Mintzberg’s Emergent and Deliberate Strategies: Tracking Alcan’s Activities in

Europe, 1928–2007

The management scholar Henry Mintzberg has situated com-pany strategies on a continuum that ranges from those that are the result of deliberate internal decisions, on one extreme, to those that emerge largely as a response to external forces, on the other. This framework is applied to the strategies of the Canadian aluminum producer Alcan, in Europe, from its ori-gins as a spin-off from Alcoa, in 1928, until its acquisition by Rio Tinto, in 2007. Throughout this period, the company grad-ually moved from emergent to more deliberate strategies, al-though external forces continued to infl uence its decisions. The increasing centralization of Alcan’s organizational structure paralleled its shift toward reliance on deliberate strategies.

he Canadian company that eventually became known as Alcan (Aluminum Company of Canada) emerged as a major player in the

European aluminum industry during the interwar period.1 In 1902, the Pittsburgh Reduction Company (renamed Aluminum Company of Amer-ica, or Alcoa, in 1907) established a smelter in Québec, offi cially char-tering a subsidiary there under the name Northern Aluminum Com-pany Limited. In 1928, Alcoa moved most of the activities it had been

MATTHIAS KIPPING is professor of strategic management and chair in business history at the Schulich School of Business, York University, Toronto, Canada. LUDOVIC CAILLUET is associate professor of strategy at the Graduate School of Management (IAE), University of Toulouse, France.

We gratefully acknowledge the France–Canada Research Foundation, which supported our research for this article. Earlier versions were presented at the International Conference on Business History at Waseda University in Tokyo, on January 26 and 27, 2008, and at the Wilson Seminar at McMaster University in Hamilton, Ontario, on October 15, 2009. We thank the participants for their helpful comments. We are also indebted to two anonymous reviewers for this journal.

1 For simplicity, we will refer to the company as Alcan, even though it was formally known as Aluminium Limited until 1966; Douglas C. Campbell, Global Mission: The Story of Alcan, vols. 1–3 (Montréal, 1990), 1: 38.

Matthias Kipping and Ludovic Cailluet / 80

conducting outside the United States into the Canadian company and made it legally independent.2 Alcan was thus “born global”—not by de-sire or design, but out of necessity, following the radical divestment decision by its U.S. parent.3 Most of the overseas activities Alcan in-herited from Alcoa were located in Europe, where the company also exported a substantial share of the aluminum ingots it produced in Canada. Over subsequent decades, Alcan considerably expanded its Eu-ropean activities through a series of important investments and acqui-sitions, until it was itself taken over by the Anglo-Australian metals giant Rio Tinto in 2007.

In this overview, we assess whether the fi rm’s developments were the result of a “deliberate” or an “emergent” strategy—a distinction fi rst introduced by the management scholar Henry Mintzberg, who tracked the strategies of several companies “across decades in their histo-ries.”4 Mintzberg applies the term “deliberate” to strategies that are fi rst formulated internally and then implemented, contrasting them to “emergent” approaches that form gradually through a learning process, usually in response to external forces. He also suggests that, ex-post facto, many strategies appear or are rationalized to have been devised deliberately, whereas they were actually the result of “actions simply converg[ing] into patterns.” These two types of strategy formation are not mutually exclusive but, rather, form the opposite ends of a contin-uum. Ultimately, according to Mintzberg, “reality falls between the two,” and “some of the most effective strategies” combine “deliberation and control with fl exibility and organizational learning.” Effective con-trol, he suggests, can take the form of either an “umbrella strategy” or a “process strategy,” which are both “partly deliberate, partly emergent.”5 These are the two ideal types located in the middle of the continuum: toward the deliberate end, one fi nds planned, entrepreneurial, and ide-ological strategies; toward the other—emergent—end, one fi nds uncon-nected, consensus, and imposed strategies.6

2 For the origins of Alcoa, its original investment in Canada, and the 1928 divestment, see George David Smith, From Monopoly to Competition: The Transformations of Alcoa, 1888–1986 (Cambridge, Mass., 1988); and Donald H. Wallace, Market Control in the Aluminum Industry (Cambridge, Mass., 1937), 74–76.

3 This term was originally coined by Michael W. Rennie, in “Born Global,” McKinsey Quarterly 4 (1993): 45–52.

4 Henry Mintzberg, “Crafting Strategy,” in Mintzberg on Management: Inside Our Strange World of Organizations (New York, 1989), 25–42, quote on p. 25. These case stud-ies were reprinted with a new introduction and conclusion in Henry Mintzberg, ed., Tracking Strategies: Toward a General Theory (Oxford, 2007).

5 Mintzberg, “Crafting Strategy,” 31, 34.6 See, for details, Henry Mintzberg and James A. Waters, “Of Strategies, Deliberate and

Emergent,” Strategic Management Journal 6, no. 3 (1985): 257–72; for a summary, see Mintzberg, ed., Tracking Strategies, 7–8.

Mintzberg’s Emergent and Deliberate Strategies / 81

Drawing from a wide variety of original and secondary sources, we examine the characteristics of Alcan’s European strategies and trace their development along the deliberate–emergent continuum. We were fortunate to have been granted access to archival material regarding Al-can’s activities in Britain, the fi rm’s major European market for most of its history.7 We also consulted the company’s in-house magazine, from its initial publication in 1957 up to 2008.8 In addition, we examined the company’s annual reports.9 In certain cases, we perused the archives of two of the company’s major European-based competitors, the British Aluminium Company (BACo) and Pechiney in France, which were both eventually acquired by Alcan. By combining these original sources with the existing literature on the evolution of the aluminum industry, we gained a comprehensive picture of Alcan’s European strategies as they unfolded over the past eight decades.

In preparing this article, one of our goals was to expand the histori-ography of the aluminum industry, which features certain topics, such as the part played by governments, the roles of cartels and of innova-tion, and the contributions of specifi c companies.10 Alcan itself has been examined in a number of studies, both for its social and economic role in Québec and as a case in studies of regulation and (international) com-petition.11 Most of these studies have relied on secondary sources, rather than drawing from Alcan’s internal corporate records, which have re-mained closed to most outside researchers. The sole archive-based com-pany history was written in the mid-1980s by a former public-relations executive.12 While the multiple volumes he compiled are a valuable re-source for any historian of Alcan, they have certain limitations: they

7 We are grateful to Nicole Hébert from the Business Information Center at Rio Tinto Al-can in Montréal [hereafter, RTA] for granting us access and helping to identify the relevant documents.

8 Called Compass until 2000, it underwent several name changes thereafter, most re-cently to Our World.

9 Most of these are available at http://digital.library.mcgill.ca/hrcorpreports/ (retrieved on 30 July 2009). The missing ones were made available to us by Laura Linard and Christine Riggle from the Historical Collection of the Baker Library at Harvard Business School, whose help is gratefully acknowledged.

10 E.g., Wallace, Market Control; Merton J. Peck, Competition in the Aluminum Industry, 1945–1958 (Cambridge, Mass., 1961); Margaret B. W. Graham and Bettye H. Pruitt, R & D for Industry: A Century of Technical Innovation at Alcoa (Cambridge, 1990); Smith, From Monopoly to Competition; Florence Hachez-Leroy, L’Aluminium Français: L’invention d’un marché, 1911–1983 (Paris, 1999).

11 E.g., Carmine Nappi, “Structural Changes in the International Aluminum Industry: The Situation in Canada,” HEC Montréal, discussion paper, IEA 34-02 (1984); Isaiah A. Litvak and Christopher J. Maule, “Assessing Industry Concentration: The Case of Aluminum,” Jour-nal of International Business Studies 15, no. 1 (1984): 97–104; Yves Plourde, “L’infl uence de la division des activités d’Alcoa de 1928 sur l’internationalisation d’Alcan et d’Alcoa,” unpub-lished masters thesis, HEC Montréal, 2007.

12 Campbell, Global Mission.

Matthias Kipping and Ludovic Cailluet / 82

refl ect the company ideology at the time of writing; they do not de-scribe more recent events; and, most critically, they do not cover all the aspects of the company’s formulation of strategy, especially the part played by its subsidiaries in that process. Nor do they address its rela-tions with competitors and governments.13 By expanding the temporal scope and including internal as well as external factors, we offer a unique perspective on the historiography of Alcan. At the same time, we hope to show how the deliberate–emergent continuum can be ap-plied fruitfully to a long-term historical study. Last, but not least, we hope to contribute to the development of that framework by examining a resource-based business—a type that was not represented in the cases studied by Mintzberg and his team.

The article is divided into fi ve main sections. The fi rst provides the context for examining the company’s strategy by outlining the character-istics of the industry and surveying Alcan’s origins and corporate culture. The next three chronologically organized sections recount the compa-ny’s European strategy. In conclusion, we offer a general assessment of the company’s strategy during its eighty-year existence and speculate on the broader implications of the fi rm’s actions, for both the history of the aluminum industry and the formulation of strategy.

Characteristics of the Aluminum Industry and Alcan

Technological Constraints. The operations of the aluminum in-dustry can be divided into fi ve main stages. (See Table 1.) The fi rst three, which date back to the late nineteenth century, form the basis of the technology today and are specifi c to the industry: the mining of bauxite ores; the Bayer process for turning bauxite into aluminum oxide, com-monly referred to as alumina; and the Hall–Héroult process for pro-ducing aluminum ingots through the electrolysis of alumina dissolved in molten cryolite.14 The fabrication stage, in contrast, has more in com-mon with general metallurgy. It occurs in two steps involving different, increasingly fi ne, treatments of the primary metal. In the fi nal stage, the resulting fabricated aluminum is transformed into a wide range of end products, including packaging materials, cooking utensils, and air-plane parts.

Cost issues constrained location decisions for the production of

13 The same is true for Pierre Lanthier, “Alcan from 1945 to 1975: The Uncertain Road to Maturity,” Cahiers d’histoire de l’aluminium, special issue 1 (2003): 47–72, who relies heav-ily on Campbell. See also Bradford Barham, “Strategic Capacity Investments and the Alcoa-Alcan Monopoly, 1888–1945,” in States, Firms, and Raw Materials, ed. Bradford Barham, Stephen G. Bunker, and Denis O’Hearn (Madison, 1994), 69–110.

14 Paul Morel, Histoire technique de la production de l’aluminium (Grenoble, 1992).

Mintzberg’s Emergent and Deliberate Strategies / 83

aluminum. Thus, proximity to sources of bauxite ores for the initial transformation into alumina and availability of cheap sources of elec-tric power for the production of primary aluminum were critical.15 Can-ada’s “abundant, fi rm and generally inexpensive suppl[y] of hydroelec-tric power” was the main reason for Alcoa’s initial investment north of the border, a decision that constituted a lasting competitive advantage for Alcan—even after other sources of energy emerged.16 In general, gov-ernments of countries with bauxite ores and plentiful energy sources could support the growth of domestic or foreign aluminum producers by granting mining concessions and giving companies access to, or owner-ship of, power sources.

While, technically, it was not necessary to integrate all the stages of manufacture, historically, most major aluminum-producing companies became vertically integrated from the time of their inceptions.17 In terms of backward integration, their decision can be explained by the

Table 1Stages of Aluminum Production

Stage Products and Methods of Production

1. Bauxite Bauxite ore (open strip mined)2. Alumina Alumina (extracted from bauxite by chemical

processes)3. Ingot fabricated products Reduced from alumina by electrolytic process,

i.e., primary aluminum, or refi ned or remelted from scrap, i.e., secondary aluminum

4. Fabricated products: A. Semi-fabrications Reroll stock sheet (hot rolled)

Rod, bar, wire stock (hot rolled)Extrusion (heated aluminum forced through metal dies)Castings (foundry)Powder and pigmentForging (preheated metal is hammered between

shaped or fl at dies) B. Final fabrications 1. Sheet (cold rolled): plate (cold rolled), foil

(cold rolled)2. Wire/cable; rod and bar (cold rolled)3. Anodizing, organic coating

5. End product Wide range of durable manufactured products (from kitchenware to aircraft structures)

15 Ibid.16 Nappi, “Structural Changes,” 54.17 Alfred D. Chandler, Jr., Scale and Scope: The Dynamics of Industrial Capitalism (Cam-

crucial role of raw-material inputs: namely, the scarcity of high-grade bauxite deposits. In terms of forward integration, aluminum producers initially had to work hard to fi nd applications for the new material and to convince potential users of its benefi ts.18 Once some applications had become strategic, as occurred in the production of aircraft and other transportation equipment, the companies tended to remain integrated in order to extract economic rents. Western governments, beginning in the 1930s, usually opted for long-term supply contracts and stockpil-ing in order to address their strategic needs. Communist countries—particularly after World War II—and most developing nations after the 1960s went the route of state ownership. As a result, by 1980, 46 per-cent of global aluminum-production capacity was under government control.19 Government supply contracts and stockpiling, as well as the threat of cheap imports from the Communist countries, were important infl uences on Alcan’s European strategy.

Industry Structure. These technical characteristics had two ma-jor consequences for the industry structure. First, the companies were international from the outset. In the early twentieth century, known de-posits of bauxite ores were restricted to a few countries and the vast amounts of energy required to produce primary aluminum were techni-cally diffi cult, if not impossible, to transmit over long distances. Most producers therefore had to look for at least one, sometimes both, of these crucial resources outside their home country. In their search for energy, companies sought out countries, such as Canada or Norway, which had an abundance of hydroelectric power. In seeking bauxite, in-dustry participants rushed to secure deposits, particularly in France, since the ability to control this substance “had considerable infl uence in barring new entrants to the producing industry.”20 The need for econo-mies of scale in the production of aluminum was an even more daunt-ing entry barrier, leading to a high level of concentration and often re-sulting in the survival of only a single producer in most countries.21

This degree of concentration in turn facilitated the rise of inter-national cartels, which were formed in order to protect the participants’ home markets while fi xing prices and/or quotas for export markets.22

18 Peck, Competition in the Aluminum Industry, 120.19 OECD, Industrie de l’aluminium: Aspects énergétiques et changements structurels

(Paris, 1983), 118.20 Winifred Lewis, The Light Metals Industry (London, 1949), 10.21 Chandler, Scale and Scope, 124.22 For this and the following observations, see George W. Stocking and Myron W. Wat-

kins, “The Aluminum Alliance,” in Cartels in Action: Case Studies in International Business Diplomacy (New York, 1946), 216–73; and Florence Hachez-Leroy, “Stratégie et cartels in-ternationaux, 1901–1981,” in Industrialisation et sociétés en Europe occidentale de la fi n du XIXè siècle à nos jours: L’Âge de l’aluminium, ed. Ivan Grinberg and Florence Hachez-Leroy (Paris, 1997), 164–74.

Mintzberg’s Emergent and Deliberate Strategies / 85

An international agreement was fi rst reached in 1896 between Alcoa’s predecessor, the Pittsburgh Reduction Company, and the Swiss-based, but largely German-owned, Aluminium Industrie A.G. (AIAG). In 1901, Alcoa and the four major European producers established a more com-prehensive cartel, the Aluminium Association. The U.S. company left the Association in 1906 to avoid antitrust problems, but continued to participate through its Canadian subsidiary. After World War I, the European and North American producers acted through “conferences,” meeting to fi x prices and set territorial limits. A fully fl edged cartel was re-established in 1926, but was initially limited to European-based companies.

During the fi rst half of the twentieth century, European and U.S. governments took different approaches toward cartels. While they were a favored system of market governance in Europe before 1945, in the United States growing antitrust sentiment and legislation made it all but impossible to form domestic cartels.23 As early as 1912, the Anti-trust Division of the U.S. Justice Department investigated Alcoa, citing its domestic monopoly position and anticompetitive practices.24 As part of a consent decree, Alcoa agreed to abandon most of these practices and to remain outside any international cartel agreements. After World War II, attitudes and policies toward cartels and concentrations of eco-nomic power also changed in Europe. Laws and regulations prohibiting cartels and subjecting mergers and acquisitions to public approval were fi rst introduced within the countries of the nascent European Union, and were then gradually incorporated into law in most European coun-tries.25 The cartel regimes that prevailed in the pre–World War II pe-riod, and their demise after 1945, had a strong infl uence on the struc-ture of the aluminum industry and on Alcan’s European activities.

The Company. While under Alcoa’s ownership, Northern Alumi-num’s only overseas activities were in the United Kingdom, where the company established a sales subsidiary as early as 1909; in 1926, it ac-quired a 50 percent stake in F. H. Adams Ltd., a nonferrous-metals foundry located in Birmingham.26 The situation changed dramatically in 1928. On May 31, Alcoa chartered a Canadian company called Alumi-num Limited, to which it transferred the majority of its foreign proper-ties in exchange for the latter’s common stock. Antitrust considerations

23 Jeffrey Fear, “Cartels,” in The Oxford Handbook of Business History, ed. Geoffrey Jones and Jonathan Zeitlin (Oxford, 2007), ch. 12; see also Harm G. Schröter, “Cartelization and Decartelization in Europe, 1870–1995: Rise and Decline of an Economic Institution,” Journal of European Economic History 25, no. 1 (1996): 129–53.

24 Stocking and Watkins, “The Aluminum Alliance,” 225, 239.25 Hervé Dumez and Alain Jeunemaître, La concurrence en Europe (Paris, 1991).26 Campbell, Global Mission, vol. 1, 180.

Matthias Kipping and Ludovic Cailluet / 86

seem to have motivated this move. By creating a formally independent entity outside the United States, Alcoa hoped to escape legal action. Ap-parently, the idea was that Aluminum Limited would represent and de-fend Alcoa’s interests in the international arena, notably vis-à-vis the European cartel.27

Over the next three decades, ownership in the two companies re-mained integrated. Alcoa’s founding families (the Mellons, Davises, and Hunts) continued to hold a majority stake in Alcan until 1950, when a U.S. judge ordered the large group of U.S. shareholders to dis-pose of their interests in one of the two companies within a ten-year pe-riod.28 Subsequently, the number of shareholders in Alcan increased signifi cantly—from 3,559 to 28,000 within six years—and, by 1972, Ca-nadian investors controlled 55 percent of the company’s common stock.29 Joint family control was even more important than ownership. Thus, Alcoa’s president and chairman, Arthur V. Davis, who was also the larg-est individual shareholder in both companies, appointed his younger brother Edward K. Davis, who had previously been the general sales manager at Alcoa, as president and CEO of the Canadian company. In 1947, Edward handed control over to his son Nathanael, who stayed at the helm of Alcan until 1979 and remained chairman of the board of di-rectors until 1986.30 Edward K. Davis actually ran the company from Boston, and Nathanael did not move his offi ce to Montréal until the end of the 1950s.

The two generations of Davises who led Alcan after it became inde-pendent strongly imbued the company with their own philosophy. In a speech delivered on the occasion of Nathanael Davis’s retirement in 1986, his successor, David Culver, mentioned “two constant threads—Alcan’s internationalism and Alcan’s values.” Regarding the former, he referred to the “vision to lead and grow an international organization, at a time when the idea of the multinational corporation, as we know it now, had scarcely been born”; regarding the latter, he cited “a blend of integrity and understanding in its commercial dealings, with its em-ployees, with host communities around the world.” This vision of Alcan also appears in the offi cial company history written at that time.31 Ac-cording to the author, in organizational terms, Nathanael Davis viewed

27 Stocking and Watkins, “The Aluminum Alliance,” 255–57; Wallace, Market Control, 369–70; Smith, From Monopoly to Competition, 321.

28 Stocking and Watkins, “The Aluminum Alliance,” 257n100. See also United States v. Aluminium Co. of America et al., 148 F.2d 416 (2nd Cir. 1945).

29 Smith, From Monopoly to Competition, 271–73.30 For this and the following, see Anon., “The Davis Legacy—It’s Quite a Different Com-

pany,” Compass 23, no. 6 (Sept. 1979): 9–12; Duncan C. Campbell, “Nathanael V. Davis Re-tires,” Compass 30, no. 2 (1986): 6–11.

31 Campbell, Global Mission.

Mintzberg’s Emergent and Deliberate Strategies / 87

Alcan as “a family of interdependent operations,” resembling a holding company and managed in a decentralized, even distributed, way.

However, as we will demonstrate, the fi rm gradually became more centralized over time, while the “family ambiance” began to disintegrate in the mid-1980s as the founders’ infl uence waned and top managers were replaced more frequently.32

In the remainder of the article, we will examine how the changes in organizational structure and corporate culture combined with the evolv-ing competitive and regulatory environment to affect the company’s European strategies.

Learning to Be an International Player: 1930s to 1950s

During this period, the pressing question for Alcan, once it became independent, was whether it would be able to shape its own strategy or whether it would be “organized only as a creature of ‘Alcoa.’ ”33 The close coordination between the companies became apparent when the inter-national aluminum cartel was established in 1931. The negotiations were initiated by Alcoa’s Arthur V. Davis during a trip he made to Europe in October 1930 and were subsequently conducted by Alcan’s Edward K. Davis, in close consultation with his brother, leading to the signing of an agreement on July 3, 1931. The cartel was established as a Swiss cor-poration, the Alliance Aluminium Compagnie (AAC), in October 1931. Alcoa remained formally outside the cartel, relying on Alcan to repre-sent its interests. Members were given shares that refl ected their global production capacities, which translated into voting rights and shares of the cartel’s production volume. Alcan received 29 percent of the shares. Moreover, the Alliance guaranteed a certain minimum price by buying up any unsold quota shares at that price.34

The often drawn conclusion that Alcan was Alcoa’s “creature” is less obvious, and even questionable, in terms of its industrial activities in Europe. An internal report dated August 1933 provides an overview of the company’s involvement in the upstream stages of the European market fi ve years after its formal independence.35 The report shows that Alcan’s investments in bauxite mining and alumina production were

32 So states Wharton professor Howard Perlmutter, based on interviews at Alcan’s head offi ce: “Corporate Culture in Transition,” Compass 28, no. 3 (May-June 1984): 9–10.

33 United States v. Aluminium Co. of America et al. 148 F.2d 416 (2nd Cir. 1945). This opinion is widely shared in the academic literature. See, e.g., Smith, From Monopoly to Com-petition, 147; Stocking and Watkins, “The Aluminum Alliance,” 256–58.

more important than its reduction capacities: it owned mines in France, Italy, and Yugoslavia, as well as an alumina plant in Italy, all of which were part of the Alcoa heritage.36 In terms of aluminum production, Alcan only held stakes in a few smaller smelters in Italy, Norway, and Wales, which was not surprising, given the company’s interest in selling ingots from its low-cost Canadian operations.

More signifi cant is the fact that Alcan had started to move beyond preserving the Alcoa heritage. Thus, the company almost instantly sold its share in a smelter in the Spanish Pyrenees, which Alcoa had built and operated jointly with the French producer Pechiney, in exchange for the remaining 50 percent of Società dell’Alluminio Italiana (S.A.I.), which operated a small smelter north of Turin. This deal allowed Alcan to continue imports of ingots from Canada into Spain, which Pechiney wanted to restrict.37

But the most important departure from the Alcoa heritage occurred in the fabricating stage that Alcan began to develop during the 1930s and 1940s. The shift was a logical step, since it freed the company from the cartel discipline. In 1930, the Canadian company bought two small German businesses that made cast and sheet aluminum.38 Alcan also moved downstream in France, where it had inherited the Société des Bauxites du Midi (SBM). André Henry-Couannier, a personal friend of Edward K. Davis, had established SBM on behalf of Alcoa in 1912, in order to purchase mining rights in southern and eastern Europe. Henry-Couannier remained at its helm and expanded the company’s mining interests in French colonial Africa. More critically, he developed a keen interest in new applications, including the manufacture of aircraft.39 By making him a company vice president and board member of all its fully or partially owned European subsidiaries, Alcan ensured cohesion within its decentralized holding structure.40

But, after 1928, Alcan expanded most aggressively in the United Kingdom. This is not surprising, as Canada had instituted tariff pref-erences with “sister countries of the [British] Empire” since the late nineteenth century. Trade with these countries became even more im-portant after the United States adopted the protective Smoot-Hawley tariff in 1930. In the summer of 1932, Canada’s prime minister, R. B. Bennett, organized the Imperial Economic Conference in Ottawa, where

36 For the following, see Stocking and Watkins, “The Aluminum Alliance,” 248–51.37 René Bonfi ls, “Pechiney en Espagne, 1925–1985,” Cahiers d’histoire de l’aluminium,

nos. 38/39 (2007): 77–92.38 Anon., “Alcan Germany: Rolling with the Times,” Compass 30, no. 4 (1986): 3–9, here 3.39 Wallace, Market Control, 71; for more details, see Anon., Mémoire d’Alcan en France,

1912–1992 (Paris, 1992).40 For the former, see the annual report for 1930; for the latter, “European Aluminium.”

Mintzberg’s Emergent and Deliberate Strategies / 89

participants agreed upon a series of new preferences.41 Alcan’s annual report for that year stressed the benefi ts of these agreements: “They give our products, made within the British Empire either free entry into these markets or preferential rates of duty over similar products of non-E mpire countries,” an arrangement that was very important, since “nearly 70 percent of our investments are within the British Empire.” Already before the outbreak of World War II, the United Kingdom had become the single most important market for Canadian ingots, absorb-ing 38 percent of its output in 1939.

During the interwar period, Alcan invested in downstream activi-ties in the United Kingdom in order to take advantage of the growth potential in the automotive and aircraft industries. In the early 1930s, it built an extrusion unit and a rolling mill for the production of alu-minum sheet in Banbury (Oxfordshire), where it also opened a re-search laboratory in 1938. In 1932, it took complete control of F. H. Adams Ltd., the Birmingham foundry over which it had acquired par-tial control in 1926. Finally, but critically, London became Alcan’s global commercial hub through its subsidiary Aluminium Union Ltd. This organization dealt with all trading issues in Europe, as well as with the fi nancing of overseas sales, including billing in more than eighty currencies.42

Although Alcan originally based its operations on a policy of pro-gressing along a similar path—downstream—in all its European loca-tions, the outbreak of World War II caused it to evolve in divergent di-rections. In occupied France, its primary interest was preservation. Alcan escaped German expropriation by founding a Swiss corporation, called Stand S.A., in Geneva and transferring all its assets there. In the United Kingdom, in contrast, the war provided an opportunity for fur-ther expansion. The British government signed a guaranteed-supply agreement with Alcan and offered the company preferential loans to fund capacity expansion. In exchange, the U.K. government became the exclusive importer and distributor of Canadian ingots in the United Kingdom until the end of wartime controls in 1953.43 The British govern-ment not only relied on Alcan to supply primary aluminum; it also asked

41 Michael Bliss, Northern Enterprise: Five Centuries of Canadian Business (Toronto, 1987), 301, 414–15, 423.

42 British Alcan Extrusions Limited, “60 Years at Banbury, 1931–1991,” 00195-20, RTA; L. Fletcher, “History of the Birmingham Works,” 16 Jan. 1947, 00161-08, no. 28, RTA. See also Campbell, Global Mission, vol. 1, 179–88.

43 See the company’s annual report for 1953, and Andrew Perchard, “A Marriage of Mu-tual Convenience? The British Government and the U.K. Aluminium Industry in the Twentieth Century,” paper presented at the annual conference of the European Business History Asso-ciation, Bergen, 21–23 Aug. 2008.

Matthias Kipping and Ludovic Cailluet / 90

the company to build and operate on its behalf a giant rolling mill at Rogerstone, in South Wales, which started up in January 1940.44

Thus, during the fi rst two decades after it became formally inde-pendent, Alcan seems to have had little room to maneuver, hemmed in as it was by the expectations of its former parent Alcoa, on the one hand, and by the strict discipline of the international cartel, on the other. Within the Mintzberg framework, this would be considered a highly emergent “imposed strategy,” one in which “the environment dictate[d] patterns in actions either through direct impositions or through implic-itly preempting or bounding organizational choice.”45 This applied to the upstream stages of production, which were the most important at the time. Downstream, the company had more freedom to act, and many European subsidiaries “naturally converge[d] on the same theme, or pat-tern” by developing activities that led to an emergent “consensus strat-egy.” During the war, the forced separation of markets turned these ac-tivities into “unconnected strategies.”46 After 1945, Alcan faced a very different environment, in which, although market liberalization opened up new choices, government policies and changes in energy prices in-troduced other types of constraints.

From Ingot Supplier to Leading Fabricator: The Midcentury through the 1970s

After World War II, and especially after the mid-1950s, Alcan faced signifi cant challenges in its global and European operations. The com-pany’s earlier competitive advantage, based on cheap hydroelectric power, eroded as a result of the reduction in government stockpiling of aluminum, and it began to face much stronger competition. The end of the international cartel removed the protections the fi rm had once en-joyed, and European economic integration created new growth oppor-tunities. Alcan responded by moving more decisively downstream, and it eventually became the largest aluminum fabricator in Europe. It also expanded production of alumina and aluminum ingots—although it sometimes did so in response to external factors rather than as a delib-erate choice.

Until 1955, hydroelectric power had provided 90 percent of the en-ergy used in Western countries to produce primary aluminum. Twenty years later, this share had decreased to 54 percent; the rest was sup-plied by coal, hydrocarbons, or nuclear energy. This evolution had a

44 Centre d’Études Industrielles (CEI-Genève), typed case study of Rogerstone West Works Sheet Mill, c.1930–1955, Alcan UK, UGD 347/23/1, University of Glasgow Archives.

45 Mintzberg, ed., Tracking Strategies, 8.46 Ibid. and Mintzberg and Waters, “Of Strategies,” 267.

Mintzberg’s Emergent and Deliberate Strategies / 91

signifi cant effect on Alcan, as its aluminum production had benefi ted from access to cheap energy sources in Canada.47 At the same time, the gradual nationalization of electricity in Québec in 1944 and 1963 re-duced Alcan’s control over power generation, forcing the company to rely increasingly on long-term supply contracts with the government-owned utility, which were granted at favorable rates in exchange for employment guarantees.48 Moreover, during the 1960s and 1970s, metal from government-controlled producers, which also benefi ted from cheap or heavily subsidized energy costs, appeared on the market. As a result, Canada’s share of global ingot production decreased from 23 percent to 9 percent in these decades.49 Finally, from the late 1950s onward, West-ern governments slowed and eventually decreased their stockpiling, which had maintained the demand for aluminum after the end of World War II. In 1954, for instance, two-thirds of Alcan’s ingot deliveries had been made to the U.K. and U.S. governments.50

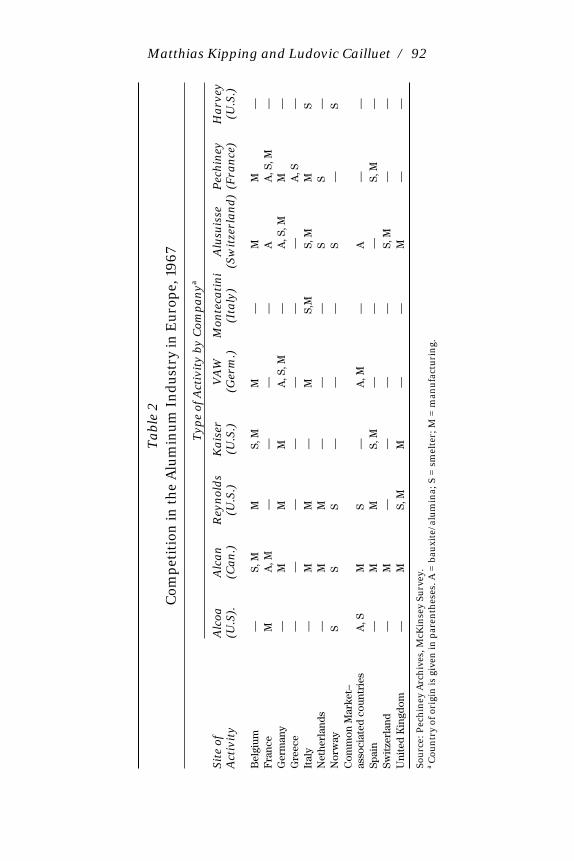

In subsequent years, Alcan not only lost this assured demand; it also faced more intense competition in Europe, from both local pro-ducers and outsiders, including the Soviet Union. As a result, in 1958, Alcan cut its price for the fi rst time in seventeen years.51 At the same time, U.S. producers expanded to Europe, focusing initially on the United Kingdom. In 1959, after a takeover battle with Alcoa, Reynolds took control of the British Aluminium Company (BACo), together with Birmingham-based Tube Investments, which held 51 percent of the ownership.52 Subsequently, Alcoa formed a joint venture with Imperial Chemical Industries. And, in late 1959, the third U.S. producer, Kaiser, together with the British fi rm Delta Metals Ltd., created a company called James Booth Aluminium Ltd.53 Table 2 shows the extent to which the U.S. producers had established an important presence in Europe by the end of the 1960s.

47 Lanthier, “Alcan from 1945 to 1975.”48 Christian Stoffaës, ed., Entre monopole et concurrence: La régulation de l’énergie en

perspective historique (Paris, 1994), 403–41. “Rio Tinto’s proposed acquisition of Alcan re-spects the agreements between Alcan and the Québec government,” press release, 7 Aug. 2007; http://www.mdeie.gouv.qc.ca/index.php?id=328&tx_ttnews[tt_news]=1345&tx_ttnews[backPid]=314&cHash=e4ce5697ce, accessed 27 Aug. 2009.

49 Nappi, “Structural Changes,” 9.50 Lanthier, “Alcan from 1945 to 1975,” 59–61.51 Anon., “Foreign Trade: Red Offensive,” Time, Mar. 1958; “Metals: Cut to Compete,”

Time, Apr. 1958.52 Stephen Hatch and Michael Fores, “The Struggle for British Aluminium,” Political

Quarterly 31, no. 4 (Oct. 1960): 477–87; see also Ludovic Cailluet, “The British Aluminium Industry, 1945–80s: Chronicles of a Death Foretold?” Accounting, Business and Financial History 11, no. 1 (2001): 79–97.

53 Anon., “Kaiser Acquires Interest in U.K. Firm,” Compass 4, no. 1 (Jan.–Feb. 1960): 7. The origins of James Booth go back to a small Birmingham-based rolling and extrusion com-pany, which Delta Metals acquired in 1957; see Anon., “A New Market Leader in Alcan Booth,” Compass 14, no. 5 (June 1970): 3–6, here 4–5.

Matthias Kipping and Ludovic Cailluet / 92

Ta

ble

2C

omp

etit

ion

in t

he

Alu

min

um

In

du

stry

in E

uro

pe,

19

67

Site

of

Act

ivit

y

Typ

e of

Act

ivit

y by

Com

pa

nya

Alc

oa

(U.S

).A

lca

n(C

an

.)R

eyn

old

s (U

.S.)

Ka

iser

(U.S

.)V

AW

(G

erm

.)M

onte

cati

ni

(Ita

ly)

Alu

suis

se(S

wit

zerl

an

d)

Pec

hin

ey

(Fra

nce

)H

arv

ey

(U.S

.)

Bel

gium

—S,

MM

S, M

M—

MM

—F

ranc

eM

A, M

——

——

AA

, S, M

—G

erm

any

—M

MM

A, S

, M—

A, S

, MM

—G

reec

e—

——

——

——

A, S

—It

aly

—M

M—

MS,

MS,

MM

SN

ethe

rlan

ds—

MM

——

—S

S—

Nor

way

SS

S—

——

S—

SC

omm

on M

arke

t–as

soci

ated

cou

ntri

es

A, S

MS

—A

, M—

A—

—Sp

ain

—M

MS,

M—

——

S, M

—Sw

itze

rlan

d—

M—

——

—S,

M—

—U

nite

d K

ingd

om—

MS,

MM

——

M—

—

Sou

rce:

Pec

hin

ey A

rch

ives

, McK

inse

y Su

rvey

.a

Cou

ntr

y of

ori

gin

is g

iven

in p

aren

thes

es. A

= b

auxi

te/a

lum

ina;

S =

sm

elte

r; M

= m

anu

fact

uri

ng.

Mintzberg’s Emergent and Deliberate Strategies / 93

The table also reveals that Alcan reacted to these challenges by fo-cusing even more intensely on downstream activities and by extending its geographic scope. The Canadians could now pursue their strategy more independently, since they were no longer closely tied to Alcoa. The shareholders of the two companies increasingly diverged, and the retire-ment of Arthur V. Davis in 1957, and his death in 1962, removed family bonds from the leadership equation.

To accommodate the forward integration strategy, the company changed its corporate structure, introducing a decentralized multi-divisional organization (or M-form)—following the advice of the m anagement-consulting fi rm McKinsey.54 According to Nathanael V. Davis, the decision to reorganize was propelled by the changing nature of the company, which was being transformed “from a basic metal man-ufacturer to increasingly, a leading producer of semi-fabricated and fi n-ished products.”55 The new structure gave the Montréal headquarters a better system of control, providing it with more information and over-sight than the previous holding-like structure had been equipped to do. Subsequently, McKinsey also introduced a product-based divisional structure in the company’s European operations. However, country man-agers remained powerful, since they retained control over the impor-tant extrusion activities and continued to “share with division managers responsibility for national companies.”56

Geographically, Alcan made signifi cant downstream investments in many of the countries that formed the European Economic Community in 1957. In Belgium, Alcan bought a controlling stake in an extrusion plant in 1962.57 In Italy, it gradually took over a family-owned com-pany in Milan that operated one of the largest rolling mills in the coun-try, acquiring full control in 1972.58 In France, the company built two extrusion units between 1959 and 1967 and invested in Technal, a com-pany that had developed and patented a modular building system.59 Alcan acquired 75 percent of Technal’s French operations in 1978, took full control of them in 1982, and, in 1984, bought 65 percent of Technal International, which held the worldwide patents for the company’s sys-tems.60 Finally, in Germany, Alcan merged its two fabricating units in

54 See Compass 11, no. 10 (Dec. 1967), entirely dedicated to the reorganization.55 Royal Commission on Corporate Concentration, Alcan Aluminium Limited: A Case

Study, Study no. 13 (1977): 109–10.56 Anon., “Reorganization in Europe,” Compass 13, no. 10 (Dec. 1969): 3.57 Anon., “Aluminium Limited Purchases Belgian Plant,” Compass 6, no. 1 (Jan. 1962):

13.58 Anon., “Alcanac Now Fully-Owned,” Compass 16, no. 6 (June 1972): 19.59 Anon., “New Company in France,” Compass 22, no. 5 (Sept.–Oct. 1978): 20; Campbell,

Global Mission, vol. 2, 504–6.60 Anon., “Technal: A Success Story to be Continued,” Compass 22, no. 6 (Nov.–Dec.

1962 and expanded the production capacity for castings and rolled products.61 Jointly with Germany’s leading producer, Vereinigte Alu-miniumwerke AG (VAW), it erected a new rolling mill at Norf, near Düsseldorf. After opening in 1968, the mill became the largest of its kind in Europe, with an initial capacity of 200,000 tons per year, which subsequently expanded to 700,000 tons of hot and 630,000 tons of cold rolled aluminum.62

Alcan invested even more heavily outside the nascent European Economic Community (EEC), particularly by expanding its upstream activities in Norway, Spain, and the United Kingdom. Closer analysis reveals, however, that the company was often drawn into these invest-ments and made them reluctantly, since it preferred importing ingots from the Canadian smelters. Norway was probably an exception, since Alcan had been present in the country since the interwar period.63 In January 1967, Alcan acquired a 50 percent stake in the previously fully state-owned Aardal og Sunndal Verk (ASV), which operated two smelt-ers with a combined capacity of 185,000 tons per annum. As part of the agreement, Alcan transferred its existing interests in Norway to ASV.64 Alcan probably took this step to develop a geographically closer supply base for its most important European market, the United Kingdom. In 1960, both countries had become members of the European Free Trade Area (EFTA), an alternative to the more thoroughly integrated EEC. A reorganization that occurred during the fi rst half of 1967 attributed the management of Alcan’s Scandinavian interests to a new British holding, Alcan Aluminium (U.K.) Ltd.65

In the United Kingdom itself, Alcan had continued to expand its downstream activities to take advantage of a growing market for con-sumer goods. After 1945, Alcan took ownership of the Rogerstone Works, which it had built and operated during the war on behalf of the British government. The company fi tted the factory with a new continu-ous strip mill, a move that, by 1950, turned it into “the largest rolling plant in Europe.”66 Subsequently, the British subsidiary embarked on a strategy of forward integration, acquiring, for example, several manu-facturers of aluminum foil and interests in wholesalers.67 The major

61 Anon., “Uphusen: Another Doorway to ECM,” Compass 6, no. 9 (Oct. 1962): 8–9.62 Anon., “Operations Begin at Norf,” Compass 12, no. 1 (Jan.–Feb. 1968): 19; Anon., “Al-

can Germany: Rolling with the Times,” Compass 30, no. 4 (1986): 3–9, here 6.63 “Aluminium Limited in Norway,” Apr. 1961, 00038-09, RTA.64 Anon., “Major Move in Norway,” Compass 11, no. 1 (Jan.–Feb. 1967): 3–4.65 Oliver Marriott, “Alcan Consolidates Capital Operations in U.K.,” Times (London), 19

June 1967, 00161-08, no. 6, RTA.66 CEI-Genève, typed case study of Rogerstone West Works Sheet Mill.67 Anon., “Alindustries Adds Foil in U.K.,” Compass 8, no. 9 (Nov. 1964): 6; Anon., “A

New Home for Polyfoil,” Compass 10, no. 7 (Sept. 1966): 8–9; Anon., “Alindustries Buys In-terest in Aston-Stedall,” Compass 9, no. 4 (May 1965): 15.

Mintzberg’s Emergent and Deliberate Strategies / 95

investment occurred in 1968, when the company acquired a 50 percent share of the large fabricator James Booth from Delta Metals; the other 50 percent remained in the hands of Kaiser.68 While the acquisition was in line with the fi rm’s overall downstream strategy, the decision is an-other example of Alcan’s opportunistic behavior. The managing direc-tor of the British subsidiary described how the deal was closed: “The possibility of Alcan buying 50 percent of James Booth was fi rst raised on Ilkley golf course at 4 p.m. and an answer had to be obtained by the following morning. By 3 o’clock in the morning, the answer ‘Yes’ came from Montreal.”69 In January 1970, Alcan agreed with Kaiser to inte-grate their downstream operations in the United Kingdom under the name Alcan Booth Industries Limited, making it the largest fabricator in the United Kingdom. Alcan initially held 75 percent of the shares, and it purchased the remainder in 1977.70

Although these acquisitions were intentional, during the same pe-riod Alcan was also constrained to invest in a new smelter in the United Kingdom.71 Until then, the country had covered most of its needs through imports, namely, from Canada. In 1966, Rio Tinto–Zinc (RTZ), a new-comer to the industry, proposed the construction of a domestic smelter in Wales that would be supplied by nuclear power. While initially reluc-tant to approve the plan because of the subsidies that might be involved, the U.K. government eventually latched on to the idea, because the smelter could improve the country’s balance of payments by reducing imports of ingots and increasing exports of fi nished aluminum prod-ucts. The government’s approval prompted both BACo and Alcan to argue that RTZ had little experience in aluminum production. In the fall of 1967, the British government announced its intention to support the construction of two smelters with a total capacity of 240,000 tons. Alcan had little interest in increasing its European ingot production, es-pecially after its recent expansion in Norway. Nor was the Norwegian government pleased with the U.K. proposal, as it had embarked on an

68 Alcan, “This is Alcan Booth,” Apr. 1970, 00161-08, no. 3, RTA.69 According to P. J. Elton, “Profi le of a Merchant Banker,” Compass, May 1977, 6–7;

can Aluminium (UK) Limited,” R. H. A. Forbes to J. G. Holloway, 24 Aug. 1981; 00161-08, no. 34, RTA.

71 For the following discussion, see, in detail, Perchard, “A Marriage of Mutual Conve-nience?”; Niall G. MacKenzie, “Be Careful What You Wish For: Comparative Advantage and the Wilson Smelters Project, 1967–82,” paper presented at the annual conference of the Eu-ropean Business History Association, Bergen, 21–23 Aug. 2008; and, from the perspective of Alcan, Ludovic Cailluet and Matthias Kipping, “Strategizing in a Complex Environment: Business, Government and the Lynemouth Aluminium Smelter, 1965–1973,” paper presented at the 29th annual conference of the Strategic Management Society, Washington, D.C., 11–14 Oct. 2009.

Matthias Kipping and Ludovic Cailluet / 96

ambitious expansion of primary aluminum production that would en-tail large exports to the United Kingdom.72 However, Alcan was left with little choice: had the new investments gone to its competitors, Al-can’s position in the United Kingdom would have become vulnerable, especially given the fi rm’s recent expansion of downstream capacity and uncertainty about future tariffs on ingots. P. J. Elton, managing director for the British Isles and Scandinavia, contacted the Executive Commit-tee in Montreal, which, despite obvious misgivings, gave its “permis-sion to try to get one of the projects envisaged by the British Govern-ment,” leaving all the planning and execution to the subsidiary.73

Elton and his staff prepared a detailed proposal for a new smelter at Invergordon in the Scottish Highlands, intensely lobbied local decision-makers, and launched a public-relations campaign stressing Alcan’s “Britishness.” However, BACo had also set its sights on Invergordon and was more successful in its lobbying efforts. Alcan therefore changed course and advocated the construction of a dedicated coal-fi red power plant, claiming that it was more cost effi cient than nuclear electricity, which was largely unproved. In so doing, the company gained the deci-sive support of the National Coal Board. Alcan was the fi rst to be autho-rized to build a new smelter at Lynemouth in Northumberland. It began production in 1972, eventually reaching a capacity of 120,000 tons. Au-thorizations and huge government loans—to help build two nuclear-power plants—were also given to BACo for the Invergordon smelter and to the RTZ-led consortium in Wales.74 In hindsight, Alcan’s coal strat-egy proved correct, even though it was conceived out of desperation, rather than by design. Nuclear energy was more expensive than its pro-ponents had forecast at the time. BACo’s Invergordon smelter never be-came profi table and was closed in 1981, burdening the company and leading to its takeover by Alcan in 1982.

Reynolds and Tube Investments, BACo’s owners, had fi rst ap-proached Alcan with the idea of a merger in 1968, when the market was “under the burden of at least one-third over-capacity in semi-manufacturing plants.”75 Alcan refused the offer then, but went ahead when the opportunity again presented itself in the early 1980s. At that time BACo had been adversely affected by the closure of the Inver-gordon smelter and had lost the support of Reynolds, which had sold its

72 Hans Otto Frøland, “The Political Economy of European Expansion Programs: The A nglo-Norwegian Aluminium Confl ict, 1967–70,” paper presented at the annual conference of the European Business History Association, Bergen, 21–23 Aug. 2008.

73 According to Christopher Tugendhat, The Multinationals (New York, 1972), 101–2, who seems to have interviewed Elton.

74 MacKenzie “Be Careful What You Wish For.”75 Anon., “Welcome Rationalisation,” Economist, 5 Oct. 1968.

Mintzberg’s Emergent and Deliberate Strategies / 97

49 percent share to its partner, Tube Investments. Alcan was also expe-riencing losses in its U.K. operations at the time, and the company saw the “merger, and the rationalization of facilities” as “an opportunity to create an aluminum company in the U.K. which should be competi-tive.”76 The British government signaled its acceptance, despite possible site closures and job losses, and, after several months of partially secret preparations, the merger to create British Alcan Aluminium Limited was formally concluded on November 30, 1982.77 Despite some initial hesi-tations and doubts, the merger proved a success. Emerging from heavy losses, the combined entity gained healthy profi ts in 1983 and 1984.78

During this period, Alcan also entered both downstream and up-stream production in Spain. In 1928, Alcan had divested from Aluminio Español, but continued to sell ingots in the country. One of its clients, the fabricator Manufacturas Metálicas Madrileñas (MMM), asked the company to participate in the construction of a rolling mill. Alcan agreed, apparently at least partly encouraged by the fond reminiscences of certain executives about their lives in Spain during the 1920s.79 In 1951, it established Alcan Aluminio Iberico (Aliberico) S.A., in order to build a rolling mill in Alicante on the Mediterranean coast. Subsequently, Alcan was drawn into the power struggle between Pechiney and the state holding INI (Instituto Nacional de Industria), which had estab-lished the Empresa Nacional del Aluminio SA (Endasa) in 1943 and had built a smelter in Valladolid, with technical help from Pechiney. In 1967, INI bought MMM’s share in Aliberico and merged it with Endasa the following year, giving Alcan a 26 percent share in the company.

In 1973, INI pressed Alcan and its long-standing rival Pechiney to join forces in order to build a complex for the production of both alu-mina and aluminum in Galicia. Endasa held 55 percent of this venture, the Pechiney subsidiary Alugasa 20 percent, and Spanish banks the re-mainder. Alcan was to provide technical assistance for the alumina stage, and Pechiney was expected to do the same for the ingot production. Alú-mina Aluminio Español was offi cially inaugurated on October 6, 1980. Already, in June, Alcan had increased its participation in Endasa to 42 percent, and had agreed to invest heavily in modernizing existing facilities and constructing downstream activities. As the company’s in-house magazine proudly noted, these Spanish investments made Alcan not only “Europe’s largest aluminium fabricator, en route to becoming its

76 Alcan, Annual Report, 1982.77 Anon., “The Birth of British Alcan,” Compass 27, no. 1 (Jan.–Feb. 1983): 13–17.78 Anon., “British Alcan Gets in Shape,” Compass 29, no. 1 (Jan.–Feb. 1985): 3–10.79 Campbell, Global Mission, vol. 3, 879–886. For the following, see, in detail, Matthias

Kipping and Ludovic Cailluet, “Ménage à Trois: Alcan in Spain, 1950s to 1980s,” Cahiers d’histoire de l’aluminium, nos. 44/45, forthcoming, Oct. 2010.

Matthias Kipping and Ludovic Cailluet / 98

second largest producer of alumina,” but “also moved [it] . . . into third place (after Pechiney and VAW) among European ingot producers.”80

During the 1960s and 1970s, Alcan had made considerable progress in its downstream strategy. In 1970, for the fi rst time in its history, the company shipped a higher tonnage proportion—51 percent—of fabri-cated and semi-fabricated aluminum than of ingot, compared to the proportion of 30 to 70 percent it shipped in 1952.81 In Mintzberg’s termi-nology, Alcan during this period seemed to have been pursuing a “partly deliberate, partly emergent” “umbrella strategy,” whereby “leadership . . . defi ne[d] strategic boundaries or targets within which other actors re-spond[ed] [to their] own forces or to complex, perhaps unpredictable environment[s].”82 Detailed execution and the choice of targets to be acquired were left to the country managers, who sometimes acted op-portunistically, but usually proceeded gradually and cautiously, by par-ticipating initially in a small way or in joint ventures, and then taking control at a later stage. However, some of Alcan’s actions were, once again, forced on it by outside pressures, namely, by the increase in up-stream capacity in the United Kingdom and Spain, where Alcan had to make additional investments in order to protect its established position. While Alcan could claim success at the end of the 1970s, the repeated energy crises during the decade, as well as the entry of new competi-tors, changed the fundamentals of the aluminum industry and prompted the company to review and eventually revise its European strategy.

Focus, Scale, and Profi tability: The 1980s to the Present

While the energy crises of the 1970s favored Alcan by making hy-droelectric power once again the most cost-competitive energy source, other developments were less auspicious. Competition in the global aluminum industry continued to intensify as new entrants from the chemical and manufacturing industries expanded into primary alumi-num and rolled products. There was also a shift in production locations as new capacity was added in Australia, Brazil, and India, rather than in Europe or North America. Increased competition and additional capac-ity contributed to a long-term price decline. (See Figure 1.) Another im-portant development was the fact that, since 1978, primary aluminum traded on the London Metals Exchange, which, as Alcan noted in its 1982 annual report, “tend[ed] to increase the amplitude of price swings between the top and bottom of a business cycle.” For the fi rst time since the industry began, prices for ingots escaped the control of the “six

80 Anon., “Into the Big League with Spain,” Compass 24, no. 5 (Aug. 1980): 6–8.81 Alcan, Annual Report, 1971.82 Mintzberg, Tracking Strategies, 7.

Mintzberg’s Emergent and Deliberate Strategies / 99

majors”: Alcoa, Alcan, Alusuisse (formerly AIAG), Kaiser, Reynolds, and Pechiney.

These developments created pressure for change. Alcan’s vice pres-ident, David H. Clarke, noted, “Most prices in the aluminum industry are not good enough to assure us an acceptable long-term return if Alcan remains just as it is.” It had to “make the transition from a sort of bureaucratic, complacent organization to one that [was] leaner and keener,” namely, by creating small profi t centers and “letting people run their own shows.”83 In 1986, an Alcan mission statement made the new philosophy explicit. Culminating efforts “over the last few years,” the statement was developed by seventy of the company’s senior managers during a one-week retreat in June. Their main point was that it was necessary to improve profi t performance, which they judged to be “me-diocre.”84 The suggested changes went beyond declarations, affecting both leadership and the scope of activities. Thus, Patrick Rich, who as the executive vice president of Europe, Africa, and the Middle East, had presided over much of the expansion until that point, left the company. Among top management, CEO David Culver took more of a back seat, naming David Morton, previous head of the U.K. subsidiary, as president and chief operating offi cer. Morton became chairman and CEO in 1989.85 Alcan also increased the coordination across European operations. For example, in foil production, seventy managers met in 1987 “to conclude planning the strategy for the European sheet and foil system.”86

Figure 1. Evolution of the primary aluminum price in constant U.S. dollars, 1945–2007. (Source: U.S. Geological Survey.)

83 Anon., “Change Brings Opportunities,” Compass 29, no. 4 (Nov.–Dec. 1985): 35.84 Anon., “Determined to Be the Best,” Compass 30, no. 3 (1986).85 Anon., “Morton to Succeed Culver,” Compass 32, no. 4 (1988): 14.86 Anon., “Alcan’s European Sheet Foil Operations Unite,” Compass 31, no. 2 (1987): 20.

Matthias Kipping and Ludovic Cailluet / 100

In terms of the scope of its activities, following advice from the Bos-ton Consulting Group, the company made the radical divestment deci-sion to sell all its European extrusion activities to Norsk Hydro in 1986.87 Around the same time, the company slowly and painfully extri-cated itself from what had become an untenable situation in Spain. The new alumina-aluminum production complex in Galicia, inaugurated in 1980, was never cost competitive and, after fewer than two years of op-erations, had to ask for bankruptcy protection. Pechiney sold its stake in the venture and then sold its subsidiary Alugasa to INI, which merged it with Endasa to form Industria Española del Aluminio SA (Inespal). Alcan initially retained a 24 percent share in the merged entity, but after years of labor unrest and a major accident in the Galician plant in December 1987, it also sold out to INI.88

A more fundamental shift in Alcan’s European and global strategy occurred under Jacques Bougie, who was named president and chief operations offi cer in 1989 and then replaced Morton as chairman and CEO in 1993.89 At the 2000 annual meeting, Bougie retrospectively de-tailed the changes under his leadership: “In 1993 Alcan tightened its strategic focus to concentrate on the core business of low-cost primary metal and high-quality rolled products.” The fi rm concentrated on “the automobile industry as a priority growth market” and adopted a shareholder-value metric as “a key performance indicator.”90 In organi-zational terms, Bougie centralized Alcan’s European operations in 1996 by establishing Alcan Europe Limited. He appointed Jean-Pierre M. Ergas as president of Alcan Europe, executive chairman of British Alcan, and CEO of Alcan Deutschland. This not only meant more unifi ed con-trol over the most important European subsidiaries; it also signaled a cultural shift. While, until that point, senior managers had risen to their positions within the company, Ergas had only joined Alcan the year be-fore, after spending twenty-two years at archrival Pechiney.91

In terms of vertical integration, Alcan divested all the activities it considered to be peripheral, including many fabricating subsidiaries in the United States and Europe—notably, British Alcan Aluminium in the United Kingdom in 1996 and Technal in France in 1999.92 But Alcan also made some investments, namely, by increasing its rolling capacity in

87 Interview with G. de Saint Rémy, former CEO of Alcan France, 4 Apr. 2009; Anon., “Norsk Hydro Buys Five Alcan Extrusion Plants,” Compass 30, no. 4 (1986): 26.

88 For details, see Kipping and Cailluet, “Ménage à Trois.” Inespal was privatized in 1998 and bought by Alcoa.

89 Anon., “Alcan’s Dynamic Duo,” Compass 33, no. 3 (Sept. 1989): 19–21.90 Anon., “Focusing on Growth and Value,” Compass 44, no. 2 (May 2000): 4–6.91 Anon., “Alcan Restructures in Europe,” Compass 40, no. 4 (Aug. 1996): 10.92 The latter was bought by Monitor Clipper Partners, which sold it to Norsk Hydro in

Mintzberg’s Emergent and Deliberate Strategies / 101

Germany to supply the car industry.93 This strategy was common enough among major aluminum producers, including Pechiney and Alcoa, to give the impression that they were all imitating each other.94

After making these divestments, Alcan’s profi tability improved, but its revenues declined signifi cantly. In 1998, its sales of US$8 billion compared unfavorably with Alcoa’s US$20 billion. Bougie therefore de-cided to change direction, so he undertook a series of major takeovers—breaking with the company’s previous philosophy of careful, step-by-step acquisitions. With the help of the strategy-consulting fi rm Monitor Group, Bougie identifi ed potential targets.95 In 1999, Alcan agreed to a three-way merger with its major European rivals Pechiney and Algroup (formerly Alusuisse). This step would have created “the world’s largest aluminum company and the global leader in both fl exible and specialty packaging,” producing total revenues of $21.6 billion in 1998.96 But soon problems surfaced between Alcan and Pechiney that were partly per-sonal, partly practical.97 Regarding the former, Bougie and Pechiney’s CEO Jean-Pierre Rodier never developed a personal chemistry. Regard-ing the latter, there were disagreements about which plants should be divested in order to satisfy the conditions imposed by the European Com-mission in order to approve the merger. Consequently, Pechiney with-drew in 2000, leaving an opening for Alcan to acquire Algroup.98

With his reputation scarred by the failure of the three-way merger, Bougie resigned as leader of the company in 2001. His successor, Tra-vis Engen, continued to focus on the automotive sector.99 He further strengthened the fi rm’s packaging activities, acquiring the packaging arm of German producer VAW in 2003.100 In the same year, Alcan fi nally took over Pechiney, which had remained isolated—and rather small—within the consolidating global aluminum industry. Engen also continued the policy of vertical divestments. At the beginning of 2005, Alcan spun off

93 Anon., “Nachterstedt Plant to Link with Norf Expansion,” Compass 38, no. 4 (Oct. 1994): 10–11.

94 See esp. Kenneth Gooding, “Survey of Aluminium: On the Side of the Angels,” Finan-cial Times, 25 Oct. 1989.

95 Philippe Thaure, Pechiney? . . . vendu! (Paris, 2007), 182. Alcoa followed a similar strat-egy, acquiring Alumax in the United States, then buying Spanish and Italian companies, as well as parts of the former British Alcan Aluminium. In 2000 it merged with Reynolds Metals.

97 According to Thaure, Pechiney? . . . vendu!, who interviewed most of the major protagonists.

98 Anon., “Focusing on Growth and Value,” Compass 44, no. 2 (May 2000): 4–6, here 5; Anon., “Proposed Alcan-Algroup Merger Takes Shape,” Compass 44, no. 3 (July 2000): 4; Anon., “Management Team Announced for Proposed New Alcan,” Compass 44, no. 4 (Sept. 2000): 8–9.

99 Anon., “Expansion Planned for Automotive Components in Europe,” Alcan World 2, no. 3 (Dec. 2002): 7.

100 Anon., “FlexPac Will Be a Big Boost for Packaging,” Alcan World 3, no. 1 (Apr. 2003): 12; Anon., “Welcome New Colleagues,” Alcan World 3, no. 2 (2nd Quarter, 2003): 1.

Matthias Kipping and Ludovic Cailluet / 102

most of its rolling operations under the name Novelis. Originally head-quartered and listed in Toronto, Novelis was acquired by the Indian company Hindalco for close to US$6 billion in February 2007.101

In May 2007, Alcan, now under the leadership of Richard Evans, became the subject of a hostile takeover bid by Alcoa. But rather than reversing history and returning to its erstwhile founder and parent, Alcan found a white knight in the diversifi ed British metals group Rio Tinto, which paid US$38 billion for the company. As part of the deal, which became offi cial at the end of October 2007, Alcan agreed to di-vest its packaging business and concentrate on upstream activities.102 Rio Tinto contributed its bauxite, alumina, and primary aluminum ac-tivities, which were mainly located in Australia. This merger was part of a global rush by natural-resource-based businesses to secure deposits and primary metal-production capacity in what seemed at the time would be a never-ending boom.103 The combined entity, Rio Tinto Alcan, con-ducted activities all over the world and had offi ces in Montreal, Paris, and Brisbane.104 Europe, once the center of Alcan’s downstream opera-tions, became marginal.

During this period, Alcan gradually developed what Mintzberg would call an “ideological strategy” that was expressed in its new mission state-ment, which centered on cost reduction. Under the leadership of several determined CEOs, whose reigns were nevertheless short lived, the com-pany assumed an even more deliberate “entrepreneurial strategy” based on a strong “central vision” regarding profi tability. Assisted by outside consultants, the vision also had elements of a “planned strategy” in terms of both divestments and acquisitions.105 As in previous periods, outside pressures played a part. This time, they came from the stock market, which forced the company to espouse strategies that maximized share-holder value, forcing it eventually to sell itself to the highest bidder.

Conclusion

Our analysis of the development of Alcan’s European strategies since its formal independence in 1928 gives rise to three insights. First, we have shown that the company’s strategies evolved along the deliberate-emergent continuum proposed by Mintzberg. In the case of Alcan, the

103 Anon., “Aluminium: Gimme Smelter,” Economist, 19 July 2007: Anon., “BHP Billiton and Rio Tinto: Financial Prospecting,” Economist, 15 Nov. 2007.

104 Anon., “Built on Strengths,” Our World 1, no. 1 (1st Quarter 2008): 6–7.105 Mintzberg, ed., Tracking Strategies, 7; in detail, Mintzberg and Waters, “Of Strate-

gies,” 259–62.

Mintzberg’s Emergent and Deliberate Strategies / 103

direction was from emergent toward deliberate strategies, partly in re-sponse to external challenges and partly as a result of changes in the company’s leadership. But while Alcan gradually adopted more deliber-ate strategies, highly emergent “imposed strategies” were also apparent during all of the three periods we have discussed. The “external individ-ual or group with a great deal of infl uence over the organization [that] impose[d] a strategy on it” varied over time, changing from the inter-national cartel and the former parent Alcoa during the interwar period, to interventionist governments in the United Kingdom and Spain in the 1960s and 1970s, to the London Metals Exchange as well as the stock market from the 1980s onward.106 However, Alcan’s strategies were never entirely controlled from the outside; the company always found ways to chart its own course.

The second, more tentative, insight concerns the relation between strategy and organizational structure, which became a central theme of business history research after publication of Chandler’s seminal book Strategy and Structure and fi gures prominently in Mintzberg’s frame-work.107 In the case of Alcan, there was some correlation between the fi rm’s strategy and its organization throughout its history. Thus, the evolution of its strategy from emergent to more deliberate paralleled the evolution of its organization, which developed from a loosely cou-pled, holding-like structure in the interwar period to a more integrated, albeit still decentralized, multidivisional form after the late 1960s, and then, most recently, to a more tightly controlled hierarchy. This co-evolution and the forces that drove it warrant additional research.

Our third, even more tentative, insight concerns the crucial role of mergers, acquisitions, and divestments in Alcan’s European strategies, which also moved along the emergent–deliberate continuum during the company’s eighty-year history. Thus, in the interwar and post–World War II periods, mergers and acquisitions were part of an emergent strat-egy as a “pattern of action” that developed in response to (a) external constraints, which limited new investments, and (b) opportunities that presented themselves, sometimes accidentally. In recent decades, by con-trast, mergers and acquisitions became a tool for implementing a delib-erate strategy of scale and focus. Whether the company throughout the whole period actually developed a kind of “organizational capability” in conducting mergers and acquisitions, similar to what Geoffrey Jones observed in his study of Unilever, has to remain an open question until a more detailed study of the fi rm’s internal decisions can be carried out.108

106 Ibid., 268.107 Alfred D. Chandler, Jr., Strategy and Structure: Chapters in the History of the American

Within the historiography of the aluminum industry, the Alcan story refl ects its broader evolution: in the early race toward low-cost produc-tion sites, which prompted Alcoa to establish a smelter in Québec; in the “obsession” with cartelization, which led the U.S. company to place all international activities into its Canadian subsidiary and to make it legally independent; in the development of downstream activities when increasing competition and the end of lucrative government contracts reduced the attractiveness of ingot production; and, fi nally, following further commoditization of aluminum, in attempts to reduce costs and increase shareholder returns, mainly through scale in primary metal and a focus on high-value-added products. The latest wave of mergers and acquisitions, some involving the world’s largest mining companies, brought the industry full circle, that is, close to its origins, when power rested with those controlling both cheap energy and raw materials.

Within these broader developments, Alcan’s own evolution revealed a unique “personality,” due largely to its origins. This personality mani-fested itself in a cautious, incremental, sometimes opportunistic ap-proach, which, to use Mintzberg’s terminology, tended to take the form of umbrella strategies, albeit within the constraints imposed by the broader, evolving industry environment. This particular approach enabled the company to build successfully on the Alcoa heritage and to gradually extend its activities in Europe, enabling it eventually to become, fi rst, the continent’s largest aluminum fabricator and, then, its leading ingot producer. Toward the end of the 1980s, the company went in a differ-ent direction as its management changed and the environment became more competitive.

Moving beyond Alcan, our long-term historical analysis confi rms the usefulness of a framework that looks at a continuum of deliberate and emergent strategies and goes beyond entrenched notions of a largely analytical top-down process. This suggests that future historical studies of company strategy could benefi t from an application of Mintzberg’s ideas. At the same time, our study adds one important insight to the ex-isting framework by highlighting the role of the highly emergent “im-posed strategies.” Mintzberg and his colleagues considered these strat-egies to represent extreme cases, because they seemed to indicate that external forces had signifi cant control over company strategy. However, in the case of Alcan, and probably of resource-based businesses more generally, different kinds of imposition seem to play an important role most of the time, be they in the form of cartels, highly interventionist governments, or pressures from commodity or stock markets.

Copyright of Business History Review is the property of President & Fellows of Harvard College and its

content may not be copied or emailed to multiple sites or posted to a listserv without the copyright holder's

express written permission. However, users may print, download, or email articles for individual use.