Osum Oil Sands Corp. Annual General Meeting

Metropolitan Centre, Calgary

June 1, 2016

Disclaimer ForwardLookingStatementsThis presenta,on contains statements that may cons,tute "forward-looking statements” within the meaning of applicable securi,es legisla,on. Thesestatementsinclude,amongothers,statementsregardingbusinessstrategy,beliefs,plans,goals,objec,ves,assump,onsorstatementsaboutfutureeventsorperformance. Bytheirnature,forwardlookingstatementsaresubjecttonumerousrisksanduncertain,es,someofwhicharebeyondtheCompany'scontrol,includingtheimpactofgeneraleconomiccondi,ons,industrycondi,ons,vola,lityofcommodityprices,currencyfluctua,ons,environmentalrisks,compe,,onfromother industrypar,cipants, lackofavailabilityofqualifiedpersonnelormanagement,stockmarketvola,lityandabilitytoaccesssufficientcapital frominternalandexternalsources.Readersarecau,onedthattheassump,onsusedintheprepara,onofsuchinforma,on,althoughconsideredreasonableatthe,meofprepara,on,mayprovetobeincorrectand,assuch,unduerelianceshouldnotbeplacedonforward-lookingstatements.Actualresults,performanceorachievementcoulddiffermateriallyfromthoseexpressedin,orimpliedbyanyforwardlookingstatementsinthispresenta,on,andaccordingly,noassurancecanbegiventhatanyoftheeventsan,cipatedbytheforward-lookingstatementswilltranspireoroccur,orifanyofthemdoso,whatbenefitstheCompanywillderivetherefrom.

TheCompanydisclaimsanyinten,onorobliga,ontoupdateorreviseanyforward-lookingstatements,whetherasaresultofnewinforma,on,futureeventsorotherwise.

ReservesandResourceExceptwherenotedtobefromanothersource,thereservees,mateshereinwereextractedfromreportspreparedbyGLJPetroleumConsultantsLtd.(GLJ),anindependentprofessionalpetroleumengineeringfirm,inaccordancewithCanadianSecuri,esAdministrators’Na,onalInstrument51-101(NI51-101)andtheCanadian Oil and Gas Evalua,on Handbook (COGEH). Under NI 51-101, proved reserves are those reserveswhich can be es,matedwith a high degree ofcertaintytoberecoverable.Itis90percentlikelythatactualremainingquan,,eswillexceedes,matedprovedreserves.Probablereservesarethoseaddi,onalreservesthatarelesscertaintoberecoveredthanprovedreserves.Itisequallylikelythattheactualremainingquan,,esrecoveredwillbegreaterorlessthanthesumofprovedplusprobablereserves.Possiblereservesarethoseaddi,onalreservesthatarelesscertaintoberecoveredthanprobablereserves.Thereisonlya10percentprobabilitythatthequan,,esactuallyrecoveredwillequalorexceedthesumofprovedplusprobablepluspossiblereserves.

Theprepara,onofanevalua,onrequirestheuseofjudgementinapplyingthestandardsanddefini,onscontainedinCOGEHandNI51-101.AstheCompany’sindependentreserveevaluator,GLJappliesthosestandardsanddefini,onsbasedonitsexperienceandknowledgeofindustryprac,ce.However,becausetheapplica,onofthestandardsanddefini,onscontained inCOGEHandNI51-101requiretheuseof judgementthere isnoassurancethatgoverningsecuri,esregulator(s)willnottakeadifferentviewthanGLJastosomeofthedetermina,onsinanevalua,on.

Resourcees,mateshereinarethoseoftheCompany’smanagementandarenotinaccordancewithNI51-101orCOGEH.

Presenta7onofFinancialInforma7onUnlessotherwisestated,allfigurespresentedareinCanadianDollars.

2015 Corporate Highlights

3

Solid Financial Position(1)

• $199mm in net working capital(2), US$15mm undrawn revolver • $284mm term loan(3) maturing in 2020 • Active commodity hedging program covering about 50% of production • Prudently managing spending within context of current environment

1. As at December 31, 2015 2. Excludes net unrealized hedging assets. Includes $100 million from proceeds of callable warrants. 3. Long term portion of principal outstanding on US$210 million term loan converted at December 31, 2015 foreign exchange rate.

Leadership & Support

• Strong shareholder group including Blackstone Capital, Warburg Pincus, Azimuth Capital, GIC, KIC and two Canadian pension funds

• Experienced Management & Board of Directors

Positioned for Growth

• High quality assets with defined and approved growth projects in the Cold Lake region that allow for staged expansions to over 50,000 bpd, when commodity prices allow

• Significant long-term upside in the bitumen carbonate resource play (Saleski)

Production and

Cashflow

• 7,736 bbl per day of commercial production from Cold Lake • Positive field-level netbacks below US$40 WTI - significant structural

advantages compared to Athabasca thermal producers

Core Areas

Cold Lake

• Profitable production and growth

Grosmont Carbonates (Saleski)

• An enormous opportunity in the bitumen carbonate resource play

4

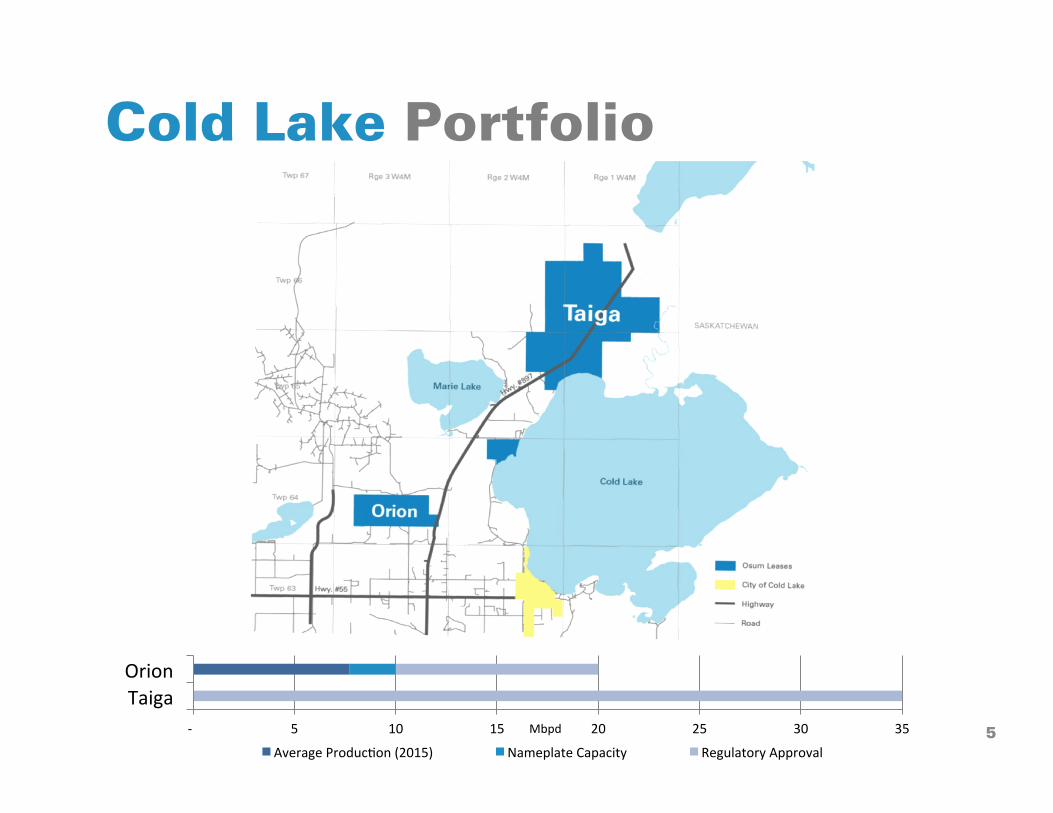

Cold Lake Portfolio

5 - 5 10 15 20 25 30 35

TaigaOrion

Mbpd

AverageProduc,on(2015) NameplateCapacity RegulatoryApproval

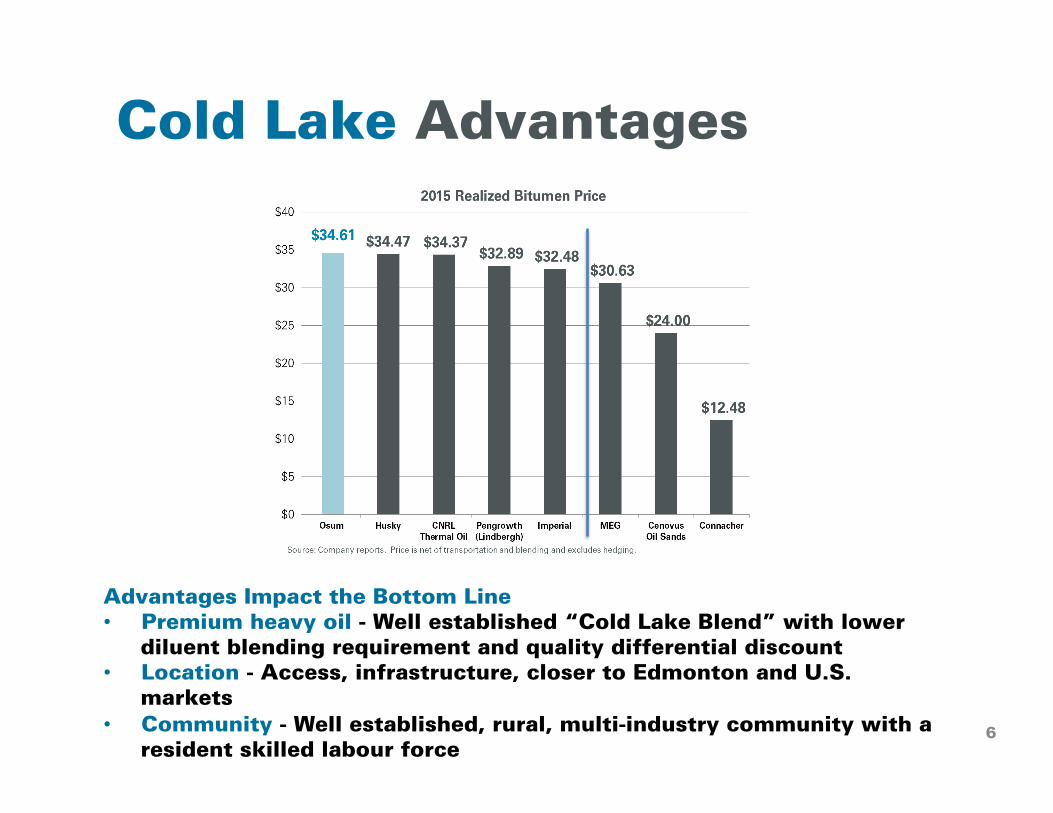

Cold Lake Advantages

Advantages Impact the Bottom Line • Premium heavy oil - Well established “Cold Lake Blend” with lower

diluent blending requirement and quality differential discount • Location - Access, infrastructure, closer to Edmonton and U.S.

markets • Community - Well established, rural, multi-industry community with a

resident skilled labour force 6

Cold Lake Orion • Orion SAGD asset was acquired from Shell in July 2014

• 100% WI in a production facility, 5,440 acres of land, and 22 well pairs on 6 well pads

• Regulatory approval for expansion to 20,000 bbl per day

• Production: 7,736 bbl per day (2015 Average)

• Reserves: Proven (1P) 47 MMbbl, Proven plus Probable (2P) 127 MMbbl 1

71. GLJPetroleumConsultants.ReservesandresourcesasatDec.31,2015.

Cold Lake Taiga

• Thermal in-situ project to be developed through staged expansions

• Regulatory approval in place for 35,000 bpd and the potential to reach 45,000 bpd at full development

• 100% W.I. in 22,422 acres located 10 miles from Orion

• Two proven commercial high quality, laterally predictable shoreface reservoir zones

• Producing Analogs

• Clearwater – Osum Orion

• Lower Grand Rapids – Pengrowth Lindbergh & CNRL Wolf Lake B10

• Reserves: Proven plus Probable (2P) 376 MMbbl1

TaigaProject

1. GLJPetroleumConsultants.ReservesandresourcesasatDec.31,2015.8

Saleski&LiegeProjects

Grosmont Carbonates Portfolio

High quality resource position in world scale play

• Over 4 billion bbl (net) recoverable resources1

• Thick, laterally extensive oil columns in stacked target zones

Established commercial potential through pilot project (shut-in in Q3 2015)

Leveraging knowledge gained to date to refine our plans with a focus on Osum’s Grosmont C position

1. Managementes,mate.See“ReservesandResources”Disclaimeronpage2.9

2015 Review

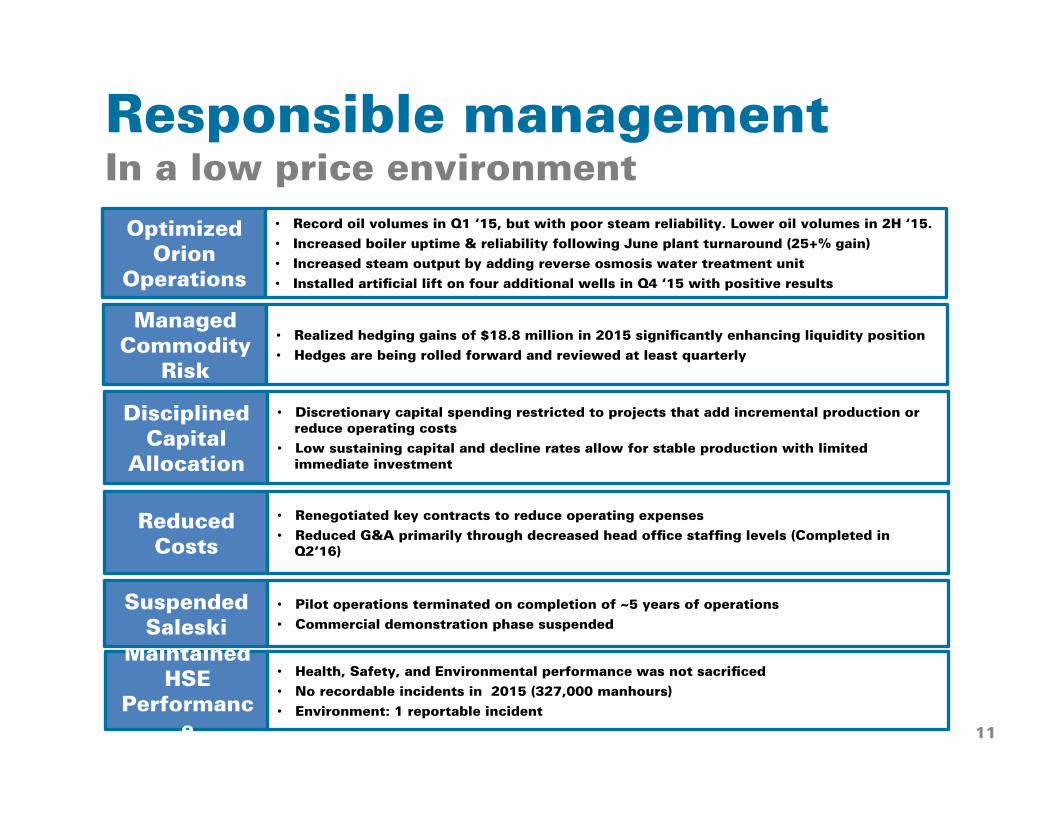

Optimized Orion

Operations

• Record oil volumes in Q1 ‘15, but with poor steam reliability. Lower oil volumes in 2H ‘15.

• Increased boiler uptime & reliability following June plant turnaround (25+% gain)

• Increased steam output by adding reverse osmosis water treatment unit

• Installed artificial lift on four additional wells in Q4 ‘15 with positive results

Managed Commodity

Risk

• Realized hedging gains of $18.8 million in 2015 significantly enhancing liquidity position

• Hedges are being rolled forward and reviewed at least quarterly

Disciplined Capital

Allocation

• Discretionary capital spending restricted to projects that add incremental production or reduce operating costs

• Low sustaining capital and decline rates allow for stable production with limited immediate investment

Reduced Costs

• Renegotiated key contracts to reduce operating expenses

• Reduced G&A primarily through decreased head office staffing levels (Completed in Q2‘16)

Responsible management In a low price environment

Maintained HSE

Performance

• Health, Safety, and Environmental performance was not sacrificed

• No recordable incidents in 2015 (327,000 manhours)

• Environment: 1 reportable incident

Suspended Saleski

• Pilot operations terminated on completion of ~5 years of operations

• Commercial demonstration phase suspended

11

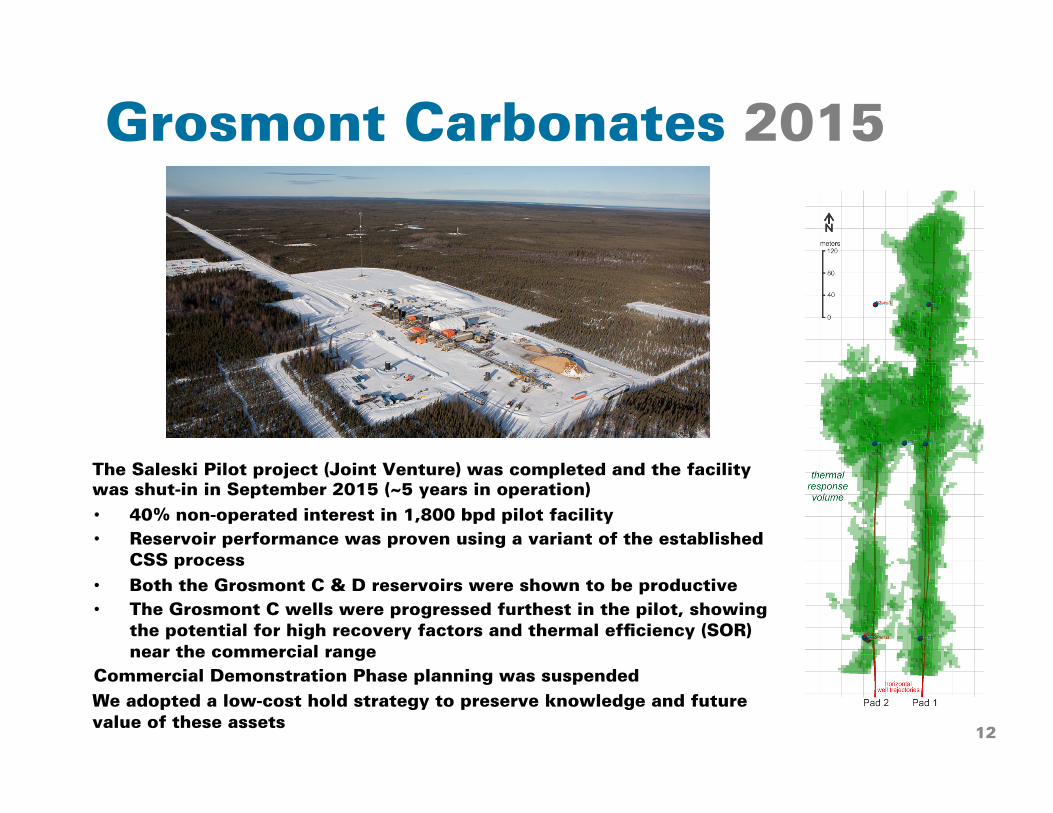

Grosmont Carbonates 2015

The Saleski Pilot project (Joint Venture) was completed and the facility was shut-in in September 2015 (~5 years in operation)

• 40% non-operated interest in 1,800 bpd pilot facility

• Reservoir performance was proven using a variant of the established CSS process

• Both the Grosmont C & D reservoirs were shown to be productive

• The Grosmont C wells were progressed furthest in the pilot, showing the potential for high recovery factors and thermal efficiency (SOR) near the commercial range

Commercial Demonstration Phase planning was suspended

We adopted a low-cost hold strategy to preserve knowledge and future value of these assets

12

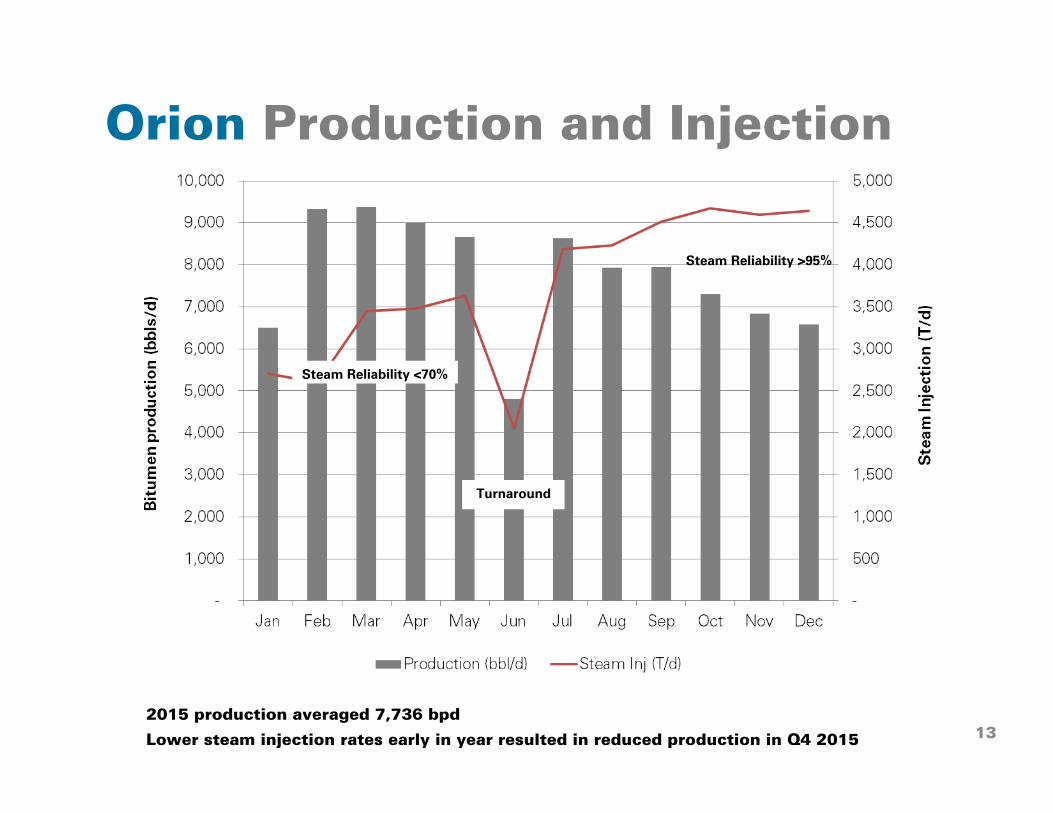

Orion Production and Injection

Turnaround

Steam Reliability >95%

Steam Reliability <70%

2015 production averaged 7,736 bpd

Lower steam injection rates early in year resulted in reduced production in Q4 2015 13

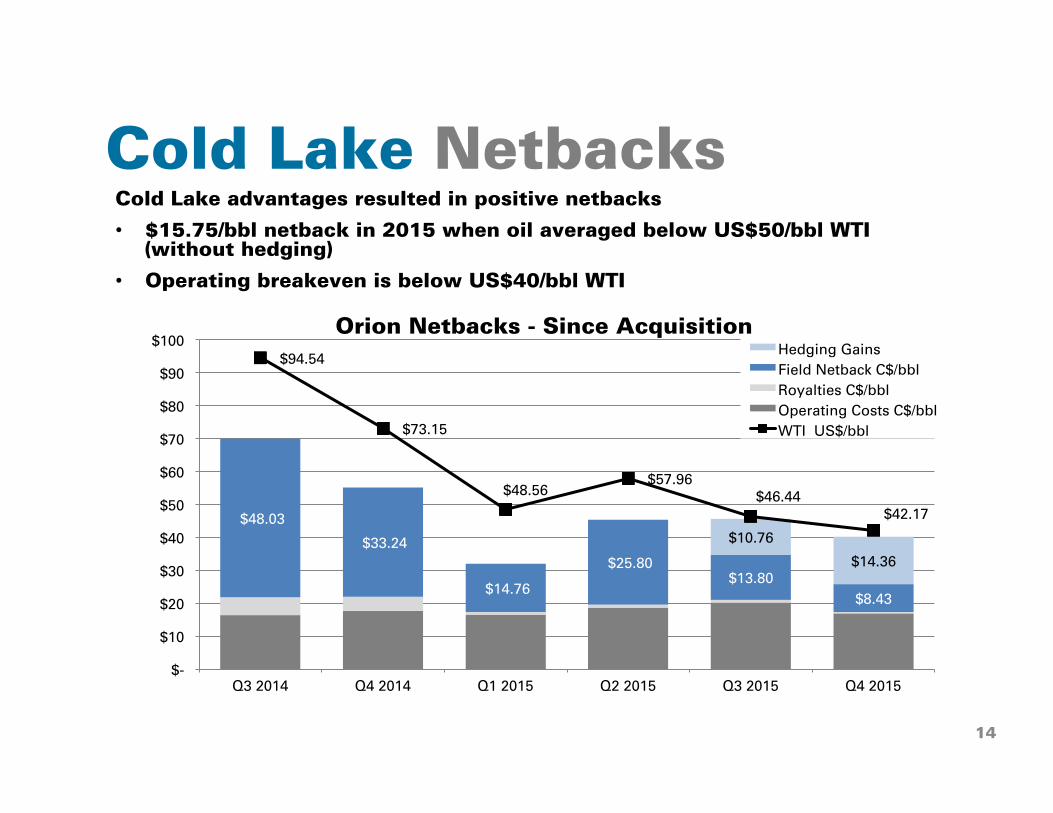

Cold Lake Netbacks Cold Lake advantages resulted in positive netbacks

• $15.75/bbl netback in 2015 when oil averaged below US$50/bbl WTI (without hedging)

• Operating breakeven is below US$40/bbl WTI

$48.03

$33.24

$14.76

$25.80 $13.80

$8.43

$10.76

$14.36

$94.54

$73.15

$48.56 $57.96

$46.44 $42.17

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015

Orion Netbacks - Since Acquisition Hedging Gains

Field Netback C$/bbl

Royalties C$/bbl

Operating Costs C$/bbl

WTI US$/bbl

14

Orion Operating Results

15

1VolumesfromtheSaleskipilotarenotincluded22014representstheperiodfollowingtheOrionacquisi,ononly3Financialhedginggainsonly.Physicalhedginggainsareincludedinbitumenrevenue

2015 2014(2) Change-$ Change-%BitumenProduc,on(1) bbl/d 7,736 7,996 (260) (3%) WTI US$/bbl 48.76 81.70 (32.94) (40%)ColdLakeBlend US$/bbl 33.84 63.84 (30.00) (47%)Differen,al US$/bbl 14.92 17.86 (2.94) (16%)Differen,al % 30.6% 21.90% 8.70% 40%ForeignExchangeRate US$/C$ 0.782 0.892 (0.110) (12%)AECOGasPrice C$/mcf 2.77 4.01 (1.24) (31%) BitumenFieldPrice C$/bbl 34.61 60.76 (26.15) (43%)Royal,es C$/bbl 0.69 4.67 (3.98) (85%)Opera,ngCosts C$/bbl 18.18 17.28 0.90 5%FieldNetbackBeforeHedging C$/bbl 15.74 38.81 (23.07) (59%)RealizedHedgingGains C$/bbl 6.10 - 6.10 -CashOpera,ngNetbackAmerHedging C$/bbl 21.84 38.81 (16.97) (44%)

FieldNetbackBeforeHedging C$000 44,446RealizedHedgingGains(3) C$000 17,223CashOpera,ngNetbackAmerHedging C$000 61,669

Balance Sheet

16

31-Dec-15 31-Dec-14

Cash and Cash Equivalents (1) C$ MM 109.4 115.6

Working Capital Surplus (2) C$ MM 199.3 208.5

Long Term Debt Outstanding (3) C$ MM 284.1 230.5

Basic Shares Outstanding (4) MM 130.4 130.4

(1)

Includes restricted cash

(2)Excludes net unrealized hedging assets. Includes $100MM proceeds from callable common share purchase warrants

(3)Consists of the outstanding non-current portion of the term loan translated to C$ at the period-end exchange rate. The current portion is included in the working capital surplus. The term loan bears a floating interest rate based on the greater of LIBOR or 1%, plus 5.5%.

(4)Includes 8.0 million callable common share purchase warrants with an exercise price of $12.50/share

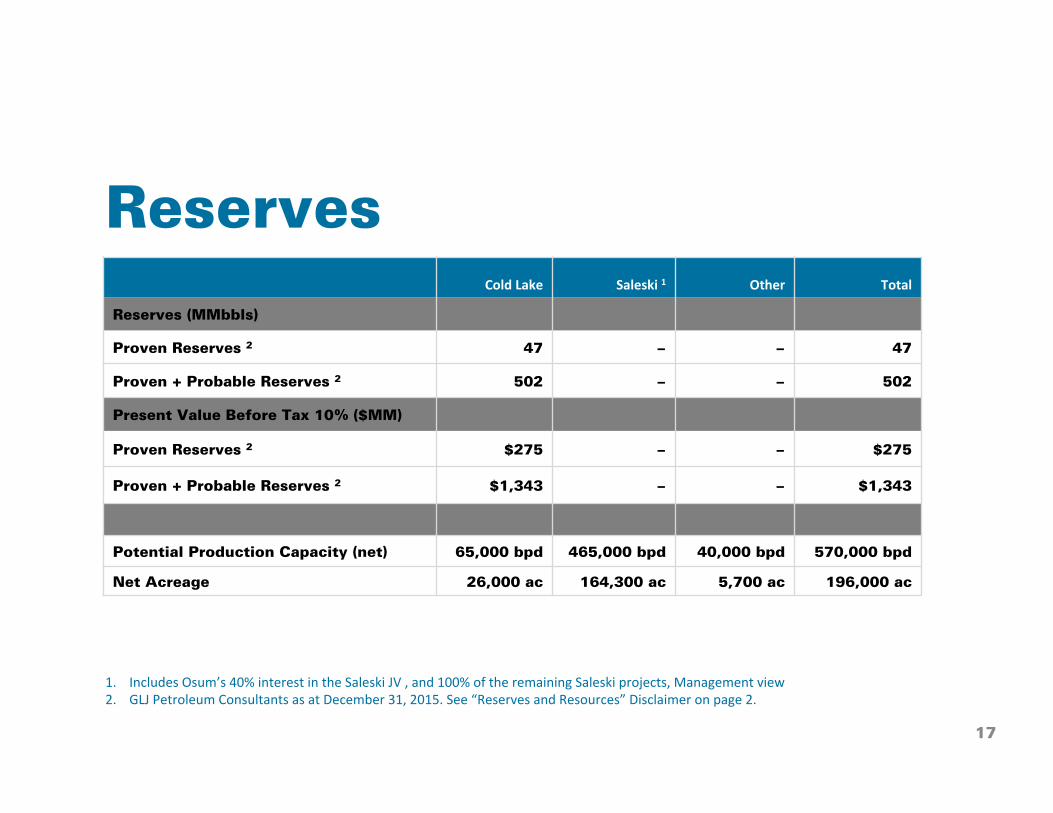

Reserves

17

ColdLake Saleski1 Other Total

Reserves (MMbbls)

Proven Reserves 2 47 − − 47

Proven + Probable Reserves 2 502 − − 502

Present Value Before Tax 10% ($MM)

Proven Reserves 2 $275 − − $275

Proven + Probable Reserves 2 $1,343 − − $1,343

Potential Production Capacity (net) 65,000 bpd 465,000 bpd 40,000 bpd 570,000 bpd

Net Acreage 26,000 ac 164,300 ac 5,700 ac 196,000 ac

1. IncludesOsum’s40%interestintheSaleskiJV,and100%oftheremainingSaleskiprojects,Managementview2. GLJPetroleumConsultantsasatDecember31,2015.See“ReservesandResources”Disclaimeronpage2.

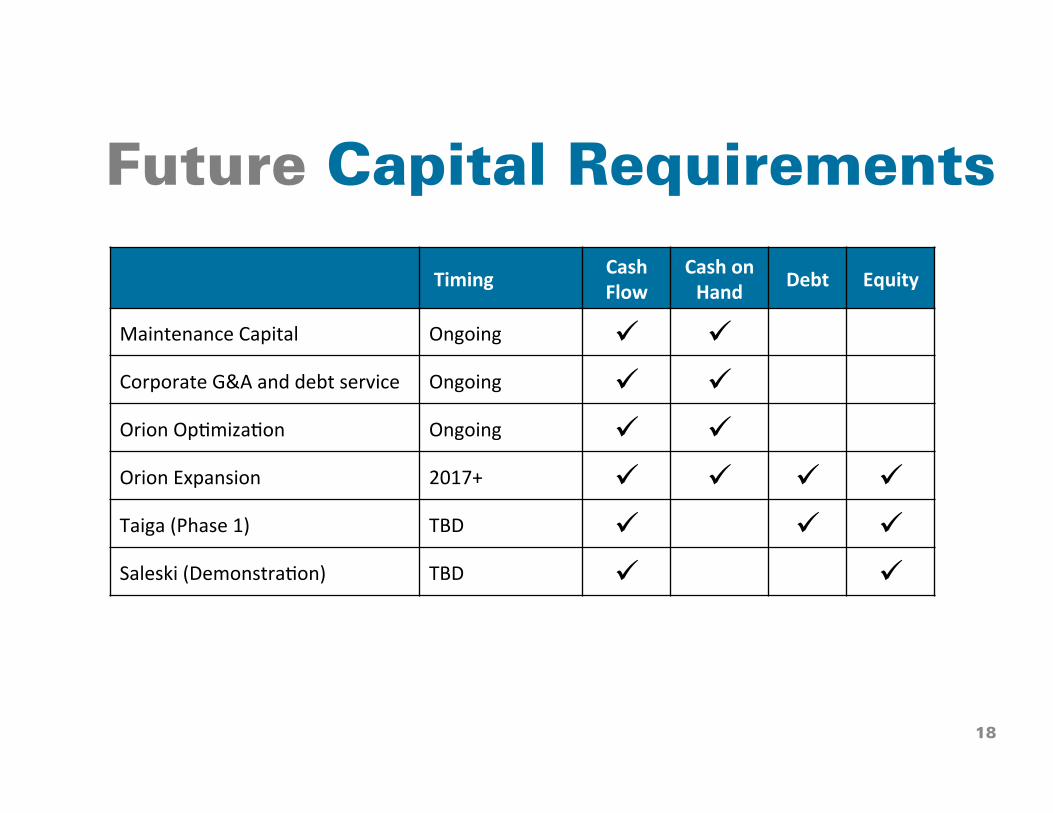

Future Capital Requirements

Timing CashFlow

CashonHand Debt Equity

MaintenanceCapital Ongoing ü üCorporateG&Aanddebtservice Ongoing ü üOrionOp,miza,on Ongoing ü üOrionExpansion 2017+ ü ü ü üTaiga(Phase1) TBD ü ü üSaleski(Demonstra,on) TBD ü ü

18

2016 Focus • Manage our finances prudently to protect the business

through the downturn

• Focus on our Cold Lake assets in the near term, adding production and reducing structural costs

• Pursue small production enhancement projects at Orion that are profitable in today’s business conditions, and make the business more robust (e.g. debottlenecking, well stimulations)

• Larger expansions will be considered as oil prices recover to a point that provides the confidence to move forward

• Deliver superior safety and environmental performance

19

Summary • 2015 was a challenging year characterized by declining oil

prices and production swings

• We achieved positive operating netbacks through the year, which were further uplifted by a successful hedging program

• Our liquidity remains strong

• We have positioned the business to weather the downturn and will continue to manage our finances prudently

• Our operational priorities for 2016 are to stabilize production, and further reduce costs

• Our near term discretionary capital expenditures are focused on small production enhancement projects at Orion that are profitable in today’s business conditions

• We are well positioned for the long term with a portfolio of significant growth opportunities

20

Board of Directors

21

Name/Title RelevantPriorExperienceRichard(Rick)George,OCChairman

¡ FormerCEO&DirectorofSuncorEnergy¡ DirectoroftheRoyalBankofCanada,AnadarkoPetroleum,andPennWestExplora,on

(Chairman)¡ Partner,NovoInvestmentGroup

AngeloAcconcia ¡ SeniorManagingDirector,BlackstoneCapitalPartnersandBlackstoneEnergyPartners¡ DirectorofAltaEnergy,HunterOil&Gas,LLOGExplora,on,andRoyalResources

VincentChahley ¡ IndependentBusinessman¡ FormerManagingDirectorofCorporateFinanceatFirstEnergyCapital

GeorgeCrookshank ¡ IndependentBusinessman¡ FormerVicePresidentofFinanceandChiefFinancialOfficerofOPTICanadaInc.(2002to2007)

WilliamA.Friley ¡ IndependentBusinessman¡ PresidentandChiefExecu,veOfficerofTellurideOilandGasandPresidentofSkyelandOils

DavidKrieger ¡ ManagingDirector,WarburgPincusLLC¡ DirectorofBlackSwanEnergy,CanbriamEnergy,Ceres,EnduranceEnergy,FirstGreen

Partners,KosmosEnergy,MEGEnergy,VelvetEnergyandWestValleyEnergy

GaryLevin ¡ Principal,BlackstoneCapitalPartnersandBlackstoneEnergyPartners¡ DirectorofLLOGExplora,onandVineOil&Gas

CameronMcVeigh ¡ President,CamcorPartnersInc.¡ DirectorofTangleCreekEnergy

BrianReinsborough ¡ Founder,President&CEO,VenariResourcesLLC¡ FormerPresidentofNexenPetroleumU.S.A.

JeffvanSteenbergen ¡ ManagingPartner,AzimuthCapitalManagement¡ DirectorofAduroResources,AltexEnergy,CobaltInterna,onalEnergy(US),FairfieldEnergy

(UK),MagmaGlobalLtd.,andSevenGenera,onsEnergy

SteveSpence ¡ President&CEOofOsum

Thank You