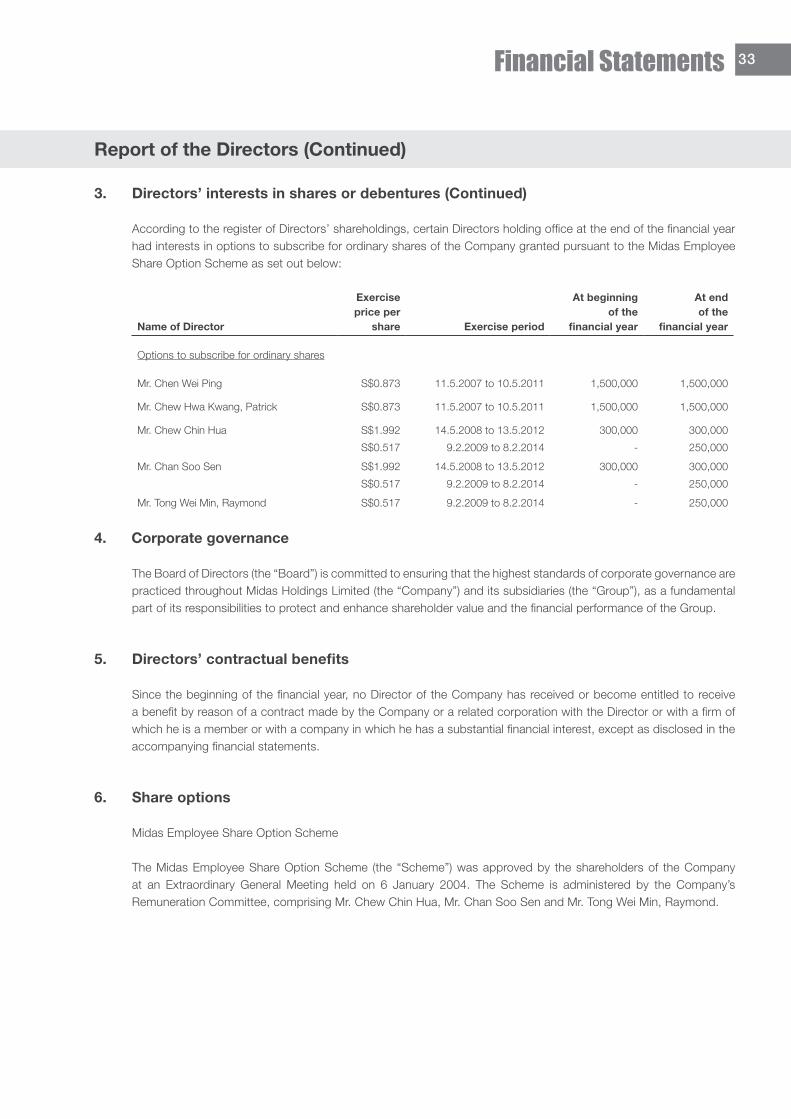

104

Midas Holdings Limited

Midas Holdings Limited

ContentsCorporate Structure 01

Corporate Profile 02

Corporate Information 06

Message from the Executive Chairman 08

Message from the Chief Executive Officer 12

Board of Directors 15

Executive Officers 16

Financial Highlights 17

Financial Contents 18

Corporate StructureCorporate OfficeChen Wei Ping, Executive ChairmanChew Hwa Kwang, Patrick, Chief Executive OfficerTan Kai Teck, Chief Financial OfficerYang Xiao Guang, General Manager (Business Development) Jilin Midas Aluminium Industries Co., LtdWang Jiaxin, General Manager Shanxi Wanshida Engineering Plastics Co., LtdMa Mingzhang, General Manager

Incorporated on 17th of November 2000 as an investment

holding company, and listed on 23rd of February 2004 in

Singapore Stock Exchange, Midas Holdings Limited has

grown over the years to gain recognition as a leading

manufacturer of aluminium alloy extrusion products for the

rail transportation sector in the PRC.

Under the Midas Group are two business divisions,

namely:

(a) the Aluminium Alloy Division, and

(b) the PE Pipes Division

These two divisions are strategically located in the PRC

to take on the opportunities as well as to capitalise on the

potential benefits of the vast developments that are taking

place in the infrastructure and rail transport sectors.

Our customer base consists of all of the major domestic

train manufacturers such as CNR Changchun Railway

Vehicles Co., Ltd, CNR Tangshan Railway Vehicles Co.,

Ltd, Nanjing SR Puzhen Rail Transport Co., Ltd, CSR

Zhuzhou Electric Locomotive Co., Ltd., Bombardier

Sifang (Qingdao) Transportation Ltd, and the top three

global train manufacturers, namely, Alstom, Siemens and

Bombardier.

Besides our core business, we have a 32.5% stake in a

licensed metro train manufacturing company in the PRC,

Nanjing SR Puzhen Rail Transport Co., Ltd.

We are one of only six companies, and the only aluminium

alloy extrusion products manufacturer, in Asia to be

included in the Forbes Asia’s “Best Under A Billion” list for

four consecutive years from 2006 to 2009, in recognition

of our consistent growth and profitability.

Aluminium Alloy DivisionOur Aluminium Alloy Division, Jilin Midas Aluminium

Industries Co., Ltd (“Jilin Midas”), is a leading manufacturer

of aluminium alloy extrusion products for the passenger

rail transportation sector in the PRC. Our Aluminium Alloy

Division is our principal business division and accounted

for 95.4% of our total revenue from continuing operations

for the financial year ended 31 December 2009. We are

also one of the first and amongst the few in the aluminium

alloy extrusion industry in the PRC to possess capabilities

for the downstream fabrication of passenger train car

body components. We have an established track record of

supplying aluminium alloy extrusion products to more than

30 metro and high speed train projects in the PRC since

2003, representing a majority of the aluminium metro and

high speed train projects in the PRC during this period.

In December 2009, our Aluminium Alloy Division was

awarded the prestigious EN 15085-2 certification for the

welding of railway vehicles and components issued by

GSI SLV Duisburg, one of the largest welding engineering

institutes in Europe. The EN 15085-2 welding quality

assurance certification is recognised internationally,

including the Group’s major customers in the PRC, and is a

testimony of the Group’s capabilities to meet international

quality assurance standards for welding works in the

new build, conversion and repair of railway vehicles and

their components. This certification enhances our ability

to provide a complete suite of downstream fabrication

services and strengthens our competitive edge in the

market.

Also in 2009, our Aluminium Alloy Division was awarded

the prestigious International Railway Industry Standard

(IRIS) certification. Jilin Midas is the first company in the

PRC to receive the IRIS certification under the category of

“Manufacturing and Services of Aluminium Alloy Carbody

Profile and Parts for Rail Cars”. Promoted by the European

Rail Industry (UNIFE) and supported by operators, system

I Midas Holdings Limited I Annual Report 20092

Corporate Profile

integrators and equipment manufacturers, the IRIS

complements the internationally recognised ISO 9001

quality standard introducing rail specific requirements.

Chosen based on an assessment of its performance in

innovation, quality, financial health and organisation, our

Aluminium Alloy Division is the first supplier in China to

be included in Alstom’s “Leading Partners 150” (“LP150”)

programme in 2008. Under the terms of the agreement,

our Aluminium Alloy Division is a preferred supplier for

all Alstom’s new and re-sourcing projects globally. Our

Aluminium Alloy Division will also receive resources and

technology support from Alstom to develop key new

products and improve industrial quality standards.

Our Aluminium Alloy Division is accredited with the Quality

Focus Global Sourcing Grade “A” international certification

by ALSTOM Transport SA (“Alstom”), in accordance

to Alstom Transport Standard. As a testimony to our

capability to manufacture large-section aluminium alloy

extrusion products, this certification enables us to be the

global sourcing partner of all Alstom’s units.

In addition, our Aluminium Alloy Division has entered into a

Master Agreement with Siemens Aktiengesellschaft, Berlin

and Munich, Transportation Systems Group (“Siemens”).

Under this agreement, Siemens will engage our Aluminium

Alloy Division as a long term high technology supplier of

aluminium alloy extrusion products in the context of long

term partnership-based cooperation on a global basis.

In recognition of our ability to supply the highest quality

aluminium extrusion products, our Aluminium Alloy Division

was certified as an approved supplier to Changchun

Bombardier Railway Vehicles Co., Ltd (“CBRC”) in January

2006. CBRC is a joint venture between Bombardier

Transportation, the world leader in rail cars manufacturing,

and China’s leading train manufacturer, CNR Changchun

Railway Vehicles Co., Ltd.

We are a PRC certified supplier for the world’s three

renowned train manufacturers, which is a testimony and

endorsement of the quality of our aluminium alloy extrusion

products. This recognition given by Alstom, Siemens and

CBRC has provided us the platform to expand and grow

our business both in the PRC and the international export

markets.

In addition, our Aluminium Alloy Division was named

“2007 China’s Top Brand” by the General Administration

of Quality Supervision, Inspection and Quarantine of the

People’s Republic of China (“AQSIQ”) (国家质量监督检

验检疫总局) , in recognition of our product quality and

strong brand position.

Our Aluminium Alloy Division currently has two production

lines, with annual production capacity of up to 20,000

tonnes. Our production lines can produce large section

aluminium alloy extrusion products of up to 28 metres in

length and 0.7 metres in width for profiles and 0.48 metres

in diameter for large diameter tubes and rods. Our large

section aluminium alloy products are used in a variety

of industries. They are utilised in the rail transportation

industry to manufacture body frames of high-speed

trains and MRT/LRT trains. In addition, our aluminium

alloy products are also used in power stations for power

transmission purposes, electrical energy distribution,

transmission cables as well as production of mechanical

parts for industrial equipment.

In order to meet the increasing demand from our PRC

passenger rail transportation customers, we are in the

process of significantly expanding our production capacity.

In February 2009, we purchased a 110MN extrusion press

which will be installed in one of our current production

plants in Liaoyuan and is scheduled to commence

installation and commissioning in the second quarter of

2010. In August 2009, we purchased a 36MN extrusion

press and a 95MN extrusion press. Our 36MN extrusion

Business Review 3

press was delivered for installation and commissioning in

the first quarter of 2010. Our 95MN extrusion press, on

the other hand, is expected to be delivered for installation

and commissioning in August 2010. The addition of these

three new extrusion production lines will increase our total

annual production capacity from 20,000 tonnes to 50,000

tonnes by the end of 2010. Our Aluminium Alloy Division

currently has one fabrication line, with the capability to

fabricate car body components for 300 train cars. We are

increasing our capacity to fabricate car body components

for 1000 train cars by adding two additional fabrication

lines by the end of 2010.

Since 2004, we have successfully exported / secured

contracts for our large section aluminium alloy profiles to

manufacture body frames for the Singapore Downtown

Line Project, Singapore Circle Line Project, the Metro

Oslo MRT Project in Norway, the Valero Rus Project for

the Russian market, the Desiro Mainline Project for the

European and ex-European markets, the Helsinki –

St. Petersburg High Speed Train Project, the Incheon

International Airport Railroad Project in South Korea and

RS-Citadis Project for the European market and Saudi

Arabia Metro Project and Iran Metro Project for the Middle

East market.

We are involved in many high profile rail transport projects

in the PRC since 2003. Some of these metro projects

include:

• ShanghaiMRTLine1ExtensionProject

• ShanghaiMRTLine1Extension2Project

• ShanghaiMRTLine2Extension1Project

• ShanghaiMetroLine6Project

• ShanghaiMetroLine7Project

• ShanghaiMetroLine8Project

• ShanghaiMetroLine9Project

• ShanghaiMetroLine10Project

• ShanghaiMetroLine11Project

• ShanghaiYangpuMRTLinePhase1Project

• ShanghaiPearlLineProject

• ShenzhenMRTLine1ExtensionProject

• ShenzhenMRTLine4Project

• NanjingMetroLine1Project

• NanjingMetroLine2Project

• GuangzhouMRTLine2Project

• GuangzhouMRTLine3Project

• GuangzhouMRTLine8Project

• GuangzhouLine3AirportLineProject

• TianjinMRTProject

• ChangchunCityLightRailProject

We are currently the market leader in supplying large

section aluminium alloy profiles for the railway industry

in the PRC. Significantly, we were appointed the supplier

for some major high speed train projects in the PRC,

namely:

• RegionalLinePhase1Project

• BeijingtoTianjinHighSpeedTrainProject

• CRH3-380Project

• CRH3-300Project

• CRH5EMUProject

• CRH1EMUProject

• MagneticLevitationTrainPrototypeProject

The recognition for our manufacturing capability of

aluminium alloy extrusion products positions us for greater

growth in the PRC market. Moving forward, we aim to

expand our presence internationally by capitalising on

opportunities emanating from the overseas market.

I Midas Holdings Limited I Annual Report 20094

Corporate Profile

PE Pipes DivisionOur PE Pipes Division manufactures PE pipes for use in

various types of piping networks, including gas piping

networks and water distribution networks.

Made of high density polyethylene, PE pipes are relatively

light-weight and chemically inert. Considered as viable

substitutes for traditional concrete and metal pipes, PE

pipes are easier and safer to install, more durable and

flexible. A proponent that is non-toxic in nature, our PE

pipes are cost efficient and possess high resistance to

corrosion.

Broadly categorised into two types of PE pipes, namely

the Gas PE Pipes and the Water PE Pipes which are

manufactured through the extrusion process, we

manufacture the various parts required in a piping

network, including pipes, joints and fittings. We also have

an installation team which assists customers in installing

and commissioning the PE pipes used in water distribution

networks. We do not undertake any installation work for

PE pipes used in gas distribution networks.

Our PE Pipes Division accounted for 4.6% of our total

revenue from continuing operations for the year ended 31

December 2009. As we consider our PE Pipes Division

to be a non-core business, representing a relatively small

portion of our Group’s revenue, we currently do not have

plans to further expand our PE Pipes business.

Joint VentureWe have a 32.5% equity stake in a Sino-foreign joint

venture, Nanjing SR Puzhen Rail Transport Co., Ltd.

(“NPRT”), which started commercial production in

FY2007. Through NPRT, we are able to further entrench

our position in the PRC railway industry as NPRT is one

of the four rolling stock companies in the PRC licensed to

manufacture and sell metro trains on a nationwide basis.

Many PRC cities have plans to build metro lines to facilitate

urban transportation; we believe that NPRT will be a direct

beneficiary of the high growth metro train industry in the

PRC given the limited number of players in the market.

Since inception, NPRT, together with its consortium

partners, has secured several high profile metro train

projects in the PRC, namely:

• NanjingMetroLine2Project,

• ShanghaiMetroLine10Project,

• NanjingMetroLine1ExtensionProject,

• ShanghaiMetroLine2EasternExtensionProject,

• ShenzhenMetroLine4Phase2Project,

• HangzhouMetroLine1Project,

• PearlRiverDeltaInter-CityTrainProject

(Dongguan-Shenzhen Section), and

• Dongguan-HuizhouInter-CityTrainProject.

Moving ForwardIn our comparatively short history, we are encouraged by

our current success. Moving forward, we are committed

to springboard towards greater expansion, growth value

creation, as well as strengthen our key competencies.

Business Review 5

BOARD OF DIRECTORS

Mr. Chen Wei Ping, Executive Chairman

Mr. Chew Hwa Kwang, Patrick, Chief Executive Officer

Mr. Chan Soo Sen, Independent Director

Mr. Chew Chin Hua, Independent Director

Mr. Tong Wei Min, Raymond, Non-Executive Director

Dr. Xu Wei Dong, Independent Director

AUDIT COMMITTEE

Mr. Chew Chin Hua, Chairman

Mr. Chan Soo Sen

Mr. Tong Wei Min, Raymond

NOMINATING COMMITTEE

Mr. Chan Soo Sen, Chairman

Mr. Tong Wei Min, Raymond

Mr. Chew Chin Hua

REMUNERATION COMMITTEE

Mr. Chan Soo Sen, Chairman

Mr. Chew Chin Hua

Mr. Tong Wei Min, Raymond

COMPANY SECRETARY

Ms. Tan Cheng Siew @ Nur Farah Tan, ACIS

REGISTERED OFFICE

2 Shenton Way

#04-01 SGX Centre 1

Singapore 068804

Tel: (65) 6438 3052

Fax: (65) 6438 3053

Website: www.midas.com.sg

Company Registration No. 200009758W

AUDITORS

BDO LLP

19 Keppel Road, #02-01

Jit Poh Building

Singapore 089058

Partner-in-charge: Mr Chan Hock Leong(Appointed with effect since financial year ended

31 December 2007)

SHARE REGISTRAR

Intertrust Singapore Corporate

Services Pte Ltd

3 Anson Road #27-01

Springleaf Tower

Singapore 079909

Corporate Information

BANKERS

DBS Bank

6 Shenton Way

DBS Building Tower 1

Singapore 068809

Oversea-Chinese Banking

Corporation Limited

65 Chulia Street

OCBC Centre

Singapore 049513

Industrial & Commercial

Bank of China

Liaoyuan City Branch

518 Renmin Avenue,

Liaoyuan City,

Jilin Province, PRC 136200

China Construction Bank

Liaoyuan City Branch

418 Renmin Avenue,

Liaoyuan City,

Jilin Province, PRC 136200

Agricultural Bank of China

Liaoyuan City Branch

303 Renmin Avenue,

Liaoyuan City,

Jilin Province, PRC 136200

Industrial & Commercial

Bank of China

Shanxi Branch

Da Yu West Street,

Ruicheng County,

Shanxi Province, PRC 044600

SUBSIDIARIES

Green Oasis Pte Ltd

2 Shenton Way

#04-01 SGX Centre 1

Singapore 068804

Tel: (65) 6438 3052

Fax: (65) 6438 3053

North East Industries Pte Ltd

2 Shenton Way

#04-01 SGX Centre 1

Singapore 068804

Tel: (65) 6438 3052

Fax: (65) 6438 3053

Midas Ventures Pte. Ltd.

2 Shenton Way

#04-01 SGX Centre 1

Singapore 068804

Tel: (65) 6438 3052

Fax: (65) 6438 3053

Jilin Midas Aluminium Industries Co., Ltd

188 Fuzhen Road

Liaoyuan City

Jilin Province

PRC 136200

Tel: (86) 437 - 508 2536

Fax: (86) 437 - 508 2500

Shanxi Wanshida Engineering Plastics

Co., Ltd

108 Yongle South Road

Ruicheng County

Shanxi Province

PRC 044600

Tel: (86) 359 - 303 0518

Fax: (86) 359 - 302 7431

Midas Trading (Beijing) Co., Ltd

Room 2007, Unit B, North Tower,

SOHO Shangdu,

8 Dongdaqiao Road

Chao Yang District

Beijing 100020

Tel: (86) 10 - 5869 8872

Fax: (86) 10 - 5869 8873

ASSOCIATE

Nanjing SR Puzhen Rail Transport

Co., Ltd.

No. 208 Puzhu Middle Road, Nanjing, Jiangsu

Province

PRC 210031

Tel: (86) 25 – 8584 8111

Fax: (86) 25 – 8584 7392

IR CONTACT

Citigate Dewe Rogerson,

i.MAGE Pte Ltd

1 Raffles Place

#26-02 OUB Centre

Singapore 048616

Tel: (65) 6534 5122

Fax: (65) 6534 4171

I Midas Holdings Limited I Annual Report 20096

We are on track to more than double our

existing production capacity of 20,000

tonnes to 50,000 tonnes per annum by end

2010. This expansion in capacity will allow

us to better cater to market demand and

expected increase in customers’ orders.

“Increased Sustainability”

Dear Shareholders,

On behalf of the Board of Directors, I am delighted to

present to you our annual report for the financial year

ended 31 December 2009 (“FY2009”).

It was an eventful year for Midas. As part of the PRC

government’s high speed railway development plan, the

PRC government has allocated a substantial amount of

funding for the development of railway projects across the

country. In addition, many PRC cities have plans to build

mass rapid transit systems to ease traffic congestion.

As a result of these initiatives, the PRC high speed railway

and metro train industries are experiencing rapid growth,

which we expect will translate into increased demand for

our aluminium alloy extrusion products for the production

of high speed trains and metro trains.

Riding on this uptrend, our Group achieved an outstanding

performance during the year. Since June 2009, our core

business unit – Aluminium Alloy Division or Jillin Midas

Aluminium Industries Co., Ltd (“Jilin Midas”) (吉林麦达

斯铝业有限公司) bagged several contracts totalling

more than RMB1.5 billion to supply to prominent rail and

metro projects in the PRC and internationally.

As a Singapore-incorporated company, we are pleased

that our subsidiary Jilin Midas had successfully secured

a contract to supply aluminium alloy extrusion profiles

to the Downtown Line Project in Singapore. This is our

second metro project in Singapore following the Circle

Line Project in FY2003.

Jilin Midas also made its first foray into downstream

train car bodies fabrication services in FY2009, with the

award of three downstream train car bodies fabrication

contracts. This was in line with our long-term strategy

Message from the Executive Chairman

I Midas Holdings Limited I Annual Report 20098

to become an integrated manufacturer and one-stop

service supplier to the rail transportation industry.

During the year, our associate company, Nanjing SR

Puzhen Rail Transport Co., Ltd (南京南车浦镇城轨

车辆有限公司) (“NPRT”), also gained headway in its

operations by clinching several significant contracts each

worth more than RMB 1 billion, namely the Hangzhou

Metro Line 1 Project, as well as the Pearl River Delta

Inter-City Train (Dongguan – Shenzhen Section) and

Dongguan – Huizhou Inter-City Train Projects. NPRT’s

contribution to our Group’s profit increased 73.1% to

S$3.3 million in FY2009.

For FY2009, our net profit rose 14.9% to S$37.5 million, on

the back of an 8.6% increase in revenue from continuing

operations, namely our Aluminium Alloy Division and our

PE Pipes Division, to S$150.0 million during the year. To

focus on our core business, we ceased operations of our

Agency & Procurement Division in March 2009.

Going forward, we are optimistic of our Group’s growth

ahead as we tap on the increasing market demand in

FY2010. Our third, fourth and fifth production lines are

expected to progressively contribute to our production

capacity from the second quarter of FY2010, and will

bring total annual production capacity to 50,000 tonnes

by the end of FY2010. With the expansion, we believe

that we will be able to further strengthen our market

position as we continue to deliver quality products and

services to our customers.

In July 2009, we successfully raised gross proceeds of

S$90.6 million through a private placement of 120 million

new ordinary shares, at the price of S$0.755 per share.

Proceeds from the placement were used mainly for the

expansion of our Aluminium Alloy Division’s production

capacity (including the purchase of our fourth and fifth

production lines). We would like to thank our investors

for their strong show of support.

For our next step of growth, we have proposed a secondary

listing on the Main Board of The Stock Exchange of

Hong Kong Limited and undertake a global offering of

new ordinary shares, which was announced in March

2010. Besides raising additional capital expenditure for

the future expansion of Jilin Midas and other business

plans, the proposed listing will also enable us to widen

our investor base and increase our visibility in the PRC

and Hong Kong markets. This will be beneficial to our

long-term growth and development.

We would also like to welcome on board Dr. Xu Wei Dong,

who joined us as an Independent Non-Executive Director

on 17 March 2010. Currently a professor at the Jilin

University Law School, Dr. Xu also holds directorships in

listed companies in the PRC.

On behalf of the Board, I would like to thank everyone

who has been growing with Midas thus far. To our

shareholders, business partners, customers and

colleagues, we hope that we will be able to persist on

with your unwavering support as Midas enters into a new

and exciting development phase.

Chen Wei Ping

Executive Chairman

Business Review 9

主席致词

亲爱的股东:

我非常荣幸能代表董事会,向大家呈献我们截至

2009年12月31日的年报。

麦达斯度过了精彩的一年。在中国全力发展国家

高速铁路的计划下,中国政府斥资巨款,扩展全

国上下的铁路工程。为了减轻交通拥挤的现象,

中国许多城市也计划建设地铁系统和网络。

这一系列的措施使中国高速铁路以及地铁行业取

得高速增长。高速列车以及地铁列车制造生产的

提高,也预料会带动市场对我们的铝合金型材产

品的需求。

乘着这股升势,集团在2009年取得了令人亮眼的

成绩。自2009年6月,我们的主要业务——铝合金

业务,即吉林麦达斯铝业有限公司,取得了多项

合同,总值逾15亿人民币,供应列车车体铝合金

型材给中国以及海外的重要铁路与地铁工程。

作为一家在新加坡成立的公司,我们也非常高兴

子公司吉林麦达斯成功获得了为新加坡滨海市区

线(Downtown Line)提供铝合金车体型材的合

同。滨海市区线是麦达斯继2003年所获的环线

(Circle Line)项目合同后,第二个在新加坡的

地铁项目。

集团的长期策略是成为一家综合制造商,并为铁

路交通业提供一站式服务。吉林麦达斯在2009年

取得三项下游车体型材大部件深加工的合同,成

功开拓了下游大部件深加工的业务,让集团进一

步向目标前进。

另外,我们的合资公司南京南车浦镇城轨车辆有

限公司(“NPRT”)在过去一年也在营运上有所

突破。NPRT荣获了几项各值10亿人民币的项目合

同。这些项目分别是杭州地铁一号线项目以及珠

江三角洲穗莞深城际轨道交通项目(莞深段)与

东莞至惠州城际轨道交通项目。NPRT对集团盈利

的贡献也在2009年劲增73.1%至330万新元。

来自集团持续经营业务——铝合金以及聚乙烯管

道业务的营业额在2009年增长8.6%至1亿5000万

新元,净利则上升14.9%至3750万新元。集团为

了要把重心放在主要业务上,在2009年3月结束了

在北京公司的代理和采购业务。

展望未来,鉴于市场需求在2010年仍不断提高,

我们对集团的增长保持乐观。我们的第三、第四

和第五条生产线预计在2010年第二季度陆续开始

对我们的产能有所贡献。到了2010年底,我们的

年总产能更是能提升至5万吨。我们相信,扩充产

能之后,我们能够进一步加强市场地位,继续为

顾客提供优质的产品和服务。

2009年7月,集团成功通过私人配售1亿2000万新

普通股,以每股75.5分筹集9060万新元的款项。

所筹的资金主要用在扩充集团铝合金业务的产能

(包括购置第四和第五条生产线)。为此,我们

衷心地感谢投资者的大力支持。

针对下一步发展,我们在2010年3月宣布了在香

港交易所主板上进行第二上市的计划,并同时进

行全球性的公开发售招股活动。上市计划除了能

让集团筹集额外资金作为吉林麦达斯日后扩充和

其他业务计划的资本开支,也能够让集团扩大投

资群,并在中国和香港市场中提高知名度。这无

疑将有利于集团的长期增长与发展。

在此,我们也热烈欢迎徐卫东教授加入麦达斯的

董事会,从2010年3月17日开始,成为集团的非

执行独立董事。徐教授目前任职于吉林大学法学

院,同时也担任中国几家上市公司的董事。

我谨代表董事会,向所有陪伴麦达斯成长的各位

致谢。对于我们的股东、生意伙伴、客户以及同

事们,希望我们能够继续拥有你们不间断的支

持,迈入麦达斯振奋人心的崭新发展阶段。

陈维平

执行主席

I Midas Holdings Limited I Annual Report 200910

The railway industry in the PRC has been

boosted by the Ministry of Railways’ plans

for new inter-city high-speed trains in the

country. As a result, the PRC government

will progressively award contracts for the rail

infrastructure projects.

“Igniting Our

Growth Dynamics”

Dear Shareholders,

FY2009 was an important year for Midas as we

strengthened our capabilities to tap the burgeoning

opportunities in the PRC rail transportation industry.

Besides putting in place capacity expansion plans for

our Aluminium Alloy Division, we also expanded into

the provision of downstream train car bodies fabrication

services. This brings us another step closer to our

strategy to being an integrated manufacturer and one-

stop service supplier to the industry.

Leveraging on the PRC government’s sizeable

investments in public railways and metro networks during

the year, we secured a number of significant projects,

which further cemented Midas’ leadership position in the

industry. We also made our first foray into new markets in

the Middle East and further heightened our international

presence.

Financial ReviewThe revenue from our continuing operations, namely

our Aluminium Alloy Division and PE Pipes Division,

increased 8.6% to S$150.0 million in FY2009. We

had ceased operations of our Agency & Procurement

Division in March 2009 to place greater focus on our core

business.

During the year, Aluminium Alloy Division, our Group’s

core revenue contributor, achieved revenue of S$143.0

million, a 12.9% increase from a year ago. This

accounted for 95.4% of our Group’s revenue and 98.4%

of profit before tax. The Transport Industry continued to

play a significant role, with 64.8% of our Aluminium Alloy

Division’s revenue originating from this segment.

Overall gross profit margin was up 3.5 percentage points

from 34.2% in FY2008 to 37.7% in FY2009. The increase

was due to a higher gross profit margin of 38.4% at our

Aluminium Alloy Division, compared to 35.2% in FY2008,

resulting from a decline in raw material cost.

Message from the Chief Executive Officer

I Midas Holdings Limited I Annual Report 200912

We are also pleased with NPRT’s outstanding report

card for FY2009 as its profit contribution surged 73.1%

to S$3.3 million.

Combined with S$0.3 million in profit from our

discontinued Agency and Procurement Division, FY2009

ended with a 14.9% growth in net profit attributable to

shareholders from S$32.7 million in FY2008 to S$37.5

million.

With the injection of additional funds following our

successful share placement exercise in July 2009 and

the increase in bank borrowings, our Group registered

cash and bank balances of S$101.2 million as at 31

December 2009.

We had conducted a successful private share placement

in July 2009, raising a total of approximately S$90.6

million in gross proceeds, mainly for the expansion of the

Group’s aluminium alloy production capacity (including

the purchase of our fourth and fifth production lines).

The enthusiastic response of investors to our share

placement is a clear indicator that the investing public

appreciates Midas’ business and our prospects and is

willing to continue to invest in us.

Strengthening Our Market PositionSince FY2003, Midas has increasingly built up our industry

reputation as a supplier of quality aluminium alloy rail car

profiles. To date, our Group’s Aluminium Alloy Division,

has secured contracts for more than 30 projects in the

PRC and internationally.

Since June 2009, Jilin Midas has clinched contracts

worth more than RMB1.5 billion. They include:

The PRC- Metro train projects

• ShenzhenLine4Project

• GuangzhouLine3AirportLineProject

• ChangchunLightRailProject

- Inter-city high-speed train projects

• CRH3-380Project

• CRH3-300Project

• CRH5EMUProject

• CRH1EMUProject

International- Metro train projects

•SingaporeDowntownLineProject

•SaudiArabiaMetroProject

•IranMetroProject

To enhance our Group’s competitive advantage as a

market leader and better tap on the booming opportunities

in the PRC rail transportation industry, we implemented

our long-term strategy in FY2009 to become an

integrated manufacturer and one-stop service supplier

to the industry.

Our strategy took off as Jilin Midas successfully expanded

into the provision of downstream train car bodies

fabrication services following three contracts awarded

by CNR Tangshan Railway Vehicles Co., Ltd and CNR

Changchun Railway Vehicles Co., Ltd, two of our repeat

customers, during the year.

International AccreditationsDuring the year under review, the Group continued to

gain international recognition for our quality products and

services.

Jilin Midas’ position in the global rail transportation

industry was further entrenched in July 2009 when

it became the first company in the PRC to receive

the International Railway Industry Standard (IRIS)

certification under the category of “Manufacturing and

Services of Aluminium Alloy Carbody Profile and Parts

for Rail Cars”. Promoted by the European Rail Industry

(UNIFE) and supported by operators, system integrators

and equipment manufacturers, the IRIS complements

the internationally recognised ISO 9001 quality standard

introducing rail specific requirements. Jilin Midas’ ability

to meet the highest quality standards worldwide and

standing as an international supplier has undoubtedly

received affirmation from the industry.

As a testimony of our capabilities to meet international

quality assurance standards for welding works in the new

build, conversion and repair of railway vehicles and their

components, Jilin Midas was awarded the prestigious

EN 15085-2 certification by GSI SLV Duisburg, one of

the largest welding engineering institutes in Europe and a

manufacturer certification body accredited by the German

Railway Authority.

Business Review 13

Embarking On The Next Journey Of GrowthThere is an increasing demand for new and upgraded

railway and metro networks across the PRC as a result

of rapid urbanisation and economic development in the

country. According to the PRC’s Ministry of Railway, the

government is set to invest a substantial RMB823.5

million in the country’s railway infrastructural network in

2010, following the RMB600 million that was expended

in 2009. Plans for the development of railway projects,

such as the inter-city high-speed train projects, are set to

continue in the year ahead. In addition, many cities in the

PRC have continued with plans to enhance their metro

train infrastructure in a bid to improve traffic conditions.

Strengthening Our CapabilitiesTo capitalise on the PRC government’s considerable

focus on the rail and metro transportation industry and

the resulting increase in market demand for train cars, we

are adding three more production lines for the production

of aluminium alloy extrusion profiles. With an aggregate

capacity of 30,000 tonnes, the new production lines

are expected to come onstream progressively from the

second quarter of FY2010. By the end of FY2010, our

annual production capacity will increase from 20,000

tonnes to 50,000 tonnes. At the same time, we are in

the process of putting up three downstream train car

bodies fabrication lines which are expected to be able

to process car bodies components for 1,000 train cars

by the end of FY2010. This will allow us to gear up our

integrated suite of services to tap the opportunities in the

PRC railway market.

Growing revenue stream from NPRTWe are also positive on the outlook of our associate

company, NPRT. Since its inception in FY2007, NPRT has

won contracts to supply to a number of landmark metro

projects in the PRC, During the year, NPRT continued

to strengthen its industry profile with the addition of the

Hangzhou Metro Line 1 Project, as well as the Pearl River

Delta Inter-City Train (Dongguan – Shenzhen Section)

and Dongguan – Huizhou Inter-City Train Projects to its

project line-up. As one of the only four manufacturers

with a licence to manufacture metro trains in the PRC,

NPRT is poised to benefit from the advancement of the

country’s metro train industry.

Proposed Hong Kong ListingTo further strengthen Midas’ growth prospects, the Board

of Directors announced in March 2010, the Group’s

application for a secondary listing on The Stock Exchange

of Hong Kong Limited, and in conjunction, a global offering

of up to 300 million new ordinary shares in the capital of

the Company, with an over-allotment option of 40 million

additional shares. On top of providing additional capital

for the Group’s future business expansion and expanding

our investor base, we believe that the proposed listing

will enhance Midas’ profile in the PRC and Hong Kong,

maximising the value of the Company, and benefitting our

shareholders in the long term.

In Utmost AppreciationAs we embark on the next journey of growth, I would like

to extend my gratitude to each and every shareholder who

has been here for us each step of the way. In appreciation

of your support and confidence in Midas all this while, we

have proposed a final dividend of 0.25 Singapore cents

per ordinary share, bringing the total dividend payout to

1.0 cents per share for FY2009.

Not forgetting our valued customers and business

partners who form the pillar of Midas’ growth, thank you

for your trust and recognition given to us over the years.

Finally, I would like to thank our Board of Directors and

staff of Midas for your steadfast commitment to the good

of Midas.

We are optimistic that our Group will continue to achieve

good performance in FY2010 and we hope to progress

with your continued support.

Chew Hwa Kwang, Patrick

Chief Executive Officer

Message from the Chief Executive Officer

I Midas Holdings Limited I Annual Report 200914

1. Mr. Chen Wei Ping, aged 49, was appointed as our

Director on 21 August 2002 and has been Executive

Chairman of our Company since March 2003. Mr.

Chen is instrumental in developing and steering our

Group’s corporate directions and strategies. Mr. Chen

is responsible for the effective management of business

relations with our strategic partners. In addition, Mr. Chen

spearheaded the listing of our Company’s shares on the

SGX-ST on 23 February 2004. Mr. Chen has more than

twenty years of management experience and holds a

Bachelor Degree in Economics from Jilin Finance & Trade

College (PRC) as well as a Master Degree in Economics

from Jilin University (PRC).

2. Mr. Chew Hwa Kwang, Patrick, aged 47, is a founding

member of our Group and is our Chief Executive Officer

who is responsible for the overall operations and finance

of our Group and its financial well-being. Mr. Chew is

responsible for identifying future business opportunities

and services which our Group may provide to drive future

growth. Mr. Chew is also in charge of overseeing the day-

to-day management of our Group as well as our Group’s

strategic and business development. Mr. Chew has

served as our Executive Director since November 2000

and played a major role in the listing of our Company’s

shares on the SGX-ST on 23 February 2004. Mr. Chew

has more than twenty years of management experience.

Board of Directors

3. Mr. Chew Chin Hua, aged 55, was appointed

as an Independent Non-Executive Director of our

Company on 6 January 2004. Mr. Chew is a member

of the Association of Chartered Certified Accountants

and the Institute of Certified Public Accountants in

Singapore and has many years of experience in the

accounting and auditing profession. Mr. Chew is also

a director of another listed company in Singapore.

4. Mr. Chan Soo Sen, aged 53, was appointed as

an Independent Non-Executive Director on 29 June

2006. Mr. Chan is currently Executive Vice President

of Singbridge International Singapore Pte Ltd, and

Member of Parliament for Joo Chiat Constituency. Mr.

Chan was a Minister of State and had served in several

ministries including the Ministry of Education, Ministry

of Trade and Industry and Ministry of Community

Development, Youth and Sports. Before entering

the political scene, Mr. Chan started up the China-

Singapore Suzhou Industrial Park as the founding

CEO in 1994, laying the foundation and framework

for infrastructure and utilities development. Mr. Chan

holds a Master of Management Science from the

University of Stanford, United States of America and

is a director of a few listed companies in Singapore.

125 436

Business Review 15

Board of Directors

Executive Officers

5. Mr. Tong Wei Min, Raymond, aged 43, was

appointed as an Independent Non-Executive Director

on 15 November 2008, and was redesignated as Non-

Executive Director on 17 March 2010. Mr. Tong is a

partner and head of the Equity Capital Markets practice

group at WongPartnership LLP. Mr. Tong graduated from

the University of Nottingham and is a Barrister at Law

(Middle Temple). Mr. Tong was admitted to the Singapore

Bar in 1993.

In the course of his legal career, Mr. Tong has advised

on numerous capital markets transactions including

initial public offerings and subsequent fund-raising

transactions. Mr. Tong has also advised extensively on

corporate governance and compliance issues. Mr. Tong is

also a director of another listed company in Singapore.

6. Dr. Xu Wei Dong, aged 50, was appointed as an

Independent Non-Executive Director on 17 March 2010.

Dr. Xu is currently a professor and a PhD supervisor of the

School of Law, Jilin University (PRC). Dr. Xu graduated

from the School of Law (formerly known as the Law

Department), Jilin University (PRC) with a Bachelor

Degree in 1982. He obtained a Master Degree in law

in 1989 and a Doctoral Degree in economics in 2002,

both from Jilin University (PRC). Between June 2000 and

Mr. Tan Kai Teck, aged 40, is our Chief Financial

Officer responsible for our financial management and

the reporting functions of our Group. Mr. Tan holds a

Bachelor Degree in Accountancy (Second Upper Class

Honours) from the Nanyang Technological University and

is a Fellow Member of the Institute of Certified Public

Accountants of Singapore (FCPA Singapore).

Mr. Yang Xiao Guang, aged 50, is our General Manager

(Business Development) responsible for the execution

and implementation of the development and business

strategies of our Group. Mr. Yang is also involved in new

business development and new venture management.

Mr. Yang holds a Bachelor Degree in Economics from

Jilin Finance & Trade College (PRC) and a Master Degree

in the Science of Law from Jilin University (PRC).

December 2004, Dr. Xu served as the Deputy Dean of

the School of Law, Jilin University. He was promoted to

become the Dean of the School of Law, Jilin University

in December 2004 and held such position till December

2008. Dr. Xu concurrently holds senior positions in

various law related institutions and organisations. Dr. Xu

is the deputy chairman of Commercial Law Research

Department of the China Law Society, executive director

and secretary general of the Legal Education Research

Department of the China Law Society, deputy chairman

of the Jilin Province Law Society, executive director of

Jilin Province’s Intellectual Property Right Research

Commission, an arbitrator with China International

Economic and Trade Arbitration Commission, and a

lawyer with the Changchun Branch of Dacheng Law

Office. Dr. Xu is also a member and secretary general

of the Legal Teaching Guidance Committee of the PRC

Education Department; a member of the National Legal

Profession Examination Coordination Committee; a

member of the Advisory Committee of the Jilin Municipal

Government; and a member of the Legislation Advisory

Committee of the Heilongjiang Municipal Government. Dr.

Xu is currently an independent non-executive director of

a company listed on the Shanghai Stock Exchange and a

company listed on the Shenzhen Stock Exchange.

Mr. Wang Jiaxin, aged 54, is the General Manager of

Jilin Midas Aluminium Industries Co., Ltd. Mr. Wang is

responsible for the overall business operations of our

Aluminium Alloy Division. Mr. Wang holds a Bachelor

Degree in Mechanical Engineering from Jilin University

(PRC).

Mr. Ma Mingzhang, aged 57, is the General Manager of

Shanxi Wanshida Engineering Plastics Co., Ltd. Mr. Ma

is responsible for the overall business operations of our

PE Pipes Division. Mr. Ma holds a Bachelor Degree in

Industrial Automation Instrument from Harbin Industry

University (PRC) and a Master Degree in Science and

Engineering from Chengdu Science and Technology

University (PRC).

I Midas Holdings Limited I Annual Report 200916

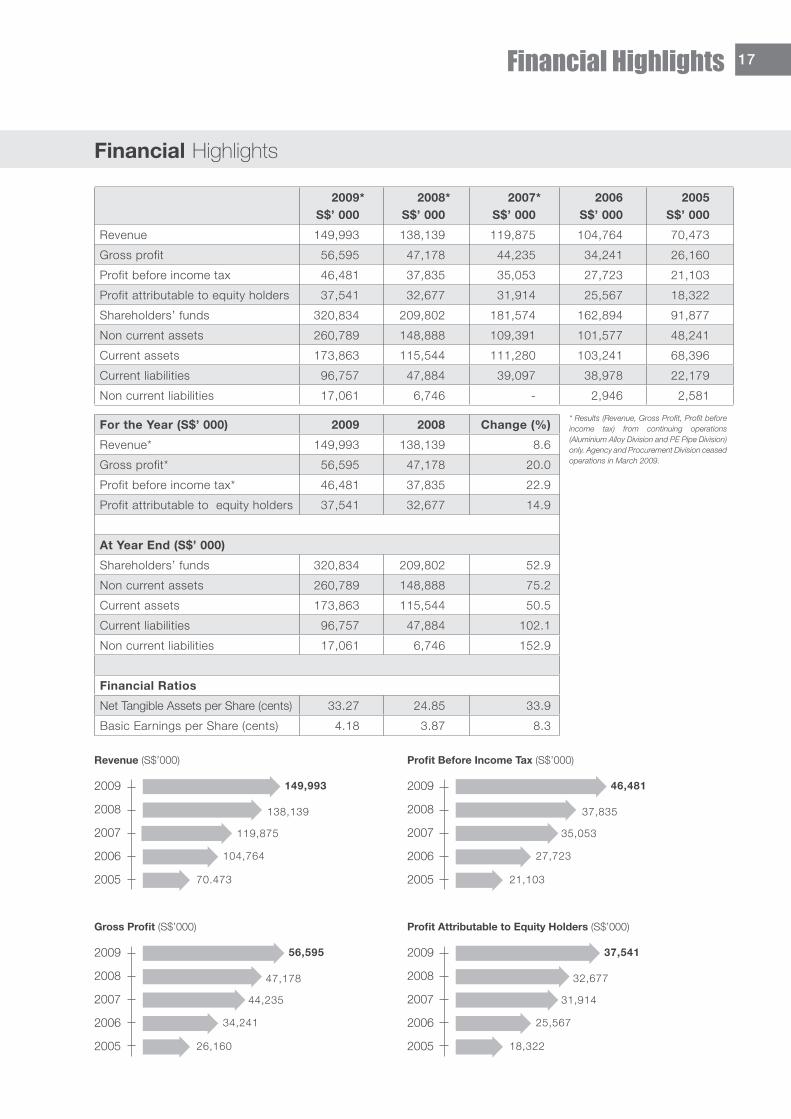

2009*S$’ 000

2008*S$’ 000

2007*S$’ 000

2006S$’ 000

2005S$’ 000

Revenue 149,993 138,139 119,875 104,764 70,473

Gross profit 56,595 47,178 44,235 34,241 26,160

Profit before income tax 46,481 37,835 35,053 27,723 21,103

Profit attributable to equity holders 37,541 32,677 31,914 25,567 18,322

Shareholders’ funds 320,834 209,802 181,574 162,894 91,877

Non current assets 260,789 148,888 109,391 101,577 48,241

Current assets 173,863 115,544 111,280 103,241 68,396

Current liabilities 96,757 47,884 39,097 38,978 22,179

Non current liabilities 17,061 6,746 - 2,946 2,581

For the Year (S$’ 000) 2009 2008 Change (%)

Revenue* 149,993 138,139 8.6

Gross profit* 56,595 47,178 20.0

Profit before income tax* 46,481 37,835 22.9

Profit attributable to equity holders 37,541 32,677 14.9

At Year End (S$’ 000)

Shareholders’ funds 320,834 209,802 52.9

Non current assets 260,789 148,888 75.2

Current assets 173,863 115,544 50.5

Current liabilities 96,757 47,884 102.1

Non current liabilities 17,061 6,746 152.9

Financial Ratios

Net Tangible Assets per Share (cents) 33.27 24.85 33.9

Basic Earnings per Share (cents) 4.18 3.87 8.3

Revenue (S$’000)

* Results (Revenue, Gross Profit, Profit before income tax) from continuing operations (Aluminium Alloy Division and PE Pipe Division) only. Agency and Procurement Division ceased operations in March 2009.

Profit Before Income Tax (S$’000)

Gross Profit (S$’000) Profit Attributable to Equity Holders (S$’000)

2009 2009

2009 2009

2008 2008

2008 2008

2007 2007

2007 2007

2006 2006

2006 2006

2005 2005

2005 2005

70.473 21,103

26,160 18,322

104,764 27,723

34,241 25,567

119,875 35,053

44,235 31,914

138,139 37,835

47,178 32,677

149,993 46,481

56,595 37,541

Financial Highlights

17Financial Highlights

19 Financial Review

22 Risk Management

24 Corporate Governance Statement

32 Report of the Directors

37 Statement by the Directors

38 Independent Auditors’ Report

40 Consolidated Statement of Comprehensive Income

41 Consolidated Statement of Financial Position

42 Statement of Financial Position of the Company

43 Consolidated Statements of Changes in Equity

44 Consolidated Statement of Cash Flow

46 Notes to the Financial Statements

92 Statistics of Shareholdings

93 Substantial Shareholders

94 Notice of Annual General Meeting

Proxy Form

Financial Contents

We believe that our established track record,

quality products and services will enable us to

seize the opportunities ahead.

“More Value Driven”

19Financial Review

Financial Review

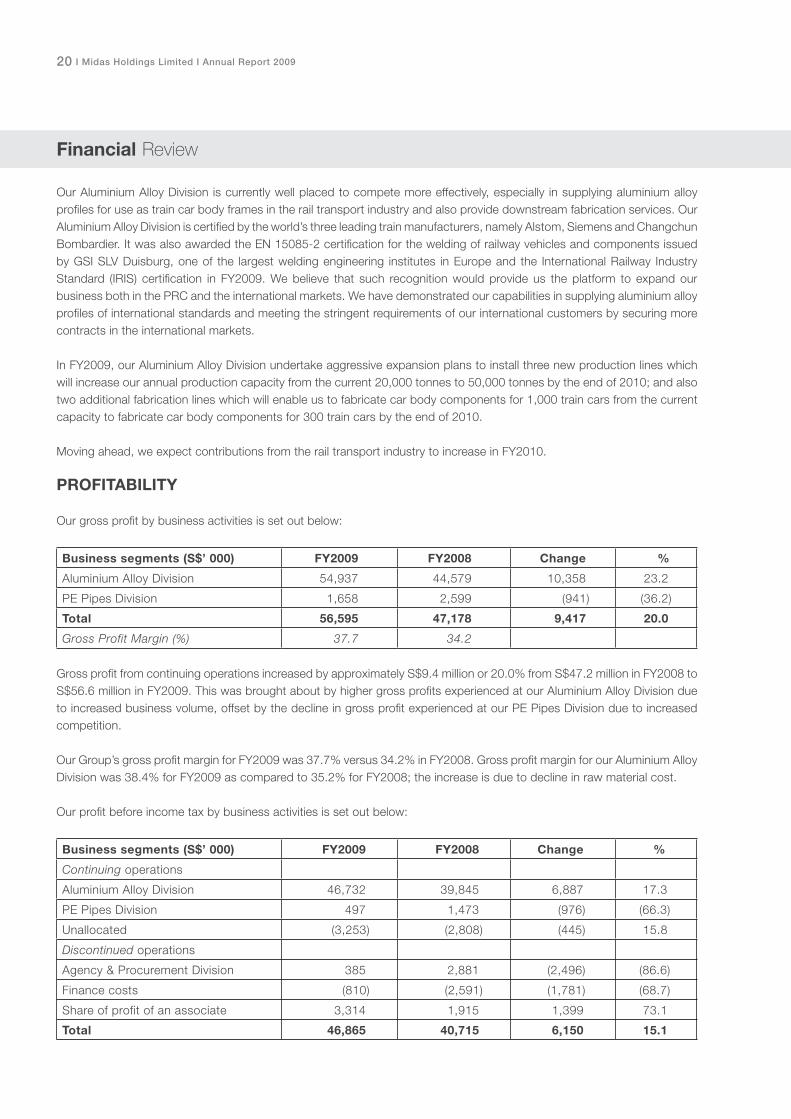

REVENUE

Our Group’s principal activities for FY2009 are as follows: a. manufacture of large section aluminium alloy extrusion products for use mainly in the following:

•RailTransportIndustry-Weproducealuminiumalloyprofileswhichareusedtomanufacturetraincarbodyframesforuse by high-speed trains, MRT and LRT trains;

•Power Industry - We produce aluminium alloy tubings which are used in power stations for power transmissionpurposes, electrical energy distribution and transmission cables; and

•Others-Weproducealuminiumalloyrodsandotherspecializedprofileswhichareusedintheproductionofmechanicalparts for industrial machinery.

b. manufacture of PE pipes for use in various types of piping networks including gas piping networks and water distribution

networks.

Our revenue from continuing operations by business activities is set out below:

Business segments (S$’ 000) FY2009 FY2008 Change %

Aluminium Alloy Division 143,030 126,702 16,328 12.9

PE Pipes Division 6,963 11,437 (4,474) (39.1)

Total 149,993 138,139 11,854 8.6

Our revenue from continuing operations increased by about S$11.9 million or 8.6% from S$138.1 million in FY2008 to S$150.0 million in FY2009. Our Aluminium Alloy Division recorded an increase in revenue by approximately 12.9% or S$16.3 million in FY2009 mainly driven by an increase in the demand for our products in the PRC rail transport industry and our effort to concentrate on our Aluminium Alloy Division. Our PE Pipes Division recorded a decrease in revenue by 39.1% or S$4.5millioninFY2009duetoincreasedcompetition.InMarch2009,weceasedoperationsofourAgency&ProcurementDivision.

The table below show the revenue segmentation in percentage terms by end usage at the Aluminium Alloy Division for the financialyearended31December2009:

Aluminium Alloy Division

FY2009 FY2008

% %

RailTransportIndustry 64.8 64.3

PowerIndustry 17.9 23.4

Others 17.3 12.3

Total 100.0 100.0

Sales by end usage indicate that revenue contribution from the rail transport industry is still the major revenue contributor, contributing approximately 64.8% of the revenue for the Aluminium Alloy Division. “Others” segment included mainly revenue fromthesupplyofaluminiumalloyrodsandotherspecializedprofilesforindustrialequipment.

20 I Midas Holdings Limited I Annual Report 2009

Financial Review

Our Aluminium Alloy Division is currently well placed to compete more effectively, especially in supplying aluminium alloy profilesforuseastraincarbodyframesintherailtransportindustryandalsoprovidedownstreamfabricationservices.OurAluminiumAlloyDivisioniscertifiedbytheworld’sthreeleadingtrainmanufacturers,namelyAlstom,SiemensandChangchunBombardier.ItwasalsoawardedtheEN15085-2certificationfortheweldingofrailwayvehiclesandcomponentsissuedbyGSISLVDuisburg,oneof the largestweldingengineering institutes inEuropeand the InternationalRailway IndustryStandard (IRIS) certification in FY2009. We believe that such recognition would provide us the platform to expand ourbusinessbothinthePRCandtheinternationalmarkets.Wehavedemonstratedourcapabilitiesinsupplyingaluminiumalloyprofilesofinternationalstandardsandmeetingthestringentrequirementsofourinternationalcustomersbysecuringmorecontracts in the international markets. InFY2009,ourAluminiumAlloyDivisionundertakeaggressiveexpansionplanstoinstallthreenewproductionlineswhichwill increase our annual production capacity from the current 20,000 tonnes to 50,000 tonnes by the end of 2010; and also two additional fabrication lines which will enable us to fabricate car body components for 1,000 train cars from the current capacity to fabricate car body components for 300 train cars by the end of 2010. Moving ahead, we expect contributions from the rail transport industry to increase in FY2010.

PROFITABILITY

Ourgrossprofitbybusinessactivitiesissetoutbelow:

Business segments (S$’ 000) FY2009 FY2008 Change %

Aluminium Alloy Division 54,937 44,579 10,358 23.2

PE Pipes Division 1,658 2,599 (941) (36.2)

Total 56,595 47,178 9,417 20.0

Gross Profit Margin (%) 37.7 34.2

GrossprofitfromcontinuingoperationsincreasedbyapproximatelyS$9.4millionor20.0%fromS$47.2millioninFY2008toS$56.6millioninFY2009.ThiswasbroughtaboutbyhighergrossprofitsexperiencedatourAluminiumAlloyDivisionduetoincreasedbusinessvolume,offsetbythedeclineingrossprofitexperiencedatourPEPipesDivisionduetoincreasedcompetition. OurGroup’sgrossprofitmarginforFY2009was37.7%versus34.2%inFY2008.GrossprofitmarginforourAluminiumAlloyDivision was 38.4% for FY2009 as compared to 35.2% for FY2008; the increase is due to decline in raw material cost.

Ourprofitbeforeincometaxbybusinessactivitiesissetoutbelow:

Business segments (S$’ 000) FY2009 FY2008 Change %

Continuing operations

Aluminium Alloy Division 46,732 39,845 6,887 17.3

PE Pipes Division 497 1,473 (976) (66.3)

Unallocated (3,253) (2,808) (445) 15.8

Discontinued operations

Agency&ProcurementDivision 385 2,881 (2,496) (86.6)

Finance costs (810) (2,591) (1,781) (68.7)

Share of profit of an associate 3,314 1,915 1,399 73.1

Total 46,865 40,715 6,150 15.1

21Financial Review

Other operating income decreased by about S$1.4 million in FY2009 mainly due to lower reinvestment tax credit received by our Aluminium Alloy Division. Selling and distribution expenses increased by approximately S$0.9 million, driven by the higher business volume recorded at our Aluminium Alloy Division, which resulted in an increase in packaging, advertising and transport costs. Administrative expenses increased by about S$1.6 million in FY2009 due mainly to higher payroll costs from an increase headcount and salary revision and also increase in travelling, depreciation and property taxes. Financecostcomprisedinterestpaidforbankborrowingsandfinancingcostsrelatingtoearlyutilisationofnotesreceivable.ApproximatelyS$2.6millionoftheinterestonbankborrowingsthataredirectlyarisingfromloansobtainedtofinancetheconstruction of property, plant and equipment for our new production lines were capitalised. Ourassociatedcompany,NanjingSRPuzhenRailTransportCo.,Ltd.contributedS$3.3millioninFY2009. Income tax expense for FY2009 increased as a result of higher profits. With effect from 1 January 2008, all the PRCsubsidiariesaresubjecttostatutorycorporate incometaxrateof25%inaccordancewiththePRC’sCorporate IncomeTaxLaw.However,ourAluminiumAlloyDivisionwasgranteda50%reliefofEnterpriseIncomeTaxinrespectofitsprofitsderived from the second production line until FY2010. FY2009endedwithnetprofitattributabletoshareholdersofaboutS$37.5millionwhichrepresenteda14.9%increaseoverFY2008.

UPDATE ON USE OF PROCEEDS

Update on the use of proceeds from the placement of 120,000,000 new ordinary shares in the capital of the company pursuanttotheplacementagreementdated16July2009: The net proceeds of S$89.4 million had been utilised as follows:

(i) An amount of approximately S$76.3 million had been used for its intended purpose for the acquisition of two aluminium alloy extrusion presses, auxiliary machineries and infrastructure for our Aluminium Alloy Division. Approximately S$4.7 million has been set aside for the remaining payments in relation to the machineries and would be disbursed accordingly when the payments due, and

(ii) The remaining balance of approximately S$8.4 million is being held for general corporate and working capital requirements.

Financial Review

22 I Midas Holdings Limited I Annual Report 2009

Risk Management

Business Risk

Our revenue is mainly derived in the PRC from the sales of aluminium alloy extrusion products and PE pipes for the transport and infrastructure industries. We intend to further our growth opportunities by marketing our productsoverseas to minimise any over reliance on the local PRC markets. Since FY2004, we have successfully exported or secured orders for our large section aluminium alloy profiles to manufacture train car body frames for the Singapore CircleLineandDowntownLineProject,theMetroOsloMRTProjectinNorway,theValeroRusProjectfortheRussianmarket, the Desiro Mainline Project for the European and ex-European markets, the Helsinki – St. Petersburg High SpeedTrainProject,theIncheonInternationalAirportRailroadProjectinSouthKorea,theRS-CitadisProjectfortheEuropeanmarketandSaudiArabiaMetroProjectandIranMetroProjectfortheMiddleEastmarket.

The raw materials used in our manufacturing processes are plastic resins (for our PE Pipes Division) and aluminium alloy billets (for our Aluminium Alloy Division). Raw materials make up a significant component of the cost of sales. Wearethereforevulnerabletofluctuationsinthepricesoftheserawmaterialsandcomponents.Wegenerallydonotpurchase or store raw materials in advance. Purchases of raw materials are generally made in response to customers’ order. Our Group makes use of this natural hedge to minimise any impact of fluctuations in raw materials prices on our Group’s profitability.

Interest Rate Risk Our interestrateriskrelatesprimarilytoourpledgedbankdeposits,bankdepositsandbankborrowings.Weplaceour cash balances with reputable banks and financial institutions. Our policy is to obtain the most favourable rates available.Wecurrentlyhavenotentered into interest rate swaps tohedgeagainstourexposure tochanges in fairvalues of our borrowings. Inaddition,totheextentthatwemayneedtoraisedebtfinancinginthefuture,upwardfluctuationsininterestrateswillincrease the cost of new debts. Fluctuations in interest rates can also lead to significant fluctuations in the fair values of our debt obligations. Wecurrentlydonotuseanyderivativeinstrumentstomanageourinterestrate.Totheextentwedecidetodosointhefuture, there can be no assurance that any future hedging activities will protect us from fluctuations in interest rates. Liquidity Risk

Liquidityriskistheriskthatwehavenetcurrentliabilitiesattheendofareportingperiod.Weareexposedtoliquidityrisk if we are unable to raise sufficient funds to meet our financial obligations when they fall due. To manage liquidity risk, we monitor and maintain a level of cash and cash equivalents considered adequate by our management to finance our operations and mitigate the effects of fluctuations in cash flow. In doing so, ourmanagement monitors the utilisation of borrowings to ensure adequate unutilised banking facilities and compliance with loan covenants.

23Risk Management

Risk Management

Foreign Currency Risk Foreign currency risk refers to the risk that movement in foreign currency exchange rates will affect our Group’s financial results and cash flow. Certain of our bank accounts, deposits, receivables and payables are denominated in Singapore dollars, U.S. dollars and Euros, which are different from the functional currency of our entities, which exposes us to foreign currency risk. However, most of our operating expenses, including our operating and administrative costs are denominated in Renminbi,andwecollectmostofourrevenueinRenminbi.Weexpecttocontinuetoincurasignificantportionofouroperating costs, and to recognise operating revenue, in Renminbi. As a result, we do not believe we are exposed to significant foreign currency risk. However, our Company’s cash flow is derived from dividend income from our subsidiaries in Singapore dollars. Hence, our Company would be exposed to foreign exchange risks when we receive dividends from our PRC subsidiaries in Renminbi. As we expand our operations, we may incur a certain portion of our cash flow in currencies other than Renminbi and, thereby, may increase our exposure to fluctuations on exchange rates. Our policy is not to take speculative positions through forward currency contracts and we have not engaged in any foreign currency hedging activities as at the date of this prospectus.

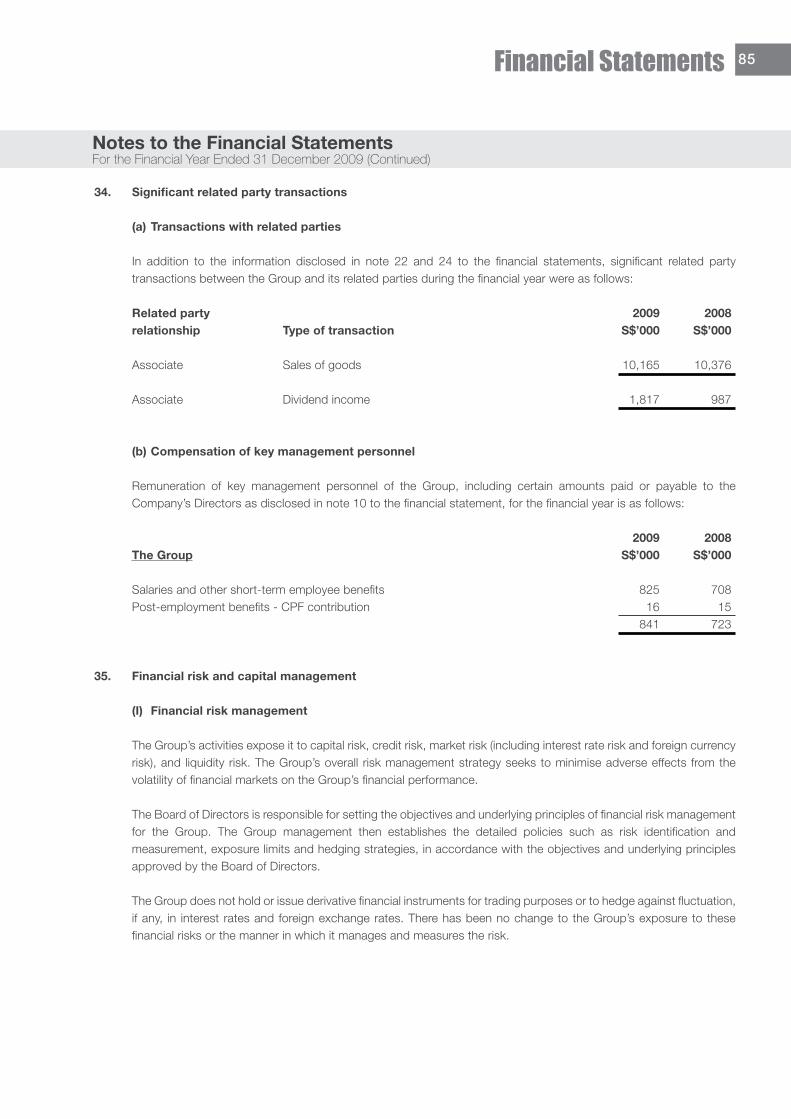

Credit Risk

Our principal financial assets are trade and other receivables and bank balances, which represent our maximum exposure to credit risk in relation to financial assets. Ourcreditriskisprimarilyattributabletotradereceivables.Inordertominimisecreditrisk,ourmanagementcontinuouslymonitorsthelevelofourexposuretoensurethatfollow-upactionistakentorecoveroverduedebts.Inaddition,wereview the recoverable amount of each individual trade debt at each balance sheet date to ensure that adequate impairment lossesaremade for irrecoverableamounts. In this regard,ourDirectorsconsider thatourcredit risk issignificantly reduced. Our trade receivables are mainly generated by customers in the PRC. Although we rely on a few key customers, our historical experience in the collection of trade and other receivables falls within the recorded allowance for doubtful debts.Weareoftheopinionthatadequateprovisionforuncollectibletradereceivableshasbeenmadeinthefinancialstatements. In addition, the credit risk on bank deposits and bank balances is limited because a majority of thecounterparties are state-owned banks with good reputations and credit ratings.

24 I Midas Holdings Limited I Annual Report 2009

Corporate Governance Statement

Midas Holdings Limited (“the Company”) is committed to maintaining a high standard of corporate governance in complying with the benchmark set by the Code of Corporate Governance 2005 (“the Code”) issued by the Ministry of Financeon14July2005.

The main corporate governance practices that were in place since are set out below.

A BOARD MATTERS Board’s conduct of its affairs

The Board of Directors (“the Board”) supervises the management of the business and affairs of the Company and its subsidiaries (“the Group”). The Board approves the Group’s corporate and strategic direction, appointment of Directors and key managerial personnel, major funding and investment proposals, and reviews the financial performance of the Group. To assist in the execution of its responsibilities, the Board has established an Audit Committee (“AC”), a Remuneration Committee (“RC”) and a Nominating Committee (“NC”). Each of these committees has its own written terms of reference and whose actions are reported to and monitored by the Board. The Company has adopted internal guidelines setting forth matters that require Board approval.

The types of material transactions that require the Board’s approval under such guidelines included the following: • Approvalofquarterlyresultsannouncement;• Approvaloftheannualreportsandaccounts;• Declarationofinterimdividendsandproposaloffinaldividends;• Conveningofshareholders’meetings;• Approvalofbroadpolicies,strategiesandfinancialobjectivesoftheGroupandmonitoringthe performance of management;• Overseetheprocessesforevaluatingtheadequacyofinternalcontrols,riskmanagement, financial reporting and compliance;• ApprovalofnominationsofDirectors;• Approvalofmaterialacquisitionsanddisposalsofassets;and• Authorisationofmajortransactions. The Board comprises business leaders and professionals with financial backgrounds. Profiles of our Directors are found on pages 15 to 16 of this Report. The Board conducts scheduled meetings on a regular basis. Ad hoc meetings will be convened to deliberate on urgent substantive matters when necessary. Telephonic attendance and conference via audio-visual communications at Board meetings are allowed under the Company’s Articles of Association. The attendance of the Directors at meetings of the Board and Board committees, as well as the frequency of such meetings, is disclosed in Part E of this Report. The Directors are provided with important and relevant information of the Company and the Group. The Directors are also provided with the phone numbers and email addresses of the Company’s senior management and Company Secretary to facilitate access to information. Newly appointed Directors are given an orientation on the Group’s business strategies and operations, including factory visits to ensure their familiarity with the Group’s operations and governance practices.

Corporate Governance Statement 25

Corporate Governance Statement

The Company Secretary and/or her representative attend(s) all Board meetings and, together with the Directors, are responsible for ensuring that the Board procedures are followed and that applicable rules and regulations are complied with. The Company Secretary and/or her representative administer(s), attend(s) and prepare(s) minutes of all Board and Board committee meetings.

Directors are welcome to request further explanations, briefings or informal discussions on any aspects of the Group’s operations or business issues from the management. The Chief Executive Officer (“CEO”) will make the necessary arrangements for the briefings, informal discussions or explanations required by the Directors.

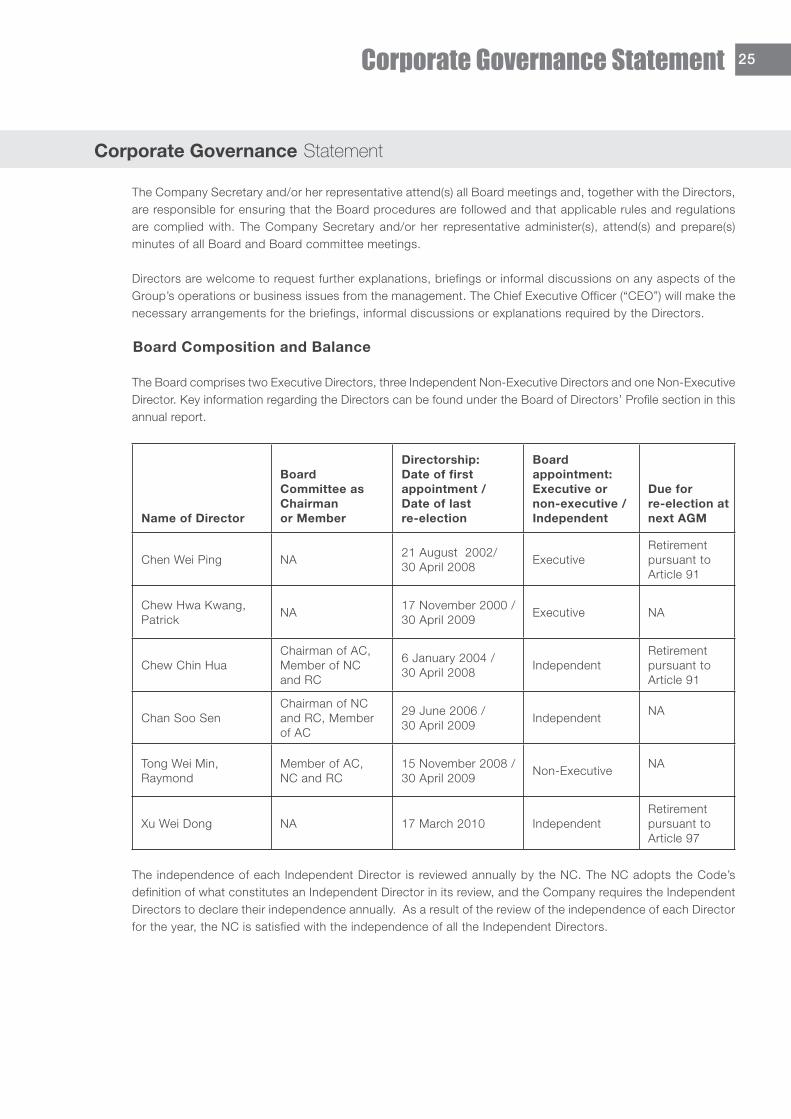

Board Composition and Balance TheBoardcomprisestwoExecutiveDirectors,threeIndependentNon-ExecutiveDirectorsandoneNon-ExecutiveDirector.KeyinformationregardingtheDirectorscanbefoundundertheBoardofDirectors’Profilesectioninthisannual report.

Name of Director

Board Committee asChairmanor Member

Directorship:Date of firstappointment /Date of lastre-election

Boardappointment:Executive ornon-executive /Independent

Due forre-election atnext AGM

ChenWeiPing NA21 August 2002/30 April 2008

ExecutiveRetirementpursuant to Article 91

ChewHwaKwang,Patrick

NA17 November 2000 /30 April 2009

Executive NA

Chew Chin HuaChairman of AC, Member of NCand RC

6January2004/30 April 2008

IndependentRetirementpursuant to Article 91

Chan Soo SenChairman of NC and RC, Member of AC

29June2006/30 April 2009

IndependentNA

TongWeiMin,Raymond

Member of AC,NC and RC

15 November 2008 /30 April 2009

Non-ExecutiveNA

XuWeiDong NA 17 March 2010 IndependentRetirementpursuant to Article 97

The independenceofeach IndependentDirector is reviewedannuallybytheNC.TheNCadoptstheCode’sdefinitionofwhatconstitutesanIndependentDirectorinitsreview,andtheCompanyrequirestheIndependentDirectors to declare their independence annually. As a result of the review of the independence of each Director fortheyear,theNCissatisfiedwiththeindependenceofalltheIndependentDirectors.

26 I Midas Holdings Limited I Annual Report 2009

Corporate Governance Statement

Role of Chairman and CEO

TherolesforbothChairmanandCEOintheCompanyareseparatelyassumedbyMr.ChenWeiPingandMr.ChewHwaKwang,Patrick.Assuch,thereisacleardivisionofresponsibilitiesatthetopoftheGroup.Mr. Chen bears responsibility for the workings of the Board and ensures that the procedures are introduced to comply with the Code while Mr. Chew bears executive responsibility for the Group’s business.

Nominating Committee (“NC”) TheNCcomprises2Independentand1Non-ExecutiveDirectors: •Mr.ChanSooSen,ChairmanoftheNCandIndependentDirector•Mr.ChewChinHua,IndependentDirector•Mr.TongWeiMin,Raymond,Non-ExecutiveDirector The principal functions of the NC are to: • IdentifysuitablecandidatesandreviewallnominationsfortheappointmenttotheBoardofDirectorsbefore making recommendations to the Board for appointment.• AssesstheindependenceoftheDirectorsannuallyandisoftheopinionthattheDirectorswhohavebeen classified as independent under the “Board of Directors” section are indeed independent.•DecidewhetherornotaDirectorisabletoandhasbeenadequatelycarryingouthisdutiesasaDirector of the Company particularly where the Director has multiple board representations.• AccesstheeffectivenessoftheBoard.• TorecommendDirectorswhoareretiringbyrotationtobeputforwardforre-election,havingregardto their contribution and performance. The NC is of the view that the current Board comprises persons who as a group, provide core competencies necessarytomeettheCompany’stargetsandthatthecurrentboardsizeisadequate,takingintoaccountthenature and scope of the Group’s operations. KeyinformationontheindividualDirectorsoftheCompanyissetoutonpages15to16ofthisAnnualReport.Their shareholdings are also disclosed on page 32 of this Annual Report. None of the Directors hold shares in the subsidiaries of the Company.

Board Performance The NC will use its best efforts to ensure that Directors appointed to the Board possess the relevant background, experience and knowledge to enable balanced and well-considered decisions to be made. The performance criteria the NC will consider in relation to an individual Director include the Director’s industry knowledge and/or functional expertise, contribution and workload requirements, sense of independence and attendance at the Board and committee meetings. One of the NC’s responsibilities is to undertake a review of the Board’s performance. The NC will consider practicable methods to assess the effectiveness of the Board.

Corporate Governance Statement 27

B REMUNERATION MATTERS Remuneration Committee (“RC”) TheRCcomprises2Independentand1Non-ExecutiveDirectors: 1.Mr.ChanSooSen,ChairmanoftheRCandIndependentDirector2.Mr.ChewChinHua,IndependentDirector3.Mr.TongWeiMin,Raymond,Non-ExecutiveDirector

The principal functions of the RC are to: •ReviewandadvisetheBoardontheremunerationpackagesofseniormanagementemployeesoftheGroup.•ReviewandapproveannuallytheremunerationfortheDirectors.•DeterminetargetsforanyperformancerelatedpayschemesoperatedbytheCompany.•AdministertheMidasEmployeesShareOptionScheme(“theScheme”). ThemembersoftheRCdonothavespecializedknowledgeinthefieldofexecutivecompensation.However,they have gained experiences in this area via managing the business and/or the human resources matters of the Group and companies outside the Group. The Company will ensure that the RC has access to expert advice on thehumanresourcematterwheneverthereisaneedtoconsultexternally.Insettingremunerationpackages,the Group takes into account pay and employment conditions within the same industry and in comparable companies, as well as the Group’s performance and individual’s performance. No Director or executive will be involved in deciding his own remuneration. The remuneration packages for our Executive Chairman and CEO include a basic salary component, a profit sharing component as well as share option elements, which are performance related. Both our Executive ChairmanandCEOhaveenteredintoserviceagreementswiththeGroupwitheffectfrom1January2009fora period of three years. IndependentandNon-ExecutiveDirectorsdonothaveservicecontractswiththeCompany.IndependentandNon-Executive Directors will receive directors’ fees, in accordance with their contributions, taking into factors such as effort and time spent, responsibilities of the Directors and the need to pay competitive fees to attract, retain and motivate the Directors. Directors’ fees have been recommended by the Board for approval at the Company’s Annual General Meeting (“AGM”).

Corporate Governance Statement

28 I Midas Holdings Limited I Annual Report 2009

Corporate Governance Statement

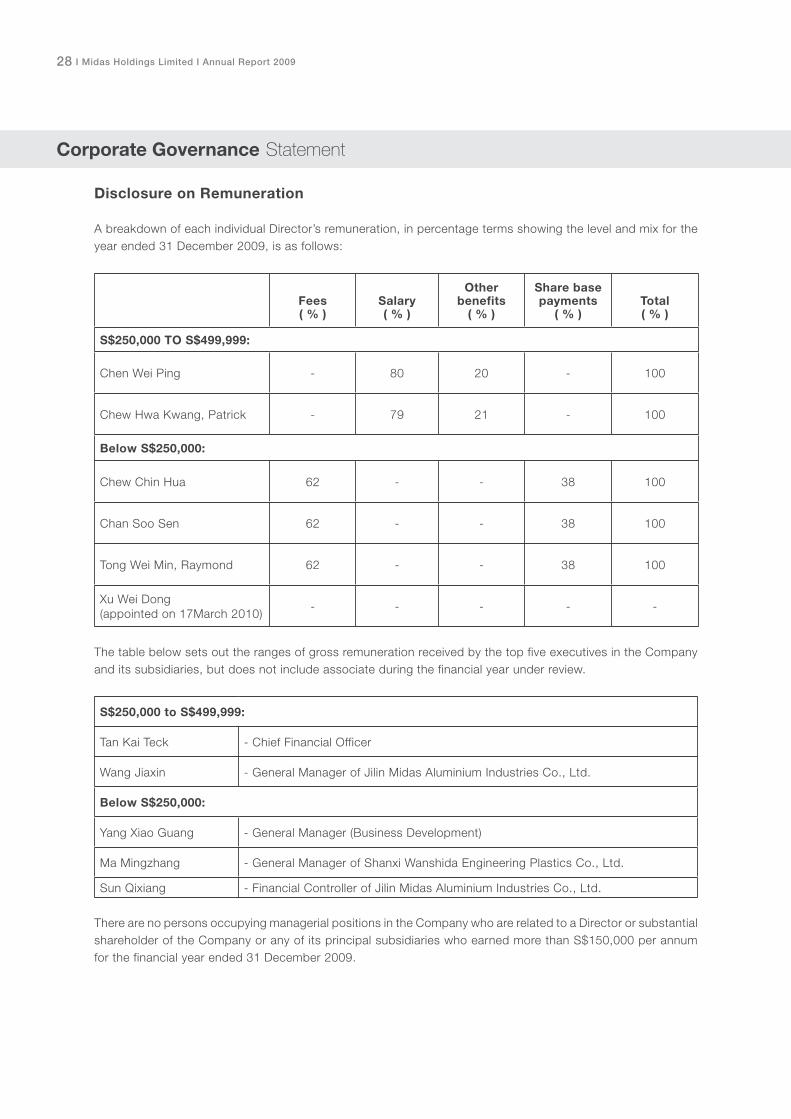

Disclosure on Remuneration A breakdown of each individual Director’s remuneration, in percentage terms showing the level and mix for the year ended 31 December 2009, is as follows:

Fees( % )

Salary( % )

Other benefits

( % )

Share basepayments

( % )Total( % )

S$250,000 TO S$499,999:

ChenWeiPing - 80 20 - 100

ChewHwaKwang,Patrick - 79 21 - 100

Below S$250,000:

Chew Chin Hua 62 - - 38 100

Chan Soo Sen 62 - - 38 100

TongWeiMin,Raymond 62 - - 38 100

XuWeiDong(appointed on 17March 2010)

- - - - -

The table below sets out the ranges of gross remuneration received by the top five executives in the Company and its subsidiaries, but does not include associate during the financial year under review.

S$250,000 to S$499,999:

TanKaiTeck - Chief Financial Officer

WangJiaxin -GeneralManagerofJilinMidasAluminiumIndustriesCo.,Ltd.

Below S$250,000:

Yang Xiao Guang - General Manager (Business Development)

MaMingzhang -GeneralManagerofShanxiWanshidaEngineeringPlasticsCo.,Ltd.

Sun Qixiang -FinancialControllerofJilinMidasAluminiumIndustriesCo.,Ltd.

There are no persons occupying managerial positions in the Company who are related to a Director or substantial shareholder of the Company or any of its principal subsidiaries who earned more than S$150,000 per annum for the financial year ended 31 December 2009.

Corporate Governance Statement 29

C ACCOUNTABILITY AND AUDIT Audit Committee (“AC”) TheACcomprises2Independentand1Non-ExecutiveDirectors: •Mr.ChewChinHua,ChairmanoftheACandIndependentDirector•Mr.ChanSooSen,IndependentDirector•Mr.TongWeiMin,Raymond,Non-ExecutiveDirector

The chairman of the AC, Mr. Chew Chin Hua has many years of experience in the auditing and accounting profession.Mr.ChanSooSenandMr.TongWeiMin,Raymondhavemanyyearsofexperience inbusinessand financial management. The AC members bring with them extensive managerial and financial expertise. All of them are also board members of various listed companies in Singapore. The AC meets at least 4 times a year, with further meetings if circumstances require. The Board is of the view that the members of the AC have sufficient financial management expertise and experience to discharge the AC’s functions. The AC assists the Board to maintain a high standard of corporate governance, particularly in the areas of effective financial reporting and the adequacy of internal control systems of the Group. During the year, the AC reviewed and approved the audit plans submitted by both the internal and external auditors. The AC reviewed the findings and recommendations from the auditors. The AC also reviewed and discussed the announcements of the quarterly, half year and full year results. The AC evaluates the assistance given by management to the external auditors and also reviews any interested person transactions. TheAChasfullaccesstomanagementandisgiventheresourcesrequiredforittodischargeitsfunctions.Ithas the full authority and discretion to invite any Director or executive officer to attend its meetings. The AC meets with the external auditors, without the presence of management, at least once a year. The AC, having reviewed all non-audit services provided by the external auditors to the Group, is satisfied that the nature and extent of such services would not affect the independence of the external auditors. The AC recommends BDO LLP to the Board of Directors for re-appointment as external auditors of the Company.

Internal Control The Board believes that, in the absence of any evidence to the contrary, the system of internal control maintained by the Group throughout the financial year and up to the date of this report, provides reasonable, but not absolute, assurance against material financial misstatements or loss, and include the safeguarding of assets, the maintenance of proper accounting records, the reliability of financial information, compliance with appropriate legislation, regulation and best practice, and the identification and containment of business risk. The Board notes that no system of internal control could provide absolute assurance against the occurrence of material errors, poor judgement in decision-making, human error, losses, fraud or other irregularities.

Corporate Governance Statement

30 I Midas Holdings Limited I Annual Report 2009

Corporate Governance Statement

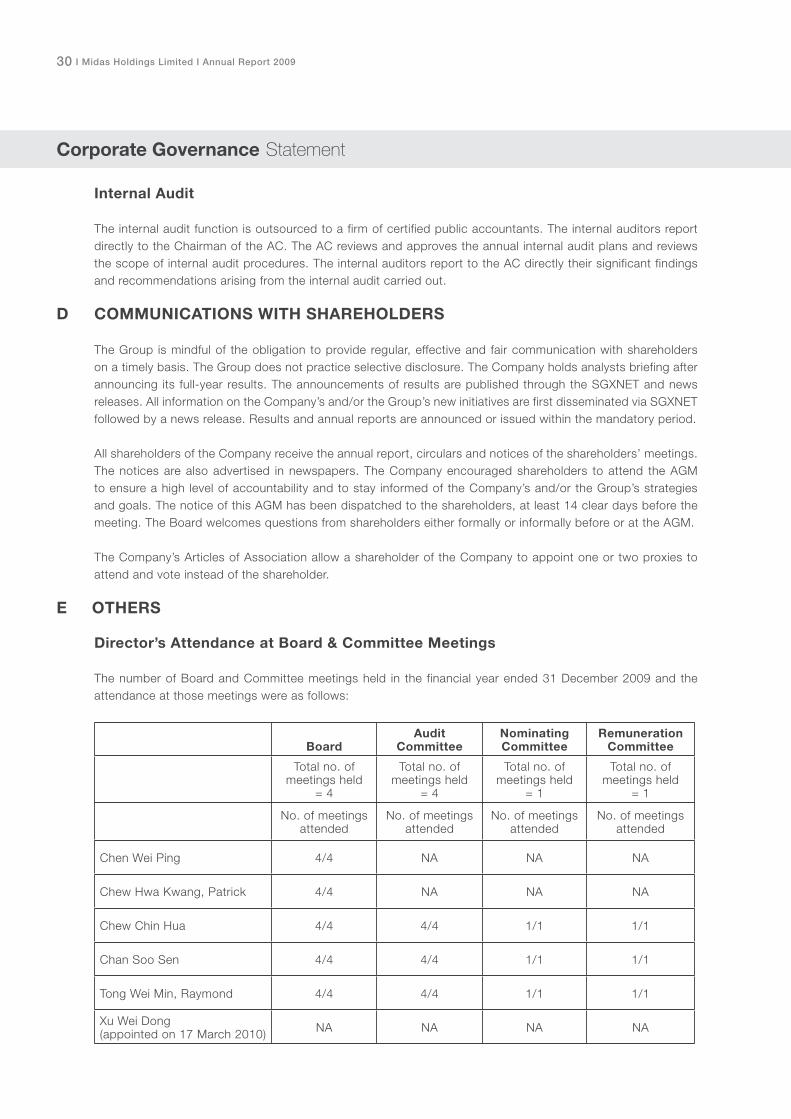

Internal Audit The internal audit function is outsourced to a firm of certified public accountants. The internal auditors report directly to the Chairman of the AC. The AC reviews and approves the annual internal audit plans and reviews the scope of internal audit procedures. The internal auditors report to the AC directly their significant findings and recommendations arising from the internal audit carried out.

D COMMUNICATIONS WITH SHAREHOLDERS The Group is mindful of the obligation to provide regular, effective and fair communication with shareholders on a timely basis. The Group does not practice selective disclosure. The Company holds analysts briefing after announcing its full-year results. The announcements of results are published through the SGXNET and news releases. All information on the Company’s and/or the Group’s new initiatives are first disseminated via SGXNET followed by a news release. Results and annual reports are announced or issued within the mandatory period. All shareholders of the Company receive the annual report, circulars and notices of the shareholders’ meetings. The notices are also advertised in newspapers. The Company encouraged shareholders to attend the AGM to ensure a high level of accountability and to stay informed of the Company’s and/or the Group’s strategies and goals. The notice of this AGM has been dispatched to the shareholders, at least 14 clear days before the meeting. The Board welcomes questions from shareholders either formally or informally before or at the AGM. The Company’s Articles of Association allow a shareholder of the Company to appoint one or two proxies to attend and vote instead of the shareholder.

E OTHERS Director’s Attendance at Board & Committee Meetings The number of Board and Committee meetings held in the financial year ended 31 December 2009 and the attendance at those meetings were as follows:

BoardAudit

CommitteeNominatingCommittee

RemunerationCommittee

Total no. ofmeetings held

= 4

Total no. ofmeetings held

= 4

Total no. ofmeetings held

= 1

Total no. ofmeetings held

= 1

No. of meetings attended

No. of meetings attended

No. of meetings attended

No. of meetings attended

ChenWeiPing 4/4 NA NA NA

ChewHwaKwang,Patrick 4/4 NA NA NA

Chew Chin Hua 4/4 4/4 1/1 1/1

Chan Soo Sen 4/4 4/4 1/1 1/1

TongWeiMin,Raymond 4/4 4/4 1/1 1/1

XuWeiDong(appointed on 17 March 2010) NA NA NA NA

Corporate Governance Statement 31

Securities Trading The Group has adopted the best practices stipulated in Listing Rule 1207(18) of the SGX-ST Listing Manual withrespecttothedealingsinsecuritiesfortheguidanceofDirectorsandofficers.Inlinewiththeguidelines,Directors and executive officers of the Group are not permitted to deal in the Company’s shares during the period commencing two weeks before the announcement of the Group’s financial statements for each of the first three quarters of its financial year, or one month before the announcement of the Group’s annual results and ending on the date of the announcement of the relevant results, or when they are in possession of any unpublished price sensitive information on the Group.

Interested Person Transactions Policy The Group has adopted an internal policy in respect of any transactions with interested persons and has set out the procedures for periodic review and approval of these transactions by the AC.

Risk Management The Group regularly reviews and improves its business and operational activities to take into account the risk management perspective. The Group seeks to identify areas of significant business risks as well as appropriate measures to control and mitigate these risks. The Group reviews all significant control policies and procedures and highlights all significant matters to the AC.

Whistle-Blowing Program As a further enhancement to internal risk control processes, the Company introduced and implemented the “Policy onReportingWrongdoing”acrosstheGroup.Underthis“Whistleblowing”policy,allformsof“wrong-doings”canbereportedtoaninvestigationunit,withthe“whistle-blower”beingprovidedconfidentialityprotection.“Wrong-doings”can include fraud, theft, abuse of authority, breach of regulations or non-compliance with corporate policy such as improperbankingorfinancialtransactions.