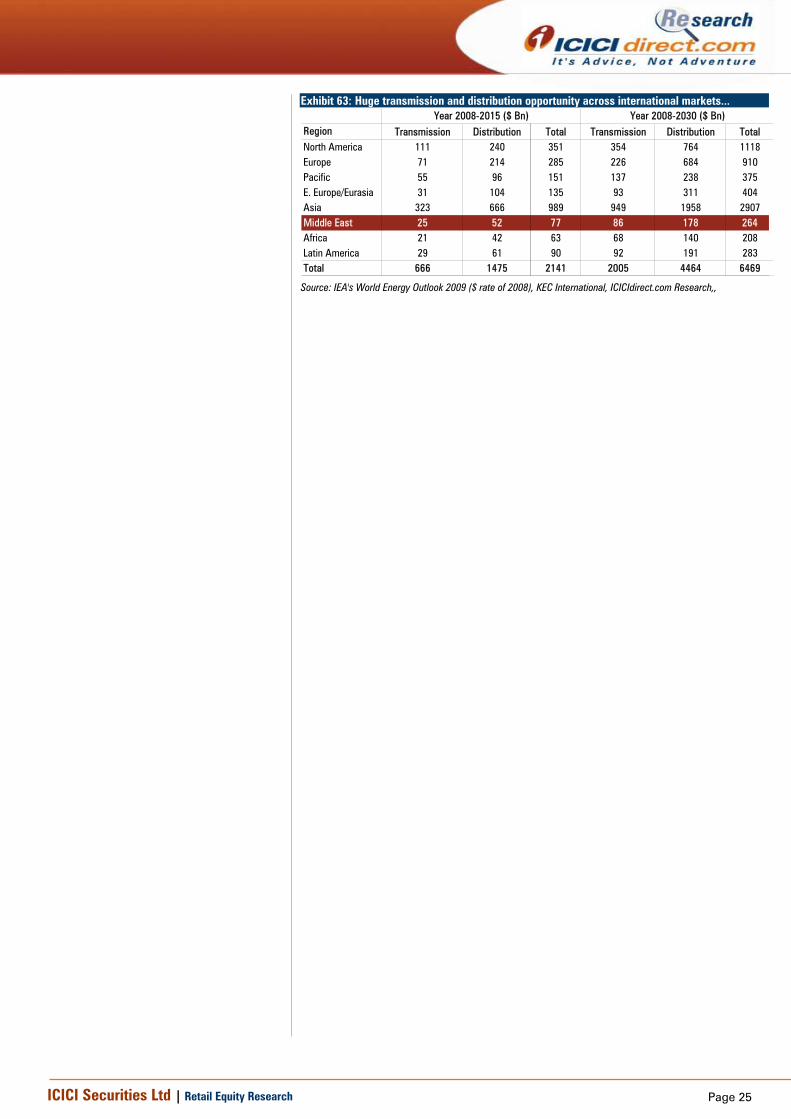

Exhibit 63: Huge transmission and distribution opportunity across international markets...

Region Transmission Distribution Total Transmission Distribution TotalNorth America 111 240 351 354 764 1118Europe 71 214 285 226 684 910Pacific 55 96 151 137 238 375E. Europe/Eurasia 31 104 135 93 311 404Asia 323 666 989 949 1958 2907Middle East 25 52 77 86 178 264Africa 21 42 63 68 140 208Latin America 29 61 90 92 191 283Total 666 1475 2141 2005 4464 6469

Year 2008-2015 ($ Bn) Year 2008-2030 ($ Bn)

Source: IEA's World Energy Outlook 2009 ($ rate of 2008), KEC International, ICICIdirect.com Research,,

Page 26ICICI Securities Ltd | Retail Equity Research

Hydrocarbons: Velocity of capex from public enterprises the key In the hydrocarbon space, YTD FY12 L&T has secured orders worth | 6500 crore in the hydrocarbon space. Out of these, 77% of the inflows came in from the Middle East markets. Going ahead, ONGC has planned a capex of | 65000 crore in the Twelfth plan and about ~| 25000 crore opportunity is feasible from Saudi Arabia, thereby proving scope to L&T in this segment. The capex in this segment is mainly committed by government agencies and velocity of project movement/ordering will hold the key, going ahead.

Exhibit 64: Order wins in hydrocarbons space

Order Details Client YearOrder size (|

Crore)

Order from Petroleum Development Oman, LLC for 3 MMSCMD grenfield gas project Public FY12 700EPC of 123 km pipleline order from GASCO: Abu Dhabhi, Public FY12 $189 mnOrder for four wellhead towers and one mainhead tower platform from ADNOC, UAE Public FY12 $450 mn Order for three wellhead and associated works for PTT Public Ltd Co Public FY12 $250 mnOffshore platform contract from Gujarat State Petroleum Co Public FY12 1450Additional processing units for gas proessing for ONGC Public FY11 1195Offshore platform contract from Gujarat State Petroleum Corp Public FY11 1060

Source: Company, ICICIdirect.com Research

Exhibit 65: Capex plan of ONGC across the 12th five year plan (FY13E-FY17E) Particulars (| crore) FY13 BE FY14 STP FY15 STP FY16 STP FY17 STP Total 12th PlanSurvey 1,720 2,467 889 662 556 6,293 Exploratory drilling 7,667 10,918 9,648 8,242 8,187 44,662 Development drilling 5,831 8,058 6,472 3,245 2,899 26,505 Capital Projects 15,607 13,317 1,553 17,207 17,581 65,264 R&D & Institutes 246 410 430 452 17,581 19,118

Source: ONGC, ICICIdirect.com Research

Exhibit 66: Hydrocarbon opportunity in Saudi Arabia till 2024

2525933561

48668

0

10000

20000

30000

40000

50000

60000

2014 2019 2024

(| C

rore

)

Source: Ministry of Economy and Planning (Kingdom of Saudi Arabia), ICICIdirect.com Research

Going ahead, ONGC has planned a capex of | 65000 crore

in the Twelfth Plan and about ~|25000 crore opportunity

is feasible from Saudi Arabia, thereby proving scope to L&T

in the hydrocarbon segment

Page 27ICICI Securities Ltd | Retail Equity Research

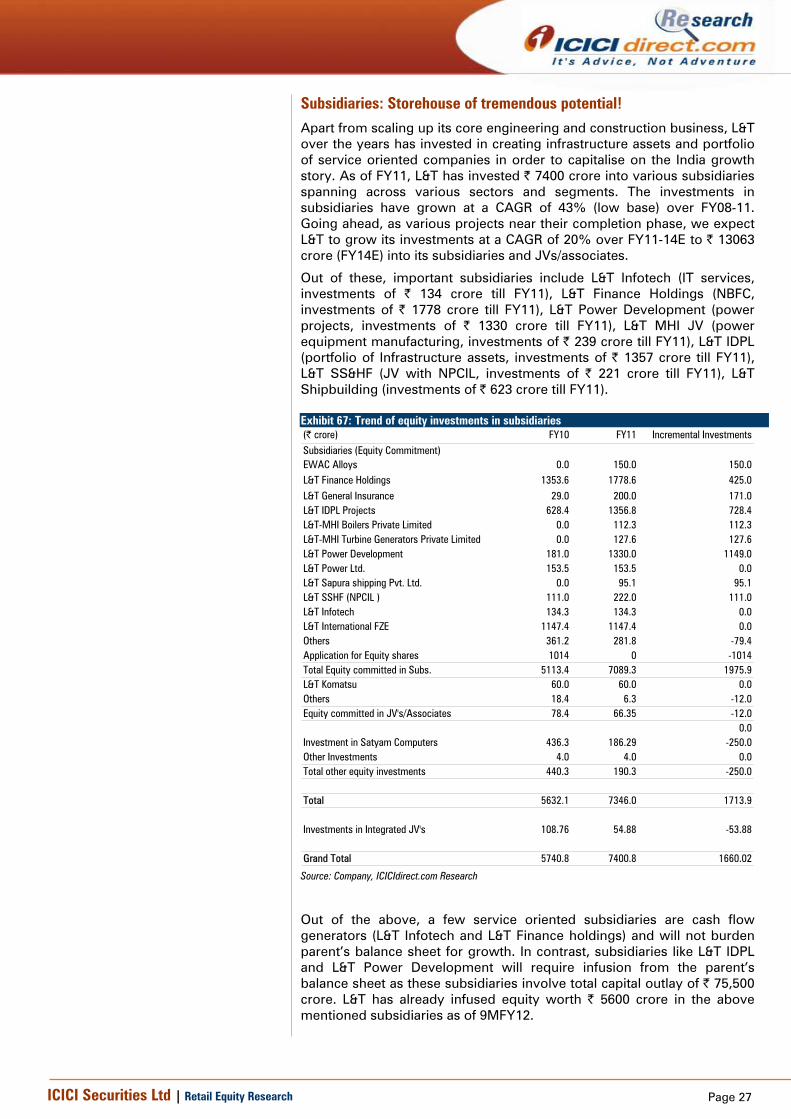

Subsidiaries: Storehouse of tremendous potential!

Apart from scaling up its core engineering and construction business, L&T over the years has invested in creating infrastructure assets and portfolio of service oriented companies in order to capitalise on the India growth story. As of FY11, L&T has invested | 7400 crore into various subsidiaries spanning across various sectors and segments. The investments in subsidiaries have grown at a CAGR of 43% (low base) over FY08-11. Going ahead, as various projects near their completion phase, we expect L&T to grow its investments at a CAGR of 20% over FY11-14E to | 13063 crore (FY14E) into its subsidiaries and JVs/associates.

Out of these, important subsidiaries include L&T Infotech (IT services, investments of | 134 crore till FY11), L&T Finance Holdings (NBFC, investments of | 1778 crore till FY11), L&T Power Development (power projects, investments of | 1330 crore till FY11), L&T MHI JV (power equipment manufacturing, investments of | 239 crore till FY11), L&T IDPL (portfolio of Infrastructure assets, investments of | 1357 crore till FY11), L&T SS&HF (JV with NPCIL, investments of | 221 crore till FY11), L&T Shipbuilding (investments of | 623 crore till FY11). Exhibit 67: Trend of equity investments in subsidiaries (| crore) FY10 FY11 Incremental InvestmentsSubsidiaries (Equity Commitment)EWAC Alloys 0.0 150.0 150.0L&T Finance Holdings 1353.6 1778.6 425.0L&T General Insurance 29.0 200.0 171.0L&T IDPL Projects 628.4 1356.8 728.4L&T-MHI Boilers Private Limited 0.0 112.3 112.3L&T-MHI Turbine Generators Private Limited 0.0 127.6 127.6L&T Power Development 181.0 1330.0 1149.0L&T Power Ltd. 153.5 153.5 0.0L&T Sapura shipping Pvt. Ltd. 0.0 95.1 95.1L&T SSHF (NPCIL ) 111.0 222.0 111.0L&T Infotech 134.3 134.3 0.0L&T International FZE 1147.4 1147.4 0.0Others 361.2 281.8 -79.4Application for Equity shares 1014 0 -1014Total Equity committed in Subs. 5113.4 7089.3 1975.9L&T Komatsu 60.0 60.0 0.0Others 18.4 6.3 -12.0Equity committed in JV's/Associates 78.4 66.35 -12.0

0.0Investment in Satyam Computers 436.3 186.29 -250.0Other Investments 4.0 4.0 0.0Total other equity investments 440.3 190.3 -250.0

Total 5632.1 7346.0 1713.9

Investments in Integrated JV's 108.76 54.88 -53.88

Grand Total 5740.8 7400.8 1660.02

Source: Company, ICICIdirect.com Research

Out of the above, a few service oriented subsidiaries are cash flow generators (L&T Infotech and L&T Finance holdings) and will not burden parent’s balance sheet for growth. In contrast, subsidiaries like L&T IDPL and L&T Power Development will require infusion from the parent’s balance sheet as these subsidiaries involve total capital outlay of | 75,500 crore. L&T has already infused equity worth | 5600 crore in the above mentioned subsidiaries as of 9MFY12.

Page 28ICICI Securities Ltd | Retail Equity Research

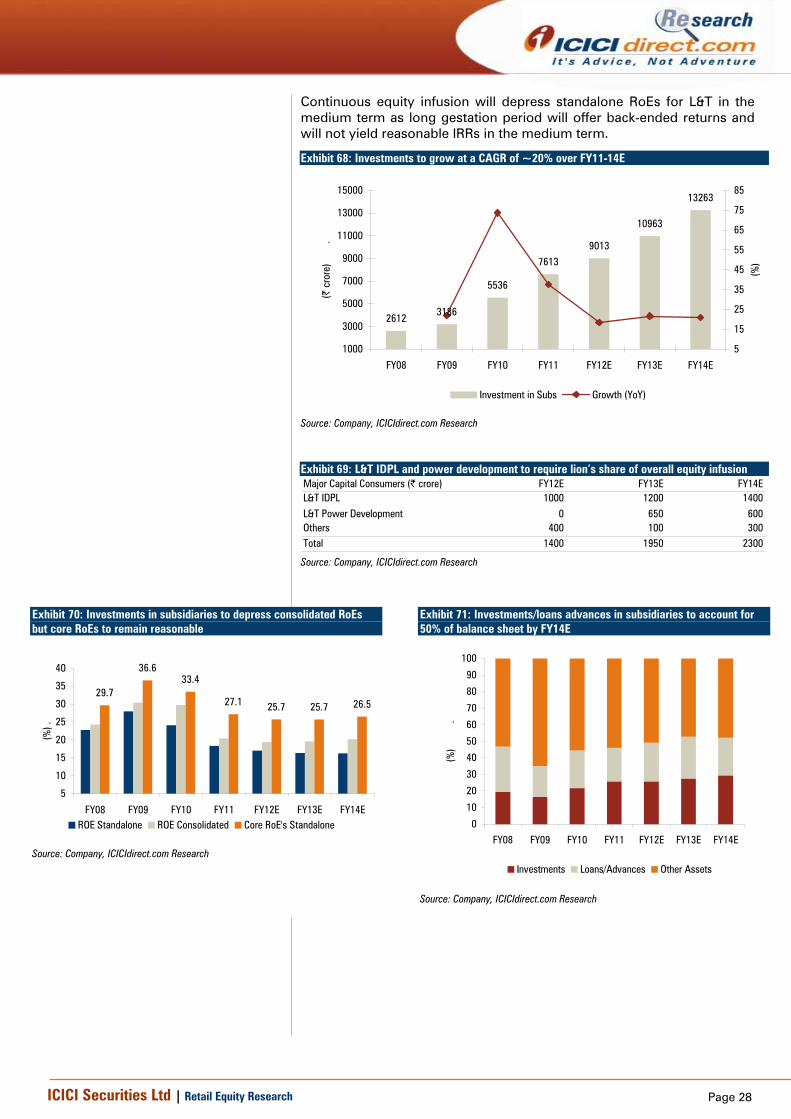

Continuous equity infusion will depress standalone RoEs for L&T in the medium term as long gestation period will offer back-ended returns and will not yield reasonable IRRs in the medium term.

Exhibit 68: Investments to grow at a CAGR of ~20% over FY11-14E

26123186

5536

76139013

10963

13263

1000

3000

5000

7000

9000

11000

13000

15000

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(| c

rore

)

.

5

15

25

35

45

55

65

75

85

(%)

Investment in Subs Growth (YoY)

Source: Company, ICICIdirect.com Research

Exhibit 69: L&T IDPL and power development to require lion’s share of overall equity infusion Major Capital Consumers (| crore) FY12E FY13E FY14EL&T IDPL 1000 1200 1400L&T Power Development 0 650 600Others 400 100 300Total 1400 1950 2300

Source: Company, ICICIdirect.com Research

Exhibit 70: Investments in subsidiaries to depress consolidated RoEs but core RoEs to remain reasonable

Exhibit 71: Investments/loans advances in subsidiaries to account for 50% of balance sheet by FY14E

0

10

20

30

40

50

60

70

80

90

100

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(%)

.

Investments Loans/Advances Other Assets

Source: Company, ICICIdirect.com Research

Page 29ICICI Securities Ltd | Retail Equity Research

L&T Finance Holdings: (post IPO no more dependent on parent for equity)

L&T Finance houses two NBFCs i.e. L&T Finance and L&T Infra Finance. The former caters to segment like corporate and retail financing (these include construction & transportation equipment finance, microfinance, corporate loans & lease, supply chain finance and capital market finance), asset backed finance and also houses a mutual fund unit (L&T MF). The latter focuses on project finance and advisory.

Over FY08-FY11, the subsidiary has grown its asset base at a CAGR of 52%. Given the moderation in the economy, we expect the growth rate to moderate. Hence, we have modelled in a business CAGR of 32% over FY11-14E. We expect NIMs to moderate owing to the overall slowdown and rise in borrowing costs to 5.8% in FY13E from 7.2%. Hence, PAT is expected to grow at a CAGR of 27% over FY11-14E due to a moderation in core business and rise in provisions on the assets. In our view, L&T has the lever to increase its RoEs, which is expected at 14.8% in FY14E on the back of rising leverage (comfortable at 6x in FY12E and 7.8x in FY14E).

L&T Finance Holding’s net interest income (NII) will contribute about 2.3% and 2.5% to the overall consolidated revenues in FY13E and FY14E.

Exhibit 72: CAGR of 32% in overall business (FY11-14E)….

2000

12000

22000

32000

42000

52000

62000

72000

82000

FY10 FY11 FY12E FY13E FY14E

(| c

rore

)

.

Loans Borrowings Business

Source: Company, ICICIdirect.com Research

Exhibit 73: … to drive NII and PAT growth (FY11-FY14E)

0

500

1000

1500

2000

2500

FY10 FY11 FY12E FY13E FY14E

(| c

rore

)

.

NII PPP PAT

Source: Company, ICICIdirect.com Research

Exhibit 74: Pick-up in leverage to improve RoEs by 210 bps over FY12E-14E

6.06.8

6.06.9

7.6

2.6 2.5 2.02.02.01

2

3

4

5

6

7

8

FY10 FY11 FY12E FY13E FY14E

(X)

0

5

10

15

20

25

(%)

Leverage ROA (RHS) ROE (RHS)

Source: Company, ICICIdirect.com Research

For L&T Finance Holdings, PAT is expected to grow at a

CAGR of 27% over FY11-14E due to moderation in core

business and rise in provisions on assets

In our view, L&T has the lever to increase its RoEs, which

is expected at 14.8% in FY14E on the back of rising leverage (comfortable at 6x in FY12E and 7.8x in FY14E)

Page 30ICICI Securities Ltd | Retail Equity Research

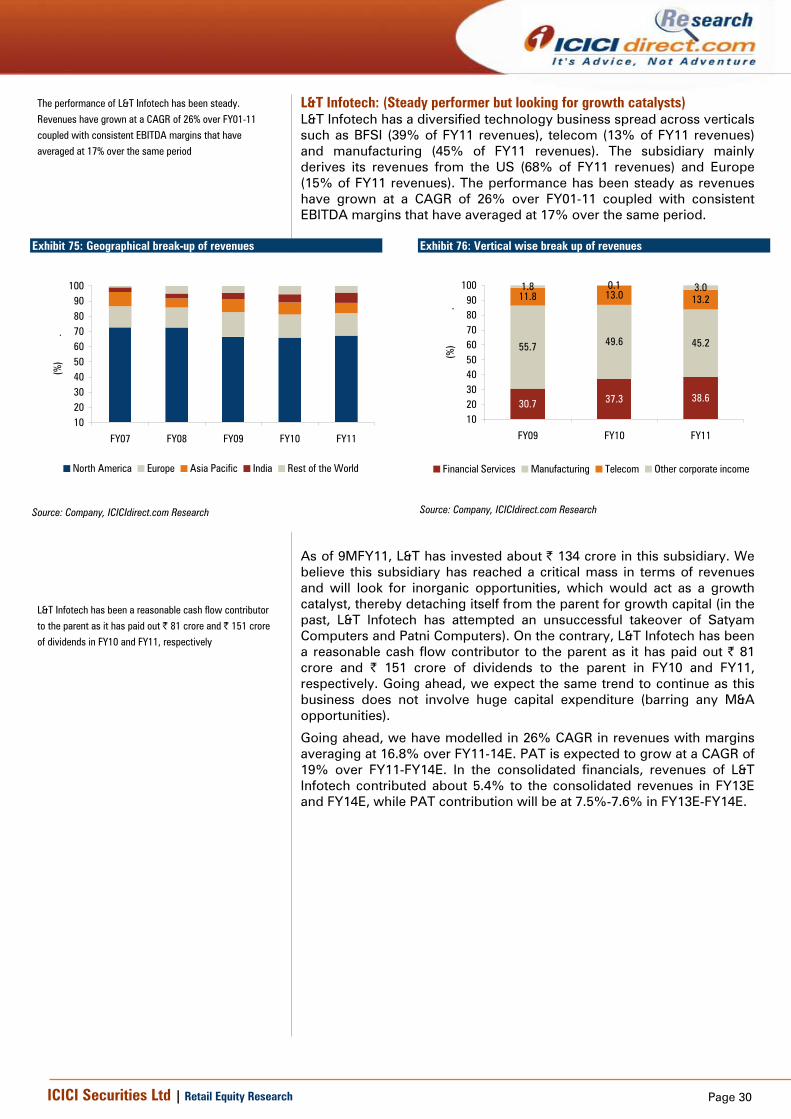

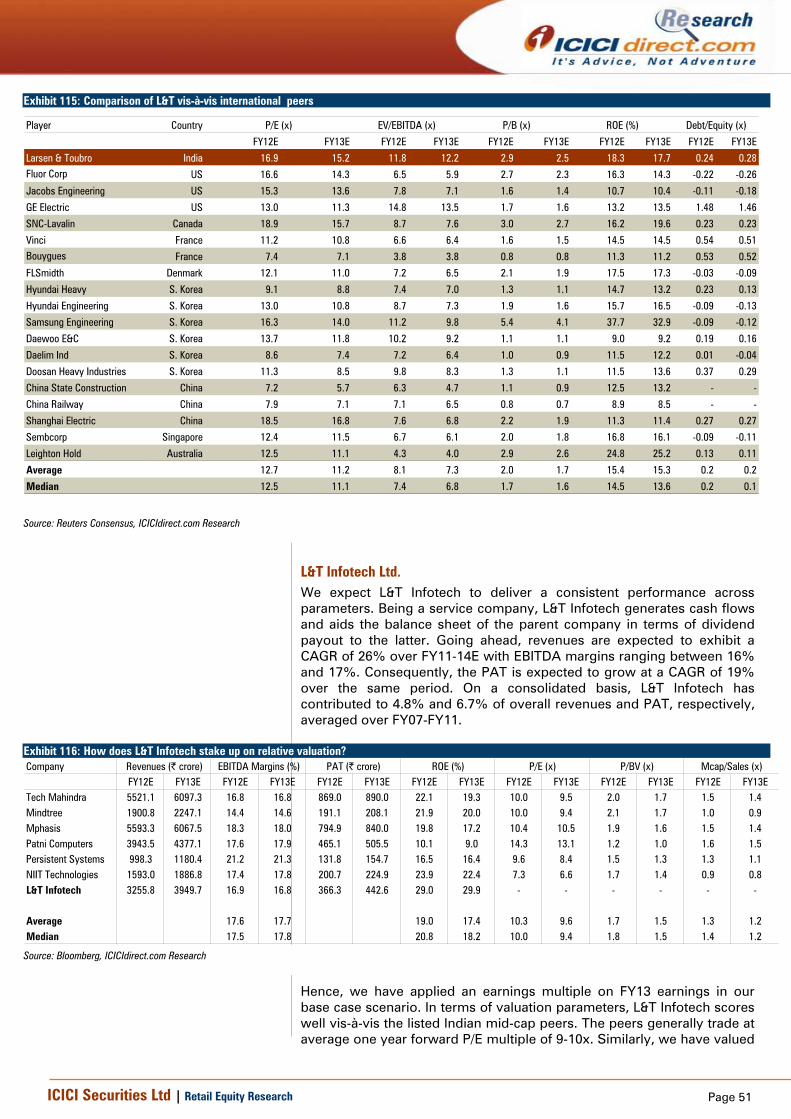

L&T Infotech: (Steady performer but looking for growth catalysts) L&T Infotech has a diversified technology business spread across verticals such as BFSI (39% of FY11 revenues), telecom (13% of FY11 revenues) and manufacturing (45% of FY11 revenues). The subsidiary mainly derives its revenues from the US (68% of FY11 revenues) and Europe (15% of FY11 revenues). The performance has been steady as revenues have grown at a CAGR of 26% over FY01-11 coupled with consistent EBITDA margins that have averaged at 17% over the same period.

Exhibit 75: Geographical break-up of revenues

102030405060708090

100

FY07 FY08 FY09 FY10 FY11

(%)

.

North America Europe Asia Pacific India Rest of the World

Source: Company, ICICIdirect.com Research

Exhibit 76: Vertical wise break up of revenues

30.7 37.3 38.6

55.7 49.6 45.2

11.8 13.0 13.21.8 0.1 3.0

102030405060708090

100

FY09 FY10 FY11(%

)

.

Financial Services Manufacturing Telecom Other corporate income

Source: Company, ICICIdirect.com Research

As of 9MFY11, L&T has invested about | 134 crore in this subsidiary. We believe this subsidiary has reached a critical mass in terms of revenues and will look for inorganic opportunities, which would act as a growth catalyst, thereby detaching itself from the parent for growth capital (in the past, L&T Infotech has attempted an unsuccessful takeover of Satyam Computers and Patni Computers). On the contrary, L&T Infotech has been a reasonable cash flow contributor to the parent as it has paid out | 81 crore and | 151 crore of dividends to the parent in FY10 and FY11, respectively. Going ahead, we expect the same trend to continue as this business does not involve huge capital expenditure (barring any M&A opportunities).

Going ahead, we have modelled in 26% CAGR in revenues with margins averaging at 16.8% over FY11-14E. PAT is expected to grow at a CAGR of 19% over FY11-FY14E. In the consolidated financials, revenues of L&T Infotech contributed about 5.4% to the consolidated revenues in FY13E and FY14E, while PAT contribution will be at 7.5%-7.6% in FY13E-FY14E.

The performance of L&T Infotech has been steady. Revenues have grown at a CAGR of 26% over FY01-11 coupled with consistent EBITDA margins that have averaged at 17% over the same period

L&T Infotech has been a reasonable cash flow contributor

to the parent as it has paid out | 81 crore and | 151 crore

of dividends in FY10 and FY11, respectively

Page 31ICICI Securities Ltd | Retail Equity Research

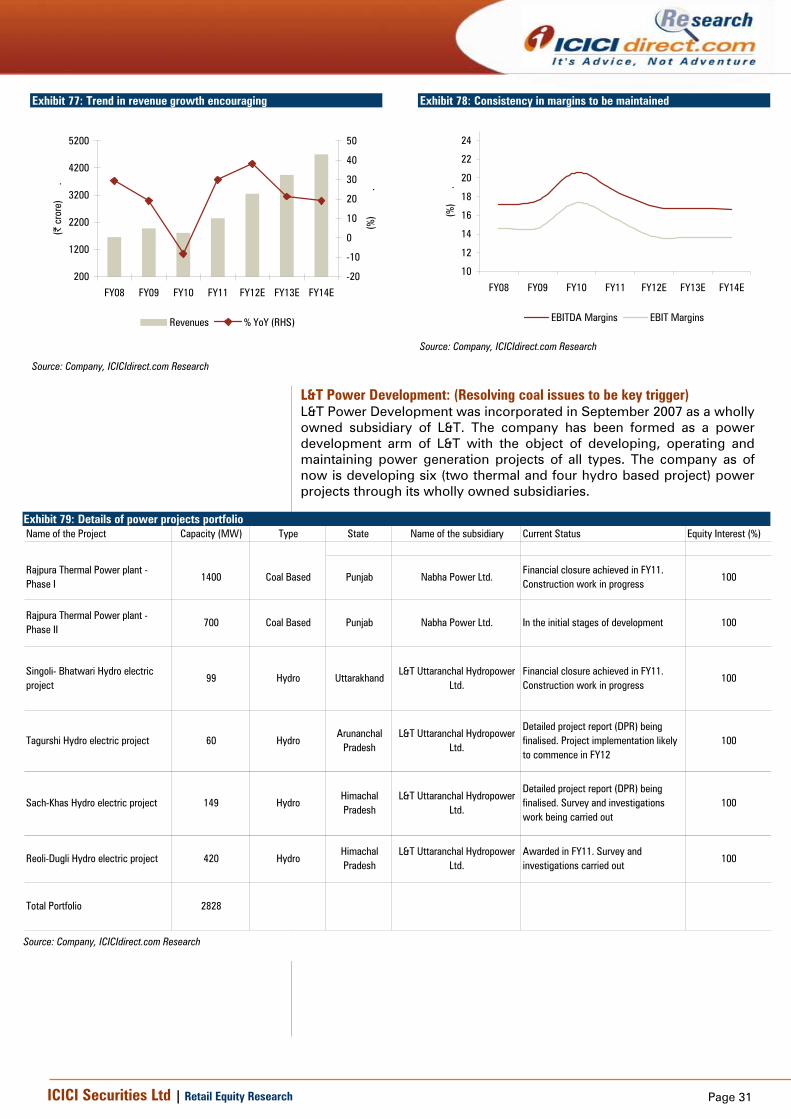

Exhibit 77: Trend in revenue growth encouraging

200

1200

2200

3200

4200

5200

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(| c

rore

)

.

-20

-10

0

10

20

30

40

50

(%)

.

Revenues % YoY (RHS)

Source: Company, ICICIdirect.com Research

Exhibit 78: Consistency in margins to be maintained

10

12

14

16

18

20

22

24

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

(%)

.

EBITDA Margins EBIT Margins

Source: Company, ICICIdirect.com Research

L&T Power Development: (Resolving coal issues to be key trigger) L&T Power Development was incorporated in September 2007 as a wholly owned subsidiary of L&T. The company has been formed as a power development arm of L&T with the object of developing, operating and maintaining power generation projects of all types. The company as of now is developing six (two thermal and four hydro based project) power projects through its wholly owned subsidiaries.

Exhibit 79: Details of power projects portfolio Name of the Project Capacity (MW) Type State Name of the subsidiary Current Status Equity Interest (%)

Rajpura Thermal Power plant - Phase I

1400 Coal Based Punjab Nabha Power Ltd.Financial closure achieved in FY11. Construction work in progress

Rajpura Thermal Power plant - Phase II

700 Coal Based Punjab Nabha Power Ltd. In the initial stages of development

Singoli- Bhatwari Hydro electric project

99 Hydro UttarakhandL&T Uttaranchal Hydropower

Ltd.Financial closure achieved in FY11. Construction work in progress

Detailed project report (DPR) being finalised. Project implementation likely to commence in FY12

L&T Uttaranchal Hydropower Ltd.

Arunanchal Pradesh

Hydro60Tagurshi Hydro electric project

Awarded in FY11. Survey and investigations carried out

L&T Uttaranchal Hydropower Ltd.

Sach-Khas Hydro electric project 149 HydroHimachal Pradesh

Himachal Pradesh

Hydro420Reoli-Dugli Hydro electric project

Total Portfolio 2828

100

100

100

100

100

100

L&T Uttaranchal Hydropower Ltd.

Detailed project report (DPR) being finalised. Survey and investigations work being carried out

Source: Company, ICICIdirect.com Research

Page 32ICICI Securities Ltd | Retail Equity Research

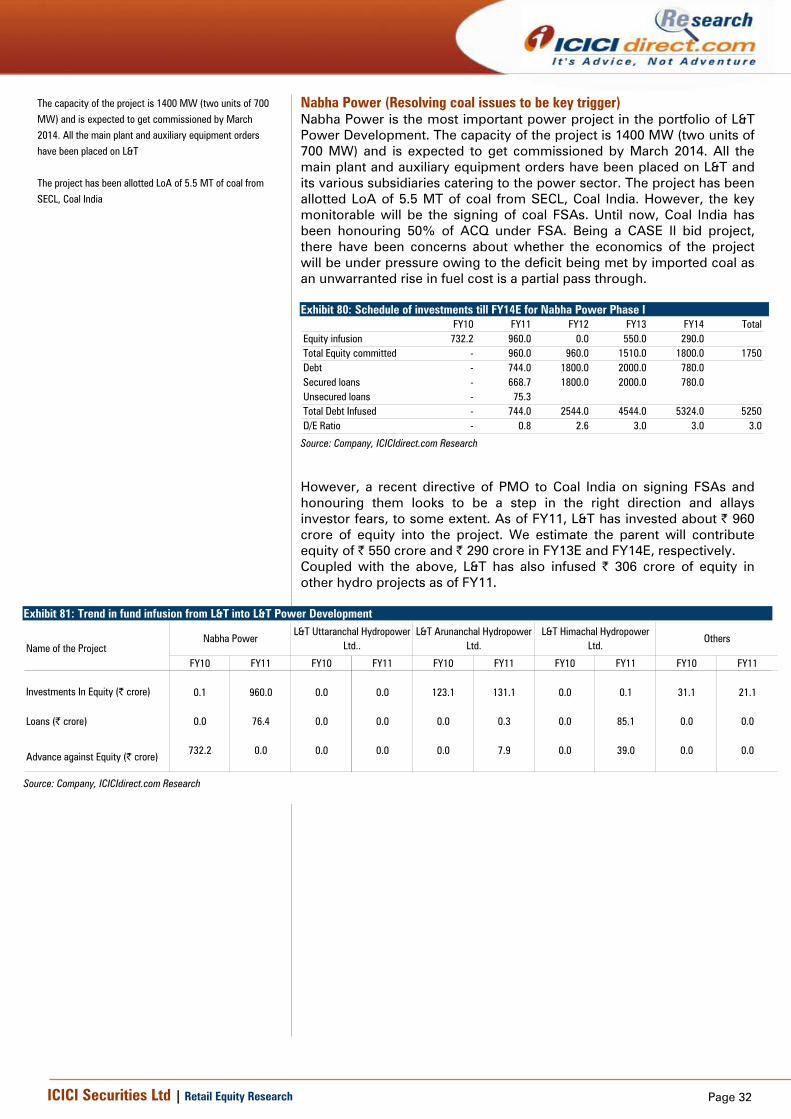

Nabha Power (Resolving coal issues to be key trigger) Nabha Power is the most important power project in the portfolio of L&T Power Development. The capacity of the project is 1400 MW (two units of 700 MW) and is expected to get commissioned by March 2014. All the main plant and auxiliary equipment orders have been placed on L&T and its various subsidiaries catering to the power sector. The project has been allotted LoA of 5.5 MT of coal from SECL, Coal India. However, the key monitorable will be the signing of coal FSAs. Until now, Coal India has been honouring 50% of ACQ under FSA. Being a CASE II bid project, there have been concerns about whether the economics of the project will be under pressure owing to the deficit being met by imported coal as an unwarranted rise in fuel cost is a partial pass through. Exhibit 80: Schedule of investments till FY14E for Nabha Power Phase I

However, a recent directive of PMO to Coal India on signing FSAs and honouring them looks to be a step in the right direction and allays investor fears, to some extent. As of FY11, L&T has invested about | 960 crore of equity into the project. We estimate the parent will contribute equity of | 550 crore and | 290 crore in FY13E and FY14E, respectively. Coupled with the above, L&T has also infused | 306 crore of equity in other hydro projects as of FY11.

Exhibit 81: Trend in fund infusion from L&T into L&T Power Development

Name of the ProjectFY10 FY11 FY10 FY11 FY10 FY11 FY10 FY11 FY10 FY11

The capacity of the project is 1400 MW (two units of 700 MW) and is expected to get commissioned by March 2014. All the main plant and auxiliary equipment orders have been placed on L&T The project has been allotted LoA of 5.5 MT of coal from SECL, Coal India

Page 33ICICI Securities Ltd | Retail Equity Research

L&T IDPL: (Potential value creator but demands capital in medium term)

L&T Infrastructure Development Projects Ltd (L&T IDPL) has been a major player in public private partnership (PPP) projects in India. L&T IDPL currently handles a portfolio of infrastructure assets comprising 17 road projects, three ports and a metro rail project. As of 9MFY12, L&T has infused over | 5600 crore of equity towards this portfolio of assets. Going ahead, we believe infusion in this subsidiary (including L&T Power Development) will range over | 1800 crore -2000 crore in FY13E-14E. Hence, we expect this subsidiary to be a capital guzzler (on L&T’s standalone balance sheet). However, successful commissioning of these projects would provide robust back ended returns in the longer term. There also exists a higher probability of value unlocking in this subsidiary via an IPO, which would be a win-win situation as value unlocking would meet further equity commitments on the one hand and would lessen the burden on L&T’s balance sheet. Exhibit 82: Portfolio of assets Segment No of Projects Other details Project Cost (| crore)Roads & Bridges 17 7171 lane Km 16900Ports 3 45 MTPA 5700Metro Rail 1 71.16 Km 16400Urban Infra 14 25.1 Million Sq. Ft. 15400