Important disclosures and certifications are contained from page 9 of this report. www.danskeresearch.com Investment Research — General Market Conditions We expect euro-area GDP growth to be above consensus in 2015 despite our view of deflation in 2015. The euro area will, in our view, experience deflation during most of 2015, but it will mainly be due to the low oil price, which boosts private consumption. In addition to stronger growth in private consumption the recovery should also follow as a result of fading headwinds to economic activity. First, exporters will benefit from the depreciation of the effective exchange rate, which should continue to weaken as a result of further easing from the ECB. Secondly, the expansion of the ECB’s balance sheet should improve credit to the private sector as banks’ supply conditions have improved. Related to that lower costs of borrowing also support business investments and private consumption. Finally, the headwind from fiscal tightening continues to fade, while European politicians are likely to support the recovery through an investment project. The market factors in low future growth and inflation and forward rates are consistent with the ECB not lifting its key rates the next five years. The market is in other words pricing in a Japanese scenario as the EUR swap curve is now lower across all tenors compared with Japan in the 1990s. Fading headwinds imply we expect the recovery to strengthen in 2015 Source: ECB, OECD, Danske Bank Markets. Note: All changes are permanent and the impact on GDP is one year after the shock Easing headwind/tailwind Impact on economic activity Rule of thumb Rate cuts Oil price decline Lower inflation, higher real wage growth and thus increasing private consumption 10% oil price decline lifts GDP by 0.08% Effective euro depreciation Improved price competitiveness hence higher exports and lower imports 10% euro depreciation lifts GDP by 0.7% Higher real money supply Can result in more credit to the private sector and thus support investments and private consumption Real money supply growth of 7% y/y cor- responds to GDP growth of 0.5% q/q Improved credit supply conditions Demand for credit gives more bank lending which increases investments and private consumption A credit impulse of 0.2 corresponds to GDP growth of 1.5% y/y Lower cost of borrowing Lower financing costs support investments and private consumption A decline in the Eonia rate of 0.16pp lifts GDP growth by 0.12pp Less fiscal tightening Higher growth in public comsumption Increase in public expenditures of 1% of GDP lifts GDP by 0.8% 12 January 2015 Senior Analyst Pernille Bomholdt Nielsen +45 45 13 20 21 [email protected]Senior Analyst Lars Tranberg Rasmussen +45 45 12 85 34 [email protected]Assistant Analyst Lars Sparresø Merklin [email protected]Research papers 1. Recovery despite deflation 12 January 2. Short-term weakness fades 13 January 3. Deflation but the good kind 14 January 4. ECB will buy government bonds 15 January 5. Impact of broad-based QE 16 January Euro-area outlook for 2015 Recovery despite deflation

Transcript

Important disclosures and certifications are contained from page 9 of this report. www.danskeresearch.com

Investment Research — General Market Conditions

We expect euro-area GDP growth to be above consensus in 2015 despite our

view of deflation in 2015.

The euro area will, in our view, experience deflation during most of 2015, but it

will mainly be due to the low oil price, which boosts private consumption.

In addition to stronger growth in private consumption the recovery should also

follow as a result of fading headwinds to economic activity.

First, exporters will benefit from the depreciation of the effective exchange rate,

which should continue to weaken as a result of further easing from the ECB.

Secondly, the expansion of the ECB’s balance sheet should improve credit to the

private sector as banks’ supply conditions have improved. Related to that lower

costs of borrowing also support business investments and private consumption.

Finally, the headwind from fiscal tightening continues to fade, while European

politicians are likely to support the recovery through an investment project.

The market factors in low future growth and inflation and forward rates are

consistent with the ECB not lifting its key rates the next five years.

The market is in other words pricing in a Japanese scenario as the EUR swap

curve is now lower across all tenors compared with Japan in the 1990s.

Fading headwinds imply we expect the recovery to strengthen in 2015

Source: ECB, OECD, Danske Bank Markets.

Note: All changes are permanent and the impact on GDP is one year after the shock

Easing headwind/tailwind Impact on economic activity Rule of thumb

Rate cuts

Oil price declineLower inflation, higher real wage growth and thus increasing private consumption

10% oil price decline lifts GDP by 0.08%

Effective euro depreciationImproved price competitiveness hence higher exports and lower imports

10% euro depreciation lifts GDP by 0.7%

Higher real money supply

Can result in more credit to the private sector and thus support investments and private consumption

Real money supply growth of 7% y/y cor-responds to GDP growth of 0.5% q/q

Improved credit supply conditions

Demand for credit gives more bank lending which increases investments and private consumption

A credit impulse of 0.2 corresponds to GDP growth of 1.5% y/y

Lower cost of borrowingLower financing costs support investments and private consumption

A decline in the Eonia rate of 0.16pp lifts GDP growth by 0.12pp

Less fiscal tightening Higher growth in public comsumptionIncrease in public expenditures of 1% of GDP lifts GDP by 0.8%

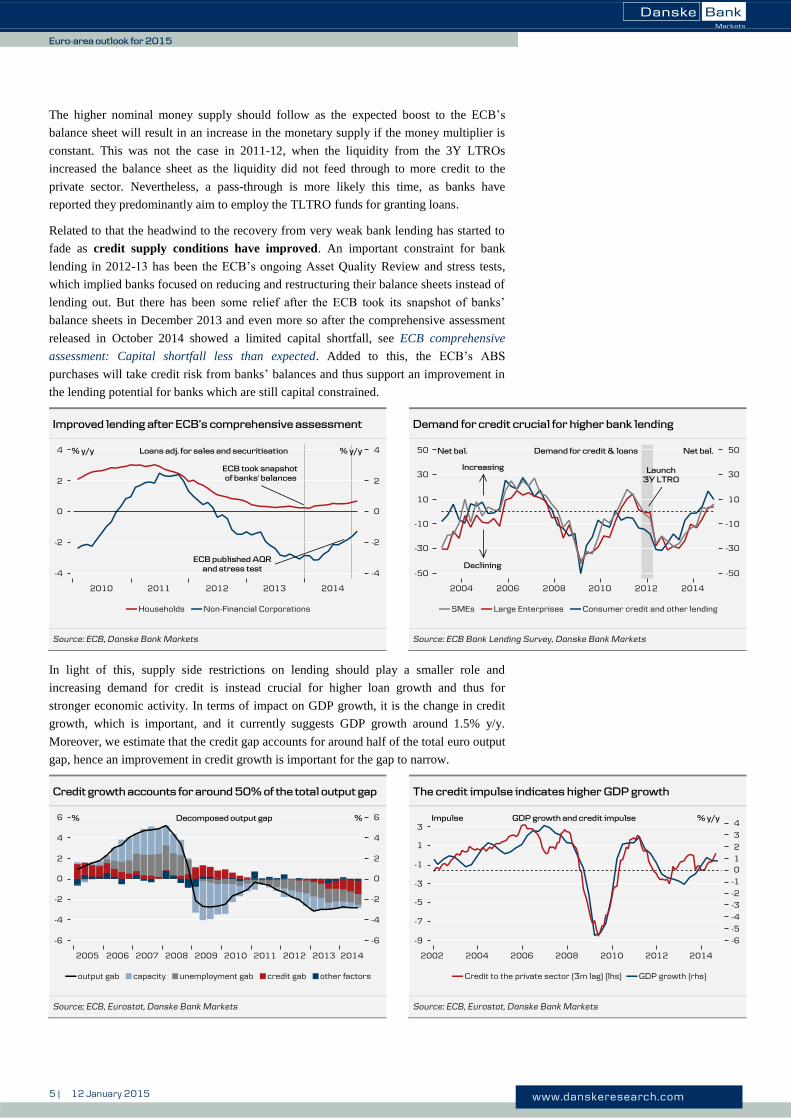

Importantly, more credit to the private sector is coming at a lower cost of borrowing.

The ECB’s Bank Lending Survey shows that banks in 2014 eased price terms on loans to

enterprises for the first time since the financial crisis kicked-in. Similarly the composite

cost of borrowing have declined since the ECB eased in June. In Spain and Italy, the costs

of borrowing to non-financial corporations have also declined, which is also likely to

reflect a transmission of the significant decline in sovereign bond yields. A lowering of

the policy rate, which lower the Eonia rate by 0.16pp is estimated to increase GDP

growth by close to 0.18pp after around two years.

Banks ease price terms for the first time since the crisis Lower cost of borrowing after the ECB eased monetary policy

Source: ECB Bank Lending Survey, Danske Bank Markets Source: ECB, Danske Bank Markets

Fiscal headwind fading

Fiscal policy tightening has also been a significant headwind to economic activity in

previous years, but in 2014 it faded and in 2015, the European Commission estimates that

fiscal policy will be slightly expansionary. Although this could turn out to be a bit too

optimistic, as it only includes measures that have already been approved, the headwind in

2015 should be much smaller compared to the situation in 2011-13.

Added to this, European politicians are likely to strengthen the recovery through a

EUR315bn investment project. The plan is to carry out infrastructure projects without the

use of money from taxpayers, but instead using a small amount of EU funds as a

guarantee to raise new private cash in the capital markets. The investments will start in

mid-2015 and are scheduled to be completed in 2017. According to the European

Commission, the investment plan could potentially add 0.3-0.4% to GDP.

Small fiscal headwind compared to previous years Investments boosted by policy initiatives

Source: Eusopean Commission, IMF, OECD, Danske Bank Markets Source: Eurostat, Danske Bank Markets

-5

-4

-3

-2

-1

0

1

2

2010 2011 2012 2013 2014 2015

Impact on growth Change in cyclically adjusted primary balance

%-points of GDP Fiscal headwind

7 | 12 January 2015 www.danskeresearch.com

Eu

ro-a

rea o

utlo

ok fo

r 20

15

Euro-area outlook for 2015

The market price in a Japanese scenario

European fixed income markets have performed in recent years as growth has been weak

and inflation low and declining. The ECB has pushed down shorter-dated rates through

lowering its key policy rates and adding liquidity to the markets to enhance the growth

outlook. However it has helped little and consequently the long-end rates have fallen,

which reflects that the market factors in lower future growth – i.e. flatter 2/10 and 10/30

slopes in EUR swaps. In fact, as the chart below shows the EUR swap curve is now lower

across all tenors comparing with Japan in the 1990s. Further, it is in line with the current

Japanese curve, which is not really pricing in future rate hikes in any significant way.

Japanese zero coupon yield curve on selected dates EUR swap curve on selected dates

Source: JPN Ministry of Finance (Govies), Danske Bank Markets

Note: We have used government yields in order to have data back to the 90s

Source: Danske Bank Markets

Zooming in on the EUR forward curve, we can derive the following conclusions. Forward

rates are consistent with the ECB not lifting its key rates the next five years. Measured

from the point in time when the first rate hike is priced in, only one rate hike of 25bp per

year is discounted in the following four years. In fact, one could argue that the curve is

not pricing in any rate hikes at all since the upward sloping curve could just be viewed as

a term premium. In other words, the market does not believe that growth and inflation

will return in the next ten years. (In our paper #2, we will look at how the market is likely

to respond once growth returns).

Eonia curve consistent with the ECB on hold next for five years 10Y EUR swap below 1%

Source: Danske Bank Markets Source: Danske Bank Markets

-0.20%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

06

Feb

15

07

Jul1

50

7D

ec1

50

6M

ay1

60

7O

ct1

60

7M

ar1

70

7A

ug1

70

5Ja

n1

80

7Ju

n1

80

7N

ov1

80

5A

pr1

90

6S

ep1

90

7Fe

b2

00

7Ju

l20

07

Dec

20

07

May

21

07

Oct

21

07

Mar

22

05

Au

g22

06

Jan

23

07

Jun

23

07

Nov

23

05

Ap

r24

06

Sep

24

07

Feb

25

07

Jul2

50

5D

ec2

5

1M Eonia forwards

8 | 12 January 2015 www.danskeresearch.com

Eu

ro-a

rea o

utlo

ok fo

r 20

15

Euro-area outlook for 2015

Lessons from Japan: Cost of moderate deflation is not high

Before comparing the euro area to Japan, it is important to remember that from a cyclical point of view Japan has in the past decade done much better than its bad reputation. The recovery in Japan in the wake of the financial crisis has actually been stronger than in the US if it is adjusted for the population growth. Additionally, the unemployment rate in Japan is now back at its level before the financial crisis. Based on this, the lesson from Japan seems to be that the impact on GDP growth of having deflation, which we expect for the euro area during most of 2015, is not that harmful, although the costs are larger compared to having positive inflation. Despite moderate deflation Japan experienced its longest post-war recovery from 2002-07. The private non-residential investment ratio has also been higher than in Germany and the US, underlying that moderate deflation did not weigh substantially on business investments. A cost of deflation is that it is hard to reduce the debt burden, but in Japan this was compensated for by lower real rates. Like in Japan the output gap in the euro area is set to remain very large despite our expectations of a recovery. In isolation, this suggests substantial risk of slipping into broad-based deflation. (We will analyse the inflation outlook in our paper #3). Moreover, the euro area faces some of the same structural challenges that Japan faced in the 1990s and particularly the demographic development will be a challenge going forward. Nonetheless, potential growth in the euro area should not slow as fast as it did in Japan. An important factor behind the weakness in Japan in 1990 was also the banking sector, which was not recapitalised before 1999. In light of this, the capital improvements in the euro area during 2014 and the limited capital shortfall among banks which was revealed in the ECB’s comprehensive assessment should be important for a stronger recovery, as we have also concluded above.

Source: Macrobond, Danske Bank Markets Source: Macrobond, Danske Bank Markets

9 | 12 January 2015 www.danskeresearch.com

Eu

ro-a

rea o

utlo

ok fo

r 20

15

Euro-area outlook for 2015

Disclosure This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske

Bank’). The authors of the research report are Pernille Bomholdt Nielsen, Senior Analyst, Lars Tranberg

Rasmussen, Senior Analyst, and Lars Sparresø Merklin, Assistant Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the

research report accurately reflect the research analyst’s personal view about the financial instruments and issuers

covered by the research report. Each responsible research analyst further certifies that no part of the compensation

of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed

in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject

to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske

Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority

(UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation

Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’

rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-

quality research based on research objectivity and independence. These procedures are documented in Danske

Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any

request that might impair the objectivity and independence of research shall be referred to Research Management

and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do

not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes

investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate

finance or debt capital transactions.

Financial models and/or methodology used in this research report

Calculations and presentations in this research report are based on standard econometric tools and methodology

as well as publicly available statistics for each individual security, issuer and/or country. Documentation can be

obtained from the authors upon request.

Risk warning

Major risks connected with recommendations or opinions in this research report, including as sensitivity analysis

of relevant assumptions, are stated throughout the text.

Date of first publication

See the front page of this research report for the date of first publication.

General disclaimer This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for

informational purposes only. It does not constitute or form part of, and shall under no circumstances be

considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments

(i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or

options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial

Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that

Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not

untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates

and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation

any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and

reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not

10 | 12 January 2015 www.danskeresearch.com

Eu

ro-a

rea o

utlo

ok fo

r 20

15

Euro-area outlook for 2015

undertake to notify any recipient of this research report of any such change nor of any other changes related to the

information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be

reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior

written consent.

Disclaimer related to distribution in the United States This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer

and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S.

Securities and Exchange Commission. The research report is intended for distribution in the United States solely

to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this

research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence

of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are

not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements

of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial

Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-

U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be

registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and

auditing standards of the U.S. Securities and Exchange Commission.