21

Microfinance and intra-household management Lessons from rural South-India Isabelle Guérin Institut de recherche pour le Développement French Institute of Pondicherry March 2009

| Date post: | 31-Dec-2015 |

| Category: |

Documents |

| Upload: | laurel-paul |

| View: | 214 times |

| Download: | 0 times |

Microfinance and intra-household management

Lessons from rural South-India

Isabelle Guérin

Institut de recherche pour le Développement

French Institute of Pondicherry

March 2009

Guérin March 2009

Problem to be adressed

Microfinance: above all a matter of women! Controversial results (Kabeer 2001)

Empowerment (Hashemi et al. 1996; Khandker et al. 1995; Holvoet 2005)

Or disempowerment (Rahman 1989; Goetz & Gupta 1989; Rao 2005; Rankin 2002; Molyneux 2002)

Intra-household management: a black box!

Guérin March 2009

Research Objectives

Opening the household black box Analysis of gender financial responsabilities Analysis of gender financial practices (saving,

borrowing)

→ Better understanding of microfinance effects

Guérin March 2009

Literature review Intra-household management literature

Complexity and diversity of intra-household management systems

Gap between responsabilities and control History (Fontaine, 2001; Perrot 2001; Zelizer 1995) Sociology and Anthropology (Guyer & Peters, 1989; Pahl 1989, 2000; Vogler 1998;

Bruce and Dwyer 1988, Burgoyne, 2008). Economics (Kabeer, 1994)

Intra-household management and microfinance Main question: who control the loans?

Male appropriation → domination (Goetz & Gupta 1996; Rahman 1989)

Male appropriation → Negociations and compromises (Kabeer 2001)

Guérin March 2009

Main results

Result 1. Women in household budget management: a permanent paradox Balancing the budget without controlling income

Result 2. Women-led financial circuits Diversity of financial practices, partly secrete

Result 3. What about microfinance? More responsabilities more pressure Microcredit use: a bargaining process Better management or risks of over-

indebtedness?

Guérin March 2009

Theoretical framework

Intra-household relationships Conflicts and cooperation (Folbre 1990 ; Kabeer

1994; Sen 1990) Patriarchal bargain (Kandioty 1988) Compromise and resistance (Agarwal 1994)

→ hypothesis suggested here: financial circulation within households is at the core of this permanent process of bargaining, compromises and resistance

Guérin March 2009

Methodology

Descriptive statisticsDescriptive statistics 170 households170 households

For specific questions, For specific questions, women women and menand men have been have been interviewedinterviewed

All are microfinance clientsAll are microfinance clients

Qualitative analysisQualitative analysis Semi-structured interviewsSemi-structured interviews Group discussionGroup discussion ObservationObservation Informal discussionsInformal discussions

Guérin March 2009

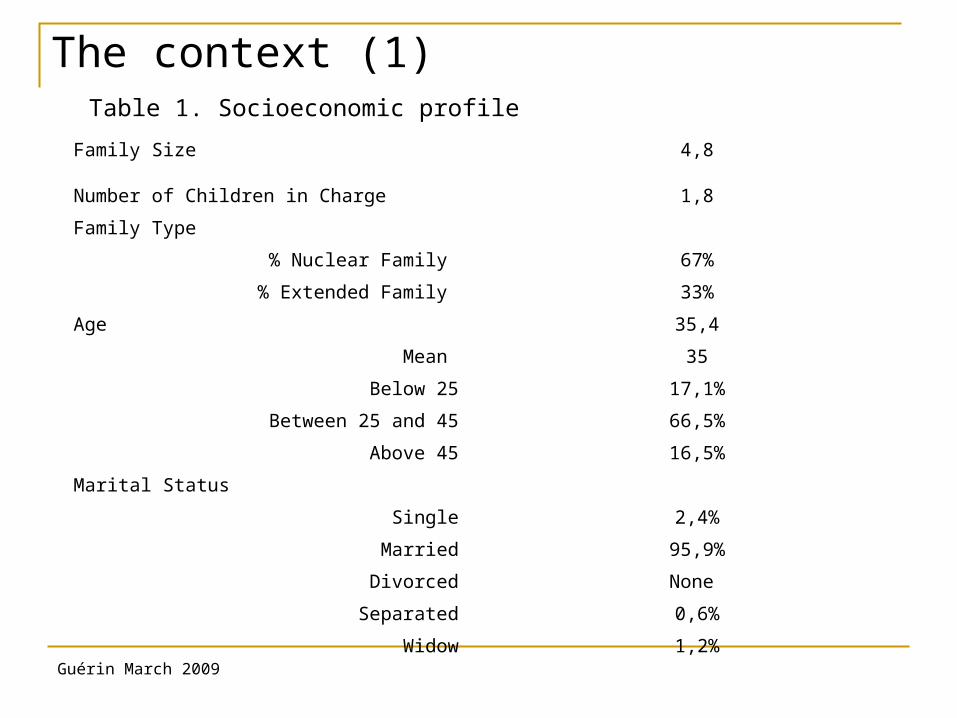

The context (1)

Family Size 4,8

Number of Children in Charge 1,8

Family Type

% Nuclear Family 67%

% Extended Family 33%

Age 35,4

Mean 35

Below 25 17,1%

Between 25 and 45 66,5%

Above 45 16,5%

Marital Status

Single 2,4%

Married 95,9%

Divorced None

Separated 0,6%

Widow 1,2%

Table 1. Socioeconomic profile

Guérin March 2009

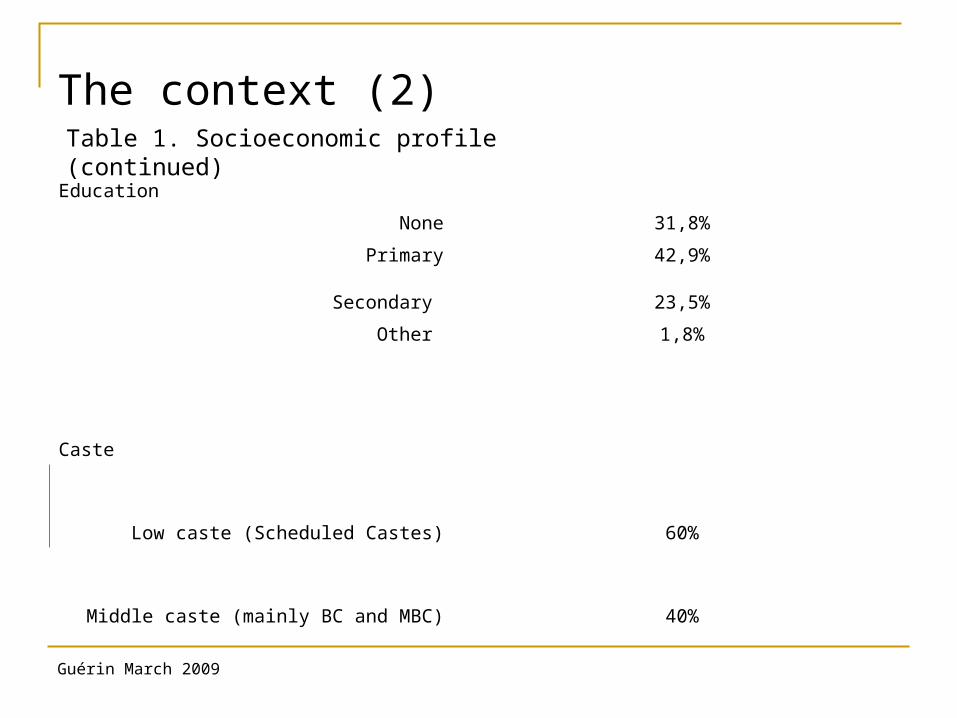

The context (2)

Education

None 31,8%

Primary 42,9%

Secondary 23,5%

Other 1,8%

Caste

Low caste (Scheduled Castes) 60%

Middle caste (mainly BC and MBC) 40%

Table 1. Socioeconomic profile (continued)

Guérin March 2009

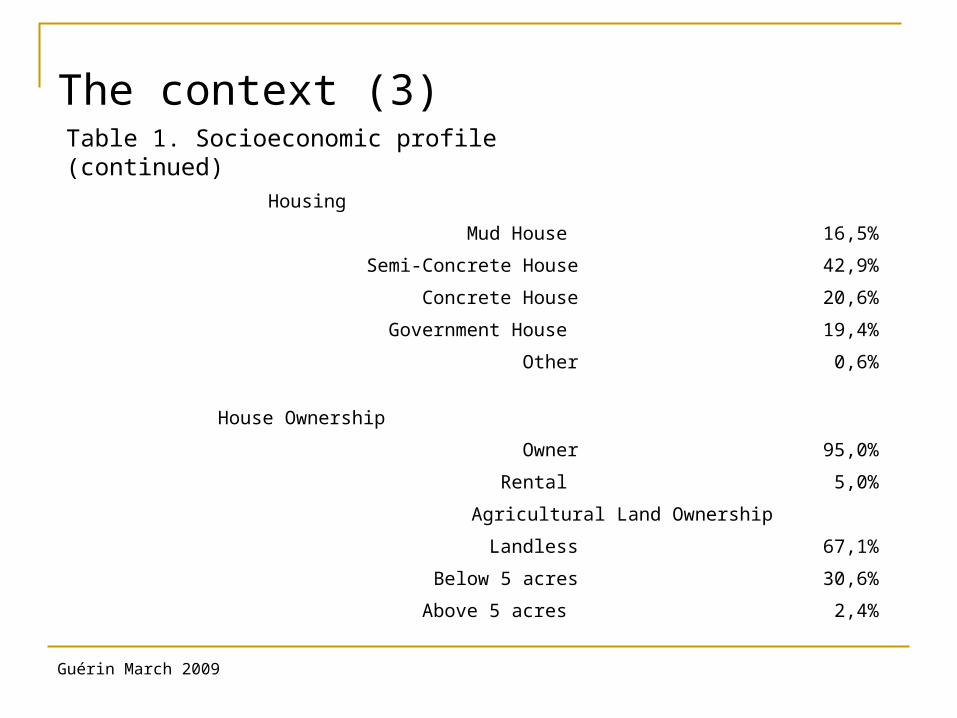

The context (3)

Housing

Mud House 16,5%

Semi-Concrete House 42,9%

Concrete House 20,6%

Government House 19,4%

Other 0,6%

House Ownership

Owner 95,0%

Rental 5,0%

Agricultural Land Ownership

Landless 67,1%

Below 5 acres 30,6%

Above 5 acres 2,4%

Table 1. Socioeconomic profile (continued)

Guérin March 2009

The context (4)

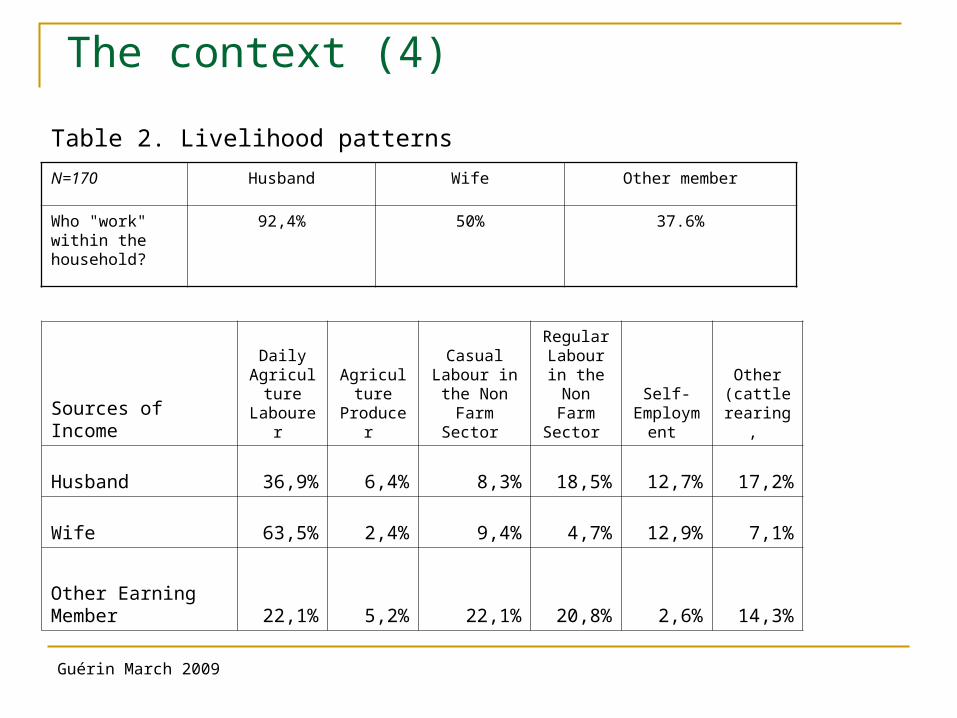

N=170 Husband Wife Other member

Who "work" within the household?

92,4% 50% 37.6%

Sources of Income

Daily Agricultur

e Labourer

Agriculture

Producer

Casual Labour in the Non

Farm Sector

Regular Labour in the Non

Farm Sector

Self-Employm

ent

Other (cattle

rearing,

Husband 36,9% 6,4% 8,3% 18,5% 12,7% 17,2%

Wife 63,5% 2,4% 9,4% 4,7% 12,9% 7,1%

Other Earning Member 22,1% 5,2% 22,1% 20,8% 2,6% 14,3%

Table 2. Livelihood patterns

Guérin March 2009

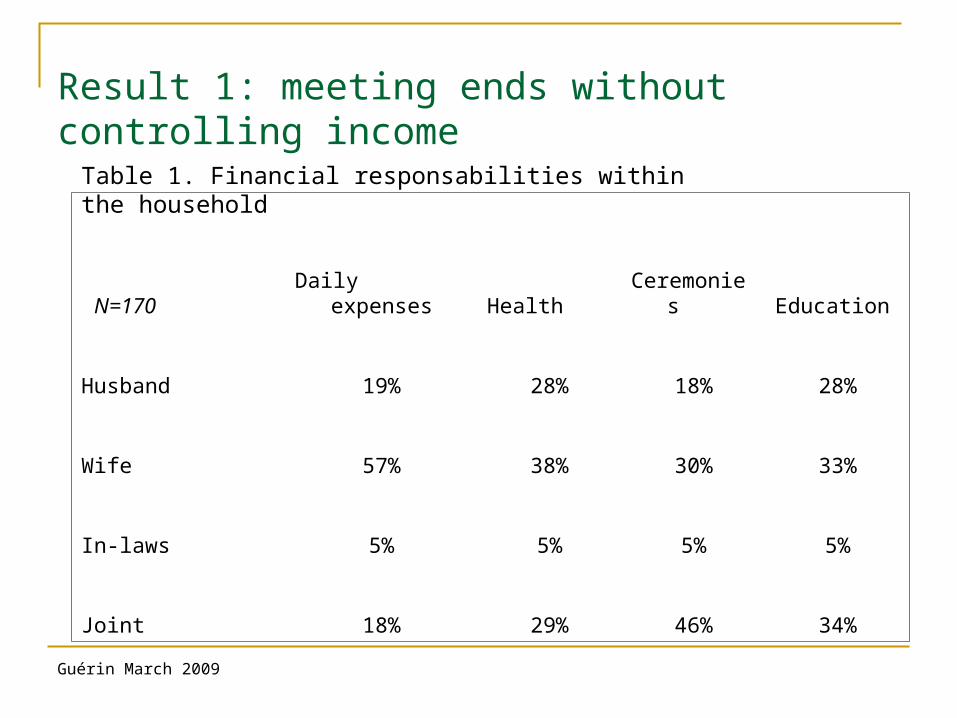

Result 1: meeting ends without controlling income

N=170 Daily expenses Health Ceremonies Education

Husband 19% 28% 18% 28%

Wife 57% 38% 30% 33%

In-laws 5% 5% 5% 5%

Joint 18% 29% 46% 34%

Table 1. Financial responsabilities within the household

Guérin March 2009

Result 1: meeting ends without controlling income → huge responsabilities in terms of saving, borrowing and repayment

N=170% resp income

% resp saving

% resp borrowing % repayment

No role 19% 2% 1% 3%

Minor role (<20%) 46% 46% 51% 62%

Moderate role (20-60%) 28% 34% 25% 18%

Major role (>60%) 6% 17% 23% 16%

Table 2. Women responsabilities in terms of income, saving borrowing and repayment

Guérin March 2009

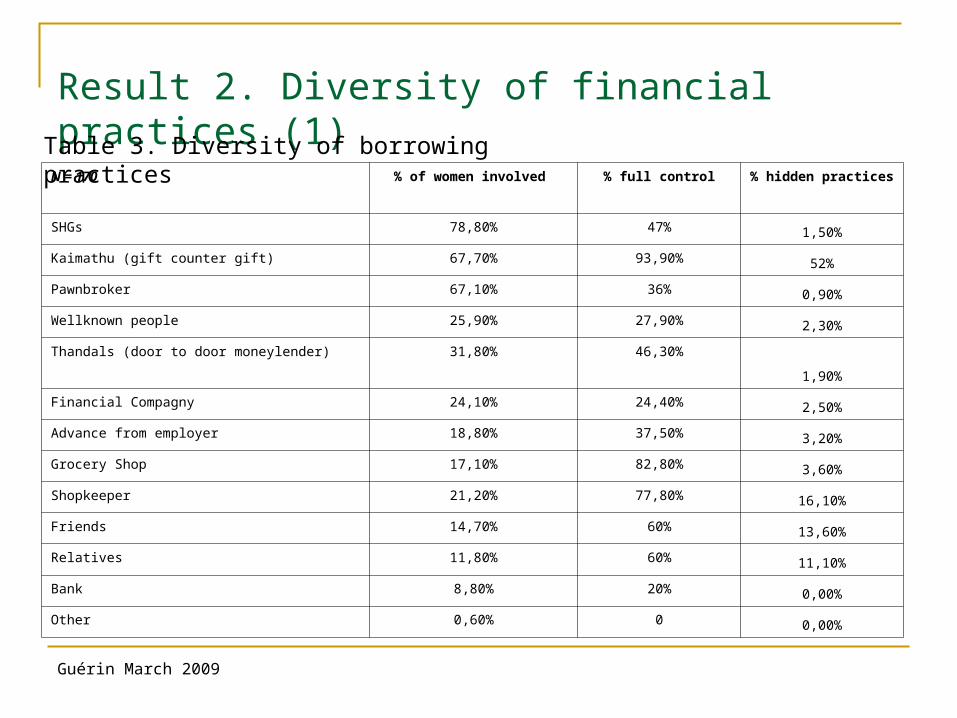

Result 2. Diversity of financial practices (1)

N = 170 % of women involved % full control % hidden practices

SHGs 78,80% 47% 1,50%

Kaimathu (gift counter gift) 67,70% 93,90% 52%

Pawnbroker 67,10% 36% 0,90%

Wellknown people 25,90% 27,90% 2,30%

Thandals (door to door moneylender) 31,80% 46,30%

1,90%

Financial Compagny 24,10% 24,40% 2,50%

Advance from employer 18,80% 37,50% 3,20%

Grocery Shop 17,10% 82,80% 3,60%

Shopkeeper 21,20% 77,80% 16,10%

Friends 14,70% 60% 13,60%

Relatives 11,80% 60% 11,10%

Bank 8,80% 20% 0,00%

Other 0,60% 0 0,00%

Table 3. Diversity of borrowing practices

Guérin March 2009

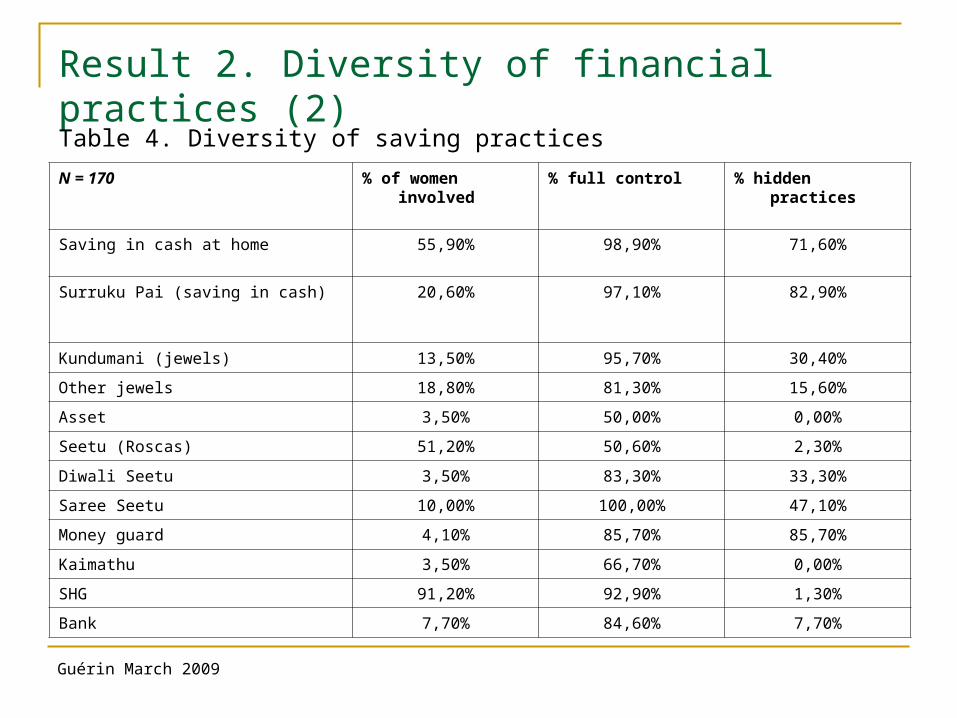

Result 2. Diversity of financial practices (2)

N = 170 % of women involved % full control % hidden practices

Saving in cash at home 55,90% 98,90% 71,60%

Surruku Pai (saving in cash) 20,60% 97,10% 82,90%

Kundumani (jewels) 13,50% 95,70% 30,40%

Other jewels 18,80% 81,30% 15,60%

Asset 3,50% 50,00% 0,00%

Seetu (Roscas) 51,20% 50,60% 2,30%

Diwali Seetu 3,50% 83,30% 33,30%

Saree Seetu 10,00% 100,00% 47,10%

Money guard 4,10% 85,70% 85,70%

Kaimathu 3,50% 66,70% 0,00%

SHG 91,20% 92,90% 1,30%

Bank 7,70% 84,60% 7,70%

Table 4. Diversity of saving practices

Guérin March 2009

Result 2. Diversity of financial practices (3)

0% 10% 20% 30% 40% 50% 60% 70%

Borrow from other women

Exchange jewels

Act as guarantor

Friend act as guarantor

Exchange SHG loans

Figure 1. Women-led financial circuits

Guérin March 2009

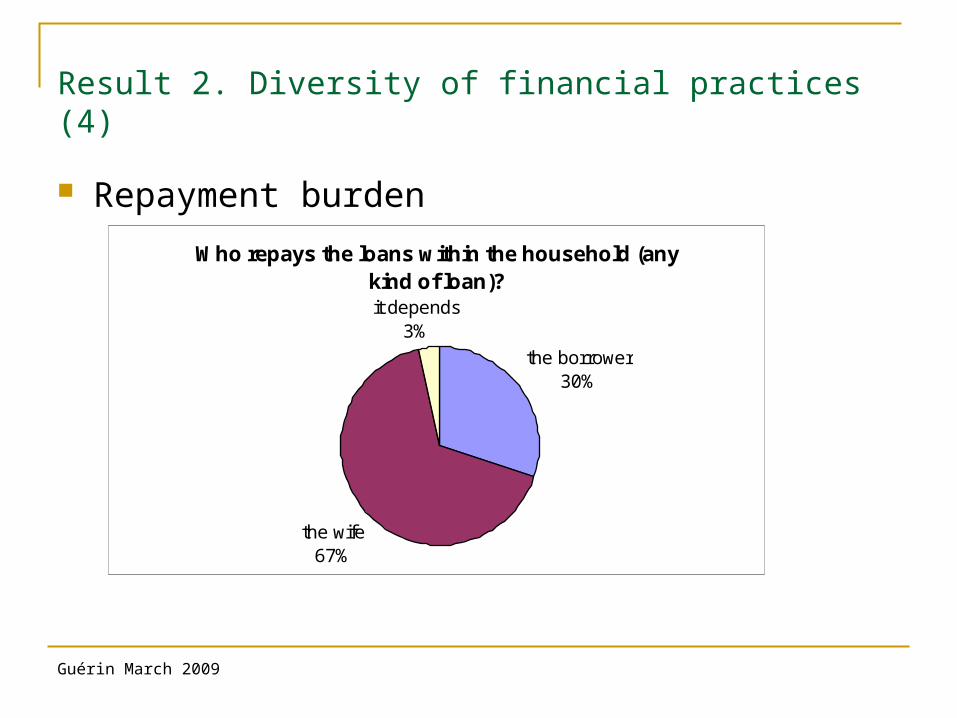

Result 2. Diversity of financial practices (4)

Repayment burden

Who repays the loans within the household (any kind of loan)?

the borrower30%

the wife 67%

it depends3%

Guérin March 2009

Result 3. Microfinance effects on financial management

More responsabilities → more pressure

More involved in financial decisions 40%

Better cashflow management 65%

Better access to the financial market 95%

Less dependant from moneylenders 25%

More pressure 45%

Guérin March 2009

Result 3. Microfinance effects on financial management (2)

N=170 Who controls microcredit?

Husband 17,1%

Wife 47,6%

In-laws 4,1%

Joint 31,2%

Microcredit control: bargaining and compromises

Guérin March 2009

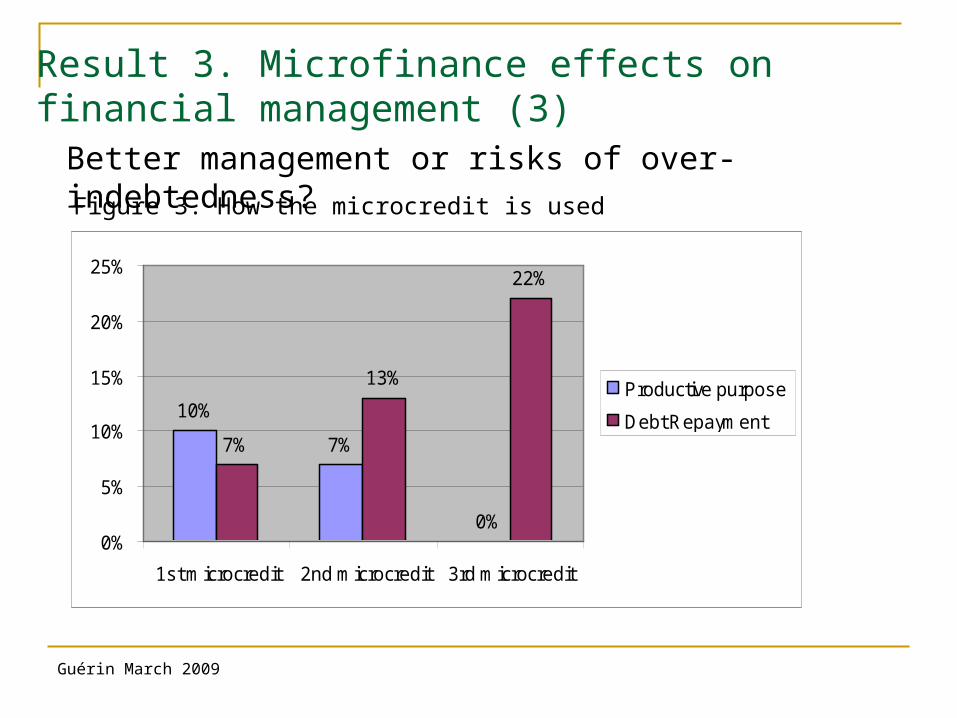

10%

7%

0%

7%

13%

22%

0%

5%

10%

15%

20%

25%

1st microcredit 2nd microcredit 3rd microcredit

Productive purpose

Debt Repayment

Figure 3. How the microcredit is used

Better management or risks of over-indebtedness?

Result 3. Microfinance effects on financial management (3)

Guérin March 2009

Future research

Diversity of women behaviors Diversity of gender practices