20

Mindray Medical International Limited Second Quarter Earnings September 4, 2008

Mindray Medical International Limited

Second Quarter EarningsSeptember 4, 2008

1

Disclaimer

This material contains forward-looking statements with respect to the Company's anticipated operating results for 2008, the anticipated integration of the recently acquired business, the Company's geographic expansion, the Company's outlook regarding drivers, developments, and trends affecting its worldwide markets, opening of international offices, new product development and commercial launch dates, projected revenues, net income margins, earnings per share, revenue growth targets, net income growth targets, sales force and distributor targets, projections of the size of China's healthcare market, estimated government expenditures, research and development expenditure targets, the company's manufacturing development plan, and the anticipated results of its product development activities. These statements are based on information available at the time they are made and are subject to a number of risks and uncertainties. Actual results could differ materially from those anticipated by these forward-looking statements as a result of a number of factors, some of which may be beyond the Company's control. Factors that affect the Company's business operations and product development, as well as a further list and description of risks and uncertainties associated with Mindray's business, are discussed in its reports filed with the Securities and Exchange Commission, including its most recent annual report on Form 20-F. Mindray disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

2

2Q08 Highlights

A world class competitor with strong sales & profitability growthNet revenues US$145.7 million, an increase of 99.5% YoYNet income¹ US$35.2 million, an increase of 54.4% YoY

Domestic net revenues grew over 40% for the 5th consecutive quarter2Q08 growth rate reached 59.4% in USD terms

International expansion from DPM acquisitionGained an established brand line, extensive sales networks and experienced engineers in U.S. & Western Europe from DPM acquisitionContinued international growth from integration of newly acquired direct sales network with expanding distribution network

Expanded product offerings to broaden market reachLaunched three products (BC-5300/5380, DigiEye-560T, AS-3000)

Maintained a disciplined cost focus54.8% gross margin¹, 27.5% operating margin¹ and 24.2% net margin¹

A world class competitor with strong sales & profitability growthNet revenues US$145.7 million, an increase of 99.5% YoYNet income¹ US$35.2 million, an increase of 54.4% YoY

Domestic net revenues grew over 40% for the 5th consecutive quarter2Q08 growth rate reached 59.4% in USD terms

International expansion from DPM acquisitionGained an established brand line, extensive sales networks and experienced engineers in U.S. & Western Europe from DPM acquisitionContinued international growth from integration of newly acquired direct sales network with expanding distribution network

Expanded product offerings to broaden market reachLaunched three products (BC-5300/5380, DigiEye-560T, AS-3000)

Maintained a disciplined cost focus54.8% gross margin¹, 27.5% operating margin¹ and 24.2% net margin¹

Note: 1 Non-GAAP figure - excludes impact from share-based compensation and amortization of intangible assets as defined in the Company's September 4 earnings press release and SEC filing that these slides accompany.

3

Financials – 2Q08 Results Highlights

Note: 1 Non-GAAP figure - excludes impact from share-based compensation and amortization of intangible assets as defined in the Company's September 4 earnings press release and SEC filing that these slides accompany.

USD (in millions,except EPS, A/R, A/P, Inventory days)

2Q08 2Q07 1Q08 YoY

Net Revenues 145.7 73.0 87.4 99.5%

Operating Income¹GAAP Operating Income

40.027.8

23.721.3

30.827.9

68.5%30.8%

Net Income¹GAAP Net Income

35.224.1

22.820.4

27.825.1

54.7%17.6%

Diluted EPS¹GAAP Diluted EPS

0.310.21

0.200.18

0.250.22

55.0%16.7%

Cash and Cash Equivalents 75.0

A/R Days 32 21 32

Inventory Days 57 59 64

A/P Days 50 57 68

4

Domestic

Domestic net revenues growth again exceeded 40%59.4% YoY growth5th consecutive quarter of greater than 40% growth

Growth primarily driven by:Increasing contribution from higher value equipmentIncreasing penetration in Tier 3 hospitals

Continue to build sales force and distribution channelsMR products are now in over 30,000 hospitals and clinics in ChinaDomestic sales & service headcount increased by 11% to more than 1,000 during the quarter

Continue to leverage sales and service teamsSales per head increased from US$26,070 in 2Q07 to US$30,350 in 2Q08

Domestic net revenues growth again exceeded 40%59.4% YoY growth5th consecutive quarter of greater than 40% growth

Growth primarily driven by:Increasing contribution from higher value equipmentIncreasing penetration in Tier 3 hospitals

Continue to build sales force and distribution channelsMR products are now in over 30,000 hospitals and clinics in ChinaDomestic sales & service headcount increased by 11% to more than 1,000 during the quarter

Continue to leverage sales and service teamsSales per head increased from US$26,070 in 2Q07 to US$30,350 in 2Q08

5

International

Significant beneficial effects from DPM acquisitionExperienced international growth from integration of newly acquired direct sales network with expanding distribution networkAdded 458 employees from Datascope’s patient monitoring divisionGained an established brand line, extensive sales networks and experienced engineers in U.S. & Western Europe

Continued benefit from global trendsBenefited from aging populations, healthcare affordability, increasing pricing pressure on hospitals and clinics

Well-balanced growth across geographiesContinued investment in overseas infrastructure, recruiting and localizing staff to increase awareness of the Mindray brand

Significant beneficial effects from DPM acquisitionExperienced international growth from integration of newly acquired direct sales network with expanding distribution networkAdded 458 employees from Datascope’s patient monitoring divisionGained an established brand line, extensive sales networks and experienced engineers in U.S. & Western Europe

Continued benefit from global trendsBenefited from aging populations, healthcare affordability, increasing pricing pressure on hospitals and clinics

Well-balanced growth across geographiesContinued investment in overseas infrastructure, recruiting and localizing staff to increase awareness of the Mindray brand

6

Patient Monitoring and Life Support

Net revenue (in USD millions) 2Q08 2Q07 1Q08 YoY%

$67.0 $26.0 $29.2 157.7%

Substantial patient monitoring and life support revenues added through international acquisition

Organic growth drivers:

Beneview series led growth

Domestically, higher end tier 3 hospitals contributed a higher percentage to total segment revenues

Continued strong demand in Latin America and China

Substantial patient monitoring and life support revenues added through international acquisition

Organic growth drivers:

Beneview series led growth

Domestically, higher end tier 3 hospitals contributed a higher percentage to total segment revenues

Continued strong demand in Latin America and China

iPM Monitor(4Q 2008)

Defibrillator(4Q 2008)2008 New

Product Pipeline

Expected launchNote:

All numbers include the acquisition of Datascope’s Patient Monitoring Business (“DPM”) as of May 1, 2008

7

In-Vitro Diagnostics

Net revenue (in USD millions) 2Q08 2Q07 1Q08 YoY%

$34.9 $21.5 $29.2 62.3%

Biochemistry line led growth

Reagent sales increased to 19% of the IVD product line

Launched 6 new products in first half ‘08

BS-380, a 300 T/H biochemistry analyzer, will provide significant market potential in 2009

Biochemistry line led growth

Reagent sales increased to 19% of the IVD product line

Launched 6 new products in first half ‘08

BS-380, a 300 T/H biochemistry analyzer, will provide significant market potential in 2009

2008 New Product Pipeline

BC-5300/5380 5-PartHematology Analyzer(Apr. 2008)

BS-380 Biochemistry Analyzer(4Q 2008)

5 new reagents(1H 2008)Additional reagents (2H 2008)

Start shipping

Expected launch

8

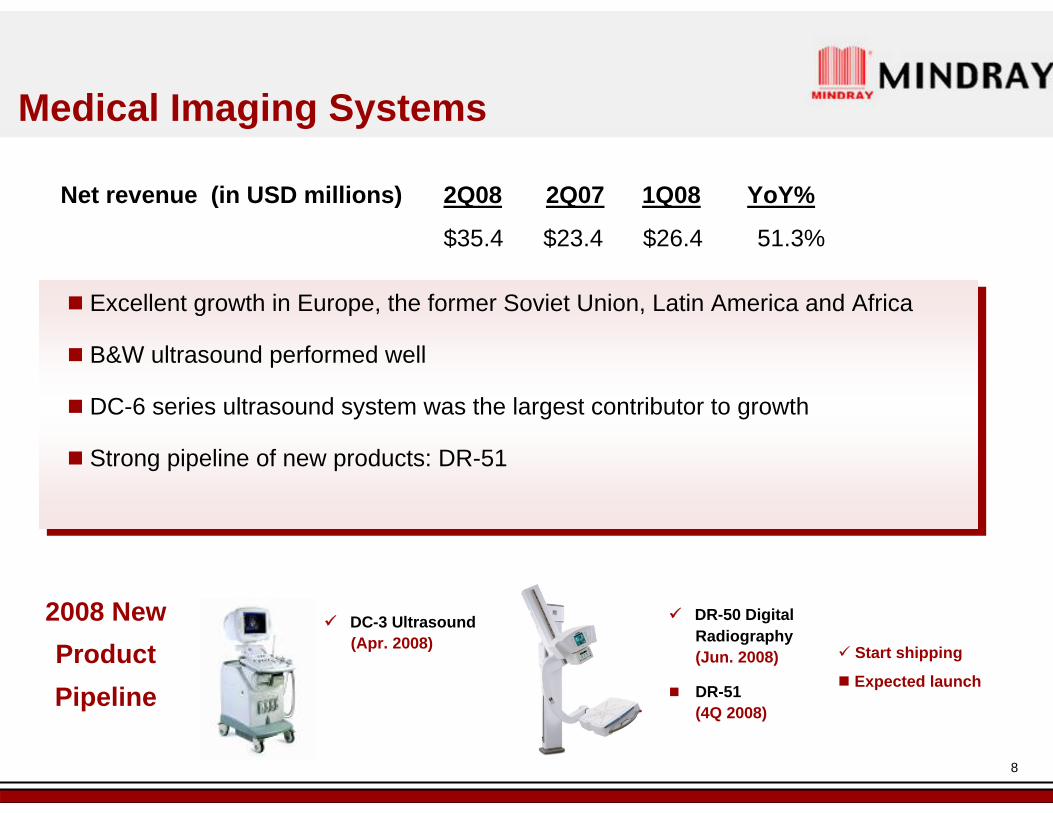

Medical Imaging Systems

Net revenue (in USD millions) 2Q08 2Q07 1Q08 YoY%

$35.4 $23.4 $26.4 51.3%

Excellent growth in Europe, the former Soviet Union, Latin America and Africa

B&W ultrasound performed well

DC-6 series ultrasound system was the largest contributor to growth

Strong pipeline of new products: DR-51

Excellent growth in Europe, the former Soviet Union, Latin America and Africa

B&W ultrasound performed well

DC-6 series ultrasound system was the largest contributor to growth

Strong pipeline of new products: DR-51

2008 New Product Pipeline

DC-3 Ultrasound (Apr. 2008)

DR-50 Digital Radiography(Jun. 2008)

DR-51(4Q 2008)

Start shipping

Expected launch

9

Acquisition Integration UpdateSeptember 2008

Acquisition Integration Update

10

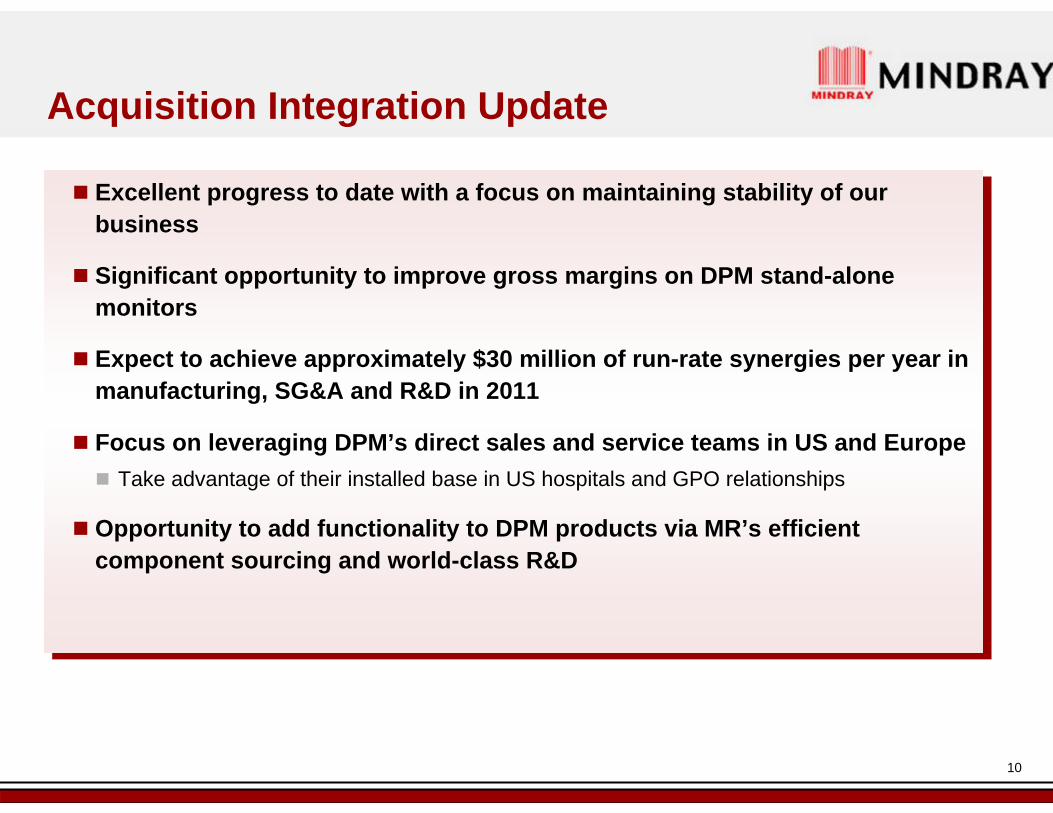

Excellent progress to date with a focus on maintaining stability of our business

Significant opportunity to improve gross margins on DPM stand-alone monitors

Expect to achieve approximately $30 million of run-rate synergies per year in manufacturing, SG&A and R&D in 2011

Focus on leveraging DPM’s direct sales and service teams in US and EuropeTake advantage of their installed base in US hospitals and GPO relationships

Opportunity to add functionality to DPM products via MR’s efficient component sourcing and world-class R&D

Excellent progress to date with a focus on maintaining stability of our business

Significant opportunity to improve gross margins on DPM stand-alone monitors

Expect to achieve approximately $30 million of run-rate synergies per year in manufacturing, SG&A and R&D in 2011

Focus on leveraging DPM’s direct sales and service teams in US and EuropeTake advantage of their installed base in US hospitals and GPO relationships

Opportunity to add functionality to DPM products via MR’s efficient component sourcing and world-class R&D

Integration Highlights To Date

11

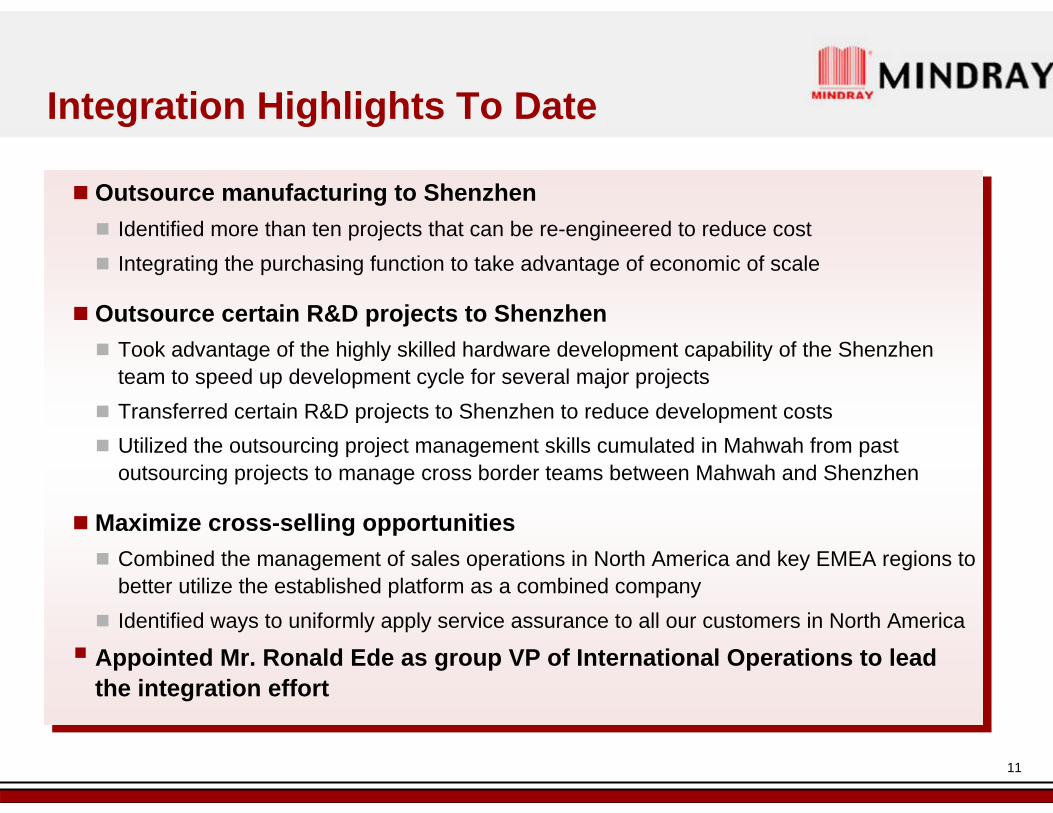

Outsource manufacturing to ShenzhenIdentified more than ten projects that can be re-engineered to reduce costIntegrating the purchasing function to take advantage of economic of scale

Outsource certain R&D projects to ShenzhenTook advantage of the highly skilled hardware development capability of the Shenzhen team to speed up development cycle for several major projectsTransferred certain R&D projects to Shenzhen to reduce development costs Utilized the outsourcing project management skills cumulated in Mahwah from past outsourcing projects to manage cross border teams between Mahwah and Shenzhen

Maximize cross-selling opportunitiesCombined the management of sales operations in North America and key EMEA regions to better utilize the established platform as a combined companyIdentified ways to uniformly apply service assurance to all our customers in North America

Appointed Mr. Ronald Ede as group VP of International Operations to lead the integration effort

Outsource manufacturing to ShenzhenIdentified more than ten projects that can be re-engineered to reduce costIntegrating the purchasing function to take advantage of economic of scale

Outsource certain R&D projects to ShenzhenTook advantage of the highly skilled hardware development capability of the Shenzhen team to speed up development cycle for several major projectsTransferred certain R&D projects to Shenzhen to reduce development costs Utilized the outsourcing project management skills cumulated in Mahwah from past outsourcing projects to manage cross border teams between Mahwah and Shenzhen

Maximize cross-selling opportunitiesCombined the management of sales operations in North America and key EMEA regions to better utilize the established platform as a combined companyIdentified ways to uniformly apply service assurance to all our customers in North America

Appointed Mr. Ronald Ede as group VP of International Operations to lead the integration effort

(in US millions, except EPS) 2008E 2007 YoY growth (%)

Net sales $560~580 $294 90%~97%

Gross margin (%)2 53%~54%2 55%

Net income2 $132 ~135 $88.6 49%~52%

Diluted EPS2,3 $1.16~1.18 $0.78 49%~51%

Capital expenditure $90~110 $46.2

Share-based compensation $10 $7.7

Financials -- 2008 Guidance1

1 Forecast financials as publicly provided on September 4, 2008 2 Non-GAAP figure - excludes impact from share-based compensation and amortization of intangible assets as

defined in the Company's September 4 earnings press release and SEC filing that these slides accompany.3 2008 fully diluted EPS is calculated using an estimated 114 million total shares outstanding

13

Thank you!

Q&A

14

Supplementary InformationSeptember 2008

15

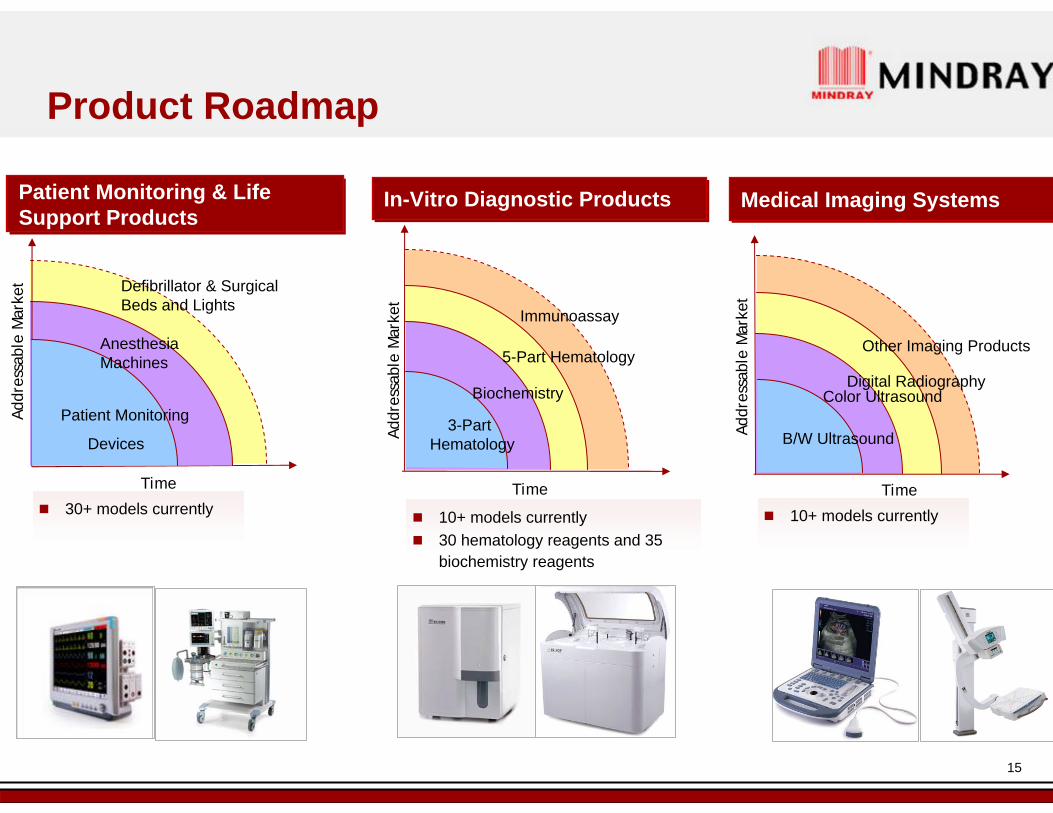

3-part Hematology

Patient Monitoring & Life Support ProductsPatient Monitoring & Life Support Products

In-Vitro Diagnostic ProductsIn-Vitro Diagnostic Products Medical Imaging SystemsMedical Imaging Systems

Time

Immunoassay

Addr

essa

ble

Mar

ket

3-Part Hematology

5-Part Hematology

Biochemistry

Addr

essa

ble

Mar

ket

B/W Ultrasound

Digital Radiography

Time

Other Imaging Products

Color UltrasoundPatient Monitoring

Devices

Anesthesia Machines

Addr

essa

ble

Mar

ket Defibrillator & Surgical

Beds and Lights

Time

30+ models currently 10+ models currently30 hematology reagents and 35 biochemistry reagents

10+ models currently

Product Roadmap

16

Leading Market Position in China

Strong Brand Recognition Brand loyalty enjoyed among domestic hospitals across ChinaHigh-quality products and customer support services

Extensive Sales Network900 sales and service staff in 29 sales and sales support offices900 exclusive distributors

Competitive Price to Performance Ratio

Around 30% discount vs. international players20% premium vs. domestic players

Sales Force ManagementLow turnover rateEffective incentive scheme

Strong Brand Recognition Brand loyalty enjoyed among domestic hospitals across ChinaHigh-quality products and customer support services

Extensive Sales Network900 sales and service staff in 29 sales and sales support offices900 exclusive distributors

Competitive Price to Performance Ratio

Around 30% discount vs. international players20% premium vs. domestic players

Sales Force ManagementLow turnover rateEffective incentive scheme

Urumchi

Shenyang

DalianBeijing

QingdaoJinan

Taiyuan

Zhengzhou

Xi’an

Lanzhou

ShanghaiNanjing

Hangzhou

Fuzhou

HefeiWuhan

NanchangChangsha

Guangzhou

Hong Kong

ShenzhenNanning

Chengdu

Chongqing

Kunming

Guiyang

Changchun

Shijiazhuang

Other11.9%

North Am erica

6.8%

Europe18.4%

Other Asia

13.5%

China49.4%

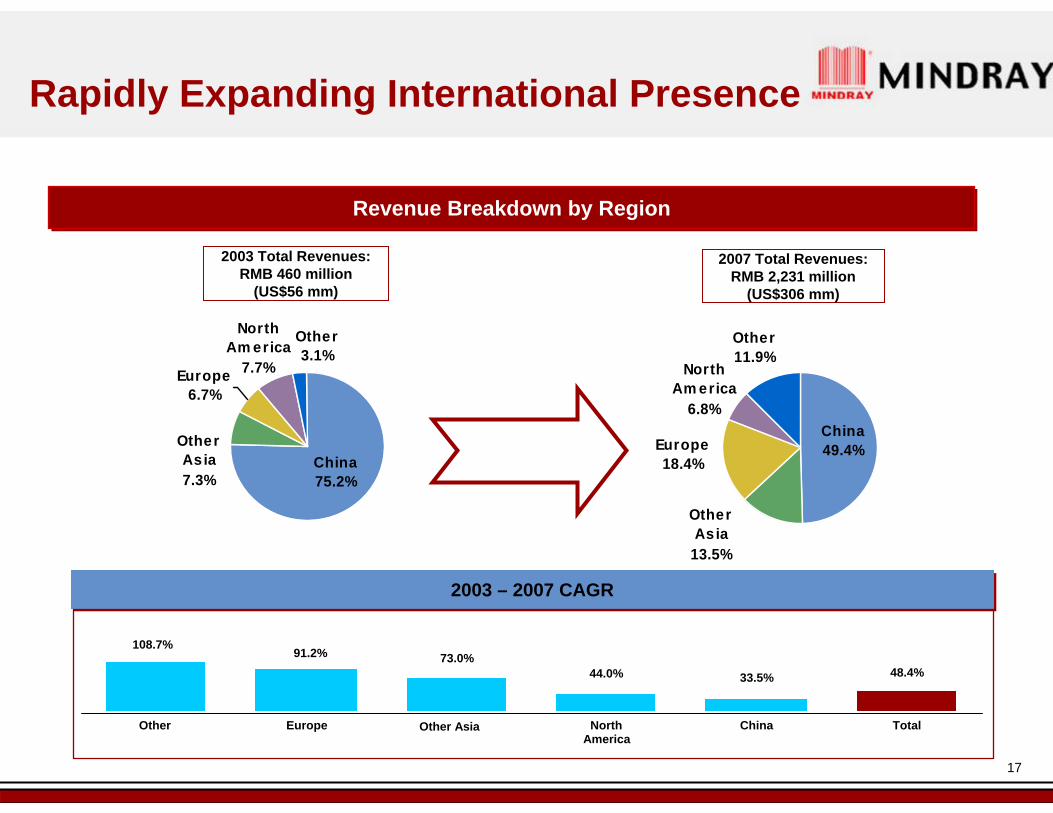

17

Revenue Breakdown by RegionRevenue Breakdown by Region

2003 Total Revenues: RMB 460 million

(US$56 mm)

2007 Total Revenues: RMB 2,231 million

(US$306 mm)

Rapidly Expanding International Presence

Other3.1%

North Am erica

7.7%Europe6.7%

Other Asia7.3%

China75.2%

2003 – 2007 CAGR2003 – 2007 CAGR

America

91.2% 73.0%44.0% 33.5% 48.4%

Other Asia EuropeOther North China Total

108.7%

18

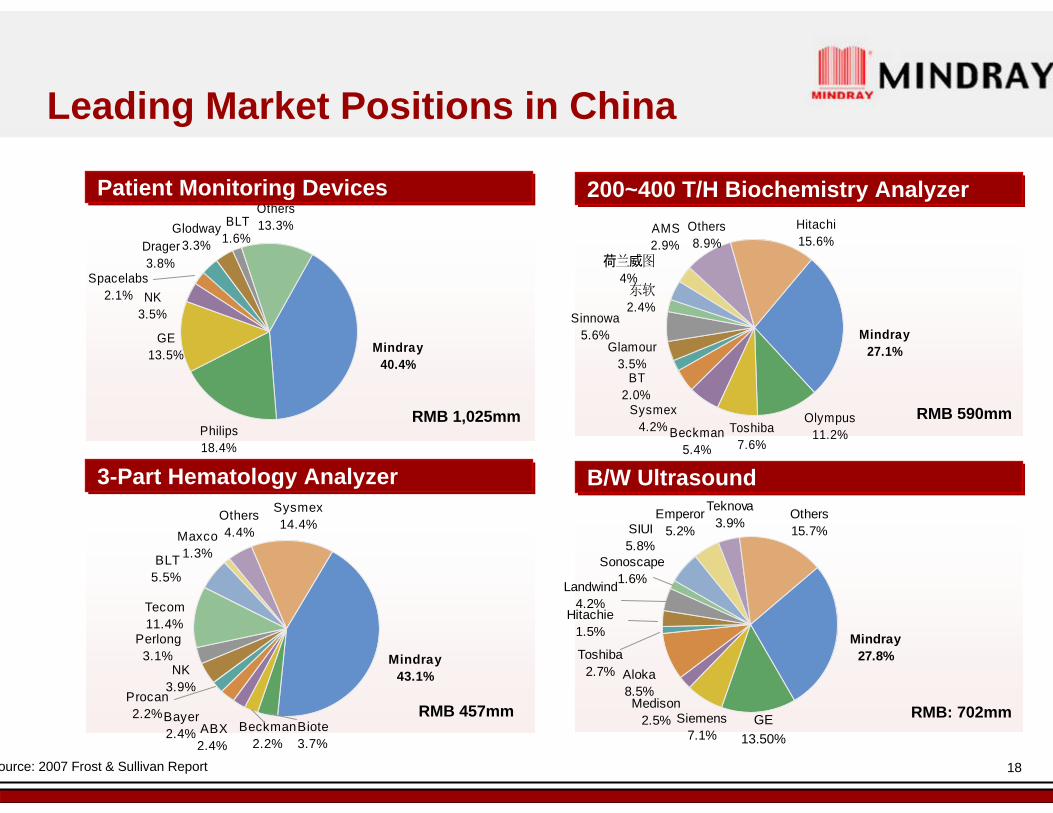

Others15.7%

Teknova3.9%

Emperor5.2%

Aloka8.5%

Hitachie1.5%

SIUI5.8%

Landwind4.2%

Sonoscape1.6%

Toshiba2.7%

Siemens7.1%

Medison2.5%

Mindray27.8%

Sysmex14.4%

Maxco1.3%

Others4.4%

Bayer2.4%

Procan2.2%

BLT5.5%

Perlong3.1%

Tecom11.4%

NK3.9%

Beckman2.2%

ABX2.4%

Biote3.7%

Mindray43.1%

Mindray27.1%

Olympus11.2%Beckman

5.4%

Toshiba7.6%

Glamour3.5%

东软2.4%

Sinnowa5.6%

荷 威兰 图4%

BT 2.0%

Sysmex4.2%

Others8.9%

AMS2.9%

Hitachi15.6%

Leading Market Positions in China

Spacelabs2.1%

Drager3.8%

BLT1.6%

Others13.3%Glodway

3.3%

GE 13.5%

NK3.5%

Philips18.4%

Mindray40.4%

RMB 1,025mm

RMB 457mm

Patient Monitoring DevicesPatient Monitoring Devices

3-Part Hematology Analyzer3-Part Hematology Analyzer

200~400 T/H Biochemistry Analyzer200~400 T/H Biochemistry Analyzer

RMB 590mm

ource: 2007 Frost & Sullivan Report

RMB: 702mm

B/W UltrasoundB/W Ultrasound

GE13.50%

19

GE29.8%

Others4.8%Tearson

0.7%

SonoSite0.4%

Esaote3.5%SIUI

0.3%SonoScape

1.7%

Toshiba5.3% Hitachi

3.1%Aloka6.7%

Medison5.0%

Philips18.3%

Mindray4.8%

Bayer4.0%

NK8.9%

Sysmex33.8%

Others4.6%

Beckman18.2%ABX

7.9%

Abbott8.6%

Mindray13.9%

New Growth Areas in China

Mindray4.0%

Penlon2.1%

GE(欧美达)29.2%

Kontron2.5%

长峰8.9%

Kaitai3.4%

Yi'an4.3%

Others2.6%

Zhongyuan14.5% 英国百斯

0.9%

Drager24.2%

RMB 307mm

5-Part Hematology Analyzer5-Part Hematology Analyzer

ource: 2007 Frost & Sullivan Report

RMB 2,562mm

Color UltrasoundColor Ultrasound

RMB 654mm

Anesthesia MachineAnesthesia Machine Biochemistry AnalyzerBiochemistry AnalyzerHitachi16.5%

Others10.1%AMS

1.6%Caihong

2.5%Rayto1.5%

春光机长1.3%

Vital Scientific2.4%

Neusoft1.8%

Bayer1.5%

Sysmex2.1%Roche

5.8%

Sinnowa4.1%

BT 1.0%

Glamour3.8%

Abbott2.0%

Toshiba6.5%

Beckman9.7%

Olympus12.1%

Mindray14.8%

RMB 1,182mm

Siemens

15.50%