Page 1

May 2020 150/-

Kamdhenu

Demerges its

Paint Business

ACQUISITION

RESTRUCTURINGHindustan Foods simplifies

organizational structure

Hindalco closes acquisition

of Aleris; becomes world's largest

aluminium company

LEGALOrient Refractories–

RHI Magnesita Composite

Scheme rejected

MERGERReliance Jio - Facebook deal:

Network Synergy at the Core

Page 2

A One of a Kind Online Portal for all your restructuring needs.

The site will soon launch the models apart from various other online models available

as of now to enable professionals and businessman to make a better decision of choosing

and executing a restructuring for their clients and companies.

AIN M FEATURES:

The module enables you to monitor the steps for execution of your deal Online

RESTRUCTURING WIZARD

By

Step Execution Support

Restructuring Modules A Step

Buy & Sell Revamp Expand

Features of Modules:

- Enables you to arrive at an optimal business decision

- Provides you with available modes to execute a transaction

- Relevant Online Support Services. eg. Quick Valuation, Scheme Drafting etc.

For your off line support please turn to the

last page for our parent company which

takes a company restructuring from idea

to integrations. Contact Details too on the

last page.

Other Online & Off line Models:Other Online & Off line Models:Other Online & Off line Models:Other Online & Off line Models:Other Online & Off line Models:Other Online & Off line Models:Know your Company's Worth (Valuation Models)

Stamp duty calculator

Legal & Compliance Support

Buy-Sell Center (An online marketplace for buyers and sellers)

Assets Turnaround Services

Enhance Business Performance

m i .ergers ndia com

Page 3

Editor: Dr. Haresh Shah

Editorial Board

Mr. Upendra Shah

Mr. Vikram Trivedi

Mr. Nitin Gutka

Mr. Neeraj Marathe

Advisors

Mr. Aniruddha Jain

Mr. Padam Singh

Miss. Apurva Nair

Mr. Sanket Joshi

Mr. Shriprasad Pise

Mr. Ravi Lohiya

Mr. Aniket Malpani

Research Team

First Floor, Matruchaya building,

Plot no 27, Mitramandal Colony, Pune 411 009.

Telefax : (020) 2442 5826

Email : [email protected]

Editorial & Marketing Office

Manilal Kher, Ambalal & Co.

MKA Chambers, Crossley House,

Britiesh Hotel Lane,

Off Bombay Samachar Marg,

Fort, Mumbai 400 001

Email : [email protected]

Legal Associate

Mrs. Jyoti Shah on behalf of

HU Mergersindia.com Pvt. Ltd.,

First Floor, Flat no 1, Matruchaya building,

Plot no 27, Mitramandal Colony,

Parvati, Pune - 411 009.

Telefax : 020 24420209

Printed & Published by

or any of it's

sister concerns are not legally or otherwise

liable for any consequences arising out of the view

expressed. HU Mergersindia.com Pvt. Ltd. assumes

no liability or responsibility for any inaccurate,

delayed or incomplete information, nor for any

actions taken in reliance thereon. The information

contained about each individual, event or

organization has been provided by such individual,

event organizers or organization without verification by

us.

Disclaimer

HU Mergersindia.com Pvt. Ltd.

Dr. Haresh Shah

Along with our regular features

Happy Reading…..

www.mergersindia.com www.mnacritique.com 03

ED

ITO

RIA

L

This issue, we have our first guest article on Reliance Jio – Facebook deal. The article covers

what are the synergies from this Facebook collaboration which has data from their social

networks of Facebook, WhatsApp and Instagram and Jio which has been valued at $60

Billion in this deal of investment of $5.7 Billion for 9.99% stake. In the race of gathering users

this collaboration goes one step forward for both Facebook and Jio. The valuation is

accepted by multiple venture funds as they invested at premium to above valuation.

Kamdhenu group has two main business viz. steel and paint business cater to the

infrastructure sector in the country. The businesses are conducted through a number of

group companies with complex cross-shareholding. In an attempt to simplify its corporate

structure and segregate the steel and paint business, the management has decided to

demerge the paint business for reasons not clear as subsidiary of shell listed holding

company and amalgamate the group companies into one.

This is the second edition of the magazine where

everything was done remotely without having any

face to face (or rather inside the same office)

conversation with our writers and editorial team. I

am sure we are not the only getting used to working

remotely and from home and it might be the new

normal for quite some time. Whilst getting used to

working remotely isn't easy and for everyone we

did a thought exercise on how do we see which kind

of M&A activity will happen over coming months.

Will we see many companies coming up for sale (in

distressed state), but companies with a cash chest

start or revisit their options of buying such

distressed businesses and even if yes, how soon.

Change in FDI regulations and increased focus of

countries for localisation, Cross-Border M&A will get

adversely affected. Though ,we believe there will be

increased foreign Joint ventures and alliances of

large multinationals wanting to create its base in

India as part of its strategies to diversify its global supply chain and also to create multiple

geographical base. We will just have to see how it all unfolds in coming months, but we need

to also think that the regulatory and approval authorities should also become more

equipped and digital in nature to smoothen the process.

Hindalco Ltd is the metals flagship company of the Aditya Birla Group and it has been on

strategically acquiring companies in India and abroad. The latest in this to get acquired is

Aleris Inc, an US-based company, a global leader in aluminium rolled products having 13

different manufacturing units spread across US, Europe and Asia. The acquisition will

happen through Novelis, an US-based wholly-owned subsidiary of Hindalco. This

acquisition will make Hindalco the world's largest value-added aluminium downstream

player.

Our legal article is analysis of NCLT decision on composite scheme of Orient Refractories

and RHI Magnesita rejecting the scheme. We, in our analysis, with due respect to

honourable NCLT, find inconsistency in its views. Honourable NCLT discussed in detail

about having valuation report based on date earlier to Appointed Date and how it can have

negative impact of minority shareholders of the Amalgamated Company. You can look at

the analysis in our October 2018 issue when the transaction was announced.scheme

Hindustan Foods has been in contract manufacturing of food, beverages, household

consumables and some Agri-products since more than 3 decades now manufacturing for

some the biggest names in Consumer goods brands. It has several manufacturing units. In

an attempt to consolidate all its food and beverages under one company it has announced

a composite scheme of demerger of Coimbatore Unit from the its subsidiary Avalon

Cosmetics and merging its subsidiary ATC beverages into itself. The scheme as structured

efficiently captures tax losses and benefits .

Page 4

INSI

DE

ACQUISITION

COVER ARTICLE Kamdhenu Demerges its

Paint Business

RESTRUCTURINGHindustan Foods simplifies

organizational structure

20

Hindalco closes acquisition of Aleris;

becomes world's largest aluminium company

13

16

08

05

04

LEGALOrient Refractories–

RHI Magnesita Composite Scheme rejected

Vol. XXIX Issue No. 2 May 2020

MERGERReliance Jio - Facebook deal:

Network Synergy at the Core

M&A

DigestTHE WHYS and THE HOWSwww.mnacritique.comM&A DIGEST

26

Page 5

ACQ

UIS

ITIO

N

Hindalco closes acquisition of Aleris;

becomes world's largest aluminium company

the project in four years and hand over

the flats to the owners, who have put in

their life-time savings to invest in the

property. The NCLT also pointed out that

Rs 750 crore, which was deposited by the

promoter of Jaiprakash Associates Ltd

(JAL) in the Supreme Court, can be used to

complete the stuck projects. For the

record, NBCC is a public sector unit with

www.mergersindia.com www.mnacritique.com 05

Saikat Neogi

Aleris will be Hindalco's second acquisitionin the US aer Novelis.

Page 6

06 Vol. XXIX Issue No. 2 May 2020

Hindalco Industries Limited, the Aditya

Birla Group metals flagship company, has

become the world's largest value-added

aluminium downstream player in the

world with a global footprint spanning 49

state-of-the-art manufacturing facilities

in North America, Europe and Asia. This

feat was achieved aer the company's

whol ly owned subs id iary Nove l is

Inc,completed the acquisition of Ohio-

based Aleris nearly two years aer

signing the deal for an enterprise value of

$2.8 billion, slightly higher than the initial

estimate of $2.58 billion. The deal in

indeed a long-term strategic bet, much

like Novelis was in 2007, a point which

Kumar Mangalam Birla, Chairman of the

Aditya Birla Group has underlined.

Aleris will be Hindalco's second acquisition

in the US aer Novelis, which it had

bought for $6 billion in 2007. Hindalco's

purchase of Novelis was the second

biggest overseas deal by an Indian entity

aer Tata Steel's $13 billion acquisition of

Corus. Aleris was privately held by private

equity firms Apollo Management, Oaktree

Capital Management and Sankaty

Advisors.

Novelis will acquire Aleris' 13 plants across

North America, Europe and Asia. However,

as per anti-trust regulatoryconditions,

the company will have to divest Aleris'

plants in Lewisport, Kentucky, USA, and

Duffel, Belgium. In September last year,

the US Department of Justice filed an

antitrust lawsuit seeking to block the

Aleris purchase by Novelis as it was said

to be violating the competition norms in

the auto parts industry in North America.

However, the company obtained a nod

from the antitrust body on the condition

that the company wi l l sel l Aler is '

a l u m i n i u m s h e e t s o p e ra t i o n s i n

Lewisport, Kentucky. The Group is

currently negotiating with Liberty House

to close Duffel transaction, subject to

China approval. It is also in discussion with

the US Department of Justice to define

timeline and terms for divestment of

Lewisport.

The $2.8-billion deal consists of $775

million for the equity value, $2 billion for

the assumption or extinguishment* of

Aleris' current outstanding debt and a

$50 million earn-out payment. Aleris' debt

levels have increased since the initial

acquisition announcement two years ago

due to rise in working capital to support

the ramp up of operations. The deal will be

funded by a one-year bridge loan, a five-

year term loan and equity investment.For

Hindalco, the debt burden will rise as the

company has to take considerable debt to

fund the deal. It would raise Hindalco's

consolidated debt by about Rs 16,500

crore.

*Novelis will have to divest Aleris' plants in

Lewisport (US), and Duffel (Belgium).

Aleris' plant in Duffel will be bought by UK-

based Liberty House for $337 million. The

divestment amount of Lewisport plant is

to be worked out. These two will help

Hindalco and Novelis to cut down the

*Cash includes $400 million proceeds from Novelis senior notes issued in January 2020

Table 1: Standalone Financials (Trailing 12 mths ending Dec 19)

Particulars

FRP Shipments (kilo tonnes)

Revenue ($ millions)

Adjusted EBITDA ($ millions)

Adjusted EBITDA/ton ($)

Net Debt ($ millions)

Net Debt/Adjusted EBITDA

Novelis

3,332

11,575

1,446

434

3,394

2.3x

Aleris

858

3,376

388

452

1,900

4.9x

Page 7

acquisition price.

Transaction Financing

and Funding

Acquisition shall be done via debt funding

by Novelis. $1,110 million 1-year bridge

loan at LIBOR +0.95% and $775 million 5-

year term loan at LIBOR + 1.75% and the

remaining would be from ABL and cash* of

close to $900 million which gives a total of

$2.8 billion price tag for Aleris.

Advantage Novelis

The Aleris deal will enable Hindalco to

further diversify its metals downstream

portfolio into other premium market

segments, most notably aerospace. In

fact , Aler is has long-term supply

contracts with aircra makers Boeing,

Airbus and Bombardier. For Novelis, one of

the biggest advantages of the deal will be

in aerospace. In fact, a report by Emkay,

shows that between 2017 and 2036,

aerospace demand is likely to grow by

3 4 , 0 0 0 a i r c ra s . H o w e v e r, w i t h

coronavirus pandemic grounding all

a ir l ine services across the world ,

companies facing humongous losses, and

demand for travel likely to remain tepid for

the next one to two years, it is unlikely

that the demand for new aircras will rise

much in the next few years.

The acquisition will also give Hindalco

access to aluminium supply market for

the building and construction segments.

With the addition of Aleris' operational

assets and workforce, Novelis can more

efficiently serve the growing Asia market

by integrating complementary assets in

the region including recycling, casting,

rolling and finishing capabilities.

Among the other strategic benefits, the

deal will generate are around $150 million

in synergies and create a strong financial

profile. The deal insulates Hindalco-

Novelis from global price volatility and

sharpen the company's focus on the

downstream business.With the closure of

the acquisition, Novelis will operate under

four value streams: Can, Automotive,

Aerospace, Spec ia l t ies , inc lud ing

applications for building, construction,

transportation, etc. Till now, beverage

industry sales (mainly cans) accounted

for 60% of Novel is' volume, whi le

automotive and specialty end markets

accounted for 20% each. With the

completion of the acquisition, the volume

share will change as aerospace is the

major business for Aleris, especially in

North America.

The transaction will make Hindalco a $21-

billion entity in terms of revenues, with an

employee base of 40,000.However, the

debt amount is manageable.

As a global leader in innovative products

and services and the world's largest

recycler of aluminum, the company

p a r t n e r s w i t h c u s to m e r s i n t h e

automotive, beverage can and specialties

industries to deliver solutions that

maximise the benefits of sustainable

lightweight aluminum throughout North

America, Europe, Asia and South America.

Novelis is a subsidiary of Hindalco

Industries Limited., Hindalco acquired

Atlanta-based company Novelis, a world

leader in aluminium rolling and flat-rolled

aluminium products, on May 15, 2007. This

acquisition was done to gain immediate

About Novelis

Hindalco Industries Limited is the metals

flagship company of the Aditya Birla

G ro u p . A U S $1 8 .7 b i l l i o n m e t a l s

powerhouse, Hindalco is the world's

largest aluminium rolling and recycling

company, and a major copper player.

Hindalco's global footprint spans 36

manufacturing units across 10 countries.

It is also one of Asia's largest producers of

primary aluminium. Its wholly owned

subsidiary Novelis Inc. is the world's

largest producer of aluminium beverage

can stock and the largest recycler of used

beverage cans. Hindalco's copper facility

in India comprises a world-class copper

smelter, downstream facilities, a fertiliser

plant and a captive jetty. The copper

smelter is among the world's largest

custom smelters at a single location.

About Hindalco

www.mergersindia.com www.mnacritique.com 07

The transaction will make Hindalco a$21-billion entity in terms of revenues,with an employee base of 40,000

The closure of the landmark dealis

indeed beneficial for Novelis and its

ultimate holding company due to

better market penetration and

product mix. However, it is done at a

time when the metals and mining

sector is undergoing a severe

downturn because of lower demand

globally particularly of airplanes due

to the Covid-19 outbreak. No doubt

the integration of Aleris into Novelis

should be done at the earliest,

excluding Lewisport and Duffel and

N o v e l i s . H I N D A L C O s h o u l d

concentrate to deleverage at the

earliest to minimize its finance cost by

raising its risk capital or refinancing

loans with cheaper interest as the

largest Indian company is planning by

making huge right issue of above Rs

50000 crores . Mult ip le Ind ian

corporate should have a strategy to

become MNCs with similarly high

value strategic deals to take India to

$5 trillion economy.

Aleris is a privately held, global leader in

aluminum rolled products serving diverse

i n d u s t r i e s i n c l u d i n g a e ro s p a c e ,

automotive, building and construction,

commercial transportation and industrial

manufactur ing. Headquartered in

C l eve l a n d , O h i o , A l e r i s o p e ra te s

production facilities in North America,

Europe and Asia.In 2016, the private

equity owners of Aleris, Oaktree Capital,

Apollo and Sankaty Advisors entered into

a contract with Chinese aluminium

billionaire Liu Zhongtain for $2.3 billion.

However, the deal fell through because of

regulatory and national security issues

involving a Chinese company.

About Aleris

scale and a global footprint. Acquiring

Novelis gave Hindalco access to sheet

mills that supplied to can manufacturers

and auto companies.

Page 8

08 Vol. XXIX Issue No. 2 May 2020

RE

STR

UCT

UR

ING

Hindustan Foods simplifies

organizational structure

Aniket Malpani

minority shareholders, as relevant sub-

sections (11) and (12) of section 230 of the

Companies Act 2013 were not notified till

Page 9

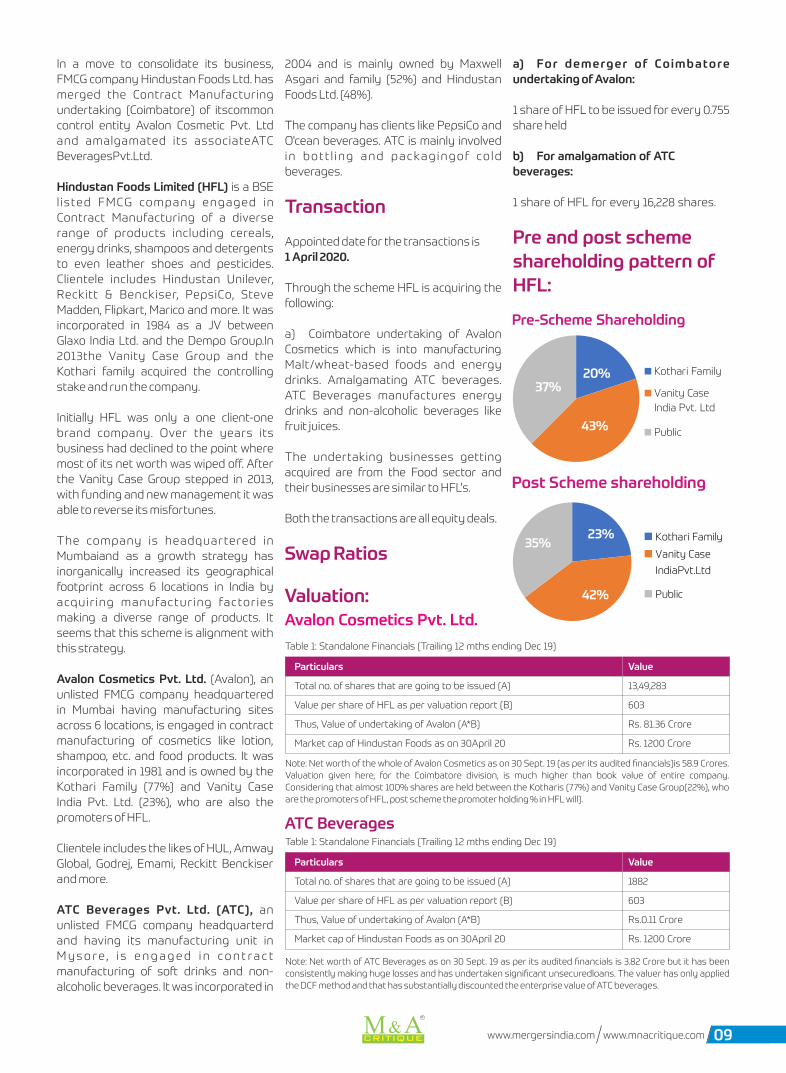

a) For demerger of Coimbatore

undertaking of Avalon:

1 share of HFL to be issued for every 0.755

share held

b) For amalgamation of ATC

beverages:

1 share of HFL for every 16,228 shares.

Pre and post scheme

shareholding pattern of

HFL:

Hindustan Foods Limited (HFL) is a BSE

l isted FMCG company engaged in

Contract Manufacturing of a diverse

range of products including cereals,

energy drinks, shampoos and detergents

to even leather shoes and pesticides.

Clientele includes Hindustan Unilever,

Reckitt & Benckiser, PepsiCo, Steve

Madden, Flipkart, Marico and more. It was

incorporated in 1984 as a JV between

Glaxo India Ltd. and the Dempo Group.In

2013the Vanity Case Group and the

Kothari family acquired the controlling

stake and run the company.

In a move to consolidate its business,

FMCG company Hindustan Foods Ltd. has

merged the Contract Manufacturing

undertaking (Coimbatore) of itscommon

control entity Avalon Cosmetic Pvt. Ltd

and amalgamated its associateATC

BeveragesPvt.Ltd.

Initially HFL was only a one client-one

brand company. Over the years its

business had declined to the point where

most of its net worth was wiped off. Aer

the Vanity Case Group stepped in 2013,

with funding and new management it was

able to reverse its misfortunes.

The company is headquartered in

Mumbaiand as a growth strategy has

inorganically increased its geographical

footprint across 6 locations in India by

acquiring manufacturing factories

making a diverse range of products. It

seems that this scheme is alignment with

this strategy.

Avalon Cosmetics Pvt. Ltd. (Avalon), an

unlisted FMCG company headquartered

in Mumbai having manufacturing sites

across 6 locations, is engaged in contract

manufacturing of cosmetics like lotion,

shampoo, etc. and food products. It was

incorporated in 1981 and is owned by the

Kothari Family (77%) and Vanity Case

India Pvt. Ltd. (23%), who are also the

promoters of HFL.

Clientele includes the likes of HUL, Amway

Global, Godrej, Emami, Reckitt Benckiser

and more.

ATC Beverages Pvt. Ltd. (ATC), an

unlisted FMCG company headquarterd

and having its manufacturing unit in

M y s o re , i s e n g a g e d i n co n t ra c t

manufacturing of so drinks and non-

alcoholic beverages. It was incorporated in

2004 and is mainly owned by Maxwell

Asgari and family (52%) and Hindustan

Foods Ltd. (48%).

The company has clients like PepsiCo and

O'cean beverages. ATC is mainly involved

in bott l ing and packagingof co ld

beverages.

Transaction

Appointed date for the transactions is

1 April 2020.

Through the scheme HFL is acquiring the

following:

a) Coimbatore undertaking of Avalon

Cosmetics which is into manufacturing

Malt/wheat-based foods and energy

drinks. Amalgamating ATC beverages.

ATC Beverages manufactures energy

drinks and non-alcoholic beverages like

fruit juices.

The undertaking businesses getting

acquired are from the Food sector and

their businesses are similar to HFL's.

Both the transactions are all equity deals.

Swap Ratios

20%

43%

37%

Pre-Scheme Shareholding

Kothari Family

Vanity Case

India Pvt. Ltd

Public

23%

42%

35%

Post Scheme shareholding

Kothari Family

Vanity Case

IndiaPvt.Ltd

Public

Table 1: Standalone Financials (Trailing 12 mths ending Dec 19)

Particulars

Total no. of shares that are going to be issued (A)

Value per share of HFL as per valuation report (B)

Thus, Value of undertaking of Avalon (A*B)

Market cap of Hindustan Foods as on 30April 20

Value

13,49,283

603

Rs. 81.36 Crore

Rs. 1200 Crore

Valuation:Avalon Cosmetics Pvt. Ltd.

Note: Net worth of the whole of Avalon Cosmetics as on 30 Sept. 19 (as per its audited financials)is 58.9 Crores.

Valuation given here, for the Coimbatore division, is much higher than book value of entire company.

Considering that almost 100% shares are held between the Kotharis (77%) and Vanity Case Group(22%), who

are the promoters of HFL, post scheme the promoter holding % in HFL will).

Table 1: Standalone Financials (Trailing 12 mths ending Dec 19)

Particulars

Total no. of shares that are going to be issued (A)

Value per share of HFL as per valuation report (B)

Thus, Value of undertaking of Avalon (A*B)

Market cap of Hindustan Foods as on 30April 20

Value

1882

603

Rs.0.11 Crore

Rs. 1200 Crore

ATC Beverages

Note: Net worth of ATC Beverages as on 30 Sept. 19 as per its audited financials is 3.82 Crore but it has been

consistently making huge losses and has undertaken significant unsecuredloans. The valuer has only applied

the DCF method and that has substantially discounted the enterprise value of ATC beverages.

09

Page 10

The NCLT's final decision, passed

aer multiple appeals and litigation in

civil court, through all the legal

process, has paved a way for

aggrieved home buyers to get similar

relief in others stuck-real estate

projects across the country. It was

once again made clear by NCLT order

and based on honourable Supreme

Court observations that 'The focus of

the code was to ensure revival and

continuation of the corporate debtor,

where liquidation is to be availed of

only as a last resort. The Code is a

beneficial legislation to put the

corporate debtor on its feet, and not

a mere recovery legislation for the

creditors. It is now up to NBCC to

deliver on its promise and set a

benchmark for the real estate

industry to not squander with the

money of homebuyers who have put

in their lifetime savings to buy their

dream homes.

Please share your experiences/feedback with

us on [email protected]

10 Vol. XXIX Issue No. 2 May 2020

Page 11

11

Post scheme, promoter holding has

g o n e u p b eca u s e i n o n e o f t h e

companies involved in the scheme i.e.

Avalon, the promoters (Kothari family

and Vanity Case) are holding 99% shares

Rationale of the Scheme:

1. The amalgamation of ATC beverages

(Mysore) is beneficial in following ways:

a) Amalgamation proves to be tax

efficient. Both companies involved are

industrial undertaking asper sec 72A, ITA

1961.Thus,the carried forward losses of

ATC Beverages of up to Rs. 35 crore and

will be available for set off subject to

compliance of stringent conditions under

Sec 72A of The Income tax act,1961.

b) The acquisition is also in alignment

with the overall growth strategy of the

company of acquiring manufacturing

entities in different products in the food

sectors and different geographical

locations.

c) HFL already had a stake of 40% in

ATC beverages which was bought in

FY19for Rs1.42 Crores. Then in early FY

20HFLalso converted, to equity, a loan of

Rs.1.75 crore, increasing HFL's holding to

4 8 % . N o w, o n l y a y e a r l a t e r ,

amalgamation of ATC indicates that HFL

saw an acquisition opportunity at a

reasonable valuation. ATC beverage had

a poor financial posit ion Now the

valuation given to the company (as per

the Valuation report) is about Rs. 11 Lakhs

for equity value and enterprise value of Rs

13.11 crores considering unsecured loans

of more than 13 crores.

d) In fact, in FY 2019, HFL had converted

an unsecured loan of Rs. 1.75 cores which it

had given to ATC beverages into equity

shares. This was done despite the poor

performance of the company over the

previous years. ATC beverages were

suffering losses since a few years and

unsecured loans were piling on. HFL's

earlier acquisition of 40% stake, the

subsequent conversion of the loan of Rs.

1.75 Crore(which brought holding to 48%)

and now the amalgamation clearlyisa

bailout for ATC and its promoters.

Besides, ATC has PepsiCo and O'cean

beverages as its clients and beverages is

a n ew s e g m e n t fo r H F L s o t h i s

amalgamation might as wel l be a

38.7

138.9

236.6

2.9 10.120.4

0

50

100

150

200

250

FY 17 FY 18 FY 19

INR

Cro

res

Year

Revenue and EBITDA

Revenue

EBITDA

Performance Analysis of HFL:a. Trend of Revenue and EBITDA over the years of HFL:

Note:The company made 2 major acquisitions in 2017-18 apart from getting new clients and more funding,

leading to a dramatic increase in turnover.The acquisitions were of G Shoe Export Ltd.(Mumbai) and a factory of

Reckitt Benckiser (India) Pvt. Ltd, on slump sale basis, in Jammu and Kashmir, which makes pest control

products for the brand “Mortein”. The J & K unit particularly has a huge manufacturing capacity.

10.24.6

30.2

50.3

10.916.7

45.7

85.9

0

10

20

30

40

50

60

70

80

90

100

FY 2016 FY2017 FY 2018 FY 2019

INR

Cro

res

Year

Long term Debt Non-Current Assets

b. Long term debt and Non-current Assets:

c. Some financial ratios of HFL over the years:

Particulars

Receivable Days

Inventory days

Fixed Asset Turnover

ROCE (%)

FY10

282

24

0.44

-5.38

FY11

258

63

0.46

3.26

FY12

161

60

0.80

-14.51

FY13

204

72

0.68

-2.56

FY14

390

132

0.28

-5.67

FY15

57

39

1.21

39.32

FY16

44

31

1.48

8.55

FY17

49

35

2.77

7.25

FY18

47

40

5.3

18.64

FY19

50

46

3.9

18

Category: Restructuring Author : Aniket

Malpan iCov id-19 has bad ly h i t a l l

companies across all sectors. Indian

economy was already struggling, and this

pandemic has worsened the scenario.

Hindustan Foods Ltd., being an FMCG

manufacturer will see a decrease in

business but since many of its products

are consumer staples and other essentials

it maybe in a better position than

companies in other industries. This

scheme can prove to be helpful since it

brings efficiency not only in HFL's

organizational structure but also reduces

GST compliance costs and leads to direct

tax benefits. With uncertain times ahead,

we can expect more such re-structuring

and also acquisitions where the big

players l ike HFL absorb the small ,

struggling players like ATC Beverages. No

doubt it will all depend how quickly HFL is

able to turn around the loss making

operations of ATC Beverages and also

reduce tax cost by successfully en-cashing

looses incurred by like ATC Beverages.

synergetic business decision also.

2. This is the second acquisition of HFL

from Avalon Cosmetics. In 2017-18, its

Hyderabad undertaking (manufactures

fabric cleaning products like detergents)

was acquired by HFL. Avalon is 100%

owned by promoters of HFL. So, selling of

one Avalon's businesses to HFL at good

valuations benefits the promoters

directly. From the point of view of public

investors, this staggered acquisition of

Avalon avoids a huge cash outflow in one

go. Besides, entering one sector at a time

Page 12

helps HFL realize value from each such

acquisition.

The related party transactions between

both the companies are insignificant

barring a purchase of land by HFL for Rs.

2.8 crore in FY 2019.

3. GST benefits:

With the GST implementation, a trend has

been seen with many companies like HUL,

Lux Industries, Orient Refractories

acquiring their unlisted manufacturing

entities which have businesses same as

the controlling entity. This reduces the

compliance costs, GST cost because of

related party transactions and simplifies

the organizational structure. Having

entities in different geographic locations

also brings the entity closer to the

markets and makes it easier to establish a

GST efficient supply chain.

Accounting treatment in

b o o k s o f H i n d u s t a n

Foods:

The demerger will be accounted for using

the “Pooling of Interest” Method as per

Appendix C of IndAS103: Business

Combinations. Avalon Cosmetics is

controlled by the promoters of HFL as the

transaction being common control

combination.

The company has been growing and

ex p a n d i n g i t s b u s i n e s s t h ro u g h

acquisitions, and hence needing more

funds, and the same in reflective in the

graph above.

As can be seen since 2013 there has

been a massive improvement across all

ratios. This was the year when the

Vanity Case Group entered the scene.

Covid-19 has badly hit all companies across

all sectors. Indian economy was already

struggling, and this pandemic has

worsened the scenario. Hindustan Foods

Ltd., being an FMCG manufacturer will see

a decrease in business but since many of

its products are consumer staples and

other essentials it maybe in a better

posit ion than companies in other

industries. This scheme can prove to be

helpful since it brings efficiency not only in

HFL's organizational structure but also

reduces GST compliance costs and leads

to direct tax benefits. With uncertain times

ahead, we can expect more such re-

structuring and also acquisitions where

the big players like HFL absorb the small,

struggling players like ATC Beverages. No

doubt it will all depend how quickly HFL is

able to turn around the loss making

operations of ATC Beverages and also

reduce tax cost by successfully en-cashing

looses incurred by like ATC Beverages.

Every month M & A critique gives valuable insights to

over 5000 Readers from Corporate World on-

- Recent Deals in the M & A Space

- Updated News on National, International & Cross-Border News

- M & A Happening s in High Court Updated every month

Advertise with us to reach the key decision makers

in the Corporate World.

For more info,

Contact:- 020-24425826

Email: [email protected]

May 2020 150/-

Kamdhenu

Demerges its

Paint Business

ACQUISITION

RESTRUCTURINGHindustan Foods simplifies

organizational structure

Hindalco closes acquisition

of Aleris; becomes world's largest

aluminium company

LEGALOrient Refractories–

RHI Magnesita Composite

Scheme rejected

MERGERReliance Jio - Facebook deal:

Network Synergy at the Core

12 Vol. XXIX Issue No. 2 May 2020

Page 13

LEG

ALOrient Refractories–

RHI Magnesita Composite Scheme rejected

RHI Magnesita a g lobal leader in

refractory operating in India through its

various subsidiaries and wants to merge

three subsidiaries where two companies

are private limited, and one is listed entity.

The merger is designed to optimally

position RHI Magnesita's operations in the

strategically important Indian market to

capture growth opportunities more

effectively and efficiently. We had covered

the scheme details in our previous article

in the our October 2018 issue.

The Scheme in brief:

RHI India Private Limited (Transferor

Company-1) a Private Limited Company a

subsidiary of Dutch Brasil Holding B.V.

which is u l t imate ly ho lds by RHI

Magnesita N.V.

RHI Clasil Private Limited (Transferor

Company-2) a private limited Company, a

subsidiary of VRD Americas B.V. which is

ultimately owned by RHI Magnesita N.V.

O r i e n t R e f ra c t o r i e s L i m i t e d

(Transferee Company) listed entity,

wherein majority of shares are hold by

Dutch U.S. Holding B.V. which is ultimately

owned by RHI Magnesita N.V. The Shares

of the transferee company is listed on BSE

and NSE.

The Companies has filed the scheme

before Hon'b le NCLT Mumbai for

amalgamation of transferor companies

into Transferee Company.

Post-Merger Orient Refractories will

be renamed RHI Magnesita India.

Al l three companies primari ly

engaged into business of manufacturing,

trading, marketing of refractories and

allied products.

Objective of the Scheme:

All the companies are into same and allied

business activities.

The objectives were:

NCLT rejected thecomposite scheme throughits order dated 2.3.2020

CS Shriprasad Pise

13

Page 14

I. Simplification of corporate structure

and consolidation of India business.

ii. To e s t a b l i s h co m p re h e n s i v e

refractory product portfolio

iii. Real is ing business efficiencies

through optimum utilisation of resources

iv. To o p t i m i s e c a s h fl o w t h i s

contributes to overall growth prospects of

combined company.

v. Creation of larger asset base and

facilitation of access to better financial

resources.

vi. E n h a n ce d s h a re h o l d e r va l u e

pursuant to economies of scale and

business efficiencies.

The purpose behind the merger was to

consolidate India business of RHIM Group,

by which two private limited company will

merge into the listed entity Orient

Refractories Limited and RHI Magnesita

N.V. the Parent Company will have

approximately 70% stake in the Orient

Refractories which will be renamed RHI

Magnesita India.

Swap Ratio

For every fully paid up 100 (One

hundred) equity shares of Rs. 10 (Ten)

each of RHI India, Orient will issue 7044

(Seven Thousand Forty-Four) fully paid

up Equity shares of Rs. 1/- (One) each

For every fully paid up 1000 (One

Thousand) equity shares of Rs. 10 (Ten)

each of RHI Clasil, Orient will issue 908

(Nine Hundred and Eight) fully paid up

Equity shares of Rs. 1/- (One) each.

Accounting Treatment:

As per the Composite scheme, the

Transferee Company will give effect to the

amalgamation in its books of account

as“Business Combinations” in accordance

with Indian Accounting Standard (IND AS

103), Business combination and other

accounting principles prescribed under

the Companies (Indian Accounting

Standards) Rules, 2015 (Ind AS) as

prescribed under Section 133 of the

Companies Act, 2013.

Decision of NCLT:

The order of the Hon'ble NCLT-Mumbai

dated 02.03.2020 has not sanctioned /

approved the proposed Scheme of

Amalgamation. Neither Regional director

nor official liquidator has objected to the

scheme. Even shareholders approved the

scheme with requisite majority.

The Regional Director has filed his report

dated 24 June 2019, among other things

observing as follows:

In paragraphs IV (f) as per Definition of the

scheme, “Appointed Date” means 1st day

of January 2019 or such other date as

may be approved by the NCLT or such

co m p e te n t a u t h o r i t y a s m a y b e

applicable. In this regard, it is submitted

that Section 232(6) of the Companies Act,

2013 states that the scheme under this

section shall clearly indicate an appointed

date from which it shall be effective and

the scheme shall be deemed effective

from such date and not at a date

subsequent to the appointed date.

Honourable NCLT found an anomaly in

date of approval of the scheme and date

of valuat ion report by Chartered

Accountant and Merchant banker as

against Appointed Date which is a future

date. To support its view, NCLT quoted the

Order of NCLT, Mumbai Bench dated

05.09.2018 in the matter of Scheme of

Arrangement (Demerger) between East

We s t P i p e l i n e Lt d . a n d P i p e l i n e

Infrastructure Pvt. Ltd. in CSA No.719/2018,

wherein the Bench has dealt with the

issue of “Appointed Date” and the

relevant portion from the Order is

reproduced/ discussed below:-

Point No. 24 of the order:

The logic behind asking appointed date at

the time scheme presented before

Tribunal is that, appointed date must be

conceived as date from which demerged

company undertaking is deemed as

transferred to resulting company with all

financial implications. And it will come into

effect if scheme is approved by NCLT as

well as approved by all regulatory and

Sectoral Authorit ies, or else, that

undertaking will continue as part of the

demerged company as before.

Point No. 25 of the order:

To k n o w t h e fi n a n c i a l s o f t h i s

arrangement, the assets proposed to be

transferred to the Resulting company

shall be valued, so that the consideration

payable for transfer of the assets can be

fixed, then if any share swapping, then to

decide swap ratio, like wise to decide

transferability of assets or liabilities;

stamp duty liability, tax (direct and

indirect) liability and loss or gain of Tax

benefits by valuation of. So Tax benefits

by valuation of. So this cut off date taken

into consideration for valuation shall be

the appointed date, because all the

financial implications are dependent upon

the cut off date and valuation thereof.

Point No. 26 of the order:

Appointed date shall be the date

determining the value of the transfer of

Assets and its implications, so that

shareholders, creditors and all other

stakeholders will be in a position to know

the permutations and combinations of

that arrangement, therefore, basing on

which they will make up their mind how to

go about the Scheme. Likewise, the Tax

Authorities as well as Stamp Duty

Authorities will be in a position to assess

the Tax Liability as well as Stamp Duty

payable over such transfer.'

Point No. 30 of the order:

In view thereof, there won't be any

appointed date in future, because scheme

always dependent upon the valuation

and for valuation of the assets having to

be done before presenting scheme, it is

inconceivable to visualise appointed date

in future.

NCLT found an anomaly in date of approval of thescheme and date of valuation report by CharteredAccountant and Merchant banker as againstAppointed Date which is a future date.

Every month M & A critique gives valuable insights to

over 5000 Readers from Corporate World on-

- Recent Deals in the M & A Space

- Updated News on National, International & Cross-Border News

- M & A Happening s in High Court Updated every month

Advertise with us to reach the key decision makers

in the Corporate World.

For more info,

Contact:- 020-24425826

Email: [email protected]

May 2020 150/-

Kamdhenu

Demerges its

Paint Business

ACQUISITION

RESTRUCTURINGHindustan Foods simplifies

organizational structure

Hindalco closes acquisition

of Aleris; becomes world's largest

aluminium company

LEGALOrient Refractories–

RHI Magnesita Composite

Scheme rejected

MERGERReliance Jio - Facebook deal:

Network Synergy at the Core

14 Vol. XXIX Issue No. 2 May 2020

Page 15

Point No. 22 of the order:

The Bench has also considered the

Circular No.09/2019 dated August 21, 2019

issued by the Ministry of Corporate

Affairs on the issue of appointed date

wherein it is clarified that the provision of

section 232(6) of the Act enables the

companies in question to choose and

state in the scheme an 'appointed date'.

This date may be a specific calendar date

or may be tied to the occurrence of an

event such as grant of license by a

competent authority or fulfilment of any

preconditions agreed upon by the parties,

or meeting any other requirement as

greed upon between the parties, etc.,

which are relevant to the scheme. In the

current Scheme of Amalgamation, a

specific date, i.e. 01.01.2019 has been fixed

as Appointed Date whereas as discussed

above, valuation report, fairness opinion,

Board Resolution of all the Petitioner

Companies were dated 31.07.2018.

Therefore, we are of the considered view

that as clarified by the Ministry of

Corporate Affairs, the Scheme is not tied

to the occurrence of an event or fulfilment

of any pre-conditions agreed upon by the

parties, hence the appointed date should

be the valuation date i.e. 31st July,2018 as

against 1st January ,2019 as per the

scheme. as discussed above.

Considering the above factual details, the

profit earning capacity and other

financia ls of the Transferor- I and

Transferor-II Companies, the share

exchange ratio as per the valuation given

by the Auditor and the Fairness Opinion

given by the Merchant Banker appears to

be too high which results in undue

a d v a n t a g e / e n r i c h m e n t t o t h e

shareholders of both the Transferor

Companies and to the shareholders of the

ultimate holding Company RHI Magnesita.

Therefore, we are of the considered view

that the Scheme is devised/ designed

majorly to benefit the Two shareholders

of Transferor Company-I and few

shareholders of Transferor Company-II

which in turn the undue advantage

ultimately flows to the shareholders/

holding Company, i.e. RHI Magnesita. In

view of the above analysis, we are of the

considered view that the Scheme appears

to benefit only a few shareholders of

Transferor Company to be unfair and

unreasonable and contrary to the public

policy, public shareholders of the listed

Company therefore, we deem it fit not to

sanction/ approve the proposed Scheme

of Amalgamation. Therefore, we do not

sanction/ approve the Scheme as prayed

for.

Hon'ble NCLT Mumbai in the given matter

concluded that there cannot be Appointed

Date in future and even if the scheme is

considered and approved by all concerned

i.e. shareholders, Regional Director and

Official liquidator. It applied the ratio of the

Order of NCLT, Mumbai Bench dated

05.09.2018 in the matter of Scheme of

Arrangement (Demerger) between East

We s t P i p e l i n e L t d . a n d P i p e l i n e

Infrastructure Pvt. Ltd. in CSA No.719/2018,

though the present case is that of merger

wherein The Transferee Companies will

cease. Further it didn't change the

Appointed Date and sanctioned the

scheme as in the case of East West

Pipeline.The honorable NCLT failed to

differentiate financial consequences in

case of demerger and merger. It seems

while applying circular No.09/2019 dated

August 21, 2019 also it failed to appreciate

the fact that the scheme is an agreement

and arrangement between companies and

hence The Appointed Date as per the

scheme can be considered in line with the

circular read with Section 232(6).

Ultimately The scheme was rejected on

the ground that it is beneficial for only few

shareholders, where in it is held even by

The honorable Supreme Court that , the

court has no powers to go into fairness of

valuation report ,if it s by qualified experts

and approved by all the parties to the

transaction.

In our opinion, the scheme could have been

approved as presented or at least aer

the change in The Appointed Date to

31stJuly2018.The companieshave decided

to move to NCLAT against the order by

filing appeal aer the current Corona

pandemic.

Please share your experiences/feedback with

us on [email protected]

15

Page 16

ME

RG

ER

Reliance Jio - Facebook deal:

Network Synergy at the Core

Facebook Inc. will invest $5.7 billion to pick

up 9.99% stake in the digital business of

Reliance Industries Ltd. The investment

from Facebook values the Jio Platform

close to $60 billion. What synergies the

combined business will generate that

propelled Facebook to pay this hey

amount?

Connected Ecosystem of

the Combined Business

Jio Platform is the digital services entity

that houses Reliance's telecoms arm Jio

Infocomm, as well as its news, movie and

music apps, along with other businesses.

The platform was launched to bring

India's No. 1 connectivity platform, leading

Debasish Sarkar

Magnesita N.V.

RHI Clasil Private Limited (Transferor

Company-2) a private limited Company, a

subsidiary of VRD Americas B.V. which is

ultimately owned by RHI Magnesita N.V.

O r i e n t R e f ra c t o r i e s L i m i t e d

(Transferee Company) listed entity,

wherein majority of shares are hold by

Dutch U.S. Holding B.V. which is ultimately

owned by RHI Magnesita N.V. The Shares

of the transferee company is listed on BSE

and NSE.

The Companies has filed the scheme

before Hon'b le NCLT Mumbai for

amalgamation of transferor companies

into Transferee Company.

lectures available

Reliance Jio Platform

16 Vol. XXIX Issue No. 2 May 2020

Page 17

digital app ecosystem, and the world's

best tech capabilities to create a digital

society for each Indian. The platform was

growing through mergers and acquisition

such as Saavn's merger with Jio Music in

2018 and Haptick acquisition in 2019. The

Jio Platform includes leading digital apps,

digital ecosystem and India's No. 1 high

speed connectivity platform under one

umbrella.

With more than 300 million Facebook

users and 400 million WhatsApp users in

the country, India is home to Facebook's

largest user base on the planet. In 2017, it

launched a commercial Wi-Fi program

called Express Wifi, which allows mom-

and-pop stores to provide internet access

to shoppers via hotspots at a nominal

rate. It currently has 500 local retailers

signed up, and more than 10,000 hotspots

across India. In 2019, it has also invested in

Indian startup Meesho, an e-commerce

company that leverages social media to

connect customers with resellers.

The focus of the deal is to come up with

digital-based solutions for 60 million

micro, small and medium businesses, 120

mi l l i on farmers , 3 0 mi l l i on sma l l

merchants and millions of small and

medium enterprises in the informal sector.

Given the reach and scale of the digital

ecosystem, Facebook has invested in the

platform to create and unlock meaningful

value through Network Synergy. The

deal will unlock a huge network effect with

the combined power of Facebook and Jio's

subscribers across plays in commerce

and payments. On one hand, it gives

Facebook a wider audience with Jio's 388

million client, on the other hand it helps

Reliance Jio leverage the reach of

Whatsapp, Facebook Chat's service.

Facebook can help Jio move to the next

level as they have the expert ise,

technology and global talent.

The two companies could leverage each

other's strengths to build a Connected

Ecosystem compr is ing of d ig i ta l

payments, telecom and offline and online

commerce.

What is Network Effect?

Network effects are the incremental

benefit gained by an existing user for

each new user that joins the network.

There are two types of network effects:

Facebook Ecosystem

digital app ecosystem, and the world's

best tech capabilities to create a digital

society for each Indian. The platform was

growing through mergers and acquisition

such as Saavn's merger with Jio Music in

2018 and Haptick acquisition in 2019. The

Jio Platform includes leading digital apps,

digital ecosystem and India's No. 1 high

speed connectivity platform under one

umbrella.

for one user group when a new user of a

different user group joins the network.

Two or more user groups are needed to

ach ieve ind irect network effects .

Platforms business have two or more

user groups exchanging value with one

another. In most platforms, there are two

users groups: producers and consumers.

The more consumers on the network, the

more valuable that network is to

producers, and vice versa. Taking e-

commerce as an example, as more buyers

(i.e. consumers) join the platform, the

more useful and valuable it is to sellers (i.e.

producers), because they have more

direct and indirect network effects.

Direct network effects are also known as

same-side effects. The value of a service

simply goes up as the number of users

goes up. If we take the example of

telephone, it is only useful if the people

that we need to reach also have

telephones. The more people there are

who have phones, the more useful it is to

have one yourself.

Indirect network effect, also known as

cross-side effects. With indirect network

effects, the value of the service increases

Individual Segments User Base

17

Page 18

business opportunities. The reverse is

also true.

Network Synergy for the

Connected Ecosystem

The deal will jointly create an ecosystem

that take advantage of Facebook's high

daily active users and engaged customer

base and Jio's platform assets. For

Facebook , th is dea l pre sents an

opportunity to leverage the partner's

significant reach in India and explore the

next-billion-user landscape. It also means

the social media giant has a better

partner in India's complex policy lobby,

where Reliance has a strong hand. For

Reliance Jio, the business will not be

dependent solely on how successful the

next generation is, as it will continue to

grow with the strategic partner. A partner

with the ability to build capable and

desirable technologies, like Facebook,

could certainly help turn the tide for the

enterprising carrier.

The various driver of the network

synergies are:

1. Phygital (Physical +

Digital) Commerce

Strategy

At its core, the deal will create an

ecosystem by combining both offline and

online retail. WhatsApp will empower

nearly 30 million small Indian kirana

(grocery) shops to digitally transact with

every customer in their neighborhood

through JioMart, the e-commerce venture

of Reliance's retail arm, which will offer

customers free expre ss grocery

deliveries from neighborhood mum-and-

pop stores. Facebook, through its

investment in Meesho, is a lready

evaluating the SME space for e-commerce

in India. Shopping in India could transform

into a giant, end-to-end network of

services with buyers connecting with

retailers and placing orders through

WhatsApp. The company can also create

an 'e- commerce monopoly' and upturn

ecommerce ecosystem.

Financial Returns of the

Network Effects

(Synergies)

The joint value created by a platform

stems from its group based advantages.

These advantages depends on the

platform's effectiveness in competing

with rival platforms.

Just as a firm's competitive advantages

are shaped by the strategy and resources

of the firm, so it goes with platform based

advantages. When the platform yields

synergy, each member can be thought of

as adding something to the network

based advantages.

As a platform scales, its costs per unit sold

decreases logarithmically in comparison

to linear business.

A platform grows not by buying more

assets, but by acquiring more users,

which has a near-zero cost. This costs the

platform next to nothing. Platforms boast

higher profit margins and higher price-to-

revenue multiples. Perhaps this explains

some of the high valuations we see in

platform businesses today including the

recent Facebook – Reliance Jio deal.

The article is written by Debasish Sarkar

- IT Mergers & Acquisition - Associate

Director - Deloitte India in his personal

capacity and doesn't reflect the views of

his employer.

2. 360 Degree Data

Monetizing

Facebook constellation is sitting on a

huge pile of data which they weren't able

to monetize. The vast quantities of data

generated by users of online services can

n ow b e p ro ce s s e d i n to va l u a b l e

information for commercial and strategic

gains by leveraging Jio Mart's reach.

In reverse data sharing, WhatsApp,

through its commercial agreement with

JioMart, could end up providing deeper

and richer data to Facebook which will

provide more intense and localized insight

into the consumption patterns of Indian

customers. This new perspective on

Indian consumers will add to Facebook's

already formidable advertising revenue

stream.

3. Digital Payment Reach

WhatsApp could leverage Jio's Payments

Bank as a sponsor bank to power its UPI-

based payments. The deal will open up

Whatsapp's entire user base for Reliance

Jio, including the customers on rival

telecom partners.

Jio's plan to pull all Kirana stores and

combine it with payments mechanism will

be an amazing partnership on the

payment side. Between Whatsapp,

Instagram and Facebook , a l l the

co m m e rce ca n b e d o n e t h ro u g h

Whatsapp Pay. Having a local partner

could help Whatsapp Pay in navigating

various regulatory issues, including those

related to privacy and local storage.

The power of content, commerce, and

community supported by the mobile

network can be unleashed for these

services at scale, making the impact

widespread from e-commerce to telecom

to mobile payments and potentially even

healthcare and education. Through this

deal, JioMart could become a one stop

shop for e-commerce, social media

consumption, instant messaging and

digital payments. The network effect also

helps in creating an ecosystem that

disincentives users from leaving.

Platform Business Cost Model

18 Vol. XXIX Issue No. 2 May 2020

Total

addressable

Market

Volume

Co

st

pe

r in

tera

ctio

n

Page 19

On�M&A�and�Joint�Venture�

24425826

[email protected]

Annual Subscription - India - Rs. 1,000 + 18% GST = 1180

only - for all Digital Access to the portal for a year.

19

May 2020 150/-

Kamdhenu

Demerges its

Paint Business

ACQUISITION

RESTRUCTURINGHindustan Foods simplifies

organizational structure

Hindalco closes acquisition

of Aleris; becomes world's largest

aluminium company

LEGALOrient Refractories–

RHI Magnesita Composite

Scheme rejected

MERGERReliance Jio - Facebook deal:

Network Synergy at the Core

Page 20

COV

ER

ST

OR

Y

20 Vol. XXIX Issue No. 2 May 2020

Kamdhenu

Demerges its

Paint Business

The transaction may look

straight forward but the

consideration, transaction

structure and re-organisation

makes it complicated.Anirudha Jain

Page 21

In a move to separate the Paint Business

from its Core Steel Business, Kamdhenu

L i m i t e d a n n o u n c e d S c h e m e o f

Arrangement (“Scheme”) whereby, it will

de-merge its Paint Business to the newly

incorporated step-down wholly-owned

subsidiary of the Kamdhenu Limited.

The Scheme inter-alia also provides for

amalgamation of Promoter entities

(which together holds substantial stake in

Kamdhenu Limited) in Kamdhenu Limited

thereby collapsing the inter-company

holding structure.

Though apparently, the transaction look

simple, the consideration, transaction

structure and re-organisation of share

capital post-transaction makes it

complicated.

Kamdhenu Limited (“the Transferee

Company/Demerged Company”) is

engaged in manufacturing, branding,

m a r k e t i n g a n d d i s t r i b u t i o n o f

KAMDHENU brand products like Steel

TMT bars, decorative paints and allied

products. Thus, the Demerged Company

has two distinct business segments-Steel

Division and Paint Division.

In the Steel Business, Kamdhenu has its

own TMT manufacturing plant at

Bhiwandi from where it is catering the

market of Delhi and NCR. The rest of India

is being catered by the Franchisee

Network of the Company. Kamdhenu

TMT is one of the largest selling TMT

brand in India, in the retail segment.

In the Paint Business, the Demerged

Company is into decorative paint

segment wherein it manufactures all

types of paints including interior, exterior,

emulsions, textures, designer paints and

all varieties of paints, competing with the

leading paint manufacturers in India. The

Company is also outsourcing the Paint

Products to meet the Market Demand.

Kamdhenu Concast Limited (Transferor

Company 1) is an unlisted closely held

company. Presently, the Transferor

Company 1 is engaged in marketing and

branding of steel and allied products and

other related activities. The Transferor

Company 1 has also made investments in

securities (including investment in

Kamdhenu Ltd).

Kamdhenu Overseas Limited (Transferor

Company 2) is an unlisted closely held

company. Presently, the Transferor

Note: The number of RSUs outstanding as on 11 December 2019 is 17,54,894 against which 10,52,937 Equity Shares are

proposed to be allotted before the effectiveness of the Scheme.

As the Equity Shares of RRL are not listed on any stock exchanges, RRL has been receiving requests from the employees

holding Equity Shares for providing them options for exit and liquidity, including by way of listing of the Equity Shares.

However, the Company has no plan to list its equity shares.

www.mergersindia.com www.mnacritique.com 21

The government finally rescued Yes Bank,

the country's biggest-ever banking

failure, by asking state-run State Bank of

India to infuse Rs 7,250 crore and take 45%

stake in the bank. Reserve Bank of India

cleared the ground for the takeover.

Proactively, the central bank had unveiled

a dra reconstruction scheme on March 6

for the capital-starved Yes Bank and even

superseded the bank's board for 30 days

on ground of a “serious deterioration” in

its financial position and the absence of a

viable revival plan. The government had

even put a sudden moratorium on cash

withdrawals. While the country's largest

lender may have rescued Yes Bank, the

crisis clearly indicates the level of financial

stress in the banking and financial sector.

If one looks at Q3 FY20 results of YES

Bank LTD published soon aer the

announcement of the reconstruction

scheme , it is crystal clear that the bank

net worth is wiped out fully with negative

capital hence in common parlance it has

collapsed and cannot continue to do its

business without augmenting its capital

and have confidence of its creditors

including all current, fixed deposit and

saving account holders.

Crumbling of a bank this size can have

loss of confidence in the whole financial

systems which could lead to a collapse of

multiple institutions and companies. Aer

the bank on its own failed to get the

investors in last six months to avoid its

collapse, the government has no choice

but to come out with the bailout plan in

the form of the scheme.

The Central Government has notified the

“YES Bank Limited Reconstructed

Scheme, 2020” (Reconstruction Scheme)

in exercise of powers conferred by sub-

section (4) and sub-section (7) ofsection

45 of the Banking Regulation Act, 1949

which came into force on 13th March 2020.

Reserve Bank of India (RBI) has power to

make application to Central Government

for an order of moratorium in respect of

Banking Company when RBI is of the

opinion that there is “Good Reason” to do

so. Banking Regulation Act, 1949 does not

list down the specific events on the

occurrence of which RBI may make

application to Central Government for an

o r d e r o f m o r a t o r i u m . R B I h a s

discretionary power to make such

application to Central Government.

The transaction may look straightforwardbut the consideration, transaction structureand re-organisation makes it complicated.

Page 22

22 Vol. XXIX Issue No. 2 May 2020

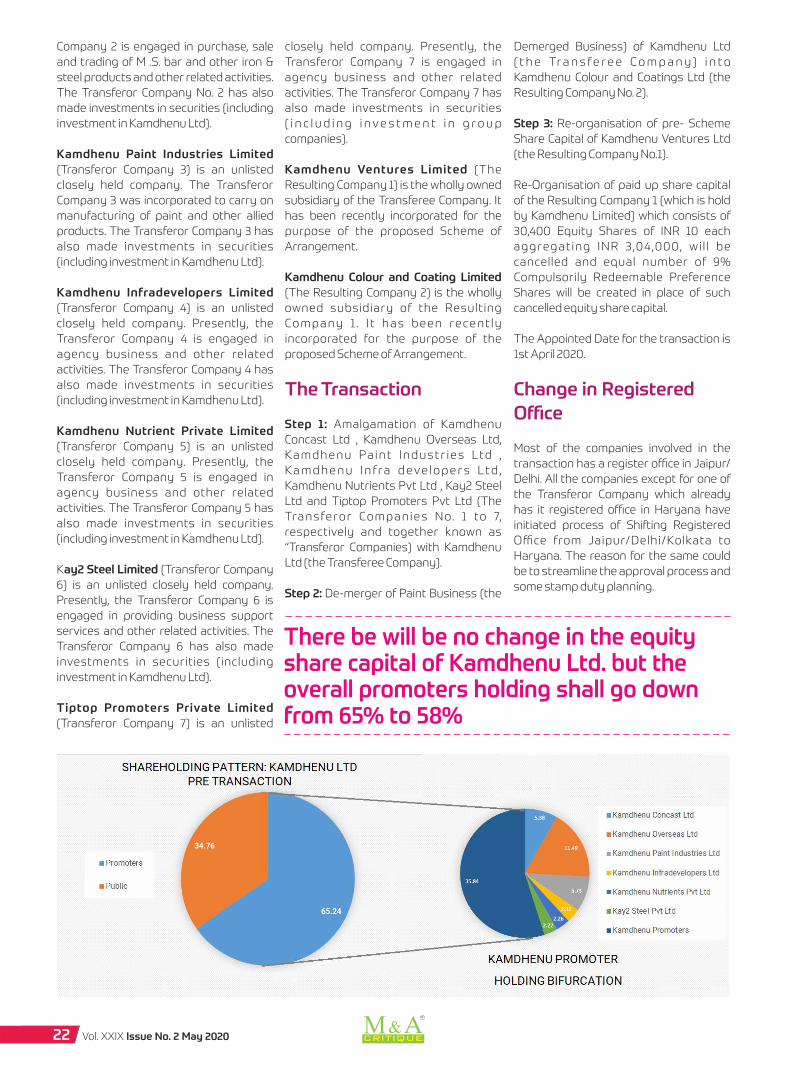

Company 2 is engaged in purchase, sale

and trading of M .S. bar and other iron &

steel products and other related activities.

The Transferor Company No. 2 has also

made investments in securities (including

investment in Kamdhenu Ltd).

Kamdhenu Paint Industries Limited

(Transferor Company 3) is an unlisted

closely held company. The Transferor

Company 3 was incorporated to carry on

manufacturing of paint and other allied

products. The Transferor Company 3 has

also made investments in securities

(including investment in Kamdhenu Ltd).

Kamdhenu Infradevelopers Limited

(Transferor Company 4) is an unlisted

closely held company. Presently, the

Transferor Company 4 is engaged in

agency business and other related

activities. The Transferor Company 4 has

also made investments in securities

(including investment in Kamdhenu Ltd).

Kamdhenu Nutrient Private Limited

(Transferor Company 5) is an unlisted

closely held company. Presently, the

Transferor Company 5 is engaged in

agency business and other related

activities. The Transferor Company 5 has

also made investments in securities

(including investment in Kamdhenu Ltd).

Kay2 Steel Limited (Transferor Company

6) is an unlisted closely held company.

Presently, the Transferor Company 6 is

engaged in providing business support

services and other related activities. The

Transferor Company 6 has also made

investments in securities (including

investment in Kamdhenu Ltd).

Tiptop Promoters Private Limited

(Transferor Company 7) is an unlisted

closely held company. Presently, the

Transferor Company 7 is engaged in

agency business and other related

activities. The Transferor Company 7 has

also made investments in securities

( i n c l u d i n g i n v e s t m e n t i n g r o u p

companies).

Kamdhenu Ventures Limited (The

Resulting Company 1) is the wholly owned

subsidiary of the Transferee Company. It

has been recently incorporated for the

purpose of the proposed Scheme of

Arrangement.

Kamdhenu Colour and Coating Limited

(The Resulting Company 2) is the wholly

owned subsidiary of the Resulting

Company 1 . I t has been recent ly

incorporated for the purpose of the

proposed Scheme of Arrangement.

The Transaction

Step 1: Amalgamation of Kamdhenu

Concast Ltd , Kamdhenu Overseas Ltd,

Kamdhenu Pa int Industr ies Ltd ,

Ka m d h e n u I n fra d eve l o p e r s Ltd ,

Kamdhenu Nutrients Pvt Ltd , Kay2 Steel

Ltd and Tiptop Promoters Pvt Ltd (The

Transferor Companies No. 1 to 7,

respectively and together known as

“Transferor Companies) with Kamdhenu

Ltd (the Transferee Company).

Step 2: De-merger of Paint Business (the

There be will be no change in the equityshare capital of Kamdhenu Ltd. but theoverall promoters holding shall go downfrom 65% to 58%

Demerged Business) of Kamdhenu Ltd

( t h e Tra n s f e r e e C o m p a n y ) i n t o

Kamdhenu Colour and Coatings Ltd (the

Resulting Company No. 2).

Step 3: Re-organisation of pre- Scheme

Share Capital of Kamdhenu Ventures Ltd

(the Resulting Company No.1).

Re-Organisation of paid up share capital

of the Resulting Company 1 (which is hold

by Kamdhenu Limited) which consists of

30,400 Equity Shares of INR 10 each

aggregating INR 3,04,000, wi l l be

cancelled and equal number of 9%

Compulsorily Redeemable Preference

Shares will be created in place of such

cancelled equity share capital.

The Appointed Date for the transaction is

1st April 2020.

Change in Registered

Office

Most of the companies involved in the

transaction has a register office in Jaipur/

Delhi. All the companies except for one of

the Transferor Company which already

has it registered office in Haryana have

initiated process of Shiing Registered

Office from Jaipur/Delhi/Kolkata to

Haryana. The reason for the same could

be to streamline the approval process and

some stamp duty planning.

Page 23

www.mergersindia.com www.mnacritique.com 23

Shareholding Pattern

The Transferor Companies 1 to 6 are the

promoter group companies of the

Transferee Company. The Transferor

Companies1 to 6 are jointly holding

29.40% of the present share capital of the

transferee Company.

The Sharehold ing pattern of the

Transferor Companies is complex. There is

cross-holding among many of the

Transferor Companies. Further, apart

from promoters, Public Shareholders also

he ld some stake in many of the

companies.

Swap Ratio

Consideration for

Amalgamation:

The consideration of the amalgamation of

the Transferor Companies with the

Transferee Company; in respect of the

investment in the Transferee Company,

the shareholders of the Transferor

C o m p a n i e s w i l l b e i s s u e d , o n

proportionate basis, exactly the same

number of equity shares , as the

Transferor Companies are holding in the

Transferee Company i.e. the same number

of equity shares held by the Transferor

Companies of Transferee Company will be

issued to the shareholders of the

Transferor Company.

In respect to the remaining businesses of

these Transferor Companies , the

s h a re h o l d e r s o f t h e Tra n s f e ro r

Companies will be issued Noncumulative

Compulsory Redeemable Preference

Shares ("CRPS") in the Transferee

Company of INR 10 each, on proportionate

basis.

Please share your experiences/feedback with

us on [email protected]

Table 2: NPA Ratios of YES Bank as on 31.12.2019

Number of Shares

40,709.20

27,710.44

31,071.20

18.87 %

5.97%

Particulars

Gross NPA balance

Provision made in 9 months ending

Cl. Bal. of Provision

Gross NPA to Gross Advances%

Net NPAs to Net Advances %

Source: Basel III disclosures 31-12-2019

Transferor Companies

Investment in Transferee Co.

Equity Shares

Other Business

Non-Redemable Preference Shares

Page 24

24 Vol. XXIX Issue No. 2 May 2020

Not allowing YES Bank to collapse for

Indian banking and financial systems is

similar tonot allowing COVID-19 to infect

the large popu lat ion . The new

management needs to define priorities.

Identify and communicate the three to

five most important ones. Early in the

crisis, those might include employee's

retention, financial liquidity, customer

care both depositors and lenders, and

operational continuity. Document the

i s s u e s i d e n t i fi e d , e n s u re t h a t

leadership is fully aligned with them,

and make course corrections as events

unfold. Make smart trade-offs. It may

not be easy in any way.What conflicts

might arise among the priorities?

B e t w e e n t h e u r g e n t a n d t h e

important? Between survival today and

success tomorrow? Instead of thinking

about al l possibi l i t ies , the best

m a n a g e m e n t s h o u l d u s e t h e i r

priorities as a scoring mechanism to

force trade-offs.

The above is possible if the bank name

the decision makers. In the central

co m m a n d “wa r ro o m , ” i t m u s t

beestab l ished who owns what .

Empower the front l ine to make

decisions where possible, and clearly

state what needs to be escalated, by

when, and to whom. Your default

should be to push decisions downward,

not up.The management should

embrace action, and not waste time to

punish mistakes. In triage situations,

it's crucial to have an accurate, current

picture of what is happening on the

ground. leaders must get situational

assessments early and oen. One way

is to create a network of local leaders

and influencers who can speak with

deep knowledge about the impact of

the crisis and the sentiments of

customers, depositors, employees, and

other stakeholders. Technology can

bring the parties together; and in fact

on online payments and use of UPI,YES

Bank is the leader. The success

depends on how the management can

lead with empathy and handle

changing dynamics.

Every month M & A critique gives valuable insights to

over 5000 Readers from Corporate World on-

- Recent Deals in the M & A Space

- Updated News on National, International & Cross-Border News

- M & A Happening s in High Court Updated every month

Advertise with us to reach the key decision makers

in the Corporate World.

For more info,

Contact:- 020-24425826

Email: [email protected]

Reconstruction

Scheme for YES Bank –

Key to Survival of

the Indian

financial systems

INSOLVENCY

LEGALWays for Compulsory exit to

minority shareholders of unlisted firms

NCLT clears state-owned NBCC's

bid for Jaypee Infratech

MERGERPowerhouse in the making: RIL merges media

content and distribution with Network18

INSOLVENCYReverse corporate insolvency resolution:

A panacea in case of real estate sector

April 2020 150/-

The Sharehold ing pattern of the

Transferor Companies is complex. There is

cross-holding among many of the

Transferor Companies. Further, apart

from promoters, Public Shareholders also

he ld some stake in many of the

companies.

In respect to the remaining businesses of

these Transferor Companies , the

s h a r e h o l d e r s o f t h e Tra n s f e r o r

Companies will be issued Noncumulative

Compulsory Redeemable Preference

Shares ("CRPS") in the Transferee

Company of INR 10 each, on proportionate

basis.

The total number of Equity Shares to be

issued by the Transferee Company to the

S h a re h o l d e r s o f t h e Tra n s f e ro r

Companies will be equal to the aggregate

number o f Equ i ty Share s o f the

Transferee Company held by the

Transferor Companies. Hence, there be

will be no change in the equity share

capital of the Transferee Company post-

transaction. However, as some stake in

Transferor Companies are held by the

public, the promoter holding in the

Kamdhenu Limited post-transaction will

be reduced to circa 58% from current circa

65%.

Compulsorily Redeemable Preference

Shares to be issued will carry a coupon

rate of 9% per annum. CRPS shall be

redeemed in terms of the provisions of the

Companies Act, 2013, at Par within a

period of 5 years from the date of issue of

such Redeemable Preference Shares with

a call option available to the Issuer

Company for early redemption. The CRPS

will not be listed on exchanges.