Market Models for Forward Swaps Density Processes of Martingale Measures Market Models for CDS Spreads Towards Generic Swap Models Market Models for Forward Swap Rates and Credit Default Swap Spreads Marek Rutkowski School of Mathematics and Statistics University of New South Wales Sydney, Australia Joint work with Libo Li Workshop on Stochastic Analysis and Finance City University of Hong Kong June 29-July 03, 2009 Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Transcript

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Market Models for Forward Swap Ratesand Credit Default Swap Spreads

Marek RutkowskiSchool of Mathematics and Statistics

University of New South WalesSydney, Australia

Joint work with Libo Li

Workshop on Stochastic Analysis and FinanceCity University of Hong Kong

June 29-July 03, 2009

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Outline

1 Forward Swaps

2 Admissible Sets of Forward Swap Rates

3 Market Models of Swap Rates

4 Forward CDS Spreads

5 Market Models of CDS Spreads

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

References on Modelling of Swap Rates

M. Davis and V. Mataix-Pastor: Negative Libor rates in the swap marketmodel. Finance and Stochastics 11 (2007), 181–193.

S. Galluccio, J.-M. Ly, Z. Huang, and O. Scaillet: Theory and calibrationof swap market models. Mathematical Finance 17 (2007), 111–141.

F. Jamshidian: LIBOR and swap market models and measures. Financeand Stochastics 1 (1997), 293–330.

F. Jamshidian: Bivariate support of forward Libor and swap rates.Mathematical Finance 18 (2008), 427–443.

F. Jamshidian: Trivariate support of flat-volatility forward Libor rates.Working paper, University of Twente, 2007.

R. Pietersz and M. van Regenmortel: Generic market models. Financeand Stochastics 10 (2006), 507–528.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

References on Modelling of CDS Spreads

N. Bennani and D. Dahan: An extended market model for creditderivatives. Presented at the international conference StochasticFinance, Lisbon, 2004.

D. Brigo: Constant maturity credit default swap pricing with marketmodels. Working paper, Banca IMI, 2004.

D. Brigo and M. Morini: CDS market formulas and models. Workingpaper, Banca IMI, 2005.

S.L. Ho and L. Wu: Arbitrage pricing of credit derivatives. Workingpaper, HKUST, 2007.

F. Jamshidian: Valuation of credit default swaps and swaptions.Finance and Stochastics 8 (2004), 343–371.

L. Schlögl: Note on CDS market models. Working paper, LehmanBrothers, 2007.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Goals

We would like to address the following issues.1 A unified approach to modelling of market rates.2 A comparison of the top-down and bottom-up approaches.3 Separate study of two related inverse problems.4 Positivity of rates within market models.5 Construction of default times consistent with CDS spreads.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Problems

The following problems arise in the context of market models.1 The choice of admissible families of swaps and/or credit default swaps.2 Computation of Radon-Nikodym densities for martingale measures.3 Computation of dynamics of forward swap rates and CDS spreads under

swap/CDS measures.4 Existence and construction of default times consistent with CDS

spreads.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Families of Forward Swaps

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Forward Swap

Terminology and notation:1 Let 0 < T0 < T1 < · · · < Tn−1 < Tn be a fixed sequence of dates

representing the tenor structure T.2 We denote ai = Ti − Ti−1 for i = 1, . . . , n.3 Let B(t ,Ti ) stand for the price of the zero-coupon bond maturing at Ti .4 Let S = S1, . . . ,Sl be any family of l distinct forward swaps associated

with the tenor structure T.5 Any reset or settlement date for any swap Sj in S belongs to T.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Forward Swap Rates

The forward swap rate κj for the forward swap Sj starting at Tsj and maturingat Tmj equals

κjt = κ

sj ,mjt =

B(t ,Tsj )− B(t ,Tmj )∑mji=sj +1 aiB(t ,Ti )

=P

sj ,mjt

Asj ,mjt

, ∀ t ∈ [0,Tsj ].

where we set

Psj ,mjt = B(t ,Tsj )− B(t ,Tmj ), t ∈ [0,Tsj ],

and

Asj ,mjt =

mj∑i=sj +1

aiB(t ,Ti ), t ∈ [0,Tsj +1].

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Bond Numeraire

Let us choose the bond maturing at Tb as a bond numéraire. In terms of thedeflated bond prices Bb(t ,Ti ) = B(t ,Ti )/B(t ,Tb), i = 1, . . . , n, we obtain

κsj ,mjt =

Bb(t ,Tsj )− Bb(t ,Tmj )∑mji=sj +1 aiBb(t ,Ti )

=P

b,sj ,mjt

Ab,sj ,mjt

, ∀ t ∈ [0,Tsj ∧ Tb].

We call the process Ab,sj ,mj , defined as

Ab,sj ,mjt =

mj∑i=sj +1

aiBb(t ,Ti ), t ∈ [0,Tsj +1 ∧ Tb],

the deflated swap annuity or deflated swap numéraire.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Modelling Issues

We will deal with the following interrelated modelling issues.

1 Under which assumptions the joint dynamics of a given family of swaprates is supported by an arbitrage-free term structure model, whereby a term structure model we mean the joint dynamics of deflated bondprices?

2 How to specify the joint dynamics for a given family of forward swaps interms of “drifts” and “volatilities” under a single probability measure?

3 Under which assumptions the swap rates and/or CDS spreads followpositive processes and the default time can be constructed?

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Swap Equation and Inverse Problem

1 Each forward swap corresponds to the linear equation in which deflatedbond prices are treated as “unknowns”.

2 Specifically, we deal with the following swap equation associated withthe forward swap Sj and the numéraire bond B(t ,Tb)

Bb(t ,Tsj )−mj−1∑

i=sj +1

κsj ,mjt aiBb(t ,Ti )− (1 + κ

sj ,mjt )amj B

b(t ,Tmj ) = 0.

3 The following inverse problem is of interest: describe all families offorward swaps such that the knowledge of the corresponding familyof swap rates is sufficient to uniquely specify the associated familyof non-zero (or positive) deflated bond prices for any choice of thenuméraire bond.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Notation

1 Let xi stand for a generic value of the deflated bond price Bb(t ,Ti ) andlet κj be a generic value of the forward swap rate κj

t = κsj ,mjt .

2 Since xi and κj are aimed to represent generic values of thecorresponding processes in some stochastic model we have that(x0, . . . , xn) ∈ Rn+1 and (κ1, . . . , κl ) ∈ Rl .

3 However, if the bond B(t ,Tb) is chosen to be the numéraire bond then,by the definition of the deflated bond price, the variable xb satisfiesxb = 1 and thus it is more adequate to consider a generic value(x0, . . . , xb−1, xb+1, . . . , xn) ∈ Rn.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Swap Linear System

1 We thus obtain, for every j = 1, . . . , l ,

κj =xsj − xmj∑mj

i=sj +1 aixi.

2 For brevity, we write cj,i = κjai and cj,mj = (1 + κj )amj

−xsj +

mj−1∑i=sj +1

cj,ixi + cj,mj xmj = 0.

3 For a given family S = S1, . . . ,Sl of forward swaps with tenor T, anyfixed b ∈ 0, . . . , n, and an arbitrary (κ1, . . . , κl ) ∈ Rl , we thus deal withthe linear system Cbxb = eb where xb = (x0, . . . , xb−1, xb+1, . . . , xn) isthe vector of n unknowns and eb is some vector of zeros and ones.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Cycles

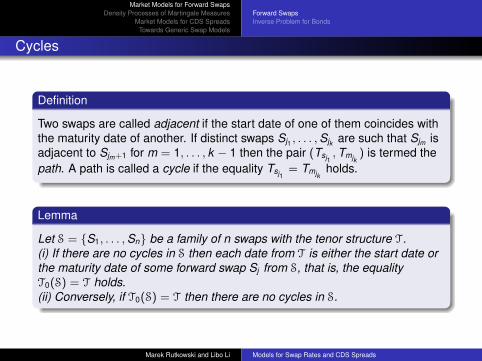

Definition

Two swaps are called adjacent if the start date of one of them coincides withthe maturity date of another. If distinct swaps Sj1 , . . . ,Sjk are such that Sjm isadjacent to Sjm+1 for m = 1, . . . , k − 1 then the pair (Tsj1

,Tmjk) is termed the

path. A path is called a cycle if the equality Tsj1= Tmjk

holds.

Lemma

Let S = S1, . . . ,Sn be a family of n swaps with the tenor structure T.(i) If there are no cycles in S then each date from T is either the start date orthe maturity date of some forward swap Sj from S, that is, the equalityT0(S) = T holds.(ii) Conversely, if T0(S) = T then there are no cycles in S.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

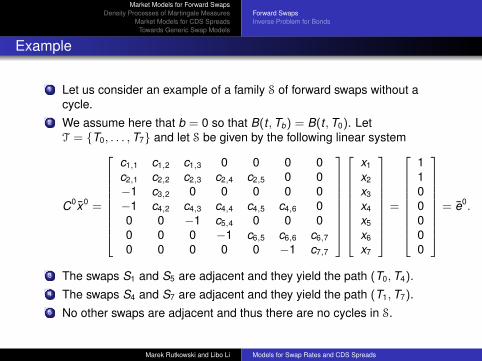

Example

1 Let us consider an example of a family S of forward swaps without acycle.

2 We assume here that b = 0 so that B(t ,Tb) = B(t ,T0). LetT = T0, . . . ,T7 and let S be given by the following linear system

3 The swaps S1 and S5 are adjacent and they yield the path (T0,T4).4 The swaps S4 and S7 are adjacent and they yield the path (T1,T7).5 No other swaps are adjacent and thus there are no cycles in S.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

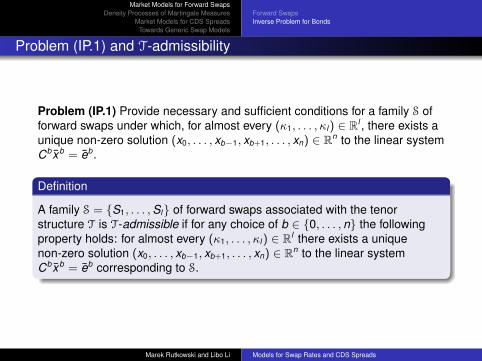

Problem (IP.1) and T-admissibility

Problem (IP.1) Provide necessary and sufficient conditions for a family S offorward swaps under which, for almost every (κ1, . . . , κl ) ∈ Rl , there exists aunique non-zero solution (x0, . . . , xb−1, xb+1, . . . , xn) ∈ Rn to the linear systemCbxb = eb.

Definition

A family S = S1, . . . ,Sl of forward swaps associated with the tenorstructure T is T-admissible if for any choice of b ∈ 0, . . . , n the followingproperty holds: for almost every (κ1, . . . , κl ) ∈ Rl there exists a uniquenon-zero solution (x0, . . . , xb−1, xb+1, . . . , xn) ∈ Rn to the linear systemCbxb = eb corresponding to S.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

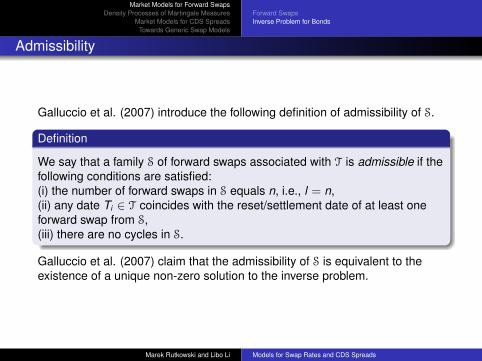

Admissibility

Galluccio et al. (2007) introduce the following definition of admissibility of S.

Definition

We say that a family S of forward swaps associated with T is admissible if thefollowing conditions are satisfied:(i) the number of forward swaps in S equals n, i.e., l = n,(ii) any date Ti ∈ T coincides with the reset/settlement date of at least oneforward swap from S,(iii) there are no cycles in S.

Galluccio et al. (2007) claim that the admissibility of S is equivalent to theexistence of a unique non-zero solution to the inverse problem.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

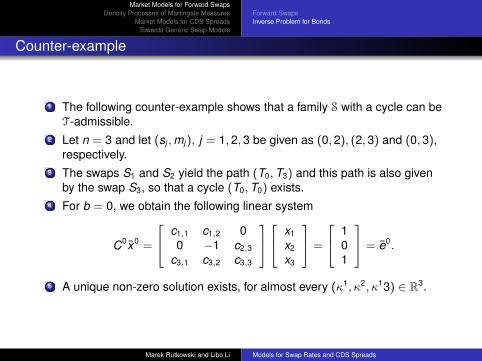

Counter-example

1 The following counter-example shows that a family S with a cycle can beT-admissible.

2 Let n = 3 and let (sj ,mj ), j = 1, 2, 3 be given as (0, 2), (2, 3) and (0, 3),respectively.

3 The swaps S1 and S2 yield the path (T0,T3) and this path is also givenby the swap S3, so that a cycle (T0,T0) exists.

4 For b = 0, we obtain the following linear system

C0x0 =

c1,1 c1,2 00 −1 c2,3

c3,1 c3,2 c3,3

x1

x2

x3

=

101

= e0.

5 A unique non-zero solution exists, for almost every (κ1, κ2, κ13) ∈ R3.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Notation

1 We say that a date Ti , i = 1, . . . , n is the relevant date for the swap Sj

when the term cj,i is non-zero.2 In addition, the date T0 is the relevant date for the swap Sj if it starts at

T0.3 Let T(Sj ) stand for the set of all relevant dates for the swap Sj and let

T0(Sj ) = Tsj ,Tmj .4 We denote

T0(S) – the set of all start/maturity dates for a family S, that is,

T0(S) =l⋃

j=1

T0(Sj ) =l⋃

j=1

Tsj ,Tmj .

T(S) – the set of all relevant dates (i.e., reset/settlement dates) for afamily S, that is,

T(S) =l⋃

j=1

T(Sj ).

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

(T, b)-inadmissibility

Definition

For a fixed b ∈ 0, . . . , n, we say that a cycle Sc ⊂ S is (T, b)-inadmissible ifthe number of dates in T(Sc) \ Tb is strictly less than the number of swapsin Sc .

Lemma

Let S be a family of forward swaps containing a (T, b)-inadmissible cycle Sc

for some b ∈ 0, . . . , n. Then the family S is not T-admissible.

Lemma

Assume that l = n and T(S) = T. If there is no (T, b)-inadmissible cycle in S

for any b ∈ 0, . . . , n then for any b ∈ 0, . . . , n there exists a permutationof S = S1, . . . ,Sn such that all entries on the diagonal of Cb are non-zero.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Forward SwapsInverse Problem for Bonds

Sufficient Conditions

Lemma

Assume that l = n, the equality T(S) = T holds and the graph associatedwith S is connected, that is, for every s,m ∈ 0, . . . , n such that m < s thereexist a path (Ts,Tm) generated by S. Then either:(i) T0(S) = T and there are no cycles in S, or(ii) T0(S) 6= T and there are no (T, b)-inadmissible cycle in S.

Proposition

Assume that l = n, the equality T(S) = T holds and the graph associatedwith S is connected. Then a unique solution to the linear system Cbxb = eb

exists and it is non-zero, for almost all (κ1, . . . , κn) ∈ Rn. Hence the family S

of forward swaps is T-admissible.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

Density Processes Martingale Measures

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

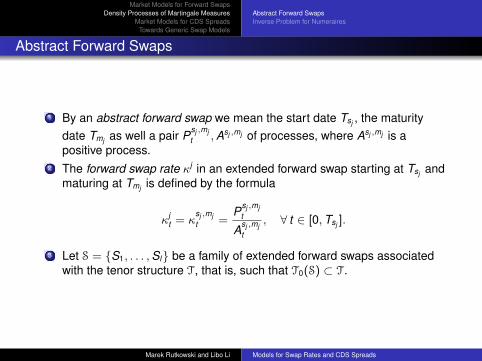

Abstract Forward Swaps

1 By an abstract forward swap we mean the start date Tsj , the maturitydate Tmj as well a pair P

sj ,mjt ,Asj ,mj of processes, where Asj ,mj is a

positive process.2 The forward swap rate κj in an extended forward swap starting at Tsj and

maturing at Tmj is defined by the formula

κjt = κ

sj ,mjt =

Psj ,mjt

Asj ,mjt

, ∀ t ∈ [0,Tsj ].

3 Let S = S1, . . . ,Sl be a family of extended forward swaps associatedwith the tenor structure T, that is, such that T0(S) ⊂ T.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

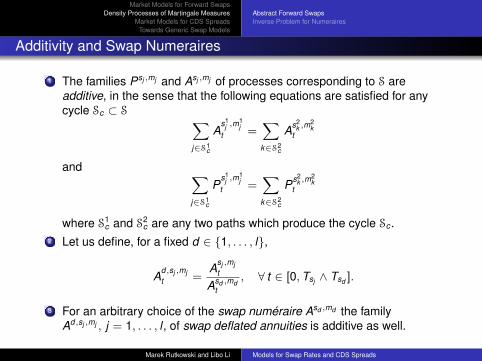

Additivity and Swap Numeraires

1 The families Psj ,mj and Asj ,mj of processes corresponding to S areadditive, in the sense that the following equations are satisfied for anycycle Sc ⊂ S ∑

j∈S1c

As1

j ,m1j

t =∑k∈S2

c

As2k ,m

2k

t

and ∑j∈S1

c

Ps1

j ,m1j

t =∑k∈S2

c

Ps2k ,m

2k

t

where S1c and S2

c are any two paths which produce the cycle Sc .2 Let us define, for a fixed d ∈ 1, . . . , l,

Ad,sj ,mjt =

Asj ,mjt

Asd ,mdt

, ∀ t ∈ [0,Tsj ∧ Tsd ].

3 For an arbitrary choice of the swap numéraire Asd ,md the familyAd,sj ,mj , j = 1, . . . , l , of swap deflated annuities is additive as well.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

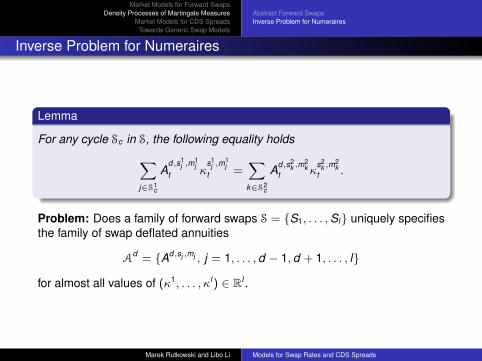

Inverse Problem for Numeraires

Lemma

For any cycle Sc in S, the following equality holds∑j∈S1

c

Ad,s1

j ,m1j

t κs1

j ,m1j

t =∑k∈S2

c

Ad,s2k ,m

2k

t κs2

k ,m2k

t .

Problem: Does a family of forward swaps S = S1, . . . ,Sl uniquely specifiesthe family of swap deflated annuities

Ad = Ad,sj ,mj , j = 1, . . . , d − 1, d + 1, . . . , l

for almost all values of (κ1, . . . , κl ) ∈ Rl .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

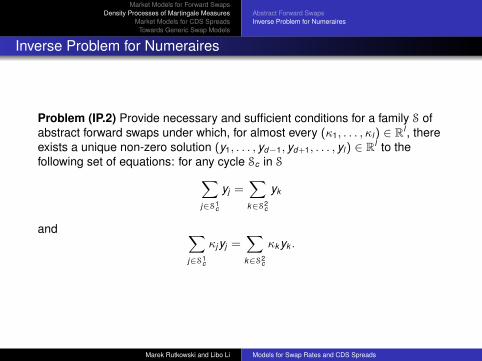

Inverse Problem for Numeraires

Problem (IP.2) Provide necessary and sufficient conditions for a family S ofabstract forward swaps under which, for almost every (κ1, . . . , κl ) ∈ Rl , thereexists a unique non-zero solution (y1, . . . , yd−1, yd+1, . . . , yl ) ∈ Rl to thefollowing set of equations: for any cycle Sc in S∑

j∈S1c

yj =∑k∈S2

c

yk

and ∑j∈S1

c

κjyj =∑k∈S2

c

κk yk .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

Example: Swap Rates

1 Take n = 2 and S = S1,S2,S3 with (sj ,mj ) equal to (0, 1), (1, 2) and(0, 2).

2 For b = 0 we obtain the following linear system parametrized by(κ1, κ2, κ3) ∈ R3

C0x0 =

c1,1 0−1 c2,2

c3,1 c3,2

[ x1

x2

]=

101

= e0.

3 It is easily seen that no solution exists, for almost all (κ1, κ2, κ3) ∈ R3,and thus Problem (IP.1) has no solution.

4 The corresponding Problem (IP.2) has the form, for d = 1,

1 + y2 = y3, κ1 + κ2y2 = κ3y3.

5 For almost all (κ1, κ2, κ3) ∈ R3, the unique solution reads

y2 =κ1 − κ3

κ3 − κ2, y3 =

κ1 − κ2

κ3 − κ2.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

Abstract Forward SwapsInverse Problem for Numeraires

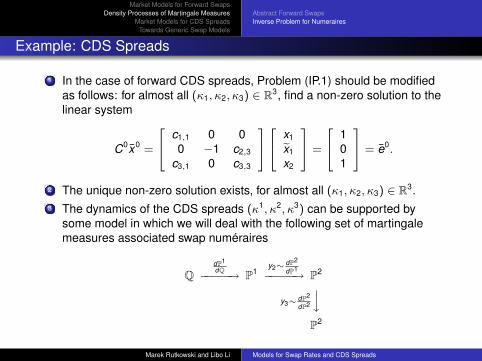

Example: CDS Spreads

1 In the case of forward CDS spreads, Problem (IP.1) should be modifiedas follows: for almost all (κ1, κ2, κ3) ∈ R3, find a non-zero solution to thelinear system

C0x0 =

c1,1 0 00 −1 c2,3

c3,1 0 c3,3

x1

x1

x2

=

101

= e0.

2 The unique non-zero solution exists, for almost all (κ1, κ2, κ3) ∈ R3.3 The dynamics of the CDS spreads (κ1, κ2, κ3) can be supported by

some model in which we will deal with the following set of martingalemeasures associated swap numéraires

QdP1dQ−−−−−→ P1

y2∼ dP2

dP1−−−−−→ P2

y3∼ dP2

dP2

yP2

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Market Models for CDS Spreads

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Set-up and Notation

1 Let (Ω,G,F,Q) be a filtered probability space, where F = (Ft )t∈[0,T ] is afiltration such that F0 is trivial.

2 We assume that the random time τ defined on this space is such thatthe F-survival process Gt = Q(τ > t |Ft ) is positive.

3 The probability measure Q is interpreted as the risk-neutral measure.4 Let 0 < T0 < T1 < · · · < Tn be a fixed tenor structure and let us write

ai = Ti − Ti−1.5 We denote ai = ai/(1− δi ) where δi is the recovery rate if default occurs

between Ti−1 and Ti .6 We denote by D(t ,T ) the default-free discount factor over the time

period [t ,T ].

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Top-down Approach under Deterministic Interest Rate

1 Assume first that the interest rate is deterministic.2 The pre-default forward CDS spread κi corresponding to the

single-period forward CDS starting at time Ti−1 and maturing at Ti

equals

1 + aiκit =

EQ(

D(t ,Ti )1τ>Ti−1∣∣Ft)

EQ(

D(t ,Ti )1τ>Ti∣∣Ft) , ∀ t ∈ [0,Ti−1].

3 Since the interest rate is deterministic, we obtain, for i = 1, . . . , n,

1 + aiκit =

Q(τ > Ti−1 |Ft )

Q(τ > Ti |Ft ), ∀ t ∈ [0,Ti−1],

and thusQ(τ > Ti |Ft )

Q(τ > T0 |Ft )=

i∏j=1

11 + ajκ

jt

, ∀ t ∈ [0,T0].

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

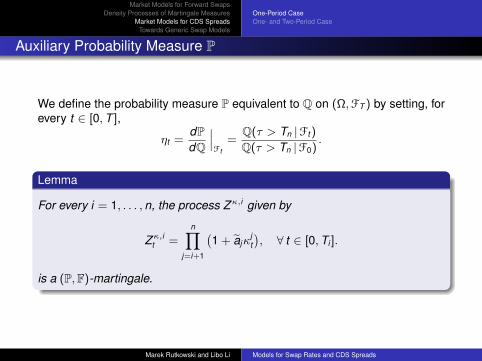

Auxiliary Probability Measure P

We define the probability measure P equivalent to Q on (Ω,FT ) by setting, forevery t ∈ [0,T ],

ηt =dPdQ

∣∣∣Ft

=Q(τ > Tn |Ft )

Q(τ > Tn |F0).

Lemma

For every i = 1, . . . , n, the process Zκ,i given by

Zκ,it =n∏

j=i+1

(1 + ajκ

jt

), ∀ t ∈ [0,Ti ].

is a (P,F)-martingale.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

CDS Martingale Measures

1 For any i = 1, . . . , n we define the probability measure Pi equivalent to P(and thus also to Q) on (Ω,FT ) by setting

dPi

dP

∣∣∣Ft

= Z it = ciZκ,it =

Q(τ > Ti )

Q(τ > Tn)

n∏j=i+1

(1 + ajκ

jt

)2 Note that Zκ,nt = 1 and thus Pn = P.3 Assume that the PRP holds under P = Pn with the Rk -valued spanning

(P,F)-martingale M.4 Then PRP is also valid with respect to F under any probability measure

Pi for i = 1, . . . , n.5 Hence the positive process κi satisfies, for i = 1, . . . , n,

κit = κi

0 +

∫(0,t]

κisσ

is · dΨi (M)s

where σi is an Rk -valued, F-predictable process and Ψi (M) is thePi -Girsanov transform of M.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Dynamics of Forward CDS Spreads

Proposition

Assume that the PRP holds with respect to F under P with the spanning(P,F)-martingale M = (M1, . . . ,Mk ). Assume that the positive processesκi , i = 1, . . . , n are such that the process

Zκ,it =n∏

j=i+1

(1 + ajκ

jt

)is a (P,F)-martingale for i = 1, . . . , n. Then there exist Rk -valued,F-predictable processes σi−1 such that the joint dynamics of processesκi , i = 1, . . . , n under P are given by

dκit =

k∑l=1

κitσ

i,lt dM l

t −n∑

j=i+1

ajκitκ

jt

1 + ajκjt

k∑l,m=1

σi,lt σ

j,mt d [M l,c ,Mm,c ]t

− 1Z i

t−∆Z i

t

k∑l=1

κitσ

i,lt ∆M l

t .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

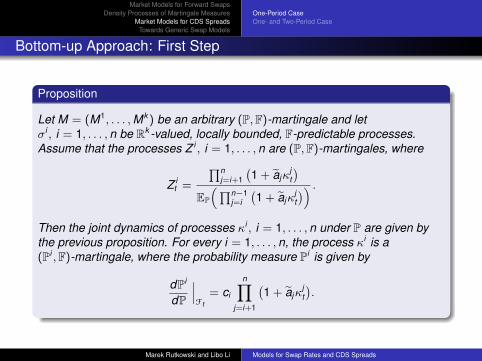

Bottom-up Approach: First Step

Proposition

Let M = (M1, . . . ,Mk ) be an arbitrary (P,F)-martingale and letσi , i = 1, . . . , n be Rk -valued, locally bounded, F-predictable processes.Assume that the processes Z i , i = 1, . . . , n are (P,F)-martingales, where

Z it =

∏nj=i+1

(1 + ajκ

jt

)EP

(∏n−1j=i

(1 + ajκ

jt

)) .Then the joint dynamics of processes κi , i = 1, . . . , n under P are given bythe previous proposition. For every i = 1, . . . , n, the process κi is a(Pi ,F)-martingale, where the probability measure Pi is given by

dPi

dP

∣∣∣Ft

= ci

n∏j=i+1

(1 + ajκ

jt

).

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

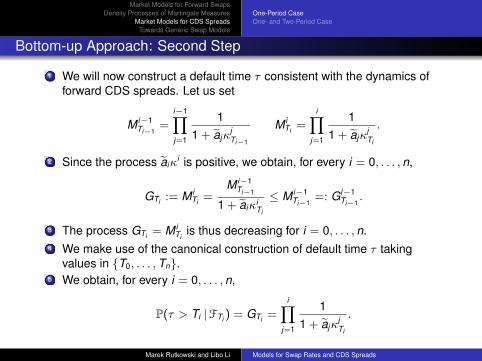

Bottom-up Approach: Second Step

1 We will now construct a default time τ consistent with the dynamics offorward CDS spreads. Let us set

M i−1Ti−1

=i−1∏j=1

11 + ajκ

jTi−1

M iTi =

i∏j=1

11 + ajκ

jTi

.

2 Since the process aiκi is positive, we obtain, for every i = 0, . . . , n,

GTi := M iTi =

M i−1Ti−1

1 + aiκiTi

≤ M i−1Ti−1

=: Gi−1Ti−1

.

3 The process GTi = M iTi

is thus decreasing for i = 0, . . . , n.4 We make use of the canonical construction of default time τ taking

values in T0, . . . ,Tn.5 We obtain, for every i = 0, . . . , n,

P(τ > Ti |FTi ) = GTi =i∏

j=1

11 + ajκ

jTi

.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Top-down Approach under Independence

Assume that we are given a model for Libors (L1, . . . , Ln) whereLi = L(t ,Ti−1) and CDS spreads (κ1, . . . , κn) in which:

1 The default intensity γ generates the filtration Fγ .2 The interest rate process r generates the filtration Fr .3 The probability measure Q is the spot martingale measure.

4 The H-hypothesis holds, that is, FQ→ G, where F = Fr ∨ Fγ .

5 The PRP holds with the (Q,F)-spanning martingale M.

Then it is possible to determine the joint dynamics of Libors and CDSspreads (L1, . . . , Ln, κ1, . . . , κn) under any martingale measure Qi .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Bottom-up Approach under Independence

To construct a model we assume that:1 A martingale M = (M1, . . . ,Mk ) has the PRP with respect to (P,F).2 The family of process Z i given by

Z L,κ,it :=

n∏j=i+1

(1 + ajLjt )(1 + ajκ

jt )

are martingales on the filtered probability space (Ω,F,P) so that thereexists a family of probability measure Pi , i = 1, . . . , n on (Ω,FT ) with the

density function given bydPi

dP= ciZ L,κ,i .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Dynamics of LIBORs and CDS Spreads

The dynamics of Li and κi under Pn with respect to the spanning(P,F)-martingale M are given by

dLit =

k∑l=1

ξi,lt dM l

t −n∑

j=i+1

aj

1 + ajLjt

k∑l,m=1

ξi,lt ξ

j,mt d [M l,c ,Mm,c ]t

−n∑

j=i+1

aj

1 + ajκjt

k∑l,m=1

ξi,lt σ

j,mt d [M l,c ,Mm,c ]t −

1Z i

t∆Z i

t

k∑l=1

ξi,lt ∆M l

t

and

dκit =

k∑l=1

σi,lt dM l

t −n∑

j=i+1

aj

1 + ajLjt

k∑l,m=1

σi,lt ξ

j,mt d [M l,c ,Mm,c ]t

−n∑

j=i+1

aj

1 + ajκjt

k∑l,m=1

σi,lt σ

j,mt d [M l,c ,Mm,c ]t −

1Z i

t∆Z i

t

k∑l=1

σi,lt ∆M l

t .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Top-down Approach: One- and Two-Period Spreads

1 Let (Ω,G,F,Q) be a filtered probability space, where F = (Ft )t∈[0,T ] is afiltration such that F0 is trivial.

2 We assume that the random time τ defined on this space is such thatthe F-survival process Gt = Q(τ > t |Ft ) is positive.

3 The probability measure Q is interpreted as the risk-neutral measure.4 Let 0 < T0 < T1 < · · · < Tn be a fixed tenor structure and let us write

ai = Ti − Ti−1.5 We no longer assume that the interest rate is deterministic.6 We denote by D(t ,T ) the default-free discount factor over the time

period [t ,T ].

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

One-Period CDS Spreads

The one-period forward CDS spread κi = κi−1,i satisfies, for t ∈ [0,Ti−1],

1 + aiκit =

EQ(

D(t ,Ti )1τ>Ti−1∣∣Ft)

EQ(

D(t ,Ti )1τ>Ti∣∣Ft) .

Let Ai−1,i be the one-period CDS annuity

Ai−1,it = ai EQ

(D(t ,Ti )1τ>Ti

∣∣Ft)

and let

P i−1,it = EQ

(D(t ,Ti )1τ>Ti−1

∣∣Ft)− EQ

(D(t ,Ti )1τ>Ti

∣∣Ft).

Then

κit =

P i−1,it

Ai−1,it

, ∀ t ∈ [0,Ti−1].

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

One-Period CDS Spreads

Let Ai−2,i stand for the two-period CDS annuity

Ai−2,it = ai−1 EQ

(D(t ,Ti−1)1τ>Ti−1

∣∣Ft)

+ ai EQ(

D(t ,Ti )1τ>Ti∣∣Ft).

and let

P i−2,it =

i∑j=i−1

(EQ

(D(t ,Tj )1τ>Tj−1

∣∣∣Ft

)− EQ

(D(t ,Tj )1τ>Tj

∣∣∣Ft

)).

The two-period CDS spread κi = κi−2,i is given by the following expression

κit = κi−2,i

t =P i−2,i

t

Ai−2,it

=P i−2,i−1

t + P i−1,it

Ai−2,i−1t + Ai−1,i

t

, ∀ t ∈ [0,Ti−1].

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

One-Period CDS Measures

1 Our aim is to derive the semimartingale decomposition of κi , i = 1, . . . , nand κi , i = 2, . . . , n under a common probability measure.

2 We start by noting that the process An−1,n is a positive (Q,F)-martingaleand thus it defines the probability measure Pn on (Ω,FT ).

3 The following processes are easily seen to be (Pn,F)-martingales

Ai−1,it

An−1,nt

=n∏

j=i+1

aj (κjt − κ

jt )

aj−1(κj−1t − κj

t )=

an

ai

n∏j=i+1

κjt − κ

jt

κj−1t − κj

t

.

4 Given this family of positive (Pn,F)-martingales, we define a family ofprobability measures Pi for i = 1, . . . , n such that κi is a martingaleunder Pi .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Two-Period CDS Measures

1 For every i = 2, . . . , n, the following process is a (Pi ,F)-martingale

Ai−2,it

Ai−1,it

=ai−1EQ

(D(t ,Ti−1)1τ>Ti−1

∣∣Ft)

+ aiEQ(

D(t ,Ti )1τ>Ti∣∣Ft)

EQ(

D(t ,Ti )1τ>Ti∣∣Ft)

= ai−1

(Ai−2,i−1

t

Ai−1,it

+ 1

)

= ai

(κi

t − κit

κi−1t − κi

t

+ 1

).

2 Therefore, we can define a family of the associated probability measuresPi on (Ω,FT ), for every i = 2, . . . , n,

3 It is obvious that κi is a martingale under Pi for every i = 2, . . . , n.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

One and Two-Period CDS Measures

We will summarise the above in the following diagram

QdPndQ−−−−−→ Pn

dPn−1dPn−−−−−→ Pn−1

dPn−2

dPn−1−−−−−→ . . . −−−−−→ P2 −−−−−→ P1

d PndPn

y d Pn−1

dPn−1

y y d P2

dP2

yPn Pn−1 . . . P2

wheredPn

dQ= An−1,n

t

dPi

dPi+1 =Ai−1,i

t

Ai,i+1t

=ai+1

ai

(κi+1

t − κi+1t

κit − κ

i+1t

)d Pi

dPi =Ai−2,i

t

Ai−1,it

= ai

(κi

t − κit

κi−1t − κi

t

+ 1

).

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

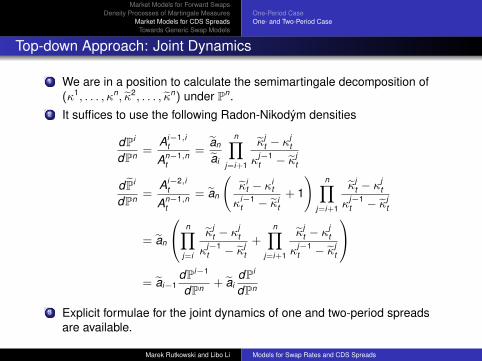

Top-down Approach: Joint Dynamics

1 We are in a position to calculate the semimartingale decomposition of(κ1, . . . , κn, κ2, . . . , κn) under Pn.

2 It suffices to use the following Radon-Nikodým densities

dPi

dPn =Ai−1,i

t

An−1,nt

=an

ai

n∏j=i+1

κjt − κ

jt

κj−1t − κj

t

d Pi

dPn =Ai−2,i

t

An−1,nt

= an

(κi

t − κit

κi−1t − κi

t

+ 1

)n∏

j=i+1

κjt − κ

jt

κj−1t − κj

t

= an

n∏j=i

κjt − κ

jt

κj−1t − κj

t

+n∏

j=i+1

κjt − κ

jt

κj−1t − κj

t

= ai−1

dPi−1

dPn + aidPi

dPn

3 Explicit formulae for the joint dynamics of one and two-period spreadsare available.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Bottom-up Approach: Postulates

1 The processes κ1, . . . , κn and κ1, . . . , κn are F-adapted.2 For every i = 0, . . . , n the process Zκ,i

Zκ,it =cn

ci

n∏j=i+1

κjt − κ

jt

κj−1t − κj

t

is a positive (P,F)-martingale where c1, . . . , cn are normalizingconstants.

3 For every i = 0, . . . , n the process Z κ,i given by the formula

Z κ,i = Zκ,i + Zκ,i−1 =κi−1 − κi

κi−1 − κi Zκ,i

is a positive (P,F)-martingale.4 The process M = (M1, . . . ,Mk ) is the (P,F)-spanning martingale.5 Probability measures Pi and Pi , i = 1, . . . , n have the density processes

Zκ,i and Z κ,i , i = 1, . . . , n. In particular, Pn = P since Zκ,n = 1.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

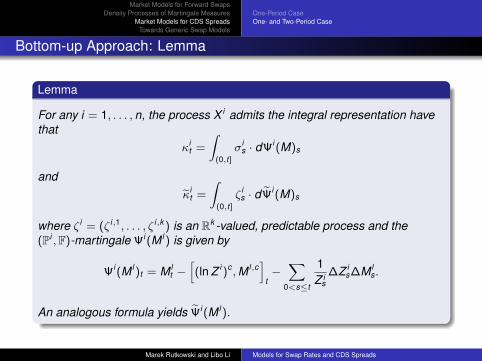

Bottom-up Approach: Lemma

Lemma

For any i = 1, . . . , n, the process X i admits the integral representation havethat

κit =

∫(0,t]

σis · dΨi (M)s

andκi

t =

∫(0,t]

ζ is · dΨi (M)s

where ζ i = (ζ i,1, . . . , ζ i,k ) is an Rk -valued, predictable process and the(Pi ,F)-martingale Ψi (M l ) is given by

Ψi (M l )t = M lt −[(ln Z i )c ,M l,c

]t−∑

0<s≤t

1Z i

s∆Z i

s∆M ls.

An analogous formula yields Ψi (M l ).

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Bottom-up Approach: Joint Dynamics

Proposition

The semimartingale decomposition of the (Pi ,F)-spanning martingale Ψi (M)under the probability measure Pn = P is given by, for i = 1, . . . , n,

Ψi (M)t = Mt −n∑

j=i+1

∫(0,t]

(κj−1s − κj

s) ζ js · d [Mc ]s

(κjs − κj

s)(κj−1s − κj

s)−

n∑j=i+1

∫(0,t]

σjs · d [Mc ]s

κjs − κj

s

−n∑

j=i+1

∫(0,t]

σj−1s · d [Mc ]s

κj−1s − κj

s

−∑

0<s≤t

1Z i

s∆Z i

s∆Ms.

An analogous formula holds for Ψi (M). Hence the joint dynamics of theprocess (κ1, . . . , κn, κ2, . . . , κn) under P = Pn are explicitly known.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

One-Period CaseOne- and Two-Period Case

Towards Generic Swap Models

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

PostulatesCommentsVolatilitiesConclusions

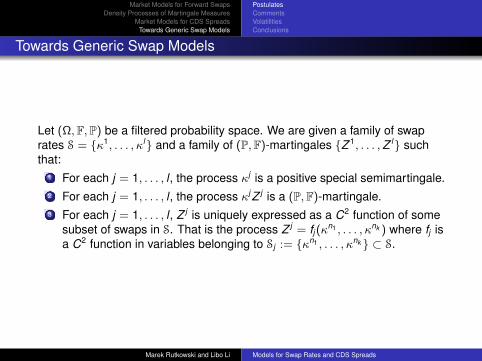

Towards Generic Swap Models

Let (Ω,F,P) be a filtered probability space. We are given a family of swaprates S = κ1, . . . , κl and a family of (P,F)-martingales Z 1, . . . ,Z l suchthat:

1 For each j = 1, . . . , l , the process κj is a positive special semimartingale.2 For each j = 1, . . . , l , the process κjZ j is a (P,F)-martingale.3 For each j = 1, . . . , l , Z j is uniquely expressed as a C2 function of some

subset of swaps in S. That is the process Z j = fj (κn1 , . . . , κnk ) where fj isa C2 function in variables belonging to Sj := κn1 , . . . , κnk ⊂ S.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

PostulatesCommentsVolatilitiesConclusions

Comments

1 Assumption 1 forces the semi-martingale decomposition of κj to beuniquely determined.

2 Assumption 2 gives the existence of a family of probability measuresP1, . . . ,Pl, for which κj is a martingale under Pj .

3 Assumption 3 together with the fact that the process Z j is a(P,F)-martingale implies that Z j has the following integral representation

Z jt =

nk∑i=n1

∫[0,t)

∂fj∂xi

(κn1s , . . . , κ

nks )d(κi )m

s ,

where (κi )m stands for the (unique) martingale part of κi .

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

PostulatesCommentsVolatilitiesConclusions

Volatilities

1 We claim that the semi-martingale decomposition of a swap rate processκn ∈ S can be chosen under P by choosing a family of “volatility”processes.

2 Hence κj = N j ∈M(Pj ,F) and by inverse Girsanov’s transform themartingale part of κn must have the following representation under P

(κj )m = N jt −∫

(0,t]Z j

s d[ 1

Z j ,Nj]

s= Nt

or, equivalently, the semi-martingale decomposition of κn under P isgiven by

κj = N jt = Nt +

∫(0,t]

Z js d[ 1

Z j ,Nj]

s

where N is unique since the Girsanov transform is a bijection.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads

Market Models for Forward SwapsDensity Processes of Martingale Measures

Market Models for CDS SpreadsTowards Generic Swap Models

PostulatesCommentsVolatilitiesConclusions

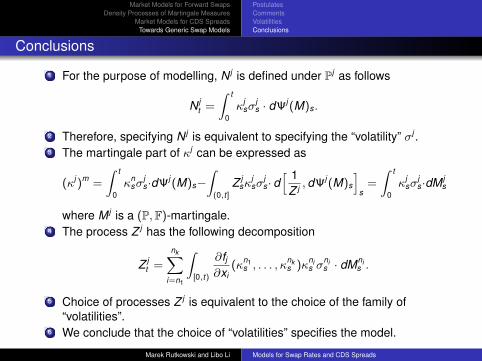

Conclusions

1 For the purpose of modelling, N j is defined under Pj as follows

N jt =

∫ t

0κj

sσjs · dΨj (M)s.

2 Therefore, specifying N j is equivalent to specifying the “volatility” σj .3 The martingale part of κj can be expressed as

(κj )m =

∫ t

0κn

sσjs·dΨj (M)s−

∫(0,t]

Z jsκ

jsσ

js· d[ 1

Z j , dΨj (M)s

]s

=

∫ t

0κj

sσjs·dM j

s

where M j is a (P,F)-martingale.4 The process Z j has the following decomposition

Z jt =

nk∑i=n1

∫[0,t)

∂fj∂xi

(κn1s , . . . , κ

nks )κ

nis σ

nis · dMni

s .

5 Choice of processes Z j is equivalent to the choice of the family of“volatilities”.

6 We conclude that the choice of “volatilities” specifies the model.

Marek Rutkowski and Libo Li Models for Swap Rates and CDS Spreads