42

Oil and Mineral Commodities, and the Financial Crisis 30 March 2009 Olle Östensson

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | madison-summers |

| View: | 217 times |

| Download: | 0 times |

Oil and Mineral Commodities, and the Financial Crisis

30 March 2009

Olle Östensson

Outline

• A short history of the commodites price boom

• Why did oil and mineral prices rise and why did they rise by so much?

• The downturn: How much was due to the financial crisis?

• The recession: – How deep and how long?– Will things go back to « normal »?

The commodity price boom

0

50

100

150

200

250

300

350

400

450

50001.1

997

07.1

997

01.1

998

07.1

998

01.1

999

07.1

999

01.2

000

07.2

000

01.2

001

07.2

001

01.2

002

07.2

002

01.2

003

07.2

003

01.2

004

07.2

004

01.2

005

07.2

005

01.2

006

07.2

006

01.2

007

07.2

007

01.2

008

07.2

008

Price Index - All groups (current dollars terms) Food

Tropical beverages Vegetable oilseeds and oils

Agricultural Raw Materials Minerals, ores and metals

Crude petroleum*

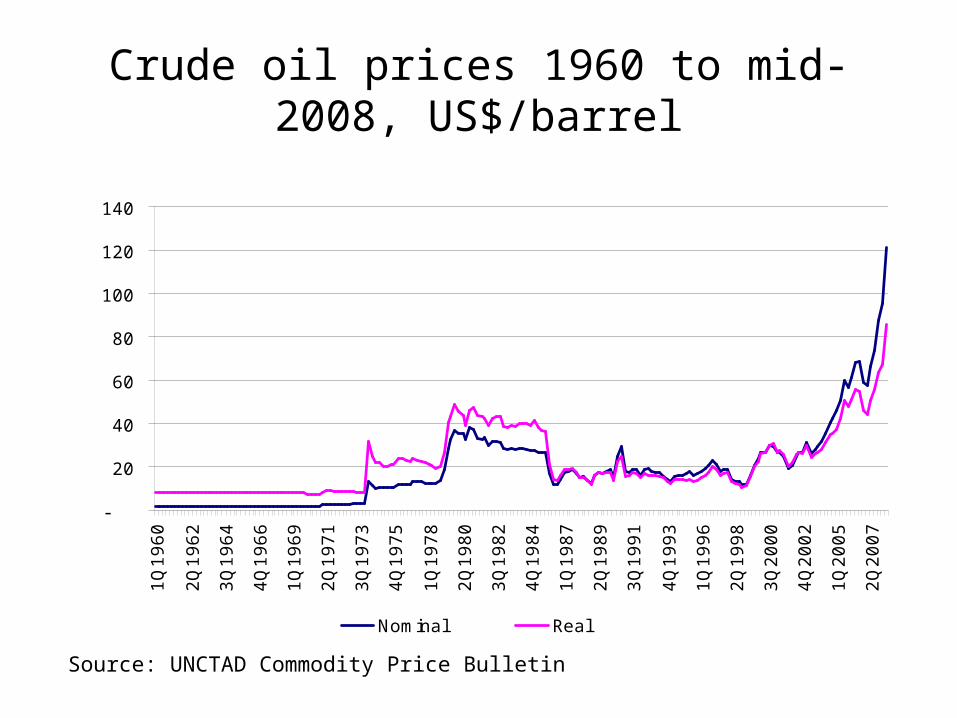

Crude oil prices 1960 to mid-2008, US$/barrel

-

20

40

60

80

100

120

140

1Q

1960

2Q

1962

3Q

1964

4Q

1966

1Q

1969

2Q

1971

3Q

1973

4Q

1975

1Q

1978

2Q

1980

3Q

1982

4Q

1984

1Q

1987

2Q

1989

3Q

1991

4Q

1993

1Q

1996

2Q

1998

3Q

2000

4Q

2002

1Q

2005

2Q

2007

Nominal Real

Source: UNCTAD Commodity Price Bulletin

Reasons for the price increase

• Demand– Two years – 2003 and 2004 – with above trend increases– Geographical differences– Expectations

• Supply– Slow capacity expansion– Low spare capacity, concentrated in one place– Inventories

• Supply-demand imbalances and price spikes in commodity markets

• Other factors– US$ depreciation– Mismatch of refinery capacity– Speculation?

Global oil demand, change on previous year, %

Source: International Energy Agency, Oil Market Report, various issues

-2

-1

0

1

2

3

4

5

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

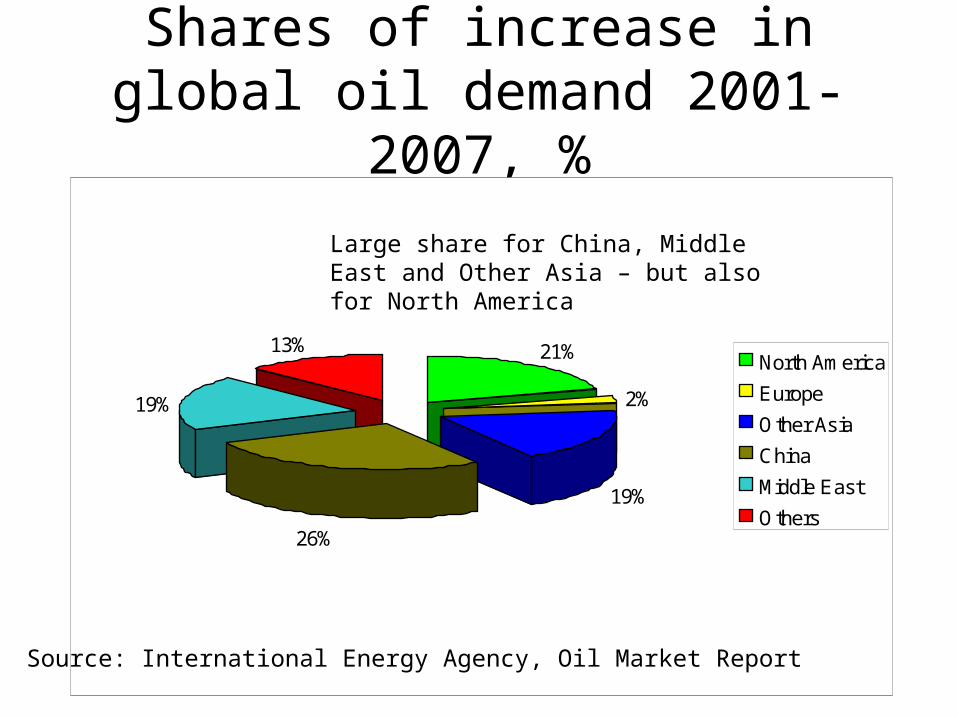

Shares of increase in global oil demand 2001-2007, %

21%

2%

19%

26%

19%

13%North America

Europe

Other Asia

China

Middle East

Others

Source: International Energy Agency, Oil Market Report

Large share for China, Middle East and Other Asia – but also for North America

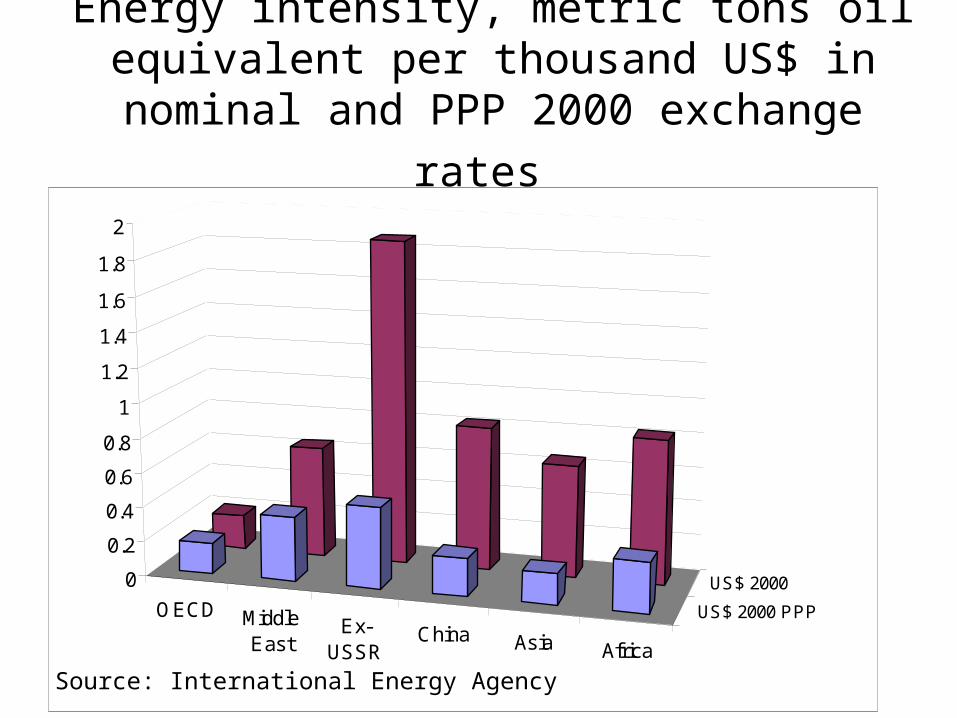

Energy intensity, metric tons oil equivalent per thousand US$ in nominal and PPP 2000

exchange rates

OECD MiddleEast

Ex-USSR

China Asia Africa

US$ 2000 PPP

US$ 20000

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Source: International Energy Agency

China was expected to follow “the Korean path”, but didn’t

Figure 8. Energy intensity 1965-2007, tons of oil equivalent per million $ in GDP, PPP adjusted

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

China

India

Japan

Republic of Korea

USA

Russian Federation

Reasons for price spikes in commodity markets

• Very low short term price elasticity of demand because of lack of substitutes and because use cannot be postponed

• Very low short term elasticity of supply because of fixed capacity and high capacity utilization (a logical consequence of product standardization)

• When prices are perceived to be rising, target inventory levels are raised because buyers want to avoid paying higher prices

• If there is a perceived risk of shortage, target inventory levels are raised to avoid having to default on deliveries

• Precautionary stocking is insensitive to price increases and will continue long after prices have exceeded “reasonable” levels

Supply side factors: Capacity developments

• Slow capacity increase– Low oil prices in the 1990s reduced the incentive to

add to capacity – There was no spare capacity among non-OPEC

producers

• OPEC spare capacity– In the 1990s, OPEC had cut back production– As late as 2001, OPEC spare capacity was 5.6 million

barrels/day– In June 2008, it was 1.5 million barrels/day (less than

a week’s world consumption), all in Saudi Arabia

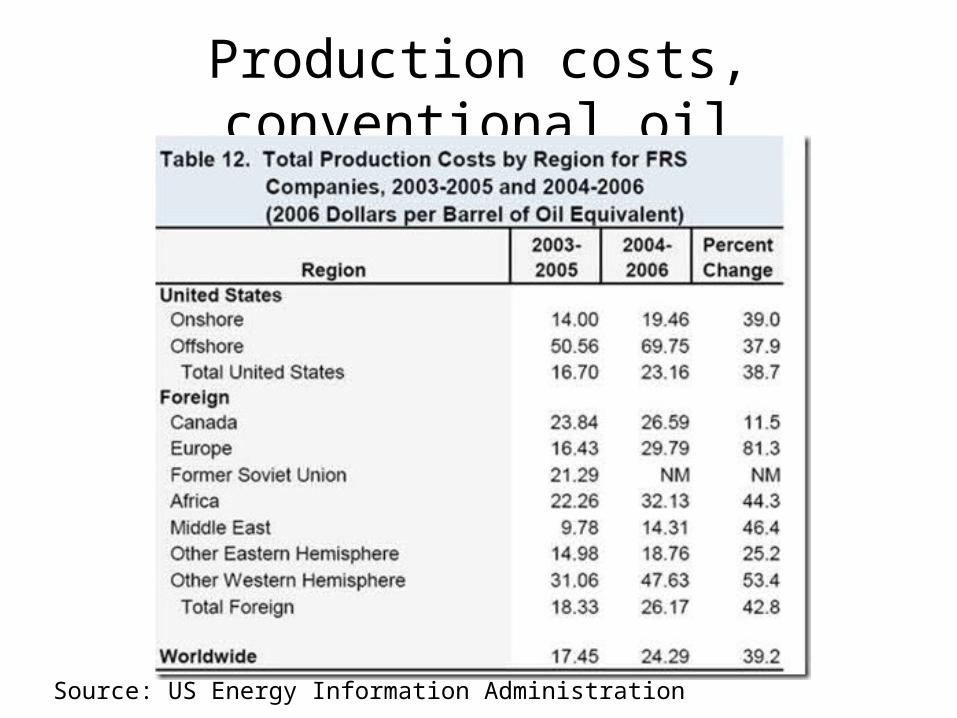

Supply side factors: Production costs

• Production costs rose rapidly after 2000, both reducing incentives to invest and creating expectations about future price increases

• The “peak oil” theory made arguments based on rising costs of production more credible

Production costs, conventional oil

Source: US Energy Information Administration

Supply side factors: Inventories

• The history of inventory changes is ambiguous – total OECD stocks were actually higher than normal in the first half of 2007

• OECD stocks fell in early 2008, particularly in Asia, creating an imbalance

• Official stock build ups took place throughout the period of price increases and rumours of massive increases in Chinese stocks abounded

• Very little information was available about stocks in producing countries

• It is likely that a general atmosphere of uncertainty contributed to precautionary stocking behaviour

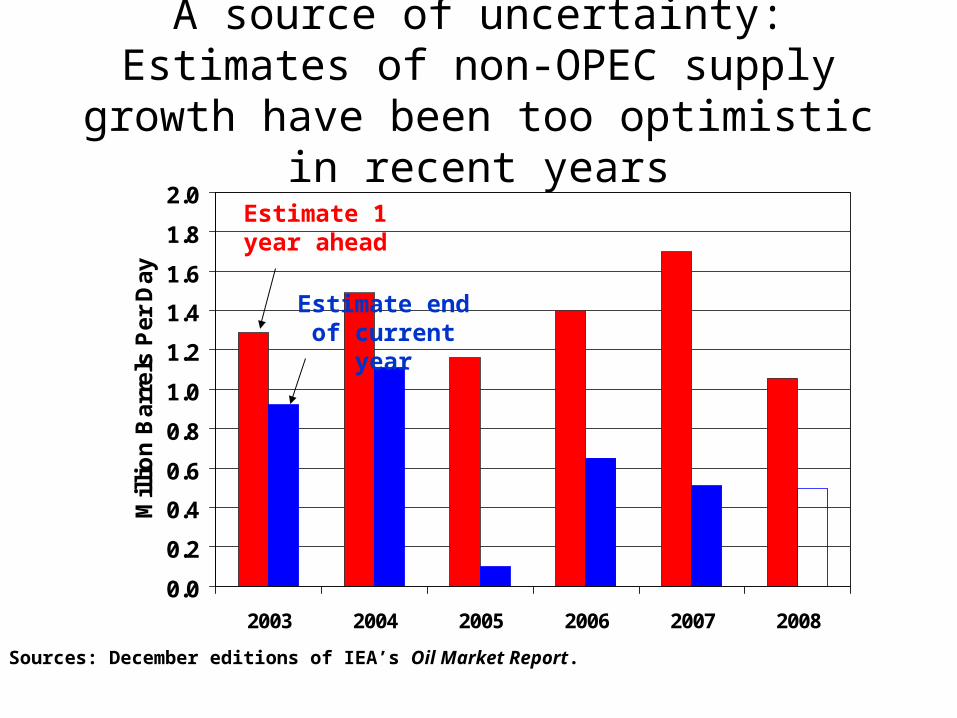

A source of uncertainty: Estimates of non-OPEC supply growth have been too

optimistic in recent years

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2003 2004 2005 2006 2007 2008

Mil

lio

n B

arre

ls P

er D

ay

?

Estimate 1 year ahead

Estimate end of current year

Sources: December editions of IEA’s Oil Market Report.

Summary of factors

0

30

60

90

120

150ja

nv

.94

jan

v.9

5

jan

v.9

6

jan

v.9

7

jan

v.9

8

jan

v.9

9

jan

v.0

0

jan

v.0

1

jan

v.0

2

jan

v.0

3

jan

v.0

4

jan

v.0

5

jan

v.0

6

jan

v.0

7

jan

v.0

8

jan

v.0

9

$200

8 D

oll

ars

Per

Bar

rel/

Day

s S

up

ply

0

2

4

6

8

10

Mil

lio

n B

arre

ls p

er D

ay

WTI Spot ($2008)

OECD Days Supply

World Excess Production Capacity (right axis)

Sources: WTI: Reuters; OECD Days Supply: International Energy Agency and U.S. Energy Information Administration estimates; World Excess Production Capacity: U.S. Energy Information Administration estimates.

Other factors

• US$ depreciation

• Demand rose particularly fast in the transportation sector

• Refineries produce products in fixed proportions, composition of crude oil is crucial

• A shortage of light crude oil may have further fuelled the price increases

Speculation?The argument

• Low returns on stocks and other assets led hedge funds and other investors to invest in commodity markets, particularly oil

• The volume of investment was very large and, it is argued, drove up prices

How do futures markets for commodities work?

• Futures markets trade contracts for future delivery of a certain quantity of a commodity

• The contracts are almost always cashed in and very seldom do buyers actually take delivery in commodities

• The attraction to investors or speculators compared to dealing in the physical commodity is (1) you avoid storage and handing costs and (2) you only have to pay a small part, usually 10 per cent, of the total price in advance; therefore the potential for profits is very large

Who invested in oil futures and what was the effect?

• Banks and others sold “commodity index funds”, that is, financial instruments that were intended to replicate the price movements of commodities

• Oil is usually a large component in the indices, since it is an important commodity in world trade

• Since the sellers of commodity indices wanted to avoid losses, they hedged by buying contracts on commodity exchanges that corresponded to the indices that they sold – thus they would be able to pay off the investors; this activity was responsible for the vast majority of futures market investment

• The sellers rolled over their hedges, that is, they sold the contracts for cash before the due date and bought new ones for more distant dates

• Accordingly, no oil ever changed hands and the price of physical oil was not affected

• The process can be compared to betting on the outcome of a tennis tournament – the bettors do not decide who wins the Wimbledon

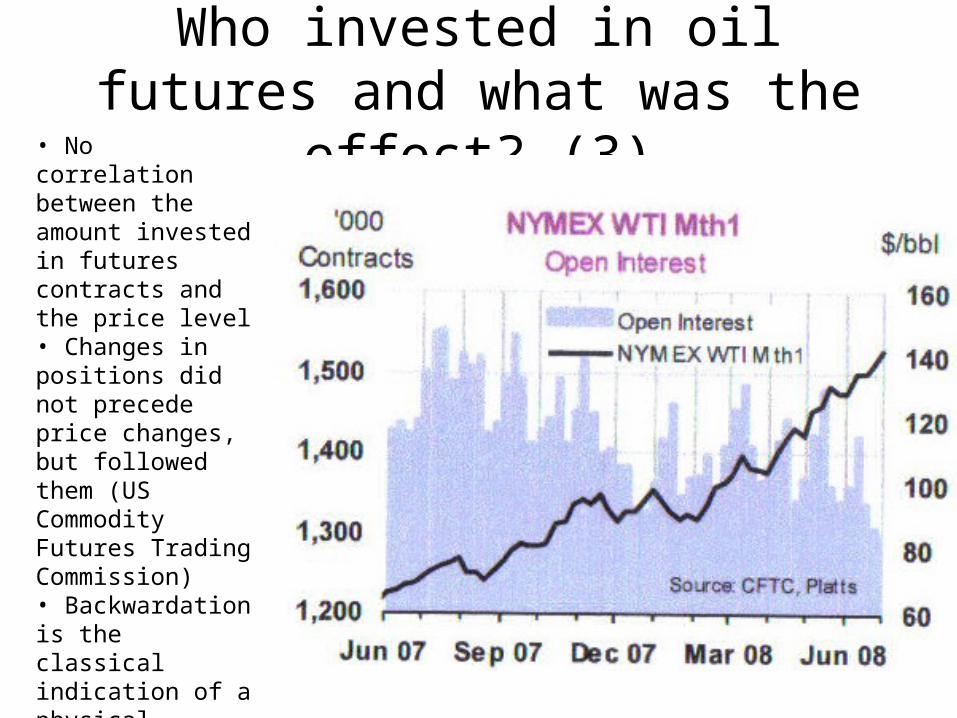

Who invested in oil futures and what was the effect? (3)• No correlation

between the amount invested in futures contracts and the price level• Changes in positions did not precede price changes, but followed them (US Commodity Futures Trading Commission)• Backwardation is the classical indication of a physical shortage, speculators exploit physical shortages

0 50 100 150 200 250 300 350 400 450 500 550 600 650 700 750 800 850 900 950

RhodiumCadmium

ManganeseCobalt

Iron oreRice

Crude petroleumTin

CopperSilverNickelLead

MaizeZinc

Aluminium

A. JUNE 2008 VS. JANUARY 2002(Percentage change)

-100 -90 -80 -70 -60 -50 -40 -30 -20 -10 0 10

Manganese

Iron ore

RiceCobalt

Cadmium

Rhodium

Silver

ZincMaize

Lead

Tin

Aluminium

NickelCopper

Crude petroleum

B. DECEMBER 2008 VS. JUNE 2008(Percentage change)

Exchange-traded commoditiesCommodities either not traded on commodity exchanges or not included in the major commodity indices

Mineral commodities

• Above trend growth in usage

• Under investment in the 1980s and 1990s because of low prices – therefore, capacity became a constraint

• Inventories were gradually depleted

• Price spikes resulted from precautionary buying – all buyers tried to ensure that they would be able to meet their needs

Average annual growth rates of usage of minerals, % per year

0123456789

Alum

inium

Copper

Iron

ore

Lead

Zinc

1996-2001

2002-2007

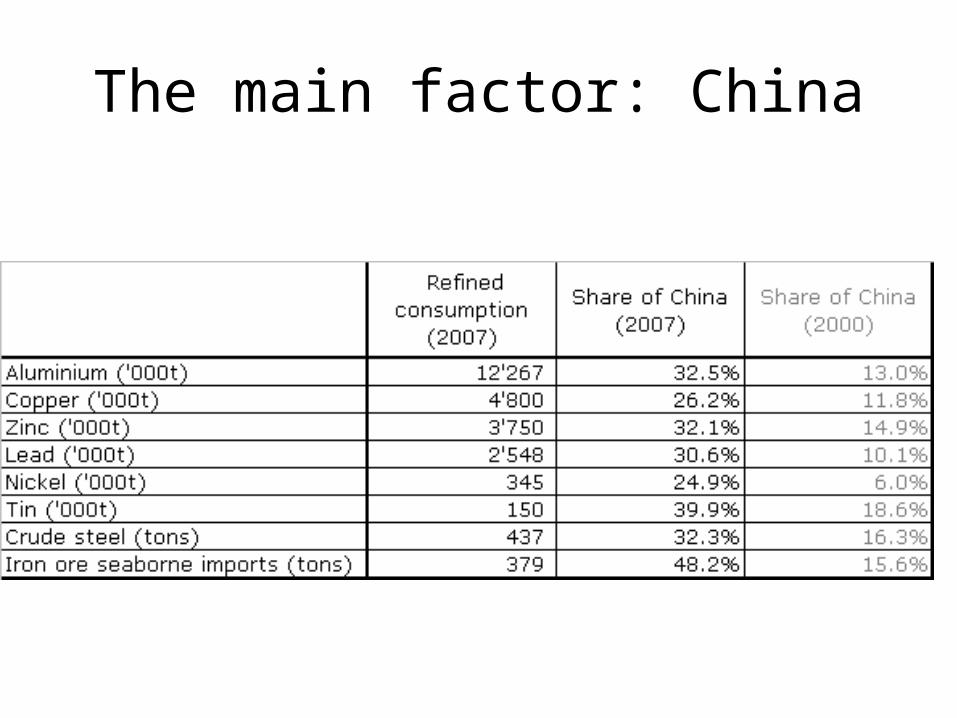

The main factor: China

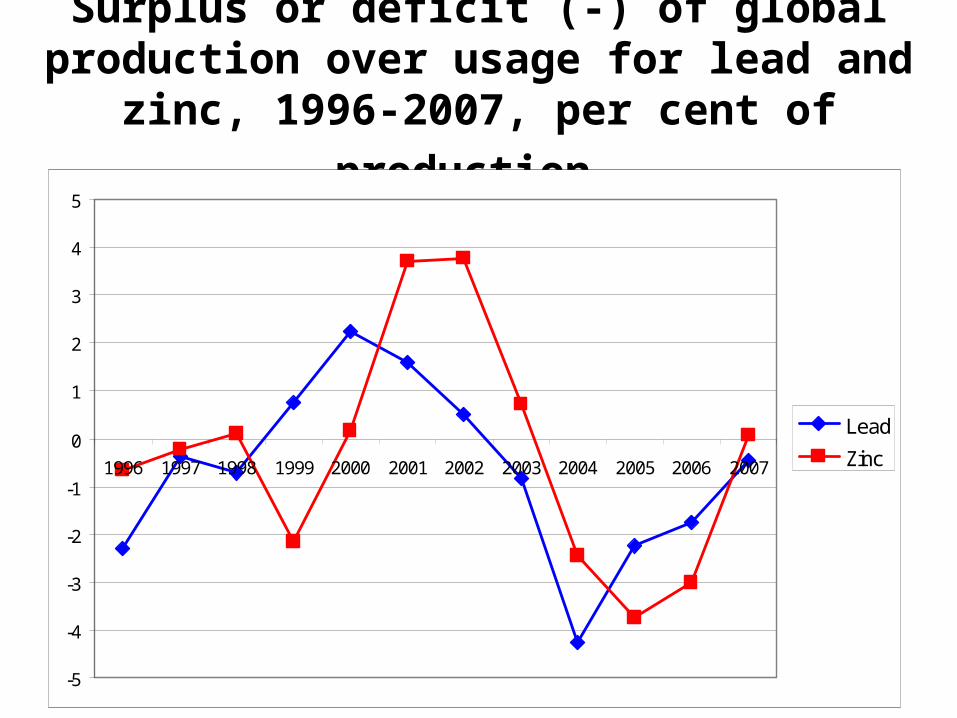

Surplus or deficit (-) of global production over usage for lead and zinc, 1996-2007, per

cent of production

-5

-4

-3

-2

-1

0

1

2

3

4

5

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Lead

Zinc

Average quarterly prices and end of quarter inventories (LME) of lead and zinc, % of 4th

quarter 2003 prices and end 2003 inventories

0

50

100

150

200

250

300

350

400

450

500

4Q200

3

1Q200

4

2Q200

4

3Q200

4

4Q200

4

1Q200

5

2Q200

5

3Q200

5

4Q200

5

1Q200

6

2Q200

6

3Q200

6

4Q200

6

1Q200

7

2Q200

7

3Q200

7

4Q200

7

1Q200

8

2Q200

8

3Q200

8

Lead stocks

Zinc stocks

Lead prices

Zinc prices

Iron ore prices, US$/ton

0

50

100

150

200

25011

.03.

2005

11.0

7.20

05

11.1

1.20

05

11.0

3.20

06

11.0

7.20

06

11.1

1.20

06

11.0

3.20

07

11.0

7.20

07

11.1

1.20

07

11.0

3.20

08

11.0

7.20

08

11.1

1.20

08

Spot price, mid-point ofrange

Hamersley fines, cfrChina

Carajas fines, cfr China

Sources: UNCTAD Iron Ore Trust Fund, TEX Report, Metal Bulletin

Freight rates reflected the overall boomExample: Iron ore freight rates, 1999-2008, US$/ton

0

20

40

60

80

100

120

janv

.99

Jul

janv

.00

Jul

janv

.01

Jul

janv

.02

Jul

janv

.03

Jul

janv

.04

Jul

janv

.05

Jul

janv

.06

Jul

janv

.07

Jul

janv

.08

Jul

Brazil-China

Australia-China

Sources: Drewry, SSY

The downturn

• Did not happen at the same time for all commodities • The recession in the US began in the 4th quarter of 2007

– well before the collapse of Lehman Brothers in September 2008

• It started as a “typical” recession brought on by a commodity price boom– High commodity prices lead to higher general inflation, deterring

investment and constraining production– Tightened monetary policies reinforce the trend, causing an end

to the boom• But it became a financial crisis: “when the tide goes out,

you can see who’s been swimming naked” (Warren Buffett)

• As a result, worst recession since the Great Depression

Characteristics of the recession for commodities

• Widespread downturn led to falls in demand• Note: Mineral commodities are used in

construction, capital equipment and durable household goods, first sectors to be hit in the crisis

• Lack of credit led to:– No trade finance – No working capital finance– No finance for investment

• As a result, world trade was strangled and commodity demand fell precipitously

Monthly world crude steel production, % change year-on-year

-30

-25

-20

-15

-10

-5

0

5

10

Febr

uary

200

8

Mar

chApr

ilM

ayJu

ne July

Augus

t

Septe

mber

Octob

er

Novem

ber

Decem

ber

Janu

ary 2

009

Implications, oil and mineral exporters

• Real exchange rate appreciation during boom

• Undiversified exports and economic structure, low productivity growth

• Subsidized fuel consumption, leading to allocation errors and inefficiencies

• Widening income differences• Eventually, slow growth• But, the scenario takes place against a

background of high incomes

Implications, oil importers

• High energy costs act as a tax on development, reducing real income

• For commodity exporters, effect is offset – at least to some extent - by high prices for export products, and prices of most commodites have fallen less than oil prices

• Exporters of manufactures experience income losses

Terms of trade, developing countries and countries in transition

Source: UNCTAD, Trade and Development Report, 2008

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

2000

2001

2002

2003

2004

2005

2006

2007

Oil exporters

Exporters of minerals andmining products

Exporters of agriculturalproducts

Exporters ofmanufactures

What happens now?

• How long and how much will commodity prices be depressed?

• Short to medium term

• Long term

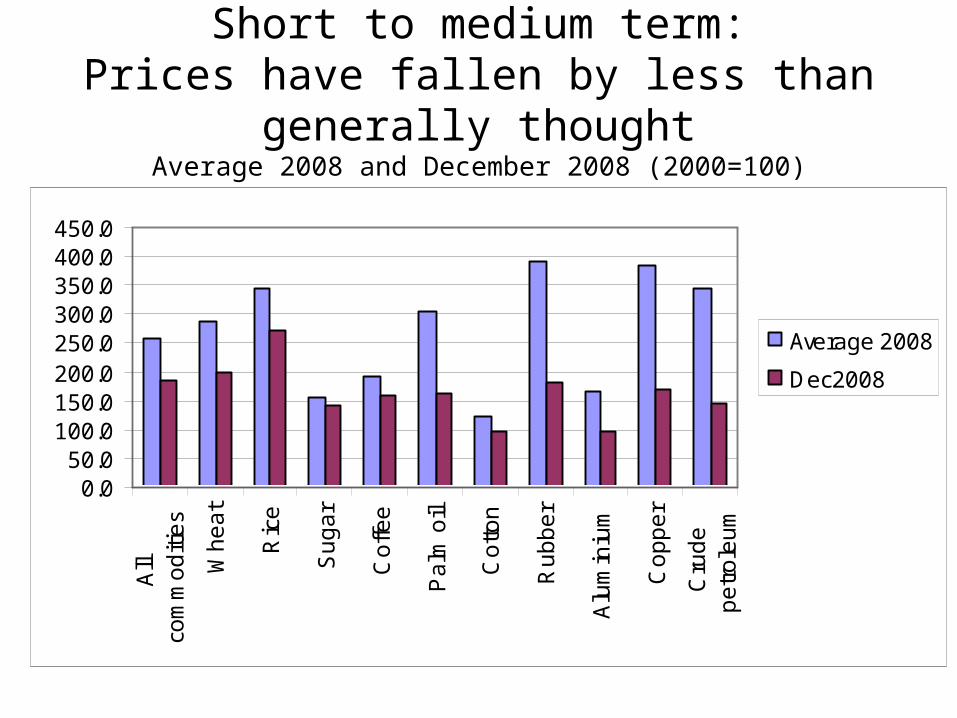

Short to medium term:Prices have fallen by less than generally

thoughtAverage 2008 and December 2008 (2000=100)

0.050.0

100.0150.0200.0250.0300.0350.0400.0450.0

All

com

mo

diti

es

Wh

ea

t

Ric

e

Su

ga

r

Co

ffee

Pa

lm o

il

Co

tton

Ru

bb

er

Alu

min

ium

Co

pp

er

Cru

de

pe

tro

leu

m

Average 2008

Dec2008

Short to medium term, cont’d• Demand for food commodities has held up

relatively well – people have to eat, even in a recession

• Minerals and metals producers have cut production drastically, reducing the impact on prices

• Oil producers (OPEC) have instituted cutbacks, but quota limits are not observed

Short to medium term, cont’d

• The impact on investment has been severe, but has mainly hit projects that are in the midst of the project cycle– Projects that were almost finished are going

ahead but may not enter into production– Long term projects are continuing, but at

lower spending rates

• Prices have probably bottomed out and will start rising slowly towards the end of 2009

The long term1. The new oil economy

• The lesson learned from the oil crisis is that energy diversification is a necessity

• This is reinforced by the need to slow climate change• Accordingly, oil demand will grow more slowly than

otherwise• A “floor” to prices will be set by production costs for

alternatives – US$ 50/barrel?• A ceiling will be set by moderate demand growth – US$

80/barrel?• OPEC discipline will hold up if prices fall too far• Unknown factor: risk for new supply shortages due to

under investment in exploration and development• What is the future for oil economies?

The long term2. Minerals and metals

• Chinese transformation from export orientation to push for domestic demand – effect on minerals demand?

• In spite of this, minerals demand is likely to grow fast in emerging economies because of rising incomes and need to improve infrastructure

• Because of cuts in investment, bottlenecks may emerge quickly and prices could rise to new heights

• Reinforcement of existing pattern of production, Africa may have lost its opportunity…and Russia?

Thank you!