Occasional Paper - 21 •f.:v.''.!ii.rt%VI ^'''!^iM,}S^X^^^tv...U^ .raifri-^->;..%<£ Recovery Management in Rural Credit mm^^^.M^^i'^mstm^^Mmmm'¥^^mM K.C. SHARMA RJOSH J C MISHRA SANJAY KUMAR R. AMALORPAVANATHAN R. BHASKARAN \T/ National Bank for Agriculture and Rural Developnnent Munnbai 2001

\T/ National Bank for Agriculture and Rural Developnnent

Munnbai

2001

Occasional Paper - 21

Recovery Managennent in Rural Credit

K.C, SHARMA R JOSH

J.C. MISHRA SANJAY KUIVIAR

R. AMALORPAVANATHAN R. BHASKARAN

\T/ National Bonk for Agriculture and Rural Developnnent

Munnbai

2001

Published by National Bank for Agriculture and Rural Development, Department of Economic Analysis and Research, 4th floor, 'C Wing, Plot No. C-24, 'G' Block, Bandra-Kuria Complex, P.B. No. 8121, Bandra(East), Mumbai - 400 051. Printed at Shubhamkaroti Printers, Ghatkopar (E), Mumbai.

ii

Acknowledgement

Authors are grateful to National Bank for Agriculture and Rural Development (NABARD)

for commissioning this occasional paper to Bankers Institute of Rural Development (BIRD).

Authors prepared the paper as a team. The views expressed are those of the authors and are

not in any way attributed to the Institute they belong. The authors are thankful to DEAR,

NABARD for reviewing the paper and offering critical comments for revision. Some revision

has been done but all could not be done due to lack of relevant disaggregated data. Many

thanks to Arindam Chakrabarty for his patient typing and cheerful attitude while carrying out

editorial corrections over many drafts of the paper.

October, 2001 Authors BIRD, Lucknow

III

Authors

K.C. Sharma, P.Josh, R.Amaiorpavanathan and J.C.MIshra are Faculty Members, BIRD, Lucknow.

Sanjay Kumar Is Faculty Associate, BIRD, Lucknow

R.Bhaskaran Is Joint Director, BIRD, Lucknow.

The usual disclaimer about the responsibility of the National Bank as to the facts cited and views expressed in the paper is implied.

IV

CONTENTS

Page No

CHAPTERI

CHAPTER II

CHAPTER III

CHAPTER IV

CHAPTERV

ACKNOWLEDGEMENT

INTRODUCTION

CONCEPTUAL ASPECTS OF OVERDUES, RECOVERY AND PRUDENTIAL NORMS

IMPACT OF NPAs ON HEALTH OF RFIs

NON-PERFORMING ASSETS IN RURAL FINANCIAL INSTITUTIONS

RECOVERY PERFORMANCE

1

3

11

15

27

CHAPTER VI RECOVERY AND NPA MANAGEMENT 37

REFERENCES

CHAPTER I

INTRODUCTION

This occasional paper on recovery management in rural credit is prepared

at the behest of National Bank for Agriculture and Rural Development (NABARD),

Head Office, Mumbai. The focus is on rural financial institutions (RFIs). Regional

Rural Banks (RRBs), Co-operative banks and rural branches of Commercial Banks

(CBs) are the RFIs for the purpose of this paper.

The Broad Objectives of the Paper are

• To discuss the conceptual aspects of overdues, recovery and prudential norms.

• To analyse the pattern of build up of overdues in Rural Financial Institutions.

• To discuss the factors affecting recovery of loans in Rural Financial

Institutions.

• To suggest methods and strategies for better recovery and NPA Manage

ment in Rural Financial Institutions.

The paper is based on the review of earlier work in the area of overdues and

recovery management. Empirical analysis in the paper is based on relevant data

and information that are available to throw light on the issue of overdues and

recovery management in Rural Financial Institutions (RFIs).

Rural credit relates to credit for agriculture and non-agricultural purposes,

the former being the major component (about 85% of the total disbursement during

1998-99). The relative share of commercial banks, co-operative banks and RRBs

in the total institutional credit disbursement to agriculture is about 49, 44 and 7

per cent respectively for TE 1998-99 (Economic Survey 2000-01).

For in-depth understanding of the problem of overdues in RFIs,

NABARD had earlier sponsored three studies in Karnataka, Orissa and Madhya

Pradesh. These studies were undertaken by the National Institute of Rural Development

(NIRD 1999), Hyderabad; National Institute of Bank Management (NIBM 1996),

1

Pune; and the Bankers Institute of Rural Development (BIRD 1997), Lucknow,

respectively. This occasional paper makes use of these three study reports in addition

to other literature available on the subject. The information from RRBs and co-operative

banks (short term and long term stnjcture) is available in some detail and has been

used in the paper. However, the exact position in rural branches of CBs is not readily

available.

This occasional paper is organised in six Chapters. Chapters 2 and 3 present

the conceptual aspects of overdues, recovery, prudential norms and non-performing

assets (NPAs) that impact on the financial health of RFIs. Chapters 4 and 5 deal

with empirical analysis of NPAs and recovery performance across institutions, states

and regions. Chapter 6 deals with recovery and NPA management along with

macro policy issues including legal changes required for better recovery.

CHAPTER II

CONCEPTUAL ASPECTS OF OVERDUES, RECOVERY AND PRUDENTIAL NORMS

2.1 Overdues, Recovery and NPAs

2.1.1 Overdues and Recovery

The magnitude of recovery amount overdue is one of the most important

indicators of financial health of RFIs. Currently, the accepted standard of measurement

of overdues is in relation to demand. The logic for the demand as the basis is that it

is the amount which has become due and not the amount which is yet to become

due for repayment. This distinction is important because loans will have varying

due dates for instalments as they are issued on the basis of future cash flow from

investments.

The term "overdues" is used to convey the meaning that instalments of

loans and Interest thereon are not paid on due date. The term "recovery" of dues

relates to repayments of loans and interest thereon in time. Therefore, overdues exist

if recovery of loans is not in time.

There exists a provision in RFIs to block the part of defaults that are legally

disputed or against which legal proceedings have been initiated. This amount does

not get included in the total amount due for repayment i.e. "demand". For example,

if a RFI has Rs. 100 in default including Rs. 20, on which legal case is filed and

recovery out of Rs. 80 is Rs. 50. The recovery percentage will be calculated as

62.5% and not 50%. Therefore, exclusion of disputed amount leads to overestimation

of recovery performance.

RFIs often fail to write off bad loans due to various reasons. When bad

debts are not written off, the reported loan recovery performance may be highly

distorted. For example, assume that an RFIs lends Rs. 100 every year and recovers

90 of that each year and Rs. 10 become bad.

The Following illustration shows how the recovery percentage is calculated over a

It is clear from the above example that though recovery percent on the current

year basis is 90% throughout, on a cumulative basis it becomes 47% in tenth year.

It is therefore, not easy to accurately measure the recovery performance of RFIs if

there is no provision for writing off bad debts.

2.1.2 Non-Performing Asset (NPA)

An amount under any of the credit facilities viz., term loan, overdrafts, cash

credit account, etc. is to be treated as 'past due' when it remains unpaid for 30 days

beyond the due date. A non-performing asset (NPA) is defined as a credit facility in

respect of which interest or instalment of principal is past due for 'two quarters'. In

respect of advances for agricultural plirposes, if interest has not been paid during

the last 2 seasons of harvest (covering two half years), after it has become 'past due'

then such advance should be treated as NPA. Further, if any one of the credit

facilities enjoyed by a client becomes NPA, all of the other credit facilities enjoyed

by the client also deemed to have become NPA and are treated accordingly. In case

of RFIs, the lumping poses a problem. There are instances where the borrower

had serviced one account but not the other. Further, when there is limited

repayment to be made borrowers normally do not have option as to where the

repayment need to be applied.

2.1.3 Repayment

The assumption in delivery of credit as a source of finance is that the use of

credit would generate enough income to repay the loan with interest. However,

generation of adequate additional income has to be accompanied by willingness of

borrower to repay the loan with interest. Failure of investment may result in

non-generation of income, failure of expected income may lead to inadequate

income, perception or pressure of more important and urgent use of income

may incapacitate the repayment and finally the borrower's willingness and

desire has to be there to fulfil repayment obligation. If loans are not repaid, the RFI

loses both its interest income as well as its capital. Good management of recovery

of dues is, therefore, a complex issue encompassing economic and non-economic

factors and has implications for profitability of the RFIs.

Repayment of loan together with interest by borrowers is crucial for

recycling of funds deployed in rural credit. The fuelling of development process by

dispensing credit is meaningful only when timely repayment is forthcoming. Othenwise

expansion of credit delivery is seriously vitiated and the delivery system gets

chocked limiting the continued supply of credit by financial institutions in rural

areas. Good recovery is an important ingredient for profitability of RFIs as it leads

to increased financial capacity to deliver credit.

2.2 Prudential Norms

The introduction of banking sector reforms in 1992 is a watershed in the

Indian banking system. The reforms have not only brought about structural changes

in the Indian banking system but have also greatly influenced all types of banking

entities in various aspects of operations, governance, transparency and accountability.

Though the reforms were initially directed towards the commercial banks, they were

subsequently extended to cover the rural banking sector of the country corriprising

also of regional rural banks and co-operative banks.

Out of the various reform measures, the introduction of prudential norms

has been the cornerstone of banking sector reform process. The prudential norms

mainly cover the following four major aspects: Capital Adequacy; Income Recognitiop;

Asset Classification; and Provisioning. Herg it will be pertinent to mention the views

of the Committee on the Financial Systerri, .j 991 popularly known as Narasimh^m

Committee I.

"The committee believes that a proper system of income recognition and

provisioning is fundamental to the preservation of the strength and stability of the

banking system. A proper asset classification will however, have to precede this

exercise." (Committee on the Financial System, 1991)

The prudential norms for income recognition have to be objective and based

on "the record of recovery" rather than on any subjective or security consideration.

Likewise, the classification of assets has to be done on the basis of objective criteria

which would ensure a uniform and consistent application of norms. Under income

recognition, banks were advised not to charge and take to income account interest

on all non-performing assets. They were also required to classify all their loans

and advances into four broad group (i) standard assets (ii) sub-standard assets

(iii) doubtful assets and (iv) loss assets by compressing the existing eight health

codes on the basis of pre-defined parameters. While no provision is required to be

made in case of standard assets, provision is required to be made in case of sub

standard, doubtful and loss assets in varying degrees.

In respect of non-performing assets, interest is not recognised on accrual

basis but is booked as income only when actually received.

2.3 Applicability of Prudential Norms

The timeframe and manner of application of prudential norms to commercial

banks (CBs), regional rural banks (RRBs) and co-operative banks have been as

foiiows:

2.3.1 Commercial Banks and Regional Rural Banks

The prudential norms were introduced to CBs vide Reserve Bank of

India (RBI) circular no. DBOD.BP.BC. 129/21.04.043-92 dated 27 April 1992 in a

phased manner over a three-year period commencing with the accounting year

beginning 1 April 1992. In case of RRBs, the prudential norms relating to income

recognition, assets classification were made applicable with effect from the

accounting year 1995-96 and provisioning from the financial year 1996-97 vide RBI

circular no.03.05.34/95-96 dated 22 March 1996.

2.3.2 Co-operatives Banks

Co-operative banks in India occupy a unique position and are organised on

co-operative principles. Co-operatives are governed by the co-operative societies

act of the concerned state, while Banking Regulation Act is applicable to them only

in a limited form. Thus, co-operatives in India enjoy a quasi-banking position. Under

three tier system, the village or taluka level co-operatives are independent units that

are federated into District Central Co-operative Banks which are in turn along with

other state level societies federated into State Co-operative Banks (SCBs). Some

states have no middle tier, but have only two tier systems. In a few states, there is

only unitary system without affiliated federal membership.

Co-operative banks in the country are given preferential treatment and support

by RBI and NABARD as regards maintenance of Statutory Liquidity Ratio (SLR)

and Cash Reserve Ratio (CRR) because of their unique and quasi-banking position.

The discipline of prudential regulation was extended to co-operative banks at a

laterstagei.e 1996-97,

The prudential norms were introduced to SCBs and DCCBs vide RBI circular

No. RPCD. BC. 155/07.37.02/95-96 dated 22 June 1996 from the accounting year

1996-97 in the same form as applicable to CBs and RRBs. Though there was no

phasing in the assets classification norms as allowed in case of CBs and RRBs in

the initial years, considerable relaxation as regards provisioning in the first year

was provided to SCBs and DCCBs. The phasing in provisioning requirement was

as follows:

(i) First year of introduction of prudential norms (1996-97): 100% in re

spect of loss assets and not less than 30% of the provisioning needed

in respect of sub-standard and doubtful assets.

(ii) Second year (1997-98): The balance provisioning needed in respect

of the above categories of assets together with current provision needed in

respect of assets classified in the second year (1997-98). In other words, all

the doubtful and sub-standard assets have to be provided fully as in case of

CBs from second year onwards in addition to 100% for loss assets.

However, as some cooperative banks reported difficulties in introducing

prudential norms due to lack of relevant data / information, experience and expertise

in making provisions, Reserve Bank of India gave further relaxation of one year to

them so that the norms may be fully operationalised.

For State Go-operative Agriculture and Rural Development Banks

(SCARDBs), the long term credit structure of co-operative banks, the prudential

norms have been made applicable since 1997-98.

Income recognition on realisation basis and provisioning in respect of bad

advances were not totally new concepts to the co-operative banks before prudential

regulation. It is not that co-operative banks were unaware of the prudential norms

and provisioning aspect. In fact, there exists a system of recognizing income on

actual realization basis and not on accrual basis. They also, in most states, make

provisions on a very conservative basis which is more stringent than the present

provisioning norms in some respects. The profit appropriation stipulates norms for

bad debt reserves, statutory reserves, stabilisation fund, etc. As such, it was

observed that most of the SCBs and DCCBs, mainly profit making, had higher loan

loss provisions than what was required by the prudential norms. Nevertheless, the

prudential norms have not only standardised the whole exercise of income recognition,

classification of loan assets and provisioning but also brought about uniformity in

maintenance and disclosure of financial information which has facilitated an objective

inter-bank comparison overtime.

8

The time frame of applicability of prudential norms to the three types of RFIs

mentioned above are summarised in Table 1.1

Table 1:1 : Timeframe of Applicability of Prudential Norms in CBs, RRBs and Co-operative Banks

Prudential Norms CBs RRBs Co-operative Banks

Income Recognition

Assets classification

Provisioning

1992-93

1992-93

1995-96

1995-96

1996-97

1996-97 (with three years (with three years (No phasing for NPAs) phasing of NPAs) phasing of NPAs)

1992-93 1996-97 1996-97 (with relaxation in

the first year)

2.4 Stringency in Prudential Norms and Capital Adequacy

Initially, as mentioned above, the prudential norms were introduced to different

types of RFIs in a phased manner and that, too, in a diluted form so that RFIs may

suitably adjust to new discipline and stabilise in due course of time. It was also

expected that only a robust and vibrant RFI can cope up with stringent prudential

norms at par with international standards. The Committee on Banking Sector

Reforms (Narasimham Committee II, 1998) also emphasised this aspect and

recommended gradual tightening of the prudential norms. RBI after examining the

same and taking into account the perfomriance of the banks, have further strengthened

the prudential norms for CBs only, with a gradual time frame as follows:

• Provision for loans guaranteed by government and public financial

institutions from 31.3.99.

• Income recognition and provisioning on government guaranteed advances on

par with those on other advances with effect from 2000-2001.

• Provision for standard assets @ 0.25% with effect from 31.3.2000.

• Reduction of time frame from 24 month to 18 months for categorising advances

as doubtful from 31.3.2001.

The above stringent prudential norms have also been made applicable to

RRBs and Co-operative banks in a phased manner. Further, for CBs, the norms

shall be made more stringent as an on-going process to cope up with the new and

complex banking risks and also to keep them at par with international standards.

Alongwith the prudential norms, the capital adequacy norms were also

introduced to commercial banks with a liberal timeframe. The CBs were required to

attain a capital adequacy of minimum 8% by 31 March 1996. These norms have

been further raised to 9% with enhancement and extension of risk weights on

investments, government guaranteed advances and other assets with effect from

31.3.2000. RRBs and co-operative banks are at present, excluded from capital

adequacy norms in viewof their weak financial position, however it is expected that

these norms shall be made applicable to them also once their financial position

improves and stabilises.

10

CHAPTER III

IMPACT OF NPAs ON HEALTH OF RFIs

The non-performance of loans affects RFIs in several ways and slowly

incapacitates the institution over time. A few notable areas are discussed below:

3.1 Solvency

The solvency of the RFI as exhibited by capital adequacy ratio is directly

related to quality of its loan portfolio. Like any company, RFIs can make losses and

so need capital which acts as a cover for such difTiculties. Since the loan portfolio is

a major part of net assets of any RFI, loan defaults are a prime source of potential

losses. Thus, new equity is required whenever such loan losses occur. As loan

loss provisions are a charge to profit, the RFI's owned funds are significantly

reduced. If tax provisions are ignored, an increase in loan loss provision or writing

off an asset requires an equal amount of increase in the mandated capital (Beattie

et al, 1995). A substantial portion of non performing assets in loan portfolio, thus,

jeopardises solvency of the RFI as accretion to owned fund is reduced due to higher

provision and consequently less profit. Besides, minimum capital is to be

maintained even for hard core non performing assets falling under doubtful or loss

category which are, in effect, dead assets and are carried over in the balance

sheet over the years in the absence of write off. Thus, every time NPAs increase,

RFI has to look for additional avenues to raise minimum capital to cover them.

3.2 Profitability

After the introduction of prudential norms, the NPAs have adversely affected

the profitability of RFIs in two ways. First, there is a loss of interest income to the

extent of interest accrued on NPAs since income recognition is limited to only

standard assets. Thus, RFI's income is affected to the extent of proportion of NPAs

in loan portfolio. Secondly, the RFI has to divert a part of profit for loan loss provisions

to cover the incremental portion of NPAs. This affects the net-profit and thereby

11

erodes the solvency.

3.3 Liquidity

Banking business is a highly leveraged one. The intermediation involves

mobilizing short term deposit resources and lending for longer term on the strength

of future flow of deposits and the repayment of loans. Increasing NPAs not only

critically affect the liquidity of RFIs but also force the RFIs to maintain more liquid

assets thereby increasing the cost. Since the NPAs remain in the balance sheet of

the RFIs till they are written off or adjusted against loan loss provision which is a

long-winded process, they have to be funded either through deposits or capital so

far as they continue to remain in the balance sheet. Capital enhancement is not

always possible and can not be resorted to every year. Hence, every time NPAs

increase, deposits are mobilised to fund the incremental NPAs, thereby,

increasing interest expenditure. Further, because of the mandated obligations,

like SLR and CRR, RFIs not only have to fund the non-performing assets but for

every Rs 100 of such assets, RFIs have to look for more than Rs 100 of resources.

This can be expressed as follows:

NPAs

Deposits Required =

1- (SLR + CRR)

Where SLR = Statutory Liquidity Ratio

CRR= Cash Reserve Ratio

Thus, as the level of NPAs to total loans and advances increases, the liquidity

risk of RFI also increases.

3.4 Loan Assets Turnover

RFIs with high NPAs have a regressive loan portfolio. As large amount is

blocked in NPAs and is not available for recycling, the loan availability starts shrinking

over the period. This invariably reduces the real rate of expansion of loan portfolio.

12

RFIs as financial intermediaries provide multiplier effect to the economy by the

process of credit creation and are required to maintain a fast moving effective turnover

of loans assets. With increase in NPAs, the turnover of loan assets becomes gradually

slow and the very essence of banking i.e., credit creation is greatly hampered.

3.5 Interest Rate

Another fallout of lower profitability and shrinkage of performing loan portfolio

due to high NPAs is that the RFIs are not able to reduce the lending rate in relation

to bank rate which adversely affects their competitiveness and leads to poor credit

expansion. Moreover, as a result of higher provisioning due to incremental NPAs

and the cost of servicing the resources, the RFIs have to perforce charge higher

interest on the performing borrowers.

As the interest rate becomes higher than the market rate, the RFIs are left

with the option of adverse selection i.e., availability of only low rated borrowers for

their credit expansion which again increases the risk of creating new NPAs. Thus,

starts a vicious cycle as given below:

Low rated borrowers

Incremental NPAs High interest rate

(r> PLR)

Higher Provisioning ^ Lower Profitability

The following excerpt effectively summarises the catch-22 position of the

RFIs in this regard (Jilani, 1999).

"Besides affecting their ability to lower their interest rates, such overhang also

compels banks to maintain higher spreads to protect their profit position. In the

recent period when the inflation levels have been at all-time low, it has been

13

suggested that lending rates should also come down. Although theoretically such

reduction is relevant, yet in the context of the huge burden of NPAs and need to

maintain higher spreads to protect their profit position, banks have not been in a

position to do so."

3.6 Risk Taking Ability

Lastly, high level of NPAs reduces risk taking ability of the RFIs. It also

affects the credit rating of the RFIs thereby restricting their ability to approach the

public for capital subscription (Tier I Capital). Alternatively, a low rating substantially

increases the cost of raising funds even for Tier II Capital.

3.7 Sum Up

Thus, it can be concluded that NPAs greatly affect the financial health of the

RFIs. Nothing can highlight the importance of NPAs and their impact more than the

Narasimham Committees (I and II) whose reports have become the precursor of

the financial reforms in general and banking reforms in particular. The Committee

on Banking Sector Reforms (Narasimham Committee II, 1998) is quoted in this

regard as follows:

" NPAs constitute a real economic cost to the nation in that they reflect the

application of scarce capital and credit funds to unproductive uses. The moneys

locked up in NPAs are not available for productive use and to the extent that banks

seek to make provisions for NPAs or write them off, it is a charge on their profits. To

be able to do so, banks have to charge their productive and diligent customers a

higher rate of interest. It thus becomes a tax on efficiency. It is the customer who

uses credit efficiently that subsidises the inefficiency represented by NPAs. This

also raises the transaction costs in the system thus denying the diligent credit

customers the benefit of lower rates, which would help them to be more

efficient and competitive. NPAs, in short, are not just a problem for banks. They are

bad for the economy".

14

CHAPTER IV

NON- PERFORMING ASSETS IN RURAL

FINANCIAL INSTITUTIONS

The introduction of prudential norms has been a turning point in the reform

process of the RFIs. NPAs are the key to the whole range of prudential norms as

mentioned earlier. It will, therefore, be pertinent to have an analysis of the

Non-Performing Assets from various dimensions for three important RFIs viz., CBs,

RRBs and Co-operative banks for which data are available. The discussion on the

levels of NPAs and recovery performance is done together wherever data are available.

This is done as NPA levels and recovery performance are highly negatively correlated.

That is better recovery performance corresponds to lower NPAs.

4.1 NPAs in Commercial Banks

RBI conducted a study of NPAs in 27 public sector commercial banks. The

study reveals that the gross Non Performing Advances of these banks were marginally

reduced to 17.84% as on 31 March 1997 after introduction of objective norms. Under

the earlier concept of sticky advances, the position as on 13 March 1989 was at

17.91%. However, a paper brought out by FITCHIBCA, an international credit rating

agency, observes "there is significant improvement since 1991 when gross

Non-Performing Loans (NPL) to total loans were estimated to be around 23%, or

even in 1995-96, when this ratio was 17.5%. The bulk of the NPLs in the banking

sector are due to historical reasons and incremental NPLs, until now, were not a serious

problem".

Rajaraman, et al (1999) report bank specific percentage of net NPAs to net

advances in commercial banks for the year 1996-97. These range from 2 per cent

in case of 9 new private sector banks to 9 per cent in case of 27 public sector

banks.

15

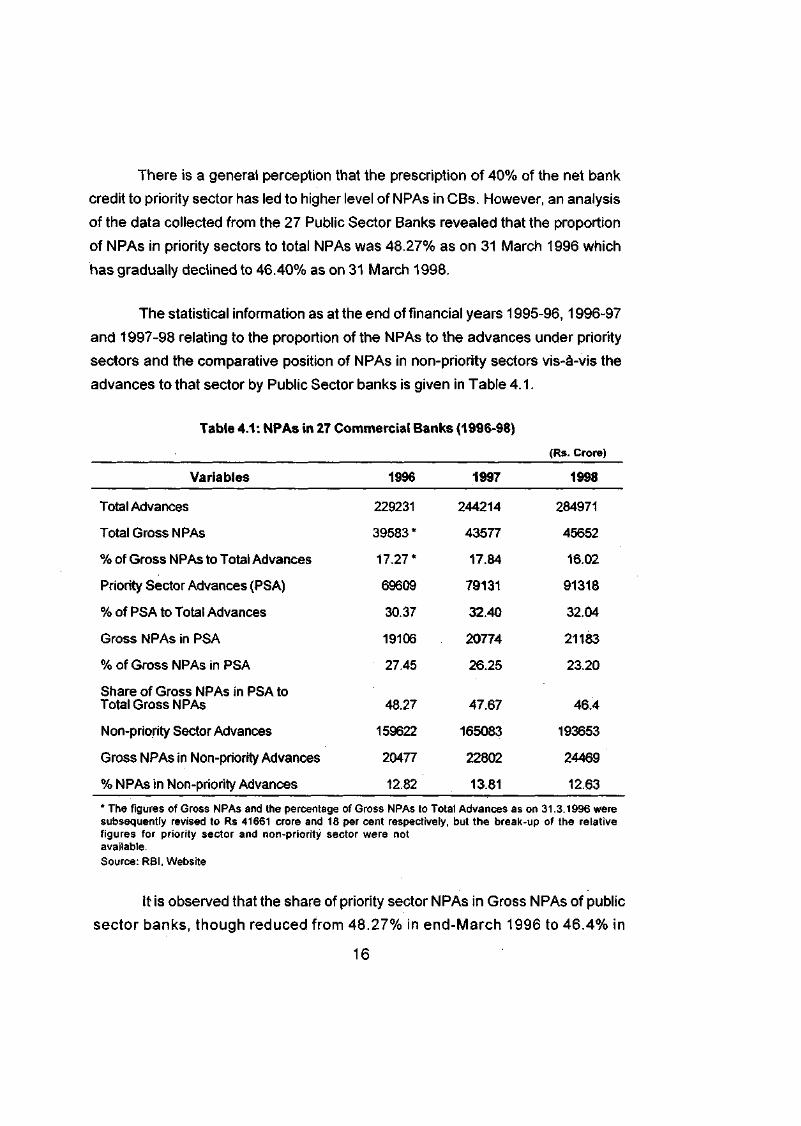

There is a general perception that the prescription of 40% of the net bank

credit to priority sector has led to higher level of NPAs in CBs. However, an analysis

of the data collected from the 27 Public Sector Banks revealed that the proportion

of NPAs in priority sectors to total NPAs was 48.27% as on 31 March 1996 which

has gradually declined to 46.40% as on 31 March 1998.

The statistical information as at the end of financial years 1995-96,1996-97

and 1997-98 relating to the proportion of the NPAs to the advances under priority

sectors and the comparative position of NPAs in non-priority sectors vis-a-vis the

advances to that sector by Public Sector banks is given in Table 4.1.

Table 4.1: NPAs in 27 Commercial Banks (1996-98)

(Rs. Crore)

Variables 1996 1997 1998

Total Advances 229231 244214 284971

Total Gross NPAs 39583 * 43577 45652

% of Gross NPAs to Total Advances 17.27* 17.84 16.02

Priority Sector Advances (PSA) 69609 79131 91318

% of PSA to Total Advances 30.37 32.40 32.04

Gross NPAs in PSA 19106 20774 21183

% of Gross NPAs in PSA 27.45 26.25 23.20

Share of Gross NPAs in PSA to Total Gross NPAs 48.27 47.67 46.4

Non-priority Sector Advances 159622 165083 193653

Gross NPAs in Non-priority Advances 20477 22802 24469

% NPAs in Non-priority Advances 12.82 13.81 12.63

* The figures of Gross NPAs and the percentage of Gross NPAs to Total Advances as subsequently revised to Rs 41661 crore and 18 per cent respectively, but the break figures for priority sector and non-priority sector were not available. Source: RBI, Website

on 31.3.1996 were •up of the relative

It is Observed that the share of priority sector NPAs in Gross NPAs of public

sector banks, though reduced from 48.27% in end-March 1996 to 46.4% in

16

end-March 1998, was significantly higher than the proportion of priority sector ad

vances to total advances, which ranged between 30% and 32% during the above

period. The percentage of gross NPAs in priority sector advances, though came

down from 27.45 per cent in end-March 1996 to 23.2 per cent in end-March 1998,

was almost twice the NPAs in Non-priority sector advances in per cent terms, which

ranged from 12.8% to 13.8% during the above period. It could be inferred that the

higher NPAs in priority sector advances have pushed up the overall proportion of

NPAs of these banks by about 3% to 4 %. However, the gradual increase in the

proportion of NPAs in non-priority sectors could indicate that NPAs are increasingly

occurring on credit accounts of industrial sector during the recent years.

4.2 NPAs in Regional Rural Banks

For a majority of RRBs, the high level of NPAs has been a major stumbling

block to attain profitability and solvency. However, at all India level, percentage of

NPAs to loans declined from 43.07% in 1995-96 to 27.89% in 1998-99. The median

NPAs in per cent, too, has come down from 45.2% in 1995-96 to 26.2% in 1998-99.

Undoubtedly, RRBs in general suffer from a high proportion of NPAs and

therefore, command a low esteem in Indian banking industry. This is due to past

policies of directed credit, faulty appraisal, poor monitoring and recovery efforts in

RRBs, etc. To have a proper perspective of NPAs in RRBs, it is necessary to

analyse the incidence of NPAs in further detail.

4.2.1 Distribution of RRBs According to NPA Level

Table 4.2 shows that over the last four years, there has been significant

improvement in terms of reduction of NPAs in RRBs. In the above 70% NPAs

category, there is only 1 RRB in 98-99 as against 22 in 95-96 and that too the lone

RRB is Tripura Gramin Bank having peculiar socio-political problems of North Eastern

(NE) region.

17

Table 4.2: Distribution of RRBs according to Percent NPA to Total Advances

% of NPA to Loans

Years Above 41% to 10% to Below Total Median 70% 70% 40% 10% NPA ratio

95-96 22 91 79 4 196 45.2

96-97 10 88 88 10 196 40.0

97-98 4 71 109 20 196 32.3

98-99 1 56 119 20 196 26.2

Source: Key Statistics on Regional Rural Banks 1996, 97,98, and 99, NABARD, Mumbai,

Initially, there has been major shift of RRBs from higher level NPA categories

(viz., above 70% and between 41 % to70%) to lower level categories but the improvement

has not further progressed downward from the 3"* category of 10% to 40% to 4*

category of below 10%. The concentration of majority of RRBs in the 3'" size

category indicates that after major reduction in NPAs, it becomes increasingly difficult

to effect marginal reduction in NPAs position & stupendous efforts are

required to further reduce the NPAs of the RRB.

4.2.2 State Wise Analysis

NPAs and recovery perfonnance of RRBs of major states of India are given in

Table 4.3

Table 4.3 : NPAs and Recovery Performance of RRBs: Major States

State 1996-97 1997-98 1998-99 % NPAs Recovery % NPAs Recovery %NPAs to loans %* to loans %* to loans

A. States with NPAs% below National Average (98-99)

1. Kerala 6.44 85.59 6.11 88.16 5.25 2. Tamil Nadu 11.06 79.24 -10.29 79.37 10.04 3. H.P. 22.33 58.97 19.33 68.95 15.58

Loss 52.07 0.30 268.74 1.34 627.37 2.37 791.43 2.65

Total Assets 17293.27 100.00 20107.73 100.00 26513.01 100.00 29907.25 100.00

Total NPAs 1626.47 9.41 2419.75 12.03 5223.85 19.70 5451.13 18.23

Source: Dossier on Co-operatlves-State-wise status of the Co-operative Credit Structure, March 1998, NABARD, Mumbai.

21

It may be observed that non-performing assets of SCBs in each category

have increased both in absolute and relative terms during the period. It may be due

to more accurate classification of non-performing assets in the subsequent year

since co-operative banks took some time to stabilise to the new system. Besides,

there might be slippage of high grade assets to the next low grades. Though, the

former factor explains the substantial increase in non-performing assets to a great

extent, there is no empirical evidence or in- depth analysis to isolate the causal

factors. However, it is expected that in later years the proportion of NPAs for SCBs

will come down with increase in loan portfolio and no fresh or marginal accretion to

existing NPAs.

Percent-wise, NPAs in both SCBs and DCCBs as a whole are pegged around

12% and 18% respectively as compared to 28% in case of RRBs. To certain extent,

the progressively low levels of NPA at higher tiers of the co-operative credit system

is the result of absorption of the burden of NPAs by lower tiers, consisting of PACS,

marketing societies etc. Further, the higher recovery rate among co-operatives as

compared to RRBs, which again is a reflection of more efficient legal recourse

available to co-operatives for recovery of overdue loans, has also helped the

co-operatives to have lower incidence of NPA. The share of NPAs in case of DCCBs

has marginally come down from 19.70% to 18.23%. It seems that DCCBs have

been able to contain the level of existing NPAs i.e., there is no fresh accretion,

however they have not been able to effectively noanage and reduce the NPAs in

absolute terms. There is no significant improvement in the first two NPAs categories

over the period though, per cent-wise, both have come down due to increase in the

size of loan portfolio.

4.3.2 Size Wise Analysis

The frequency distribution of SCBs in terms of percentage of NPAs to total

loans for the two years has been given in Table 4.6.

22

Table 4.6: Frequency Distribution of SCBs as per percentage of NPAs to Total Loans (1996-97 to 1997- 98)

% of NPAs to Loans 1996-9r 1997-98" Below 5% 6 7 5% to 10% 5 3 11% to 20% 4 4 21% to 50% 9 8 Above 50% 2 3 Total 26 25

* The data relate to 26 SCBs. Data for Arunachal Pradesh are not available. ** Data for Delhi SCB and Arunachal Pradesh are not available. Source: Dossier on Co-operatives-State-wise status of the Co-operative Credit Structure, March 1998,

NABARD, Mumbai.

In addition to Himachal Pradesh, Jammu & Kashmir, and Bihar, SCBs of

north-eastern states and union territories with peculiar socio-political problems

and poor co-operative base have NPAs above 20% in 1997-98. Thus, majority of

SCBs, specially of large states having strong co-operative base fall in the categories

of below 20%) NPAs. This is a very heartening feature. With concerted efforts, the

position can further be improved by bringing down NPAs in SCBs of North Eastern

(NE) states. The frequency distribution of NPAs percentage for DCCBs could not

be presented due to non-availability of bank-wise data for all the states.

4.3.3 State Wise Analysis

The state-wise analysis of NPAs and recovery performance for the two years

has been attempted for both SCBs and DCCBs and is presented in Tables

4.7 and 4.8, respectively.

23

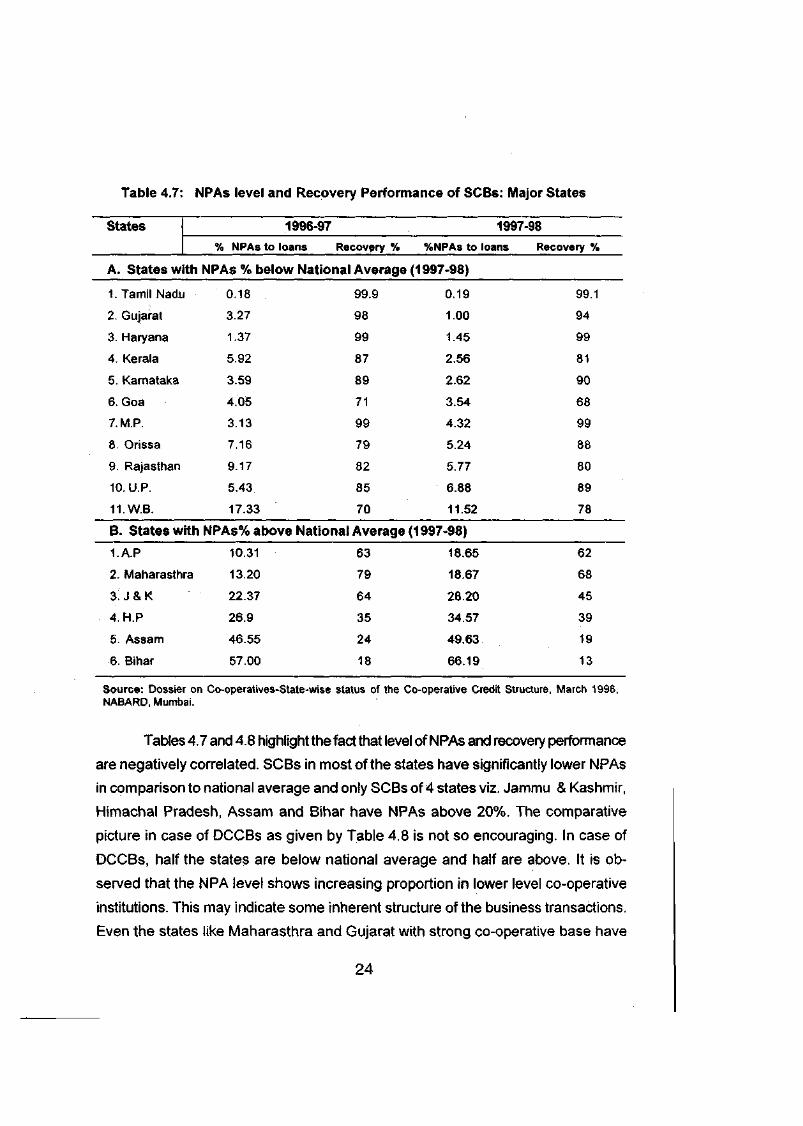

Table 4.7: NPAs level and Recovery Performance of SCBs: Major States

States 1996-97 1997-98

% NPAs to loans Recovery % %NPAs to loans Recovery %

A. States with NPAs % below National Average (1997-98)

1. Tamil Nadi 0.18 99.9 0.19 99.1

2. Gujarat 3.27 98 1.00 94

3. Haryana 1.37 99 1.45 99

4. Kerala 5.92 87 2.56 81

5. Karnataka 3.59 89 2.62 90

6. Goa 4.05 71 3.54 68

7.M.P. 3.13 99 4.32 99

8. Orissa 7.16 79 5.24 88

9. Rajasthan 9.17 82 5.77 80

10. U.P. 5.43 85 6.88 89

11.W.B. 17.33 70 11.52 78

B. States with NPAs% above National Average (1997-98)

1.A.P 10.31 63 18.65 62

2. Maharasth ra 13.20 79 18.67 68

3: J & K 22.37 64 28.20 45

4. H.P 26.9 35 34.57 39

5. Assam 46.55 24 49.63 19

6. Bihar 57.00 18 66.19 13

Source: Dossier on Co-operatives-State-wise status of the Co-operative Credit Structure, March 1998, NABARD, Mumbai.

Tables 4.7 and 4.8 highlight the fact that level of NPAs and recovery perfonnance

are negatively correlated. SCBs in most of the states have significantly lower NPAs

in comparison to national average and only SCBs of 4 states viz. Jammu & Kashmir,

Himachal Pradesh, Assam and Bihar have NPAs above 20%. The comparative

picture in case of DCCBs as given by Table 4.8 is not so encouraging. In case of

DCCBs, half the states are below national average and half are above. It is ob

served that the NPA level shows increasing proportion in lower level co-operative

institutions. This may indicate some inherent structure of the business transactions.

Even the states like Maharasthra and Gujarat with strong co-operative base have

24

weak co-operative intermediaries as indicated by high NPAs percent at DCCBs

level while it is not so in case of SCBs of these states.

Table 4.8: NPAs level and Recovery Performance of tlGCBsiMajof States

States 1996-97 1997-98

% NPAs to loans Recovery % %NPAs to loans Recovetv %

A. States with NPAs % below National Average (1997-98)

1. Haryana

2. Rajasthan

3. Tamil Nadu

4. Karnataka

5. H.P.

6. W.B.

7.A.P.

8. Kerala

4.35 12.23

10.76

31.36

15.87

16.50

11.87

15.49

79 5.98 78

83 8.84 85

60.2 12.51 76.4

75 13.35 69

63 14.97 56

72 15.11 74

75 15.52 71

80 18.12 79

B. State with NPAs % above National Average (1997-98)

LMadhya 21.36

Pradesh

2. Maharasthra 21.43

3. Orrisa 22.13

4. U.P. 28.01

5. Gujarat 20.03

6. J & K 40.60

7. Bihar 73.34

8. Assam 88.83

62 18.63 58

64 19.60 66

58 20.33 57

56 23.18 36

70 24.85 70

17 48.18 17

18 72.56 11

7 88.54 4

Source: Dossier on Co-operatives-State-wise status of the Co-operative Credit structure, March 1998, NABARD, Mumbai.

4.4 A Comparative Position of NPAs in CBs, RRBs and Co-operative Banks

To sum up. Table 4.9 gives a comparative position of growth of NPAs in CBs,

RRBs, SCBs and DCCBs for the last 3 years.

25

Table 4.9: Growth of NPAs in CBs, RRBs, SCBs and DCCBs

(1996-97 to 1998-99)

Category of Banks

NPAas%of to ta l Advances

Volume of NPAs (Rs. Crores) Share in the total NPAs

3. Jammu & Kashmir 74 64 45 34 23 17 17 26 NA NA NA

4. Punjab 99 99 100 96 89 87 87 88 83 83 85

5. Rajasthan 85 85 81 89 80 83 85 83 71 68 70

6. Chandigarh 48 49 34 22 NA NA NA NA NA NA NA

7. Delhi 53 48 51 39 NA NA NA NA NA NA NA

North- Eastern

Region

1. Arunnachal Pradesh28 25 22 37 NA NA NA NA NA NA NA

2. Assam 24 24 20 27 6 7 4 5 NA NA NA

3. Manipur 9 8 4 4 NA NA NA NA NA NA NA

4. Meghalaya 39 41 40 44 NA NA NA NA NA NA NA

5. Mizoram 11 31 43 42 NA NA NA NA NA NA NA

6. Nagaland 39 28 23 13 NA NA NA NA NA NA NA

7. Tripura 25 28 19 34 NA NA NA NA NA NA NA

Eastern Region

1. Bihar 20 18 13 7 18 18 11 12 NA NA NA

2, Orissa 78 79 88 91 61 58 57 48 63 40 49

3. West Bengal 62 70 78 78 76 72 74 75 67 72 NA

4. Andaman & 44 55 61 64 NA NA NA NA 52 55 60

Nicobar

Central Region

1. Madya Pradesh 97 99 99 94 59 52 58 60 50 52 64

2. Uttar Pradesh 85 85 89 80 58 56 54 53 67 43 41

Western Region

1. Goa 74 72 68 66 NA NA NA NA 47 51 47

2. Gujarat 99 98 94 90 67 70 70 66 71 69 69

3. Maharashtra 86 84 78 84 66 64 68 66 57 57 55

Southern Region

1. Andhra Pradesh 68 63 62 72 69 75 71 72 55 NA NA

2. Karnatal<a 92 89 90 91 73 68 69 71 67 65 79

3. Kerala 96 87 81 88 77 80 79 84 79 NA 83

4. Tamil Nadu 99.8 99.9 97.3 94.6 77.7 80.2 76.4 77.4 70 62 62

5. Pondicherry 61 59 63 NA NA NA NA NA 53 48 44 Source: Dossier on Cooperatives, NABARD, Manual 1998 & 1999. NA= Not Available/ Applicable.

31

Recovery percentage in relation to long term co-operative credit is lower

compared to short term co-operative credit generally. However, recovery patterns

are similar across states in case of short term and long term co-operative credit.

Table 5.4 : Recovery Percentage of Long Term Cooperative Credit (% of Collection to Demand)

states SCARDB PCARDBs

95-96 96-97 97-98 98-99 95-96 96-97 97-98 98-99 A. Northern Region 1. Haryana 95 96 93 94 66 70 65 69 2. Himachal Pradesh 65 70 67 69 69 80 80 81 3. Jammu & Kashmir 39 32 33 37 NA NA NA NA 4. Punjab 100 100 100 100 89 82 83 83 5. Rajasthan 80 84 85 82 69 72 67 65 6. Chandigarh 48 49 34 22 NA NA NA NA 7. Delhi NA NA NA NA NA NA NA NA B. Northern -Easterr 1 Region 1, Arunachal Pradesh NA NA NA NA NA NA NA NA 2. Assam 2 24 16 1 NA NA NA NA 3. Manipur 11.91 11.15 4.99 NA NA NA NA NA 4. Mehhalaya NA NA NA NA NA NA NA NA 5. Mizoram NA NA NA NA NA NA NA NA 6. Nagaland NA NA NA NA NA NA NA NA 7. Tripura 66 51 44 57 NA NA NA NA C. Eastern Region 1. Bihar 33 38 38 36 NA NA NA NA 2. Orissa 18 11 6 7 39 31 24 23 3. West Bengal 60 61 62 64 60 63 62 59 4. Andaman & Nicobar NA NA NA NA NA NA NA NA D. Central Region 1. iVIadhya Pradesh 39 42 37 42 52 55 48 60 2. Uttar Pradesh 79 80 81 82 NA NA NA NA E. Western Region 1. Goa 2. Gujarat 66 65 66 64 NA NA NA NA 3. Maharashtra 52 50 44 45 NA NA NA NA F. Southern Region 1. Andhra Pradesh NA NA NA NA NA NA NA NA 2. Karnatal<a 38 41 31 33 36 38 32 34 3. Kerala 92 93 93 95 75 76 73 73 4 Tamil Nadu 50 55 51 52 42 47 43 47 5. Pondicherry 49 53 36 41 NA NA NA NA

Source: Dossier on Cooperatives, NABARD Manual 1998 & 1999. NA = Not Available/ Applicable.

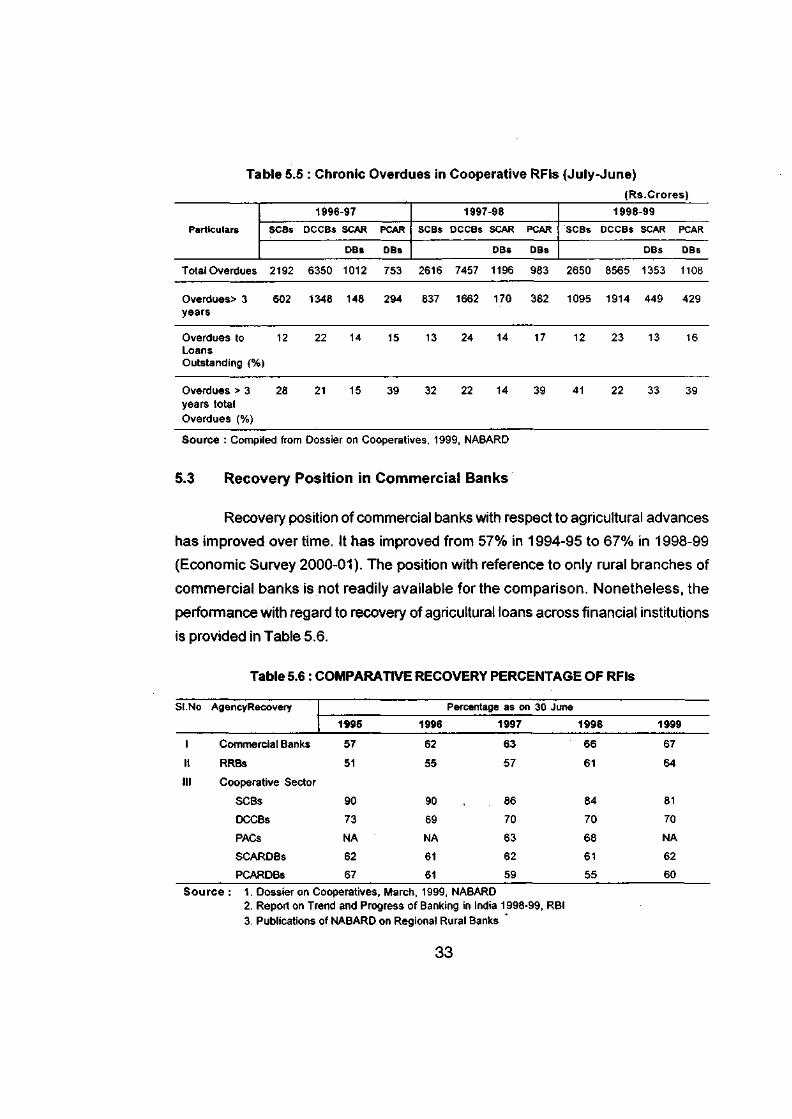

The amount of overdues in co-operative RFIs is shown in Table 5.5. Overall

picture that emerges is that of increasing overdues in short term and long term

co-operative credit in India.

32

Table 5.5 : Chronic Overdues in Cooperative RFIs (July-June) (Rs.Crores)

Source : Compiled from Dossier on Cooperatives, 1999, NABARD

5.3 Recovery Position in Commercial Banks

Recovery position of commercial banks with respect to agricultural advances

has improved overtime. It has improved from 57% in 1994-95 to 67% in 1998-99

(Economic Survey 2000-01). The position with reference to only rural branches of

commercial banks is not readily available for the comparison. Nonetheless, the

performance with regard to recovery of agricultural loans across financial institutions

is provided in Table 5.6.

Table 5.6 : COMPARATIVE RECOVERY PERCENTAGE OF RFIs

SI.No AgencyRecovery Percentage as on 30 June AgencyRecovery

1995 1996 1997 1998 1999

1 Commercial Banks 57 62 63 66 67

II RRBs 51 55 57 61 64

III Cooperative Sector

SCBs 90 90 86 84 81

DCCBs 73 69 70 70 70

PACs NA NA 63 68 NA

SCARDBs 62 61 62 61 62

PCARDBs 67 61 59 55 60

Source : 1. Dossier on Cooperatives, March, 1999, NABARD 2. Report on Trend and Progress of Banking in India 1998-99, RBI 3. Publications of NABARD on Regional Rural Banks

33

Table 5.6 shows that recovery percentage is improving in case of CBs and

RRBs whereas it is worsening in case of co-operatives. However, in absolute sense,

recovery percentage is higher in case of co-operatives (SCBs and DCCBs) generally

compared to that of CBs and RRBs.

5.4 Feasibility of Demand Collection Balance (DOB) Reporting

Demand collection balance (DCB) data relating to recovery are presented

July to June every year whereas other banking statistics are presented April to

March every year. It seems reasonable to think that if DCB is also reported April to

March every year, it would make it consistent with other banking statistics.

However, rural credit being largely agricultural credit, its recovery season

coincides with agricultural season. Recoveries start coming after the Rabi crop in

March and April. If DCB is reported in March, it would provide an underestimate of

actual amount recovered which in fact belongs to that year.

Nonetheless, it is an interesting point to investigate the difference between

DCB ending March and DCB ending June. If the difference is significant, it is

worthwhile to see the figures for few years. If the difference is not significant, it

could very well be changed to ending March every year to make it consistent with

other banking statistics. As a matter of fact, both DCB figures can be compared

and it should not be difficult to do so with available information technology with

RFIs, at least at corporate level.

As regards the shift from June to March, it would make a difference only in

the first year when DCB will be reported for nine months. From the next year onward,

it would be for the whole year. Therefore, the transition from June ending to March

ending should not be difficult if the shift is considered appropriate for comparison with

other banking statistics which are reported according to the financial year ending

March every year.

34

5.5 Factors Affecting Recovery of Loans in RFIs

The discussion above points to the fact that recovery performance of

commercial banks (CBs) and RRBs has improved in the recent past whereas

it has stagnated or worsened in case of co-operatives. However, there are inter-

institutional and intra-institutional differences in recovery performance. This, however,

should not be taken as a matter for complacency because recovery percentage

should be close to hundred per cent if the build-up of NPAs has to be arrested.

Therefore, it is important to consider the factors which are responsible for low

recovery of loans in RFIs.

The factors affecting the recovery of loans by RFIs may be broadly grouped

into two, the external and the internal. Among the internal factors, some are related

to the borrowers and some are related to the RFIs. A few important factors responsible

for poor recovery of loans and therefore build up of NPAs in RFIs are illustrated in

Box. 1.

35

Box 1: REASONS FOR POOR RECOVERY OF LOANS IN RFIs

A. External

Natural calamities Political Interference Loan waiver, write off, etc. Geographical factors Changes in Policy environment Changes in Technology Changes in Economic Conditions Target approach under Government sponsored programmes Legal process

B. Internal

I. RFI Related:

Credit Decisions

Improper identification of borrower—| Lack of appraisal skills Delay in loan sanctioning Under or over financing Insufficient gestation or repayment period Lack of post-disbursement follow-up Lack of borrower contact and poor understanding of rural clientele No thrust on recovery Laxity in internal control systems Poor Management Information System Failure to ensure adequate rapport with government agencies Low motivation and involvement of staff Perception of bank as a charity institution Poor Industrial Relations climate

II. Borrower Related:

Misutilisation of Loan Diversion of Funds Lack of Technical and Managerial Skills Poor maintenance of Assets Wilful Default Personal accident, death, etc. Shifting of place of residence or business

The external factors such as natural calamities, political interference, policy

changes and legal process are outside the control of RFIs but are critical for

creating conducive recovery climate. The internal factors - be related to the

borrower or the RFI, are within the zone of influence of RFIs. Proper methods of

borrower appraisal and credit management may yield good results if RFIs conduct

the job of recovery management well under the changed economic environment of

financial reforms. Various methods to improve recovery performance and NPA

management are discussed in the following section.

36

CHAPTER VI

RECOVERY AND NPA MANAGEMENT

RFIs were never so serious in their efforts to ensure timely recovery and

consequent reduction of NPAs as they are today. It is important to remember that

recovery management, be of fresh loans or old loans, is central to NPA management.

This management process needs to start at the loan initiating stage itself. Effective

management of recovery and NPA comprise two pronged strategy. First relates to

arresting of the defaults and creation of NPA thereof and the second is to handling

of loan delinquencies. The tenets of financial sector reforms were revolutionary

which created a sense of urgency in the minds of staff of RFIs and gave them a

message that either they perform or perish. The prudential norms has forced the

RFIs to look into the asset quality. The recovery and NPA management strategies

adopted by the RFIs may be classified into two broad categories viz. 1. Preventive

and 2. Corrective strategies. While preventive methods are aimed at preventing the

event of a default within the prescribed procedures, the corrective methods are^

aimed at ensuring recoveries once credit is due for payment.

6.1 Preventive Methods

The preventive methods include-

• More careful and responsible scrutiny and appraisal. This includes timely

sanction, realism in fixing repayment schedule and adequacy of credit with

efficient delivery.

• Evolving a broad loan recovery policy and implementing through the cadres

with adequate accountability and empowerment.

• Regular and effective follow up with borrowers and timely action on sensing

the likely default.

• Title, value, etc. and additional security are to be investigated before the

disbursement of loan.

• More detailed information about the borrowers is to be obtained in terms of

37

his/her family background such as i) size of the family ii) number of depen

dents in the family iii) earning members in the family iv) standard of living v)

length of residency in the area, etc.

• Reviewing the advances in time and taking appropriate immediate action.

• Sending demand notices in time.

• Contacting the borrower before the harvest or cash inflow.

• Proper supervision of the borrowal account through personal visits and

calling for periodical returns to get incipient signals of default.

• Efficient MIS system on the borrowers and on the branches.

• Credit rating of clientele.

• Developing an early warning system for identifying potential weakness in

the accounts.

• Strict observance of time schedules.

• Timely extension of period of limitation through debt acknowledgement,

partial payment, renewal of documents etc.

• Timely rephasement or rescheduling of loan in the event of natural

calamities.

RFIs particularly the Regional Rural Banks in recent years have resorted to

the preventive methods to ensure prompt recovery. These methods are seldom

resorted to by the co-operative system because under the co-operative laws strin

gent legal actions could be ensured to force a recovery. In case of Commercial

Banks performing in rural areas, the preventive methods are not so much visible.

This may be because they have a wider option to relocate or consolidate their rural

branches or may be as a percentage the rural lending is small against their total

loans and advances.

6.2 Corrective Methods

The corrective methods conventionally start with initiating legal action for

recovery and followed by lodging insurance claims with DICGCI wherever possible

and initiating coercive action against the borrower and the surety. However, corrective

methods, in recent years, have become more innovative and participatory.

38

The distinction between preventive and corrective methods has become blurred.

Some corrective methods, as practiced mainly by RRBs, are discussed here.

(i) Sharing the Threat Perception

The top management conducts seminars and meetings with the staff and

conveys the crisis in which the RRB is in. It indicates that unless recoveries start

coming the RRB would be closed. Periodical seminars involving small group

of Branch Managers and other staff including the sub-staff are conducted to

educate them about the impact of NPA accounts on the overall profitability of the

branch and RRB and how it affects the very existence of the RRB.

(ii) Staff Motivation

Some Regional Rural Banks have dismantled the demotivated mindset of

their staff by releasing staff benefits like conveyance allowance, housing loan, etc.

and some have effected promotions. These measures have motivated the staff to

perform better in every area and particularly the areas which hurt the bank the most

viz. recovery of loans and management of NPAs. In some banks the organisational

development intervention (ODI) has motivated the staff to step up recovery efforts

(e.g., Howrah Gramin Bank).

Shields, trophies and appreciation certificates are awarded to the staff and

branches showing good recovery performances, in some cases transfer to cen

tres of choice are linked to recovery performance of the concerned staff. In some

banks, in each branch the NPA accounts are allotted to each staff right from the

officer to the messenger for personal follow-up and monitoring.

(iii) Constitution of Special Recovery Cells and Related Measures

The special recovery cell in some RRBs maintains rapport with Nodal Officers

and branches for effecting recoveries. For example in the case of RRBs sponsored

by Syndicate Bank, the Head Office of RRB identifies branches which constitute

39

50% of the total NPA of the bank so that Head Office can have control over the

recovery efforts initiated at the selected high NPA branches through intensive

monitoring. In some cases, top 100 NPA accounts of the bank pertaining to various

branches are identified and monitored directly from the Head Office in co-ordination

with branches. Following steps are taken.

• Executives of RRBs visit selected 100 NPA parties and establish direct

personal contact for ensuring recovery. The RRBs arrange for customers'

meet especially of NPA clients at various important centres to discuss and

address their problems.

The RRBs arrange periodical lawyers' meet to review the status of suit filed

cases.

Pragmatic approach is followed for out of court settlement of loan accounts

and bringing compromise proposals to logical end at the earliest.

Identification of potential NPAs Is done by the end of the first quarter of the

financial year so that preventive measures could be initiated at the beginning.

Staff mobility is ensured and the recovery staff is allowed to hire transport to

suit their needs and no questions are asked.

Staff are deputed to Sub Divisional Officer (SDO) orTehsil courts to assist

the court staff for issuing notices to borrowers In case of overdue loans.

Periodical recovery camps are held In villages In co-ordination with Government

officials.

The borrowers are constantly reminded about their overdues and notice to

clear them are regularly sent.

List of defaulters is displayed in the notice board of the branch without

disclosing the account number, amount of loan, overdue, etc. The Idea is

simply to draw attention of the defaulters to contact the Branch Manager.

A copy of the list Is also given to the counter clerk so that he/she can ask the

defaulters whenever they come to the branch to transact to meet the Branch

Manager.

40

(iv) Involvement of Government Agencies

There are instances where RRBs are able to recover overdue loans by

involving District Administration. Some of the methods adopted to involve government

machinery are listed below:-

• Revenue recovery notices are issued by the District Magistrate or Sub-

Divisional Officer once a year advising Ixjrrowers to deposit the overdue amount

in the RRB to avoid legal actions permitted under the law.

• The list of defaulters is given to the Revenue Authorities or Tehsildars in case

of agriculture loans, in case of industrial loans the list is given to District

Industries Centres for follow-up.

• Joint recovery teams are formed in which Tehsildars, Revenue Inspector,

Patwari and RRB Staff jointly participate to expedite the execution of

decrees.

• Help of Block Development Officer (BDO) is solicited in case of Government

sponsored schemes. Joint inspections are carried out with BDO and incase

of accounts where misutilisation of loans and subsidy amount is noticed,

joint First information reports (FIRs) are lodged.

(v) Extraordinary Methods

Apart from what has been stated above some RRBs have

adopted certain extra-ordinary methods to ensure recovery and a few of

such methods adopted by the RRBs are narrated here.

• Announcing the names of the defaulters in market places through drum beating.

• Approaching influential bon-owers who are defaulters, while important functions

such as thread ceremony, marriage, etc. are going on in their houses. Cases

have been reported where the branch staff have directly asked for repayment

during such functions and loans have been repaid because the borrowers

(defaulters) tried to protect their self prestige in the presence of invited guests

and relatives. But there are also instances where the branch staff have simply

41

attended the marriage ceremony with gifts and repayments have followed.

In some cases, the branch staff have paid money for the performance of

last rites in the event of the death in the family of the borrower (defaulter)

and repayments have followed.

• List of defaulters prepared and pasted at public places and the recovery

van, a hired jeep, was flag marched with banner Vasuli Dal (recovery squad)

by order of district administration. Bank records related to recovery were kept

wrapped in red cloth to impress the public that Government officials are also

involved in the recovery of bank dues.

• In some places the visit of a police constable to a particular person's house is

considered inauspicious and banks' taking advantage of this aspect have

served recovery notices through police constables and have put pressure

to get the loans recovered.

The methods mentioned above have either tried to tarnish the social image

or appeal to the morale of the borrower to repay the banks' dues. While these meth

ods have yielded fruitful results in some places it may be dangerous and risky to

adopt such methods everywhere.

To sum up, it may be seen that whether it is preventive or corrective method,

proper motivation and commitment of the bank staff, strict adherence to proper loan

supervision and monitoring and a congenial relationship with Government machinery

contribute to good recovery. But there may be cases where all or any of these

methods fail and consequently the loans have to be finally written off. Moreover, the

legal procedure in regard to recovery of bank dues is cumbersome, lengthy and

time consuming and it is time to critically examine these laws for their efficacy.

42

(vi) Corrective Management for NPA Management

The following diagram shows the corrective management of NPAs.

Study the problems of NPAs - branch-wise, amount-wise and age-wise

I Prepare a loan recovery policy and strategies exclusively for NPAs

1 Create Special Recovery Cell at various levels

I jnd

I 'en

I Identify critical branches for intensive recovery

t Fix targets of recovery and draw timebound action programme i

gtf

i Select proper strategy for solving the problem of each NPA account

I Monitor implementation of time bound action plan

Under corrective management, each NPA has to be examined in totality and

on the basis of various factors like past efforts, period of overdue, client profile,

natural calamities etc. and suitable strategy is decided. Since the reasons or factors re

sponsible for sliding a good loan into bad one vary for each loan account, it is neces

sary to adopt different strategies for different NPA accounts. Some corrective man

agement strategies for reducing NPAs are:

• Recovery Strategies

effect recovery

compromises to improve recovery status of account

partial write off

adjustment of collateral securities

pressure on guarantors

43

special recovery drive

help from revenue authorities

Rephasement of loans or Rescheduling of demands

Rehabilitation of potentially viable units

Compromise with borrowers for final settlements

Calling up the advances and filing of civil suits

Approaching debt recovery tribunals

Settlement of claims with Deposit Insurance and Credit Guarantee

Corporation of India (DICGCI) and Export Credit Guarantee Corporation

of India (ECGCI).

Write off the outstandings

6.3 Recovery Through Legal Process

Experience has shown that legal support is critical to recovery management.

The recovery of loans through crystallised collateral and other back-stoppings is

subject to a prolix process as the present legal system normally does not provide a

fast and effective exit route. Discussion on recovery process through legal means

amenable to RFIs is presented in the following section.

6.3.1 Legal System Administration

The security obtained for a loan account has only one major objective, that,

in the event of default, the RFI should be able to recover the money through the

security. It could be by sale of the security or through the compromise process as the

borrower would not like to lose the security.

The process of recovery through legal process involves proper documentation

of credit, issue of notices, filing and sustaining of suit in the court of law, obtaining the

decree, issue advertisement in the newspapers on the intention of execution of decree,

arrange for execution, make the sale, realize the proceeds and adjust the loan. In

almost all the activities, the RFI needs the services of professionals such as lawyers,

court receivers, etc. The bank has to meet all these expenses and adjust or seek

44

reimbursement once the decree is executed from out of sale proceeds as per decree.

However, in most cases the cost aJlowed is far less than the actual, inflicting high

expenditure to the banks. It is seen that in case of RFIs, the legal process is not only long

drawn buK also expensive.ln the meantime, as per prudent accounting procedure, the money

will remain in the books of accounts without earning anyinterest. Also, making it imperative

to make provisions as per directives. The following points are worth mentioning.

i The law does not allow sale as an automatic right of the creditor - except

through a court process even in the case of mortgage,

i The procedure for seizure and foreclosure is involved and costly,

ii In many cases, such as tribals, property alienation is not permitted,

iv In case of small loans to poor, there is no asset available for attachments.

Therefore, proper and effective legal process is very crucial in creating a

repayment atmosphere. If it is proved that the legal process is time consuming and

long, it would make the security ineffective. Once this is well known, borrowers would

not hesitate to offer security as they can default with impunity and get compromises.

Maharastra Land Development Bank (LDB) has, in fact put the entire compromise

process in the form of Bye-Laws which encourage a borrower to default to and then

settle the dues after getting substantial interest waiver. Nowadays, compromise

proposals are on the increase. For the compromise process to start the RFI will have

to complete the legal process and obtain the decree. Once the borrower is apprehensive

of losing the security he comes to the compromise table. In case of loan accounts

where there are no assets to proceed against, the compromise is a non-starter.

6.3.2 Use of Collaterals and Collateral Substitute

It is seen that the recovery process through legal system with or without collat

eral is equally costly and lengthy. The court fee is payable on the amount of default or on

the amount to be recovered and not on the value of the security. Judiciary and Revenue

machinery have been generally unable to help the RFIs in recovery. The sheer volume

of cases weighs them down even if the system has the intention. Except for the

demonstrative effect, filing of summary or money suit for unsecured loans does not

45

provide any tangible benefit for the RFIs. RFIs observe that pursuing such suits to a

logical end is not prudent as it involves higher administrative and risk costs for them.

The expenses made on the court lie in the books of accounts until their

recovery is made by effecting the sale. This is a drain on the RFI's resources and

is often without any return for the RFI during the period. The RFIs feel that the cost of executing the collateral is quite high for the RFIs.

6.3.3 Efficacy of Cooperative Law

Under State enactments, the Cooperative Banks and Credit Societies enjoy

certain privileges like 'change' and priority over other creditors for recovery of dues

from members. They also enjoy exemption from payment of stamp duty and

registration charges for mortgaged land while availing agricultural loans (upto

some financial ceiling) and the creation of mortgage by the borrower by simple

declaration.

In addition, the Cooperative Banks enjoy special facilities to expedite the

process of recovery of their dues without recourse to civil courts. State Laws

authorise some officials of the Government (Registrars of Cooperative Societies)

to exercise the powers of a civil court to order attachment and sale of property of

debtor to fulfill the repayment obligation to a cooperative society.

The essence of these special facilities, usually referred to as summary procedure,

is that the authorised officials are empowered to issue an order having the force of a

decree of a civil court for payment of any sum due to the banks by sale of the

property changed or mortgaged in favour of the bank. These powers have been

granted to facilitate recovery of dues of cooperatives without having to resort to time

consuming litigation in civil courts. The Recovery performance of the cooperatives is

not improving despite the above special facilities showing the inept handling by

government machinery. The cost, despite the easy procedure, is high as the high

cost of the departmental officials for the semi judiciary process is met by these

banks in addition to recovery officers of the bank. Further, the execution of awards

46

through sale gets, most often, vitiated by external forces, as being the government

agency, cutting the root of the efficacy of the special facilities supposedly given to

co-operatives.

6.3.4 Revenue Recovery Acts

An Expert Group headed by Shri R.K. Talwar in 1970 had recommended

extension of similar facilities to commercial banks by appropriate State legislation

(TalwarCommittee, 1970). On the basis of the recommendations of the Talwar Committee,

the State Governments (barring nine) have passed the Agricultural Credit Operations

and Miscellaneous Provisions (Banks) Act, The act empowers designated officials

of Revenue Department to issue an order having a force of decree of a civil court

for payments of any sum due to a bank by sale of the property charged or mortgaged

in favour of the bank. This facilitates foreclosure of mortgage on land in bank's

favour and brings the property for sale. Under the act a nominal fee and not the

entire salary of the government official, is charged to the bank.

The recovery officers under the Act have helped in recovering small loans of

the banks. The banks, in States like Uttar Pradesh, Karnataka, have taken proactive

steps to fund the cost (salary of recovery officers and other incidental expenses) by

making a collective contribution for their establishment and/or allowing a recovery fee

of 5% to 10% of the recovered amount towards their maintenance. But the above

system has not worked uniformly well in all the states. The state governments had

found it difficult to spare officials possessing zeal for this type of work which is a

prerequisite for a supporting machinery to work efficiently. Use of government official

machinery helps in infusion of the threat perception amongst people, but the political

interference becomes a part of it. Therefore, the lack of political will beconrles a

hindering factor in the process. It would perhaps be necessary to study the

relative efficiency of the system across the country, so that improvements wherever

possible, could be made.

47

6.3.5 Debt Recovery Tribunals

Special Debt Recovery Tribunals (SDRTs) have been set up under the Recovery

of Debts due to banks and Financial Institutions Act, 1993 for expeditious adjudication

and recovery of debts. These courts now adjudicate banks' suits involving amount

of Rs 10 lakh and above by transferring the cases pending with the civil courts.

These loans are nomnally secured with collaterals. Only six such tribunals are operative

now. The number of such tribunals is inadequate resulting in large number of cases

pending before them. They are not yet equipped with proper infrastructure and flexibility

to function smoothly.

For recovery of small loans and to ensure quick justice on settlement of

dues, Lok Adalats (People's Courts) have been set up in some States. These

courts are headed by retired high court judges and two other members. These

small courts are found to be of success in selected pockets. Efforts are continuing

to popularise this arrangement. The judgement of these courts are found to lack

the teeth of a civil court judgement for their enforceability. But these courts have

provided good opportunity to narrow or bridge the differences between the banker

and the defaulter by creating a favourable environment for a settlement and also in

formalising such settlements.

6.3.6 Legal Changes Required

From the above and the immensity of cases pending in the courts it is obvi

ous that the recovery of RFI dues through the legal process has not been encouraging.

With the introduction of the NPA norms and as the secured NPA loans are

subject to lesser provisions than the unsecured NPA loans, it is essential to look

into the effectiveness of security and legal process towards recovery. There is no

doubt that the laws governing the collaterals need to be improved and the legal

process expedited. It is perhaps essential to start many units of the Revenue Recovery

(RR) procedures in each state. Increasing the efficiency of the RR courts, SDRTs

and making the sale of a mortgaged or hypothecated asset possible without court

intervention are some of the steps that need to be taken in this direction. As more

48

and more RFIs feel the pressure of NPAs such improvements are crucial to the

success of rural financial intermediation.

One of the most important causes hampering the recoveries of NPAs, among

other things is a long-winded and ineffective legal recourse available to RFIs in India. A

legal framework that clearly defines the rights and liabilities of parties to contracts

and provides for a speedy resolution of disputes is essential for efficient financial

intermediation. It is true that existing legal framework is archaic, slow and outright

non-productive as discussed above. It is also not in tune with the changing commercial

practices and banking refonns. Some of the legal acts which were enacted in nineteenth

century and therefore require immediate overhauling are Indian Contract Act 1872,

Transfer of Property Act 1882 and Indian Stamp Act 1899.

It is understood that RBI has already constituted committees for looking into

the necessary amendments to various banking related Acts. Simultaneously, there is

a committee which is looking into the amendments necessary in the plethora of

Acts that affect the collateral and collateral efficiency.

Improvements in the legal process involving collaterals will have no impact

in the case of small loans where the borrowers have no collaterals to offer. It is

here that the propagation of various models of microfinance will be welcome.

6.4 Macro Policy issues

6.4.1 Central Government and State Governments

The great contribution central and state governments can make in improving

recovery management of RFIs is by not announcing politically motivated schemes

like distribution of loans through loan melas, loan waivers, interest waivers, etc.

State government have to ensure that no state law governing the business

of co-operative banking is curtailing the liabilities provided under B.R. Act by RBI.

That is, state governments need to liberate banking co-operatives in line with

B.R.Act. This includes freedom on interest rate matters, terms of lending etc.

49

Regarding the law of mortgage, the response has been to enact the

separate enactments by many states to remove difficulties in recovery of loans

and to speed up the process of enforcement and foreclosure. Besides, suggesting

amendments in the various legal Acts, Narasimham Committee II (1998) has

recommended two approaches to recover NPAs and thus, to cleanse the balance

sheet of the banks. They are:

(i) Setting up of Special Tribunals for recovery of dues to banks

and financial institutions. (Originally suggested by the Tiwari Committee

(1984) and subsequently endorsed by both the Narasimham

Committees)