22

Osum Oil Sands Corp. Annual General Meeting Metropolitan Centre, Calgary June 1, 2016

Osum Oil Sands Corp. Annual General Meeting

Metropolitan Centre, Calgary

June 1, 2016

Disclaimer ForwardLookingStatementsThis presenta,on contains statements that may cons,tute "forward-looking statements” within the meaning of applicable securi,es legisla,on. Thesestatementsinclude,amongothers,statementsregardingbusinessstrategy,beliefs,plans,goals,objec,ves,assump,onsorstatementsaboutfutureeventsorperformance. Bytheirnature,forwardlookingstatementsaresubjecttonumerousrisksanduncertain,es,someofwhicharebeyondtheCompany'scontrol,includingtheimpactofgeneraleconomiccondi,ons,industrycondi,ons,vola,lityofcommodityprices,currencyfluctua,ons,environmentalrisks,compe,,onfromother industrypar,cipants, lackofavailabilityofqualifiedpersonnelormanagement,stockmarketvola,lityandabilitytoaccesssufficientcapital frominternalandexternalsources.Readersarecau,onedthattheassump,onsusedintheprepara,onofsuchinforma,on,althoughconsideredreasonableatthe,meofprepara,on,mayprovetobeincorrectand,assuch,unduerelianceshouldnotbeplacedonforward-lookingstatements.Actualresults,performanceorachievementcoulddiffermateriallyfromthoseexpressedin,orimpliedbyanyforwardlookingstatementsinthispresenta,on,andaccordingly,noassurancecanbegiventhatanyoftheeventsan,cipatedbytheforward-lookingstatementswilltranspireoroccur,orifanyofthemdoso,whatbenefitstheCompanywillderivetherefrom.

TheCompanydisclaimsanyinten,onorobliga,ontoupdateorreviseanyforward-lookingstatements,whetherasaresultofnewinforma,on,futureeventsorotherwise.

ReservesandResourceExceptwherenotedtobefromanothersource,thereservees,mateshereinwereextractedfromreportspreparedbyGLJPetroleumConsultantsLtd.(GLJ),anindependentprofessionalpetroleumengineeringfirm,inaccordancewithCanadianSecuri,esAdministrators’Na,onalInstrument51-101(NI51-101)andtheCanadian Oil and Gas Evalua,on Handbook (COGEH). Under NI 51-101, proved reserves are those reserveswhich can be es,matedwith a high degree ofcertaintytoberecoverable.Itis90percentlikelythatactualremainingquan,,eswillexceedes,matedprovedreserves.Probablereservesarethoseaddi,onalreservesthatarelesscertaintoberecoveredthanprovedreserves.Itisequallylikelythattheactualremainingquan,,esrecoveredwillbegreaterorlessthanthesumofprovedplusprobablereserves.Possiblereservesarethoseaddi,onalreservesthatarelesscertaintoberecoveredthanprobablereserves.Thereisonlya10percentprobabilitythatthequan,,esactuallyrecoveredwillequalorexceedthesumofprovedplusprobablepluspossiblereserves.

Theprepara,onofanevalua,onrequirestheuseofjudgementinapplyingthestandardsanddefini,onscontainedinCOGEHandNI51-101.AstheCompany’sindependentreserveevaluator,GLJappliesthosestandardsanddefini,onsbasedonitsexperienceandknowledgeofindustryprac,ce.However,becausetheapplica,onofthestandardsanddefini,onscontained inCOGEHandNI51-101requiretheuseof judgementthere isnoassurancethatgoverningsecuri,esregulator(s)willnottakeadifferentviewthanGLJastosomeofthedetermina,onsinanevalua,on.

Resourcees,mateshereinarethoseoftheCompany’smanagementandarenotinaccordancewithNI51-101orCOGEH.

Presenta7onofFinancialInforma7onUnlessotherwisestated,allfigurespresentedareinCanadianDollars.

2015 Corporate Highlights

3

Solid Financial Position(1)

• $199mm in net working capital(2), US$15mm undrawn revolver • $284mm term loan(3) maturing in 2020 • Active commodity hedging program covering about 50% of production • Prudently managing spending within context of current environment

1. As at December 31, 2015 2. Excludes net unrealized hedging assets. Includes $100 million from proceeds of callable warrants. 3. Long term portion of principal outstanding on US$210 million term loan converted at December 31, 2015 foreign exchange rate.

Leadership & Support

• Strong shareholder group including Blackstone Capital, Warburg Pincus, Azimuth Capital, GIC, KIC and two Canadian pension funds

• Experienced Management & Board of Directors

Positioned for Growth

• High quality assets with defined and approved growth projects in the Cold Lake region that allow for staged expansions to over 50,000 bpd, when commodity prices allow

• Significant long-term upside in the bitumen carbonate resource play (Saleski)

Production and

Cashflow

• 7,736 bbl per day of commercial production from Cold Lake • Positive field-level netbacks below US$40 WTI - significant structural

advantages compared to Athabasca thermal producers

Core Areas

Cold Lake

• Profitable production and growth

Grosmont Carbonates (Saleski)

• An enormous opportunity in the bitumen carbonate resource play

4

Cold Lake Portfolio

5 - 5 10 15 20 25 30 35

TaigaOrion

Mbpd

AverageProduc,on(2015) NameplateCapacity RegulatoryApproval

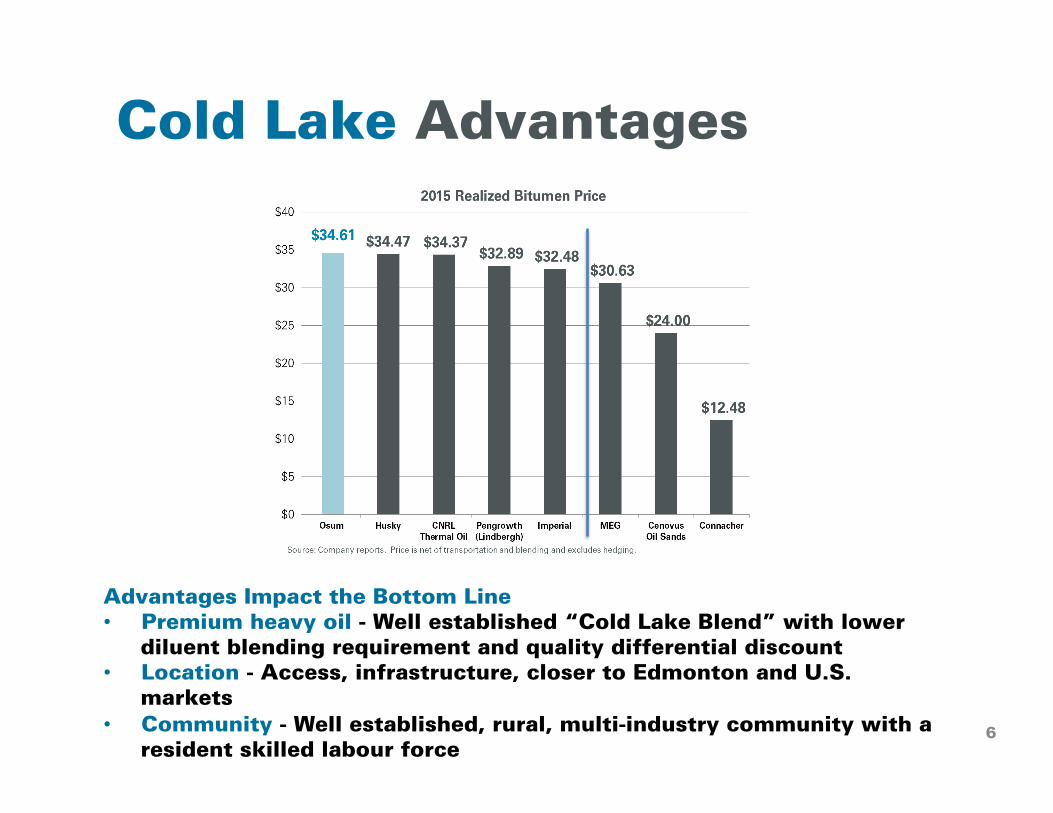

Cold Lake Advantages

Advantages Impact the Bottom Line • Premium heavy oil - Well established “Cold Lake Blend” with lower

diluent blending requirement and quality differential discount • Location - Access, infrastructure, closer to Edmonton and U.S.

markets • Community - Well established, rural, multi-industry community with a

resident skilled labour force 6

Cold Lake Orion • Orion SAGD asset was acquired from Shell in July 2014

• 100% WI in a production facility, 5,440 acres of land, and 22 well pairs on 6 well pads

• Regulatory approval for expansion to 20,000 bbl per day

• Production: 7,736 bbl per day (2015 Average)

• Reserves: Proven (1P) 47 MMbbl, Proven plus Probable (2P) 127 MMbbl 1

71. GLJPetroleumConsultants.ReservesandresourcesasatDec.31,2015.

Cold Lake Taiga

• Thermal in-situ project to be developed through staged expansions

• Regulatory approval in place for 35,000 bpd and the potential to reach 45,000 bpd at full development

• 100% W.I. in 22,422 acres located 10 miles from Orion

• Two proven commercial high quality, laterally predictable shoreface reservoir zones

• Producing Analogs

• Clearwater – Osum Orion

• Lower Grand Rapids – Pengrowth Lindbergh & CNRL Wolf Lake B10

• Reserves: Proven plus Probable (2P) 376 MMbbl1

TaigaProject

1. GLJPetroleumConsultants.ReservesandresourcesasatDec.31,2015.8

Saleski&LiegeProjects

Grosmont Carbonates Portfolio

High quality resource position in world scale play

• Over 4 billion bbl (net) recoverable resources1

• Thick, laterally extensive oil columns in stacked target zones

Established commercial potential through pilot project (shut-in in Q3 2015)

Leveraging knowledge gained to date to refine our plans with a focus on Osum’s Grosmont C position

1. Managementes,mate.See“ReservesandResources”Disclaimeronpage2.9

2015 Review

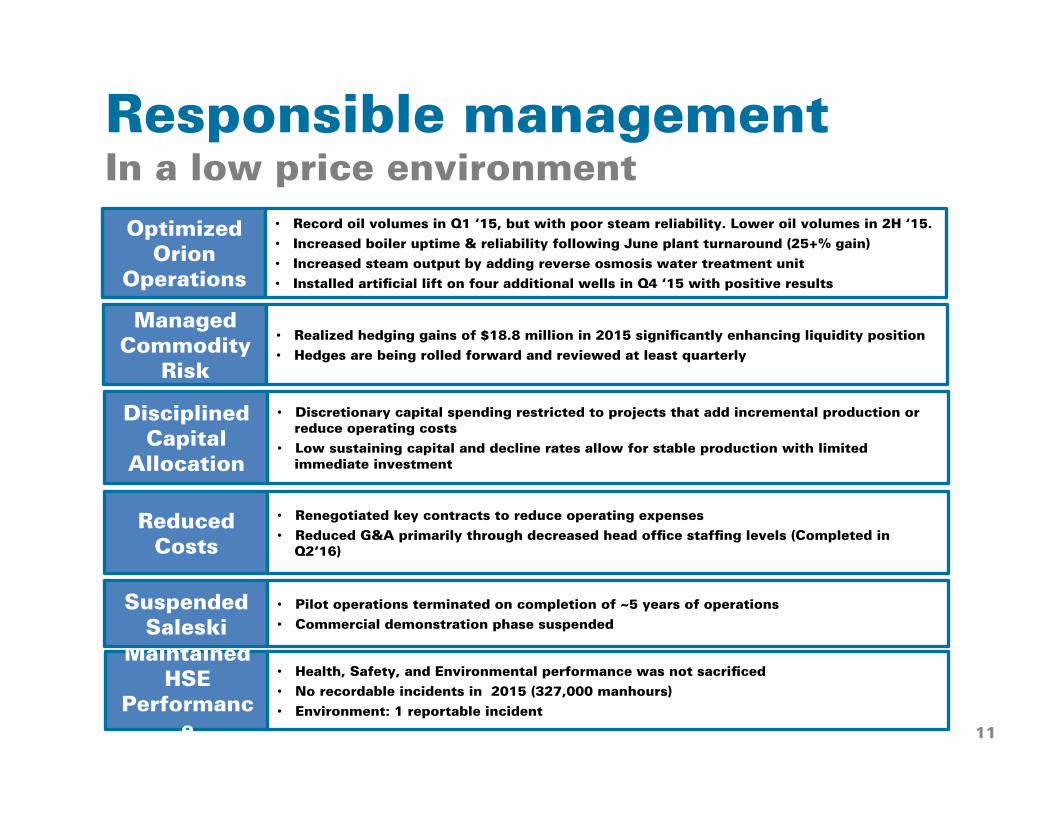

Optimized Orion

Operations

• Record oil volumes in Q1 ‘15, but with poor steam reliability. Lower oil volumes in 2H ‘15.

• Increased boiler uptime & reliability following June plant turnaround (25+% gain)

• Increased steam output by adding reverse osmosis water treatment unit

• Installed artificial lift on four additional wells in Q4 ‘15 with positive results

Managed Commodity

Risk

• Realized hedging gains of $18.8 million in 2015 significantly enhancing liquidity position

• Hedges are being rolled forward and reviewed at least quarterly

Disciplined Capital

Allocation

• Discretionary capital spending restricted to projects that add incremental production or reduce operating costs

• Low sustaining capital and decline rates allow for stable production with limited immediate investment

Reduced Costs

• Renegotiated key contracts to reduce operating expenses

• Reduced G&A primarily through decreased head office staffing levels (Completed in Q2‘16)

Responsible management In a low price environment

Maintained HSE

Performance

• Health, Safety, and Environmental performance was not sacrificed

• No recordable incidents in 2015 (327,000 manhours)

• Environment: 1 reportable incident

Suspended Saleski

• Pilot operations terminated on completion of ~5 years of operations

• Commercial demonstration phase suspended

11

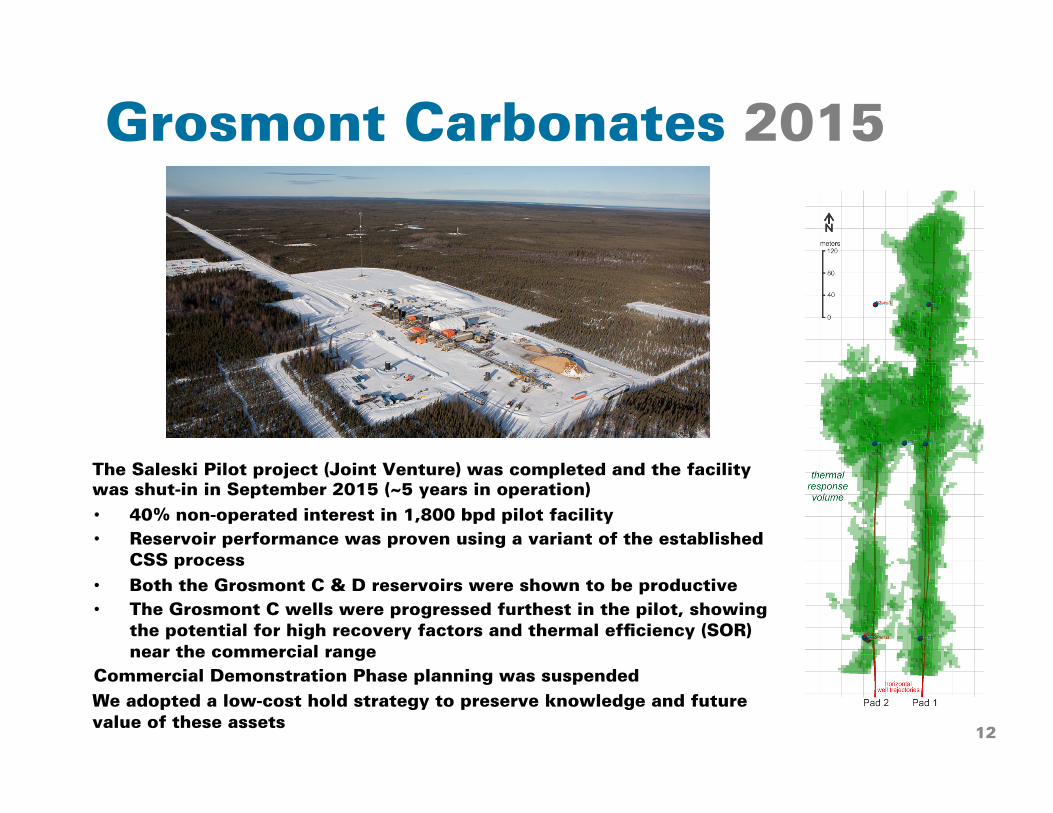

Grosmont Carbonates 2015

The Saleski Pilot project (Joint Venture) was completed and the facility was shut-in in September 2015 (~5 years in operation)

• 40% non-operated interest in 1,800 bpd pilot facility

• Reservoir performance was proven using a variant of the established CSS process

• Both the Grosmont C & D reservoirs were shown to be productive

• The Grosmont C wells were progressed furthest in the pilot, showing the potential for high recovery factors and thermal efficiency (SOR) near the commercial range

Commercial Demonstration Phase planning was suspended

We adopted a low-cost hold strategy to preserve knowledge and future value of these assets

12

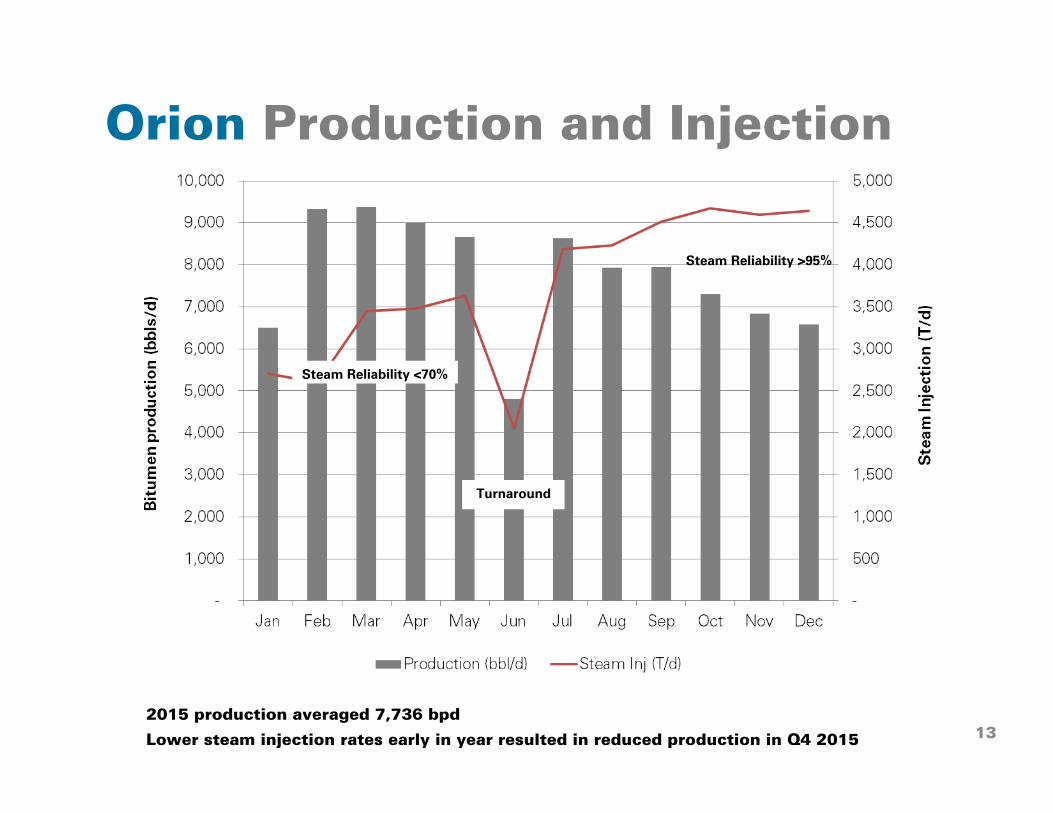

Orion Production and Injection

Turnaround

Steam Reliability >95%

Steam Reliability <70%

2015 production averaged 7,736 bpd

Lower steam injection rates early in year resulted in reduced production in Q4 2015 13

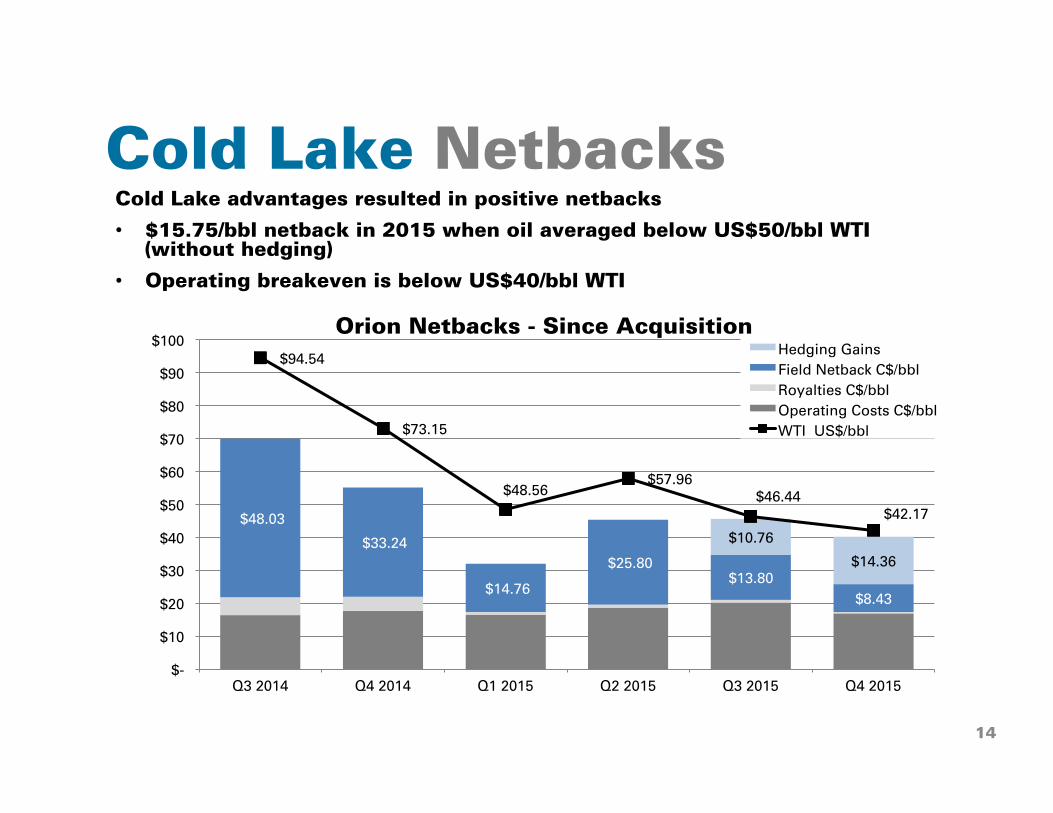

Cold Lake Netbacks Cold Lake advantages resulted in positive netbacks

• $15.75/bbl netback in 2015 when oil averaged below US$50/bbl WTI (without hedging)

• Operating breakeven is below US$40/bbl WTI

$48.03

$33.24

$14.76

$25.80 $13.80

$8.43

$10.76

$14.36

$94.54

$73.15

$48.56 $57.96

$46.44 $42.17

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Orion Netbacks - Since Acquisition Hedging Gains

Field Netback C$/bbl

Royalties C$/bbl

Operating Costs C$/bbl

WTI US$/bbl

14

Orion Operating Results

15

1VolumesfromtheSaleskipilotarenotincluded22014representstheperiodfollowingtheOrionacquisi,ononly3Financialhedginggainsonly.Physicalhedginggainsareincludedinbitumenrevenue

2015 2014(2) Change-$ Change-%BitumenProduc,on(1) bbl/d 7,736 7,996 (260) (3%) WTI US$/bbl 48.76 81.70 (32.94) (40%)ColdLakeBlend US$/bbl 33.84 63.84 (30.00) (47%)Differen,al US$/bbl 14.92 17.86 (2.94) (16%)Differen,al % 30.6% 21.90% 8.70% 40%ForeignExchangeRate US$/C$ 0.782 0.892 (0.110) (12%)AECOGasPrice C$/mcf 2.77 4.01 (1.24) (31%) BitumenFieldPrice C$/bbl 34.61 60.76 (26.15) (43%)Royal,es C$/bbl 0.69 4.67 (3.98) (85%)Opera,ngCosts C$/bbl 18.18 17.28 0.90 5%FieldNetbackBeforeHedging C$/bbl 15.74 38.81 (23.07) (59%)RealizedHedgingGains C$/bbl 6.10 - 6.10 -CashOpera,ngNetbackAmerHedging C$/bbl 21.84 38.81 (16.97) (44%)

FieldNetbackBeforeHedging C$000 44,446RealizedHedgingGains(3) C$000 17,223CashOpera,ngNetbackAmerHedging C$000 61,669

Balance Sheet

16

31-Dec-15 31-Dec-14

Cash and Cash Equivalents (1) C$ MM 109.4 115.6

Working Capital Surplus (2) C$ MM 199.3 208.5

Long Term Debt Outstanding (3) C$ MM 284.1 230.5

Basic Shares Outstanding (4) MM 130.4 130.4

(1)

Includes restricted cash

(2)Excludes net unrealized hedging assets. Includes $100MM proceeds from callable common share purchase warrants

(3)Consists of the outstanding non-current portion of the term loan translated to C$ at the period-end exchange rate. The current portion is included in the working capital surplus. The term loan bears a floating interest rate based on the greater of LIBOR or 1%, plus 5.5%.

(4)Includes 8.0 million callable common share purchase warrants with an exercise price of $12.50/share

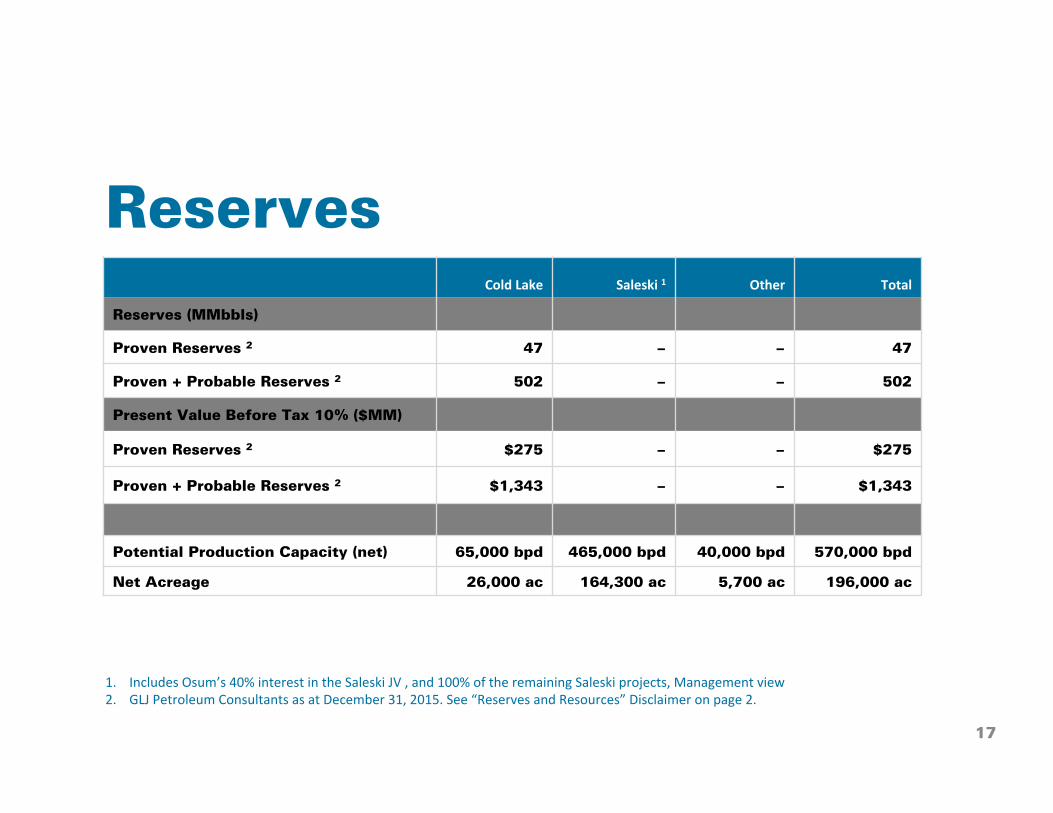

Reserves

17

ColdLake Saleski1 Other Total

Reserves (MMbbls)

Proven Reserves 2 47 − − 47

Proven + Probable Reserves 2 502 − − 502

Present Value Before Tax 10% ($MM)

Proven Reserves 2 $275 − − $275

Proven + Probable Reserves 2 $1,343 − − $1,343

Potential Production Capacity (net) 65,000 bpd 465,000 bpd 40,000 bpd 570,000 bpd

Net Acreage 26,000 ac 164,300 ac 5,700 ac 196,000 ac

1. IncludesOsum’s40%interestintheSaleskiJV,and100%oftheremainingSaleskiprojects,Managementview2. GLJPetroleumConsultantsasatDecember31,2015.See“ReservesandResources”Disclaimeronpage2.

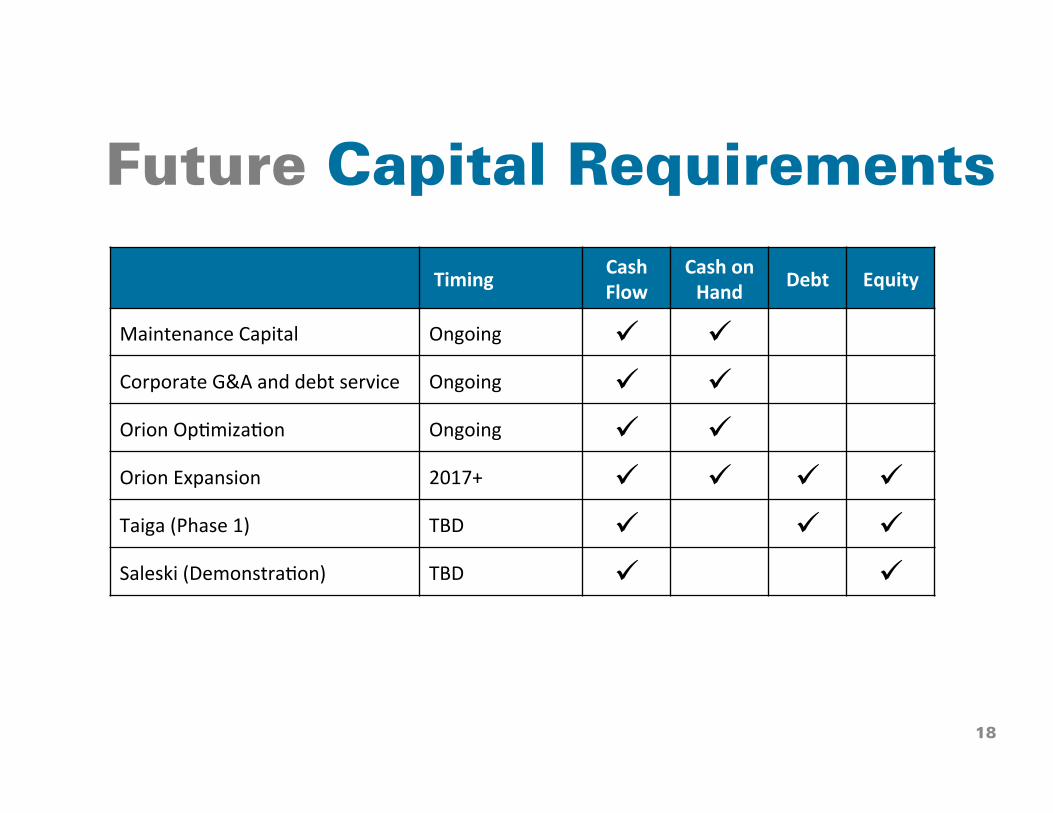

Future Capital Requirements

Timing CashFlow

CashonHand Debt Equity

MaintenanceCapital Ongoing ü üCorporateG&Aanddebtservice Ongoing ü üOrionOp,miza,on Ongoing ü üOrionExpansion 2017+ ü ü ü üTaiga(Phase1) TBD ü ü üSaleski(Demonstra,on) TBD ü ü

18

2016 Focus • Manage our finances prudently to protect the business

through the downturn

• Focus on our Cold Lake assets in the near term, adding production and reducing structural costs

• Pursue small production enhancement projects at Orion that are profitable in today’s business conditions, and make the business more robust (e.g. debottlenecking, well stimulations)

• Larger expansions will be considered as oil prices recover to a point that provides the confidence to move forward

• Deliver superior safety and environmental performance

19

Summary • 2015 was a challenging year characterized by declining oil

prices and production swings

• We achieved positive operating netbacks through the year, which were further uplifted by a successful hedging program

• Our liquidity remains strong

• We have positioned the business to weather the downturn and will continue to manage our finances prudently

• Our operational priorities for 2016 are to stabilize production, and further reduce costs

• Our near term discretionary capital expenditures are focused on small production enhancement projects at Orion that are profitable in today’s business conditions

• We are well positioned for the long term with a portfolio of significant growth opportunities

20

Board of Directors

21

Name/Title RelevantPriorExperienceRichard(Rick)George,OCChairman

¡ FormerCEO&DirectorofSuncorEnergy¡ DirectoroftheRoyalBankofCanada,AnadarkoPetroleum,andPennWestExplora,on

(Chairman)¡ Partner,NovoInvestmentGroup

AngeloAcconcia ¡ SeniorManagingDirector,BlackstoneCapitalPartnersandBlackstoneEnergyPartners¡ DirectorofAltaEnergy,HunterOil&Gas,LLOGExplora,on,andRoyalResources

VincentChahley ¡ IndependentBusinessman¡ FormerManagingDirectorofCorporateFinanceatFirstEnergyCapital

GeorgeCrookshank ¡ IndependentBusinessman¡ FormerVicePresidentofFinanceandChiefFinancialOfficerofOPTICanadaInc.(2002to2007)

WilliamA.Friley ¡ IndependentBusinessman¡ PresidentandChiefExecu,veOfficerofTellurideOilandGasandPresidentofSkyelandOils

DavidKrieger ¡ ManagingDirector,WarburgPincusLLC¡ DirectorofBlackSwanEnergy,CanbriamEnergy,Ceres,EnduranceEnergy,FirstGreen

Partners,KosmosEnergy,MEGEnergy,VelvetEnergyandWestValleyEnergy

GaryLevin ¡ Principal,BlackstoneCapitalPartnersandBlackstoneEnergyPartners¡ DirectorofLLOGExplora,onandVineOil&Gas

CameronMcVeigh ¡ President,CamcorPartnersInc.¡ DirectorofTangleCreekEnergy

BrianReinsborough ¡ Founder,President&CEO,VenariResourcesLLC¡ FormerPresidentofNexenPetroleumU.S.A.

JeffvanSteenbergen ¡ ManagingPartner,AzimuthCapitalManagement¡ DirectorofAduroResources,AltexEnergy,CobaltInterna,onalEnergy(US),FairfieldEnergy

(UK),MagmaGlobalLtd.,andSevenGenera,onsEnergy

SteveSpence ¡ President&CEOofOsum

Thank You