27

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 1

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 1

The Greek LettersThe Greek LettersCh t 17Chapter 17

2

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008

ExampleExampleExampleExample

A b k h ld f $300 000 EA bank has sold for $300,000 a European call option on 100,000 shares of a non-dividend paying stockp y gS0 = 49, K = 50, r = 5%, σ = 20%,

T = 20 weeks, μ = 13%The Black-Scholes value of the option is $240,000H d th b k h d it i k t l kHow does the bank hedge its risk to lock in a $60,000 profit?

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 3

Naked & Covered PositionsNaked & Covered PositionsNaked & Covered PositionsNaked & Covered Positions

Naked positionNaked positionTake no action

Covered positionCovered positionBuy 100,000 shares today

Both strategies leave the bank exposed to significant riskto significant risk

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 4

StopStop--Loss StrategyLoss StrategyStopStop Loss StrategyLoss Strategy

This involves:Buying 100,000 shares as soon as price reaches $50price reaches $50Selling 100,000 shares as soon as price falls below $50p $This deceptively simple hedging strategy does not work well

B / ll t 50 δ th b hi h ll l !!Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 5

Buy/sell at 50±δ, thus buy high, sell low!!

Delta Delta (See Figure (See Figure 17.217.2, page , page 361)361)

Delta (Δ) is the rate of change of the option price with respect to the underlying

OptionOptionprice

Slope = Δ

A

BSlope Δ

Stock priceOptions, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 6

A Stock price

Delta HedgingDelta Hedging

This involves maintaining a delta neutralThis involves maintaining a delta neutral portfolioThe delta of a European call on a non-The delta of a European call on a nondividend paying stock is N (d 1)The delta of a European put on the stockThe delta of a European put on the stock is

N (d 1) – 1( 1)Example: if S0=$100 c=$10 and Δ=0.6, and investor is short 20 contracts (100 shares/contract), she could buy 0.6×2000=1200 shares Then gain(loss) in options is offset by loss(gain) of the

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 7

shares. Then gain(loss) in options is offset by loss(gain) of the stocks.

Delta HedgingDelta Hedgingi di dcontinuedcontinued

The hedge position must be frequently rebalanced Delta changes quickly with S !!rebalancedDelta hedging a written option involves a “buy high, sell low” trading rule

D g qu y w

y g , gSee Tables 17.2 (page 364) and 17.3 (page 365) for examples of delta hedging

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 8

Options, Futures, and Other Derivatives, 4th edition ©

1999 by John C. Hull 13.9

ThetaThetaThetaThetaTheta (Θ) of a derivative (or portfolio ofTheta (Θ) of a derivative (or portfolio of derivatives) is the rate of change of the value with respect to the passage of timeThe theta of a call or put is usually negative. This means that, if time passes with the price of the underlying asset and its volatilityof the underlying asset and its volatility remaining the same, the value of a long option declinesS f fSee Figure 17.5 for the variation of Θ with respect to the stock price for a European call

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 10

Options, Futures, and Other Derivatives, 4th edition ©

1999 by John C. Hull 13.11

GammaGammaGammaGammaGamma (Γ) is the rate of change of delta (Δ) with respect to the price of the underlying assetG fGamma is greatest for options that are close to the money (see Figure 17.9, page 372)372)

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 12

Gamma Addresses Delta Hedging Gamma Addresses Delta Hedging Errors Caused By Curvature Errors Caused By Curvature (Figure (Figure 17.717.7, page , page 369)369)

Callpriceprice

C''

C

CC'

S

CStock price

S'

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 13

S S

Interpretation of GammaInterpretation of GammaFor a delta neutral portfolio,

ΔΠ ≈ Θ Δt + ½ΓΔS 2

ΔΠΔΠ

ΔSΔS

Negative GammaPositive Gamma

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 14

Options, Futures, and Other Derivatives, 4th edition ©

1999 by John C. Hull 13.15

Relationship Between Delta, Relationship Between Delta, G dG d ThThGamma, and Gamma, and Theta Theta (page 373)(page 373)

For a portfolio of derivatives on a pstock paying a continuous dividend yield at rate qy q

Π=Γ+Δ−+Θ rSSqr 22

21)( σ2

ƒƒ ½ƒƒ2

222 r

SS

SrS

t=++

∂∂σ

∂∂

∂∂

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 16

2SSt ∂∂∂

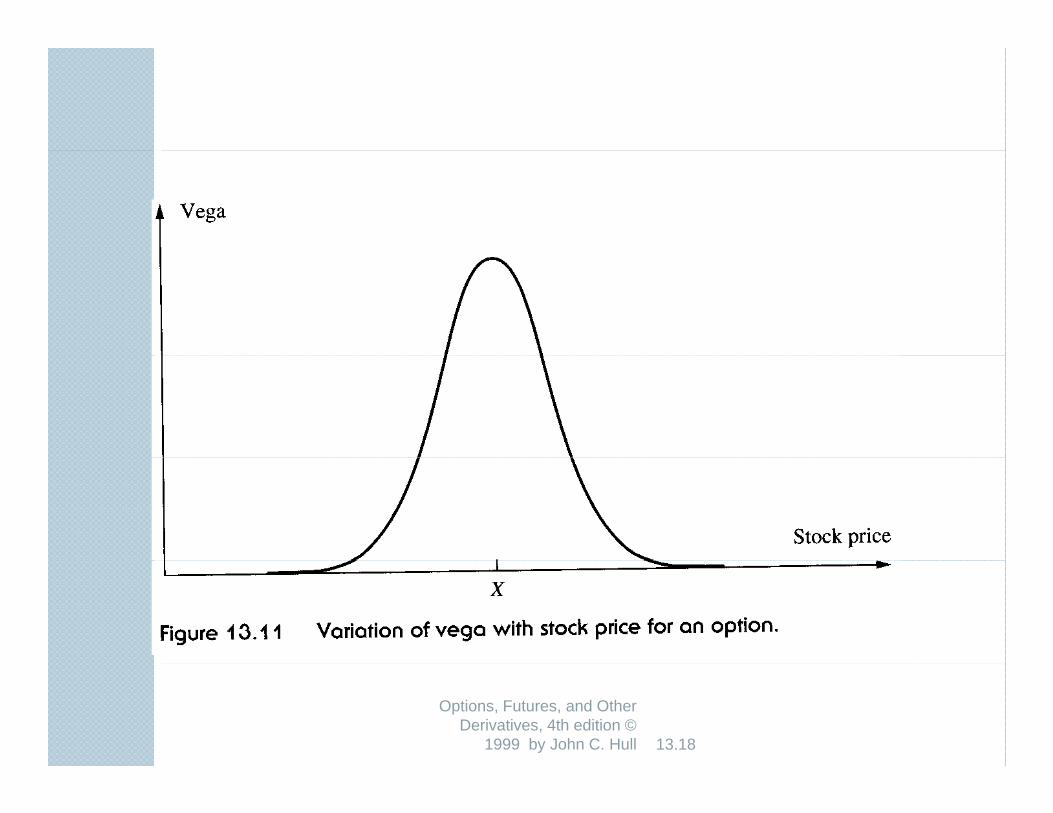

VegaVegaVegaVega

Vega (ν) is the rate of change of the value of a derivatives portfolio with respect to volatilityrespect to volatilityVega tends to be greatest for options that are close to the money (See Figureare close to the money (See Figure 17.11, page 374)

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 17

Options, Futures, and Other Derivatives, 4th edition ©

1999 by John C. Hull 13.18

Managing Delta, Gamma, & Managing Delta, Gamma, & VVVegaVega

• Δ can be changed by taking a position in the underlyingy gTo adjust Γ & ν it is necessary to take a position in an option or other derivative

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 19

RhoRhoRhoRho

Rho is the rate of change of the valueRho is the rate of change of the value of a derivative with respect to the interest rateinterest rate

For currency options there are 2 rhosy p

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 20

Hedging in PracticeHedging in PracticeHedging in PracticeHedging in PracticeTraders usually ensure that their portfolios are delta-neutral at least once a dayWhenever the opportunity arises, they improve gamma and vegaAs portfolio becomes larger hedging b l ibecomes less expensive

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 21

Scenario AnalysisScenario AnalysisScenario AnalysisScenario AnalysisA scenario analysis involves testing the effect on the value of a portfolio of different assumptions concerning asset prices and their volatilitiestheir volatilities

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 22

Futures Contract Can Be Used Futures Contract Can Be Used f H d if H d ifor Hedgingfor Hedging

The delta of a futures contract on an asset paying a yield at rate q is e(r-q)T times the

fdelta of a spot contractThe position required in futures for delta h d i i th f (r q)T ti thhedging is therefore e-(r-q)T times the position required in the corresponding spot contractcontract

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 23

Hedging vs Creation of an Hedging vs Creation of an O i S h i llO i S h i llOption SyntheticallyOption Synthetically

When we are hedging we take positions that offset Δ, Γ, ν, etc.When we create an option synthetically we take positions that match Δ, Γ, & ν

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 24

Portfolio InsurancePortfolio Insurance

In October of 1987 many portfolioIn October of 1987 many portfolio managers attempted to create a put option on a portfolio syntheticallyp y yThis involves initially selling enough of the portfolio (or of index futures) to match the p ( )Δ of the put option

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 25

Portfolio InsurancePortfolio Insurancei di dcontinuedcontinued

As the value of the portfolio increases, the Δof the put becomes less negative and some

f fof the original portfolio is repurchasedAs the value of the portfolio decreases, the Δ f th t b ti dΔ of the put becomes more negative and more of the portfolio must be sold

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 26

Portfolio InsurancePortfolio Insurancei di dcontinuedcontinued

The strategy did not work well on October 19 19819, 1987...

Options, Futures, and Other Derivatives, 7th Edition, Copyright © John C. Hull 2008 27