17

ORIGINAL RESEARCH FOR INQUISITIVE INVESTORS BRANDES.COM/INSTITUTE [email protected] Organizational Design and Long-Term Investing by David Iverson and Geoff Warren

ORIGINAL RESEARCH FOR INQUISITIVE INVESTORS

BRANDES.COM/INSTITUTE [email protected]

Organizational Design and Long-Term Investingby David Iverson and Geoff Warren

PAGE 2

Overview

A previous Brandes Institute paper considered what it means to be a long-term investor (Warren, 2016). It was argued that long-term investors are best characterized by their latitude and their intent to pursue long-term goals. Important for latitude is a capacity for patience, supported by discretion to decide when to buy, when to sell or if to continue holding where necessary. Intent reveals itself in both the objectives pursued, and how investment decisions are made. It was also suggested that long-term investing might be seen as a matter of attitude and perspective—even a mindset. In sum, long-term investors have the capacity to look through the short-term noise and pressures to deliver immediate performance, and retain a focus on the long term.

Given that investing is often undertaken by institutional investors on behalf of their end-investors or “beneficiaries,” the following question arises:

What are the characteristics or attributes that are required to enable an investment organization to successfully pursue long-term investment opportunities?

We respond to this question in this paper. We identify and discuss four “success drivers” for long-term investing: (A) investment beliefs, (B) governance, (C) aligned interests and (D) people. These drivers might be seen as overlapping and self-reinforcing areas to consider when addressing whether an organization has positioned itself to be a successful long-term investor. We discuss them in the context of multilayered investment organizations, where investment decisions are often handed down along a

“chain of delegations.” The litmus test of whether the organization is configured properly is that those ultimately responsible for making investment decisions feel they are given the latitude to pursue long-term opportunities, and are operating with the full intent to doing so. After having discussed the nature of the four success drivers, we then use them to assess how well various types of long-term institutional investors are set up for successful long-term investing.

We believe investment organizations that can effectively address the four drivers will greatly improve the chances of delivering success over the long term for their beneficiaries. Genuine long-term investors are able to pursue a wider range of investment strategies, including some that are challenging for investors with shorter horizons. Important examples are the ability to take contrarian positions in mispriced markets and providing liquidity when it is in short supply, even though the timing of the payoff may be quite uncertain. Addressing the four drivers should also lead to improved capacity for coherent decision-making. Long-term investors who stay focused on the destination are less likely to be seduced into counterproductive actions along the path, such as getting caught up in the euphoria of overheated markets, responding to information that is irrelevant for long-term fundamentals, and trading out at the wrong time in response to pressure to limit the pain of losses. Addressing the four drivers outlined below thus not only should help an organization deliver over the long run but also make it a more effective investor in general.

We believe investment organizations that can effectively address the four drivers will greatly improve the chances of delivering success over the long term for their beneficiaries.

PAGE 3

What Do We Mean by Organizational Design?

Organizational design relates to the structures and procedures under which an organization operates. For the purpose of this paper, our focus is the link between organizational design and investment decisions. Various authors have contributed to thought on this topic. For example, Ambachtsheer and Ezra (1998) address pension fund design. Ambachtsheer (2017) provides further discussion centered around cost-effectiveness, i.e., whether an investment organization is delivering value for the risk it takes, and whether value for money being achieved. The authors of this paper have also had their own say on the matter. Iverson (2013) discusses this as a strategic risk management issue. Warren (2014b) specifically addresses organizational design from the perspective of capacity to pursue long-term investment opportunities. He discusses four “building blocks” of broader scope than covered here, including: organizational features; incentives; investment approach; and extent to which there exists discretion over trading. Ideas from all these authors and others make their way into this paper.

It is important to establish up front that there is no “right” approach to designing an organization for long-term investing. The appropriate approach will differ by organization, depending on the context under which it operates. Purpose, objectives, investment beliefs, resourcing, legislation, environmental settings—and, most importantly, the nature of its beneficiaries and funding—can all play a role. Our four drivers represent broad aspects that cut across organizations of all types, although how they are applied depends on the circumstances. The drivers center on influences over how various players within an organization behave and act, for which we make no excuse. Investment organizations are composed of people—and people make investment decisions. In our opinion, the trick is to get those involved to make those decisions with a focus on the long term.

PAGE 4

Investment beliefs should be framed around how long-term investing can provide access to good opportunities that the organization is well positioned to capture.

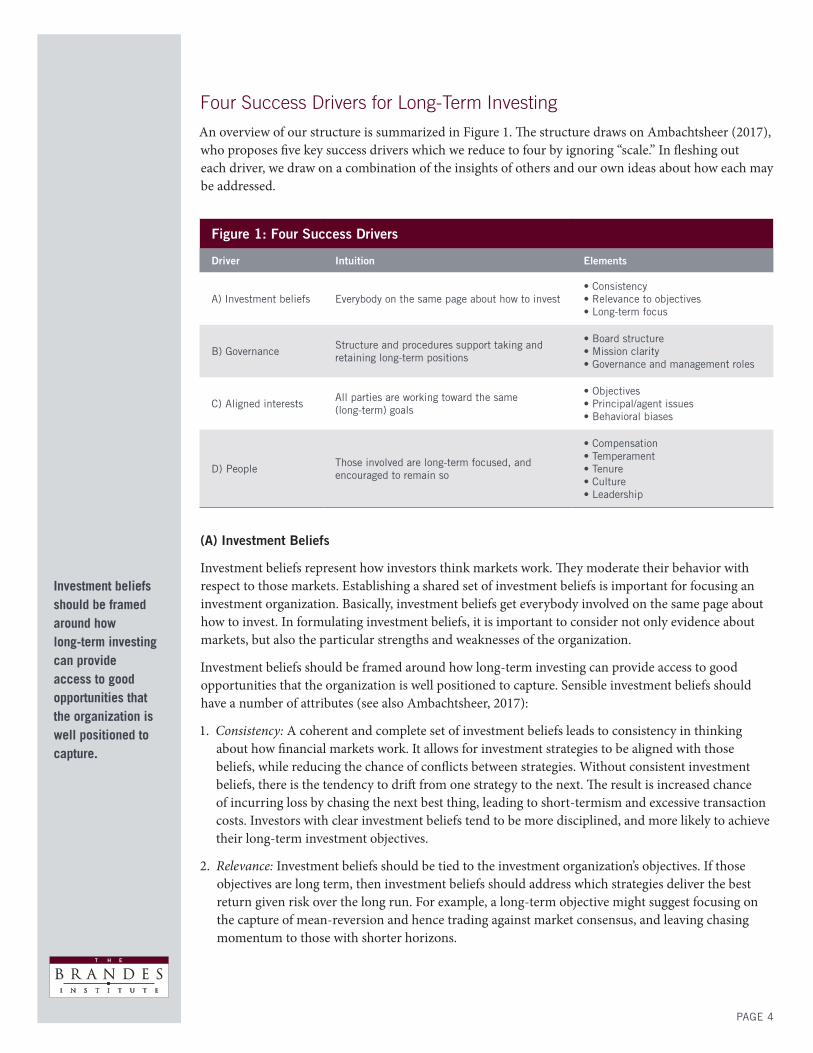

Four Success Drivers for Long-Term Investing

An overview of our structure is summarized in Figure 1. The structure draws on Ambachtsheer (2017), who proposes five key success drivers which we reduce to four by ignoring “scale.” In fleshing out each driver, we draw on a combination of the insights of others and our own ideas about how each may be addressed.

(A) Investment Beliefs

Investment beliefs represent how investors think markets work. They moderate their behavior with respect to those markets. Establishing a shared set of investment beliefs is important for focusing an investment organization. Basically, investment beliefs get everybody involved on the same page about how to invest. In formulating investment beliefs, it is important to consider not only evidence about markets, but also the particular strengths and weaknesses of the organization.

Investment beliefs should be framed around how long-term investing can provide access to good opportunities that the organization is well positioned to capture. Sensible investment beliefs should have a number of attributes (see also Ambachtsheer, 2017):

1. Consistency: A coherent and complete set of investment beliefs leads to consistency in thinking about how financial markets work. It allows for investment strategies to be aligned with those beliefs, while reducing the chance of conflicts between strategies. Without consistent investment beliefs, there is the tendency to drift from one strategy to the next. The result is increased chance of incurring loss by chasing the next best thing, leading to short-termism and excessive transaction costs. Investors with clear investment beliefs tend to be more disciplined, and more likely to achieve their long-term investment objectives.

2. Relevance: Investment beliefs should be tied to the investment organization’s objectives. If those objectives are long term, then investment beliefs should address which strategies deliver the best return given risk over the long run. For example, a long-term objective might suggest focusing on the capture of mean-reversion and hence trading against market consensus, and leaving chasing momentum to those with shorter horizons.

Figure 1: Four Success Drivers

Driver Intuition Elements

A) Investment beliefs Everybody on the same page about how to invest • Consistency• Relevance to objectives• Long-term focus

B) GovernanceStructure and procedures support taking and retaining long-term positions

• Board structure • Mission clarity• Governance and management roles

C) Aligned interestsAll parties are working toward the same (long-term) goals

• Objectives• Principal/agent issues• Behavioral biases

D) PeopleThose involved are long-term focused, and encouraged to remain so

• Compensation• Temperament• Tenure• Culture • Leadership

PAGE 5

Governance is about oversight and decision-making processes. Ideally, the trustee board governs rather than manages.

3. Long-term focus: For instance, a long-term focus might emerge by addressing three questions: (i) what creates investment value over the long term; (ii) how are investments priced today relative to that value; and (iii) what is the risk of suffering a permanent loss of capital? Addressing these questions might lead to developing a belief that superior returns can be generated over the long run by focusing on long-term cash flows, and identifying assets that are cheap relative to those cash flows with a solid margin of safety.

One of the key advantages of shared investment beliefs is they provide resistance to agency pressures and behavioral biases. While we will say more about these two aspects below, investment beliefs should be framed with this in mind. By giving guidance on how to interpret markets, they can help counter the natural tendency toward shortsighted reaction when volatility inevitably occurs. They can also help focus strategy formulation and execution on the needs of the beneficiaries, rather than those of the investment professionals.

A survey of 685 asset owners, managers and consultants about investment beliefs was conducted by P&I/Oxford University (2012). The survey showed that many of the attributes highlighted above are echoed by the survey participants. In particular, the majority of respondents thought that:

• Long-term strategies offer better risk-adjusted returns than short-term strategies; and,

• Long-term investors have several advantages over short-term investors, including:

• Access to certain risk premiums, (e.g., illiquidity and complexity)

• Scope to take advantage of secular themes or macro trends

• Resistance to certain psychological biases

• Reduced sensitivity to short-term volatility.

(B) Governance

Proper and effective functioning of any organization depends on governance. Governance is about oversight and decision-making processes. Ideally, the trustee board governs rather than manages. The challenge is for the board members to do so in a way that encourages those investing the assets to sustain a focus on the long term. The fact that the outcomes from long-term investments may take time to be revealed makes it problematic for the board to monitor by performance alone. The governance structure should be built to foster ongoing engagement and understanding of investment decisions from the board, with a view towards monitoring whether actions reflect the diligent pursuit of long-term objectives. A long-term board should be composed of experts who support and appreciate a long-term investment strategy, and are involved over long intervals (Clark and Urwin, 2008).

Ellis (2011) discusses the factors for good governance: board structure, mission clarity, and the separation of governance and management. We discuss these factors below in the context of what they mean from the perspective of long-term investing.

1. Board Structure

The structure of the board is important to ensure its proper and effective functioning. Key features include board size, expertise and stability.

• Size. The size of the board should be large enough to have diverse experience and expertise, but small enough to ensure everyone is heard and understood. Ellis (2011) suggests between five to nine members is optimal. Littlepage (1991) shows that performance declines as a board grows beyond 10 members, due to lack of group coordination and the dilutive effects of too many opinions.

PAGE 6

Under long-term investing it is critical that the board understands the reasoning behind investment strategies and decisions.

• Expertise. Investment experience is paramount. Not all board members need be experienced investors, but they should represent the majority. However, the nature of this experience can influence the ability to provide oversight of long-term investment programs. Stockbrokers, bankers and traders often tend to be transactional by nature, and may have shorter horizons than required to oversee long-term investment strategies. More suitable characteristics would be a history of involvement in long-term investment programs, or the creation of value for stakeholders over long periods.

• Stability of members. While overly frequent rotation of members can have negative effects on any board, it can be particularly disruptive in the case of long-term investing. Too much turnover can impair the ability of the board to learn how to work together and listen to each member; cause the loss of the stabilizing benefits of institutional memory; and undermine buy-in to long-term investment strategies. Ellis (2011) suggests the optimal tenure of members of around six to seven years. We suspect this may be too short to foster a long-term mindset. More emphasis might be placed on creating the expectation among board members that they could be around for the long haul, than on board renewal. If there is resistance to committing to long board tenures, a compromise may make those tenures renewable to provide a path to potential longevity.

2. Mission Clarity

Mission clarity concerns an explicit understanding of a fund's purpose, and how it fits with the investment objectives. Long-term investing requires not being overly cautious on taking short-term market risks, but rather being concerned with avoiding permanent loss of capital that may impair achievement of mission. Permanent loss can stem from the board overreaching into matters of management rather than governance, or losing faith in well-founded long-term investment strategies. To guard against this, the board and management should rigorously ensure that the guiding principles under which the fund operates are revisited, reevaluated and reinforced on an ongoing basis. This includes purpose, objectives, investment beliefs and investment policy guidelines. The aim is to both ensure they remain relevant and enjoy continued support from those involved, so that the

“long-term mission” is clear to all.

3. Governance and Management Roles

The role of the board is to govern, and the role of management is to manage. Overreaching by the board by attempting to undertake a management role, which requires real time involvement, is simply bad process. One example is where the board does not have adequate knowledge on selecting managers, and attempts to hire managers solely on the basis of consultant recommendations. Inadequate knowledge about what constitutes a suitable manager may lead to short-term, reactive outcomes where managers are hired and fired on the basis of recent performance; and selection of managers based on the persuasiveness of presentations and physical presence. This can be to the detriment of achieving long-term objectives. Further, it is bad practice for the board to second-guess management. When this occurs, the latter starts to focus more on managing their relationship with the board, than on working towards long-term goals.

It is important not to interpret the need to separate functions as implying the board should dispassionately monitor from a distance, focusing only on investment performance rather than on how it was generated. To the contrary, under long-term investing it is critical that the board understands the reasoning behind investment strategies and decisions. If the objective is long term, the outcome may

PAGE 7

A long-term investment strategy requires strong alignment to be faithfully implemented.

Source: World Economic Forum (2011)

not be known for some years. In the meanwhile, the board and management should engage, so that the board can judge whether the organization is effectively working towards agreed long-term objectives and not merely pursuing short-term performance (for further discussion, see Neal and Warren, 2015).

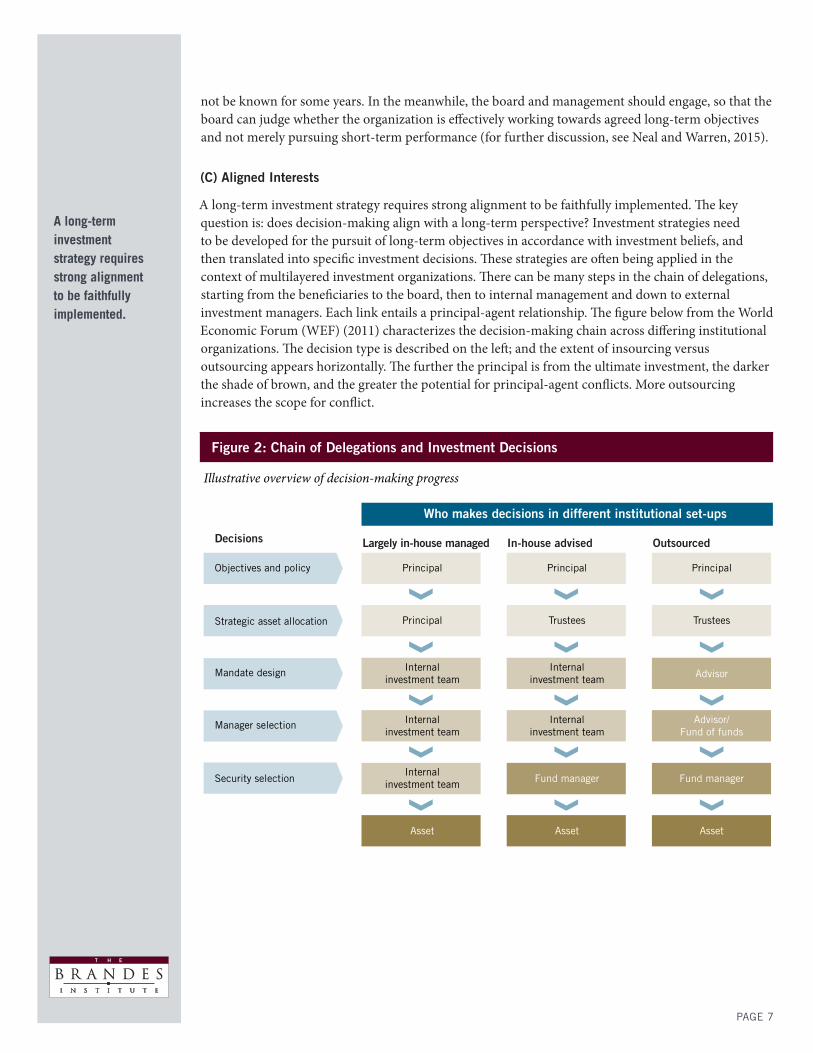

(C) Aligned Interests

A long-term investment strategy requires strong alignment to be faithfully implemented. The key question is: does decision-making align with a long-term perspective? Investment strategies need to be developed for the pursuit of long-term objectives in accordance with investment beliefs, and then translated into specific investment decisions. These strategies are often being applied in the context of multilayered investment organizations. There can be many steps in the chain of delegations, starting from the beneficiaries to the board, then to internal management and down to external investment managers. Each link entails a principal-agent relationship. The figure below from the World Economic Forum (WEF) (2011) characterizes the decision-making chain across differing institutional organizations. The decision type is described on the left; and the extent of insourcing versus outsourcing appears horizontally. The further the principal is from the ultimate investment, the darker the shade of brown, and the greater the potential for principal-agent conflicts. More outsourcing increases the scope for conflict.

Figure 2: Chain of Delegations and Investment Decisions

Objectives and policy

Illustrative overview of decision-making progress

Who makes decisions in different institutional set-ups

Decisions Largely in-house managed In-house advised Outsourced

Principal Principal Principal

Principal Trustees Trustees

Internalinvestment team

Internalinvestment team Advisor

Internalinvestment team

Fund manager Fund manager

Asset Asset Asset

Internalinvestment team

Internalinvestment team

Advisor/Fund of funds

Strategic asset allocation

Mandate design

Manager selection

Security selection

PAGE 8

Long-term investing is more prone to principal-agent concerns because of greater potential for meaningful differences in time horizons.

The challenge for multilayered investment organizations is to not only engender a shared understanding of the mission as discussed above, but also to build alignment with pursuit of that mission along the entire chain of delegations. Two problems emerge. The first is that investment outcomes can take a long time to become apparent, which makes it difficult to establish alignment with mission, and gauge the diligence with which it is being pursued. The second is that many of the individual players may be operating to their own agendas, and these could involve shorter horizons.

Although our focus is on organizational design for the long term, alignment of interests needs to focus not only on the internal staff but also on external parties—from beneficiaries through to external investment managers. With this in mind, we discuss three areas to address to strengthen alignment of a long-term-focused organization: objectives, principal-agent issues and behavioral biases.

1. Objectives

Well-defined objectives are important for ensuring alignment. Ideally, the stated investment objectives should have a long-term focus only. It is also important to make it apparent to those managing the investments what they are expected to achieve, and hence how they will be evaluated. If people are presented with clear, long-term objectives, and they have confidence they will be evaluated on how effectively they work towards them, then they are more likely to pursue those objectives. As an example, Marathon (2007) recommends setting clear objectives with a horizon over a full cycle, such as five to seven years. Dual objectives that also refer to short-term outcomes should be avoided, such as being required to produce top-quartile performance over a 12-month period. Such objectives may draw attention away from producing long-term outcomes. If dual objectives cannot be avoided, clear guidance should be given to weighing short-horizon versus long-horizon objectives.

2. Principal-Agent Issues

Principal-agent issues arise when differing goals are held by the principals of an institution—such as beneficiaries of a fund or the shareholders of a company—and their agents, such as investment managers or executives of a company. Long-term investing is more prone to principal-agent concerns because of greater potential for meaningful differences in time horizons. Investment managers are more likely to pursue shorter horizon investments than are appropriate for the beneficiaries for a number of reasons:

• Performance evaluation. Approaches to performance evaluation often act to discourage long-term investment. It is common to focus on recent performance (even daily attribution analysis!), and to evaluate performance relative to benchmarks such as the S&P 500 index. This draws focus towards short-term return drivers, and raises concerns over the risk of underperforming over a few years— or less. All this discourages committing to long-term investments that may not pay off immediately, or could perform differently versus the benchmark. It is also common to use volatility-based risk metrics that may limit a manager’s ability to take on short-term volatility in return for superior longer-term performance.

• Compensation. Bonuses and other forms of remuneration are typically set over short periods, usually once a year. Investment managers are hence incentivized to ensure their portfolios perform well over shorter time horizons. The manner in which investors’ fund flows respond to recent performance only compounds the issue, as it creates an incentive for fund managers to chase short-term performance in order to maximize assets under management and hence profits.

PAGE 9

Long-term investments that may not pay off immediately often look like a form of career risk.

• Career risk. Investment performance of staff over short periods can have a major impact on career potential. Promotions and new opportunities typically go to those responsible for recent successes, while those who have been underperforming recently may be signaled out for the next cull. Long-term investments that may not pay off immediately often look like a form of career risk. The average tenure of a public pension plan chief investment officer is about four years, and is usually shorter for more junior staff (WEF, 2011). When those investing the money are managing their next career move, they become far less likely to be longsighted in their investments.

• Chain of decision-makers. Long chains from the owner of capital to the investment manager that ultimately invests that capital only compound the agency problem, and may help encourage the pursuit of shorter-term performance (Kay, 2012; WEF, 2011). Longer chains of decision-makers make it all the more difficult to establish clarity and alignment over the mission. It also makes it less likely that those managing the investments will have confidence that their superiors are maintaining a long-term investment horizon and stay the course during those inevitable times of adversity. Reduced confidence by investment managers can induce them to take on less volatile investments (usually relative to their benchmark), or pass over opportunities where there is potential for substantial return but its timing is unclear. This may cut against the long-term investing objectives of the ultimate beneficiaries.

A number of actions might be taken to address the problems listed above. It is important that evaluations and associated rewards are based around evidence of progression towards long-term objectives, if not achievement of those objectives. Concentrating on behaviors and actions, and whether they are consistent with the pursuit of long-term objectives, is far preferable to focusing on short-term investment performance. In addition, principals should be careful to react only to developments that matter for long-run outcomes. They should aim to send a message to the agents down the chain that they are expected to pursue long-term objectives, will be evaluated on this basis and will be rewarded for it. Links should also be removed from the chain of delegations, if possible.

3. Managing Behavioral Biases

Behavioral biases can play a role in shortening investing horizons. While there are many behavioral biases, some of the more important for deterring long-term investing are listed below (for further discussion, see Warren, 2014a):

• Myopic loss aversion and hyperbolic discounting. These are two related behavioral characteristics that amount to heightened concern with short-term outcomes, including overweighting of the potential for near-term versus future gains, and avoidance of the risk of short-term loss. These biases inhibit the capacity to adopt long-term investments which are subject to near-term uncertainties, and grate against mean-reverting strategies.

• Recency bias and saliency. These biases relate to the tendency to overweight information that is more readily available. This can lead to momentum chasing, and encourages overreaction to short-term

“noise.” It can create blockages in implementing mean-reverting strategies, where it is important to take a longer view and be cognizant about how the existing order may change. Such biases result in investors becoming too optimistic when financial assets rise in price, and too pessimistic when financial assets fall in price. The increasing dissemination of financial news and data only feed these biases, making it difficult to focus on longer-term outcomes.

• Optimism bias and anchoring. Kay (2012) argues that these aspects create a bias towards action, as individuals overreact to imperfect information in the hope of making returns.

PAGE 10

Hiring people with a long-term mindset and placing them in an environment that encourages investing for the long run is essential.

• Herding. This is identified by some commentators as an important aspect of short-term, pro-cyclical behavior (e.g., WEF, 2011), although it is worth pointing out that herding can be rational where group members have superior information.

• Groupthink. This refers to the propensity for irrational or dysfunctional decision-making by groups as a consequence of the desire for harmony or conformity. Groupthink can act as a barrier for contrarian investing, an important strategy for long-term investors.

With the exception of groupthink, many of the above biases operate at the individual level, and the translation to the organizational level is another discussion. However, there is little doubt that all the listed biases are mirrored in the behavior of institutional investors on occasion. Various strategies exist for addressing these biases, and we are loath to venture into detail here. (Some discussion appears in Warren, 2014b.) Nevertheless, the first step is being aware that they exist. One idea might be to assign the specific responsibility to someone in the organization to monitor and highlight any behavioral issues that may be inhibiting the sound practice of long-term investment. Adherence with the principles outlined elsewhere within this paper should also assist, including establishing clear guiding principles, governance structures and dealing with the personnel aspects of decision implementation.

(D) People

At the end of the day, organizations consist of people—and people make the investment decisions. There is even a person behind every model or computer program. Hiring people with a long-term mindset and placing them in an environment that encourages investing for the long run is essential. A number of elements related to the human resources side of the equation are discussed below.

• Compensation. One of the key influences in a high-performing, long-term investment organization is a well-structured compensation scheme. Compensation is about what is measured and how those metrics are used. The challenge is to balance the industry standard of using short-term measures and rewards against providing incentives to pursue the long-term mission. This is no easy feat. It is human nature to want to see immediate results. A manager of one public pension plan suggests that compensation should be based on a rolling three- to five-year time horizon with clawbacks on the incentive part. The clawbacks permit the full amount of the incentive payment to be regularly awarded, but this is coupled with a vesting requirement that leads to refunds if long-term hurdles are not achieved (WEF, 2012). Another approach is to include a subjective component in performance remuneration, and then use it to explicitly recognize, reward and hence encourage behaviors that are consistent with pursuit of long-term objectives (see Neal and Warren, 2015; Warren, 2014b).

• Temperament. The people employed should have an affinity and commitment to long-term investing (Ambachtsheer, 2014; Gray, 2006; Vaughan, 1992). While temperament or character is important for successful investing in general, employees need to be a good fit for the long-term investment strategies chosen. If a valuation-based investment style is preferred as a long-term approach, then a person’s character must fit that style. For example, Seth Klarman states: “Ultimately, value investing needs to fit your character. If you’re predisposed to be patient ... [and] appreciate the idea of buying bargains, you’re likely to be good at it. If you have a need for action, if you want to be involved in new and exciting technological breakthroughs ... you’re not a value investor, and you shouldn’t be one.” (Taub, 2010)

• Tenure. If committees, staff and managers anticipate a long tenure, they are much more likely to be comfortable in pursuing long-term outcomes rather than a near-term result. Further, they must establish a significant level of trust to work well together in an environment marked by long-cycle feedback and uncertain metrics. A key concern is longevity among the staff, as a large amount of

PAGE 11

A culture that supports people who can focus on where the market could be wrong, and reflects an interest in non-mainstream views, is well positioned for successful long-term investing.

intellectual capital accumulates over time and can be eroded by staff turnover. Long-term career paths should be created within the organization itself that are based around alignment with mission rather than recent investment performance, and offer the employee long-term opportunity and purpose.

• Culture. An organization’s culture is defined by what it values and rewards. Bad culture produces bad outcomes; and good culture produces good outcomes. Lo (2016) points to the role that organizational culture played in some of the more spectacular post-1980 failures, such as Long-Term Capital Management, American International Group, Lehman Brothers and Societe Generale. A culture that encourages learning and a team attitude can provide emotional rewards that can encourage loyalty and commitment. Furthermore, a shared sense of purpose can engender pride in and devotion to an organization’s work (WEF, 2012). Such traits can further encourage staff to adopt a long-term view, as they become more likely to anticipate sticking with the organization rather than looking for the exit.

• Ability to take non-consensus positions. Willingness to take non-consensus views and positions is important, given that some of the better long-term opportunities emerge from market extremes driven by crowd behavior. A culture that supports people who can focus on where the market could be wrong, and reflects an interest in non-mainstream views, is well positioned for successful long-term investing.

• Leadership. Leaders set the tone from the top. Leadership matters for establishing, driving and cementing a long-term culture. Leaders can influence culture through the examples they set; what they chose to focus on; what they reward; and what they are not willing to tolerate. Good leaders of long-term organizations will take every opportunity to reinforce the need to focus on the long term, through the statements they make and asking the right questions at the right time.

Organizations for the Long Term

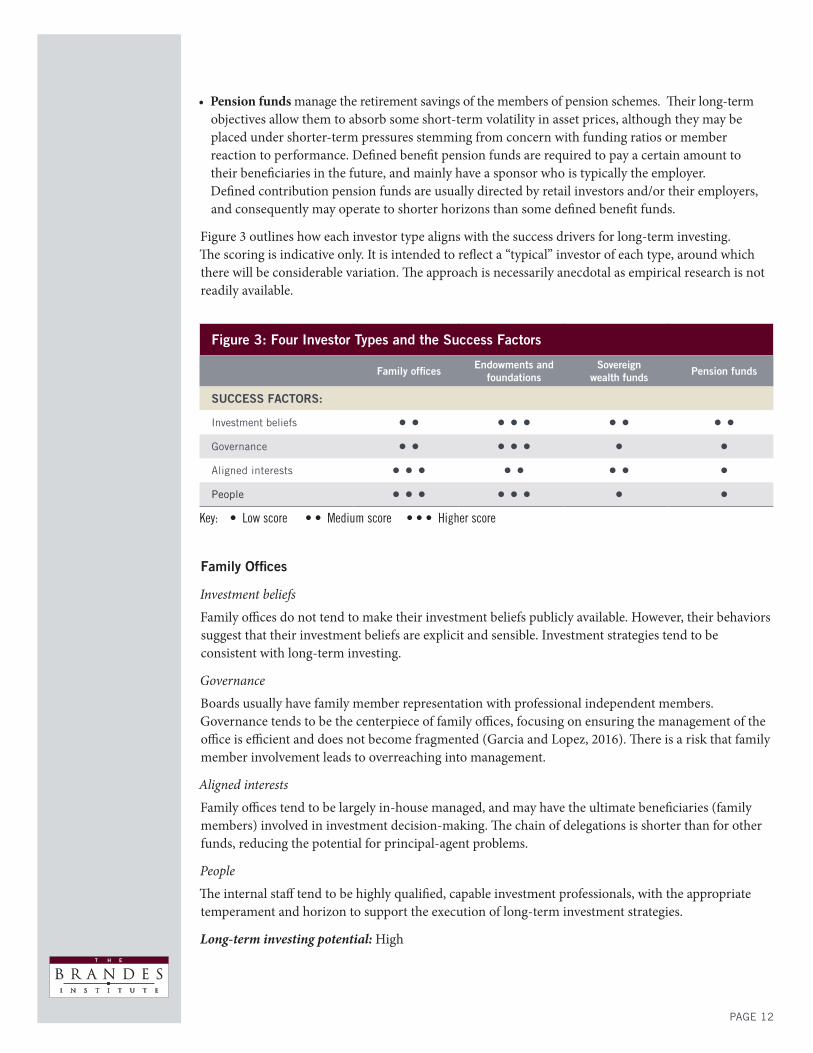

We now consider the four success drivers in reviewing various organizational structures and their suitability to long-term investing. WEF (2011) outlines types of funds that are capable of being long-term investors. Below we examine four types: family offices, endowments and foundations, sovereign wealth funds and pension funds. A brief summary of each organization appears below, drawing on WEF (2011):

• Family offices are investors that manage the wealth of one or more high-net-worth families. Family offices often are mandated to manage wealth for future generations of family members.

• Endowments and foundations exist to fund some or all of the expenses of non-profit organizations. Endowments and foundations are generally mandated to exist in perpetuity, and to provide a steady stream of income to their beneficiaries.

• Sovereign wealth funds are state-owned organizations with responsibility to invest for the long-term benefit of the nation. There are three types of sovereign wealth funds, each of which has a different mandate: stabilization, development and multigenerational funds. The latter two types of funds are usually more likely to be long-term investors since their mandate is to either channel economic surpluses into the long-term promotion of the national economy (development funds), or to provide financial support for future generations (multigenerational funds).

PAGE 12

• Pension funds manage the retirement savings of the members of pension schemes. Their long-term objectives allow them to absorb some short-term volatility in asset prices, although they may be placed under shorter-term pressures stemming from concern with funding ratios or member reaction to performance. Defined benefit pension funds are required to pay a certain amount to their beneficiaries in the future, and mainly have a sponsor who is typically the employer. Defined contribution pension funds are usually directed by retail investors and/or their employers, and consequently may operate to shorter horizons than some defined benefit funds.

Figure 3 outlines how each investor type aligns with the success drivers for long-term investing. The scoring is indicative only. It is intended to reflect a “typical” investor of each type, around which there will be considerable variation. The approach is necessarily anecdotal as empirical research is not readily available.

Family Offices

Investment beliefs

Family offices do not tend to make their investment beliefs publicly available. However, their behaviors suggest that their investment beliefs are explicit and sensible. Investment strategies tend to be consistent with long-term investing.

Governance

Boards usually have family member representation with professional independent members. Governance tends to be the centerpiece of family offices, focusing on ensuring the management of the office is efficient and does not become fragmented (Garcia and Lopez, 2016). There is a risk that family member involvement leads to overreaching into management.

Aligned interests

Family offices tend to be largely in-house managed, and may have the ultimate beneficiaries (family members) involved in investment decision-making. The chain of delegations is shorter than for other funds, reducing the potential for principal-agent problems.

People

The internal staff tend to be highly qualified, capable investment professionals, with the appropriate temperament and horizon to support the execution of long-term investment strategies.

Long-term investing potential: High

Figure 3: Four Investor Types and the Success Factors

Family offices Endowments and foundations

Sovereign wealth funds Pension funds

SUCCESS FACTORS:

Investment beliefs • • • • • • • • •Governance • • • • • • • Aligned interests • • • • • • • • People • • • • • • • •

Key: • Low score • • Medium score • • • Higher score

PAGE 13

Endowments and Foundations

Investment beliefs

It is typical for endowments and foundations to have explicit investment beliefs. These may not always be publicly available given their more private nature. One well-known example is the Yale Investment Office. Yale has explicit beliefs regarding:

• A disciplined approach to asset allocation

• The foundation of academic theory and market judgment

• The existence of manager skill, which can be identified and successfully captured

Governance

The governing boards and investment committees tend to be composed of professional investment members. The boards also typically contain members with a diverse mix of skills, knowledge and expertise. Boards tend to be small in size.

Aligned interests

Endowments and foundations tend to employ external investment managers, but may have a few strategies that are managed in-house. Beneficiaries often come in the form of large groups, such as university staff and students, or those that benefit from philanthropic activities. Trustees typically oversee the asset allocation decision, with an internal investment team implementing the allocation, and the management of the assets mostly outsourced to external investment managers. This means a longer chain of delegations, and potential for misalignment of interests. Nevertheless, alignment of interests tends to be well managed by creating long-term, trusted relationships with external managers, and hiring the right people. Alignment is often helped by a strong sense of purpose.

People

The internal staff tend to be highly qualified and well paid. They are often capable investment professionals with the appropriate temperament and supporting culture to undertake and execute on long-term investment strategies. Leadership tends to be superior, as the structure and purpose of endowments and foundations engenders high integrity, develops internal talent and leads to an ingrained sense of mission. This creates a collaborative environment, and a culture that allows people to grow.

Long-term investing potential: High

Sovereign Wealth Funds

Investment beliefs

Sovereign wealth funds are created for a variety of purposes, with differing missions. However, their general investment behavior suggests that their investment beliefs are sensible and appropriate given their specific purpose and mission, even though the beliefs tend not to be made public. They often engage in longer-term investment strategies, which is consistent with the holding of long-term investment beliefs.

Governance

Governance structures tend to vary, although it is typical that the government has board representation. Some funds tend to fall down on adhering to a clear separation between governance and management, to the extent that the government may choose to direct investment decisions. Boards that tend to overreach into investment decisions potentially undermine the full potential to engage in long-term strategies.

PAGE 14

Aligned interests

These funds tend to be in-house advised. Beneficiaries are extended in nature, being the population of a country in many cases; and these beneficiaries are often represented by a single entity, (i.e., the government). It is typical that trustees make asset allocation decisions while an internal investment team implements that allocation. Alignment of interests tend to be well managed because of the shorter chain of delegations.

People

The internal staff tend to be appropriately qualified, and usually display the appropriate temperament to undertake long-term investment strategies. However, being a sovereign entity can draw public attention to compensation. This creates a bias against hiring the best internally, in favor of hiring more expensive external investment managers.

Long-term investing potential: Medium (but probably more variable than other investor types)

Pension Funds

Investment beliefs

Whether pension funds have explicit statements of investment beliefs can vary. For example, Canadian funds by and large have explicit beliefs, and sometimes make them publicly available. In other cases, the investment behavior of pension funds suggests they either may not have sensible investment beliefs, or do not adhere to them. There can be a tendency to engage in short-horizon “beauty contest” investing, rather than genuine long-horizon wealth-creating behavior (Ambachtsheer, 2017).

Governance

Many boards are aligned with the fund’s mission and purpose. Separation of the governance function from the management function tends not to be well observed, as boards can become deeply involved in investing functions such as tactical asset allocation decisions and manager selection. Board composition may be disparate with varying levels of independence, including a mixture of professionals and lay persons representing the beneficiary constituency.

Aligned interests

Most pension funds employ many layers of agents in the execution of their mission. They tend to have the longest decision-making chain. Third party consultants (asset and actuarial) are often employed to advise on asset allocation and manager selection, with ratification by the board. The scope of internal investment capability varies across the sector from none, to executives who play an investment oversight function, to direct in-house management of investments among some of the larger funds. The ultimate investment decisions are often delegated to external investment managers across most of the industry, and in some cases the entire investment function is outsourced under an “implemented consulting” arrangement. The greater the number of layers of agents tends to make the pension fund sector more exposed to principal-agent problems.

People

Executing long-horizon wealth-creating investment strategies requires the right people working inside the organization. Focus on internal costs tends to bias against hiring such people internally, in favor of effectively hiring more expensive people through outsourcing to investment managers. In this way, the true cost can be buried by only reporting net returns to fund members or sponsors (Ambachtsheer, 2017).

Overall long-term investing potential: Low-medium

PAGE 15

The discussion in this paper mentions some practical ideas for addressing the four success drivers, although not to a comprehensive extent. We leave this for the third paper in the series.

Conclusion

We address the organizational characteristics or attributes required to enable an investment organization to successfully pursue long-term investment opportunities. We discuss four success drivers: (A) investment beliefs, (B) governance, (C) aligned interests and (D) people. We use this structure to review four types of investment organizations, and make a broad evaluation of their potential to successfully pursue long-term investing. Family offices and endowments and foundations seem best positioned to successfully sustain a long-term investment program. Sovereign wealth fund structures tend to rank lower due to governance and people factors. Pension plans rank lower again, reflecting the many layers of delegation and the challenges this brings for governance and alignment.

The aim of this paper was to set down some areas to consider when addressing whether an investment organization has positioned itself to be a successful long-term investor. The four success drivers are centered on aspects that influence how various players within an organization behave and act. In doing so, we have not ventured into other features that are important for the successful pursuit of long-term investing, such as investment process and the nature of funding sources. The discussion in this paper mentions some practical ideas for addressing the four success drivers, although not to a comprehensive extent. We leave this for the third paper in the series.

PAGE 16

References

Ambachtsheer, Keith P. “The Case for Long-Termism,” Rotman International Journal of Pension Management, 2014, 7(2), 6-15.

Ambachtsheer, Keith P. The Future of Pension Management: Integrating Design, Governance, and Investing, Wiley Finance, John Wiley & Sons, 2017.

Ambachtsheer, Keith P. and Ezra, Don D. Pension Fund Excellence: Creating Value for Stakeholders, John Wiley & Sons, Inc., 1998.

Clark, G. and Urwin, R. “Best-Practice Pension Fund Governance,” Journal of Asset Management, 2008.

Ellis, C. D. “Best Practice Investment Committees,” Journal of Portfolio Management Winter 37, no. 2 (Winter 2011): 139–147.

Garcia, Alberto and Lopez, E. Rivo. “Family Office: A New Category in Family Business Research,” University of Vigo Working Paper, June 2016.

Gray, Jack. “Avoiding Short-Termism in Investment Decision Making,” CFA Institute, December 2006.

Iverson, David. Strategic Risk Management: A Practical Guide to Portfolio Risk Management, Wiley Finance Series, John Wiley & Sons Singapore Pte. Ltd, September 2013.

Kay, John. “The Kay Review of UK Equity Markets and Long-Term Decision Making: Final Report,” The UK Crown, July 2012.

Littlepage, Glenn E. “Effects of Group Size and Task Characteristics on Group Performance: A Test of Steiner’s Model,” Personality and Social Psychological Bulletin 17, no. 4 (August 1991): 449–456.

Lo, Andrew. “The Gordon Gekko Effect: The Role of Culture in the Financial Industry,” Federal Reserve Bank of New York Economic Policy Review, August 2016.

Marathon. “Guidance Note for Long-Term Investing,” Marathon Club, Spring 2007.

Neal, David and Warren, Geoff. “Long-Term Investing as an Agency Problem,” CIFR Research Working Paper, No. 063/2015, June 2015.

P&I/Oxford University Investment Beliefs Survey Results, July 23, 2012.

Taub, Stephen. “The Value of Seth Klarman,” Institutional Investor’s Alpha, June 1, 2010.

Vaughan, Eugene H. “The Importance of Investing for the Long Term,” AIMR Conference Proceedings, CFA Institute, 1992.

Warren, Geoff. “Long-Term Investing: What Determines Investment Horizon?,” CIFR Research Working Paper, No. 024/2014, May, 2014a.

Warren, Geoff. “Designing an Investment Organization for Long-Term Investing,” CIFR Research Working Paper, No. 40/2014, October, 2014b.

Warren, Geoff. “What Does It Mean To Be A Long-Term Investor,” Brandes Institute, July 2016.

World Economic Forum. “The Future of Long-term Investing,” A World Economic Forum Report (with Oliver Wyman), 2011.

World Economic Forum. “Measurement, Governance and Long-term Investing,” A World Economic Forum Report, March 2012.

Margin of safety: The discount of a security’s market price to its estimated intrinsic value.

The S&P 500 Index with gross dividends measures equity performance of 500 of the top companies in leading industries of the U.S. economy.

This material was prepared by the Brandes Institute, a division of Brandes Investment Partners®. It is intended for informational purposes only. It is not meant to be an offer, solicitation or recommendation for any products or services. The foregoing reflects the thoughts and opinions of the Brandes Institute.

The recommended reading has been prepared by independent sources which are not affiliated with Brandes Investment Partners. Any securities mentioned reflect independent analysts’ opinions and are not recommendations of Brandes Investment Partners. These materials are recommended for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security. Past performance is not a guarantee of future results. No investment strategy can assure a profit or protect against loss.

Copyright © 2018 Brandes Investment Partners, L.P. ALL RIGHTS RESERVED. Brandes Investment Partners® is a registered trademark of Brandes Investment Partners, L.P. in the United States and Canada. Users agree not to copy, reproduce, distribute, publish or in any way exploit this material, except that users may make a print copy for their own personal, non-commercial use. Brief passages from any article may be quoted with appropriate credit to the Brandes Institute. Longer passages may be quoted only with prior written approval from the Brandes Institute. For more information about Brandes Institute research projects, visit our website at www.brandes.com/institute.

Brandes Investment Partners does not guarantee that the information supplied is accurate, complete or timely, or make any warranties with regard to the results obtained from its use. Brandes Investment Partners does not guarantee the suitability or potential value of any particular investment or information source.

The information provided in this material should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any security transactions, holdings or sector discussed were or will be profitable, or that the investment recommendations or decisions we make in the future will be profitable or will equal the investment performance discussed herein. Strategies discussed herein are subject to change at any time by the investment manager in its discretion due to market conditions or opportunities. International and emerging markets investing is subject to certain risks such as currency fluctuation and social and political changes; such risks may result in greater share price volatility. Please note that all indices are unmanaged and are not available for direct investment.

David Iverson is Head of Asset Allocation with the Guardians of New Zealand Superannuation Fund and a member of the Brandes Institute Advisory Board.

Dr. Geoff Warren is an Associate Professor at the Australian National University, where he is Convenor of the Student Managed Fund and a Director of External Research Engagement. He is also a member of the Brandes Institute Advisory Board.

The Brandes Institute11988 El Camino Real Suite 600 P.O. Box 919048 San Diego CA 92191-9048858.755.0239800.237.7119

Get the Latest Research and Ideas:

BRANDES.COM/INSTITUTE [email protected]