20

NEDBANK GROUP LIMITED Renaissance Capital Business Banking Investor Day 12 th June 2014

NEDBANK GROUP LIMITED

Renaissance Capital

Business Banking Investor Day12th June 2014

2

Business Banking – leadership team

Effective 1 June 2014

1 Nedbank Group Exco member; appointed to Old Mutual plc wef 1 July 2014

2 Nedbank Group Exco member

Ingrid Johnson (47)

Group Managing Executive:

Retail and Business Banking1

20 years service

20 years banking experience

BCom, BAcc, CA(SA), AMP

(Harvard)

Sandile Shabalala (47)

Managing Executive:

Business Banking2

18 years service

22 years banking experience

BAdmin, NHD: Management Practice,

CAIB (SA), MBL, Strategic Management in

Banking (Insead), AMP (Harvard)

Douglas Lines (42)

Divisional Executive:

Strategic Business Unit

Goolam Kader (47)

Divisional Executive:

Business Banking Cape

Craig Evans (48)

Divisional Executive:

Business Banking Coastal &

Inland

Herman de Kock (40)

Divisional Executive:

Business Banking Northern

Kandis Swanepoel (47)

Divisional Executive:

Business Banking Gauteng

Bedresh Dhanjee (43)

Executive Head:

Business Banking Risk

Jan Bosch (41)

Executive Head: Business

Banking & Retail

Relationship Banking

Specialist Services

Brinsley du Plessis (43)

Executive Head:

Innovation, Process and

Project Integration

Lebo Biko (38)

Executive Head:

Strategy, Marketing &

Communications

13 years service

17 years banking experience

BAcc, Dip Acc CA(SA), AMP

(Duke)

14 years service

27 years banking experience

BCom , CAIB (SA) , GEDP

(GIBS), Strategic Management

in Banking (Insead)

20 years service

23 years banking experience

BSc Agriculture Economics,

CAIB (SA), AMP (Insead)

11 years service

11 years banking experience

MA, MBA, IEP (Insead),

Strategic Management in

Banking (Insead)

18 years service

18 years banking experience

BCom, BAcc, CA(SA), MBA

(Univ of Wales), AMP (Insead)

24 years service

24 years banking experience

Bcompt, EDP (GIBS)

9 years service

13 years banking experience

BA Hons (NMMU), IEDP (Wits)

15 years service

15 years banking experience

BCom Hons, CA(SA), IEP (Insead)

23 years service

23 years banking experience

Executive MBA (Henley) , TGM

(Insead)

3 years service

3 years banking experience

Bcoms, MBA (Wits), Manager of

Function (Duke)

Name and position Experience and qualificationExperience and qualification Name and position

Nomaxabiso Teyise (34)

Executive Head:

Business Banking Human

Resources

3

Nedbank – segmentation of business market

Business Banking

Retail

Relationship

Banking

Retail

Consumer

Banking

Individual Businesses

Business

Banking

Turnover proxy R10-700m pa incl.

complex start ups; business owners

& their household

Higher complexity

Decentralised, accountable model,

leveraging localised knowledge of

clients, industry and geography

Retail Relationship Banking

Turnover proxy R0-10m incl. start

ups; business owner; upper middle

individuals, incl seniors & their

household

Lower complexity

Centralised processes, leveraging

integrated channels

SmallBusiness Services

Start-up

R10m t/o*

R700m t/o*R1.5m pa*

R500k pa*

* Turnover & salary guideline – emphasis on client needs & complexity

Nedbank Wealth Corporate;

Capital

4

Business Banking – sustainably transformed &

competitively positioned

2005 Baseline 2013

15% main banker

market share

20% main banker market

share1

Limited client

management

capabilities

Globally ranked 2nd / 900

CMAT and 1st/ 92 SCHEMA

assessments2

Seen as the market

laggard

Rated 2nd best Business Bank

in SA3

Client loyalty at multi-year high

and ahead of peers4

Limited presence in

small business

Comprehensive, innovative

offering

Ranked as the bank of choice

for small business5

Source of

distinctiveness

• Decentralised,

accountable business

model with clear

frameworks & high

cultural alignment

• Holistic relationship

banked offering

through localised

Client Service Teams

• “Influencer” strategy

to unlock virtuous

circle

• Effective client-

centred risk culture

1 BMI-T / KPI Electronic Banking Survey (companies with annual turnover above R20m)

2 Reap Consulting independent assessment of 334 customer mgt capabilities against global best practice

3 Business Day ‘Top Business Bank’ survey 2013

4 Consulta customer satisfaction survey

5 Nedbank Small Business Tracker survey

Source: Nedbank 2013 results presentation

5

Business Banking – worldclass customer mgt

capabilities as measured by CMATTM

59

72 76

BB 2010 BB 2012 Best Ever

Overall CMAT score Intention, Reality and

Effect scores

72

82

59

73

48

60

2010 2012

Reality

Effect

Intention

2nd

highest

score5th

highest

score

What is CMAT?

• CMAT stands for Customer Management Assessment Tool. It is a diagnostic and benchmarking tool.

• The CMAT model requires that the business be assessed according to 260 practices which are then scored in three dimensions,

namely Intention, Reality and Effect.

• CMAT had a track record of 13 years and was used over 900 times by blue-chip companies across the globe as well as several

well-known JSE-listed brands.

7067

78

78

79

7271

64

71

76

72

87

88

76

83

87

86 91

73

79

72

100

47 42

35

35

40 38

43

40

37

46

55 59

57

54

51

54

46

78

56

43

55

79

Strategy andLeadership

People andOrganisation

CustomerInformation

UnderstandingCustomers

Planning theActivity

CustomerPropositions

CustomerChannels

Day-to-dayExperience

Customer ValueEnhancement

Measuringthe Impact

Working theWider Context

Best ever score

for category

NBB 2012

Top Decile Entry

B2B average2nd

highest

globally

3rd

highest

globally

Section scores

Key findings & results from CMAT report 2012

NBB has scored 72% this year, a 13% increase over 2010. This is an extremely creditable performance, placing NBB as the 2nd

highest CMAT scorer ever from any sector anywhere in the world (up from 5th). This score means that NBB has reached its 2010

Intention score in just two years, which is an excellent achievement. NBB’s Intention score has increased by 10 points, Reality scores

have leapt by 14 points (i.e. faster than Intentions), and the Effect score has improved by 12 points.

Peter Lavers, REAP Consulting

6

Business Banking – consistent, quality

performance through challenging cycle

Headline earnings (Rm)

11

21

82

5

86

6

94

4

92

9

757 744850

920 929

2009 2010 2011 2012 2013

52

40

53

34

65

2009 2010 2011 2012 2013

Credit loss ratio (bps)TTC target range:

RoE (%)

Net new primary clients (#)

26

,6

26

,4

21

,3

21

,5

19

,4

18,4 18,7 18,520,2 19,4

2009 2010 2011 2012 2013

60-80

44

6

60

1

74

8

77

5

96

5

2009 2010 2011 2012 2013

55-75

Aligned1Aligned1

1 Aligned ECAP volumes to 2013 capital ratio & endowment earnings to an assumed 8,5% interest rate; carries 24% of Group IRR - since 2009, as avg.

prime rate reduced 7pp to 8,5%, ~R1bn less endowment NII was replaced with core revenue

Source: Nedbank 2013 international investor roadshow with some refinements

7

Business Banking – strong growth momentum

across core transactional business

Growth drivers

• Client review approach to identify

cross-sell opportunities to counter

reducing volumes in challenging

economy & choice of price reduction

• Pricing disciplines & automation in fee

collections

• Rigour in contact management

(interaction frequency, touch points)

• New client acquisition, with focus on

small business

• Acquisition sales force,

complementing organic relationship

managers; shared with RRB for

optimal effectiveness

• Growth in liabilities as a consequence

of transactional client growth

• Investments in sales force

effectiveness

NIR

1 211 1 342

1 486 1 578

1 729

2009 2010 2011 2012 2013

Rm

CAGR:

+9,3%

10,7 12,1 13,5 12,1

13,5

2009 2010 2011 2012 2013

Rbn

CAC1

1 Current Account Creditor balances

CAGR:

+6,0%

8

Business Banking – market share growth

balanced with risk appetite

Market share (%)2

n = 500, R20m-2b, urban based

39 39

37

42 42

35

42

39

36

39

35 36

3433

35

27

23 23

25

2324

29

2425

24 24

21

22

28

26

20

23

21 1819

20 1518

16 16

21

20 2019

20

1415

1615

16

21

14

19 2221

20

24 23

20

19

1998 1999 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Nedbank

Risk management

principles

consistently applied

• Proactive measures

to reduce exposures

in high risk, low EP

advances

• Emphasis on primary

banked advances (no

stand-alone assets)

• Rigorous pricing for

risk, applying client

value management

principles

Initiated in 2007, with

cultural shift & impact

accelerated from 2009

9

55-7560-80

Weighted average product rate relative to

prime

bps

14,3 8,6 10,3 11,6 11,5

15,2

8,3

6,1 1,74,6

7,6

7,7

22,6

14,712,0

16,219,1

22,9

Asset payouts

Rbn

-114

-55 -27 -25 -20 -16

2008 2009 2010 2011 2012 2013

ABF, HLs & commercial mortgages

Overdrafts & other loans

Credit loss ratio (CLR)

bps

Target range

58 5240

53

34

65

2008 2009 2010 2011 2012 2013

Quality advances growth at higher pricing… …while maintaining CLR within target range

+20%Actual

Business Banking – client centred risk culture

key to quality advances & consistently low CLR

Source: Nedbank 2013 results presentation

10

Business Banking – diverse asset portfolio

Finance and insurance

28%

Private Households

19%

Manufacturing18%

Wholesale & Retail10%

Transport & communication

7%

Community & Social

7%

Agriculture6%

Construction4% Mining & Other

1%

Actual advances portfolio by sector

% of total client assets as at Dec 2013

100% = R64bn

GDP growth by sector

Indexed performance

85

90

95

100

105

110

115

120

Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan 2013 Jan 2014

Agriculture

Mining & Quarrying

Manufact.

Construction

Retail trade & accomm.

Transport & comm.

Finance& Bus Services

GDP at Market Prices

CAGR

for period

1,7%

0,1%

3,1%

Source: Nedbank 2013 results presentation

11

Business Banking & Small Business Services –

investing and innovating in the SME sectorSmall Business Index PocketPOSTM e-Commerce

Small business credit card Integrated accounting Small Business Seminars

SimplyBiz Debtor Management AppSuite for business

Cash

revolve

card

Rewards

revolve

card

12

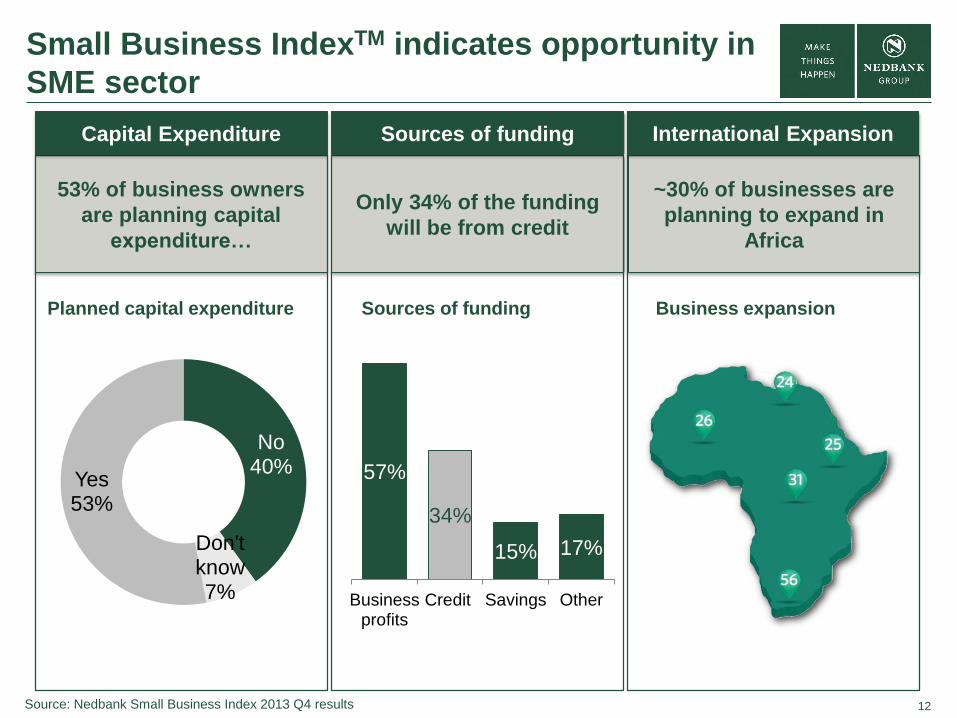

Small Business IndexTM indicates opportunity in

SME sector

~30% of businesses are

planning to expand in

Africa

53% of business owners

are planning capital

expenditure…

Only 34% of the funding

will be from credit

Capital Expenditure Sources of funding International Expansion

57%

34%

15% 17%

Businessprofits

Credit Savings Other

Sources of funding Business expansion

No40%

Don't know7%

Yes53%

Planned capital expenditure

Source: Nedbank Small Business Index 2013 Q4 results

13

Small Business Services – well positioned for

small business growth

1915 15 14 15

34 3328 28 2625

3034

31 32

16 17 1822 21

Bank for smallbusinesses and

understandstheir needs

Offer acomprehenive

range ofproducts and

services

Show anunderstandingof my business

Knowledgeableand

professionalrelationshipmanagers

Provide valueadded services

34 3330

27

28

26

21

25

2825

29

33

14 15 1619

1714

3026

26 25 2426

42 2

2008 2009 2010 2011 2012 2013

Small business market share

Businesses with <R7.5m annual turnover, %

How the banks are positioned in the minds of small business owners

2013 survey, no of respondents*

…but small business segment now well positioned for growth

1412 13 14 14

29 28 27 26 2731

2931 32

30

2224 23 23 23

Innovative intheir approach

to smallbusinesses

Offer value formoney

Best bank forstart ups

Supportsentrepreneurs

Looks after mypersonal and

banking needs

Market share has dropped…

• Small Business now represented in all branches

(from less than 38% in 2009)

• Upper middle clients serviced by all branches

(previously only 16 private banking suites)

• Nedbank Integrated Channels (NIC) cohesively

drives front line team through one aligned area

management structure (for >R60m run-rate savings

and greater effectiveness)

• Leveraging efforts with BB (e.g. marketing,

acquisition sales force, value propositions)

• Strengthened marketing presence & offering

NedbankNedbank

*Question: Excluding your primary business bank, which other ONE bank do you associate with these

statements? Source: KPI Research & strategy, Nedbank small business tracking study

Source: Nedbank 2013 Retail investor day presentation with small refinements

14

Small Business Services – seamless professional

offering to feed small business pipeline

Qualified

Professional

Entrepreneur / bus. owner

Young

Professional

Established

Professional

Student

Lifecycle of professional clients

Time

Complexity

of needs

(Youth)

(Relationship

banking)

(Private Wealth)

(Small Business/

Bus. Banking)

15

Retail & Business Banking – unlocking the

virtuous circle of household & business

Retail strategic

wheel

(capturing elements

of organisational

design)

BB Delivery model

(evolved to capture

the opportunity

around the business

owner & employees)

1. Including their household

EMPLOYEES

ENTREPRENEUR/

SMALL BUSINESS

OWNERBUSINESS

OWNER

BUSINESS SENIORSYOUTH

16

Retail & Business Banking – leveraging key

trends for distinctive positioning

Source: 2012 Investor Day Presentation; United Nations; IFC; Financial Inclusion Expert Group;

World bank – doing business; team analysis

Sources of distinctivenessTrends

Consumer preference for choice,

simplicity, increased transparency and lower

cost banking

Technological innovation (e.g. mobile &

digital, big data) offering opportunity for

lower cost distribution and process simplicity

Higher cost of capital and liquidity from

Basel regulations put risk management and

liabilities at a premium

Rising demographics and 6% p.a. small

business growth represent tomorrow’s

valued, aspirational clients

Collaborative cultures increasingly

recognised as central to organizations

effectiveness and innovation

A choice of distinctive client

centred banking experiences,

delighting in moments of truth

Integrated channels strategy leveraging digital, high potential micro-markets & optimising cost

Collaborative people culture

with a client-centred, relationship-

oriented DNA

Robust risk management for quality asset portfolios & Deposit innovation sustaining historical strength

A rigorous approach to capturing

virtuous circle of household &

business

17

Retail and Business Banking – prospects

Accelerate client gains especially SMEs, professional & seniors

Area collaboration across 213 micro-markets

Client usage of extensive product innovation

Leverage strong wholesale relationships (e.g. for Card & N@W)

Growth

potential

Sustainable

investment

Strategically well positioned to grow with downside risk protection

Zero price increase for client retention, cross-sell and growth

(R346m NIR impact in 2014)

R2,1bn in ‘Branch of the Future’ roll-out (next 5 years)

Strategic

Momentum

Compelling CVPs leveraging the influencer in household/business

Integrated channels ensuring relevance & accessibility

Shift in brand perception; client & staff metrics at multi-year highs

Source: Nedbank 2013 results presentation

18

2 086 2 324 2 472 2 543 2 731 2 860 3 411 3 521 3 818 760 949 1 356 1 808 1 287 911

907 981 1 019 2 846 3 273

3 828 4 351 4 018 3 771

4 318 4 502 4 837

2005 2006 2007 2008 2009 2010 2011 2012 2013+1275

Gross Operating

Income

(Rm)

1 705 1 799 2 033 2 055 2 120 2 339 2 722 2 936 3 119 227 162

152 330 284 210 324 206 410

2005 2006 2007 2008 2009 2010 2011 2012 2013

+80

+1064

Costs

(Rm)

2 028 2 184 2 342 2 281 2 229 2 259 2 212 2 171 2 213

2005 2006 2007 2008 2009 2010 2011 2012 2013

1333

-68

Headcount

(#, as at Dec)

Avg Prime (%)

GDP growth (%)

10,6 9,09,911,915,111,1 13,1

5,3 3,53,1(1,5)3,65,6 5,5

11

Endowment income

Income excl endowment

Impairments

Operating costs

1333

1

2,5

8,8

1333

1333

1 Aligned ECAP volumes to 2013 capital ratio & endowment earnings to an assumed 8.5% interest rate

2 Restated for internal transfers to align with Corporate Saver / TB moves in 2008

3 Imperial Bank staff

1,5

8,5

4

RoE (%)20,3 21,326,426,631,525,0 29,6 21,5 19,4

2 2 2

Aligned RoE

(%)118,3 18,518,718,415,321,7 18,6 20,2 19,4

Change

2008 - 2013

-789

Rate impact

-989

4 Based on actual Q1 (0,9), actual Q2 (3,0) and actual Q3 (0,7)

Business Banking – consistent, quality

performance through challenging cycle

Source: Nedbank 2013 results presentation

19

Business Banking – Nedbank context

Nedbank

CapitalNedbank

Corporate

Nedbank

Business Banking

Nedbank

Retail

Nedbank

Wealth

Investment banking, global

markets & treasury solutions to

institutional and corporate

clients.

Offices: SA & London

Rep offices: Angola, Toronto

Lending, deposit taking,

transactional banking, property

finance to SA corporates with

t/over >R700m p.a.

Commercial banking solutions

to small- to medium-sized

businesses with turnover of

R10m – R700m p.a.

Holistic offering for the business,

business owners / households

and employees

A bank for all financial needs of

individuals & small businesses

<R10m turnover p.a.

Transactional, card, lending,

deposit taking, risk management

and investment products /

services, as well as card-

acquiring services for business

Insurance, asset management

& wealth management solutions

Offices in SA, London, Isle of

Man, Jersey, Guernsey &

Middle East.

AUM:

R190bn

Clients amongst Top 200 SA

corporates & parastatals

Top 3 M&A player

Industry expertise:

› Infrastructure

› Mining & resources

› Oil & Gas

› Telecoms

› Energy

Top 2 SA corporate bank

>600 large corporate clients

Strong market share in public

sector loans

Continued market leadership in

commercial property finance

25 000 client groups & strong

primary clients gains

A leader in corporate saver

deposits & debtor mgt

Excellent client-centred risk

management and world-class

customer management

capabilities

Distinctive CVP’s & accountable

empowered decentralised

business model

6,4m clients (+529k y-o-y)

763 branches & alternate outlets

and 3382 ATMs

Strong positioning in household

motor finance (28% share),

household deposits (20%)

Compelling, innovative CVPs for

all segments

>10k HNW clients

AUM: >R190bn

Life embedded value: R2,1bn

Raging Bull Awards: Top 3

management company in SA

Morningstar awards: overall third

place.

SA: ranked 2nd in the ‘Up-and-

coming professionals’ category in

the 2013 SA’s Top Private Bank

survey.

International: ‘Best Private Best

Private Bank for HNW clients’

Strong Investment Banking (IB)

pipeline with more cross-sell

across businesses.

Strategic growth in Africa and

leverage Ecobank and Bank of

China.

Leverage industry expertise.

Leverage trading systems.

Participating strongly in SA’s

infrastructure build programme,

including renewable energy.

Strong client relationships.

Continued product and NIR

growth through enhanced

capabilities and primary-client

growth.

Increased Pan-African focus.

Strong risk management.

A choice of distinctive client-centred banking experiences.

A rigorous approach to capturing virtuous circle and interdependencies

between client segments.

Integrated-channels strategy leveraging mobile innovation, digital channels

and social media; selected micro markets for growth/optimisation; area

collaboration.

Robust risk management supporting strong product niches.

Liabilities innovation sustaining historical strength.

Collaborative, people-centred culture.

Explore broader complimentary

financial services growth

opportunities.

Leverage momentum in Wealth

and Asset Management.

Further CVP enhancements and

focus on service excellence.

Product expansion and delivering

client centred solutions.

Continued investment in brand

profiling.

Leverage advantage through

group collaboration.

Description

Opera

tional

overv

iew

Fin

ancia

l

metr

ics

Key s

trate

gic

drivers

AssetsHeadline

earnings AssetsHeadline

earnings AssetsHeadline

earnings AssetsHeadline

earnings

Headline

earnings

ROE: 29,4% ROE: 26,4% ROE: 19,4% ROE: 11,6% ROE: 36,2%

24% 20% 25% 26% 13% 11% 27% 29% 10%

Source: Nedbank 2013 international investor roadshow

20

Contact us & Disclaimer

Nedbank Group

www.nedbankgroup.co.za

Nedbank Group Limited

Tel: +27 (0) 11 294 4444

Physical address

135 Rivonia Road

Sandown

2196

South Africa

Download the Nedbank Investor Centre App from the

Nedbank App Suite:

Nedbank Investor Relations

Head of Investor Relations

Alfred Visagie

Direct tel: +27 (0) 11 295 6249

Cell: +27 (0) 82 855 4692

Email: [email protected]

Investor Relations Consultant

Penny Him Lok

Direct tel: +27 (0)11 295 6549

Email: [email protected]

Investor Relations Analyst

Caron Askew

Direct tel: +27 (0) 11 294 0752

Email: [email protected]

Disclaimer

Nedbank Group has acted in good faith and has made every reasonable effort to ensure the accuracy and completeness of the information contained in this document,

including all information that may be defined as 'forward-looking statements' within the meaning of United States securities legislation.

Forward-looking statements may be identified by words such as ‘believe’, 'anticipate', 'expect', 'plan', 'estimate', 'intend', 'project', 'target', 'predict' and 'hope'.

Forward-looking statements are not statements of fact, but statements by the management of Nedbank Group based on its current estimates, projections, expectations,

beliefs and assumptions regarding the group's future performance.

No assurance can be given that forward-looking statements will prove to be correct and undue reliance should not be placed on such statements.

The risks and uncertainties inherent in the forward-looking statements contained in this document include, but are not limited to: changes to IFRS and the interpretations,

applications and practices subject thereto as they apply to past, present and future periods; domestic and international business and market conditions such as exchange

rate and interest rate movements; changes in the domestic and international regulatory and legislative environments; changes to domestic and international operational,

social, economic and political risks; and the effects of both current and future litigation.

Nedbank Group does not undertake to update any forward-looking statements contained in this document and does not assume responsibility for any loss or damage

whatsoever and howsoever arising as a result of the reliance by any party thereon, including, but n limited to, loss of earnings, profits, or consequential loss or damage.