26

Jakarta, May 2015 The Effect of US Dollar Reinforcement to Indonesia Capital Market

| Date post: | 13-Aug-2015 |

| Category: |

Presentations & Public Speaking |

| Upload: | zola-azaria |

| View: | 307 times |

| Download: | 1 times |

Jakarta, May 2015

The Effect of US Dollar Reinforcement to Indonesia Capital Market

IDX Latest Highlights

-

600

1,200

1,800

2,400

3,000

3,600

4,200

4,800

5,400

Jakarta Composite Index and Capital Market Milestones

3

*) 22 May 2015

1992 – 22 May 2015

02-Jan-2013New Trading Hours

4,254.816

1992 1993 1994 19961995 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

30-Nov-2007Consolidation of the SSX

into JSX to become the IDX2,688.332

6-Oct-2004Launching of Stock Option

856.060

28-Mar-2002Implementation of

Remote Trading481.775

9-Sep-2002T+4 to T+3 Settlement430.271

21-Jul-2000Scriptless Trading

512.617

23-Dec-1997Founding ofKSEI397.031

23-Jul-1997Financial Crisis

718.189

6-Aug-1996Founding of KPEI

554.790

24-Jul-1995 Merging process of SSX into

Bursa Paralel Indonesia509.532

22-May-1995JATS

461.389

13-Jul-1992Privatization of JSX321.544

8-Oct-2008Suspend Trading

1,451.669

7-Apr-2015Highest Index

5,523.290

2-Mar-2009JATS Next G 1,256.109

28-Oct-2008Lowest Index in 2008

1,111.390

2010 2011 2012 2014

06-Jan-2014New Lot Size & Tick Size

4,202.809

2013 2015*

Source: IDX

Jakarta Composite Index : Annual Return

4

Source: IDX

1000.233

1162.635

1805.523

2745.826

1355.408

2,534.356

3,703.512

3821.992

4316.687

4,274.177

5,226.947

5,315.153

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

55.30% 52.08%

2004 2005 2006 2007 2008 2009

86.98%-50.64%

3.20%

2010 2011

*) 22 May 2015

44.56% 16.24%

2012

46.13% 12.94%

2013

2004 – 22 May 2015

-0.98%

2014

22.29%

2015*

1.69%

5Average Daily Trading and Market Capitalization

*) 22 May 2015

Volume (in Million Share) Value (in IDR Billion)

Frequency (in Times) Market Capitalization ( in IDR Trillion)

3,283

6,090 5,432

4,873 4,284

5,503 5,484 6,491

2008 2009 2010 2011 2012 2013 2014 2015*

4,436 4,046 4,801 4,953 4,537

6,238 6,006 6,633

2008 2009 2010 2011 2012 2013 2014 2015*

55,905 87,040

105,790 113,454 121,712 153,686

212,635 228,146

2008 2009 2010 2011 2012 2013 2014 2015*

1,076

2,019

3,247 3,5374,127 4,219

5,228 5,363

2008 2009 2010 2011 2012 2013 2014 2015*

Source: IDX

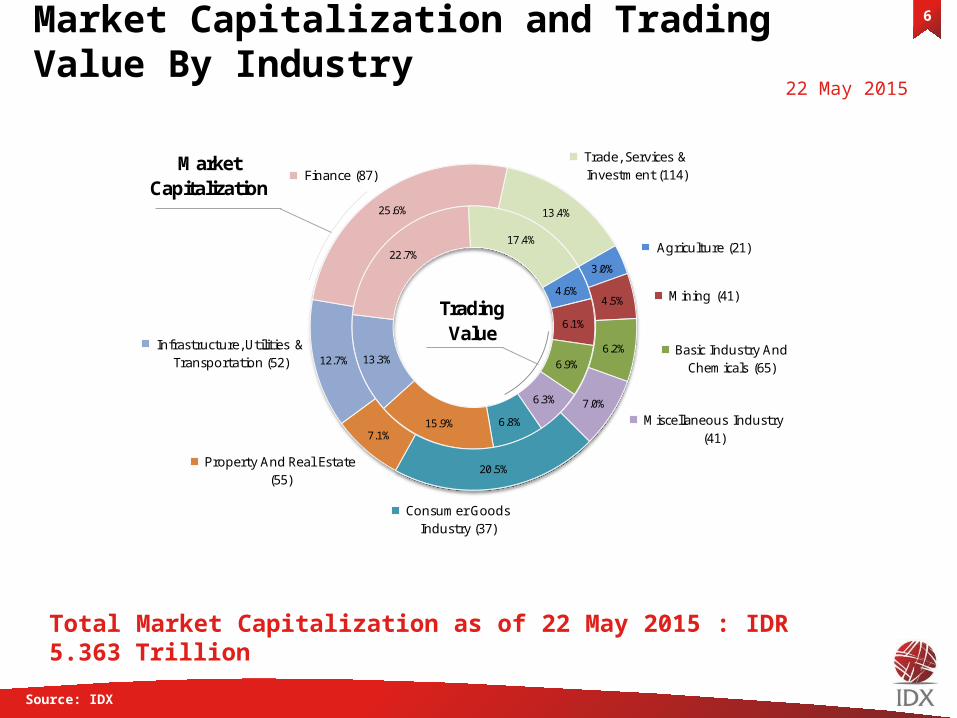

Market Capitalization and Trading Value By Industry

6

Total Market Capitalization as of 22 May 2015 : IDR 5.363 Trillion

Source: IDX

4.6%

6.1%

6.9%

6.3%

6.8%15.9%

13.3%

22.7%17.4%

3.0%

4.5%

6.2%

7.0%

20.5%

7.1%

12.7%

25.6% 13.4%

Agriculture (21)

Mining (41)

Basic Industry And Chemicals (65)

Miscellaneous Industry (41)

Consumer Goods Industry (37)

Property And Real Estate (55)

Infrastructure, Utilities & Transportation (52)

Finance (87)Trade, Services & Investment (114)

MarketCapitalization

TradingValue

22 May 2015

[S] Sharia Compliant Stock

Top 20 in Market Capitalization7

Source: IDX

Market Capitalization

(in Trillion Rp)

1. BBCA Bank Central Asia Tbk. 350.26 6.53

2. UNVR Unilever Indonesia Tbk. [S] 334.00 6.23

3. HMSP HM Sampoerna Tbk. 317.55 5.92

4. BBRI Bank Rakyat Indonesia (Persero) Tbk. 307.72 5.74

5. ASII Astra International Tbk. [S] 306.66 5.72

6. TLKM Telekomunikasi Indonesia (Persero) Tbk. [S] 289.30 5.39

7. BMRI Bank Mandiri (Persero) Tbk. 263.92 4.92

8. BBNI Bank Negara Indonesia (Persero) Tbk. 130.62 2.44

9. PGAS Perusahaan Gas Negara (Persero) Tbk. [S] 101.81 1.90

10. GGRM Gudang Garam Tbk. 90.58 1.69

11. UNTR United Tractors Tbk. [S] 86.82 1.62

12. KLBF Kalbe Farma Tbk. [S] 86.25 1.61

13. INTP Indocement Tunggal Prakarsa Tbk. [S] 82.55 1.54

14. ICBP Indofood CBP Sukses Makmur Tbk. [S] 81.20 1.51

15. SMGR Semen Indonesia (Persero) Tbk. [S] 77.85 1.45

16. EMTK Elang Mahkota Teknologi Tbk. 64.72 1.21

17. INDF Indofood Sukses Makmur Tbk. [S] 60.37 1.13

18. CPIN Charoen Pokphand Indonesia Tbk. [S] 52.56 0.98

19. LPPF Matahari Department Store Tbk. 51.21 0.95

20. JSMR Jasa Marga (Persero) Tbk. 44.71 0.83

3,180.65 59.31

5,363.00

%

Market Capitalization of The 20 Stocks

Total IDX

No. Code Company

22 May 2015

8

Dec-10

May-11

Sep-11

Jan-12

May-12

Sep-12

Jan-13

May-13

Sep-13

Jan-14

May-14

Sep-14

Jan-15

May-15

0

50

100

150

200

250

300

350

Agriculture

Mining

Miscellaneous Industry

Consumer Goods Industry

Property, Real Estate And Building Construction

Basic Industry and Chem-ical

Infrastructure, Utilities, & Transportation

Finance

Trade, Services & Investment

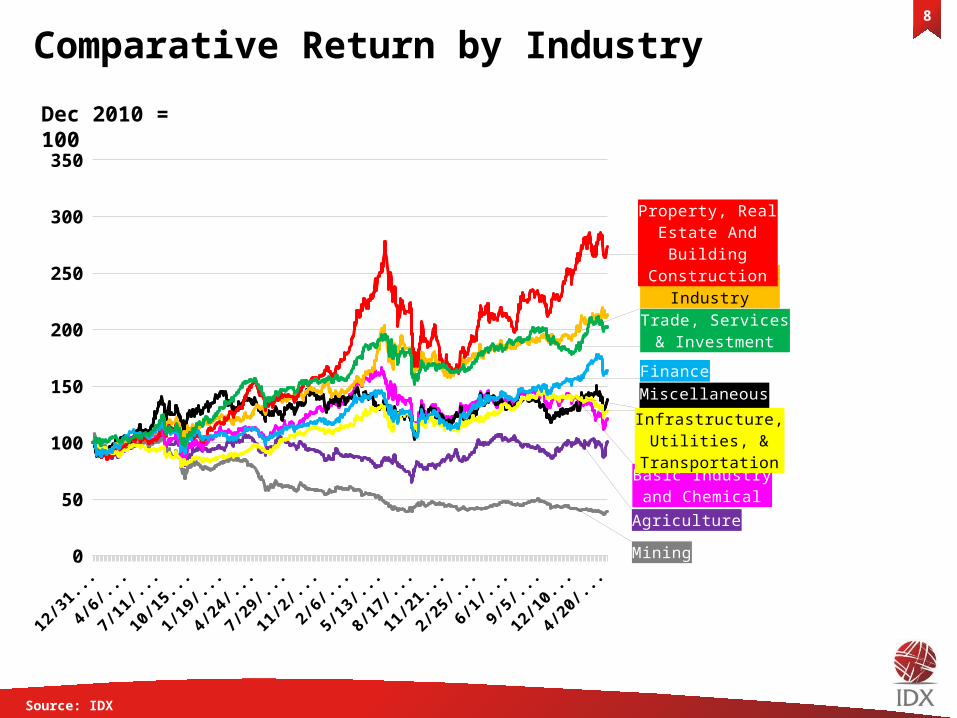

Comparative Return by Industry

Dec 2010 = 100

Source: IDX

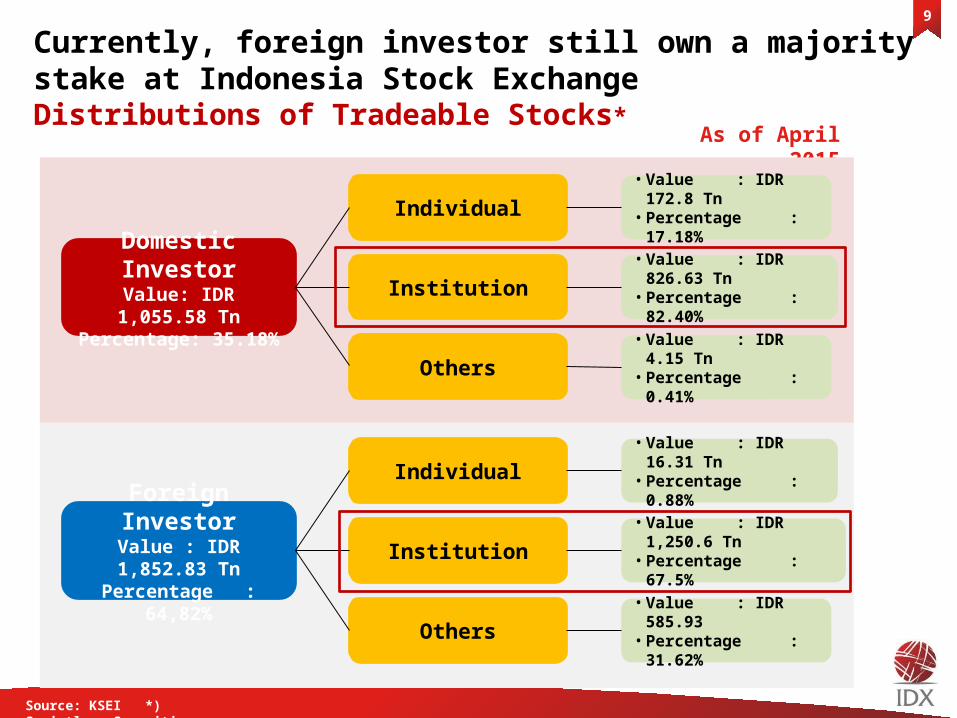

Currently, foreign investor still own a majority stake at Indonesia Stock ExchangeDistributions of Tradeable Stocks*

9

As of April 2015

Source: KSEI *) Scriptless Securities

Domestic InvestorValue: IDR 1,055.58 Tn

Percentage: 35.18%

Foreign InvestorValue : IDR 1,852.83 Tn

Percentage : 64,82%

Individual

Institution

Others

• Value : IDR 172.8 Tn

• Percentage : 17.18%

• Value : IDR 826.63 Tn

• Percentage : 82.40%

• Value : IDR 4.15 Tn

• Percentage : 0.41%

Individual

Institution

Others

• Value : IDR 16.31 Tn

• Percentage : 0.88%

• Value : IDR 1,250.6 Tn

• Percentage : 67.5%

• Value : IDR 585.93• Percentage : 31.62%

The Effect of US Dollar Reinforcement To Indonesia Capital Market

JCI and IDR : Trend Comparison

11

Source: Bloomberg

• The rupiah has fallen by more than 5% this year, a contrasting performance compared to the Jakarta Composite Index (JCI) which achieved highest level in April, 7Th 2015 at 5,523.29.

• Unexpectedly, JCI dropped 7.9% from its highest level to 5,086.43 in the end of April.• Nevertheless, JCI ready to rebound gradually after tumbling 400 points.

2-Ja

n8-

Jan

14-Ja

n20

-Jan

26-Ja

n1-

Feb

7-Fe

b13

-Feb

19-F

eb25

-Feb

3-M

ar9-

Mar

15-M

ar21

-Mar

27-M

ar2-

Apr

8-Ap

r14

-Apr

20-A

pr26

-Apr

2-M

ay8-

May

14-M

ay20

-May

4,6004,7004,8004,9005,0005,1005,2005,3005,4005,5005,600 11,800

12,000

12,200

12,400

12,600

12,800

13,000

13,200

13,400

5,313.21

13,150

IHSG (LHS) IDR/USD (RHS)

What happened to JCI in recent weeks ?Company financial performance was below expectation

12

Q1-2014 Q1-2015 Q1-2014 Q1-2015

BBRI PT Bank Rakyat Indonesia (Persero) Tbk 5.93 6.14 16.7% 3.5%

BMRI PT Bank Mandiri (Persero) Tbk 4.92 5.14 14.4% 4.3%

BBCA PT Bank Central Asia Tbk 3.70 4.10 28.0% 10.8%

ASII PT Astra International Tbk 4.73 3.99 9.7% -15.6%

TLKM PT Telekomunikasi Indonesia (Persero) Tbk 3.65 3.81 4.9% 4.4%

UNVR PT Unilever Indonesia Tbk 1.36 1.59 -4.9% 16.9%

HMSP PT HM Sampoerna Tbk 2.75 2.89 5.4% 5.1%

BBNI PT Bank Negara Indonesia (Persero) Tbk 2.39 2.82 15.6% 17.7%

PGAS PT Perusahaan Gas Negara (Persero) Tbk 2.09 1.40 -18.7% -32.9%

GGRM PT Gudang Garam Tbk 1.42 1.28 35.3% -9.6%

INDF PT Indofood Sukses Makmur Tbk 1.37 0.87 89.8% -36.5%

SMGR PT Semen Indonesia (Persero) Tbk 1.30 1.19 4.8% -8.5%

ICBP PT Indofood CBP Sukses Makmur Tbk 0.69 0.80 7.0% 15.7%

AALI PT Astra Agro Lestari Tbk 0.78 0.16 120% -80.0%

KLBF PT Kalbe Farma Tbk 0.49 0.53 11% 7.1%

* earning growth down, up or slowed compared to previous quarter

CompaniesQuarterly Earning (Rp Trillion) Earning Growth (%)

Code Changes*

Source: IDX

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0

1

2

3

4

5

6

7

8

5.14

5.03 4.92

5.01

4.71

% YoY

Weak companies performance was also translated into economic slowdown in the Q1-2015

13

Source: Statistics Indonesia

Average Indonesia economic

growth for 10 years is 5.73%

“Indonesia is one of only few countries survive Global Economic Slowdown in 2008-9 without falling into a recession”

Indonesia economy in the first quarter 2015 is recorded 4.71% (yoy) or lower than previous quarter at 5.01% (yoy) and analyst forecast at 4.94%. This is the slowest economic growth since Q3-2009 or during the global financial crisis.

Almost all sectors point to flat-to-lower growth. The main driver was mining sector as it contracted 2.32% yoy in 1Q15 from 2.22% yoy in 4Q14 particularly caused by coal

Other sectors contributing to growth slowdown were wholesale & retail trade, manufacturing, and construction

Furthermore, economic slowdown also contributed by weak government expenditure & investment activities

Brazilian Real

Turkish Lira

Bulgarian Lev

Romanian Leu

Czech Koruna

Indonesian Rupiah

Argentine Peso

Peruvian New Sol

Colombian Peso

Hungarian Forint

Polish Zloty

Malaysian Ringgit

Mexican Peso

South African Rand

Thai Baht

Indian Rupee

Singapore Dollar

South Korean Won

Hong Kong Dollar

Chinese Renminbi

Chilean Peso

Philippine Peso

Taiwanese Dollar

Russian Ruble

-11.49

-8.95

-7.71

-7.04

-6.60

-5.58

-5.55

-5.50

-4.81

-4.65

-3.11

-2.89

-2.55

-1.88

-1.52

-0.96

-0.70

-0.27

0.03

0.14

0.29

0.58

3.62

21.77

Dec-12

Mar-13

May-13

Jul-13

Sep-13

Nov-13

Jan-14

Mar-14

May-14

Jul-14

Sep-14

Nov-14

Jan-15

Mar-15

May-15

78

80

82

84

86

88

90

92

94

96

98

100

102

Indonesia economic slowdown was overshadowed by the trend of US dollar appreciation

14

Source: Bloomberg

Currency changes against US Dollar31 Dec 2014 – 21 May 2015 (%) US Dollar Index* Movement

USD has appreciated around 19.4% against world's major currencies since early 2013

*) The US Dollar Index is an index that measures the relative value of the US dollar against a basket of currencies of major countries includeEuro (EUR), Japanese Yen (JPY), Poundsterling (GBP), Canadian Dollar (CAD), Swedish Krona (SEK), and Swiss Franc (CHF)

Average US Dollar Index Dec 2012-21 May 2015 :

84.2

+19.4%

How is the impact on Indonesia capital market ? (1/2)Rupiah depreciation provides additional risk to foreign investor

15

Source: Bloomberg

60

70

80

90

100

110

120

130

140

150

160143.2

97.56

JCI in IDR (Domestic Investor)

JCI in USD (Foreign Investor)

Dec 2010 = 100

16

Source: IDX

How is the impact on Indonesia capital market ? (2/2)Rupiah depreciation has raised concern on recent capital outflow

Figures in Billion Rupiah

5,695

11,242

1,828 722

(356)

(20,132)

(2,480)

(5,695)

(365)(1,981)

(3,859)(5,266)

2,330

7,817

14,476

8,672 8,089

2,738

13,070

(1,317)

(7,402)

(3,202)

5,281

(7,954)

212

10,608

(5,426)

5,896

(3,018)2011

2012

2013

J an Feb Mar Apr

May Jun Jul Aug Sep Oct Nov Dec20

14 J an Feb Mar Apr May Jun Jul

Aug Sep Oct

Nov

Dec

2015 J an Feb

Mar

Apr

May

24,290

15,881

(20,647)

42,598

8,272

Going forward, volatility in the financial sectors are still in placeMarkets are assessing the Fed policy on potential rate hikes – Fed Fund Rate (timing, size, & pace)

17

Source: Bloomberg, Fed minutes

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '150

1

2

3

4

5

6

7

8

Fed Fund Rate

“The Fed had raised FFR up to 400 bps before The U.S. subprime mortgage crisis”

• In the latest FOMC meeting, majority of members has reduced the FFR projection in 2015 to 0.625 %, lower than previous projection of 1.125%.

• Meanwhile, FFR projection in 2016 is also lowered to 1.875% compared to the previous projection of 2.5%.

%

The increase in FFR will lift the short term volatility in the stock market

18

The period in which The Fed start to reduce its assets purchase program and raising the plan to increase FFR

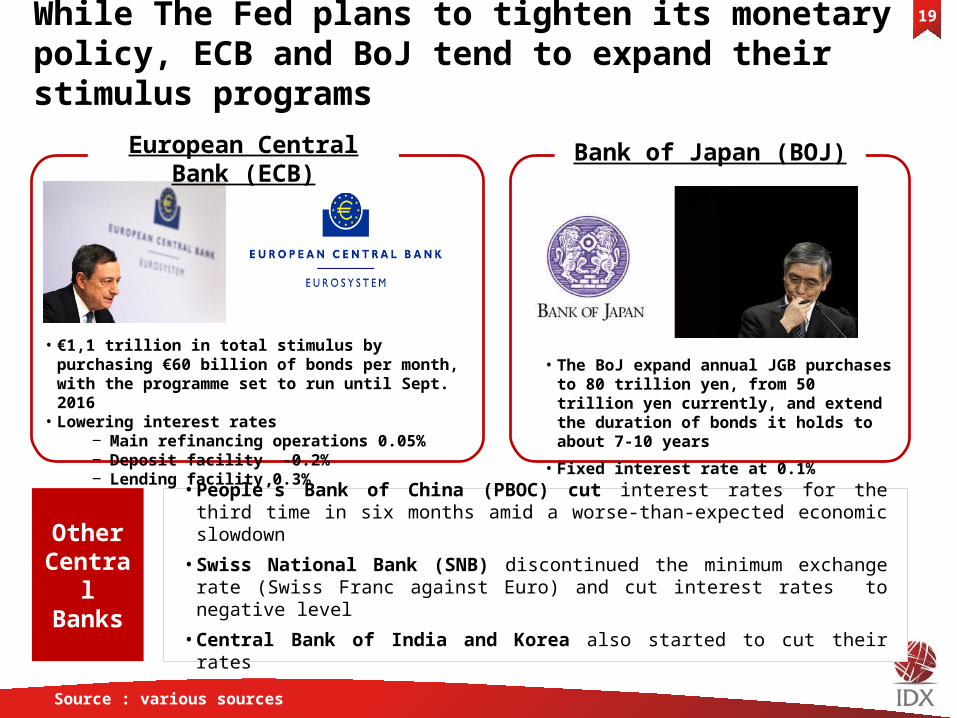

While The Fed plans to tighten its monetary policy, ECB and BoJ tend to expand their stimulus programs

19

Other Central Banks

European Central Bank (ECB) Bank of Japan (BOJ)

• €1,1 trillion in total stimulus by purchasing €60 billion of bonds per month, with the programme set to run until Sept. 2016

• Lowering interest rates ‒ Main refinancing operations 0.05%‒ Deposit facility -0.2%‒ Lending facility 0.3%

• The BoJ expand annual JGB purchases to 80 trillion yen, from 50 trillion yen currently, and extend the duration of bonds it holds to about 7-10 years

• Fixed interest rate at 0.1%

• People’s Bank of China (PBOC) cut interest rates for the third time in six months amid a worse-than-expected economic slowdown

• Swiss National Bank (SNB) discontinued the minimum exchange rate (Swiss Franc against Euro) and cut interest rates to negative level

• Central Bank of India and Korea also started to cut their rates

Source : various sources

As ECB and BoJ move to greater stimulus, increase in global liquidity is expected to drive sentiment higher

20

(Central Bank balance sheet as % of GDP)

2008 2009 2010 2011 2012 2013 2014 20150

10

20

30

40

50

60

70

80

90

Japan

Eurozone

Average

US

BoJ to buy JGBs at an annual rate of ¥80 tn (USD705 bn)

Projection

ECB to start simulus amounting USD1,2 trillion until September 2016

Source : Eastpring Investment, Bloomberg

Global Liquidity Projection in 2015Index Return

(Jan 2015 - 21 May 2015)

India : BSE Sensex 30

Indonesia: IHSG

Thailand : SET Index

Malaysia: FTSE Bursa Malaysia

Singapore: Straits Times

US: Dow Jones

US: S&P500

Australia : All Ordinaries

UK : FT100

Philippines : PSE Index

South Korea: KOSPI

Japan: Nikkei 225

Hong Kong: Hang Seng

France : CAC 40

Germany : DAX

China: Shanghai

1.13%

1.65%

1.91%

1.92%

2.22%

2.60%

3.49%

5.10%

6.81%

8.36%

10.82%

15.77%

16.60%

20.45%

21.00%

40.03%

IDX Future Prospects And Challenges

Despite the potential pressure in the stock market, the prospects for Indonesia economy is predicted to remain solid

22

Consuming Class population estimation by 2030

Million People1

Supported by the fact that most of the population is in the productive age and it is

expected to increase ...... along with the increasing numbers of people that would

join Indonesia’s consuming class

40

2010 20203 2030 in 5-6% GDP Scenario

2030 in 7% GDP Scenario

240 265 280 280

Indonesia Population Pyramid2010 Indonesia Census

1) Rounded to the nearest five million2) Consuming class defined as individuals with an annual net income of above $3.600 at 2005 purchasing power parity (PPP)3) Based on annual GDP growth of between 5 %and 6%

Population Median Age: 29 year

Supported by young and productive ages population

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495+

0-45-910-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495+

12,0

00,0

00

8,00

0,00

0

4,00

0,00

0 0

4,00

0,00

0

8,00

0,00

0

12,0

00,0

00

WomanMan

Pro

du

ctiv

e

Ag

eBelow

Consuming Class

Consuming Class2

Population

Additional people in the consuming class 90 125

Source: McKinsey

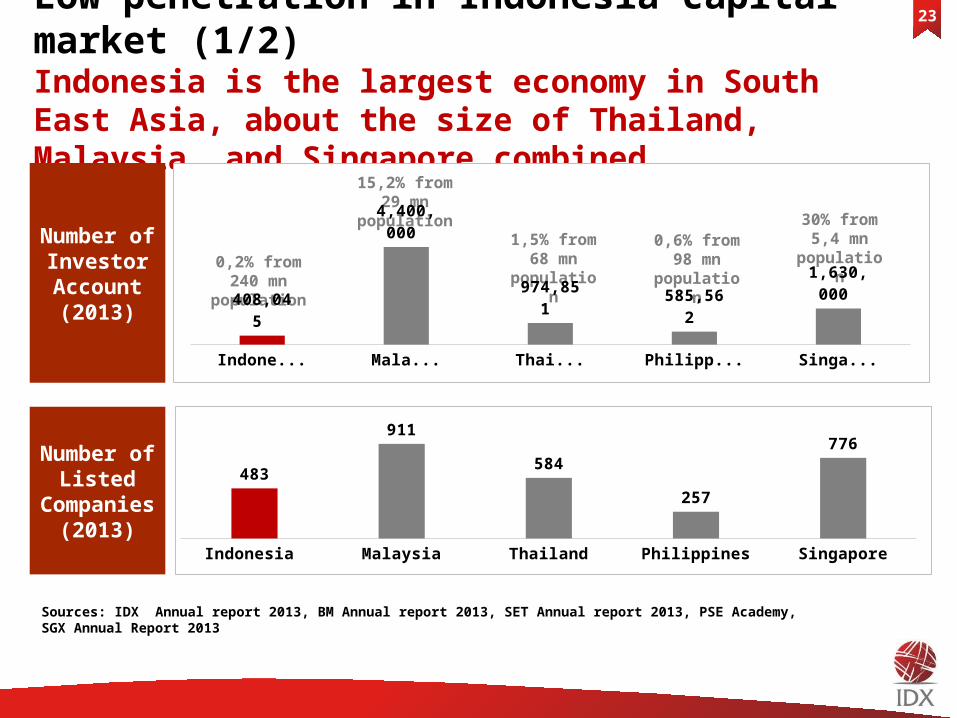

Low penetration in Indonesia capital market (1/2)Indonesia is the largest economy in South East Asia, about the size of Thailand, Malaysia, and Singapore combined

23

Number of Investor Account(2013)

Number of Listed

Companies(2013)

0,2% from 240 mn population

15,2% from 29 mn population

1,5% from 68 mn

population

0,6% from 98 mn

population

30% from 5,4 mn

population

Indonesia Malaysia Thailand Philippines Singapore

408,045

4,400,000

974,851 585,562

1,630,000

Indonesia Malaysia Thailand Philippines Singapore

483

911

584

257

776

Sources: IDX Annual report 2013, BM Annual report 2013, SET Annual report 2013, PSE Academy, SGX Annual Report 2013

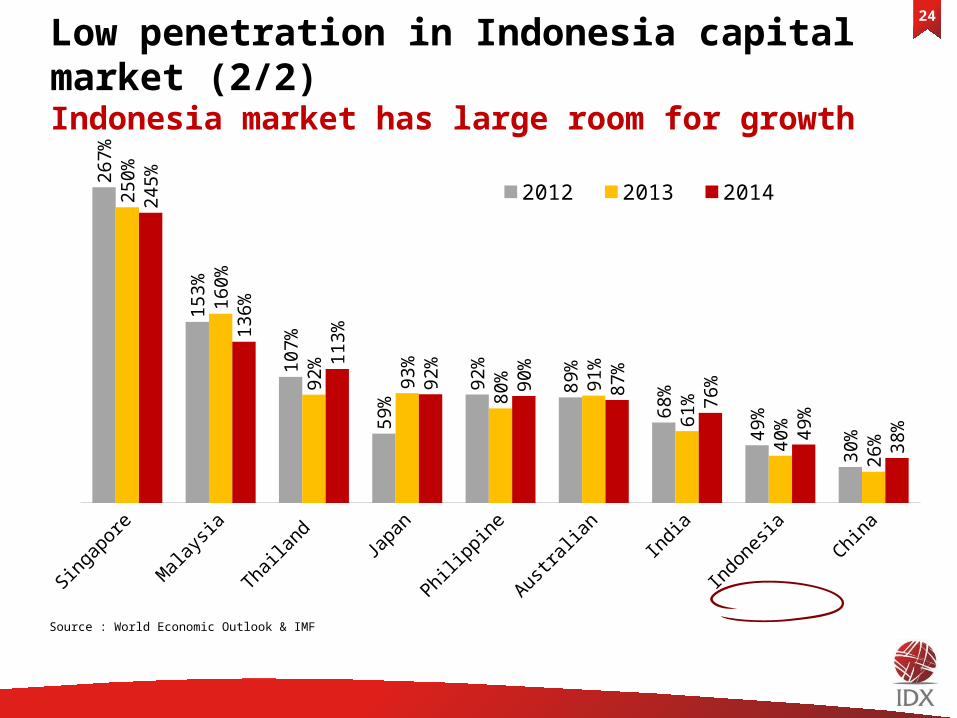

24

Singapore Malaysia Thailand Japan Philippine Australian India Indonesia China

267%

153%

107%

59%

92%

89%

68%

49%

30%

250%

160%

92%

93%

80% 91

%

61%

40%

26%

245%

136%

113%

92%

90%

87%

76%

49%

38%

2012 2013 2014

Source : World Economic Outlook & IMF

Low penetration in Indonesia capital market (2/2)Indonesia market has large room for growth

25

Potential Challenges for Indonesia Capital Market

• Supply To increase number of issuers Developing new product

• Demand To increase number of domestic investors Improving public awareness about investment in capital

market• Infrastructure & Technology

To provide high capacity of trading and surveillance system

• Increased HR/Professional in Capital Market The Regulatory & Supervision Function (OJK, IDX, KPEI, KSEI) The Capital Market Supporting Profession (Brokerages, Fund

Managers, Underwriters, Auditors, Bank Custody, etc)

1

2

3

4

26

Thank you

![CMPEN 472 Lecture Reference Materialkxc104/class/cmpen472/17s/lec/L02CMPEN472Lec… · imm dir ext rel idx idx idx idx idx idx idxi idx2 [idx2] [d,idx] ... 3905 3909 390b 390e 3910](https://static.documents.pub/doc/80x56/5aa3101d7f8b9a1f6d8e0e86/cmpen-472-lecture-reference-kxc104classcmpen47217slecl02cmpen472lecimm-dir.jpg)