28

– Issues for a MNC in doing business in Pharmaceuticals in India Homi R Khusrokhan (Sr. Adviser Private Equity, Tata Capital Ltd.) 14 th September 2011

– Issues for a MNC in doing business in Pharmaceuticals in India

Homi R Khusrokhan (Sr. Adviser Private Equity, Tata Capital Ltd.)14th

September 2011

1.

India’s changing business scenario:

a)

A quick retrospective & dramatic changes seen in the last 2 decades

b)

What’s attractive about India?

c)

Understanding Indian Markets & Indian Mind‐sets

2.

India’s Pharmaceuticals Scenario:

a)

A quick retrospective

b)

The Indian Pharma Market & some important differences

c)

Approaches possible

In the 18th Century China & India accounted for 50% of the world’s GDP – in line with their populationsThis fell precipitously to just 15% over the next 250 years & ~85% of the world’s wealth moved to~15% of the world’s population – Colonization + the Industrial Revolution in Europe China & India – similar but dissimilar – China, is far more homogenous ‐ ruled by successive dynasties ‐ India, extremely diverse – ruled by >560 princely statesBoth selected their own paths – Communism & SocialismAdvent of change ‐ opening of the economy ‐1991 for India ‐perhaps ~10 years earlier in China

1.

(Finally) shaken off “the Hindu rate of growth”

and

hopefully no more “Snakes & Ladders”

hereafter

2.

The significant change in the composition of GDP

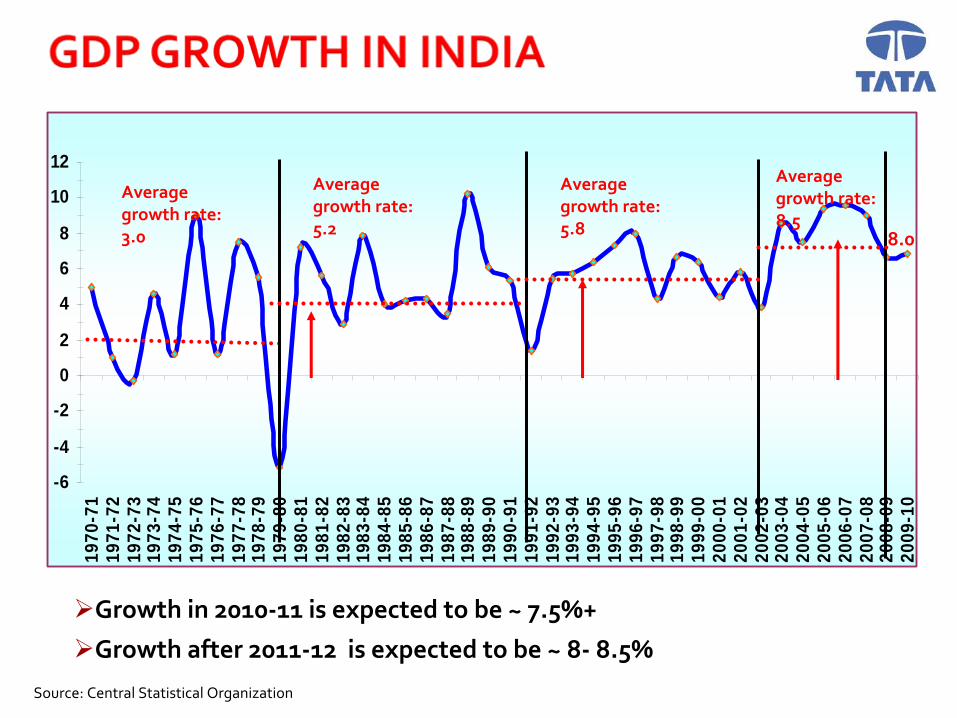

Growth in 2010‐11 is expected to be ~ 7.5%+

Growth after 2011‐12 is expected to be ~ 8‐ 8.5%

-6

-4

-2

0

2

4

6

8

10

12

1970

-71

1971

-72

1972

-73

1973

-74

1974

-75

1975

-76

1976

-77

1977

-78

1978

-79

1979

-80

1980

-81

1981

-82

1982

-83

1983

-84

1984

-85

1985

-86

1986

-87

1987

-88

1988

-89

1989

-90

1990

-91

1991

-92

1992

-93

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

Average

growth rate:

3.0

Average

growth rate:

5.2

Average

growth rate:

5.8

Average

growth rate:

8.5

8.0

Source: Central Statistical Organization

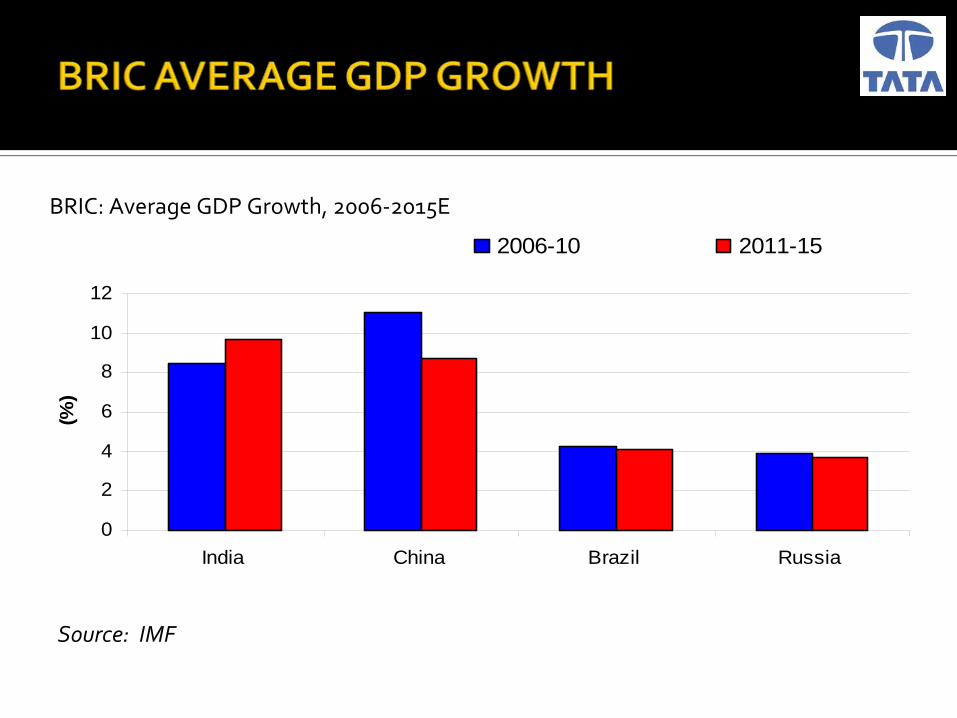

0

2

4

6

8

10

12

India China Brazil Russia

(%)

2006-10 2011-15

BRIC: Average GDP Growth, 2006‐2015E

Source: IMF

1950‐51

5715

28

GDP

Agriculture

Industry

Services

2009‐10

15

2857

GDP

Agriculture

Industry

Services

Agriculture &Allied

Industry Services

Share of employment ‐

INDIA 52% 21% 27%

CHINA 11% 48% 41%

1.

(Finally) shaken off “the Hindu rate of growth”

and hopefully no more “Snakes & Ladders”

2.

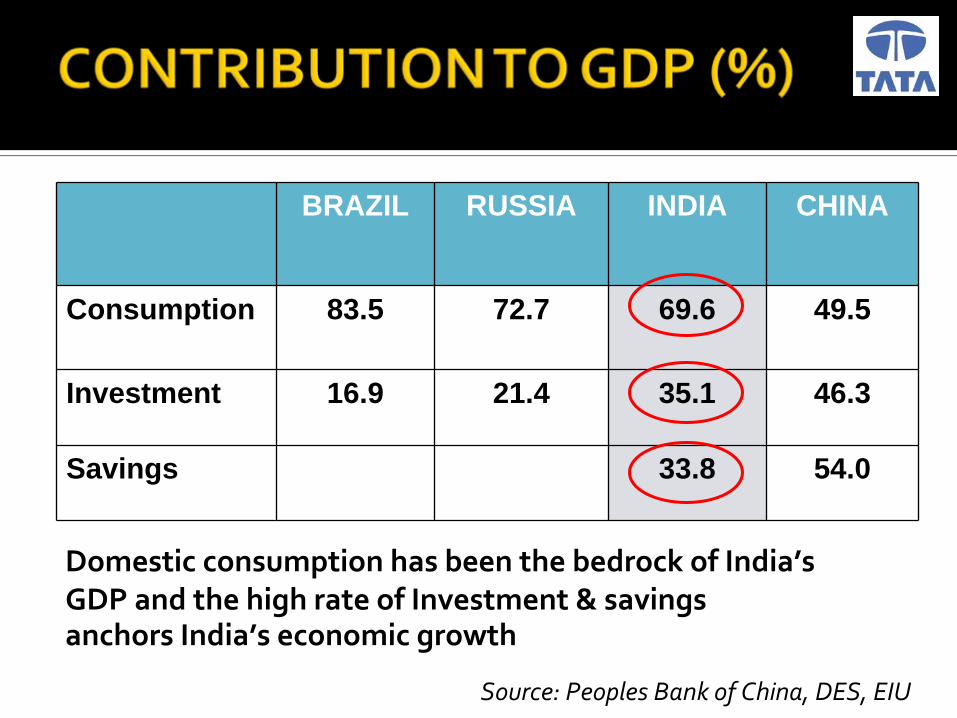

The significant change in the composition of our

GDP

3.

Domestic Consumption – a significant component

of GDP + High Rate of Investment (& savings)

4.

Significant planned investments in Infrastructure

BRAZIL RUSSIA INDIA CHINA

Consumption 83.5 72.7 69.6 49.5

Investment 16.9 21.4 35.1 46.3

Savings 33.8 54.0

Domestic consumption has been the bedrock of India’s

GDP and the high rate of Investment & savings

anchors India’s economic growth

Source: Peoples Bank of China, DES, EIU

The 11th 5‐Year Plan (2007‐12) envisages large investments in infrastructure

China: US$ 400 Billion (2009)

*at Rs 40/$ (at 2006‐07 prices)Source: Planning Commission of India

02040

6080

100120

140160

2007-08 2008-09 2009-10 2010-11 2011-12

$Bn

012345678910

%of

GD

P

Investment in Infrastructure in India as % of GDP

Eleventh Plan (Projected Investment)

Sectors Rs Bn.US $ Bn*

Share (%)

Electricity 6665.25 166.63 32.42

Roads and Bridges 3141.52 78.54 15.28

Telecommunication 2584.39 64.61 12.57

Railways (incl MRTS) 2618.08 65.45 12.73

Irrigation (incl Watershed) 2533.01 63.33 12.32

Water Supply and sanitation 1437.30 35.93 6.99

Ports 879.95 22.00 4.28

Airports 309.68 7.74 1.51

Storage 223.78 5.59 1.09

Gas 168.55 4.21 0.82

Total 20561.51 514.04 100

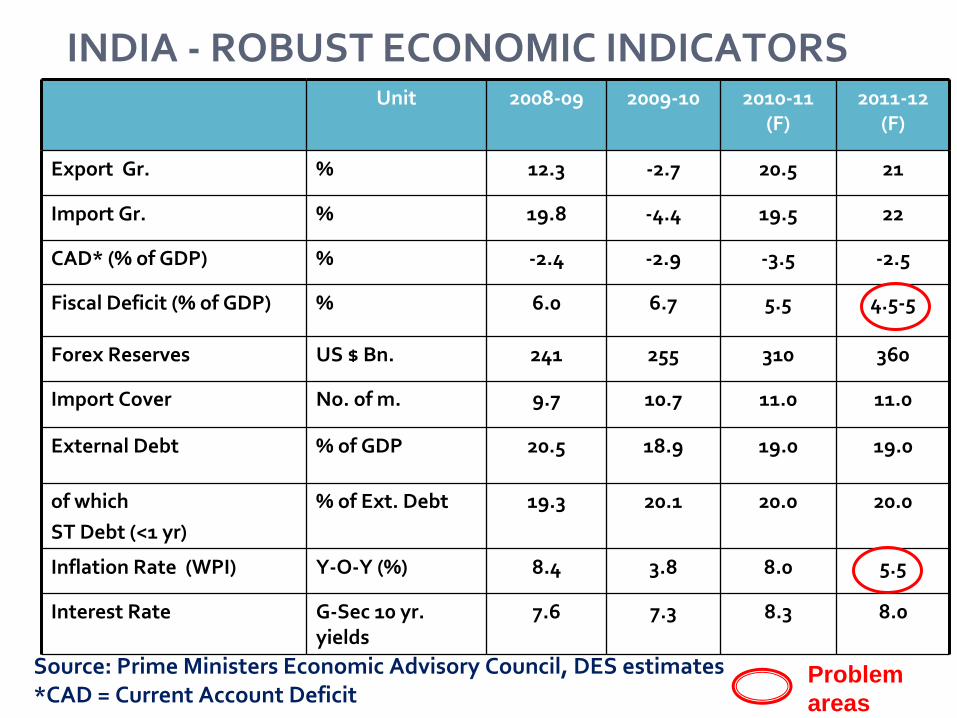

INDIA ‐

ROBUST ECONOMIC INDICATORS Unit 2008‐09 2009‐10 2010‐11

(F)

2011‐12

(F)

Export Gr. % 12.3 ‐2.7 20.5 21

Import Gr. % 19.8 ‐4.4 19.5 22

CAD* (% of GDP) % ‐2.4 ‐2.9 ‐3.5 ‐2.5

Fiscal Deficit (% of GDP) % 6.0 6.7 5.5 4.5‐5

Forex Reserves US $ Bn. 241 255 310 360

Import Cover No. of m. 9.7 10.7 11.0 11.0

External Debt % of GDP 20.5 18.9 19.0 19.0

of which ST Debt (<1 yr)

% of Ext. Debt 19.3 20.1 20.0 20.0

Inflation Rate (WPI) Y‐O‐Y (%) 8.4 3.8 8.0 5.5

Interest Rate G‐Sec 10 yr.

yields

7.6 7.3 8.3 8.0

Source: Prime Ministers Economic Advisory Council, DES estimates

*CAD = Current Account Deficit

Problem areas

Reforms in Progress

Labour Laws

GST

FDI in Retail

Subsidies Cut

PSU Divestments

Problem Areas

Infrastructure Poor HDI

Land acquisition Social Unrest

Agric. P/y Terrorism

Fiscal Deficit Poor Governance

Skill Shortages The BIG “C”

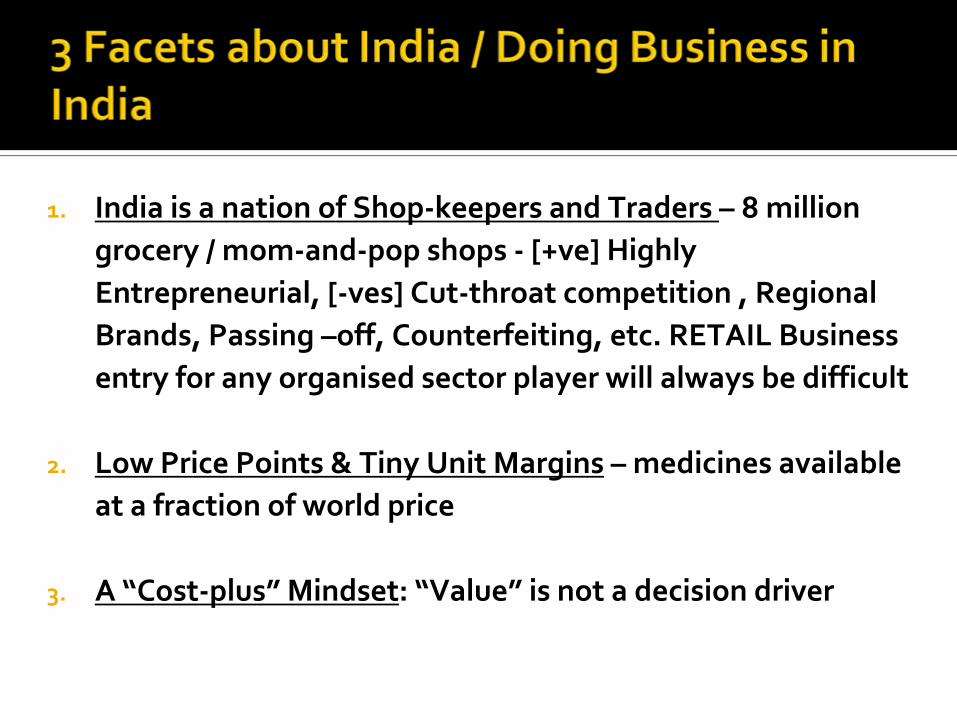

1.

India is a nation of Shop‐keepers and Traders – 8 million

grocery / mom‐and‐pop shops ‐

[+ve] Highly

Entrepreneurial, [‐ves] Cut‐throat competition , Regional

Brands, Passing –off, Counterfeiting, etc. RETAIL Business

entry for any organised sector player will always be difficult

2.

Low Price Points & Tiny Unit Margins

–

medicines available

at a fraction of world price

3.

A “Cost‐plus”

Mindset: “Value”

is not a decision driver

1.

India’s changing business scenario:

a)

A quick retrospective & dramatic changes seen in the last 2 decades

b)

What’s attractive about India?

c)

Understanding Indian Markets & Mind‐sets

2.

India’s Pharmaceuticals Scenario:

a)

A quick retrospective

b)

The Indian Pharma Market & some important differences to recognise

c)

Approaches possible

Regulation has played a huge role in shaping this industry

‘Virtual abolition’ of IPR Law by the Indian Patents Act 1970

Rigorous (cost‐based) pricing by the Drugs (Prices Control) Order (1979)

Overt favouring of the “Indian Sector” against the MNC’s (1974 ‐2000) – two clear camps with battle‐lines drawn

But… in an areas where Drug Laws should have been tight they are still very lax – licensing (of manufacture), pharmacies, doctor’s prescription practices

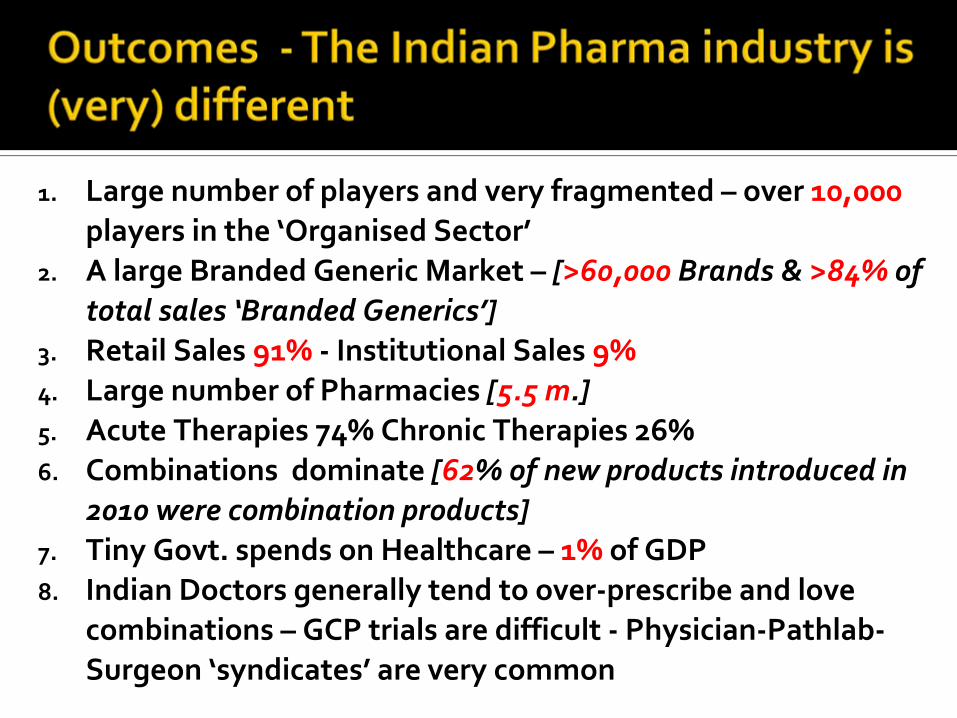

1.

Large number of players and very fragmented – over 10,000

players in the ‘Organised Sector’2.

A large Branded Generic Market –

[>60,000 Brands & >84% of

total sales ‘Branded Generics’]3.

Retail Sales 91%

‐

Institutional Sales 9%

4.

Large number of Pharmacies [5.5 m.]5.

Acute Therapies 74% Chronic Therapies 26%6.

Combinations dominate [62% of new products introduced in

2010 were combination products]7.

Tiny Govt. spends on Healthcare –

1%

of GDP

8.

Indian Doctors generally tend to over‐prescribe and love

combinations – GCP trials are difficult ‐

Physician‐Pathlab‐

Surgeon ‘syndicates’

are very common

1.

Company Rankings

Top 10 Companies Market Share

1. Abbotts 6.2

2. Cipla 5.4

3. GSK 4.7

4. Ranbaxy 4.6

5. Sun Pharma 4.2

6. Zydus Cadilla 3.9

7. Alkem 3.3

8. Lupin 3.2

9. Mankind 3.0

10. Pfizer + Wyeth 3.0

MNC INDIAN

Post –

Piramal Deal 13.9 (33%) 27.6 (67%)

Pre –

Piramal Deal 10.0 (25%) 31.6 (75%)

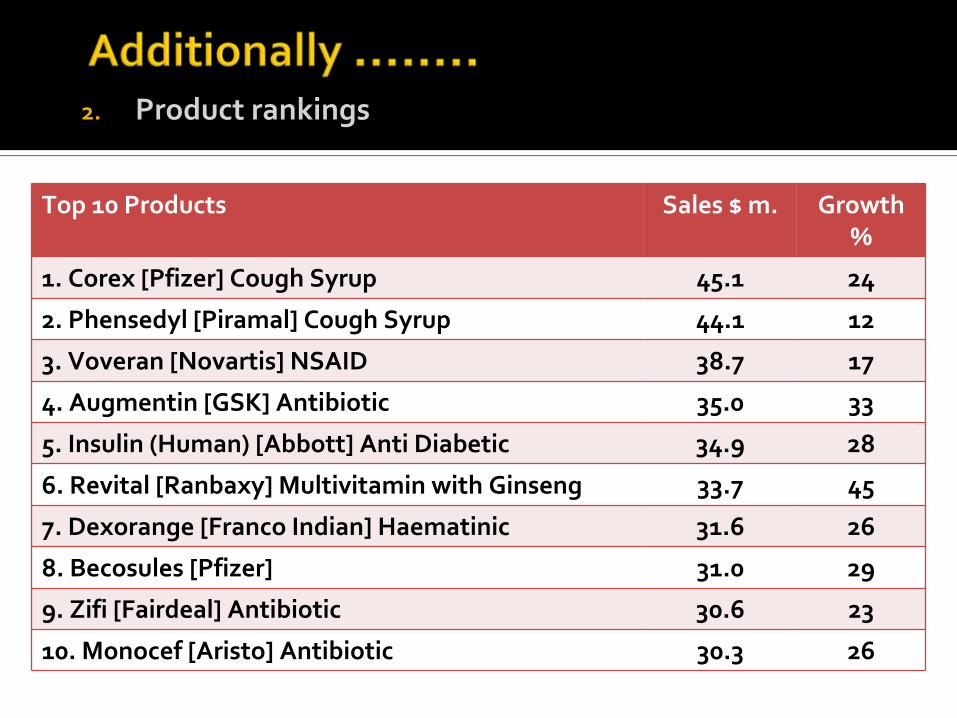

2.

Product rankings

Top 10 Products Sales $ m. Growth

%

1. Corex [Pfizer] Cough Syrup 45.1 24

2. Phensedyl [Piramal] Cough Syrup 44.1 12

3. Voveran [Novartis] NSAID 38.7 17

4. Augmentin [GSK] Antibiotic 35.0 33

5. Insulin (Human) [Abbott] Anti Diabetic 34.9 28

6. Revital [Ranbaxy] Multivitamin with Ginseng 33.7 45

7. Dexorange [Franco Indian] Haematinic 31.6 26

8. Becosules [Pfizer] 31.0 29

9. Zifi [Fairdeal] Antibiotic 30.6 23

10. Monocef [Aristo] Antibiotic 30.3 26

Only 35% of the population has access to allopathic medicines – as prosperity increases this industry will see significant growth [@ 12‐15% y‐o‐y growth it is already one of the fastest growing Pharma markets in the world]

There is a significant cost advantage to operations in India

Manufacturing [119 USFDA & 84 UKMHRA approved plants]R&D [particularly, Discovery & Development CRO’s]Clinical Research [Living Laboratory]Back‐office and data management

Increase in Chronic and life‐style diseases

Rapid growth in Hospital Sector [>70% in last 3 years]

CategoryNo. of

Households% of

TotalPopulation (m)

Annual

Household

Income in US $

Growth

in last

Decade

Deprived 114.4 51.5 620 2,000 ‐2.10%

Aspirers 75.3 34.0 405 2,000 ‐

4,000 7.80%

Middle Class 28.4 12.8 150 4,000 ‐

21,000 12.90%

Rich 3.8 1.7 20 > 21,000 21.40%

TOTAL 221.9 # 100.0 1,195

# RURAL 70.14

# URBAN 29.86

1.

Do not look at India through ‘Western Eyes’Respect and learn to accept with the differencesLook for the strengths (and find own solutions for weaknesses)

2.

The 3 biggest problemsPrice control Lack of IPR [less of a problem today but still an issue] Dealing with the bureaucracy of the Indian Regulator

3.

Seek out Examples of Companies that have succeeded and

placed their bets differentlyGE [$ 3Bn. business – JW Tech Centre 5,500 Sc., 1,000 Patents]IBM [160,000 employees (more than US)]TI [entered early (1985) ‐ R&D Chip Design & Digital Signal]

4.

Glaxo – “the Multinational with a Brown Face”

4 Price Control Orders: 1971, 1979, 1987, 1995Span of Price Control under 1995 Order 20% [today 12%] + Rest under Price Monitoring:

(a) Incr. < 10% p.a. (b) Overall Profit : Sales < 10%2002 Order stalled because of a PIL – not implementedNLEM created at instance of Supreme Court in 2003 & 20062006 list contains 348 Medicines – 3 categories‐ Prim / Sec / TertBut still not implementedReference Pricing System now under consideration –Weighted Av. Price of top 3 brandsCompanies have started receiving notices for exceeding the ‘Profit Ceiling’ of 10% of Sales

1.

Pre & Post Grant Opposition + Revocation Proceedings

2.

No Regulatory Data Protection

3.

No Improvements recognized without proven efficacy testing

4.

Threat of Compulsory Licensing (on commercial considerations

5.

Almost no Preliminary Injunctions

1.

‘EXPLORER’

(versus Harvester)

2.

‘COST CONSCIOUS INNOVATOR’

(versus large R&D spends)

3.

GO INDIAN (List Company on Indian Sock Exchanges)

& at all times:a)

Think and Act Local

b)

Devolve authority

c)

Have patience and do things the ‘Indian’

way

Tata values

• Integrity: Fair, honest & transparent in all dealings

• Understanding: Care, respect, compassion for customers and colleagues

• Excellence: Highest possible standards in quality of goods & services

• Unity: Strong relationships with partners and customers

• Responsibility: What comes from the people must go back to the people – many times over

Tata Sons

3%

18%

Tata Industries

49.5% 50.5%

Public trusts

Tata companies

Individuals

Other Corporates

Other Tata companies

Tata Sons & its Subsidiaries

Promotes group entry into new businesses

Shareholding in main Operating Companies

Invests to facilitate growth of main Operating Companies

''In a free enterprise, the Community is not just another stakeholder of the

business but its very purpose''Jamshetjee

Tata