41

Origination Overview III

Origination Overview III

Topics covered in this training:

1. Sourcing of Assets2. Jumbo Loans

Origination Overview III

Source of Down Payment or Earnest Money Deposit:

Determine down payment funds are from an acceptable source:

• Funds did not come from a cash advance on a credit card or cash is unable to be sourced

• Gifts came from an acceptable gift source as determined by guidelines

Do assets need to be liquidated to establish an acceptable down payment

• Confirm borrower had ownership of the asset prior to sale

• Document the market value of the asset• Document and source transfer of asset

and proceeds from sale to bank deposits

Does the borrower have the minimum amount of liquid assets required to complete the transaction

• Does the minimum contribution meet the program requirement outside of AUS findings meeting investor guidelines

• Investment properties or second homes have minimum borrower contributions

• In addition to closing costs reserve requirements must be met

For FHA loans, if the source was a gift must verify that the gift is in compliance with Gifts (Personal and Equity) from the 4000.1 handbook

Origination Overview III

Gift Funds: Fannie Mae Minimum Contribution Requirements

• Gift Funds are acceptable for a mortgage loan secured by a principal residence or second home

• Minimum contribution requirements may be necessary **please refer to investor guidelines

• Borrowers must have their own funds for the purchase of investment properties

Note: For correct gift letter format and guidelines please refer to the Resource Center

LTV, CLTV, or HCLTV Ratio

Minimum Borrower Contribution Requirement from Borrower’s Own Funds

80% or Less

One- to four-unit principal residence Second home

A minimum borrower contribution from the borrower’s own funds is not required. All funds needed to complete the transaction can come from a gift.

Greater than 80%

One-unit principal residence A minimum borrower contribution from the borrower's own funds is not required. All funds needed to complete the transaction can come from a gift.

Two- to four-unit principal residence Second home

The borrower must make a 5% minimum borrower contribution from his or her own funds. After the minimum borrower contribution has been met, gifts can be used to supplement the down payment, closing costs, and reserves.

Origination Overview III

Gift Donors:• Acceptable Donors

• Generally a relative, defined as the borrower’s spouse, child, or other dependent, or by any other individual who is related to the borrower by blood, marriage, adoption, or legal guardianship; or a fiancé, fiancée, or domestic partner

• FHA does not allow a cousin as a donor, but allows a close friend with a clearly defined interest in the borrower

• FHA requires donor bank statements on all FHA gifts

• Gift funds may not be provided by or have affiliation with (even if they are a relative):

• Builder• Developer• Real Estate Agent• Any party interested to the transaction

• Gift funds not allowed at closing on Freddie Mac approved transactions, must be given to borrower Prior to Closing (PTC)

Origination Overview III

Documentation Requirements:

• Gift funds must be evidenced by a letter signed by the donor called a gift letter

• All borrowers and all donors need to sign the gift letter

• The gift letter must specify the following:1. Dollar amount of the gift (dollar amount on gift

must match the dollar amount given and deposited)

2. Date the funds were transferred3. Include a statement that no repayment is

expected4. Provide the donor’s name, address, telephone

number and relationship to the borrower5. Property address the gift is to be applied towards

• Bank statement to document donor’s ability to give and that gift funds are from an acceptable source is always required on FHA transactions

Origination Overview III

Complete Bank Statements:

• Two months bank statements required for each account supported by the loan application (1003)

* Or follow AUS findings unless investor guidelines state otherwise

Complete Brokerage Statements:

• Two months brokerage statements required for each account supported by the loan application (1003)

Origination Overview III

Complete Bank/Investment Statements:

• Bank/Investment statements must include all pages

• Blank pages within bank/investment statements will indicate page intentionally left blank and must be included

• Summary Screen shots of accounts are NOT ALLOWED: Transaction history allowed if we can identify borrower account information

Origination Overview III

Cashier’s Check or Wire:

• Cashier’s check must show the borrower as the remitter along with the approved institution which matches the assets considered in the AUS findings

• Account numbers on the cashier’s check or wire must match the account number verified and supported on the loan application (1003) and AUS findings

• Sourcing of funds required on all cashiers checks

• If a cashier’s check or wire comes from a different account not considered in the AUS findings then proper paper trail to document must be obtained

• Wire must show the institution name, name on account and account number the funds are being wired from

Origination Overview III

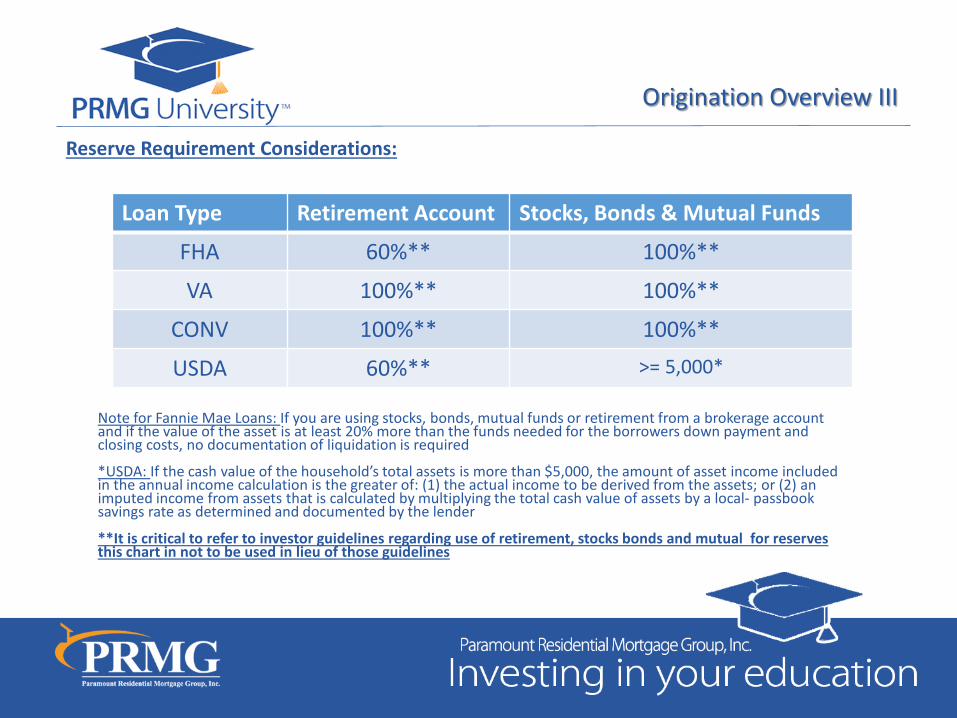

Reserve Requirement Considerations:

Loan Type Retirement Account Stocks, Bonds & Mutual Funds

FHA 60%** 100%**

VA 100%** 100%**

CONV 100%** 100%**

USDA 60%** >= 5,000*

Note for Fannie Mae Loans: If you are using stocks, bonds, mutual funds or retirement from a brokerage account and if the value of the asset is at least 20% more than the funds needed for the borrowers down payment and closing costs, no documentation of liquidation is required

*USDA: If the cash value of the household’s total assets is more than $5,000, the amount of asset income included in the annual income calculation is the greater of: (1) the actual income to be derived from the assets; or (2) an imputed income from assets that is calculated by multiplying the total cash value of assets by a local- passbook savings rate as determined and documented by the lender

**It is critical to refer to investor guidelines regarding use of retirement, stocks bonds and mutual for reserves this chart in not to be used in lieu of those guidelines

Origination Overview III

FHA 100% Access Letter:

• A 100% access letter is a letter to underwriting confirming you have access to all funds in a shared account

• It is requested when there is a borrower on a bank statement where there is a non-borrowing individual

• Relationship to borrower must be indicated in FHA 100% access letter

Origination Overview III

Types of Assets and Proof Required:

Asset Type Proof of AssetsChecking and Savings Account Bank Statements (all pages)

Stocks/Bonds/Mutual Funds Brokerage Statement (all pages)

Deposited Gift (Given Directly to Borrower) Donor Bank Statement and/or proof of withdrawal along with a borrower’s deposit slip and borrower’s bank statement to show proof of deposit documentation obtained for the donor’s withdrawal must reflect the donors name and account number in addition to the gift amount

Deposited Gift (given to Settlement Agent) Receipt of deposit verifying funds came from donor. Wire confirmation/cashiers check reflecting donors name and account number which matches gift letter and proof of withdrawal (donor bank statement required for FHA)

Retirement Funds Retirement Statement (Interval provided is acceptable Monthly/Quarterly) and terms of withdrawal

Sale Proceeds from a Home Bank Statements showing wire or check deposit and Proof of Sale (Closing Statement) from recent sale

Trust Account Proof of ownership, value and access to funds

Note: Documentation to be within all agency age requirements

Origination Overview III

Large Deposits:• Conventional: Any deposit that is 50% greater than the

total qualifying income being used

• FHA: Earnest Money Deposit is 1% of the sales price and large deposits on the bank statement is 1% of the value or is excessive based on the borrowers history of accumulating savings

• VA: Underwriter is required to make sense of the file and request documentation for large deposits that look out of the ordinary

• USDA: A large deposit that is not representative of employment earnings will need to be sourced

• If large deposits are utilized that go over the percentages described above a written letter of explanation (LOE) and documentation will be required to source such deposits

• Business assets may be used but cash analysis must be performed to determine the impact the withdrawal will have on the business **eligibility based on investor guidelines

• CPA Letter may be required for use of business assets **eligibility based on investor guidelines

• Cash on hand may not be allowed depending on loan program

Origination Overview III

Reviewing Bank Statements:

• Proof bank statement is in borrower’s name and consistent with loan application (1003)

• Verify bank statement includes account number and additional names

• Two (2) months consecutive bank statements provided all pages

• Large Deposits must be explained and properly sourced

Origination Overview III

Reviewing Bank Statements:• Payroll deposits support income provided in loan

application (1003)

• Loan payments and or recurring payments that are not indicated in the liabilities section of 1003 and credit report

• Earnest money deposit check cleared in bank statement

• Tampering has not taken place (no arts and crafts):

• Look at prior months balance and verify statements are cohesive

• Check fonts• Check interest payments

• Time period of statement covers time period of transactions

• Instances of overdrafts or insufficient funds

• Consistent online transactions generating income may require review of tax returns

Origination Overview III

Working with Jumbo Loans

1/30/2017

Locating Product Profiles

• Product Profiles can be located at the following url:

http://www.eprmg.net/guidelines/PRMGProductProfileLinks.pdf

1. Select the Product Profile for the desired loan product

Note: Product Profiles should be reviewed by Originators and Processors each time and prior to committing and locking loan program with a borrower

Jumbo and niche matrices are also available to determine the best product/fit for the borrower

Origination Overview III

Minimum and Maximum Loan Amounts

• Minimum and Maximum Loan amounts are located individually inside each product profile under the following sections:

1. Minimum Loan Amount

2. Maximum Loan Amount

Origination Overview III

Minimum Trade Line Requirements

• Credit scores are required for most mortgage loans purchased or securitized by investors, and by all of PRMG’s investors

• It is important to review the Housing Payment section within the guidelines

• Some investors require a minimum number of creditor trade lines and a minimum credit depth trade to validate credit bureau credit scores

• To determine the minimum trade line requirements for a particular loan product locate the section named Trade Line History and/or Credit section in the investor profile

Origination Overview III

Cash Reserve Requirements

• Cash Reserves are located individually inside each product profile under the following sections: Cash Reserves

Appraisal Requirements

• Please refer to product profile for appraisal requirements

Qualifying Ratios

• Please refer to specific product profiles for debt-to-income ratio requirements

Origination Overview III

Credit Seasoning Requirements:

• Do recent credit inquires suggest borrower is obtaining a new loan?

• Do recent inquiries suggest borrower is having challenges qualifying for a loan?

• Are there conflicting address references on the 1003 vs. the actual credit report, depository statements and employment documentation?

• Does the report have multiple social security numbers on credit, AKAs, fraud alerts, victim of identity theft, modified or restructured mortgages, rapid acquisition of properties?

• Does the credit report include evidence of undisclosed short sale or deed-in-lieu with verbiage such as P&L loss or settled accounts?

• If borrower is qualifying as an individual or married sole and separate, are the majority of the trade-lines individual vs. joint accounts?

• Are student loans deferred while the application shows seasoned active employment?

• Are borrowers trade line accounts open/ active trade lines sufficient without authorized user accounts?

Origination Overview III

Automated Underwriting Requirements:

• Jumbo guidelines may require the lender to run DU in addition to manually underwriting a file. You cannot follow DU findings, must follow investor guidelines

• To determine if this is a loan product requirement please locate the specific Jumbo Product profile link and search for Automated Underwriting or Desktop Underwriter within the guideline

• Automated Underwriting provides lenders a tool to conduct a comprehensive risk assessment and will evaluate the following:

1. A borrowers equity investment2. Credit history3. Liquid reserves4. Reliable and recurring income and the impact

these and other risk factors will have on borrower loan performance

If required, findings must receive an Approve/Ineligible

Note: Ineligible due to loan amount exceeding conforming limit

Origination Overview III

Delegated Underwriting

• Delegated Underwriting is when the investors decision to approve a loan is completed by our underwriters based on guidelines set by the investor

Advantages

• More control of the underwriting process and turn times

Disadvantages

• Lender is subject to greater risk through an established reps and warrants

Non-Delegated Underwriting

• Non-Delegated Underwriting is when the investor requires underwriting decisions to be completed solely by the investor within established guidelines

Advantages

• Lender risk is significantly reduced as final loan approval is determined by the investor

Disadvantages

• Underwriting turn times are subject to investor turn times

Origination Overview III

ATR/QM Rule:

• The ATR/QM rule requires that you make a reasonable, good-faith determination before or when you consummate a mortgage loan that the consumer has a reasonable ability to repay the loan, considering such factors as the consumer’s income or assets and employment status (if relied on) against:

1. The mortgage loan payment

2. Ongoing expenses related to the mortgage loan or the property that secures it, such as property taxes and insurance you require the consumer to buy

3. Payments on simultaneous loans that are secured by the same property

4. Other debt obligations, alimony, and child-support payments

5. You are required to consider and verify the consumer’s credit history

6. Limit prepayment penalties

7. Require that you retain records for three years after consummation showing you complied with ATR and other provisions of this rule

In addition to ATR/QM, you must meet documentation requirements in product profiles if more restrictive

Origination Overview III

Source of Down Payment or Earnest Money Deposit:

Determine down payment funds are from an acceptable source:

• Funds did not come from a cash advance on a credit card or cash is unable to be sourced

• Gifts came from an acceptable gift source as determined by guidelines

Do assets need to be liquidated to establish an acceptable down payment

• Confirm borrower had ownership of the asset prior to sale

• Document the market value of the asset• Document and source transfer of asset

and proceeds from sale to bank deposits

Does the borrower have the minimum amount of liquid assets required to complete the transaction

• Does the minimum contribution meet the program requirement outside of AUS findings meeting investor guidelines

• Investment properties or second homes have minimum borrower contributions

• In addition to closing costs reserve requirements must be met

It is important to review the Required Down Payment/Source of Funds and Ineligible Source of Funds sections of each product profile for each loan product

Origination Overview III

Complete Bank Statements:

• Two months bank statements required for each account supported by the loan application (1003),

Complete Brokerage Statements:

• Two months brokerage statements required for each account supported by the loan application (1003)

Origination Overview III

Complete Bank/Investment Statements:

• Bank/Investment statements must include all pages

• Blank pages within bank/investment statements will indicate page intentionally left blank and must be included

• Summary Screen shots of accounts are NOT ALLOWED: Transaction history allowed if we can identify borrower account information

Origination Overview III

Cashier’s Check or Wire:

• Cashier’s check must show the borrower as the remitter along with the approved institution which matches the assets considered

• Account numbers on the cashier’s check or wire must match the account number verified and supported on the loan application (1003) and AUS findings

• Sourcing of funds required on all cashier’s checks

• If a cashier’s check or wire comes from a different account not considered in the AUS findings then proper paper trail to document must be obtained

• Wire must show the institution name, name on account and account number the funds are being wired from

Origination Overview III

Types of Assets and Proof Required:

Asset Type Proof of AssetsChecking and Savings Account Bank Statements (all pages)

Stocks/Bonds/Mutual Funds Brokerage Statement (all pages)

Deposited Gift (Given Directly to Borrower) Donor Bank Statement and/or proof of withdrawal along with a borrower’s deposit slip and borrower’s bank statement to show proof of deposit documentation obtained for the donor’s withdrawal must reflect the donors name and account number in addition to the gift amount

Deposited Gift (given to Settlement Agent) Receipt of deposit verifying funds came from donor. Wire confirmation/cashiers check reflecting donors name and account number which matches gift letter and proof of withdrawal

Retirement Funds Retirement Statement (Interval provided is acceptable Monthly/Quarterly) and terms of withdrawal

Sale Proceeds from a Home Bank Statements showing wire or check deposit and Proof of Sale (Closing Statement) from recent sale

Trust Account Proof of ownership, value and access to funds

Note: Documentation to be within all investor age requirements

Origination Overview III

Reviewing Bank Statements:

• Proof bank statement is in borrower’s name and consistent with loan application (1003)

• Verify bank statement includes account number and additional names

• Two (2) months consecutive bank statements provided all pages

• Large Deposits must be explained and properly sourced

Origination Overview III

Reviewing Bank Statements:• Payroll deposits support income provided in loan

application (1003)

• Loan payments and or recurring payments that are not indicated in the liabilities section of 1003 and credit report

• Earnest money deposit check cleared in bank statement

• Tampering has not taken place (no arts and crafts):

• Look at prior months balance and verify statements are cohesive

• Check fonts• Check interest payments

• Time period of statement covers time period of transactions

• Instances of overdrafts or insufficient funds

• Consistent online transactions generating income may require review of tax returns

Origination Overview III

Complete Submissions:

• Most recent (1) one month's paystubs

• Most recent two years Federal Tax Returns (all pages/all schedules for all income received)

• Most recent two years W2s/1099s AND/OR K-1s for all income received

• Most recent two years corporate/partnership tax returns (if applicable/all pages/all schedules)

• Most recent 2 months’ bank statements for all asset accounts (all pages-even if blank)

• Most recent 2 months’ retirement statements (if applicable for all 401K/IRA/pension)

• Copy of mortgage payment statement, tax bill, insurance premium page and HOA statement (if applicable) for all property(s) owned

• Copy of drivers licenses for borrower and co-borrower

• Copy of divorce decree/property settlement (if applicable)

• Copy of bankruptcy discharge and all schedules (if applicable)

Origination Overview III

Jumbo and Niche Product Workflow:

Disclosures

•For wholesale transactions, all initial disclosures/LEs and subsequent COC/LE must be completed by PRMG Corporate http://www.prmg.net/tpo-le-disclosure-request/

•For retail transactions, all subsequent COC/LE after initial disclosures must be completed by PRMG Corporate

Loan Submission

•Complete file submission required to submit for underwrite/eligibility review•Files must contain all required documentation per submission checklist and must be thoroughly processed

•Missing documentation required for eligibility review will result in suspense for documentation

PRMG Underwrite

•Full file review/underwrite performed by Designed Underwriter for Diamond Platinum products•Cursory file review performed by Designated Underwriter for other Jumbo/Niche products•Loan submitted for eligibility review by underwriter to [email protected]•For Niche products only, Jumbo Review team to email [email protected] to notify of submission to investor so that all subsequent COC/LEs are submitted to investor for review

Origination Overview III

Jumbo and Niche Product Workflow (Continued):

Eligibility Review

•Eligibility review is performed, decision rendered and returned to underwriter with conditions

•Loan decision issued by underwriter with all conditions

Additional Reviews

•Condo projects that require separate investor approval can be submitted at any point in the workflow with all the proper documentation to [email protected]

•CDA (appraisal review), when required, can be ordered through [email protected] upon receipt of the appraisal (CDA may be required prior to Eligibility Review submission)

Conditions

•Conditions are sent to underwriter who reviews and submits to [email protected] •All PTD eligibility conditions must be cleared, time for condition review can vary by product•For Niche products only, final approval will not be issued until CD is reviewed by investor. When all other PTD conditions are cleared, Jumbo Review team will copy [email protected] to authorize CD creation

Origination Overview III

Jumbo and Niche Product Workflow (Continued):

Eligibility Review

•Eligibility review is performed, decision rendered and returned to underwriter with conditions

•Loan decision issued by underwriter with all conditions

Additional Reviews

•Condo projects that require separate investor approval can be submitted at any point in the workflow with all the proper documentation to [email protected]

•CDA (appraisal review), when required, can be ordered through [email protected] upon receipt of the appraisal (CDA may be required prior to Eligibility Review submission)

Conditions

•Conditions are sent to underwriter who reviews and submits to [email protected] •All PTD eligibility conditions must be cleared, time for condition review can vary by product•For Niche products only, final approval will not be issued until CD is reviewed by investor. When all other PTD conditions are cleared, Jumbo Review team will copy [email protected] to authorize CD creation

Origination Overview III

Jumbo and Niche Product Workflow (Continued):

Prior to Doc Compliance

Review

•Conditions are sent to underwriter who reviews and submits to [email protected] •All PTD eligibility conditions must be cleared, time for condition review can vary by product•For Niche products only, final approval will not be issued until CD is reviewed by investor. When all other PTD conditions are cleared, Jumbo Review team will copy [email protected] to authorize CD creation

Prior to Funding Compliance

Review

•Early CD process not allowed for Jumbo or Niche products•For wholesale/retail, fulfillment center to request CD creation from [email protected]

•For wholesale/retail, Compliance must generate initial CD•For correspondent, PRMG's Correspondent Compliance team must review initial CD

Special Notes

•Be sure to set proper expectations with borrowers and realtors. These products take longer than others to move through the system. Provide extra time for unexpected contingencies, and let your partners know that it may occur

Origination Overview III

Collateral Desktop Analysis (CDA):

• Appraisals may contain workmanship discrepancies or errors which increase lender risk

• Performing a CDA will take a second look into the appraisal provided during origination to:

1. Validate Appraisal Integrity

2. Ensure accurate representation of subject and comparable transactions

3. Support appraised value

4. Recommend further appraisal review such as a field review

Origination Overview III

Jumbo Underwriting:

All jumbo loans must be submitted for an eligibility review prior to being underwritten

Jumbo loans must be underwritten by a Level 4 Designated underwriter

Jumbo loans have more extensive underwriting and take longer (please take this into consideration when locking)

No exceptions to documentation or compliance requirements

Loan products must be underwritten to investor guidelines/requirements

Credit documentation must be signed prior to consummation (note) date

Documentation expiration timeframes may be shorter than standard agency products

Additional Compliance review required on each loan

Origination Overview III

Jumbo Considerations:

• 1003 and 1008 (and all other underwriting documents) must be accurate, accounts must be listed separately, balances and amounts must be updated, etc.

• Use submission checklist to ensure all necessary information is included

• You are highly encouraged to review the product profiles and expanded guidelines to become familiar with these products and the additional requirements

• Link to Product Profiles: http://www.eprmg.net/guidelines/PRMGProductProfileLinks.pdf

• Anticipate and plan for the time it is going to take to get these loans through the system

• Set proper expectations with the borrowers and Realtors®

Origination Overview III

Jumbo Eligibility Review:

• An eligibility review is required for (Platinum, Silver, Emerald, Diamond, Gold and Niche Products)

• Appraisal in first generation PDF (the version provided from the appraiser to PRMG – to determine if it is the correct version you must be able to "search" (i.e., using Ctrl + F) for text in the document) must be attached to the email request sent to [email protected]

• Eligibility Review Submission Form must be completed and attached to the email request sent to:

• This form can be found on the Resource Center or in the product profiles

Origination Overview III

Jumbo Eligibility Review (Continued):

• PRMG Designated Jumbo Underwriter must complete Eligibility Review Submission form and send an email request for review submission to:

• 1008, underwriter's 1003 and current approval must be uploaded into eFolder before submission to:

• All documentation required on Eligibility Review Submission Form must be uploaded into eFolder prior to submitting request for eligibility review, it does not need to be sent to:

• It will be downloaded directly from FT360

Origination Overview III