29

1/29 Opportunities in offshore wind for the Norwegian supply chain 8 th Offshore Wind Supply Chain Conference 26 April 2017 Dr Alun Roberts, Associate Director, BVG Associates

1/29

Opportunities in offshore wind for

the Norwegian supply chain

8th Offshore Wind Supply Chain Conference

26 April 2017

Dr Alun Roberts, Associate Director, BVG Associates

2/29

BVG AssociatesA renewable energy consultancy focusing on wind, wave and tidal, and energy systems

Alun Roberts leads projects for BVG Associates in supply

chain and technology analysis and development. He brings

to this a deep knowledge of offshore wind technologies, the

structure of the supply chain, the requirements of the major

players in the sector, and the development of global

markets.

He has used this insight for several developers in recent

years in helping them to develop their supply chain plans

for the UK government , supporting smaller companies

about the opportunities in the sector and analysing the

market of different products and services.

A key area of work for him is helping clients understand the

economic impacts of their investments through

assessments of local content, gross value added (GVA)

and jobs.

Alun Roberts

BVG Associates is a renewable energy consultancy

focusing on wind, wave and tidal, and energy systems.

Company

© BVG Associates 2017

3/29

2. Introduction to marketsAvailable as part of report or printouts to take home

© BVG Associates 2017

4/29

Contents

© BVG Associates 2017

• European offshore wind

market

• Offshore wind value chain

• Procurement strategies

• Overview of opportunities

• Challenges to diversification

• Conclusions

5/29

0

10

20

30

40

50

0

1

2

3

4

5

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25 Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

BE DE DK

FR NL UK

Other Europe Cumulative

Source: BVG Associates CAGR: 11%

1. The marketEurope leads globally

© BVG Associates 2017

• Europe had almost 13GW installed capacity at the end of

2016

• In comparison, rest of world had just under 2GW

• By 2020, anticipated to reach about 25GW

• Main markets after 2020: UK, Germany, Netherlands and

France

6/29

1. The marketUK focus – the largest European market

© BVG Associates 2017

• P50 scenario sees around 1.5GW of new capacity

annually from 2023 to 2025

• 2017 to 2019 has high installation from build out of FIDER

and ROC projects

• Drop in installed capacity in 2020 due to transition

between support mechanisms

• First project under CfD support anticipated to have first

turbine installed in 2019

• Next CfD round in 2017 for projects to be delivered

2021/2022

0

5

10

15

20

0.0

0.5

1.0

1.5

2.0

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

Year of turbine installationUK annual Cumulative

Source: BVG Associates

7/29

1. The marketDE focus – the second largest European market

© BVG Associates 2017

• P50 scenario sees around 600MW of new capacity

annually from 2023 to 2025

• Market regulation seeing significant overhawl with

introduction of Offshore Wind Act “WindSeeG”

• Moving from a FiT to CfD support mechanism

• First competitive auction in 2017 (1.55GW to be installed

from 2020)

0

5

10

15

20

0.0

0.5

1.0

1.5

2.0

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25

Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

Year of turbine installationGermany annual Cumulative

Source: BVG AssociatesSource: BVG Associates

8/29

1. The marketRest of Europe

Denmark France

Belgium Netherlands

© BVG Associates 2017

0

1

2

3

0.0

0.3

0.6

0.9

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25 Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

Annual Cumulative

Source: BVG Associates

0

1

2

3

4

0.00

0.20

0.40

0.60

0.80

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25 Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

Annual Cumulative

Source: BVG Associates

0

2

4

6

8

0.00

0.20

0.40

0.60

0.80

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25 Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

Annual Cumulative

Source: BVG Associates

0

1

2

3

4

0.00

0.20

0.40

0.60

0.80

'16 '17 '18 '19 '20 '21 '22 '23 '24 '25 Cum

ula

tive in

stalle

d c

ap

aci

ty

(GW

)

Insta

lled c

apaci

ty (G

W)

Annual Cumulative

Source: BVG Associates

9/29

1. Opportunities in offshore wind for the Norwegian supply

chainThe findings

© BVG Associates 2017

• BVG Associates has undertaken a study into the opportunities for the Norwegian offshore supply chain in the emerging

offshore wind sector.

• The report covers:

• Introduction to markets

• Procurement strategies

• Overview of opportunities

• Norwegian supply chain assessment, and

• Strategies for market entry.

10/29

2. Offshore wind supply chainThe real opportunities

© BVG Associates 2017

11/29© BVG Associates 2017

3%

28%

19%

12%

35%

4%

Environmental surveys

0.1%

Consenting and development services

0.5%

Site investigations

0.5%

Project management

2.1%

Turbine assembly1.2%

Blades5.1%

Drive train5.2%

Power conversion8.3%

Large fabrications1.3%

Towers3.5%

Small components3.0%

Subsea cables4.8%

Transmission3.2%

Substation structures

2.1%

Turbinefoundations

7.6%

Secondary steelwork1.4%

Installation ports and logistics

0.6%

Turbine and

foundationinstallation

4.9%Cable installation

2.4%Substation installation

0.4%

Installation equipment and

support services3.0%

Onshore works0.6%

Maintenance and inspection services

14.8%

Vessels and equipment16.4%

O&M ports3.8%

Ports and logistics0.2%

Marineoperations

3.3%

Salvage and recycling0.0%

Project management0.1%

Wind turbine supply

Balance of plant

Installation and commissioning

Operation, maintenance

and service

Decommissioning

Source: BVG Associates

Development and project

management

2. Offshore wind supply chain

12/29

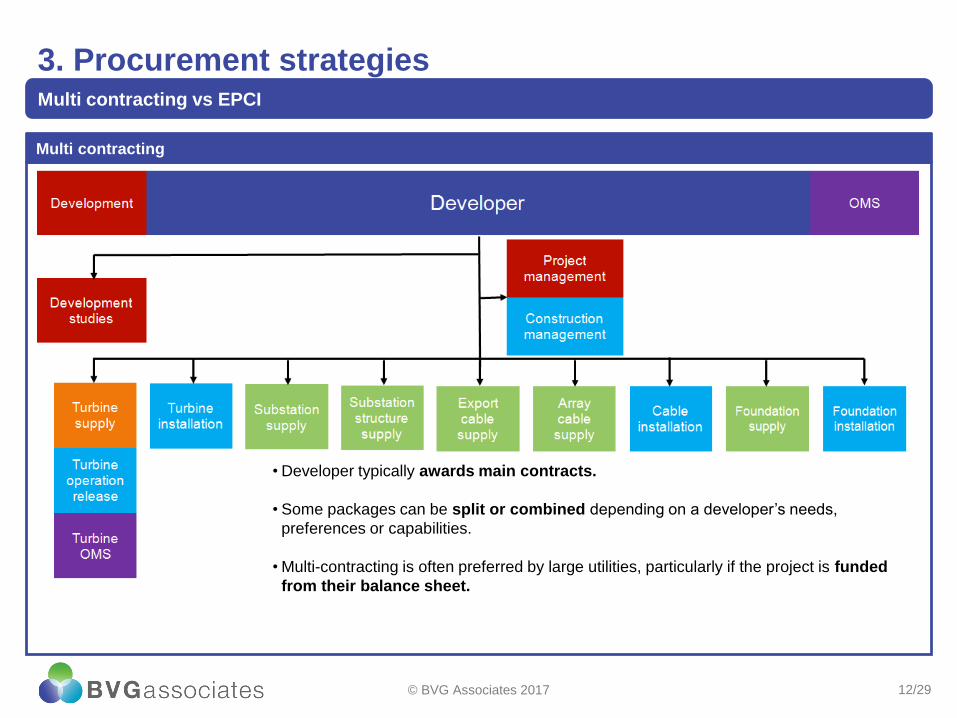

3. Procurement strategiesMulti contracting vs EPCI

Multi contracting

© BVG Associates 2017

• Developer typically awards main contracts.

• Some packages can be split or combined depending on a developer’s needs,

preferences or capabilities.

• Multi-contracting is often preferred by large utilities, particularly if the project is funded

from their balance sheet.

13/29

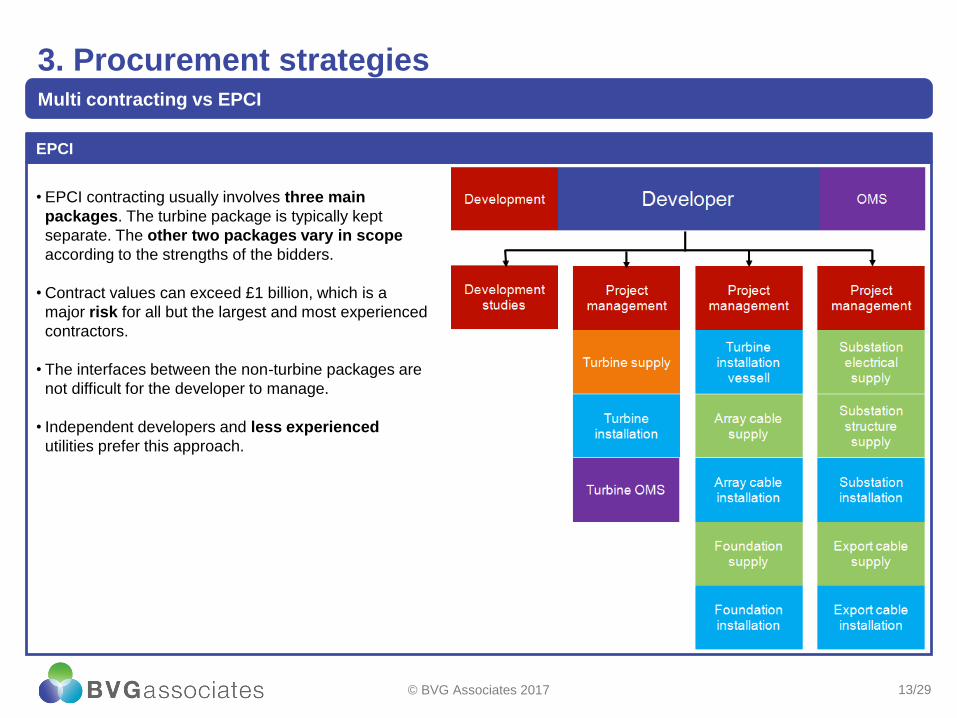

3. Procurement strategiesMulti contracting vs EPCI

EPCI

© BVG Associates 2017

• EPCI contracting usually involves three main

packages. The turbine package is typically kept

separate. The other two packages vary in scope

according to the strengths of the bidders.

• Contract values can exceed £1 billion, which is a

major risk for all but the largest and most experienced

contractors.

• The interfaces between the non-turbine packages are

not difficult for the developer to manage.

• Independent developers and less experienced

utilities prefer this approach.

14/29© BVG Associates 2017

4. Overview of the Norwegian supply chain

• The offshore wind supply chain has been split into 29 sub elements under six headline categories

• These sub elements were assessed using the following criteria:

• Track record in offshore wind

• Synergies with parallel sectors

• Appetite from offshore wind

• Potential for levelised cost of energy (LCOE) benefit from new involvement by Norwegian suppliers

• Size and timing of investments

• Size of the opportunity

• Reviewed company data held by NORWEP and BVG Associates and considered:

• Relevant areas of company expertise

• Experience of offshore wind

• Green-light opportunities have been identified as those areas of the offshore wind supply chain that present Norwegian

suppliers with the greatest opportunity to support.

• Areas of supply denoted as amber or red are still an opportunity for supply, the assessment simply considers where the

logical argument exists for the best chance of diversification success.

15/29

4.1 Development and project managementOverview

• Makes up 3% of lifetime expenditure

• Contractors carry out geotechnical and geophysical

studies, wildlife studies, human impact studies and

cable route assessments during site selection

• A number of specialists needed across all stages of

development

• Developers may subcontract project management and

coordination of tasks

© BVG Associates 2017

Sub element Lifetime spend* Norwegian

suppliers

Environmental

surveys

0.1% 55 kr

million

Consenting and

development

services

0.5% 264 kr

million

Site investigations 0.5% 264 kr

million

Project management 2.1% 1,156 kr

million

* For a 1GW offshore wind farm

Environmental surveys

3%

Consenting and development

services15%

Site investigations

15%

Project management

67%

Development and project

management3%

16/29

4.1 Development and project managementOverview

© BVG Associates 2017

Sub-element Track record Synergies

with other

sectors

Appetite from

offshore wind

Potential for

LCOE benefit

Size and

timing of

investments

Size of the

opportunity

Opportunity

for Norwegian

companies

Environmental

surveys1 2 1 1 3 1

Consenting and

development

services

1 2 1 1 3 1

Site

investigations2 2 2 1 2 1

Project

management2 3 2 2 3 2

17/29

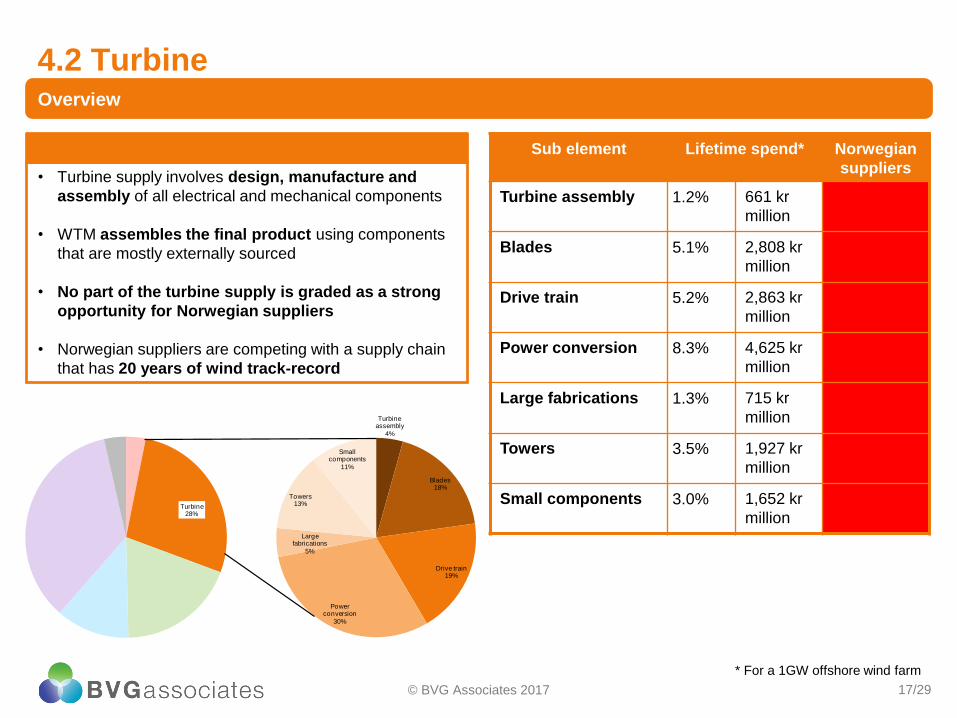

4.2 TurbineOverview

• Turbine supply involves design, manufacture and

assembly of all electrical and mechanical components

• WTM assembles the final product using components

that are mostly externally sourced

• No part of the turbine supply is graded as a strong

opportunity for Norwegian suppliers

• Norwegian suppliers are competing with a supply chain

that has 20 years of wind track-record

© BVG Associates 2017

Sub element Lifetime spend* Norwegian

suppliers

Turbine assembly 1.2% 661 kr

million

Blades 5.1% 2,808 kr

million

Drive train 5.2% 2,863 kr

million

Power conversion 8.3% 4,625 kr

million

Large fabrications 1.3% 715 kr

million

Towers 3.5% 1,927 kr

million

Small components 3.0% 1,652 kr

million

* For a 1GW offshore wind farm

Turbine assembly

4%

Blades18%

Drive train19%

Power conversion

30%

Large fabrications

5%

Towers13%

Small components

11%

Turbine28%

18/29

4.2 TurbineOverview

© BVG Associates 2017

Sub-element Track record Synergies

with other

sectors

Appetite from

offshore wind

Potential for

LCOE benefit

Size and

timing of

investments

Size of the

opportunity

Opportunity

for Norwegian

companies

Turbine assembly 1 2 2 1 2 2

Blades 1 1 1 1 1 3

Drive train 1 1 1 1 1 3

Power

conversion1 1 1 1 2 3

Large

fabrications1 2 1 1 2 2

Towers 1 2 1 1 2 3

Small

components1 2 1 1 2 2

19/29

4.3 Balance of plantOverview

• Balance of plant is expected to deliver significant

LCOE improvement

• Oil and gas suppliers have a strong track-record in this

area

• Array cables, substation structures, turbine

foundations and secondary steelwork all show good

opportunities

© BVG Associates 2017

Sub element Lifetime spend* Norwegian

suppliers

Subsea cables 4.8% 2,643 kr

million

Transmission 3.2% 1,762 kr

million

Substation

structures

2.1% 1,156 kr

million

Turbine foundations 7.6% 4,185 kr

million

Secondary

steelwork

1.4% 771 kr

million

* For a 1GW offshore wind farm

Subsea cables25%

Transmission17%

Substations structures

11%

Turbine foundations

40%

Secondary steelwork

7%

Balance of plant

19%

20/29

4.3 Balance of plantOverview

© BVG Associates 2017

Sub-element Track record Synergies

with other

sectors

Appetite from

offshore wind

Potential for

LCOE benefit

Size and

timing of

investments

Size of the

opportunity

Opportunity

for Norwegian

companies

Subsea cables 3 3 3 2 2 2

Transmission 1 2 2 2 2 3

Substation

structures2 3 2 2 2 3

Turbine

foundations2 3 3 3 2 3

Secondary

steelwork2 2 2 2 3 2

21/29

4.4 Installation and commissioningOverview

• Few oil and gas companies have a track-record in

turbine and foundation installation although contractors

draw on experience in oil and gas.

• Vessels used are now bespoke and often high-

specification jack-up vessels built in the Gulf states or

east Asia

• Main opportunities lie in installation equipment and

support services, to engineer efficient offshore

solutions for a range of installation activities

© BVG Associates 2017

Sub element Lifetime spend* Norwegian

suppliers

Installation ports

and logistics

0.6% 330 kr

million

Turbine and

foundation

installation

4.9% 2,698 kr

million

Cable installation 2.4% 1,322 kr

million

Substation

installation

0.4% 220 kr

million

Installation

equipment and

support services

3.0% 1,652 kr

million

Onshore works 0.6% 330 kr

million

* For a 1GW offshore wind farm

Installation ports and logistics

5%

Turbine and foundation

installation41%

Cable installation

20%

Substation installation

4%

Installation equipment and

support services25%

Onshore works

5%

Installation and commissioning

12%

22/29

4.4 Installation and commissioningOverview

© BVG Associates 2017

Sub-element Track record Synergies

with other

sectors

Appetite from

offshore wind

Potential for

LCOE benefit

Size and

timing of

investments

Size of the

opportunity

Opportunity

for Norwegian

companies

Installation ports

and logistics1 2 2 1 2 1

Turbine and

foundation

installation

2 2 2 2 2 2

Cable installation 2 3 2 2 3 2

Substation

installation1 3 2 1 3 2

Installation

equipment and

support services

2 3 3 3 3 2

Onshore works 1 1 1 1 3 1

23/29

4.5 Operation, maintenance and serviceOverview

• Maintenance and inspection services present a good

opportunity for Norwegian suppliers seeking to

diversify

• Opportunities for the supply of vessels and equipment

from Norway will increase as the market moves towards

SOVs which include walk to work solutions.

• There is little benefit of combining offshore wind port

requirements within existing oil and gas service hubs.

© BVG Associates 2017

Sub element Lifetime spend* Norwegian

suppliers

Maintenance and

inspection services

14.8% 8,192 kr

million

Vessels and

equipment

16.4% 9,091 kr

million

O&M ports 3.8% 2,109 kr

million

* For a 1GW offshore wind farm

Maintenance and inspection

services42%

Vessels and equipment

47%

O&M ports11%

Operation, mantenance

and service35%

24/29

4.5 Operation, maintenance and serviceOverview

© BVG Associates 2017

Sub-element Track record Synergies

with other

sectors

Appetite from

offshore wind

Potential for

LCOE benefit

Size and

timing of

investments

Size of the

opportunity

Opportunity

for Norwegian

companies

Maintenance and

inspection

services

2 3 3 3 3 3

Vessels and

equipment2 3 3 3 3 2

O&M ports 1 3 2 1 2 1

25/29

4.6 DecommissioningOverview

• Only one small offshore wind farm has been

decommissioned.

• One of the key challenges is in the large number of

assets spread over a wide area

• Given the current deployment profile and lifetime of the

installations there will not be significant activity before

2030.

• Norway is likely to be in a strong position to support the

marine operations sub-element.

© BVG Associates 2017

Sub element Lifetime spend* Norwegian

suppliers

Ports and logistics 0.2% 88 kr

million

Marine operations 3.3% 1,817 kr

million

Salvage and recycling 0.0% 22 kr

million

Project management 0.1% 33 kr

million

* For a 1GW offshore wind farm

Ports and logistics

4%

Marine operations

93%

Salvage and recycling

1%

Project management

2%Decommissioning 4%

26/29

4.6 DecommissioningOverview

© BVG Associates 2017

* For a 1GW offshore wind farm

Sub-element Track record Synergies

with other

sectors

Appetite from

offshore wind

Potential for

LCOE benefit

Size and

timing of

investments

Size of the

opportunity

Opportunity

for Norwegian

companies

Ports and

logistics1 3 2 1 3 1

Marine

operations1 3 2 1 3 1

Salvage and

recycling1 3 3 1 3 1

Project

management1 3 2 1 3 1

27/29

5. Challenges to diversificationUnderstand core competence, address supply gaps in offshore wind seeking highest LCOE savings

© BVG Associates 2017

Lack of

track

record

Risk-

adverse

investors

Cost

competitive

ness

Contracts

(lump sum

vs fixed

price)

Warranties

and asset

uptime

linked

reward

Target

multiple

projects

Long-term

OPEX

focus high

local

contentFloating wind

high O&G

structure

synergy

Disruptive

innovation /

cost

competitive

Understand

differences

with clear

strategy

28/29

6. Conclusions

• Diversification can be a great business strategy - a

targeted move into a new sector can spread risk, generate

new revenue and reduce unit costs.

• Key to successful diversification - ensure there is

capability overlap between “legacy” and “new “ industry.

• The oil & gas overlap - offshore wind open to suppliers

from all sectors but capability correlation between offshore

wind and oil and gas is naturally very high.

• Two-way learning - processes and innovative thinking

developed over decades in other sectors can be

transferred to offshore wind. Rapid cost reduction,

standardisation and faster deployment techniques in

offshore wind can benefit oil and gas as well as other

sectors

© BVG Associates 2017

29/29

Thank you….

Please get in touch

BVG Associates Ltd

The Blackthorn Centre

Purton Road

Cricklade, Swindon

SN6 6HY UK

tel +44 (0) 1793 752 308

@bvgassociates

www.bvgassociates.com

This presentation and its content is copyright of BVG Associates Limited

© BVG Associates 2017

Tel: +44 1793 799 022

Mob: +44 7595 400262

Coming soon….

BVG Associates report on

offshore wind opportunities

for Norwegian supply chain..