AR17/16373 26/04/2017 NOTICE OF AUDIT COMMITTEE MEETING MEMBERSHIP Mr John Comrie - Chairperson Mayor Sam Johnson Mr Chad McKnight Cr Phillip Brown Mr Alan Morris Notice is hereby given pursuant to Section 126 of the Local Government Act 1999, that an AUDIT COMMITTEE MEETING will be held in the Council Chambers, 4 Mackay Street, Port Augusta on WEDNESDAY 26 APRIL 2017 commencing at 4:00pm. A copy of the Agenda for the above meeting is attached to this notice. ANNE O’REILLY ACTING DIRECTOR CORPORATE SERVICES 21/04/2017 Civic Centre: 4 Mackay Street Port Augusta South Australia 5700 Postal Address: PO Box 1704 Port Augusta South Australia 5700 Telephone (08) 8641 9100 Facsimile (08) 8641 0357 [email protected]www.portaugusta.sa.gov.au

Transcript

AR17/16373 26/04/2017

NOTICE OF AUDIT COMMITTEE MEETING

MEMBERSHIP

Mr John Comrie - Chairperson

Mayor Sam Johnson Mr Chad McKnight Cr Phillip Brown Mr Alan Morris

Notice is hereby given pursuant to Section 126 of the Local Government Act 1999, that an AUDIT COMMITTEE MEETING will be held in the Council Chambers, 4 Mackay Street, Port Augusta on WEDNESDAY 26 APRIL 2017 commencing at 4:00pm. A copy of the Agenda for the above meeting is attached to this notice.

ANNE O’REILLY ACTING DIRECTOR CORPORATE SERVICES 21/04/2017

Civic Centre: 4 Mackay Street Port Augusta South Australia 5700

Postal Address: PO Box 1704 Port Augusta South Australia 5700

3. CONFLICT OF INTEREST 4. CONFIRMATION OF PREVIOUS MINUTES Recommendation

That the minutes of the previous Audit Committee Meeting (AR17/1820) held on 17/01/2017, be confirmed as a true and accurate record of proceedings

5. REPORTS

5.1 AR17/15878 Internal Control Update 31/03/2017 (Telephone link-up with Galpins)

5.2 AR17/15859 Audit Committee Terms of Reference Update

5.3 AR17/15960 Budget Update as at 18 April 2017

5.4 AR17/15965 Treasury Management Review 31/03/2017 5.5 2016/17 Draft Audit Committee Work Plan

6. CONFIDENTIAL REPORTS

Nil 7. NEXT MEETING Date to be determined (week of 22 May 2017) 8. DECLARE THE MEETING CLOSED

AR17/1820 17/01/2017

MINUTES OF AUDIT COMMITTEE HELD ON TUESDAY 17 JANUARY 2017

PRESENT Mayor Sam Johnson (Chairperson) Cr Colleen Hutchison Cr Phillip Brown Mr Alan Morris Mr Chad McKnight OFFICERS PRESENT Mr John Banks, Chief Executive Officer Mrs Anne O’Reilly, Acting Director Corporate Services Mrs Rebecca McCarthy, Financial Accountant WELCOME The Chairperson declared the meeting open at 4:35pm. APOLOGY/IES Nil CONFLICT OF INTEREST

Nil

MINUTES OF PREVIOUS MEETING

Alan Morris/Cr Brown that the Minutes of the previous Audit Committee Meeting (AR16/41799) held on 18/10/2016 be confirmed as a true and accurate record of proceedings. CARRIED

INTERNAL CONTROL UPDATE 31/12/2016 AR16/52885 F10/67

Alan Morris/Cr Brown that Audit Committee receives and notes the Internal Control Update as at 31 December 2016 (AR16/52885). CARRIED

MID YEAR REVIEW AS AT 21 DECEMBER 2016

Alan Morris/Cr Hutchison that Audit Committee receives and notes the Mid-Year Review as at 21 December 2016 (AR16/52884). CARRIED

ROLE OF AUDIT COMMITTEE

A report will be presented to the next Audit Committee Meeting providing a draft work program for 2017/18 and updates for the Terms of Reference for the Committee.

NEXT MEETING April 2017 The meeting was declared closed at 5:35pm.

REPORT FOR: Audit Committee MEETING DATE: 26 April 2017 REPORT FROM: Acting Director Corporate Services REPORT TITLE: Internal Control Update 31/03/2017 FILE NAME: F10/67 RECORD NO: AR17/15878 COMMUNITY VISION & STRATEGIC PLAN OUTCOMES 6 We Achieve 6.5 We use and manage our financial and physical resources in the best interests of our

community, and to ensure financial sustainability and organisational efficiency now and into the future.

PURPOSE & BACKGROUND This ‘internal control update’ report provides Audit Committee members with information regarding financial incidents and internal control processes. RECOMMENDATION Audit Committee: 1. Receives and notes the “Internal Control Update 31/03/2017” as at 31st March

2017 (AR17/15878). ______________________________________________________________________ BACKGROUND The Local Government Act 1999 (“the Act”) and the Local Government (Financial Management) Regulations 2011 (“the Regulations”) specify roles for: Councils (implementing and maintaining); and Audit Committees (reviewing the adequacy); and external auditors (considering the adequacy); and the chief executive officer and principal Member (certifying the adequacy); of internal controls. Section 125 of the Act provides: “A council must ensure that appropriate policies, practices and procedures of internal control are implemented and maintained in order to assist the council to carry out its activities in an efficient and orderly manner to achieve its objectives, to ensure adherence to management policies, to safeguard the council’s assets, and to secure (as far as possible) the accuracy and reliability of council records.” Section 126 (4) (c) of the Act identifies one of the functions of an Audit Committee as: “reviewing the adequacy of the accounting, internal control, reporting and other financial management systems and practices of the council on a regular basis.”

Section 129 (1) (b) of the Act requires the auditor to audit: “the controls exercised by the council during the relevant financial year in relation to the receipt, expenditure and investment of money, the acquisition and disposal of property and the incurring of liabilities.” Section 129 (3) (b) of the Act requires the auditor to provide:1 “an audit opinion as to whether the controls audited under subsection (1)(b) are sufficient to provide reasonable assurance that the financial transactions of the council have been conducted properly and in accordance with law.” Regulations 14 (e) of the Regulations requires the chief executive officer and the principal member of the Council and the chair of the board of management of a Council subsidiary or regional subsidiary to sign a statement, certifying that: “internal controls implemented by the council, council subsidiary or regional subsidiary (as the case may be) provide a reasonable assurance that its financial records are complete, accurate and reliable and were effective throughout the financial year.” Regulation 19 (1) (b) of the Regulations requires that: “an audit of the internal controls of a council referred to in section 129(1)(b) of the Act must be carried out in accordance with the Australian Standards on Assurance Engagements published (and amended from time to time) by the Auditing and Assurance Standards Board established under the Australian Securities and Investment Commission Act 2001 of the Commonwealth.” Regulation 19 (3) of the Regulations provides: “in forming an opinion for a council under section 129(3)(b) of the Act, the auditor must assess the internal controls of the council referred to in section 129(1)(b) of the Act based on criteria in the Better Practice Model – Internal Financial Controls.” In response to the new Regulation, the SA Local Government Financial Management Group and Deloitte developed the Better Practice Model. This model explains the areas of council financial risk and what controls should be in place to mitigate this risk. It contains 328 core controls and a large number of additional controls.

DISCUSSION 2016/17 Interim Audit Report The 2016/17 Interim Audit was conducted by Galpins during the period 22-24 February 2017. A draft report has been received for response. There were no “high risk” items identified.

Galpins have indicated that they will be present at the Audit Committee to discuss their findings. Financial Incidents There has been two financial incidents during the period 1st January 2017 to 31st March 2017. These incidents occurred on 3rd February 2017 and 26th March 2017. Details of these incidents and subsequent investigations will be tabled at the Audit Committee meeting. Better Practice Model As discussed at the previous Audit Committee meeting, the Better Practice Model is still in draft and will be tabled at a future Audit Committee once finalised.

1.1 Background During our interim audit, we perform procedures to gain an understanding of the internal controls in place relevant to the financial statements, and perform tests of design and effectiveness for these controls. Based on the results of the control testing, we then assess the audit risks to define the extent and nature of our substantive procedures (e.g. inspection of documents, recalculation, reconciliation, etc.) for our final visit. Amendments to s129 of the Local Government Act 1999 require auditors to provide an opinion regarding internal controls of councils. This applies to prescribed (metropolitan) councils from 2013-14 onwards, and to non-prescribed (regional) councils from 2015-16 onwards. This opinion focuses on councils’ obligations under s125 of the Local Government Act 1999:

“A council must ensure that appropriate policies, practices and procedures of internal control are implemented and maintained in order to assist the council to carry out its activities in an efficient and orderly manner to achieve its objectives, to ensure adherence to management policies, to safeguard the council's assets, and to secure (as far as possible) the accuracy and reliability of council records.”

The audit opinion is restricted per s129 of the Act to the application of s125 as it relates to financial internal controls, specifically the controls exercised by the council during the relevant financial year in relation to the receipt, expenditure and investment of money, the acquisition and disposal of property and the incurring of liabilities. In order to assist the Council in addressing the requirements of s129, we have reviewed a prioritised list of controls from the better practice model based on our initial audit risk assessment. See more details about our scope in the item 1.2 of this report.

1.2 Objectives and Scope The objectives of our interim audit were to:

understand Council’s business, business cycles and processes relevant to the financial statements

understand the internal controls in place for the areas we consider critical for the audit of the financial statements

design internal controls tests for the internal controls identified perform the internal controls tests to determine the final risks of material

misstatements in the financial statements to be addressed in our final audit. review a prioritised list of internal financial controls we consider critical for the

purpose of issuing a controls opinion. This financial year the scope of our audit was extended to include a review of internal controls we consider key controls to be in place for the purpose of addressing the requirements of s129.

4

These key internal controls consist of a prioritised list of controls from the better practice model. This list was defined based on our risk assessment to determine the key business cycles, and key risks within these business cycles, that we understand should be the focus of the Council’s control self-assessment. The identification of key core controls and key business risks included the following risk assessment procedures: Risk Review – A review of Council’s inherent risk assessment for internal financial controls. Financial Statement Review – A high level financial statement review performed to identify key accounts and transaction streams. Internal / External Audit Results Review – The findings and recommendations of internal / external financial audits are reviewed to identify known areas of weakness, and areas known to be attracting audit attention. The key core controls for the following key business cycles have been identified as critical for the purpose of issuing a controls opinion next financial year:

Fixed Assets Purchasing and Procurement Contracting Rates / Rates Rebates Payroll Accounts Payables Debtors Receipting Banking General ledger.

We have included a list of key controls identified by the audit for these business cycles as an appendix to this report (see Appendix 1). This list does not represent a complete population of internal controls that the Council should have in place. There is an expectation that controls not in this list will still exist and be operating effectively within Council. The list of controls is only intended to be a guide for Council to prioritise its resourcing in readiness for the new audit opinion, and for the ongoing monitoring of internal controls i.e. it is a risk based listing of controls which may be desirable for Council to include in its ongoing monitoring program for internal financial controls. The list should not be considered a minimum standard – rather, it is a starting reference point for Council to consider. It is expected that Council will have performed a risk assessment of financial risks, and given consideration to the need to monitor controls that address High / Extreme risks that may not be included in this listing. The control descriptions are as per the Better Practice Model, and have not been personalised to the Council. Council may have different descriptions of controls that address the same risk provided by the better practice model. Council may consider tailoring the controls description to better describe the actual controls in place.

5

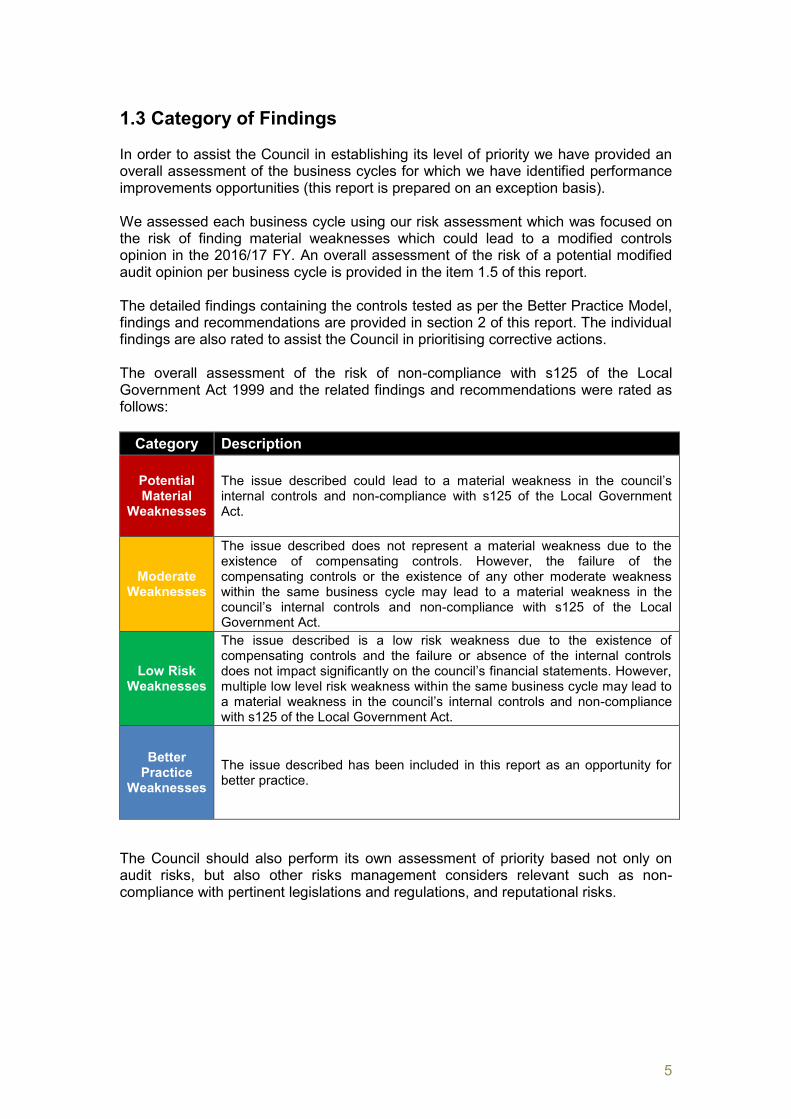

1.3 Category of Findings In order to assist the Council in establishing its level of priority we have provided an overall assessment of the business cycles for which we have identified performance improvements opportunities (this report is prepared on an exception basis). We assessed each business cycle using our risk assessment which was focused on the risk of finding material weaknesses which could lead to a modified controls opinion in the 2016/17 FY. An overall assessment of the risk of a potential modified audit opinion per business cycle is provided in the item 1.5 of this report. The detailed findings containing the controls tested as per the Better Practice Model, findings and recommendations are provided in section 2 of this report. The individual findings are also rated to assist the Council in prioritising corrective actions. The overall assessment of the risk of non-compliance with s125 of the Local Government Act 1999 and the related findings and recommendations were rated as follows:

Category Description

Potential Material

Weaknesses

The issue described could lead to a material weakness in the council’s internal controls and non-compliance with s125 of the Local Government Act.

Moderate Weaknesses

The issue described does not represent a material weakness due to the existence of compensating controls. However, the failure of the compensating controls or the existence of any other moderate weakness within the same business cycle may lead to a material weakness in the council’s internal controls and non-compliance with s125 of the Local Government Act.

Low Risk Weaknesses

The issue described is a low risk weakness due to the existence of compensating controls and the failure or absence of the internal controls does not impact significantly on the council’s financial statements. However, multiple low level risk weakness within the same business cycle may lead to a material weakness in the council’s internal controls and non-compliance with s125 of the Local Government Act.

Better Practice

Weaknesses The issue described has been included in this report as an opportunity for better practice.

The Council should also perform its own assessment of priority based not only on audit risks, but also other risks management considers relevant such as non-compliance with pertinent legislations and regulations, and reputational risks.

6

1.4 Overall Review of the Council’s Internal Controls Overall, the Council demonstrated further progress towards the implementation of an internal control framework consistent with the principles within the Better Practice Model. The principles underpinning the model were used by the Council in the identification of its business cycles, the establishment of its internal controls and the implementation of its risk management processes. During our interim visit, we noted that an increased number of the key internal controls reviewed were in place and were operating effectively (65 out of 78 core controls reviewed, compared to 53 out of 78 in 2015/16). The most significant areas of improvement were Rates/Rates Rebates and Accounts Payable. The area of concern (IT access controls) that resulted in a qualification to the internal controls opinion in 2015-16 has been addressed satisfactorily. There are no new issues identified in our audit processes to date that pose a risk of qualification for 2016-17. A summary of the results of our review is provided in the table below:

Audit identified no high risk findings. We recommend that Council prioritises the moderate risk findings as failure of compensating controls addressing the same risk or existence of any other moderate weakness within the same business cycle may lead to a material weakness and non-compliance with s125 of the Local Government Act. We noted that Council was in the process of establishing mechanisms to ensure ongoing monitoring of effectiveness of the internal controls. Many of the findings provided in this report had already been identified by Council during its own self-assessment. Council already has plans in place to make the necessary improvements.

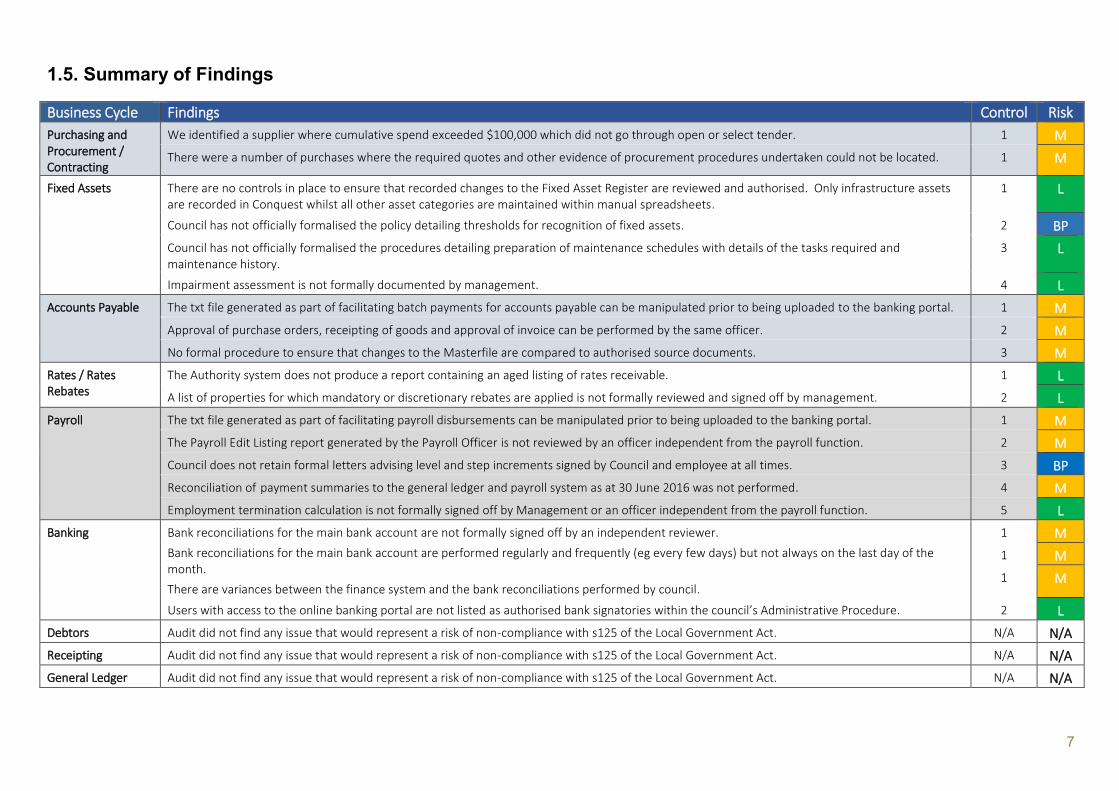

1.5. Summary of Findings Business Cycle Findings Control Risk

Purchasing and Procurement / Contracting

We identified a supplier where cumulative spend exceeded $100,000 which did not go through open or select tender. 1 M

There were a number of purchases where the required quotes and other evidence of procurement procedures undertaken could not be located. 1 M

Fixed Assets

There are no controls in place to ensure that recorded changes to the Fixed Asset Register are reviewed and authorised. Only infrastructure assets are recorded in Conquest whilst all other asset categories are maintained within manual spreadsheets.

1 L

Council has not officially formalised the policy detailing thresholds for recognition of fixed assets. 2 BP

Council has not officially formalised the procedures detailing preparation of maintenance schedules with details of the tasks required and maintenance history.

3 L

Impairment assessment is not formally documented by management. 4 L

Accounts Payable The txt file generated as part of facilitating batch payments for accounts payable can be manipulated prior to being uploaded to the banking portal. 1 M

Approval of purchase orders, receipting of goods and approval of invoice can be performed by the same officer. 2 M

No formal procedure to ensure that changes to the Masterfile are compared to authorised source documents. 3 M

Rates / Rates Rebates

The Authority system does not produce a report containing an aged listing of rates receivable. 1 L

A list of properties for which mandatory or discretionary rebates are applied is not formally reviewed and signed off by management. 2 L

Payroll The txt file generated as part of facilitating payroll disbursements can be manipulated prior to being uploaded to the banking portal. 1 M

The Payroll Edit Listing report generated by the Payroll Officer is not reviewed by an officer independent from the payroll function. 2 M

Council does not retain formal letters advising level and step increments signed by Council and employee at all times. 3 BP

Reconciliation of payment summaries to the general ledger and payroll system as at 30 June 2016 was not performed. 4 M

Employment termination calculation is not formally signed off by Management or an officer independent from the payroll function. 5 L

Banking Bank reconciliations for the main bank account are not formally signed off by an independent reviewer.

Bank reconciliations for the main bank account are performed regularly and frequently (eg every few days) but not always on the last day of the month.

There are variances between the finance system and the bank reconciliations performed by council.

1 M

1 M

1 M

Users with access to the online banking portal are not listed as authorised bank signatories within the council’s Administrative Procedure. 2 L

Debtors Audit did not find any issue that would represent a risk of non-compliance with s125 of the Local Government Act. N/A N/A

Receipting Audit did not find any issue that would represent a risk of non-compliance with s125 of the Local Government Act. N/A N/A

General Ledger Audit did not find any issue that would represent a risk of non-compliance with s125 of the Local Government Act. N/A N/A

8

2. DETAILED AUDIT FINDINGS 2.1 Purchasing and Procurement / Contracting

Control Risk Findings Recommendations Management Response

1. Robust and transparent selection processes to ensure effective and qualified suppliers / contractors are selected by Council, including compliance with Code of Conduct, Conflict of Interest and procurement Policies.

Moderate Risk

Weakness

We conducted procurement testing across a sample of purchases to verify they were in accordance with Councils’ procurement policy and procedures.

Purchases over $100,000 and below $300,000.

The Procurement and Tendering policy requires an open or selective tender as the procurement method for purchases (above) $100,000 and below $300,000.

As part of our audit, we noted one supplier with cumulative spending in excess of $100,000 that did not go through either a selective or open tender. The supplier and current expenditure information is provided below.

Bou & Lam Pty Ltd – Current expenditure in 2017 is $119,906.88

Purchases over $20,000.01 and below $100,000.

The Procurement and Tendering policy requires that at a minimum 3 written quotes be obtained for purchases over $20,000 and below $100,000.

No evidence of written quotes obtained have been provided for the following suppliers:

LH Perry & Sons Pty Ltd –

Current expenditure of $73,991.54 for the 2016/17 financial year. We note that this supplier is likely to exceed $100,000 cumulative spend within the financial year.

Kemps Credit Solution –

Council to include greater guidance in the policy in relation to cumulative spend to ensure consideration of cumulative spend with each supplier in its procurement practices is undertaken.

Council to maintain evidence of procurement documentation such as request for tenders, tender responses, evaluation forms detailing the decision made.

Where a decision is made to not follow procurement policy, council to document reasoning and approvals for the exemption and maintain as part of council records.

Bou & Lam CEO verbal permission had been granted for this supplier back in 2014. Kemps Credit Solutions Kemps have a current LG Procurement Panel Contract Council has recently adopted a revision to the Purchasing, Contracts & Tendering Policy. The Policy has now been updated to include an Exemption Form. Council is participating in a procurement project with other Spencer Gulf Cities and has flagged procurement as an issue to be considered as part of the planned organisation restructure.

9

Control Risk Findings Recommendations Management Response

Current expenditure of $59,525.69 for the 2016/17 financial year.

10

2.2 Fixed Assets

Control Risk Findings Recommendations Management Response

1. Recorded changes to the Fixed Asset Register (FAR) and/or Masterfile are approved by management, compared to authorised source documents and General Ledger to ensure accurate input.

Moderate Risk

Weakness

There are no controls in place to ensure that recorded changes to the FAR master file are reviewed and authorised.

Management is not aware of any report that Conquest can generate to report changes to the asset master file (e.g. unit rates, useful lives, condition assessment, etc.)

In addition, only infrastructure assets are recorded in Conquest. All other category of assets are maintained in manual spreadsheets.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Council to investigate with Conquest IT provider whether it is possible to generate an audit trail of changes to the asset master file.

Council to consider using the software to record all category of assets.

Council is meeting with Tonkin’s to discuss full utilisation of Conquest capabilities.

2. Council has an asset accounting policy which details thresholds for recognition of fixed assets.

Better Practice

Weakness

In response to previous recommendation from the interim audit conducted for the 2015/16 financial year, Council has developed a formal asset accounting policy which details thresholds for recognition of fixed assets.

The policy is currently in the draft stage.

Council to formally adopt asset accounting policy.

Council to adopt the asset accounting policy in the coming months.

3. Asset maintenance schedules are prepared, updated, and monitored by management and activity per the asset maintenance history register are compared to source documents to ensure that they were input accurately.

Low Risk Weakness

Council does not have formal procedures detailing preparation of maintenance schedules containing details of the tasks required and record of maintenance history.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Council to develop a formal procedure detailing preparation of maintenance schedules and record of maintenance history.

This is being investigated as part of the Asset Management Plan finalisation and full utilisation of Conquest.

4. The annual review of assets includes reviewing the appropriateness of categories of assets and impairment testing.

Low Risk Weakness

Impairment assessment is not formally documented by management.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

We recommend council to request asset officers to sign off impairment declarations for each category of assets.

The declaration should include a statement saying that to the best of

To be implemented for 2016/17 financial year (end of year process)

11

Control Risk Findings Recommendations Management Response their knowledge there have been no assets impaired this FY. If any asset was impaired the officers should include a list of assets impaired in the document.

12

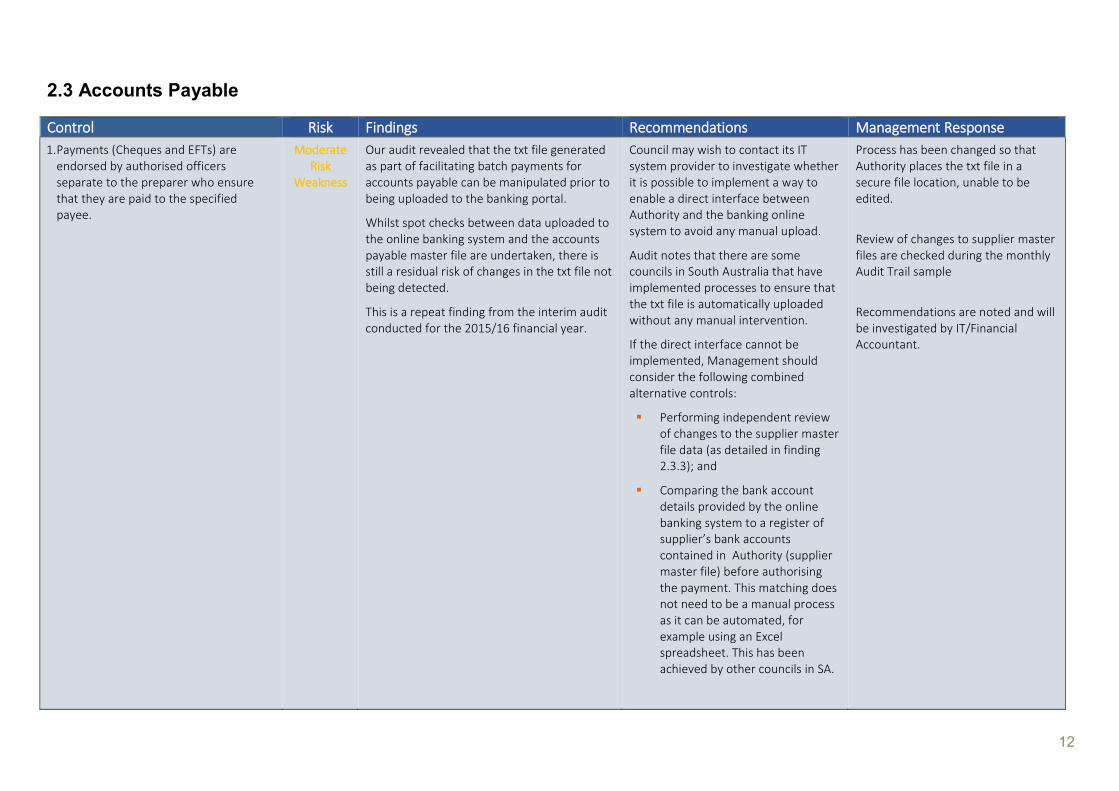

2.3 Accounts Payable

Control Risk Findings Recommendations Management Response

1. Payments (Cheques and EFTs) are endorsed by authorised officers separate to the preparer who ensure that they are paid to the specified payee.

Moderate Risk

Weakness

Our audit revealed that the txt file generated as part of facilitating batch payments for accounts payable can be manipulated prior to being uploaded to the banking portal.

Whilst spot checks between data uploaded to the online banking system and the accounts payable master file are undertaken, there is still a residual risk of changes in the txt file not being detected.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Council may wish to contact its IT system provider to investigate whether it is possible to implement a way to enable a direct interface between Authority and the banking online system to avoid any manual upload.

Audit notes that there are some councils in South Australia that have implemented processes to ensure that the txt file is automatically uploaded without any manual intervention.

If the direct interface cannot be implemented, Management should consider the following combined alternative controls:

Performing independent review of changes to the supplier master file data (as detailed in finding 2.3.3); and

Comparing the bank account details provided by the online banking system to a register of supplier’s bank accounts contained in Authority (supplier master file) before authorising the payment. This matching does not need to be a manual process as it can be automated, for example using an Excel spreadsheet. This has been achieved by other councils in SA.

Process has been changed so that Authority places the txt file in a secure file location, unable to be edited.

Review of changes to supplier master files are checked during the monthly Audit Trail sample

Recommendations are noted and will be investigated by IT/Financial Accountant.

13

Control Risk Findings Recommendations Management Response

2. Individuals who authorise payment of suppliers are authorised officers who are independent of the processing of invoices

Moderate Risk

Weakness

Approval of purchase order, receipting of goods and approval of invoice for payment can be performed by the same officer.

We note that council has informed us of the lack of staffing resources to achieve full compliance of this control from the previous year’s management letter.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Council to ensure adequate segregation of duties among officers who issue POs, receipt goods and approve invoices for payment.

This is an ongoing issue due to lack of staffing resources. To be considered during organisation restructure & procurement project.

3. Recorded changes to the supplier master file are compared to authorised source documents to ensure that they were input accurately.

Moderate Risk

Weakness

We note that there is no formal procedure to ensure that changes to the Masterfile are compared to authorised source documents.

An audit trail of changes to the supplier Masterfile to be generated at the time of facilitating the batch payment.

Changes to supplier details to then be verified to the authorised source documents when reviewing the batch payments listing. This review to be conducted by an officer (Financial Accountant) independent of the Accounts Payable function prior to approving and facilitating the batch payment.

Process to be reviewed.

14

2.4 Rates / Rates Rebates

Control Risk Findings Recommendations Management Response

1. Regular independent review of the rates aged receivables reports and independent check of rates payable by rates staff.

Low Risk Weakness

The Authority system does not produce a report containing an aged listing of rates receivable.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

In addition, the Rates Officer has not completed a declaration form declaring what properties (if any) they own within the council area.

Council to contact the IT provider to investigate ways to produce an aged listing of rates receivable.

Council to ensure staff that prepare rates notices complete a declaration stating any properties that they own within the council area.

This will allow appropriate steps to ensure independent review of rates notices issued to rates officers.

Council Rates Officers have now provided a statement that they do not own any properties in the Port Augusta City Council area.

2. Council approves rate rebates to rate payers in accordance with Delegations of Authority and as per legislation.

Low Risk Weakness

A list of properties for which mandatory or discretionary rebates are applied is not formally reviewed and signed off by management.

We note council has informally reviewed list of discretionary rates, but minutes of this meeting have not been yet formally accepted.

Council to ensure that a list of properties where mandatory or discretionary rebates are applied be reviewed and signed off on an annual basis.

Rate Rebates policy and process has been recently reviewed. Report for 2017/18 year will be provided to Council for formal sign off.

15

2.5 Payroll

Control Risk Findings Recommendations Management Response

1. The transfer of the bank file is restricted to authorised officers who are not involved in the preparation of the pay run.

Moderate Risk

Weakness

Audit reviewed the process of payroll payments and noted the following:

Council’s financial system Authority generates an ABA file which is stored on council’s internal drive prior to being manually uploaded into the online banking system. The ABA file can be opened as a TXT file and manipulated prior to being uploaded.

Council may wish to contact its IT system provider to investigate whether it is possible to implement a way to enable a direct interface between Authority and the banking online system to avoid any manual upload.

Audit noted that there are some councils in South Australia that have implemented processes to ensure that the txt file is automatically uploaded without any manual intervention.

Further investigation to be conducted regarding this process.

2. Payroll system generates exception reports detailing all payroll changes that are regularly reviewed by management who investigate & approve variances.

Moderate Risk

Weakness

The Payroll Edit Listing report generated by the Payroll Officer, and containing all payroll changes and amounts to be paid for each employee, is not reviewed by an officer independent from the payroll function.

The payroll officer performs a review of this report to certify the accuracy of the amounts presented and to certify that the report represents a list of bona-fide employees of the Council.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Council to ensure that the Pay Edit Listing report is reviewed by an officer independent from the payroll function.

Process to be reviewed.

3. Employee records to include employment details and/or contract terms and conditions, authorisations for payroll deductions and leave entitlements.

Better Practice-

Weakness

As per different EBAs and Awards, yearly increments of step levels are conditional to a number of different criteria including:

hours of experience;

automatic increases based on performance assessment; and

qualification and certificates.

Council to ensure that levels and steps increments are signed by Council and employee at all times.

Audit acknowledges that most of the time these increments are documented by email.

16

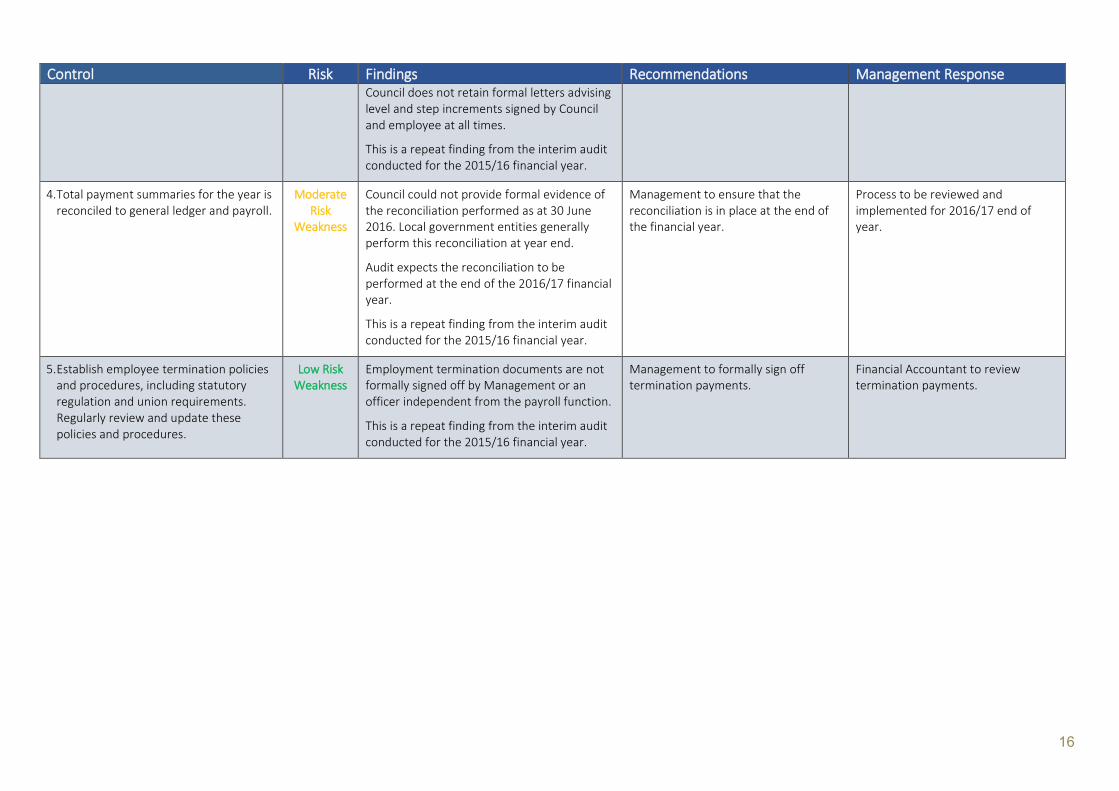

Control Risk Findings Recommendations Management Response Council does not retain formal letters advising level and step increments signed by Council and employee at all times.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

4. Total payment summaries for the year is reconciled to general ledger and payroll.

Moderate Risk

Weakness

Council could not provide formal evidence of the reconciliation performed as at 30 June 2016. Local government entities generally perform this reconciliation at year end.

Audit expects the reconciliation to be performed at the end of the 2016/17 financial year.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Management to ensure that the reconciliation is in place at the end of the financial year.

Process to be reviewed and implemented for 2016/17 end of year.

5. Establish employee termination policies and procedures, including statutory regulation and union requirements. Regularly review and update these policies and procedures.

Low Risk Weakness

Employment termination documents are not formally signed off by Management or an officer independent from the payroll function.

This is a repeat finding from the interim audit conducted for the 2015/16 financial year.

Management to formally sign off termination payments.

Financial Accountant to review termination payments.

17

2.6 Banking

Control Risk Findings Recommendations Management Response

1. Bank reconciliations are performed on a predetermined basis and are reviewed by an authorised officer. Any identified discrepancies are investigated immediately.

Moderate Risk

Weakness

Bank reconciliations for the main bank account are not formally signed off by an independent reviewer.

Bank reconciliations for the main bank account are performed regularly and frequently (eg every few days). However, reconciliations are not always performed as at the last day of the month.

Discrepancies on the bank statement:

We noted variances between the finance system and the bank reconciliations performed by council.

We confirmed during the walkthrough process that this is due to the finance system not allowing for partial receipting of cash & EFT at the end of day.

Bank reconciliations to be independently reviewed and signed as evidence of review.

End of month bank reconciliations to be undertaken for the main bank account.

It is worth noting that councils in South Australia that use the Authority system who have been able to rectify the issue of partial receipting of cash and EFT at the end of day.

Council may wish to contact these councils to gain an understanding of how this issue can be resolved.

Financial Accountant reviews and signs the Bank Reconciliation

Authority has recently installed a patch which splits the cash and EFT deposits.

2. EFT bank signatories is restricted to appropriately designated personal.

Low Risk Weakness

We noted that the Manager of Wadlata has access to the online banking system. However, they are not listed as an authorised bank signatory within the council’s Administrative Procedure.

The council to update the Administrative Procedure to include the Manager of Wadlata or amend the access rights to the banking system.

The manager of Wadlata was given access to view only the Wadlata Website Account to check that website sales had been processed. This access has not been required for some time and she is set to “No Access” in Business Banking Online.

18

APPENDIX 1 – CRITICAL INTERNAL FINANCIAL CONTROLS

19

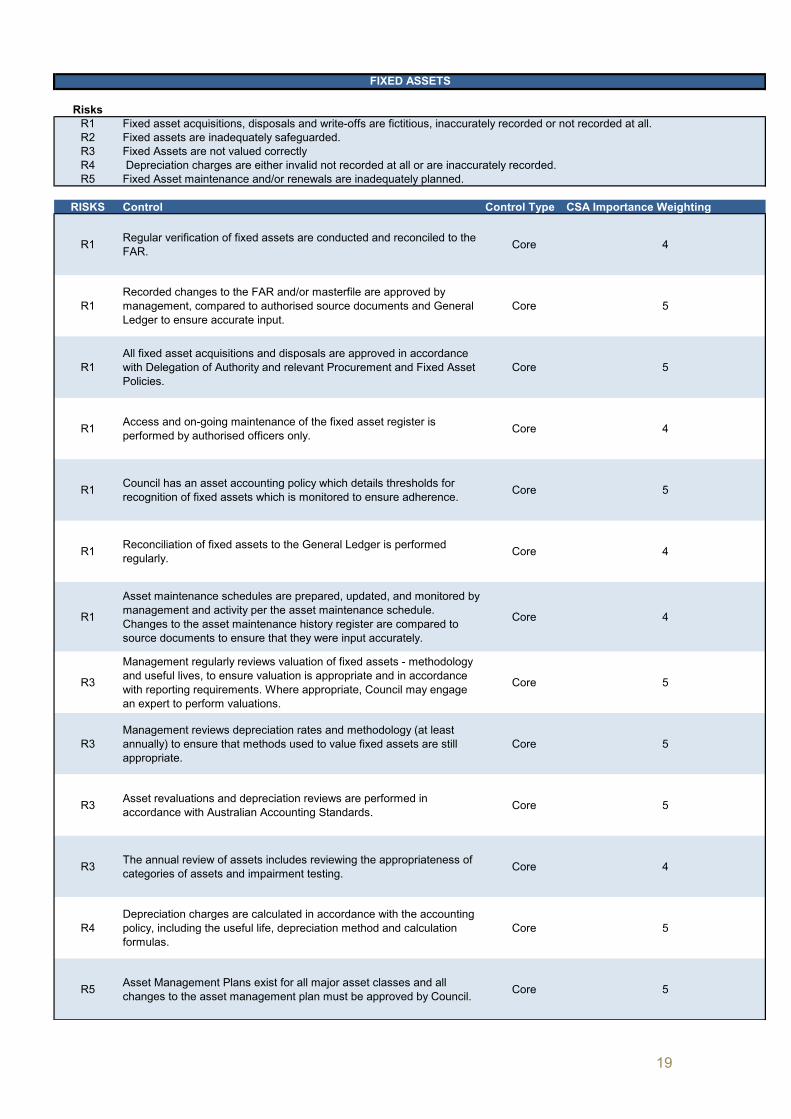

RisksR1 Fixed asset acquisitions, disposals and write-offs are fictitious, inaccurately recorded or not recorded at all.R2 Fixed assets are inadequately safeguarded.R3 Fixed Assets are not valued correctlyR4 Depreciation charges are either invalid not recorded at all or are inaccurately recorded.R5 Fixed Asset maintenance and/or renewals are inadequately planned.

RISKS Control Control Type CSA Importance Weighting

R1 Regular verification of fixed assets are conducted and reconciled to the FAR. Core 4

R1Recorded changes to the FAR and/or masterfile are approved by management, compared to authorised source documents and General Ledger to ensure accurate input.

Core 5

R1All fixed asset acquisitions and disposals are approved in accordance with Delegation of Authority and relevant Procurement and Fixed Asset Policies.

Core 5

R1 Access and on-going maintenance of the fixed asset register is performed by authorised officers only. Core 4

R1 Council has an asset accounting policy which details thresholds for recognition of fixed assets which is monitored to ensure adherence. Core 5

R1 Reconciliation of fixed assets to the General Ledger is performed regularly. Core 4

R1

Asset maintenance schedules are prepared, updated, and monitored by management and activity per the asset maintenance schedule. Changes to the asset maintenance history register are compared to source documents to ensure that they were input accurately.

Core 4

R3

Management regularly reviews valuation of fixed assets - methodology and useful lives, to ensure valuation is appropriate and in accordance with reporting requirements. Where appropriate, Council may engage an expert to perform valuations.

Core 5

R3Management reviews depreciation rates and methodology (at least annually) to ensure that methods used to value fixed assets are still appropriate.

Core 5

R3 Asset revaluations and depreciation reviews are performed in accordance with Australian Accounting Standards. Core 5

R3 The annual review of assets includes reviewing the appropriateness of categories of assets and impairment testing. Core 4

R4Depreciation charges are calculated in accordance with the accounting policy, including the useful life, depreciation method and calculation formulas.

Core 5

R5 Asset Management Plans exist for all major asset classes and all changes to the asset management plan must be approved by Council. Core 5

FIXED ASSETS

20

RisksR1 Council does not obtain value for money in its purchasing & procurement.R2 Purchases of goods and services are made from non-preferred suppliers.R3 Purchase orders are either recorded inaccurately or not recorded at all.R4 Purchase orders are placed for unapproved goods and services.

RISKS Control Control Type CSA Importance Weighting

R1 Council has a comprehensive Contract and Procurement Policy that is reviewed regularly. Core 5

R1, R2, R4 Employees must ensure all purchase orders are approved in accordance with the Delegations of Authority and relevant policies. Core 5

R3 Purchase orders are issued in accordance with the Council’s Purchasing and Procurement Policy. Core 5

PURCHASING AND PROCUREMENT

RisksR1R2 Council does not obtain value for money in relation to its Contracting.

RISKS Control Control Type CSA Importance Weighting

R1,R2

Robust and transparent selection processes to ensure effective and qualified suppliers / contractors are selected by Council, including compliance with Code of Conduct, Conflict of Interest and procurement Policies.

Core 5

R1 Council to maintain a contract register. Core 4

R1 The Contracts, Tenders and Procurement Policy and Procedures should be reviewed regularly. Core 4

R2 Council does not release milestone payments to suppliers / contractors until they meet all their associated objectives. Core 5

CONTRACTING

Council is not able to demonstrate that all probity issues have been addressed in the Contracting process.

21

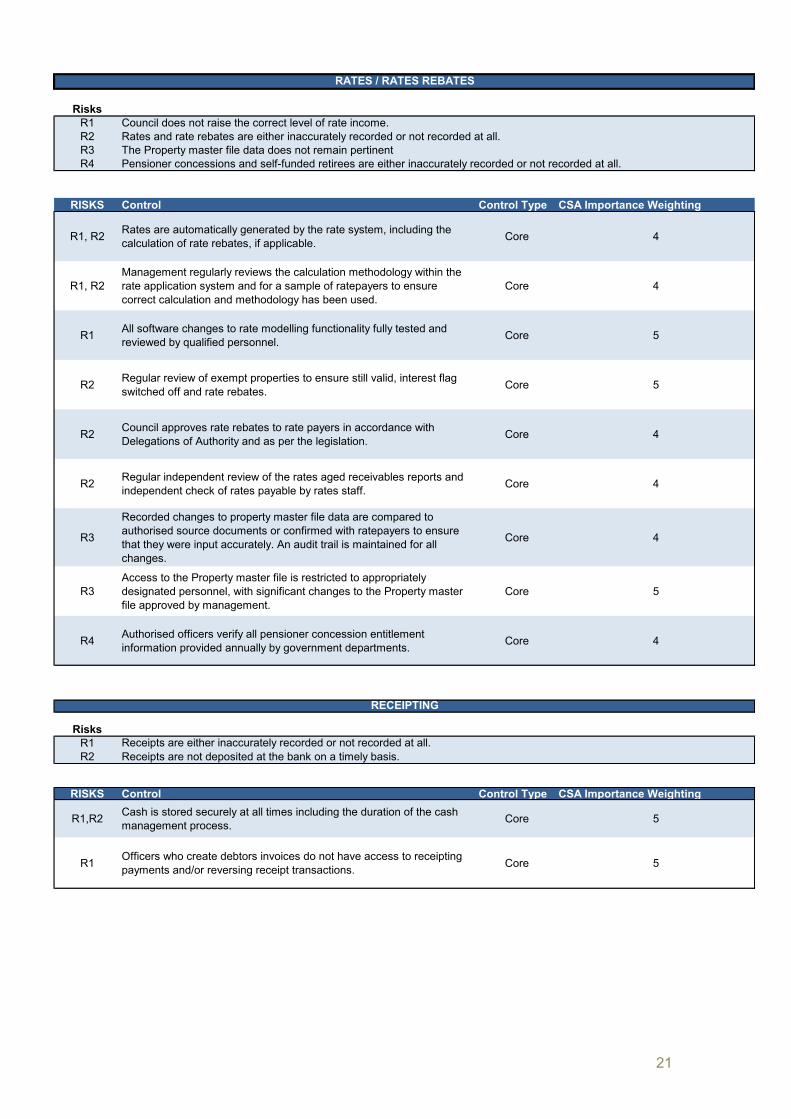

RisksR1 Council does not raise the correct level of rate income.R2 Rates and rate rebates are either inaccurately recorded or not recorded at all.R3 The Property master file data does not remain pertinentR4 Pensioner concessions and self-funded retirees are either inaccurately recorded or not recorded at all.

RISKS Control Control Type CSA Importance Weighting

R1, R2 Rates are automatically generated by the rate system, including the calculation of rate rebates, if applicable. Core 4

R1, R2Management regularly reviews the calculation methodology within the rate application system and for a sample of ratepayers to ensure correct calculation and methodology has been used.

Core 4

R1 All software changes to rate modelling functionality fully tested and reviewed by qualified personnel. Core 5

R2 Regular review of exempt properties to ensure still valid, interest flag switched off and rate rebates. Core 5

R2 Council approves rate rebates to rate payers in accordance with Delegations of Authority and as per the legislation. Core 4

R2 Regular independent review of the rates aged receivables reports and independent check of rates payable by rates staff. Core 4

R3

Recorded changes to property master file data are compared to authorised source documents or confirmed with ratepayers to ensure that they were input accurately. An audit trail is maintained for all changes.

Core 4

R3Access to the Property master file is restricted to appropriately designated personnel, with significant changes to the Property master file approved by management.

Core 5

R4 Authorised officers verify all pensioner concession entitlement information provided annually by government departments. Core 4

RATES / RATES REBATES

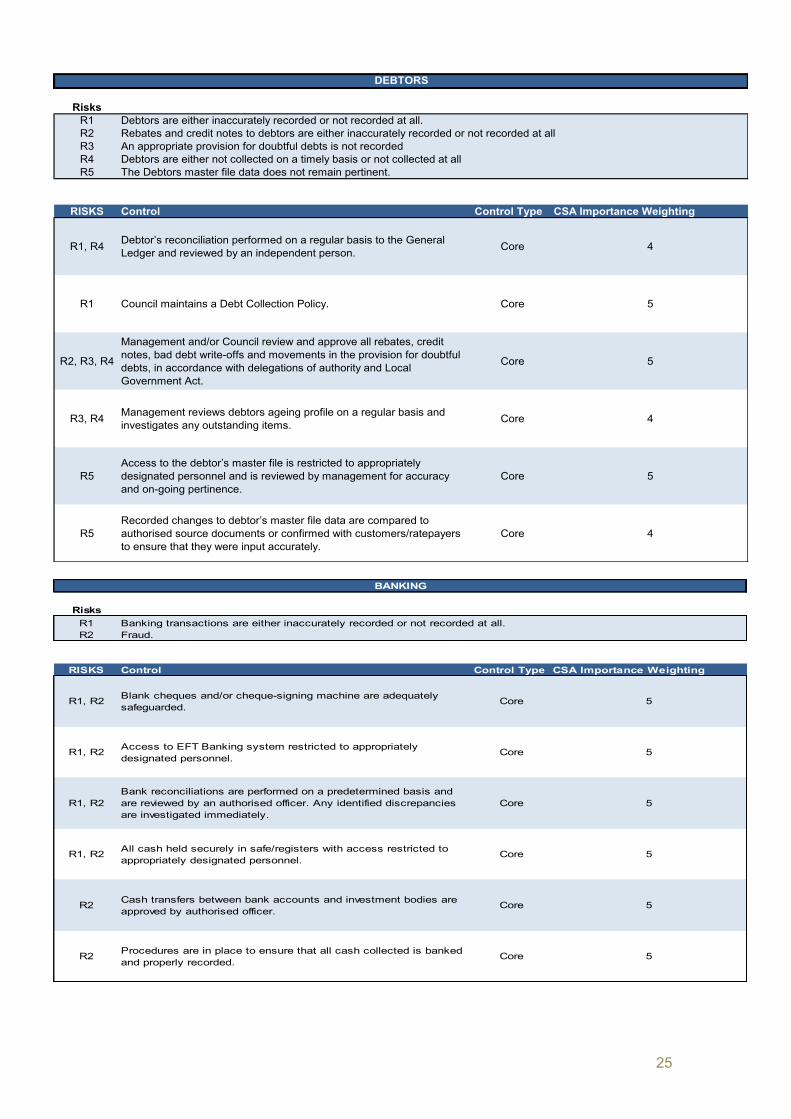

RisksR1 Receipts are either inaccurately recorded or not recorded at all.R2 Receipts are not deposited at the bank on a timely basis.

RISKS Control Control Type CSA Importance Weighting

R1,R2 Cash is stored securely at all times including the duration of the cash management process. Core 5

R1 Officers who create debtors invoices do not have access to receipting payments and/or reversing receipt transactions. Core 5

RECEIPTING

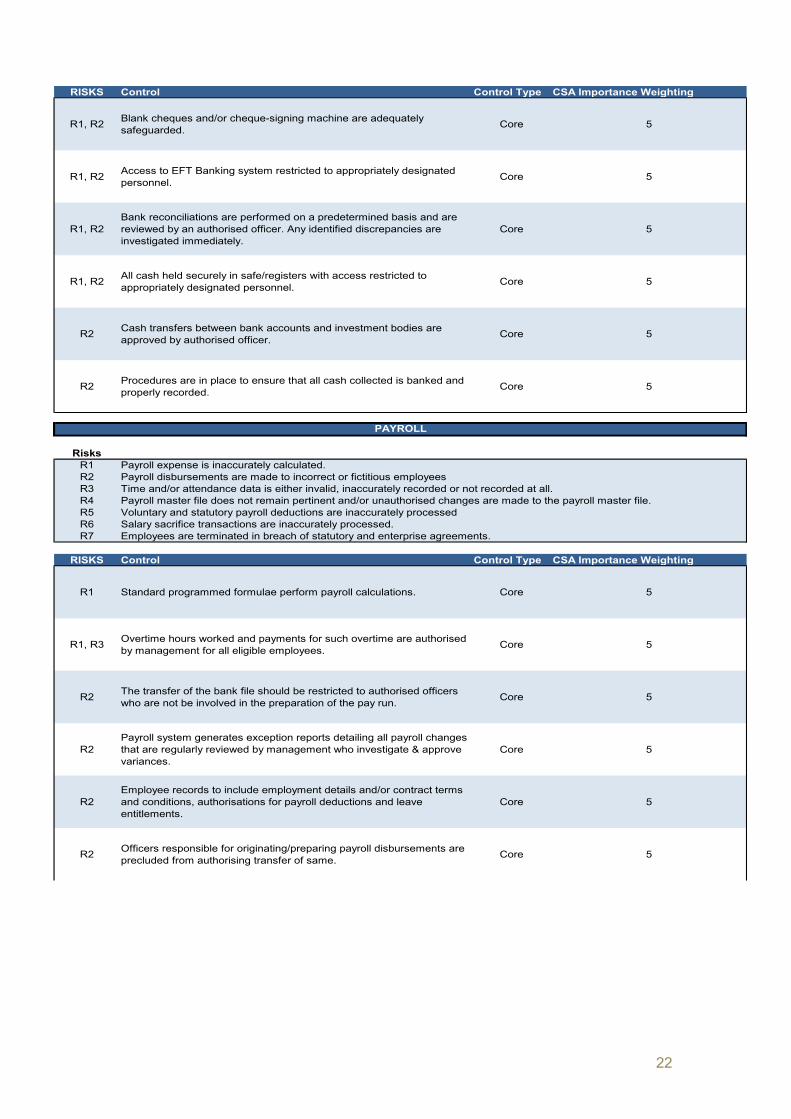

22

RISKS Control Control Type CSA Importance Weighting

R1, R2 Access to EFT Banking system restricted to appropriately designated personnel. Core 5

R1, R2Bank reconciliations are performed on a predetermined basis and are reviewed by an authorised officer. Any identified discrepancies are investigated immediately.

Core 5

R1, R2 All cash held securely in safe/registers with access restricted to appropriately designated personnel. Core 5

R2 Cash transfers between bank accounts and investment bodies are approved by authorised officer. Core 5

R2 Procedures are in place to ensure that all cash collected is banked and properly recorded. Core 5

RisksR1R2 Payroll disbursements are made to incorrect or fictitious employeesR3 Time and/or attendance data is either invalid, inaccurately recorded or not recorded at all.R4 Payroll master file does not remain pertinent and/or unauthorised changes are made to the payroll master file.R5 Voluntary and statutory payroll deductions are inaccurately processedR6 Salary sacrifice transactions are inaccurately processed.R7 Employees are terminated in breach of statutory and enterprise agreements.

RISKS Control Control Type CSA Importance Weighting

R1 Standard programmed formulae perform payroll calculations. Core 5

R1, R3 Overtime hours worked and payments for such overtime are authorised by management for all eligible employees. Core 5

R2 The transfer of the bank file should be restricted to authorised officers who are not be involved in the preparation of the pay run. Core 5

R2Payroll system generates exception reports detailing all payroll changes that are regularly reviewed by management who investigate & approve variances.

Core 5

R2Employee records to include employment details and/or contract terms and conditions, authorisations for payroll deductions and leave entitlements.

Core 5

R2 Officers responsible for originating/preparing payroll disbursements are precluded from authorising transfer of same. Core 5

PAYROLL

Payroll expense is inaccurately calculated.

23

RisksR1R2 Data contained within the General Ledger is permanently lost.

RISKS Control Control Type CSA Importance Weighting

R1, R2 All updates and changes to General Ledger programmes are authorised, tested and documented. Core 5

R1, R2 Access to General Ledger maintenance is restricted to authorised personnel. Core 5

R1General Ledger reconciliations (including control and clearing accounts) are prepared on a regular basis; all reconciliations independently reviewed.

Core 4

R1 Manual journal entries recorded in the register are authorised by the officer preparing the journal and an independent reviewer. Core 5

R1, R2 Off-site backup of data, program and documentation. Core 4

R1 System does not allow posting of unbalanced journals. Core 5

R1 Amendments to the structure of the General Ledger framework are approved by an authorised officer. Core 5

R1, R2General Ledger policies and procedures are appropriately created, updated & communicated to relevant personnel in the finance department.

Core 5

R2 Formal disaster recovery plan adopted by Council or Senior Executive. Core 5

GENERAL LEDGER

General Ledger does not contain accurate financial information

24

RisksR1R2 Credit notes and other adjustments to accounts payable are either inaccurately recorded or not recorded at allR3 Disbursements are not authorised properly.R4 Accounts are not paid on a timely basisR5 Supplier master file data does not remain pertinent and/or unauthorised changes are made to the supplier master file.

RISKS Control Control Type CSA Importance Weighting

R1, R2, R4Statements received from suppliers are reconciled to the supplier accounts in the accounts payable subledger regularly and differences are investigated.

Core 4

R1 Invoices received are authorised and accompanied by appropriate supporting documentation. Core 5

R1Payments (Cheques and EFT’s) are endorsed by authorised officers separate to the preparer who ensure that they are paid to the specified payee.

Core 5

R2 Access to the supplier master file is restricted to authorised officers. Core 5

R2, R5 Separation of Accounts Payable and Procurement duties. Core 5

R3 All disbursements must be approved by an authorised officer in accordance with relevant policies and/or Delegations of Authority. Core 5

R3Purchase Orders must be raised for the purchase of goods and services in line with the Council's Procurement policy or over a predetermined amount where applicable.

Core 5

R3 Individuals who authorise payment of suppliers are authorised officers who are independent of the processing of invoices. Core 5

R4 Authorised officer to review aged payables listing on a predetermined basis and investigate where appropriate. Core 5

R5 Recorded changes to the supplier master file are compared to authorised source documents to ensure that they were input accurately. Core 5

R5 The accounts payable system and or supplier master file prevents users from making unauthorised adjustments to supplier accounts. Core 5

ACCOUNTS PAYABLE

Accounts payable amounts and disbursements are either inaccurately recorded or not recorded at all

25

RisksR1R2 Rebates and credit notes to debtors are either inaccurately recorded or not recorded at allR3 An appropriate provision for doubtful debts is not recordedR4 Debtors are either not collected on a timely basis or not collected at allR5 The Debtors master file data does not remain pertinent.

RISKS Control Control Type CSA Importance Weighting

R1, R4 Debtor’s reconciliation performed on a regular basis to the General Ledger and reviewed by an independent person. Core 4

R1 Council maintains a Debt Collection Policy. Core 5

R2, R3, R4

Management and/or Council review and approve all rebates, credit notes, bad debt write-offs and movements in the provision for doubtful debts, in accordance with delegations of authority and Local Government Act.

Core 5

R3, R4 Management reviews debtors ageing profile on a regular basis and investigates any outstanding items. Core 4

R5Access to the debtor’s master file is restricted to appropriately designated personnel and is reviewed by management for accuracy and on-going pertinence.

Core 5

R5Recorded changes to debtor’s master file data are compared to authorised source documents or confirmed with customers/ratepayers to ensure that they were input accurately.

Core 4

DEBTORS

Debtors are either inaccurately recorded or not recorded at all.

RisksR1R2 Fraud.

RISKS Control Control Type CSA Importance Weighting

R1, R2 Blank cheques and/or cheque-signing machine are adequately safeguarded.

Core 5

R1, R2 Access to EFT Banking system restricted to appropriately designated personnel.

Core 5

R1, R2Bank reconciliations are performed on a predetermined basis and are reviewed by an authorised officer. Any identified discrepancies are investigated immediately.

Core 5

R1, R2 All cash held securely in safe/registers with access restricted to appropriately designated personnel.

Core 5

R2 Cash transfers between bank accounts and investment bodies are approved by authorised officer.

Core 5

R2 Procedures are in place to ensure that all cash collected is banked and properly recorded.

Core 5

BANKING

Banking transactions are either inaccurately recorded or not recorded at all.

REPORT FOR: Audit Committee MEETING DATE: 26 April 2017 REPORT FROM: Acting Director Corporate Services REPORT TITLE: Audit Committee Terms of Reference Update FILE NAME: F10/67 RECORD NO: AR17/15859 COMMUNITY VISION & STRATEGIC PLAN OUTCOMES 6 We Achieve 6.3 We aim to provide good governance practices and compliance with all legislative

requirements in delivery of services. 6.5 We use and manage our financial resources in the best interests of our community,

and to ensure financial sustainability and organisational efficiency now and into the future.

PURPOSE To advise Audit Committee members of the updated Audit Committee Terms of Reference and Audit Committee membership as endorsed by Council at a Council Meeting on 27/03/2017. RECOMMENDATION Audit Committee: 1. Notes the updated Terms of Reference as attached.

BACKGROUND Section 126 of the Local Government Act sets out requirements for Council’s to have an audit committee and the membership and functions of that committee. It is preferable for independent members to have appropriate qualifications and experience in accounting, finance and risk management. At a Council meeting held on 27th March 2017, Council resolved to:

1. Accept Cr Hutchison’s resignation from the Audit Committee and thank her for her service to this Committee.

2. Appoint Mr John Comrie as an independent member of Council’s Audit Committee for a period to 30th November 2018.

3. Accepts Mayor Johnson’s resignation as Chairperson of the Audit Committee. 4. Appoints Mr John Comrie as Chairperson of the Audit Committee. 5. Amends the Terms of Reference for the Audit Committee to reflect the above

changes.

2

DISCUSSION

Cr Hutchison advised in writing of her resignation from Council’s Audit Committee. Cr Hutchison is thanked for her commitment to the Audit Committee over recent years. Council previously had the expertise of Mr John Ewen, a senior local government Auditor who conducted Council’s external audit for many years on the Audit Committee. Following Mr Ewen’s resignation and with the changes in key positions within Management, it was considered prudent for Council to appoint an independent member with a strong background in Local Government finance to the Audit Committee. Mr John Comrie has extensive experience in Local Government finance and is currently a member of other Local Government Audit Committees. John has previously provided training through the Local Government Association to Audit Committee members and Council staff on the role of Audit Committees. Current membership of the Audit Committee for all Independent Members ends on 30th November 2018. Mayor Johnson has provided his resignation as Chairperson of the Audit Committee, however intends to remain on the Audit Committee as one of two Elected Members allowed under the Terms of Reference. Mr John Comrie indicated his willingness to take on the role of Chairperson if appointed to the Audit Committee. John’s expertise would support current members of the Audit Committee to undertake roles and responsibilities as per the Local Government Act. The Terms of Reference for the Committee with proposed amendments is attached to this report for Members’ information. CONFIDENTIALITY PROVISIONS n/a RISK MANAGEMENT 1: Financial/Budget Audit Committee sitting fees are included within the Mayor & Elected Member expenditure. Sitting fees for Independent Members are $300 per meeting attended. It is considered appropriate for a travel allowance to be paid to Mr Comrie for attendance at Audit Committee meetings. 2: Legal/Policy Section 126 of the Local Government Act sets out Council’s obligations in relation to Audit Committees. 3: Environment/Planning n/a 4: Community

4.1 General The Port Augusta community has an expectation that Council will undertake sound financial management. The Audit Committee has a role in reviewing Council’s financial management.

4.2 Aboriginal Community Consultation n/a

Anne O’Reilly 18/04/2017

3

Audit Committee

Terms of Reference

PREAMBLE A Committee of Council may be established by resolution of the Council. A Committee can be established to assist the Council in the performance of its functions, to inquire into and report to the Council on matters, provide advice to the Council and to exercise, perform or discharge delegated powers, functions or duties. Pursuant to Section 41(10) of the Local Government Act 1999 the establishment of a committee does not derogate from the power of the Council to act in a matter. 1. Establishment of the Audit Committee Pursuant to Sections 126 and 41 of the Local Government Act 1999 the Council

establishes a Committee to be known as the Audit Committee (referred to in these Terms of Reference as ‘the Committee’).

2. Committee Objectives To report and provide advice to Council on its financial reporting and

sustainability, internal controls and risk management systems, whistleblowing, and internal and external auditing processes.

3. Committee Activities

i) Financial Reporting (a) The Committee shall monitor the integrity of the financial statements of

the Council, including its annual report, reviewing significant financial reporting issues and judgments which they contain.

(b) The Committee shall review and challenge where necessary:

1) the consistency of, and/or any changes to, accounting policies;

2) the methods used to account for significant or unusual transactions where different approaches are possible;

3) whether the Council has followed appropriate accounting standards and made appropriate estimates and judgments, taking into account the views of the external auditor;

4) the clarity of disclosure in the Council’s financial reports and the context in which statements are made; and

5) all material information presented with the financial statements, such as the operating and financial review and the corporate governance statement (insofar as it relates to the audit and risk management).

4

ii) Internal Controls and Risk Management Systems

The Committee shall: (a) keep under review the effectiveness of the Council’s internal controls and

risk management systems; and

(b) review and recommend the approval, where appropriate, of statements to be included in the annual report concerning internal controls and risk management.

[Note: it is important that the Audit Committee understands the business of

the Council to appreciate the risks it manages on a daily basis, and to ensure that there are appropriate management plans to manage and mitigate this business risk. This will include insurance matters, financial reporting, legal and regulatory compliance, business continuity, and statutory compliance. This can be facilitated by discussions with the external auditors and by presentations by Management on how business risks are identified and managed.

iii) Whistleblowing The Committee shall review the Council’s arrangements for its employees to

raise concerns, in confidence, about possible wrongdoing in financial reporting or other matters. The Committee shall ensure these arrangements allow independent investigation of such matters and appropriate follow-up action.

iv) External Audit The Committee shall:

(a) develop and implement a policy on the supply of non-audit services by the external auditor, taking into account any relevant ethical guidance on the matter;

(b) consider and make recommendations to the Council, in relation to the appointment, re-appointment and removal of the Council’s external auditor. The Committee shall oversee the selection process for new auditors and if an auditor resigns the Committee shall investigate the issues leading to this and decide whether any action is required;

(c) oversee Council’s relationship with the external auditor including, but not limited to:

1) recommending the approval of the external auditor’s remuneration,

whether fees for audit or non-audit services, and recommending whether the level of fees in appropriate to enable an adequate audit to be conducted;

2) recommending the approval of the external auditor’s term of engagement, including any engagement letter issued at the commencement of each audit and the scope of the audit;

3) assessing the external auditor’s independence and objectivity taking into account relevant professional and regulatory requirements and the extent of Council’s relationship with the auditor, including the provision of any non-audit services;

5 4) satisfying itself that there are no relationships (such as family,

employment, investment, financial or business) between the external auditor and the Council (other than in the ordinary course of business).

5) monitoring the external auditor’s compliance with legislative requirements on the rotation of audit partners; and

6) assessing the external auditor’s qualifications, expertise and resources and the effectiveness of the audit process (which shall include a report from the external auditor on the Audit Committee’s own internal quality procedures.

(d) meet as needed with the external auditor. The Committee shall meet the external auditor at least once a year, without Management being present; to discuss the external auditor’s report and any issues arising from the audit;

(e) review and make recommendations on the annual audit plan and in

particular its consistency with the scope of the external audit engagement;

(f) review the findings of the audit with the external auditor. This shall

include, but not be limited to, the following:

1) a discussion of any major issues which arose during the external audit;

2) any accounting and audit judgments; and

3) level of errors identified during the external audit. The Committee shall also review the effectiveness of the external audit.

(g) review any representation letter(s) requested by the external auditor

before they are signed by Management;

[Note that these representation letters are a standard practice of any audit and provide the auditor confirmation from Management, (in particular the Director Corporate Services) that, amongst other matters, accounting standards have been consistently applied, that all matters that need to be disclosed have been so disclosed and that the valuation of assets has been consistently applied].

(h) review the management letter and Management’s response to the

external auditor’s findings and recommendations; (i) at least once a year, review its own performance, constitution and Terms

of Reference to ensure it is operating at maximum effectiveness and recommend changes it considers necessary to the Council for approval.

(j) give due consideration to laws and regulations of the Local Government

Act 1999.

4. Membership: The membership of the Audit Committee shall be at least 2 Elected Members and

2 Independent Members. The Membership of the Audit Committee comprises the following:

Elected Members: Mayor Sam Johnson and Cr Phillip Brown Independent Members: Mr Chad McKnight, Mr Alan Morris, & Mr John Comrie.

6 Council Officers may attend meetings as observers only.

Council’s external auditor may be invited to attend meetings to provide advice to the Committee.

5. Presiding Member of the Committee The Chairperson is appointed by Council. Council appointed Mr John Comrie as

the Chairperson of the Audit Committee. 6. Term of Office Elected Members are appointed for a 4 year term and this terminates at the end

of each Council term. Independent Members term will conclude on 30 November 2018. 7. Reporting Arrangements The Committee reports and makes recommendations to the Council on any item

on the Committee agenda. Appropriate Officers will forward reports to the Committee for consideration on

matters that relate to Council’s financial reporting and sustainability, internal controls and risk management systems, whistleblowing, and internal and external auditing processes.

8. Confidentiality The confidential provisions of the Local Government Act 1999 shall apply to ALL

members of the Committee. This in short means that those matters that are deemed to be ‘confidential’ (which includes the report discussions and any resulting decision) must remain confidential, and is not to be discussed outside the forum of the Committee Meeting, until the matter is discussed and determined by the Council. There are substantial penalties for breaches of confidentiality.

9. Delegated Authority The Committee has authority to seek any information it requires from any

employee of the Council (after advising the Chief Executive Officer in order to perform its duties and to obtain, at the Council’s expense, (after consultation with the Chief Executive Officer) outside legal or other professional advice on any matter within its Terms of Reference.

10. Conduct and Conflict of Interest of Committee Members Elected Members of the Committee must comply with the Code of Conduct for

Elected Members as published by the Minister for Planning for the purposes of Section 63 (1) of the Local Government Act 1999 and Chapter 5 Part 4 of the Local Government Act 1999 relating to Conduct and Disclosure of Interests.

As a member of the Committee, you must not make improper use of your

position to gain (directly or indirectly) an advantage for yourself or for another person closely associated with you. You must make sure there is no conflict between your private interests and your role as a public decision maker. As a Committee Member you will have to declare what your interest is in any matter before the Committee.

7 11. Meeting Times & Place The Audit Committee shall meet at least four times a year at appropriate times in

the reporting and audit cycle. Meetings are held in the Council Chamber, Civic Centre, 4 Mackay Street, Port Augusta on a day and time determined as acceptable to all Members.

12. Quorum & Voting by Members The quorum shall be 50% of the number of members, plus one. Each member of the Committee present at a relevant meeting, must vote of any

motion put at that meetings. The Presiding Member shall have a deliberative vote but does not in the event of

an equality of votes have a casting vote. 13. Meeting Procedures Meetings of the Audit Committee will be held in accordance with:

i) Local Government Act 1999 ii) Local Government (Procedures at Meetings) Regulations 2013 iii) Council’s Code of Practice – Meeting Procedures 1.1.15 iv) Council’s Code of Practice – Access to Council and Committee Meetings and

Documents 1.1.06

14. Access and Documents Pursuant to Section 87 of the Local Government Act 1999 a minimum of three

clear days’ notice of the meeting, accompanied by the agenda, will be provided to Members of the Committee and the public.

Minutes will be available within five clear days after a meeting in accordance with

Section 91 of the Local Government Act 1999 and will be provided to all Members of the Committee and placed on Council’s Website www.portaugusta.sa.gov.au and a hardcopy placed in the Council Office, Civic Centre, 4 Mackay Street, Port Augusta.

Members of the public are able to attend all meetings of the Committee, unless

excluded from the meeting by the confidentiality provision of Section 90 of the Local Government Act 1999.

NOTE: For the purposes of the calculation of clear days in relation to the giving

of notice before a meeting, the day on which the notice is given, and the day on which the meeting occurs, will not be taken into account; and Saturdays, Sundays and public holidays will be taken into account. However, if a notice is given after 5pm on a day, the notice will be taken to have been given on the next day.

15. Responsible Officer Director Corporate Services 16. Liability and Insurance Pursuant to Section 80 of the Local Government Act 1999 Council must take out a

policy of insurance insuring every member of the Council, and a spouse, domestic partner or another person who may be accompanying a member of the Council, against risks associated with the performance or discharge of official functions or duties by members.

8 Further, pursuant to Section 41(12) of the Local Government Act 1999 no civil

liability attaches to a member of a committee for an honest act or omission in the exercise, performance or discharge, or purported exercise, performance or discharge, of the member’s or committee’s powers, functions or duties.

17. Administrative Support The Chief Executive Officer shall provide sufficient administrative support to the

Committee to adequately carry out its functions. The Executive Officer – Director Corporate Services shall be the Council Officer

responsible for fulfilling the executive role for the Committee including arranging the preparation of agendas, ensuring reports are provided as required and ensuring that Committee decisions are implemented.

The Committee shall:

i) have access to reasonable resources in order to carry out its duties; [Note that this is subject to any budget allocation being approved by Council ii) be provided with appropriate and timely training, both in the form of an

induction program for new members and on an ongoing basis for all members;

18. Sitting Fee Council has approved a Sitting Fees for meetings attended by the Members of the

Audit Committee. The Sitting Fees are as follows: Elected Members –Member Allowances apply as determined by the Remuneration

Tribunal Independent Members - $300 per meeting attended

REPORT FOR: Audit Committee MEETING DATE: 26 April 2017 REPORT FROM: Acting Director Corporate Services REPORT TITLE: Budget Update as at 18 April 2017 FILE NAME: F10/67 RECORD NO: AR17/15960 COMMUNITY VISION & STRATEGIC PLAN OUTCOMES 6 We Achieve 6.5 We use and manage our financial resources in the best interests of our community,

and to ensure financial sustainability and organisational efficiency now and into the future.

PURPOSE This ‘Budget Update’ report is required under the Local Government (Financial Management) Regulations 2011. RECOMMENDATION Audit Committee: 1. Receives and notes the “Budget Update” as at 18 April 2017 (AR17/15960). BACKGROUND Under the Local Government (Financial Management) Regulations 2011: (1) A council must prepare and consider the following reports: (a) at least twice, between 30 September and 31 May (both dates inclusive) in the relevant financial year report showing a revised forecast of its operating and capital investment activities for the relevant financial year compared with the estimates for those activities set out in the budget presented in a manner consistent with the note in the Model Financial Statements entitled Uniform Presentation of Finances; (b) between 30 November and 15 March (both dates inclusive) in the relevant financial year—a report showing a revised forecast of each item shown in its budgeted financial statements for the relevant financial year compared with estimates set out in the budget presented in a manner consistent with the Model Financial Statements. (2) A council must also include in a report under subregulation (1)(b) revised forecasts for the relevant financial year of the council's operating surplus ratio, net financial liabilities ratio and asset sustainability ratio compared with estimates set out in the budget presented in a manner consistent with the note in the Model Financial

DISCUSSION Attached for members’ information is a budget update as at 18th April 2017. The 2016/17 budgeted operating deficit is $3.578M. At this stage, the forecasted operating deficit is $3.271M. This prediction is based on current year to date figures as well as knowledge of activities scheduled for coming months. Employee costs are forecast to be lower than budget due to several vacant positions across the Council. Savings will be offset by an increase of depreciation by approx. $2.3M compared to 2015/16 ($1.6M more than budgeted) due to the revaluations of all asset classes, and particularly the removal of residual values and inclusion of Central Oval.

RISK MANAGEMENT 1: Financial/Budget As per attached. 2: Legal/Policy n/a 3: Environment/Planning n/a 4: Community

4.1 General n/a

4.2 Aboriginal Community Consultation n/a Anne O’Reilly 18/04/2017

PORT AUGUSTA CITY COUNCIL

BUDGET UPDATEFOR THE PERIOD ENDING 18 APRIL 2017

2015-16AUDITED

2016-17BUDGET

2016-17YTD ACTUAL

2016-17FORECAST

Income 36,826,855 37,600,500 30,871,161 38,528,322less Expenses 39,867,920 41,179,100 30,773,070 41,799,992

(3,041,065) (3,578,600) 98,090 (3,271,669)

less Net Outlays on Existing AssetsCapital Expenditure on renewal and replacement of Existing Assets 1,615,856 2,048,900 790,028 1,667,900less Depreciation, Amortisation and Impairment (5,602,200) (6,379,400) (6,456,692) (7,994,000)less Proceeds from Sale of Replaced Assets (103,182) (100,000) (81,818) (100,000)

(4,089,526) (4,430,500) (5,748,482) (6,426,100)

less Net Outlays on New and Upgraded Assets

Capital Expenditure on New and Upgraded Assets (Including investment property & real estate developments) 2,362,303 1,000,000 493,774 1,381,000less Amounts specifically for New and Upgraded Assets (458,000) (762,000) (500,000) (762,000)

less Proceeds from Sale of Surplus Assets (including investment property and real estate developments) - - - -

1,904,303 238,000 (6,226) 619,000

Net Lending / (Borrowing) for Financial Year (855,842) 613,900 5,852,799 2,535,431

REPORT FOR: Audit Committee MEETING DATE: 26 April 2017 REPORT FROM: Acting Director Corporate Services REPORT TITLE: Treasury Management Review 31/03/2017 FILE NAME: F10/67 RECORD NO: AR17/15965 COMMUNITY VISION & STRATEGIC PLAN OUTCOMES 6 We Achieve 6.3 We aim to provide good governance practices and compliance with all legislative

requirements in delivery of services. 6.5 We use and manage our financial resources in the best interests of our community,

and to ensure financial sustainability and organisational efficiency now and into the future.

PURPOSE This ‘Treasury Management Review’ report provides Audit Committee members with information regarding Councils debt (fixed debenture loans and variable cash advances). RECOMMENDATION Audit Committee: 1. Receives and notes the “Treasury Management Review 31/3/2017” as at 31

March 2017 (AR17/15965).

BACKGROUND The Local Government Association Financial Sustainability Information Paper No. 15 – Treasury Management provides information regarding the key elements of treasury management and a model policy. Council’s Treasury Management Policy 2.6.11 provides clear direction to management, workers and Council in relation to the treasury function. It underpins Council’s decision-making regarding the financing of its operations as documented in its annual budget and long-term financial plan and associated projected and actual cash flow receipts and outlays. The Treasury Management Policy establishes a decision framework to ensure that: a) funds are available as required to support approved outlays b) interest rate and other risks (e.g. liquidity and investment credit risks) are acknowledged and responsibly managed c) the net interest costs associated with borrowing and investing are reasonably likely to be minimised on average over the longer term.

2 The Council’s Treasury Management Strategy is to restructure its portfolio of borrowings, as old borrowings mature and new ones are raised, to progressively achieve, and then maintain, not less than 30% of its gross debt on average in any year in the form of variable interest rate borrowings. The Treasury Management Policy requires that “at least once a year Council’s Audit Committee shall receive a specific report regarding treasury management performance relative to this policy document. The report shall highlight:

• for each Council borrowing and investment – the quantum of funds, its interest rate and maturity date, and changes in the quantum since the previous report; and

• the proportion of fixed interest rate and variable interest rate borrowings at the end date of the reporting period and an estimate of the average of these proportions across this period along with key reasons for significant variances compared with the targets specified in this policy.”

DISCUSSION

Please find attached a listing of Councils fixed interest rate Debenture Loans, and variable interest Cash Debentures. The portion of fixed and variable debt is shown in a percentage, to be compared with the Treasury Management target. From July 2016 to March 2017, the average percentage is as follows: Variable 45.8% Fixed 54.2% CONFIDENTIALITY PROVISIONS n/a RISK MANAGEMENT 1: Financial/Budget n/a 2: Legal/Policy n/a 3: Environment/Planning n/a 4: Community

4.1 General The Port Augusta community has an expectation that Council will undertake sound financial management. The Audit Committee has a role in reviewing Council’s financial management.

4.2 Aboriginal Community Consultation n/a

Anne O’Reilly 18/04/2017

3

PORT AUGUSTA CITY COUNCIL - TREASURY MANAGEMENT

No Details Cost Code AUTH TAKEN % YEARS AMOUNT Bal 30.6.2016 JUL AUG SEP OCT NOV DEC JAN FEB MARDebentures 02 /

PORT AUGUSTA CITY COUNCIL AUDIT COMMITTEE WORK PLAN

PROJECT ACTIONS PLANNED DATE COMMENTS/STATUS DATE COMPLETED1 FINANCIAL REPORTING

• ensure consistency between plans

• review appropriateness of targets established by Council for financial subsustainability indicators

• review appropriateness of assumptions included in the development of LTFP and IAMP

• comment on Draft ABP & Budget prior to formal consideration for adoption by Council• ensure consistency with strategic management plans

• ensure statutory information is included

• provide comment on ongoing financial sustainability

• review integrity of AFS

• review clarity of disclosures