42

Edelweiss Professional Investor Research Insightful. Independent. Decisive. Minda Industries Ltd Date: 16th April 2019 Vishal Srivastav Research Analyst [email protected]

Edelweiss Professional Investor Research Insightful. Independent. Decisive.

Minda Industries Ltd

Date: 16th April 2019

Vishal Srivastav

Research Analyst

Edelweiss Professional Investor Research

Long Term Recommendation

Minda Industries Ltd Fast and Furious Growth Ahead…

5

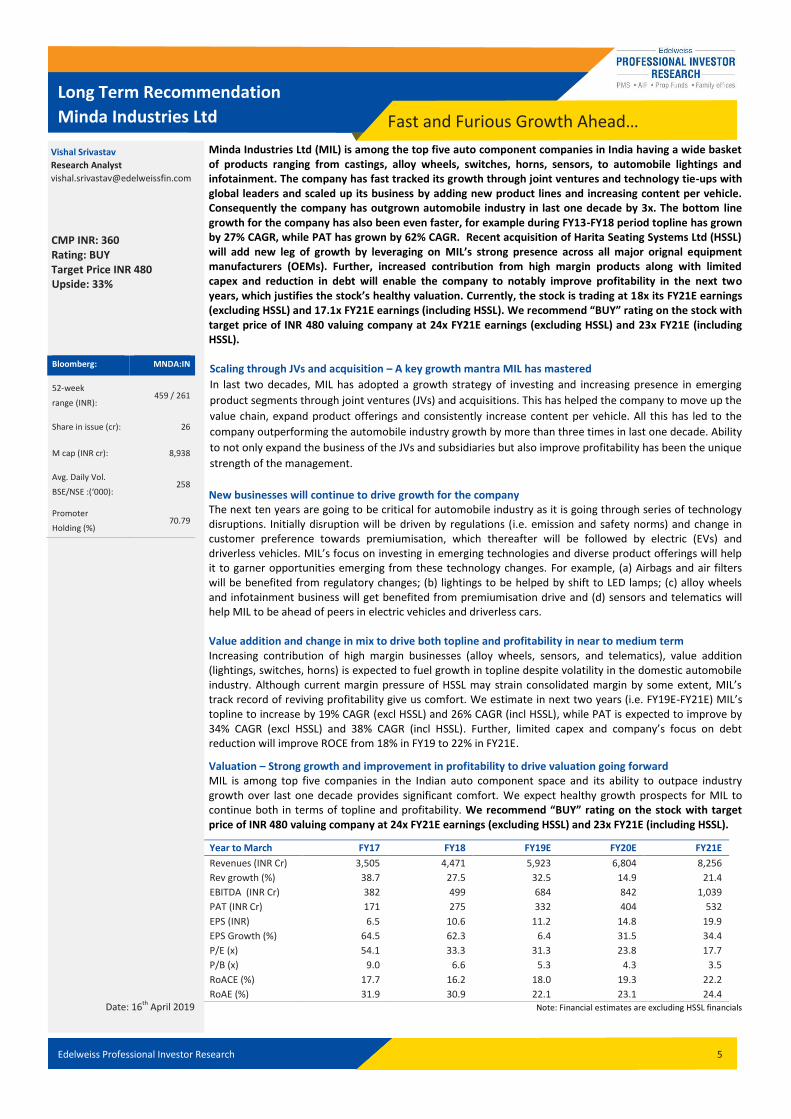

Minda Industries Ltd (MIL) is among the top five auto component companies in India having a wide basket of products ranging from castings, alloy wheels, switches, horns, sensors, to automobile lightings and infotainment. The company has fast tracked its growth through joint ventures and technology tie-ups with global leaders and scaled up its business by adding new product lines and increasing content per vehicle. Consequently the company has outgrown automobile industry in last one decade by 3x. The bottom line growth for the company has also been even faster, for example during FY13-FY18 period topline has grown by 27% CAGR, while PAT has grown by 62% CAGR. Recent acquisition of Harita Seating Systems Ltd (HSSL) will add new leg of growth by leveraging on MIL’s strong presence across all major orignal equipment manufacturers (OEMs). Further, increased contribution from high margin products along with limited capex and reduction in debt will enable the company to notably improve profitability in the next two years, which justifies the stock’s healthy valuation. Currently, the stock is trading at 18x its FY21E earnings (excluding HSSL) and 17.1x FY21E earnings (including HSSL). We recommend “BUY” rating on the stock with target price of INR 480 valuing company at 24x FY21E earnings (excluding HSSL) and 23x FY21E (including HSSL). Scaling through JVs and acquisition – A key growth mantra MIL has mastered

In last two decades, MIL has adopted a growth strategy of investing and increasing presence in emerging

product segments through joint ventures (JVs) and acquisitions. This has helped the company to move up the

value chain, expand product offerings and consistently increase content per vehicle. All this has led to the

company outperforming the automobile industry growth by more than three times in last one decade. Ability

to not only expand the business of the JVs and subsidiaries but also improve profitability has been the unique

strength of the management.

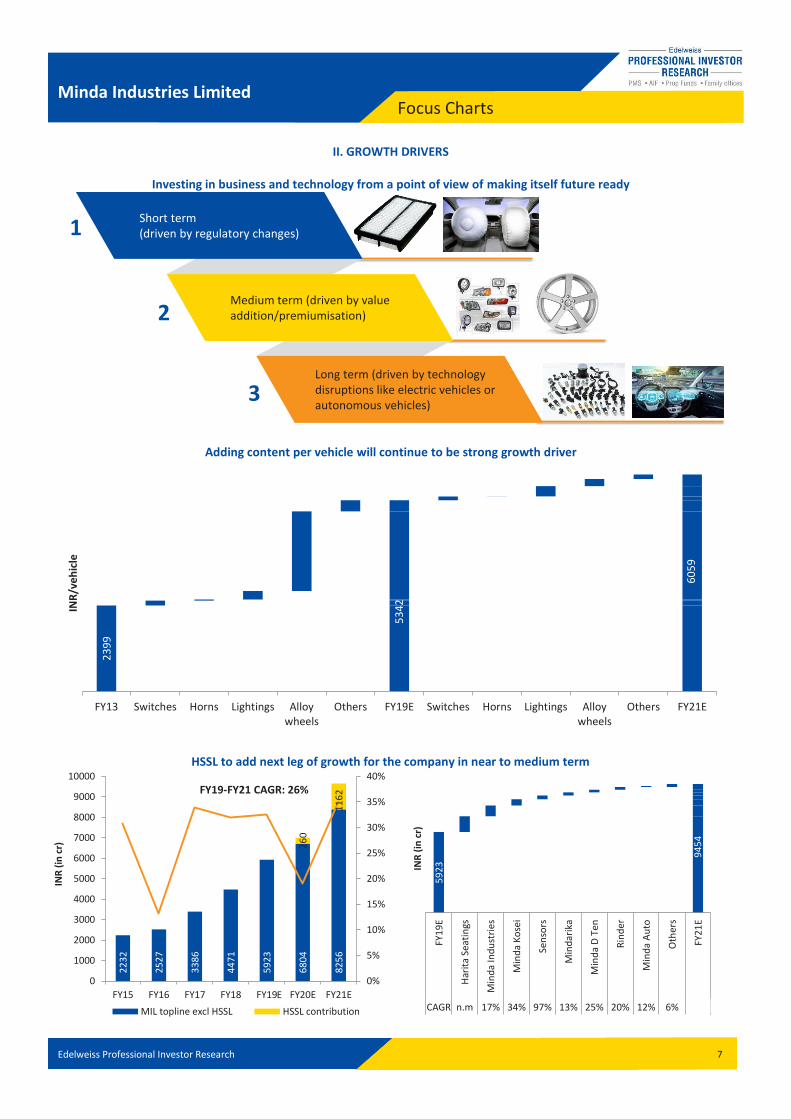

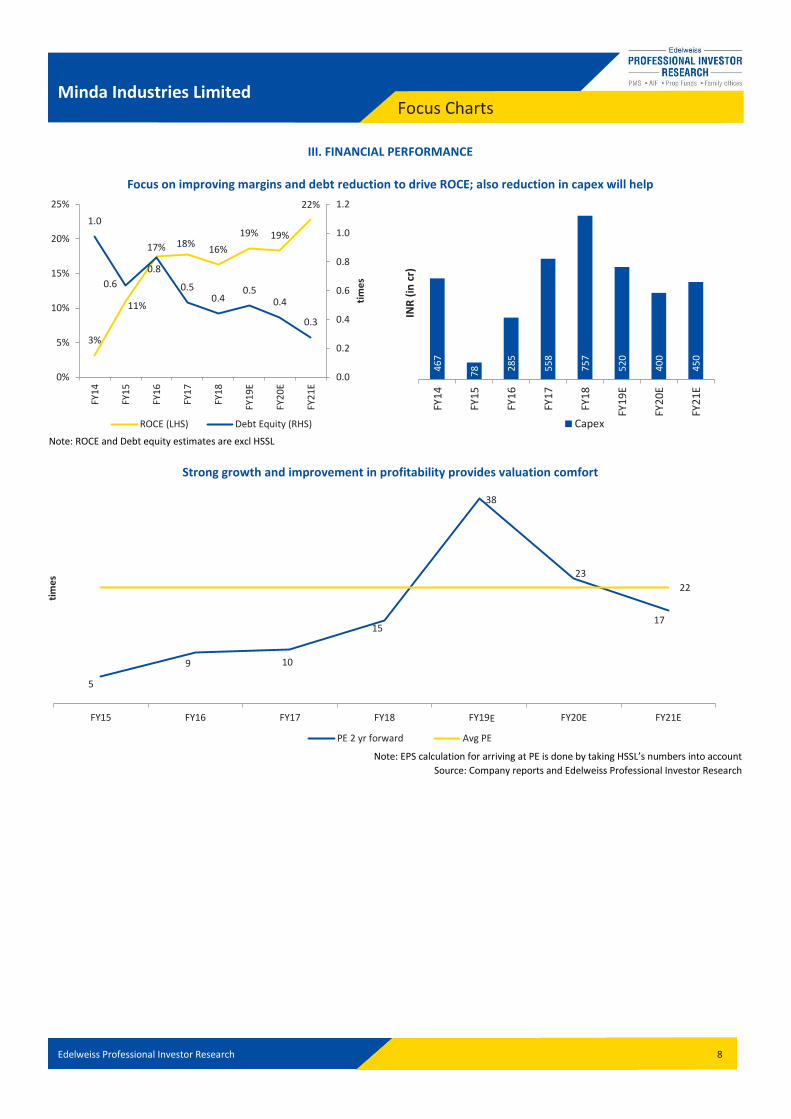

New businesses will continue to drive growth for the company The next ten years are going to be critical for automobile industry as it is going through series of technology disruptions. Initially disruption will be driven by regulations (i.e. emission and safety norms) and change in customer preference towards premiumisation, which thereafter will be followed by electric (EVs) and driverless vehicles. MIL’s focus on investing in emerging technologies and diverse product offerings will help it to garner opportunities emerging from these technology changes. For example, (a) Airbags and air filters will be benefited from regulatory changes; (b) lightings to be helped by shift to LED lamps; (c) alloy wheels and infotainment business will get benefited from premiumisation drive and (d) sensors and telematics will help MIL to be ahead of peers in electric vehicles and driverless cars. Value addition and change in mix to drive both topline and profitability in near to medium term Increasing contribution of high margin businesses (alloy wheels, sensors, and telematics), value addition (lightings, switches, horns) is expected to fuel growth in topline despite volatility in the domestic automobile industry. Although current margin pressure of HSSL may strain consolidated margin by some extent, MIL’s track record of reviving profitability give us comfort. We estimate in next two years (i.e. FY19E-FY21E) MIL’s topline to increase by 19% CAGR (excl HSSL) and 26% CAGR (incl HSSL), while PAT is expected to improve by 34% CAGR (excl HSSL) and 38% CAGR (incl HSSL). Further, limited capex and company’s focus on debt reduction will improve ROCE from 18% in FY19 to 22% in FY21E.

Valuation – Strong growth and improvement in profitability to drive valuation going forward MIL is among top five companies in the Indian auto component space and its ability to outpace industry growth over last one decade provides significant comfort. We expect healthy growth prospects for MIL to continue both in terms of topline and profitability. We recommend “BUY” rating on the stock with target price of INR 480 valuing company at 24x FY21E earnings (excluding HSSL) and 23x FY21E (including HSSL).

Year to March FY17 FY18 FY19E FY20E FY21E

Revenues (INR Cr) 3,505 4,471 5,923 6,804 8,256

Rev growth (%) 38.7 27.5 32.5 14.9 21.4

EBITDA (INR Cr) 382 499 684 842 1,039

PAT (INR Cr) 171 275 332 404 532

EPS (INR) 6.5 10.6 11.2 14.8 19.9

EPS Growth (%) 64.5 62.3 6.4 31.5 34.4

P/E (x) 54.1 33.3 31.3 23.8 17.7

P/B (x) 9.0 6.6 5.3 4.3 3.5

RoACE (%) 17.7 16.2 18.0 19.3 22.2

RoAE (%) 31.9 30.9 22.1 23.1 24.4 Note: Financial estimates are excluding HSSL financials

Vishal Srivastav

Research Analyst

CMP INR: 360 Rating: BUY Target Price INR 480 Upside: 33%

Bloomberg: MNDA:IN

52-week

range (INR): 459 / 261

Share in issue (cr): 26

M cap (INR cr): 8,938

Avg. Daily Vol.

BSE/NSE :(‘000): 258

Promoter

Holding (%) 70.79

Date: 16th April 2019

Edelweiss Professional Investor Research 5

Long Term Recommendation

Minda Industries Ltd Table of Contents

Structure ................................................................................................................................. 5

Focus Charts 1 ......................................................................................................................... 6

Focus Charts 2 ......................................................................................................................... 7

Focus Charts 3 ......................................................................................................................... 8

I. Success Mantras.................................................................................................................... 9

II. Business’ Growth Drivers ..................................................................................................... 13

III. Financial Performance ........................................................................................................ 32

IV. Valuation and Peer Analysis ............................................................................................... 35

Business Model ........................................................................................................................ 37

Financials ................................................................................................................................. 38

Edelweiss Professional Investor Research 5

Long Term Recommendation

Minda Industries Ltd Structure

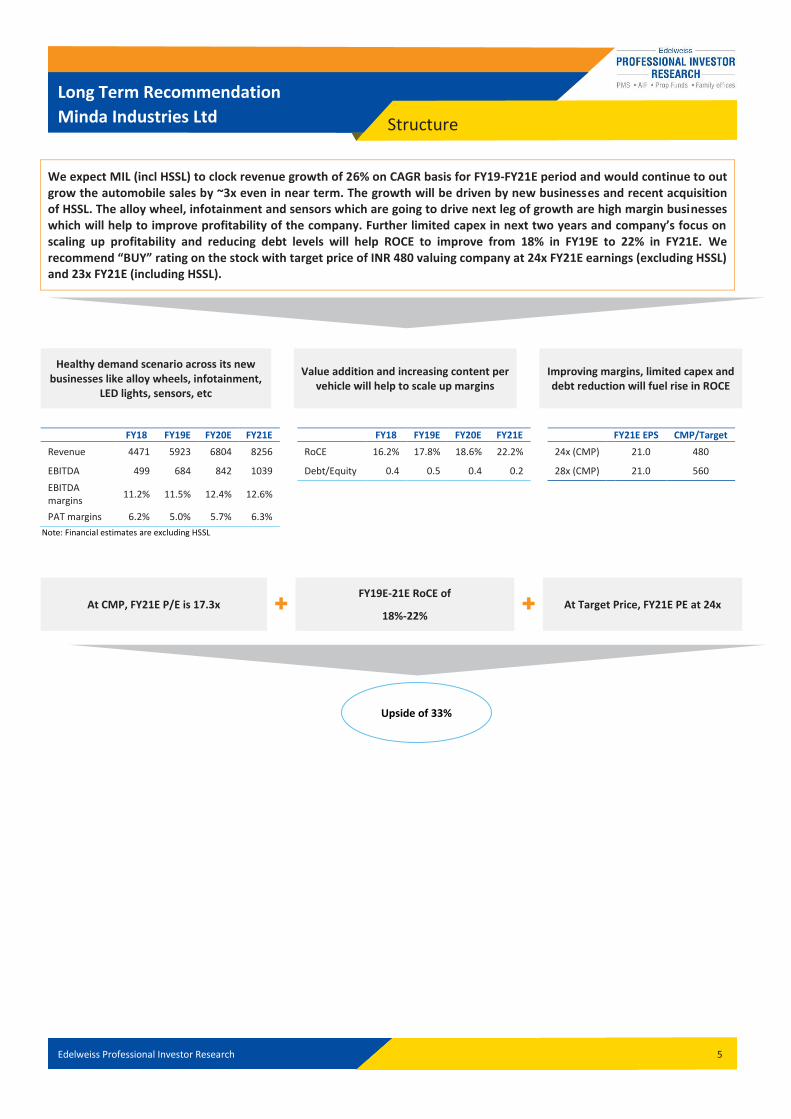

We expect MIL (incl HSSL) to clock revenue growth of 26% on CAGR basis for FY19-FY21E period and would continue to out grow the automobile sales by ~3x even in near term. The growth will be driven by new businesses and recent acquisition of HSSL. The alloy wheel, infotainment and sensors which are going to drive next leg of growth are high margin businesses which will help to improve profitability of the company. Further limited capex in next two years and company’s focus on scaling up profitability and reducing debt levels will help ROCE to improve from 18% in FY19E to 22% in FY21E. We recommend “BUY” rating on the stock with target price of INR 480 valuing company at 24x FY21E earnings (excluding HSSL) and 23x FY21E (including HSSL).

Healthy demand scenario across its new businesses like alloy wheels, infotainment,

LED lights, sensors, etc

Value addition and increasing content per vehicle will help to scale up margins

Improving margins, limited capex and debt reduction will fuel rise in ROCE

FY18 FY19E FY20E FY21E FY18 FY19E FY20E FY21E FY21E EPS CMP/Target

Revenue 4471 5923 6804 8256 RoCE 16.2% 17.8% 18.6% 22.2% 24x (CMP) 21.0 480

EBITDA 499 684 842 1039 Debt/Equity 0.4 0.5 0.4 0.2 28x (CMP) 21.0 560

EBITDA margins

11.2% 11.5% 12.4% 12.6%

PAT margins 6.2% 5.0% 5.7% 6.3%

Note: Financial estimates are excluding HSSL

At CMP, FY21E P/E is 17.3x FY19E-21E RoCE of

18%-22% At Target Price, FY21E PE at 24x

Upside of 33%

Edelweiss Professional Investor Research 6

Minda Industries Limited Focus Charts

I. BUSINESS MODEL

Building scale through JVs and acquisitions – A key growth strategy adopted by MIL

New businesses enabled company to consistently outgrow industry by around 3x

Product diversification and client diversification helps to reduce concentration risks for FY18

Source: Company reports and Edelweiss Professional Investor Research

62

0

95

4

11

79

13

40

17

06

22

32

25

27

35

05

44

71

59

23

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

Emer: CNG Kits Roki Minda: Air Filters

Kyoraku: Blowmoulding Toyoda Gosei: Safety systems and Hoses

DensoTen: Infotainment AMS: LED lamps

Kosei: Alloy wheels

Onkyo: Entertainment Rinder: LED Lightings

TTE: DAPS

Sensata: Sensors Katolec: PCB

iSYS: Sensors Harita Seatings: Auto Seatings

Clarton: Swithces

Topline growth CAGR FY10-FY19: 29%

54%

24%

14%

27% 31%

13%

39% 28%

35%

27%

14%

2% 5% 9%

3% 6%

14% 8%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E

Net Sales 2W+PVs

CAGR FY15-FY19 2w+PV industry: 8% Revenues: 28%

CAGR FY11-FY15 2w+PV industry: 7% Revenues: 24%

Industry production

Switches 35%

Horns 15%

Lighting 26%

Others 24%

Segmental mix for FY18

MSIL, 25.2%

TKML, 11.2% HMSI, 7.2%

BAL, 6.5%

TVS, 5.7%

HCIL, 2.4%

MML, 2.4%

REML, 1.6% RNPO, 1.5%

HMCL, 1.4% IYM, 1.0% Others, 3.2%

Customer mix for FY18

E

Edelweiss Professional Investor Research 7

Minda Industries Limited Focus Charts

II. GROWTH DRIVERS

Investing in business and technology from a point of view of making itself future ready

Adding content per vehicle will continue to be strong growth driver

HSSL to add next leg of growth for the company in near to medium term

Medium term (driven by value addition/premiumisation)

Short term (driven by regulatory changes)

Long term (driven by technology disruptions like electric vehicles or autonomous vehicles)

1

2

3

23

99

FY13 Switches Horns Lightings Alloywheels

Others FY19E Switches Horns Lightings Alloywheels

Others FY21E

INR

/ve

hic

le

53

42

60

59

22

32

25

27

33

86

44

71

59

23

68

04

82

56

26

0

11

62

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

FY15 FY16 FY17 FY18 FY19 FY20E FY21E

INR

(in

cr)

MIL topline excl HSSL HSSL contribution

FY19-FY21 CAGR: 26%

E

59

23

FY

19

E

Har

ita

Seat

ings

Min

da

Ind

ust

ries

Min

da

Ko

sei

Sen

sors

Min

dar

ika

Min

da

D T

en

Rin

der

Min

da

Au

to

Oth

ers

FY2

1E

CAGR n.m 17% 34% 97% 13% 25% 20% 12% 6% 0%

INR

(in

cr)

94

54

Edelweiss Professional Investor Research 8

Minda Industries Limited Focus Charts

III. FINANCIAL PERFORMANCE

Focus on improving margins and debt reduction to drive ROCE; also reduction in capex will help

Note: ROCE and Debt equity estimates are excl HSSL

Strong growth and improvement in profitability provides valuation comfort

Note: EPS calculation for arriving at PE is done by taking HSSL’s numbers into account

Source: Company reports and Edelweiss Professional Investor Research

3%

11%

17% 18% 16%

19% 19%

22%

1.0

0.6

0.8

0.5 0.4

0.5 0.4

0.3

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0%

5%

10%

15%

20%

25%

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9E

FY2

0E

FY2

1E

tim

es

ROCE (LHS) Debt Equity (RHS)4

67

78

28

5

55

8

75

7

52

0

40

0

45

0

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9E

FY2

0E

FY2

1E

INR

(in

cr)

Capex

5

9 10

15

38

23

17

22

FY15 FY16 FY17 FY18 FY19 FY20E FY21E

tim

es

PE 2 yr forward Avg PE

E

Edelweiss Professional Investor Research 9

Minda Industries Limited Investment Hypothesis

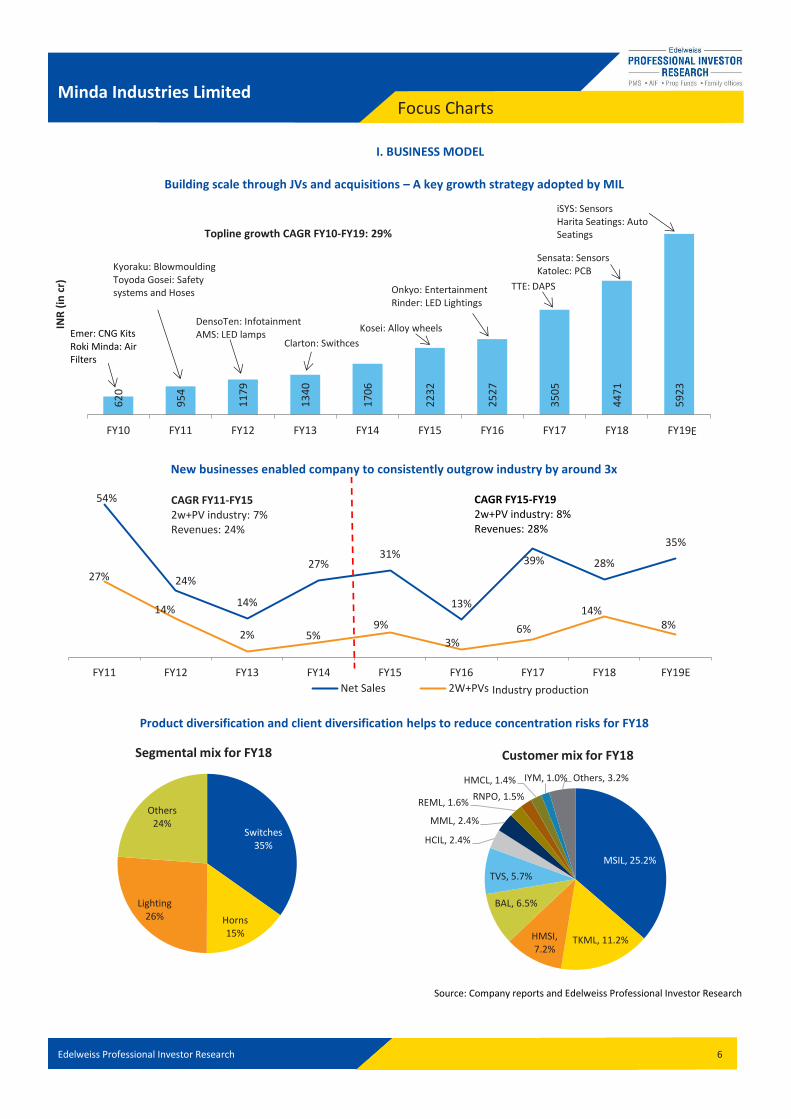

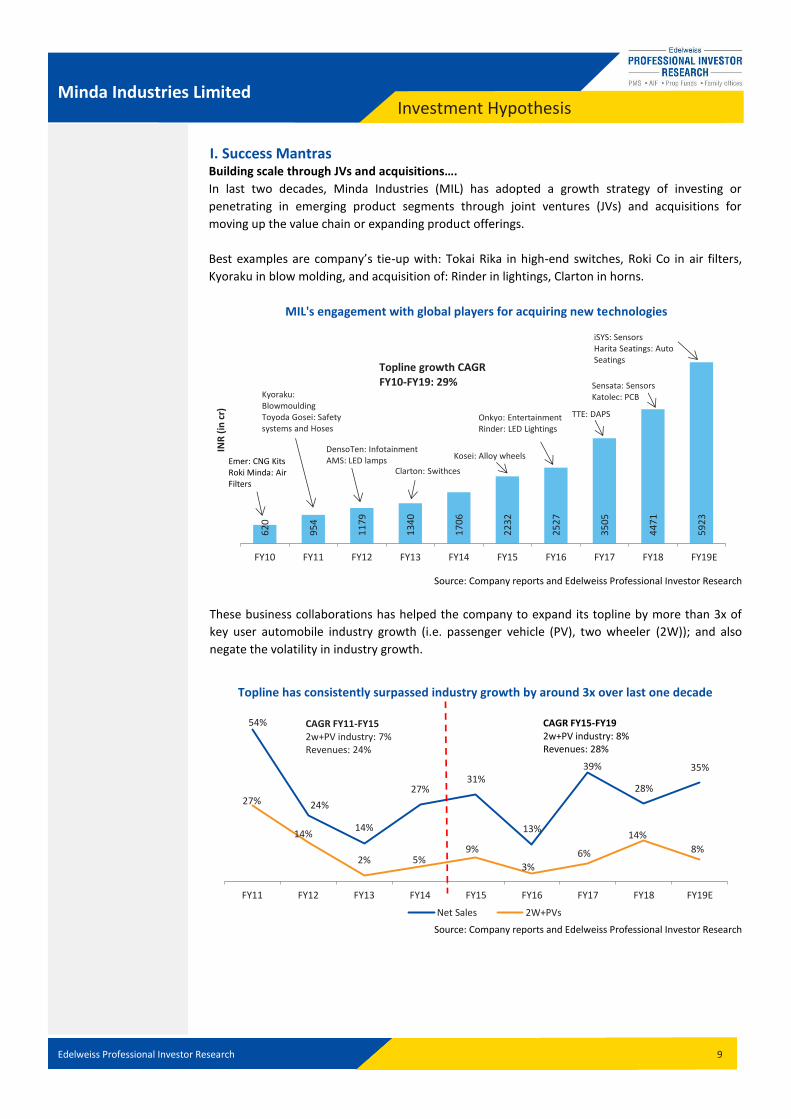

I. Success Mantras Building scale through JVs and acquisitions….

In last two decades, Minda Industries (MIL) has adopted a growth strategy of investing or

penetrating in emerging product segments through joint ventures (JVs) and acquisitions for

moving up the value chain or expanding product offerings.

Best examples are company’s tie-up with: Tokai Rika in high-end switches, Roki Co in air filters,

Kyoraku in blow molding, and acquisition of: Rinder in lightings, Clarton in horns.

MIL's engagement with global players for acquiring new technologies

Source: Company reports and Edelweiss Professional Investor Research

These business collaborations has helped the company to expand its topline by more than 3x of

key user automobile industry growth (i.e. passenger vehicle (PV), two wheeler (2W)); and also

negate the volatility in industry growth.

Topline has consistently surpassed industry growth by around 3x over last one decade

Source: Company reports and Edelweiss Professional Investor Research

62

0

95

4

11

79

13

40

17

06

22

32

25

27

35

05

44

71

59

23

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

Emer: CNG Kits Roki Minda: Air Filters

Kyoraku: Blowmoulding Toyoda Gosei: Safety systems and Hoses

DensoTen: Infotainment AMS: LED lamps Kosei: Alloy wheels

Onkyo: Entertainment Rinder: LED Lightings

TTE: DAPS

Sensata: Sensors Katolec: PCB

iSYS: Sensors Harita Seatings: Auto Seatings

Clarton: Swithces

Topline growth CAGR FY10-FY19: 29%

E

54%

24%

14%

27% 31%

13%

39%

28%

35%

27%

14%

2% 5% 9%

3%

6%

14%

8%

FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E

Net Sales 2W+PVs

CAGR FY15-FY19 2w+PV industry: 8% Revenues: 28%

CAGR FY11-FY15 2w+PV industry: 7% Revenues: 24%

Edelweiss Professional Investor Research 10

Minda Industries Limited Investment Hypothesis

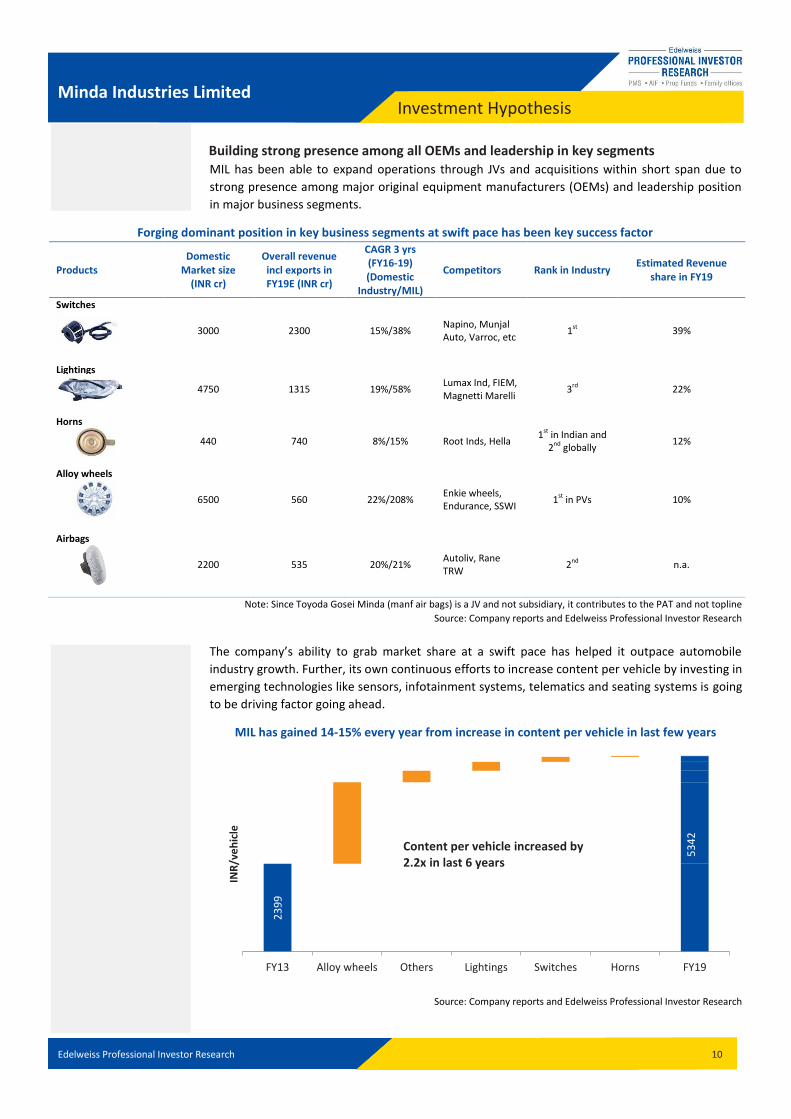

Building strong presence among all OEMs and leadership in key segments MIL has been able to expand operations through JVs and acquisitions within short span due to

strong presence among major original equipment manufacturers (OEMs) and leadership position

in major business segments.

Forging dominant position in key business segments at swift pace has been key success factor

Products Domestic

Market size (INR cr)

Overall revenue incl exports in FY19E (INR cr)

CAGR 3 yrs (FY16-19) (Domestic

Industry/MIL)

Competitors Rank in Industry Estimated Revenue

share in FY19

Switches

3000 2300 15%/38% Napino, Munjal Auto, Varroc, etc

1st 39%

Lightings

4750 1315 19%/58% Lumax Ind, FIEM, Magnetti Marelli

3rd 22%

Horns

440 740 8%/15% Root Inds, Hella 1st in Indian and

2nd globally 12%

Alloy wheels

6500 560 22%/208% Enkie wheels, Endurance, SSWI

1st in PVs 10%

Airbags

2200 535 20%/21% Autoliv, Rane TRW

2nd n.a.

Note: Since Toyoda Gosei Minda (manf air bags) is a JV and not subsidiary, it contributes to the PAT and not topline

Source: Company reports and Edelweiss Professional Investor Research

The company’s ability to grab market share at a swift pace has helped it outpace automobile

industry growth. Further, its own continuous efforts to increase content per vehicle by investing in

emerging technologies like sensors, infotainment systems, telematics and seating systems is going

to be driving factor going ahead.

MIL has gained 14-15% every year from increase in content per vehicle in last few years

Source: Company reports and Edelweiss Professional Investor Research

23

99

FY13 Alloy wheels Others Lightings Switches Horns FY19

INR

/ve

hic

le

Content per vehicle increased by 2.2x in last 6 years

53

42

Edelweiss Professional Investor Research 11

Minda Industries Limited Investment Hypothesis

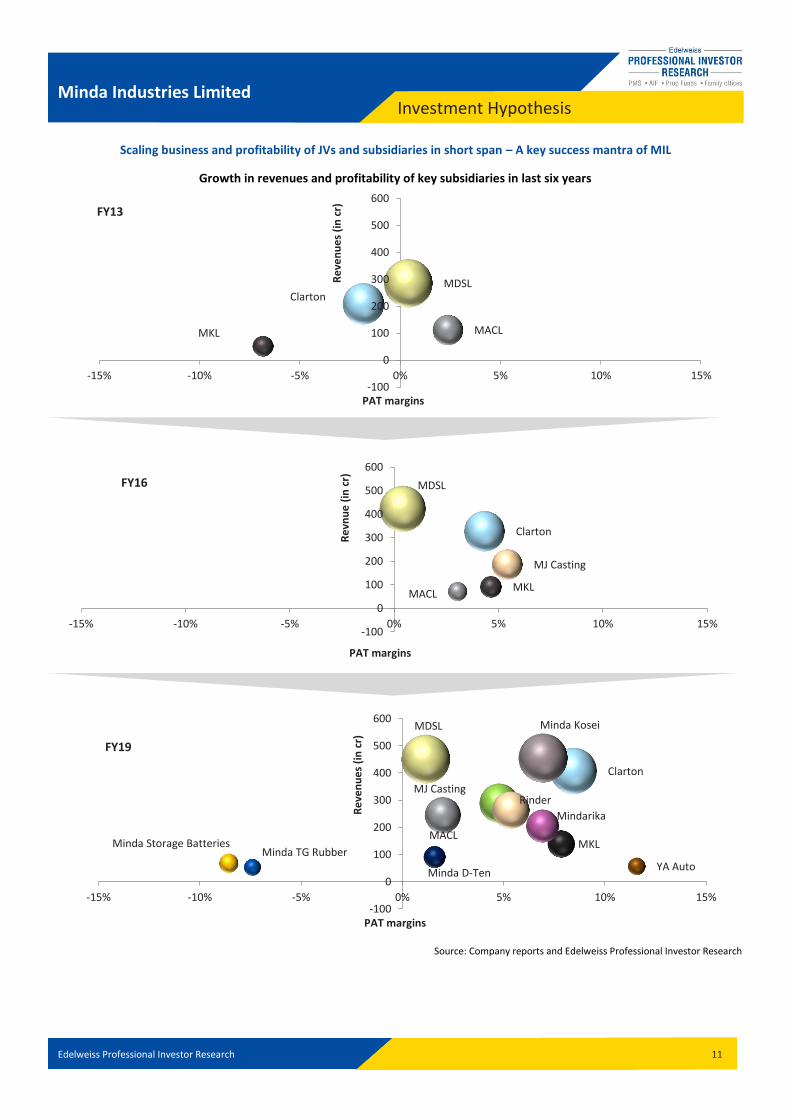

Scaling business and profitability of JVs and subsidiaries in short span – A key success mantra of MIL

Growth in revenues and profitability of key subsidiaries in last six years

Source: Company reports and Edelweiss Professional Investor Research

MACL MKL

MDSL Clarton

-100

0

100

200

300

400

500

600

-15% -10% -5% 0% 5% 10% 15%

Re

ven

ue

s (i

n c

r)

PAT margins

FY13

MACL MKL

MDSL

Clarton

MJ Casting

-100

0

100

200

300

400

500

600

-15% -10% -5% 0% 5% 10% 15%

Re

vnu

e (

in c

r)

PAT margins

FY16

MACL MKL

MDSL

Clarton

Minda TG Rubber

Minda Kosei

MJ Casting

YA Auto

Rinder

Minda Storage Batteries

Minda D-Ten

Mindarika

-100

0

100

200

300

400

500

600

-15% -10% -5% 0% 5% 10% 15%

Re

ven

ue

s (i

n c

r)

PAT margins

FY19

Edelweiss Professional Investor Research 12

Minda Industries Limited Investment Hypothesis

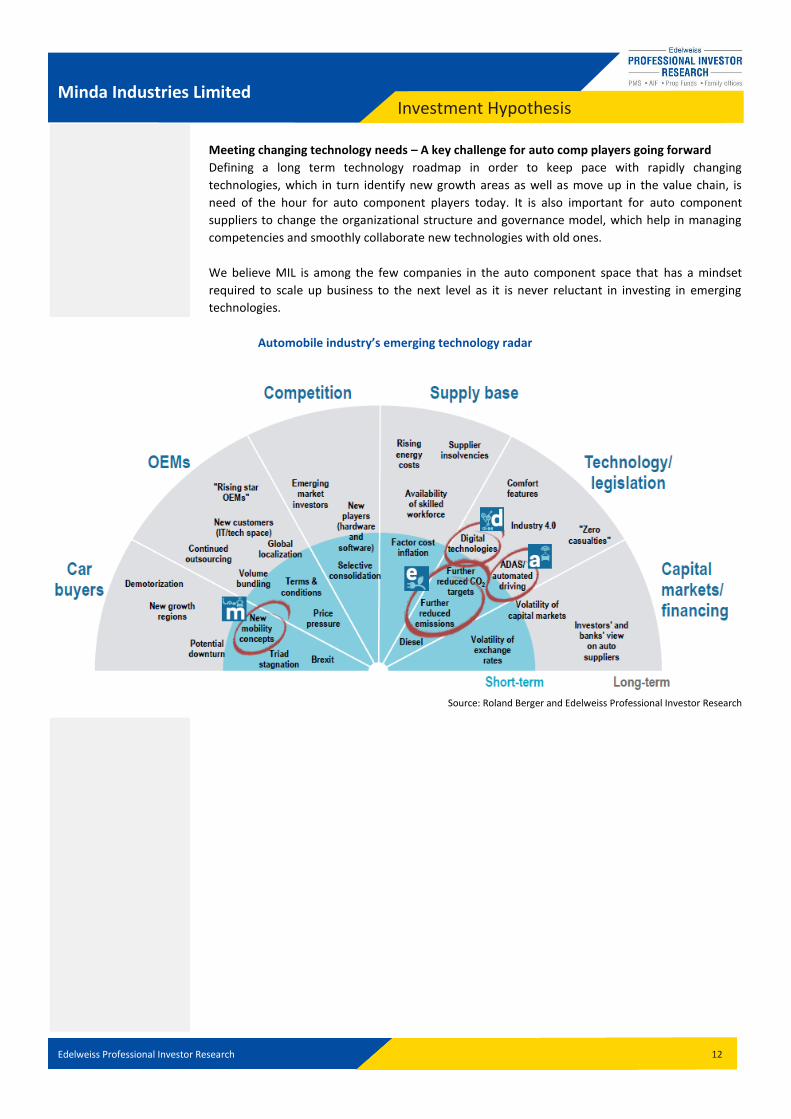

Meeting changing technology needs – A key challenge for auto comp players going forward

Defining a long term technology roadmap in order to keep pace with rapidly changing

technologies, which in turn identify new growth areas as well as move up in the value chain, is

need of the hour for auto component players today. It is also important for auto component

suppliers to change the organizational structure and governance model, which help in managing

competencies and smoothly collaborate new technologies with old ones.

We believe MIL is among the few companies in the auto component space that has a mindset

required to scale up business to the next level as it is never reluctant in investing in emerging

technologies.

Automobile industry’s emerging technology radar

Source: Roland Berger and Edelweiss Professional Investor Research

Edelweiss Professional Investor Research 13

Minda Industries Limited Investment Hypothesis

II. Business’ Growth Drivers

MIL’s diverse product basket in emerging/ new technologies will help to garner the benefits of

potential growth drivers across different time spans. Also, its focus on emerging technologies at

an early stage will help to reduce “go to market” time and consequently gain market share at an

early stage.

MIL getting ready to reap the benefits from different technology changes going forward

Source: Roland Berger and Edelweiss Professional Investor Research

A. Upcoming regulatory changes to drive growth for MIL’s air bags and air filters

business

Domestic automobile industry will be going through slew of regulatory in next one year. Alarming

number of road accidents i.e. 55 accidents out of which 17 deaths every hour forced government

of implement series of regulations related to installation of safety equipment in cars (for example

air bags, reverse parking, sensors, seat belts, etc).

Implementation of emission and safety regulations and timelines

Source: Society of Indian Automobile Manufacturers (SIAM)

Medium term (driven by value addition/premiumisation)

Short term (driven by regulatory changes)

Long term (driven by technology disruptions like electric vehicles or autonomous vehicles)

1

2

3

Edelweiss Professional Investor Research 14

Minda Industries Limited Investment Hypothesis

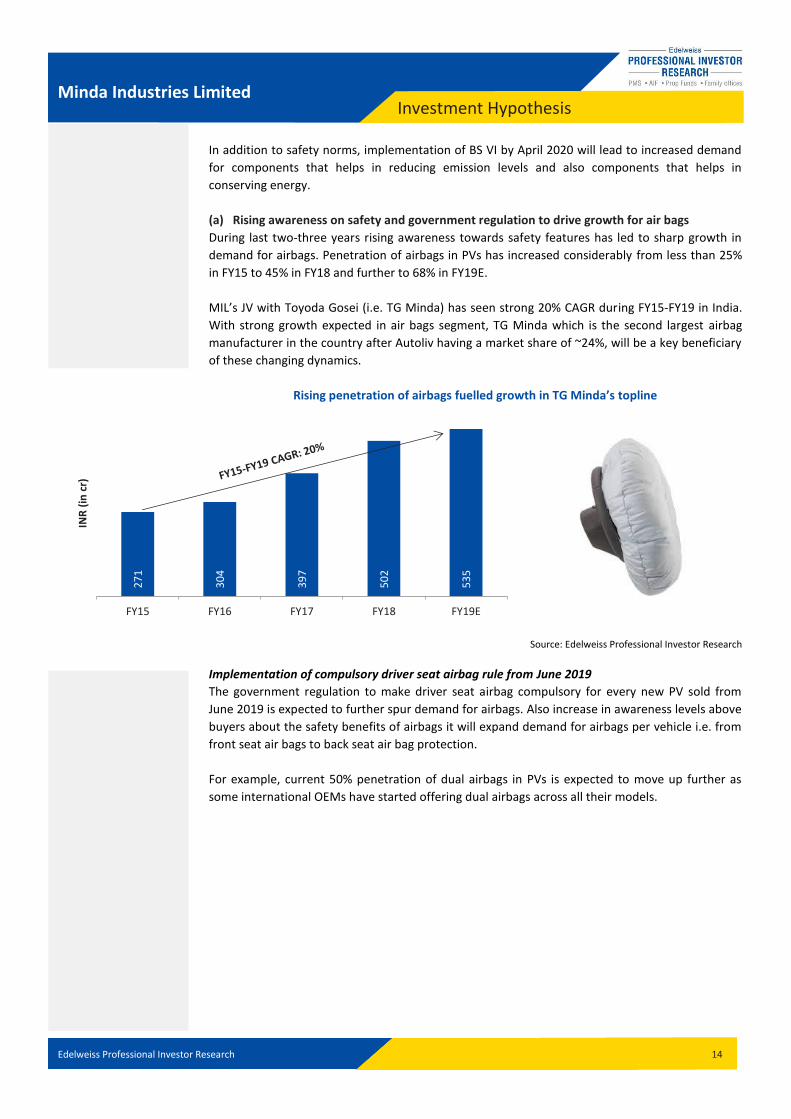

In addition to safety norms, implementation of BS VI by April 2020 will lead to increased demand

for components that helps in reducing emission levels and also components that helps in

conserving energy.

(a) Rising awareness on safety and government regulation to drive growth for air bags

During last two-three years rising awareness towards safety features has led to sharp growth in

demand for airbags. Penetration of airbags in PVs has increased considerably from less than 25%

in FY15 to 45% in FY18 and further to 68% in FY19E.

MIL’s JV with Toyoda Gosei (i.e. TG Minda) has seen strong 20% CAGR during FY15-FY19 in India.

With strong growth expected in air bags segment, TG Minda which is the second largest airbag

manufacturer in the country after Autoliv having a market share of ~24%, will be a key beneficiary

of these changing dynamics.

Rising penetration of airbags fuelled growth in TG Minda’s topline

Source: Edelweiss Professional Investor Research

Implementation of compulsory driver seat airbag rule from June 2019

The government regulation to make driver seat airbag compulsory for every new PV sold from

June 2019 is expected to further spur demand for airbags. Also increase in awareness levels above

buyers about the safety benefits of airbags it will expand demand for airbags per vehicle i.e. from

front seat air bags to back seat air bag protection.

For example, current 50% penetration of dual airbags in PVs is expected to move up further as

some international OEMs have started offering dual airbags across all their models.

27

1

30

4

39

7

50

2

53

5

FY15 FY16 FY17 FY18 FY19E

INR

(in

cr)

Edelweiss Professional Investor Research 15

Minda Industries Limited Investment Hypothesis

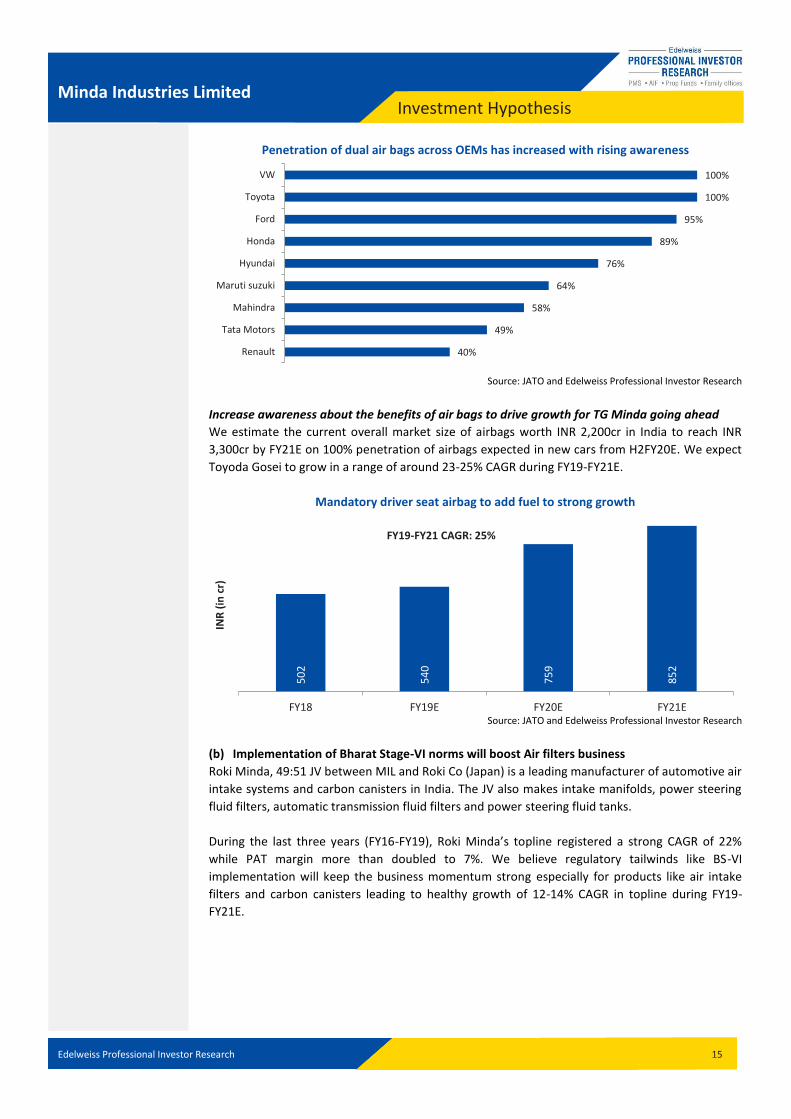

Penetration of dual air bags across OEMs has increased with rising awareness

Source: JATO and Edelweiss Professional Investor Research

Increase awareness about the benefits of air bags to drive growth for TG Minda going ahead

We estimate the current overall market size of airbags worth INR 2,200cr in India to reach INR

3,300cr by FY21E on 100% penetration of airbags expected in new cars from H2FY20E. We expect

Toyoda Gosei to grow in a range of around 23-25% CAGR during FY19-FY21E.

Mandatory driver seat airbag to add fuel to strong growth

Source: JATO and Edelweiss Professional Investor Research

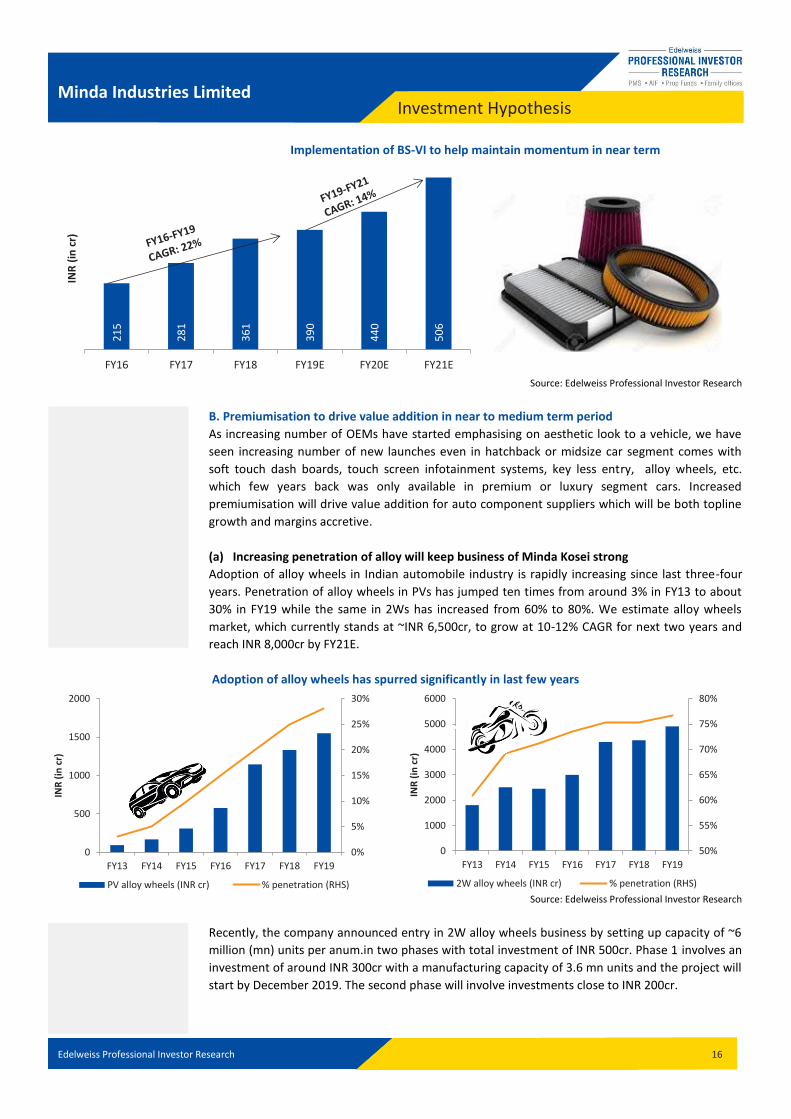

(b) Implementation of Bharat Stage-VI norms will boost Air filters business

Roki Minda, 49:51 JV between MIL and Roki Co (Japan) is a leading manufacturer of automotive air

intake systems and carbon canisters in India. The JV also makes intake manifolds, power steering

fluid filters, automatic transmission fluid filters and power steering fluid tanks.

During the last three years (FY16-FY19), Roki Minda’s topline registered a strong CAGR of 22%

while PAT margin more than doubled to 7%. We believe regulatory tailwinds like BS-VI

implementation will keep the business momentum strong especially for products like air intake

filters and carbon canisters leading to healthy growth of 12-14% CAGR in topline during FY19-

FY21E.

40%

49%

58%

64%

76%

89%

95%

100%

100%

Renault

Tata Motors

Mahindra

Maruti suzuki

Hyundai

Honda

Ford

Toyota

VW

50

2

54

0

75

9

85

2

FY18 FY19E FY20E FY21E

INR

(in

cr)

FY19-FY21 CAGR: 25%

Edelweiss Professional Investor Research 16

Minda Industries Limited Investment Hypothesis

Implementation of BS-VI to help maintain momentum in near term

Source: Edelweiss Professional Investor Research

B. Premiumisation to drive value addition in near to medium term period

As increasing number of OEMs have started emphasising on aesthetic look to a vehicle, we have

seen increasing number of new launches even in hatchback or midsize car segment comes with

soft touch dash boards, touch screen infotainment systems, key less entry, alloy wheels, etc.

which few years back was only available in premium or luxury segment cars. Increased

premiumisation will drive value addition for auto component suppliers which will be both topline

growth and margins accretive.

(a) Increasing penetration of alloy will keep business of Minda Kosei strong

Adoption of alloy wheels in Indian automobile industry is rapidly increasing since last three-four

years. Penetration of alloy wheels in PVs has jumped ten times from around 3% in FY13 to about

30% in FY19 while the same in 2Ws has increased from 60% to 80%. We estimate alloy wheels

market, which currently stands at ~INR 6,500cr, to grow at 10-12% CAGR for next two years and

reach INR 8,000cr by FY21E.

Adoption of alloy wheels has spurred significantly in last few years

Source: Edelweiss Professional Investor Research

Recently, the company announced entry in 2W alloy wheels business by setting up capacity of ~6

million (mn) units per anum.in two phases with total investment of INR 500cr. Phase 1 involves an

investment of around INR 300cr with a manufacturing capacity of 3.6 mn units and the project will

start by December 2019. The second phase will involve investments close to INR 200cr.

21

5

28

1

36

1

39

0

44

0

50

6

FY16 FY17 FY18 FY19E FY20E FY21E

INR

(in

cr)

0%

5%

10%

15%

20%

25%

30%

0

500

1000

1500

2000

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

PV alloy wheels (INR cr) % penetration (RHS)

50%

55%

60%

65%

70%

75%

80%

0

1000

2000

3000

4000

5000

6000

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

2W alloy wheels (INR cr) % penetration (RHS)

Edelweiss Professional Investor Research 17

Minda Industries Limited Investment Hypothesis

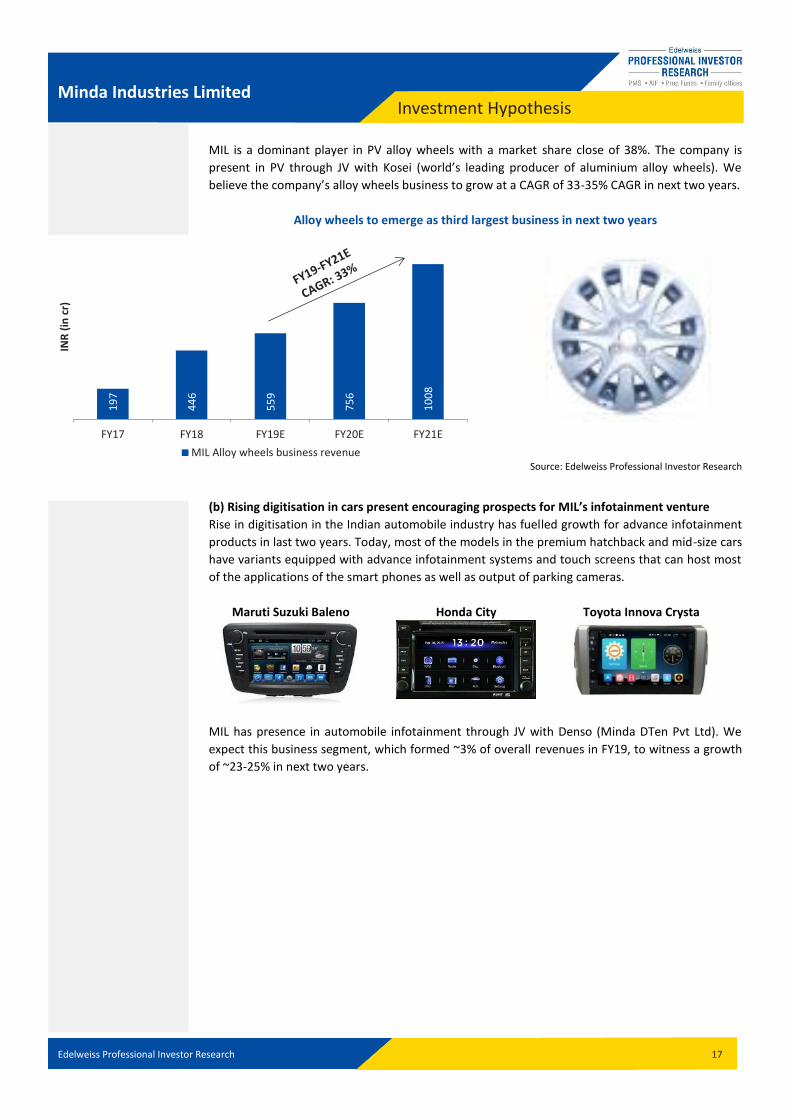

MIL is a dominant player in PV alloy wheels with a market share close of 38%. The company is

present in PV through JV with Kosei (world’s leading producer of aluminium alloy wheels). We

believe the company’s alloy wheels business to grow at a CAGR of 33-35% CAGR in next two years.

Alloy wheels to emerge as third largest business in next two years

Source: Edelweiss Professional Investor Research

(b) Rising digitisation in cars present encouraging prospects for MIL’s infotainment venture

Rise in digitisation in the Indian automobile industry has fuelled growth for advance infotainment

products in last two years. Today, most of the models in the premium hatchback and mid-size cars

have variants equipped with advance infotainment systems and touch screens that can host most

of the applications of the smart phones as well as output of parking cameras.

Maruti Suzuki Baleno

Honda City

Toyota Innova Crysta

MIL has presence in automobile infotainment through JV with Denso (Minda DTen Pvt Ltd). We

expect this business segment, which formed ~3% of overall revenues in FY19, to witness a growth

of ~23-25% in next two years.

19

7

44

6

55

9

75

6

10

08

FY17 FY18 FY19E FY20E FY21E

INR

(in

cr)

MIL Alloy wheels business revenue

Edelweiss Professional Investor Research 18

Minda Industries Limited Investment Hypothesis

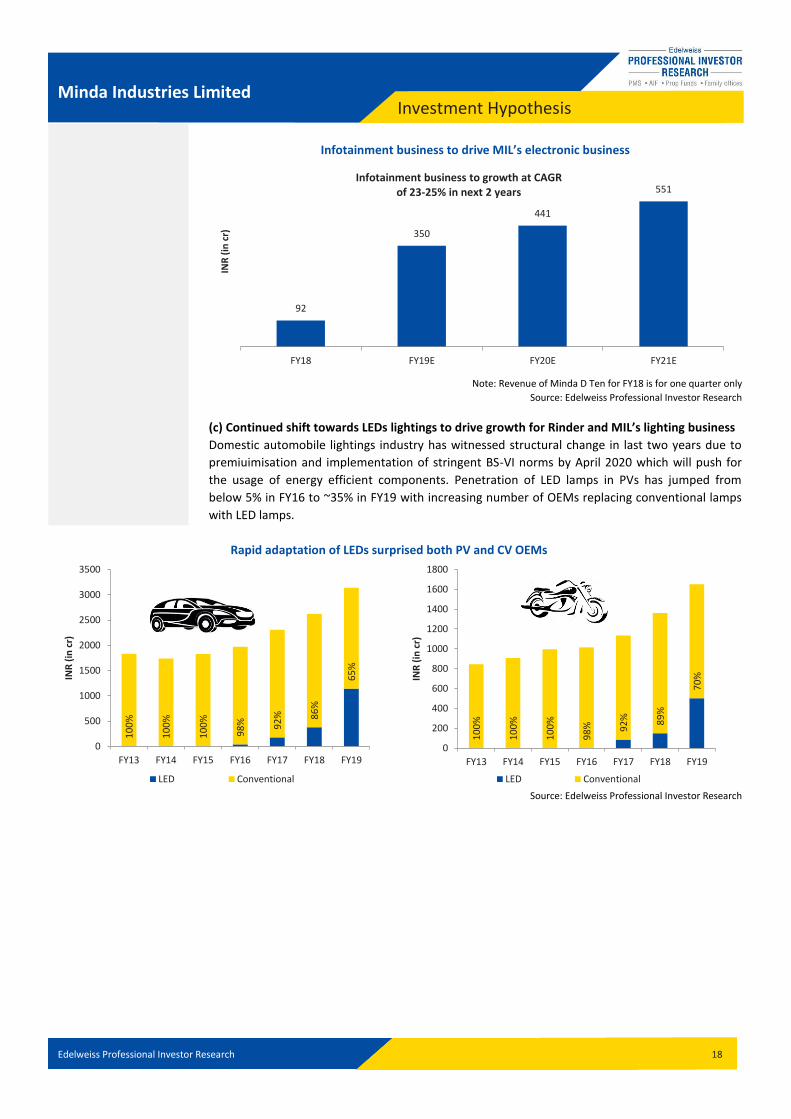

Infotainment business to drive MIL’s electronic business

Note: Revenue of Minda D Ten for FY18 is for one quarter only

Source: Edelweiss Professional Investor Research

(c) Continued shift towards LEDs lightings to drive growth for Rinder and MIL’s lighting business

Domestic automobile lightings industry has witnessed structural change in last two years due to

premiuimisation and implementation of stringent BS-VI norms by April 2020 which will push for

the usage of energy efficient components. Penetration of LED lamps in PVs has jumped from

below 5% in FY16 to ~35% in FY19 with increasing number of OEMs replacing conventional lamps

with LED lamps.

Rapid adaptation of LEDs surprised both PV and CV OEMs

Source: Edelweiss Professional Investor Research

92

350

441

551

FY18 FY19E FY20E FY21E

INR

(in

cr)

Infotainment business to growth at CAGR of 23-25% in next 2 years

10

0%

10

0%

10

0%

98

%

92

%

86

%

65

%

0

500

1000

1500

2000

2500

3000

3500

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

LED Conventional

10

0%

10

0%

10

0%

98

%

92

%

89

%

70

%

0

200

400

600

800

1000

1200

1400

1600

1800

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

LED Conventional

Edelweiss Professional Investor Research 19

Minda Industries Limited Investment Hypothesis

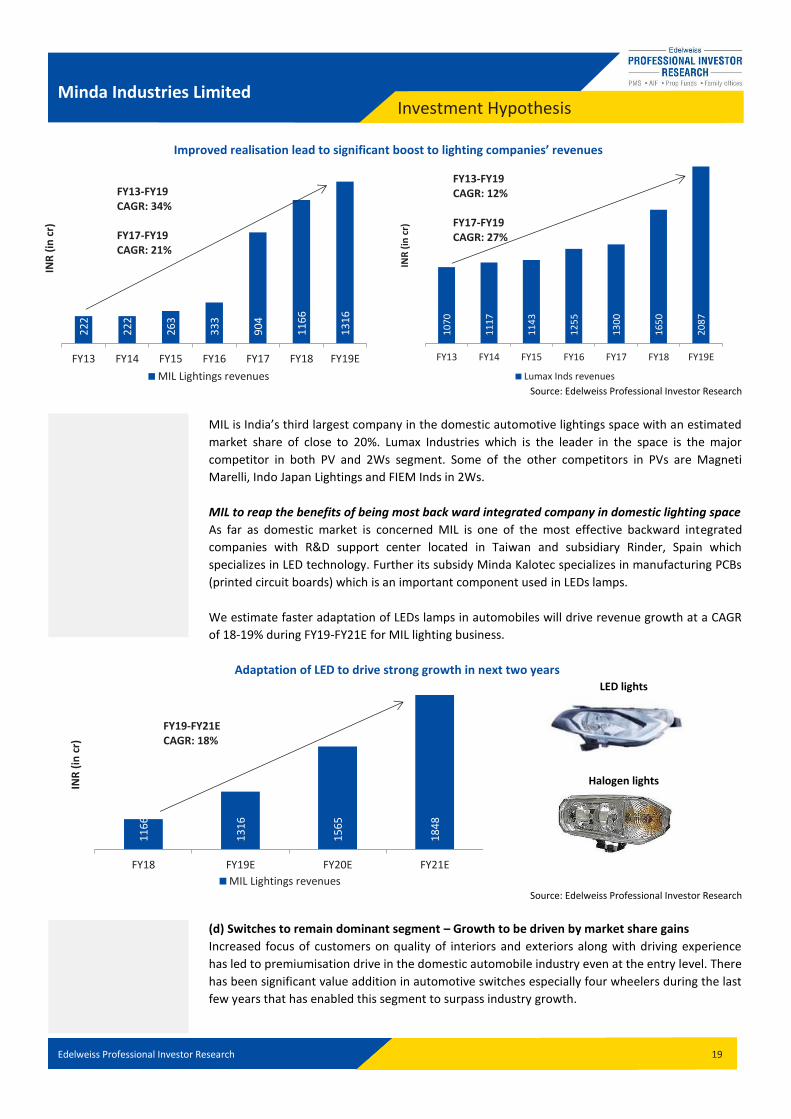

Improved realisation lead to significant boost to lighting companies’ revenues

Source: Edelweiss Professional Investor Research

MIL is India’s third largest company in the domestic automotive lightings space with an estimated

market share of close to 20%. Lumax Industries which is the leader in the space is the major

competitor in both PV and 2Ws segment. Some of the other competitors in PVs are Magneti

Marelli, Indo Japan Lightings and FIEM Inds in 2Ws.

MIL to reap the benefits of being most back ward integrated company in domestic lighting space

As far as domestic market is concerned MIL is one of the most effective backward integrated

companies with R&D support center located in Taiwan and subsidiary Rinder, Spain which

specializes in LED technology. Further its subsidy Minda Kalotec specializes in manufacturing PCBs

(printed circuit boards) which is an important component used in LEDs lamps.

We estimate faster adaptation of LEDs lamps in automobiles will drive revenue growth at a CAGR

of 18-19% during FY19-FY21E for MIL lighting business.

Adaptation of LED to drive strong growth in next two years

LED lights

Halogen lights

Source: Edelweiss Professional Investor Research

(d) Switches to remain dominant segment – Growth to be driven by market share gains

Increased focus of customers on quality of interiors and exteriors along with driving experience

has led to premiumisation drive in the domestic automobile industry even at the entry level. There

has been significant value addition in automotive switches especially four wheelers during the last

few years that has enabled this segment to surpass industry growth.

10

70

11

17

11

43

12

55

13

00

16

50

20

87

FY13 FY14 FY15 FY16 FY17 FY18 FY19E

INR

(in

cr)

Lumax Inds revenues

FY13-FY19 CAGR: 12% FY17-FY19 CAGR: 27%

22

2

22

2

26

3

33

3

90

4

11

66

13

16

FY13 FY14 FY15 FY16 FY17 FY18 FY19E

INR

(in

cr)

MIL Lightings revenues

FY13-FY19 CAGR: 34% FY17-FY19 CAGR: 21%

11

66

13

16

15

65

18

48

FY18 FY19E FY20E FY21E

INR

(in

cr)

MIL Lightings revenues

FY19-FY21E CAGR: 18%

Edelweiss Professional Investor Research 20

Minda Industries Limited Investment Hypothesis

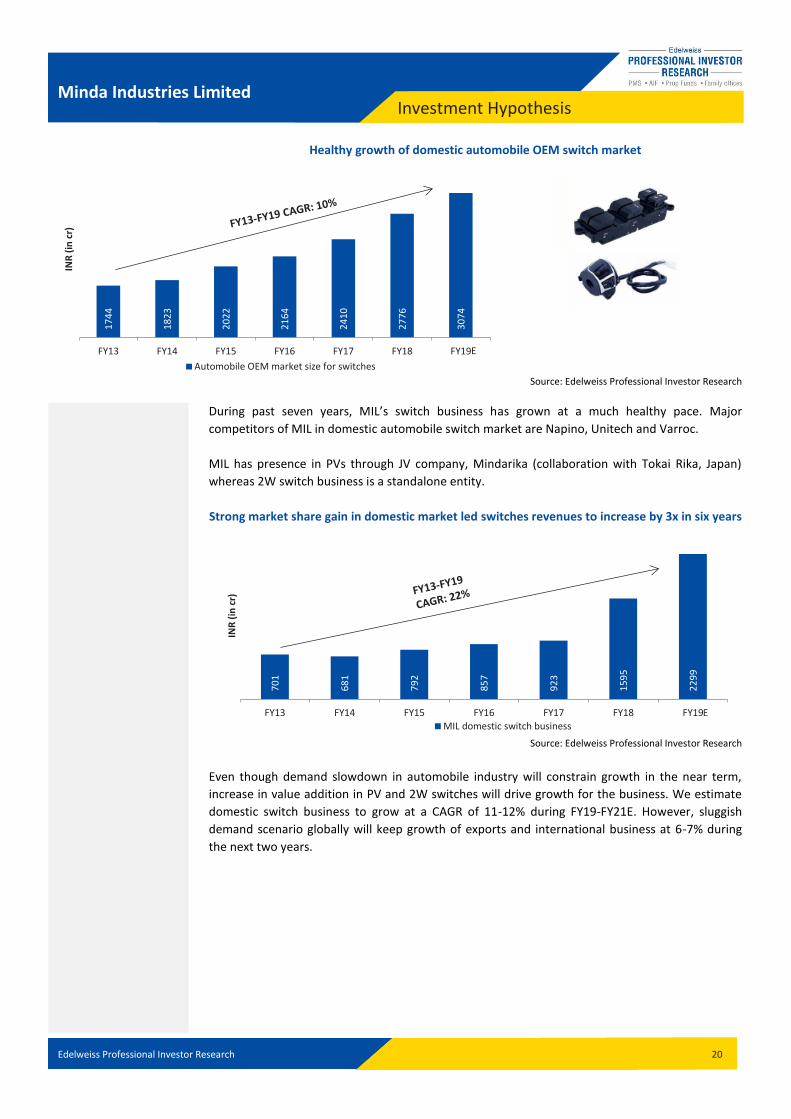

Healthy growth of domestic automobile OEM switch market

Source: Edelweiss Professional Investor Research

During past seven years, MIL’s switch business has grown at a much healthy pace. Major

competitors of MIL in domestic automobile switch market are Napino, Unitech and Varroc.

MIL has presence in PVs through JV company, Mindarika (collaboration with Tokai Rika, Japan)

whereas 2W switch business is a standalone entity.

Strong market share gain in domestic market led switches revenues to increase by 3x in six years

Source: Edelweiss Professional Investor Research

Even though demand slowdown in automobile industry will constrain growth in the near term,

increase in value addition in PV and 2W switches will drive growth for the business. We estimate

domestic switch business to grow at a CAGR of 11-12% during FY19-FY21E. However, sluggish

demand scenario globally will keep growth of exports and international business at 6-7% during

the next two years.

17

44

18

23

20

22

21

64

24

10

27

76

30

74

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

Automobile OEM market size for switches

E

70

1

68

1

79

2

85

7

92

3

15

95

22

99

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

MIL domestic switch businessE

Edelweiss Professional Investor Research 21

Minda Industries Limited Investment Hypothesis

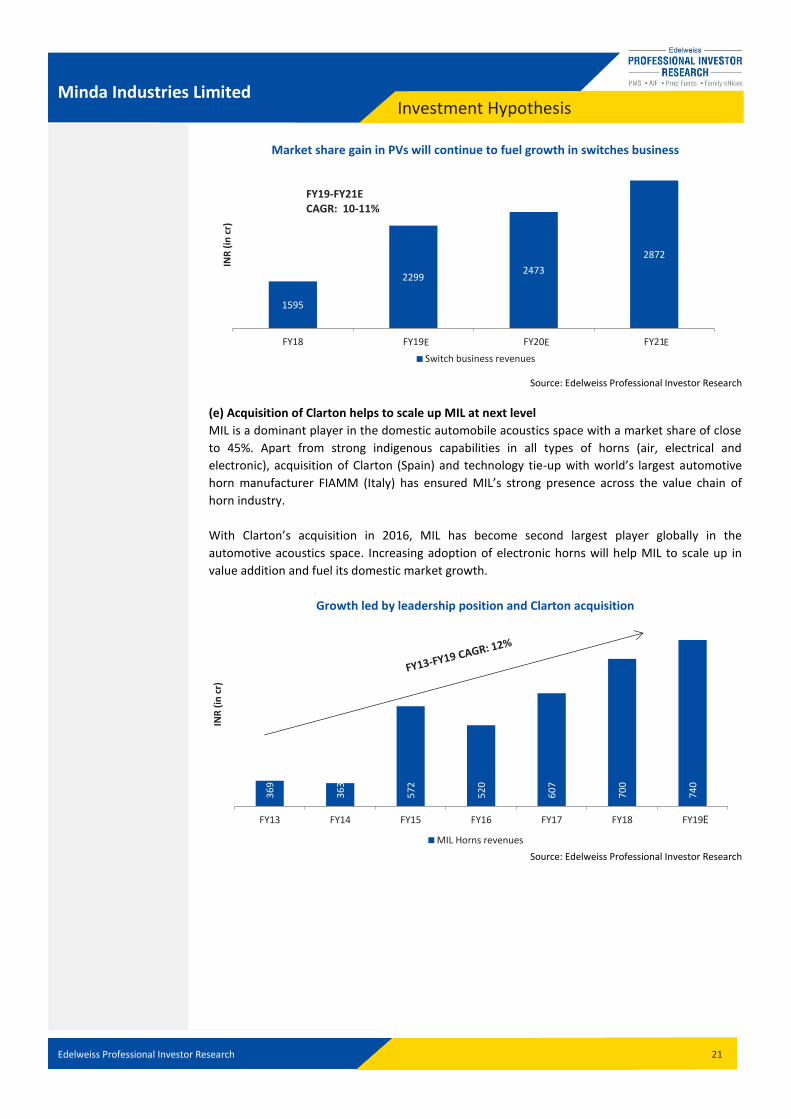

Market share gain in PVs will continue to fuel growth in switches business

Source: Edelweiss Professional Investor Research

(e) Acquisition of Clarton helps to scale up MIL at next level

MIL is a dominant player in the domestic automobile acoustics space with a market share of close

to 45%. Apart from strong indigenous capabilities in all types of horns (air, electrical and

electronic), acquisition of Clarton (Spain) and technology tie-up with world’s largest automotive

horn manufacturer FIAMM (Italy) has ensured MIL’s strong presence across the value chain of

horn industry.

With Clarton’s acquisition in 2016, MIL has become second largest player globally in the

automotive acoustics space. Increasing adoption of electronic horns will help MIL to scale up in

value addition and fuel its domestic market growth.

Growth led by leadership position and Clarton acquisition

Source: Edelweiss Professional Investor Research

36

9

36

3

57

2

52

0

60

7

70

0

74

0

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

MIL Horns revenues

E

1595

2299 2473

2872

FY18 FY19 FY20 FY21

INR

(in

cr)

Switch business revenues

FY19-FY21E CAGR: 10-11%

E E E

Edelweiss Professional Investor Research 22

Minda Industries Limited Investment Hypothesis

Transition towards premiumisation in horns to drive growth in domestic market

Air Horns

Electrical Horns

Electronic Horns

However, we estimate acoustics business to grow at a CAGR of only 7-8% during FY19-FY21E due

to sluggish growth in some of the company’s major overseas markets (forming more than two-

third of the overall revenues).

Lower growth in international business to pull down overall growth of acoustics business

Source: Edelweiss Professional Investor Research

C. Next generation business to lead next leg of growth Investments in technologies

Recently, there has been significant thrust amongst leading auto component players globally on

investing in recent technologies like artificial intelligence and digitisation. Few examples are

advance driver assistance system (ADAS), microelectromechanical systems (MEMS) and sensors.

MIL too was gradually and incrementally focused in these areas in last two-three years and was

manufacturing products that can be used in future mobility. We believe focus in these areas at an

early stage will provide the company a competitive edge in the longer run.

Key initiatives by the company in this direction recenty were series acquisitions: iSYS RTS Germany

(embedded systems and software provider for automobiles) in, telematics business of KPIT

(telematics hardware products for automotive) and Magnetic Speed & Position Sensors (Cam,

Crank & TISS sensor products) business from Sensata Technologies, and tie-ups (JV with TTE in

driving assistance systems and products (DAPS).

174 189 202 234

45 46 47

51

482 506

531 573

FY18 FY19 FY20 FY21

INR

(in

cr)

MIL domestic horns business Exports business Clarton Horns

FY19-FY21 CAGR Domestic: 10-11% Exports: 5-6% Clarton: 6-7%

E E E

Edelweiss Professional Investor Research 23

Minda Industries Limited Investment Hypothesis

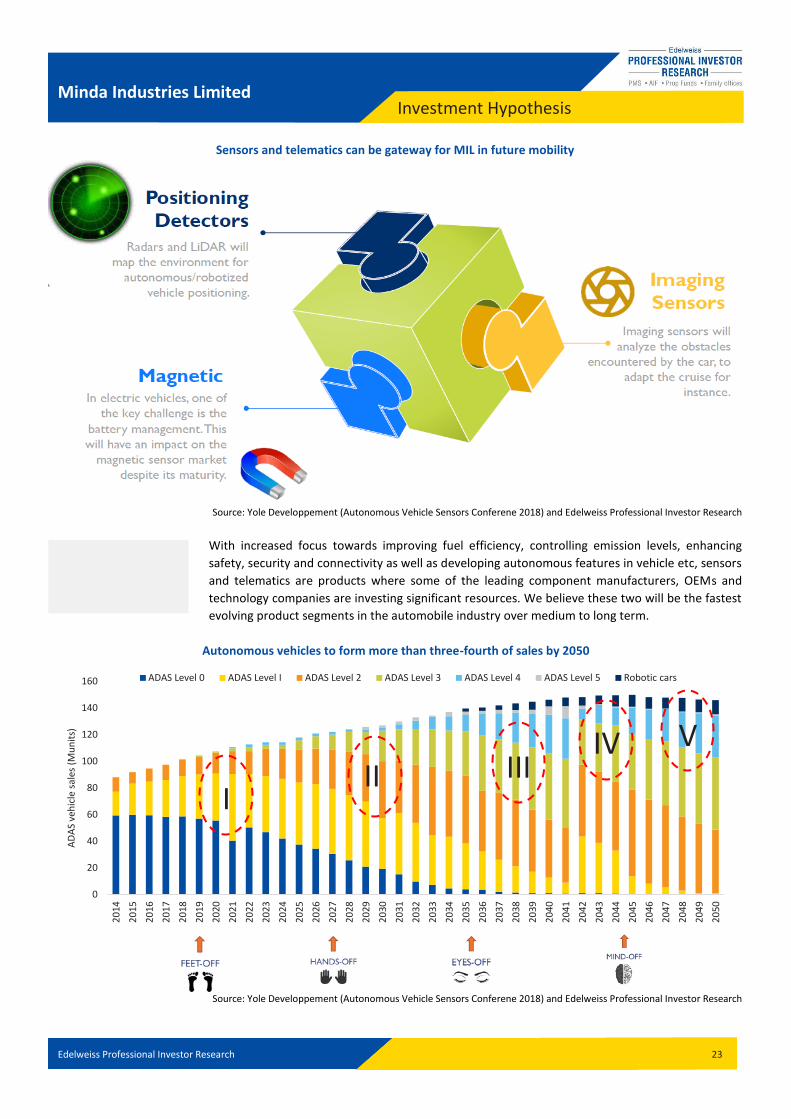

Sensors and telematics can be gateway for MIL in future mobility

Source: Yole Developpement (Autonomous Vehicle Sensors Conferene 2018) and Edelweiss Professional Investor Research

With increased focus towards improving fuel efficiency, controlling emission levels, enhancing

safety, security and connectivity as well as developing autonomous features in vehicle etc, sensors

and telematics are products where some of the leading component manufacturers, OEMs and

technology companies are investing significant resources. We believe these two will be the fastest

evolving product segments in the automobile industry over medium to long term.

Autonomous vehicles to form more than three-fourth of sales by 2050

Source: Yole Developpement (Autonomous Vehicle Sensors Conferene 2018) and Edelweiss Professional Investor Research

0

20

40

60

80

100

120

140

160

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

20

43

20

44

20

45

20

46

20

47

20

48

20

49

20

50

AD

AS

veh

icle

sal

es (

Mu

nit

s)

ADAS Level 0 ADAS Level I ADAS Level 2 ADAS Level 3 ADAS Level 4 ADAS Level 5 Robotic cars

I II III

IV V

Edelweiss Professional Investor Research 24

Minda Industries Limited Investment Hypothesis

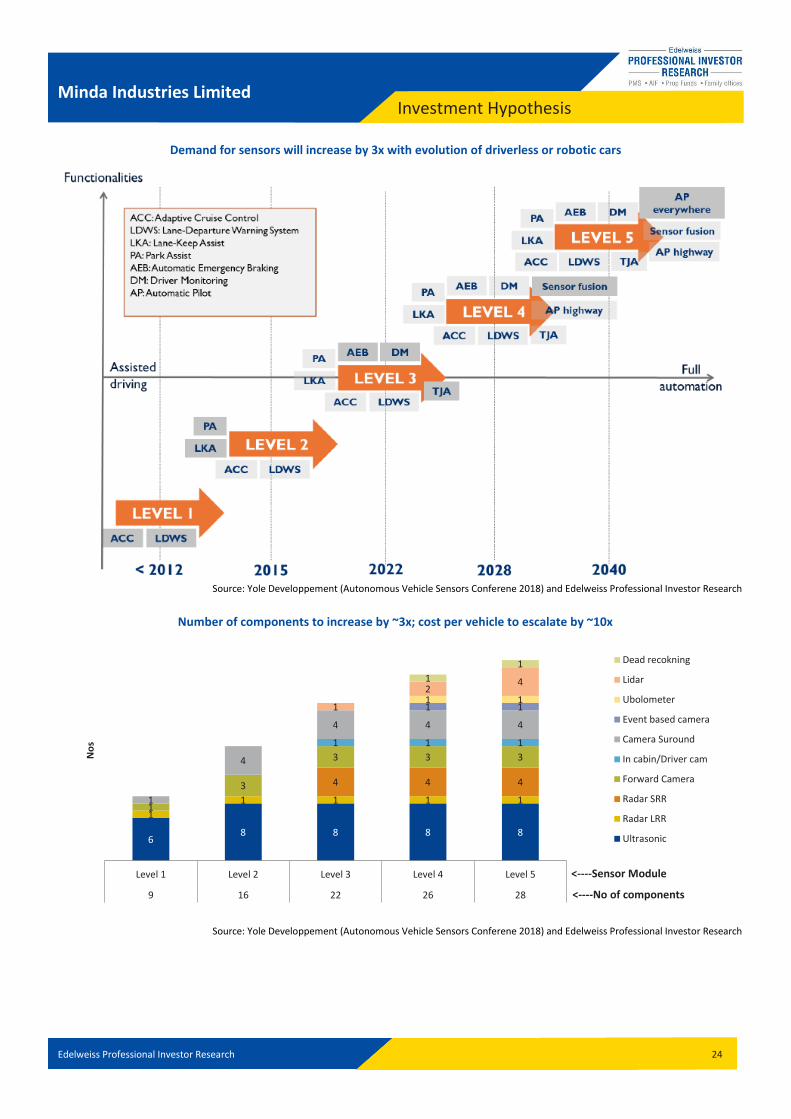

Demand for sensors will increase by 3x with evolution of driverless or robotic cars

Source: Yole Developpement (Autonomous Vehicle Sensors Conferene 2018) and Edelweiss Professional Investor Research

Number of components to increase by ~3x; cost per vehicle to escalate by ~10x

Source: Yole Developpement (Autonomous Vehicle Sensors Conferene 2018) and Edelweiss Professional Investor Research

6 8 8 8 8

1

1 1 1 1

4 4 4

1

3

3 3 3

1 1 1

1

4

4 4 4

1 1 1 1

1

2 4 1

1

Level 1 Level 2 Level 3 Level 4 Level 5

9 16 22 26 28

No

s

Dead recokning

Lidar

Ubolometer

Event based camera

Camera Suround

In cabin/Driver cam

Forward Camera

Radar SRR

Radar LRR

Ultrasonic

<----Sensor Module

<----No of components

Edelweiss Professional Investor Research 25

Minda Industries Limited Investment Hypothesis

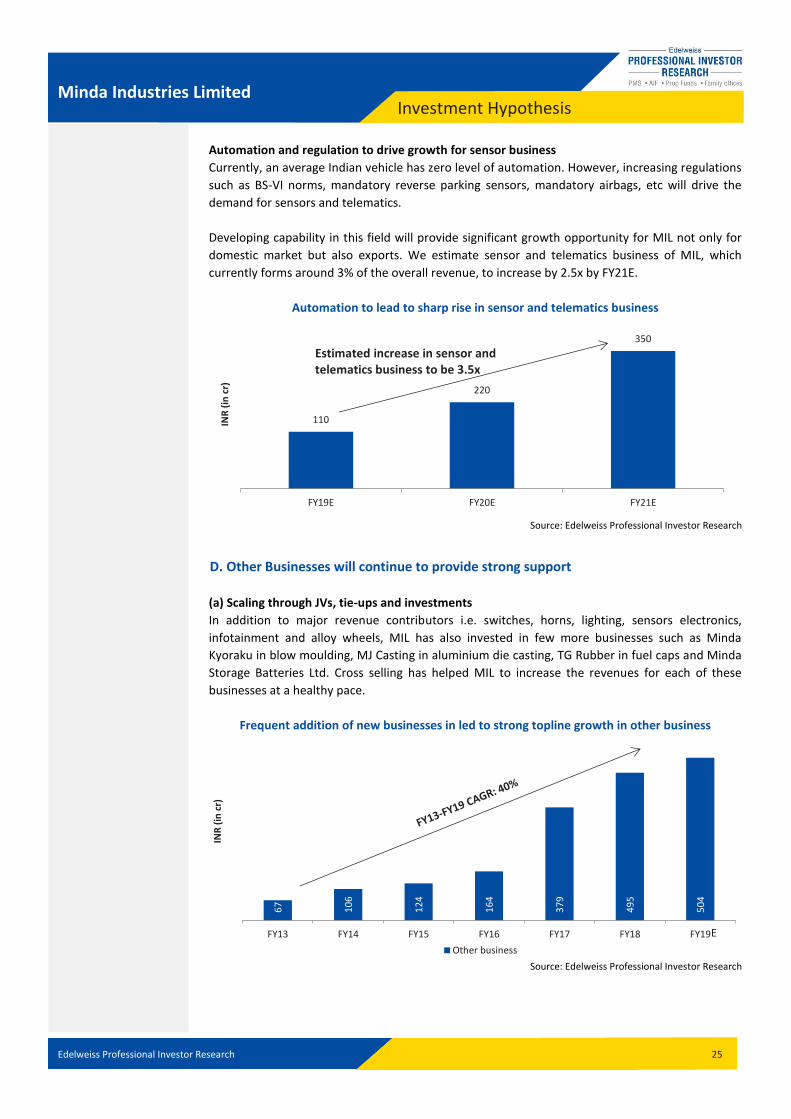

Automation and regulation to drive growth for sensor business

Currently, an average Indian vehicle has zero level of automation. However, increasing regulations

such as BS-VI norms, mandatory reverse parking sensors, mandatory airbags, etc will drive the

demand for sensors and telematics.

Developing capability in this field will provide significant growth opportunity for MIL not only for

domestic market but also exports. We estimate sensor and telematics business of MIL, which

currently forms around 3% of the overall revenue, to increase by 2.5x by FY21E.

Automation to lead to sharp rise in sensor and telematics business

Source: Edelweiss Professional Investor Research

D. Other Businesses will continue to provide strong support

(a) Scaling through JVs, tie-ups and investments

In addition to major revenue contributors i.e. switches, horns, lighting, sensors electronics,

infotainment and alloy wheels, MIL has also invested in few more businesses such as Minda

Kyoraku in blow moulding, MJ Casting in aluminium die casting, TG Rubber in fuel caps and Minda

Storage Batteries Ltd. Cross selling has helped MIL to increase the revenues for each of these

businesses at a healthy pace.

Frequent addition of new businesses in led to strong topline growth in other business

Source: Edelweiss Professional Investor Research

110

220

350

FY19E FY20E FY21E

INR

(in

cr)

Estimated increase in sensor and telematics business to be 3.5x

67

10

6

12

4

16

4

37

9

49

5

50

4

FY13 FY14 FY15 FY16 FY17 FY18 FY19

INR

(in

cr)

Other business

E

Edelweiss Professional Investor Research 26

Minda Industries Limited Investment Hypothesis

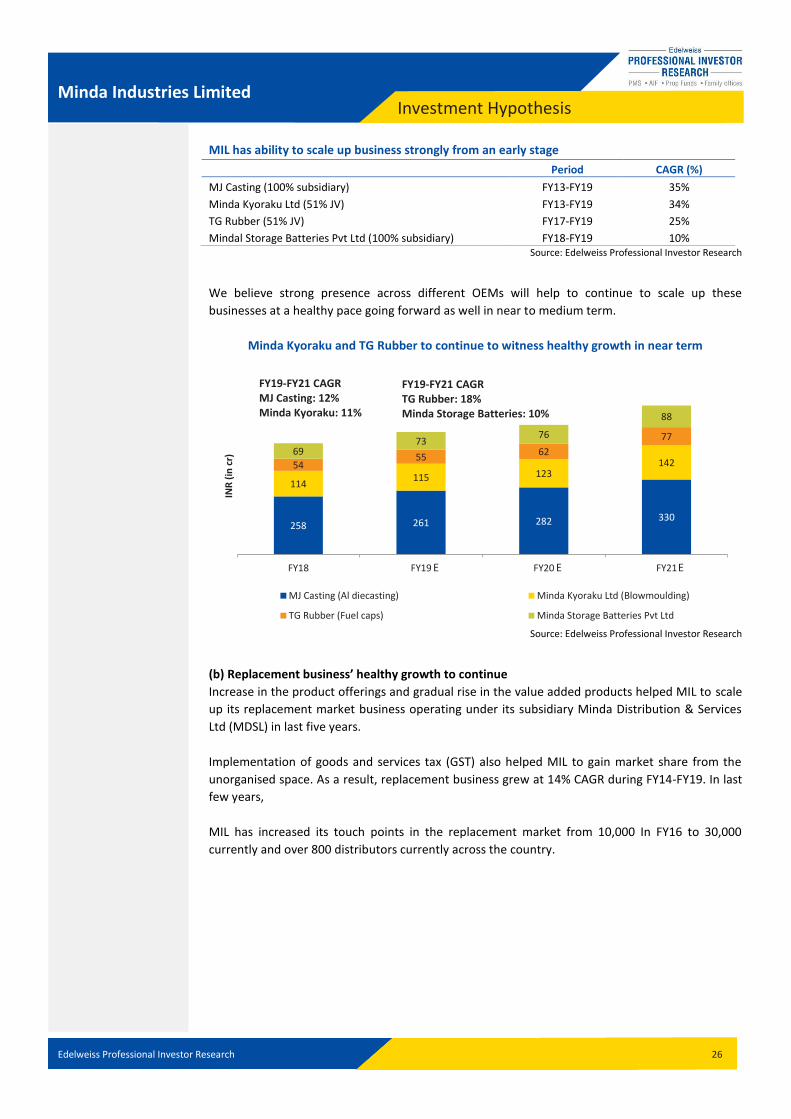

MIL has ability to scale up business strongly from an early stage

Period CAGR (%)

MJ Casting (100% subsidiary) FY13-FY19 35%

Minda Kyoraku Ltd (51% JV) FY13-FY19 34%

TG Rubber (51% JV) FY17-FY19 25%

Mindal Storage Batteries Pvt Ltd (100% subsidiary) FY18-FY19 10% Source: Edelweiss Professional Investor Research

We believe strong presence across different OEMs will help to continue to scale up these

businesses at a healthy pace going forward as well in near to medium term.

Minda Kyoraku and TG Rubber to continue to witness healthy growth in near term

Source: Edelweiss Professional Investor Research

(b) Replacement business’ healthy growth to continue

Increase in the product offerings and gradual rise in the value added products helped MIL to scale

up its replacement market business operating under its subsidiary Minda Distribution & Services

Ltd (MDSL) in last five years.

Implementation of goods and services tax (GST) also helped MIL to gain market share from the

unorganised space. As a result, replacement business grew at 14% CAGR during FY14-FY19. In last

few years,

MIL has increased its touch points in the replacement market from 10,000 In FY16 to 30,000

currently and over 800 distributors currently across the country.

258 261 282 330

114 115 123

142 54 55

62

77

69 73

76

88

FY18 FY19 FY20 FY21

INR

(in

cr)

MJ Casting (Al diecasting) Minda Kyoraku Ltd (Blowmoulding)

TG Rubber (Fuel caps) Minda Storage Batteries Pvt Ltd

FY19-FY21 CAGR MJ Casting: 12% Minda Kyoraku: 11%

FY19-FY21 CAGR TG Rubber: 18% Minda Storage Batteries: 10%

E E E

Edelweiss Professional Investor Research 27

Minda Industries Limited Investment Hypothesis

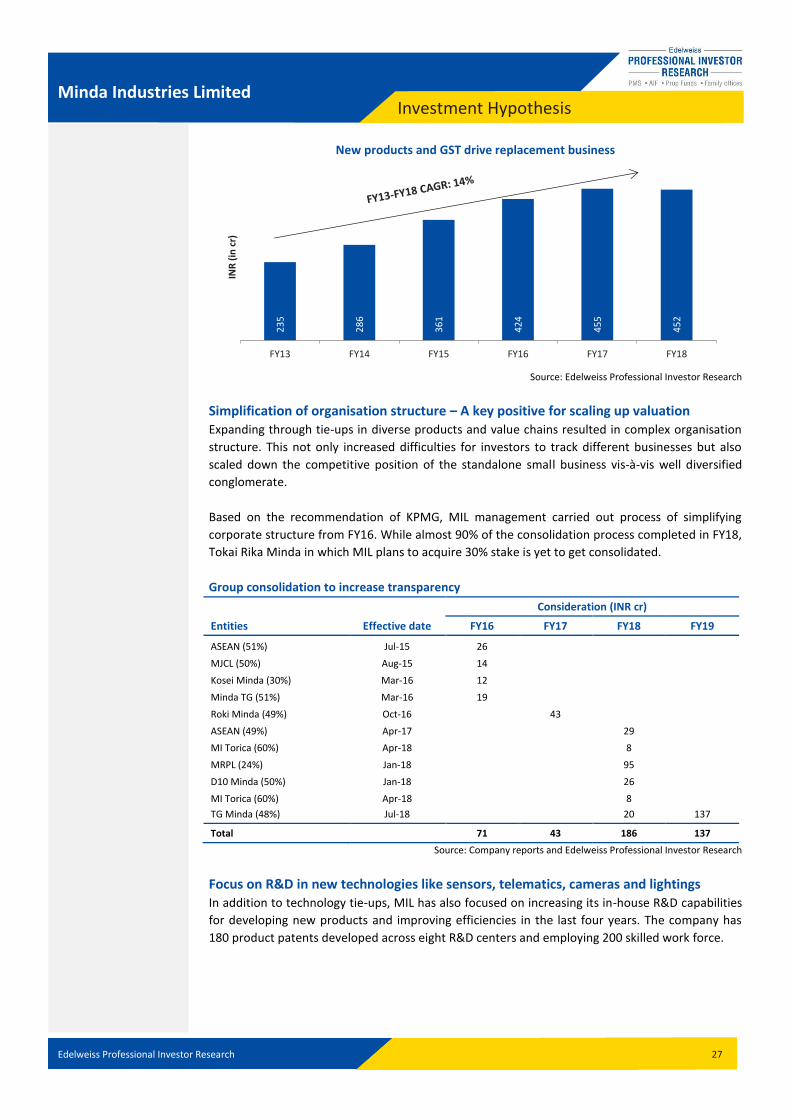

New products and GST drive replacement business

Source: Edelweiss Professional Investor Research

Simplification of organisation structure – A key positive for scaling up valuation Expanding through tie-ups in diverse products and value chains resulted in complex organisation

structure. This not only increased difficulties for investors to track different businesses but also

scaled down the competitive position of the standalone small business vis-à-vis well diversified

conglomerate.

Based on the recommendation of KPMG, MIL management carried out process of simplifying

corporate structure from FY16. While almost 90% of the consolidation process completed in FY18,

Tokai Rika Minda in which MIL plans to acquire 30% stake is yet to get consolidated.

Group consolidation to increase transparency

Consideration (INR cr)

Entities Effective date FY16 FY17 FY18 FY19

ASEAN (51%) Jul-15 26 MJCL (50%) Aug-15 14 Kosei Minda (30%) Mar-16 12 Minda TG (51%) Mar-16 19 Roki Minda (49%) Oct-16

43

ASEAN (49%) Apr-17

29 MI Torica (60%) Apr-18

8

MRPL (24%) Jan-18

95 D10 Minda (50%) Jan-18

26

MI Torica (60%) Apr-18

8 TG Minda (48%) Jul-18 20 137

Total 71 43 186 137

Source: Company reports and Edelweiss Professional Investor Research

Focus on R&D in new technologies like sensors, telematics, cameras and lightings In addition to technology tie-ups, MIL has also focused on increasing its in-house R&D capabilities

for developing new products and improving efficiencies in the last four years. The company has

180 product patents developed across eight R&D centers and employing 200 skilled work force.

23

5

28

6

36

1

42

4

45

5

45

2

FY13 FY14 FY15 FY16 FY17 FY18

INR

(in

cr)

Edelweiss Professional Investor Research 28

Minda Industries Limited Investment Hypothesis

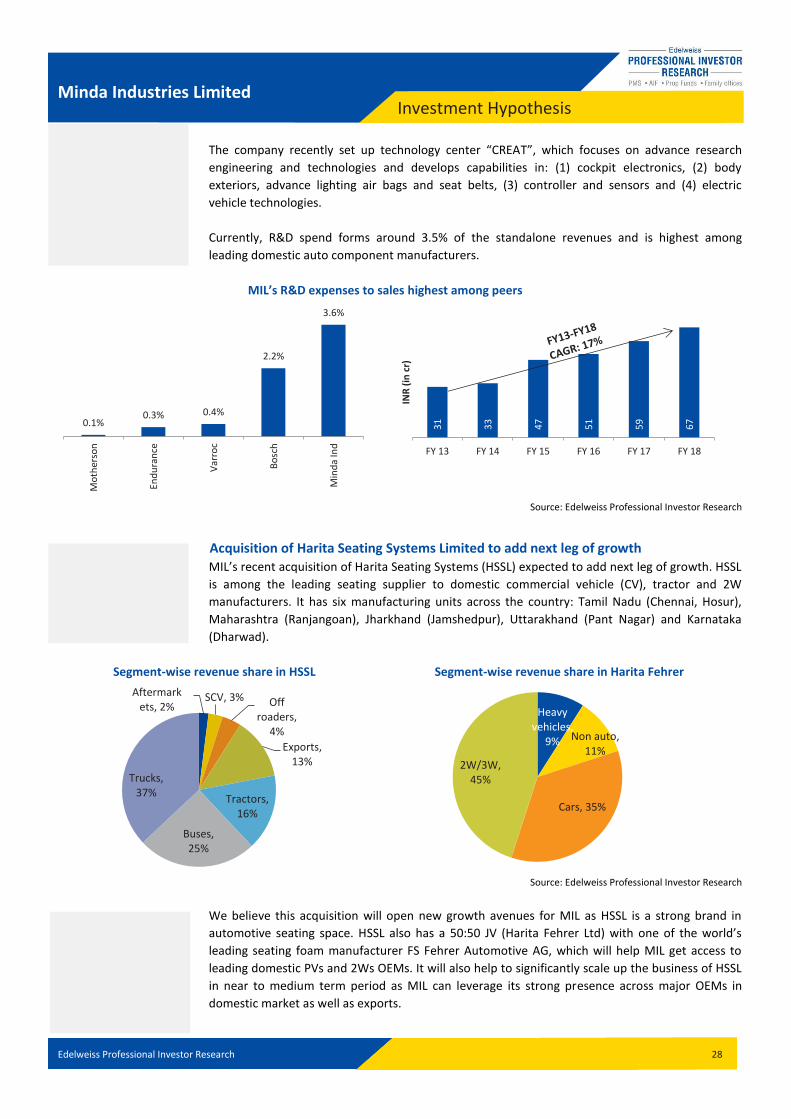

The company recently set up technology center “CREAT”, which focuses on advance research

engineering and technologies and develops capabilities in: (1) cockpit electronics, (2) body

exteriors, advance lighting air bags and seat belts, (3) controller and sensors and (4) electric

vehicle technologies.

Currently, R&D spend forms around 3.5% of the standalone revenues and is highest among

leading domestic auto component manufacturers.

MIL’s R&D expenses to sales highest among peers

Source: Edelweiss Professional Investor Research

Acquisition of Harita Seating Systems Limited to add next leg of growth

MIL’s recent acquisition of Harita Seating Systems (HSSL) expected to add next leg of growth. HSSL

is among the leading seating supplier to domestic commercial vehicle (CV), tractor and 2W

manufacturers. It has six manufacturing units across the country: Tamil Nadu (Chennai, Hosur),

Maharashtra (Ranjangoan), Jharkhand (Jamshedpur), Uttarakhand (Pant Nagar) and Karnataka

(Dharwad).

Segment-wise revenue share in HSSL Segment-wise revenue share in Harita Fehrer

Source: Edelweiss Professional Investor Research

We believe this acquisition will open new growth avenues for MIL as HSSL is a strong brand in

automotive seating space. HSSL also has a 50:50 JV (Harita Fehrer Ltd) with one of the world’s

leading seating foam manufacturer FS Fehrer Automotive AG, which will help MIL get access to

leading domestic PVs and 2Ws OEMs. It will also help to significantly scale up the business of HSSL

in near to medium term period as MIL can leverage its strong presence across major OEMs in

domestic market as well as exports.

0.1% 0.3% 0.4%

2.2%

3.6%

Mo

ther

son

End

ura

nce

Var

roc

Bo

sch

Min

da

Ind

31

33

47

51

59

67

FY 13 FY 14 FY 15 FY 16 FY 17 FY 18

INR

(in

cr)

Aftermarkets, 2%

SCV, 3% Off roaders,

4%

Exports, 13%

Tractors, 16%

Buses, 25%

Trucks, 37%

Heavy vehicles,

9% Non auto, 11%

Cars, 35%

2W/3W, 45%

Edelweiss Professional Investor Research 29

Minda Industries Limited Investment Hypothesis

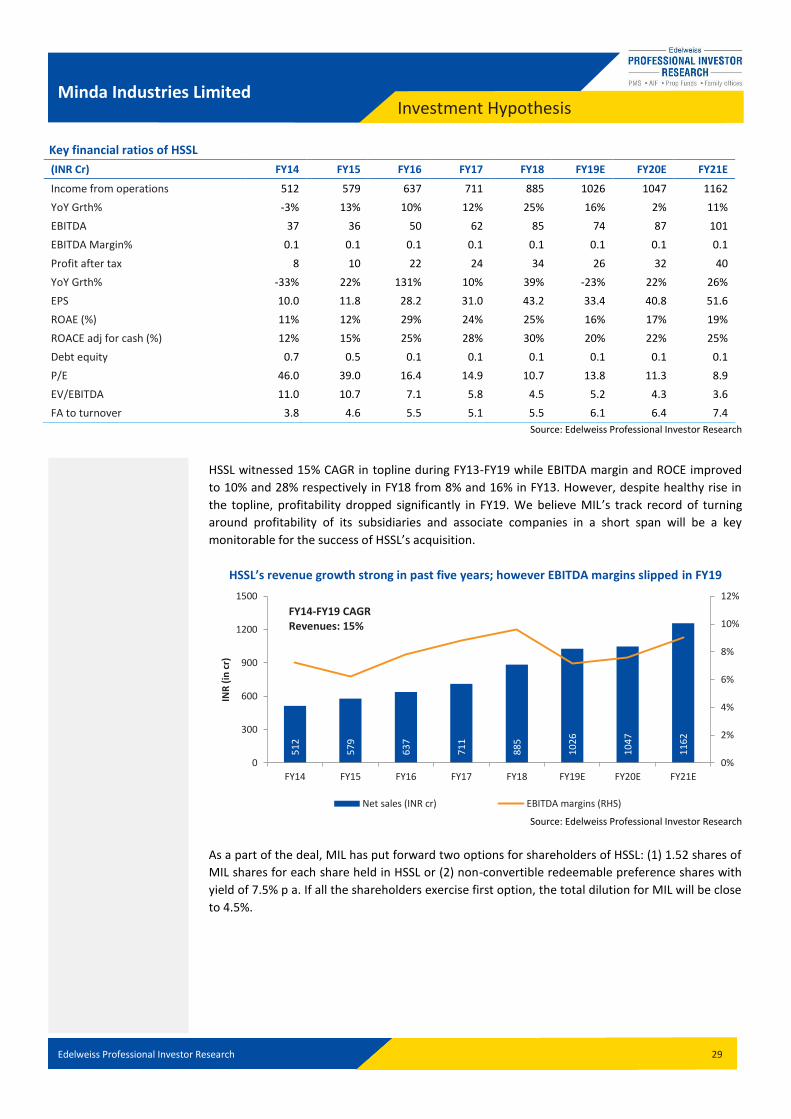

Key financial ratios of HSSL

(INR Cr) FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Income from operations 512 579 637 711 885 1026 1047 1162

YoY Grth% -3% 13% 10% 12% 25% 16% 2% 11%

EBITDA 37 36 50 62 85 74 87 101

EBITDA Margin% 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1

Profit after tax 8 10 22 24 34 26 32 40

YoY Grth% -33% 22% 131% 10% 39% -23% 22% 26%

EPS 10.0 11.8 28.2 31.0 43.2 33.4 40.8 51.6

ROAE (%) 11% 12% 29% 24% 25% 16% 17% 19%

ROACE adj for cash (%) 12% 15% 25% 28% 30% 20% 22% 25%

Debt equity 0.7 0.5 0.1 0.1 0.1 0.1 0.1 0.1

P/E 46.0 39.0 16.4 14.9 10.7 13.8 11.3 8.9

EV/EBITDA 11.0 10.7 7.1 5.8 4.5 5.2 4.3 3.6

FA to turnover 3.8 4.6 5.5 5.1 5.5 6.1 6.4 7.4

Source: Edelweiss Professional Investor Research

HSSL witnessed 15% CAGR in topline during FY13-FY19 while EBITDA margin and ROCE improved

to 10% and 28% respectively in FY18 from 8% and 16% in FY13. However, despite healthy rise in

the topline, profitability dropped significantly in FY19. We believe MIL’s track record of turning

around profitability of its subsidiaries and associate companies in a short span will be a key

monitorable for the success of HSSL’s acquisition.

HSSL’s revenue growth strong in past five years; however EBITDA margins slipped in FY19

Source: Edelweiss Professional Investor Research

As a part of the deal, MIL has put forward two options for shareholders of HSSL: (1) 1.52 shares of

MIL shares for each share held in HSSL or (2) non-convertible redeemable preference shares with

yield of 7.5% p a. If all the shareholders exercise first option, the total dilution for MIL will be close

to 4.5%.

51

2

57

9

63

7

71

1

88

5

10

26

10

47

11

62

0%

2%

4%

6%

8%

10%

12%

0

300

600

900

1200

1500

FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

INR

(in

cr)

Net sales (INR cr) EBITDA margins (RHS)

FY14-FY19 CAGR Revenues: 15%

Edelweiss Professional Investor Research 30

Minda Industries Limited Investment Hypothesis

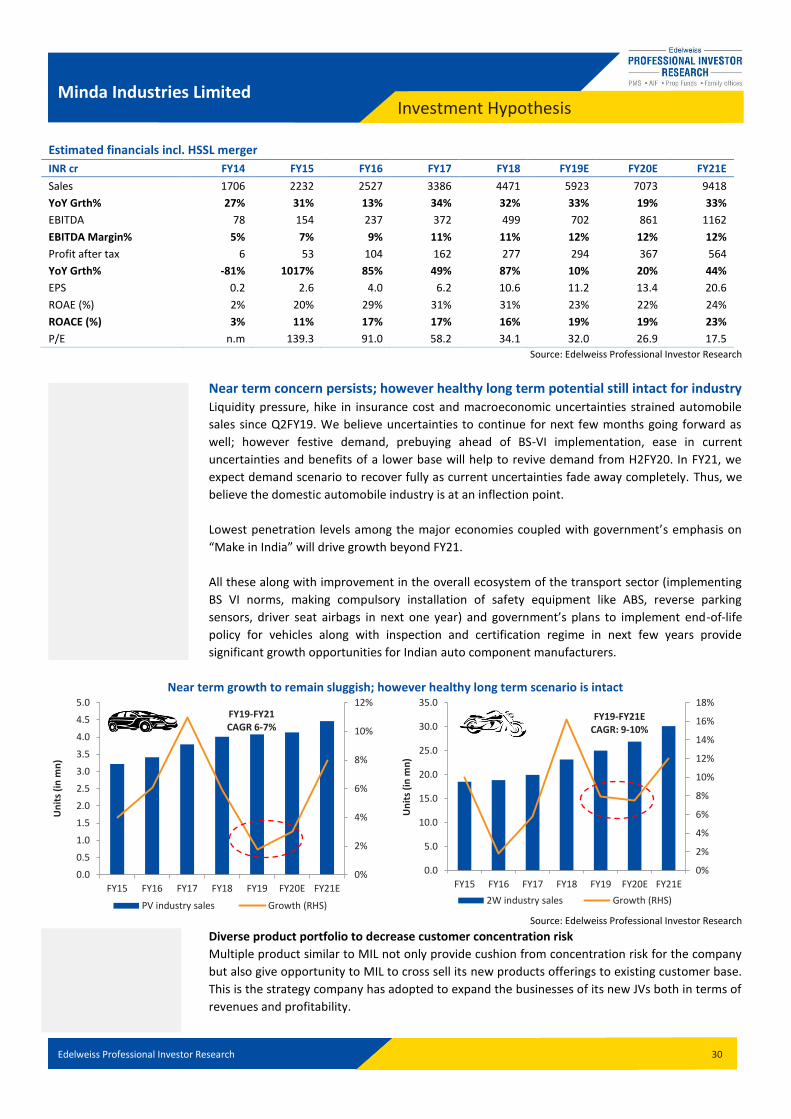

Estimated financials incl. HSSL merger

INR cr FY14 FY15 FY16 FY17 FY18 FY19E FY20E FY21E

Sales 1706 2232 2527 3386 4471 5923 7073 9418

YoY Grth% 27% 31% 13% 34% 32% 33% 19% 33%

EBITDA 78 154 237 372 499 702 861 1162

EBITDA Margin% 5% 7% 9% 11% 11% 12% 12% 12%

Profit after tax 6 53 104 162 277 294 367 564

YoY Grth% -81% 1017% 85% 49% 87% 10% 20% 44%

EPS 0.2 2.6 4.0 6.2 10.6 11.2 13.4 20.6

ROAE (%) 2% 20% 29% 31% 31% 23% 22% 24%

ROACE (%) 3% 11% 17% 17% 16% 19% 19% 23%

P/E n.m 139.3 91.0 58.2 34.1 32.0 26.9 17.5

Source: Edelweiss Professional Investor Research

Near term concern persists; however healthy long term potential still intact for industry

Liquidity pressure, hike in insurance cost and macroeconomic uncertainties strained automobile

sales since Q2FY19. We believe uncertainties to continue for next few months going forward as

well; however festive demand, prebuying ahead of BS-VI implementation, ease in current

uncertainties and benefits of a lower base will help to revive demand from H2FY20. In FY21, we

expect demand scenario to recover fully as current uncertainties fade away completely. Thus, we

believe the domestic automobile industry is at an inflection point.

Lowest penetration levels among the major economies coupled with government’s emphasis on

“Make in India” will drive growth beyond FY21.

All these along with improvement in the overall ecosystem of the transport sector (implementing

BS VI norms, making compulsory installation of safety equipment like ABS, reverse parking

sensors, driver seat airbags in next one year) and government’s plans to implement end-of-life

policy for vehicles along with inspection and certification regime in next few years provide

significant growth opportunities for Indian auto component manufacturers.

Near term growth to remain sluggish; however healthy long term scenario is intact

Source: Edelweiss Professional Investor Research

Diverse product portfolio to decrease customer concentration risk

Multiple product similar to MIL not only provide cushion from concentration risk for the company

but also give opportunity to MIL to cross sell its new products offerings to existing customer base.

This is the strategy company has adopted to expand the businesses of its new JVs both in terms of

revenues and profitability.

0%

2%

4%

6%

8%

10%

12%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E

Un

its

(in

mn

)

PV industry sales Growth (RHS)

FY19-FY21 CAGR 6-7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E

Un

its

(in

mn

)

2W industry sales Growth (RHS)

FY19-FY21E CAGR: 9-10%

Edelweiss Professional Investor Research 31

Minda Industries Limited Investment Hypothesis

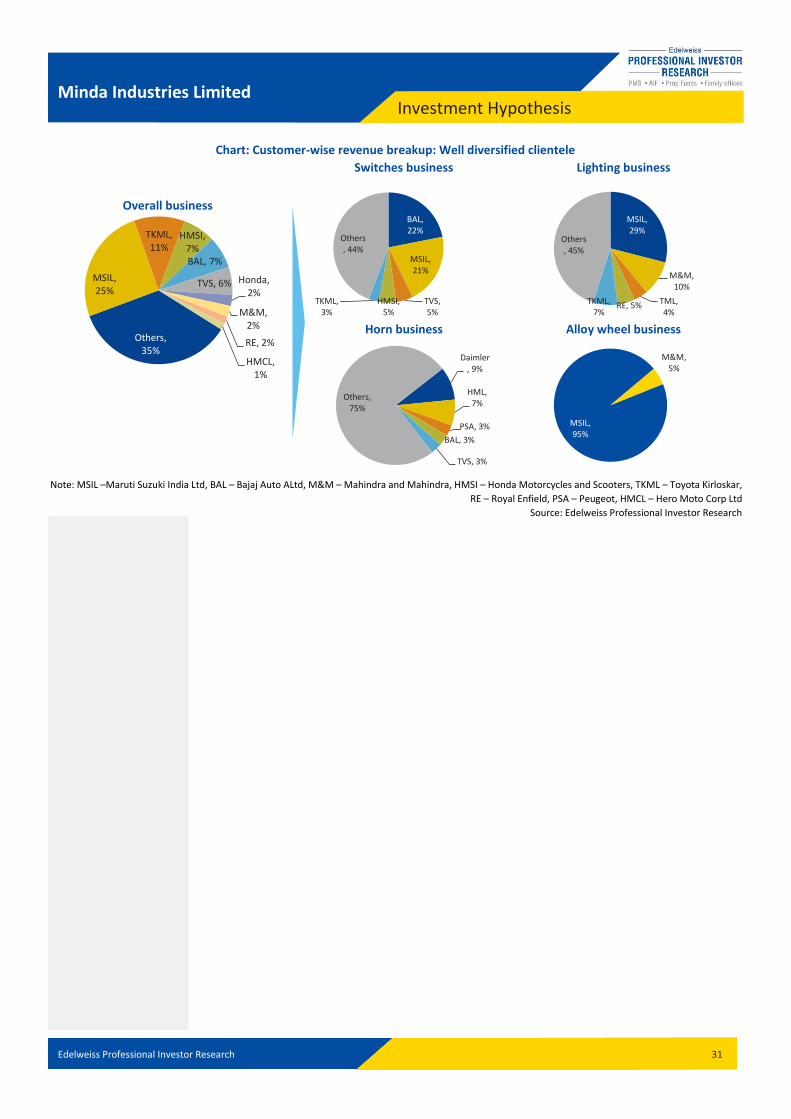

Chart: Customer-wise revenue breakup: Well diversified clientele

Overall business

Switches business Lighting business

Horn business Alloy wheel business

Note: MSIL –Maruti Suzuki India Ltd, BAL – Bajaj Auto ALtd, M&M – Mahindra and Mahindra, HMSI – Honda Motorcycles and Scooters, TKML – Toyota Kirloskar,

RE – Royal Enfield, PSA – Peugeot, HMCL – Hero Moto Corp Ltd

Source: Edelweiss Professional Investor Research

BAL, 22%

MSIL, 21%

TVS, 5%

HMSI, 5%

TKML, 3%

Others, 44%

MSIL, 29%

M&M, 10%

TML, 4%

RE, 5% TKML, 7%

Others, 45%

Daimler, 9%

HML, 7%

PSA, 3%

BAL, 3%

TVS, 3%

Others, 75%

MSIL, 95%

M&M, 5%

Others, 35%

MSIL, 25%

TKML, 11%

HMSI, 7% BAL, 7%

TVS, 6% Honda, 2%

M&M, 2%

RE, 2%

HMCL, 1%

Edelweiss Professional Investor Research 32

Minda Industries Limited Investment Hypothesis

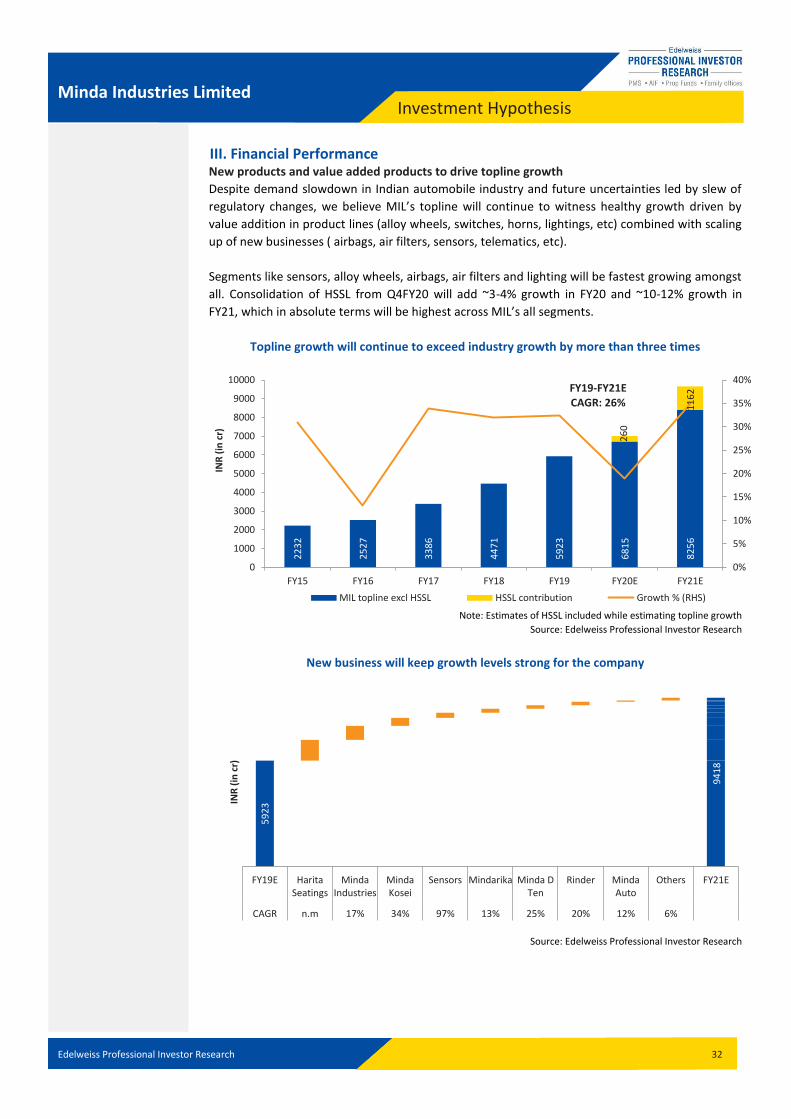

III. Financial Performance New products and value added products to drive topline growth

Despite demand slowdown in Indian automobile industry and future uncertainties led by slew of

regulatory changes, we believe MIL’s topline will continue to witness healthy growth driven by

value addition in product lines (alloy wheels, switches, horns, lightings, etc) combined with scaling

up of new businesses ( airbags, air filters, sensors, telematics, etc).

Segments like sensors, alloy wheels, airbags, air filters and lighting will be fastest growing amongst

all. Consolidation of HSSL from Q4FY20 will add ~3-4% growth in FY20 and ~10-12% growth in

FY21, which in absolute terms will be highest across MIL’s all segments.

Topline growth will continue to exceed industry growth by more than three times

Note: Estimates of HSSL included while estimating topline growth

Source: Edelweiss Professional Investor Research

New business will keep growth levels strong for the company

Source: Edelweiss Professional Investor Research

22

32

25

27

33

86

44

71

59

23

68

15

82

56

26

0

11

62

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

FY15 FY16 FY17 FY18 FY19 FY20E FY21E

INR

(in

cr)

MIL topline excl HSSL HSSL contribution Growth % (RHS)

FY19-FY21E CAGR: 26%

59

23

FY19E HaritaSeatings

MindaIndustries

MindaKosei

Sensors Mindarika Minda DTen

Rinder MindaAuto

Others FY21E

CAGR n.m 17% 34% 97% 13% 25% 20% 12% 6% 0%

INR

(in

cr)

94

18

Edelweiss Professional Investor Research 33

Minda Industries Limited Investment Hypothesis

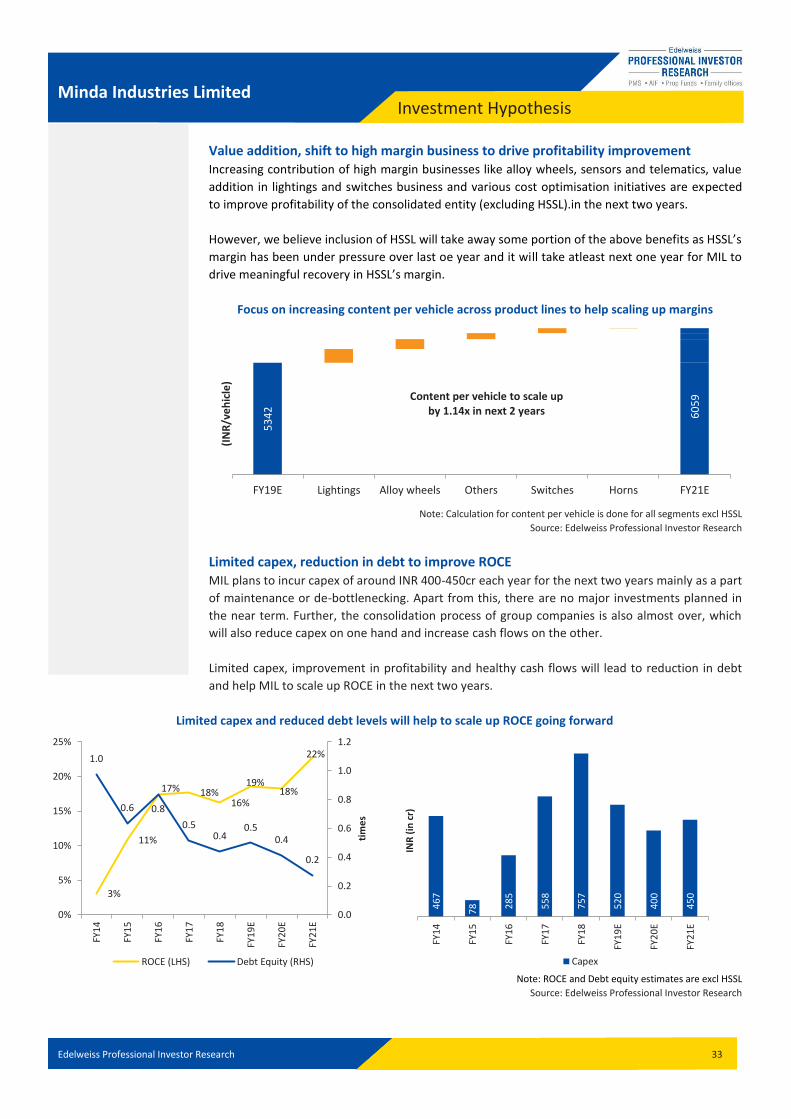

Value addition, shift to high margin business to drive profitability improvement Increasing contribution of high margin businesses like alloy wheels, sensors and telematics, value

addition in lightings and switches business and various cost optimisation initiatives are expected

to improve profitability of the consolidated entity (excluding HSSL).in the next two years.

However, we believe inclusion of HSSL will take away some portion of the above benefits as HSSL’s

margin has been under pressure over last oe year and it will take atleast next one year for MIL to

drive meaningful recovery in HSSL’s margin.

Focus on increasing content per vehicle across product lines to help scaling up margins

Note: Calculation for content per vehicle is done for all segments excl HSSL

Source: Edelweiss Professional Investor Research

Limited capex, reduction in debt to improve ROCE MIL plans to incur capex of around INR 400-450cr each year for the next two years mainly as a part

of maintenance or de-bottlenecking. Apart from this, there are no major investments planned in

the near term. Further, the consolidation process of group companies is also almost over, which

will also reduce capex on one hand and increase cash flows on the other.

Limited capex, improvement in profitability and healthy cash flows will lead to reduction in debt

and help MIL to scale up ROCE in the next two years.

Limited capex and reduced debt levels will help to scale up ROCE going forward

Note: ROCE and Debt equity estimates are excl HSSL

Source: Edelweiss Professional Investor Research

53

42

FY19E Lightings Alloy wheels Others Switches Horns FY21E

(IN

R/v

eh

icle

)

60

59

Content per vehicle to scale up by 1.14x in next 2 years

3%

11%

17% 18% 16%

19% 18%

22% 1.0

0.6 0.8

0.5 0.4

0.5 0.4

0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

0%

5%

10%

15%

20%

25%

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9E

FY2

0E

FY2

1E

tim

es

ROCE (LHS) Debt Equity (RHS)

46

7

78

28

5

55

8

75

7

52

0

40

0

45

0

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9E

FY2

0E

FY2

1E

INR

(in

cr)

Capex

Edelweiss Professional Investor Research 34

Minda Industries Limited Investment Hypothesis

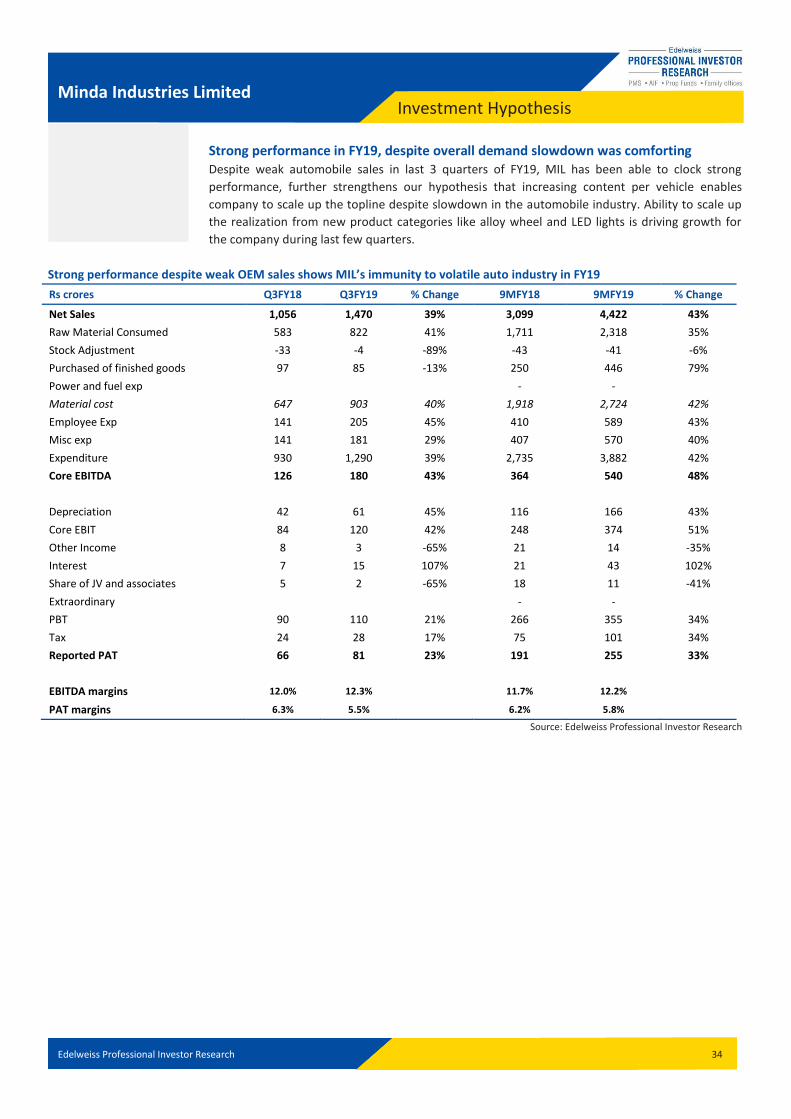

Strong performance in FY19, despite overall demand slowdown was comforting Despite weak automobile sales in last 3 quarters of FY19, MIL has been able to clock strong

performance, further strengthens our hypothesis that increasing content per vehicle enables

company to scale up the topline despite slowdown in the automobile industry. Ability to scale up

the realization from new product categories like alloy wheel and LED lights is driving growth for

the company during last few quarters.

Strong performance despite weak OEM sales shows MIL’s immunity to volatile auto industry in FY19

Rs crores Q3FY18 Q3FY19 % Change 9MFY18 9MFY19 % Change

Net Sales 1,056 1,470 39% 3,099 4,422 43%

Raw Material Consumed 583 822 41% 1,711 2,318 35%

Stock Adjustment -33 -4 -89% -43 -41 -6%

Purchased of finished goods 97 85 -13% 250 446 79%

Power and fuel exp

- -

Material cost 647 903 40% 1,918 2,724 42%

Employee Exp 141 205 45% 410 589 43%

Misc exp 141 181 29% 407 570 40%

Expenditure 930 1,290 39% 2,735 3,882 42%

Core EBITDA 126 180 43% 364 540 48%

Depreciation 42 61 45% 116 166 43%

Core EBIT 84 120 42% 248 374 51%

Other Income 8 3 -65% 21 14 -35%

Interest 7 15 107% 21 43 102%

Share of JV and associates 5 2 -65% 18 11 -41%

Extraordinary

- -

PBT 90 110 21% 266 355 34%

Tax 24 28 17% 75 101 34%

Reported PAT 66 81 23% 191 255 33%

EBITDA margins 12.0% 12.3%

11.7% 12.2%

PAT margins 6.3% 5.5%

6.2% 5.8%

Source: Edelweiss Professional Investor Research

Edelweiss Professional Investor Research 35

Minda Industries Limited Peer Comparison - Valuations

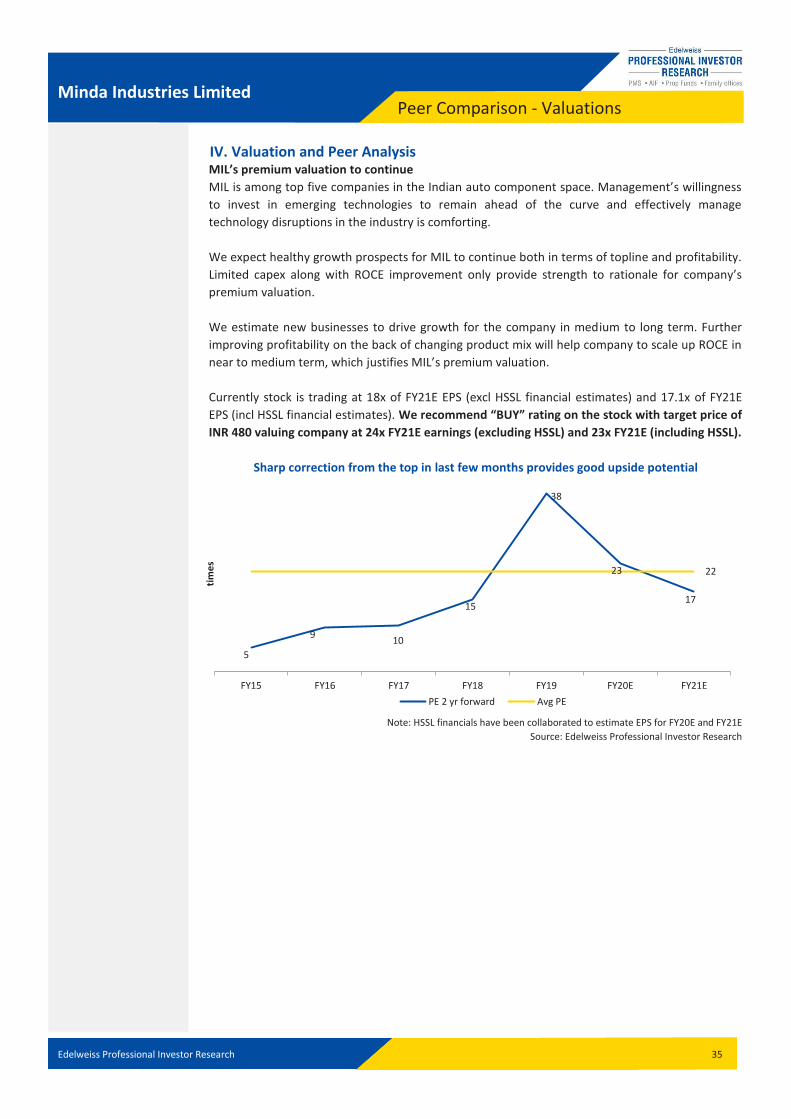

IV. Valuation and Peer Analysis MIL’s premium valuation to continue

MIL is among top five companies in the Indian auto component space. Management’s willingness

to invest in emerging technologies to remain ahead of the curve and effectively manage

technology disruptions in the industry is comforting.

We expect healthy growth prospects for MIL to continue both in terms of topline and profitability.

Limited capex along with ROCE improvement only provide strength to rationale for company’s

premium valuation.

We estimate new businesses to drive growth for the company in medium to long term. Further

improving profitability on the back of changing product mix will help company to scale up ROCE in

near to medium term, which justifies MIL’s premium valuation.

Currently stock is trading at 18x of FY21E EPS (excl HSSL financial estimates) and 17.1x of FY21E

EPS (incl HSSL financial estimates). We recommend “BUY” rating on the stock with target price of

INR 480 valuing company at 24x FY21E earnings (excluding HSSL) and 23x FY21E (including HSSL).

Sharp correction from the top in last few months provides good upside potential

Note: HSSL financials have been collaborated to estimate EPS for FY20E and FY21E

Source: Edelweiss Professional Investor Research

5

9 10

15

38

23

17

22

FY15 FY16 FY17 FY18 FY19 FY20E FY21E

tim

es

PE 2 yr forward Avg PE

Edelweiss Professional Investor Research 36

Minda Industries Limited Peer Comparison - Valuations

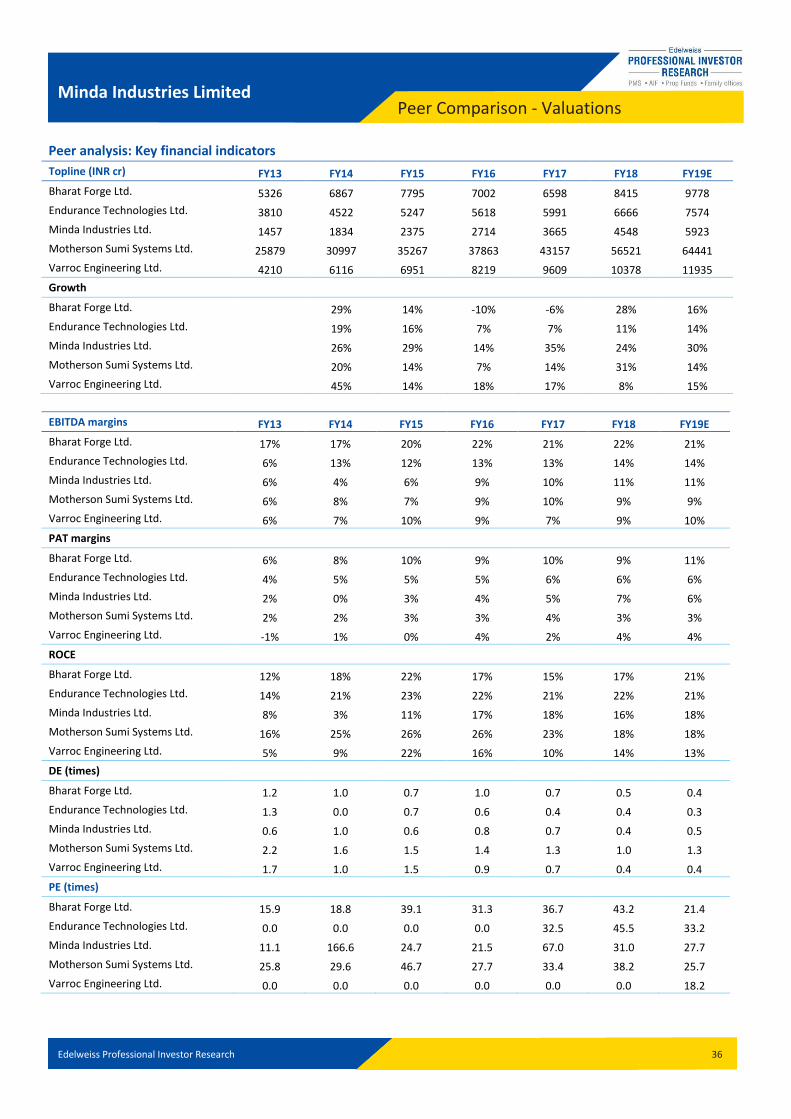

Peer analysis: Key financial indicators

Topline (INR cr) FY13 FY14 FY15 FY16 FY17 FY18 FY19E

Bharat Forge Ltd. 5326 6867 7795 7002 6598 8415 9778

Endurance Technologies Ltd. 3810 4522 5247 5618 5991 6666 7574

Minda Industries Ltd. 1457 1834 2375 2714 3665 4548 5923

Motherson Sumi Systems Ltd. 25879 30997 35267 37863 43157 56521 64441

Varroc Engineering Ltd. 4210 6116 6951 8219 9609 10378 11935

Growth

Bharat Forge Ltd.

29% 14% -10% -6% 28% 16%

Endurance Technologies Ltd.

19% 16% 7% 7% 11% 14%

Minda Industries Ltd.

26% 29% 14% 35% 24% 30%

Motherson Sumi Systems Ltd.

20% 14% 7% 14% 31% 14%

Varroc Engineering Ltd.

45% 14% 18% 17% 8% 15%

EBITDA margins FY13 FY14 FY15 FY16 FY17 FY18 FY19E

Bharat Forge Ltd. 17% 17% 20% 22% 21% 22% 21%

Endurance Technologies Ltd. 6% 13% 12% 13% 13% 14% 14%

Minda Industries Ltd. 6% 4% 6% 9% 10% 11% 11%

Motherson Sumi Systems Ltd. 6% 8% 7% 9% 10% 9% 9%

Varroc Engineering Ltd. 6% 7% 10% 9% 7% 9% 10%

PAT margins

Bharat Forge Ltd. 6% 8% 10% 9% 10% 9% 11%

Endurance Technologies Ltd. 4% 5% 5% 5% 6% 6% 6%

Minda Industries Ltd. 2% 0% 3% 4% 5% 7% 6%

Motherson Sumi Systems Ltd. 2% 2% 3% 3% 4% 3% 3%

Varroc Engineering Ltd. -1% 1% 0% 4% 2% 4% 4%

ROCE

Bharat Forge Ltd. 12% 18% 22% 17% 15% 17% 21%

Endurance Technologies Ltd. 14% 21% 23% 22% 21% 22% 21%

Minda Industries Ltd. 8% 3% 11% 17% 18% 16% 18%

Motherson Sumi Systems Ltd. 16% 25% 26% 26% 23% 18% 18%

Varroc Engineering Ltd. 5% 9% 22% 16% 10% 14% 13%

DE (times)

Bharat Forge Ltd. 1.2 1.0 0.7 1.0 0.7 0.5 0.4

Endurance Technologies Ltd. 1.3 0.0 0.7 0.6 0.4 0.4 0.3

Minda Industries Ltd. 0.6 1.0 0.6 0.8 0.7 0.4 0.5

Motherson Sumi Systems Ltd. 2.2 1.6 1.5 1.4 1.3 1.0 1.3

Varroc Engineering Ltd. 1.7 1.0 1.5 0.9 0.7 0.4 0.4

PE (times)

Bharat Forge Ltd. 15.9 18.8 39.1 31.3 36.7 43.2 21.4

Endurance Technologies Ltd. 0.0 0.0 0.0 0.0 32.5 45.5 33.2

Minda Industries Ltd. 11.1 166.6 24.7 21.5 67.0 31.0 27.7

Motherson Sumi Systems Ltd. 25.8 29.6 46.7 27.7 33.4 38.2 25.7

Varroc Engineering Ltd. 0.0 0.0 0.0 0.0 0.0 0.0 18.2

Edelweiss Professional Investor Research 37

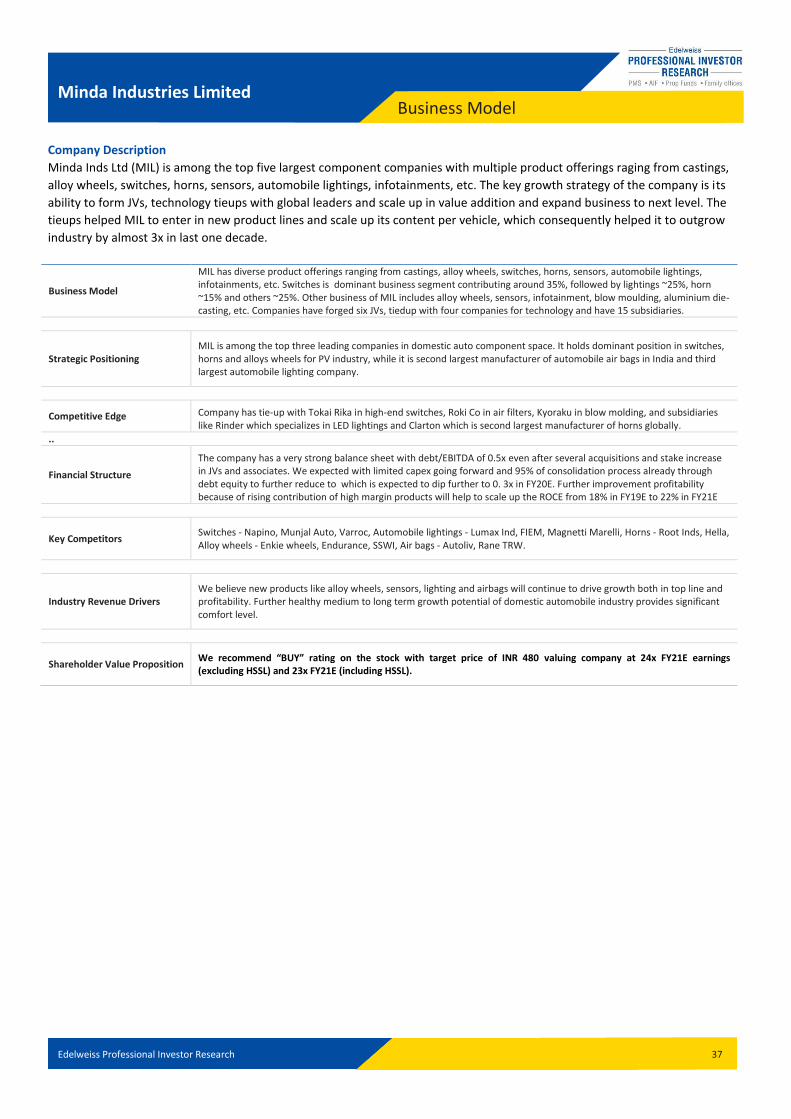

Minda Industries Limited Business Model

Company Description

Minda Inds Ltd (MIL) is among the top five largest component companies with multiple product offerings raging from castings,

alloy wheels, switches, horns, sensors, automobile lightings, infotainments, etc. The key growth strategy of the company is its

ability to form JVs, technology tieups with global leaders and scale up in value addition and expand business to next level. The

tieups helped MIL to enter in new product lines and scale up its content per vehicle, which consequently helped it to outgrow

industry by almost 3x in last one decade.

Business Model

MIL has diverse product offerings ranging from castings, alloy wheels, switches, horns, sensors, automobile lightings, infotainments, etc. Switches is dominant business segment contributing around 35%, followed by lightings ~25%, horn ~15% and others ~25%. Other business of MIL includes alloy wheels, sensors, infotainment, blow moulding, aluminium die-casting, etc. Companies have forged six JVs, tiedup with four companies for technology and have 15 subsidiaries.

Strategic Positioning MIL is among the top three leading companies in domestic auto component space. It holds dominant position in switches, horns and alloys wheels for PV industry, while it is second largest manufacturer of automobile air bags in India and third largest automobile lighting company.

Competitive Edge Company has tie-up with Tokai Rika in high-end switches, Roki Co in air filters, Kyoraku in blow molding, and subsidiaries like Rinder which specializes in LED lightings and Clarton which is second largest manufacturer of horns globally.

..

Financial Structure

The company has a very strong balance sheet with debt/EBITDA of 0.5x even after several acquisitions and stake increase in JVs and associates. We expected with limited capex going forward and 95% of consolidation process already through debt equity to further reduce to which is expected to dip further to 0. 3x in FY20E. Further improvement profitability because of rising contribution of high margin products will help to scale up the ROCE from 18% in FY19E to 22% in FY21E

Key Competitors Switches - Napino, Munjal Auto, Varroc, Automobile lightings - Lumax Ind, FIEM, Magnetti Marelli, Horns - Root Inds, Hella, Alloy wheels - Enkie wheels, Endurance, SSWI, Air bags - Autoliv, Rane TRW.

Industry Revenue Drivers We believe new products like alloy wheels, sensors, lighting and airbags will continue to drive growth both in top line and profitability. Further healthy medium to long term growth potential of domestic automobile industry provides significant comfort level.

Shareholder Value Proposition We recommend “BUY” rating on the stock with target price of INR 480 valuing company at 24x FY21E earnings (excluding HSSL) and 23x FY21E (including HSSL).

Edelweiss Professional Investor Research 38

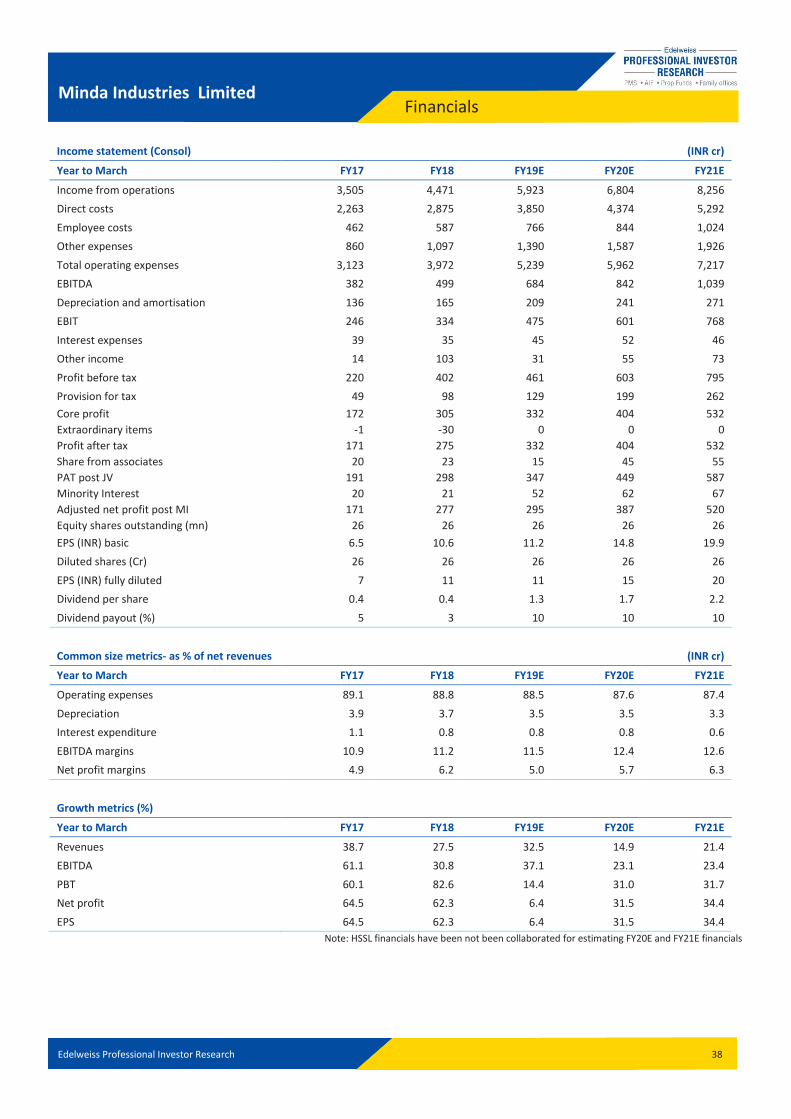

Financials Minda Industries Limited

Income statement (Consol)

(INR cr)

Year to March FY17 FY18 FY19E FY20E FY21E

Income from operations 3,505 4,471 5,923 6,804 8,256

Direct costs 2,263 2,875 3,850 4,374 5,292

Employee costs 462 587 766 844 1,024

Other expenses 860 1,097 1,390 1,587 1,926

Total operating expenses 3,123 3,972 5,239 5,962 7,217

EBITDA 382 499 684 842 1,039

Depreciation and amortisation 136 165 209 241 271

EBIT 246 334 475 601 768

Interest expenses 39 35 45 52 46

Other income 14 103 31 55 73

Profit before tax 220 402 461 603 795

Provision for tax 49 98 129 199 262

Core profit 172 305 332 404 532

Extraordinary items -1 -30 0 0 0

Profit after tax 171 275 332 404 532

Share from associates 20 23 15 45 55

PAT post JV 191 298 347 449 587

Minority Interest 20 21 52 62 67

Adjusted net profit post MI 171 277 295 387 520

Equity shares outstanding (mn) 26 26 26 26 26

EPS (INR) basic 6.5 10.6 11.2 14.8 19.9

Diluted shares (Cr) 26 26 26 26 26

EPS (INR) fully diluted 7 11 11 15 20

Dividend per share 0.4 0.4 1.3 1.7 2.2

Dividend payout (%) 5 3 10 10 10

Common size metrics- as % of net revenues

(INR cr)

Year to March FY17 FY18 FY19E FY20E FY21E

Operating expenses 89.1 88.8 88.5 87.6 87.4

Depreciation 3.9 3.7 3.5 3.5 3.3

Interest expenditure 1.1 0.8 0.8 0.8 0.6

EBITDA margins 10.9 11.2 11.5 12.4 12.6

Net profit margins 4.9 6.2 5.0 5.7 6.3

Growth metrics (%)

Year to March FY17 FY18 FY19E FY20E FY21E

Revenues 38.7 27.5 32.5 14.9 21.4

EBITDA 61.1 30.8 37.1 23.1 23.4

PBT 60.1 82.6 14.4 31.0 31.7

Net profit 64.5 62.3 6.4 31.5 34.4

EPS 64.5 62.3 6.4 31.5 34.4

Note: HSSL financials have been not been collaborated for estimating FY20E and FY21E financials

Edelweiss Professional Investor Research 39

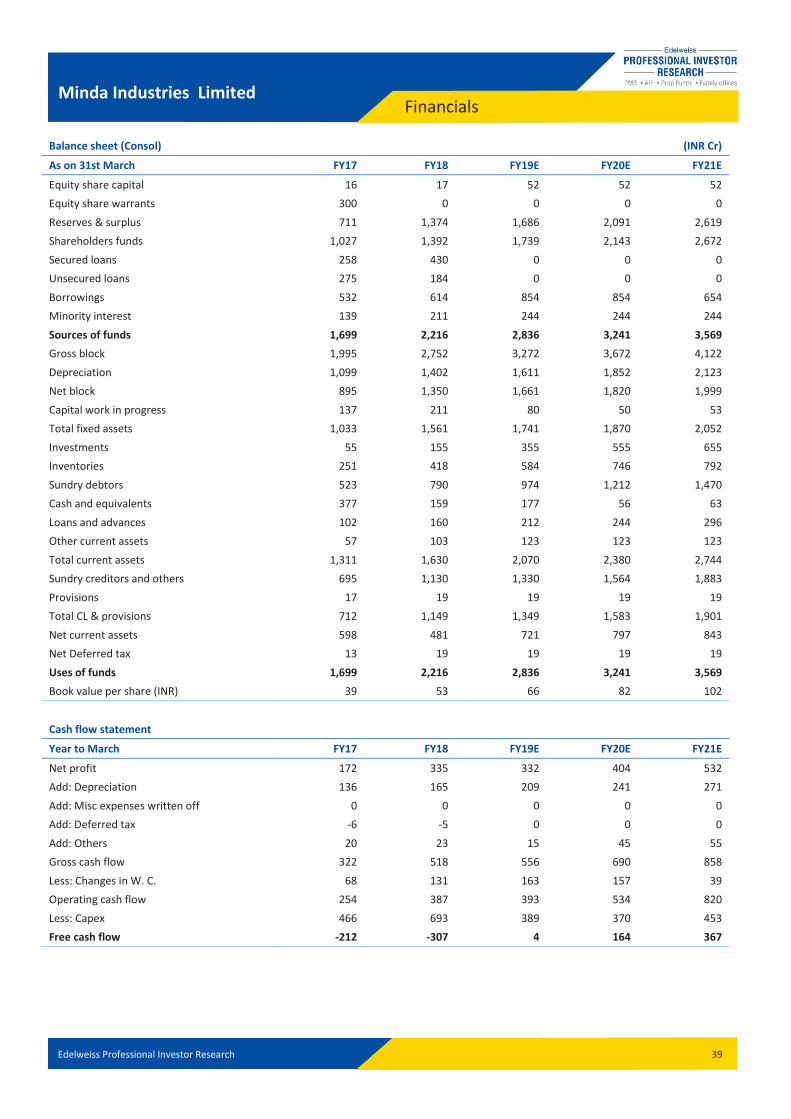

Financials Minda Industries Limited

Balance sheet (Consol)

(INR Cr)

As on 31st March FY17 FY18 FY19E FY20E FY21E

Equity share capital 16 17 52 52 52

Equity share warrants 300 0 0 0 0

Reserves & surplus 711 1,374 1,686 2,091 2,619

Shareholders funds 1,027 1,392 1,739 2,143 2,672

Secured loans 258 430 0 0 0

Unsecured loans 275 184 0 0 0

Borrowings 532 614 854 854 654

Minority interest 139 211 244 244 244

Sources of funds 1,699 2,216 2,836 3,241 3,569

Gross block 1,995 2,752 3,272 3,672 4,122

Depreciation 1,099 1,402 1,611 1,852 2,123

Net block 895 1,350 1,661 1,820 1,999

Capital work in progress 137 211 80 50 53

Total fixed assets 1,033 1,561 1,741 1,870 2,052

Investments 55 155 355 555 655

Inventories 251 418 584 746 792

Sundry debtors 523 790 974 1,212 1,470

Cash and equivalents 377 159 177 56 63

Loans and advances 102 160 212 244 296

Other current assets 57 103 123 123 123

Total current assets 1,311 1,630 2,070 2,380 2,744

Sundry creditors and others 695 1,130 1,330 1,564 1,883

Provisions 17 19 19 19 19

Total CL & provisions 712 1,149 1,349 1,583 1,901

Net current assets 598 481 721 797 843

Net Deferred tax 13 19 19 19 19

Uses of funds 1,699 2,216 2,836 3,241 3,569

Book value per share (INR) 39 53 66 82 102

0 -0 0 0 0

Cash flow statement

Year to March FY17 FY18 FY19E FY20E FY21E

Net profit 172 335 332 404 532

Add: Depreciation 136 165 209 241 271

Add: Misc expenses written off 0 0 0 0 0

Add: Deferred tax -6 -5 0 0 0

Add: Others 20 23 15 45 55

Gross cash flow 322 518 556 690 858

Less: Changes in W. C. 68 131 163 157 39

Operating cash flow 254 387 393 534 820

Less: Capex 466 693 389 370 453

Free cash flow -212 -307 4 164 367

Edelweiss Professional Investor Research 40

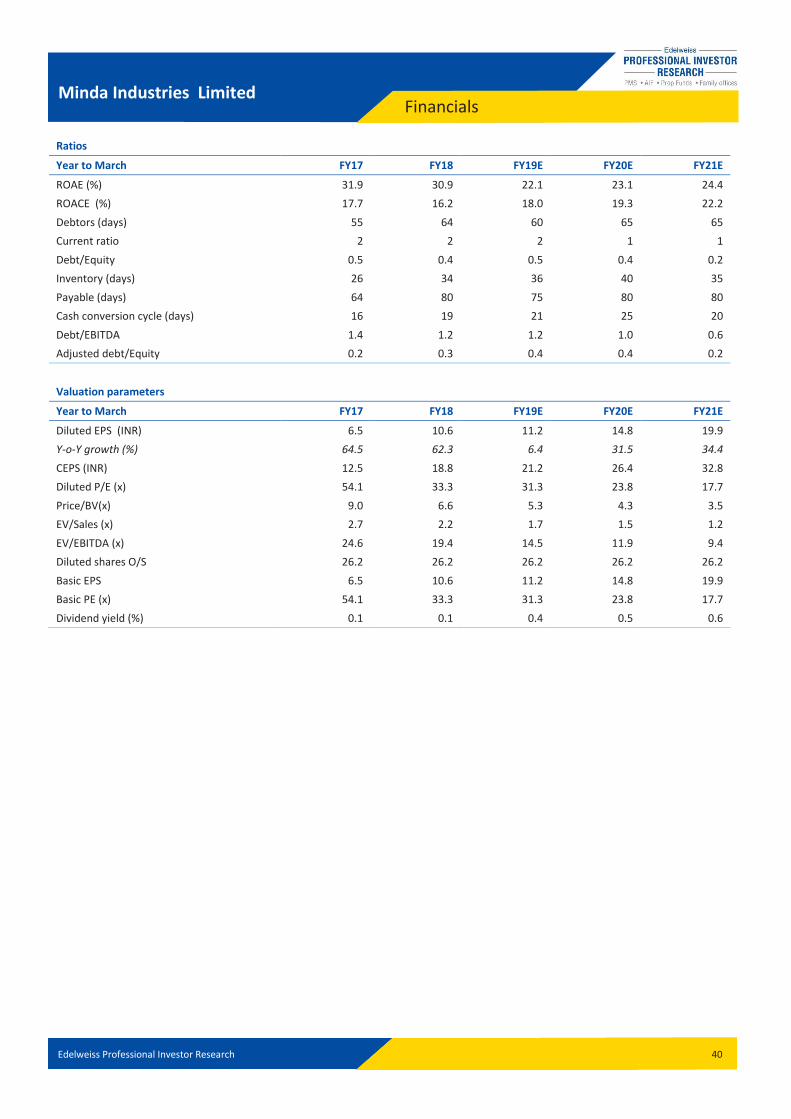

Financials Minda Industries Limited

Ratios

Year to March FY17 FY18 FY19E FY20E FY21E

ROAE (%) 31.9 30.9 22.1 23.1 24.4

ROACE (%) 17.7 16.2 18.0 19.3 22.2

Debtors (days) 55 64 60 65 65

Current ratio 2 2 2 1 1

Debt/Equity 0.5 0.4 0.5 0.4 0.2

Inventory (days) 26 34 36 40 35

Payable (days) 64 80 75 80 80

Cash conversion cycle (days) 16 19 21 25 20

Debt/EBITDA 1.4 1.2 1.2 1.0 0.6

Adjusted debt/Equity 0.2 0.3 0.4 0.4 0.2

Valuation parameters

Year to March FY17 FY18 FY19E FY20E FY21E

Diluted EPS (INR) 6.5 10.6 11.2 14.8 19.9

Y-o-Y growth (%) 64.5 62.3 6.4 31.5 34.4

CEPS (INR) 12.5 18.8 21.2 26.4 32.8

Diluted P/E (x) 54.1 33.3 31.3 23.8 17.7

Price/BV(x) 9.0 6.6 5.3 4.3 3.5

EV/Sales (x) 2.7 2.2 1.7 1.5 1.2

EV/EBITDA (x) 24.6 19.4 14.5 11.9 9.4

Diluted shares O/S 26.2 26.2 26.2 26.2 26.2

Basic EPS 6.5 10.6 11.2 14.8 19.9

Basic PE (x) 54.1 33.3 31.3 23.8 17.7

Dividend yield (%) 0.1 0.1 0.4 0.5 0.6

Edelweiss Professional Investor Research 41

Edelweiss Broking Limited, 1st Floor, Tower 3, Wing B, Kohinoor City Mall, Kohinoor City, Kirol Road, Kurla(W)

Board: (91-22) 4272 2200

Vinay Khattar

Head Research

Rating Expected to

Buy appreciate more than 15% over a 12-month period

Hold appreciate between 5-15% over a 12-month period

Reduce Return below 5% over a 12-month period

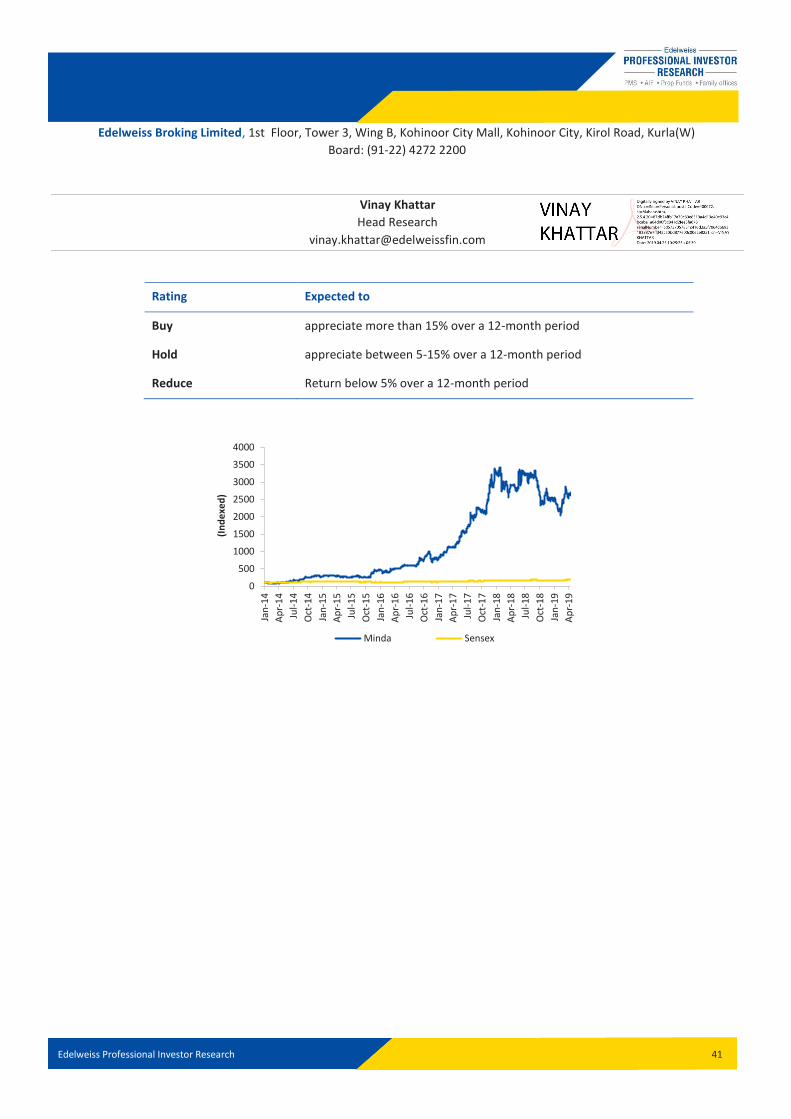

0

500

1000

1500

2000

2500

3000

3500

4000

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

(In

de

xed

)

Minda Sensex

Edelweiss Professional Investor Research 42

Disclaimer Edelweiss Broking Limited (“EBL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, depository

services and related activities. The business of EBL and its Associates (list available on www.edelweissfin.com) are organized around five broad business groups – Credit including

Housing and SME Finance, Commodities, Financial Markets, Asset Management and Life Insurance.

Broking services offered by Edelweiss Broking Limited under SEBI Registration No.: INZ000005231; Name of the Compliance Officer: Mr. Brijmohan Bohra, Email ID:

[email protected] Corporate Office: Edelweiss House, Off CST Road, Kalina, Mumbai - 400098; Tel. 18001023335/022-42722200/022-40094279

This Report has been prepared by Edelweiss Broking Limited in the capacity of a Research Analyst having SEBI Registration No.INH000000172 and distributed as per SEBI (Research

Analysts) Regulations 2014. This report does not constitute an offer or solicitation for the purchase or sale of any financia l instrument or as an official confirmation of any transaction.

The information contained herein is from publicly available data or other sources believed to be reliable. This report is pro vided for assistance only and is not intended to be and must

not alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such

investigation as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks

involved), and should consult his own advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors.

This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or

indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or