38

© OECD/IEA 2010

© OECD/IEA 2010

© OECD/IEA 2010 © OECD/IEA 2011

Overview

1. The cutting edge

2. Getting the infrastructure right

3. Evolved system operation

4. Opening up the power market

5. Integration economics

© OECD/IEA 2010 © OECD/IEA 2011

Germany

50Hertz Amprion EnBW TNG TenneT Germany

Date & time

01/01/1

1

06:00

07/09/1

1

14:00

25/04/11

13:00

08/05/1

1

13:00

08/05/11

13:00

Wind 6 383 2 404 54 5 034 8 070

PV 0 1 517 1 793 5 987 12 627

Load (MW) 5 145 11 082 4 617 6 876 34 435

Max ratio 124% 35% 40% 160% 60%

Share of wind in 2011: 6%

Share of solar PV: 2%

Instantaneous share of wind and PV in Germany

© OECD/IEA 2010 © OECD/IEA 2011

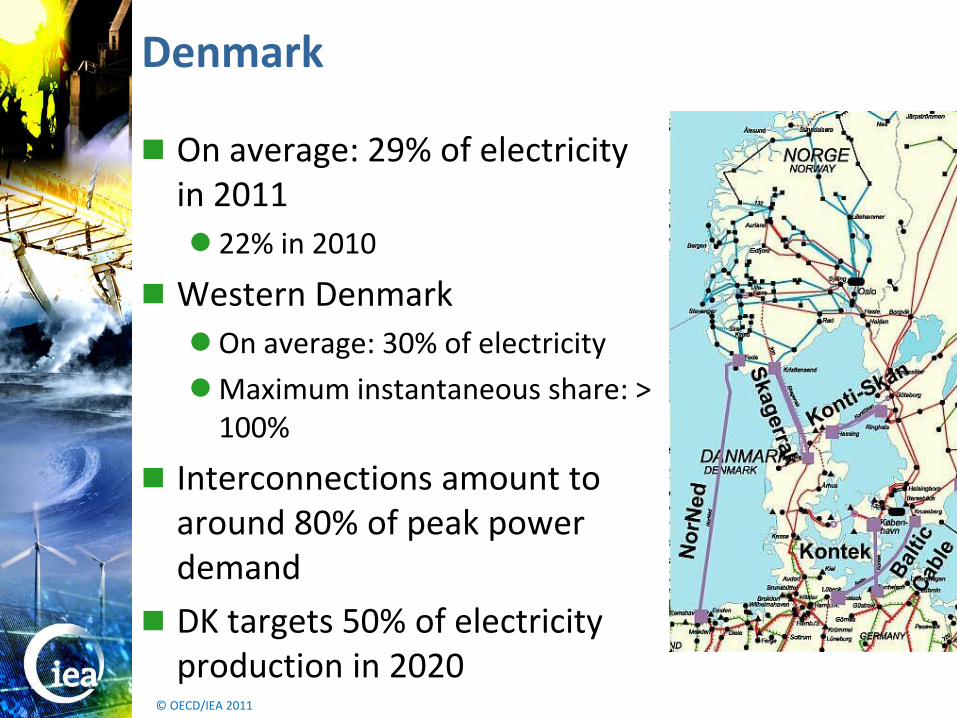

Denmark

On average: 29% of electricity in 2011

22% in 2010

Western Denmark

On average: 30% of electricity

Maximum instantaneous share: > 100%

Interconnections amount to around 80% of peak power demand

DK targets 50% of electricity production in 2020

© OECD/IEA 2010 © OECD/IEA 2011

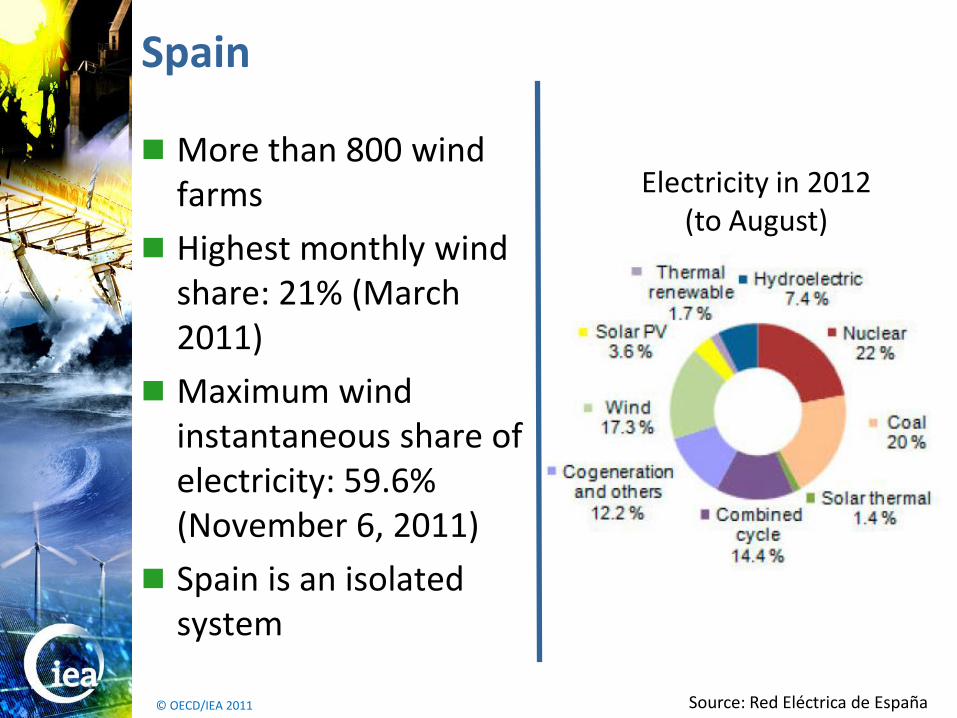

Spain

More than 800 wind farms

Highest monthly wind share: 21% (March 2011)

Maximum wind instantaneous share of electricity: 59.6% (November 6, 2011)

Spain is an isolated system

Source: Red Eléctrica de España

Electricity in 2012 (to August)

© OECD/IEA 2010 © OECD/IEA 2011

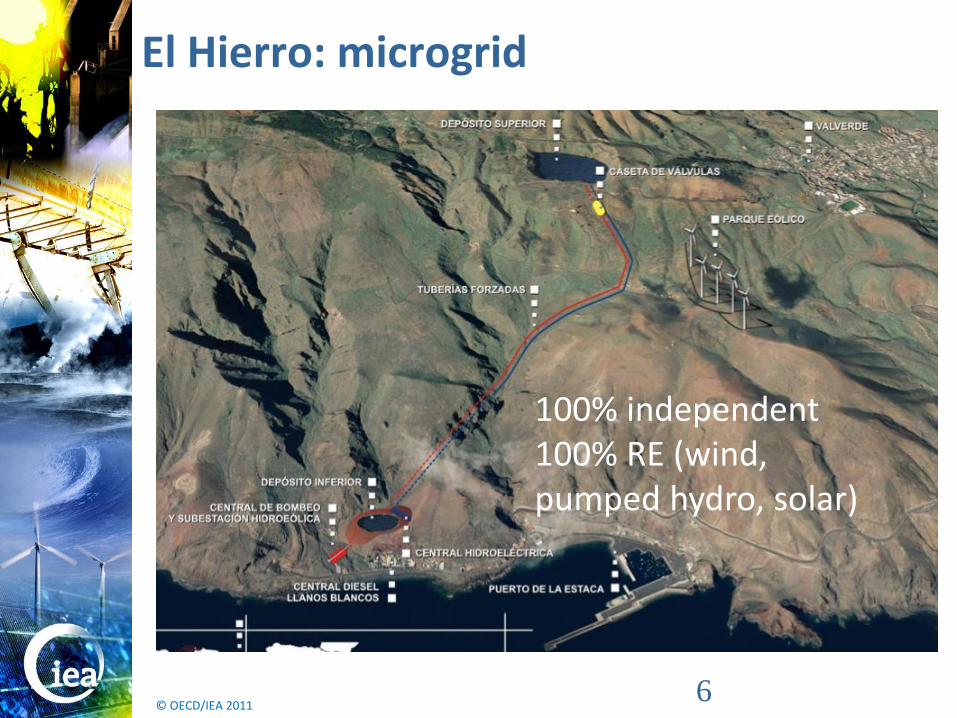

El Hierro: microgrid

100% independent 100% RE (wind, pumped hydro, solar)

6

© OECD/IEA 2010 © OECD/IEA 2011

Overview

1. The cutting edge

2. Getting the infrastructure right

3. Evolved system operation

4. Opening up the power market

5. Integration economics

© OECD/IEA 2010 © OECD/IEA 2011

Grid planning at continental scale

EU: 10 year Network Development Plan of all European system operators

Advance warning of bottle necks

© OECD/IEA 2010 © OECD/IEA 2011

European transmission drivers

Source: ENTSOE 2012: 10 year network development plan 2012

© OECD/IEA 2010 © OECD/IEA 2011

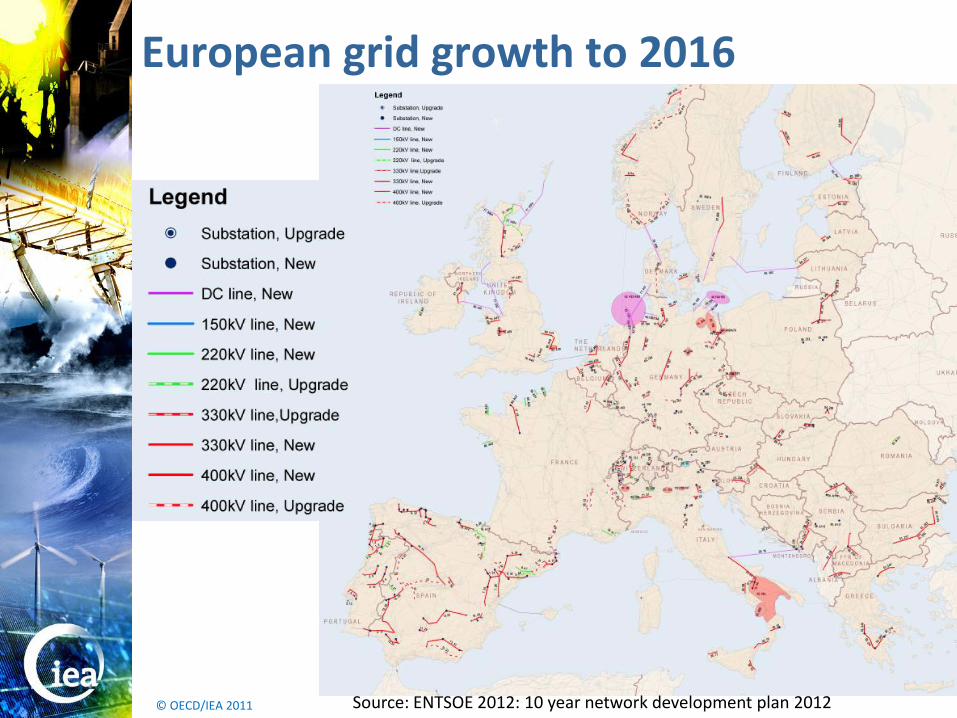

European grid growth to 2016

Source: ENTSOE 2012: 10 year network development plan 2012

© OECD/IEA 2010 © OECD/IEA 2011

European grid growth from 2017

Source: ENTSOE 2012: 10 year network development plan 2012

© OECD/IEA 2010 © OECD/IEA 2011

Germany transmission planning

2009 Power Grid Expansion Act

HV electricity highways to manage congestion

DE: 2010 Energy Concept: system-wide planning

Wind no longer in isolation Conventional and renewable plants

Extension, reinforcement

Additional flexibility

2011 Grid Expansion Acceleration Law

Reduced delays in planning and permitting From 10 years at present to max 4 years

Federal Plan for Transmission Networks

Informed by EU-wide Ten Year plan

© OECD/IEA 2010 © OECD/IEA 2011

Texas CREZ

Which comes first: wind plant or transmission?

Objective: to move 18.5 GW of wind power from West Texas and the Panhandle to metropolitan areas

Source: PUCT 2012

© OECD/IEA 2010 © OECD/IEA 2011

Mexico consolidation

Baja California’s 2 grids are isolated from the the SEN

The north is connected to WECC

CFE plans to interconnect by 2015

And to increase trade with USA

?

© OECD/IEA 2010 © OECD/IEA 2011

Public support for transmission

German population environmentally aware, relatively wealthy

But who really wants new transmission pylons?

Public support campaign in Energy Concept

To Build understanding that more VRE = more grid.

New website launched by TSOs

Range of new-build scenarios

Presentation of first grid development plan in June

Compensation for new-build hosts?

10 year delays not uncommon in Europe

© OECD/IEA 2010 © OECD/IEA 2011

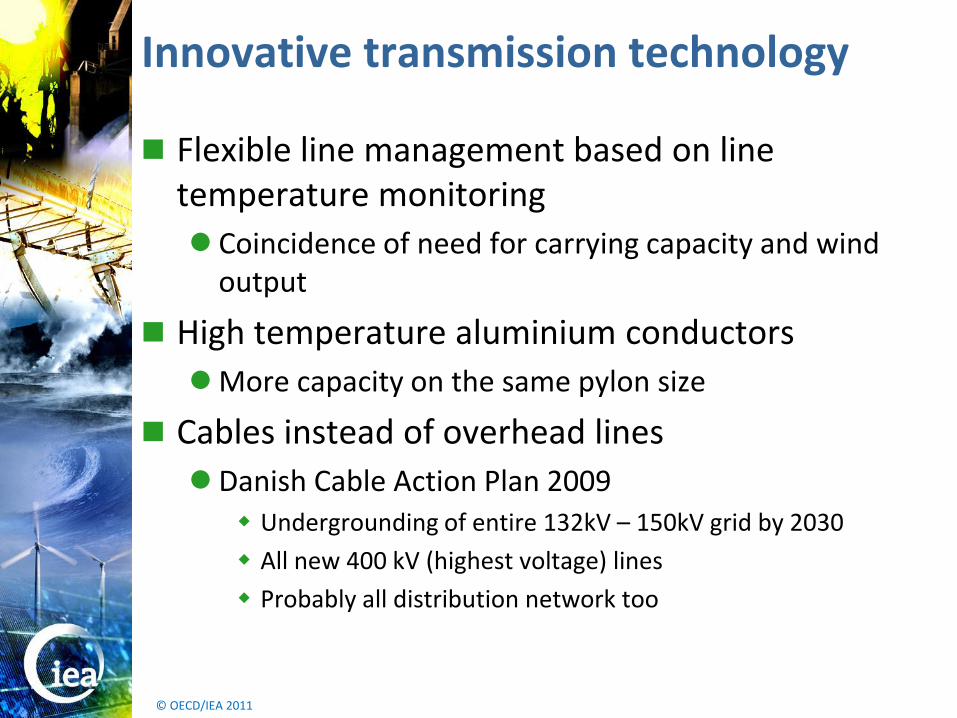

Innovative transmission technology

Flexible line management based on line temperature monitoring

Coincidence of need for carrying capacity and wind output

High temperature aluminium conductors

More capacity on the same pylon size

Cables instead of overhead lines

Danish Cable Action Plan 2009 Undergrounding of entire 132kV – 150kV grid by 2030

All new 400 kV (highest voltage) lines

Probably all distribution network too

© OECD/IEA 2010 © OECD/IEA 2011

Overview

The cutting edge

Getting the infrastructure right

Evolved system operation

Opening up the power market

Integration economics

© OECD/IEA 2010 © OECD/IEA 2011

Spain: CECRE

Real time monitoring of every grid-connected wind and solar PV power plant in the country

© OECD/IEA 2010 © OECD/IEA 2011

Denmark: System operator

Single grid entity

Merger of ELTRA and ELKRAFT

East and west recently connected

100% state-owned

Controlled by Ministry of Climate and Energy Key driver towards government target of 50% wind by 2020

No conflict of interest Extension / reinforcement delays minimal

Energinet has responsibility for market operation (with other Nordic TSOs)

Can develop market to reflect needs of VRE

Can address congestion signaled by the market

© OECD/IEA 2010 © OECD/IEA 2011

Germany: Supportive RE

Distribution (low voltage) grids are usually not actively managed… But more and more plant is installed at this level

DE 2011: remote curtailment ceiling lowered from 100 kW to 30 kW – mainly due to PV proliferation

From village orphan… to pillar of the community

New German wind and PV plants are required to support the grid; Incentives to refurbish older plants too

In Denmark since 1999 on HV grid

© OECD/IEA 2010 © OECD/IEA 2011

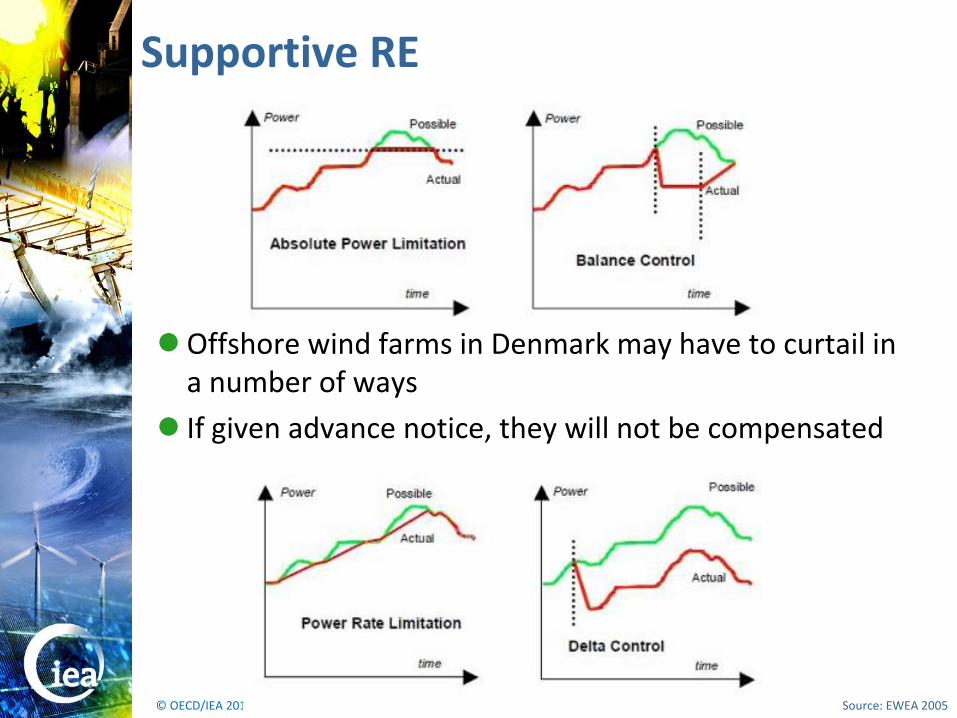

Supportive RE

Source: EWEA 2005

Offshore wind farms in Denmark may have to curtail in a number of ways

If given advance notice, they will not be compensated

© OECD/IEA 2010 © OECD/IEA 2011

Flexible resources

German fund encourages new-build fossil plants to use most flexible available technology

New generation of super flexible gas plants – GE Siemens, Alstom

To be more complementary with VRE output

CHP plants

Larger heat storage – to decouple heat and power production

Electric heaters can take advantage of surplus cheap electricity Danish tax on electricity use in CHP reduced in 2008

© OECD/IEA 2010 © OECD/IEA 2011

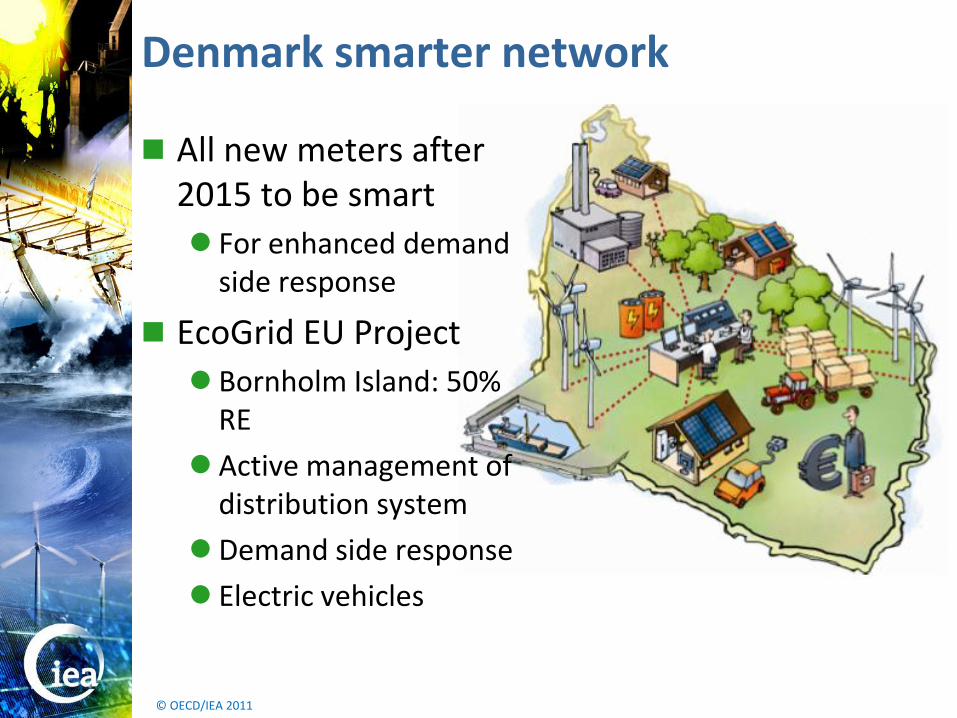

Denmark smarter network

All new meters after 2015 to be smart

For enhanced demand side response

EcoGrid EU Project

Bornholm Island: 50% RE

Active management of distribution system

Demand side response

Electric vehicles

© OECD/IEA 2010 © OECD/IEA 2011

Overview

The cutting edge

Getting the infrastructure right

Evolved system operation

Opening up the power market

Integration economics

© OECD/IEA 2010 © OECD/IEA 2011

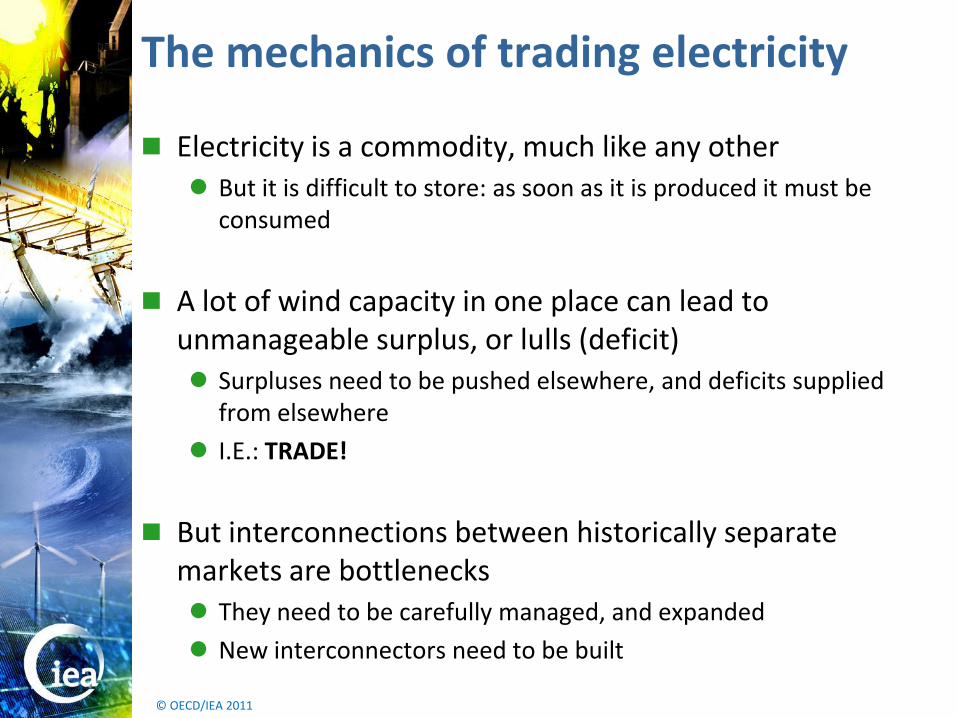

The mechanics of trading electricity

Electricity is a commodity, much like any other But it is difficult to store: as soon as it is produced it must be

consumed

A lot of wind capacity in one place can lead to unmanageable surplus, or lulls (deficit) Surpluses need to be pushed elsewhere, and deficits supplied

from elsewhere

I.E.: TRADE!

But interconnections between historically separate markets are bottlenecks They need to be carefully managed, and expanded

New interconnectors need to be built

© OECD/IEA 2010 © OECD/IEA 2011

Balancing through trade

Netherlands

Interconnection turns surplus into income

Enables aggregation (smoothing) of output over the connected area

E.G.: Planned Denmark – Netherlands COBRAcable

As weather front moves

south, flow is reversed

© OECD/IEA 2010 © OECD/IEA 2011

European market couplings

Nordic market splitting

DE

Central and West European Market Coupling Interim Tight

Volume Market Coupling

NO

FR

SE

© OECD/IEA 2010 © OECD/IEA 2011

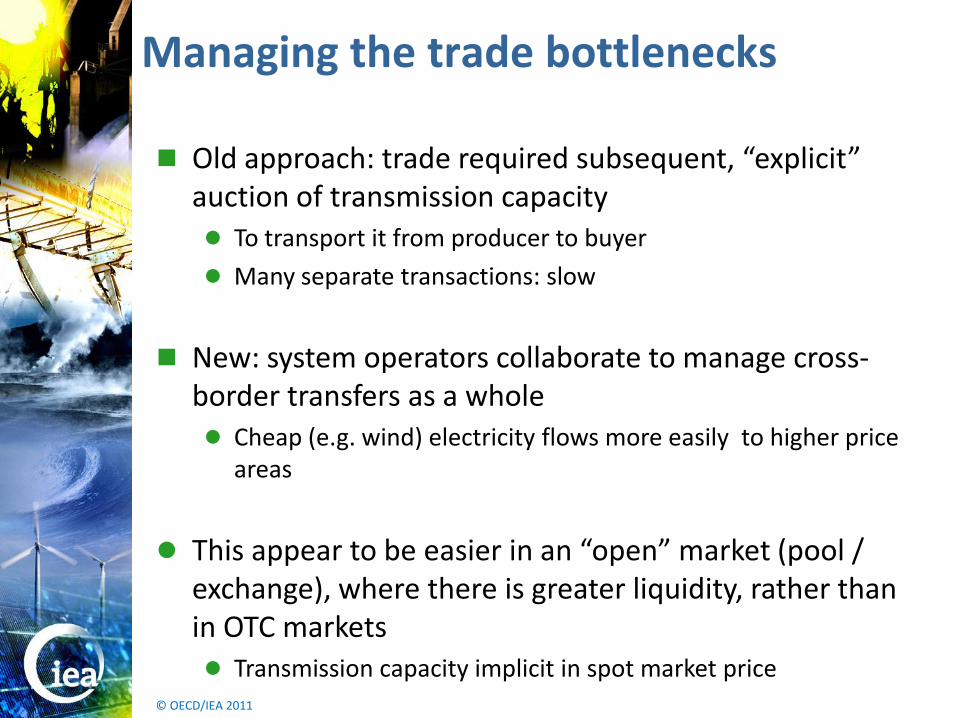

Managing the trade bottlenecks

Old approach: trade required subsequent, “explicit” auction of transmission capacity To transport it from producer to buyer

Many separate transactions: slow

New: system operators collaborate to manage cross-border transfers as a whole Cheap (e.g. wind) electricity flows more easily to higher price

areas

This appear to be easier in an “open” market (pool / exchange), where there is greater liquidity, rather than in OTC markets Transmission capacity implicit in spot market price

© OECD/IEA 2010 © OECD/IEA 2011

Flexible power market

EPEX (FR,DE,AT,CH): 33% of European power 25% of German power

Intra-day trading grew 500% in the three years to 2010.

Needs resulting from wind forecast uncertainty to be traded on the intra-day since 2011

Gate closure times reduced to 45 minutes ahead in both day ahead and intra-day markets

Balancing market (after EPEX closes) Now all tenders disclosed through online platform

Secondary reserves common across all 4 areas

© OECD/IEA 2010 © OECD/IEA 2011

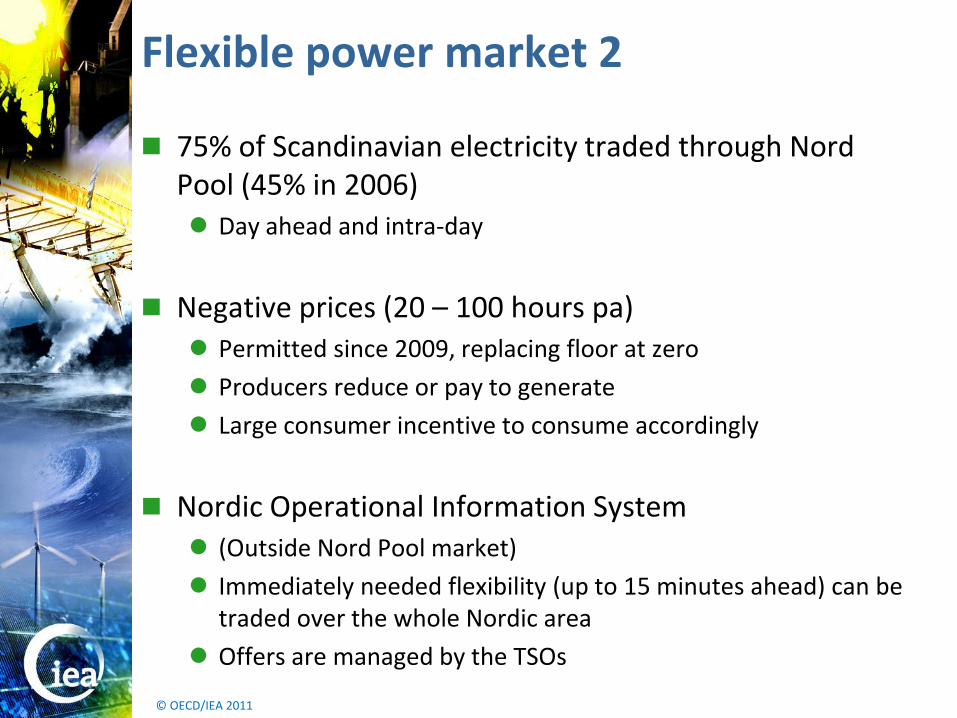

Flexible power market 2

75% of Scandinavian electricity traded through Nord Pool (45% in 2006) Day ahead and intra-day

Negative prices (20 – 100 hours pa) Permitted since 2009, replacing floor at zero

Producers reduce or pay to generate

Large consumer incentive to consume accordingly

Nordic Operational Information System (Outside Nord Pool market)

Immediately needed flexibility (up to 15 minutes ahead) can be traded over the whole Nordic area

Offers are managed by the TSOs

© OECD/IEA 2010 © OECD/IEA 2011

Overview

The cutting edge

Getting the infrastructure right

Evolved system operation

Opening up the power market

Integration economics

© OECD/IEA 2010 © OECD/IEA 2011

Balancing costs

Differences: conventional portfolio, geospread, interconnection, storage, market design, system operation…

© OECD/IEA 2010 © OECD/IEA 2011

© OECD/IEA 2010 © OECD/IEA 2011

The impact of long distance

© OECD/IEA 2010 © OECD/IEA 2011

Chinese costs without transmission

The gradient of the curve reflects where the cheapest wind is

© OECD/IEA 2010 © OECD/IEA 2011

… and with transmission

The gradient of the curve reflects where the cheapest wind is

© OECD/IEA 2010 © OECD/IEA 2011

In summary…

Variability is not stopping deployment

There may be a massive grid building / renewal task But transmission of RE should not be viewed in isolation

Governments can reduce investment risk by “leading” with the grid

Long distance transmission has a major impact on cost

An able system operator is a priceless ally

Wind and solar can help support the grid

The search for additional flexibility is on

Open markets enable optimal use of variable and flexible power plants

Balancing costs are more modest than expected

© OECD/IEA 2010 © OECD/IEA 2011

Seminar follow-up: Hugo Chandler [email protected] London +44 207 287 1288