Page 1

Multi-Level Risk-Controlled Sector Optimization for Opportunistic Global Fixed-Income Portfolios

Ron D'Vari, Juan C. Sosa, KishoreYalamanchilli

State Street Research & Management

CIFEr, New York

March 27th, 2000

Page 2

State Street Research, Multilevel Risk-Controlled Optimization

2

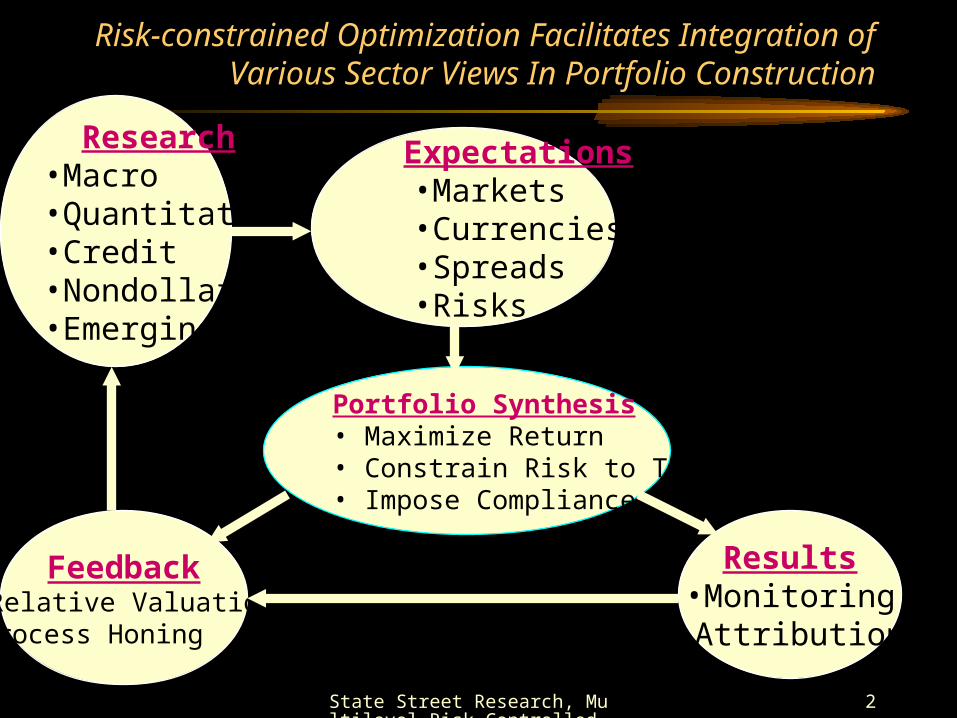

Risk-constrained Optimization Facilitates Integration of Various Sector Views In Portfolio Construction

Feedback•Relative Valuation•Process Honing

Results•Monitoring•Attribution

Expectations•Markets•Currencies•Spreads•Risks

Portfolio Synthesis • Maximize Return• Constrain Risk to Tolerance• Impose Compliance

Research•Macro •Quantitative•Credit•Nondollar•Emerging

Page 3

State Street Research, Multilevel Risk-Controlled Optimization

3

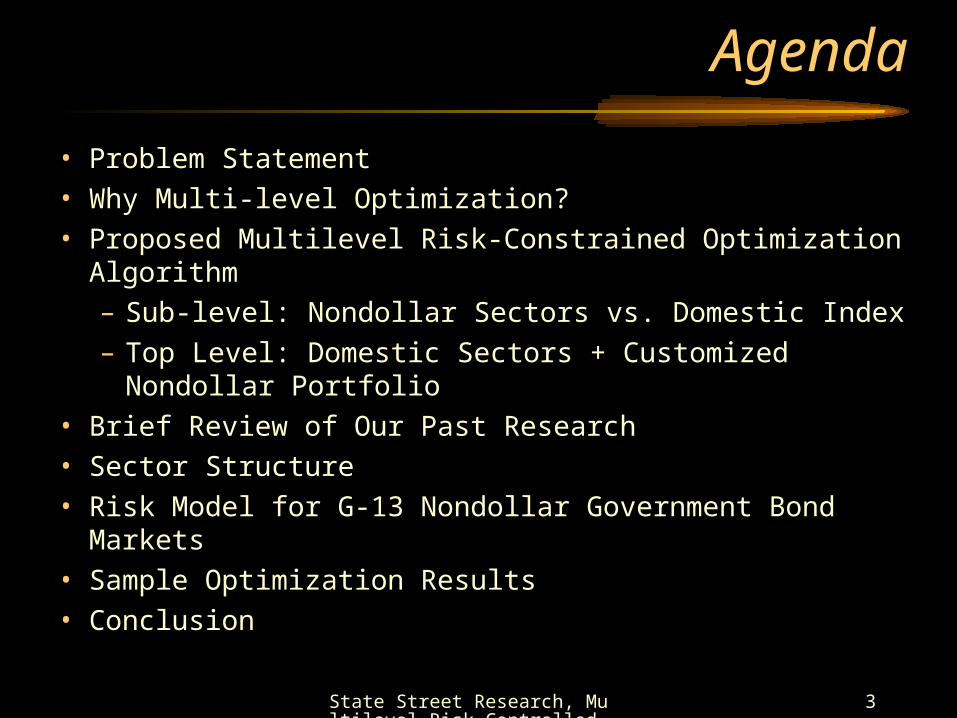

Agenda

• Problem Statement

• Why Multi-level Optimization?

• Proposed Multilevel Risk-Constrained Optimization Algorithm

– Sub-level: Nondollar Sectors vs. Domestic Index

– Top Level: Domestic Sectors + Customized Nondollar Portfolio

• Brief Review of Our Past Research

• Sector Structure

• Risk Model for G-13 Nondollar Government Bond Markets

• Sample Optimization Results

• Conclusion

Page 4

State Street Research, Multilevel Risk-Controlled Optimization

4

Risk-Constrained Optimization Problem Definition

Decision Variable Characteristics

Static Dynamic(Modeled as Normal, Garch or

Garch-PJ)

Sector

Weight CurrencyForward

Duration,Convexity

BaseYield

OASor

Spread

Spot Rate

Domestic Inv. GradeSubsector ith

(By Sector, Credit, andDuration)

DWi-- DEDuri

DEConi

DEYieldiDEspreadi --

Domestic High-YieldSubsector ith

(By Sector, Credit, andDuration)

HWi-- HEDuri

HEConi

HEYieldiHEspreadi --

Nondollar GovernmentSubsector ith

(By Country andMaturity)

NWi

CURWiNEDuriNEConi

NEYieldiNEspreadi

CURSi

Dollar-denominatedEmerging Subsector ith

(By Country andMaturity)

EWi

-- EEDuriEEConi

EEYieldiEEspreadi --

Page 5

State Street Research, Multilevel Risk-Controlled Optimization

5

Problem Definition (Cont’d)

• Maximize Relative or Absolute Return Under a Single View or Probably Weighted View– Requires explicit views on all sectors

– Coordinated effort by all research teams

– Could blend short (tactical) and long term views (strategic)

• Subject To Constraints– Relative or Absolute Conditional VaR at CL= X < CVaR Limit

– Under performance under defined scenarios < Scenario Return Limit

– Traditional Relative or Absolute Risk Measures• Duration

• Curve Risk Measures

• Duration Contributions from Various Sectors

Page 6

State Street Research, Multilevel Risk-Controlled Optimization

6

Why Multi-Level Optimization

• Avoid ill-conditioned problem of joint risk characterization – Simultaneous optimization of a large number of subsectors

• Requires a large length of time histories for joint risk characterization

• Can lead to numerical instabilities and noise

• Dependency of returns tend to be stable when considering – Cells within each sector, and

– Different sectors as aggregate

• Dependency of returns tend to be noisy when considering – Cells that fall in diverse sectors

• e.g. 5-year AAA CMBS spread vs. 10-year JGB yield)

Page 7

State Street Research, Multilevel Risk-Controlled Optimization

7

Proposed Multilevel Optimization Algorithm

• Sub-level:

– Optimize Relative Return of Nondollar Sectors to Domestic Index (Decision Variables: NWi, Cwi )

– Subject to:• Relative CVaR Limit Allotted to Nondollar

– Example (3-Month, 97.5% Confidence Level):

• Total Relative CVaR =100bp

• Allotted Nondollar CVaR at Total Portfolio Level = 30bp

• Allotted Nondollar Relative CVaR at Sector Level = 300bp

(All numbers measured w.r.t. domestic index)

• Hedge limits (i.e., 0.95 <[CWi/ NWi ]< 1.05)

• Scenario constraints

• Other constraints (related to guideline or research view)– Country weight or duration contribution

Page 8

State Street Research, Multilevel Risk-Controlled Optimization

8

Proposed Multilevel Optimization Algorithm (Cont’d)

• Top-level:

– Optimize Relative Return vs. Overall Index with Decision Variables as

• Domestic Sector Weights (DWi)

• Weight of Customized Nondollar Portfolio (Nwcustomized index )

– Specific opportunistic countries can be segregated and optimized at the top level (e.g. Greece)

– Subject to:• Relative CVaR Limit vs.. Overall benchmark

• Scenario constraints

• Traditional constraints

Page 9

State Street Research, Multilevel Risk-Controlled Optimization

9

Brief Review of Our Past Research

• Risk Models Used

• Rolling GARCH-PJ

• Sample Domestic Results

Page 10

State Street Research, Multilevel Risk-Controlled Optimization

10

Methodology Requirements for Risk Models

• Accuracy– Nonstationary – Non-normal

• Robustness

• Feasible automation and maintenance

Page 11

State Street Research, Multilevel Risk-Controlled Optimization

11

Risk Models Used

• Rolling Variance-Covariance– G-13 Government Bond Yields

– Investment Grade Corporate and ABS OASs

• GARCH and Garch-t– Mortgage passthroughs

– G-13 currencies • Garch-PJ

– Used for high yield and emerging markets • Univariate GARCH with Persistent Jumps

• Rolling white noise correlation matrix

• Exogenized jump frequencies

Page 12

State Street Research, Multilevel Risk-Controlled Optimization

12

Rolling GARCH-PJ (univariate)

• A variation of GARCH(1,1) that features Bernoulli-style jumps

st = a0 + et, where

et = sqrt(ht)ut + jt, with ut ~ N(0,1) i.i.d.

ht = g0 + g1 e2t-1 + g2ht-1

jt ~ N(j,j2) with probability p

0 with probability 1-p

• Jump occurrences in this model will induce a volatility spike in subsequent days

• Bernoulli, rather than Poisson jumps, simplify and speed up the parameter estimation procedure

• VaR estimates are also produced via simulation

• Jump frequencies are also allowed to depend on exogenous or past data

Page 13

State Street Research, Multilevel Risk-Controlled Optimization

130 25 50 75 100 125 150 175 200 225 250

-3

-2

-1

0

1

2

3 Brazil: Daily Series of 1-day spread changes, Jan/01/98-Jan/22/99

and 90%&99% Var-Covar VaR estimates

Page 14

State Street Research, Multilevel Risk-Controlled Optimization

140 25 50 75 100 125 150 175 200 225 250

-3

-2

-1

0

1

2

3

4 Brazil: Daily Series of 1-day spread changes, Jan/01/98-Jan/22/99and 90%&99% GARCH(1,1) VaR estimates

Page 15

State Street Research, Multilevel Risk-Controlled Optimization

150 25 50 75 100 125 150 175 200 225 250

-3

-2

-1

0

1

2

3

4

Brazil: Daily Series of 1-day spread changes, Jan/01/98-Jan/22/99and 90%&99% GARCH-PJ(1,1) VaR estimates

Page 16

State Street Research, Multilevel Risk-Controlled Optimization

160 25 50 75 100 125 150 175 200 225 250

-3

-2

-1

0

1

2

3

4

Brazil: Daily Series of 1-day spread changes, Jan/01/98-Jan/22/99and 90%&99% GARCH-PJ(1,1) w/ Exogenized Jumps VaR estimates

Page 17

State Street Research, Multilevel Risk-Controlled Optimization

17

Model Choice

The skewness and kurtosis of the standardized

innovations support GARCH-PJ

Brazil 1992-1999: Skewness Kurtosis

Rolling Var-Covar 5.94 99.67

GARCH 2.96 47.20

GARCH-PJ * 0.16 3.50

GARCH-PJ Exo* 0.12 3.42*jump days excluded

Page 18

State Street Research, Multilevel Risk-Controlled Optimization

18

Multivariate ARCH Issues

• Multivariate ARCH models suffer from estimation problems, deriving from the inclusion of correlation parameters

• Our ad-hoc approach: a 3-month sample correlation matrix estimated from (non-jump) standardized innovations

Page 19

State Street Research, Multilevel Risk-Controlled Optimization

19

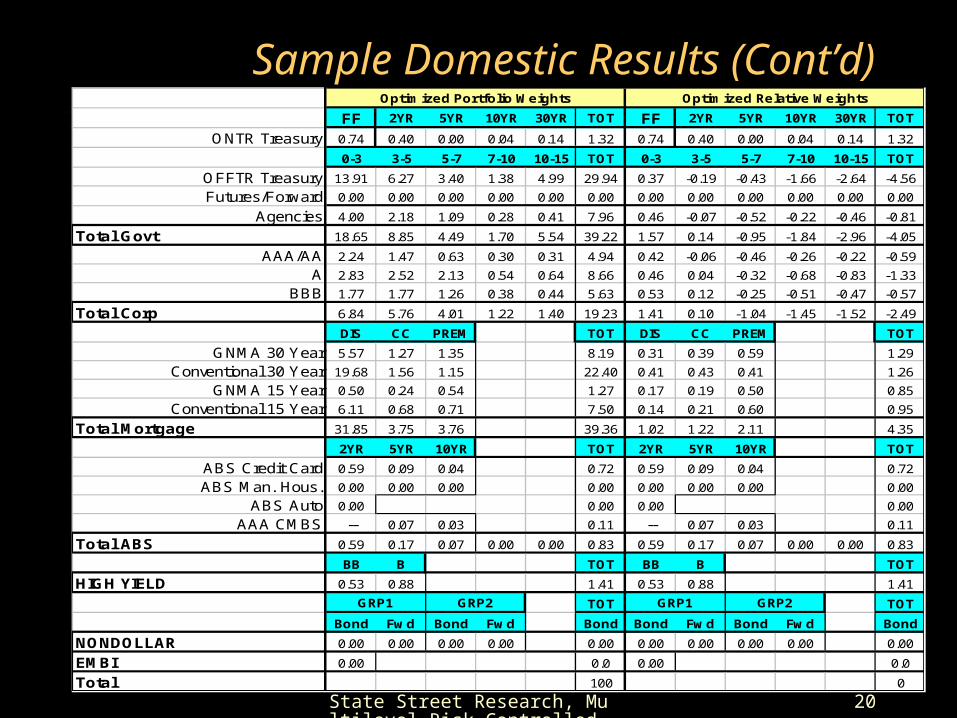

Sample Domestic Results (Cont’d)Optimized Portfolio Weights Optimized Relative Weights

FF 2YR 5YR 10YR 30YR TOT FF 2YR 5YR 10YR 30YR TOT

ONTR Treasury 0.74 0.40 0.00 0.04 0.14 1.32 0.74 0.40 0.00 0.04 0.14 1.32

0-3 3-5 5-7 7-10 10-15 TOT 0-3 3-5 5-7 7-10 10-15 TOT

OFFTR Treasury 13.91 6.27 3.40 1.38 4.99 29.94 0.37 -0.19 -0.43 -1.66 -2.64 -4.56

Futures/Forward 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Agencies 4.00 2.18 1.09 0.28 0.41 7.96 0.46 -0.07 -0.52 -0.22 -0.46 -0.81

Total Govt 18.65 8.85 4.49 1.70 5.54 39.22 1.57 0.14 -0.95 -1.84 -2.96 -4.05

AAA/AA 2.24 1.47 0.63 0.30 0.31 4.94 0.42 -0.06 -0.46 -0.26 -0.22 -0.59

A 2.83 2.52 2.13 0.54 0.64 8.66 0.46 0.04 -0.32 -0.68 -0.83 -1.33

BBB 1.77 1.77 1.26 0.38 0.44 5.63 0.53 0.12 -0.25 -0.51 -0.47 -0.57

Total Corp 6.84 5.76 4.01 1.22 1.40 19.23 1.41 0.10 -1.04 -1.45 -1.52 -2.49

DIS CC PREM TOT DIS CC PREM TOT

GNMA 30 Year 5.57 1.27 1.35 8.19 0.31 0.39 0.59 1.29

Conventional 30 Year 19.68 1.56 1.15 22.40 0.41 0.43 0.41 1.26

GNMA 15 Year 0.50 0.24 0.54 1.27 0.17 0.19 0.50 0.85

Conventional 15 Year 6.11 0.68 0.71 7.50 0.14 0.21 0.60 0.95

Total Mortgage 31.85 3.75 3.76 39.36 1.02 1.22 2.11 4.35

2YR 5YR 10YR TOT 2YR 5YR 10YR TOT

ABS Credit Card 0.59 0.09 0.04 0.72 0.59 0.09 0.04 0.72

ABS Man. Hous. 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

ABS Auto 0.00 0.00 0.00 0.00

AAA CMBS -- 0.07 0.03 0.11 -- 0.07 0.03 0.11

Total ABS 0.59 0.17 0.07 0.00 0.00 0.83 0.59 0.17 0.07 0.00 0.00 0.83

BB B TOT BB B TOT

HIGH YIELD 0.53 0.88 1.41 0.53 0.88 1.41

GRP1 GRP2 TOT GRP1 GRP2 TOT

Bond Fwd Bond Fwd Bond Bond Fwd Bond Fwd Bond

NONDOLLAR 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

EMBI 0.00 0.0 0.00 0.0

Total 100 0

Page 20

State Street Research, Multilevel Risk-Controlled Optimization

20

Sample Domestic Results (Cont’d)Optimized Portfolio Weights Optimized Relative Weights

FF 2YR 5YR 10YR 30YR TOT FF 2YR 5YR 10YR 30YR TOT

ONTR Treasury 0.74 0.40 0.00 0.04 0.14 1.32 0.74 0.40 0.00 0.04 0.14 1.32

0-3 3-5 5-7 7-10 10-15 TOT 0-3 3-5 5-7 7-10 10-15 TOT

OFFTR Treasury 13.91 6.27 3.40 1.38 4.99 29.94 0.37 -0.19 -0.43 -1.66 -2.64 -4.56

Futures/Forward 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Agencies 4.00 2.18 1.09 0.28 0.41 7.96 0.46 -0.07 -0.52 -0.22 -0.46 -0.81

Total Govt 18.65 8.85 4.49 1.70 5.54 39.22 1.57 0.14 -0.95 -1.84 -2.96 -4.05

AAA/AA 2.24 1.47 0.63 0.30 0.31 4.94 0.42 -0.06 -0.46 -0.26 -0.22 -0.59

A 2.83 2.52 2.13 0.54 0.64 8.66 0.46 0.04 -0.32 -0.68 -0.83 -1.33

BBB 1.77 1.77 1.26 0.38 0.44 5.63 0.53 0.12 -0.25 -0.51 -0.47 -0.57

Total Corp 6.84 5.76 4.01 1.22 1.40 19.23 1.41 0.10 -1.04 -1.45 -1.52 -2.49

DIS CC PREM TOT DIS CC PREM TOT

GNMA 30 Year 5.57 1.27 1.35 8.19 0.31 0.39 0.59 1.29

Conventional 30 Year 19.68 1.56 1.15 22.40 0.41 0.43 0.41 1.26

GNMA 15 Year 0.50 0.24 0.54 1.27 0.17 0.19 0.50 0.85

Conventional 15 Year 6.11 0.68 0.71 7.50 0.14 0.21 0.60 0.95

Total Mortgage 31.85 3.75 3.76 39.36 1.02 1.22 2.11 4.35

2YR 5YR 10YR TOT 2YR 5YR 10YR TOT

ABS Credit Card 0.59 0.09 0.04 0.72 0.59 0.09 0.04 0.72

ABS Man. Hous. 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

ABS Auto 0.00 0.00 0.00 0.00

AAA CMBS -- 0.07 0.03 0.11 -- 0.07 0.03 0.11

Total ABS 0.59 0.17 0.07 0.00 0.00 0.83 0.59 0.17 0.07 0.00 0.00 0.83

BB B TOT BB B TOT

HIGH YIELD 0.53 0.88 1.41 0.53 0.88 1.41

GRP1 GRP2 TOT GRP1 GRP2 TOT

Bond Fwd Bond Fwd Bond Bond Fwd Bond Fwd Bond

NONDOLLAR 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

EMBI 0.00 0.0 0.00 0.0

Total 100 0

Page 21

State Street Research, Multilevel Risk-Controlled Optimization

21

Sample Domestic Results

Dur 3-Month Total Return

Yrs Sc1 Sc2 Sc3 Sc4 Sc5 Sc6 Sc7 Comp

Benchmark (yrs or %) 4.97 1.80 -0.22 2.75 3.89 1.15 0.78 11.42 -0.22

Portfolio (yrs or %) 4.32 1.82 0.13 2.63 3.76 0.95 1.28 10.16 0.13

Relative (yrs or bp) -0.66 2 35 -12 -13 -20 50 -126 35Relative Constraint (yrs or bp) -- -- -- -- -- -- -- -- --

13WK 95% CVaR 13WK 95% Rel. CVaR Equiv. Annual T.E.

(%) bp bpBenchmark (%) -2.34% -- --

Portfolio (%) -1.83% -70 bp 97 bpRelative (bp) 51 bp -- --

Relative Constraint (bp) -- -70 bp